Crypto World

South Korea FIU Urges Wider Travel Rule for Small Crypto Transfers

South Korea’s Financial Intelligence Unit (FIU) has pressed for tighter global reporting standards for cryptocurrency transfers, urging a broader application of the FATF “Travel Rule” to reduce gaps in cross-border anti-money laundering (AML) controls. The push reflects concerns that current implementation leaves smaller transactions and counterparties outside meaningful compliance coverage.

During a FATF plenary session in Paris last week, the FIU proposed expanding the Travel Rule obligations to smaller crypto transfers and called for more comprehensive coverage across both originating and receiving crypto asset service providers (CASPs). The FIU also highlighted the continuing policy divergence that can enable regulatory arbitrage, while FATF approved additional work related to decentralized finance (DeFi) risk.

Key takeaways

- South Korea’s FIU urged expanding FATF Travel Rule requirements to cover smaller crypto transfers, not only large-value movements.

- The FIU recommended that Travel Rule obligations apply to both originating and receiving CASPs to reduce cross-border compliance gaps.

- FIU officials called for tougher scrutiny of offshore and unregistered crypto platforms, citing increased misuse in illicit finance cases.

- FATF approved a DeFi-focused report, while South Korea’s FIU warned that jurisdictional licensing and supervision differences continue to drive regulatory arbitrage.

Expanding the Travel Rule: from thresholds to broader coverage

The FIU’s proposal focuses on the practical operation of the FATF Travel Rule, an AML standard intended to improve traceability for crypto transfers by requiring exchanges and other CASPs to transmit relevant sender and recipient information when transfers exceed defined thresholds. According to FIU materials, the goal is to ensure that the compliance perimeter is not limited to large transactions that may be more likely to be detected under existing frameworks.

South Korea already applies Travel Rule obligations to crypto transfers above 1 million won (approximately $650). The FIU’s latest recommendation seeks to extend those requirements downward, which would likely increase the number of transfers subject to information-sharing expectations and create additional operational and compliance burdens for regulated firms.

For institutional compliance programs, this matters because threshold-based controls can create exploitable boundaries. Reducing the value cutoffs can change how monitoring systems are configured, what data fields are required, and how firms document and evidence compliance during audits and supervisory reviews.

Closing cross-border gaps: originating and receiving CASPs

Beyond lowering transaction thresholds, the FIU argued that Travel Rule requirements should cover both sides of a transfer. Specifically, it called for obligations to apply to originating and receiving CASPs, reflecting an emphasis on end-to-end information flows rather than fragmented compliance limited to only one entity in a transaction chain.

The FIU’s position is aligned with a broader policy objective: AML regimes are only as effective as the continuity of controls between jurisdictions. If receiving CASPs do not have compatible obligations—or if counterparties in different regulatory environments are not required to provide or obtain the same information—then traceability can be lost even when rules exist at the point of origin.

The FIU also tied its recommendations to the broader problem of cross-border regulatory fragmentation. It warned that differences in licensing structures, supervisory approaches, and offshore oversight can produce inconsistent enforcement outcomes—an environment in which regulatory arbitrage becomes a systemic risk rather than an edge case.

Enforcement emphasis: unregistered platforms and offshore activity

In addition to tightening data-sharing expectations, the FIU called for stronger action against offshore and unregistered crypto platforms. The FIU linked this to what it characterized as heightened misuse in illicit finance cases, as well as the risk that criminals can shift activity to venues with weaker oversight.

For regulated market participants, this direction suggests greater compliance attention not only to transaction monitoring but also to counterparty risk management. Institutional firms typically implement controls to assess whether counterparties are properly licensed or subject to effective supervision, and proposals like this can raise the expectation that those controls remain robust even when counterparties are operating abroad.

From a compliance and legal perspective, stronger action against unregistered platforms can also increase pressure on regulated entities to demonstrate due diligence regarding onboarding, ongoing monitoring, and contractual safeguards. It may affect how firms interpret “compliance reach” when interacting with cross-border service providers whose regulatory status or supervision quality is uncertain.

FATF also advances work on DeFi risk and implementation unevenness

Alongside the Travel Rule discussion, FATF approved a new report examining risks associated with decentralized finance (DeFi), according to FIU reporting. FIU Commissioner Lee Hyung Ju welcomed adoption of the DeFi-related work but emphasized that much of the regulatory arbitrage seen across jurisdictions stems from structural differences—particularly the divergence in licensing, supervision, and offshore oversight.

The Travel Rule debate also comes against the backdrop of FATF’s broader assessment of implementation. The FIU referenced FATF’s update indicating that compliance with parts of Recommendation 15 remains inconsistent globally, even years after FATF extended its AML framework to cover crypto assets and CASPs.

According to a FATF-targeted update cited by the FIU for April 2025, 49% of jurisdictions were assessed as only partially compliant with requirements for CASPs, 21% were rated non-compliant, and roughly 29% were rated largely compliant or compliant. The unevenness is significant because global standards depend on coordinated implementation to be effective in practice—especially for cross-border activity where regulated and less-regulated actors may interact.

This gap also matters for supervised entities operating in multiple markets. When compliance expectations differ across jurisdictions, firms may face higher compliance costs and greater legal uncertainty in determining which standard applies to particular counterparties and transaction pathways.

Policy context: seven years after FATF expanded the framework

The FIU’s proposals are part of ongoing discussions on implementing FATF Recommendation 15, the international standard updated in 2019 to bring AML measures to crypto assets and CASPs. Seven years on, FATF has continued to refine its understanding of how the Travel Rule should be applied operationally and what gaps remain in implementation.

For South Korea’s regulated sector, the FIU’s stance indicates a move toward closer alignment with stronger, more expansive interpretations of the Travel Rule. Since South Korea already implements Travel Rule controls for transfers above a defined threshold, expanding coverage to smaller transfers would represent an escalation in the scope of information-sharing obligations.

However, the policy question that remains open is how jurisdictions will calibrate thresholds and practical implementation requirements without creating disproportionate operational friction. Differences in data availability, transaction routing mechanics, and system interoperability can influence whether the compliance intent of the Travel Rule translates into consistent implementation at scale.

Closing perspective

With FATF’s continued work on Travel Rule implementation and DeFi risk, regulators are signaling that AML expectations for digital-asset activity will likely tighten over time—particularly around information-sharing coverage and supervision of cross-border counterparties. For compliance leaders and legal teams, the next developments to monitor include how FATF operational guidance evolves and whether South Korea and other jurisdictions move toward lower thresholds and broader CASP-to-CASP obligations.

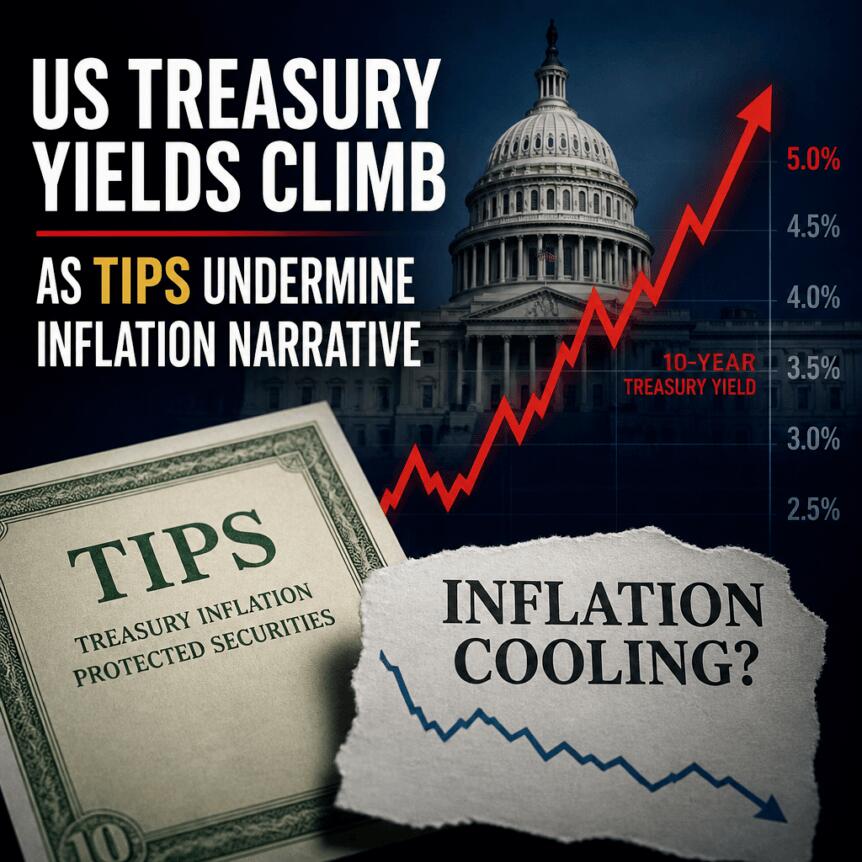

US Treasury yields have been rising for months, and the market’s latest move has pushed 30-year rates to their highest level since 2007. While mainstream coverage has largely pinned the sell-off on inflation concerns tied to higher energy prices, analysis of inflation-protected bonds suggests the more important driver is the climb in real yields—an outcome that can be especially challenging for assets that don’t pay investors along the way, including Bitcoin.

The shift is also changing the trade-offs between traditional fixed-income strategies and crypto exposure. According to Glassnode’s latest research, government bond investments have become more profitable than certain cash-and-carry style trades in crypto markets for the first time since 2019.

Key takeaways

- 30-year Treasury yields have surged to the highest levels since 2007 amid a multi-month sell-off in government debt.

- Market pricing for a September rate hike is elevated, with CME FedWatch placing the probability at 63%.

- Treasury Inflation-Protected Securities point to falling five-year inflation expectations (around 2.2% and trending down since May), even as nominal yields rise.

- Data indicates the nominal yield increase is driven more by rising real yields than by higher inflation expectations—typically a headwind for non-yielding assets.

- Multiple potential transmission channels to crypto exist, but the direction is generally bearish if higher real rates reflect weaker growth or tighter liquidity.

Why Treasuries are selling off again

After US government debt yields hit local lows in early March, Treasuries have entered a prolonged period of selling. Following the most recent FOMC meeting, 30-year Treasury yields made headlines by reaching levels not seen since 2007. Within the same window, the two-year yield climbed by 76 basis points, and markets increasingly price another Fed move: a September rate hike is currently weighted at 63% according to CME FedWatch.

The higher the yield environment becomes, the more investors compare alternatives across asset classes. Glassnode’s research—published in its “The Week Onchain” series—notes that, for the first time since 2019, returns from government bond investments have become more attractive than cash-and-carry style trades involving crypto futures.

Inflation fears are loud, but TIPS tell a different story

Many observers have connected the bond sell-off to rising commodity and energy prices. The timing overlaps with the start of the Iran war and the resulting closure of the Strait of Hormuz, and the daily moves in oil and interest rates have tracked each other since March. In that framing, stronger crude prices feed directly into inflation expectations, pushing yields higher.

However, inflation-protected securities complicate that narrative. Treasury Inflation-Protected Securities (TIPS) are designed so their principal—and therefore their coupon payments—are adjusted to reflect the Consumer Price Index. Because TIPS exist alongside regular Treasuries of similar maturity, comparing their yields allows investors to estimate the market’s implied inflation path through the breakeven rate.

According to data referenced from FRED, the five-year breakeven inflation rate has dropped sharply since May and is currently around 2.2%. That figure suggests the market expects the Fed to achieve its 2% inflation target over the medium term. More importantly, the breakeven rate has been moving in the opposite direction to nominal Treasury yields: while nominal yields rise, the inflation component implied by TIPS declines.

In the dataset cited, a 33-basis-point increase in the five-year nominal yield is paired with an 84-basis-point rise in the real yield, partially offset by a 51-basis-point decline in expected inflation. In other words, the market’s “real yield” story is changing—and it is the real rate that appears to be doing the heavy lifting.

What higher real yields can mean for Bitcoin and other non-yielding assets

In general, when real returns on traditional investments rise—after adjusting for CPI—investors may prefer assets that offer carry rather than those that do not. Bitcoin is typically treated as a non-yielding asset in this framework, so the direction of travel in real rates can matter.

Still, the impact on crypto depends on why real yields are moving higher. The analysis outlines several mechanisms that can coexist, with different implications for liquidity and demand.

1) FX or reserve liquidation pressures: unclear for crypto

One possible explanation involves global currency and funding dynamics. Higher oil prices can worsen trade balances for energy importers in Asia because oil is priced and settled in US dollars. That can lead to pressure in offshore US-dollar funding markets and force central banks to intervene to defend exchange rates.

The discussion cites Cointelegraph coverage of yen defense and Bloomberg reporting on interventions involving the Philippine peso and Indian rupee. It also notes that these interventions can be funded by selling US Treasury reserves, which can increase upward pressure on yields. In this scenario, the bond sell-off may reflect external funding strain rather than a direct verdict on the dollar or inflation.

As a result, the direct implications for crypto are not automatic: if the driver is more about FX mechanics than about deteriorating growth expectations, crypto’s reaction could be muted or different from the classic “rates up, risk assets down” story.

2) Demand destruction and recession risk: bearish setup

Another pathway is growth damage. If an oil shock persists long enough, the argument goes, it stops being merely inflationary and begins to suppress economic output. Neuberger Berman’s fixed-income outlook—referenced in the analysis—suggests investors may be underpricing how sustained energy costs could hit output.

That matters because a recessionary environment typically tightens liquidity. In such conditions, both equities and Bitcoin can face pressure as credit conditions worsen and risk appetite declines. The analysis also points to the expectation of widening credit spreads as a sign that credit could deteriorate.

It further references Cointelegraph reporting on early signals of stress, connected to rising costs to insure AI-linked debt amid an Asian semiconductor pullback. While that example is specific, it underscores the broader theme: if credit markets begin to price higher risk, non-yielding and speculative assets often struggle.

3) Capital competition from AI issuance: another headwind

A third channel is that higher real rates may be tied to expected growth and capital demand—especially from the AI sector. The analysis argues that as corporate bond issuance, including from major AI-related players, becomes unusually large, government issuance competes more directly for investor capital.

Goldman Sachs Research is cited projecting roughly $755 billion of AI capex in 2026 and about $920 billion in 2027. UBS is also cited as raising its 2026 investment-grade issuance forecast to $1.8 trillion, with technology supply lifted to $360 billion based on hyperscaler guidance. In that environment, investors’ willingness to allocate incremental capital to crypto could be constrained, not necessarily because crypto is “bad,” but because the fundraising pipeline elsewhere is intense.

What to watch next

For crypto investors, the critical question is whether TIPS-implied breakevens stabilize while real yields remain elevated—or whether the market reinterprets the move as a growth scare. Watching the evolution of TIPS breakevens and real-yield dynamics, alongside credit conditions such as spreads, may provide the clearest signal on whether this bond sell-off turns into a sustained liquidity headwind or fades as a temporary funding/energy-driven episode.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

XRP ETF inflows surpass $1.5 billion as investors explore alternative digital asset strategies, including cloud mining and DeFi yield platforms.

Summary

- Rising XRP ETF inflows are boosting interest in EX DeFi as investors explore cloud mining and yield opportunities.

- As XRP ETF inflows top $1.5 billion, EX DeFi highlights cloud mining as an alternative way to earn on XRP holdings.

- Institutional demand lifts XRP ETF inflows past $1.5 billion, while EX DeFi promotes long-term crypto yield solutions.

The XRP-backed ETF has just surpassed a significant milestone in inflows, further boosting institutional investor confidence. Simultaneously, a growing number of investors are turning their attention to ex-DeFi, hoping to explore more long-term yield opportunities beyond simply waiting for XRP prices to rise.

The continued inflows into the XRP ETF further demonstrate the growing demand for XRP from institutional investors. While retail investors remain cautious due to market volatility and price uncertainty, institutional funds continue to allocate XRP through regulated financial products, keeping it one of the most watched mainstream digital assets in the market.

As the regulatory environment and funding conditions continue to improve, many investors are beginning to consider a practical question: are there more efficient and sustainable ways to participate in the long-term returns of XRP besides waiting for prices to rise?

The milestone of XRP ETF inflows surpassing $1.5 billion is significant.

As of the closing on July 29, the XRP spot ETF market has reached a significant milestone. According to data released by the analytics platform uToday, driven by continuous net inflows, XRP-related exchange-traded funds (ETFs) have seen cumulative inflows exceeding $1.5 billion.

Meanwhile, the overall market liquidity has continued to improve. Although secondary market trading activity has slowed somewhat, and retail investor sentiment remains relatively cautious, institutional investor allocation demand has remained stable, resulting in net inflows on most trading days.

A new option for XRP investors: The yield growth path of EX DeFi

In light of this trend, more and more XRP investors are turning their attention to EX DeFi, exploring more stable and sustainable yield models through cloud mining and yield aggregation mechanisms.

Compared to more volatile futures trading or ETF investment, EX DeFi offers a more intuitive and convenient way to participate in digital assets, helping users improve the efficiency of digital asset utilization while participating in the development of the XRP ecosystem. For users with a certain amount of capital, this model is expected to offer higher daily return potential.

About EX DeFi

EX DeFi is headquartered in the UK and operates within European regulatory frameworks such as MiCA and MiFID II, continuously improving its transparency, operational standards, and user protection mechanisms.

The platform employs a multi-layered security architecture, including:

- PwC’s annual financial and security compliance audit;

- Lloyd’s of London digital asset custody insurance;

- Cloudflare enterprise-grade network protection and McAfee® security system;

- Multi-layered encryption architecture, AI-powered intelligent risk control, and 2FA verification protection.

Currently, EX DeFi supports multiple mainstream digital assets such as XRP, BTC, ETH, USDT, USDC, DOGE, LTC, and SOL, providing users with a more flexible and convenient digital asset service experience.

Start earning daily yields easily in just three steps:

1. Register an account

Visit the EX DeFi official website and register using an email address to receive a $17 trial bonus.

2. Choose a Mining Package

Based on a person’s budget and needs, choose a cloud mining contract that suits their needs and start mining with one click.

3. Start Earning Profits

After the contract is activated, the system will automatically allocate computing power, and profits will be automatically settled 24 hours a day. Users can withdraw profits at any time or continue participating as needed, achieving long-term asset compounding.

Example DeFi Popular Contracts

BTC (Beginner Trial Contract): Investment of $100, Term: 2 days, Daily Yield: $4, Total Profit: $100 + $8

DOGE (Golden Shell Mini Dogecoin Pro): Investment of $500, Term: 6 days, Daily Yield: $6.5, Total Profit: $500 + $39

BTC (Canaan-Avalon-A1466): Investment of $1000, Term: 10 days, Daily Yield: $13.4, Total Profit: $1000 + $134

LTC (Bitmain Antminer L7): Investment of $5,000, Term: 20 days, Daily Yield: $73.5, Total Profit: $5,000 + $1,470

BTC (Bitmain S19K-Pro): Investment of $10,000, Term: 30 days, Daily Yield: $161, Total Profit: $10,000 USD + $4,830

For more details on the program, please visit the EX DeFi official website.

Summary

The continued inflow of funds into the XRP ETF, coupled with the improving regulatory environment, further reflects XRP’s gradual integration into the mainstream financial system. EX DeFi provides XRP investors with more diversified participation methods, shifting from “simply relying on price fluctuations” to “price growth and yield generation in parallel.”

As a new market cycle develops, investors are no longer just focused on price increases and decreases, but are paying more attention to stable and sustainable asset management strategies. This trend also reflects the maturing development of digital asset investment.

Still hesitating? Join EX DeFi now and earn daily passive income from digital assets.

Disclosure: This content is provided by a third party. Neither crypto.news nor the author of this article endorses any product mentioned on this page. Users should conduct their own research before taking any action related to the company.

A study from the Bank of Italy has challenged a common argument for crypto payments: that stablecoin-based remittances automatically deliver lower costs and faster settlement than traditional money transfer rails. After testing remittances funded and settled with USDC across multiple corridors, the researchers found that most of the expense and delay came from fiat conversion and payment-rail frictions—factors that blockchain networks alone do not control.

The findings are based on experiments moving 200 USDC across 10 bidirectional corridors connecting Italy with Brazil, Argentina, Japan, the United Arab Emirates, and South Africa. The study compared the end-to-end cost and settlement time to traditional remittance services, concluding that crypto network fees made up only a small portion of overall costs.

Key takeaways

- Fiat on- and off-ramp frictions dominated remittance costs: exchange fees and currency conversion accounted for most expenses, while blockchain transaction fees were comparatively minor.

- Speed depended on local payment rails: transfers settled in under 20 minutes where instant payment systems were available, but took one to two business days when they weren’t.

- Cost advantages were corridor-specific: total costs across stablecoin remittances ranged from 0.3% to nearly 9%, with savings versus some benchmarks not universal.

- Regulatory design influenced user behavior and efficiency: overly restrictive rules increased operational complexity, while prohibitionist approaches pushed users toward offshore and unregulated options.

Stablecoins don’t eliminate the biggest frictions

The Bank of Italy’s experiment was designed to isolate where the money-transfer pipeline spends time and money. Researchers reported that, across the stablecoin remittances tested, exchange fees and currency conversion were the primary cost drivers. By contrast, blockchain transaction fees were only a small share of total costs—meaning the core bottlenecks for cross-border transfers largely sit outside the chain.

In practical terms, the corridor matters because stablecoin remittances often still require converting value into local currency at the sending and receiving ends. Even when the transfer occurs on-chain, users may face fees and processing delays at the interfaces where fiat enters or leaves the system.

Costs and settlement times vary by corridor

According to the study, total costs for the stablecoin remittances ranged from 0.3% to nearly 9%, depending on the corridor. This wide spread underscores that stablecoin-based transfers are not a single “set it and forget it” alternative to traditional remittances; rather, they are shaped by the quality and pricing of the surrounding payment infrastructure.

Settlement times showed an even clearer relationship with local payment systems. The researchers found transfers were typically completed in less than 20 minutes when instant payment networks were available. Where those systems were not in place, settlement stretched to one to two business days.

To frame the results against a broader global benchmark, the study used the World Bank’s reported global average remittance cost of 6.65%. On that basis, stablecoin transfers were cheaper in most corridors examined. However, they were less expensive than Wise in only three of seven corridors where direct comparisons were possible—suggesting that established digital remittance providers can still outperform stablecoin routes in certain environments.

Why infrastructure investment matters more than token choice

The Bank of Italy argues that improving the competitiveness of stablecoin-based cross-border payments depends heavily on payment-rail upgrades—particularly domestic instant payment infrastructure. In other words, the study’s central implication is that stablecoin settlement can be fast only if the start and end points of the transfer process are equally efficient.

The authors also emphasized an important structural point: the potential benefits expand if stablecoins can be used in the real economy without repeated reconversion into local fiat. They wrote that:

If stablecoins could be spent directly in the real economy, for goods and services, rents, or school fees, without reconversion into local fiat currency, the economic advantages of stablecoin-based transfers would be substantially higher.

This framing highlights a key asymmetry in many cross-border use cases today. Even if blockchain rails reduce settlement friction, remittance economics can remain constrained when end users ultimately need local currency access and the process requires multiple conversions.

Regulation can either enable or complicate real-world use

The study also found that regulatory design plays a decisive role in shaping remittance efficiency. According to the authors, prohibitionist regimes have not fully eliminated stablecoin demand; instead, they can push users toward offshore platforms and other unregulated channels. Conversely, overly restrictive frameworks may increase operational complexity for retail users.

The analysis arrives as policy frameworks for crypto assets and stablecoins are taking shape in major jurisdictions. The European Union has implemented the Markets in Crypto-Assets (MiCA) framework, while the United States has enacted the GENIUS Act, which governs crypto assets and payment stablecoins, respectively.

In terms of broader market momentum, the stablecoin market has grown to about $307 billion, up roughly 16% over the past year, according to DefiLlama data on stablecoins.

That growth provides context for why regulators and payment operators are increasingly focused on remittance and tokenized payments. But the Bank of Italy’s results suggest that the route to efficiency is not purely about allowing stablecoin settlement—it’s also about aligning regulatory expectations with workable payment flows and infrastructure.

What readers should watch next

The study implies that the next meaningful improvements in stablecoin remittances will likely come from upgrades to instant payment rails and from reducing the need for repeated fiat conversion at either end of the transfer. Investors and builders should monitor how policy changes under MiCA in Europe and the GENIUS framework in the US translate into compliant on- and off-ramp experiences—because, according to the Bank of Italy, that’s where most of the cost and delay still lives.

Robinhood stock recovered more than 2% on Thursday after Bernstein maintained its $160 target, betting that tokenization and prediction markets can offset weaker crypto trading.

Summary

- Bernstein maintained an Outperform rating and $160 target, implying roughly 81% upside from Thursday’s close.

- Robinhood’s second-quarter net revenue rose 32% year over year to $1.31 billion.

- Event contracts generated $156 million, surpassing the company’s $100 million in crypto trading revenue.

- HOOD traded at $88.55, but remained below its 20-, 50- and 100-day moving averages.

Robinhood stock rebounds from $83.68

Robinhood Markets shares traded at $88.55 on Friday, up approximately 2.25% after moving between $83.68 and $89.48 during the session. Despite the rebound, HOOD remained about 26% below its July high near $120.

HOOD had closed Wednesday at $89.84 before coming under renewed selling pressure. Thursday’s recovery kept the stock above its 200-day simple moving average at approximately $86.52, a level that could determine whether the recent decline develops into a deeper correction.

Bernstein maintained its Outperform rating and $160 price target following Robinhood’s second-quarter results. From Thursday’s closing price, the target represents potential upside of about 81%.

Goldman Sachs also retained a Buy rating but reduced its 12-month target from $137 to $118. The revised target still implies more than 33% upside, though it reflects a more cautious outlook for near-term growth.

Robinhood reported second-quarter net revenue of $1.31 billion, up 32% from $989 million a year earlier. The result exceeded analysts’ consensus estimate of approximately $1.26 billion.

Prediction markets overtake crypto revenue

Bernstein’s bullish case rests partly on Robinhood’s expansion beyond conventional stock and cryptocurrency trading. The brokerage identified prediction markets, tokenized stocks and blockchain infrastructure as longer-term revenue drivers.

Robinhood’s Rothera exchange went live in June and has processed more than 3.5 billion contracts. Around 2.1 billion contracts changed hands during the second quarter, generating $17 million in revenue.

Total event-contract revenue reached $156 million during the quarter, exceeding the $100 million generated by crypto trading. Bernstein described Rothera as the third-largest U.S. exchange in its category.

The figures show that prediction markets are becoming a larger part of Robinhood’s business as weaker digital-asset activity weighs on transaction revenue. Bernstein cut its estimate for Robinhood’s 2026 crypto trading revenue by 49% to reflect lower market volumes.

Commenting on how Rothera could develop, Bernstein analysts said:

“Management expects a greater share of prediction market flow to migrate to Rothera over time, while continuing to distribute event contracts from third-party exchanges and retaining the longer-term optionality to offer Rothera as a B2B platform for other FCMs.”

That strategy would allow Robinhood to earn revenue from its own exchange while continuing to distribute contracts supplied by outside venues. A future business-to-business offering could also provide access to other futures commission merchants, though that remains a longer-term option rather than a confirmed source of revenue.

Tokenization becomes a second growth pillar

Bernstein also pointed to Robinhood Chain, Bitstamp, Robinhood Earn and tokenized stocks as evidence that the company is developing infrastructure beyond its retail brokerage.

Robinhood Chain has recorded more than $12 billion in decentralized exchange volume and processed over 150 million transactions since its launch. Robinhood Earn has attracted more than $200 million in deposits.

Stock Tokens are available through Robinhood Wallet in more than 120 countries, extending the company’s tokenization business outside the United States. The service gives eligible international users blockchain-based exposure to listed securities, while U.S. investors continue to access conventional shares through Robinhood’s regulated brokerage platform.

Robinhood has also opened its Agentic Trading platform to its full customer base. The system lets customers connect artificial intelligence agents through Robinhood’s Model Context Protocol server and assign specific investing tasks.

These products widen Robinhood’s addressable market, but they also introduce execution and regulatory risks. Tokenized securities can face different ownership, disclosure, and investor-protection rules across jurisdictions, while prediction markets remain under scrutiny from U.S. federal and state authorities.

HOOD must reclaim $96 to strengthen recovery

Robinhood’s daily chart remains technically weak despite Thursday’s rebound. HOOD is trading below its 20-day moving average at $103.79, its 50-day average at $96.67, and its 100-day average at $99.30.

The cluster between $96.67 and $103.79 creates a broad resistance area. A close above the 50-day average would be the first sign that buyers are regaining control, while a move above $103.79 could reopen a path toward the July range between $110 and $120.

Bear-bull power stood at minus 20.01, showing that sellers still hold the near-term advantage. Negative bars have also expanded during the latest retreat, suggesting that Thursday’s bounce has not yet reversed the broader loss of momentum.

On the downside, the 200-day moving average near $86.52 provides immediate support. HOOD briefly traded below that level before recovering, making the $83.68 intraday low the next level to watch if selling resumes.

A sustained break below $83.68 could expose the June consolidation area around $75 to $80. Conversely, holding above the 200-day average and reclaiming $96.67 would improve the technical outlook.

Bernstein’s $160 target depends on Robinhood converting newer products into durable revenue as crypto trading slows. For U.S. investors, the next test will be whether prediction markets and tokenization can continue expanding without tighter regulation limiting their contribution.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Ken Griffin’s Citadel reportedly bought a large proportion of the public stock portfolio of Situational Awareness, the hedge fund founded by former OpenAI researcher Leopold Aschenbrenner.

The Financial Times first reported Thursday that Citadel bought the portfolio holdings after heavy losses during July’s artificial intelligence stock market rout.

The transaction followed Aschenbrenner’s fund falling about 67% in July, according to The Wall Street Journal, citing a person who saw a letter sent to investors. The letter said the fund remained up about 80% for the year. The Financial Times previously reported the fund was up 439% through June.

Those reports suggested Situational had approached existing investors and lenders for fresh capital and offered some investors the option to buy portfolio assets. The Journal also reported Situational needed cash to meet margin calls from its lenders and that the fund agreed late Wednesday to sell $3.5 billion of Anthropic shares to a group led by Greenoaks and Sequoia Capital before withdrawing from the deal Thursday morning.

Reuters separately reported the leveraged portfolio detail but said it could not determine whether formal margin calls had been issued before the sale. Reuters said Situational retained roughly $10 billion in stocks and private investments, including Anthropic. Situational had grown to about $24 billion in assets in under two years before the reversal, according to the FT’s follow-up profile.

AI holdings suffered steep July falls

Several stocks linked to the fund suffered sharp declines in July. Sandisk remained down about 44% for the month even after closing Thursday up 26%. CoreWeave fell nearly 26% in July, while Bloom Energy was down around 32%, Yahoo Finance data shows.

Related: Former OpenAI researcher foresees AGI reality in 2027

Situational’s US Securities and Exchange Commission filing showed direct share positions in all three companies as of March 31.

The same filing showed about $1.11 billion in shares of seven Bitcoin (BTC) mining companies, including Iren, Core Scientific, Riot Platforms and CleanSpark. Cointelegraph previously reported that the positions gave Situational exposure to miners expanding into AI and high-performance computing by repurposing their power supplies and data center sites.

It remains unclear what stocks were part of the transaction between Citadel and Situational or whether the fund retained any of its Bitcoin miner positions.

Related: Bitcoin miner Core Scientific shifts to AI with 1.5GW data center push

Aschenbrenner’s fund takes its name from his 2024 essay series, “Situational Awareness: The Decade Ahead,” which argued that artificial general intelligence could arrive by 2027 and drive enormous demand for computing power and electricity.

Before joining OpenAI, Aschenbrenner was a member of the FTX Future Fund’s five-person team and signed its November 2022 resignation notice as FTX collapsed.

Cointelegraph contacted Situational Awareness and Citadel for comment but had not received a response by publication.

Magazine: The 100x obsession: Fundamentals grow in importance as crypto matures

Japan’s central bank held interest rates steady at 1.0% on Friday after a reported major intervention in the yen.

Key points:

- Japan holds interest rates at 1.0%, following market expectations.

- Both Japan and South Korea’s central banks reportedly engage in currency interventions, as the JPY briefly gains 3.5% overnight.

- Bank of Japan warns of incoming CPI inflation headwinds in the second half of the year.

Yen rises up to 3.5% as Korea joins intervention

In its latest statement, the Bank of Japan (BoJ) revealed broad consensus among officials for holding rates at current levels — an outcome that markets had anticipated in advance.

“The Bank will encourage the uncollateralized overnight call rate to remain at around 1.0 percent,” it confirmed.

Eight out of nine members of the bank’s Policy Board voted for the outcome, with only Hajime Takata proposing a 0.25% rate hike.

Japan benchmark interest rate (screenshot). Source: BoJ

Japan’s benchmark rate remains at its highest levels since 1995, with the BoJ meeting result coming just hours after the yen saw snap volatility. Against the US dollar, the currency rose by as much as 3.5% on Thursday, per data from TradingView, in a move that has widely been attributed to central bank intervention

JPY/USD one-day chart. Source: Cointelegraph/TradingView

The BoJ did not officially comment on the latest moves, which coincided with a significant rebound in the South Korean stock market after days of heavy selling concentrated on semiconductor stocks. The Korean won was up by around 1% at the time of writing amid reports of a joint intervention between the BoJ and Korea’s central bank. Analysts referenced “tightly aligned” mutual interests of the two countries as facilitating the joint move.

“The interests of each country aligned. For Korea-Japan cooperation, the won and the yen are so tightly coupled that a joint intervention could double the impact,” Lee Min-hyuk, an analyst at KB Kookmin Bank, commented to local media outlet Straits Times.

The Nikkei newspaper earlier noted that the US had engaged in rate checks — a form of soft intervention which can precede a more pronounced operation — during Thursday’s trading session, resulting in speculation over a three-way coordinated move.

“The key signal from last night’s move is that MOF remains uncomfortable with excessive yen weakness. The line in the sand is probably better viewed as a zone around 162-165 rather than a specific level,” Masahiko Loo, senior fixed income strategist at asset manager State Street Investment Management, told CNBC.

BoJ sees CPI inflation headwinds increasing in 2026

As the yen came off its highest levels against the dollar since 1986, the BoJ warned of future upside in the Consumer Price Index (CPI) inflation.

Related: Rate path still divides investors: Five things to know in Bitcoin this week

“The year-on-year rate of increase in the consumer price index […] is likely to accelerate to a level clearly above 2 percent from the second half of fiscal 2026,” it stated in its latest quarterly Outlook for Economic Activity and Prices report.

In addition to rising prices of durable goods, the report referenced “waning of the effects of high crude oil prices” due to the ongoing US-Iran war and closure of the Strait of Hormuz oil-transit route.

Gyrations in the yen have remained an important consideration in crypto trading circles ever since the “unwinding” of the yen carry trade sparked major Bitcoin and altcoin downside pressure in August 2024.

Earlier this year, Arthur Hayes, former CEO of crypto exchange BitMEX, suggested that the combination of a weak yen and rising Japanese bond yields may cause investors to move away from low-yielding US bond allocations. He linked central bank liquidity interventions to positive moves in crypto markets.

“This discussion of Japanese financial markets is important because for Bitcoin to exit its sideways funk, it needs a healthy dose of money printing,” he wrote in a blog post.

In December 2025, Hayes predicted that USD/JPY could rise as high as 200.

The New York trust charter allows Circle’s subsidiary to provide fiduciary and custody services under state banking law.

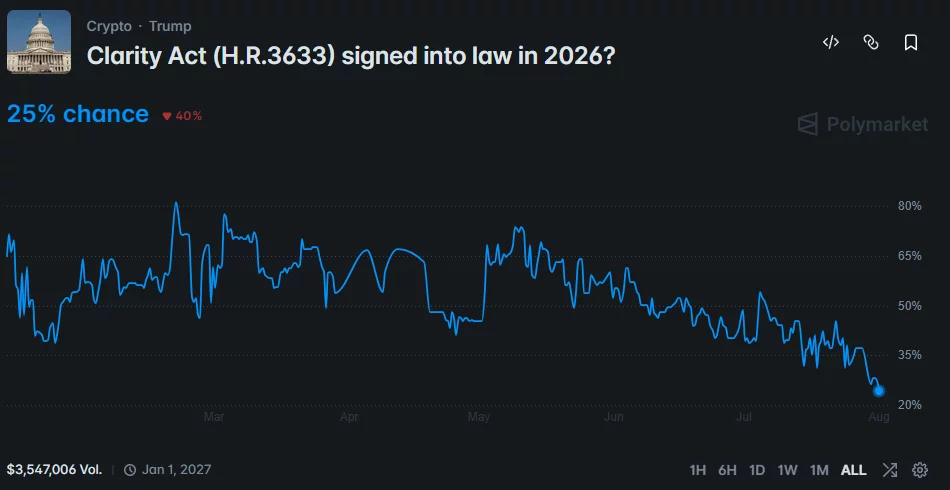

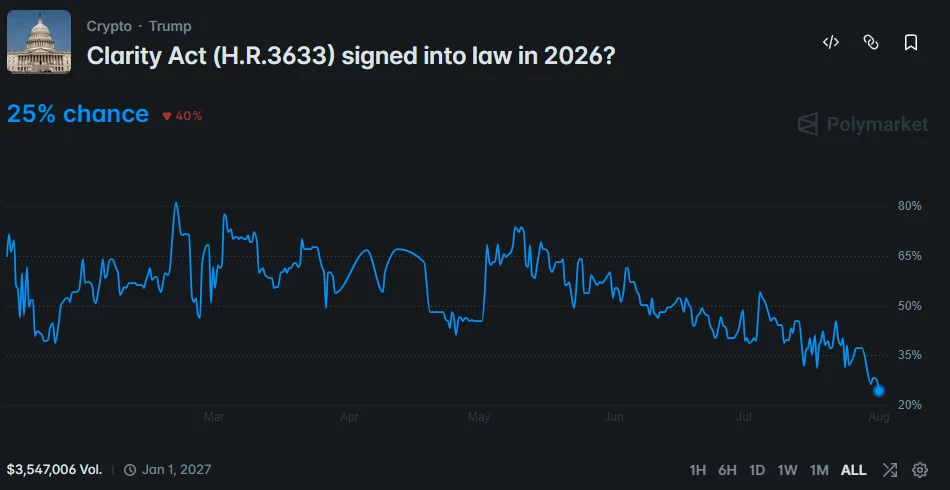

CLARITY Act passage odds have fallen to 25% as the White House reviews a bipartisan ethics proposal that could determine whether the Senate takes up the crypto market structure bill before its August recess.

Summary

- Polymarket traders give the CLARITY Act a 25% chance of becoming law in 2026.

- Anthony Scaramucci expects President Donald Trump to approve the bipartisan ethics proposal.

- Sens. Thom Tillis and Ruben Gallego reportedly submitted the compromise language to the White House.

- Senate leaders have not confirmed the timing of any floor action.

Scaramucci expects Trump to approve ethics deal

SkyBridge Capital founder Anthony Scaramucci said he expects Trump to accept the revised ethics language negotiated by Republican Sen. Thom Tillis and Democratic Sen. Ruben Gallego.

“If POTUS ultimately signs off, which I think he will, who will stand in the way of Clarity?” Scaramucci wrote on X. “If Dems (or GOPs in the pocket of bank lobby) stand in the way, they will regret it in November.”

Scaramucci’s statement represents his assessment of the negotiations. Neither Trump nor the White House has publicly confirmed acceptance of the proposal.

Tillis and Gallego reportedly sent the counterproposal to the White House on Thursday. The text has not been released publicly, but crypto journalist Eleanor Terrett reported that it would give state attorneys general a role in enforcing restrictions on federal officials’ digital-asset activities. Terrett’s report said the full scope of those state powers remained unclear.

Scaramucci also claimed in a now-deleted post that Trump’s children supported the compromise. That assertion has not been independently confirmed.

Ethics dispute remains central to CLARITY Act talks

Senate Democrats objected to an earlier Republican-backed ethics proposal because it reportedly placed enforcement authority solely with federal prosecutors.

The disputed language would restrict the president, vice president and other federal officials from issuing or sponsoring digital assets while in office. Democrats have sought stronger enforcement mechanisms and broader protections addressing conflicts of interest linked to officials’ crypto businesses.

Giving state attorneys general enforcement authority could help attract Democratic votes. It could also address concerns raised by Tillis, who had withheld support without changes to the ethics section.

However, an agreement on ethics would not guarantee passage. Senators remain divided over other provisions involving stablecoin rewards, protections for blockchain developers, and the division of regulatory authority between the Securities and Exchange Commission and Commodity Futures Trading Commission.

The House passed its version of the CLARITY Act by a 294–134 vote in July 2025, with 78 Democrats supporting it. Any amended Senate version would still need approval from both chambers before reaching Trump’s desk.

CLARITY Act odds fall to record-low 25%

Polymarket traders now assign a 25% probability that Trump will sign the CLARITY Act into law before the end of 2026, down from 30% earlier this week. The decline reflects uncertainty over both the remaining negotiations and the limited Senate calendar.

Prediction-market probabilities represent traders’ positions rather than a formal legislative forecast. The odds can change quickly if the White House accepts the ethics compromise or Senate Majority Leader John Thune schedules floor proceedings.

Industry groups are also pressing lawmakers to act. Digital Currency Group, the parent company of Grayscale, sent a letter to Thune and Senate Minority Leader Chuck Schumer requesting a vote before the recess. The company argued that continued regulatory uncertainty was driving US crypto investment and jobs overseas.

Treasury Secretary Scott Bessent issued a similar call this week, saying the Senate needed to vote on the legislation “now.”

Senate timetable remains uncertain

Sen. Cynthia Lummis said Thune has reserved space for the CLARITY Act on the Senate agenda and still intends to begin considering it before lawmakers leave Washington.

“Senator Thune has kept a place for the Clarity Act on the agenda before the August recess for many, many weeks now,” Lummis said. “I believe he does intend to go through with it.”

Still, no floor schedule has been confirmed. Nominations, government funding negotiations and votes concerning Iran and Russia-Ukraine sanctions are competing for the Senate’s remaining time. Lummis’ comments indicate that proceedings could begin within days, but they do not guarantee a final passage vote before the recess. Crypto.news previously reported that amendments and procedural votes could push final action into the post-recess calendar.

For US crypto companies and investors, the outcome will determine whether Congress advances a federal division of SEC and CFTC oversight this summer or leaves the regulatory framework unresolved heading into the November elections.

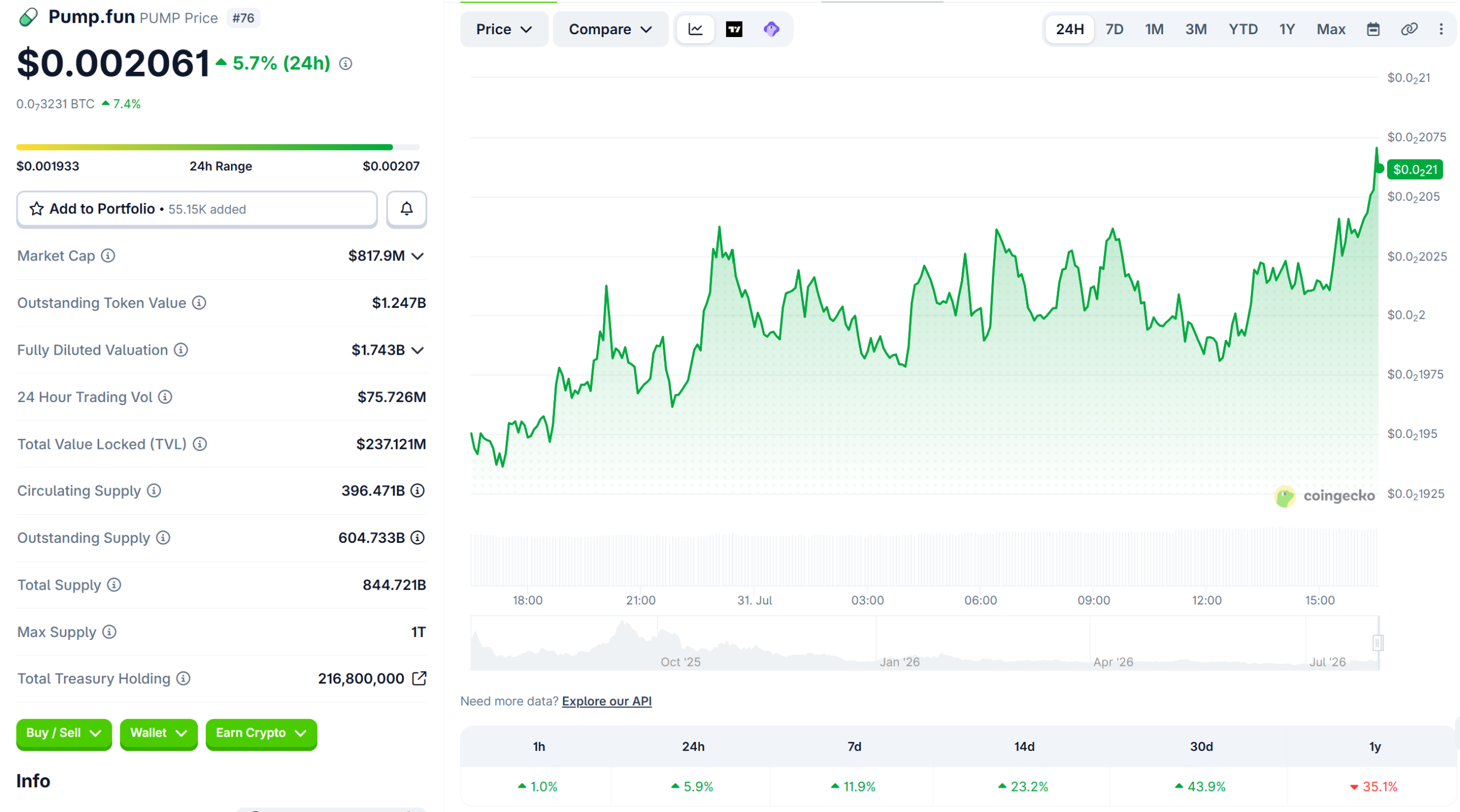

Former Pump.fun employees say they were dismissed two months before their PUMP tokens vested. Weeks after those dates passed, the team unlocked 50 billion tokens of its own.

An anonymous X (Twitter) account claiming to speak for more than 40 ex-staff began publishing termination emails this week. Pump.fun has not addressed the allegations publicly.

April Brought Layoffs and a $370 Million Burn

Sandmark reported that the Solana launchpad terminated contracts in early April. A quarter of each staff allocation was due to vest roughly two months later. Grant agreements had been signed in mid-June 2025, according to documents the outlet reviewed.

Co-founder Noah Tweedale attributed the cuts to a business that “grew too quickly” and could no longer move “fast and rough.” Severance ran to one week of salary for every month worked. One departing employee reportedly lost PUMP worth seven figures at current prices.

That same month, however, the platform destroyed $370 million of repurchased PUMP, wiping out roughly 36% of circulating supply. Co-founder Alon Cohen defended the April token burn at the time.

“Every dollar not burned is a dollar being put to work toward the same outcome”

Follow us on X to get the latest news as it happens

What the July 12 Cliff Released

The insider cliff expired on July 12, one year to the day after PUMP sold at $0.004 in its initial coin offering. Tokenomist data put the 82.5 billion token release at 50 billion for the team and 32.5 billion for existing investors.

At Friday’s price, the team slice alone is worth about $102 million. Measured against operations, that figure is striking.

Pump.fun booked $19.1 million of revenue in the 30 days to July 22, according to DefiLlama. That measure counts the platform’s cut of trade fees plus graduation and Mayhem fees. The team tranche therefore exceeds five months of it.

Revenue was also climbing rather than shrinking. DefiLlama logged $764,802 on July 22, a 22.6% rise month over month, against $1.07 billion earned since March 2024.

The Grievance Runs Through the Launchpad

Markets have not flinched. PUMP traded near $0.0020 on Friday, up almost 6% in a day. It still sits 77% under its September 2025 peak and 49% below the ICO price.

Verification remains thin. Sandmark could not confirm the second layoff wave, and the one public record that would settle headcount is late.

Baton Corporation Ltd is the UK entity behind Pump.fun. Its accounts for the period to 30 September 2025 were due at Companies House by 30 June. Those accounts disclose employee numbers, and they remain unfiled. The last set covers the year to March 2024.

Tweedale and Cohen are also personally named in a securities class action. Plaintiffs filed it in the Southern District of New York in January 2025.

Pump.fun did not immediately respond to BeInCrypto’s request for comment.

A billion dollars of tracked revenue sits behind this company, and one overdue filing sits in front of it. Until that document lands, April stays a matter of claim against claim.

The post Pump.fun Layoffs Spark Fury After Workers Miss Million-Dollar Token Payouts appeared first on BeInCrypto.

The largest tokenized securities platform cleared its SEC probe, secured FINRA authorization, and put BlackRock’s IVV onchain. Now it is shopping for a target worth up to half a billion dollars while the market it helped build outgrows it.

Summary

- Ondo Finance is exploring an acquisition valued between $250 million and $500 million to expand into wealthtech and adjacent financial sectors, though no formal advisers have been appointed and no target has been identified.

- The company’s SEC-registered broker-dealer subsidiary received additional FINRA authorizations in July 2026, covering tokenized corporate equities, ETFs, and other investment products.

- Ondo debuted the SEC’s third-party custodial tokenization model with BlackRock’s IVV ETF and Micron shares as the first securities tokenized under a domestic U.S. framework.

- The total real world asset market onchain has crossed $36 billion in 2026, with tokenized U.S. Treasuries alone reaching approximately $12.88 billion, up from roughly $5 billion in late 2024.

- Ondo abandoned its planned Layer 1 blockchain in favor of Ondo Network, a high speed execution layer pairing centralized exchange level speeds with non-custodial, onchain-verifiable settlement.

Ondo Finance spent the first half of 2026 clearing every regulatory hurdle that has historically killed tokenization platforms. It closed an SEC investigation without charges. It secured FINRA authorization for tokenized equities. It put BlackRock’s flagship ETF onchain under a framework the SEC itself endorsed. And now, with $2.5 billion in assets under management and a market that has tripled in eighteen months, it is looking to spend up to half a billion dollars on an acquisition that would transform it from a tokenization protocol into something closer to a financial conglomerate.

The acquisition report, first published by CoinDesk on July 30, described Ondo as exploring targets in wealthtech and adjacent sectors valued between $250 million and $500 million. The company’s response was carefully calibrated: “We are not in conversations with any party at this time.” The denial did not say the exploration was not happening. It said no specific target had been engaged. The ONDO token rose approximately 6% on the news, a move that valued the company’s circulating supply at roughly $1.5 billion.

The timing is not coincidental. Ondo has spent two years building infrastructure that most tokenization platforms never get close to completing. It has an SEC-registered broker-dealer. It has FINRA authorization. It has a custodial model that the SEC endorsed through formal guidance. What it does not have is the distribution network, advisory relationships, and client assets that a wealthtech acquisition would provide. The $250 million to $500 million price range suggests Ondo is looking at established platforms with existing customer bases, not early stage startups.

The regulatory clearance that changed everything

The most important development in Ondo’s 2026 was not a product launch. It was the closing of an SEC investigation that had been running since October 2023.

The probe, opened during Gary Gensler’s chairmanship, examined whether Ondo’s tokenized securities products constituted unregistered securities offerings. Under Chair Paul Atkins, the investigation was closed without enforcement action. The closure removed the single largest existential risk facing the company and cleared the path for everything that followed.

Within weeks of the probe closing, Ondo’s SEC-registered broker-dealer subsidiary, Oasis Pro Markets, received additional FINRA authorizations covering tokenized corporate equities, ETFs, and other investment products. The authorization expanded Oasis Pro’s permissions beyond its original scope, which had been limited to digital asset securities under Regulation D and Regulation S exemptions.

The FINRA authorization is significant because it addresses the distribution problem that has constrained every tokenization platform to date. Tokenizing a security is technically straightforward. Distributing that tokenized security to investors through regulated channels requires broker-dealer infrastructure that most crypto companies do not possess. Ondo now has that infrastructure at a level that only Securitize among its direct competitors can match.

The regulatory sequence matters. The SEC probe closure came first, establishing that Ondo’s existing products did not violate federal securities law. The FINRA authorization came second, expanding what Ondo could offer through regulated channels. The BlackRock IVV tokenization came third, providing the marquee product that validated the regulatory framework. Each step depended on the one before it. A company still under SEC investigation could not have received expanded FINRA authorization. A company without expanded authorization could not have tokenized a major ETF under the SEC’s endorsed model. The entire 2026 regulatory sequence was sequential by necessity, and Ondo executed it faster than any competitor.

Ondo also filed a confidential registration statement with the SEC for Ondo Global Markets, providing issuer-level disclosures for all investors. The confidential filing is a precursor to full public registration, a step that would make Ondo Global Markets subject to the same reporting requirements as traditional securities exchanges. No other tokenization platform has progressed this far toward full SEC registration for a tokenized securities marketplace.

On July 1, 2026, Ondo debuted what may be the most consequential product in the tokenization industry’s short history. It put BlackRock’s IVV ETF and Micron shares onchain under the SEC’s third-party custodial tokenization model. This was not an offshore workaround. It was not a synthetic exposure product. It was the actual security, tokenized under a framework the SEC had formally described in its January 2026 guidance. BlackRock’s IVV became the first major ETF to exist simultaneously in traditional brokerage accounts and on a blockchain, with identical investor protections and ownership rights in both formats.

The $36 billion market Ondo helped build

The market context for Ondo’s acquisition ambitions is a sector that has grown faster than almost anyone projected. Total real world assets onchain crossed $36 billion in 2026. Tokenized U.S. Treasuries alone reached approximately $12.88 billion, up from roughly $5 billion in late 2024. BCG projects the broader RWA market reaching $16 trillion by 2030, a figure that would make it one of the largest asset classes in financial services.

Ondo’s position within this market is both dominant and precarious. Its OUSG and USDY products, which provide onchain exposure to short-term U.S. government debt, have accumulated more than $2.5 billion in assets. That makes Ondo one of the largest tokenization providers by assets under management. But the market is attracting competitors with resources that dwarf Ondo’s.

The DTCC’s tokenization initiative launched in July 2026 with more than 50 participating firms, including BlackRock, JPMorgan, and Goldman Sachs. The initiative covers Russell 1000 equities, major index ETFs, and U.S. Treasuries. When the world’s largest securities depository begins tokenizing assets, the competitive landscape for standalone tokenization platforms changes fundamentally.

Ondo joined the DTCC consortium rather than competing against it, a strategic decision that acknowledges the reality of institutional finance. The company sits alongside the firms whose assets it tokenizes, a position that provides access to deal flow and legitimacy but also raises questions about differentiation. If BlackRock can tokenize its own ETFs through the DTCC framework, why does it need Ondo to do it?

The answer, for now, is speed and specialization. The DTCC’s tokenization service is designed for traditional market hours and settlement cycles. Ondo offers 24/7 trading access and near-instant settlement. The DTCC covers DTC-custodied assets. Ondo covers assets that exist outside traditional custody networks, including international equities and structured products. The two approaches are complementary today. Whether they remain complementary as the DTCC expands its scope is the central competitive question facing every tokenization platform.

Ondo Network and the infrastructure pivot

In one of the most underreported strategic shifts in crypto during 2026, Ondo abandoned its planned Layer 1 blockchain entirely. Instead, it launched Ondo Network, a high speed execution layer that pairs centralized exchange level performance with non-custodial, onchain-verifiable settlement.

The decision to drop the L1 plan reflects a maturation in how tokenization platforms think about infrastructure. Building a standalone blockchain creates a cold start problem. Liquidity, developers, and users must be attracted to a new chain from scratch. The costs are enormous and the failure rate is high. Ondo’s leadership concluded that the company’s competitive advantage lies in regulatory infrastructure and institutional relationships, not in consensus mechanisms and validator economics.

Ondo Network’s first application is Ondo Perps, a perpetual futures platform that uses tokenized assets as collateral. The product targets a specific gap in the derivatives market: the ability to post tokenized equities and Treasuries as margin for derivatives positions. If a trader holds $1 million in tokenized IVV, Ondo Perps would allow that position to serve as collateral for futures trades without liquidating the underlying holding.

The collateral use case is potentially transformative for tokenized assets. One of the persistent criticisms of tokenization has been that holding a tokenized security offers no practical advantage over holding it through a traditional broker. If tokenized assets can serve as collateral across DeFi and CeFi platforms simultaneously, the tokenized version becomes strictly superior to the traditional version. The asset earns yield in one protocol while securing positions in another, a form of capital efficiency that traditional finance cannot replicate.

The infrastructure pivot also positions Ondo to capture a revenue stream that does not depend on asset management fees. Ondo Network can charge execution fees on every trade processed through its matching engine, transaction fees on settlement, and licensing fees to third-party platforms that integrate its execution layer. This is the infrastructure-as-a-service model that traditional exchanges like Nasdaq and ICE have used to build durable revenue streams independent of trading volume cycles. If Ondo Network achieves meaningful adoption, it would diversify the company’s revenue beyond the management fees that currently drive its economics.

The partnership architecture

Ondo’s institutional partnership roster reads like a directory of the firms that control traditional financial infrastructure. Mastercard integrated Ondo into its Multi-Token Network for RWA settlement. Fidelity incorporated OUSG into tokenized fund strategies. PayPal established a $25 million facility connecting PYUSD with Ondo yield products. SBI partnered with Ondo to bring Japanese stocks onchain with the JPYSC stablecoin.

Each partnership represents a different distribution channel. Mastercard provides access to its merchant network for settlement use cases. Fidelity provides access to institutional asset allocators. PayPal provides access to its 400 million consumer accounts. SBI provides access to the Japanese market, the third largest equity market in the world.

The partnership strategy also reveals what Ondo is not. It is not a consumer facing platform. It is not competing with Coinbase or Robinhood for retail traders. It is building the infrastructure layer that sits between traditional financial institutions and blockchain networks, processing the tokenization, custody, and settlement that allows those institutions to offer blockchain based products to their own customers.

This positioning explains the acquisition interest. A wealthtech company would provide what Ondo’s current partnership model lacks: direct relationships with financial advisors and their clients. The $250 million to $500 million price range suggests targets with meaningful assets under advisory, likely platforms serving registered investment advisors or independent broker-dealers.

The partnership strategy also highlights the founder question that has hung over Ondo since the sudden death of Nathan Allman earlier in 2026. Allman, a former Goldman Sachs vice president who founded Ondo in 2021, had been the primary relationship holder with many of the company’s institutional partners. His absence creates both a leadership vacuum and a strategic opportunity. An acquisition that brings in experienced financial services executives could address the leadership gap while simultaneously expanding distribution. The company has not publicly named a permanent replacement, and the acquisition exploration may be partly motivated by the need to rebuild the institutional relationship infrastructure that Allman personally maintained.

The token question

The ONDO token presents one of the more complex value accrual questions in crypto. The company oversees $2.5 billion in tokenized assets. It has partnerships with the largest names in finance. It has regulatory clearances that no competitor can easily replicate. Yet the token trades at approximately $0.41, well below its historical highs, with a market capitalization of roughly $1.5 billion.

The disconnect between platform growth and token price reflects a structural issue common to many institutional crypto projects. Ondo’s revenue comes from management fees on tokenized products, not from onchain activity that directly benefits token holders. The ONDO token’s primary utility is governance. The Ondo DAO recently approved a burn of 100 million tokens, approximately 1% of the 10 billion total supply. The burn is a step toward aligning token economics with platform growth, but it does not create a direct revenue sharing mechanism.

The circulating supply of approximately 4.87 billion tokens, against a total supply of 10 billion, means significant dilution remains. Token unlocks have historically pressured the price during periods when market conditions provide no offsetting demand. The token rallied 6% on the acquisition news, but that move occurred from a base of $0.39, a level that represents a fraction of the implied valuation of the operating business.

The token’s performance through July illustrates the challenge. ONDO traded in the $0.31 to $0.33 range for much of the month before the acquisition report pushed it above $0.41. The rally was driven entirely by the prospect of corporate action, not by organic growth in onchain activity or fee generation. Compare this to the tokenized assets Ondo manages, which grew steadily throughout the same period regardless of token price movements. The platform’s fundamental metrics are on an upward trajectory that the token price does not reflect.

Part of the explanation is structural. Institutional investors who custody assets through Ondo’s tokenization platform have no need to hold the ONDO governance token. The token serves the DAO; the platform serves institutions. These are two separate constituencies with different incentive structures, and the market prices the token based on governance utility, not platform economics. Until Ondo creates a mechanism that directly links platform revenue to token value, this disconnect is likely to persist.

The acquisition could change this dynamic if the acquired company’s revenue streams are structured to flow through the ONDO token or the Ondo DAO. A wealthtech platform generating advisory fees could theoretically distribute those fees to token holders through a buy-and-burn or staking mechanism. Whether Ondo’s legal structure permits such a design under U.S. securities law is an open question that the SEC’s favorable disposition toward the company may help resolve.

The competitive landscape

Ondo operates in a market where the competitive dynamics are shifting quarterly. Securitize, backed by BlackRock, has its own FINRA-approved broker-dealer and has tokenized more than $2 billion in assets. Franklin Templeton’s BENJI token provides onchain Treasury exposure. Superstate offers tokenized Treasury funds. Each competitor has a slightly different regulatory posture and institutional backing.

The DTCC’s entry into tokenization in July 2026 changed the competitive calculus for all of these players. When the entity that settles virtually every U.S. equity trade begins tokenizing those same equities, standalone tokenization platforms must either integrate with the DTCC framework or carve out niches that the DTCC does not serve.

Ondo has chosen integration. Its membership in the DTCC consortium positions it as a technology provider to the traditional settlement infrastructure rather than a replacement for it. This is a pragmatic positioning that sacrifices the revolutionary narrative in favor of institutional relevance. The question is whether the market will reward pragmatism or whether a competitor willing to challenge the DTCC directly will capture the narrative premium.

The international dimension adds complexity. Ondo’s partnership with SBI for Japanese equities and its expansion into other Asian markets puts it ahead of most competitors in cross-border tokenization. The global opportunity is significantly larger than the U.S. domestic market alone. If tokenized securities can settle across borders in seconds rather than days, the efficiency gains for international investors are substantial enough to drive adoption regardless of what happens in the U.S. regulatory environment.

Ondo Global Markets, which launched with more than 100 tokenized U.S. stocks and ETFs offering 24/5 trading access, represents the company’s most aggressive competitive move. The platform provides non-U.S. investors with access to American equities outside of traditional market hours, a service that directly competes with the growing number of 24-hour trading venues that traditional exchanges are developing in response to crypto’s always-on culture.

The MyEtherWallet integration announced on July 28 extended this reach further. By listing Ondo’s tokenized stocks through one of the oldest and most widely used non-custodial wallets in the Ethereum ecosystem, Ondo made its tokenized equities accessible to millions of self-custody users who would never open a brokerage account. The integration is a distribution play that bypasses traditional financial intermediaries entirely, putting tokenized Apple and Tesla shares in the same interface where users already hold ETH and stablecoins.

The competitive map is further complicated by the entrance of traditional exchanges into tokenization. Nasdaq received SEC approval for its tokenized securities trading proposal in early 2026. The London Stock Exchange has announced plans for overnight trading sessions designed to compete with crypto’s 24-hour markets. These are not theoretical competitive threats. They are funded, regulated competitors with existing market infrastructure and client relationships that no crypto-native platform can match.

What to watch

- The acquisition target and structure. Whether Ondo pursues a wealthtech platform, a broker-dealer, or an advisory network will signal its strategic direction for the next several years. The $250 million to $500 million range suggests a meaningful operating business, not an acqui-hire.

- DTCC tokenization expansion timeline. The DTCC’s initial production trades began in July 2026, with a full launch planned for October. How quickly the DTCC expands asset coverage will determine how much room standalone tokenization platforms have to differentiate.

- Token unlock schedule and DAO governance. With approximately 5.13 billion tokens still locked, the pace and structure of future unlocks will significantly impact ONDO’s price trajectory. Watch for DAO proposals that create direct links between platform revenue and token value.

- International expansion pace. The SBI partnership for Japanese equities is a template. If Ondo replicates this model across additional Asian and European markets before competitors secure footholds, the first mover advantage in cross-border tokenization could prove durable.

- SEC regulatory posture. Ondo’s success depends on continued regulatory favorability. Any shift in SEC leadership or policy toward tokenized securities could affect the company’s operating model and competitive position.

Frequently asked questions

What acquisition is Ondo Finance considering?

CoinDesk reported on July 30 that Ondo Finance is exploring an acquisition valued between $250 million and $500 million, targeting wealthtech and adjacent financial sectors. No formal advisers have been appointed and no specific target has been identified. Ondo stated it is not currently in conversations with any party.

What FINRA authorization did Ondo receive?

Oasis Pro Markets, Ondo’s SEC-registered broker-dealer subsidiary, received additional FINRA authorizations on July 23, 2026, covering tokenized corporate equities, ETFs, and other investment products. This expands the subsidiary’s permissions beyond its original scope of digital asset securities under Regulation D and S exemptions.

How did Ondo tokenize BlackRock’s IVV ETF?

Ondo used the SEC’s third-party custodial tokenization model, which the SEC formally described in January 2026 guidance. BlackRock’s IVV ETF and Micron shares became the first securities tokenized under a domestic U.S. framework, providing identical investor protections and ownership rights as traditional holdings.

What is Ondo Network?

Ondo Network is a high speed execution layer that replaced Ondo’s earlier plans for a standalone Layer 1 blockchain. It pairs centralized exchange level performance with non-custodial, onchain-verifiable settlement. Its first application is Ondo Perps, a perpetual futures platform using tokenized assets as collateral.

How large is the tokenized asset market in 2026?

Total real world assets onchain crossed $36 billion in 2026. Tokenized U.S. Treasuries alone reached approximately $12.88 billion, up from roughly $5 billion in late 2024. BCG projects the broader RWA market reaching $16 trillion by 2030.

What happened with the SEC investigation into Ondo?

The SEC investigation, opened in October 2023 under Chair Gary Gensler, examined whether Ondo’s tokenized securities constituted unregistered offerings. Under Chair Paul Atkins, the probe was closed without enforcement action, removing the single largest regulatory risk facing the company.

What institutional partnerships does Ondo have?

Ondo’s partners include Mastercard (Multi-Token Network integration), Fidelity (tokenized fund strategies), PayPal ($25 million PYUSD facility), SBI (Japanese stocks onchain), and membership in the DTCC tokenization consortium alongside BlackRock, JPMorgan, and Goldman Sachs.

What is the ONDO token price and supply?

ONDO trades at approximately $0.41 with a market capitalization of roughly $1.5 billion. The circulating supply is approximately 4.87 billion of a 10 billion total supply. The Ondo DAO recently approved a burn of 100 million tokens, representing 1% of total supply.

Disclaimer: This article is for informational purposes only and does not constitute financial or investment advice. The information presented reflects publicly available data as of July 31, 2026. Readers should conduct their own research and consult qualified financial advisors before making investment decisions.

Broiler – Money (Broiler remix)

Fleadh Cheoil map for navigating Belfast city centre during the festival

Every decision of government needn’t be a big reform: Anand Mahindra

![Sie wollen, dass du reich wirst, ABER nicht so [Gold und Bitcoin]](https://wordupnews.com/wp-content/uploads/2026/08/1785542166_maxresdefault-80x80.jpg)

-

Sports5 days ago

Sports5 days agoCommonwealth Games boxing: Jadumani Singh seals dominant 5-0 win over Pakistan’s Sumama Rehman to enter quarter-finals | Commonwealth Games News

-

Business2 days ago

Business2 days agoWhy Trees Belong on the Risk Register

-

Tech5 days ago

Tech5 days agoIntel is reversing course and bringing hyper-threading back to its server chips

-

Fashion6 hours ago

Fashion6 hours agoWeekend Open Thread: Wit & Wisdom

-

Politics3 hours ago

Politics3 hours agoMeta enters AI-training agreement with far-right ‘propaganda rag’ Newsmax

-

Crypto World6 days ago

Crypto World6 days agoRipple bought a bank in pieces. The $4 billion audit

-

Politics5 days ago

Politics5 days agoLuke Littler dismantles Gerwyn Price to retain title in Blackpool

-

Politics4 days ago

Politics4 days agoThe Part of the Electric Transition Nobody Wants to Discuss

-

News Videos5 days ago

News Videos5 days agoBITCOIN JUST ENTERED THIS CRITICAL ZONE…

-

Entertainment3 days ago

Entertainment3 days ago‘Stargate’ Creator’s New Sci-Fi Series Returns for Season 3 Tomorrow

-

Crypto World6 days ago

Crypto World6 days agoXRP Ledger adds $2.6B as RWA inflows rank second

-

Business3 days ago

Business3 days agoMajor shareholder moves on Canyon

-

Politics5 days ago

Politics5 days agoSpain sweeps the board at 2026 World Cup with individual awards

-

News Videos2 days ago

News Videos2 days agoBitcoin Enters the 3rd Stage of the Bear Market

-

Entertainment6 days ago

Entertainment6 days agoSara Gilson Killed By Husband After Viral “Pedophile” TikTok Video

-

Crypto World3 days ago

Crypto World3 days agoKraken Enables Retail Access to Jersey Mike’s IPO via Tokenized Shares

-

Tech7 days ago

Tech7 days agoAnthropic launches Claude Opus 5, a cheaper AI model for coding, agents and enterprise workflows

-

Tech4 days ago

Tech4 days agoNew macOS Sequoia & Sonoma security updates for older Macs

-

News Videos3 days ago

News Videos3 days agoClaude: Build Financial Dashboards in Minutes (2026)

-

Politics1 day ago

Politics1 day agoLuke Littler’s dominance sparks GOAT debate

You must be logged in to post a comment Login