Crypto World

US Dollar Strengthens as Japanese Yen Plunges to Four-Decade Low

Key Takeaways

- The greenback maintained positions near 12-month highs amid growing expectations of Federal Reserve rate increases

- Japan’s currency weakened to approximately 161.73 per dollar, approaching its lowest point since the mid-1980s

- British Prime Minister Keir Starmer’s resignation announcement triggered downward pressure on sterling

- Diplomatic progress between Washington and Tehran on nuclear negotiations led to crude oil dropping almost 2%

- Market positioning data reveals bullish dollar wagers have reached approximately $30 billion, the highest in over a year

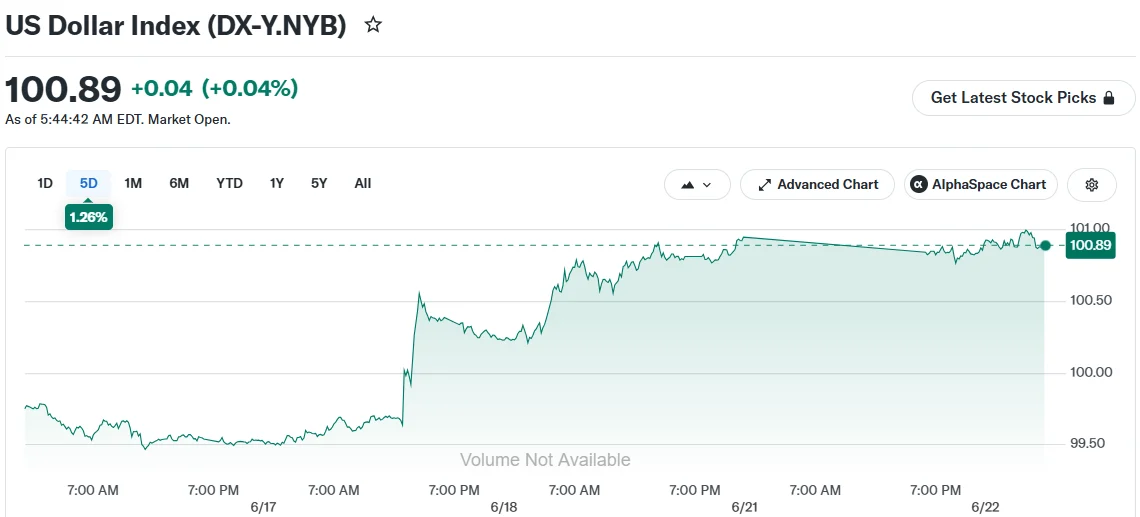

The US dollar continues to maintain strength near its highest point in twelve months as financial markets anticipate the Federal Reserve will implement interest rate increases. Meanwhile, Japan’s currency hovers dangerously close to a four-decade nadir, and political developments in Britain have pressured the pound sterling.

Following last week’s Federal Reserve policy meeting, central bank officials indicated the possibility of rate hikes materializing before year-end. This messaging prompted market participants to adjust their timing expectations for monetary tightening.

The dollar index, a benchmark measuring the greenback’s performance against a basket of six major global currencies, was hovering around the 101 mark. Year-to-date, the index has climbed nearly 3%.

Market speculators have significantly increased their bullish dollar positions. According to Commodity Futures Trading Commission data, these wagers have reached approximately $30 billion — representing the most substantial positioning in sixteen months.

Jeremy Stretch, who serves as head of G10 currency strategy at CIBC, indicated the dollar’s strength is likely to persist. He emphasized that market expectations for at least one Fed rate increase this year provide support for additional dollar appreciation.

Stretch further suggested that even aggressive action from the Bank of Japan may prove insufficient to halt the dollar’s advance against the yen.

Japanese Currency Approaches Four-Decade Weakness

The Japanese yen was changing hands at approximately 161.73 against the dollar during Monday trading sessions. A breach of the 161.96 level would mark the currency’s weakest position since 1986.

Satsuki Katayama, Japan’s Finance Minister, emphasized that government officials stand prepared to address currency market movements whenever necessary.

However, market observers remain doubtful about intervention effectiveness. Matt Simpson, a senior market analyst at StoneX, suggested Tokyo might feel “powerless” considering the substantial momentum driven by Federal Reserve rate expectations.

Japanese authorities deployed a record 11.7 trillion yen in market intervention efforts as recently as April 30. Despite this historic spending, those stabilization gains have been completely erased.

British Political Developments Impact Sterling

UK Prime Minister Keir Starmer announced his intention to step down on Monday, triggering a 0.1% decline in the pound to $1.322.

Andy Burnham, a Labour Party rival, has emerged as the leading candidate to succeed him. Burnham has reassured financial markets of his intention to maintain the United Kingdom’s existing fiscal framework.

Lee Hardman, an analyst at MUFG, noted this fiscal commitment has offered markets some comfort, helping to contain further sterling weakness in the immediate term.

Crude Prices Decline Following Diplomatic Breakthrough

Negotiations between the United States and Iran yielded a framework for reaching a comprehensive agreement within a 60-day timeline, according to statements from mediating countries Qatar and Pakistan. Oil prices responded with nearly 2% declines, pushing Brent crude down to $79.10 per barrel.

Iran simultaneously announced closure of the Strait of Hormuz, maintaining an element of market uncertainty.

Thu Lan Nguyen, an analyst at Commerzbank, observed that declining oil prices have not undermined dollar strength because interest rate expectations remain the primary market driver. Should crude prices rebound and intensify inflationary pressures, that development could further reinforce rate increase expectations — and consequently boost the dollar even more.

The dollar index touched a one-year peak of 101.127 on Friday before experiencing modest pullback during Monday’s trading.

A Hong Kong woman reportedly lost around $3.3 million after an online romantic partner directed her to a fraudulent cryptocurrency investment platform.

Summary

- 25 romance-linked investment scams were reported in Hong Kong between July 24 and 30.

- Combined losses from the cases approached nearly $9 million, according to local police statistics.

- One victim saw supposed returns of more than 800% before the platform blocked withdrawals.

- Hong Kong also recorded a 92.1% rise in online employment scams during early 2025.

Crypto romance scams cost victims nearly $9M

Hong Kong authorities recorded 25 investment fraud cases involving online romantic relationships during the week ending July 30, according to police statistics cited by Binance Square News.

The reported losses totaled nearly HK$70 million, or roughly $9 million. One case accounted for more than a third of that amount.

A 50-year-old insurance professional reportedly met a person online who presented himself as a car dealer. After establishing a romantic relationship, the person persuaded her to invest in virtual currencies through an unfamiliar platform.

The victim continued transferring money after the platform displayed rising account balances. By last month, it claimed that her portfolio had generated returns exceeding 800%.

However, the platform denied her withdrawal request. The purported romantic partner and an alleged investment adviser then stopped responding, leaving the woman with cumulative losses exceeding HK$26 million or around $3.3 million.

Authorities did not disclose which cryptocurrencies were involved or whether any of the transferred funds had been recovered.

Fake profits kept the victim investing

The case follows a common pattern in relationship-based cryptocurrency fraud. Scammers first build trust through dating applications, social media or messaging services before introducing an investment opportunity.

Victims are then directed to trading websites or applications controlled by the fraudsters. These platforms may display fabricated profits, allow a small initial withdrawal, or encourage victims to increase their deposits.

The scheme typically becomes apparent when a victim attempts to withdraw a larger amount. Operators may block the transaction or demand additional payments described as taxes, processing charges or penalties.

Hong Kong police urged investors to treat investment recommendations from newly established online contacts with caution. Warning signs include guaranteed returns, unusually high profits and requests to transfer funds through an unfamiliar platform.

The FBI describes the same method, saying criminals control the supposed investments and often steal all funds deposited by victims.

Hong Kong employment scams also surged

The romance cases add to a wider increase in online fraud affecting Hong Kong residents.

Police recorded 2,148 online employment scams between January and May 2025, up 92.1% from the same period a year earlier, according to figures reported by the South China Morning Post and HRD Asia.

Reported losses increased from HK$260 million to HK$480 million, an 89% rise. Authorities registered 621 cases in May alone, with 60% originating on WhatsApp and another 22% on Telegram.

Investigators attributed much of the increase to “click farming” schemes. Fraudsters initially pay participants small commissions for completing simple online tasks, such as following social media accounts or purchasing products to inflate a seller’s activity.

After gaining trust, scammers ask victims to commit larger sums for higher-paying assignments. Withdrawal attempts are then rejected, with operators claiming the victim made an error or damaged a company system and must pay a penalty.

US crypto fraud losses reached $7.2B

Similar investment schemes remain a major threat to US users. Cryptocurrency investment fraud produced $7.2 billion in reported US losses during 2025, making it the country’s largest category of financial loss reported to the FBI’s Internet Crime Complaint Center.

The FBI’s 2025 report said scammers commonly approach victims through social media, dating platforms and unsolicited messages before moving conversations to private messaging services.

US authorities advise victims to stop sending money immediately and preserve wallet addresses, transaction hashes, platform domains and communications. The FBI also warns against paying supposed recovery services, which may operate a second scam targeting people who have already lost funds.

Hong Kong police similarly advised users not to lower their financial safeguards because of emotional attachment or trust. Investors should independently verify platforms and avoid offers promising guaranteed or abnormally high returns.

One of the most recognizable and well-known figures in the cryptocurrency space has displayed a somewhat controversial approach to his Ethereum investments over the past few months.

The most recent data shared by Lookonchain doubled down on his sporadic approach, as he had realized another loss.

The analytics resource informed that the former BitMEX CEO deposited nearly 2,365 ETH into Cumberland and Galaxy Digital earlier today, and received 4.3 million USDC in return.

According to the analysts, this meant that his selling price was at $1,821 given the asset’s retreat over the past few days from a multi-month peak of $1,980.

Hayes secured a sizeable loss of $241,000 (or 5.3%) on this trade because he went on an accumulation spree during the aforementioned ascent from ETH. As previously reported, he bought 7,213 ETH for $13.87 million at an average price of $1,923.

Arthur Hayes(@CryptoHayes) bought high and sold low again!

Over the past 2 hours, he deposited 2,364.38 $ETH into Cumberland and Galaxy Digital, receiving 4.3M $USDC in return.

His selling price was $1,821, resulting in a loss of $241K (-5.3%).

He had previously bought 7,213… pic.twitter.com/4AVZpjANZD

— Lookonchain (@lookonchain) August 1, 2026

What’s interesting here is that this is not the first time Hayes has lost on ETH by buying high only to sell low weeks later. His previous major ETH trade was several weeks ago, when he accumulated at prices well over $1,900 again after the token jumped to $1,950.

Once it started to nosedive, though, Hayes was quick to sell off his stash at an average price of under $1,700. Thus, he incurred another major loss in just weeks, while ETH’s price rebounded shortly after.

The post Arthur Hayes Does It Again: Buys ETH High, Sells It Low appeared first on CryptoPotato.

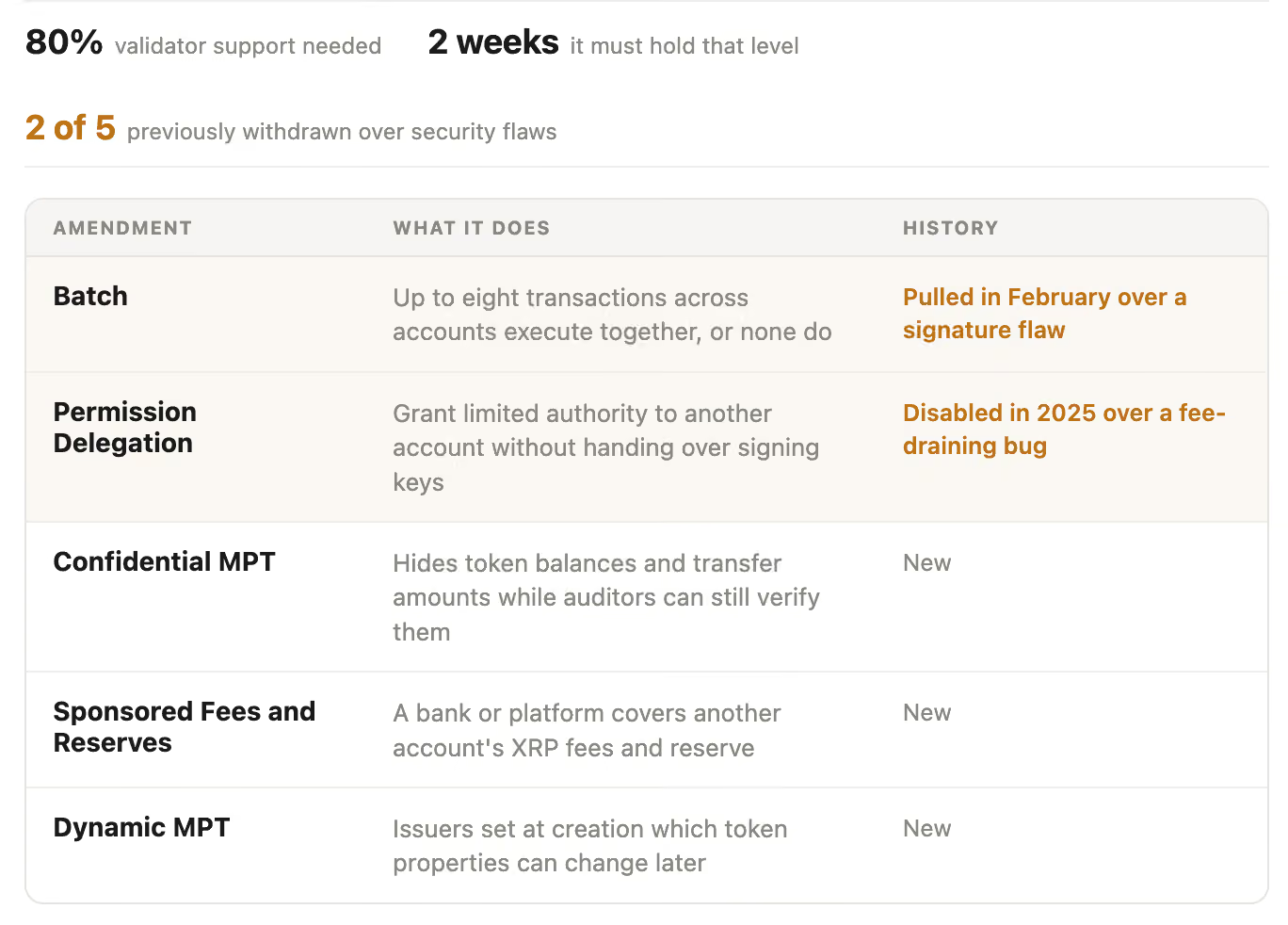

XRP Ledger developers are preparing five proposed amendments for the upcoming xrpld 3.3.0 release, targeting privacy, atomic settlement, and easier institutional onboarding.

Summary

- Five proposed amendments are expected to accompany the xrpld 3.3.0 software release.

- Confidential MPT would support private token balances and transfer amounts using cryptographic proofs.

- Batch transactions would enable delivery-versus-payment and atomic settlement across multiple accounts.

- Amendments require validator approval before they can activate on the XRP Ledger.

XRP Ledger v3.3.0 targets institutional transactions

Jazzi Cooper, head of product at RippleX, outlined the proposed changes in a post on X. The xrpld 3.3.0 release is anticipated next week, although releasing the software will not immediately activate its amendments.

“XRPL has already proven it can support tokenized assets at scale. Now it’s time to put these assets to use: global transfers, trading, collateralizing, and settling,” Cooper said.

She added that the five amendments would move the network closer to supporting those activities. The proposals cover confidential token transactions, transaction batching, delegated permissions, sponsored costs, and adjustable token properties.

Each amendment must pass through the XRP Ledger’s validator-governed approval process. Amendments affecting transaction processing generally need at least 80% support from trusted validators for two consecutive weeks before taking effect.

The upgrade follows the activation of fixCleanup3_2_0 on July 29. XRPScan data showed that the amendment received support from 30 of 35 participating trusted validators, equivalent to 85.71%.

Its activation made version 3.2.0 the minimum software release compatible with the updated mainnet rules. Nodes running version 3.1.0 or earlier became amendment-blocked and could no longer follow validated ledgers correctly.

Confidential MPT would add token privacy

Confidential MPT would add native privacy features for Multi-Purpose Tokens on XRPL. The proposal uses elliptic-curve encryption and zero-knowledge proofs to conceal token balances and transfer amounts while allowing authorized verification.

Issuers and holders could keep transaction data private from the public while granting access to a designated third party, such as an auditor or regulator. The arrangement is intended to balance commercial confidentiality with institutional reporting and compliance requirements.

“For financial institutions, privacy is often a prerequisite for using public blockchain infrastructure,” Cooper said.

The proposal could be relevant to US-regulated institutions evaluating public blockchains for tokenized assets. Banks, broker-dealers and asset managers often need transaction confidentiality while retaining records that can be reviewed by auditors or regulators.

However, the amendment would represent a network-level technical function, not regulatory approval for any specific financial product or activity.

Batch and delegated permissions support settlement

The proposed Batch amendment would allow transactions involving multiple accounts to execute atomically within one ledger. Either every part of the batch would succeed, or the entire operation would fail.

The structure can support delivery-versus-payment, where the transfer of an asset and its corresponding payment occur together. It could also reduce settlement risk in more complicated workflows involving several accounts or assets.

Permission Delegation would allow an account holder to grant narrowly defined transaction permissions without transferring control of the account’s signing authority. An institution could therefore authorize a treasury or operations team to perform specific tasks while keeping its issuance keys under separate control.

Sponsored Fees and Reserves would address another onboarding issue by allowing a bank, issuer, or platform to cover transaction fees and account reserves for users.

“Users continue to own their accounts and keys, while removing one of the biggest onboarding hurdles: requiring every participant to acquire and manage XRP before they can interact with the network,” Cooper said.

Dynamic MPT would make issued tokens adjustable

Dynamic MPT, the fifth proposed amendment, would let issuers modify selected token properties after issuance. Adjustable fields could include transfer fees, metadata, and other predefined features.

Issuers currently may need to create a replacement token when important terms require changes. Dynamic MPT is intended to provide limited flexibility without requiring an entirely new issuance, although the final amendment specifications will determine which properties can be changed.

The proposed features arrive as XRPL records increased tokenized real-world asset activity. RWA.xyz data showed that the network added approximately $2.6 billion in RWA value during the six months through July 26, excluding stablecoins.

That ranked XRPL second among tracked networks for net RWA inflows, behind BNB Chain at about $3 billion and ahead of Stellar at roughly $2.1 billion. XRPL’s combined distributed and represented RWA value reached approximately $4.38 billion.

Validator operators will be able to review the amendments as their specifications become available. Activation will depend on whether each proposal independently secures the required consensus after xrpld 3.3.0 is released.

Validators (entities that supply their resources to run and maintain a network) were advised to reject it, and an emergency server release marked it unsupported to prevent activation. No funds were lost, because it never reached the main network.

Permission Delegation, which lets an institution grant another account narrowly scoped authority without handing over full signing power, was disclosed as vulnerable in September 2025 and disabled.

The bug allowed one account to charge transaction fees to another and potentially drain its balance. The ledger’s documentation has listed both amendments as obsolete since, to be replaced by revised versions.

The other three are new. Confidential MPT combines zero-knowledge proofs, which let someone prove a statement is true without revealing the underlying data, with elliptic-curve encryption, so that balances and transfer amounts on Multi-Purpose

Tokens stay private while auditors or regulators can still verify them when required.

Sponsored Fees and Reserves lets a bank or platform cover another account’s XRP fees and reserve requirement, removing the need for every user to acquire XRP before transacting.

Lastly, Dynamic MPT lets an issuer specify at creation which token properties can be changed later, avoiding a full migration to a new token when fees or metadata need updating.

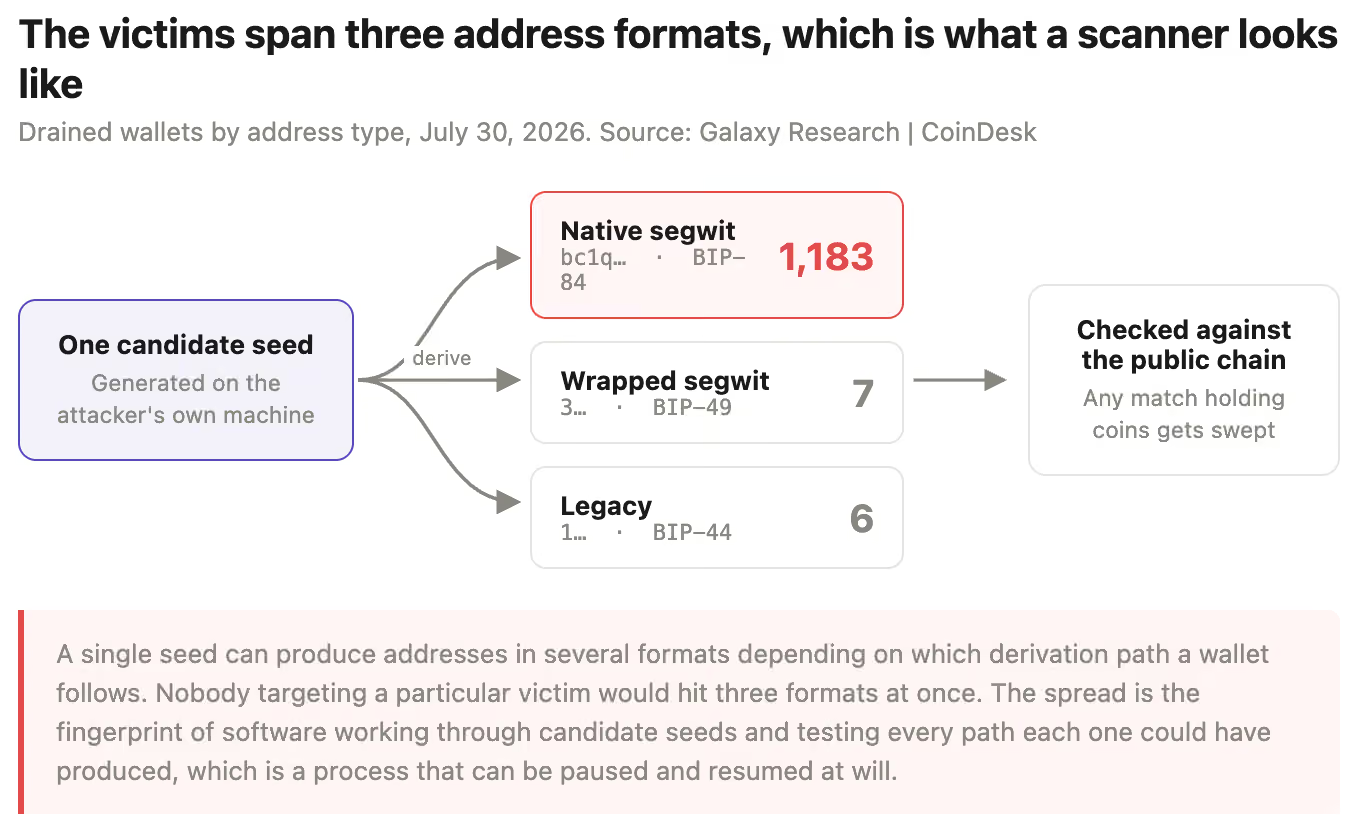

Every step of that runs on the attacker’s machine. The victim’s device is not involved at any point and could be powered off in a safe on another continent.

Galaxy’s breakdown shows the process running. Of the drained wallets, 1,183 used the modern native segwit address format, seven used an older standard and six an older one still. Nobody targets a specific victim across three address formats at once.

That is systematic enumeration, checking each candidate seed against every path it might have produced. The operator can widen the search, refine it and return whenever they choose.

Galaxy warned further waves are likely if owners do not move their funds.

Nor can an owner determine whether they are exposed. There is no test to run against your own wallet that reveals whether your seed sits inside the reproducible range.

Attack might not be fully finished

Coinkite, Coldcard’s maker, has warned Mk3 owners and says its newer devices are unaffected, while Block’s report places the Mk2, Mk4, Q and Mk5 in scope as well. Until that is resolved, anyone who generated a seed on the affected firmware has to assume the worst rather than verify it.

The attacker did make one mistake, however.

Block’s Clay Garrett said on X that the operator used a paid account at a “well-known blockchain data provider” to query the source addresses during the sweeps, and that the provider’s internal logs matched the suspected workflow with what he called extraordinary specificity, down to the number, timing and sequence of requests.

Bitcoin tried but failed at $65,000 on several occasions in the past week, and there are now multiple and different signals suggesting that another leg down is on the cards.

From war escalation to ETF withdrawals, let’s dive in.

Macro Factors

Let’s start with the Wednesday developments on US soil when the central bank decided to leave interest rates unchanged. At first glance, this doesn’t sound too bearish, right? After all, the alternative was to hike them, and there was a real possibility.

However, history shows that essentially all recent FOMC meetings, no matter what the outcome was, have been followed by a BTC price correction. Popular analysts have caught this rather negative pattern, which materialized with a $3,000 price decline over the past few days.

On the plus side, we can argue that the Friday correction to a 2-week low of $62,400 has priced in that almost mandatory post-FOMC retracement.

But there’s another macro factor that tends to harm risk-on assets like bitcoin: the war in the Middle East. Tension escalated over the past 24 hours, which included Iran reportedly striking tankers under US escort in the Strait of Hormuz.

Subsequent reports from the WSJ claimed that Trump has ordered a fresh attack on Iran to get it to surrender. According to CBS News, the US plans to attack Iranian energy assets, and this substantial escalation is expected to begin over the weekend.

Internal Reasons

The first in this section comes from the ETF behavior. The financial vehicles had a solid three-week run in which they attracted over $200 million in net inflows. However, the tides turned once again last week, with $61.53 million in net outflows. Friday was the day that changed the course, as investors pulled out over $265 million to reverse the $233 million in net inflows on Thursday.

Lastly, let’s explore a technical tool. Ali Martinez warned that the TD Sequential, a metric used to determine whether the underlying asset might reverse its price trend soon, has flashed a major sell signal on the 3-day chart.

The analyst added that this red sign comes as August begins, which has historically been associated with BTC pullbacks.

“History doesn’t have to repeat, but it’s a setup worth watching,” he added.

One for the Bulls

Let’s not begin the month only with negativity and review the opposite side of the coin. Michaël van de Poppe noted earlier that BTC could be primed for a major rebound due to its historical connection with the Nasdaq and South Korea’s KOSPI. Both major indices skyrocketed at the end of the business week, with KOSPI notching a massive 18% surge.

“The last time this happened, Bitcoin rallied to $83,000,” said van de Poppe. His expectation contrasts Ali Martinez’s warning for a weak start to August.

An enormous bounce on the Nasdaq and therefore a massive weekly candle, just as $KOSPI has bounced upwards.

I repeat, the last time this happened, #Bitcoin rallied to $83,000.

I would expect to see a strong start of August coming week for #Bitcoin as a response to the current… https://t.co/EJF8PcmOSI

— Michaël van de Poppe (@CryptoMichNL) July 31, 2026

The post BTC Price Warning: 4 Reasons Bitcoin Could Drop Further Next Week appeared first on CryptoPotato.

The broader crypto market posted some much-needed gains in July, and Ripple’s cross-border token extended a very impressive streak that began in 2020.

However, the new month is already here, and the past four Augusts weren’t very bullish for the asset. Can XRP defy its painful August performance, or is another leg down looming?

7 in a Row

Before we get to the four-in-a-row streak for August, let’s examine XRP’s most bullish one. Data from CryptoRank shows that the cross-border token has just equaled its best performance in terms of monthly gains. With the July 2026 edition coming with a minor 3% increase, this meant that eight Julys since 2014 (the first one after the asset saw the light of day) have been in the green out of 13. The only other month that has seen similar increases is April.

What’s even more favorable for the relationship between the altcoin and July, though, is its consecutive streak. As the subheading of this paragraph suggests, XRP managed to close its seventh July in a row with gains. This trend extends to July 2020, when the token skyrocketed by over 48%.

Other honorable mentions in terms of July gains came in 2023 (47.6%), 2024 (31.2%), and 2025 (35%). 2026’s minor 3% increase is quite modest, and in fact, it’s the lowest gain of all previous green Julys. The reason is the ongoing bear market, global uncertainty, inflation fears, and a few raging wars.

Nevertheless, Ripple’s coin still managed to rebound slightly from the June dump, when it plummeted by over 22%.

And Now The Bad News

Let’s get straight to it – the past four editions of the eighth month of the year have been in the red for XRP. In 2022, the asset fell by 13.6%. It dumped a lot harder a year later, losing 26.6% of its value. More modest but still red Augusts followed, with a 9.17% decline in 2024 and an 8.15% drop in 2025.

History shows that only four out of the 13 Augusts on record have ended higher for the cross-border token. Two of those brought massive gains: a 52% surge in 2017 and a massive 60% rise in 2021. Both of those took place during a bull market, something we are clearly not experiencing at the moment. Separately, the median data shows a 6.57% decline throughout previous Augusts, which is in stark contrast to the 6.91% gain for July.

The post Four in a Row: Will XRP Buck Its Bearish August Streak? appeared first on CryptoPotato.

Every twelve seconds, the Ethereum network asks a question that would have seemed absurd before 2022: who gets to write the next page of a $400 billion ledger, and how do you stop them from lying? The answer, for Ethereum and the majority of active blockchains by market value, is proof of stake, a consensus mechanism that replaced the energy-intensive puzzle-solving of proof of work with a simpler, older idea: put your money where your mouth is. Validators lock cryptocurrency as collateral, propose and verify blocks, and face the destruction of their deposit if they cheat. No mining rigs, no electricity arms race, no warehouse full of ASICs. Just capital at risk and code that enforces the consequences.

Summary

- Proof of stake secures blockchains by requiring validators to lock cryptocurrency as collateral, replacing the computational competition of proof of work with economic incentives and penalties.

- Ethereum’s September 2022 Merge was the largest proof-of-stake transition in history, cutting the network’s energy use by 99.95% while enabling a path to future scaling upgrades.

- The mechanism now underpins the majority of major blockchains by market cap, but carries its own risks: centralization of stake, slashing penalties, lock-up periods, and an evolving US regulatory landscape around staking services.

The idea predates crypto itself. Traditional finance has always understood that people with money on the line behave differently from people without it. Margin requirements, performance bonds, insurance deposits – the financial system is built on collateral as a behavior constraint. Proof of stake applied the same logic to distributed consensus: instead of proving you spent electricity (proof of work), you prove you have wealth locked up that the protocol can destroy if you misbehave. The mechanism was first described in a 2012 Peercoin whitepaper by Sunny King and Scott Nadal, spent a decade in Bitcoin’s shadow while proof of work dominated the conversation, and then became the consensus mechanism of choice for virtually every major blockchain launched after 2020. Ethereum’s adoption of it in 2022, the single largest infrastructure migration in crypto’s history, settled the debate about whether proof of stake could secure serious money. It can. It does. And the questions that remain are not about whether it works, but about the particular ways it concentrates, centralizes, and regulates differently from the mechanism it replaced.

The core mechanism: how validators replace miners

In proof of work, security comes from physical scarcity: miners burn electricity to find a hash that satisfies the network’s difficulty target, and the cost of that electricity is what makes attacks expensive. The security guarantee is thermodynamic. You cannot fake the work because the work is physics.

Proof of stake replaces this with economic scarcity. Instead of burning electricity, validators deposit tokens, their stake, into a smart contract controlled by the protocol. This stake serves three purposes simultaneously: it is the validator’s entry ticket (you cannot validate without it), their incentive (correct behavior earns staking rewards), and their punishment (incorrect or malicious behavior triggers slashing, the partial or total destruction of the deposit). The protocol’s security guarantee is economic: attacking the network requires acquiring and risking an enormous amount of the network’s own currency, and a successful attack would destroy the value of the very asset the attacker holds. The mechanism is self-referential by design. The thing securing the network is the thing the network produces, and that circularity is both the mechanism’s elegance and its most debated vulnerability.

The practical difference for the network is dramatic. Proof of work requires specialized hardware running continuously, consuming energy on the scale of a small country. Proof of stake requires a server, a stable internet connection, and the staked capital. Ethereum’s energy consumption dropped by an estimated 99.95% the day it switched, from roughly 78 terawatt-hours per year to the equivalent of a few thousand homes. The environmental argument for proof of stake is settled. The security argument is subtler, and understanding it requires walking through how a block actually gets produced.

The lifecycle of a block under proof of stake

Ethereum’s implementation, the most battle-tested proof-of-stake system by value secured, runs on a twelve-second heartbeat called a slot. Every slot, the protocol selects one validator to propose a block and a committee of validators to attest that the proposal is valid. The selection process uses a pseudorandom algorithm seeded by on-chain data, weighted by stake size: a validator with 64 ETH staked has twice the chance of selection as one with 32 ETH, but the randomness prevents anyone from predicting assignments more than a few minutes ahead.

The proposer assembles a block from the transaction pool, constructs it according to protocol rules, and broadcasts it. The committee members, typically several hundred validators per slot, then independently verify the block: they check that transactions are valid, that the proposer followed the rules, and that the block builds correctly on the chain’s history. Each committee member publishes an attestation, a signed vote that says “this block is valid and extends the chain correctly.” These attestations accumulate, and when enough are collected, the block is considered justified.

Finalization, the point at which a block becomes irreversible, takes longer. Ethereum uses a finality gadget called Casper FFG that finalizes blocks once two-thirds of the total staked ETH has attested to them across two consecutive epochs (each epoch is 32 slots, roughly 6.4 minutes). After finalization, reversing the block would require at least one-third of all staked ETH to be slashed, a cost that currently exceeds $35 billion. This is the concrete security guarantee: the price of rewriting Ethereum’s history is the destruction of tens of billions of dollars of capital.

The fork-choice rule, the algorithm validators use to decide which chain is the “real” one when they see competing versions, is called LMD-GHOST (Latest Message-Driven Greedy Heaviest Observed SubTree). It follows the branch with the most recent attestation weight, meaning the chain that the most stake has most recently voted for wins. Together, Casper FFG and LMD-GHOST create a system where blocks are produced quickly (every 12 seconds), justified within minutes, and finalized within roughly 13 minutes, with finality backed by the full economic weight of staked ETH.

Proof of stake vs proof of work: the real tradeoffs

The debate between proof of stake and proof of work is one of the oldest in crypto, and it is not as settled as either side claims. Both mechanisms solve the same fundamental problem, how to reach agreement in a network where participants do not trust each other, but they do so with genuinely different security models, and those differences produce different failure modes.

Proof of work ties security to the physical world. Mining requires electricity and hardware, both of which have real, external costs that cannot be faked or printed. An attacker needs to acquire 51% of the network’s hash rate, which means outspending the entire existing mining infrastructure. The cost of attacking Bitcoin is, roughly, the cost of all the mining hardware and electricity currently deployed to secure it, a cost that exists regardless of Bitcoin’s token price. This externality, security coming from outside the system, is what proof-of-work advocates consider its fundamental advantage: it anchors the digital to the physical.

Proof of stake ties security to the system’s own token. An attacker needs to acquire roughly one-third of all staked tokens (for finality-breaking attacks) or one-half (for censorship attacks), which means buying an enormous position in the network’s own currency. The attack is self-deterring because the act of attacking would crash the token’s price, destroying the attacker’s own holdings. But the security is circular: the network is secured by its token’s value, and its token’s value depends on the network being secure. Critics argue this creates a reflexivity problem that proof of work avoids. Defenders argue that the economic incentives are strong enough that the circularity is academic rather than practical.

The energy argument is overwhelmingly one-sided. Proof of work networks consume enormous amounts of electricity: Bitcoin alone uses an estimated 150 terawatt-hours per year, comparable to a medium-sized country. Proof of stake networks use a tiny fraction of that. Whether Bitcoin’s energy consumption is “wasteful” or “the cost of decentralized security” is a values question, not a technical one, but the gap in energy use is not debatable.

Hardware centralization cuts differently in each model. Proof of work has centralized around ASIC manufacturers (principally Bitmain) and regions with cheap electricity. Proof of stake centralizes around large token holders and staking service providers. Both mechanisms concentrate influence; they just concentrate it in different places. On Ethereum, Lido controls approximately 28% of all staked ETH as of mid-2026, a concentration that would be alarming in a proof-of-work context and is increasingly alarming in proof of stake as well.

Finality is the clearest practical advantage of proof of stake. Bitcoin transactions are never truly “final” in the mathematical sense; each new block makes reversal harder but never impossible, and merchants conventionally wait for six confirmations (roughly an hour) before considering a payment settled. Ethereum’s proof of stake provides deterministic finality: once a block is finalized by Casper FFG, reversing it requires destroying at least one-third of all staked ETH. The transaction is done, period, within roughly 13 minutes.

Why Ethereum switched: the Merge and what it changed

Ethereum’s transition from proof of work to proof of stake, called the Merge, occurred on September 15, 2022. It was the most complex and consequential upgrade in blockchain history: a live, $200 billion network switched its entire consensus mechanism without downtime, without a chain split, and without losing a single block. The execution was flawless, which tends to make people forget how extraordinary it was.

The Merge had been planned since Ethereum’s earliest days. Vitalik Buterin’s original roadmap always envisioned proof of stake as the endgame; proof of work was an interim measure while the research team, principally Vlad Zamfir and later the Ethereum Foundation’s consensus team, worked out the formal properties of a secure PoS protocol. The Beacon Chain, Ethereum’s proof-of-stake chain, launched in December 2020 as a parallel system running alongside the proof-of-work chain. Validators staked ETH on the Beacon Chain for nearly two years before the Merge merged the two systems into one.

What the Merge changed immediately: energy consumption dropped by 99.95%. Ethereum went from consuming roughly as much electricity as Chile to consuming roughly as much as a small town. Mining ceased entirely. GPU prices dropped as miners sold off their hardware. Ethereum’s environmental narrative reversed overnight.

What the Merge changed economically: issuance dropped by approximately 90%. Under proof of work, Ethereum issued roughly 13,000 ETH per day to miners. Under proof of stake, issuance fell to approximately 1,700 ETH per day to validators. Combined with EIP-1559’s fee-burning mechanism, which destroys a portion of every transaction fee, this made Ethereum’s supply dynamics deflationary during periods of high network activity. More ETH is burned than issued, and the total supply slowly decreases, a property no proof-of-work chain can replicate because miners need revenue to cover their physical costs.

What the Merge did not change: gas fees, transaction speed, and throughput remained the same. The Merge was a consensus-layer change, not an execution-layer change. Scaling improvements depend on layer-2 solutions, Arbitrum, Optimism, Base, and others, that settle batches of transactions on Ethereum’s mainnet. The Merge was a prerequisite for these scaling plans, because future upgrades like danksharding require proof of stake’s validator architecture to process data blobs, but the Merge itself did not make Ethereum faster or cheaper. The common misconception that the Merge would reduce gas fees was one of the most persistent communication failures of the entire project.

The landscape: which blockchains use proof of stake

Proof of stake is no longer an alternative; it is the default. The overwhelming majority of blockchains launched since 2020 use some variant of proof of stake, though the implementations differ significantly in their validator economics, finality properties, and centralization profiles.

Ethereum uses the Casper FFG and LMD-GHOST combination described above, with a minimum stake of 32 ETH per validator (approximately $110,000 at current prices). The high minimum creates a barrier to solo validation that has driven much of the staking volume toward pooling services. As of mid-2026, approximately 33 million ETH is staked, roughly 27% of the total supply, across over 1 million active validators.

Solana uses proof of stake combined with proof of history, a cryptographic clock that timestamps transactions before they enter consensus, enabling the network to order events without validators needing to communicate about sequencing. This architecture allows Solana to process thousands of transactions per second with sub-second finality, though it requires significantly more powerful hardware to validate than Ethereum, which introduces its own centralization pressures. Solana’s validator count is smaller and its hardware requirements higher, a deliberate tradeoff of accessibility for performance.

Cardano runs Ouroboros, a proof-of-stake protocol developed through academic peer review at the University of Edinburgh and IOHK. Ouroboros divides time into epochs and slots, uses a verifiable random function for leader selection, and was the first proof-of-stake protocol to be formally proven secure under a rigorous cryptographic model. Cardano’s approach prioritizes formal correctness over speed, a philosophy that has earned it both respect in academic circles and criticism for slower development velocity.

Polkadot uses nominated proof of stake, a system where nominators back validators with their tokens and share in both rewards and slashing risk. Polkadot’s unique contribution is its relay chain architecture, where a central chain provides consensus and security for multiple application-specific parachains that run in parallel. The staking mechanism secures not just one chain but an entire ecosystem of connected chains.

Cosmos, through its Tendermint BFT consensus engine, pioneered delegated proof of stake with instant finality. Tendermint produces blocks that are final the moment they are committed, with no possibility of reversal, a property that makes it especially suitable for financial applications. The Cosmos ecosystem’s hub-and-spoke model, where independent chains communicate through the Inter-Blockchain Communication protocol, has made it the backbone for dozens of application-specific blockchains, from the Osmosis DEX to dYdX’s order-book exchange.

Avalanche uses a novel consensus protocol based on repeated random sampling: validators poll random subsets of other validators about their preferences, and consensus emerges through the accumulation of confidence, similar to how snowflakes form through repeated crystallization, hence the consensus family’s name: Snowball, Snowflake, Snowman. The approach achieves sub-second finality and high throughput while maintaining a relatively low hardware barrier.

BNB Chain, Binance’s blockchain, uses proof of staked authority, a hybrid where a small set of 21 validators are elected through staking but also meet identity and reputation requirements. This is the most centralized of the major proof-of-stake implementations, trading decentralization for performance and the institutional backing of Binance.

Bitcoin remains the most prominent proof-of-work holdout, and its community has shown no inclination to switch. The Bitcoin argument against proof of stake is philosophical as much as technical: proof of work anchors security to the physical world, and that anchoring is considered a feature that proof of stake cannot replicate. Whether this position will hold indefinitely as the industry standardizes around proof of stake is an open question, but as of 2026, it holds firmly.

The risks validators and stakers actually face

The staking ecosystem has matured enough that its risks are well-documented, and they are not trivial.

Slashing is the mechanism’s enforcement tool: validators who provably violate protocol rules, principally by signing two conflicting blocks or attestations, lose a portion of their staked tokens. On Ethereum, the minimum slashing penalty is 1/32 of a validator’s stake, roughly 1 ETH, but the penalty scales with how many other validators are slashed in the same time period. If a single validator is slashed in isolation, the penalty is modest. If hundreds are slashed simultaneously, suggesting a coordinated attack or a catastrophic infrastructure failure, the penalties escalate toward total stake destruction. This correlation penalty is by design: it punishes systemic threats more than individual mistakes, but it also means that a bug in a widely-used validator client could trigger mass slashing of validators who did nothing individually wrong. The concentration of the validator ecosystem around a few major clients, principally Prysm and Lighthouse on Ethereum, makes this a non-theoretical risk.

Lock-up and unbonding periods vary by network but create real liquidity risk. Ethereum introduced withdrawals in April 2023 with the Shanghai/Capella upgrade, but the withdrawal queue can extend to days or weeks during periods of high exit demand. Other networks impose fixed unbonding periods: Cosmos chains typically require 21 days, Polkadot requires 28 days, and during those windows the staker cannot sell or use their tokens regardless of market conditions. A 28-day lock-up during a market crash is not a theoretical concern; it has happened.

Liquid staking protocols solve the liquidity problem but introduce smart contract risk. When you stake through Lido, your ETH goes into Lido’s smart contracts, and you receive stETH, a liquid token that represents your staked position. This stETH can be used across DeFi: lent, borrowed against, or provided as liquidity. But the arrangement is only as safe as Lido’s contracts. A bug or exploit in a liquid staking protocol could result in the loss of all deposited tokens, and because liquid staking concentrates enormous amounts of stake in single contract systems, the blast radius of such an exploit would be severe. Lido holds roughly $15 billion in staked ETH as of mid-2026; Rocket Pool, the second-largest, holds several billion more. These are among the largest smart-contract honeypots in existence.

Centralization pressure is the most debated long-term risk. On Ethereum, Lido controls approximately 28% of all staked ETH. If Lido’s governance were compromised or its operators coordinated, they could theoretically influence block production or censorship decisions for a significant fraction of the network. The Ethereum community has debated self-imposed caps on liquid staking dominance, and Lido has made governance decentralization changes, but the structural incentive favoring large staking pools, economies of scale, professional operations, integration with DeFi, has not changed. Proof of stake does not inherently centralize, but it centralizes differently from proof of work, and the patterns are already visible.

Validator MEV, the extraction of value from transaction ordering, affects proof of stake validators just as it affected proof-of-work miners, but the dynamics differ. Under proof of work, MEV accrued to miners who could order transactions within blocks. Under proof of stake, MEV accrues to the block proposer for that slot, and the MEV-Boost system, which allows proposers to outsource block construction to specialized builders, has created a sophisticated supply chain around transaction ordering. The relationship between validators, builders, relays, and searchers is complex, and the MEV flowing through this pipeline represents billions of dollars per year, revenue that disproportionately benefits sophisticated operators and further concentrates the staking economy.

Proof of stake and US regulation: where it stands

The US regulatory treatment of proof of stake is fragmented across multiple agencies, each approaching staking through a different lens.

The SEC’s interest in staking crystallized in February 2023 when it charged Kraken with offering unregistered securities through its staking-as-a-service program. Kraken settled for $30 million and shut down its US staking service. The SEC’s theory was that Kraken’s staking program, where users deposited tokens with Kraken and received yield in return, constituted an investment contract under the Howey test: users invested money in a common enterprise with an expectation of profit derived from Kraken’s efforts. The action targeted the service model, not the proof-of-stake mechanism itself, but it sent a clear signal that centralized staking services would face scrutiny. Coinbase challenged a similar SEC action and secured partial judicial skepticism about the SEC’s approach, but the legal landscape remains unsettled.

The tax treatment of staking rewards is the most practically consequential question for individual stakers. The IRS treats staking rewards as ordinary income, taxable at fair market value when received. This creates an immediate tax liability on tokens that may subsequently lose value. In 2023, a Tennessee couple won a partial victory in Jarrett v. United States, where the court accepted their argument that newly created staking rewards, like newly created property, should not be taxable until sold. The IRS refunded the Jarretts’ taxes but has not adopted their reasoning as policy, and the question remains unresolved. The practical implication: most tax advisors still recommend treating staking rewards as income at receipt, because the IRS’s position has not formally changed.

State-level regulation has been more accommodating. Wyoming’s blockchain-friendly legislation explicitly addresses staking as a permitted activity. Several states have introduced or passed legislation recognizing that operating a proof-of-stake validator is distinct from issuing securities. The patchwork of state approaches creates complexity but also creates jurisdictions where staking operations can operate with legal clarity.

The GENIUS Act and other proposed federal legislation may eventually clarify the regulatory framework, particularly around stablecoins and digital asset classification, but as of mid-2026, staking regulation in the US is primarily a product of enforcement actions and court decisions rather than comprehensive legislation. The gap between how the technology works and how regulators categorize it remains wide.

How to stake: the three paths and what each costs

For someone who has decided to stake, the choice comes down to three models, each with a distinct risk-reward profile.

Exchange staking is the simplest entry point. Coinbase, Binance, and other major exchanges offer one-click staking for supported tokens. You deposit your tokens, the exchange handles validator operations, and you receive rewards minus a commission, typically 10-25% of the yield. The advantage is simplicity: no technical knowledge, no hardware, no key management. The disadvantage is custodial risk: your tokens are held by the exchange, which means you are exposed to the exchange’s solvency, security, and regulatory risk. The collapse of FTX in November 2022, where customers lost billions in deposits, is the cautionary tale that hangs over every custodial staking arrangement. Exchange staking yields on Ethereum currently run 2.5-3.5% APR after the platform’s commission.

Liquid staking offers a middle path. Protocols like Lido, Rocket Pool, Jito (on Solana), and others accept deposits and return a liquid receipt token, stETH, rETH, JitoSOL, that represents the staked position plus accumulated rewards. The receipt token can be traded, used as collateral in lending protocols, or deposited into liquidity pools, allowing the staker to earn additional yield on top of staking rewards. This composability is liquid staking’s core advantage: your capital works twice. The risks are smart contract exposure (the protocol’s contracts hold your tokens), oracle risk (the receipt token’s exchange rate depends on accurate price feeds), and the possibility of depegging, where the liquid staking token trades below its theoretical value during periods of market stress, as stETH briefly did during the Three Arrows Capital collapse in June 2022. Liquid staking typically charges a 10% fee on rewards, yielding net returns of roughly 3-3.5% APR for Ethereum.

Solo staking is the gold standard for decentralization and the most operationally demanding option. On Ethereum, solo staking requires depositing 32 ETH (approximately $110,000 at current prices), running a validator node on dedicated hardware or a cloud server with reliable uptime, and maintaining the software through upgrades. The staker earns the full yield, currently around 3.5-4% APR, with no intermediary taking a cut, and keeps full custody of their withdrawal keys. The staker also contributes maximally to network decentralization, because each solo validator is an independent node that makes its own attestation decisions. The barriers are capital (32 ETH is a significant commitment), technical competence (running a validator is not difficult but requires ongoing attention), and responsibility (downtime means missed rewards and minor penalties, and a misconfigured setup risks slashing). Ethereum’s community actively encourages solo staking through resources like ethstaker.cc and various client diversity initiatives, recognizing that the network’s long-term health depends on maintaining a large base of independent validators rather than concentrating stake in a few large operators.

The decision between these paths is ultimately about what risks you are comfortable with. Exchange staking trades custodial risk for convenience. Liquid staking trades smart contract risk for capital efficiency. Solo staking trades operational burden for maximum independence. There is no universally correct choice, only the one that matches a given staker’s capital, technical ability, and risk tolerance, and the honest answer is that most people should start with the simplest option and graduate to more self-sovereign approaches as their understanding and commitment deepen.

Frequently asked questions

Is proof of stake safe?

Proof of stake secures hundreds of billions of dollars across Ethereum, Solana, Cardano, and dozens of other networks. Ethereum’s implementation has been live since the Beacon Chain launch in December 2020 and operating as the sole consensus mechanism since September 2022, without a consensus-level exploit. The main risks are not in the mechanism itself but in its surrounding infrastructure: smart contract bugs in staking protocols, centralization of stake among a few large operators, and the potential for correlated slashing events caused by validator client bugs.

Can you lose money staking crypto?

Yes, in several ways. If the price of the staked token drops, your position loses value regardless of staking rewards, and a 3% annual yield does not protect against a 50% price decline. Validators can lose tokens through slashing penalties if their infrastructure fails or is misconfigured. Staking through liquid staking protocols adds smart contract risk: a bug or exploit could result in the loss of deposited funds. And on networks with unbonding periods, you cannot sell during market downturns, potentially locking in losses.

How much can you earn staking crypto?

Annual yields depend on the network, the staking method, and market conditions. Ethereum staking yields approximately 3-4% APR as of mid-2026. Solana offers roughly 6-7%. Cosmos ecosystem chains range from 8-15% depending on the specific chain. Newer or smaller networks may offer higher rates to attract validators, but higher rates almost always correlate with higher risk: token volatility, smaller validator sets, less-audited code, and thinner liquidity for exits.

Does Bitcoin use proof of stake?

No, and the Bitcoin community has firmly resisted any suggestion of switching. Bitcoin uses proof of work, secured by an enormous global network of ASIC miners. The Bitcoin argument is that proof of work’s energy expenditure is not a bug but a feature: it anchors the network’s security to physical reality, costs that exist outside the system and cannot be manipulated within it. Whether this philosophical position will hold as the rest of the industry standardizes on proof of stake is an open question, but there is currently no serious proposal to change Bitcoin’s consensus mechanism.

What happens if a validator goes offline?

On Ethereum, validators that go offline lose a small amount of their stake through inactivity penalties, designed to be mild for short outages (a few hours or days of missed attestations cost a fraction of the rewards earned during normal operation) but significant for extended downtime. If a validator is offline for weeks, the inactivity leak accelerates to drain the validator’s balance until it falls below the minimum (16 ETH, the ejection threshold). Crucially, going offline is not slashing: validators are only slashed for provably malicious behavior like signing two conflicting blocks or attestations. The distinction matters because slashing is rare and severe, while brief offline periods are routine and their penalties are designed to be recoverable.

Disclaimer: This article is for informational purposes only and should not be considered financial or investment advice.

In April 2024, a single on-chain vote moved $165 million from Uniswap’s treasury into a two-year grants program. No CEO signed off. No board convened. A collection of token holders, pseudonymous and scattered across every time zone, debated the proposal on a forum, cast their votes through a smart contract, and the funds moved, automatically, irreversibly, exactly as the code specified. This is what a decentralized autonomous organization does: it replaces the corporate hierarchy of officers, boards, and bylaws with token-weighted voting and smart contracts that execute the results. Whether that replacement is an upgrade, a sidegrade, or a new category of organizational failure depends entirely on which DAO you examine and when you examine it.

Summary

- A DAO is an internet-native organization governed by smart contracts and token-holder votes, replacing traditional corporate hierarchy with programmable governance rules.

- DAOs manage over $30 billion in combined treasury assets across hundreds of active organizations, governing everything from DeFi protocols and investment funds to social clubs and collector groups.

- The model solves real coordination problems, particularly for open-source protocols with global stakeholders, but faces persistent challenges: voter apathy, plutocratic voting, governance attacks, legal ambiguity, and the fundamental tension between decentralization and decisiveness.

The concept emerged from a simple observation: if a blockchain can execute financial transactions without intermediaries, it should also be able to execute organizational decisions without intermediaries. The first serious attempt, confusingly named “The DAO,” launched on Ethereum in April 2016, raised $150 million in a crowdfunding campaign, and was drained of $60 million by an attacker who exploited a recursive call vulnerability in its smart contract within two months. The hack was so catastrophic that it split Ethereum itself into two chains, Ethereum and Ethereum Classic, and cast a shadow over the concept of decentralized governance that took years to lift. The shadow was worth remembering, because it established the central truth about DAOs: code is law until the code has a bug, and then the humans behind the code must decide what law actually is.

The model survived The DAO’s failure because the underlying need was real. Open-source protocols with billions in treasury assets, global communities of stakeholders who had never met, token-based economies that needed parameter adjustments, all of these required some decision-making mechanism, and the traditional options (a company, a foundation, a benevolent dictator) all introduced the centralization that the protocols were designed to avoid. DAOs became that mechanism, imperfect but structurally aligned with the decentralized systems they governed. By 2026, DAOs collectively manage over $30 billion in treasury assets across hundreds of active organizations, and the governance infrastructure, voting systems, delegation platforms, proposal frameworks, has matured into a small industry of its own.

The anatomy of a DAO: how token governance works

The standard DAO governance cycle has five stages, and understanding each reveals where the mechanism works and where it breaks.

The first stage is token distribution. Governance power in a DAO is represented by tokens, typically ERC-20 tokens on Ethereum, that grant voting rights proportional to holdings. How these tokens are distributed determines the DAO’s power structure from birth. Some DAOs airdrop tokens broadly to past users (Uniswap distributed UNI to every wallet that had ever made a swap). Others sell tokens in public sales, grant them to early investors and team members with vesting schedules, or distribute them through liquidity mining programs. The initial distribution is the most consequential decision a DAO makes, because it sets the electorate. A DAO where 40% of tokens are held by the founding team and investors is not meaningfully decentralized, regardless of what the governance documentation says.

The second stage is proposal submission. Any token holder meeting a minimum threshold can submit a governance proposal. On Uniswap, the threshold is 2.5 million UNI (roughly $15 million worth), a bar so high that most proposals are submitted by delegates, large holders, or protocol teams rather than individual community members. On smaller DAOs, the threshold may be as low as a single token. Proposals are typically structured documents specifying the action to be taken, the rationale, the implementation details, and the expected impact. They are published on governance forums, usually hosted on Discourse, Commonwealth, or Snapshot.

The third stage is deliberation. Before a formal vote, proposals are discussed in forums and on governance calls. This phase is the most important and the least automated: it is where arguments are refined, concerns are raised, alternatives are proposed, and the community’s actual preferences emerge. The quality of deliberation varies enormously between DAOs. Some, like MakerDAO (now Sky), have developed sophisticated governance frameworks with working groups, delegates, and structured feedback processes. Others are chaotic free-for-alls where discussions are dominated by a few vocal participants while the majority remains silent.

The fourth stage is the on-chain vote. Token holders cast their votes, weighted by the number of tokens they hold. Most DAOs use a simple token-weighted model: one token equals one vote. Some have experimented with quadratic voting (where the cost of additional votes increases quadratically, giving more weight to breadth of support over depth) or conviction voting (where the longer you stake your vote, the more weight it carries). The vote requires reaching both a quorum, a minimum level of participation, and a passing threshold, typically a simple majority or supermajority. Voting mechanisms include on-chain transactions (expensive, gas costs apply) and off-chain signature-based systems like Snapshot (free, but not binding without a separate execution step).

The fifth stage is execution. If the vote passes, the proposed action is executed. In the most mature DAOs, execution is automatic: the governance contract, typically a timelock controller like OpenZeppelin’s Governor or Compound’s GovernorBravo, queues the approved transaction and executes it after a delay period (usually 24-48 hours), giving the community time to react if something unexpected was approved. In less mature DAOs, execution may depend on a multisig, a set of trusted signers who manually execute the approved action, reintroducing human trust into a system designed to eliminate it.

The species: what kinds of DAOs exist

The DAO model has diversified into several distinct categories, each with different governance challenges and success metrics.

Protocol DAOs govern decentralized protocols and are the largest by treasury size. Uniswap DAO controls over $1.5 billion in treasury assets and governs the most widely-used decentralized exchange. Aave DAO manages the parameters of a lending protocol with billions in deposits: interest rate curves, collateral factors, risk parameters, and new asset listings. MakerDAO (now Sky) governs DAI, one of crypto’s most important stablecoins, making decisions about what assets can serve as collateral, what stability fees to charge, and how to manage the protocol’s balance sheet. These DAOs face the most consequential decisions, because governance failures can directly threaten the deposits of millions of users who never participate in governance themselves.

Investment DAOs pool capital from members to invest collectively. The LAO, MetaCartel Ventures, and Flamingo DAO pioneered the model, using token-based voting to make investment decisions that traditional venture capital structures handle through partnership agreements. The legal structure of investment DAOs is complex, typically involving a Delaware LLC wrapper and compliance with securities regulations, which limits most investment DAOs to accredited investors.

Social DAOs organize around shared identity or interests. Friends With Benefits (FWB) uses a token-gated membership model for cultural events, media projects, and community access. The token serves as both a membership credential and a governance instrument, and FWB has navigated the tension between exclusivity and decentralization more visibly than most social DAOs.

Collector DAOs pool funds to acquire high-value assets. PleasrDAO has acquired culturally significant NFTs and assets, including the original Doge meme photograph. ConstitutionDAO raised $47 million in a week to bid on a first-edition copy of the US Constitution at Sotheby’s auction in November 2021. ConstitutionDAO lost the auction but demonstrated the model’s fundraising power, and its aftermath, a chaotic refund process where gas costs consumed a significant portion of small contributors’ deposits, demonstrated the model’s operational limitations.

Service DAOs function as decentralized agencies or talent networks. Raid Guild coordinates web3 development projects, and its members vote on project acceptance, pricing, and revenue distribution. The model replaces the traditional agency’s management hierarchy with contributor-led governance, though it faces the challenge that client relationships and project management require responsiveness that token-based voting does not always provide.

The case studies: DAOs that defined the model

Three DAOs illustrate the spectrum of governance outcomes more clearly than any theoretical framework.

Uniswap DAO is the clearest success story, though even its success requires qualification. Since launching in September 2020, UNI governance has directed billions in treasury spending, deployed the protocol to over a dozen blockchains, managed the protocol’s fee switch debate (whether to direct trading fees to UNI holders), and funded a multi-year grants program. The governance process works, proposals are submitted, debated, voted on, and executed, but it works slowly and with low participation. Typical governance proposals pass with less than 5% of tokens voting. The effective governing body is a small number of large delegates, protocol team members, and active community participants, perhaps a few hundred people governing a protocol used by millions. The question of whether this is a decentralized organization or a representative democracy with extremely low voter turnout is left as an exercise.

MakerDAO, now rebranded to Sky, is the most ambitious governance experiment in crypto. Since its inception, MKR holders have governed every parameter of the DAI stablecoin system: stability fees, collateral ratios, debt ceilings, oracle configurations, and the onboarding of new collateral types including real-world assets like US Treasury bonds. In 2024, MakerDAO underwent a radical restructuring, rebranding to Sky and splitting into specialized SubDAOs, each focused on specific functions like lending, real-world assets, and growth. The restructuring was itself a governance decision, approved through the DAO’s voting process, making it perhaps the only example of an organization voting to fundamentally redesign itself while continuing to operate billions of dollars in financial infrastructure. Whether the SubDAO structure succeeds in solving Maker’s governance scalability challenges remains to be seen.

Arbitrum DAO illustrates governance’s failure modes. When Arbitrum launched its ARB token in March 2023, the foundation published a proposal requesting ratification of actions it had already taken, including the spending of $1 million. The community reacted furiously to what it perceived as retroactive governance theater: asking for a vote on something already done. The episode exposed the tension between operational speed (the foundation needed to act quickly) and governance legitimacy (the community expected to be asked first). Arbitrum has since developed a more structured governance process, but the early controversy established that DAOs cannot simply bolt governance onto an organization that was built to operate without it. The culture of governance must precede the mechanics.

The original sin: The DAO hack and Ethereum’s fork

No discussion of DAOs is complete without the event that gave the concept its first, and most brutal, stress test. The DAO, launched in April 2016, was a venture fund governed by token holders on Ethereum. It raised $150 million in a crowdfunding campaign, making it the largest crowdfund in history at that time, and it was hacked within two months.

The exploit used a reentrancy vulnerability in The DAO’s smart contract. The attacker called the withdraw function in a way that allowed them to withdraw their share repeatedly before the contract updated its balance, draining approximately $60 million worth of ETH, roughly one-third of The DAO’s holdings. The attack was not a hack in the traditional sense: the attacker did not break into a system or guess a password. They used the code exactly as written. The code allowed the drain; the code was law; and by the code’s own logic, the attacker had done nothing wrong.

The Ethereum community did not accept this argument. After intense debate, the network executed a hard fork, a retroactive change to the blockchain’s history, that reversed the theft and returned the funds to The DAO’s depositors. The fork was approved by the majority of the community but rejected by a minority who argued that “code is law” must mean something, even when the law produces unjust outcomes. That minority continued operating the unforked chain as Ethereum Classic (ETC), which still exists today.

The DAO hack established several principles that continue to shape DAO design. First: smart contract risk is existential, and no amount of governance sophistication matters if the contract holding the treasury has a bug. Second: the “code is law” ideology has limits that are tested by real money and real consequences. Third: decentralized governance is only as strong as the community’s willingness to act when the code fails, and acting requires the very centralized decision-making that decentralization is supposed to eliminate. The tension has never been resolved. It has only been managed, through audits, timelocks, bug bounties, and the hard-won institutional knowledge of a community that watched $60 million disappear into a recursive function call.

The failure modes: what actually goes wrong

A decade of DAO operations has produced a well-documented catalog of failure modes, and they are not the failures most people expect.

Voter apathy is the most pervasive problem. On paper, DAOs are governed by their entire token-holder base. In practice, they are governed by whoever shows up, which is usually less than 5% of token holders. Uniswap governance proposals routinely pass with a fraction of the total supply participating. Compound governance once had a proposal pass with votes from three wallets. The dynamic is structurally familiar: it is the same low-turnout problem that plagues democratic elections, intensified by the fact that governance tokens often have no direct economic incentive to vote (your token’s value is the same whether you participate or not) and each vote requires either a gas-cost transaction or the minor friction of signing a message.

Plutocracy is the flip side. One token, one vote means that governance power is proportional to wealth. A single whale holding 2% of a token’s supply can outvote thousands of smaller holders combined, and in practice, many important DAO votes are decided by fewer than ten wallets. Delegation systems, where small holders delegate their voting power to trusted representatives, partially address this, but delegates are themselves subject to capture and often represent narrow interests. The quadratic voting model, where each additional vote costs exponentially more, has been proposed as a solution but faces its own problem: sybil attacks, where one person splits their holdings across many wallets to circumvent the cost curve.

Governance attacks represent the most acute risk. In 2024, BonkDAO lost approximately $20 million when an attacker accumulated enough voting power to pass a proposal draining the treasury. The attack exploited the DAO’s low quorum requirements and the community’s governance apathy: by the time enough legitimate voters noticed the malicious proposal, it had already passed. The BonkDAO incident is the clearest illustration of a paradox at the heart of DAO governance: the same permissionless participation that makes DAOs open also makes them vulnerable to anyone willing to acquire enough tokens to cross the governance threshold.

Speed is a structural disadvantage. Corporate decisions happen in hours: a CEO convenes the relevant people, a decision is made, and execution begins immediately. DAO proposals typically require a discussion period (3-7 days), a voting period (3-7 days), and a timelock period (1-2 days), meaning even urgent decisions take one to three weeks to execute. During the March 2023 banking crisis, when USDC briefly depegged and MakerDAO needed to adjust its collateral parameters, the slow governance process was a real liability. Some DAOs have introduced emergency governance mechanisms, guardian multisigs that can act quickly in crises, but these mechanisms reintroduce centralization through the back door.

Legal ambiguity is the final persistent problem. Most DAOs have no legal entity, which means they cannot sign contracts, open bank accounts, hire employees, pay taxes, or defend lawsuits. When a DAO is sued, the question of who is liable, all token holders? The founders? The active voters?, has no settled answer. This ambiguity does not prevent DAOs from operating, but it creates a latent risk that grows as DAOs manage larger treasuries and interact more with the traditional legal system.

DAOs and US law: the liability question

The legal status of DAOs in the United States is evolving through a combination of state legislation, federal enforcement, and case law, with no comprehensive framework yet in place.

Wyoming became the first state to recognize DAOs as legal entities in 2021, passing legislation that allows DAOs to register as limited liability companies. A Wyoming DAO LLC provides its members with the same liability protection as a traditional LLC, shielding them from personal liability for the organization’s debts and legal obligations. The tradeoff is compliance: the DAO must designate a registered agent, maintain a Wyoming presence, and file annual reports. Tennessee and Utah have passed similar legislation, creating a small but growing number of jurisdictions where DAOs can operate with legal clarity.

Federal enforcement has taken a different approach. The CFTC’s 2023 action against Ooki DAO established that DAO token holders who actively participate in governance can be held personally liable for the DAO’s activities. Ooki DAO operated a decentralized margin trading platform without proper registration, and the CFTC argued that voters who participated in governance were functioning as the DAO’s operators. The ruling sent shockwaves through the DAO community: it suggested that merely voting on a governance proposal could expose a participant to regulatory liability. The practical impact has been chilling but selective, affecting DAOs that clearly operated in regulated financial activities while leaving non-financial DAOs largely unaffected.

The SEC has approached DAOs primarily through the lens of securities law. The SEC’s 2017 DAO Report, published after The DAO hack, concluded that DAO tokens sold to investors as part of a common enterprise with an expectation of profit may constitute securities. This framework has informed subsequent enforcement actions and created uncertainty around governance tokens that also carry economic rights, such as fee sharing, buybacks, or revenue distribution. The distinction between a governance token (which grants only voting rights) and a securities token (which grants economic rights) is legally significant but practically blurry: many governance tokens have both properties, and the SEC has not drawn a clear line.

Tax treatment compounds the complexity. The IRS has not issued specific guidance on DAO treasury distributions, but income received through DAO participation, whether through grants, contributor payments, or token distributions, is generally treated as taxable. DAO treasuries themselves exist in a tax gray area: they are not corporations, not partnerships, not trusts, and not individuals, and the appropriate tax treatment depends on the specific legal structure, if any, that the DAO has adopted.

For US residents considering DAO participation, the practical guidance is straightforward: participation in governance carries legal risk that scales with the DAO’s activities and your level of involvement. Registering as a DAO LLC in Wyoming or a similar jurisdiction provides liability protection. Active participation in governance of unregistered DAOs that operate in regulated financial markets carries the most risk. Passive token holding without governance participation carries the least, though even this is not risk-free in the wake of the Ooki DAO ruling.

DAOs vs corporations: the honest comparison

The comparison between DAOs and traditional corporations reveals that DAOs are not replacements for corporations in most contexts, but genuine improvements in a few specific ones.

DAOs excel at governing shared resources where no single party should have unilateral control. Open-source protocol treasuries, community funds, and parameter governance for decentralized financial infrastructure are the use cases where DAOs have proven most effective. The Uniswap protocol, used by millions and holding billions in user deposits, benefits from having its governance distributed across thousands of token holders rather than concentrated in a corporate board. The alignment of incentives, where token holders benefit from the protocol’s success, creates a governance model that is structurally resistant to the kind of extraction that corporate governance sometimes enables.

Corporations excel at speed, accountability, and operational execution. A CEO can make a decision in an hour, fire an underperforming employee in a day, and pivot the company’s strategy in a week. A DAO cannot do any of these things without a multi-week governance process, and the lack of formal employment relationships means that “firing” an underperforming contributor is a governance proposal rather than a management decision. The DAO model’s inefficiency is not a bug that will be fixed with better tooling; it is an inherent property of distributed decision-making, and any DAO that becomes efficient enough to operate like a company has, in practice, centralized its decision-making around a small group of active participants.