Crypto World

Strategy Faces Legal Storm As Mstr Falls Deeper With Bitcoin Rout

Strategy faces new legal pressure after Rosen Law Firm opened a securities investigation into the Bitcoin treasury company this week. The review follows a steep MSTR selloff and a deeper Bitcoin decline across the wider crypto market and related shares. Together, the events place Michael Saylor’s firm under legal, market, and balance sheet pressure during a volatile trading week.

Strategy Faces Securities Investigation

Rosen Law Firm said it began an investigation into potential securities claims against Strategy and related securities. The firm linked the review to allegations of misleading business information shared with market participants during recent disclosures. It said affected shareholders may seek compensation through a contingency fee arrangement if claims move forward in court.

The firm also said it is preparing a class action to recover possible market losses through the planned lawsuit. Therefore, the legal process could add another challenge for Strategy and its securities program during a weak market. The company already faces pressure because its business model depends heavily on Bitcoin prices, capital markets, and equity sentiment.

The investigation comes after Peter Schiff criticized Saylor’s Bitcoin-backed securities push in recent public comments as Bitcoin prices weakened. Schiff argued that STRC buyers could bring claims tied to promotional statements and offering materials for the security. However, that argument remains separate from Rosen Law Firm’s planned legal action and any future court filing.

Mstr Stock Slides To New Lows

MSTR fell to a new low near $86 after breaking below $100 earlier this week. TradingView data showed the stock dropped more than 5% on the day during regular trading as pressure accelerated. The stock also lost about 23% across the past week as sellers controlled momentum.

The decline reflects heavy selling pressure across crypto-linked equities and Bitcoin treasury names during the current session. Moreover, MSTR often trades as a leveraged proxy for Bitcoin exposure in public markets during volatile trading. That link strengthens during rallies, but it also magnifies losses during sharp selloffs as market risk rises.

Market commentator Zerohedge pointed to heavy put buying across the latest trading session as prices fell today. That options activity added pressure as traders positioned for more downside in the stock during the session. Meanwhile, Bitcoin also weakened after PCE inflation reached 4.1%, the highest level since 2023.

Bitcoin Drop Tests Strategy Treasury Model

Bitcoin’s drop below $60,000 deepened concern over Strategy’s treasury-heavy structure and balance sheet risk. The company holds a large Bitcoin reserve on its balance sheet, so BTC price moves affect sentiment. As a result, every major Bitcoin selloff can weigh on MSTR shares and financing conditions.

Strategy reportedly carries an unrealized Bitcoin loss of more than $13.6 billion after the latest crash. That figure reflects current market prices rather than completed asset sales by the company. Still, it raises questions about leverage, liquidity, and future capital decisions if market stress continues.

Schiff has suggested that Strategy may sell Bitcoin to fund stock buybacks if pressure increases. However, Strategy has not announced any plan to sell its Bitcoin reserves despite the market pressure. Saylor has instead said current reserves exceed debt by over $40 billion, unlike the 2022 downturn.

SpaceX (SPCX) stock is sliding toward a make-or-break level as a selloff drags it more than 30% below its June peak, with the speculative heat that powered its record debut burning off fast.

Two weeks after its $75 billion IPO, the stock has round-tripped from euphoria to fragility. A fresh Starlink launch could not lift it, and cooling hype, weak space peers, and short-heavy positioning now point lower.

Hype Has Burned Out of the SpaceX Selloff

The SpaceX stock selloff has a clear tell, the hype is gone. A proprietary composite Hype Score, which blends momentum, volume intensity, volatility, and overbought readings into a 0 to 100 gauge of speculative intensity, has fallen to 18 and reads as cooling.

That marks a sharp reset from the debut. The SpaceX IPO share performance has flipped from a peak near $228 to slightly $150, at press time.

Want more insights like this? Sign up for Editor Harsh Notariya’s Daily Newsletter here.

A Falcon 9 Starlink launch from Vandenberg on June 25 did nothing for the tape yet, a sign the speculative bid has left. However, once the market opens it would be interesting to see if the Spacex stock price today reacts to the Starlink launch.

The same apathy shows up in volume as the decline grinds on. Buying and selling have both faded since June 23, leaving the stock range-bound for roughly 48 hours.

Underneath that quiet tape, money flow is split. Chaikin Money Flow (CMF), a proxy for buying and selling pressure, sits at a mild positive 0.10, yet price still trades below its volume-weighted average price (VWAP).

That mix matters because trading under VWAP means the average buyer since launch is now underwater. With even a rocket launch failing to lift it, the next clue is what SPCX actually moves with.

SPCX Trades Like a Space Stock, Not a Musk Stock

What SPCX moves with answers a defining question for the stock. Over 15-minute returns, it correlates 0.46 with space sector stocks like AST SpaceMobile (ASTS) and Rocket Lab (RKLB), but only 0.23 with Tesla (TSLA).

That gap makes the read clear. SPCX is trading on space-sector dynamics, not the Musk founder premium. That distinction matters because the sector is weak. Rocket Lab sits down roughly 44% month-on-month, and AST SpaceMobile has slid 45% in the same duration after a Q1 revenue miss.

SpaceX itself deepened that weakness, pulling capital out of smaller names and back into the giant on its debut. If a soft sector is setting the direction, positioning data shows who is leaning hardest into the move.

Smart Money Is Short, but Options Hold the Real Lever

Leaning hardest into the downside is the smart money. On Nansen data for the Hyperliquid perpetual that tracks SPCX, smart traders, whales and public figures are all net short, a rare unanimous stance.

That stance runs deep. Whales alone sit net short about $21.8 million, while the perp saw a net $140.6 million of selling over seven days, and the whale holder count fell about 24% in 10 days, which suggests distribution.

That positioning is a warning, not a trigger. The perpetual is oracle-priced and tracks the stock, so it reflects smart money positioning and sentiment but cannot by itself move the underlying.

What can move it is the options market, through dealer hedging. The debut set a single-stock record near 1.6 million contracts and sparked gamma squeeze talk toward $400, before at-the-money implied volatility fell from about 169% to the mid-80s.

That cooling has shifted the structure. The debut frenzy concentrated in short-dated calls struck at $210 to $250, well above the roughly $200 stock at the time, so with price now far below those strikes, dealer hedging can amplify declines rather than cushion them, just as Fidelity’s 15-day flipping penalty lapses around June 27 and frees up IPO supply.

SpaceX Stock Price Levels to Watch

It all comes down to one level. The SpaceX stock price today is holding above $148, the 0.786 Fibonacci level.

Hold it, and the range stays intact. Lose it on an hourly close, and the stock falls into a danger zone, opening the 1.0 retracement at $136 near the IPO price, with the 1.618 extension at $103 below.

Above it, buyers have work to do. They need to reclaim the 0.618 level at $157 to ease pressure, then $163 and $169. Even then, thin volume is the catch. A low-volume break can reverse fast, so SPCX support levels only carry weight on a closing basis.

The $148 line is make-or-break, separating a recoverable dip from a slide back toward the $136 IPO price and beyond.

The post SpaceX Stock Shrugs Off a Starlink Launch as $148 Becomes Make-or-Break appeared first on BeInCrypto.

Jeremy Grantham, the GMO co-founder known for calling past market bubbles, warned that an AI bubble has pushed US stocks to their most expensive levels in American history and could set up a decline of as much as 70%.

The veteran strategist made the remarks on CNBC, and his core advice was blunt. He urged investors to step away from US equities and look abroad.

An AI Bubble at Record Valuations

Grantham said the market’s price-to-earnings ratio has averaged more than 60% higher since 2010 than over the prior century. He ties that premium to years of cheap money. He does not dispute that AI is transformative. Instead, he says near-universal faith in the technology has fueled dangerous overinvestment, echoing growing AI bubble fears across Wall Street.

His bubble model holds that every prior speculative extreme eventually reverts to trend. A retreat toward those norms, he says, points to a drop closer to 70% than 50% in the biggest winners. The timing, he conceded, could land anywhere from two weeks to two years.

Grantham called the dot-com peak in 2000 and warned of a US housing bubble in 2007. That record carries weight, though his 2021 epic-bubble warning proved early as stocks climbed before stumbling in 2022. He is not alone now, as investor Ray Dalio has flagged similar liquidity risks.

Why Crypto Investors Are Watching

A 70% unwind would not stay inside the stock market. Bitcoin (BTC) now trades like a tech stock, so a deep risk-off move tends to hit crypto first and hardest.

The strain already shows. US spot Bitcoin ETFs posted a record 30-day outflow of $6.35 billion through mid-June, according to Galaxy Research.

Bitcoin was trading near $59,663 during the pullback. Grantham, meanwhile, dismisses crypto, repeating his view that the token is worthless and headed toward zero.

His prescription favors non-US stocks, bonds, and precious metals over expensive American names. Not everyone shares the alarm.

Bulls note that today’s AI leaders earn real profits, unlike many dot-com-era firms. Federal Reserve Chair Jerome Powell has called AI spending real economic activity, not pure speculation.

“I won’t go into particular names, but they actually have earnings… These companies actually have business models and profits and that kind of thing. So it’s really a different thing [from the dot-com era],” he said.

Whether Grantham proves early or right, his record means few will dismiss the warning outright.

For crypto holders, the takeaway is that Bitcoin’s fate now rides largely on how long the AI trade holds. The coming round of AI earnings will test how much of the optimism is justified.

The post Investor Who Predicted 2008 Bubble Says Sell US Stocks Before 70% Drop appeared first on BeInCrypto.

TLDR

- Proof launched x401, an open protocol that verifies the human authority behind AI agent actions online.

- x401 pairs with x402 to cover the two core questions in agentic transactions: identity and payment.

- Proof Digital ID uses zero-knowledge proofs, letting users verify claims without exposing full identity.

- Proof will submit x401 to the FIDO Alliance’s agentic authentication standards workgroup for adoption.

Proof, an identity authorization company, has launched x401, an open protocol designed to verify the human authority behind AI agents.

As agents increasingly handle payments, contracts, and content publishing, the missing piece has been proof of who authorized them.

The x401 protocol addresses that gap directly, giving any website or API a standard way to request and verify identity credentials before permitting agent actions.

x401 Builds a Trust Layer for the Agentic Economy

The x401 protocol works by allowing services to request specific identity claims from an agent. These claims can include verified identity, age, organizational affiliation, or signing authority.

The agent then presents a compatible credential, and the service verifies the issuer, claim scope, and action before proceeding. This two-step process binds identity to authorization in a single verifiable proof.

Proof founder and CEO Pat Kinsel explained the broader shift driving the protocol’s creation. “AI is making actions and content effortless to generate,” Kinsel said.

“Trust will come from knowing who stands behind them.” He added that x401 gives every service a common way to ask for proof, while Proof Digital ID gives people and organizations a high-assurance way to answer.

The protocol is issuer-neutral by design. Any conforming issuer can deliver x401-compatible credentials, and every service decides independently which claims, issuers, and assurance levels it will accept. This approach avoids locking the internet into a single identity provider model.

Proof plans to submit x401 to the FIDO Alliance’s agentic authentication standards workgroup for broader industry adoption.

Proof’s Digital ID Delivers the First Live x401 Implementation

Proof is also releasing its own Digital ID product, the first live implementation capable of satisfying an x401 challenge.

It is built on Verifiable Credentials and supports the OID4VC Issuance and Presentation standard inline. Users can verify their identity to an IAL2 standard and re-authenticate with biometrics at any point.

Circle, one of the protocol’s co-endorsers, connected x401 to the existing x402 payment standard. Circle VP of Product Gagan Mac stated that “x402 answers how an agent pays, x401 answers who it is.”

Mac noted those are the first two questions any agentic transaction must clear, and both now have open standards.

The platform uses selective disclosure and zero-knowledge proofs. This means a person can prove nationality, age threshold, or organizational authority without exposing their full identity record. Developers request the identity claim, and Proof handles enrollment and verification behind the scenes.

Proof’s Digital ID also supports transaction signing. The API cryptographically binds a verified identity to payments, authorizations, or any signed payload.

These records serve as verifiable evidence of who authorized what, which many regulated industries now require. Full documentation is available at x401.id, with developer resources at dev.proof.com.

Crypto World

Michael Saylor’s Strategy Enters a Dangerous Feedback Loop as STRC Cracks and Bitcoin Falls

TLDR:

- Strategy’s annual STRC dividend bill surged from $300M in January to roughly $1.2B today.

- Cash reserves have dropped 38% since early 2026, cutting dividend runway to just ten months.

- Strategy sold Bitcoin directly for the first time, exposing limits on its two core funding tools.

- Outstanding STRC obligations near $10B rank above MSTR shares in repayment priority order.

Strategy feedback loop risks are drawing attention as Michael Saylor’s Bitcoin treasury firm shows signs of structural strain.

The preferred stock instrument STRC was engineered to trade near $100, with Bitcoin purchases pausing automatically when it falls below that level.

That mechanism, once seen as a safeguard, has begun cracking under the weight of rising dividend obligations, shrinking cash reserves, and a declining Bitcoin price.

The Mechanism That Was Supposed to Hold Is Breaking Down

STRC’s design rested on a simple premise: keep the stock near $100, and the entire system stays balanced. Above that level, Strategy buys Bitcoin.

Below it, the company pauses purchases and rebuilds cash instead. For months, that framework held. Then May arrived, and the cushion disappeared.

Strategy spent $1.5 billion in cash to repurchase convertible notes due in 2029. That cash was the reserve investors relied on to trust that STRC’s dividend payments would continue. Once it was gone, confidence in the preferred stock began to slip, and the numbers moved quickly after that.

The annual dividend bill jumped from roughly $300 million in January to approximately $1.2 billion today. Cash reserves have fallen 38% since the start of 2026.

Dividend coverage, which once offered nearly three years of runway, has now compressed to around ten months.

Faced with that gap, Strategy took a step it had never taken before. It sold Bitcoin directly to refill cash. The sale was small, but it still moved Bitcoin’s price.

That single test revealed something the market had not fully confronted: Strategy cannot sell meaningful amounts of Bitcoin without damaging the very asset its entire model depends on.

Once the Loop Starts, Every Move Makes It Worse

@BullTheoryio captured the bind directly: “STRC trading below $100 forces Strategy to raise the dividend yield to pull it back toward par. A higher yield means a bigger annual cash bill. That bigger bill forces more selling of MSTR or Bitcoin to cover it.”

That selling then pushes both MSTR and Bitcoin lower. Lower prices drive STRC further from its $100 peg. A wider gap demands an even higher yield to attract investors back. The cycle then repeats, each rotation tightening the pressure further than the last.

What makes this especially consequential is the repayment structure sitting underneath it all. STRC is preferred stock, which ranks above MSTR in priority.

If Strategy ever had to unwind STRC entirely, preferred holders get repaid in full before MSTR shareholders see a single dollar. Outstanding STRC obligations stand at roughly $10 billion.

As of now, MSTR has fallen below $100 for the first time since March 2024, Bitcoin has dropped below $60,000, and Strategy’s stock sale program has been paused.

Analysts estimate the company needs approximately $2.4 billion in reserves just to restore 24 months of dividend coverage.

The market is not pricing in an immediate collapse. It is pricing in a company whose two main funding tools are both constrained at the same time.

Spain’s markets regulator has drawn a hard line on the timing of the EU’s Markets in Crypto-Assets (MiCA) licensing requirements, signaling that crypto firms which have not secured authorization by the deadline will not receive extensions.

According to a Friday Reuters report, the chair of Spain’s National Securities Market Commission (CNMV), Carlos San Basilio, said there will be “no exceptions or extensions” to the July 1 MiCA deadline for companies that have not received approval to operate in European Union member states. The warning is aimed at major exchanges including Binance.

Key takeaways

- Spain’s CNMV chair says MiCA’s July 1 deadline will not be extended for unlicensed crypto firms.

- Reuters reports that Binance had not received EU regulator approval as of Friday, after its Greece license application was withdrawn.

- If approval is not granted soon, Binance may need to stop onboarding new EU users and restrict services for EU accounts from July 1.

- Other exchanges have reportedly secured last-minute MiCA authorizations, potentially reducing but not eliminating market disruption.

MiCA deadline without waivers

MiCA’s phased implementation has been a central question for Europe’s crypto industry: whether firms would be given additional time to meet licensing conditions if regulators required extra steps or review. Reuters’ report indicates Spain’s position is unequivocal.

San Basilio said the key concern is how the end of the transitional period will unfold and how regulated firms and regulators will manage the “adaptation to the new environment.” Reuters adds that the CNMV chair stated the agency is in contact with organizations that have not been granted a licence.

What happens if Binance isn’t licensed

Binance’s EU status has been under scrutiny as MiCA approaches its effective dates. Reuters reported that Binance’s operations in the EU are expected to be scaled back after the exchange withdrew its application with Greece’s Hellenic Capital Market Commission and had not received approval from any other authority as of Friday.

Under MiCA-related service rules described in earlier coverage, failure to secure authorization could force changes starting July 1, including halting the onboarding of new EU-based users and limiting certain services for EU-based accounts. The scale of the potential impact is amplified by Binance’s large user base in Europe.

Reuters’ framing suggests the immediate issue is operational continuity for customers and liquidity providers, rather than broader regulatory uncertainty alone. Even if existing users retain some access for a limited time, onboarding restrictions and service limitations can still affect trading flows and compliance processes.

Europe’s exchange scramble: approvals for some, uncertainty for others

While the CNMV’s comments emphasize no extensions, Reuters also notes that other crypto exchanges have secured late approvals under MiCA. That contrast matters for investors and traders because it implies the market may not adjust uniformly: some platforms may remain fully operational in compliance with the framework, while others face step-downs.

Earlier Cointelegraph reporting highlighted that Binance’s licensing process has been complicated by application decisions. In particular, the exchange withdrew its Greece application, a move that reduced the likelihood of receiving timely authorization through that channel.

Debate over compliance and market practices

As the deadline nears, public criticism around exchange compliance has intensified. OKX founder and CEO Mingxing Xu responded to comments attributed to former Binance CEO Changpeng “CZ” Zhao about the EU deadline, saying Binance ignores laws and regulations while misleading the public.

In that response, Xu pointed to public reporting and court filings alleging that trading activity described as “best liquidity” included conduct tied to risks involving money laundering, sanctions violations, and market manipulation.

Cointelegraph also reported that it reached out to a Binance spokesperson, who referred to a Wednesday statement from the company.

Users weighing alternatives

Some users appear to be preparing for reduced access by looking at other venues. In community posts cited by Cointelegraph, Reddit users said they were considering Kraken for moving funds. Kraken—operated through Payward—has a Crypto Asset Service Provider licence via the Central Bank of Ireland, according to the publication’s earlier reporting.

For EU customers, the practical takeaway is that exchange choice may become a compliance issue as much as a convenience one. With onboarding restrictions expected to take effect if licenses are not obtained in time, users who wait for official operational guidance could face fewer options.

Over the next days, the key uncertainty is whether Binance will secure the required authorization in time to avoid the July 1 onboarding and service restrictions. Traders and customers should watch for regulator announcements and official updates from exchanges, because the transitional arrangements are ending and compliance-driven access changes could reshape liquidity across Europe quickly.

Mark Zuckerberg has urged Meta's senior leadership to explore partnerships with Polymarket and Kalshi, according to a New York Times report cited by The Block on Friday, days after the paper revealed Meta was building its own competing prediction-market app codenamed Arena. The new reporting adds a… Read the full story at The Defiant

Australia’s securities regulator has extended temporary licensing relief for crypto firms until Sept. 30, giving businesses three more months to comply with updated digital asset rules.

Summary

- ASIC has extended temporary crypto licensing relief until Sept. 30, delaying enforcement by three months.

- The regulator expanded the relief to cover more firms while licence applications continue under INFO 225.

- The extension follows the High Court’s Block Earner ruling and comes ahead of Australia’s 2027 digital asset framework.

According to ASIC, the extension replaces the previous June 30 deadline and applies to businesses seeking an Australian Financial Services (AFS) licence, as well as companies that may require market or clearing and settlement licences.

The regulator also expanded the relief to include digital asset firms operating through authorized representatives or intermediary arrangements with licensed entities.

ASIC said it has received around 30 licence applications since updating its digital asset guidance in October 2025, when it clarified that many crypto-related products fall within Australia’s existing financial services laws.

Extension gives firms more time to comply

Following the October guidance update, ASIC introduced a no-action position so eligible businesses could continue operating while preparing licence applications. Through Information Sheet 225 (INFO 225), the regulator stated that many digital asset products qualify as financial products under Australia’s technology-neutral legal framework, meaning providers often require an AFS licence.

According to ASIC, the temporary relief is intended to support businesses transitioning into the licensing regime while applications continue to be assessed. The regulator added that companies relying on authorized representatives or similar arrangements will now also remain covered during the extended transition period.

The latest decision comes days after Australia’s High Court unanimously ruled 7-0 in ASIC’s favor in its long-running case against Block Earner. As previously reported by crypto.news, the court found that the former fixed-yield crypto product offered by Web3 Ventures Pty Ltd, which operates as Block Earner, functioned as both a financial investment facility and a derivative under the Corporations Act.

The High Court determined that investor returns depended on movements in underlying digital asset prices and exchange rates, supporting ASIC’s interpretation that certain crypto products fall within existing financial services legislation. The case will now return to the Full Federal Court, which will consider ASIC’s appeal regarding penalties.

More regulatory changes remain ahead

While the licensing relief has been extended, ASIC noted that the temporary arrangement remains separate from Australia’s Digital Asset Framework, which Parliament passed in April and is scheduled to take effect on April 9, 2027.

Under that framework, digital asset platforms and tokenized custody platforms will formally enter Australia’s financial services licensing regime. ASIC warned in a May announcement that firms obtaining licences under INFO 225 may still need to add Digital Asset Platform (DAP) and Tokenized Custody Platform (TCP) authorisations once the new framework begins.

The licensing changes also arrive as Australia considers broader reforms affecting digital asset investors. As previously reported by crypto.news, the government has proposed replacing the current 50% capital gains tax discount with an inflation-indexed model from July 1, 2027.

Under the proposal, taxable gains would be adjusted for inflation rather than automatically receiving the existing discount after a one-year holding period, a change that could increase tax bills for many long-term crypto investors during strong market cycles.

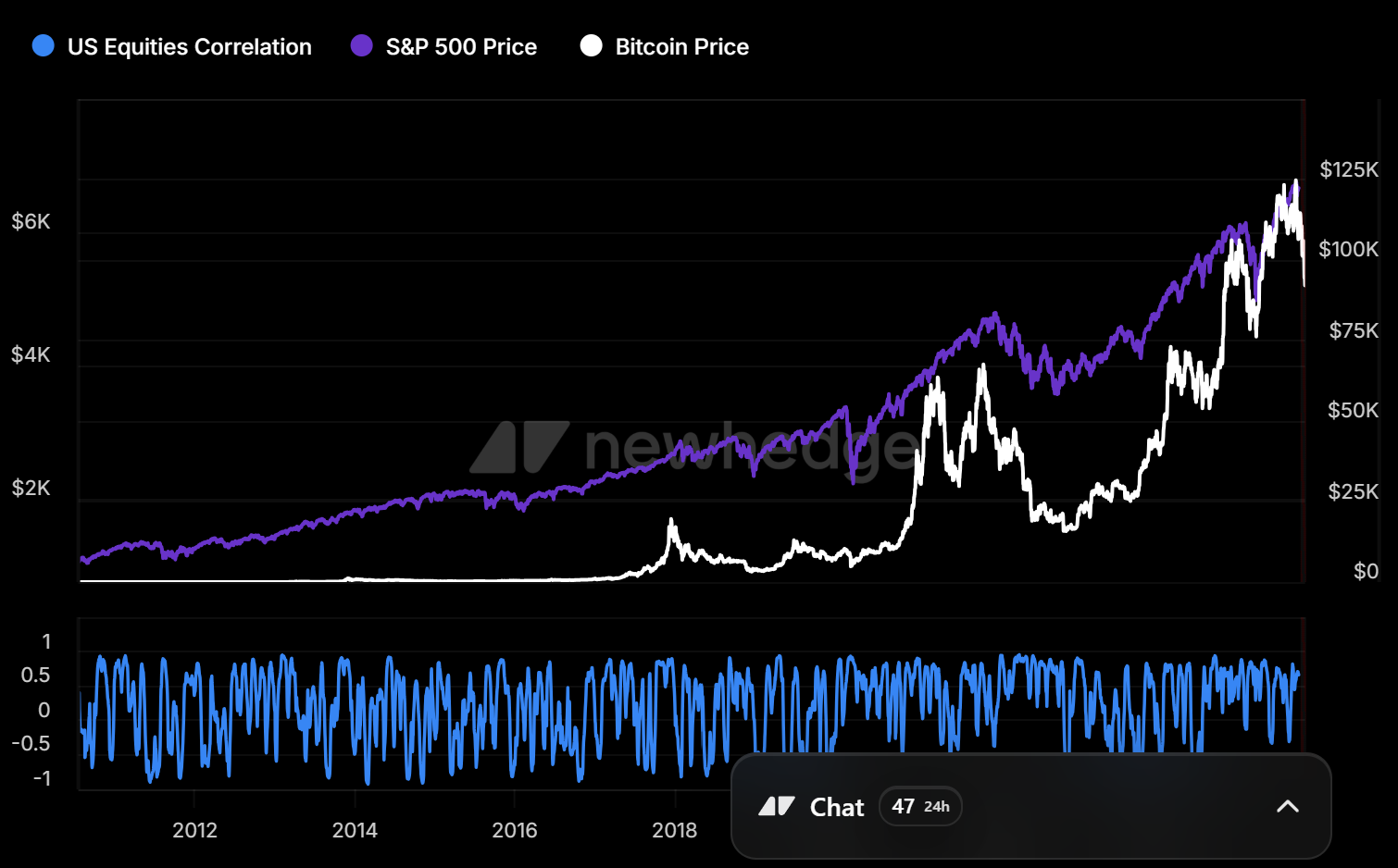

Bitcoin sits near $60,000, down more than half from its October peak, with traders in extreme fear and institutions pulling money out for six straight weeks. The single question that decides where it goes next is whether the famous four-year cycle still governs Bitcoin, or whether institutions have broken it for good.

Summary

- Bitcoin trades near $60,000, roughly 52% below its $126,000 October 2025 peak, sitting on its 200-week moving average with the Fear and Greed Index in extreme fear.

- The central debate is whether the four-year halving cycle is still in control, which would make this a textbook post-peak correction, or whether institutional demand has broken that cycle.

- The cycle-alive case fits the timing almost perfectly: Bitcoin peaked about 18 months after the 2024 halving and is now in the correction phase, the pattern predicts.

- The cycle-dead case argues that exchange-traded funds, corporate treasuries, and structural institutional demand have overridden the old retail-driven rhythm, pointing to a slow grind rather than a deep bear market.

- The crash is the test: a new low below the prior cycle bottom would vindicate the cycle, while holding here and grinding higher would suggest the pattern is broken. The outcome hinges on flows and the macro environment, not on any single price target.

Bitcoin is trading near $60,000, and depending on which framework you believe, that number is either the early stage of a painful but normal correction that ends with a familiar recovery, or the beginning of something the old playbook cannot explain.

The price is down roughly 52% from the all-time high near $126,000 set in October 2025. It is resting on a long-term technical line that traders watch closely. The sentiment gauge known as the Fear and Greed Index is buried in extreme fear, and institutions have pulled money out of Bitcoin exchange-traded funds for six consecutive weeks.

Every one of those facts can be read two ways, and the reading you choose depends almost entirely on a single question that now hangs over the entire market: is Bitcoin still governed by its famous four-year cycle, in which case this is the correction the cycle always brings, or have institutions broken that cycle, in which case the old rules no longer tell you what comes next.

This piece is built around that question, because it is the one that actually decides Bitcoin’s path through the rest of 2026, far more than any individual price level does.

The reason to frame a price prediction this way, rather than as a list of targets, is that the targets themselves flow from which thesis turns out to be right.

If the four-year cycle is alive, history points toward a deeper drawdown and a multi-quarter trough before the next halving-driven recovery. If the cycle is dead, the structural demand from funds and corporate treasuries could put a floor under the price well above where the old pattern would take it, turning a crash into a correction.

The honest work of a prediction, then, is not to pretend to know the number, but to lay out both frameworks clearly, weigh what the current evidence says about each, identify the levels and catalysts that would tip the balance, and translate all of it into concrete bull, bear, and base scenarios.

That is what follows: the cycle explained, the case for each side, what the crash is really signaling, the levels that matter, the scenarios, and the specific developments that would settle the debate.

Bitcoin at a crossroads

Start with where things actually stand, because the current picture is genuinely tense. Bitcoin fell hard through June, breaking down toward the $60,000 area in one of its worst stretches in months, with a single brutal session wiping out around $700 million in leveraged positions, the great majority of them bullish bets that were forced to close.

The drop brought Bitcoin to its 200-week moving average, a long-term trend line near $62,000 that has historically marked deep-cycle support, the kind of level that in past bear markets has roughly coincided with major bottoms.

Just below it, analysts flag the $59,000 area as the next test, and below that, the psychological $60,000 line gives way to genuine uncertainty about how far a breakdown could run.

The mood matches the chart. The Fear and Greed Index, which measures market sentiment on a scale from extreme fear to extreme greed, sits near the bottom of its range in extreme fear, a reading that reflects how thoroughly the recent decline has shaken confidence.

Institutional behavior tells a similarly cautious story, with spot Bitcoin exchange-traded funds posting six straight weeks of net outflows totaling close to $6 billion, described by analysts as the largest sustained institutional redemption wave since these funds launched.

Futures positioning has contracted sharply as traders cut leverage, a sign of de-risking rather than fresh conviction. And yet, woven through the gloom, are countervailing signals: a single day of positive fund flows late in the month, continued buying by corporate treasuries that view these levels as attractive, and the historical tendency of extreme fear to precede rebounds.

Bitcoin, in other words, is at a genuine crossroads, with the bearish evidence and the contrarian signals roughly balanced, and the cycle question is what tips the interpretation one way or the other.

The four-year cycle, explained

To weigh whether the cycle is alive or dead, you have to understand what the four-year cycle actually is, because it has been the dominant framework for understanding Bitcoin’s price for over a decade.

At the center of it sits the halving, a programmed event that occurs roughly every four years and cuts in half the rate at which new Bitcoin is created. Because Bitcoin’s supply growth slows abruptly at each halving while demand continues or grows, the halving has historically acted as a supply shock that, with a lag, drives the price upward.

The pattern that emerged across the first three cycles was remarkably consistent: in the 12-18 months following each halving, Bitcoin entered a powerful bull market and reached a new all-time high, after which it suffered a severe bear market, often falling seventy to 80% from the peak, before grinding through a recovery into the next halving and repeating the sequence.

This rhythm became almost a law in the minds of many investors. The halvings of 2012, 2016, and 2020 were each followed by a major price peak roughly a year to a year and a half later, and each peak was followed by a brutal drawdown and a multi-year trough.

The framework gave Bitcoin holders a kind of map: accumulate in the bear market, hold through the halving, ride the bull market to a new high, and brace for the crash that follows. The most recent halving occurred in April 2024, which places the present moment about 26 months into the current cycle, in what the framework would call the late-cycle or post-peak phase.

If the four-year cycle still governs Bitcoin, then the timing of the recent peak and the subsequent decline should look familiar, and the path ahead should rhyme with what happened after the previous three halvings. Whether it does is exactly what is now in dispute.

The case that the cycle is playing out exactly as it should

The argument that the four-year cycle is alive and well is, on the timing alone, strikingly persuasive. Bitcoin reached its all-time high near $126,000 in October 2025, which is roughly 18 months after the April 2024 halving, landing squarely inside the 12-18-month window in which the previous three cycles each topped out.

From the cycle’s perspective, that peak was the natural climax of the post-halving bull market, right on schedule. What has followed, a sharp decline that has now erased more than half the price, is precisely the kind of post-peak correction the pattern predicts, the opening phase of the bear market that historically arrives after each cycle high.

Seen this way, nothing about the current crash is surprising or anomalous; it is the cycle doing exactly what it has always done.

Respected voices in traditional finance hold this view. Some analysts have described 2026 as a likely correction year, the down phase of the cycle, pointing to support zones in the $60,000-$75,000 range as the kind of levels a cycle correction might test or breach.

Prominent cycle analysts have argued that the cycle bottom still lies ahead, with base cases placing a potential new low later in 2026, consistent with the historical pattern in which the trough comes well after the peak.

Under this framework, the extreme fear, the institutional outflows, and the technical breakdown are all expected features of the post-peak phase, not signs that something unprecedented is happening.

The cycle-alive case, therefore, implies real further downside: if Bitcoin follows the template of prior cycles, the current decline could deepen toward a trough materially below current levels before the next halving-driven recovery begins. It is a sobering view, but it has history and timing firmly on its side, which is what makes it so hard to dismiss.

The case that the cycle is dead

The opposing argument is that the four-year cycle was a feature of a Bitcoin market that no longer exists, and that the forces which created the cycle have been overwhelmed by something new.

The cycle, in this view, was largely a product of retail-driven speculation amplified by the halving narrative, a self-fulfilling rhythm that worked when Bitcoin was a small, speculative asset, moved mainly by individual traders and the four-year supply story.

What has changed is the arrival of institutions at scale. Spot exchange-traded funds have brought enormous, structural pools of capital into Bitcoin, corporate treasuries have adopted it as a reserve asset and accumulate it continuously, and large financial institutions now treat it as a portfolio allocation instead of a speculative flyer.

These holders do not buy and sell on the halving narrative; they respond to macro conditions, portfolio strategy, and long-term conviction, and their presence changes the market’s fundamental behavior.

Proponents of this view, including some prominent research shops, argue that Bitcoin has entered a slow bull phase more akin to a mature asset like gold than to its old boom-and-bust cycles, in which persistent institutional demand smooths out the violent four-year swings and replaces them with a steadier, longer grind higher.

In this framework, the halving still matters as a supply event, but it no longer dictates the price the way it once did, because the marginal buyer is now an institution instead of a retail speculator chasing the cycle.

The implication is that the deep, 70-80% bear markets of the past may not repeat, because structural demand provides a floor that did not exist before, turning what would once have been a cycle-ending crash into a more contained correction.

If this thesis is right, then the current decline, however painful, is a drawdown within an ongoing structural bull market instead of the start of a multi-year winter, and the $60,000 area could prove closer to a bottom than to a way station on the road down. The cycle-dead case, in short, says the old map no longer describes the territory.

What the crash is actually telling us

The natural question is whether the current crash settles the debate, and the honest answer is that it does not, because the evidence cuts both ways, which is itself revealing.

On the bearish side, the six straight weeks of exchange-traded fund outflows, totaling close to $6 billion, complicate the cycle-dead thesis, because they show that institutional demand, far from providing an unshakable floor, can reverse hard and become a source of selling pressure.

The slow-bull argument rests on institutions being steady, structural buyers, and a sustained redemption wave of this size shows that institutional money can flee risk just as retail money does, dragging the price down instead of cushioning it.

The extreme fear, the forced liquidations, and the breakdown to long-term support all fit comfortably within the cycle-alive interpretation of a post-peak correction gathering momentum.

On the other side, several signals support the cycle-dead reading. Even amid the outflows, corporate treasuries kept buying through the decline, with major holders adding to their positions at current levels and explicitly framing them as attractive entry points, behavior that reflects exactly the structural, conviction-driven demand the slow-bull thesis describes.

Late in the month, fund flows turned positive for a day, a tentative hint that the institutional selling may be exhausting itself. And the very depth of the extreme-fear reading, historically, has often preceded rebounds instead of further collapse, because it tends to mark the point of maximum pessimism where selling pressure runs out.

The takeaway is that the crash is genuinely ambiguous: it has features that fit both frameworks, and it has not yet produced the one piece of evidence that would be decisive, which is whether Bitcoin makes a new cycle low or holds here and recovers. Until that resolves, the data refuses to declare a winner, which is precisely why the cycle question remains open and why the next few months matter so much.

The levels that matter

While the big-picture debate plays out, the technical levels provide the concrete map traders are watching, and they are worth knowing because they will mark, in real time, which thesis is gaining the upper hand.

The most important support is the 200-week moving average near $62,000, the long-term trend line that has historically tracked deep-cycle bottoms; a decisive, sustained break below it would be a meaningful signal that the bearish, cycle-alive scenario is taking hold, because losing that level has in the past preceded extended declines.

Just beneath sit the $59,000 area and the round $60,000 psychological level, the latter being the line that prediction-market traders have heavily wagered Bitcoin will break to set a new yearly low, with a smaller but real probability assigned to a fall under $50,000.

On the upside, the levels that would suggest the decline is stabilizing run through the $64,000-$65,000 zone as immediate resistance, with the broader trading range capped near $66,000-$67,000. Reclaiming those levels with conviction would weaken the bearish case and lend support to the idea that structural demand is putting in a floor, while repeated rejection there would keep sellers in control.

The key point is that these levels are not just numbers but markers in the larger argument: holding the 200-week moving average and pushing back above resistance would be evidence for the cycle-dead, floor-is-holding thesis, whereas breaking down through support toward the fifties would be evidence for the cycle-alive, correction-deepening thesis.

The chart, in this sense, is where the abstract debate becomes concrete, and the next decisive move through one of these levels will tell observers a great deal about which framework is winning.

The bull, base, and bear cases for 2026

Translating all of this into scenarios means tying each outcome to the cycle question and to the levels and flows that would drive it. These are conditional ranges, not predictions, and each depends on which forces win out.

- Bull case: Bitcoin holds the 200-week moving average, the extreme fear marks a local bottom, institutional fund flows turn decisively positive, and a friendlier macro backdrop, such as signals of easier monetary policy, restores risk appetite. In this scenario, the cycle-dead, structural-demand thesis is vindicated, the $60,000 area proves to be a correction low, and Bitcoin recovers back toward and through its prior resistance, with more optimistic institutional targets pointing well into six figures over the following year as the slow bull resumes.

- Base case: the tension persists and Bitcoin chops within a wide range for an extended period, neither breaking down to a new cycle low nor mounting a clean recovery, as steady treasury buying offsets continued fund outflows and the market waits for macro clarity. In this scenario, the cycle question stays unresolved, Bitcoin grinds sideways to modestly lower around current levels, and direction depends on which flow trend wins out over the second half of the year.

- Bear case: Bitcoin loses the 200-week moving average decisively, the institutional outflows continue, and the four-year cycle reasserts itself in textbook fashion, driving a deeper correction toward the $50,000 area or below as the post-peak bear market plays out. In this scenario, the cycle-alive thesis wins, prediction-market bets on a sub-$50,000 print are realized, and Bitcoin works toward a cycle trough later in the year before any halving-driven recovery can begin.

What would settle the debate

For anyone trying to read Bitcoin’s direction over the coming months, the analysis points to a short list of developments that would actually settle the cycle question, and watching them is more useful than fixating on any single price. The first and most decisive is simply whether Bitcoin makes a new cycle low. If it breaks down through the 200-week moving average and the $60,000 area toward a materially lower trough, the four-year cycle will have shown that it still governs the market, and the bearish framework will have won.

If, instead, Bitcoin holds these levels and begins to recover, the case that structural demand has broken the cycle gains powerful support. That single binary, new low, or held floor, is the cleanest test available.

The second thing to watch is the institutional flow trend. The six-week outflow streak is the strongest evidence against the slow-bull thesis, so a durable reversal back to sustained net inflows would suggest the structural demand is reasserting itself, while a continuation or acceleration of outflows would reinforce the bearish, cycle-alive reading.

The behavior of corporate treasuries matters here too: continued accumulation through weakness supports the floor thesis, while any sign of treasuries slowing or reversing would be a serious warning.

The third factor is the macro environment, since Bitcoin now trades heavily as a risk asset, and a shift toward easier monetary policy or renewed risk appetite would support the bullish case, while tighter conditions and risk aversion would deepen the decline.

The honest conclusion is that Bitcoin’s path through 2026 is not yet written, because it depends on a genuine, unresolved question about whether the oldest pattern in crypto still holds. The cycle is either running late or it is dead, and the market is about to find out which, with the 200-week moving average, the flow data, and the macro backdrop serving as the scoreboard. Until those resolve, humility about any specific target is not weakness but accuracy.

Frequently Asked Questions

What is the four-year Bitcoin cycle?

It is the dominant framework for understanding Bitcoin’s price, built around the halving, a programmed event roughly every four years that cuts the rate of new Bitcoin creation in half. Historically, in the 12-18 months after each halving, Bitcoin entered a bull market and reached a new all-time high, then suffered a severe bear market, often falling 70-80%, before recovering into the next halving. The pattern held across the 2012, 2016, and 2020 halvings, giving investors a map of accumulation, bull run, peak, and crash that has shaped how the market thinks about Bitcoin for over a decade.

Where is Bitcoin in the cycle right now?

The most recent halving was in April 2024, which places the present moment about 26 months into the current cycle, in what the framework calls the late-cycle or post-peak phase. Bitcoin reached its all-time high near $126,000 in October 2025, roughly 18 months after the halving, squarely within the historical window for a cycle peak. The decline since then, now more than 50%, would be the post-peak correction the cycle predicts. If the cycle still governs, the trough would typically come well after the peak, potentially later in 2026.

Why do some analysts think the cycle is dead?

Because the market that created the cycle has changed. The four-year rhythm was largely driven by retail speculation amplified by the halving narrative, when Bitcoin was a small asset moved by individual traders. Now spot exchange-traded funds, corporate treasuries, and large institutions have brought structural capital that responds to macro conditions and portfolio strategy instead of the halving story. Proponents argue this has turned Bitcoin into a slow-bull asset more like gold, with steadier demand smoothing the violent four-year swings and providing a floor that could prevent the deep bear markets of the past from repeating.

What does the current crash tell us about the debate?

It does not resolve it, because the evidence cuts both ways. The six straight weeks of fund outflows show institutional demand can reverse and become selling pressure, undercutting the steady-floor thesis and fitting the cycle-alive correction view. But corporate treasuries kept buying through the decline, fund flows turned positive for a day, and extreme fear has historically preceded rebounds, all of which support the cycle-dead reading. The decisive evidence, whether Bitcoin makes a new cycle low or holds and recovers, has not yet arrived, which is why the debate remains open and the coming months are pivotal.

What price levels matter most?

The key support is the two-hundred-week moving average near $62,000, a long-term line historically tied to deep-cycle bottoms; a decisive break below it would signal the bearish scenario is taking hold. Beneath sit the $59,000 area and the $60,000 psychological level, with prediction markets heavily wagering on a break to new yearly lows and a smaller chance of a fall under $50,000. On the upside, 64,000-$65,000 is immediate resistance, with the range capped near $66,000-$67,000. Holding support and reclaiming resistance favors the bulls; breaking down favors the bears.

Could Bitcoin fall below $50,000?

It is possible, and prediction-market traders assign a real probability to it. In the bearish, cycle-alive scenario, Bitcoin loses its 200-week moving average, institutional outflows continue, and the post-peak bear market drives a deeper correction toward 50,000 or below as the cycle works toward a trough later in the year. This is not a certainty, and the bullish scenario, in which structural demand puts in a floor near current levels, is equally coherent. Which path unfolds depends on the cycle question, the flow data, and the macro environment, none of which has yet been settled, so a fall below $50,000 is a genuine risk instead of a forecast.

This article is information, not investment advice. The scenarios described are conditional ranges that depend on unresolved questions, not predictions, and Bitcoin is highly volatile. Prices, flows, and sentiment reflect reporting available as of June 26, 2026, and can change quickly. Nothing here is a recommendation to buy or sell. Verify current data from primary sources and consider your own circumstances before making any decision.

The stablecoin market has entered a new phase.

Once viewed primarily as a tool for crypto traders seeking protection from market volatility, stablecoins are increasingly becoming part of the broader financial system. Governments are introducing regulatory frameworks, payment companies are exploring blockchain settlement, and financial institutions are investing in infrastructure that connects traditional finance with digital assets.

As adoption expands, the conversation is shifting from speculation to utility. Businesses are beginning to explore stablecoins for treasury management, supplier payments, and international settlements, while consumers are gaining access to faster and more accessible digital payment options.

To better understand where this transformation is heading, Crypto Breaking spoke with Maksym Sakharov, CEO and Co-Founder of WeFi, about the future of stablecoins, the challenges facing mainstream adoption, and why he believes they are becoming a foundational layer of global financial infrastructure.

Crypto Breaking: Stablecoins have evolved far beyond their original role in crypto trading. How do you see their role developing in global payments over the next few years?

Maksym Sakharov: Stablecoins are increasingly becoming a payment layer for both individuals and businesses that need value to move faster, more predictably, and across multiple markets.

“In the early days, stablecoins primarily served crypto traders moving funds between exchanges while avoiding volatility. That use case remains relevant, but today’s strongest growth is coming from real economic activity.”

He believes businesses are beginning to recognize stablecoins as practical tools for treasury operations, vendor payments, and international settlements, while consumers benefit from easier access to stable digital value and faster cross-border transfers.

According to Sakharov, the next stage of adoption will depend less on blockchain technology itself and more on user experience.

“People shouldn’t need to understand the underlying technology. They simply need reliable access, clear balances, fiat connectivity, and payment products that make stable digital value easy to use.”

Crypto Breaking: What are the most compelling real-world use cases for stablecoins today beyond speculation?

Sakharov argues that the strongest use cases emerge wherever users already experience friction in traditional finance.

International freelancers can receive payments faster while avoiding unnecessary currency conversions. Companies paying overseas suppliers can settle transactions more efficiently without waiting through lengthy banking processes. Businesses managing treasury across different regions gain access to liquidity that operates around the clock rather than only during banking hours.

He also highlights another growing trend: individuals in many countries increasingly seek access to stable digital assets as a way to preserve purchasing power while maintaining the flexibility of digital payments.

“The common denominator is solving practical financial problems such as settlement speed, currency friction, value portability, and financial accessibility.”

Crypto Breaking: What remains the biggest obstacle preventing mainstream adoption?

While blockchain settlement has become significantly more efficient, Sakharov believes the surrounding ecosystem still requires substantial improvement.

“The biggest challenge today is fragmentation.”

Users may receive stablecoins quickly, but questions immediately follow. Can they easily spend them? Can they convert them into local currency? Can businesses integrate them into existing financial workflows? Can users trust both the provider and the underlying infrastructure?

According to Sakharov, solving these issues requires more than faster blockchains.

“The industry needs deeper liquidity, stronger fiat connectivity, clearer regulation, better compliance, broader merchant acceptance, and simpler products. None of these alone is sufficient.”

Crypto Breaking: How will regulation shape the future of stablecoins?

Regulation, Sakharov says, is likely to accelerate institutional adoption rather than slow innovation.

“For many years, stablecoins evolved faster than the regulatory frameworks surrounding them. That enabled innovation, but it also created uncertainty.”

As governments establish clearer rules around reserves, redemption, custody, compliance, and disclosure requirements, businesses will gain greater confidence in integrating stablecoins into mainstream financial operations.

At the same time, regulation raises expectations for issuers and infrastructure providers.

“Supporting stablecoins is no longer just a technical challenge. It also requires governance, compliance, risk management, and operational transparency.”

Crypto Breaking: How are stablecoins reshaping cross-border payments?

Traditional international payments often remain dependent on multiple intermediaries, limited banking hours, currency conversion processes, and delayed settlement.

Stablecoins offer an alternative model.

“Value can move digitally with faster settlement, greater transparency, and fewer intermediary steps.”

However, Sakharov emphasizes that blockchain alone is not enough.

Liquidity, regulatory compliance, local banking access, payment acceptance, and customer support all remain essential components of a complete financial ecosystem.

He explains that WeFi is focused on connecting stablecoin rails with fiat access and account-like usability to make cross-border financial services more practical for both businesses and consumers.

Crypto Breaking: What should businesses and investors watch over the next two years?

Rather than focusing exclusively on which stablecoins dominate the market, Sakharov believes attention should shift toward the infrastructure being built around them.

Businesses should monitor how stablecoins integrate into treasury management, supplier payments, and international operations.

Investors should pay close attention to companies developing access layers, payment connectivity, compliance systems, liquidity infrastructure, and products that bridge stablecoins with traditional financial services.

Consumers, meanwhile, may notice stablecoins becoming less visible while becoming more useful.

“The biggest change will be when people use stablecoins without thinking about them. They’ll simply experience clearer balances, easier payments, and better access to financial services.”

Final Thoughts

As stablecoins continue to mature, the conversation is increasingly centered on infrastructure rather than speculation.

While regulatory clarity, user experience, and interoperability remain significant challenges, industry leaders believe the technology is steadily moving toward mainstream financial adoption.

Whether stablecoins ultimately become a standard component of global finance will depend not only on blockchain innovation but also on the ability of infrastructure providers to make digital value as seamless and intuitive as today’s online banking experience.

About Maksym Sakharov

Maksym Sakharov is the CEO and Co-Founder of WeFi, a company focused on building compliant financial infrastructure that connects stablecoin payments, fiat access, and digital financial services. His work centers on improving cross-border payments and accelerating the practical adoption of stablecoin-based financial products.

Attackers exploited a third-party vendor compromise to inject malicious code into Polymarket’s frontend, triggering a phishing flow that ultimately drained funds from at least 11 user wallets, according to blockchain analyst Specter. Specter estimated the stolen amount at $2.94 million, citing activity linked to the compromised user interface.

Polymarket said it has contained the incident, removed the affected dependency, and will fully refund affected users. The case adds to a broader security trend flagged by DefiLlama, which reports that the quarter is now the most-hacked on record by incident count.

Key takeaways

- Specter attributed the Polymarket incident to a third-party vendor compromise that allowed malicious script injection into the platform’s frontend.

- The phishing mechanism reportedly led to an estimated $2.94 million drained from at least 11 Polymarket user wallets.

- Polymarket says containment is complete, the compromised dependency has been removed, and users will be fully refunded.

- DefiLlama data shows crypto security breaches in the second quarter hit a record pace, while June totals climbed to $74.9 million across 29 reported incidents.

- Across the last 30 days, DefiLlama reports private key compromises as the largest share of losses (43%), with “fake proof” exploits (10%) and reverse MEV honeypots (8%) following.

How the Polymarket frontend compromise unfolded

According to Specter, the attackers leveraged a third-party vendor breach to slip malicious scripting into Polymarket’s website experience. Specter said the injected code appeared designed to support a phishing attack—meaning users could be induced to sign or approve actions that transferred funds instead of completing the intended transaction.

Specter’s analysis estimated the theft at roughly $2.94 million, impacting at least 11 Polymarket user wallets. The figure is based on observed drain activity associated with the phishing pattern described by Specter.

Polymarket responded publicly on X, stating that it identified and contained the compromise, removed the affected dependency, and confirmed that affected users would be fully refunded. Cointelegraph sought further comment from Polymarket but did not receive a response before publication.

June exploit losses climb—still below April’s peak

While the Polymarket case is a notable incident, it sits within a wider wave of exploit activity. DefiLlama data cited in the report shows crypto exploit losses in June reached $74.9 million across 29 reported incidents, a rise from May’s $60.5 million total.

Even with the month-over-month increase, June’s total remained far below April’s $644 million figure, underscoring how uneven the exploit landscape has been across the year. The same DefiLlama dataset also marks the second quarter as the most-hacked period on record by incident count, extending the high frequency of breaches reported so far.

Largest June incidents highlight recurring bridge and exploit risk

DefiLlama’s breakdown points to several major June events that drove losses higher. The largest reported incident in June was a $36 million Humanity Protocol exploit. Other large items included a $4.7 million Secret Network bridge exploit and two separate Aztec exploits valued at $2.1 million each.

The list also includes a $1.7 million bridge exploit on Taiko. Together, these events reinforce a familiar theme in crypto security reporting: cross-chain bridge systems and complex protocol integrations continue to concentrate losses when vulnerabilities are discovered or supply-chain components are compromised.

Attack vectors shift: private key compromises lead, phishing cases remain a concern

DefiLlama’s methodology breaks down the last 30 days of reported exploit losses by technique. Private key compromises accounted for 43% of losses, making them the most common category in the period. “Fake proof” exploits represented 10%, while reverse MEV honeypots made up 8% by the same breakdown.

The Polymarket incident is described differently from those categories in the underlying reporting: Specter framed it as a frontend injection leading to phishing, which in practice can overlap with user-level security failures rather than only on-chain vulnerabilities. Regardless of the taxonomy, the operational takeaway is similar—attackers increasingly combine supply-chain weaknesses with user-targeted deception to move funds.

The threat also has a local history on Polymarket. About a month earlier, the prediction market disclosed a separate $600,000 exploit tied to a six-year-old private key used for internal top-up operations. Josh Stevens, Polymarket’s vice president of engineering, said then that contracts and user funds were safe and that permissions tied to the key had been revoked, reflecting a response approach aimed at limiting exposure after discovery.

What to watch next for Polymarket users

With Polymarket stating it has removed the compromised dependency and will refund impacted users, the next signals to monitor are whether any residual scams continue via cached pages, third-party scripts, or follow-on attempts against user approvals. More broadly, investors and users should track whether the second-quarter record pace continues and whether DefiLlama’s technique breakdown shows phishing-style incidents rising alongside private key compromises.

Supergirl Writer Reveals Scrapped Sasha Calle Movie Was “Completely Different” From the DCU Film : Coastal House Media

TV-famous former Cambridgeshire police officer asked colleague to send him sex video of female suspect

STRF: Senior Preferred, Double Digit Tax Deferred Yield, High Asset Coverage (NASDAQ:STRF)

-

Entertainment6 days ago

Entertainment6 days agoRenter of Home in Anne Heche Crash Denies Settlement With Son

-

Sports3 days ago

Sports3 days agoTwo goals and an assist by sheer aura: Cristiano Ronaldo just entered the World Cup chat

-

Tech4 days ago

Tech4 days agoMicrosoft accidentally kills epic Outlook email threads

-

Business6 days ago

Business6 days agoSoccer-U.S. defends Iran World Cup travel restrictions, says discussions ongoing

-

Fashion6 hours ago

Fashion6 hours agoWeekend Open Thread: Staud – Corporette.com

-

Politics18 hours ago

Politics18 hours agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Politics7 days ago

Politics7 days agoAndy Burnham and the meaning of Makerfield

-

Politics22 hours ago

Politics22 hours agoPotential 2028er World Cup attendee leaderboard

-

Tech1 day ago

Tech1 day agoA Look At A Gaggle Of Transputer Boards

-

Crypto World3 days ago

Bitcoin (BTC) Dips Below $62K, Ethereum (ETH) Plunges 6% Daily: Market Watch

-

Business16 hours ago

Business16 hours agoAsia stock markets slide as tech shares slump

-

Crypto World3 days ago

Crypto World3 days agoSecuritize Wraps Roubini's SEC-Registered ETF as Dubai VARA Digital Security

-

Crypto World1 day ago

Crypto World1 day agoDell (DELL) Shares Tumble Over 5% Following Analyst Downgrade to Hold

-

Business3 days ago

Entergy settles forward sale agreements, raises $672 million in cash proceeds

-

Crypto World7 days ago

Crypto World7 days agoCan Charles Hoskinson Really Rescue Cardano?

-

Business7 days ago

Business7 days agoWall Street Week Ahead: Investors see Micron earnings as pulse check of AI rally momentum

-

Sports3 hours ago

Sports3 hours agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Entertainment7 days ago

Entertainment7 days agoJose Alvarado Wants Taylor Swift at More Knicks Games

-

Crypto World7 hours ago

Crypto World7 hours agoRTX holders must register wallets before token distribution begins

-

Crypto World7 days ago

Crypto World7 days agoHIVE shares jump as $220M AI deal speeds Bitcoin mining pivot

You must be logged in to post a comment Login