Crypto World

Robinhood Chain scams are already costing users dearly

Robinhood (Nasdaq:HOOD) launched the public mainnet of its new blockchain on July 1, and unfortunately, tons of people are already losing money trading its coins. Bad actors are using a variety of scam contracts, memecoin rug-pulls, phishing links, and garden variety theft, leading to complaints of loss flooding onto social media.

Relay Protocol warned about scam tokens on the new Robinhood Chain: “If you bought one, the funds you spent are unfortunately gone.”

In this example, scam contracts are accepting a token swap, briefly crediting the buyer’s wallet yet immediately transferring the tokens back to the deployer’s wallet. In other words, users unwittingly purchased tokens for someone else.

Another trader alleged that Robinhood Wallet’s default sell screen auto-populated a Robinhood Chain scam coin called USER. Unless someone modified that default, the position would vaporize. “$600 out the window in seconds,” complained the user.

Another trader swapped ether (ETH) for a poisoned memecoin named $ROBINHOOD inside their Robinhood Wallet. The instant the swap confirmed, tokens moved to an unauthorized wallet.

Wallet drainers and fake token scams

A collector of NFTs claimed an OpenSea swap of Robinhood Chain assets sent his coins to an unauthorized address, costing him $350.

A trader tagged Robinhood CEO Vlad Tenev after losing $50 to what he called scam transactions.

An AI-branded Robinhood Chain memecoin, HOODIE, halved in price in a single afternoon.

Read more: Read this before you click on any Robinhood email

“It is absolutely crawling with wallet drainers and fake token scams right now,” warned another researcher, alleging that a holder of CASHCAT lost $56,000 to a hacked smart contract on Robinhood Chain.

Someone else asked whether Robinhood Chain had gone full rug mania. Another observer estimated thousands of users losing money bridging over assets from Solana-based PumpFun.

A researcher posted that memecoins account for more than 75% of the last two days of Robinhood Chain trading. That is not a good statistic, as a general rule, due to almost all meme coins trending toward $0 eventually.

“ROGE on Robinhood Chain is a 100% honeypot. The contract has a backdoor,” warned another trader.

Clifford asked a wallet provider to enable revoke-approvals on Robinhood Chain to help users undo their smart contract authorizations.

Another user urged traders to audit smart contracts prior to authorizing in the first place.

Protos previously tracked losses on branded memecoins and the near-total mortality rate of Pump.fun token launches. The long-term performance of most speculative digital assets like NFTs is identical.

Robinhood Chain’s permissionless architecture replicated many of those conditions and created an environment ripe for scams.

The new Robinhood Chain is nine days old.

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

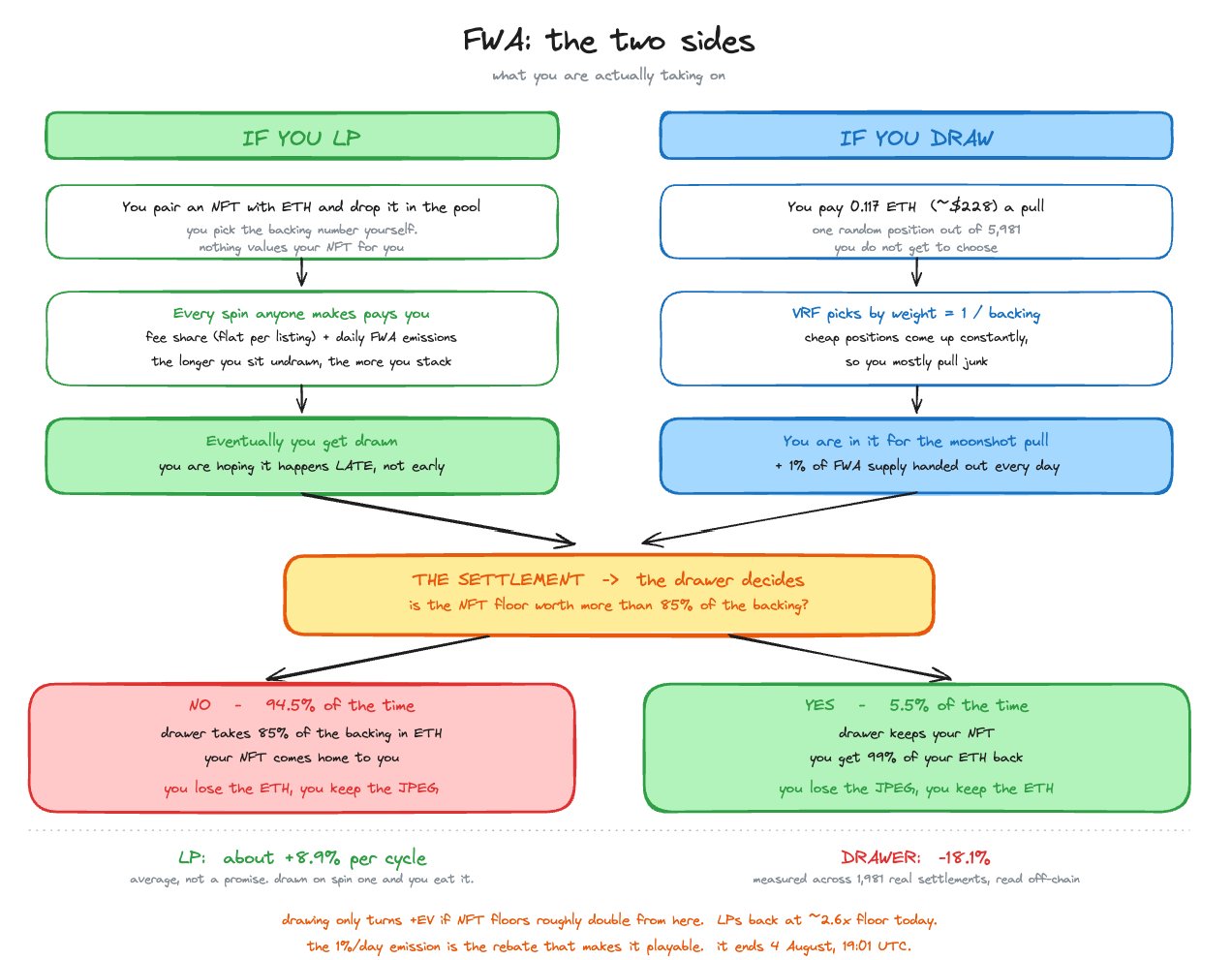

Just when you thought crypto was getting boring, a new phenomenon is lighting up Crypto Twitter — Fake World Assets (FWAs). Yes, really.

It’s the latest iteration of the onchain gacha craze, where users receive a random collectible, or collectibles, that are usually worth very little, but are sometimes worth quite a lot.

Within four days of launch, FWAs guzzled so much Ethereum gas that they briefly became the chain’s largest gas consumer by fees over a 24-hour period.

At its peak on July 25, FWAs generated approximately $1.53 million in daily fees, and even leapfrogged Tether and Circle to briefly rank among Ethereum’s biggest consumers of blockspace. Its creators, TokenWorks, proclaimed:

“4 days since launch. Fake World Assets are the next big thing.”

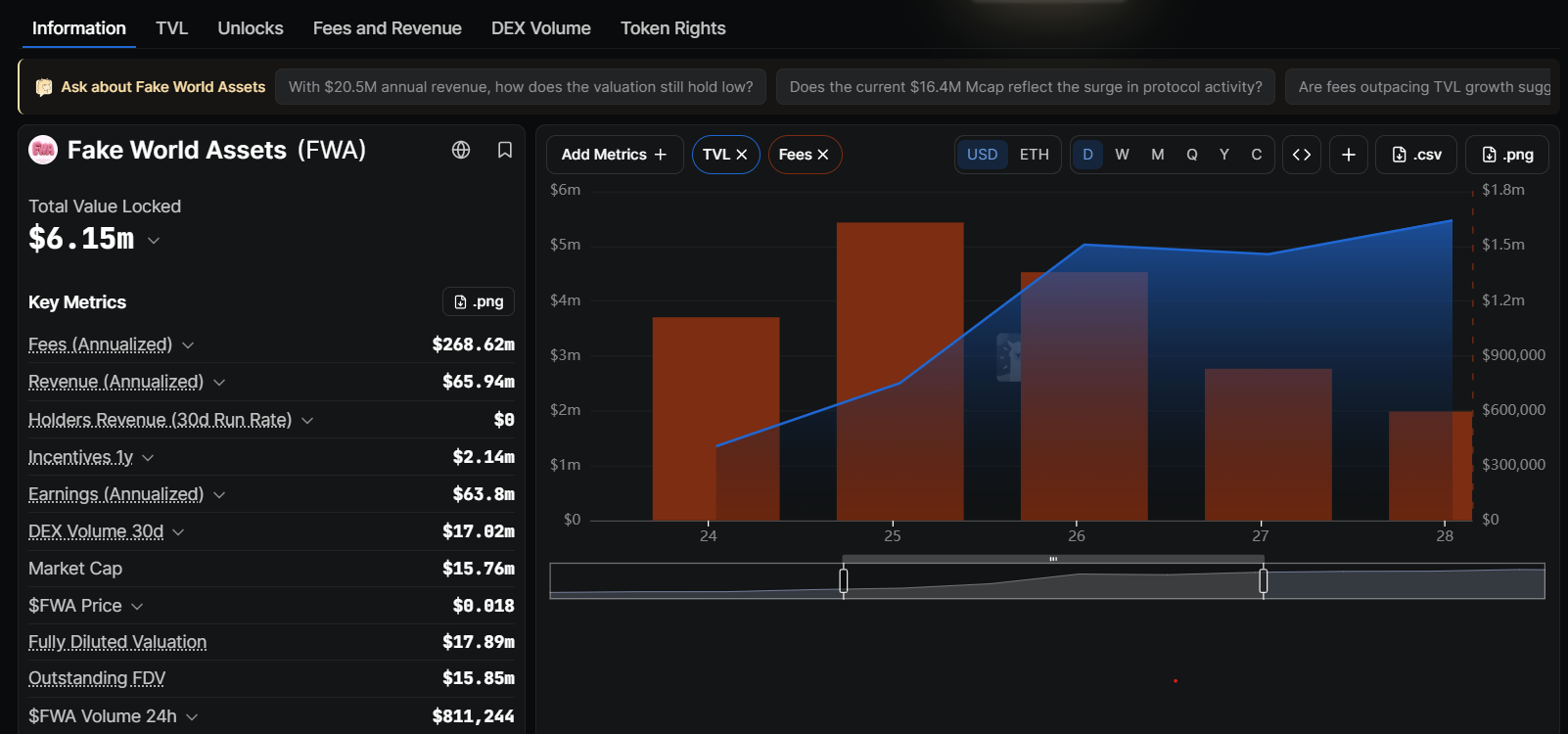

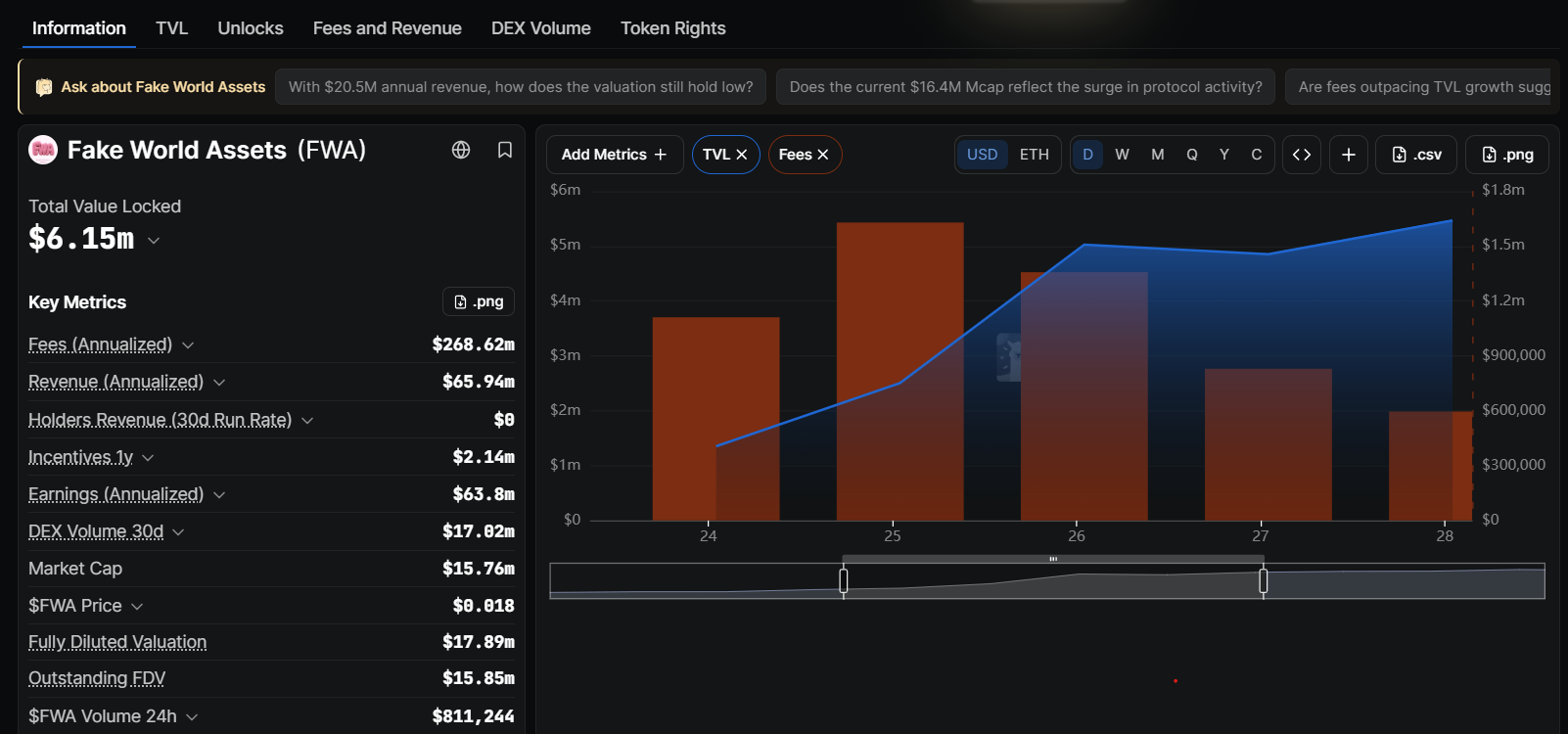

TokenWorks is far from an impartial observer, but TVL continues to climb, reaching over $6.15 million on July 31. Fee revenue has now eased to around $350,000 per day, which equates to an annualized run rate of roughly $268 million. By August 1, FWA had seen 10,000 ETH in volume, and 100,000 purchases. Some of the activity is driven by users trying to access early FWA token incentives, but there also appears to be genuine interest in the gamified mechanic.

Fake World Assets TVL and fees. Source: DeFiLlama

Not everyone is convinced the excitement around FWA will last. Simon Dedic, founder of venture capital firm Moonrock Capital, and an early backer of onchain collectible platforms, tells Magazine:

“I’m very bullish on gamified commerce… my skepticism on FWA is specific.”

Dedic argues that much of the current activity is driven by generous token incentives rather than genuine demand.

“The whole thing is purely aimed at crypto degens so they can gamble and speculate,” he says.

So, is this just another short-lived obsession, or has the industry finally stumbled upon something built to last?

All very interesting, but what the heck are FWAs?

Crypto has spent years trying to put the real world onchain, from stocks and bonds to collectible cards and Brazilian cows.

Related: Gambling on random Pokémon cards: Onchain gagcha hits record high as crypto sinks

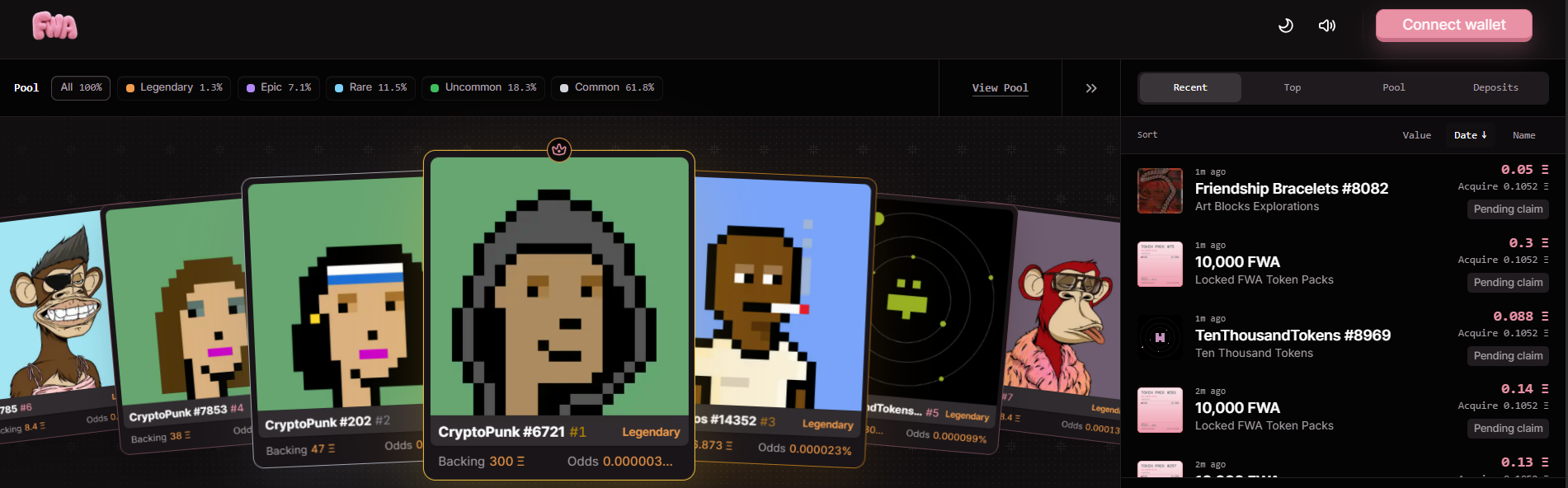

TokenWorks decided to flip the idea on its head by creating Fake World Assets, which are just NFTs. Rather than buying a specific collectible like a Bored Ape, users pay to spin an onchain “gacha” machine for the chance to win a randomly selected NFT backed by Ether.

The prizes on offer come from dozens of well-known collections, like CryptoPunks and Azuki to Lil Pudgys and Art Blocks.

Fake World Assets is just the latest Ethereum-based protocol to put a new spin on the craze.

Gacha is short for gachapon/gashapon, which are vending machines invented in Japan in the 1960s that spit out a random toy in a capsule. This mechanic migrated to mobile and browser games, with the loot boxes in Dragon Collection in 2010 often cited as the first major gacha game. Meanwhile a similar mechanic was at work with real world Pokemon trading card “booster packs” that offered a random assortment of collectible cards, of various rarity levels and values.

These cards were subsequently tokenzied onchain by projects such as Collector Crypt, Beezie and Courtyard. As Magazine reported previously, onchain gacha saw a record $324 million in volume in June. (Hundreds of these tokenized cards have now been wrapped for use on FWA.)

The concept is expanding every week, with developers experimenting with randomized “token packs” containing ERC-20 tokens, while StockRip on Robinhood chain, shows how tokenized stocks can be wrapped into NFT-based gacha packs.

Fake World Assets. Source: fwa.fun

As AzFlin, founder of DAO launchpad daos.world and a former Uniswap engineer, says:

“Just when you think everything in crypto has been invented, something new springs up.”

What is the appeal of onchain gacha?

The gacha mechanic combines crypto, collectibles and gambling . As pseudonymous crypto commentator 2Lambroz puts it, from the player’s perspective, “you’re buying a lottery ticket on the pool.”

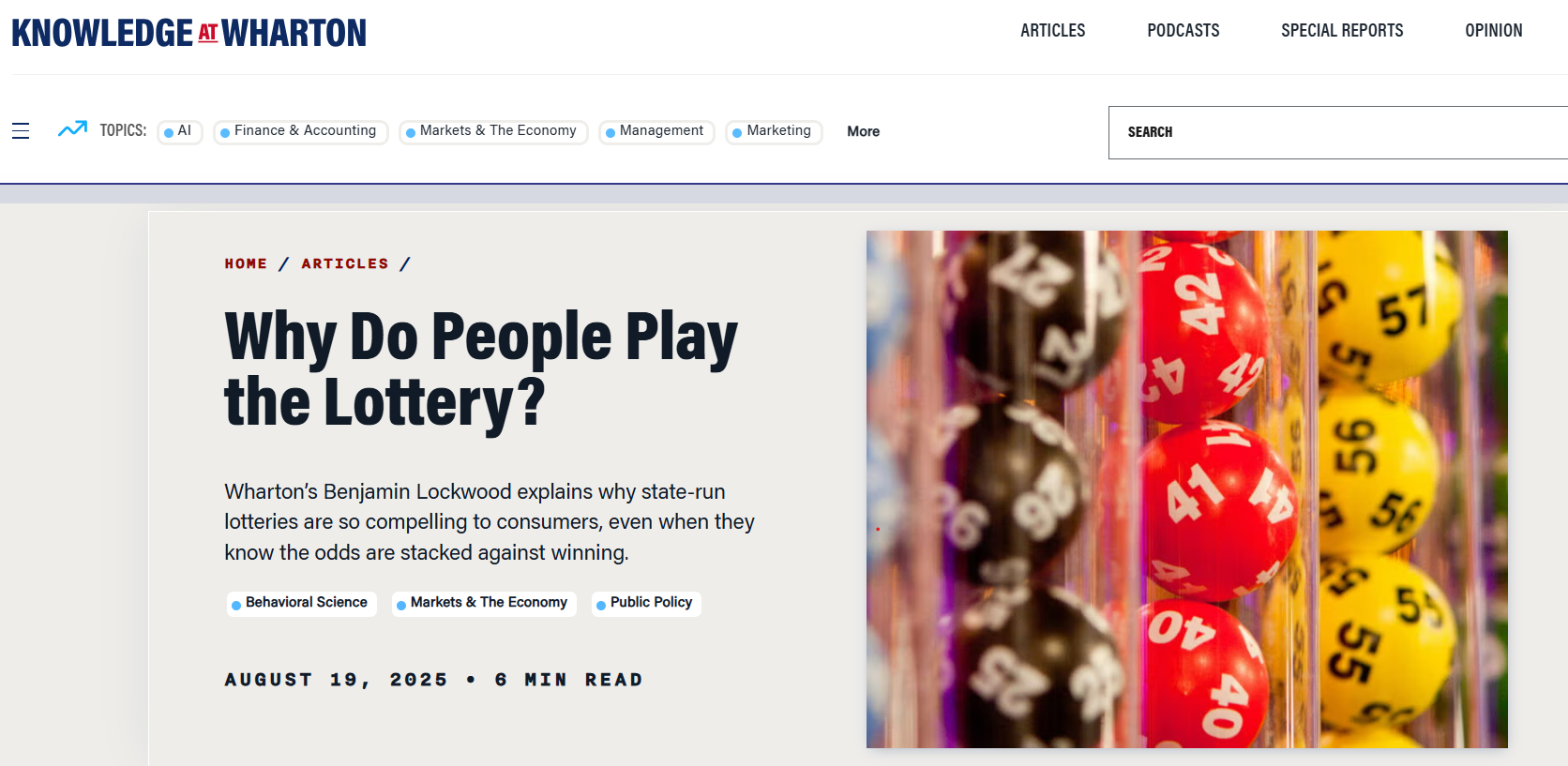

“People enjoy playing the lottery, and it’s important to take that seriously,” says Benjamin Lockwood, a Wharton economist whose research into state-run lotteries found that people value the experience itself, not just the chance of winning.

Related: Pudgy Penguins expands retail footprint with Target trading card rollout

Meir Statman, the behavioral finance pioneer and professor at Santa Clara University and author of A Wealth of Well-Being, tells Magazine:

“There is a parallel to ‘onchain gacha’ in people bidding on the contents of abandoned storage units. Most find items worth placing in the trash, but some find items they can sell on eBay. One found a painting worth hundreds of thousands of dollars. These combine hope for riches with playfulness. This is what lotteries offer.”

Two sides to every story

Why do people play the lottery? Source: Knowledge at Wharton

There are two sides to the FWA protocol.

NFT holders become liquidity providers (LPs), depositing collectibles alongside ETH and earning a share of the fees while their position remains in the pool.

Players, meanwhile, pay for the chance to pull a randomly selected NFT, deciding afterwards whether to keep it or redeem most of its attached ETH value instead. (Blockworks Research notes that at present, around 70% of purchasers choose to convert their winnings to FWA.)

As 2Lambroz explains, LPs are effectively hoping their NFT stays in the pool long enough to earn fees before it’s selected, while players are chasing the chance of landing a prize worth far more than the cost of a spin.

FWA: The two sides. Source: 2Lambroz

Self-proclaimed Ethereum maxi, Materkel says:

“The most fun NFT/casino primitive in over a decade of crypto, where users actually get to be both players and the house at the same time […] Money legos on Ethereum are back!”

Can the hype last?

While Dedic believes much of the activity relates to token incentives, he says he’s “very bullish on gamified commerce for a generational reason.”

“The further Gen Z moves into being the generation with the strongest buying power, the more shopping is going to be gamified and come with a dopamine kick attached.”

And rather than offering random NFTs from last cycle, Dedic believes the mechanism is better suited to assets people already want to own, such as collectibles like Pokémon cards, watches and even whiskey.

“I see enormous potential in selling much-demanded assets in a gamified way,” he says. “I see very little in building Ponzi schemes to create demand for assets nobody wanted in the first place.”

The real test will come when the novelty wears off and the incentives fade. If users keep spinning anyway, onchain gacha may have found a retail use case crypto has been searching for all along. If not, they’ll join the dumpster fire of failed crypto experiments that burned brightly before fading away.

Magazine: The 100x obsession: Fundamentals grow in importance as crypto matures

Cointelegraph publishes long-form journalism, analysis and narrative reporting produced by Cointelegraph’s in-house editorial team with subject-matter expertise. All articles are edited and reviewed by Cointelegraph editors in line with our editorial standards. Some articles contain affiliate links, from which Cointelegraph may earn a commission. These relationships do not influence which products we review or our editorial conclusions. Content published in here does not constitute financial, legal or investment advice. Readers should conduct their own research and consult qualified professionals where appropriate. Cointelegraph maintains full editorial independence.

Morgan Stanley downgraded shares of Circle Internet (CRCL) to underweight from equal-weight on Monday and cut its price target to $38 from $106, citing a weaker long-term earnings outlook.

The stock, which slid 6% following the report, has fallen about 30% year-to-date, reflecting growing investor concern over the outlook for USDC, the company’s dollar-backed stablecoin and its largest source of revenue.

Analyst James Faucette said Morgan Stanley expects slower USDC growth as reserve income comes under pressure and Circle shifts toward lower-margin transaction revenue.

“We downgrade Circle, as USDC contraction exposes reserve income sensitivity and points to a lower-margin shift toward transaction revenue,” Faucette wrote in a research note.

The bank reduced its USDC supply forecasts by roughly 33% for 2027 and 44% for 2028, resulting in GAAP earnings-per-share estimates that are about 3% below Wall Street consensus in 2027 and 20% below consensus in 2028.

Morgan Stanley also pointed to rising competition from tokenized money market funds and tokenized deposits, which could reduce both USDC balances and the revenue Circle earns on reserves.

Bitmine Immersion Technologies, the largest global owner of ETH, has continued with its aggressive accumulation strategy by adding 10,399 coins over the past week.

Its treasury has consistently increased over the past year and now stands at 5,797,813 ETH – just shy of the 5.8 million milestone.

Another Big Purchase

The press release shared by the former BTC miner reads that its crypto holdings, cash, and other investments total approximately $11.3 billion. Ethereum’s stash alone is currently valued at around $10.9 billion given the asset’s retreat from over $1,900 to under $1,850. Bitmine holds 4.8% of Ethereum’s circulating supply and cemented its position as the largest corporate holder of the asset.

Moreover, it has reduced the gap with the overall leader in the cryptocurrency space, Strategy. The Saylor-co-founded company has not only halted its BTC purchases, but has just announced its third sale of the year.

According to Bitmine Chairman Tom Lee, the firm has increased its ETH position every single week since it adopted the Ethereum treasury strategy on June 30 last year. Speaking on the most recent Ethereum market performance, in which the altcoin managed to outperform BTC and many other alts, Lee noted that it’s a clear sign its fundamentals continue to improve.

Moreover, he claimed that ETH outperformed the Nasdaq 100 by 25% in July, which, as we reported during the weekend, made it the asset’s strongest month in a year.

“In July, ETH outperformed the Nasdaq 100 by 2,500bp (or 25 percentage points). This is the largest outperformance since July 2025, and we believe it is reflective of the strengthening fundamentals of crypto. Last July (2025), ETH rose from $2,375 to $4,057 by the end of August,” stated Lee.

Staking Progress

Beyond accumulating ETH, the company continues expanding its staking operations through its institutional-grade platform called MAVAN. It has already deployed 4.92 million ETH to work, representing 85% of its entire treasury. Based on current yields, Bitmine projects approximately $291 million in annual staking rewards and $247 million in annualized staking revenue.

The post Bitmine Buys Another 10,399 ETH, Treasury Nears 5.8 Million Coins appeared first on CryptoPotato.

Crypto World

DeFi for Agricultural Finance: Cultivating the Future of Farming Through Decentralized Finance

Agriculture has always been the backbone of civilization, feeding billions while supporting the livelihoods of nearly 30% of the global workforce. Yet despite its importance, farmers—especially smallholder farmers—continue to face significant financial challenges. Limited access to credit, expensive intermediaries, slow cross-border payments, and lack of insurance often prevent agricultural businesses from reaching their full potential.

Enter Decentralized Finance (DeFi)—a blockchain-powered financial ecosystem that removes traditional intermediaries and enables transparent, permissionless financial services. While DeFi is commonly associated with cryptocurrency trading and lending, its potential extends far beyond digital assets. One of its most promising frontiers is agricultural finance, where blockchain technology could revolutionize how farmers access capital, manage risk, and participate in global markets.

As climate change, food security, and financial inclusion become increasingly urgent global issues, DeFi may offer the infrastructure needed to build a more resilient agricultural economy.

The Financial Challenges Facing Farmers

Agriculture is inherently risky. Farmers depend on weather conditions, fluctuating commodity prices, disease outbreaks, and seasonal income. Unfortunately, traditional financial institutions often view agriculture as a high-risk sector, resulting in:

- Limited access to affordable loans

- High interest rates

- Excessive paperwork

- Long approval processes

- Lack of collateral for smallholder farmers

- Expensive crop insurance

- Delayed international payments

In many developing countries, millions of farmers remain unbanked, making it difficult to secure financing needed for seeds, fertilizer, equipment, or irrigation.

What is DeFi?

Decentralized Finance, or DeFi, is a financial ecosystem built on blockchain networks using smart contracts instead of centralized institutions. Rather than relying on banks, DeFi platforms allow users to borrow, lend, trade, insure assets, and earn yield directly through decentralized protocols.

Key characteristics include:

- Permissionless access

- Transparent transactions

- Global availability

- Programmable financial products

- Lower transaction costs

- 24/7 accessibility

For agriculture, these features create opportunities to remove long-standing financial barriers.

How DeFi Can Transform Agricultural Finance

1. Permissionless Lending for Farmers

Traditional agricultural loans often require credit history, land titles, or extensive documentation. Many small-scale farmers simply cannot meet these requirements.

DeFi lending platforms could enable farmers to access capital through blockchain-based lending pools where lenders earn yield while borrowers receive funding more efficiently.

Potential benefits include:

- Faster loan approvals

- Reduced administrative costs

- Global liquidity access

- Transparent lending terms

- Fractional financing

Future innovations may incorporate decentralized identity systems and on-chain farming records to improve credit assessment without relying solely on conventional collateral.

2. Tokenizing Agricultural Assets

One of blockchain’s most innovative features is asset tokenization.

Real-world agricultural assets can potentially be represented as digital tokens, including:

- Crop inventories

- Grain storage

- Coffee harvests

- Livestock

- Farmland ownership

- Agricultural equipment

Tokenization enables fractional ownership, making agricultural investments accessible to a broader range of investors while allowing farmers to unlock liquidity without selling their entire assets.

3. Decentralized Crop Insurance

Weather remains one of agriculture’s greatest uncertainties.

Traditional insurance claims may take weeks—or even months—to process.

Blockchain-based insurance powered by smart contracts can automatically execute payouts when predefined conditions are met.

For example:

- Rainfall falls below a specified threshold.

- Temperature exceeds critical levels.

- Flood data reaches predefined limits.

Using trusted data sources (oracles), farmers could receive automatic compensation without lengthy claim investigations.

This automation reduces operational costs while improving trust and efficiency.

4. Stablecoins for Agricultural Payments

Farmers frequently face payment delays, particularly in international trade.

Stablecoins offer a faster alternative for:

- Export payments

- Supplier settlements

- Equipment purchases

- Cross-border remittances

Instead of waiting several days for international bank transfers, blockchain transactions can settle within minutes while maintaining lower fees.

For farmers operating in regions with volatile local currencies, stablecoins may also provide greater financial stability.

5. Supply Chain Transparency

Consumers increasingly want to know where their food comes from.

Blockchain technology allows every stage of agricultural production to be recorded immutably.

Information can include:

- Farm origin

- Harvest dates

- Transportation records

- Storage conditions

- Certifications

- Quality inspections

Combined with DeFi, this transparency could enable financing tied directly to verified production milestones, reducing fraud and improving trust among buyers, suppliers, and lenders.

6. Yield Farming Beyond Crypto

The concept of “yield” takes on a new meaning in agriculture.

Future DeFi protocols may allow investors to fund seasonal farming operations in exchange for a portion of harvest profits.

Instead of speculative investments alone, capital could directly support food production while offering returns linked to agricultural performance.

Although still an emerging concept, such models could create entirely new financing mechanisms for rural economies.

Real-World Applications

Several blockchain initiatives are already exploring agriculture-focused financial services:

Supply Chain Financing

Blockchain improves visibility into agricultural supply chains, enabling lenders to provide financing with greater confidence.

Carbon Credit Markets

Farmers practicing sustainable agriculture can tokenize verified carbon credits and sell them on decentralized marketplaces.

Weather Data Integration

Smart contracts connected to trusted weather oracles enable automated insurance and risk management products.

Commodity Tokenization

Agricultural commodities such as wheat, rice, coffee, and cocoa could eventually be represented as digital assets for trading and financing.

Benefits of DeFi in Agriculture

The integration of decentralized finance into agriculture offers several advantages:

Greater Financial Inclusion

Farmers without traditional banking relationships may gain access to financial services using only a smartphone and internet connection.

Lower Costs

Removing intermediaries can reduce transaction fees, lending costs, and administrative overhead.

Faster Transactions

Loans, insurance payouts, and international payments can settle significantly faster than conventional financial systems.

Transparency

Immutable blockchain records reduce fraud while improving accountability across agricultural supply chains.

Global Investment Opportunities

Investors worldwide may gain exposure to agricultural assets without geographic limitations.

Challenges That Must Be Addressed

Despite its promise, DeFi adoption in agriculture faces important hurdles.

Regulatory Uncertainty

Many jurisdictions are still developing legal frameworks for tokenized assets and decentralized finance.

Internet Accessibility

Reliable internet access remains limited in many rural farming communities.

Digital Literacy

Farmers need education and user-friendly tools to safely interact with blockchain technology.

Oracle Reliability

Smart contracts depend on accurate external data. Reliable oracle infrastructure is essential for insurance and financing applications.

Volatility

While stablecoins help reduce cryptocurrency price fluctuations, broader crypto market volatility remains a consideration for DeFi ecosystems.

The Road Ahead

The future of agricultural finance may lie in combining blockchain technology, decentralized finance, artificial intelligence, satellite imagery, and IoT sensors into integrated financial ecosystems.

Imagine a future where:

- AI predicts crop yields.

- Satellite data verifies farm conditions.

- Smart contracts automatically issue loans.

- Weather events trigger instant insurance payouts.

- Harvests are tokenized and financed globally.

- Carbon credits generate additional income for sustainable farming.

This vision represents a more connected, transparent, and inclusive agricultural economy.

Conclusion

Agriculture feeds the world, yet millions of farmers remain underserved by traditional financial systems. Decentralized Finance offers a compelling alternative by expanding access to capital, streamlining payments, enabling programmable insurance, and increasing transparency across supply chains.

While challenges around regulation, infrastructure, and adoption remain, the convergence of DeFi and agriculture has the potential to reshape rural finance and strengthen global food systems. By leveraging blockchain technology, farmers could gain greater financial independence, investors could discover new opportunities, and agricultural markets could become more resilient and efficient.

As DeFi continues to evolve beyond digital assets, agricultural finance stands out as one of its most impactful real-world applications—one that could help cultivate a more sustainable and financially inclusive future.

REQUEST AN ARTICLE

The Clarity Act is widely viewed as the crypto industry’s most important piece of U.S. legislation, with supporters arguing it would establish clear rules for digital assets, reduce regulatory uncertainty and unlock broader institutional adoption. Analysts say passage would improve market sentiment by giving banks, asset managers and exchanges greater confidence to invest in blockchain infrastructure and expand crypto products.

Bernstein’s analysts said they expect regulators to move more quickly on token classifications, decentralized finance (DeFi) guidance, self-custody rules and innovation exemptions for token issuance, while continuing to support tokenization, crypto derivatives and prediction markets.

The Clarity Act remains strategically important because it would provide permanent regulatory certainty, encourage banks, broker-dealers and exchanges to invest in blockchain infrastructure, clarify the division between securities and commodities oversight and establish a long-term framework for decentralized finance and digital assets regardless of future political administrations, the report said.

Even if the legislation stalls, the broker expects the crypto industry’s political influence to remain strong ahead of the U.S. midterm elections and sees the current downturn ending in late third or early fourth quarter, helped by the prospect of further White House policy support.

For listed companies, failure to pass the bill would preserve the status quo for stablecoin regulation.

Introduction

For much of its history, cryptocurrency has been associated with one thing: speculation. Headlines focused on soaring prices, dramatic crashes, meme coins, and traders chasing the next 100x opportunity. While speculation fueled early adoption and liquidity, it also overshadowed blockchain’s true potential.

Today, that narrative is changing.

The crypto industry is steadily transitioning from a market driven primarily by price movements to one powered by real-world utility. Institutions, governments, businesses, and millions of everyday users are beginning to leverage blockchain technology for payments, financial services, identity, supply chains, gaming, artificial intelligence, and countless other applications.

The next chapter of crypto isn’t about buying low and selling high—it’s about solving global problems.

Between 2017 and 2024, the cryptocurrency market experienced explosive growth largely driven by speculation.

Characteristics of this period included:

- Retail investors chasing rapid gains

- Meme coin booms

- NFT hype cycles

- Leveraged trading

- Frequent market bubbles

- Extreme volatility

Although these cycles attracted millions of new users, they also created the misconception that crypto had little purpose beyond trading.

Ironically, speculation played an important role by funding innovation. Capital flowed into blockchain startups, decentralized applications (dApps), infrastructure providers, and developer ecosystems that are now laying the foundation for real-world adoption.

Instead of asking:

“Which coin will 100x?”

The market is increasingly asking:

“Which blockchain solves real problems?”

This shift marks one of the biggest transformations in crypto’s history.

Utility creates sustainable demand because people use blockchain regardless of market conditions.

Examples include:

- Cross-border payments

- Stablecoin settlements

- Decentralized finance (DeFi)

- Tokenized real-world assets

- Digital identity

- Gaming economies

- Supply chain verification

- Machine-to-machine payments

- AI infrastructure

- Decentralized cloud computing

These applications generate economic activity independent of speculative trading.

Perhaps no crypto product demonstrates utility better than stablecoins.

Millions of users now rely on stablecoins to:

- Send money internationally

- Protect savings from inflation

- Pay freelancers

- Trade digital assets

- Access dollar-denominated finance

- Settle transactions instantly

Businesses increasingly prefer blockchain settlements because they reduce costs while operating 24/7.

Stablecoins have quietly become one of crypto’s most practical and widely adopted use cases.

Decentralized Finance has matured far beyond yield farming.

Modern DeFi enables:

- Lending

- Borrowing

- Decentralized exchanges

- Prediction markets

- Bond issuance

- Treasury management

- Derivatives

- Cross-chain liquidity

- Automated investment strategies

Rather than replacing banks overnight, DeFi is becoming an open financial layer that anyone with an internet connection can access.

For regions with limited banking infrastructure, this represents a major leap toward financial inclusion.

Another major catalyst is the tokenization of real-world assets (RWAs).

Assets such as:

- Government bonds

- Stocks

- Real estate

- Commodities

- Private credit

- Carbon credits

- Intellectual property

can increasingly be represented as blockchain-based tokens.

Benefits include:

- Fractional ownership

- Instant settlement

- Greater transparency

- Lower administrative costs

- Global accessibility

- Improved liquidity

Tokenization is bridging traditional finance and decentralized infrastructure rather than forcing them to compete.

For years, critics argued that crypto was too slow or volatile for everyday payments.

That is changing rapidly.

Modern blockchain networks now offer:

- Near-instant settlements

- Low transaction fees

- Global interoperability

- Mobile wallet integration

- Merchant payment solutions

- Stablecoin-based transactions

Consumers may soon use blockchain without even realizing it, much like most people use the internet today without understanding TCP/IP.

The technology becomes invisible while the experience improves.

Blockchain utility extends beyond finance.

Decentralized identity solutions allow users to control their digital credentials without relying entirely on centralized platforms.

Applications include:

- Educational certificates

- Medical records

- Professional licenses

- Voting systems

- Identity verification

- Digital passports

Privacy-enhancing technologies like Zero-Knowledge Proofs (ZKPs) and Fully Homomorphic Encryption (FHE) are enabling secure verification without exposing sensitive personal information, making blockchain more practical for enterprises and governments alike.

Artificial intelligence increasingly requires decentralized infrastructure.

Blockchain provides:

- Verifiable data

- Transparent payments

- Permissionless marketplaces

- Decentralized compute networks

- Incentive systems

- Trustless coordination

Meanwhile, AI can improve blockchain through:

- Smart contract auditing

- Fraud detection

- Governance analysis

- Automated trading

- Personalized financial tools

Together, AI and blockchain form a powerful foundation for the next generation of digital services.

Institutional adoption has accelerated significantly.

Major financial institutions are exploring:

- Tokenized funds

- Digital asset custody

- Stablecoin infrastructure

- Blockchain settlement systems

- Asset tokenization

- Digital securities

Meanwhile, governments are experimenting with blockchain for:

- Public records

- Tax reporting

- Supply chain management

- Digital identity

- Land registries

- Central Bank Digital Currencies (CBDCs)

The conversation has shifted from “Should we use blockchain?” to “How do we integrate blockchain responsibly?”

Despite significant progress, challenges remain.

The industry must continue improving:

- User experience

- Wallet security

- Regulatory clarity

- Cross-chain interoperability

- Scalability

- Consumer protection

- Education

- Developer tooling

Mass adoption will depend not only on technological breakthroughs but also on making blockchain products simple enough for everyday users.

The future of crypto will likely be measured less by token prices and more by real-world impact.

Success won’t come from speculation alone, but from building systems that people rely on every day.

As blockchain becomes embedded in payments, finance, commerce, AI, gaming, healthcare, and digital identity, users may interact with crypto-powered services without ever thinking about the underlying technology.

That’s often the hallmark of transformative innovation: it fades into the background while making everyday life more efficient.

Final Thought

Crypto is evolving beyond its speculative roots into a global utility layer for the digital economy. While market cycles and price volatility will always be part of the ecosystem, long-term value is increasingly being created through practical applications that improve how people move money, verify identity, access financial services, and exchange value across borders.

The transition won’t happen overnight, but the direction is becoming clear. The next wave of blockchain adoption will be driven not by hype, but by usefulness. And as more industries embrace decentralized technologies, crypto’s greatest achievement may not be creating the next billion-dollar token—it may be quietly becoming the infrastructure that powers the world’s digital future.

REQUEST AN ARTICLE

Last week, hackers discovered a five-year-old bug in Coldcard software and used it to drain over 1,158 BTC worth over $72 million from over 2,600 addresses.

By Sunday, the tally rose to 1,359 BTC and continues to rise today.

A rudimentary dashboard is charting the rising number of thefts, with many security experts warning of additional waves of attacks.

The essence of the bug is that, despite claims by Coldcard’s manufacturer and documentation, many of its devices didn’t actually use a true random number generator (RNG) with sufficient entropy to protect users trusting the device to generate private keys and seed phrases.

Instead, the device used a fallback, a pseudo RNG, with far lower entropy.

Unfortunately, trivial amounts of computation can guess these low entropy seed phrases generated by Coldcard devices.

Once in possession of these private keys, a quick scan of the blockchain reveals associated public keys holding BTC, and hackers then steal those funds.

The bug has existed since March 2021, but security researchers only publicly discovered it last week. As theft transactions began, customers and members of the community began to track the horrifying timeline of events.

As brute-force attacks continue to crack private keys, here’s a summary of the series of events that led up to the ongoing catastrophe.

Read more: Crypto wallet seeds crackable with gaming PC via this security flaw

Timeline of the Coldcard hack

6 years ago

November 18, 2020, 19:19 UTC: There are disputed histories and allegations about Coldcard maker Coinkite’s motivation during this time to end its commitment to free and open source software (FOSS).

In any case, by late 2020, Coinkite announced its intention to restrict commercial use of its firmware (on-device software), and by early 2021, the company began migration to a new software license.

It would develop a proprietary library called “libNgU.”

5 years ago

March 1, 2021, 14:03 UTC: Coinkite commits code titled “First pass w/ libNgU,” its final step away from FOSS and moving Coldcard firmware (on-device sofware) onto its proprietary library, libNGU.

5 years ago

March 29, 2021, 19:27 UTC: Firmware 4.0.1 reaches owners as the first public build with the flaw. Coldcard devices shipping with or upgrading to this new firmware would begin generating insecure seed phrases.

The bug of pseudo RNG on versions 4.0.1 and later would persist on Coldcard software for over five years from March 29, 2021 through July 30, 2026.

5 days ago

July 30, 2026, 01:10 UTC: Bitcoin block 960,183 includes the first Coldcard hack transactions from a hacker.

4 days ago

July 30, 2026, 13:19 UTC: A user posts the first widely read account to Reddit, “Full panic — one of my wallets was drained.”

4 days ago

30 July 2026, 17:35 UTC: Kevin Loaec, a BTC security researcher, asks his followers to check their balances. “I’m hearing a potential issue with some Coldcard wallets being drained,” he wrote. “I will not FUD, but would like to get at least reports of trusted people.”

4 days ago

30 July 2026, 18:58 UTC: Less than 90 minutes later, Loaec drops the hedge. “Alright I’m convinced THIS IS NOT A DRILL.”

4 days ago

30 July 2026, 22:50 UTC: The official Coldcard social media account publishes a Mk3-only advisory that has since drawn more than two million views.

It would claim “Mk4, Q and Mk5 are not affected based on our early analysis,” which would later turn out to be false.

On its website, Coinkite formally discloses the vulnerability and quickly publishes a bug patch via firmware 4.2.0.

3 days ago

July 31, 2026, 01:49 UTC: A Block engineer circulates its independent analysis of the incident, which identifies the root cause.

“COLDCARD firmware contains an RNG integration error that causes ngu.random to use MicroPython’s deterministic Yasmarang fallback instead of the STM32 hardware RNG.”

3 days ago

July 31, 2026, 04:54 UTC: Block 960,345 inclues additional theft transactions, which would continue for another four hours.

3 days ago

July 31, 2026, 06:46 UTC: Coinkite posts a technical disclosure widening the scope to its Mk4, Mk5, and Q Coldcard devices.

3 days ago

July 31, 2026, 08:36 UTC: Block 960,369 carries another drain of funds alongside 250 others.

3 days ago

July 31, 2026, 13:19 UTC: Kevin Loaec, another security researcher, warns that more theft transactions are underway.

3 days ago

July 31, 2026, 13:43 UTC: Coinkite releases Mk3 firmware 4.2.0. It emphasizes that the update will fix new private key generations but cannot repair a past, compromised seed phrase.

3 days ago

July 31, 2026, 15:42 UTC: Coinkite co-founder and chief executive Rodolfo Novak apologizes in an open letter. “We take full accountability for the firmware bug and we offer our sincere apologies to those affected.”

3 days ago

July 31, 2026, 16:30 UTC: Bitcoin Core contributor Antoine Poinsot tells his followers the scope is wider than Coinkite initially admitted.

“Coldcard MK3, MK4, MK5 and Q are being drained. A bug lets attackers find your seed phrase without any action on your part.”

3 days ago

July 31, 2026, 16:39 UTC: Coinkite concedes that seed phrases from compromised firmware carry “about 72 bits of entropy rather than the expected 128 bits.”

3 days ago

July 31, 2026, 17:42 UTC: Block engineering lead Clay Garrett claims that an attacker queried source addresses through a paid account at a blockchain data provider, raising the possibility that customer records from the company might assist law enforcement.

“Their internal logs matched the suspected workflow with extraordinary specificity, including the number, timing and sequence of requests.”

4 days ago

July 31, 2026, 18:27 UTC: Chainalysis, a US government contractor and forensic blockchain service, said, “Our team is actively monitoring the exploiter wallet and a consolidation address.”

3 days ago

July 31, 2026, 23:17 UTC: A developer launches a vibe-coded webite as a free dashboard counting the drained BTC. The website is helpful yet incomplete.

2 days ago

August 1, 2026, 12:29 UTC: Security researcher Loaec confirms that hackers are draining newer models. “It’s happening. Mk4, Mk5, Q are now actively drained,” he notes while publishing a detailed incident analysis.

2 days ago

August 1, 2026 18:38 UTC: Galaxy Research estimates ongoing losses from the Coldcard hack exceed 1,367 BTC from 4,585 addresses.

Coldcard contained a true RNG generator that was never properly switched on, so its physical entropy didn’t actually matter for the majority of customers over five years.

Devices fell back to a pseudo RNG generator and produced seed phrases that merely appeared to be secure.

The largest consolidation address belonging to the hacker(s) holds 562 BTC and had not spent outputs. That’s the only good news due to the possibility of that inaction indicating a potential law enforcement apprehension of the perpetrator(s).

Many victims have filed police and FBI reports or similar law enforcement submissions around the globe.

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

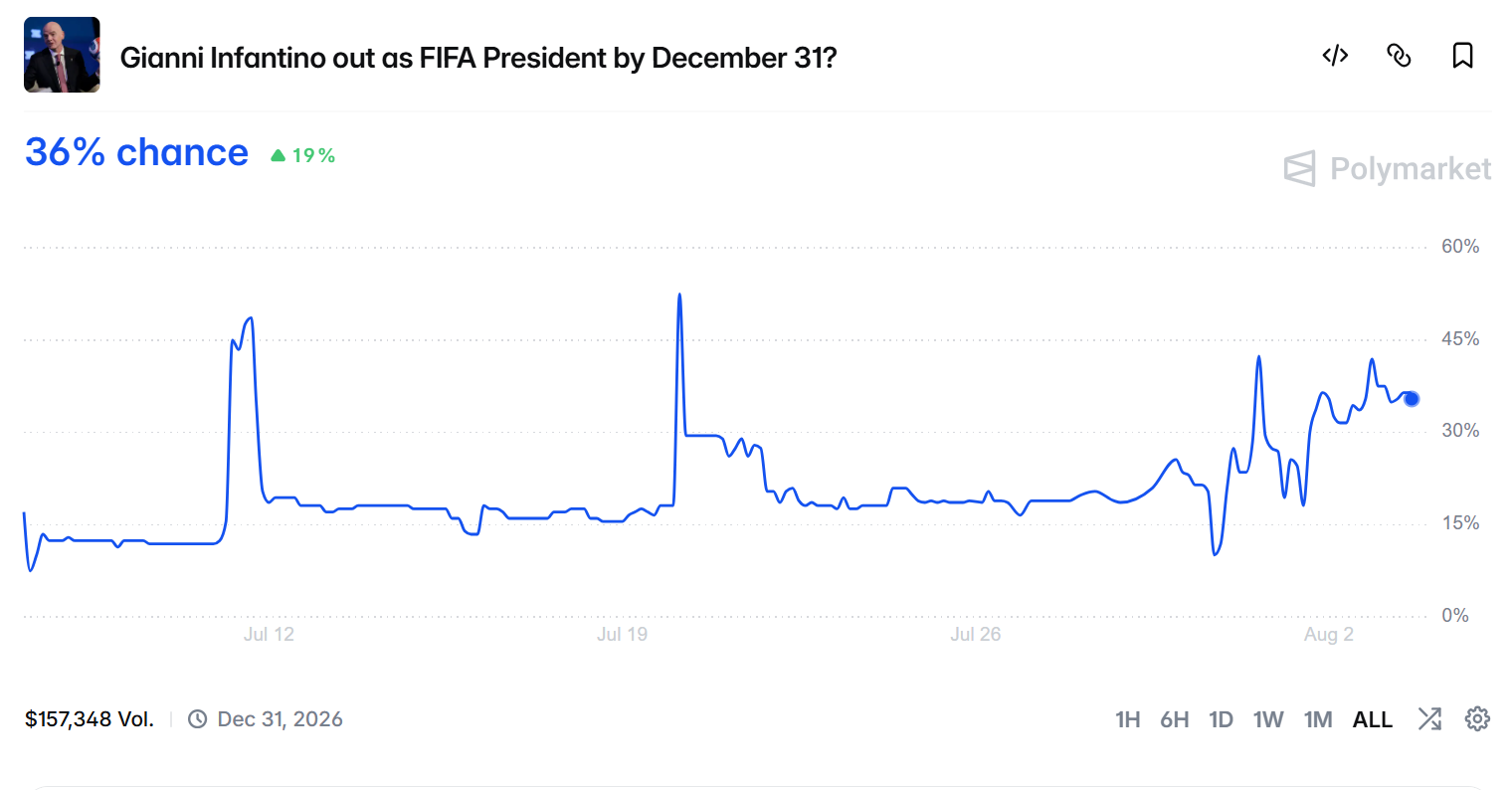

FIFA President Gianni Infantino has reportedly asked the Trump administration to help him keep his job, arranging a call with Secretary of State Marco Rubio, the New York Post reported Monday.

Polymarket traders price his exit by December 31 at 36.5%, up from roughly 19% a week ago. Almost all of the contract’s lifetime volume arrived in the past seven days.

Why Infantino Thinks Trump Owes FIFA a Favor

The reported ask lands four weeks after FIFA handed the White House a win. Its disciplinary committee cleared Folarin Balogun for Belgium, suspending the striker’s automatic red card ban on probation.

Trump had pushed for the reversal and claimed credit for it publicly.

“Thank you to FIFA for doing what was right, and reversing a great injustice!” Trump wrote on Truth Social.

Rubio is not a cold call. He sat in the Oval Office with Trump and Infantino last November. The occasion was a task force meeting on the World Cup.

FIFA’s bridge into that room is now gone. Carlos Cordeiro, the former Goldman Sachs banker who represented FIFA on the task force, resigned Friday over the sale plan. He had joined Infantino on repeated White House visits.

BeInCrypto could not independently verify the Rubio call, which the Post attributed to two people familiar with it.

Polymarket Traders Price the Fallout

The market read the revolt faster than the headlines did. It still traded near 20% on the afternoon of July 30. That was when all 55 UEFA member associations unanimously backed a boycott.

It broke above 40% the following day, once Infantino’s own executives turned on him. Chief operating officer Kevin Lamour told the Associated Press that staff had been deceived.

“It is the project of one person,” Kevin Lamour, chief operating officer of FIFA, in a statement to the Associated Press.

Follow us on X to get the latest news as it happens

Volume backs the repricing. The contract has handled $156,400 since it opened on July 6, and $151,700 of that traded in the past week. Open interest sits near $76,000.

The expiry date shapes how traders read it. The contract pays out only on a departure before December 31, while FIFA’s election falls next March. Challengers have until November 18 to declare, so the market is pricing resignation rather than defeat.

The asset in dispute is large. Cordeiro put FIFA’s revenue at $15 billion over the World Cup cycle. Josh Kushner’s fund offered $4.2 billion for 20% of a new FIFA subsidiary.

Crypto already has a claim on that value. The tournament drove $20 billion in World Cup prediction volume, Chainalysis found. FIFA’s own collectibles platform cleared at least $6 million in fees.

Whether Rubio’s call buys Infantino anything should show up in the odds before it shows up in a FIFA statement.

The post Infantino Wants to Collect on Trump’s World Cup Favor but Polymarket Says He’s 36% Out appeared first on BeInCrypto.

Miller’s previous controversies

Before being elected to the House in 2022, Miller spent six years in the Marine Corps Reserve. He also previously served in Trump’s first-term Administration, including as a senior advisor to the President.

Politico and the Washington Post have previously reported on Miller’s run-ins with the law as a young adult, including charges, which were later dismissed, for underage drinking, assault, disorderly conduct, and resisting arrest.

From 2019 to 2020, Miller dated Stephanie Grisham, a White House press secretary during Trump’s first-term Administration. Grisham has also accused Miller of abuse: she wrote in a 2021 op-ed for the Post and in a memoir the same year, without naming Miller, that her relationship with a White House staffer had “turned abusive” and that she had told Trump himself about her former partner who had “anger issues and a violent streak.”

The partner was later identified as Miller, who then sued Grisham for defamation, though he voluntarily dropped the suit in 2023 as part of a confidential settlement agreement.

BlackRock, the world’s largest asset manager, has expanded its tokenized cash platform, introducing a couple of new tokenized money market products, the firm said on Monday.

Back in May of this year, BlackRock filed for the new products with the U.S. Securities and Exchange Commission (SEC).

BlackRock is offering onchain shares of the BlackRock Select Treasury Based Liquidity Fund (BSTBL), a tokenized share class on Ethereum for an existing BlackRock money market fund. In addition, a new BlackRock Daily Reinvestment Stablecoin Reserve Vehicle (BRSRV) has also been unveiled with daily dividend reinvestment and access across multiple blockchains, said BlackRock in a press release.

Both funds intend to qualify as eligible reserve assets for permitted U.S. payment stablecoin issuers under the GENIUS Act, the asset manager said.

The move deepens BlackRock’s push into tokenized finance, blockchain-based representations of traditional financial assets such as funds, bonds or equities. Advocates say the technology can speed up settlement, enable round-the-clock trading and improve transparency.

NDIS support services provider 4lifeskills calls in administrators

How Fake World Assets Became Crypto’s Latest Craze

Brand New Day’ Is Officially Coming to IMAX

-

Business5 days ago

Business5 days agoWhy Trees Belong on the Risk Register

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: Wit & Wisdom

-

Politics3 days ago

Politics3 days agoMeta enters AI-training agreement with far-right ‘propaganda rag’ Newsmax

-

Entertainment6 days ago

Entertainment6 days ago‘Stargate’ Creator’s New Sci-Fi Series Returns for Season 3 Tomorrow

-

Crypto World2 days ago

Crypto World2 days agoMicroStrategy Post-Earnings CLARITY Act Push Could Add New Catalyst for Its Stock

-

Politics6 days ago

Politics6 days agoThe Part of the Electric Transition Nobody Wants to Discuss

-

Business5 days ago

Business5 days agoMajor shareholder moves on Canyon

-

Crypto World2 days ago

Crypto World2 days agoXRP Ledger v3.3.0 brings five institutional features

-

News Videos4 days ago

News Videos4 days agoBitcoin Enters the 3rd Stage of the Bear Market

-

Crypto World6 days ago

Crypto World6 days agoKraken Enables Retail Access to Jersey Mike’s IPO via Tokenized Shares

-

Tech7 days ago

Tech7 days agoNew macOS Sequoia & Sonoma security updates for older Macs

-

Politics4 days ago

Politics4 days agoLuke Littler’s dominance sparks GOAT debate

-

News Videos6 days ago

News Videos6 days agoClaude: Build Financial Dashboards in Minutes (2026)

-

Business6 days ago

Business6 days agoJohnson & Johnson agrees to $5.5B settlement over talc cancer claims

-

Sports4 days ago

Sports4 days agoSeema Kaliramna Wins Discus Throw Bronze, Takes India’s CWG Medals Tally To 17

-

Crypto World1 day ago

Crypto World1 day agoCrypto PAC spending tops $2M in Michigan House race

-

Business3 days ago

Business3 days agoTrump Announces Hamas Disarmament Agreement as Iran Strikes Kuwait Air Base and US Attacks Pause Overnight

-

Tech5 days ago

Tech5 days agoGemini can now summarize the messiest comment threads in Google Docs

-

Crypto World3 days ago

Crypto World3 days agoNew York sues Kalshi over prediction market gambling

-

Tech1 day ago

Tech1 day agoESET tracks rise in malicious AI skills and adaptable malware

You must be logged in to post a comment Login