Crypto World

SpaceX’s Bitcoin Trojan horse: what 18,712 BTC means

SpaceX went public in the largest IPO ever, and tucked inside its balance sheet are 18,712 bitcoin. Now every index fund and pension that buys the stock owns a sliver of BTC whether they meant to or not. Bulls call it a Trojan horse that could put a floor under Bitcoin. Here is what the holding actually does, and what it does not.

Summary

- SpaceX went public around June 12, 2026, in the largest IPO ever, priced at $135 a share, raising roughly $75 billion at about a $1.75 trillion valuation, with the stock spiking over 26% before sliding back below its opening price.

- The company disclosed 18,712 bitcoin, worth about $1.29 billion as of March 31, in its filing, so anyone who buys the stock gains indirect, passive exposure to Bitcoin.

- The bullish thesis is that index funds, pensions, and ETFs buying SpaceX for its aerospace and AI exposure will inherently and mechanically hold Bitcoin, creating price-insensitive demand and legitimizing BTC as a corporate treasury asset.

- The skeptical view is that the holding is a tiny fraction of a $1.75 trillion company, so the per-share Bitcoin exposure is minuscule, and that a giant risk-on IPO can drain capital from crypto in the near term rather than support it.

- The story also raises a Tesla-merger overhang that could concentrate roughly 30,000 BTC under Elon Musk, and a copycat question about whether other pre-IPO giants disclose Bitcoin to court crypto-correlated investors.

SpaceX went public around June 12, 2026, in the largest initial public offering in history, and inside the balance sheet of the most anticipated listing of the decade sits a detail that the crypto market has fixated on: the company holds 18,712 bitcoin. The offering priced at $135 a share, raised roughly $75 billion, and valued SpaceX at about $1.75 trillion, with the stock spiking more than 26% in early trading before sliding back below its opening price, a debut dramatic enough that reports described Elon Musk crossing into trillionaire territory on paper. For the broader market, the headline was the sheer scale of the raise and the arrival of a private giant on public markets. For crypto, the headline was the bitcoin.

With 18,712 BTC on its books, worth roughly $1.29 billion as of the end of March, SpaceX is now one of the larger corporate holders of the asset, and that holding has been folded, through the IPO, into a stock that thousands of funds will own. The argument that has spread across crypto social media is that this makes SpaceX a Trojan horse: a vehicle that smuggles Bitcoin exposure into the portfolios of investors who never set out to own any. That framing is catchy, and it points at something real, but it deserves to be examined rather than simply repeated, because the truth is more nuanced and more interesting than the slogan. The best version of the story is not that SpaceX suddenly controls Bitcoin’s price, but that Bitcoin has been made slightly more normal inside public-market infrastructure.

This article works through what the SpaceX bitcoin holding actually means for crypto, taking both the bullish and the skeptical cases seriously. It covers the IPO and the bitcoin inside it, the Trojan-horse thesis in its strongest form, why that thesis has genuine force, the math problem that cuts against it, the opposite argument that a giant IPO can pull capital out of crypto rather than feed it, the Tesla-merger overhang that could concentrate an enormous bitcoin position under one person, the question of whether other companies will copy the template, and a net read of what it all means. The forecasts and interpretations here are information, not advice. The goal is to let a reader walk away understanding both why the Trojan-horse idea caught fire and why the sober version of the story is more modest than the headline, because the gap between the two is where the real lesson about Bitcoin’s institutionalization lives.

The IPO and the bitcoin inside it

Start with the facts of the listing, because the scale is the context for everything else. SpaceX priced its IPO at $135 a share in a deal that raised roughly $75 billion, the largest public offering ever attempted, and valued the company at about $1.75 trillion, a figure lifted further by its earlier integration of Musk’s artificial-intelligence venture. The demand was extraordinary, with the offering reportedly several times oversubscribed and total interest running into the hundreds of billions of dollars, and the stock jumped more than a quarter in its first trading before giving much of that back and slipping below its opening price, a volatile debut that matched the hype around it. SpaceX’s business underneath the listing is real and large: 2025 revenue ran around $18.7 billion, driven heavily by Starlink, with rockets and the AI division making up the rest, though the company posted a substantial net loss for the year tied to the AI integration.

The bitcoin is the part that concerns crypto. SpaceX has held Bitcoin as a strategic reserve asset since 2021, viewing it, in Musk’s framing, as a long-term hedge, and its filing disclosed a position of 18,712 BTC with a fair value of roughly $1.29 billion as of March 31. Ahead of the listing, the company tidied up its holdings, consolidating legacy addresses into a single institutional custody arrangement, the kind of housekeeping a company does when it expects scrutiny of its balance sheet during an audit. For readers trying to understand how corporate BTC holdings work, this is the key difference between a private balance-sheet rumor and a public-market disclosure: the asset becomes visible, auditable, and part of the company’s reported financial picture.

What matters for the Trojan-horse argument is that this holding did not stay private. By going public, SpaceX wrapped its bitcoin inside a widely held stock, and the disclosure landed in the prospectus right alongside the Starlink revenue, which some observers read as a deliberate signal to bitcoin-friendly investors instead of an incidental footnote. The position is now a permanent, audited line on the balance sheet of one of the most important companies in the world, which is precisely what gives the next argument its appeal. SpaceX is not a Bitcoin treasury company in the Saylor sense; it is an operating giant with a crypto reserve attached, and that is exactly why the signal carries weight.

The Trojan-horse thesis in its strongest form

The bullish case is worth stating in its most compelling version before testing it. The argument runs like this. When a company the size of SpaceX lists on a major exchange, it becomes eligible for inclusion in the large stock indices, and inclusion in an index like a major large-cap benchmark means that every fund tracking that index must buy the stock, mechanically, regardless of any view on its components. Index funds, exchange-traded funds, pension funds, and other passive vehicles collectively command trillions of dollars and are required by their mandates to hold the constituents of the indices they track.

So once SpaceX enters the major indices, an enormous pool of capital will buy its shares not because those investors want aerospace, AI, or bitcoin, but simply because the stock is in the index. And because the stock carries 18,712 bitcoin on its balance sheet, every one of those passive buyers gains indirect exposure to Bitcoin whether they want it or not. That is the passive-buying mechanism explained in its simplest form: a mandate can create exposure without a fresh discretionary decision. The buyer thinks they are getting SpaceX, and buried inside that exposure is a tiny piece of BTC.

The thesis extends from there into a price argument and a legitimacy argument. On price, the claim is that this passive, mandate-driven buying creates a form of demand for Bitcoin that is insensitive to Bitcoin’s own price, because the funds are buying SpaceX for index reasons, not BTC reasons, and that this could function as a kind of structural floor under the asset, a layer of forced, ongoing exposure that does not sell on bad crypto news. On legitimacy, the claim is arguably more durable: by holding bitcoin as an audited treasury reserve inside a trillion-dollar public company, SpaceX validates Bitcoin as a serious corporate asset class, the same way earlier corporate treasuries did but at far greater scale and visibility. As one widely shared version of the argument put it, the bitcoin on SpaceX’s books is not a footnote but a balance-sheet argument, and every buyer of the stock gets passive Bitcoin exposure built in.

It is a genuinely clever observation, and it is not wrong. The problem is scale. A Trojan horse can be real while carrying a much smaller payload than the army imagines. The next sections separate the valid legitimacy signal from the much weaker claim that this creates a meaningful price floor.

Why the thesis has real force

Before puncturing anything, it is worth crediting what the Trojan-horse argument gets right, because parts of it are sound. The mechanical point about passive investing is accurate. Index funds really are required to hold index constituents, and the growth of passive investing means that a large share of all stock-buying is now done by vehicles that do not exercise discretion over individual holdings. If SpaceX enters the major indices, it is true that a great deal of capital will hold the stock automatically, and it is true that those holders thereby gain some exposure to the company’s bitcoin.

That exposure is real, it is ongoing, and it does not depend on anyone deciding they like Bitcoin. In that narrow sense, the Trojan horse is not a metaphor but a description: index inclusion would smuggle a measure of BTC exposure into portfolios indifferent to it. That matters because Bitcoin’s institutionalization is not only about people choosing Bitcoin directly. It is also about Bitcoin becoming part of financial products, company balance sheets, ETF structures, and public-market plumbing until investors encounter it without seeking it out.

The legitimacy argument is even stronger, and it may be the part that matters most. There is a meaningful difference between a smaller company holding bitcoin as a treasury bet and one of the most scrutinized companies on the planet carrying an audited, multibillion-dollar bitcoin position through the most high-profile IPO in years. The disclosure normalizes Bitcoin as a reserve asset at the highest tier of corporate America, and the fact that it sat in the prospectus next to the core business, instead of being downplayed, signals that SpaceX was comfortable presenting it to institutional investors. That normalization has a compounding quality: each major company that holds bitcoin and survives the scrutiny makes it easier for the next one to do the same, gradually shifting bitcoin from a speculative oddity on a balance sheet toward an accepted, if still volatile, treasury option.

For Bitcoin’s long-term institutional adoption, a trillion-dollar company carrying it through a landmark listing is a genuinely supportive data point. The Trojan-horse framing captures this real dynamic, which is why it resonated. The trouble is only that the price-floor version of the argument oversells the scale of what is happening. A signal can be important without being a demand engine.

The math problem with the thesis

Here is where the sober counterpoint enters, and it is decisive on the narrow price-floor claim. The bitcoin holding, while large in absolute terms, is tiny relative to the company that now contains it. SpaceX holds about $1.29 billion in bitcoin against a market valuation of roughly $1.75 trillion. That means the bitcoin represents well under one tenth of 1% of the company’s value.

For an investor buying SpaceX stock, the embedded bitcoin exposure per dollar invested is therefore minuscule: putting $1,000 into SpaceX shares buys, in effect, well under $1 of indirect bitcoin exposure. The passive, mandate-driven buying that the Trojan-horse thesis celebrates is real, but the slice of that buying which flows through to Bitcoin is a rounding error on the size of the position, not a meaningful new source of demand for an asset whose own market value runs well into the trillions. This matters because the price-floor claim depends on the indirect demand being large enough to move Bitcoin, and it is not. Index funds buying SpaceX are buying aerospace, satellite connectivity, and AI; the bitcoin is incidental ballast.

The dollars that reach BTC through this channel are a vanishingly small fraction of both the funds’ purchases and Bitcoin’s market capitalization. To put a real floor under Bitcoin, you would need sustained buying measured against Bitcoin’s own trillions, and the SpaceX channel simply does not supply that. The honest framing is that the Trojan horse delivers a legitimacy signal and a tiny sliver of passive exposure, not a structural price floor. Investors who bought the slogan expecting SpaceX index inclusion to meaningfully lift Bitcoin have mis-sized the effect by orders of magnitude.

The exposure is real; its impact on price is negligible. Both things are true at once, and conflating them is the central error in the bullish version of the story. That is why where BTC sits as this lands remains driven by Bitcoin’s own market structure, liquidity, macro backdrop, and flows, not by the tiny BTC line item embedded inside SpaceX stock. The IPO may matter for narrative; the chart still needs direct demand.

The other side: a giant IPO can drain crypto

There is a further argument that runs directly against the bullish read, and in the near term it may matter more than the Trojan horse. A listing of this size does not only add a sliver of bitcoin exposure to index portfolios; it also competes ferociously for investment capital, and crypto sits high on the list of assets that get sold to fund it. The SpaceX IPO was several times oversubscribed, drawing total demand reported in the hundreds of billions of dollars, and that demand had to come from somewhere. Because Bitcoin and other digital assets compete for the same risk-on dollars as high-growth equities and hot pre-IPO names, a generational listing approaching the market can pull money out of crypto as investors raise cash to chase the shares.

In the run-up to the SpaceX debut, that is exactly what some analysts observed, with crypto described as a potential first casualty of the IPO and high-beta tokens selling off as traders trimmed positions to fund their IPO allocations. The dynamic was visible in the tape. As the listing approached, Bitcoin slid toward $60,000 and high-beta tokens fell harder, with XRP and others dropping as the broader complex weakened in what looked like a rotation out of speculative crypto and into the IPO, a move made easier when one major brokerage cut its minimum account requirement for the SpaceX offering dramatically to widen retail access. In other words, the same event that the Trojan-horse thesis frames as bullish for Bitcoin acted, in the short term, as a drain on crypto, because the enormous appetite for SpaceX shares competed with crypto for the same pool of risk capital.

There is a longer-term wealth-effect counter to this, namely that the $75 billion raise unlocks an enormous amount of new wealth for early private investors, capital that tends over time to be redistributed down the risk curve into assets like high-cap cryptocurrencies, so the IPO could eventually feed crypto even as it drained it at the moment of listing. But for anyone weighing the immediate impact, the capital-competition effect is a serious and arguably larger near-term force than the trickle of indirect bitcoin exposure the Trojan horse delivers. The same IPO can be bearish for crypto today and supportive years from now, and both readings have evidence behind them. The mistake is assuming that because SpaceX owns BTC, every effect of the IPO must be bullish for BTC.

That is also why the stock’s own performance matters to crypto psychology. If an investor sees a SpaceX allocation outperform years of holding a major crypto asset, the capital-rotation argument becomes easier to understand emotionally as well as mechanically. A hot public-market listing can absorb the attention, liquidity, and risk appetite that might otherwise have gone into Bitcoin, Ethereum, or high-beta altcoins. The Trojan horse carries a sliver of BTC inside it, but the horse itself can still pull capital away from crypto.

The Tesla-merger overhang

Layered on top of the SpaceX story is a related question that could amplify everything: the possibility of a SpaceX and Tesla combination. Tesla already holds one of the larger corporate bitcoin treasuries among publicly traded companies, with a position reported at over 11,500 BTC, and Musk has at times explored the idea of combining his two largest companies. Neither company has announced a formal merger plan, so this remains speculative, but the arithmetic is striking. If SpaceX and Tesla were brought together, the combined entity would carry the sum of their bitcoin positions, roughly 18,712 plus over 11,500 BTC, which would place around 30,000 bitcoin under Musk’s control inside a single public company, one of the largest corporate bitcoin holdings in public markets.

A combined Musk bitcoin treasury of that size would sharpen both sides of the debate explored above. On the bullish side, it would deepen the legitimacy signal, concentrating a very large, audited bitcoin position inside an even more widely held and index-significant company, and it would extend the passive-exposure dynamic to an even broader base of investors. On the skeptical side, the same math problem would apply, only more so in absolute terms but still small relative to the combined company’s likely valuation, and it would introduce a concentration risk: a very large bitcoin position controlled by one individual, whose decisions about whether to hold, add to, or sell that position could move sentiment if not price. The merger is not on the table as an announced plan, and it may never happen, so it belongs in the analysis as an overhang and a scenario instead of a forecast.

But it is part of why the SpaceX listing drew such attention from crypto, because it hints at a future in which a single corporate vehicle, under a single famous owner, could hold one of the most significant bitcoin treasuries in the world. That prospect is worth watching precisely because it would magnify the dynamics this article describes instead of change them in kind. It would make the legitimacy signal louder and the concentration question sharper. It would not magically turn a corporate balance-sheet allocation into a guaranteed Bitcoin floor.

The copycat question

The final forward-looking thread is whether SpaceX has created a template that other companies will copy, which would matter far more than any single holding. The observation driving this is that SpaceX disclosed its bitcoin position prominently in its prospectus, alongside its core business, in a way some read as a deliberate pitch to bitcoin-correlated investors, the kind of allocators who might pay a slight premium for a stock that offers embedded crypto exposure. If that read is correct, then the bitcoin disclosure was partly a marketing decision, and a successful one could encourage other large private companies preparing to go public to do the same: hold some bitcoin, disclose it in the filing, and capture incremental demand from crypto-friendly investors during the listing. Some commentators speculated that other large pre-IPO technology and AI companies could adopt the template before long, disclosing bitcoin positions to court that pool of allocators.

This is the most speculative part of the story and should be treated as such, because it rests on inference about motives and on unconfirmed reports about other companies’ plans instead of on announced facts. It is entirely possible that SpaceX’s holding reflects nothing more than Musk’s long-standing personal conviction about Bitcoin, with no broader template intended, and that other companies will not follow because their leadership lacks the same view or sees no benefit. But the structural logic is real enough to watch: if disclosing a bitcoin treasury during an IPO measurably helps a company’s reception with a slice of investors, rational companies may do it, and a wave of large listings each carrying some bitcoin would, cumulatively, normalize the asset on corporate balance sheets far more than any single holding could. That cumulative legitimization, instead of the price-floor mechanics, is where the SpaceX precedent could matter most.

Whether other companies copy the template is the single most important thing to watch in the wake of this IPO. For now, it is a plausible hypothesis, not an established trend, and the honest framing keeps it in that category. The broader comparison is the corporate bitcoin-treasury meta, where companies are already being judged on whether their crypto holdings create value or financial stress. SpaceX may make the treasury idea more respectable, but Strategy shows how quickly the same theme can become fragile when market prices move against it.

What it actually means for crypto

Pulling the threads together, the SpaceX bitcoin story is real, important, and considerably more modest than its loudest framing, and holding all of that at once is the mark of understanding it. The Trojan-horse thesis is correct that index inclusion would mechanically give a vast pool of passive capital some indirect bitcoin exposure, and it is correct that a trillion-dollar company carrying audited bitcoin through a landmark IPO is a meaningful legitimacy milestone for the asset. Those points are sound and worth taking seriously, because the institutionalization of Bitcoin is a genuine, multiyear trend and SpaceX is a significant marker along it. Where the thesis overreaches is in the price-floor claim: the bitcoin is well under a tenth of 1% of the company’s value, so the demand that actually flows through to BTC via SpaceX is a rounding error against Bitcoin’s trillions, not a structural support for its price.

Set against that small positive is a real near-term negative, namely that an IPO of this magnitude competes for risk capital and can pull money out of crypto as investors fund their allocations, a dynamic that was visible in the weakness across Bitcoin and altcoins heading into the listing. The longer-term wealth-effect argument, that the raise will eventually redistribute capital down the risk curve toward crypto, cuts the other way but operates on a slower clock. The net read, then, is that the SpaceX IPO is best understood as a legitimization signal for Bitcoin instead of a demand engine, with a small structural exposure benefit, a real short-term capital-competition cost, and a more important open question about whether other companies copy the template and whether a Tesla combination concentrates an even larger position under Musk. For a crypto investor, the practical takeaway is to resist the slogan in both directions: SpaceX did not put a floor under Bitcoin, and it did not doom it either.

It made Bitcoin a little more normal as a corporate asset, took some capital out of the room on its way in, and set a precedent worth watching. That measured reading is less exciting than a Trojan horse, and far closer to the truth. It also leaves room for the other crypto angle of the IPO, where SpaceX exposure became part of the tokenized-stock race rather than only the corporate-treasury story. The IPO pulled crypto into the conversation from several directions at once: BTC on the balance sheet, capital rotation in markets, and tokenized equity products trying to package the shares on-chain.

Frequently asked questions

How much bitcoin does SpaceX hold?

SpaceX disclosed a holding of 18,712 bitcoin in its IPO filing, with a fair value of roughly $1.29 billion as of March 31, 2026. The company has held Bitcoin as a strategic reserve since 2021, viewing it, in Elon Musk’s framing, as a long-term hedge. Ahead of the listing, it consolidated its holdings into a single institutional custody arrangement, the kind of housekeeping done before balance-sheet scrutiny. The position makes SpaceX one of the larger known corporate holders of Bitcoin, and because the company is now public, that holding sits inside a widely held stock, which is the basis for the Trojan-horse argument that buyers of the shares gain indirect bitcoin exposure.

What is the SpaceX bitcoin Trojan-horse thesis?

It is the argument that because SpaceX holds bitcoin and is now a public company eligible for major stock indices, the index funds, pensions, and ETFs that must buy the stock will gain indirect, passive exposure to Bitcoin whether they want it or not. The bullish version claims this creates price-insensitive demand that could put a floor under Bitcoin and that it legitimizes BTC as a corporate treasury asset. The mechanical and legitimacy parts are sound: passive funds really would hold some bitcoin exposure through the stock, and a trillion-dollar company carrying audited bitcoin is a real validation. The price-floor part is where it overreaches, because the holding is too small relative to the company to move Bitcoin meaningfully.

Will the SpaceX IPO push Bitcoin’s price up?

Probably not in any meaningful, direct way, despite the Trojan-horse framing. The bitcoin holding is well under one tenth of 1% of SpaceX’s roughly $1.75 trillion valuation, so the demand that flows through to Bitcoin when funds buy the stock is a rounding error against Bitcoin’s multi-trillion-dollar market. In the near term, a giant IPO can actually weigh on crypto, because it competes for the same risk-on capital and investors sell crypto to fund share purchases, a dynamic visible in the weakness across Bitcoin and altcoins before the listing. The more durable effect is legitimization of Bitcoin as a corporate asset, which supports long-term adoption, instead of a direct price catalyst.

Could the SpaceX IPO actually hurt crypto?

In the short term, yes, and this is the underappreciated side of the story. An IPO of this size, several times oversubscribed with demand in the hundreds of billions, competes fiercely for investment capital, and crypto sits high on the list of assets sold to fund such allocations because it shares investors with high-beta tech and pre-IPO speculation. Heading into the SpaceX debut, Bitcoin slid and high-beta tokens like XRP fell harder, in what analysts described as crypto being a potential first casualty of the IPO drain. Over the longer term, the wealth unlocked by the raise could redistribute toward crypto, but the immediate capital-competition effect is a real headwind that runs opposite to the bullish Trojan-horse narrative.

What does a possible Tesla merger have to do with it?

Tesla already holds one of the larger corporate bitcoin treasuries, reported at over 11,500 BTC, and Musk has at times explored combining SpaceX and Tesla, though neither company has announced a formal plan. If they merged, the combined entity would hold roughly 30,000 bitcoin, around 18,712 from SpaceX plus over 11,500 from Tesla, placing one of the largest corporate bitcoin positions in public markets under Musk’s control. That would deepen the legitimacy signal and broaden the passive-exposure dynamic, while also concentrating a very large bitcoin holding under one individual. It remains a speculative overhang instead of an announced event, but it is part of why the SpaceX listing drew so much attention from the crypto market.

Will other companies copy SpaceX and disclose bitcoin?

It is a real possibility but unconfirmed. SpaceX disclosed its bitcoin prominently in its prospectus, which some read as a deliberate pitch to bitcoin-correlated investors who might favor a stock with embedded crypto exposure. If that helped its reception, other large pre-IPO companies, including major technology and AI firms, could adopt the same template, disclosing bitcoin positions to court those allocators. Some commentators have speculated exactly that. If it became a trend, a series of large listings each carrying bitcoin would normalize the asset on corporate balance sheets far more than any single holding. For now it is a plausible hypothesis based on inference instead of announced plans, and whether companies actually copy it is the most important thing to watch from here.

This article is information, not financial or investment advice. Figures on SpaceX’s bitcoin holding, valuation, IPO terms, and related companies reflect reporting available as of June 30, 2026, are point-in-time, and can change. References to a possible Tesla merger and to other companies disclosing bitcoin are speculative and unconfirmed. Cryptocurrency and equities are volatile and you can lose money. Do your own research and consult a qualified financial professional before making any decision.

Beyond the Robinhood Chain ecosystem, the company announced several additional product launches and international expansion efforts. Robinhood said it is expanding perpetual futures trading in Europe to include commodities, ETFs and foreign exchange markets alongside crypto. It also plans to launch crypto trading in the U.K. and said its services are now available in Canada following its acquisition of WonderFi.

The company also unveiled Agentic Accounts for crypto, an AI-powered trading tool that will allow eligible U.S. users to connect AI models to Robinhood’s trading infrastructure while retaining control over capital allocation and trading parameters.

“Decentralized finance unlocks possibilities beyond what traditional finance can offer, but historically, it has required technical expertise to navigate,” Johann Kerbrat, Robinhood’s senior vice president of crypto.

Robinhood’s product push shows how the lines between crypto and traditional finance are continuing to blur. The brokerage has steadily expanded beyond stocks and spot crypto trading into tokenized equities, derivatives and event contracts, better known as prediction markets. That strategy fits into the race for the “everything exchange” to host all kinds of trading and financial activity under one roof, increasingly on top of blockchain rails.

At the same time, the company also said last month it would lay off 10% of its workforce, some 290 employees, to streamline its organization and management structure.

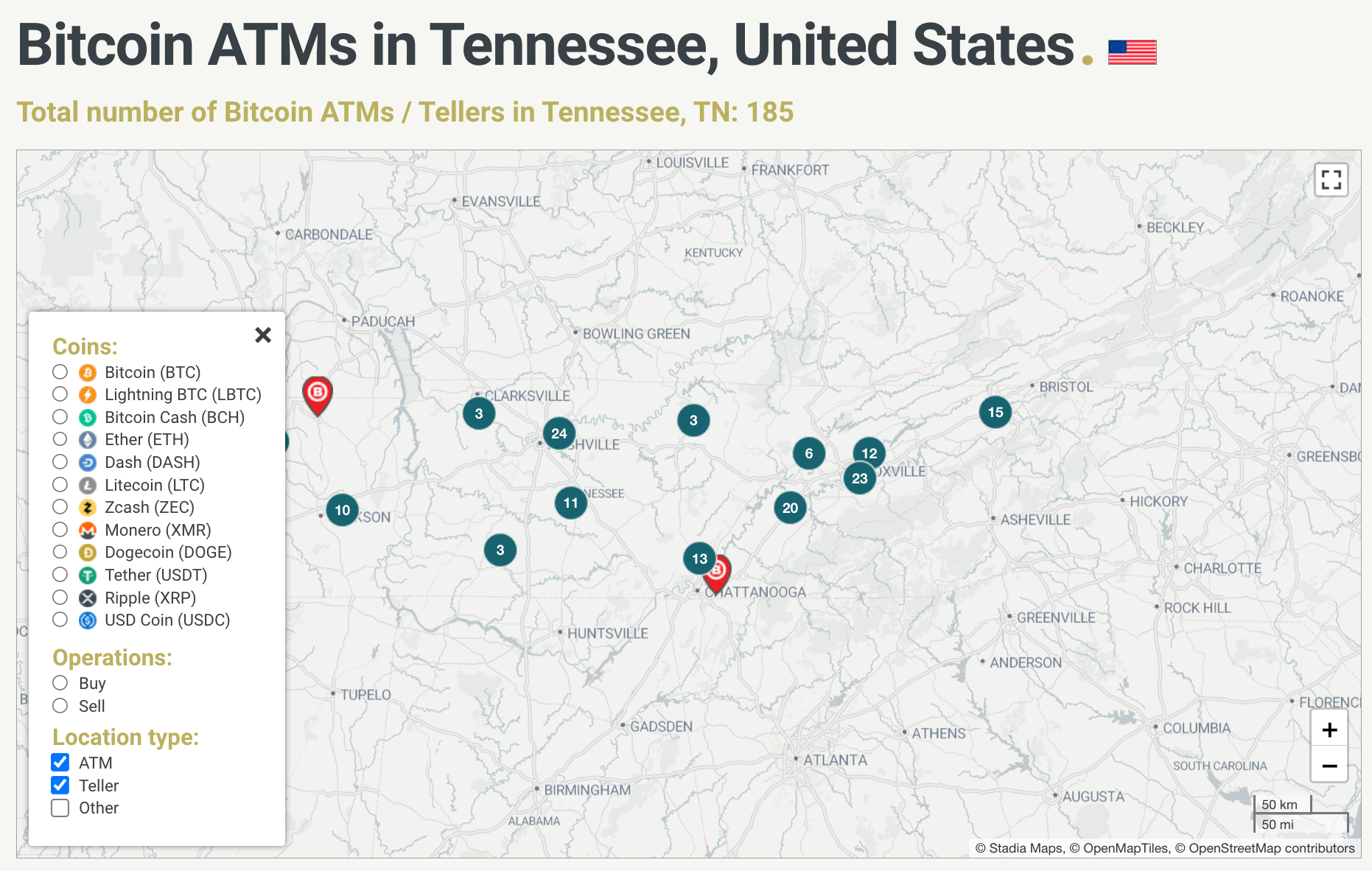

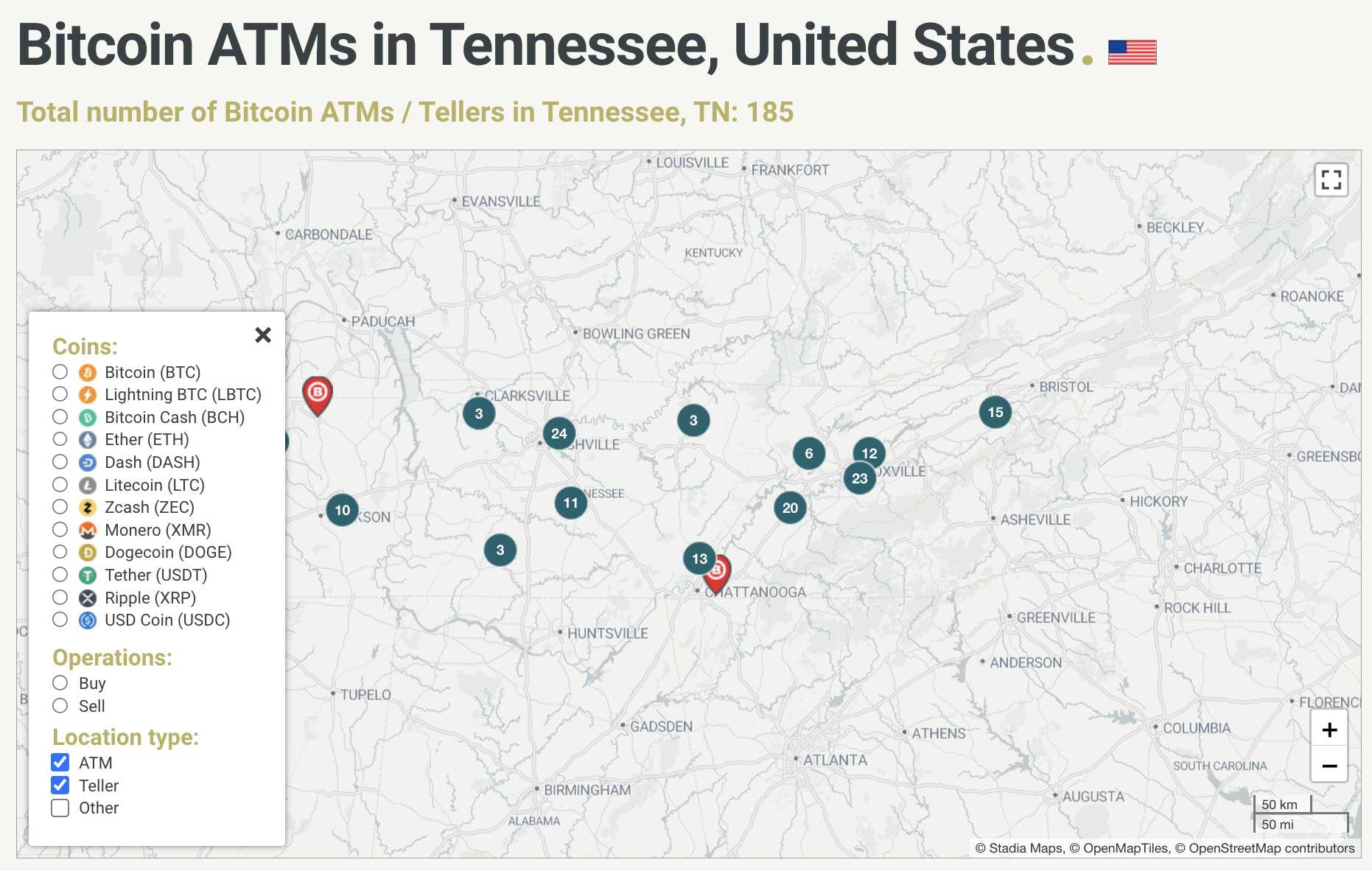

Crypto ATM availability is shrinking in the United States as new state laws designed to curb fraud and tighten consumer protections move into force. Tennessee and Georgia are the latest states to impose restrictions effective this week, following earlier actions in Indiana and upcoming enforcement in Minnesota.

The changes reflect a broader pattern: regulators and lawmakers across the US are targeting kiosks after scammers used them—often to trick vulnerable residents—into sending funds. For operators, the result is a more complex compliance landscape and, in some cases, an unsustainable business model.

Key takeaways

- Tennessee has implemented a statewide ban that prohibits the use and installation of crypto ATMs and kiosks.

- Georgia allows crypto ATMs to operate but introduces transaction caps, customer warnings, and reporting requirements, with provisions that can include refunds in certain fraud cases.

- Earlier state bans include Indiana (effective in March), while Minnesota is set to enforce a ban on Aug. 1.

- Regulatory pressure is already showing up financially, with Bitcoin Depot filing for Chapter 11 bankruptcy after signaling “substantial doubts” about its future.

Tennessee and Georgia tighten rules on crypto kiosks

Georgia and Tennessee each passed crypto ATM legislation that takes effect on Wednesday, but the approaches differ sharply. Tennessee’s law—signed by Governor Bill Lee in April—implements a complete prohibition on both installing and using cryptocurrency ATMs and kiosks.

Georgia’s law is more permissive while still aiming to reduce consumer harm. It requires operators to limit the amount of money sent by users, issue warnings to customers, and in some scenarios refund people who may have been defrauded.

Before Tennessee’s statewide ban took effect on July 1, CoinATMRadar data cited by CoinATMRadar’s Tennessee listing indicates there were 185 crypto ATMs and kiosks operating in the state.

Why lawmakers are moving from “local bans” to statewide action

The Tennessee and Georgia measures follow a wave of earlier regulatory efforts aimed at crypto ATM operators. Cointelegraph previously reported that multiple jurisdictions and municipalities have begun cracking down on kiosks, largely in response to scams in which victims—particularly older adults—were persuaded to send cryptocurrency through ATM-style machines.

Delaware and New Jersey, for example, have considered proposals that would impose complete bans, according to earlier coverage referenced in the original reporting. The direction of travel is consistent: lawmakers increasingly view crypto ATMs as high-risk access points for fraud rather than neutral on-ramps.

As these restrictions expand, operators face more than just reduced machine counts. Compliance obligations—such as monitoring transactions, handling fraud-related disputes, and meeting consumer protection requirements—can increase costs while limiting revenue options.

Regulation’s downstream effects: bankruptcy risk for operators

For the industry, the regulatory tightening is not only theoretical. The restrictions may have already contributed to at least one major operator’s distress.

In May, Bitcoin Depot filed for Chapter 11 bankruptcy. In the days leading up to the filing, the company disclosed that it had “substantial doubts” about its future amid a challenging regulatory environment and ongoing litigation.

Roshan Dharia, CEO of Echo Base and a restructuring adviser, told Cointelegraph after the Chapter 11 filing that Bitcoin Depot’s bankruptcy likely foreshadows broader pressure on the crypto ATM sector. Dharia argued that the traditional operator model relied on relatively high transaction spreads and fewer regulatory constraints, which helped offset the high costs of compliance, cash logistics, fraud remediation, and retail revenue-sharing arrangements.

That equation, Dharia said, is breaking down as states increasingly impose consumer-protection standards. Those standards can compress fees while increasing operator liability for scam-related activity and raising expectations for transaction monitoring and reimbursement—factors that can strain business viability, especially for operators with thinner margins.

Canada signals a wider policy debate

While the latest developments are focused on US states, Canada’s regulatory conversation is also moving toward harsher restrictions. Earlier, federal policymakers in Canada proposed a total ban on crypto ATMs across the country.

The proposal would still allow Canadians to buy digital assets from brick-and-mortar money services businesses, but it would remove the kiosk pathway. Officials described crypto ATMs as the “primary method” used by scammers to defraud victims and as a channel for criminals to put cash proceeds of crime into the digital asset ecosystem.

What to watch next

With Tennessee now operating under a full ban and Georgia enforcing limits and reporting, attention will likely shift to how quickly other states follow suit—particularly Minnesota ahead of its Aug. 1 deadline—and whether operators adjust by exiting certain markets or restructuring their compliance and fraud-handling processes.

Reform UK has removed a proposed crypto bill from its website amid ongoing controversy around billionaire Tether investor Christopher Harborne’s secret £5 million “gift” to the party’s leader, Nigel Farage.

The Cryptoassets and Digital Finance Bill was announced last year during the Bitcoin 2025 conference in Las Vegas. However, The Nerve reports that the bill was scrubbed from the website on May 30 this year.

The Nerve also notes that the bill’s PDF can still be found online but is no longer present on Reform UK’s own website.

A month before the bill’s removal, The Guardian revealed that Reform leader Farage was given £5 million by billionaire Christopher Harborne before he ran for election in June 2024.

Read more: Nigel Farage: £5M Christopher Harborne gift was ‘reward’ for Brexit

The gift from Harborne, who holds a 12% stake in billion-dollar stablecoin firm Tether, was kept a secret and not declared on the parliamentary register of interests.

Weeks after this report, the UK’s Parliamentary Standards Commissioner launched a probe to determine whether or not the gift breached any rules. Farage maintains it never had to be declared, and how he spends it isn’t “the public’s business.”

Reform UK crypto bill appears ‘made up by a schoolkid’

The now-deleted bill made numerous promises in a seeming attempt to portray Reform UK favorably in the eyes of crypto traders.

For example, it promised to reduce the crypto capital gains tax to 10%, introduce a UK BTC reserve, and bar banks from restricting services based on crypto transactions.

The Nerve spoke to various finance and law experts who reviewed the bill and determined that it would benefit the super-rich while failing to do little to protect users from fraud and scams.

Read more: Nigel Farage said shady alleged crypto ATM owner is ‘like a son to me’

Professor of finance at Sussex University, Carol Alexander, told The Nerve that the bill appears like it was “made up by a schoolkid.”

Meanwhile, financial economist Frances Coppola said the bill features policies “which, from an economic standpoint — even from a welfare standpoint — really make little sense.”

Dr Philipp Paech, an associate professor of law at the London School of Economics, said, “It is a nonsensical proposal in terms of public policy and would directly benefit a specific clientele.”

The Nerve also notes that across the entire bill, stablecoins are mentioned once within a list of definitions. This is despite the highly-publicised stablecoin lobbying Farage undertook against the Bank of England last year.

Many believe that the controversy over the gift has been the reason for Farage drastically cutting back on his media duties. Indeed, The Financial Times reports that he reduced his interactions with the press from 20 conferences between January and April 2026 to just one in May.

Read more: UK’s Liberal Democrats want inquiry into Nigel Farage’s £2M bitcoin purchase

Now, according to a Reform UK insider interviewed by The i Paper, Farage is scared that he may face a by-election in his constituency if the parliamentary probe concludes that he broke the rules.

One potential punishment is a 10-day suspension from Parliament. If this happens, The i Paper reports that a successful recall petition could trigger a by-election if it receives signatures from more than 10% of eligible voters

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

Anchorage Digital says it has integrated its off-exchange settlement system with Binance, enabling select institutional clients to trade on Binance without depositing their crypto or cash directly onto the exchange. Instead, clients’ assets and funds can remain in qualified custody at Anchorage—a federally chartered US crypto bank—until settlement.

The arrangement is built around margin and collateral mechanics: institutions can use crypto assets or US dollar deposits held with Anchorage to satisfy Binance’s margin requirements, without moving those holdings to Binance first. Anchorage and Binance framed the workflow as a separation of custody from trade execution, aiming to reduce the operational friction—and counterparty exposure—that can come with pre-funding trades on exchanges.

Key takeaways

- Anchorage integrated its off-exchange settlement platform with Binance to support institutional trading while keeping custody at Anchorage.

- Clients can use Anchorage-held crypto or US dollar deposits as collateral for Binance margin without transferring assets to the exchange.

- The model is positioned as a response to exchange counterparty risk and aims to improve capital efficiency by avoiding pre-funding.

- Anchorage’s Atlas platform is cited as the infrastructure behind this first off-exchange settlement implementation.

- Financial terms of the partnership were not disclosed.

How the Anchorage–Binance model changes custody and collateral

In traditional exchange-based workflows, institutions typically pre-fund trading accounts—transferring assets to the venue where trades are executed. Anchorage’s stated objective with this integration is to shift that balance. Under the collaboration, institutional clients can maintain crypto and cash in qualified custody with Anchorage while accessing trade execution through Binance.

Practically, the integration focuses on margin: Binance’s margin requirements are met using collateral held with Anchorage. The companies say this keeps assets in an independent custodian until settlement, rather than routing custody into the exchange account itself. By design, it also reduces the need for institutions to move holdings between custody providers and the trading venue ahead of every trade.

Anchorage said the rollout is available initially to select institutional clients, marking the first off-exchange settlement deployment for its Atlas platform—an infrastructure Anchorage describes as supporting institutional trading, settlement, lending, and collateral management using custody-based building blocks.

Why “off-exchange settlement” is drawing institutional attention

Exchange counterparty risk has long been one of the main frictions for institutions considering larger allocations to crypto trading. When assets must be deposited to an exchange to enable trading, risk is concentrated at the execution venue. Off-exchange settlement attempts to address that by keeping custody separate from the trading leg, with settlement handled via a different mechanism.

Anchorage and Binance framed their setup as moving closer to the custody-and-execution structure common in traditional financial markets, where institutions can separate where assets are held from where trades are executed and settled. The proposed benefit is twofold: it reduces exposure tied to pre-funding and may also improve capital efficiency by relying on custody-based collateral rather than tying funds to exchange balances.

While the companies did not disclose financial terms, they emphasized the core operational change: trades can be executed on Binance while crypto and cash remain with Anchorage through settlement—an approach intended to make institutional participation smoother without requiring full custody migration to the exchange.

Off-exchange settlement expands across major venues

This Anchorage–Binance integration sits within a broader industry pattern. Off-exchange settlement has been gaining traction among institutional crypto trading platforms throughout 2026, with multiple firms announcing similar custody-and-trade separation approaches.

According to earlier coverage from Cointelegraph, in April BitMEX partnered with Zodia Custody to allow institutional clients to trade derivatives while keeping collateral in segregated custody rather than depositing it onto the exchange. Under that structure, traders could access perpetual swaps and futures while collateral remained with Zodia and was mirrored for trading. BitMEX said the design eliminated the need to prefund exchange accounts and improved capital efficiency, while also reducing operational risks tied to moving assets between custody and trading venues.

In June, Bitget adopted a comparable model by integrating Fireblocks Off Exchange. Bitget said that its integration enables clients to execute trades from MPC-based wallets while keeping assets in trader-controlled collateral vaults rather than transferring them to the exchange. The company also claimed the platform can verify trading accounts are fully collateralized in real time without taking custody of client assets.

Separately, KuCoin Institutional expanded its custody offering earlier in the year by integrating Ceffu’s MirrorX platform in January. That system, according to the linked Ceffu and KuCoin Institutional material, is designed for institutional trading while digital assets remain in third-party custody, with funds mirrored for trading and settled off-chain every four hours.

Taken together, these deployments show a recurring theme: institutions increasingly want the flexibility of exchange liquidity and execution alongside custody structures that better match their risk controls. Off-exchange settlement is becoming a practical pathway to combine those priorities—at least for use cases offered through specific integrations between exchanges, custodians, and settlement platforms.

What investors should monitor next

For institutions, the most important questions now are likely operational and risk-related: which collateral types are supported end-to-end for margin, how settlement timing works in practice for different product categories, and how widely Anchorage’s off-exchange service will be rolled out beyond the initial select client group. Readers should also watch whether more major venues add similar custody-separated settlement layers, as that trend would further define how institutional crypto trading infrastructure evolves.

Key Takeaways

- Walmart shares plummeted more than 5% Wednesday, reaching their lowest point in eight months following a six-session losing streak

- Cleveland Research identified a deceleration in U.S. comparable store sales that may threaten analyst consensus figures, especially in July

- Shares began trading at $113.26, significantly beneath the 50-day moving average of $123.25

- Company insiders offloaded more than $1.06 billion worth of shares during the previous three months without any reported purchases

- Wall Street maintains a Moderate Buy rating with a consensus price target of $138.85, though valuation concerns have emerged

Shares of Walmart began Wednesday’s session at $113.26, representing a decline exceeding 5% and positioning the stock for its weakest closing price in eight months. This marked the sixth straight trading day of declines for WMT.

The catalyst behind the selloff was research from Cleveland Research, which identified signs of decelerating U.S. comparable store sales. The research firm cautioned that this trajectory may negatively impact consensus forecasts, with July’s performance being particularly critical.

In response to inventory challenges, Walmart has implemented price reductions and leveraged tariff refunds to cushion margin pressure. While this represents a strategic response, it underscores the genuine cost and demand challenges confronting the retailer.

The share price deterioration persists even after a robust first-quarter performance. The company delivered earnings of $0.66 per share in May, aligning with analyst projections, while revenue of $177.75 billion surpassed the anticipated $174.84 billion — representing a 7.4% year-over-year gain. Management also maintained its fiscal 2027 guidance of $2.75–$2.85 in earnings per share.

However, investors appear focused on future challenges rather than recent accomplishments.

Significant Insider Transactions Draw Attention

Insider trading patterns have been notably lopsided. Throughout the past quarter, company insiders divested more than $1.06 billion in WMT shares. No insider purchases were documented during this timeframe.

Executive Vice President Christopher Nicholas disposed of 2,900 shares at $123.92 on May 21st. Fellow EVP Latriece Watkins subsequently sold 11,000 shares at $118.97 on May 28th. Both transactions occurred through pre-established Rule 10b5-1 trading arrangements.

Although scheduled sales are standard practice, the substantial magnitude of insider selling has attracted investor scrutiny.

The stock currently trades at a P/E ratio of 39.74 — representing a premium valuation that several analysts question in light of potential growth deceleration. While its GF Score of 86/100 indicates strong long-term fundamentals, near-term momentum has turned decidedly negative.

Analyst Community Maintains Optimistic Stance

Notwithstanding the downturn, Wall Street analysts haven’t abandoned Walmart. The stock maintains a Moderate Buy consensus rating with an average price objective of $138.85 — substantially above present trading levels.

Recent analyst ratings feature a $145 Buy target from BTIG, $140 from Truist, and $137 Outperform ratings from both Wolfe Research and Royal Bank of Canada. Among 36 tracked analysts, 31 maintain Buy ratings and four recommend Hold. A single analyst assigns a Strong Buy rating.

Several institutional investors expanded positions during the first quarter. Littlejohn Financial Services established a fresh $2.81 million position, while Union Bancaire Privee UBP SA increased its holdings by 253.3%.

Walmart’s 52-week high stands at $135.15. The stock’s 200-day moving average rests at $122.22, a threshold now breached to the downside.

With a 1-year low of $94.23, there’s context for evaluating potential downside if selling momentum persists.

Miles Guo, the exiled Chinese businessman who built a following as a critic of Beijing, was sentenced to 30 years in prison for a fraud scheme that raised more than $1 billion from investors. Part of that scheme ran through a fake cryptocurrency called Himalaya Coin. US District Judge Analisa… Read the full story at The Defiant

Cryptocurrency ATMs are fast disappearing from the American landscape as kiosk operators in two US states face bans and restrictions as new laws go into effect.

Crypto ATM laws passed by Tennessee and Georgia went into effect on Wednesday, imposing a complete ban in the former and requiring transaction limits and reporting in the latter. The measures by the two states followed bans in Indiana, which went into effect in March, and Minnesota, set to enforce an ATM ban on Aug. 1.

The Tennessee law, signed by Governor Bill Lee in April, bans the use and installation of cryptocurrency ATMs and kiosks, while the Georgia law requires that ATM operators cap money sent for new and existing users, issue warnings to customers and in some cases refund those who may have been the victim of fraud.

There were 185 crypto ATMs and kiosks operating in Tennessee before the statewide ban took effect on July 1. Source: CoinATMRadar

Many US state governments and municipalities have individually begun cracking down on crypto ATM operators in response to incidents of residents, particularly senior citizens, being conned into sending funds to scammers. Delaware and New Jersey lawmakers have proposed similar measures completely banning the machines.

Related: Massachusetts city to weigh crypto ATM ban, citing financial risks

The restrictions may have already contributed to at least one ATM operator going under. In May, Bitcoin Depot filed for Chapter 11 bankruptcy. The company had disclosed just days before that it had “substantial doubts” about its future amid a challenging regulatory environment and lawsuits.

“Bitcoin Depot’s bankruptcy is likely a preview of what the broader crypto ATM industry will face in the US over the next several years,” Roshan Dharia, CEO of Echo Base and a restructuring adviser, told Cointelegraph following the Chapter 11 filing. “The traditional model depended on high transaction spreads and limited regulatory scrutiny to offset unusually high compliance, cash logistics, fraud remediation, and retail revenue sharing costs. That equation is breaking down as states increasingly impose consumer protection standards that compress fees, expand operator liability for scam related activity, and raise expectations around transaction monitoring and reimbursement.”

Canada weighs countrywide ATM ban

Although not in effect yet, federal policymakers in Canada proposed a total ban on crypto ATMs across the country. The proposed policy, which would still allow Canadians to buy digital assets from brick-and-mortar money services businesses, was in response to what officials called the ATMs being the “primary method for scammers to defraud victims and for criminals to place their cash proceeds of crime.”

Magazine: Bitcoin slides to $58K, XRP hits $1 but onchain data promising: Market Moves

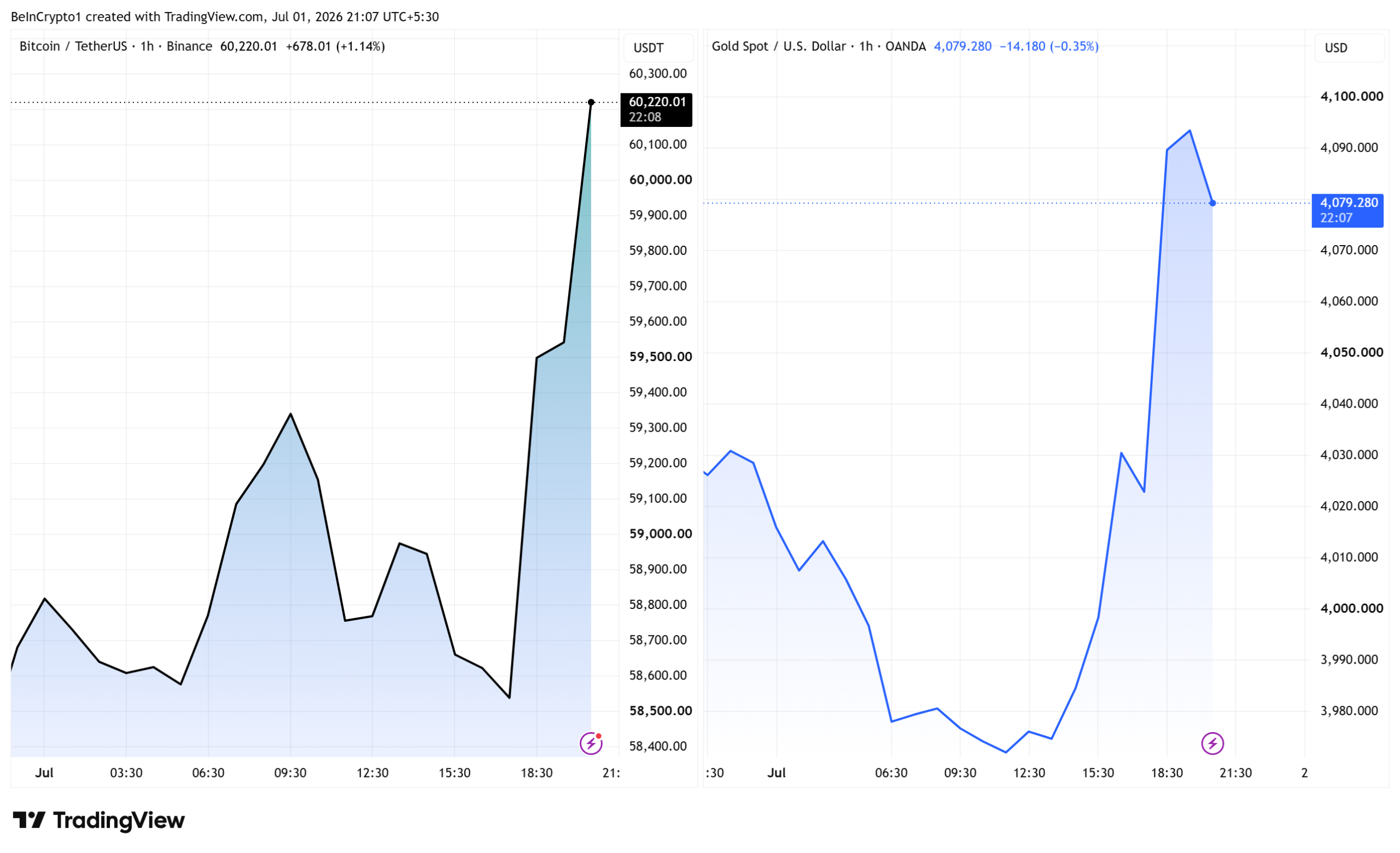

Bitcoin (BTC) reclaimed $60,000 on Wednesday after Federal Reserve Chair Kevin Warsh said inflation risks had eased and struck an open-minded tone on artificial intelligence (AI), reviving appetite for risk assets and precious metals.

The Fed chief declined to call the AI spending boom inflationary and flagged easing price risks, a tone traders judged less hawkish than his June debut. Gold also climbed alongside Bitcoin.

Kevin Warsh Cools Fears of Higher Rates

Warsh spoke at the ECB Forum on Central Banking in Sintra, Portugal, his first international appearance as Fed chair. A longtime inflation hawk, he served on the Fed board through the 2008 crisis. He resigned in 2011 over a $600 billion bond-buying plan.

His words carried weight because US inflation has run hot. Consumer prices rose 4.2% in the year to May, the fastest since 2023, as the war with Iran lifted oil.

That drove the Fed to hold rates at 3.5% to 3.75% in June and signal a possible hike. Those fears eased after oil prices retreated in late June.

Speaking on a panel in Sintra, Warsh pointed to easing price pressures since he took over.

“Inflation risks have come down.”

Yet he insisted the work was not done, recommitting to price stability.

“We’re all in the price stability business … we’ve all looked around and we’ve seen that prices are too high.”

On AI, Warsh was upbeat, calling it a driver of productivity while leaving its inflation impact open.

Notably, some Fed officials have tied AI-driven inflation concerns to the case for hikes.

“What they say is that the demand is insatiable, that these companies, these hyperscalers, will pay almost any price for those inputs, and they need things built yesterday,” Cleveland Federal Reserve President Beth Hammack said recently.

Bitcoin Reclaims $60,000 as Gold Rebounds

Bitcoin traded near $60,088, up about 2.8% in 24 hours, while Ethereum rose about 3.3% to near $1,619. The gains lifted Bitcoin back above $60,000 and its market value over $1.2 trillion.

The bounce followed a steep month. Bitcoin had slid to its 2026 low near $58,000 last week, after hot May inflation triggered $1.26 billion in liquidations. It remains down about 16% from a month ago.

Meanwhile, gold rebounded to an intra-day high of $4,115 after sliding to multi-month lows this week. Silver and other precious metals gained as bets on aggressive tightening eased.

The bond market was less convinced. Treasury yields rose, with the 10-year note near 4.46%. Rising Treasury yields mean bond investors were pricing in higher-for-longer interest rates.

It follows Warsh stressing that prices are “too high” and signaling no rate cut, a hawkish read that ran opposite to the risk-on rally in Bitcoin and gold.

Warsh held a firm line on prices and gave no hint of a July cut. This week’s US jobs report and the Fed’s next meeting, about four weeks away, will test the rally.

The post Kevin Warsh Reignites Risk Appetite: Gold Surges While Bitcoin Reclaims $60,000 appeared first on BeInCrypto.

World, a prediction market built on Solana, went live inside the Phantom wallet and at world.xyz on July 1, using Chainlink as its primary oracle infrastructure, according to the project's own X post. The platform lets users trade event contracts on crypto prices and the 2026 FIFA World Cup, with… Read the full story at The Defiant

Crypto World

Trump’s Government Filing Just Revealed $1.4 Billion in Crypto Earnings Last Year, And His Stablecoin Is Already Under Scrutiny

Donald Trump’s annual financial disclosure, filed with the U.S. Office of Government Ethics, shows at least $1.4 billion in crypto-related earnings for 2025, drawn from three distinct revenue lines: governance token sales through World Liberty Financial (~$800M), royalties from the TRUMP meme coin (~$635M), and an equity sale tied to Stablecoin Holdco (~$197M).

Reuters estimated the Trump family’s total crypto income since the president returned to the White House at $2.3 billion, placing the OGE filing’s $1.4 billion figure as 2025 income alone, not the cumulative haul.

The distinction matters: the disclosure covers the president personally; the Reuters total sweeps in family-linked entities across the broader ecosystem.

Crypto is now formally, under government reporting requirements, the dominant driver of Trump’s personal income, not real estate, not licensing, not Mar-a-Lago, which itself generated more than $77 million last year.

Discover: The Best Token Presales

What the OGE Filing Actually Shows: Three Revenue Streams, One Dominant Theme

The largest component is World Liberty Financial, the DeFi platform the Trump family launched in mid-2024. Trump-linked companies received almost $800 million from WLF, broken down as more than $520 million from governance token sales and more than $250 million from the sale of business interests.

A separate $538 million tranche came from a deal in which WLF sold tokens to ALT5 Sigma, a Trump-affiliated publicly traded crypto treasury firm, an arrangement that illustrates how interconnected the Trump crypto ecosystem has become across entities.

The structural setup that makes those numbers possible: a Trump family-owned entity, DT Marks DEFI LLC, holds entitlement to 75% of token-sale proceeds after expenses, per Reuters. WLF raised $1.4 billion through the sale of 30 billion governance tokens in total.

That revenue-share arrangement is not incidental, it is the engine behind the bulk of the Trump crypto earnings disclosed in the filing. For context on how institutional tokenization infrastructure of this scale is being built across the broader market, the Securitize NYSE listing offers a parallel structural reference point.

The TRUMP meme coin generated $635 million in disclosed income, flowing through CIC Digital LLC almost entirely as royalties tied to a license agreement with Celebration Coins.

Reuters’ parallel investigation put the family’s take from the $TRUMP venture at approximately $616 million in the first half of 2025, a figure close enough to the OGE number to confirm the royalty structure is the primary mechanism. The meme coin’s revenue model depends on trading volume and the royalty rate extracted from that activity, not on price appreciation per se, which means the income stream is partially insulated from token price volatility.

The third line, Stablecoin Holdco, generated nearly $197 million from an equity sale. Bloomberg’s coverage values the underlying USD1 stablecoin business at more than $300 million.

The USD1 stablecoin, issued by World Liberty Financial, has been the subject of intense legislative scrutiny given that the president signed the GENIUS Act stablecoin legislation while holding a direct financial stake in a competing stablecoin issuer. That overlap is not hypothetical, it is now documented in a government ethics filing.

One figure the disclosure excludes: the Trump family still holds World Liberty founder tokens worth approximately $3.8 billion at current market rates, but those remain locked and illiquid and were therefore excluded from income tallies. The realized figures in the filing are large enough on their own.

Don’t Miss Out on Our $1,000 USDT Airdrop on ByBit

The post Trump’s Government Filing Just Revealed $1.4 Billion in Crypto Earnings Last Year, And His Stablecoin Is Already Under Scrutiny appeared first on Cryptonews.

After primary flop, San Jose's mayor banks on World Cup bounce

Brian Flores Pulls Down Impressive NFL Ranking

Taiwanese AI startup sets up North American HQ in Bellevue, with potential for 500 employees

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Staud – Corporette.com

-

Politics6 days ago

Politics6 days agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Crypto World2 days ago

Crypto World2 days agoStrategy authorizes up to $1.25B in Bitcoin sales under new capital plan

-

Politics6 days ago

Politics6 days agoPotential 2028er World Cup attendee leaderboard

-

Business5 days ago

Business5 days agoAsia stock markets slide as tech shares slump

-

News Videos3 days ago

News Videos3 days agoMAJOR BITCOIN & MARKET UPDATE!!!! (MUST WATCH ASAP!!!)

-

Tech6 days ago

Tech6 days agoA Look At A Gaggle Of Transputer Boards

-

Crypto World6 days ago

Crypto World6 days agoDell (DELL) Shares Tumble Over 5% Following Analyst Downgrade to Hold

-

Crypto World4 days ago

Crypto World4 days agoCoinbase, Circle Deepen Crypto Stock Losses Despite Resilient S&P 500

-

Business2 days ago

Business2 days agoAustralia treasurer says alleged access of prime minister’s bank data ’incredibly concerning’

-

Crypto World5 days ago

Crypto World5 days agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Sports5 days ago

Sports5 days agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Crypto World6 days ago

Crypto World6 days agoBitcoin Sparks $600M Hourly Liquidations With $65,000 Set To Become Resistance

-

Tech4 days ago

Tech4 days agoBluekit phishing kit adopts browser-in-the-middle for login theft

-

Tech4 days ago

Tech4 days agoRussian hackers now target Signal backup recovery keys

-

Crypto World5 days ago

Crypto World5 days agoHyperliquid Named on Singapore MAS Investor Alert Register

-

Crypto World5 days ago

Crypto World5 days agoRTX holders must register wallets before token distribution begins

-

Crypto World7 days ago

Crypto World7 days agoRipple and SBI launch RLUSD in Japan after JFSA approval

-

Tech2 days ago

Tech2 days agoAnonymous researcher drops 0-day ‘exploitarium’ repo

-

Sports6 hours ago

Sports6 hours agoBroncos roster: OL Ben Powers (No. 74) entering final year of contract

You must be logged in to post a comment Login