Crypto World

Stablecoin Growth Poses a $500B Risk to Bank Deposits and Net Interest Margins

Standard Chartered warns stablecoins could pull up to $500B from bank deposits in developed markets by 2028.

U.S. banks are increasingly at risk of losing deposits to the digital assets space as stablecoins continue to gain traction.

The concern comes amid growing stablecoin adoption, with the total supply in circulation having risen by roughly 40% over the past year to just over $300 billion.

Long-term Funding Concerns

A Bloomberg report citing analysis from Geoff Kendrick, global head of crypto research at Standard Chartered, estimates that stablecoins could cause the exit of as much as $500 billion in deposits from lenders across industrialized nations by the end of 2028. In the U.S. specifically, the firm predicts that bank deposits could fall by an amount equivalent to one-third of the total stablecoin market capitalization.

Kendrick believes that the pace of stablecoin growth is also likely to accelerate following the passage of the Clarity Act, legislation currently moving through Congress that is meant to regulate the digital asset industry.

“U.S. banks also face a threat as payment networks and other core banking activities shift to stablecoins,” he wrote.

One of the most contentious issues between traditional financial institutions and crypto firms is whether stablecoin holders should be allowed to earn yield-like rewards. Coinbase currently offers 3.5% rewards on balances held in Circle’s USDC, a practice that bank lobbying groups argue could hasten deposit losses if allowed to continue.

“The bank lobbying groups and bank associations are out there trying to ban their competition,” said Coinbase chief executive officer Brian Armstrong at the World Economic Forum in Davos last week. “I have zero tolerance for that; I think it’s un-American, and it harms consumers.”

Despite the ongoing dispute, Kendrick expects the broader crypto market structure bill to be approved by the end of the first quarter.

Regional Lenders Identified as Most Vulnerable

To assess which banks face the greatest exposure, the analyst used the net interest margin income as a share of total revenue, describing it as the clearest indicator of deposit flight risk because it is central to NIM generation. Using this measure, regional American financial institutions emerged as being more vulnerable than diversified lenders and investment banks, which are the least exposed.

You may also like:

Among the 19 US banks and brokerages reviewed, Huntington Bancshares, M&T Bank, Truist Financial, and Citizens Financial Group were identified as facing the highest risk.

Local companies are particularly sensitive to payment outflows because they depend more heavily on traditional lending activities than their larger peers. On the positive side, market performance suggests limited immediate risk.

The KBW Regional Banking Index climbed nearly 6% in January, compared with a little over 1% for the broader metric. In the short term, expected interest rate cuts could reduce deposit costs, while government efforts to stimulate economic activity may support loan growth.

Even so, Kendrick views the longer-term shift as unavoidable.

“An individual bank’s actual exposure to a stablecoin-driven reduction in NIM income will depend largely on its own response to the threat,” he said.

He also highlighted that Tether and Circle, the two dominant stablecoin issuers, hold only 0.02% and 14.5% of their reserves in bank deposits, noting that “very little re-depositing is happening.”

SECRET PARTNERSHIP BONUS for CryptoPotato readers: Use this link to register and unlock $1,500 in exclusive BingX Exchange rewards (limited time offer).

The Solana Foundation on Monday announced a new security auditing framework for Solana-based protocols in addition to an incident-response network, warning that “adversaries are rapidly innovating.”

The Solana Foundation, a Swiss organization that supports the adoption and security of Solana, and Web3 security firm Asymmetric Research unveiled the Solana Trust, Resilience and Infrastructure for DeFi Enterprises (STRIDE), stating that it was a “structured program for evaluating, monitoring and escalating security across Solana projects.”

The initiative works to evaluate the security of protocols across eight pillars: program security, governance and access control, oracle and dependency risk, infrastructure security, supply chain security, operational security, monitoring and incident response, as well as log management and forensics.

Protocols are independently assessed against these requirements, with findings published publicly, said Asymmetric Research. “This gives users, investors, and the broader ecosystem real transparency into the security posture of the protocols they interact with.”

The announcement comes just a week after one of the largest DeFi exploits this year, with the Drift Protocol losing around $280 million following a social engineering attack from North Korean-linked threat actors.

Solana Incident Response Network

The Solana Foundation also announced the Solana Incident Response Network (SIRN), a network of security firms for real-time incident response across the Solana ecosystem.

“Members will share threat intelligence, coordinate responses to active incidents, and contribute to the ongoing evolution of the STRIDE framework,” it stated.

Related: Crypto hackers steal $169M from 34 DeFi protocols in Q1: DefiLlama

The foundation did not mention artificial-intelligence agents directly, but the announcement comes at a time when they are becoming an increasing threat to crypto protocols.

In January, $40 million was drained from the Solana DeFi platform Step Finance, with AI agents amplifying the damage by executing large transfers autonomously, KuCoin reported last week.

Attackers hit 34 DeFi protocols in Q1

Malicious actors stole over $168 million in cryptocurrency from 34 DeFi protocols in the first quarter of 2026, according to data from DefiLlama.

However, the figure has fallen significantly from the same period last year, when $1.58 billion was pilfered in Q1, 2025.

The largest exploit for the period was the private key compromise of Step Finance.

Magazine: No more 85% Bitcoin collapses, Taiwan needs BTC war reserve: Hodler’s Digest

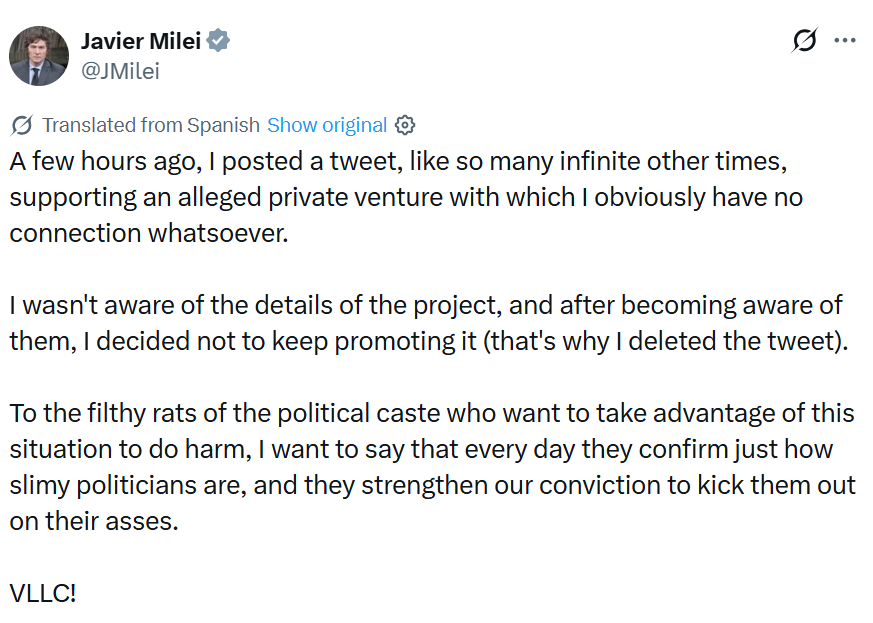

Newly uncovered call logs suggest Argentine President Javier Milei spoke with one of the entrepreneurs behind the Libra token multiple times on the night he promoted the cryptocurrency, raising questions about Milei’s assertion that he had no connection with the project.

According to logs obtained by Argentine prosecutors investigating the token’s collapse, which were seen by The New York Times, there were reportedly a total of seven phone calls between the unnamed entrepreneur and Milei before and after he made his Libra promotion post on X.

The contents of those calls remain unknown, according to the Times.

The collapse of the Libra token has seen Argentine lawyers hit Milei with fraud charges and there were also calls for his impeachment. Fraud can attract a prison sentence of between one month and six years in Argentina.

Cointelegraph has contacted Argentina’s presidential office for comment.

Libra investors lost at least $251 million

In February 2025, Milei made a post on X promoting the Libra token as a way to grow Argentina’s economy by funding small businesses and startups.

The token surged before losing more than 96% of its value from its peak, costing investors around $251 million. Milei later deleted his posts, prompting accusations of a possible rug pull.

Milei has denied any wrongdoing in promoting the short-lived token, saying he was merely highlighting a private venture and had no involvement in the project.

“A few hours ago, I posted a tweet, like so many infinite other times, supporting an alleged private venture with which I obviously have no connection whatsoever,” he said in a post on X.

“I wasn’t aware of the details of the project, and after becoming aware of them, I decided not to keep promoting it, that’s why I deleted the tweet.”

Federal investigation into Libra collapse ongoing

Following the Libra collapse, federal prosecutors launched an investigation that has named Milei as a person of interest. The case remains ongoing.

Argentina’s Anti-Corruption Office cleared Milei last June of violating public ethics rules and found his post was personal rather than in his capacity as president.

Related: Argentina turns up the heat in Libra scandal with sweeping asset freeze

In a recent March update, a judicial investigation uncovered a draft document on crypto lobbyist Mauricio Novelli’s phone suggesting a possible $5 million agreement connected to Milei’s promotion of the Libra token.

The draft note was reportedly written just three days before Milei posted about the Libra token on X, but it does not specify who would receive the funds.

Magazine: Bitcoin may take 7 years to upgrade to post-quantum — BIP-360 co-author

The proposal includes a startup exemption, a fundraising exemption and an investment contract safe harbor for issuers.

US Securities and Exchange Commission Chair Paul Atkins has revealed that a key crypto market safe harbor proposal has landed at the White House for review.

Speaking at the Digital Assets and Emerging Technology Policy Summit on Monday, Atkins said the Regulation Crypto Assets proposal — outlined by the SEC in mid-March — has now been submitted to the Office of Information and Regulatory Affairs.

“We will have reg crypto that we will be proposing here shortly. It’s in fact at OIRA right now, which is the next step before being published,” he said.

Regulation Crypto Assets covers three main ideas: a startup exemption, a fundraising exemption and an investment contract safe harbor for issuers.

If the proposal does end up becoming official rules as part of the SEC’s oversight, it could drive more crypto innovation in the US while providing further regulatory clarity for the industry.

Atkins emphasized that the SEC wants to “hear from the marketplace” to make the whole package “workable.” He did not go into many specifics but said there were a few things the SEC is “building into it” alongside measures such as crypto safe harbors and exemptive relief.

SEC proposal is taking shape

Generally, the SEC first votes to approve a formal proposal, which is then sent to OIRA for review. OIRA then completes the review and it is published in the Federal Register and put up for public feedback.

Cointelegraph reached out to the SEC for comment on the matter.

Related: CFTC chief launches innovation task force focused on crypto framework

The startup exemption would enable projects to raise up to a defined amount over a four-year period with softer disclosure requirements, while the fundraising exemption would enable issuers to raise a defined amount over 12 months while “retaining the ability to rely on other exemptions from registration under the federal securities laws.”

The investment contract safe harbor would protect certain assets from the definition of a security once the project team has ceased all of its managerial efforts “represented or promised” as part of the investment contract.

Chaos Labs has parted ways with Aave after three years of serving as the crypto lending protocol’s primary risk service provider, citing a budget dispute and fundamental disagreements over how risk should be managed. The rupture signals a notable inflection point in DeFi risk governance as Aave advances its V4 migration and navigates ongoing governance tensions within its ecosystem.

Chaos founder Omer Goldberg announced the decision on X, stressing that the move was deliberate and not made in haste. He said Aave Labs was willing to raise its budget to $5 million, but that the engagement “no longer reflected how we believe risk should be managed.” Aave Labs CEO Stani Kulechov offered a different framing, describing Chaos’s departure as the result of a push by Chaos to become the sole risk provider and to replace other partner models. Aave’s stance, the two sides said, remains professional; Chaos did not depart on acrimony, but the parties simply could not reconcile their risk-management philosophies.

Key takeaways

- Chaos Labs exits after a three-year engagement as Aave’s main risk service provider, citing a budget dispute and diverging views on risk management.

- The split underscores tensions between a single-provider model and a two-layer risk framework that Aave maintains, with Chaos allegedly seeking to replace Chainlink’s oracles and other partners.

- Aave assures that the departure has not disrupted its protocol, smart contracts, or listings, while signaling it will continue working with LlamaRisk during the transition.

- The move comes amid broader governance frictions within Aave Labs over funding and revenue control, and just weeks after a notable risk incident fueled calls for stronger safeguards.

What triggered Chaos Labs’ departure from Aave

Chaos Labs has been a cornerstone of Aave’s risk infrastructure since November 2022, handling pricing, risk assessment, and related guardrails across Aave’s V2 and V3 markets. In that period, Aave’s total value locked expanded markedly, underscoring the centrality of robust risk tooling to the protocol’s growth. By late February, Aave had crossed a historic milestone in lending activity, with cumulative lending volume advancing past the trillion-dollar mark, a milestone the project highlighted as a first for the DeFi sector.

Goldberg framed the decision as one driven by a misalignment over risk management and the scope of Chaos’s duties. “This decision was not made in haste,” he stated in a post to X. “We worked in good faith with DAO contributors. Aave Labs was professional and supported increasing our budget to $5m to retain us. However, we are leaving because the engagement no longer reflects how we believe risk should be managed.”

Aave’s account of the dispute diverges on what Chaos was seeking. Stani Kulechov contended that Chaos sought to become the sole risk manager and to substitute Chaos’s price oracles for Chainlink—an approach that would have effectively sidelined other risk partners and compromised Aave’s established two-layer risk model. Chaos’s proposal, Kulechov suggested, would have forced Aave to abandon its multi-provider framework, a move the protocol did not accept. Chaos later indicated it was examining winding down its risk consultancy, even as Aave reportedly offered to double the compensation to keep Chaos onboard.

Beyond the personnel dynamics, the departure arrives at a moment of heightened sensitivity around risk in Aave’s community. The ecosystem has recently grappled with high-profile events that tested the resilience of its risk tools, including a $50 million loss traced to a user interacting with Aave’s interface on March 12. In response, Aave rolled out a shielded risk feature designed to deter high-risk trading behavior, signaling a public push to bolster user safeguards even as internal governance wrestles with funding and control questions.

Risk architecture at stake: Chaos’s demands vs. Aave’s model

At the heart of the disagreement is Aave’s two-layer economic risk model, which blends on-chain risk pricing with external risk data. Chaos has been integrated into the back end of that risk framework, providing pricing and risk management services that supported V2 and V3 liquidity and lending operations. The move toward a broader, multi-provider risk architecture—anchored by partners like Chainlink—was a core feature of Aave’s design philosophy as it expanded and upgraded to V4.

Goldberg argued that Chaos’s push to become the sole risk provider, coupled with a desire to substitute its price oracles for Chainlink’s, would have undermined the protocol’s diversification of risk inputs. Kulechov, conversely, stressed that Chaos’s demand would displace established partners and thrust Chaos into a governance role that Aave does not appear prepared to concede. The exchange underscores a broader tension in DeFi: how to balance centralized expertise with multi-source resilience in a rapidly evolving risk landscape.

In practical terms, the split leaves Aave poised to continue with LlamaRisk and other risk partners as it advances V4 and maintains its two-layer model. Chaos had suggested it could take on a more centralized risk-management posture, but Aave’s leadership signaled a preference for a governance-driven, multi-vendor approach, particularly as the platform expands its risk surface with new features and markets. The dispute also highlights a broader industry question: what responsibilities do risk managers owe when a protocol experiences a failure, and who bears the blame when risk controls falter?

Operational realities of the migration and broader implications

The timing of Chaos’s exit aligns with Aave’s ongoing transition from V3 toward V4, a process that executives warned could stretch over months or even years as liquidity and markets migrate and the new feature set is absorbed into existing ecosystems. Goldberg noted that ongoing operations would require maintaining both V3 and V4 during the migration window, a workload that can be substantial for any risk provider. He warned that without clear safety harbors or settled legal precedents, risk governance remains an area of ambiguity with real consequences when things go wrong.

Kulechov framed the disruption as manageable and non-disruptive to Aave’s immediate operations. He emphasized that Chaos’s departure did not affect Aave’s smart contracts, token listings, or network integrations, and that the protocol would continue collaboration with LlamaRisk to ensure a smooth transition. The episode sits against a backdrop of ongoing governance debates about funding and revenue allocation within Aave Labs, a debate that has punctuated discussions about how the DAO should remunerate development and risk oversight in a high-growth, capital-intensive ecosystem.

For users and investors watching the DeFi risk space, the episode underscores two distinct strands: the push for diversified risk inputs that mitigate single points of failure, and the practical realities of a multi-year migration that tests the stamina of risk tooling and governance structures. The fact that Aave achieved a meaningful lending-volume milestone while navigating this internal shift demonstrates the resilience of its ecosystem, but it also raises questions about the pace of migration and the potential for further shuffles among risk partners as V4 scales.

Cointelegraph’s coverage of related risk and governance developments provides broader context for these tensions. For instance, Aave’s response to the March incident and the subsequent shield feature was part of a wider market emphasis on user protection and risk-aware design. The departure also sits within the wider narrative of DeFi risk management evolving from boutique, single-provider arrangements toward resilient, multi-provider ecosystems that can weather shocks and governance disputes alike.

As Aave moves forward, the roadmap will hinge on how smoothly LlamaRisk can integrate and how quickly the V4 platform absorbs legacy markets and liquidity from V3. Chaos’s exit, while financially notable—the firm had been engaged at a $5 million level—illustrates the bargaining power that risk providers can wield in a high-stakes DeFi environment and the lengthier arc of governance negotiations that can accompany critical infrastructure changes.

For readers tracking the real-world implications, the key questions are clear: will Aave maintain a diversified, resilient risk framework as V4 expands? How quickly will the migration reduce the operational overlap between V3 and V4? And what lessons will the DeFi community draw about risk governance, budgeting, and partnerships from this high-profile split?

Investors and developers should watch for updates on Aave’s transition timeline, any new risk-partner arrangements, and how the community approaches risk coverage as V4 matures. The coming months will reveal whether the industry’s move toward multi-provider risk management proves more robust in practice, or if further shifts among top risk suppliers test the protocol’s continuity and user protection standards.

In the meantime, Aave’s leadership reiterated its commitment to maintaining its two-layer risk model and to working with partners—including LlamaRisk—to ensure a seamless transition. The episode also reinforces the broader industry takeaway that risk management in DeFi remains a live, evolving discipline—one where governance choices, partner ecosystems, and architectural design all shape the safety and reliability that users rely on every day.

Readers can follow ongoing developments as Aave navigates V4 integration and the evolving risk landscape, including how new safeguards and partner arrangements influence user experience, security, and the protocol’s long-term resilience.

Related coverage: Aave’s shield initiative after a high-profile loss, and discussions around risk provision and governance within DeFi ecosystems, offer useful context for evaluating how this split may influence future risk partnerships and platform upgrades. Aave Shield rollout and ongoing governance debates illuminate the environment in which Chaos and Aave operated.

Bitcoin pulled back to $68,589 in Asian hours Tuesday after Monday’s ceasefire-driven rally faded, as U.S. president Donald Trump set a Tuesday night deadline for Iran to agree to a deal and threatened to destroy “every bridge in Iran by 12 o’clock tomorrow night” if it does not.

The largest cryptocurrency is down 0.6% over 24 hours after touching $69,350 on Monday, when an Axios report about a potential 45-day ceasefire briefly pushed prices above $69,000. That optimism lasted about 12 hours. Ether fell 1% to $2,104, solana’s SOL dropped 2.7% to $79.75, XRP lost 1.6% to $1.32, and dogecoin slid 2.2% to $0.09. BNB held relatively flat at $598.

The pattern of the past six weeks continued in textbook fashion, where positive headlines breifly boost prices before negative comments cull any chances of extended recovery.

“This move looks less like a shift in fundamentals and more like positioning getting caught offsides,” said Diana Pires, chief business officer at sFOX. “Heading into the weekend, sentiment was heavily skewed bearish and short interest had built up across the market. Once ceasefire headlines hit, that positioning had to unwind.”

Monday’s bounce produced $196.7 million in short liquidations as bearish traders got caught by the ceasefire report. Tuesday’s pullback arrived when Iran reportedly passed to mediator Pakistan a rejection of the ceasefire proposal, demanding a permanent end to the war, lifting of sanctions, and reconstruction efforts in addition to safe passage through Hormuz.

U.S. crude climbed above $112 as Trump warned the military could put every power plant in Iran “out of business” if no deal is reached, even as he said talks were “going well.” Brent traded near $115.66, up 2.9% on the session. Elsehwhere, the S&P 500 posted its longest advance since January despite the whipsaw, with equities managing to hold small gains through the volatility.

The macro backdrop remains uncertain. U.S. services data showed the economy expanded at a slower pace in March, employment contracted at the sharpest rate since 2023, and input prices accelerated, a mix that gives the Fed no clear reason to cut or hold. Key inflation readings this week will add to the picture.

Bitcoin remains inside the $65,000 to $73,000 range it has traded in for the entirety of the conflict. Every rally has failed at the upper bound, every selloff has held the lower. What happens by midnight Tuesday, when Trump’s deadline arrives, will determine which end of that range gets tested next.

Buy, hold, wait – that’s what most Bitcoin holders do, really.

After all, this is what makes the most sense when the goal is to gain exposure to an asset that investors believe will appreciate over time.

But as Bitcoin matures, that logic starts to feel somewhat incomplete. Holding may preserve upside, yet it does little to address the practical need for liquidity when real-life expenses arise. Selling Bitcoin can unlock cash, but it also means cutting into a position that may have taken years to build.

An alternative that is gaining attention is using Bitcoin not only as something to store, but as an asset that can support borrowing, spending, and measured income generation without fully exiting the trade.

That is the space Xapo Bank is trying to occupy. The bank advertises itself as a premium Bitcoin-and-USD platform built for members who want more than a wallet or exchange account, pairing services such as Bitcoin-backed loans, global spending tools, and yield-oriented products under one membership model.

Let’s explore how it works in more detail.

Using BTC as Collateral Instead of Selling It

For a long-term Bitcoin holder, selling is rarely the ideal solution. It may solve a short-term cash need, but it also reduces exposure to an asset many investors still see as a core long-term position.

That is why Bitcoin-backed borrowing has become a more compelling option for a certain class of holder – it allows them to unlock liquidity without fully exiting the market. Instead of selling BTC outright, they can use it as collateral and access cash while keeping the underlying position intact.

This is one of the central ideas behind Xapo Bank’s lending offering. The bank allows eligible members to borrow against their Bitcoin, with loans of up to $1 million and cash delivered in minutes through the app, depending on the amount of collateral posted.

Xapo says members can borrow up to 40% of their BTC value, choose flexible repayment periods, and repay early without penalty. Just as importantly, the bank frames this as a more conservative lending model than many crypto users grew used to in previous cycles.

According to Xapo, collateral remains segregated and is not rehypothecated, a distinction that carries more weight after the collapses of lending platforms that treated customer assets as fuel for broader risk-taking.

The loan becomes about access – covering a major purchase, bridging a cash-flow gap, or funding a large expense without having to dismantle a long-term Bitcoin position.

The Spending Layer

Liquidity needs to move with you. Borrowing against Bitcoin might help a holder avoid selling, but for the model to feel practical, those funds need to be usable in everyday life.

Xapo places its card right next to its loan product, allowing members to spend from BTC or USD balances globally, with zero foreign exchange fees on card spending, an ultra-low 0.1% spread when spending from Bitcoin, and cashback paid in BTC on qualifying purchases. The reward rate can reach up to 1%, although in the EEA, Switzerland, and the UK, where interchange fees are capped, cashback is lower at 0.2%.

The loan provides access to liquidity without forcing a sale, while the card helps that liquidity function in the real world.

And yes, the company offers a metal card, if you want it.

How Xapo Frames Earning on BTC

For many Bitcoin holders, there’s an opportunity cost to letting an asset sit completely still.

As the Bitcoin investor base matures and starts thinking less about short-term price action and more about long-term portfolio function, ‘earning on your Bitcoin’ is suddenly trending. The appeal, however, isn’t in taking on opaque counterparty risk. Instead, it lies in simpler, more hands-off and conservative ways to grow a BTC position over time.

Xapo’s pitch leans in directly. Instead of presenting yield as something aggressive or experimental, it frames earning as part of a broader wealth-management model for Bitcoin holders who want their assets to do more than just appreciate in price.

That model rests on a few straightforward building blocks:

- Up to 4% APY, paid in BTC, on Bitcoin-denominated investments;

- 3.35% APY, paid in BTC, on USD deposits;

- Up to 1% cashback in Bitcoin on eligible card purchases.

The goal is to create several steady paths for accumulating more sats over time – something attractive for users who have little interest in micromanaging positions or moving funds through a maze of DeFi protocols.

A Welcome Development After Crypto’s Yield Blowups

Crypto users have already seen what happens when earning turns into a euphemism for hidden risk.

Over the past few years, a wide range of lending and yield platforms promised easy returns on digital assets, only for many of those models to unravel under stress. The broader lesson was not that all yield is inherently dangerous, but that the source of the yield, the custody model, and the treatment of client assets matter far more than the headline number.

Even mainstream policy and stability analysis now separates centralised crypto lenders from other parts of the digital-asset ecosystem because of the specific liquidity, maturity, and asset-use risks they introduced. That is exactly the backdrop against which platforms like Xapo are trying to refine a more disciplined crypto wealth model.

Xapo’s positioning is deliberately aimed at that post-blowup audience. Instead of leaning on aggressive returns, it emphasises segregated collateral, a non-rehypothecation model for Bitcoin-backed loans, and a set of simpler earning tools that are easier to understand in plain financial terms.

Xapo is effectively arguing that the grown-up version of crypto earning is not the one with the biggest APY. Instead, it’s the one that makes the mechanics, custody, and trade-offs feel sustainable.

The Private Bank for Bitcoin Maximalists

We’re not looking at a mass-market crypto app trying to win users with zero-cost access and a long menu of speculative features. Xapo markets itself as a members-only private bank for Bitcoin holders, and the $1,000 annual fee is part of that identity.

On its own site, the company presents the membership as a package built around secure custody, daily Bitcoin earnings, liquidity tools, and global access, all aimed at people who see BTC as a serious component of personal wealth.

Ultimately, the industry needs a solution that will give long-term holders of Bitcoin a more complete financial structure around the asset they already believe in. If the old model was simply to buy Bitcoin and wait, Xapo is making the case for something more mature.

Disclaimer: This communication is not intended for, and must not be acted upon by persons resident in the United Kingdom.

The post How BTC Holders Can Borrow, Spend, and Earn Without Exiting Bitcoin appeared first on BeInCrypto.

Bitcoin slid toward $68,000 on Tuesday, with traditional markets closed in Hong Kong for a long weekend, as repeated failures near $70,000 left the bitcoin market vulnerable to a break lower.

The drop came after another failed push above $70,000, with prices slipping quickly once they approached the lower end of the $65,000 to $73,000 range that has defined trading since late March. Intraday losses accelerated near that boundary, highlighting how little support exists when momentum turns.

That calm is not being driven by strong demand. Recent Glassnode data shows softer trading volumes and subdued onchain activity even as prices recover, indicating limited participation behind the move.

Meanwhile, in a note to CoinDesk, crypto-native trading and liquidity firm Caladan pointed to negative demand trends and ongoing distribution by large holders, leaving bitcoin reliant on macro-driven flows and derivatives positioning rather than broad-based accumulation.

The result is a market that looks stable on the surface but is structurally fragile if that balance shifts.

That vulnerability is becoming more visible in derivatives markets. Options data shows traders are increasingly paying up for downside protection, with implied volatility holding above realized levels, a sign that investors are bracing for a larger move even as spot prices remain rangebound.

Analysts who spoke to CoinDesk earlier point to a negative gamma setup below roughly $68,000, where market makers may be forced to sell bitcoin as prices fall in order to hedge their exposure.

The danger: this dynamic can accelerate declines, transforming a gradual move into a sharper, self-reinforcing rout that could drag prices toward the $60,000 level if support breaks.

Prediction markets reflect a similar shift in sentiment. On Polymarket, traders are assigning a 68% probability that bitcoin will trade at or below $65,000 in April, while higher targets such as $80,000 have seen sharply declining odds.

Taken together, the signals point to a market where the calm may hold, but only until key levels give way.

NASHVILLE, Tenn. — The Securities and Exchange Commission is close to proposing a “regulation crypto” fleshing out its approach to overseeing the crypto industry and drawing lines between transactions that might be securities and where they aren’t, the agency’s head said Monday.

SEC Chair Paul Atkins said the commission’s new reg crypto is in front of the White House Office of Information and Regulatory Affairs, meaning it’s one step away from being published. This rulemaking is focused on the Securities Act of 1933 and will address fundraising and startup exemptions, among other issues, he said Monday at an event hosted by Vanderbilt University and the Blockchain Association.

He told CoinDesk after his question-and-answer session that the SEC also intends to put out its long-awaited innovation exemption soon.

“We’d love to have reactions and everything else,” he said. “It’s not a rule as such but obviously we need to know how it’s functioning and if people have problems with it or not.”

One aspect to this exemption, he said, is that it wouldn’t disadvantage incumbents and focus solely on startups.

“We want people really to experiment within [that] framework,” he said.

Midterm watch

At multiple points during his talk, Atkins pointed to Congress’s role, saying that his agency’s rulemaking process was well underway despite whatever Congress may do.

“I think we have enough of a runway now, even notwithstanding what may happen in the midterms — although I really still want a friendly Congress obviously — they can throw tacks on the road in front of our tires but they’re not going to really slow us down.”

Atkins also said the audience needed “to be engaged in this upcoming election,” pointing to Senator Bernie Moreno as an example.

“To have Congress really veer off track is not going to any of us any good, and it’s going to put a lot more questions into the future because people then just have ‘oh gosh, maybe this is again a passing phase,’” he said. “We’ve got to make sure that your friends are in Congress. I think you saw how that really paid benefits in the last election.”

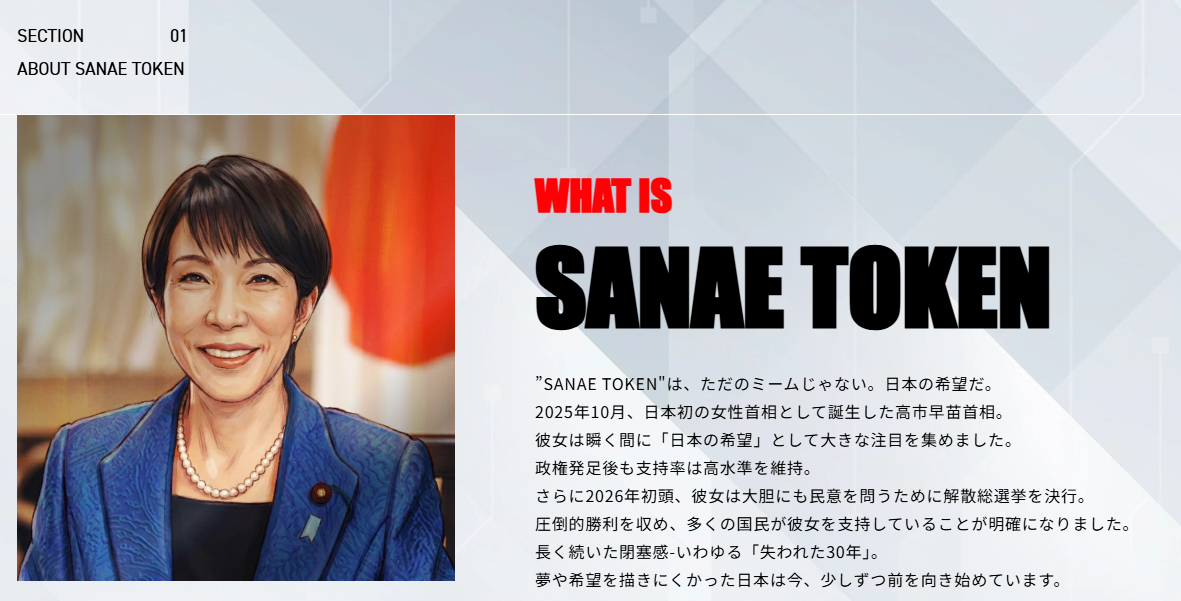

Japan’s SANAE TOKEN saga has entered a new phase, with fresh media reports alleging the prime minister’s office knew more than it admitted. But for crypto markets, the bigger story is what happens next in Tokyo’s legislature.

The political noise and the regulatory signal are arriving at exactly the same time.

How the Token Unraveled

SANAE TOKEN launched on Solana on Feb. 25, as BeInCrypto reported. NoBorder DAO — a community led by serial entrepreneur Yuji Mizoguchi — issued it as part of a “Japan is Back” initiative, with Takaichi’s name and likeness on the project website. The token surged over 40x on launch day before Takaichi’s March 2 denial triggered a 58% crash.

The FSA opened a probe into NoBorder DAO for operating without a crypto exchange license. The token’s operators halted issuance shortly after.

Japanese Tabloid Reports Secretary’s Approval

Weekly Bunshun, a Japanese tabloid known for breaking political and celebrity scandals, says developer Ken Matsui told the magazine his team informed Takaichi’s office that the project was a crypto asset. That directly contradicts her March 2 denial. Takaichi said neither she nor her office had been told anything about the token.

The publication says it obtained audio recordings of Takaichi’s chief secretary over a period of more than 20 years, reportedly describing the project favorably. Another Japanese online media reported that Takaichi’s office had not responded to media inquiries on the matter as of Tuesday. Takaichi has held no press conference since February 18, when her second cabinet was inaugurated.

The political dimension remains unresolved. What matters for crypto is whether the scandal accelerates — or complicates — Japan’s regulatory overhaul.

FSA Bill Changes the Rules

Japan’s Financial Services Agency submitted its landmark crypto reform bill to parliament this week, Asahi Shimbun reported. The legislation moves crypto from the Payment Services Act into the Financial Instruments and Exchange Act, reclassifying digital assets as financial instruments for the first time.

As BeInCrypto previously reported, the maximum prison term for unlicensed crypto sales would triple to 10 years, with fines rising from ¥3 million to ¥10 million. The SESC gains criminal investigation powers it has never held over crypto operators. The SANAE TOKEN case was explicitly cited in Nikkei’s reporting on the legislative push.

The bill would also void transactions with unregistered operators by default, making it easier for investors to seek refunds — a provision directly relevant to the SANAE TOKEN case.

The post Did Japan’s PM Actually Back the Memecoin Bearing Her Name? appeared first on BeInCrypto.

South Korea’s financial regulator has ordered all crypto exchanges to verify user asset balances every five minutes, following a massive overpayment incident that shook market confidence earlier this year.

One botched reward payout exposed systemic cracks across the entire industry.

What Triggered the Rules

In February, Bithumb accidentally sent 2,000 BTC per person instead of 2,000 Korean won ($1.40) during a promotional event. The error amounted to roughly $42 billion in misallocated crypto. The Financial Services Commission (FSC) launched emergency inspections across all five major Korean exchanges immediately after. What they found went far beyond a single human mistake.

Most exchanges were only reconciling their books once every 24 hours. Three had no automatic kill switch to halt trading when discrepancies appeared. Four lacked multi-step approval systems for high-risk manual transactions. Two exchanges hadn’t even separated their general accounts from high-risk transaction accounts — a basic safeguard.

What Exchanges Must Now Do

The FSC announced a three-pillar reform package on April 6. Exchanges must run automated balance checks every five minutes, with alerts and automatic trading halts triggered by major mismatches. Monthly external audits replace the previous quarterly schedule, and public disclosures must now include asset-by-asset blockchain holdings rather than a simple coverage ratio.

For manual, high-risk transactions such as event payouts, exchanges must use separate accounts, deploy validity-check systems that automatically reject mismatched inputs, and require cross-verification by a third party before execution.

The FSC will also require exchanges to appoint dedicated risk management officers and establish risk management committees — standards already expected of traditional financial firms. Compliance checks move from annual to twice-yearly, with results reported to regulators.

DAXA, the industry body, will complete self-regulatory amendments this month, with systems built out by May. Key provisions will feed into Korea’s forthcoming second-phase Digital Asset Act.

The post Every 5 Minutes: Korea’s New Rule for Crypto Exchanges appeared first on BeInCrypto.

Trump’s Iran Escalation Would Increase Death And Chaos Across The Middle East

‘I’d tell him I love him’

NYT Connections hints and answers for Tuesday, April 7 (game #1031)

-

NewsBeat4 days ago

NewsBeat4 days agoSteven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Business4 days ago

Business4 days agoNo Jackpot Winner and $194 Million Prize Rolls Over

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: Spanx – Corporette.com

-

Crypto World5 days ago

Crypto World5 days agoGold Price Prediction: Worst Month in 17 Years fo Save Haven Rock

-

Business1 day ago

Business1 day agoThree Gulf funds agree to back Paramount’s $81 billion takeover of Warner, WSJ reports

-

Crypto World7 days ago

Dems press CFTC, ethics board on prediction-market insider trades

-

Sports2 days ago

Sports2 days agoIndia men’s 4x400m and mixed 4x100m relay teams register big progress | Other Sports News

-

Business3 days ago

Business3 days agoExpert Picks for Every Need

-

Business5 days ago

Business5 days agoLogin and Checkout Issues Spark Merchant Frustration

-

Tech7 days ago

Tech7 days agoEE TV is using AI to help you find something to watch

-

Sports7 days ago

Sports7 days agoTallest college basketball player ever, standing at 7-foot-9, entering transfer portal

-

Tech7 days ago

Daily Deal: StackSkills Premium Annual Pass

-

Tech7 days ago

Tech7 days agoHow to back up your iPhone & iPad to your Mac before something goes wrong

-

Tech7 days ago

Tech7 days agoWhat Are The Biggest Limitations Of Supercomputers?

-

Crypto World6 days ago

Crypto World6 days agoBitcoin enters the public bond market as Moody’s gives a first-of-its-kind crypto deal a rating

-

Crypto World6 days ago

Bitcoin stalls below key resistance as technical signals skew bearish

-

Politics7 days ago

Politics7 days agoTransform Your Space with Stunning Small Works

-

Politics6 days ago

Politics6 days agoStarmer’s centre has collapsed, and the left was right all along

-

Business2 days ago

No Jackpot Winner, Prize to Climb to $231 Million

-

Fashion7 days ago

Fashion7 days agoZara Turns Up the Heat With New Swimwear

You must be logged in to post a comment Login