Crypto World

Taiko Requests Withdrawals as Bridge Exploit Cuts $1.7M

Taiko, an Ethereum layer-2 network, has asked users to immediately withdraw any assets held on bridges connected to its ecosystem after it confirmed a compromise affecting a core verification component. The incident follows a run of high-profile decentralized finance (DeFi) exploits in June, with DeFiLlama reporting at least 23 hacks across the sector so far this month.

In an update posted to X on Monday, Taiko said it “confirmed a compromise of Taiko’s chain state verification mechanism,” adding that the security assumptions underlying all bridges deployed on Taiko “can no longer be relied upon.” The team urged users to “withdraw their funds from all bridges deployed on Taiko immediately.”

Key takeaways

- Taiko has confirmed a compromise of its chain state verification mechanism and is treating bridge security guarantees as unreliable.

- Security firm Blockaid attributes the exploit to a bridge validation weakness that allowed fraudulent message proofs to be accepted.

- Estimated losses differ by analyst: Blockaid suggested at least $1 million, while others put the figure as high as $1.7 million.

- Blockchain monitoring tools show the exploiter moving value, with Arkham reporting roughly $1.5 million in ETH in associated wallets.

- The incident adds to a June cluster of major DeFi breaches, including losses tied to Humanity Protocol and Syscoin Bridge earlier this month.

Taiko warns bridge users after verification compromise

The warning is aimed specifically at bridge risk rather than at general activity on Taiko itself. Taiko framed the problem as a breach in how it verifies chain state and validates the messages bridges rely on to release assets on the other side.

Taiko also said it was coordinating with partners to contain the issue and that it had paused affected systems, signaling that bridge operations tied to the compromised verification path may require additional remediation before normal user withdrawals resume.

For users, the practical implication is straightforward: bridges are designed to move funds across trust boundaries, and if the verification assumptions behind those bridges fail, withdrawals become time-sensitive. Taiko’s instruction to withdraw immediately reflects that risk assessment.

Why the exploit worked, according to Blockaid

Blockaid said the root cause appeared to be a flaw in how the Taiko bridge validated source signals. In its explanation, the issue centered on message proofs: proofs were reportedly accepted as valid on Ethereum even when they lacked corresponding legitimate proofs on Taiko.

Blockaid described how this could let an attacker register and later retrieve fraudulent bridge messages, enabling unauthorized asset releases from an ERC20 vault. That mechanism matters because it points to a verification mismatch rather than, for example, a simple smart-contract logic error limited to a single bridge instance.

Blockaid estimated that at least $1 million was stolen, while other analysts pointed to a higher potential value. PeckShield and Lookonchain suggested the amount taken could reach about $1.7 million.

Stolen funds, wallet activity, and token transfer signals

PeckShield reported that the exploiter had already transferred 1.99 million Taiko (TAIKO) tokens—worth around $189,000 at the time of reporting—to MEXC.

PeckShield’s wallet-tracking aligns with broader on-chain monitoring. Arkham’s explorer data, as cited in the report, shows exploiter-linked wallets holding roughly $1.5 million, primarily in Ether (ETH). The presence of significant ETH balances is relevant for traders and investigators because it suggests the attacker may hold liquidity that can be deployed across exchanges or other swaps, depending on operational intent and timing.

Separately, CoinGecko data cited in the source notes TAIKO was trading down sharply versus its 2024 peak—an indication of broader market repricing for the token, though the article does not connect that move causally to this specific exploit.

June’s exploit tally keeps rising

Taiko’s incident arrives during a busy stretch for crypto security. DeFiLlama data, cited in the report, indicates at least 23 decentralized finance exploits this month.

The Taiko hack follows other notable breaches in June, including:

- Humanity Protocol, which reportedly lost over $30 million earlier in the month

- Syscoin Bridge, reported losses of about $8 million

- A Secret Network smart contract exploit discovered on Friday, resulting in theft valued at $4.67 million

- An alleged drainage of around $1.1 million from a PancakeSwap liquidity pool involving OLPC/LABUBU

The accumulation of these events matters because it highlights a recurring sector vulnerability: the bridge and cross-chain messaging layer is repeatedly targeted. Even when individual hacks differ in technical cause, the economic effect is similar—assets can be released or transferred when the conditions that should validate legitimacy fail.

For users, the repeated pattern makes operational guidance more important than ever. When bridge operators issue emergency withdrawals—like Taiko did—investors and liquidity providers should treat it as a risk-management instruction rather than a routine status update.

Looking ahead, readers should watch for Taiko’s next technical briefing on what must change for bridges to be considered safe again, whether affected systems remain paused long-term, and how quickly analytics firms confirm the final scope of stolen funds as attacker wallets are tracked and assets move.

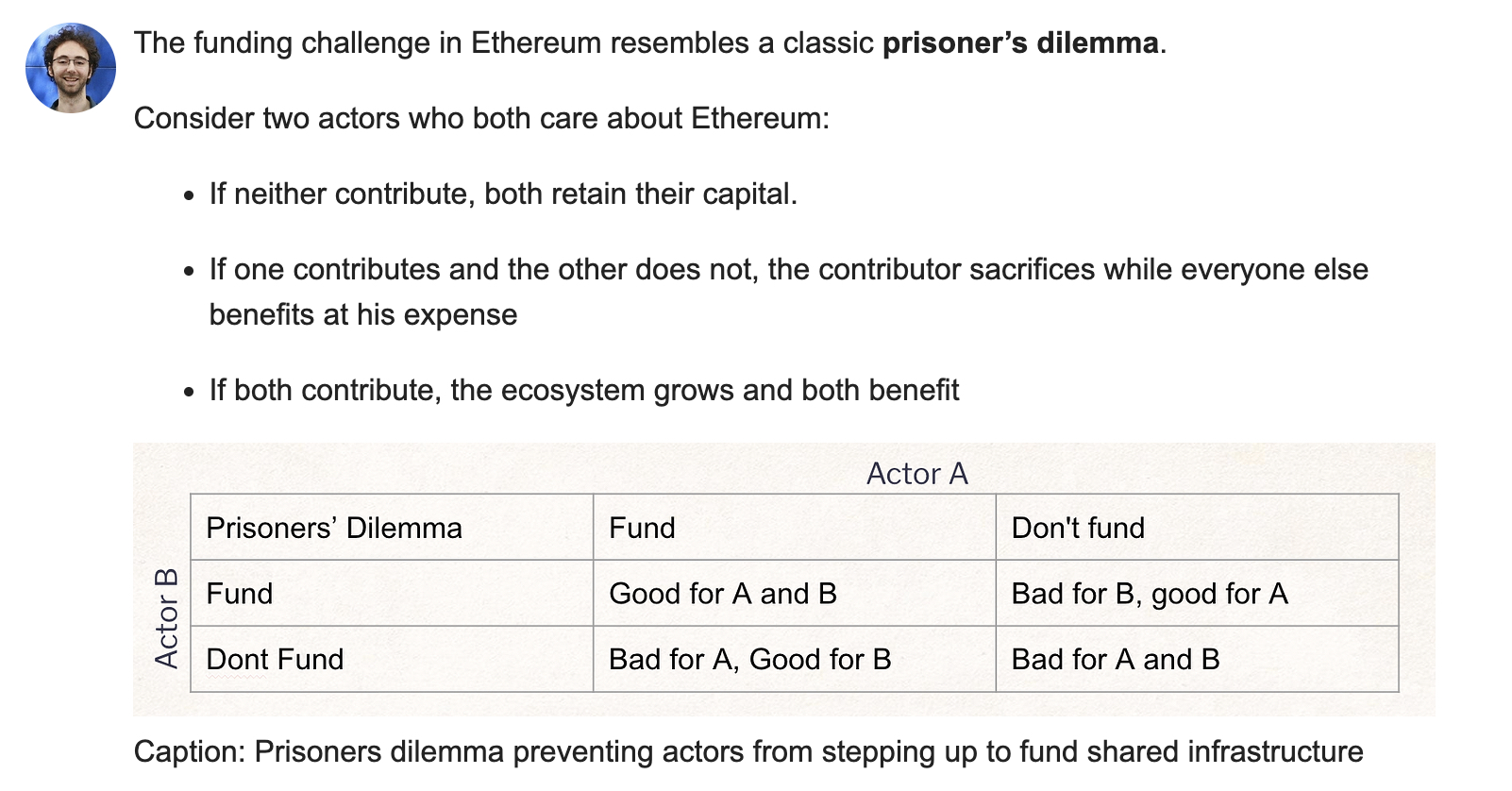

Every time you trade on-chain, an invisible competition decides the order of transactions in the next block, and whoever controls that order can extract value from yours. That is MEV. It funds a hidden industry, quietly taxes ordinary users, and shapes the design of every modern blockchain.

Summary

- MEV lets block producers profit by controlling transaction order, creating opportunities such as arbitrage, liquidations, and sandwich attacks.

- Flashbots and MEV Boost transformed MEV into a structured marketplace, allowing validators to earn rewards without directly extracting value themselves.

- Private transaction routes and MEV aware trading platforms can help users reduce exposure to predatory forms of MEV and improve trade execution.

MEV, which stands for maximal extractable value, is the profit that can be captured by whoever controls the ordering of transactions within a block on a blockchain. Because the entity that builds a block can choose which transactions to include, exclude, and in what order, that power can be turned into money by slotting a profitable trade ahead of yours, squeezing a transaction between two others, or grabbing an arbitrage the moment it appears.

The term was originally “miner extractable value,” coined when miners ordered blocks, and it became “maximal extractable value” after Ethereum moved to validators, but the idea is the same: transaction ordering is valuable, and that value gets extracted. MEV is often called crypto’s invisible tax, because most users never see it even as they pay for it through worse prices and higher fees.

This guide explains MEV in plain English, with no technical background assumed. It covers what MEV actually is, why it exists at all, the main forms it takes from harmless arbitrage to predatory sandwich attacks, the hidden supply chain of searchers, builders, and validators that has grown up around it, the Flashbots infrastructure that reshaped how MEV works, the difference between MEV that helps markets and MEV that harms users, and the tools that ordinary people and protocols now use to fight back.

By the end, you will understand why MEV is a permanent feature of any public blockchain, why billions of dollars have flowed through it, and why the battle is not to eliminate it but to control who captures it and how.

What MEV actually is

At its core, MEV comes from a simple fact about blockchains: transactions do not settle the instant you send them. They wait, and someone decides the order in which they are processed, and that someone can profit from the decision.

When you submit a transaction, a swap on a decentralized exchange, a loan repayment, a token purchase, it does not go straight into the permanent record. It enters a waiting area, and eventually a block producer gathers a batch of pending transactions, arranges them in an order, and adds them to the chain as a block. Here is the key: the block producer has discretion over that order.

They can put your transaction first or last, include it or leave it out, and slip their own transactions, or transactions from others who pay them, into any position they like. Whenever the order of transactions affects how much money can be made, that potential profit is MEV, and the people who chase it design their actions specifically to win the ordering game.

The clearest way to grasp it is by analogy. In traditional stock markets, a broker who can see your large order coming and trade ahead of it is front-running, which is illegal. On a public blockchain, your pending transaction is visible to everyone, and reordering it for profit is not against any law, it is just how the system works, so the same behavior that is banned in regulated markets is an open, competitive industry on-chain.

One researcher famously called the public mempool a “dark forest,” a place where any transaction you broadcast can be hunted by predators watching for prey. MEV is the value those predators, and also some entirely useful actors, extract from the simple power to order transactions.

Why MEV exists: the mempool and ordering

To understand why MEV is unavoidable, you have to look at the waiting room where transactions sit before they are confirmed, because that is where the whole game is played.

On a chain like Ethereum, a transaction you broadcast lands first in the mempool, a public, shared pool of pending transactions that have not yet been included in a block. The mempool is visible to anyone running a node, which means that for a brief window your intended trade is public knowledge before it is final.

Specialized bots watch this pool constantly, scanning every pending transaction for opportunities, and when they spot one, they craft their own transactions designed to profit from the order in which everything will be processed. They then compete, often by bidding higher fees, to have their transactions placed in exactly the right position relative to yours.

This is why MEV is intrinsic to public blockchains rather than a bug to be patched away. As long as there is a gap between sending a transaction and finalizing it, as long as that pending transaction is visible, and as long as someone has the power to order the block, the opportunity to extract value from ordering will exist.

The mechanics differ by network: Ethereum has a public mempool that makes pending transactions visible, Solana has no mempool in the Ethereum sense and routes transactions straight to validators, and Layer 2 networks often use a single sequencer that orders transactions first come first served.

But the underlying dynamic, that whoever controls ordering can extract value, follows the structure of how blockchains reach agreement, which is why researchers describe MEV as a permanent feature of the technology rather than a temporary flaw.

The main forms of MEV

MEV is not one behavior but a family of them, and they range from useful to openly predatory. Sorting them out is the difference between fearing MEV and understanding it.

Arbitrage is the most common and the least controversial. When the same asset trades at slightly different prices on two decentralized exchanges, a bot can buy on the cheaper one and sell on the dearer one in the same block, pocketing the difference. This is MEV, but it is widely seen as neutral or even helpful, because it pushes prices on different venues back into line and makes markets more efficient.

Liquidations are similar. In lending protocols, when a borrower’s collateral falls below the required threshold, their position becomes eligible to be liquidated, and bots compete to be the one that repays the loan and claims the collateral at a discount. This too is generally seen as beneficial, because prompt liquidations keep lending protocols solvent and protect lenders. These two forms are sometimes called “good” MEV, since the extraction performs a function the system actually needs.

Then there is the predatory end. The most notorious form is the sandwich attack, where a bot spots your large pending swap, buys the asset just before you to push the price up, lets your trade execute at that worse price, and then sells immediately after for a profit, leaving you with a worse rate than you would have gotten.

Your transaction is the filling, squeezed between the bot’s buy and sell. Front-running more broadly means jumping ahead of a known transaction to profit from it, and back-running means slipping in immediately after a transaction to capture an opportunity it created.

These forms extract value directly from ordinary users, worsening their prices and inflating fees, which is why this is the MEV that earns the “invisible tax” label. The same power to order transactions enables both the helpful arbitrage that keeps markets efficient and the harmful sandwich that quietly skims from regular traders, which is exactly why MEV is so hard to simply ban.

The MEV supply chain: searchers, builders, validators

What began as lone bots has matured into a structured, multi-party industry, and knowing the roles makes the whole system legible.

At the front are searchers, the operators who run sophisticated bots scanning the mempool and the chain for profitable opportunities, arbitrage, liquidations, sandwiches, and who construct bundles of transactions designed to capture that value. Searchers are the prospectors, finding the gold.

They do not usually build blocks themselves; instead, they hand their bundles, along with a fee they are willing to pay, to builders. Builders are specialists who assemble complete, profit-maximizing blocks out of the transactions and bundles they receive, competing to construct the single most valuable block possible.

They are the ones who actually solve the ordering puzzle at scale. Finally, the assembled block goes to a validator, the participant chosen by the network to propose the next block. The validator does not need to do the complex work of finding and arranging MEV; it simply selects the most valuable block offered to it and proposes it, collecting a share of the value as reward.

This division of labor, searchers find, builders assemble, validators propose, is the modern structure of MEV, and it exists because separating these roles turned out to be more efficient and, importantly, fairer than the alternative where every validator had to extract MEV themselves. That separation is not an accident. It was deliberately engineered, and the system that engineered it is the most important piece of MEV infrastructure in existence.

Flashbots, MEV-Boost, and proposer-builder separation

The story of how MEV went from a chaotic free-for-all to an organized market is largely the story of one organization, Flashbots, and the infrastructure it built.

In the early days, MEV extraction was destructive in a way that threatened the whole network. Searchers competing for the same opportunity would wage “gas wars,” bidding transaction fees up by ten or twenty times to win the ordering race, which spiked costs for every ordinary user and clogged the chain with failed attempts.

Worse, the competition risked pushing power toward whoever could extract MEV most aggressively, threatening to centralize the network. Flashbots, a research organization, set out to defang this by moving the MEV competition off the public chain and into a private, orderly auction, so searchers could bid for transaction ordering without flooding the network with gas wars.

The centerpiece is the architecture known as proposer-builder separation, or PBS, implemented through software called MEV-Boost. PBS splits the job of proposing a block from the job of building it, exactly the searcher-builder-validator structure described above. A validator running MEV-Boost does not build its own block; it connects to a marketplace of competing builders, receives their best offers through intermediaries called relays, and simply chooses the most valuable one to propose.

This lets even a small, solo validator earn a fair share of MEV without the technical sophistication to extract it, which keeps validating accessible and the network more decentralized. Adoption has been overwhelming, with well over ninety percent of Ethereum validators running MEV-Boost, because outsourcing block construction to specialists pays better than building blocks themselves.

The tradeoff is concentration: a handful of builders and relays now route the large majority of blocks, which is its own centralization worry, and it is why the Ethereum community is working to move PBS directly into the protocol itself, an upgrade often called enshrined PBS, as a priority for 2026. Flashbots also pursued more ambitious redesigns, and while some of those research efforts were wound down, the core insight, turn MEV into a transparent, competitive market instead of a destructive scramble, has stuck.

Good MEV, bad MEV, and the invisible tax

It is tempting to treat MEV as simply theft, but the honest picture is more divided, and the division is exactly why the problem is hard.

Some MEV is genuinely useful. Arbitrage keeps prices consistent across exchanges, and liquidations keep lending markets solvent, and both of these are services the decentralized economy needs someone to perform. The searchers who do this work are, in a sense, paid for keeping the system efficient.

The amounts are not trivial: cumulative MEV across chains crossed one billion dollars by 2025, and Flashbots’ tracking found well over six hundred thousand ether of MEV extracted on Ethereum over the years it measured, a reminder that this is real money, not a theoretical edge.

But a meaningful slice of MEV is extracted directly from ordinary users at their expense, and that is the invisible tax. When a sandwich bot worsens your swap price, the difference comes straight out of your pocket, and you may never realize it happened, because the trade still went through, just at a worse rate than it should have. Multiply that across millions of transactions and the cost to regular users is substantial.

The encouraging news is that the harm is shrinking where protection has taken hold. Data from MEV researchers shows the monthly value extracted from sandwich attacks on Ethereum fell sharply through 2024 and 2025, from roughly ten million dollars a month to a fraction of that, as more transactions moved through protected routes.

The picture, then, is not “MEV is theft” but something more nuanced: MEV is the price of having open, ordered, permissionless blockchains, part of it pays for useful work, part of it is skimmed from users, and the entire industry’s effort is now bent toward shifting the balance away from the skimming.

How users and protocols fight back

You are not helpless against MEV, and one of the most useful things a guide can do is explain the practical defenses, because they have become remarkably effective.

The first line of defense is to keep your transaction out of the public mempool entirely. Private transaction services, often called private RPCs, send your transaction directly to builders instead of broadcasting it to the public pool, so the predatory bots never see it coming.

Flashbots Protect is a widely used free option that does exactly this, hiding your transaction and even returning some recovered value, and switching to it is usually a one-line change in your wallet settings; it has shielded tens of billions of dollars of trading volume across millions of accounts.

MEV Blocker, built by the team behind CoW Protocol, is another private route that goes further by running a searcher auction and paying a large share of any recovered value back to you as a rebate, and it too has protected tens of billions in volume.

A second approach is to trade on venues designed to neutralize MEV structurally. CoW Swap settles trades in batches at a single uniform clearing price, so that everyone in a batch gets the same rate regardless of ordering, which removes the front-running advantage by design, and aggregators such as UniswapX use auction mechanisms with a similar protective effect. A third, emerging idea is to flip the model entirely, with systems that capture the MEV your transaction creates and rebate it back to you, turning the invisible tax into a refund.

The networks themselves also shape your exposure. On many Layer 2 networks, a single sequencer currently orders transactions first come first served with no public mempool, which sharply reduces sandwich risk today, though it concentrates ordering power in one operator and that protection will change as those networks decentralize their sequencing. On Solana, the lack of a traditional mempool changes the dynamics, but MEV still exists through validator-level bundle systems.

The practical takeaway for a regular user is concrete: route your important trades through a private RPC like Flashbots Protect or MEV Blocker, prefer MEV-aware venues for large swaps, and you remove yourself from the dark forest for almost no effort and no cost.

A sandwich attack, step by step

The most infamous form of MEV becomes far less abstract when you watch it happen to a single trade, so follow one swap through a sandwich, because it shows exactly how the invisible tax is collected.

You want to swap ten thousand dollars of a stablecoin for a mid-sized token on a decentralized exchange. You set your trade and broadcast it, and for a brief moment it sits in the public mempool, visible to anyone watching, waiting to be included in the next block. A searcher’s bot, scanning the pool constantly, sees your pending swap and recognizes that a trade your size will push the token’s price up on that exchange’s liquidity pool. It has found its prey.

The bot acts in three moves, all landing in the same block, all arranged by the ordering it pays to control. First, the front-run: the bot buys the same token just before your transaction, nudging the price up. Second, your trade executes, but now at the higher price the bot just created, so you receive fewer tokens than you would have, paying more than the rate you saw when you clicked.

Third, the back-run: immediately after your trade pushes the price up further, the bot sells the tokens it bought a moment earlier, cashing out at the elevated price your own swap helped produce. The bot is the bread on both sides, your trade is the filling, and the profit it skimmed came directly out of your execution. You still got your tokens, the transaction succeeded, and you may never realize anything was taken, which is precisely why it is called an invisible tax.

Now notice how the defenses described earlier would have stopped it. Had you routed the swap through a private transaction service like Flashbots Protect or MEV Blocker, your trade would never have entered the public mempool, so the bot would never have seen it coming, and the sandwich would have been impossible.

Had you traded on a batch-auction venue like CoW Swap, everyone in your batch would have settled at one uniform price, removing the ordering advantage the bot relied on. One swap shows both the attack and the cure, and it explains why the simple habit of keeping important trades out of the public mempool is the single most effective thing an ordinary user can do.

Why MEV is permanent, and why that is not the end of the story

The honest conclusion is that MEV will never be fully eliminated, because the underlying source, the value of controlling transaction ordering, is woven into how blockchains reach agreement. Any system where transactions are ordered, and where that order affects who profits, will have MEV. Pretending otherwise is a fantasy, and the most serious people working on the problem say so plainly.

But permanence is not defeat, because the real question was never whether MEV exists. It is who captures it, how transparently, and at whose expense. On that question, the progress has been substantial. A destructive free-for-all of gas wars became an orderly, mostly private auction. Predatory sandwich extraction has fallen as protection spread. Solo validators can earn a fair share of MEV without being extraction experts. Ordinary users can shield their trades with a single setting, and new designs are starting to rebate MEV back to the people who generate it.

The trajectory is from opaque and extractive toward transparent and redistributive, and the protocols are working to pull the whole auction into the base layer where it can be made fairer still. MEV is the hidden machinery beneath every on-chain trade, and understanding it changes how you transact, because once you can see the dark forest, you can choose to walk around it.

Frequently Asked Questions

What is MEV in simple terms?

MEV, or maximal extractable value, is the profit that can be made by whoever decides the order of transactions in a block on a blockchain. Because a block producer can choose which transactions to include and in what order, that power can be turned into money, for example by placing a profitable trade ahead of yours or squeezing a transaction between two others. It used to stand for “miner extractable value” but became “maximal extractable value” after Ethereum switched from miners to validators. MEV is often called crypto’s invisible tax because users pay for it without seeing it.

Why does MEV exist?

MEV exists because transactions do not settle instantly. After you send a transaction, it waits in a public pool called the mempool before a block producer orders it into a block, and during that window your intended trade is visible. Bots scan the mempool for opportunities and compete to have their own transactions placed in profitable positions relative to yours. As long as there is a gap between sending and finalizing a transaction, and someone controls the ordering, the chance to extract value from that ordering will exist, which is why MEV is intrinsic to public blockchains.

What is a sandwich attack?

A sandwich attack is a predatory form of MEV. A bot spots your large pending swap, buys the asset just before you to push the price up, lets your trade execute at that worse price, then sells right after for a profit. Your transaction is the filling squeezed between the bot’s buy and sell, and you end up with a worse rate than you should have gotten. It is one of the main reasons MEV is called an invisible tax, because the trade still goes through and most users never notice the value taken from them.

What are Flashbots and MEV-Boost?

Flashbots is a research organization that reshaped how MEV works by moving the competition for transaction ordering off the public chain into an orderly auction, ending the destructive gas wars of the early days. Its key software, MEV-Boost, implements proposer-builder separation, which splits the job of proposing a block from building it. A validator running MEV-Boost simply chooses the most valuable block offered by competing builders, so even small validators earn a fair share of MEV. Well over ninety percent of Ethereum validators run it.

How can I protect myself from MEV?

The simplest defense is to keep your transaction out of the public mempool by using a private transaction service, or private RPC, such as Flashbots Protect or MEV Blocker, which send your trade directly to builders so predatory bots never see it. Switching is usually a one-line change in your wallet, and MEV Blocker even rebates recovered value to you. You can also trade large swaps on MEV-aware venues like CoW Swap, which settles trades in batches at a uniform price that removes the front-running advantage by design.

Can MEV be eliminated?

No, not fully. MEV comes from the value of controlling transaction ordering, which is built into how blockchains reach agreement, so any system that orders transactions will have some MEV. The realistic goal is not elimination but control: making the extraction transparent, reducing the predatory kind that harms users, and redistributing the value more fairly. Progress has been real, with sandwich attacks falling, protection tools spreading, and new designs that rebate MEV back to the users who create it, and the networks are working to make the underlying auction fairer still.

This article is educational and does not constitute financial or investment advice. The MEV landscape, including infrastructure, protective tools, and extracted-value figures, changes quickly and varies by data source. As of June 22, 2026, verify current details with official sources before relying on anything described here.

Ethereum’s most prominent MEV bot operator, Jaredfromsubway.eth, escalated his response to a $15 million honeypot exploit, offering the attacker a 50% white hat bounty to return the stolen ETH within 48 hours.

Jared first broke his silence on X, attributing the attack to weeks of preparation using fake token contracts and fabricated liquidity pools. The full mechanics have already been covered in detail.

A Reverse Honeypot Turned Ethereum’s Top MEV Bot Into a Target

Jaredfromsubway.eth posted on X, calling the incident a “reverse honeypot” and describing the attacker as spending weeks setting the trap. He acknowledged the irony of being targeted while insisting he remains the king of MEV.

The loss is significant for an operator whose bot generated tens of millions in peak revenues. His tone suggests the incident has not changed his plans to continue operating.

Jaredfromsubway Issues 50% White Hat Offer and 48-Hour Deadline

Jared also addressed the attacker directly, shifting from a general recovery bounty to a time-limited deal. He offered to let the attacker keep half the stolen funds in exchange for returning the other half within two days.

The ultimatum marks a direct escalation. Nevertheless, the offer leaves room for a quiet resolution outside formal legal channels.

June 2026 Marks One of Crypto’s Worst Months for Security

The Jaredfromsubway exploit is part of a broader surge. Attackers have struck more than 20 times across crypto networks this month alone, hitting bridges, deprecated vaults, and automated trading systems. A Thetanuts vault exploit earlier this month showed that deprecated DeFi contracts remain active attack surfaces long after operators wind them down.

However, broader conditions are compounding the risk. With leverage hitting 2021 levels and value locked declining, automated systems operate with a thin margin for error. Patient attackers who invest time in preparation are finding that MEV infrastructure carries outsized exposure.

The Exploit Adds to Ethereum’s Mounting Pressure in 2026

The incident also lands at a difficult moment for Ethereum more broadly. The Ethereum Foundation lost its second co-executive director this year, following at least eight senior departures since January. A former contributor warned that core development could face a $30 million funding gap within months. Investor Tom Lee dismissed those concerns as overblown.

Security incidents like large-scale MEV exploits reinforce scrutiny of Ethereum’s infrastructure. This comes at a moment when governance structures are already under pressure. Together, the events point to a network navigating multiple stress points heading into the second half of 2026.

The post Ethereum MEV King “Jaredfromsubway” Speaks Out After Massive $15 Million Exploit appeared first on BeInCrypto.

XRP News: Ripple has nine days to file a completed Digital Financial Assets Law application with California’s Department of Financial Protection and Innovation, and as of the most recent public records through March 2026, no Ripple entity appears on the DFPI’s list of DFAL applicants.

The company formally engaged the DFPI earlier this year, citing the July 1 deadline by name in written regulatory comments. The public record does not yet show a completed filing to match that engagement.

The distinction matters structurally. July 1 is not a soft guidance date or a suggested compliance window, it is the enactment date for California’s crypto licensing regime under the Digital Financial Assets Law, and the safe harbor provision requires a completed application on file, not a placeholder.

— WrathofKahneman (@WKahneman) June 19, 2026

Key date for @Ripple – July 1.

Key date for @Ripple – July 1.

Ripple previously engaged CA's DFPI for a DFAL license noting firms can keep operating if submit by 7/1/26. Public docs through March '26 don't list any Ripple entities, though likely filed. Necessary for all CA offerings, issue/redeem/custody. pic.twitter.com/xfQK4Z3IBc

For Ripple, the immediate consequence is operational: without a filed application or an approved license, RLUSD cannot legally be issued, redeemed, or custodied for California residents after that date. California is the world’s fifth-largest economy. This is not a peripheral market.

Discover: The Best Token Presales

DFAL Explained: What the July 1 Deadline Actually Requires

California’s Digital Financial Assets Law was originally enacted under AB 39 and subsequently amended.

The operative licensing date was pushed from July 1, 2025 to July 1, 2026 by AB 1934, signed by Governor Gavin Newsom in September 2024, a delay framed explicitly as runway for both regulators and firms to build out compliance infrastructure. That runway closes on July 1, 2026.

The DFPI began accepting DFAL applications via the Nationwide Multistate Licensing System on March 9, 2026. The framework prohibits any entity from engaging in, or even holding itself out as able to engage in, digital financial asset business activity with California residents unless it is licensed, has a completed application on file, or qualifies for a specific exemption.

That “holding out” language is broad: marketing materials, app availability, and website offerings directed at Californians can trigger DFAL obligations before a single transaction occurs.

— Liana (@lianavaragian) June 21, 2026

July 1 is a major deadline for Ripple and the broader crypto industry.

July 1 is a major deadline for Ripple and the broader crypto industry.

California's Digital Financial Assets Law (DFAL) takes effect on July 1, 2026.

Any company that exchanges, transfers, stores, or manages digital assets for California residents must either: Hold a… pic.twitter.com/vD29ORD4gp

Hold a… pic.twitter.com/vD29ORD4gp

The compliance cost is not trivial. The DFAL application fee runs $7,500 plus DFPI’s reasonable review costs, and a completed filing must include corporate structure documentation, financials, AML and CTF programs, governance frameworks, information security policies, and consumer protection disclosures.

Firms that miss the deadline and continue serving California residents face cease-and-desist orders, civil penalties, and potential criminal exposure under the California Financial Code, enforcement tools the DFPI has explicit authority to deploy.

For RLUSD specifically, the covered activities, issuance, redemption, and custody, are the core of Ripple’s stablecoin business. There is no partial compliance path here. The federal-level crypto regulatory calendar is adding further pressure on firms already managing multiple jurisdictional deadlines simultaneously.

XRP News: Ripple Engaged DFPI, But Has No License Application on Public Record

The gap between Ripple’s regulatory posture and its verifiable compliance record is the analytical center of this story. Ripple submitted formal written comments to the DFPI earlier in 2026, addressed to DFPI Regulations Coordinator Diana Pha.

In that letter, the company confirmed it understood the July 1 deadline, expressed support for the DFAL framework, and requested a specific amendment to Section 80.3002(a)(5) of the proposed regulations – asking that any entity holding a DFAL license be explicitly covered under that section, eliminating a requirement to maintain a separate Money Transmitter License in parallel.

That argument is substantively sound. Ripple currently holds more than 40 money transmitter licenses across the United States and is chartered as a limited purpose trust company by the New York Department of Financial Services, which directly regulates RLUSD.

Ripple’s position, that DFAL’s background check and oversight standards are in many cases more rigorous than a standard MTL, making dual licensing redundant, reflects the kind of engagement from a firm that understands what it is filing into.

The problem is that engagement in rulemaking and submission of a completed license application are two different acts.

XRP analyst WrathofKahneman flagged this discrepancy on June 19, 2026, noting that public DFPI documentation through March 2026 does not list any Ripple entity among DFAL applicants. His post drew 13,487 views and 88 reposts.

WrathofKahneman was careful to note that a non-appearance in public records does not confirm Ripple has not filed, filings may not yet be reflected in public disclosures, and assessed an application as likely given Ripple’s direct DFPI engagement. That is the accurate epistemic position. What the record shows is awareness and active participation in rulemaking. What it does not yet show is a completed application.

Discover: The Best Crypto to Diversify Your Portfolio

The post XRP Faces Major Legal Test in Californian Court: Will Ripple Survive July 1st? appeared first on Cryptonews.

Key Takeaways

- SPCX shares are sliding over 3% in early Monday trading, continuing a retreat from post-IPO highs reached earlier this month.

- Shares launched at $135 on June 12 and rallied strongly before dropping approximately 9% across the previous two trading sessions.

- Despite recent declines, SPCX remained 37% above its debut price through Thursday’s market close.

- KeyBanc launched coverage with Sector Weight, highlighting concerns over valuation multiples of 29x P/S and 71x EV/EBITDA.

- Wall Street consensus shows six Buy recommendations, with CFRA standing alone with a Sell rating.

SpaceX (SPCX) shares are experiencing a premarket decline exceeding 3% on Monday, hovering near $178 following consecutive losses of 5% and 3.6% on Wednesday and Thursday of last week.

Space Exploration Technologies Corp., SPCX

Shares reached $185 by Thursday’s closing bell — maintaining a 37% premium over the $135 IPO price — though the initial excitement surrounding the public debut appears to be waning. Many retail investors who entered positions following the June 12 listing have watched their profits largely disappear.

The company’s public offering became one of the most anticipated market events in recent history. Market capitalization briefly exceeded both Amazon and Microsoft during the initial trading days before retreating below both tech giants.

Financial reports show a $4.9 billion net loss for 2025, with an additional $4.28 billion loss recorded in Q1 2026. Optimistic shareholders are wagering on Elon Musk’s track record of building profitable ventures over time, despite current red ink.

Musk maintains a 42% ownership stake, subject to lock-up restrictions through June 2027. With approximately 5% of the total 13 billion shares available in the initial offering, trading volume remains constrained.

KeyBanc Raises Red Flags on Premium Pricing

KeyBanc launched coverage Monday with a Sector Weight designation — essentially a neutral stance. Analysts acknowledged SpaceX as “the dominant leader in space launch and space-adjacent verticals” while noting that current pricing offers balanced risk and reward.

Trading at approximately 29x price-to-sales and 71x EV/EBITDA based on 2027 projections, KeyBanc noted SPCX commands a significant premium compared to competitors in space technology, artificial intelligence, and communications sectors.

The research team identified Starship development as the critical factor to monitor. This next-generation launch vehicle is essential for deploying Starlink V3 satellites, reducing orbital delivery costs, and ultimately enabling space-based data centers. Starship’s thirteenth flight test is scheduled for June 29.

KeyBanc indicated it takes “a conservative approach” regarding development schedules, characterizing the coming 12–24 months as a “prove it phase.”

Revenue Stream Analysis

SpaceX operates through three primary divisions. Connectivity — anchored by Starlink — contributed 61% of 2025 revenue, producing approximately $11.4 billion with a robust 63% adjusted EBITDA margin. This division currently drives profitability.

The AI division, encompassing Grok and xAI operations following the February 2026 integration, continues operating at a loss. However, it has secured substantial contracts: an agreement with Anthropic valued at approximately $1.25 billion monthly, plus a separate Google partnership generating $920 million per month.

KeyBanc forecasts AI division revenue could surge to $50.6 billion by 2027. The challenge? Grok currently captures merely 3.1% of U.S. business adoption, trailing far behind Anthropic’s 41% and OpenAI’s 39.5% market share.

Current Wall Street consensus includes six Buy ratings on SPCX. CFRA remains the only firm maintaining a Sell recommendation. The upcoming Starship flight 13 on June 29 will serve as an important near-term milestone for investors.

Key Takeaways

- For the first time since 2000, SK Hynix momentarily surpassed Samsung Electronics in market valuation on Monday, both reaching approximately $1.35 trillion

- Export data from South Chungcheong Province shows Samsung’s HBM shipments increased 79% month-over-month in May, per Bernstein’s research

- Bernstein projects Samsung’s HBM revenue will experience 58% sequential growth in Q2 2026

- A 30% increase in Samsung’s “value per weight” metric during May indicates probable HBM4 production escalation, according to Bernstein

- While SK Hynix stock has jumped over 340% year-to-date, Samsung has posted a 200% gain

For over a quarter-century, Samsung Electronics maintained its position as South Korea’s largest company by market capitalization — that streak ended on Monday.

Samsung Electronics Co., Ltd., SMSD.L

SK Hynix temporarily claimed the top spot in market valuation, climbing 5.7% to reach 2,082.5 trillion won (approximately $1.35 trillion). Samsung followed closely at 2,081.3 trillion won, posting a modest 0.4% increase.

The valuation divergence between these semiconductor giants has intensified throughout the year. SK Hynix has skyrocketed more than 340% in 2026. Samsung’s approximately 200% appreciation, while substantial, reflects a widening performance gap.

This market cap reversal occurs as both chipmakers capitalize on artificial intelligence-fueled demand for high-bandwidth memory solutions. However, investors are increasingly favoring SK Hynix for its dominant position in HBM supply to AI semiconductor manufacturers.

Yet Samsung may be positioning for a comeback. Bernstein’s examination of South Korean trade statistics reveals that Samsung’s HBM shipments from South Chungcheong Province — its primary HBM packaging facility — soared 79% from April to May, representing a 55% increase compared to February levels.

Evidence of HBM4 Production Scaling

The acceleration in Samsung’s export numbers extends beyond simple volume metrics. Bernstein monitors a “value per weight” calculation that serves as a proxy for HBM pricing dynamics. Samsung’s reading climbed 30% in May while SK Hynix’s remained unchanged.

According to Bernstein, this pattern suggests Samsung is scaling production of HBM4 — its advanced-generation offering — rather than experiencing industry-wide price increases across all HBM products. Since HBM4 carries premium pricing, a product mix shift toward it would naturally elevate this indicator.

South Korea’s aggregate HBM exports reached unprecedented levels in May, advancing 13% month-over-month and 15% above February totals.

Bernstein’s current projections indicate Samsung’s Q2 2026 HBM revenue will expand 58% sequentially. While this represents robust growth, the firm acknowledges it remains below their internal expectations — potentially reflecting postponements connected to Nvidia’s Rubin platform timeline.

SK Hynix Maintains Advantage, But Samsung Gains Ground

SK Hynix’s May export patterns presented a contrasting narrative. Shipments from its North Chungcheong and Icheon facilities declined 9% versus April and dropped 3% compared to February. Despite this, Bernstein’s model anticipates 25% quarter-over-quarter HBM revenue expansion for SK Hynix in Q2, albeit marginally below the firm’s projections.

SK Hynix recently joined Samsung and Micron in achieving the $1 trillion market capitalization threshold during May, propelled by AI infrastructure demand.

HBM pricing remained stable throughout May despite significant fluctuations in traditional memory chip prices, which experienced sharp increases during the identical timeframe. HBM value per weight metrics maintained their established range, especially for SK Hynix.

Samsung’s stock advanced 0.14% on Monday. Micron (MU) surged 8.70% during the same trading session.

A tax proposal posted to the Ethereum Research forum by Kleros founder Clément Lesaege would let ETH validators vote to redirect up to 10% of staking rewards to public goods funding. If a majority of validators signal above zero, that rate becomes mandatory for every validator on the network, including those who voted for none.

For Bitmine (BMNR), which has staked 4.72 million ETH through its MAVAN platform and projects $258 million in annual net staking revenue, the exposure range is $50–100 million in lost income per year.

That figure is not speculative padding. It represents the direct arithmetic of applying a forced yield reduction to the single largest ETH staking position held by any public company. The proposal is still a forum post, not an EIP. That distinction matters – but so does the direction of travel.

Discover: The Best Token Presales

The ETH Validator Redirected Revenue Tax Proposal

Lesaege’s post, titled “Validator Redirected Revenue,” frames the mechanism as a solution to a coordination failure. According to his ETH tax proposal, Ethereum’s shared infrastructure generates value for everyone but is funded by no one in a structured, protocol-level way.

His proposed fix is a signaling system embedded in the consensus layer. Each validator declares a preferred redirect rate between 0% and 10% of their staking rewards. If more than 50% of total staked ETH signals are above zero, a single rate is selected and applied universally.

Now, a validator that voted for 0% redirection does not retain its full yield if the majority crosses the threshold, as it gets swept into the mandatory rate alongside everyone else. Funds flow automatically to an allocation smart contract, with a splitter routing capital to designated recipients such as Gitcoin, Octant, and audit organizations.

Lesaege explicitly described the post as a conversation-starter: “We seek further feedback before working on a technical implementation to put forth as an Ethereum Improvement Proposal.” As of now, no EIP number has been assigned.

A parallel mechanism called Validator Revenue Redistribution (VRR), presented by Ethereum Foundation researcher Devansh Mehta at EthCC, provides the technical plumbing layer. Mehta described the threshold dynamically, “If 51% put their flag up, all 100% of stakers have to part with a portion of their rewards.”

Discover: The Best Crypto to Diversify Your Portfolio

Bitmine’s MAVAN Platform: The $258M Revenue Thesis Exposed to Protocol Governance

Bitmine’s May 8-K reported 4,718,677 ETH staked via MAVAN, or 87% of its 5.42 million ETH total holdings and 4.49% of total ETH supply. The 7-day annualized yield at that date was 2.73%, against a CESR benchmark of 2.81–2.84%. At full deployment, Bitmine projects $296 million in gross staking rewards and $258 million in net staking revenues annually.

The math for a protocol-level redirect is straightforward. Each 1 percentage point reduction in effective annual yield on 4.72 million ETH costs approximately $94 million per year in gross rewards at an ETH price around $2,000.

However, a 10% redirect of the current 2.73% yield diverts 0.27 percentage points, translating to $25 million per year flowing away from BMNR’s validators. At this rate alone, the direct hit is meaningful but not existential.

The $50–100 million exposure range reflects a wider scenario set. If the mandatory redirect rate compounds with any secondary compression in overall validator economics like reduced participation incentives, institutional validators exiting to restaking or L2 yield strategies, or ETH price movement, the effective yield impact on 4.72 million ETH staked.

Staking revenue is not a secondary income line for Bitmine. It constituted more than 93% of quarterly revenue in Q2 FY2026, and the company declared a $0.01 annual dividend in January 2026. Bitmine is the first large-cap crypto company to do so, funded directly by staking income.

A material yield cut would pressure that commitment in a way that no operational decision by management can offset. The ETH validator tax is not a cost Bitmine can engineer around; it is a protocol-level deduction from the asset class itself.

Discover: The Best Token Presales

The post Kleros Founder’s ETH Tax Proposal Puts Bitmine’s $258M Revenue at Risk appeared first on Cryptonews.

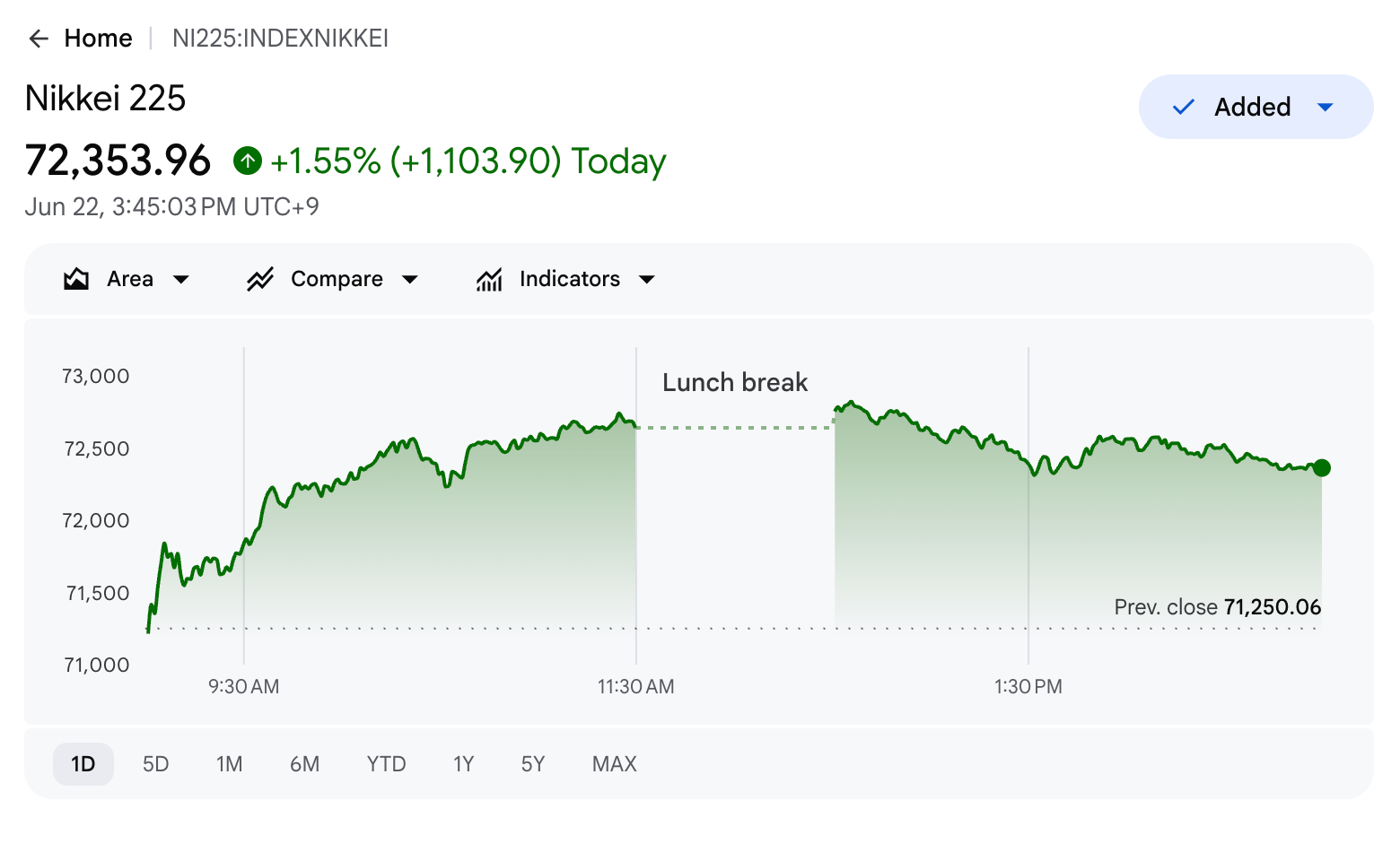

Japan’s Nikkei 225 recorded a new all-time high on Monday as the yen continued to slide.

The currency softened to 161.7 per dollar, just short of 161.96. A break past that mark would leave the yen at its weakest in nearly four decades and intensify pressure on Tokyo to respond.

Japan’s Nikkei Tops 72,000

Nikkei 225 closed at a record 72,353.96 on Monday, climbing 1.55% after hitting an intraday high of 72,831. The Topix rose 1.24% to 4,095.05.

The advance added more than ¥25.74 trillion ($156 billion) to the index’s market value, according to analyst Bull Theory. The rally extended across Asian equities, with South Korea’s KOSPI up 0.7% and China’s SSE Composite Index climbing 1.78%.

The advance followed constructive US-Iran talks in Switzerland, where technical negotiations will continue this week. Mediators Qatar and Pakistan confirmed progress, despite US President Donald Trump’s threats of military strikes.

Follow us on X to get the latest news as it happens

Yen Nears 40-Year Low

While stocks climb, Japan’s currency is heading the other way. The yen weakened to 161.7 per dollar, and a move past 161.96 would push it to its lowest point since 1986.

The decline persists despite Tokyo’s efforts to halt it. Japan spent a record ¥11.73 trillion ($73.4 billion) supporting the yen through late May.

Separately, the Finance Ministry’s reserve data showed the country’s foreign securities holdings fell by $75.6 billion from April to the end of May. That drop roughly matches the scale of Japan’s latest intervention to defend the currency.

The Bank of Japan has also tightened policy, lifting its benchmark rate to 1% from 0.75%, the highest since 1995. Higher rates typically support a currency, yet the yen’s weakness has continued regardless.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Japan’s Nikkei Hits Record High as Yen Slides Toward Its 1986 Low appeared first on BeInCrypto.

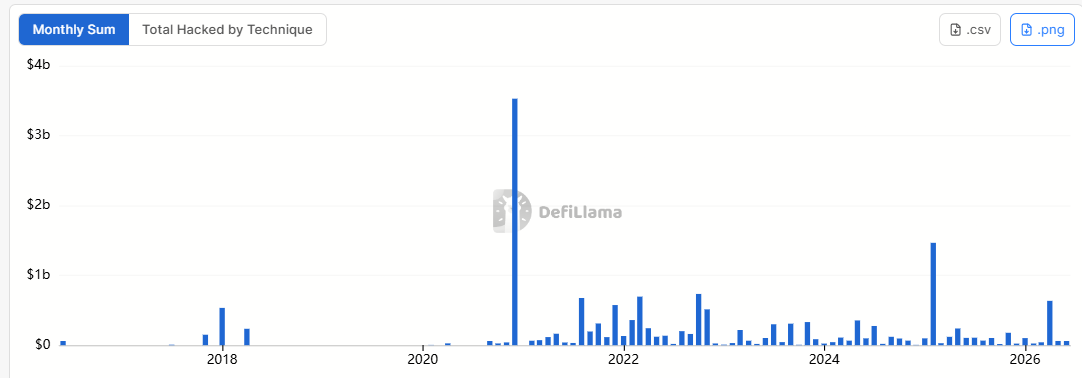

The second quarter of 2026 has already become the most-hacked quarter on record by incident count, with 83 exploits targeting cryptocurrency protocols, according to analysis by market insights platform Unfolded based on DefiLlama data.

However, the $755.3 million stolen during the quarter so far is significantly lower than the $3.56 billion lost in the fourth quarter of 2020, which remains the costliest quarter on record for crypto hacks.

KelpDAO’s $293 million hack and Drift Protocol’s $280 million exploit were the largest incidents of the quarter.

The figures suggest hacking activity is becoming more frequent, even as total losses remain below previous record levels.

Cryptocurrency hacks by monthly sum, all-time chart. Source: DefiLlama

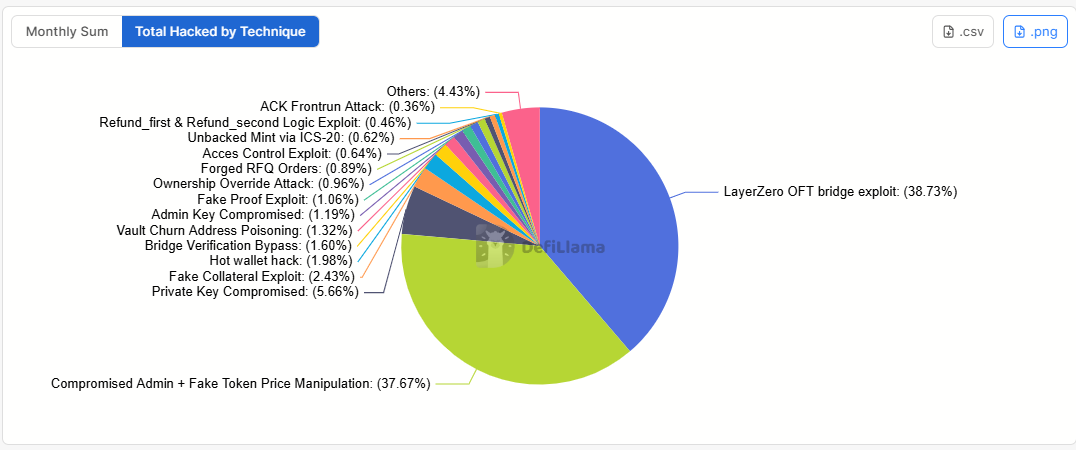

Bridge exploits emerged as leading attack vector in Q2 2026

Cross-chain bridge exploits emerged as the biggest attack vector of the quarter, with $351 million in value hacked from bridges alone.

The LayerZero OFT bridge exploit, which led to the $293 million KelpDAO hack, accounted for more than 38% of the value stolen during the quarter. Compromised admin attacks and fake token price manipulation accounted for 37% of losses, while private key compromises represented 5.66%.

Total hacked by technique in Q2 2026. Source: DefiLlama

Ethereum layer-2 blockchain Taiko was the latest network to suffer an exploit on one of its bridge protocols, as hackers stole $1.7 million by compromising Taiko’s chain state verification mechanism.

Related: Humanity Protocol’s $36M loss tied to suspected North Korean hackers: Quantstamp

Other notable incidents of the past quarter include the $36 million stolen from Humanity Protocol on June 8 and the $10.7 million exploit on THORChain on May 15.

Other recent incidents include two exploits on Aztec Connect’s abandoned smart contracts, each resulting in $2.1 million stolen and $1.3 million stolen from decentralized exchange Raydium earlier in June.

The incidents add to the ongoing debate about whether the development of new artificial intelligence models has reshaped the crypto industry’s security landscape, concerns that arose from the series of exploits in April.

During a recent interview, Mitchell Amador, the CEO of bug bounty platform Immunefi, told Cointelegraph that the proliferation of new AI models has shifted the cybersecurity playing field in favor of attackers, causing a “vulnerability apocalypse” that led to the resurgence in exploits.

Magazine: Coinbase hack shows the law probably won’t protect you — Here’s why

Key Takeaways

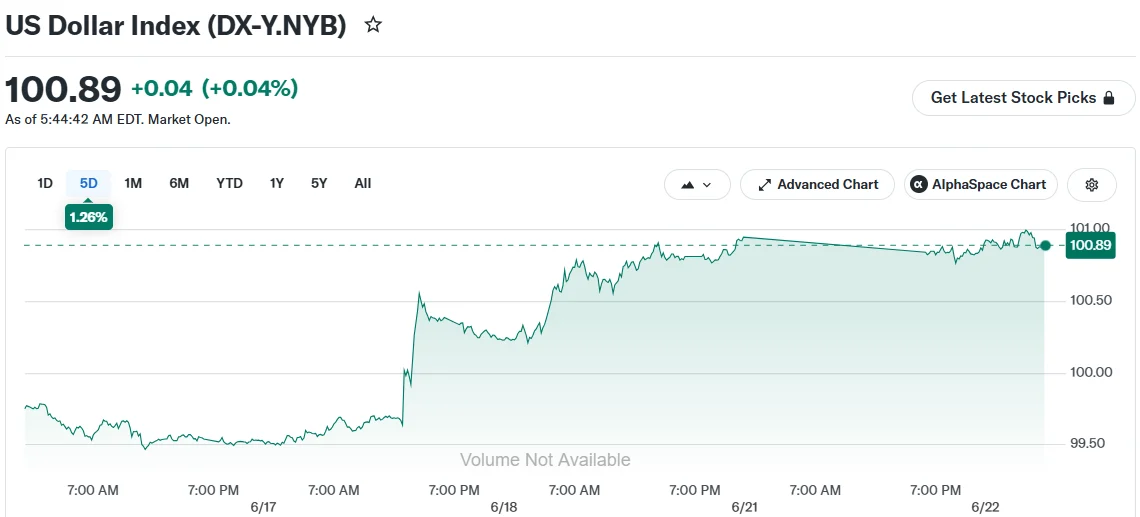

- The greenback maintained positions near 12-month highs amid growing expectations of Federal Reserve rate increases

- Japan’s currency weakened to approximately 161.73 per dollar, approaching its lowest point since the mid-1980s

- British Prime Minister Keir Starmer’s resignation announcement triggered downward pressure on sterling

- Diplomatic progress between Washington and Tehran on nuclear negotiations led to crude oil dropping almost 2%

- Market positioning data reveals bullish dollar wagers have reached approximately $30 billion, the highest in over a year

The US dollar continues to maintain strength near its highest point in twelve months as financial markets anticipate the Federal Reserve will implement interest rate increases. Meanwhile, Japan’s currency hovers dangerously close to a four-decade nadir, and political developments in Britain have pressured the pound sterling.

Following last week’s Federal Reserve policy meeting, central bank officials indicated the possibility of rate hikes materializing before year-end. This messaging prompted market participants to adjust their timing expectations for monetary tightening.

The dollar index, a benchmark measuring the greenback’s performance against a basket of six major global currencies, was hovering around the 101 mark. Year-to-date, the index has climbed nearly 3%.

Market speculators have significantly increased their bullish dollar positions. According to Commodity Futures Trading Commission data, these wagers have reached approximately $30 billion — representing the most substantial positioning in sixteen months.

Jeremy Stretch, who serves as head of G10 currency strategy at CIBC, indicated the dollar’s strength is likely to persist. He emphasized that market expectations for at least one Fed rate increase this year provide support for additional dollar appreciation.

Stretch further suggested that even aggressive action from the Bank of Japan may prove insufficient to halt the dollar’s advance against the yen.

Japanese Currency Approaches Four-Decade Weakness

The Japanese yen was changing hands at approximately 161.73 against the dollar during Monday trading sessions. A breach of the 161.96 level would mark the currency’s weakest position since 1986.

Satsuki Katayama, Japan’s Finance Minister, emphasized that government officials stand prepared to address currency market movements whenever necessary.

However, market observers remain doubtful about intervention effectiveness. Matt Simpson, a senior market analyst at StoneX, suggested Tokyo might feel “powerless” considering the substantial momentum driven by Federal Reserve rate expectations.

Japanese authorities deployed a record 11.7 trillion yen in market intervention efforts as recently as April 30. Despite this historic spending, those stabilization gains have been completely erased.

British Political Developments Impact Sterling

UK Prime Minister Keir Starmer announced his intention to step down on Monday, triggering a 0.1% decline in the pound to $1.322.

Andy Burnham, a Labour Party rival, has emerged as the leading candidate to succeed him. Burnham has reassured financial markets of his intention to maintain the United Kingdom’s existing fiscal framework.

Lee Hardman, an analyst at MUFG, noted this fiscal commitment has offered markets some comfort, helping to contain further sterling weakness in the immediate term.

Crude Prices Decline Following Diplomatic Breakthrough

Negotiations between the United States and Iran yielded a framework for reaching a comprehensive agreement within a 60-day timeline, according to statements from mediating countries Qatar and Pakistan. Oil prices responded with nearly 2% declines, pushing Brent crude down to $79.10 per barrel.

Iran simultaneously announced closure of the Strait of Hormuz, maintaining an element of market uncertainty.

Thu Lan Nguyen, an analyst at Commerzbank, observed that declining oil prices have not undermined dollar strength because interest rate expectations remain the primary market driver. Should crude prices rebound and intensify inflationary pressures, that development could further reinforce rate increase expectations — and consequently boost the dollar even more.

The dollar index touched a one-year peak of 101.127 on Friday before experiencing modest pullback during Monday’s trading.

Distributed AI training, validated for intercontinental workloads

Columbia University’s Department of Industrial Engineering and Operations Research has been involved in a research effort that, according to its organizers, demonstrates remote AI model training using GPU infrastructure located in Paraguay. The work is described as a first AI research project completed on HIVE Digital Technologies’ (NASDAQ: HIVE) GPU cluster in Asunción, with results submitted for consideration at NeurIPS, one of the largest machine learning conferences.

What the study claims

In the reported setup, researchers based in New York trained AI models on HIVE’s GPU infrastructure in Paraguay, a distance of more than 5,000 miles. The key theme is the feasibility of distributed AI training across geographies, where latency, network reliability, and software performance can materially affect training efficiency.

The organizers also say the study found that software optimizations allowed HIVE’s A40 GPU infrastructure to deliver performance that was comparable to newer-generation H100 systems once normalized for hardware capabilities. Normalization matters in these comparisons because raw throughput often varies by model, batch size, and the software stack, making apples-to-apples benchmarking difficult without explicit methodology.

Why NeurIPS submission matters

For the AI infrastructure market, peer-reviewed or conference-submitted research serves as a signal that performance claims are at least reproducible within a defined experimental framework. NeurIPS is typically used as a venue where methods, measurements, and system constraints are scrutinized by other researchers.

That said, the announcement describes a project completion and submission, not the final peer-reviewed acceptance of results. For investors and operators, the practical value will hinge on what eventually appears in the NeurIPS program, including details such as the models used, the distributed training configuration, the networking assumptions, and the definition of performance equivalence.

Intercontinental training as an infrastructure test

Beyond the headline GPU comparison, the underlying test is whether an intercontinental arrangement can support meaningful training workflows. Distributed training is typically constrained by more than compute availability. Network throughput and jitter, data movement patterns, and synchronization overhead can reduce the efficiency of scaling, especially when compute nodes are remote from model development and experiment management.

If the reported outcomes are consistent with the conference submission, they suggest that organizations do not necessarily need to locate training infrastructure next to their primary research teams to run distributed workloads. That can broaden the feasible footprint for compute capacity, including in regions where power, land, and data center expansion may be favorable.

Paraguay’s expanding role in compute availability

The announcement ties the research project to HIVE’s longer-term strategy of building GPU capacity in Paraguay using renewable power. Paraguay has drawn attention in parts of the energy and data center ecosystem for its hydropower-based generation mix, which can be relevant for power-intensive compute operations.

HIVE also describes additional infrastructure development, including a planned 100 MW substation in Yguazú intended to support a Tier III AI data center and high-performance computing campus. If completed as outlined, that would be designed to increase both the reliability and scale of power delivery for HPC and AI training workloads, which are often bottlenecked by electrical capacity and cooling requirements as much as by GPU count.

What this could mean for “sovereign AI” positioning

In the broader industry conversation, the idea of “sovereign AI compute” typically refers to building and operating compute capacity within a country or region, rather than relying entirely on external hyperscale cloud providers. For researchers and enterprises, the motivations can include data governance requirements, supply chain considerations, and resilience in procurement.

Distributed training over long distances, as described in this collaboration, could support a model where research teams remain in one geography while compute is provisioned elsewhere. Whether that becomes a mainstream workflow depends on cost, performance, and operational tooling, including orchestration, scheduling, and monitoring across networks.

Key points to watch next

- Conference details: When the NeurIPS submission is finalized, reviewers will be looking for clear methodology, model specifications, and the metrics used to compare A40 to H100 performance.

- Software and benchmarking scope: Performance comparisons that rely on “normalization” and “optimizations” should clarify what was changed and how generalizable the results are across workloads.

- Operational reproducibility: Distributed training results are strongest when they can be reproduced under different conditions, including varied network performance and dataset sizes.

- Infrastructure scaling: The next phase will likely center on whether planned power delivery and data center capacity translate into repeatable, enterprise-grade training availability.

Bottom line

The Columbia University collaboration described in connection with HIVE’s Paraguay GPU cluster adds to an emerging body of work focused on making AI training more flexible by decoupling where compute is located from where research occurs. For market participants, the most concrete validation will come from what ultimately lands in NeurIPS, particularly the technical specifics behind distributed training performance and the conditions under which newer-generation GPUs can be closely matched through software and system design.

Opinion: Fuel among top business concerns

What is MEV? Maximal Extractable Value, the invisible tax on crypto

‘Thank You, Dear Keir’: Reaction To Starmer’s Resignation Rolls In

-

Tech6 days ago

Tech6 days agoThe Adder At The Heart Of Intel’s 8087 FPU

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: Miami – Corporette.com

-

Entertainment2 days ago

Entertainment2 days agoRenter of Home in Anne Heche Crash Denies Settlement With Son

-

Business2 days ago

Business2 days agoSoccer-U.S. defends Iran World Cup travel restrictions, says discussions ongoing

-

Business2 days ago

Business2 days agoWall Street Week Ahead: Investors see Micron earnings as pulse check of AI rally momentum

-

Politics4 days ago

Politics4 days agoBBC Reporter Discusses Cross Party Criticism Of Trumps Iran Deal

-

Crypto World2 days ago

Crypto World2 days agoHIVE shares jump as $220M AI deal speeds Bitcoin mining pivot

-

Sports3 days ago

Sports3 days agoFIFA World Cup 2026: Canada beat 9-men Qatar 6-0 to register first ever win | FIFA World Cup 2026

-

Crypto World2 days ago

Crypto World2 days agoJake Chervinsky accuses CME of protecting derivatives monopoly

-

Crypto World2 days ago

Crypto World2 days agoCan Charles Hoskinson Really Rescue Cardano?

-

Business2 days ago

Business2 days agoMHP SE 2026 Q1 – Results – Earnings Call Presentation (OTCMKTS:MHPSY) 2026-06-20

-

Crypto World4 days ago

Crypto World4 days agoAnthropic’s Dario Amodei Urged AI Unity at G7, Even as US Banned His Models

-

Business4 days ago

Business4 days agoBrexit cost 6% of UK economy, Bank of England company data suggests

-

Crypto World6 days ago

Crypto World6 days agoRobinhood opens AI-powered trading to all users, sending HOOD stock past $100

-

Tech5 days ago

Tech5 days agoWeeks Of In-The-Field Testing And A Verdict

-

Politics2 days ago

Politics2 days agoAndy Burnham and the meaning of Makerfield

-

Tech4 days ago

Tech4 days agoAdobe adds its AI assistant to Premiere, Illustrator and InDesign

-

Crypto World4 days ago

Crypto World4 days agoIren (IREN) Stock Surges on Jefferies Buy Rating: AI Infrastructure Play Gains Momentum

-

Tech3 days ago

Tech3 days agoInstagram Now Lets You Add A Unique Caption To Each Carousel Slide

-

Crypto World5 days ago

Crypto World5 days agoCoinbase Stakes Out Brokerage Territory With SEC-Registered AI Advisor and Stock Options Push

You must be logged in to post a comment Login