Crypto World

Solana Treasury Giant Forward Industries Reports $283 Million Quarterly Loss

Forward Industries (FWDI), the largest corporate Solana (SOL) holder, posted a $283.1 million net loss for the fiscal second quarter ended March 31, 2026.

Despite this, total revenue still quadrupled year over year, primarily from staking rewards generated by the Company’s Solana treasury strategy.

Forward Industries Posts $283M Q2 Loss on Solana Markdowns

Solana fell from roughly $124 at the start of 2026 to about $83 by the end of March. The drawdown weighed on the balance sheets of corporate SOL holders.

According to the press release, the decline in fair value on its SOL treasury drove the net loss. The firm reported $201.7 million in losses and $85.1 million in impairments on digital assets.

“This U.S. GAAP-required treatment reflects changes in the estimated fair value of the Company’s SOL holdings and does not represent an outflow of cash or impact Forward’s liquidity,” the firm said.

Follow us on X to get the latest news as it happens

Meanwhile, the operating picture offered a counterpoint to the headline loss. Quarterly revenue climbed more than fourfold to $13 million from $3.1 million a year earlier.

Staking revenue generated by Forward’s SOL treasury accounted for almost all of the gain. The company’s validator infrastructure has delivered a gross annual percentage yield (APY) of 6.5% to 7.2% before fees since launch, ahead of peers.

Forward has accumulated 201,201 SOL in staking rewards through March 31, with nearly its entire treasury staked. Operating costs also eased.

Selling, General and Administrative Expenses fell to $6.6 million from $7.2 million in the prior quarter. The firm closed the quarter with 7,044,079 SOL on its balance sheet and roughly $16.6 million in cash.

“Against a backdrop of market volatility, we took decisive actions to position Forward for long-term value creation by securing a highly advantageous institutional debt facility with our strategic partner, Galaxy Digital, and executing a strategic share repurchase that reduced our basic shares outstanding by 7.4%. We also implemented a cost reduction plan in March that we expect to materially lower operating expenses in the coming quarters,” Kyle Samani, Chairman of Forward Industries, said.

Upexi, another major corporate holder of Solana, also posted a $109.3 million net loss for the fiscal quarter ended March 31, 2026. Unrealized digital asset losses accounted for $92.3 million of that figure.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Solana Treasury Giant Forward Industries Reports $283 Million Quarterly Loss appeared first on BeInCrypto.

The Tom Lee-chaired former bitcoin miner turned Ethereum treasury company continues to increase its ETH holdings by purchasing over $135 million worth of the asset.

Its total holdings have skyrocketed to 5,620,754 ETH, currently valued at around $10 billion, given the asset’s price today. This means that the company, whose average entry price is around $3,450, still sits on a massive unrealized loss of well over $9 billion.

ETH Holdings Keep Rising

The press release shared from the company earlier today indicated that its total stash has grown to $10.4 billion, albeit crypto prices were slightly lower at the time. Aside from the massive ETH fortune, Bitmine owns 204 BTC, $502 million in cash and marketable securities, as well as equity stakes in Beast Industries and Eightco Holdings valued at a combined $268 million.

Tom Lee described the $135 million purchase as an “elevated pace” of buying the asset despite its most recent market pullback that sent it to $1,500 at the start of the month. The company is now 93% of the way toward owning 5% of Ethereum’s total supply.

Nevertheless, Bitmine continues to be a major ETH supporter, noting that it doesn’t believe the current market downturn rightfully reflects its position in the market.

“The Series A Preferred Stock offering is good balance sheet diversification for Bitmine. The Company’s current projected annualized staking rewards of approximately $219 million provide recurring cash flow to support the dividends related to the Series A Preferred shares,” stated Lee.

Bitmine’s Staking Venture

He added that Bitmine has become a major participant in Ethereum staking, as 4.72 million ETH tokens, or more than 83% of its total holdings, have been staked through its validator operations.

Using current staking yields, the company projects annualized staking revenue of approximately $226 million. The firm estimated that if it deploys all of its ETH through staking, its annual rewards could rise to about $270 million.

Bitmine remains the second-largest cryptocurrency holder with its $10 billion worth of ETH and 204 BTC. It trails only Strategy, which, despite a minor sale completed by the end of May, has continued its substantial accumulation with another $100 million BTC purchase announced earlier today. It now owns approximately $56 billion worth of bitcoin.

The post Bitmine Adds $135M in ETH, Closing In on 5% of Ethereum Supply appeared first on CryptoPotato.

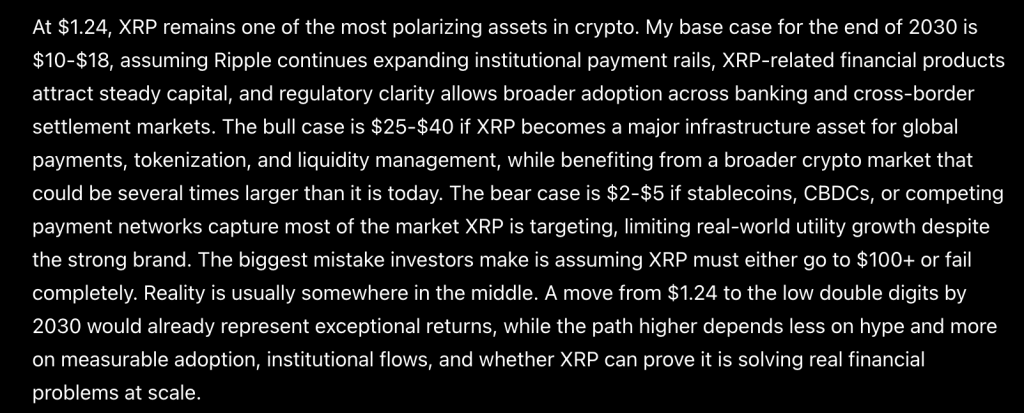

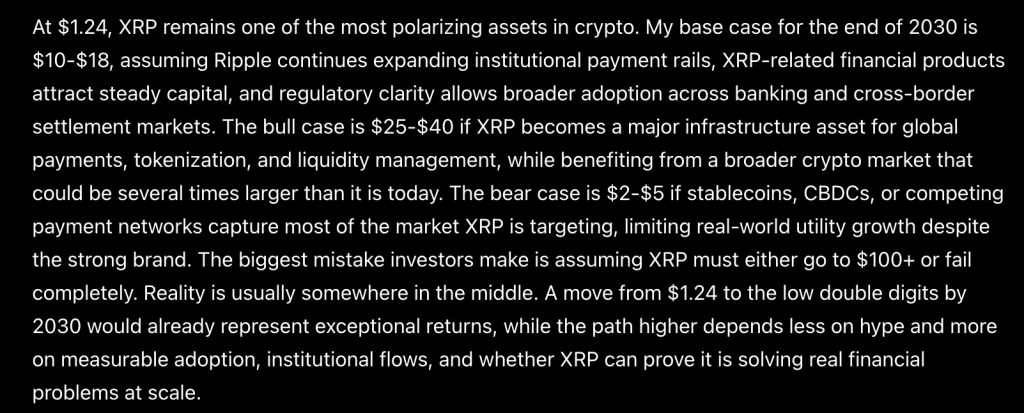

There is a line in this prediction that cuts through the noise better than any price target. The biggest mistake investors make is assuming XRP must either go to $100 plus or fail completely. Sam Altman’s ChatGPT is essentially asking the XRP community to grow up, to stop swinging between cult and obituary, and to start thinking about this asset the way you would any infrastructure play with a long runway ahead.

The base case for end of 2030 is $10 to $18 from $1.24 today, roughly an 8x to 14x over 4 years, which sounds modest until you frame it correctly.

That is the scenario where Ripple just keeps doing what it is already doing, expanding institutional payment rails, attracting steady capital into XRP-related financial products, and riding the regulatory clarity that has been slowly materializing.

No moonshot assumptions required, just execution and adoption continuing at the current pace.

The bull case at $25 to $40 is where the story gets genuinely interesting. That range implies XRP has crossed the threshold from promising network to critical global infrastructure, embedded into cross-border settlement, tokenization flows, and liquidity management at a scale that commands a serious premium.

It also assumes the broader crypto market is several times larger than today, which is not a stretch for a 4-year horizon if institutional adoption keeps compounding.

The bear case at $2 to $5 is the scenario in which stablecoins, CBDCs, or competing payment networks eat XRP’s lunch despite its brand strength, capturing the market it is targeting before it can fully claim it.

XRP Price Prediction: The Weekly Chart Has A Story To Tell Too

Pull up the weekly, and the first thing that hits you is the sheer scale of what happened in late 2024. XRP launched from under $0.70 and ran to $3.84 in a matter of weeks, one of the most violent altcoin moves in recent memory.

What followed was an equally persistent grind back down, and the weekly chart now shows price at $1.24, sitting just above the pre-breakout consolidation zone that held for most of 2023 and early 2024.

That context matters for the 2030 thesis. XRP has already proven it can reprice dramatically when conditions align.

The question ChatGPT is really asking is whether the next reprice is driven by the same speculative frenzy or by something more durable underneath.

The $1.00 to $1.30 region is now the critical zone, a range that served as resistance for years before the 2024 breakout and now sits as long-term support.

Lose it on a weekly close, and the setup gets complicated. Hold it, and you have a base that serious infrastructure tends to build from.

The RSI on the weekly is at 36.02 with the signal line just below at 35.11, nearly flat against each other, with the gap barely over 1 point.

That tight convergence after a long drift lower tells you momentum has stopped declining but has not yet found a reason to accelerate upward. It is the RSI equivalent of a held breath, compressed and waiting for a catalyst.

Given that ChatGPT’s whole argument rests on measurable adoption and institutional flows rather than hype, that compressed momentum makes sense. The chart is not pricing in $10 yet. It is simply stopping the bleeding and asking what comes next.

Here is What ChatGPT AI Predicts For LiquidChain Near Future, Could be Very Bullish

Large-cap traders are not positioning. They are standing in line.

Bitcoin, Ethereum, and XRP have been pressing against the same ceilings for weeks. The catalyst is always one print away. The institutional inflows are always next quarter. Every breakout depends on a decision made by someone else.

Early-stage infrastructure plays by different rules. Capital that disappears as noise at Bitcoin’s scale moves an undiscovered project by multiples. The return lives in the gap between what something is genuinely worth and what the market has priced it at. That gap closes the moment the project gets found.

Cross-chain fragmentation has been bleeding DeFi since the first bridge launched. Bitcoin, Ethereum, and Solana were built as separate systems with no intent to interoperate. Every transaction crossing those boundaries pays for that in fees, slippage, and failed execution. Bridges were supposed to fix it. They became the toll booth.

LiquidChain removes the toll booth entirely. Three networks inside one execution layer. One deployment. No cross-chain tax.

Copilot AI flagged it as worth watching. The presale is at $0.01454 with just over $835,000 raised.

Execution is unproven. Adoption is unknown. Established assets offer a predictable ride toward a ceiling that is already visible. LiquidChain is an entry point that disappears once the market finds it.

Explore the LiquidChain Presale

The post Sam Altman ChatGPT Predicts Explosive XRP Price by End of 2030 appeared first on Cryptonews.

Nearly all of the top 100 cryptocurrencies have recorded substantial gains over the last 24 hours, boosted by news of the peace deal between the United States and Iran.

Hyperliquid (HYPE) stands out among the top performers, with its price spiking by 12%. Some analysts believe it may jump even more in the following days, while others cautioned that the bears may soon regain control.

Going Higher?

In early June (when the broader crypto market was bleeding heavily), HYPE exploded to an all-time high of around $75. However, the historic peak was short-lived, and the price headed south to around $53 in the following days, influenced by bearish factors such as Arthur Hayes’s decision to dump all his positions in the asset.

Currently, though, the asset trades at around $68, representing a 28% increase from the local bottom. Moreover, its market capitalization has surged past $15 billion, and thus HYPE re-entered crypto’s elite top 10 club after surpassing the OG meme coin Dogecoin (DOGE).

According to some analysts, the recent pump to almost $70 simply marks the early stages of a much larger upward move. X user Cozy the Caller thinks that HYPE “just goes straight to $100 from here.”

KNIGHT and Owl Prints were also optimistic. The former projected a rise above $110 in the coming months, while the latter argued that reclaiming $64.60 (which, for the moment, seems to be the case) “opens up a clean run toward previous cycle peaks.”

The Bearish Outlook

Last week, many market observers spotted the formation of a head-and-shoulders pattern on HYPE’s chart, which has historically been a precursor to a pullback.

Several hours ago, Ali Martinez opined that the recent price action has seemingly shaped the right shoulder of that structure, labeling $65 as the key resistance level. He also warned that losing $54 could trigger a major correction down to $40.

HYPE’s current Relative Strength Index (RSI) raises the possibility of a sudden price drop. The technical analysis tool runs from 0 to 100, and ratios above 70 signal that the asset is overbought and due for a potential pullback. As of this writing, it stands at 93, showing that the valuation has surged in an unhealthy manner.

The next bearish element worth mentioning is HYPE’s exchange netflow. Over the past three days, investors have moved some of their holdings from self-custody to centralized platforms, with inflows outpacing inflows. This increases immediate selling pressure.

The post Hyperliquid (HYPE) Soars 12% in a Day: More Gains Ahead or a Bull Trap? appeared first on CryptoPotato.

Ethereum has surged nearly 6% and attracted fresh whale buying after a reported U.S.-Iran peace agreement improved risk sentiment across global markets.

Summary

- A wallet reportedly linked to Arthur Hayes received 3,000 ETH worth $5.42 million as Ethereum rallied following news of a U.S.-Iran peace agreement.

- Ethereum climbed nearly 6%, while another whale, geministar.eth, accumulated 21,136 ETH worth about $37 million from Binance.

- Technical indicators show ETH breaking above a multi-week downtrend, with analysts eyeing the $1,850-$1,860 resistance zone.

According to on-chain tracker Lookonchain, a wallet possibly linked to BitMEX co-founder Arthur Hayes received 3,000 ETH worth approximately $5.42 million from market maker Flowdesk on June 15. The transfer came as Ethereum rallied alongside other cryptocurrencies following signs that tensions in the Middle East may be easing.

The purchase follows a period in which Hayes had been reducing exposure to several altcoins. In his June 8 essay titled Reality Test, the Maelstrom chief investment officer disclosed that he had sold positions in Hyperliquid, Near Protocol, Worldcoin, and Zcash.

Hayes described the moves as a defensive response to macroeconomic risks rather than a rejection of those projects, while noting that Bitcoin and Ethereum remained among his core holdings.

Ethereum extends gains as risk appetite returns

Support for risk assets strengthened after U.S. President Donald Trump announced that a peace deal with Iran had been completed. Trump said shipping traffic through the Strait of Hormuz had resumed and that vessels carrying oil were once again moving through what he described as a secure route.

The development triggered a sharp decline in energy prices. Crude oil fell more than 5% to around $80.53 per barrel, easing concerns that disruptions in one of the world’s most important energy corridors could fuel inflation and weigh on financial markets.

Ethereum responded strongly to the change in sentiment. At press time, ETH traded near $1,828 after climbing almost 6% over the previous 24 hours. The move pushed the asset to its highest level in more than a week and helped it outperform several major cryptocurrencies during Monday’s session.

Large investors appeared to be adding exposure during the rally. Separate data shared by Lookonchain showed that wallet address geministar.eth purchased 21,136 ETH worth roughly $37.05 million from Binance through a series of transactions on June 15.

Technical indicators point toward $1,850 test

Price action has also improved from a technical perspective. On the daily chart, Ethereum has broken above a descending trendline that had capped rallies since late April. The move places ETH above the upper boundary of a bearish flag structure that had formed during the decline from roughly $2,400.

Momentum indicators have started to recover as well. The daily MACD has produced a bullish crossover, while the Chaikin Money Flow indicator has been moving higher, signaling that selling pressure is fading.

Additional upside could depend on whether Ethereum clears a key resistance zone near the 0.618 Fibonacci retracement level around $1,858. A successful move above that area would strengthen the argument that the recent breakout is invalidating the bearish flag pattern rather than confirming it.

Meanwhile, crypto analyst Ali Martinez pointed to a potential ascending triangle breakout on Ethereum’s four-hour chart. According to Martinez, confirmation of the pattern projects a move toward $1,850, placing the target almost directly in line with the resistance area currently being tested.

Even before the latest purchase, Hayes had maintained an optimistic outlook on Ethereum. In a June market thesis, he projected that ETH could reach between $10,000 and $20,000 before the current market cycle ends, citing expected liquidity growth and Ethereum’s position within decentralized finance.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Most of the crypto sector climbed over the past seven days, yet meme coins slipped 1.1% and split beneath the surface. That divergence is where the meme coins to watch are hiding.

On-chain positioning now tells a sharper story than price. One token is cooling from a record high, another shows whales accumulating then booking profit, and a third has smart money buying the dip whales are selling.

BinanceLife (币安人生)

BinanceLife, known in Chinese as 币安人生, is interesting precisely because its timeframes disagree. The token is up more than 73% over 30 days, down about 12% on the week, yet up roughly 4% on the day. That conflict captures a meme coin still trending up but fighting heavy short-term volatility.

Want more token insights like this? Sign up for Editor Harsh Notariya’s Daily Crypto Newsletter here.

It draws its entire narrative from the shared name with CZ’s memoir, with no utility or roadmap behind it. That makes positioning, not fundamentals, the only real guide to where it goes next.

The flows split sharply. Exchange outflows hit $1.2 million over seven days, a classic accumulation pattern as tokens leave exchanges for private wallets. Top profit-taking traders added $910,000 across 25 proven wallets. That is the bullish core.

The risk sits opposite. Multiple whales trimmed positions, one mega-holder sold 356 million tokens, and the top two wallets control roughly 63% of supply. Concentration is the hazard to watch.

The chart frames the next move. After topping near $0.90 on June 7, BinanceLife has corrected inside a descending channel, and its latest push higher was met by sellers (possibly whales) at the channel top. The 20-period exponential moving average, a trend gauge that weights recent prices, sits near $0.68. Holding it keeps $0.69 and then $0.73 in play, and a break above $0.73 would end the bearishness and open a move toward $0.80.

Losing $0.68 puts $0.63 in focus. That level decides whether accumulation or distribution wins.

Pepe (PEPE)

Pepe earns its spot among the meme coins to watch on a clean conflict between whale accumulation and profit-taking. The token is up about 5.2% over seven days and 2.8% on the day, a steady climb that is now drawing sellers.

The on-chain story is the hook. Whale supply, the share held by the largest wallets with exchanges excluded, jumped sharply on June 14, rising from roughly 181 trillion to about 183.6 trillion tokens. That addition is worth close to $7.5 million at current prices, a clear accumulation spike.

Then it turned. Whales have started trimming that fresh stash, easing back toward 183 trillion as the price pushed higher. That sequence, buying hard and then booking profit into strength, is the pattern that defines the week. How deep the profit-taking runs is the question.

The chart sharpens it. Pepe has rebounded almost 17% from its June 6 low near $0.00000252, but volume has thinned steadily since June 12 even as price climbed. Falling volume on a rising price is a bearish divergence, a sign buyers are losing force into resistance.

That resistance sits at $0.00000300, the level where whale selling could cap the move. A daily close above it would show buyers absorbing the distribution, opening a path toward $0.00000331. Failing there hands control back to the sellers trimming their stash. That tug-of-war is what makes Pepe one of the meme coins to watch.

Official Trump (TRUMP)

Official Trump is the macro-sensitive name among the meme coins to watch, tied closely to the US-Iran peace-deal narrative that has driven sentiment since early June. If that deal weakens, TRUMP could see a sharp sentiment swing, which makes its positioning worth tracking now.

The token has been hammered, trading near $1.99 against the $4.50 high it reached in March. A rebound stalled near $2.38, but selling pressure is now easing, which hints the next pullback may be shallower if flows cooperate.

The flows are split but lean constructive. On Hyperliquid perpetual futures, smart traders hold a roughly 3-to-1 long bias and top profit-taking traders added $158,000 over seven days, an inflow running far above their average. That is aggressive accumulation from historically winning wallets.

The offset is whale behavior. Whales cut about $393,000 over the week and one large holder shed 417,000 tokens, while exchange inflows of $457,000 hint at sell pressure. Smart money is buying the dip that whales are selling into.

The chart sets the test. Reclaiming $2.20 keeps the recovery alive, and if smart money holds while whales stay sidelined, $2.64 and $2.99 come into view.

Only a break above $3.35 would end the broader downtrend, which looks distant. If smart money flips to selling alongside the whales, $1.49 returns to the table. That balance makes Official Trump one to watch.

The post 3 Meme Coins to Watch in the Third Week of June 2026 appeared first on BeInCrypto.

Much of the activity has occurred on offshore exchanges, including fast-growing platforms such as Hyperliquid, which has attracted professional traders seeking deep liquidity and continuous access to leveraged markets. Prediction market Kalshi, which introduced perps on its platform earlier this month, saw over $1 billion in trading volume within just one week.

The debut comes weeks after the CFTC signaled that regulated platforms could offer perpetual futures. In May, the agency approved Kalshi’s bitcoin perpetual contracts and issued guidance that also cleared a path for Coinbase (COIN) to connect U.S. customers to global options and perpetual markets.

Kraken has been building toward the introduction through a series of derivatives-focused acquisitions and product releases. The company acquired NinjaTrader in May 2025 and Bitnomial a year later to gain regulated futures infrastructure. It recently added CME-listed crypto futures and margin trading for U.S. customers.

Kraken’s head of derivatives John Palmer told CoinDesk last week that adoption may mirror the trajectory of spot bitcoin exchange-traded funds (ETFs), with sophisticated traders entering first before investment advisers and asset managers follow after completing internal reviews.

At launch, Kraken’s perpetual futures cover major cryptocurrencies including BTC, ETH, SOL, XRP, ADA, LINK, DOGE, LTC and AVAX. The company said it plans to expand the range of contracts and collateral options over time.

Standard Chartered's research division initiated coverage of Uniswap, the largest decentralized exchange, with a thesis that ties its governance token to the institutional tokenization wave. The bank's Geoff Kendrick, global head of digital assets research, argues Uniswap is positioned to become… Read the full story at The Defiant

Pudgy Penguins CEO Lucas Netz claims his mobile game app Pudgy Party lost the NFT firm millions of dollars before it was shuttered last weekend.

The company announced the closure last Friday. It didn’t explain why Pudgy Party was shuttered, only that its web-based game, Pudgy World, is set to exceed Pudgy Party’s metrics.

“[Pudgy Party] being wholly ours, has everything we need to make it the flagship gaming product of the Pudgy Penguins universe,” the company said.

However, in a follow-up meeting with Pudgy Penguin NFT holders, Netz revealed the key numbers leading to Pudgy Party’s closure.

Read more: Web3 collapse accelerates as eight games fail this year

According to X user and Pudgy Penguin holder @ChefJames_, Netz claimed that the game had lost the firm millions of dollars and that if it were to continue, it would cost it another $2.5 million.

Netz added that the game experienced a few short months of popularity before its player count sharply dropped to somewhere between 200 and 300 active users.

Pudgy Party promised users more money than a minimum wage job

Pudgy Party was a third-person platformer that drew inspiration from reality show obstacle courses such as Total Wipeout, and was similar to the game Fall Guys, which itself saw player count highs of 172,026 on Steam.

Developed by Mythical Games and launched in August 2025, the game’s monetization system involved selling skins of the game’s penguin character, which buyers could trade.

Some of these listed skins were on offer for up to $100,000 despite possessing an actual value (floor price) of just 50 cents. During the game’s initial launch, some users were paying above $1,000 for skins, while others supposedly spent up to $5,000.

At one point, Netz claimed that the skin system would allow users to make more money than a minimum wage job if they just played the game full time.

Read more: Pudgy Penguins removes ‘racist’ post after Manchester City complaint

As for what will happen to the skins, @ChefJames_ noted that during the Pudgy Penguin meeting, Netz claimed that there will be a portal put in place for rewards and that skins purchased for Pudgy Party will be transferable to Pudgy World.

More Pudgy Penguin closures to come?

Things could get worse for Pudgy Penguins with the possibility of more closures and cutbacks to come. Indeed, Netz warned that across the coming two weeks, “All Band-Aids will be ripped.”

Some users speculated that Abstact, the blockchain co-founded by Netz, will be on the chopping block next, but not everyone agreed.

During the meeting, Netz also claimed that Pudgy Party didn’t match the brand’s DNA, which is pushing for a social game, aka Pudgy World.

Pudgy World was launched in March 2026 and is another attempt from the firm to create a web3 game. According to Netz, Pudgy World dwarfed Pudgy Party’s player count, with daily player counts up to 20,000.

This game appears inspired by the once popular web game Club Penguin and attempts to recreate the same social experience, albeit with a 3D third-person perspective.

Like Pudgy Party, it also features an ecosystem based around buying and selling cosmetics.

Read more: Pudgy Penguins bets $500K on Vegas Sphere — PENGU still down 85%

Web3 games have been struggling lately, with a growing number shutting down due to low player counts and insufficient revenues.

Among these is Uncharted, the developer behind crypto-based game Fishing Frenzy, which announced that the two were shutting down today.

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

Kalshi has deployed an artificial intelligence agent to help decide which prediction markets to launch as trading activity on the platform has climbed to more than $5 billion in a single week.

Summary

- Kalshi has deployed an AI agent called Harrison to help evaluate and recommend new prediction markets.

- FIFA World Cup betting activity helped push Kalshi’s weekly trading volume to a record $5.1 billion.

- The platform’s expansion comes as U.S. regulators and states continue to dispute oversight of prediction market contracts.

According to a Bloomberg report, the prediction market operator has introduced an internal AI system called Harrison to assist with several day-to-day functions tied to its exchange.

The tool is being used to review news developments, monitor competing platforms, recommend new contracts for listing, and identify where liquidity incentives may be most effective.

Bloomberg reported that Harrison forms part of Kalshi’s internal markets team and contributes to the process of evaluating potential contracts before they reach users.

Speaking to the publication, Kalshi co-founder Luana Lopes Lara said the company also employs an AI engineer whose work includes using AI systems to stress-test certification processes and identify possible weaknesses before markets go live.

The rollout comes as prediction markets continue to draw regulatory attention across the United States. State regulators have argued that some event contracts resemble traditional gambling products, while federally regulated exchanges maintain that they operate under commodities laws overseen by the Commodity Futures Trading Commission.

Sports contracts fuel record activity

Trading volumes have accelerated alongside growing interest in sports-related contracts. According to Bloomberg, demand tied to the FIFA World Cup helped push Kalshi to nearly $18 billion in notional trading volume during May, citing data from Dune Analytics.

The same report stated that Kalshi recorded approximately $5.1 billion in volume during the first week of the tournament this month, setting a new weekly high for the platform. Sports markets have become one of the exchange’s fastest-growing categories, joining election, economic, and entertainment contracts that already attract significant user activity.

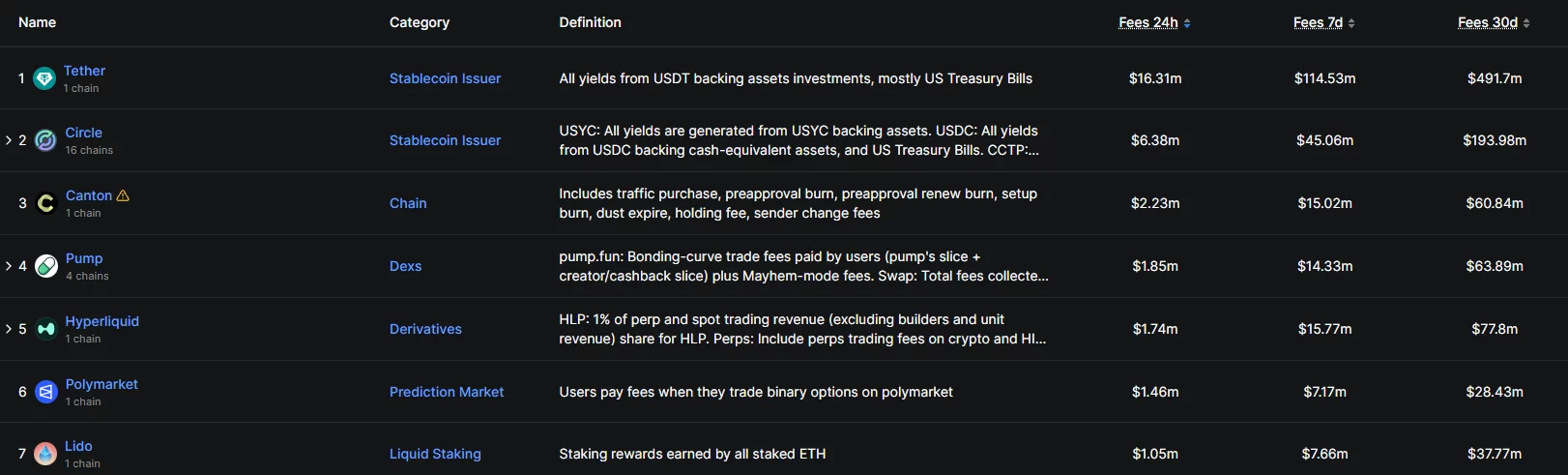

Elsewhere in the sector, sports wagering demand has also boosted activity on prediction market rival Polymarket. According to DefiLlama data, Polymarket generated around $1.46 million in fees over the last 24 hours and roughly $7.17 million during the previous seven days, placing it among the highest fee-generating crypto protocols during those periods.

Federal regulators challenge state enforcement efforts

At the same time, prediction markets remain at the center of an ongoing regulatory debate in the United States. As reported by crypto.news earlier, the CFTC has proposed new rules for prediction market platforms while also defending federally regulated exchanges against enforcement efforts by several states.

According to a lawsuit filed by the CFTC on Friday, the agency has sued New Mexico officials over efforts to apply state gaming laws to federally regulated prediction market exchanges. The regulator argued that event contracts listed on CFTC-registered exchanges fall under federal commodities law and therefore remain subject to its exclusive oversight.

The filing follows New Mexico’s June 4 lawsuit against Kalshi, in which state authorities alleged the platform was offering sports betting without a license and allowing users aged 18 to 20 to participate despite the state’s minimum gambling age of 21.

Paradigm has led a roughly $9 million funding round in El Dorado, a stablecoin-powered payments application built for Latin America. The deal pushes one of crypto's largest venture firms deeper into dollar-rails for emerging markets. The round was reported by The Block, which said Paradigm led the… Read the full story at The Defiant

Blue Jays trade Connor Seabold to Royals for minor-league pitcher

iOS 27 and macOS 27 pack strong evidence of iPhone Fold and touch MacBook Pro

How to manage your money #finance #philippines #financetips

-

Business1 day ago

Business1 day agoNo Jackpot Winner as $257 Million Prize Rolls Over to $269 Million Monday Draw

-

Crypto World4 days ago

Crypto World4 days agoOppenheimer backs SpaceX as $70 billion retail frenzy builds

-

Crypto World4 days ago

Crypto World4 days agoMarkets Rally as SpaceX IPO Looms Amid Iran Tensions and Inflation Surge

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: Tuckernuck – Corporette.com

-

Crypto World19 hours ago

Crypto World19 hours agoZimbabwe Requires Crypto Businesses to Register Annually Under New FIU Regulations

-

Entertainment6 days ago

Entertainment6 days agoThe Ryan Gosling True Crime Thriller On Netflix That Gets Even Stranger, Stream It Now

-

Sports6 days ago

Sports6 days agoBangladesh beat Australia after 20 years in ODIs, register only their second win over six-time world champions | Cricket News

-

Tech3 days ago

Tech3 days agoNanoClaw integrates JFrog registries to secure AI agent downloads

-

Tech3 days ago

Tech3 days agoThis Week In Security: Microsoft On Microsoft, Register Your Domains, Linux On ARM, And FreeBSD Joins The File Cache Club

-

Crypto World2 days ago

Crypto World2 days agoBitget enters Argentina’s regulated crypto market through PSAV registration

-

Politics4 days ago

Politics4 days agoPolitics Home | Healey Resignation Is “Colossal Failure Of Government”, Says Former Labour Defence Secretary

-

Tech4 days ago

Tech4 days agoDutton Ranch star claims they ‘didn’t see any disruption’ on set following Chad Feehan’s exit from Yellowstone spinoff fueled by Taylor Sheridan clash rumors

-

NewsBeat4 days ago

NewsBeat4 days agoEl Nino has formed in the Pacific and could set records, forecasters say

-

Tech5 days ago

Tech5 days ago‘This is Seattle’s position on AI’: City Council votes unanimously to pause big new data centers

-

Entertainment4 days ago

Entertainment4 days agoDonnie Wahlberg & More Heat Up Las Vegas at Circa’s Barry’s Downtown Prime

-

Sports4 days ago

Sports4 days agoFirst Time Since 1971: Australia Register Historic Low In ODI Cricket

-

Tech4 days ago

Tech4 days agoOpendoor Ends India Operations, Fueling a Bigger Conversation About AI and Outsourcing

-

Politics4 days ago

Politics4 days agoBelfast burns, while Met chief points finger at Iran and Russia

-

Business6 days ago

Business6 days agoThailand Ranks Second Worldwide for AI Adoption Growth, Microsoft Reports

-

NewsBeat3 days ago

NewsBeat3 days agoFBI searches office of Ohio voter registration group

You must be logged in to post a comment Login