Crypto World

Q1 2026 Digital Asset Review

In today’s newsletter, Joshua de Vos from CoinDesk breaks down cryptos performance in the first quarter, highlighting shifting institutional demand and new regulatory clarity setting the stage for Q2.

Q1 2026 Digital Asset Review

Digital assets closed Q1 2026 under meaningful pressure, extending a downturn that began in late 2025. As presented in CoinDesk’s latest “Quarterly Review and Outlook,” the quarter was shaped by escalating geopolitical tensions, a cautious Federal Reserve, and institutional flows that turned sharply negative before partially recovering into month-end.

Q1 in review

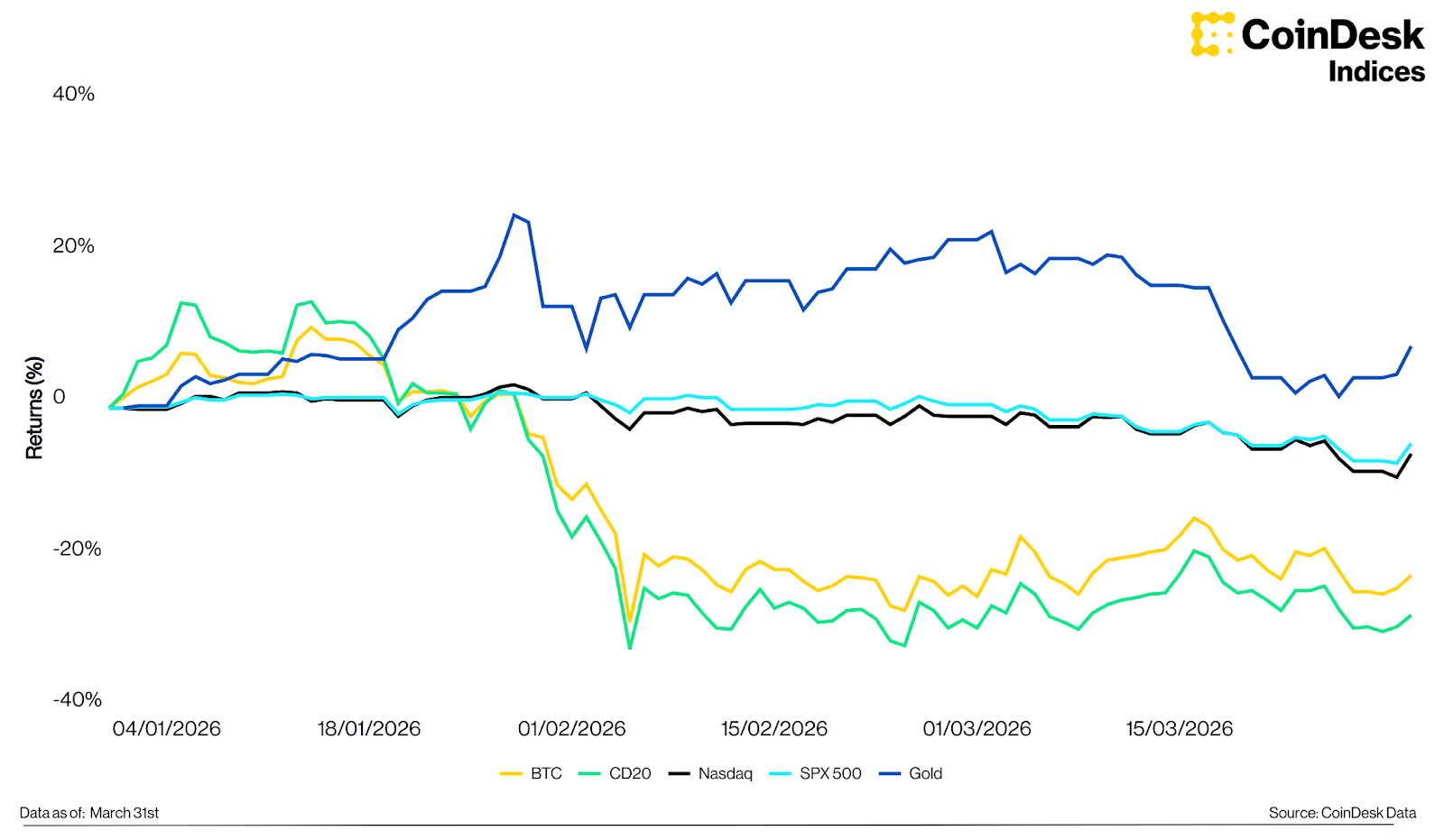

The CoinDesk 20 Index declined 27.4% to 1,952, while bitcoin fell 22.1% to $68,228; its second-largest quarterly decline since Q2 2022. Escalating tensions in the Middle East pushed crude oil above $100 per barrel, while the Federal Reserve held rates steady at 3.5%–3.75% following its March meeting. The S&P 500 and Nasdaq declined 4.63% and 5.98% respectively; gold was the standout, rising 8.19% to $4,671.

BTC vs gold vs SPX vs Nasdaq vs the CD20 Index, Q1 2026

A notable dynamic emerged in the quarter’s second half. Bitcoin had already declined roughly 30% from its February peak before geopolitical tensions escalated sharply in late February, suggesting much of the fear and forced liquidations had been priced in before the event. Since tensions intensified, bitcoin returned 3.54%, while the S&P 500 and Nasdaq fell 5.09% and 4.89%. The CoinDesk Memecoin Index was the weakest performer at -41.7%; the CoinDesk 80 outperformed bitcoin, declining 16.5%, with Hyperliquid (+43.8%) and Morpho (+40.9%) leading positive returns among its constituents.

BTC and CD20 Index vs selected assets, returns since Feb 28th

Institutional flows in focus

Among U.S. spot bitcoin ETFs, net outflows of $1.81B across January and February erased much of the institutional demand built during the prior year. Although March saw a recovery of $1.32B in inflows, Q1 closed with net redemptions of approximately $496M. Bitcoin’s stabilisation in March coincided with the return of positive net inflows, suggesting institutional positioning had begun to rebuild before the quarter ended.

Bitcoin ETF flows and BTC price, Q1 2026

In the spot ETF era, institutional flow data provides a real-time signal of sentiment unavailable in prior cycles. The March recovery sets a baseline worth watching for Q2, particularly as Morgan Stanley reportedly prepares a spot bitcoin ETF ($MSBT) at a 0.14% fee, designed to integrate into its network of over 16,000 advisors.

The regulatory picture clarifies

A joint SEC–CFTC ruling on March 17 designated 16 assets, including SOL, XRP and DOGE, as digital commodities and thus outside the securities definition. This removes a key regulatory overhang and opens the pathway for spot ETF approvals across a broader range of assets. Basket and index-based ETPs now rank second only to bitcoin-focused products by number of pending filings, with CoinDesk indices including the CD20 and CD100 increasingly referenced as natural benchmarks for these vehicles.

Number of pending crypto ETP applications, 2025

Looking ahead to Q2

Market direction in Q2 will be shaped by two variables: the trajectory of the Middle East conflict and the Federal Reserve’s response to inflation data. A de-escalation would ease energy price pressure and creates conditions for recovery; prolonged conflict would keep financial conditions tight. Bitcoin’s October 2025 peak near $126,000 and the subsequent correction are broadly consistent with the historical halving cycle, which typically produces an 18–24 month post-ATH drawdown. This cycle’s structural difference is institutionalised ETF demand; on peak days in 2024, inflows topped $1 billion, equivalent to absorbing over 30 days of mining supply in a single session. Combined with a more supportive regulatory environment and a deepening institutional product suite, the structural foundation entering this correction is meaningfully more durable than in prior cycles.

Constituent highlights

Ether declined 29.1% in Q1, with U.S. spot ether ETFs recording net outflows of $758 million. The more significant forward-looking development is Ethereum’s structural position in tokenised assets; 59.4% of total real-world asset supply resides on Ethereum as of Q1 2026. BlackRock’s ETHB staking ETF, launched on March 12 with a projected 3–7% annual yield, introduces an income-generating dimension to ETH that could broaden its appeal to yield-oriented allocators.

Solana declined 33.2% but registered a notable milestone: peer-to-peer stablecoin transaction volume reached a new all-time high of $832 billion in Q1 2026, reflecting a shift toward payments infrastructure. Solana’s real-world asset holder count also surpassed Ether for the first time, driven by platforms such as Ondo Global Markets and xStocks.

XRP declined 27.1%, but the narrative is increasingly centred on Ripple’s expanding institutional infrastructure. RLUSD reached a market capitalization of $1.42 billion by quarter-end, and Ripple’s acquisition strategy, spanning prime brokerage through Hidden Road ($1.25 billion, clearing $3 trillion annually) and treasury management through GTreasury ($1 billion), points toward a comprehensive financial ecosystem built around XRP and RLUSD. The key catalyst for Q2 is whether these integrations translate into measurable on-chain activity.

This summary was created based on CoinDesk Research’s latest report “Digital Assets: Quarterly Review and Outlook, Featuring CoinDesk 5 and CoinDesk 20.”

– Joshua de Vos, research team lead, CoinDesk

Keep Reading

- JP Morgan CEO Jamie Dimon says the bank must “move faster” with its blockchain efforts due to the threats banking faces from blockchain technology.

- Morgan Stanley’s own bitcoin ETF opened this week creating competition on Wall Street.

- The U.S. Treasury is pitching new rules for stablecoin issuers to treat them like every other financial firm that must maintain armor against illicit uses.

Key takeaways:

-

Bitcoin orderbook depth has plummeted by 50% since September 2025, signaling a substantial decline in overall market liquidity.

-

Indicators suggest that the current market fragility stems more from recent 2026 trends than from the 2025 flash crash itself.

Bitcoin (BTC) and crypto markets took a massive hit on Oct. 10, 2025, precisely 6 months ago. That devastating flash crash wiped out a record-breaking $19 billion in leveraged positions while some altcoins collapsed 40% to 80%. Many traders speculated that multiple market makers had been wiped out, while others accused the Binance exchange of blatant manipulation.

Was the crypto market structure actually altered after the October 2025 crash, and what has changed in liquidity, derivatives markets, and institutional metrics?

Bitcoin’s aggregate orderbook depth, ranging from +1% to -1%, typically oscillated between $180 million and $260 million in September 2025. On most days, there would be a healthy $90 million in bids, but that was not the case on Oct. 10, 2025. A mix of technical issues at Binance and auto-deleveraging on decentralized exchanges caused a temporary liquidity lapse.

During the flash crash, Bitcoin’s orderbook depth entered a downward spiral, stabilizing near $150 million by mid-November 2025. Currently, Bitcoin’s order book depth seldom exceeds $130 million, down 50% from levels seen in September 2025.

The already fragile market conditions deteriorated further in February 2026. Bitcoin’s orderbook depth plunged below $60 million for nearly 10 days as the price struggled to hold the $65,000 level. Cryptocurrency market volumes declined considerably, especially in the derivatives markets.

Cryptocurrency derivatives volumes oscillated between $40 billion and $130 billion over the past 30 days, falling short of the $200 billion mark commonly seen in September 2025. Still, the reduced appetite for futures contracts is not necessarily a bearish indicator as longs (buyers) and shorts (sellers) are evenly matched at all times.

Demand for bullish leverage remains weak, ETF volumes lag

The Bitcoin perpetual futures funding rate can be used to assess traders’ risk appetite.

Under normal conditions, the indicator should range between 6% to 12% to compensate for the cost of capital. Excessive demand for bearish leverage can push the indicator below 0%, meaning shorts are the ones paying to keep their positions open. Data indicate stable conditions throughout November 2025, followed by a sharp decline in February 2026.

Curiously, volumes of US-listed spot Bitcoin exchange-traded funds (ETFs) were not impacted by the Oct. 10, 2025 flash crash. In fact, by late November, activity in those instruments jumped to their highest levels in 20 months at $11.5 billion per day.

Related: Binance adds spot trading guardrails to limit abnormal executions

Bitcoin ETFs regularly traded at volumes above $4 billion per day between January and March 2026, but eventually fell below $3.3 billion by the first week of April. Similarly, US-listed Ether (ETH) ETFs average daily volume dropped to $1 billion, down from $2 billion in September 2025.

Orderbook depth, funding rate, derivatives and ETF volumes all point to a much less healthy cryptocurrency market in April 2026 relative to 6 months prior. However, given that the market structure held relatively firm through February 2026, the relevance of the Oct. 10, 2025 flash crash seems much less than previously imagined.

This article is produced in accordance with Cointelegraph’s Editorial Policy and is intended for informational purposes only. It does not constitute investment advice or recommendations. All investments and trades carry risk; readers are encouraged to conduct independent research before making any decisions. Cointelegraph makes no guarantees regarding the accuracy or completeness of the information presented, including forward-looking statements, and will not be liable for any loss or damage arising from reliance on this content.

The Ether Machine and Dynamix Corporation (NASDAQ: ETHM) have mutually terminated their business combination agreement, effective April 8, 2026.

In a post on X, the firm stated that the deal fell through due to unfavorable market conditions.

Ether Machine Cites “Unfavorable Market Conditions” as SPAC Merger Dies

The Ether Machine first unveiled plans to go public in July 2025, targeting more than $1.5 billion in fully committed capital and an initial treasury of more than 400,000 ETH.

The proposed deal drew backing from major industry players, including Pantera Capital, Kraken, and Blockchain.com.

However, the deal did not reach the finish line.

“The Ether Machine, a planned public company following a pending business combination with Dynamix Corporation (Nasdaq: ETHM) and The Ether Reserve LLC, together with certain other parties thereto, announced today that they have mutually agreed to terminate their previously announced Business Combination Agreement, effective immediately, as a result of unfavorable market conditions,’ the post read.

The termination comes as the crypto market continues to face headwinds. Asset prices have declined sharply since October, and Q1 2026 has added further pressure.

While geopolitical tensions briefly lifted Ethereum, the token still remains nearly 55% below its all-time high set in August 2025.

The impact is not limited to The Ether Machine. BitMine, the largest corporate ETH holder, is sitting on roughly $6.5 billion in unrealized losses, with its stock down 31.7% year to date.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The pattern extends beyond ETH as well. Bitcoin treasury firms have also faced pressure, with some moving to liquidate their holdings.

$50 Million Termination Fee and Indemnification Provisions

According to the 8-K filing with the SEC, the termination agreement includes mutual releases, a covenant not to sue, and non-disparagement clauses. The designated “Payor” also must pay $50 million to Dynamix within 15 days of the agreement’s effective date.

“The Termination Agreement further provides that the Payor will indemnify Dynamix, the Sponsor and their affiliates and the Berns Parties for certain losses arising out of or caused by or based upon certain actions brought by any ETHM Investor other than an ETHM Investor that is a SPAC Releasing Party and that Dynamix will indemnify Pubco, the Company, the Seller, the Payor and their affiliates and the Berns Parties for certain losses arising out of or caused by or based upon certain actions brought by any Dynamix shareholder, in their capacity as a shareholder, who is not an ETHM Investor,” the filing reads.

Dynamix has until November 22, 2026, to complete a business combination or face liquidation. If no deal is finalized, public shareholders will receive pro-rata redemptions from the trust account.

Follow us on X to get the latest news as it happens

The post $1.5 Billion Ethereum Treasury Ether Machine Deal Collapses appeared first on BeInCrypto.

SpaceX is sitting on 8,285 BTC worth $603 million in Coinbase Prime custody while reporting a loss of nearly $5 billion for 2025, according to Arkham Intelligence data and a report from The Information published late Friday.

The loss marks a sharp reversal from a year earlier when SpaceX generated roughly $8 billion in profit on revenues estimated between $15 billion and $16 billion.

Revenue grew to $18.5 billion in 2025, but the integration of xAI, Elon Musk’s artificial intelligence venture acquired in February, drove costs past the top line.

There are no changes to the company’s bitcoin position despite these losses. Transfer history analyzed by CoinDesk shows the last significant movement was an internal rebalance roughly four months ago, with 614 BTC and 1,021 BTC moving between SpaceX’s own wallets.

The balance history chart shows holdings have remained stable since mid-2024 after peaking above $1.6 billion in value during the October 2025 all-time high.

For a company that just posted a $5 billion loss and is actively pursuing an IPO, holding $603 million in a volatile asset rather than liquidating it to improve the balance sheet is a statement about how Musk (or the broad) view bitcoin as a treasury asset.

SpaceX’s position is now the fourth-largest known corporate bitcoin holding behind Strategy, Marathon Digital, and Riot Platforms.

CoinDesk reported last month that SpaceX had filed for an IPO that would disclose the bitcoin position in public filings for the first time, potentially forcing a fair-value accounting decision under the new FASB rules that took effect in late 2025.

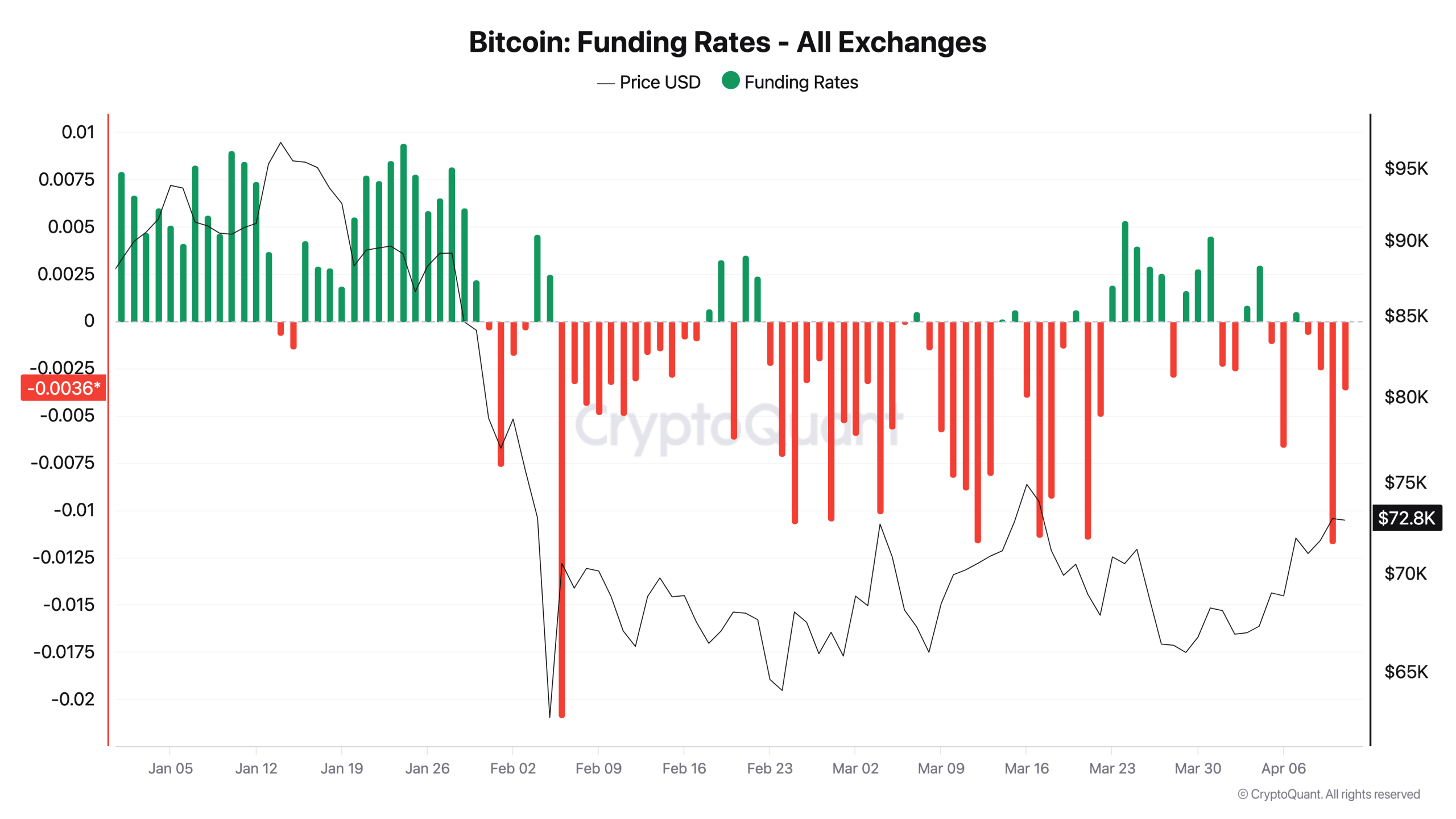

Bitcoin is set for a potential short squeeze as on-chain indicators illuminate a crowded setup against a backdrop of rising open interest and persistently negative funding rates. After BTC briefly breached $73,000 last Friday, traders are watching how leveraged shorts might be forced to cover as funding costs stay deeply negative and open interest climbs to a five-week high.

CryptoQuant’s Quicktake analysis highlighted that Bitcoin was “crowded” with short positions, noting that BTC is moving off exchanges while funding rates remain strongly negative. This combination, according to contributors, can amplify a squeeze if demand returns and shorts are compelled to unwind their bets. Source: CryptoQuant

Key takeaways

- Bitcoin open interest rose to about $24.2 billion, the highest since early March, signaling growing leverage as traders position for a potential move.

- Funding rates on major exchanges sit in deeply negative territory, indicating short positions are paying longs and increasing the risk of a forced reversal.

- Analysts say large-scale speculators have turned net long on BTC again, a posture that historically foreshadows a powerful move when conviction builds.

- After BTC cleared $73,000, some market voices eye higher targets, including $80,000 and beyond, though caution remains warranted amid persistent volatility.

- Daily liquidations across the broader crypto space remained subdued, with CoinGlass reporting under $100 million in cross-crypto liquidations over a 24-hour window.

Open interest and the squeeze dynamic

Analysts have flagged that the confluence of rising open interest and continuous negative funding rates creates a precarious setup for Bitcoin’s upside trade. Since March, negative funding has become more frequent and has persisted through April, reinforcing a narrative where shorts have dominated the market. CoinNiel summarized the situation, noting that “shorts paying longs” amid a tightening squeeze environment increases the potential for a reversal driven by forced liquidations when prices move against crowded bets. CryptoQuant analysis and accompanying posts have framed the setup as a developing risk for anyone wagering on continued upside with overweight leverage.

Bitcoin’s price action recently reignited the debate around who’s in control. BTC/USD pushed past $73,000 on Friday, a move traders interpreted as a potential catalyst for a squeeze if short bets were to unwind aggressively. Open interest’s uptick to five-week highs, paired with the negative funding climate, has kept the market on edge about a rapid shift in momentum.

“Since March, negative funding has become more frequent, and throughout April it has remained in negative territory without flipping positive.”

In this context, CoinNiel cautioned that the combination of rising open interest and negative funding suggests an accumulation of leveraged short exposure, warning that the current range could still be a zone of buying demand rather than a clean breakout. Further Quicktake notes reinforce the view that the market remains cautious despite the bounce in price.

Sentiment, positioning, and trader perspectives

Market voices have begun to point to a potential shift in sentiment as large-volume participants tilt toward a net-long stance. Trader Michaël van de Poppe noted that speculators are net long Bitcoin, drawing a parallel with prior occasions when similar positioning preceded a notable breakout in 2023. His observation, echoed by others tracking the positioning of institutional and high-net-worth traders, underscores a tension between a crowded short setup and a growing conviction among bulls that a new leg higher could be underway. Van de Poppe’s commentary highlights the evolving consensus among key market participants.

Despite the renewed optimism among some traders, risk remains. The market has not yet exhibited a sharp deleveraging that would accompany a decisive breakout; instead, it sits at a fragile equilibrium where shorts could be squeezed only if buyers sustain pressure, while a renewed wave of selling could reintroduce downward volatility.

What to watch next

Several data points will be critical to assess the likelihood and scale of any squeeze or new rally:

- Funding rates and exchange net flows: Continued negative funding and ongoing outflows from exchange wallets would reinforce the crowded-short narrative and caution against premature bullish bets.

- Open interest dynamics: Whether open interest maintains its upward trajectory or begins to roll over will signal whether leverage is expanding or unwinding.

- Liquidation activity: Short-term spikes in cross-asset liquidations could foreshadow a rapid price revaluation, though the current snapshot shows relatively modest liquidation levels (under $100 million over 24 hours according to CoinGlass).

- Key price targets and risk markers: Trader targets around $80,000 and higher are in circulation, but traders caution that the market remains vulnerable to shifts in macro momentum or regulatory headlines that could reverse the trend.

Taken together, the setup suggests a careful balance between a potential burst higher if shorts capitulate and the risk of a quick reversal if the market fails to sustain upside momentum. As always, participants should monitor on-chain signals, funding costs, and liquidity conditions to gauge whether the next move is a breakout or a test of support.

This article synthesizes observations from CryptoQuant’s Quicktake posts, CoinNiel’s summaries, CoinGlass liquidity data, and trader commentary from Michaël van de Poppe, in the context of BTC’s recent price action around $73,000 and the broader narrative on leveraged positioning in crypto markets.

TLDR:

- Bhutan reduced its Bitcoin holdings by 70%, from 13,000 BTC to 3,954 BTC, since October 2024.

- Over $215.7 million in BTC has moved out of Bhutan’s holding addresses in 2026 alone.

- Bhutan’s last Bitcoin mining inflow above $100,000 was recorded more than one year ago.

- Bhutan’s remaining 3,954 BTC is now less than what Strategy typically buys in one week.

Bhutan Bitcoin sell-off data confirms the kingdom has reduced its holdings by roughly 70% over the past 18 months.

Once sitting on approximately 13,000 BTC accumulated through a hydropower-backed mining operation, Bhutan now retains just 3,954 BTC valued at around $280.6 million.

Arkham Intelligence data shows over $215.7 million in BTC has already moved out of Bhutan’s holding addresses in 2026 alone, with no public comment from Druk Holding and Investments.

Steady Outflows and Slowing Mining Signal a Strategic Shift in Bhutan’s Bitcoin Position

Bhutan’s sell-off traces back to October 2024, when the kingdom held roughly 13,000 BTC. Arkham Intelligence data shows a steady, methodical drawdown rather than a single liquidation event.

Over $215.7 million in BTC has left Bhutan’s holding addresses in 2026 alone. A notable portion of these outflows has been routed to unlabeled wallets, while others have been sent to addresses linked to Galaxy Digital and OKX.

That pattern points to direct market sales rather than simple fund repositioning. In one recent transfer, roughly 319.7 BTC, worth $22.68 million, moved to two separate addresses in a single transaction.

Bhutan originally built its Bitcoin reserve through a hydropower-backed domestic mining operation run by Druk Holding and Investments. However, Arkham data shows no mining inflow exceeding $100,000 has been recorded in over a year.

The operation that once converted river energy into Bitcoin appears to have slowed considerably or stopped entirely.

The economics behind this shift are straightforward. Bhutan’s mining operation worked when network difficulty was lower, and Bitcoin traded above $90,000.

At current levels near $71,000, with difficulty at all-time highs and post-halving block rewards cut to 3.125 BTC, margins have compressed sharply. Selling hydropower directly to neighboring India may now generate more predictable revenue than mining Bitcoin.

Bhutan’s Retreat Stands Out as Institutional Buyers Continue Accumulating Bitcoin

Bhutan’s sell-off runs directly against the broader trend among institutional and sovereign-level holders. Strategy purchased 4,871 BTC for $330 million in a single weekend, bringing its total to 766,970 BTC.

U.S. spot Bitcoin ETFs absorbed approximately 50,000 BTC in March alone, reflecting sustained institutional demand.

The contrast sharpens further when other market participants are considered. The Ethereum Foundation staked $93 million in ether rather than selling during the same period.

Bhutan currently stands as the only sovereign-level holder visibly reducing its Bitcoin position while others continue to accumulate. Bhutan’s remaining 3,954 BTC is now smaller than what Strategy acquires in a typical week.

The kingdom once mined 13,000 BTC directly from its own rivers and mountains. Druk Holding and Investments has not responded to multiple media inquiries, leaving the future of both its reserve and mining operations publicly unanswered.

Crypto World

Ethereum (ETH) Price Prediction: ETF Inflows Hit 23,039 ETH, Pepeto Presale, and Why 2026 Changes Everything

The ethereum price prediction just got a shot of confidence after spot ETFs absorbed 23,039 ETH worth over $51 million in a single session, marking one of the strongest institutional buying days of the year.

That kind of demand is bullish for the ETH outlook long term, but months could pass before the buying pressure shows up in the price chart. Pepeto pulled in more than $8.9 million during the same correction window with the Binance listing confirmed.

Pepe went from its presale price to $11 billion, and the wallets that moved early locked in the biggest returns of their lives. That same setup is forming right now because over $8.9 million flowing in during Extreme Fear at 16 does not happen without serious conviction behind it.

Spot Ethereum ETFs recorded a net inflow of 23,039 ETH on April 10, worth roughly $51 million, while Bitcoin ETFs pulled in 4,614 BTC the same day, according to Lookonchain. TD Cowen set an ETH target of $3,650 for December 2026 in the same week, according to CoinDesk.

The real question is whether sitting for months waiting for that catalyst makes the best use of capital when a single listing event delivers the return the ethereum price prediction needs a full year to reach.

The Platform That Puts You in Control Instead of Making You Wait

Pepeto

No one can promise ETH makes a big move anytime soon, and that is exactly why the verified exchange creates such a strong opportunity right now. Pepeto is where analysts project 100x to 300x, which at current pricing could be life changing for every wallet that enters before the Binance listing.

Over $8.9 million raised while the correction crushed every chart proves the conviction behind this project. The core driver is the exchange, a full platform in one clean space that already runs. The tools find entries others miss, check contracts before your capital moves, handle research that takes hours in minutes, and track how direction shifts in real time so you never end up guessing.

Because the ETH outlook depends on macro factors that keep it range-bound, the exchange gives you a way to act now instead of sitting idle. Over $8,920,333 raised at $0.000000186 with 185% APY staking that compounds positions as stages fill. SolidProof audited every contract before the presale opened, and the founder who took the original Pepe coin to $11 billion on 420 trillion tokens engineered the exchange with a former Binance expert.

The first listing move could be massive, but the exchange and the demand it builds will stay active for years because Pepeto solves a daily problem that outlasts any single market cycle.

Ethereum Price Prediction 2026 to 2030

Ethereum (ETH) trades at $2,249 according to CoinMarketCap, holding above the $2,200 support that stabilized through the correction. The ethereum price prediction turns bullish if the price breaks $2,300 resistance and clears the 50 day SMA near $2,400, which opens a path to $2,600 and then the $3,000 level.

TD Cowen puts ETH at $3,650 by December 2026. The ETH/BTC ratio near 0.031 sits at multi-year lows, showing a wide gap between value and price. By 2027, models target $4,000 to $5,500 if institutional flows from ETFs and staking products pick up. The most bullish ethereum price prediction for 2030 targets $8,000 to $12,000 if ETF adoption mirrors the BTC path. The setup breaks if ETH loses $2,100 and slides toward $1,900.

Conclusion

The ethereum price prediction might not deliver much movement in the short term even though the ETF inflow data shows institutional money is building positions right now. Waiting for the Fed, for the CLARITY Act, and for macro conditions to clear means waiting for permission that might not come this year.

The verified exchange already has everything it needs to deliver from the Binance listing, letting the wallets inside be bullish on their own terms without needing macro permission. Visit Pepeto’s official site while the ethereum price prediction stalls, because entering now means you are the one who made the right move at the right time, and Pepe’s explosion from presale to $11 billion proved that early wallets changed their whole life while everyone who waited spent the cycle wishing they had acted when the entry was still open.

Click To Visit Pepeto Website To Enter The Presale

FAQs

What does the record ETH ETF inflow mean for the ethereum price prediction?

Spot Ethereum ETFs absorbed 23,039 ETH on April 10, adding over $51 million in institutional demand that pulls supply off the market. ETH still needs to break $2,300 and hold the 50 day SMA near $2,400 for the bullish target of $3,650 to open up.

How does Ethereum’s price at $2,249 compare to Pepeto’s expected listing return?

Ethereum needs to gain roughly 63% from $2,249 to reach TD Cowen’s $3,650 target over eight months. Pepeto’s Binance listing carries analyst projections of 100x to 300x from the presale price of $0.000000186.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

TLDR:

- Strategy holds approximately 761,000 BTC, trailing BlackRock’s IBIT by roughly 40,000 BTC currently.

- MSTR raises capital via equity and debt to buy Bitcoin directly, bypassing ETF demand dependency entirely.

- Strategy added 40,332 BTC in the first two weeks of March 2026, posting a 3.0% BTC yield.

- Bitcoin recorded eight straight days of gains, with past streaks delivering a median 30-day return of 19%.

Michael Saylor’s strategy has narrowed the Bitcoin holdings gap with BlackRock’s iShares Bitcoin Trust to roughly 40,000 BTC through relentless capital raises and direct purchases. With Bitcoin recovering steadily from February lows, the distance between the two could vanish within weeks.

Strategy’s Accumulation Model Sets It Apart

MSTR Bitcoin holdings currently stand at approximately 761,000 BTC. BlackRock’s iShares Bitcoin Trust holds roughly 781,000 BTC, leaving a gap of around 40,000 BTC.

Investor Mark Harvey noted that the difference has tightened considerably in recent weeks. Strategy raises capital through equity and preferred share issuance to fund direct Bitcoin purchases.

This model allows it to accumulate Bitcoin independent of ETF demand cycles. IBIT, by contrast, grows only when investor inflows are strong.

The company completed two multibillion-dollar Bitcoin purchases in March. Last week alone, it acquired 2,337 BTC for approximately $1.57 billion.

Over the first two weeks of March 2026, Strategy added 40,332 BTC and recorded a 3.0% BTC yield. Michael Saylor shared the firm’s year-to-date figures via X, noting sustained momentum behind its treasury approach.

Strategy frames Bitcoin accumulation as its core performance measure, using “BTC Gain” as a proxy for net income. Its long-term holding approach also removes coins from active circulation, gradually tightening available market supply.

Bitcoin’s Recovery Strengthens the Backdrop

Bitcoin bottomed near $63,000 in February amid geopolitical tensions tied to the Iran–Israel War. Prices recovered steadily after macroeconomic conditions stabilised and investor confidence returned.

The asset recently climbed from below $66,000 to $76,000 before easing near $73,800. Bitcoin has now recorded eight consecutive days of price gains.

According to Bitcoin Magazine Pro data, this streak has occurred only 15 times since Bitcoin’s creation. Past instances produced a median 30-day return of roughly 19%, though sharp pullbacks have also followed such runs.

Markets received a further boost over the weekend after signs of easing tensions around the Strait of Hormuz. Bitcoin also outperformed gold and the S&P 500 during this period.

Traders are now watching whether prices can hold above $72,000, a level that could open the path toward $80,000.

TLDR:

- Iran’s Strait of Hormuz Management Plan, passed in late March 2026, mandates Bitcoin toll payments.

- Each fully laden tanker carrying 2 million barrels faces a Bitcoin toll of up to $2 million.

- Bitcoin surged toward $73,000 as shipping firms faced the prospect of stockpiling BTC for tolls.

- Stablecoins were rejected due to freeze functions and GENIUS framework compliance requirements.

Iran Bitcoin oil toll reports are drawing wide attention across crypto and energy markets globally. Iran has reportedly implemented a mandatory Bitcoin-based payment system for oil tankers transiting the Strait of Hormuz to bypass international sanctions.

Iran’s Bitcoin Toll Structure and Payment Mechanics at the Strait of Hormuz

Financial Times report stated that Iran was considering Bitcoin payments for oil tanker tolls using the Strait of Hormuz, which handles roughly 20% of the global oil supply.

The Strait of Hormuz Management Plan, passed in late March 2026, formally codifies Bitcoin as the primary payment method.

Under this system, tankers must submit cargo details, crew lists, and destination ports to Iranian authorities up to 96 hours before arrival. A toll of $1 per barrel of crude oil is then charged, which amounts to $2 million for a fully laden Very Large Crude Carrier carrying 2 million barrels.

Vessels attempting to pass without authorization have been warned via VHF radio of serious consequences.

The original report cited officials saying ships would have only a few seconds to complete a Bitcoin payment, pointing toward the Lightning Network as the likely mechanism. However, Alex Thorn of Galaxy noted the largest known Lightning transaction to date has reached $1 million.

Given toll amounts ranging up to $2 million, Thorn suggested Iranian authorities would more likely provide a QR code or Bitcoin address upon transit approval instead.

Bitcoin’s Structure Makes It Iran’s Preferred Choice Over Stablecoins

Iran’s decision to use Bitcoin rather than stablecoins reflects a clear strategic rationale. BTC advocate Justin Bechler noted that stablecoins like USDT and USDC carry built-in blacklist functions at the smart contract level.

When an address is flagged, issuers can freeze tokens entirely, making them completely illiquid and unusable.

Bechler further noted that the GENIUS stablecoin regulatory framework introduced compliance controls that make dollar-pegged stablecoins impractical for a sanctioned nation.

Bitcoin has no issuer, no compliance officer, and no freeze function, removing any central point of control. The Iranian system also explicitly excludes the US dollar, though some reports suggest limited yuan acceptance for select nations.

Market reaction followed quickly after the reports emerged. Bitcoin prices moved toward $73,000 as shipping companies faced the prospect of holding BTC for transit payments.

Hundreds of tankers have reportedly been waiting in the Persian Gulf, navigating the new requirements, while analysts suggest similar digital toll systems could emerge at other critical waterways globally.

Pavel Durov, the co-founder of the Telegram messaging application, said that push notifications create a persistent, critical vulnerability to user privacy, allowing data retrieval even after messages and messaging applications that allow push notification data storage have been deleted from a device.

Durov cited a recent report, originally published by 404 Media, that the United States Federal Bureau of Investigation (FBI) was able to retrieve deleted messages from a Signal user by accessing device notification logs on an Apple iPhone. Durov said on Friday:

“Turning off notification previews won’t make you safe if you use those applications, because you never know whether the people you message have done the same.”

Cointelegraph reached out to Signal about the FBI’s data retrieval but did not receive a response by the time of publication.

The recent reports highlight how investigators and those with sufficient technical skills can circumvent end-to-end encryption and breach user privacy by accessing metadata and other information generated by applications, prompting a need for decentralized messaging applications that do not collect such data.

Related: Telegram founder Pavel Durov says Iranian government’s ban backfired

Alternative messaging application use surges amid spikes in civil unrest and geopolitical turmoil

Decentralized messaging applications and social media platforms experienced a surge in user interest since 2025, amid geopolitical tensions, nationwide communication blackouts and civil unrest.

Bitchat, a decentralized peer-to-peer messaging application that uses Bluetooth mesh networks to relay information between mobile devices, allows users to circumvent the internet and centralized communication networks entirely.

More than 48,000 users in Nepal downloaded the Bitchat application amid a nationwide social media ban in September 2025.

Individuals are also finding ways to circumvent national firewalls and bans on privacy-preserving applications by using virtual private networks (VPNs) and other tools that mask or obscure IP addresses and geolocation, according to Durov.

Government bans on Telegram have backfired, as users circumvent state-imposed restrictions through VPNs, allowing them to access and download banned platforms, Durov said.

“The government hoped for mass adoption of its surveillance messaging apps, but got mass adoption of VPNs instead,” he continued, adding that over 50 million users in Iran have downloaded the Telegram application, despite a years-long government ban.

Magazine: EU’s privacy-killing Chat Control bill delayed — but fight isn’t over

Bitcoin (BTC) is due a classic “short squeeze” as open interest hits five-week highs, says new analysis.

Key points:

-

Bitcoin is seeing a combination of rising open interest and negative funding rates.

-

The result could punish short positions, with funding rates at the most negative since early February.

-

Large-scale Bitcoin speculators are net long BTC again.

Bitcoin short squeeze likelihood “increasing”

In one of its “Quicktake” blog posts on Saturday, onchain analytics platform CryptoQuant said that Bitcoin was “crowded” with short positions.

“BTC is flowing out of exchanges while funding rates remain strongly negative, creating an increasingly crowded short positioning environment where the potential for a short squeeze is building,” contributor CoinNiel summarized.

After BTC/USD passed $73,000 on Friday, traders appeared eager to trap those entering the market who were betting on continued price upside. Funding rates stayed negative on exchanges, while open interest grew to $24.2 billion — its highest since early March.

“Since March, negative funding has become more frequent, and throughout April it has remained in negative territory without flipping positive,” the post continued.

“This indicates that short positions dominate the market, with shorts paying longs, and such extreme positioning can act as a trigger for a reversal through forced liquidations.”

CoinNiel said that the combination of rising open interest and negative funding rates “suggests that leveraged short positions have been rapidly accumulating.”

“The slight decrease does not yet indicate a meaningful deleveraging phase,” he acknowledged.

Fellow contributor Gaah agreed, noting that funding rates had hit their deepest negative value since Bitcoin’s dip to multiyear lows at the start of February.

“Caution is needed when establishing positions in current range, since it represents an area of buying demand,” he wrote in a further Quicktake post.

“Bears trapped? Likelihood of a short squeeze is increasing.”

Trader: Bitcoin speculators copying 2023 rebound

Earlier, Cointelegraph reported on short liquidations staying modest despite the BTC price upside.

Related: Bitcoin analysis sees $55K BTC price ‘iron bottom’ by December 2026

Data from CoinGlass showed that over the 24 hours to the time of writing, cross-crypto liquidations totaled less than $100 million.

Sentiment among market participants, meanwhile, has gradually begun to favor fresh upside, with targets including $80,000 and higher.

On Saturday, crypto trader Michaël Van de Poppe eyed increasing belief in a BTC price rebound among large-volume speculators.

“Speculators are net long on Bitcoin. Very similar to previous cases where we’ve seen the same before a big breakout in 2023,” he wrote in a post on X.

This article is produced in accordance with Cointelegraph’s Editorial Policy and is intended for informational purposes only. It does not constitute investment advice or recommendations. All investments and trades carry risk; readers are encouraged to conduct independent research before making any decisions. Cointelegraph makes no guarantees regarding the accuracy or completeness of the information presented, including forward-looking statements, and will not be liable for any loss or damage arising from reliance on this content.

Parramatta Eels vs Gold Coast Titans Tips, Odds, Teams & Predictions – NRL Round 6 2026

Spate of fires in Sherburn in Elmet prompts police action

Why Megan Fox Is Losing Millions Of Dollars With Her IG Snaps

-

Business6 days ago

Business6 days agoThree Gulf funds agree to back Paramount’s $81 billion takeover of Warner, WSJ reports

-

Sports7 days ago

Sports7 days agoIndia men’s 4x400m and mixed 4x100m relay teams register big progress | Other Sports News

-

Politics1 day ago

Politics1 day agoUS brings back mandatory military draft registration

-

Fashion1 day ago

Fashion1 day agoWeekend Open Thread: Veronica Beard

-

Tech4 days ago

Tech4 days agoHow Long Can You Drive With Expired Registration? What Florida Law Says

-

Business6 days ago

Business6 days agoNo Jackpot Winner, Prize to Climb to $231 Million

-

Fashion5 days ago

Fashion5 days agoMassimo Dutti Offers Inspiration for Your Summer Mood Board

-

Sports1 day ago

Sports1 day agoMan United discover Nico Schlotterbeck transfer fee as defender reaches Dortmund agreement

-

Fashion4 days ago

Fashion4 days agoLet’s Discuss: DEI in 2026

-

Crypto World3 days ago

Crypto World3 days agoBitcoin recovers as US and Iran Agree a Ceasefire Deal

-

Crypto World2 days ago

Crypto World2 days agoCanary Capital Files SEC Registration for PEPE ETF

-

Politics2 days ago

Politics2 days agoMalcolm In The Middle OG Turned Down ‘Buckets Of Money’ To Appear In Reboot

-

Business23 hours ago

Business23 hours agoTesla Model Y Tops China Auto Sales in March 2026 With 39,827 Registrations, Beating Cheaper EVs and Gas Cars

-

Business7 days ago

Business7 days agoAkebia Therapeutics, Inc. (AKBA) Discusses Pipeline Progress and Strategic Focus on Kidney Disease Treatments at R&D Day – Slideshow

-

Business4 hours ago

Business4 hours agoIreland Fuel Protests Enter Day 5 as Blockades Spark Shortages and Government Prepares Support Package

-

Business1 day ago

Business1 day agoOpenAI Halts Stargate UK Data Centre Project Over Energy Costs and Copyright Row

-

Tech5 days ago

Tech5 days agoHaier is betting big that your next TV purchase will be one of these

-

Tech5 days ago

Tech5 days agoGamer Restores the Original PlayStation Portal From Two Decades Ago

-

Tech6 days ago

Tech6 days agoThe Xiaomi 17 Ultra has some impressive add-ons that make snapping photos really fun

-

Tech6 days ago

Tech6 days agoSamsung just gave up on its own Messages app

You must be logged in to post a comment Login