Crypto World

Saylor’s Strategy (MSTR) sold bitcoin (BTC). These crypto treasuries are still buying

Strategy (MSTR), the company whose bitcoin accumulation strategy inspired a new generation of so-called digital asset treasury firms, sold BTC for the first time since December 2022, offloading roughly $2.5 million worth of tokens.

The move came as the scheme has faced major headwinds since gaining popularity last year.

Dozens of companies raised capital through stock and debt offerings to buy bitcoin, ether (ETH) and other cryptocurrencies, aiming to replicate Michael Saylor’s playbook. The model worked for a while last year as crypto prices surged and treasury stocks traded at premiums to their underlying values.

However, that all changed as crypto markets peaked in October. As token prices fell and treasury stocks slipped below net asset value, many firms lost the ability to raise capital on attractive terms, and some stocks fell more than 90% from their peak. Some stopped buying, while others turned into sellers.

Through all that, Strategy held strong and kept buying as its Executive Chairman, Michael Saylor, continued to advocate for buying and holding.

But that didn’t hold for long. Strategy first alluded to a potential sale earlier in May and then finally reported the first sale on Monday, June 1. With Strategy breaking its accumulation streak and many peers stepping aside, some might think it’s the final nail in the coffin for the treasury firms, as the list of active buyers has now narrowed considerably.

Still buying

However, a few remaining companies continue to buy. Among them is Bitmine (BMNR), Tom Lee’s Ethereum treasury company.

The company purchased roughly $53 million worth of ETH last week and accumulated over 338,000 tokens through May, worth roughly $665 million at current prices. It holds more than 5.4 million ETH, making it the largest corporate holder of the token.

However, Tom Lee said the firm plans to slow its accumulation pace as it approaches its goal of owning 5% of the ETH supply.

Another Ethereum-centric Bit Digital (BTBT) returned to the market in May, buying $20 million worth of ETH. That was the company’s first purchase since October.

Some bitcoin-focused firms are still buying.

Strive (ASST) disclosed acquiring roughly 1,944 BTC in May, spread across multiple purchases, at a cost of about $150 million. Japan’s Metaplanet also reported a purchase in early April, when it acquired 5,075 BTC.

Hyperliquid Strategies (PURR), the treasury firm focused on buying HYPE, the native token of red-hot Hyperliquid blockchain-based exchange and its ecosystem, said it spent $216 million to buy 7.3 million tokens between early December and the end of April. Given HYPE’s surge to record highs, the return on that investment has more than doubled since then.

Despite last week’s sale, Strategy remained one of the largest sources of bitcoin demand through May, purchasing more than 25,000 BTC for over $2 billion.

The sellers

On the other hand, several firms have been reducing crypto holdings recently.

Nakamoto Holdings (NAKA), the bitcoin treasury company led by David Bailey, sold 284 BTC in March, about 5% of its holdings. Empery Digital sold 370 BTC in April to repay a term loan. Genius Group (GNS) said in April it liquidated its remaining 84 BTC to pay down $8.5 million of debt.

Meanwhile, others have abandoned the treasury model entirely.

Forum Markets, formerly known as ETHZilla, shifted its focus to tokenization earlier this year after selling roughly $114 million worth of ether.

VivoPower, which had planned to build an XRP-focused treasury, pivoted to data center and AI infrastructure in February, divesting its Ripple-related investments and XRP holdings.

Read more: Digital asset treasuries must now earn their keep

Vitalik Buterin criticized frontier AI companies for embracing AI nationalism on the same day that Senator Bernie Sanders unveiled a plan to push 50% of those firms into a federal sovereign wealth fund.

The Ethereum (ETH) co-founder posted his rebuke as a quote-reply to the Sanders proposal, which would impose a one-time equity tax on OpenAI, Anthropic, xAI, and other frontier labs and transfer their shares into public ownership.

Bernie Sanders Proposes 50% Public Stake in Top AI Firms

Writing in the New York Times, Sanders outlined the American AI Sovereign Wealth Fund Act, planned for introduction within weeks.

The fund would hold public equity, give the government voting shares, and seat representatives on each company’s board.

Sanders argued that AI is trained on humanity’s collective knowledge, art, code, and conversations, so the wealth should not flow only to a few executives. He named Sam Altman and Elon Musk as figures whose ownership would shrink.

“Let us be clear. Artificial intelligence was not created out of thin air. The data and language used by generative A.I. tools didn’t just pop into Sam Altman’s head or Elon Musk’s imagination…Since A.I. is built on the collective knowledge of humanity, the wealth it generates must benefit humanity. Not just Mr. Musk, Mr. Altman, Dario Amodei and other moguls whose companies are positioned to dominate the industry,” he wrote.

Follow us on X to get the latest news as it happens

The targeted firms, several of which recently entered the trillion-dollar pre-IPO club, have not publicly responded.

The proposal builds on his earlier AI regulation push and on the AI Data Center Moratorium Act, which he co-sponsored with Alexandria Ocasio-Cortez.

Sanders cited Norway’s oil sovereign wealth fund as a precedent.

Vitalik Calls Out AI Nationalism Frame

Against this backdrop, Vitalik Buterin attacked the rhetoric driving frontier AI policy. He argued that labs, which once promised to serve all of humanity, now justify their concentration of power by pointing to China.

“One of the many things I dislike about the style of ‘make AI go well’ discourse from frontier AI companies is how nationalist the whole thing has gotten. In the 2010s, it was: ‘we’re here to benefit all of humanity’. In the 2020s, ‘we’re here to benefit all of 4% of humanity’,” the Ethereum executive stated.

His earlier writing on Vitalik AI totalitarian risks pushed back against zero-sum framings. The US-China AI race has dominated industry lobbying.

Legal Experts Warn of Public Backlash

Kevin Frazier, a law professor focused on AI policy, said Sanders’ essay reads as a warning shot to an industry that has avoided public input.

“Absent more meaningful mechanisms for people to share their views on AI and shape its development, the backlash will grow and ‘missed uses’ will become the default…,” he suggested.

The global AI regulation debate has split along familiar lines, with progressives backing public ownership and industry voices warning of a dampened investment climate.

Sanders said the full bill text will follow soon.

The post Vitalik Buterin Criticizes AI Nationalism as US Senator Pushes for 50% Stake in OpenAI appeared first on BeInCrypto.

SpaceX has added new IPO filing language that gives the company room to issue large amounts of stock for future deals.

Summary

- SpaceX’s amended S-1/A filing states that the company may issue significant amounts of equity for future acquisitions, divestitures, and strategic transactions.

- The filing shows SpaceX is targeting a Nasdaq listing under the ticker SPCX, with a potential $75 billion raise and a minimum valuation of $1.8 trillion.

- SpaceX’s pending acquisition of Cursor shows how the company may use Class A stock as deal currency after the IPO.

The amended S-1/A filing states that SpaceX may issue a significant amount of equity in connection with future transactions, including acquisitions, divestitures, and other strategic moves. The disclosure gives investors a clearer view of how the company may use its publicly traded shares following a planned Nasdaq debut under the ticker SPCX.

SpaceX adds deal language before listing

According to the updated filing, SpaceX is preparing for an offering that could raise up to $75 billion. The filing pegs the company’s valuation at a minimum of $1.8 trillion, down from earlier internal discussions that had set the target above $2 trillion.

SpaceX filed its amended IPO filing (S-1/A) today.

Here's everything new that I found:

• In relation to acquisitions, divestitures, or other strategic transactions, @SpaceX says they "may issue a significant amount of equity in connection with future transactions." 👀— Sawyer Merritt (@SawyerMerritt) June 1, 2026

Reuters previously reported that SpaceX was targeting a June 12 listing, with pricing expected around June 11. The company first confidentially submitted its IPO paperwork to the U.S. Securities and Exchange Commission on April 1, according to public filing details cited in the registration statement. SpaceX later made its full S-1 public on May 20.

The amended filing does not say SpaceX has finalized any additional transaction beyond those already disclosed. However, the company’s wording gives it flexibility to issue Class A stock in major corporate moves after the IPO.

Cursor deal shows how shares may be used

The clearest example in the filing is SpaceX’s pending acquisition of Cursor, the AI coding assistant. According to the S-1/A, the transaction is expected to close after the IPO and will be paid entirely in Class A common stock.

The filing places Cursor’s implied equity value at $60 billion. It also says Cursor is entitled to a $1.5 billion termination fee and an $8.5 billion deferred services fee under a separate compute agreement.

Through that structure, SpaceX is telling investors that its public equity may serve as more than IPO fundraising stock. The filing shows the company could use its shares to acquire technology, deepen its AI operations, and expand its post-listing business structure.

SpaceX’s filing describes the company as an AI services and infrastructure business, not only a launch and satellite operator. The wording follows its February 2026 merger with xAI, which valued the combined company at about $1.25 trillion, according to the filing.

The company also outlines planned work with Tesla and Intel through Terafab. According to the registration statement, those plans include modular orbital AI compute infrastructure before the end of the decade.

SpaceX also lists long-term projects tied to asteroid mining and manufacturing infrastructure on the Moon and Mars. The company presents those plans as part of its future market opportunity, although the filing notes that many goals remain subject to execution, funding, and technical risks.

Elon Musk keeps voting control

Regarding ownership, the amended filing states that Elon Musk holds about 42% of SpaceX’s equity and controls 85% of the voting power through a dual-class share structure. As a result, the filing indicates that future equity issuance would not necessarily reduce Musk’s control over the company’s decisions.

The S-1/A also reserves up to 5% of IPO shares for a directed share program covering employees, friends, and family of executive officers. The filing says friends-and-family participants will not face lock-up limits, while more than 60% of pre-IPO shares, including Musk’s holdings, will remain under an extended lock-up after the listing.

Crypto investment products recorded their second-largest weekly outflow of 2026 by the end of May, with investors pulling $1.67 billion from digital asset funds as geopolitical tensions and a broader risk-off mood weighed on markets, according to a report from CoinShares.

The withdrawals marked the third consecutive week of net outflows and brought total redemptions over the past three weeks to $4.21 billion. CoinShares said concerns surrounding Iran had overwhelmed any positive sentiment generated by recent progress on the CLARITY Act, a U.S. crypto market structure bill.

Assets under management across digital asset investment products fell to $141 billion from $148 billion the previous week, their lowest level since early April.

The latest outflows coincide with a sharp decline in crypto prices. Bitcoin fell close to the $70,000 mark on Monday after reports that Iran had halted talks with the United States in protest over Israel’s continued incursions into Lebanon. The move coincided with Strategy (MSTR), the largest holder of bitcoin, selling some of its stack after years of its executive chairman Michal Saylor vowing he wouldn’t do so. The largest cryptocurrency dropped about 3% over the past 24 hour period, adding pressure to digital asset investment products.

The United States accounted for nearly all of last week’s withdrawals, with investors pulling $1.63 billion from crypto funds. Germany, which had largely avoided earlier bouts of selling, recorded $25.7 million in outflows. Sweden and Hong Kong posted withdrawals of $6.6 million and $4.5 million, respectively.

Bitcoin investment products saw the largest share of the selling, losing $1.44 billion during the week. According to CoinShares, that was the largest weekly bitcoin outflow of 2026, surpassing both the previous week’s record and the peak reached during January’s selloff. Year-to-date bitcoin inflows have fallen sharply to $1.19 billion, down from $2.6 billion a week earlier and $3.9 billion two weeks ago.

Ethereum (ETH) funds also came under pressure, recording $257.3 million in outflows. Meanwhile, investor appetite for alternative cryptocurrencies weakened considerably. CoinShares noted that only five digital assets attracted more than $1 million in inflows, down from 11 assets three weeks ago. XRP (XRP) led with $20.3 million in inflows, followed by Hyperliquid (HYPE) at $10.8 million and Near at $7.6 million.

Despite the recent pullback, crypto investment products still hold roughly $142 billion in assets globally, underscoring how much institutional capital remains invested in the sector even as market sentiment deteriorates.

Vitalik Buterin has proposed an options-based design for crypto index products that could reduce DeFi’s dependence on forced liquidations.

Summary

- Vitalik Buterin proposed an options-based DeFi design to reduce reliance on sudden liquidation systems.

- Buterin said options contracts could help create crypto index assets without the need for collateralized debt positions.

- The proposed model could use slower oracles to reduce risks associated with manipulated price feeds.

Buterin’s research post, published Monday, set out a model where index-tracking crypto assets use options contracts instead of collateralized debt positions, the structure used across many DeFi lending and synthetic asset systems.

Buterin Proposes Options-Based DeFi Structure

In the post, the Ethereum co-founder asked whether DeFi products could use options as their base layer instead of systems built around debt and liquidation engines. According to Buterin, such a model could allow users to gain exposure to a basket of crypto assets, similar to an index product, without suffering the sudden loss of a position when collateral values fall sharply.

Many DeFi protocols today allow users to borrow against crypto collateral. When collateral drops below a required level, the protocol can automatically liquidate the position. Buterin’s post said this structure can create abrupt outcomes for users and can add pressure during volatile market periods.

Under the options-based design described by Buterin, a user’s exposure would not end through an immediate liquidation event. Instead, the position would gradually move away from its target allocation as market prices change. Buterin presented that difference as a possible way to make crypto investment products less dependent on leverage-based failure points.

Slow Oracles Could Reduce Manipulation Risk

Buterin also linked the proposal to the oracle problem in DeFi. According to his research post, many DeFi applications rely on fast price feeds because liquidation systems need current market prices to decide when positions should be closed.

Those fast feeds can become a weak point when markets move quickly or when attackers try to distort prices. Buterin said an options-based structure could work with slower-moving oracles, similar to the type used in prediction markets.

In his view, slower oracles may reduce the need for protocols to act on price updates within seconds. Buterin also said he would feel much safer holding algorithmic stablecoins built with an options-based design than holding stablecoins that depend on real-time oracles, which could be manipulated.

Algorithmic Stablecoins Remain a Key Use Case

The proposal has clear relevance for algorithmic stablecoins, which have often depended on collateral systems, price feeds, and automated market actions. Buterin’s post did not name a specific stablecoin project, and the model remains theoretical rather than deployed on Ethereum.

Buterin also acknowledged practical limits. According to the post, an options-based system would still require regular portfolio rebalancing. He said it remains unclear whether those trades can happen cheaply enough to avoid high costs, poor execution, or slippage.

The research post comes as Buterin has also changed his plans for publishing long-form work. As previously covered by crypto.news, Buterin said he will stop writing regular blog posts and instead plans to try writing science fiction stories about decentralized governance.

Buterin’s past essays have covered DAOs, Layer 2 systems, voting models, and governance design across crypto and public institutions. In the latest proposal, he returned to a familiar theme, questioning whether DeFi systems can become safer by relying less on fragile automated debt structures.

On June 1, 2026, Strategy disclosed in an 8-K filing that it sold 32 Bitcoin between May 26 and May 31 at an average price of $77,135, raising about $2.5 million. It was the company’s first Bitcoin sale since December 2022, and for an outfit built on Michael Saylor’s promise never to sell, the symbolism landed harder than the number.

Summary

- Strategy sold 32 Bitcoin for about $2.5 million, marking its first Bitcoin sale since December 2022.

- Proceeds from the sale are expected to fund preferred stock dividends as the company’s mNAV premium has narrowed.

- The transaction represented just 0.0038% of Strategy’s Bitcoin holdings, but it signaled a change from an unconditional buying approach to a more active balance sheet strategy.

Bitcoin (BTC) slipped below $72,000 within hours. More than $93 million in futures positions liquidated in a single hour, 95% of them longs. MSTR stock fell around 5%. And yet the sale itself was almost nothing: 32 coins out of 843,706, roughly 0.0038% of the stack, sold to help fund a preferred-stock dividend.

This piece separates what actually happened from what the headline implies, explains the dividend machine that forced the sale, and works through what it does and does not mean for Bitcoin holders.

What actually happened

Strip away the reaction and the event is small. Strategy sold 32 Bitcoin over six days in late May, averaging $77,135 a coin, for about $2.5 million total. The 8-K signed by general counsel Thomas Chow is blunt about the reason: proceeds are expected to fund distributions on preferred stock.

The scale is almost comically minor against the company’s position. Strategy still holds 843,706 BTC, worth roughly $61 billion at current prices, acquired at a blended cost of $75,699 per coin. The 32 coins sold represent about 0.0038% of that.

In the same week, the company raised $128.3 million selling its own common shares through its at-the-market program, which dwarfs the Bitcoin sale by a factor of fifty.

So if you are picturing Saylor dumping Bitcoin, recalibrate. This was a rounding error executed to cover a cash obligation, and it was flagged in advance.

Saylor telegraphed the possibility on the Q1 earnings call in early May, and CEO Phong Le spelled out the mechanism plainly: Bitcoin would be sold to finance dividends under specific conditions. The market knew this was coming. It still flinched when it arrived.

The reason it flinched is doctrine, not arithmetic.

Why a tiny sale broke a big rule

For five years, Saylor’s pitch was absolute. Strategy buys Bitcoin and never sells. That promise was the spine of the whole thesis, the thing that made MSTR a leveraged Bitcoin proxy rather than a fund that might trade around its position. Holders bought the stock partly because they trusted the company would ride out any drawdown without capitulating.

The December 2022 sale, the only prior one, came with an asterisk that preserved the doctrine. The company sold 704 BTC near the cycle bottom, then bought back 810 two days later in what everyone read as a tax-loss harvest. Sell to bank the loss for tax purposes, rebuy immediately, end up with more coins. It was a maneuver, not a retreat, and the “never sell” story survived it.

This time there is no asterisk. The sale funds a dividend, and the company has explicitly said future sales are part of how it will manage the balance sheet. That is a different posture. Saylor has reframed it around a new metric he calls Bitcoin per share, or BPS, which he describes as “EPS on the Bitcoin Standard.” The idea is that what matters for shareholders is not the absolute size of the stack but how much Bitcoin each share represents, and that selectively selling Bitcoin to fund obligations can, under the right conditions, protect or even raise that per-share number.

Whether you find that convincing or not, the practical point is clear: “never sell” is over, replaced by “sell when the math says to.” The market reacted to the death of the doctrine, not to the loss of 32 coins.

The dividend machine that forced it

To understand why Strategy sold anything at all, you have to look at what the company has become. It is no longer just a firm with a big Bitcoin pile. It is the largest issuer of what it calls Digital Credit in the world, with more than $13.5 billion of preferred equity outstanding across five series.

The biggest of these is STRC, branded Stretch, a perpetual preferred stock that has scaled to $8.5 billion in nine months and now pays an 11.50% annual dividend. Add the other series (STRF at 10%, STRK at 8%, STRD at 10%, and the euro-denominated STRE), and Strategy carries roughly $1.5 billion in annual dividend obligations. Those are fixed cash commitments. They come due whether Bitcoin is up or down, and the company has now met 23 consecutive distributions totaling over $693 million.

Here is the engine. Strategy normally funds those dividends by issuing new MSTR common shares through its at-the-market program and using the cash. That works as long as the stock trades at a high enough premium to the underlying Bitcoin, a ratio the company tracks as mNAV. At Q1 2026, the breakeven threshold sat around 1.22x. Above that line, issuing shares to raise cash is accretive in Bitcoin-per-share terms. Below it, the arithmetic reverses, and selling shares to pay dividends starts destroying per-share value.

The problem is that mNAV has compressed hard. It ran as high as 3.89x in late 2024. By mid-2026 it had fallen to around 1.2x, right at or below the breakeven line. When the premium gets that thin, the share-issuance engine sputters, because every share sold is barely accretive or outright dilutive. So the company reaches for the next lever: selling a small amount of Bitcoin directly to cover the cash need. That is exactly what the 32-coin sale was. Not a change of heart about Bitcoin, but the dividend machine switching fuel sources when its primary fuel got expensive.

Strategy also has context that softens the picture. Le said the company has about 18 months of dividend coverage at the current run rate, backed by nearly $60 billion in Bitcoin. The 32 coins were even sold at a small profit, about 1.9% above the blended cost basis. This is not a company scrambling. It is a company optimizing its cash position, drawing down an oversized reserve and supplementing it with selective sales rather than sitting on idle capital.

What it means for Bitcoin: the honest read

Now the question that matters for most readers. Does a Bitcoin holder need to care that Strategy sold?

In the immediate, mechanical sense, no. Thirty-two coins is nothing. It does not move supply, it does not represent meaningful selling pressure, and the price drop that followed was a sentiment and leverage reaction, not the weight of $2.5 million hitting the order book. The $93 million in liquidations came from over-leveraged longs getting flushed on a headline, which is a story about positioning and fragility, not about Bitcoin’s fundamentals.

In the larger sense, there is something real to watch, and it is not this sale. It is the precedent and the structure behind it. Strategy is the single largest corporate holder of Bitcoin, and it has now established that it will sell Bitcoin to meet fixed dollar obligations when its preferred premium compresses. As long as mNAV stays healthy, those sales remain tiny and occasional, funded mostly by share issuance. But the model has a stress point: if Bitcoin stays depressed, mNAV stays compressed, and the share-issuance channel stays expensive, the company leans harder on Bitcoin sales to service a dividend stack that does not shrink.

That dynamic is worth understanding precisely because it runs opposite to the way Strategy supported Bitcoin on the way up. For years the company was a one-way buyer, absorbing supply and amplifying rallies. The new posture introduces, for the first time, a scenario where the largest corporate holder becomes a price-sensitive seller during weakness rather than a buyer. The amounts today are trivial. The direction of the incentive is what changed.

The reassuring part: the structure has real buffers. Eighteen months of coverage, a $60 billion Bitcoin backstop, $26 billion in remaining share-issuance capacity, and a preferred-stock product that, whatever you think of its complexity, has kept paying for 23 straight distributions. None of that points to forced large-scale selling at current levels. The bears’ nightmare, a cascade where Strategy has to dump Bitcoin into a falling market to survive, would require a much deeper and longer drawdown than what exists today.

So the balanced read is this. The 32-coin sale itself is noise. The shift it confirms, from an unconditional buyer to a balance-sheet manager that will sell when the math demands, is signal. For Bitcoin holders, it means the Strategy backstop is conditional now, not absolute. That is a meaningful change in the market’s structure even though this particular sale changes almost nothing.

The 2022 parallel, and why it is shakier this time

Some bulls have seized on the timing. The last time Strategy sold, in December 2022, it marked almost the exact bottom of that cycle. Sell, rebuy two days later, and the market bottomed within weeks. The pattern-match is tempting: Strategy sells, therefore bottom.

Be careful with it. The 2022 sale was a deliberate tax maneuver executed near a known cycle low, with an immediate rebuy. This sale is a dividend-funding operation driven by a compressed premium, with no rebuy and an explicit statement that more sales may follow. The mechanism is different, the intent is different, and the company is a far more complex financial machine than it was three and a half years ago. A coincidence of “Strategy sold and price was low” is not a reliable bottoming indicator. If Bitcoin does bottom here, it will be for macro and flow reasons, not because 32 coins changed hands.

The honest bottom line

Michael Saylor sold Bitcoin, and the accurate version of that sentence is much smaller than the headline. Strategy sold 32 coins, 0.0038% of its holdings, at a small profit, to help cover a preferred-stock dividend, and it told everyone in advance that it would. The market dropped on the symbolism of a broken “never sell” promise and on leveraged longs getting liquidated, not on the weight of the sale.

What changed is the doctrine. Strategy is no longer an unconditional Bitcoin buyer. It is now a balance-sheet manager that will sell Bitcoin when its premium compresses below the level where issuing shares makes sense.

At today’s mNAV, with 18 months of dividend coverage and a $60 billion backstop, that means tiny, occasional sales. In a prolonged bear market, it could mean more. The amounts are trivial now. The incentive structure is what flipped.

For Bitcoin holders, the practical takeaway is to ignore this sale and watch the mechanism. The number that matters is not 32 coins. It is Strategy’s mNAV, the health of its preferred-stock issuance, and how long Bitcoin stays below the company’s cost basis.

As long as those stay sound, the largest corporate holder remains a net accumulator. If they deteriorate, the market will have to price in something it never had to before: a Saylor who sells.

Frequently Asked Questions

How much Bitcoin did Michael Saylor’s Strategy actually sell?

Strategy sold 32 Bitcoin between May 26 and May 31, 2026, at an average price of $77,135, for roughly $2.5 million total. That represents about 0.0038% of the company’s 843,706 BTC holdings. It was the first sale since December 2022.

Why did Strategy sell Bitcoin?

The 8-K filing states the proceeds are expected to fund distributions on the company’s preferred stock. Strategy carries roughly $1.5 billion in annual dividend obligations across five preferred series. It normally funds these by issuing common shares, but with its mNAV premium compressed to around 1.2x, selling a small amount of Bitcoin directly became the more efficient way to raise the cash.

Does this mean Saylor lost faith in Bitcoin?

No. The sale was 32 coins out of more than 843,000, executed for a specific cash-management reason and flagged in advance. Saylor has reframed strategy around a metric he calls Bitcoin per share, arguing that selective sales to fund obligations can protect per-share value. The company still holds about $61 billion in Bitcoin and remains the largest corporate holder.

Why did Bitcoin’s price drop so much on such a small sale?

The drop was driven by sentiment and leverage, not the size of the sale. The end of Saylor’s “never sell” doctrine spooked the market, and over $93 million in futures positions liquidated in a single hour, 95% of them longs. A small headline triggered a cascade among over-leveraged traders. The $2.5 million sale itself had no meaningful effect on supply.

What is mNAV and why does it matter here?

mNAV measures Strategy’s stock-market value relative to its Bitcoin holdings. When it trades at a high premium, the company can issue shares to fund dividends accretively. The breakeven threshold was around 1.22x at Q1 2026. As of mid-2026 it had compressed to around 1.2x, near the line where share issuance stops being accretive, which is why the company turned to selling Bitcoin instead.

Is this the same as the 2022 sale?

Not really. The December 2022 sale was a tax-loss harvest near the cycle bottom, with an immediate rebuy two days later, which preserved the “never sell” narrative. This sale funds a dividend, has no rebuy, and comes with an explicit statement that more sales may follow. The mechanism and intent are different, so the “this marks the bottom” comparison is shakier than it looks.

Should Bitcoin holders be worried?

The sale itself is negligible. What is worth watching is the precedent: the largest corporate Bitcoin holder has established it will sell when its premium compresses. At current levels, with 18 months of dividend coverage and a $60 billion backstop, that means tiny occasional sales. The risk only grows if Bitcoin stays depressed for a long stretch, which would pressure the structure further. The incentive has shifted from unconditional buying to conditional selling.

Could Strategy be forced to sell large amounts of Bitcoin?

Not under current conditions. The company has about 18 months of dividend coverage, nearly $60 billion in Bitcoin, and around $26 billion in remaining share-issuance capacity. Forced large-scale selling would require a much deeper and longer Bitcoin drawdown than exists today. The structure has real buffers, even if the new willingness to sell at all is a change.

This article is for informational purposes and does not constitute financial or investment advice. Cryptocurrency markets are highly volatile. The figures and analysis described reflect data available as of June 1, 2026. Always do your own research and consult with qualified financial professionals before making investment decisions.

Japan’s Liberal Democratic Party (LDP) is pushing for a set of reforms aimed at the country’s cryptocurrency taxation regime and the development of yen-denominated stablecoins, signaling a broader drive to formalize on-chain finance within its regulatory landscape. A Nada News report indicates that the LDP’s Parliamentary Association for the Promotion of Blockchain delivered recommendations to Finance Minister Satsuki Katayama, covering stablecoins, exchange-traded funds (ETFs), central bank digital currencies (CBDCs), and broader blockchain applications.

The policy brief proposes concrete steps, including doubling the leverage cap for retail cryptocurrency derivatives trading and establishing a regulatory framework for ETFs linked to digital assets. Minister Katayama reportedly signaled a sense of urgency, stating that Japan “must move forward without falling behind global developments,” a reference to evolving crypto legislation and regulatory approaches abroad. LDP member Junichi Kanda emphasized the goal of expanding on-chain finance across Asia, with a specific focus on the development and adoption of yen-denominated stablecoins.

The push comes at a time when Japan has already begun reshaping how crypto assets are treated within its financial system. Earlier this year, the government approved changes to classify crypto assets as financial instruments rather than solely as a means of payment, a shift that paves the way for broader use cases and investor protections. The Financial Services Agency (FSA) was also reported to be preparing amendments to the regulatory framework to accommodate crypto ETFs, signaling a deeper integration of digital assets into traditional financial infrastructure.

The broader regulatory dialogue in Japan is unfolding alongside global policy developments. In the United States, lawmakers have enacted legislation to create a framework for payment stability tokens, while international bodies explore standard-setting for crypto assets. Analysts note that Japan’s approach could influence regional cross-border flows and the regulatory posture of exchanges and banks seeking to participate in on-chain finance and stablecoin settlement rails.

In a related context, the Bank for International Settlements (BIS) has highlighted the comparatively small footprint of yen-denominated stablecoins relative to their U.S. dollar-pegged counterparts. A BIS report cited that yen-stablecoins account for less than 0.01% of the market capitalization of dollar-stablecoins, underscoring both the opportunity and the regulatory challenge ahead for Japan’s initiatives to scale yen-denominated crypto instruments.

Within the market ecosystem, the prediction-informed platforms operating under evolving regulatory contours are also paying attention to Japan’s regime. Polymarket, a prediction markets platform that has faced regulatory scrutiny in the United States, was reported to be seeking approval to operate in Japan by 2030. Japan’s stringent gambling laws—applied to both online and in-person formats—could complicate such a market entry, even as the platform contends with cross-border compliance requirements. The development was noted in reporting surrounding Japan’s crypto policy and market accessibility.

As Japan contemplates these changes, the regulatory conversation intersects with broader policy objectives and enforcement considerations. The shift toward treating crypto assets as financial instruments aligns with AML/KYC frameworks and licensing requirements that are central to safeguarding investors, ensuring taxation clarity, and supporting banking integration for digital-asset businesses. The evolving framework also raises questions about cross-border licensing, supervision of ETF issuers, and the appropriate balance between innovation and consumer protection as on-chain finance expands beyond a niche sector into mainstream financial infrastructure.

Key takeaways

- Japan’s LDP advocates comprehensive reform of cryptocurrency taxation and promotes yen-denominated stablecoins, signaling a shift toward formal on-chain finance within the tax and regulatory regime.

- The recommendations include doubling the leverage cap for retail crypto derivatives trading and creating a framework for ETFs tied to digital assets, indicating a move toward more sophisticated market access for individuals and institutions.

- Regulatory context is advancing: the government approved crypto-asset classification as financial instruments, and the FSA reportedly plans amendments to permit crypto ETFs, expanding the toolkit for asset managers and exchanges.

- Global regulatory dynamics—such as US policy actions and EU MiCA-like developments—frame Japan’s approach and influence cross-border compliance and licensing expectations for market participants.

- Yen-denominated stablecoins remain a small segment of the market, suggesting substantial room for growth but also highlighting regulatory and operational challenges in scaling on-shore stablecoins within a global payments and settlement ecosystem.

- Market-entry considerations for international platforms, such as Polymarket’s potential Japan trajectory, illustrate how regulatory strictness around gambling and online/offline activities intersects with crypto policy goals.

Policy momentum, market mechanics, and regulatory alignment

The LDP’s recommendations reflect a broader ambition to integrate digital assets into Japan’s financial architecture with a clear regulatory spine. By proposing a doubled leverage limit for retail crypto derivatives, the package aims to expand hedging and investment opportunities while maintaining risk controls appropriate for a mature market. The ETF framework for digital assets would enable more traditional asset-management channels to offer crypto exposure, potentially improving liquidity and price discovery while subjecting products to standard disclosures, custody, and risk management requirements.

From tax policy to asset classification, Japan’s evolving stance moves in step with an international trend toward treating crypto assets as financial instruments with recognized rights and obligations for market participants. The government’s previous move to reclassify crypto assets lays groundwork for investor protection, taxation clarity, and regulatory oversight, while the FSA’s anticipated amendments would formalize permission structures for crypto ETFs and related products. This regulatory maturation is crucial for banks and exchanges seeking to engage with digital assets at scale, including custody, settlement, and interoperability with traditional payment rails.

Within the global policy environment, Japan’s path interacts with multi-jurisdictional developments. EU policy instruments such as MiCA create a regulatory perimeter for crypto-assets and stablecoins in the European market, while US proposals and enacted laws address stablecoin governance, consumer protection, and market integrity. For Japan-based institutions, this convergence means harmonized considerations around licensing, AML/KYC adherence, and cross-border operational requirements, as well as potential alignment or friction with cross-border clearing and settlement arrangements.

Beyond regulatory architecture, the BIS assessment of yen-denominated stablecoins underscores two realities: the opportunity to reduce FX and settlement frictions, and the need to establish robust stability, reserve, and governance frameworks. If Japan scales yen-backed stablecoins, financial institutions—banks, payment providers, and other on-chain facilitators—would need to implement stringent controls, including reserve management, tax treatment, and policy-driven transparency for end users and counterparties. The regulatory posture will determine whether yen-stablecoins become a viable complement to domestic settlement networks or remain a nascent niche with limited uptake.

Market participants are watching not only the internal policy shifts but also the regulatory cadence from supervisory authorities. The potential entry of foreign platforms like Polymarket into Japan by 2030 illustrates the tension between innovation and compliance, as operators must navigate both licensing regimes and Japan’s gambling-law constraints. The outcome of these considerations will influence how institutions structure product offerings, risk frameworks, and governance architectures when engaging with prediction markets or other on-chain-native applications that touch regulated spaces.

In this context, analysts and compliance teams should monitor several moving parts: legislative timelines for tax reform and asset-class classification, the pace of FSA rule amendments for crypto ETFs, licensing criteria for digital-asset service providers, and the evolving stance on CBDCs and cross-border settlement interoperability. The integration of yen-denominated instruments into mainstream finance will hinge on robust custody, auditability, and regulatory alignment across jurisdictions, including potential cross-border collaborations to facilitate liquidity and investor protection.

Closing perspective

Japan’s policy trajectory signals a deliberate push to normalize crypto assets within its financial system, balancing innovation with regulatory guardrails. As authorities weigh tax reform, ETF-enabled access to digital assets, and the development of yen-denominated stablecoins, institutions should prepare for greater regulatory clarity, potential licensing requirements, and closer supervision of on-chain activity. The coming months will reveal the concrete steps and implementation timelines that will shape how Japan participates in the evolving global framework for crypto markets and stable value in a digital economy.

The sale of 32 bitcoin (BTC) by Michael Saylor’s Strategy (formerly Microstrategy) has led to a dispute among Polymarket users who’ve been betting on whether or not the company would sell any of its BTC by May 31, 2026.

A Securities and Exchange Commission filing revealed that Strategy sold the BTC (despite Saylor’s promises to never sell) between May 26 and May 31.

However, the firm’s Form 8-K wasn’t filed until June 1.

Before the filing was noted, the market had a proposed outcome of “No.” It then resolved to “No” again, after the original outcome was disputed.

Some UMA tokenholders in Discord attempted to justify the decision by pointing out that the announcement came after the market deadline, despite the market explicitly referring to when the sale occurs, not when it’s announced.

Needless to say, the decision by UMA token holders is controversial.

This second “No” outcome has also been disputed, and we are now in the “final review” window.

Polymarket itself has added a note to the market that says, “No information from MSTR, on-chain data, or consensus of credible reporting confirmed that MicroStrategy sold BTC within the market’s timeframe. Confirmation achieved outside of the market’s time frame does not qualify.”

Read more: Are Polymarket and Kalshi decentralized?

Similar disputes have popped up on Polymarket before. One prominent example was dubbed “Suitgate” and centered around whether or not an outfit that Volodymyr Zelenskyy wore to a NATO meeting counted as a suit.

Despite multiple outlets describing it as a suit, UMA tokenholders were reluctant to consider it as such, and it resolved to “No.”

In another example, Polymarket created a market that was meant to determine whether or not the Elon Musk-connected Department of Government Efficiency (DOGE) would “cut $3 billion of DEI contracts before March.”

The rules for this market explicitly pointed to whether or not “doge-tracker.com” showed that amount or more in cuts.

That website did show more than $3 billion in cuts, but this display was rooted in lies propagated by DOGE, and so Polymarket and UMA holders were placed between the explicit resolution criteria and reality.

Broadly, this Strategy market controversy combines with the previous failures of Polymarket resolution to undermine Polymarket’s tether to reality.

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

TLDR:

- Bitcoin active addresses fell 44%, dropping from 1.12M daily in May 2021 to roughly 624K today.

- New wallet creation declined 43%, from nearly 489K per day to approximately 278K in this cycle.

- Spot Bitcoin ETFs allow institutional investors to gain exposure without creating on-chain wallets.

- Strategy sold 32 BTC worth $2.5M, its first Bitcoin sale in 3.5 years, briefly pushing BTC below $72K.

Bitcoin’s on-chain activity has declined notably compared to the peak of the 2021 bull market. Active addresses and new wallet creation have both fallen by roughly 43–44% from their May 2021 highs.

Meanwhile, Bitcoin’s price remains well above 2021 levels for much of the current cycle. Analysts point to institutional investment vehicles and passive long-term holders as key factors behind this shift in network behavior.

On-Chain Participation Drops Despite Higher Prices

According to Santiment Intelligence, Bitcoin averaged around 1.12 million active addresses per day in May 2021. That figure has since dropped to approximately 624,000 active addresses daily. New wallet creation has followed a similar path, falling from nearly 489,000 per day to about 278,000.

These two metrics are closely watched by analysts tracking network health. Active addresses reflect how many unique participants are transacting on the network.

New wallet creation, known as network growth, tracks addresses interacting with Bitcoin for the very first time.

The decline stands out because Bitcoin’s price has largely held above 2021 peaks. Normally, higher prices tend to draw more retail participants onto the network. This cycle, however, the expected surge in new users has not materialized on-chain.

One explanation is the rise of spot Bitcoin ETFs and other institutional products. These vehicles allow investors to gain Bitcoin exposure without moving coins on-chain or opening new wallets. As a result, price action no longer directly translates into on-chain activity growth.

Strategy’s Bitcoin Sale Adds Short-Term Pressure

Santiment noted that prolonged sideways price movement is also a factor. Historically, volatility — in either direction — tends to spark a rise in on-chain activity.

With markets moving sideways and investor attention shifting toward equities and precious metals, Bitcoin activity has stayed subdued.

Adding to short-term pressure, Michael Saylor’s Strategy recently disclosed its first Bitcoin sale in approximately 3.5 years. The firm sold 32 BTC worth around $2.5 million, which briefly pushed Bitcoin below $72,000, according to Bull Theory.

The sale drew attention given Strategy’s history as one of Bitcoin’s largest corporate holders. The firm still holds 843,706 BTC, representing roughly 4% of Bitcoin’s entire supply, purchased for approximately $63.86 billion.

Saylor had previously stated that Strategy could sell Bitcoin to fund dividends, but added it would buy 20 BTC for every one it sells.

For context, Strategy sold 704 BTC in December 2022 for tax-loss purposes, then bought back 810 BTC just two days later. The latest sale appears minor relative to the company’s total holdings and long-term accumulation strategy.

Zcash (ZEC) has surged nearly 1,000% over the past year and is up almost 50% over the past month alone.

The privacy-focused crypto asset is flashing another bullish signal after an already remarkable run in 2026, largely defying the wider market’s struggles.

Another Bullish Signal

According to the latest findings from crypto analyst Ali Martinez, the TD Sequential indicator on a 12-hour chart has flashed a buy signal for ZEC, suggesting the rally may not be over yet. Martinez believes that a move toward $642 remains possible as long as the token continues to hold above the $500 level.

The latest signal comes after a period of intense volatility and growing market attention surrounding the asset. Earlier, blockchain analytics platform Santiment identified ZEC as the dominant topic across crypto social media, recording seven repeat spikes in social dominance during the week and reaching a peak social dominance score of 10.02 on May 20.

The firm noted that sentiment around the asset shifted sharply over the course of the rally, moving from positive to negative after the initial surge. Santiment linked the May 20 spike to a powerful short squeeze that sent ZEC from around $568 to an intraday high near $686 in roughly six hours, a gain of about 17%. The move reportedly triggered around $28 million in liquidations and pushed the ZEC’s market capitalization above $11 billion.

Discussion online was largely driven by claims that the rally was fueled by aggressive positioning and thin liquidity, growing excitement around Grayscale’s filing to convert its Zcash Trust into a spot ETF, and continued interest in privacy-coin investment narratives. While sentiment was initially boosted by the short squeeze and ETF-related optimism, it later turned negative as some market participants began to question the move’s sustainability and rotated into other assets.

As a result, Santiment described ZEC as one of the most consistently active and volatile assets of 2026, while adding that “signals around it tend to be tradable in either direction rather than directional on their own.”

Security Fixes

Beyond market activity, the Zcash Foundation last week released Zebra 4.5.0 and urged node operators to upgrade immediately. The update addressed multiple security vulnerabilities across the network, including a consensus-related issue and several bugs that could affect node operations.

It also introduced support for mining directly to a shielded address and included broader security and reliability improvements.

The post Zcash (ZEC) Flashes Fresh Buy Signal; Is $642 the Next Stop? appeared first on CryptoPotato.

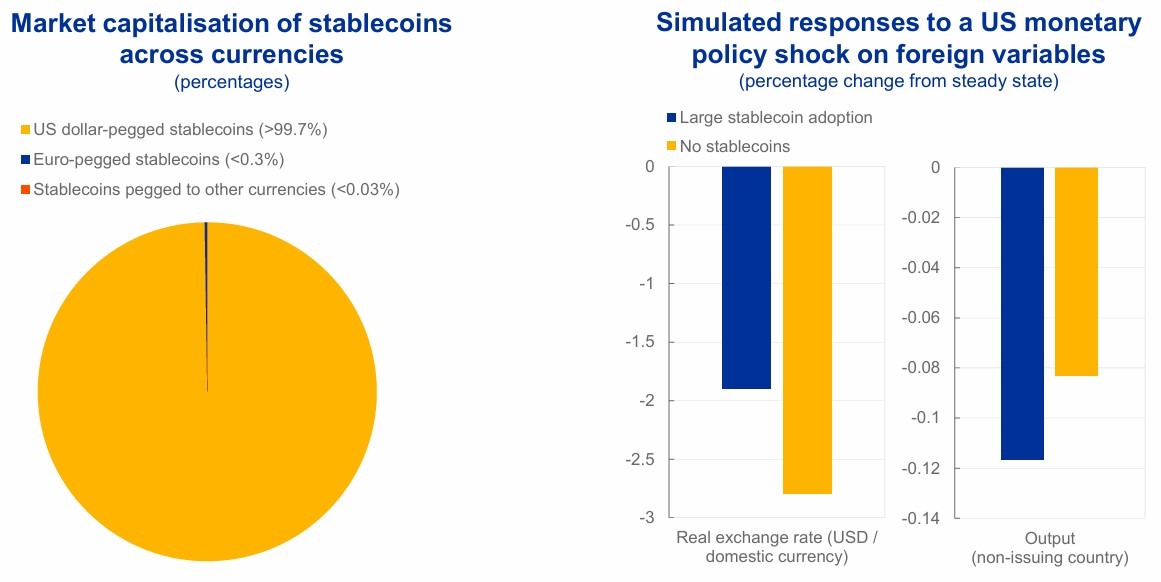

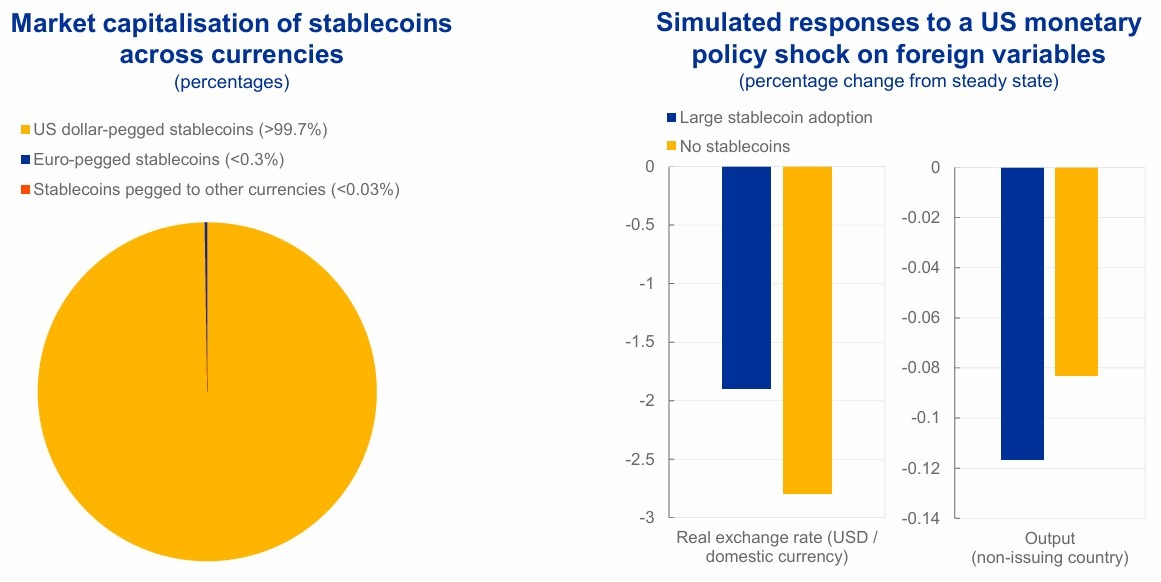

European Central Bank (ECB) Executive Board member Isabel Schnabel said stablecoins could bring old financial-market vulnerabilities into tokenized finance, while strengthening the case for central banks to modernize public money through tools such as the digital euro and tokenized central bank settlement.

In a Monday speech at the 2026 Bank of Korea International Conference on Central Banks and the Future of Money in Seoul, Schnabel compared stablecoins with money market funds, arguing that both can offer useful financial innovation while also creating risks around bank disintermediation, runs, fire sales and monetary policy transmission.

Schnabel also warned that stablecoins could reinforce the US dollar’s global role as tokenized finance develops. “The growing use of stablecoins may further cement the international dominance of the U.S. dollar,” she said, adding that “virtually all stablecoins in circulation are denominated in dollars, with other currencies playing a negligible role.”

Schnabel said the Eurosystem’s response has two parts, including a retail digital euro and tokenized wholesale central bank money. In March, the ECB unveiled its Appia roadmap for Europe’s tokenized financial markets, with Pontes set to provide a distributed ledger technology settlement bridge to the Eurosystem’s TARGET services and scheduled to launch in the third quarter of 2026.

Schnabel argued that central banks should not resist innovation but must modernize public money, including through the digital euro and tokenized wholesale central bank settlement, to preserve financial stability and monetary control.

“Central banks cannot remain passive observers of these developments,” Schnabel said, adding that private forms of money, once widely adopted, can shape the financial system “in ways that can be difficult to reverse.” She said the proper response is not to resist innovation but to ensure it develops within a framework that preserves stability, monetary control and trust in the currency.

Stablecoins are overwhelmingly dollar-pegged, while broad adoption could amplify US policy spillovers abroad, ECB data shows. Source: European Central Bank

MiCA review sharpens stablecoin debate

The speech builds on ECB messaging that Europe should not answer dollar stablecoins simply by promoting euro-denominated stablecoins.

On May 8, ECB President Christine Lagarde said stablecoins are not Europe’s best route to strengthening the euro’s international role, arguing instead that Europe should build tokenized settlement infrastructure anchored by central bank money.

The debate unfolds as the European Commission reviews the European Union’s Markets in Crypto-Assets Regulation (MiCA), with a public consultation open until Aug. 31 examining whether the bloc’s crypto rules should be updated.

Related: MiCA has made euro stablecoins safe but weak, new report argues

Crypto exchange Coinbase has used the review to call for a more competitive EU crypto framework. In a Monday blog post, Katie Harries, Coinbase’s director and head of policy for Europe and the Americas, said MiCA should recalibrate stablecoin rules on reserves, rewards and multi-issuance, while clarifying how regulated crypto firms can provide access to decentralized finance and global liquidity.

Harries also argued that allowing more reserves in high-quality sovereign assets and permitting non-interest incentives, such as cashback and loyalty points, could help make euro stablecoins more competitive.

The ECB has taken a more cautious view. On May 23, the ECB warned EU finance ministers that loosening stablecoin rules could weaken bank lending and complicate monetary policy, even as policymakers debate whether Europe risks falling behind dollar-backed tokens.

Magazine: HYPE chases $100 target, ETH could dump below $1800: Market Moves

The Money Expert: #1 Formula to Get RICH Off Your Normal Salary (It’s EASY!)

Peter Mandelson said No 10 needs ‘revamp’ and ‘infusion of purpose’, files show

CME Group launches 24/7 cryptocurrency futures trading

-

NewsBeat5 days ago

NewsBeat5 days agoIsrael says it has killed new Hamas military leader in Gaza City airstrikes

-

Tech6 days ago

Tech6 days agoNASA taps Blue Origin to deliver lunar rovers for Moon Base initiative

-

Sports7 days ago

Sports7 days ago2026 NBA Finals schedule, odds: Knicks await Thunder or Spurs after winning East

-

News Videos6 days ago

News Videos6 days agoXRP *JUST* SUCCEEDED!!!! CLARITY ACT EXPOSED!!! (SHE EXPOSED IT)

-

News Videos3 days ago

News Videos3 days agoThis is BROKEN! INSANE 5x MONEY CAR WASH WEEK! The NEW GTA Online UPDATE Today! (GTA5 New Update)

-

Crypto World6 days ago

Micron Crosses $1 Trillion Market Cap as AI Demand Reshapes Memory Sector

-

Business6 days ago

Business6 days agoSelena Gomez Reportedly Upset Over Benny Blanco’s Comments on Her ‘Terrible’ Diet

-

Business7 days ago

Business7 days agoNikkei 225 Surges Past 65,000 for First Time as Iran Peace Hopes Fuel Record Rally

-

Tech7 days ago

Tech7 days agoChina assigns ID codes to 28,000+ humanoid robots

-

Tech4 days ago

Tech4 days agoWaymo dominates autonomous vehicle registrations as Tesla trails behind

-

Entertainment7 days ago

Entertainment7 days ago‘Breaking Bad’ Star’s Easy-to-Binge 6-Part Crime Series Spin-Off Is Finally Heading to Free Streaming

-

Tech2 days ago

Tech2 days agoSpaceX just won a second Golden Dome contract. This one is $4.16 billion.

-

Tech5 days ago

Tech5 days agoThe Samsung pay deal is the moment Korean unions changed register

-

Entertainment6 days ago

Entertainment6 days agoDays of our Lives 2-Week Spoilers May 25-June 5: Gwen Rages, Abe Confesses & 2 Tragic Anniversaries!

-

News Videos3 days ago

News Videos3 days agoSHE IS KILLING XRP!!! WATCH URGENT AND ACT FAST

-

NewsBeat3 days ago

NewsBeat3 days agoFIRST NIGHT REVIEW: Take That bring the Circus back to life in spectacular sun-soaked style

-

Entertainment7 days ago

Entertainment7 days agoTaylor Swift Fans Label Travis Kelce’s Beer-Chugging A ‘Red Flag

-

Tech6 days ago

Tech6 days agoMillions of AI agents imperiled by critical vulnerability in open source package

-

Crypto World5 days ago

SpaceX’s $2 Trillion IPO: Why Tech Giants Nvidia (NVDA), Apple (AAPL), and Microsoft (MSFT) May Face Pressure

-

Crypto World3 days ago

CFTC Has Approved the First Regulated Bitcoin Perpetual Contract in the U.S.

You must be logged in to post a comment Login