Crypto World

Standard Chartered Holds to $2T Stablecoin Call, Cuts T-bill Impact

Standard Chartered’s newest briefing sticks to a bullish view on stablecoins, arguing that the sector will swell to about $2 trillion in market capitalization by late 2028, even as near-term demand for U.S. Treasuries eases. The bank’s analysts, Geoffrey Kendrick and John Davies, contend that dollar-backed stablecoins such as Tether’s USDt (USDT)(CRYPTO: USDT) and Circle’s USDC (USDC)(CRYPTO: USDC) will remain the bedrock of a shift in reserve management that could lift Treasury bill demand toward the $2.2 trillion mark by 2028. The note comes despite a cooling in the overall crypto cycle that has kept the dollar-stablecoin market cap hovering near $300 billion in recent months.

In making the case, the analysts point to policy momentum in Washington that they say underpins the thesis. The GENIUS Act, signed into law in 2025, is cited as a potential catalyst for broader acceptance and clarity around stablecoins, which in turn could influence both institutional wallet allocations and sovereign appetite for short-duration Treasuries. The report argues that the structural shift remains intact even if the pace of near-term demand is tempered by market cycles.

“We see these issues as cyclical rather than structural, and we continue to expect stablecoin market cap to reach $2 trillion by end-2028,” the Standard Chartered note states, framing a longer-run reallocation of liquidity toward crypto-enabled reserves as a core driver of T-bill demand.

Stablecoins may drive Treasury to issue more bills despite lowered demand

Standard Chartered’s forecast envisions a substantial uplift in T-bill demand driven by stablecoins acting as reserve assets. The bank now sees stablecoins generating an additional $800 billion to $1 trillion in fresh T-bill demand by late 2028, a sizeable downgrade from the $1.6 trillion projected in April 2025, even after GENIUS Act provisions took effect. The fundamental idea is that as stablecoins grow as credible cash-equivalents, institutions and cash-rich entities will prefer Treasuries as collateral or reserve holdings, prompting a broader issuance program by the Treasury.

The piece underscores that the Treasury may respond to this reserve-driven demand by issuing more T-bills. It cites Treasury Secretary Scott Bessent’s remarks in early February, which framed the GENIUS Act as a potentially important financing tool for the U.S. government, aligning policy with the evolving liquidity landscape created by stablecoins. The quarterly refunding announcement on the same day highlighted “growing demand for Treasury bills from the private sector,” the bank notes, signaling a potential loop where rising demand for crypto-backed reserves could spur additional government debt supply.

“Stablecoin-related demand, in conjunction with the Fed’s recent decision to commence RMPs [reserve management purchases] and replace its maturing MBS [mortgage-backed securities] with T-bills, could arguably cause T-bills to become overly scarce.”

Beyond the stablecoin thesis, Standard Chartered has not abandoned itsBitcoin(BTC)(CRYPTO: BTC) outlook. While the bank previously carried a bullish longer-run target, it recently trimmed its price forecast for 2026 from $150,000 to $100,000, acknowledging that BTC could dip toward $50,000 before any meaningful recovery unfolds. The downgrade illustrates the bank’s approach to balancing aggressive longer-term premises with near-term macro uncertainties.

In tandem with these macro considerations, the bank’s researchers maintain that the stablecoin storyline remains a key driver of liquidity and risk sentiment in crypto markets. The broader takeaway is that the relationship between sovereign debt management, central-bank operations, and the crypto ecosystem is evolving in a way that could rewire how liquidity is allocated in the coming years, even as the sector continues to navigate cycles of volatility and regulatory scrutiny.

Source: Standard Chartered

Market context

The forecast arrives as a broader crypto environment continues to digest policy signals and investor appetite for digital assets. The GENIUS Act is a central thread in this narrative, offering a legislative framework that could reduce regulatory friction for stablecoins while clarifying their role in institutional reserve practices. At the same time, the Fed’s reserve management purchases and its ongoing balance-sheet adjustments—alongside a possible reweighting of Treasuries in private-sector liquidity pools—shape the backdrop against which stablecoins could influence T-bill issuance and market depth.

Why it matters

The projection matters because it links stablecoin growth to sovereign debt management and macro liquidity dynamics. If stablecoins become a routine, preferred form of reserve or collateral, banks, institutions, and non-bank financials may channel more liquidity into Treasuries, potentially altering demand curves for T-bills and influencing credit conditions across markets. For crypto users and builders, the interplay between regulatory clarity, stablecoin infrastructure, and central-bank liquidity programs could translate into a more robust on-ramp to digital-asset ecosystems and a longer horizon of institutional participation.

From an investor perspective, the narrative signals that stablecoins are not simply a payments convenience but a bridge between the crypto world and traditional finance. The possibility of more T-bill issuance to accommodate rising secure-lien demand could keep risk-free yields anchored while offering new channels for liquidity and collateral management. Yet the path remains contingent on how regulators implement policy, how successfully stablecoins maintain reserve health, and how swiftly the broader market absorbs shifts in risk sentiment.

What to watch next

- Details on GENIUS Act implementation and regulatory guidance as 2025–2026 unfolds.

- Updates from the Treasury’s refunding calendar and any reported private-sector demand signals.

- Federal Reserve communications about reserve management purchases and any shifts in MBS-to-T-bill reallocation.

- Progress in stablecoin reserve frameworks, including regulatory clarity on collateral and liquidity requirements (SEC developments).

Sources & verification

- Standard Chartered report outlining a $2 trillion stablecoin market by end-2028 and the projected impact on T-bill demand.

- References to the GENIUS Act and its role in shaping stablecoin policy.

- Treasury quarterly refunding announcements and statements on private-sector demand for T-bills.

- Federal Reserve actions related to reserve management purchases (RMPs).

- SEC discussions on stablecoin exemptions or haircuts for broker-dealers.

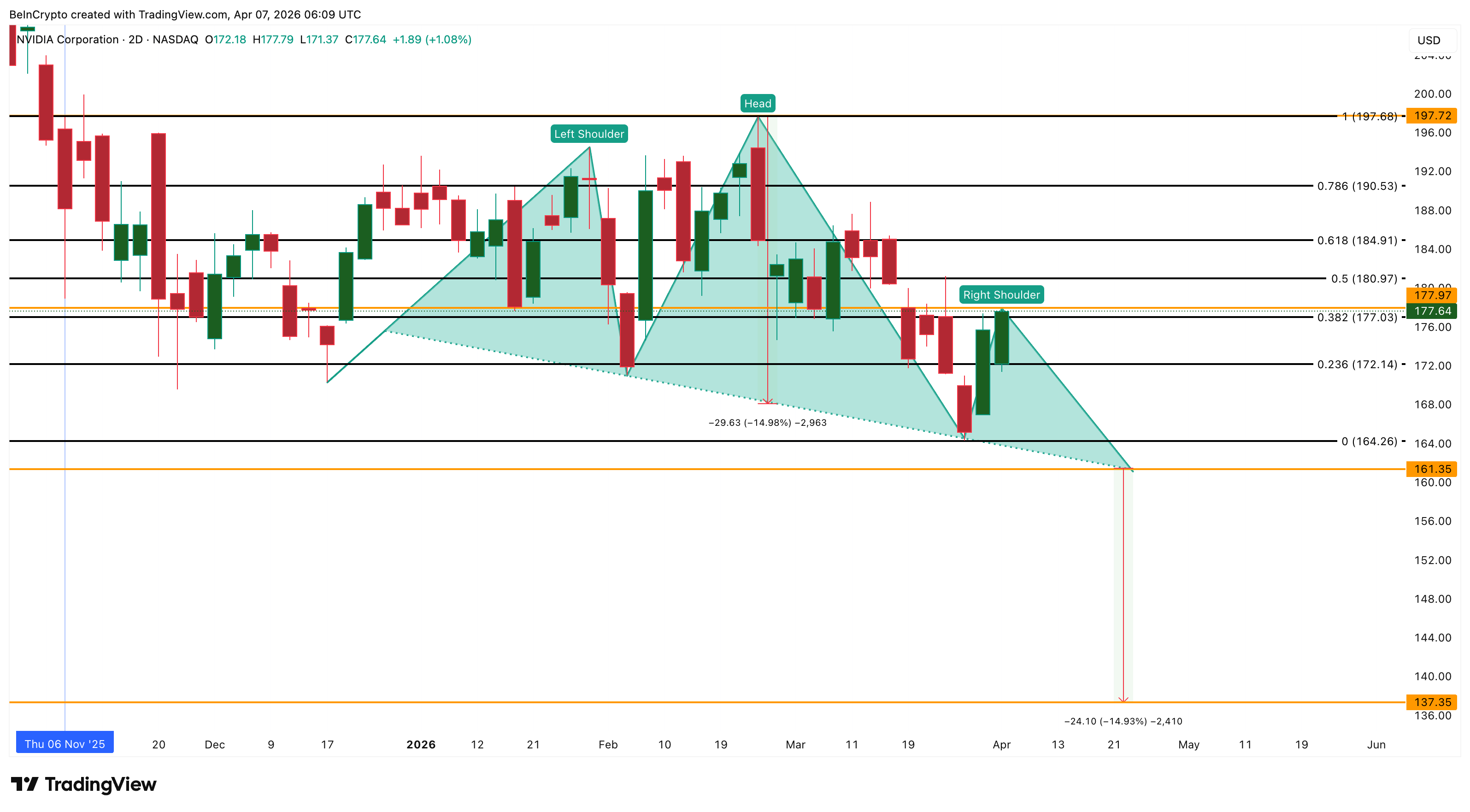

NVIDIA (NASDAQ: NVDA) stock price trades at $177.64 on the 2-day chart, up 5.31% over the past days but still down 6% year-to-date. April sits at a unique inflection for the stock. The Iran conflict could de-escalate within weeks, the FOMC meets on April 28-29 in what may be Jerome Powell’s final meeting as Chair, and pre-earnings positioning for the late May report begins building now.

The technical structure, options data, and institutional money flow each frame a different part of what April could deliver, and the causality between them narrows the range to two scenarios.

A Bearish Pattern With No Institutional Backing

The 2-day chart shows NVIDIA stock price trading inside a head and shoulders pattern. The head peaked at $197.72, a level reached on the last earnings day in late February. The right shoulder is currently building, and the pattern carries a 15% measured move if the neckline breaks.

Chaikin Money Flow (CMF), a proxy for institutional buying and selling pressure, reads -0.08. The indicator has stayed in negative territory for most of March and into April, confirming that big money has not backed the recent five-day bounce. CMF started trending upward around March 27 but has not crossed above the zero line. The last time it briefly turned positive was around the February 25 earnings release, and it quickly reversed.

Want more insights like this? Sign up for Editor Harsh Notariya’s Daily Newsletter here.

This tells a clear story. Institutional conviction has been limited to earnings events rather than the broader trend. Every bounce that happens while CMF stays negative risks building the right shoulder rather than breaking the pattern. The head at $197.72 is the invalidation level. Anything below it keeps the bearish structure alive.

The economic logic behind the negative CMF connects directly to the macro backdrop. Oil above $111 keeps inflation expectations elevated, which keeps the Fed on hold. Higher-for-longer rates compress multiples on growth stocks, including NVDA. A strengthening dollar adds further pressure on international revenue. These macro headwinds explain why institutional money has not committed despite the price bounce, and that reluctance is now visible in how options traders are positioning.

Options Traders Are Hedging More and Speculating Less

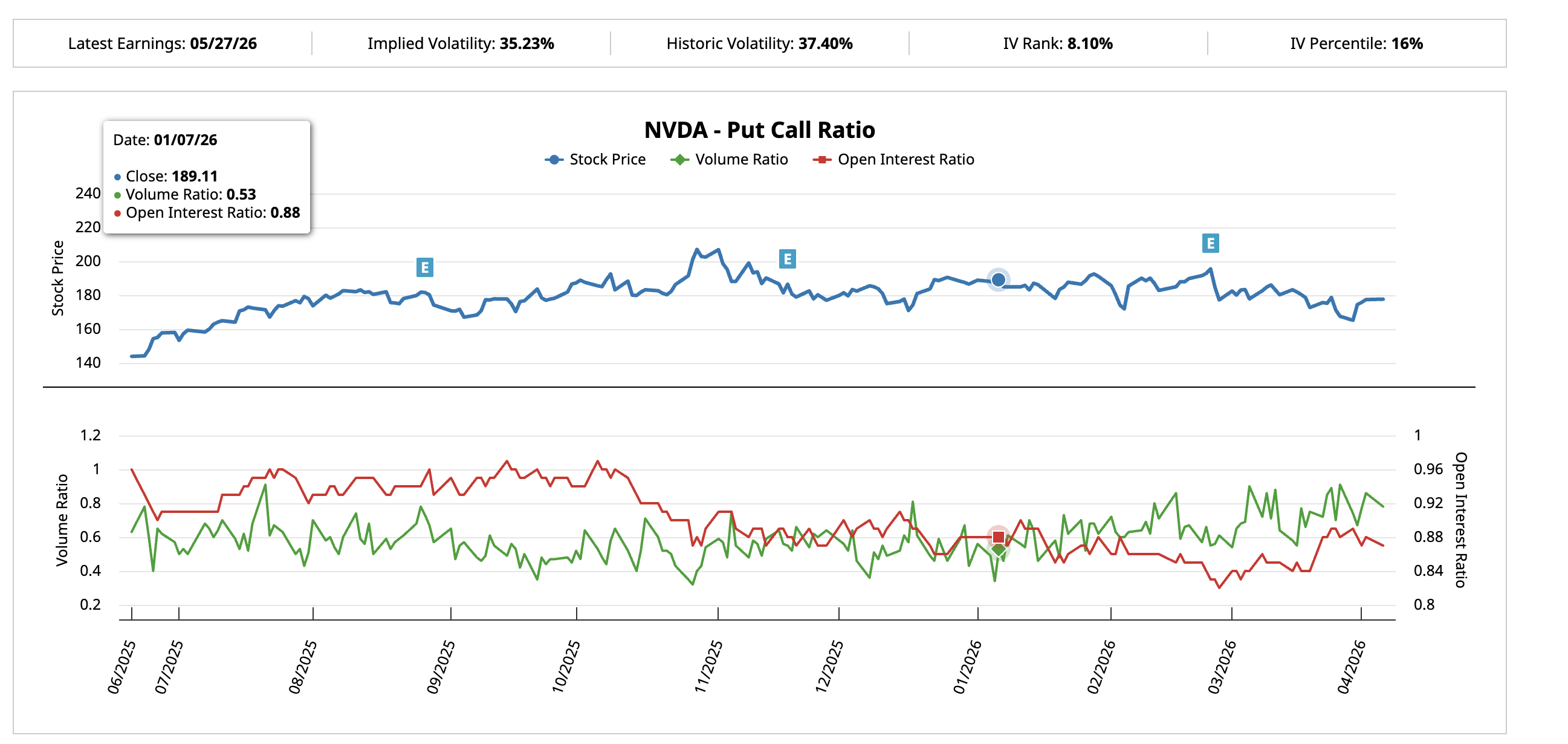

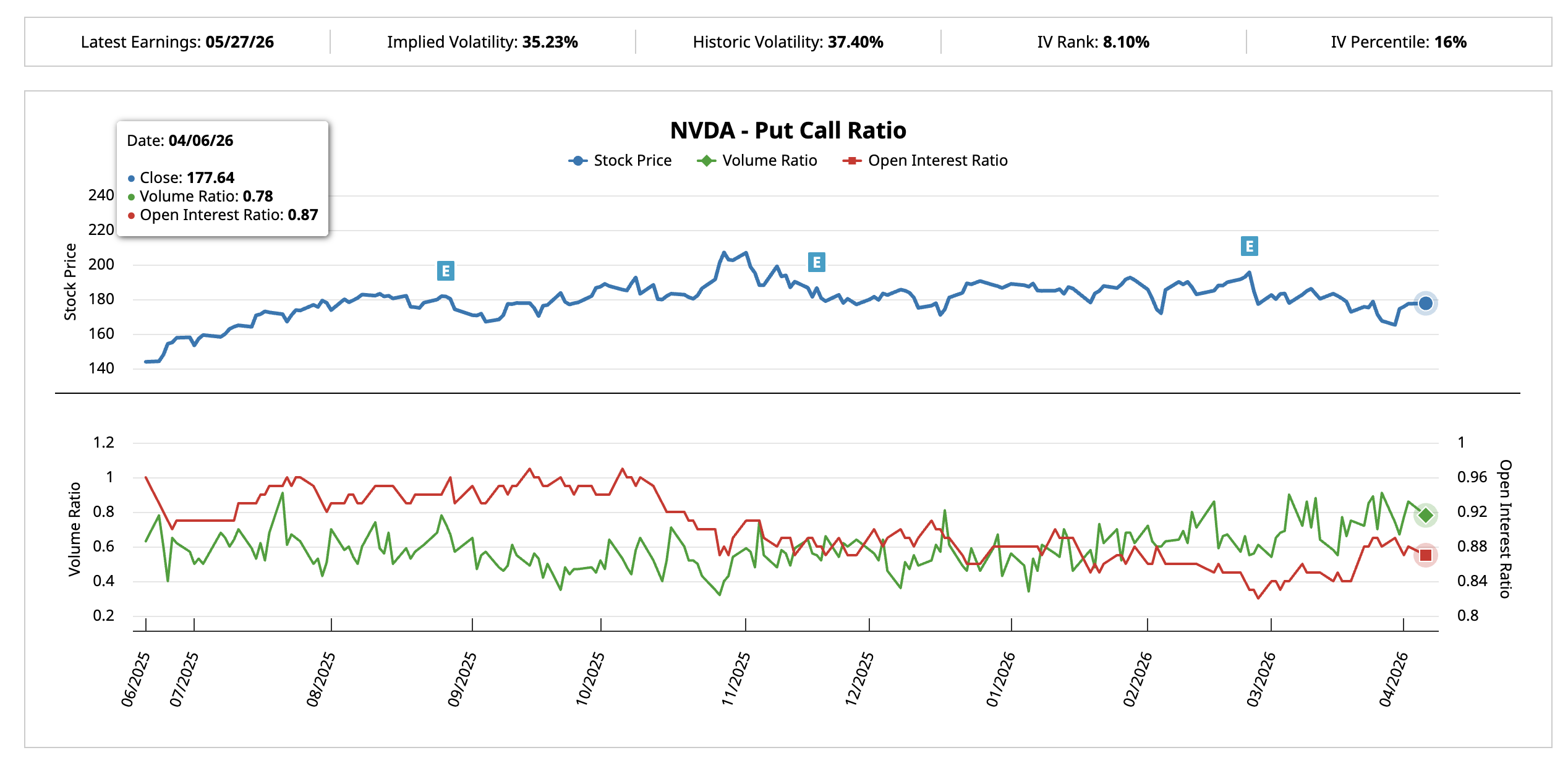

The put-call ratio data from Barchart shows a meaningful shift compared to the last pre-earnings window.

On January 7, with NVIDIA stock price at $189.11 and roughly seven weeks before the February 25 earnings, the put-call volume ratio stood at 0.53. Nearly twice as many calls as puts were trading, reflecting strong bullish conviction. The open interest ratio was 0.88.

By April 6, with a similar window before the late May earnings, the volume ratio has climbed to 0.78. The gap between call and put activity has narrowed significantly. The open interest ratio barely moved at 0.87, meaning structural long positions have held, but new bullish flow has slowed while defensive bets have grown.

The shift from 0.53 to 0.78 does not mean the market is outright bearish. It means the easy bullishness that preceded the last cycle is gone. Traders are hedging more and speculating less, which aligns with both the negative CMF reading.

The Implied Volatility (IV) Percentile, which measures where current options volatility sits relative to the past year’s range, reads just 16%. The IV Rank, a similar measure that tracks where IV stands between its 52-week high and low, sits at 8.10%.

When IV is this compressed, the market is complacent. Any surprise, whether Iran de-escalation pushing oil lower, a tariff policy shift, or an unexpected pre-earnings development, could trigger outsized moves because options have not priced in the possibility.

The combination of cautious put-call ratios and compressed IV creates a paradox. Traders are positioning more defensively, but the options market itself is not reflecting the magnitude of catalysts that could arrive in April. That disconnect means the price levels become the deciding factor for which scenario plays out.

NVIDIA Stock Price Levels That Define April

The 2-day chart with technical levels frames the month’s range.

NVIDIA stock price sits at $177.64, almost exactly at the key technical level ($177.03). The first upside hurdle is $184.91 at the 0.618 level, one of the strongest technical zones. A move above this would represent the first real test of the upper range and could push prices toward $190.53. The head at $197.72 is the level that invalidates the pattern entirely and shifts the structure bullish.

If Iran de-escalation arrives by late April and oil drops, that scenario gains traction. Falling energy prices would ease inflation fears, bring rate cut expectations forward, and lift growth stock valuations. The compressed IV means any such catalyst would be amplified because options have not priced it in.

On the downside, losing $172.14 at the 0.236 level would suggest the right shoulder has already peaked at $177.97. The neckline sits near $161.35. A confirmed break below the neckline activates the 15% measured move, projecting a decline toward $137.35.

That bearish path becomes more likely if the war extends, oil stays above $110, and the FOMC delivers hawkish language on April 28-29. In that environment, the already-cautious options positioning would accelerate into outright bearishness, and the institutional money that CMF shows has been absent would stay on the sidelines.

April is likely to be defined by which catalyst arrives first. De-escalation and falling oil favor a push toward $184 and $197. Continued conflict and a hawkish Fed favor a drift toward $161 and the neckline test. The put-call shift and low IV confirm the market has not decided yet, making this a month where the resolution could be sharp in either direction.

The post What to Expect From NVIDIA Stock Price in April 2026? appeared first on BeInCrypto.

Crypto World

Here is what Solana Foundation’s cryptic ‘Don’t waste time with crypto’ ad really means

The Solana Foundation is taking a deliberately contrarian approach to crypto marketing in San Francisco, rolling out a billboard campaign that reads: “Don’t waste time with crypto.”

At first glance, the message may seem a bit confusing as a crypto foundation is saying not to waste time with crypto. But according to the Solana Foundation, it is a bullish bet on the future of crypto that intersects with agentic AI.

Essentially, what this means is that rather than wasting your time executing transactions with crypto, which might be cumbersome and time-consuming, let your AI agents do the hard work.

The ad directs passersby to the x402 account on X, a nod to a growing push within the Solana ecosystem to position blockchain not as a consumer-facing product, but as invisible infrastructure for the next phase of the internet.

The message reflects a broader thesis the ecosystem has been advancing: that crypto’s future lies in powering an “agentic” internet, where artificial intelligence systems, not humans, initiate and execute economic activity.

Read more: Visa is ready for AI agents. So is Coinbase. They’re building very different internets

At the center of that vision is x402, a new type of payment system built for the internet. In simple terms, it lets apps, websites or AI tools automatically charge small amounts of money when they’re used, without requiring logins, subscriptions or human involvement. For example, an AI agent could request data from a service, instantly pay a small fee, and receive the result in a single seamless step. The idea is to make online payments as easy and automatic as loading a webpage — especially for very small transactions that traditional payment systems struggle to handle.

This model enables so-called “agentic payments,” often involving fractions of a cent, which are difficult to support on traditional financial rails due to high fees and latency. Solana is betting that its high throughput and low transaction costs make it a natural settlement layer for this emerging economy.

The billboard’s tongue-in-cheek directive encapsulates that shift. If the technology succeeds, the argument goes, users won’t need to think about crypto at all.

“Crypto and Solana are well on their way to being the default way AI pays,” a Solana Foundation spokesperson said, adding that agents will gravitate toward networks where “performance wins.”

Ethereum might be down by 3% today, but a structural shift inside one of the most-watched U.S. ETF products may be building a slow-burn case for recovery. The catalyst isn’t a Trump tweet or a Fed pivot. It’s staking yield, quietly compounding inside a regulated wrapper. Grayscale introduces Ethereum ETF staking delay.

In October 2025, Grayscale activated staking for ETHE, making it the first U.S. Ethereum ETP to distribute staking rewards directly to shareholders. Shares are currently priced at $16.98, with the fund posting a 3-month return of +107.87% and a 1-year return of +11.68%. That 3-month surge reflects a period when institutional appetite quietly accelerated way before most retail participants noticed.

When staking yield embedded in a regulated ETF structure, it creates a demand floor that pure spot exposure never had. ETF dynamics in 2026 have already reshaped Bitcoin’s price behavior, Ethereum may be next in line for the same institutional re-rating.

Discover: The best pre-launch token sales

Can Ethereum Price Hit $5,700 With This New Grayscale ETF Staking?

Ethereum’s current price action is compressed. Trading just above the $2,000 support zone, well below the $2,400 resistance band that capped multiple recovery attempts in Q1 2026. Volume has been underwhelming, a characteristic of a market waiting for a macro trigger.

The staking ETF development matters technically because it introduces a yield-bearing demand component. Institutional allocators who previously avoided ETH due to zero-yield exposure now have a credible on-ramp. Buyer-seller divergence data already shows accumulation signals at current levels, suggesting patient money is positioning ahead of any breakout.

ETH could reclaim $2,400 with ETF inflows accelerating on the staking yield narrative, and price targets $3,200, then $5,700 as the cycle matures in a move that would represent 180% jump from current levels.

But ETH could lso consolidates between $1,650 and $2,400 through Q2, with staking yield providing a slow but steady ETF demand floor. Price grinds higher, but the $5,700 target extends into late 2026. Or, a break below $1,500 on heavy volume would invalidate the accumulation thesis. That level represents critical long-term support; a close beneath it reopens the $1,200 range.

The staking ETF is a structural positive. It isn’t, by itself, a price ignition event. Patient positioning appears to be the play.

Discover: The best crypto to diversify your portfolio with

Maxi Doge Targets Early Mover Upside as Ethereum Tests Key Levels

Here’s the uncomfortable truth about Ethereum: even the bull case projects +180% as a multi-quarter grind. For traders who made real money in 2021, that timeline feels like watching paint dry.

Early-stage assets with compressed entry prices and community momentum have historically offered asymmetric upside during exactly these mid-cycle consolidation windows.

Maxi Doge ($MAXI) is a meme token built on Ethereum, currently in presale at $0.0002812, with $4,7 million raised for now. The project leans hard into trading culture, with holder-only trading competitions, leaderboard rewards, and a Maxi Fund treasury backing liquidity and partnerships. Staking is also live with a high 66% APY bonus for presale participants.

Two features stand out: the Holder-Only Trading Competitions create genuine competitive utility beyond speculative holding, and the meme-first marketing strategy has a track record of generating organic viral reach that paid campaigns simply can’t replicate.

Research Maxi Doge here before the next price increase.

The post Grayscale Ethereum ETF Staking Introduces Something Fresh: The Catalyst For $5,700? appeared first on Cryptonews.

BTC USD pulled back sharply to $68,000 Tuesday after topping $70,000 less than 24 hours earlier, as the Trump 8 PM deadline looming. The catalyst is as geopolitical as it gets, and the window to act may already be closing.

President Trump posted an extraordinary message to Truth Social Tuesday morning, warning:

“A whole civilization will die tonight, never to be brought back again. I don’t want that to happen, but it probably will.”

The statement, tied to his 8 PM ET deadline for Iran to reopen the Strait of Hormuz, detonated across risk assets instantly. Nasdaq 100 futures dropped 0.65%. WTI crude spiked 1.7% to $114.22 per barrel. Bitcoin shed nearly $2,000 in a matter of hours.

— Mario Nawfal (@MarioNawfal) April 7, 2026

BREAKING:

BREAKING:

'There are increasing fears within Trump’s current and former advisory circle that the President may consider ordering a NUCLEAR STRIKE on Iran’

Source: The Guardian https://t.co/Yn21aIAPZl pic.twitter.com/4KKv4zdO4m

Vice President Vance offered a partial reprieve, stating military objectives in the Iran conflict had been completed, tempering the worst of the selloff. The broader damage, though, was already done. Markets are pricing in genuine overnight risk, and Bitcoin is caught directly in the crossfire.

Discover: The best pre-launch token sales

BTC USD Under Heavy Pressure from Trump Decisions

BTC USD rejection at $70,000 is technically significant. That level has served as stiff overhead resistance across multiple sessions, and Monday’s brief breach now looks like a false breakout rather than a confirmed range expansion. Price is currently consolidating around $68,000, dropping close to 3% since last night.

The immediate support zone sits between $67,500 and $66,000. A clean hold here keeps the bullish structure intact. Lose it on a closing basis, and the next meaningful demand cluster doesn’t appear until the $65,000–$65,500 region, a level that aligns with prior consolidation from late March.

Volume context matters here. The pullback has been driven by macro fear rather than structural selling, which suggests the move could reverse quickly if tonight’s geopolitical outcome is less catastrophic than Trump’s language implies. Three scenarios dominate the tape right now:

Bitcoin’s correlation with risk assets during geopolitical shocks remains frustratingly tight; the “digital gold” narrative only seems to hold once the dust settles. Watch the 8 PM deadline closely and react to BTC USD movement.

— MSB Intel (@MSBIntel) April 7, 2026

BREAKING: Trump's 8 PM Tuesday deadline for Iran to reopen Strait of Hormuz.

BREAKING: Trump's 8 PM Tuesday deadline for Iran to reopen Strait of Hormuz.

Trump threatened bombing campaign against Iran's power plants and bridges if Hormuz not reopened by 8pm Eastern Time April 7. Iran rejected ceasefire, demands permanent war end and sanctions lift.

Discover: The best crypto to diversify your portfolio with

Bitcoin Hyper is Not Under Pressure

Here’s the uncomfortable truth for spot BTC holders: even in the bull case, Bitcoin’s upside from $68,000 to $74,000 represents roughly 9%, not nothing, but hardly the asymmetric return that first attracted most crypto investors to this space.

Macro-driven volatility compresses spot upside while amplifying downside risk. That calculus is pushing sophisticated allocators toward earlier-stage infrastructure plays with different return profiles.

Bitcoin Hyper ($HYPER) is currently raising in presale at just $0.0136, with $32 million already committed, a figure that signals serious demand for what the project is building.

The pitch is technically ambitious: the first-ever Bitcoin Layer 2 with Solana Virtual Machine (SVM) integration, delivering sub-second transaction finality while preserving Bitcoin’s underlying security model. That means fast smart contracts, low fees, and a decentralized canonical bridge for BTC transfers, breaking the three core limitations that have historically capped Bitcoin’s utility as a programmable asset.

High 36% APY staking bonus is live for presale participants. Research Bitcoin Hyper’s presale terms here and joing Hyper army today.

The post BTC USD In Shock Again: Trump Says Whole Civilization Will Die Tonight appeared first on Cryptonews.

Global crypto exchange-traded products drew $224 million in inflows last week after a $414 million outflow the week before, according to CoinShares.

The headline number looks like a recovery but a deeper look shows that the rebound is far narrower than it appears.

Switzerland alone accounted for roughly $157 million of the $224 million total, meaning 70% of global inflows came from a single country. Germany and the United States each contributed about $28 million. Canada added a much smaller $11 million.

The asset breakdown is similarly concentrated. XRP led all inflows at approximately $120 million, more than half the global total and its largest weekly intake since mid-December 2025.

Virtually none of the total from U.S. spot XRP ETFs. SoSoValue data shows the five U.S.-listed XRP spot ETFs recorded near-zero daily flows throughout the past two weeks, with total net assets sitting at $940 million across Canary, Bitwise, Franklin, 21Shares, and Grayscale products. The $120 million was almost entirely European and international ETP demand.

Bitcoin ETPs drew $107 million, but only $22 million came from U.S. spot ETFs, which remain in negative territory year-to-date. Strategy disclosed over the weekend that it bought 4,871 BTC for approximately $330 million in the same week, meaning a single company spent 15 times what the entire U.S. spot bitcoin ETF complex attracted.

ETFs absorbed approximately 50,000 BTC in March’s rolling 30-day window, the highest since October 2025, CoinDesk reported last week. But nearly all of the sustained institutional buying pressure is coming through two channels — spot ETFs and Strategy — and even the ETF channel is weakening on a weekly basis.

The broader ETP market, which includes leveraged products, short products, and altcoin funds across dozens of countries, is not confirming the “institutions are buying” narrative.

Ether products continued to bleed, posting $53 million in outflows after $222 million the prior week, bringing year-to-date outflows to $327 million. That stands in sharp contrast to Bitmine Immersion Technologies (BMNR), which bought 71,252 ETH last week in its largest single-week purchase since December 2025 and now holds 4.8 million tokens worth roughly $10 billion. ETH fund investors are leaving while the largest corporate ETH buyer on earth is accelerating.

CoinShares’ James Butterfill attributed the ether weakness partly to uncertainty around the CLARITY Act, the stablecoin legislation closely tied to Ethereum’s ecosystem.

The geographic concentration matters for reading where conviction actually sits. The Coinbase Premium Index, which tracks whether bitcoin trades at a premium or discount on the exchange most associated with US institutional flows, has been persistently negative since bitcoin’s all-time high above $126,000 in October 2025.

U.S. buyers are not stepping in at scale, and the ETP data confirms it. The $28 million in US inflows against $157 million from Switzerland suggests the marginal buyer right now is European, not American.

Split Capital, a digital asset hedge fund founded by investor Zaheer Ebtikar, is shutting down, with the founder joining Peter Thiel-backed stablecoin startup Plasma.

Ebtikar announced the news in an X post on Tuesday, saying Split Capital was profitable both in 2024 and 2025, and delivered over 100% in returns.

“We were a top performing fund by every mark,” Ebtikar claimed, adding that his decision to wind down the business was driven by a belief that the crypto market had shifted away from strategies that hedge funds are designed to capture.

“The hedge fund model did not make sense for crypto, in perpetuity,” he said.

Ebtikar’s decision came amid continued pressure on crypto hedge funds, which have reportedly faced more challenging market conditions since the 2022 market downturn.

Crypto industry no longer rewards traders chasing momentum, Ebtikar argues

Ebtikar described his early years in crypto as “PvP button-clicking,” where traders competed in fast-moving markets driven by momentum and narratives. But after nearly a decade, he said those conditions have changed.

“The industry no longer rewards traders chasing momentum, it has matured into a space where the only real question is ‘What does the future look like and where is the value?’” he said.

Ebtikar said that many investors, including critics, were ultimately right to question whether funds such as Split Capital were sustainable in a rapidly evolving market.

“As time went on, our conviction narrowed around a small number of founders and verticals I genuinely believed in,” Ebtikar said.

Betting on Plasma’s stablecoin vision

Ebtikar said his conviction in Plasma grew after working closely with its founding team throughout 2024 and 2025.

Plasma is focused on building infrastructure for stablecoin settlement and global financial access. The platform raised $24 million in February last year from investors such as Framework Ventures, Bitfinex, Peter Thiel and Tether CEO Paolo Ardoino.

Related: Standard Chartered says faster stablecoin turnover could curb demand

As chief strategy officer at Plasma, Ebtikar will work across partnerships, growth and go-to-market efforts, as well as engage with investors and policymakers ahead of the rollout of Plasma One and ongoing ecosystem expansion.

He framed the move as part of a larger belief that crypto is entering a new phase defined less by speculation and more by building global financial systems.

“The last dance of crypto’s old era and the hope and deep belief that our work at Plasma can get us to a new golden age for our space,” Ebtikar said.

The Open Network (TON) Foundation, a nonprofit organization supporting the development of TON Blockchain, is partnering with SCRYPT, Switzerland’s largest stablecoin infrastructure partner, to provide businesses with institutional-grade infrastructure to access USDT on TON Blockchain.

TON operates within one of the largest distribution networks in the world, reaching more than 1 billion users through its integration with Telegram. The network now supports over 50 million wallets and continues to see growing activity across payments, trading, and digital commerce.

TON Foundation has selected SCRYPT as its institutional infrastructure partner to meet the increasing demand of stablecoins as the settlement layer of choice for global payments, ecosystem distribution, and treasury operations, with USDT emerging as a high throughput, low cost rail for stablecoin payments. SCRYPT will provide execution, settlement, and fiat access in a move that helps TON Foundation further position TON Blockchain as a scalable alternative to existing settlement networks.

SCRYPT, the operating system for digital assets, enables banks, fintechs, payment providers, and corporate treasuries to access USDT on TON through a single, Swiss-licensed regulated platform. This includes near-instant cross-border settlement, fiat conversions, and fully compliant 24/7 on/off ramps. Combining deep liquidity, proprietary technology, and Swiss regulatory oversight, SCRYPT enables institutional clients to move, convert, and settle USDT flows on TON Blockchain at scale.

Nikola Plecas, VP of Payments at TON Foundation, commented:

“We’ve put payments innovation at the centre of our strategy for growth this year. We believe this is a key area in demonstrating how blockchain can power real-world financial infrastructure beyond tokenisation. [….]This partnership enables that next phase, bringing more and more institutions into the TON ecosystem and making the global movement of money ever more decentralised and seamless.”

Gabriel Titopoulos, MD, Markets & Trading at SCRYPT, added:

“Stablecoin rails are becoming the settlement layer for global payments. This partnership enables banks, payment operators, fintechs, and corporate treasuries to access stablecoins on TON with the trusted digital asset infrastructure partner, handling execution, settlement, custody and fiat conversions at institutional scale.”

About SCRYPT

The Operating System for Digital Assets.

SCRYPT is what institutions run on to trade, settle, store, and manage digital assets. Since 2019, SCRYPT has operated as the trusted crypto partner for firms launching or scaling their digital asset strategy.

By combining deep market access, crypto-native expertise, and proprietary infrastructure, SCRYPT provides the liquidity, full-stack infrastructure, and regulated framework that banks, asset managers, fintechs, and payment providers need to trade, store, and manage digital assets – all through a single point of access.

Built for Scale. Licensed to Deliver.

To learn more about SCRYPT, visit: www.scrypt.swiss

About TON

TON Foundation is a non-profit organisation accelerating the growth of TON Ecosystem by funding and supporting developers, creators, and businesses building on TON Blockchain. Founded in Switzerland in 2023, the Foundation brings together global expertise to advance protocol development, foster ecosystem growth, and drive adoption through grants, technical resources,

and strategic partnerships. While it advocates for TON’s mission, the Foundation does not control the network. TON is fully open-source, community-driven, and free from central control.

To learn more, visit www.ton.foundation

The post TON Partners with SCRYPT to Enable Institutional Access to Stablecoins appeared first on BeInCrypto.

Digital asset manager Grayscale backed accelerated efforts to make public blockchains quantum-resistant in a new research note arguing the technical solutions already exist but the harder challenge is getting decentralized communities to agree on implementing them.

“Public blockchains do not have CTOs; they are global communities governed by consensus,” wrote Zach Pandl, Grayscale’s head of research. “The potential threat to digital security from quantum therefore presents both a challenge and an opportunity.”

The note follows a week of intensive industry response to Google Quantum AI’s paper, which found that breaking bitcoin’s elliptic curve cryptography would require fewer than 500,000 physical qubits, roughly a 20-fold reduction from previous estimates, and could be executed in approximately nine minutes once the machine is primed.

CoinDesk’s analysis of the paper found that the attack gives an attacker a roughly 41% chance of stealing funds before a bitcoin transaction confirms.

Pandl highlighted four takeaways from the Google research that Grayscale found persuasive. Progress toward a cryptographically relevant quantum computer may come in “discrete jumps” rather than linearly, making timelines unpredictable.

The technical solutions, specifically post-quantum cryptography, are mature and already securing internet traffic and certain blockchain transactions. Quantum risk varies significantly across blockchains depending on their transaction model, consensus mechanism, and block time.

From a pure engineering standpoint, Pandl argued bitcoin has lower quantum risk than other chains because it uses a UTXO model, proof-of-work consensus, no native smart contracts, and certain address types that are not quantum-vulnerable if not reused after spending.

The harder question is what to do about the roughly 6.9 million BTC sitting in wallets where public keys are already permanently exposed on the blockchain, including an estimated 1 million believed to belong to pseudonymous creator Satoshi Nakamoto.

Binance co-founder Changpeng Zhao raised the same question last week, saying that if Satoshi’s coins move during a migration “it means he is still around, which is interesting to know,” and that if they don’t move “it might be better to lock or effectively burn those addresses.”

Grayscale frames the options similarly — burn them, do nothing, or deliberately slow their release by limiting the rate of spending from vulnerable addresses — but noted that the bitcoin community has a history of contentious debates over protocol changes, pointing to last year’s dispute around image data stored in blocks.

The contrast with Ethereum is worth noting.

CoinDesk reported last week that Google’s paper identified five separate attack vectors against Ethereum worth over $100 billion in combined exposure, spanning account keys, admin keys on stablecoins, smart contract code, consensus mechanisms, and data availability.

Ethereum Foundation researcher Justin Drake, who co-authored the Google paper, estimated at least a 10% chance of a quantum key recovery by 2032. The foundation has been staking aggressively, putting $93 million of ether into validators in a single day last week, but has not publicly addressed quantum migration timelines.

Former Biden economic advisers Ryan Cummings and Jared Bernstein would have you believe the decline in bitcoin’s price from its 2025 peak somehow vindicates their administration’s approach to cryptocurrency. A masterclass in selective memory, their February 26 New York Times opinion piece omits the most consequential fact about Biden-era crypto policy: it was not a reasoned regulatory framework.

The authors credit the Biden administration with “increasingly aggressive regulatory efforts to curb scams and fraud.” This framing is extraordinary, given what happened on their watch. FTX grew to enormous scale during the Biden administration. Sam Bankman-Fried was a top Democratic donor and met with senior administration officials (including then-Securities and Exchange Commission Chair Gary Gensler) while running what became one of the largest financial frauds in history.

The administration’s strategy of regulation-by-enforcement, rather than establishing clear rules, had a perverse effect: legitimate, compliance-minded companies were driven offshore or out of business, consumers were harmed, and American innovation was stifled. Meanwhile, bad actors like Bankman-Fried (who knew how to play political games) thrived in the confusion. When you refuse to write clear rules, the only people who benefit are those who never intended to follow them.

The authors conveniently ignore one of the most troubling episodes of the Biden era: “Operation Choke Point 2.0.” Under pressure from federal regulators, banks systematically debanked lawful crypto businesses, cutting them off from the financial system without due process, formal rulemaking, or legislative authority. The debanking campaign swept up ordinary individuals and small businesses who had turned to crypto because the traditional banking system had long underserved them. The Biden administration’s approach cut consumers off from tools they were using to participate in the financial system, without putting a single policy through the democratic process of notice-and-comment rulemaking.

The authors dismiss crypto as a “painfully slow and expensive database” with “almost no practical use.” They acknowledge in passing that crypto is used to wire money

internationally, but wave this away as though enabling fast, low-cost cross-border remittances for millions of people is a trivial achievement.

It is not. Global remittance fees average nearly 6.5%, costing migrant workers and their families billions of dollars each year. Stablecoins running on blockchain networks can execute the same transfers in minutes for a fraction of the cost. This is an immediate, material financial improvement for families in developing countries. The Biden economists sat in “dozens of meetings” and apparently came away unimpressed. One wonders whether they spoke to any of the people these tools serve.

Beyond remittances, blockchain technology underpins a rapidly growing ecosystem of financial applications. Fidelity, JPMorgan, BlackRock, BNY Mellon, Morgan Stanley, Visa, Mastercard, Meta, Stripe, Block Inc. and Franklin Templeton are actively building on blockchain infrastructure. The Biden economists’ claim that no “giant tech firms” are using this technology is flatly wrong.

The op-ed’s news hook is bitcoin’s price decline. Using short-term price movements to condemn an entire asset class is analytically unserious. Amazon’s stock fell 94 percent from its peak during the dotcom bust. By the Cummings-Bernstein standard, it should have been written off as “fundamentally worthless.” Volatility is a feature of nascent markets, not proof of worthlessness.

Moreover, it labels the Bitcoin network as “slow.” What it lacks in speed it makes up for in security – a quality that should be of the utmost importance to regulators. Outsiders or intermediaries cannot veto or reverse transactions between peers, unilaterally confiscate user funds, or tamper with its distributed ledger. That’s why it’s used worldwide in areas where regular citizens are targeted by their governments. Meanwhile, other blockchains enable payments at breakneck speed.

The authors repeatedly invoke the straw man of a taxpayer-funded bailout of the crypto industry. No serious policymaker (or crypto participant) has proposed anything of the sort. The stablecoin legislation Cummings and Bernstein reference creates fully reserved payment instruments that are overcollateralized with the most liquid government bonds on Earth. The Trump administration’s bitcoin reserve proposal involves no new taxpayer expenditure.

Meanwhile, when Silicon Valley Bank collapsed in 2023, the Biden administration authorized extraordinary measures to guarantee all deposits. Their concern about moral hazard was seemingly highly selective.

The op-ed devotes considerable space to crypto industry political donations, implying corruption. The suggestion that an industry advocating for favorable regulation through political participation is inherently corrupt would indict virtually every sector of the American economy. Denied a fair hearing by regulators, the crypto industry turned to the political process as a last resort – a cornerstone of American democracy. If political spending is problematic, the authors might start by examining their own side of the aisle during the Biden Administration, when Bankman-Fried overwhelmingly gave to Democrats.

The Biden administration had a historic opportunity to establish the United States as the global leader in digital asset regulation: to write clear, fair rules that would protect consumers while allowing innovation to flourish on American soil. Instead, it chose to weaponize the banking system against a legal industry, creating a lose-lose-lose for innovation, consumer protection and the U.S. crypto ecosystem.

Cummings and Bernstein write that crypto’s boosters “have run out of excuses.” On the contrary, it is the Biden administration’s crypto haters who owe the public an explanation.

Americans reported $11.4 billion in losses tied to cryptocurrency scams last year, 22% more than in 2024, highlighting the growing scale of digital asset fraud, an FBI report revealed Tuesday.

“Cryptocurrency investment scams are sophisticated long-term scams using psychological manipulation, the appearance of legitimacy, and exploitation of cryptocurrencies to deceive victims into investing large sums of money,” the report said.

The report also said that most crypto scams are perpetrated by organized criminal enterprises based in Southeast Asia that exploit victims of human trafficking as forced labor to run the operations.

Crypto analytics firm Chainalysis released a report in January revealing that as much as $17 billion in crypto was lost worldwide to scams and frauds in 2025. Impersonation, crypto exchange impostors and AI-generated scams against individuals were gradually surpassing losses to cyber-attacks as the leading methods criminals were using to steal digital assets, according to the Crypto Crime Report.

The FBI noted in its report that the number of victims increased significantly. In 2025, there were 181,565 complaints involving cryptocurrency, a 21% increase. The average damage per case was $62,604, highlighting how victims are often drawn into schemes that extract substantial amounts rather than small sums, the bureau said.

Losses are also heavily concentrated. Nearly 18,600 complainants each lost more than $100,000, suggesting many victims are losing life-changing amounts, including savings and retirement funds.

More broadly, crypto scams now sit at the center of a wider surge in online fraud. Americans filed more than 1 million cybercrime complaints in 2025, with losses exceeding $20.8 billion. Fraud and scams accounted for the overwhelming majority of those losses, reflecting what the FBI describes as a rapidly evolving threat landscape.

Appeal as Bury man goes missing in the Radcliffe area

What to Expect From NVIDIA Stock Price in April 2026?

Peaky Blinders Cast: Jamie Bell And Charlie Heaton To Lead New Series

-

NewsBeat5 days ago

NewsBeat5 days agoSteven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Business5 days ago

Business5 days agoNo Jackpot Winner and $194 Million Prize Rolls Over

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: Spanx – Corporette.com

-

Crypto World6 days ago

Crypto World6 days agoGold Price Prediction: Worst Month in 17 Years fo Save Haven Rock

-

Business2 days ago

Business2 days agoThree Gulf funds agree to back Paramount’s $81 billion takeover of Warner, WSJ reports

-

Business3 days ago

Business3 days agoExpert Picks for Every Need

-

Sports3 days ago

Sports3 days agoIndia men’s 4x400m and mixed 4x100m relay teams register big progress | Other Sports News

-

Business6 days ago

Business6 days agoLogin and Checkout Issues Spark Merchant Frustration

-

Crypto World7 days ago

Crypto World7 days agoBitcoin enters the public bond market as Moody’s gives a first-of-its-kind crypto deal a rating

-

Crypto World7 days ago

Bitcoin stalls below key resistance as technical signals skew bearish

-

Tech5 days ago

Tech5 days agoCommonwealth Fusion Systems leans on magnets for near-term revenue

-

Business2 days ago

No Jackpot Winner, Prize to Climb to $231 Million

-

Politics7 days ago

Politics7 days agoStarmer’s centre has collapsed, and the left was right all along

-

Crypto World6 days ago

Crypto World6 days agoRipple rolls out enterprise crypto treasury platform for corporates

-

Fashion1 day ago

Fashion1 day agoMassimo Dutti Offers Inspiration for Your Summer Mood Board

-

Crypto World7 days ago

AI Memory Rout Wipes 9% Off Nvidia Stock: Chart Says More Pain Ahead

-

Crypto World6 days ago

Crypto World6 days agoWhy It’s Partnering, Not Issuing

-

Sports7 days ago

Sports7 days agoHow to teach yourself the perfect impact position with every club

-

Tech7 days ago

Tech7 days agoSolo Leveling: Ranking All Sung Jinwoo Shadows by Power

-

Sports6 days ago

Tom Pelissero Drives the Final Nail in the Coffin

You must be logged in to post a comment Login