Crypto World

Trump to cash in by offering traders a sneak peak at his Truths

Donald Trump-founded Trump Media announced that Wall Street trading firms will be offered paid access to the president’s Truth Social posts before they’re shared with the public — a move that could be interpreted as selling insider trading information.

Specifically, firms will be able to pay for a Truth Social interface that grants “real-time access to posts from the highest-ranking Truth Social accounts” milliseconds before they’re published online.

Trump Media and Technology Group runs Truth Social, the social media app where President Trump’s account boasts 12.9 million followers.

Kathleen Clark, a conflict-of-interest expert at Washington University School of Law described the new services as “more brazen corruption,” and “an improper exploitation of government power to enrich himself.”

She added, “He’s selling expedited, privileged access to information about what he is doing as president.”

Read more: ANALYSIS: Mapping Donald Trump’s growing crypto empire

Trump Media is reportedly running at a loss, and hopes to boost its coffers by monetizing “proprietary assets” within the app.

Its new service will target multi-billion-dollar trading firms competing for increasingly early access to breaking news. Any amount of time they can claw back before news becomes public is key to making a profitable trade.

Truth Social claims that its data was already being copied by some firms, and that these third-party operations would be blocked by the company in favor of its own monetized access.

Trump administration a magnet for insider trading allegations

This paid-for access appears on its face to be a light form of insider trading from an administration that’s already been plagued with numerous allegations and investigations.

Indeed, reporting from CNN this week found Trump had used his Truth Social account to promote multiple big-name companies days after he had purchased hundreds of thousands of dollars’ worth of stock in said companies.

It claims that 20 different companies, including Nvidia, Tesla, and American Eagle, were promoted on his account days after he bought their stock.

Meanwhile, the US government’s long-time teleprompter was put on unpaid administrative leave after he allegedly made over $100,000 using Trump’s pre-written speeches to insider trade on prediction market Kalshi.

Gabriel Perez allegedly bet on dozens of prediction markets involving Trump speeches across a three-month period alone and was later flagged by the Commodity Futures Trading Commission.

The agency is reportedly seeking to settle with Perez, who has worked for Trump since 2016.

This is just one instance of the numerous signs of insider trading within Trump’s administration in relation to prediction market trades. Signs of insider trading also appeared in markets involving military actions against Venezuela’s Nicolás Maduro, and Iran.

Read more: Trump documents meltdown over Iran war on Truth Social

Insider trading and leaks are also allegedly taking place across futures oil markets, and also allegedly within ongoing US and Iran peace talks.

Drop Site reports that during these talks, Iranian officials warned Vice President JD Vance that Trump’s Special Envoy Steve Witkoff and his son-in-law, Jared Kushner, were exploiting insider negotiations to profit in financial markets, and risk undermining any deal.

Last month, Trump also pardoned Stephen Buyer, a republican who served almost two years in prison after he used insider information to trade stocks based on the around te merger of T-Mobile and Sprint.

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

XRP won. Seven years of legal limbo ended on a single Wednesday in March, when two agencies put it in writing. What almost nobody has noticed is what kind of writing it was, and how little it would take to unwrite.

Summary

- On March 17, 2026, the SEC and CFTC jointly issued a 68-page interpretive release naming XRP among the digital commodities that are not securities under federal law, ending seven years of ambiguity in one document.

- The release is binding on both agencies, which makes it far stronger than the staff guidance the industry lived on before. It is not a statute and not a formal rule.

- That places XRP’s legal status on the third rung of a four-rung ladder: staff guidance, Commission interpretation, formal rule, statute. A future Commission can reinterpret without asking Congress for anything.

- The interpretation does not replace the Howey test. It tells you what XRP is; it does not permanently settle how any particular offer or sale of it gets treated.

- Two things could upgrade it. The SEC’s Regulation Crypto rulemaking would turn interpretation into rule. The CLARITY Act would turn it into law. One is stalled in the Senate and the other is sitting at the White House awaiting review.

For most of a decade, the single most important fact about XRP was a question: is it a security? The question survived a four-year lawsuit, a split ruling, a $125 million penalty, and the end of the case itself, because none of those resolved the underlying classification for anyone other than Ripple. Then, on March 17, 2026, it stopped being a question. The Securities and Exchange Commission, joined by the Commodity Futures Trading Commission, published a joint interpretive release that named XRP outright as a digital commodity. Not a security. In writing, from both agencies, at Commission level. The most consequential American crypto policy document in years, and it arrived without a single vote in Congress. That last detail is the whole story, and it cuts in both directions.

What the March release actually did

The document runs 68 pages and carries Release Numbers 33-11412 and 34-105020. It sorts crypto assets into five categories: digital commodities, digital collectibles, digital tools, payment stablecoins, and digital securities. Only the last of those, meaning tokenized versions of traditional instruments such as stocks and Treasuries, sits fully under SEC jurisdiction. Everything else falls primarily to the CFTC or outside securities regulation entirely.

XRP is named in the first category. So are Bitcoin, Ether, Solana, Dogecoin, Cardano, Avalanche, Chainlink, Polkadot, Hedera, Litecoin, Bitcoin Cash, Shiba Inu, Stellar, Tezos, and Aptos. Press coverage generally counted 16 named assets; several SEC-filed prospectuses describe the list as 18, and the discrepancy appears to come from how the release’s examples are counted rather than from any dispute about XRP’s inclusion.

The test the release applies is worth reading closely, because it explains why XRP qualified. A digital commodity is an asset intrinsically linked to and deriving its value from the programmatic operation of a functional crypto system, together with supply and demand dynamics, instead of from the expectation of profits from the essential managerial efforts of others. That final clause is Howey’s language, inverted. XRP is a commodity precisely because the XRP Ledger runs without Ripple’s managerial effort determining its value. The thing XRP holders spent years arguing became the legal basis for the classification.

The release also addressed the mechanics that had been left dangling for years: how a non-security crypto asset may become subject to an investment contract, how it may cease to be subject to one, and how the securities laws apply to airdrops, protocol mining, protocol staking, and the wrapping of a non-security asset. It follows the SEC’s Crypto Task Force, stood up in January 2025, and Project Crypto, which became a joint SEC-CFTC initiative in January 2026, along with a memorandum of understanding announced days earlier.

Both chairs put their names on the shift in language nobody could misread. Atkins, speaking at the DC Blockchain Summit, said his agency is not the securities and everything commission anymore. Selig, for the CFTC, said the wait was over and committed to rules of the road that let the industry operate onshore.

Why this is stronger than people assume

The reflexive crypto reaction to any agency action is that it is worthless because the next administration undoes it. That reaction is lazy here, and the reason is a distinction most coverage skipped.

This is a Commission-level interpretation, not staff guidance. The difference is not cosmetic. Staff guidance represents the views of agency personnel and binds nobody, which is why the industry spent years being told that no-action letters and staff statements carried no legal weight. As Jenner and Block noted in its client alert, the March interpretation is binding on the SEC and the CFTC. The agencies have committed themselves, and the CFTC further committed to administering the Commodity Exchange Act consistently with the SEC’s reading. That is the strongest thing short of a rule.

The practical effects arrived immediately and are already load-bearing. Fund issuers began citing the release directly in registration statements: Grayscale and Hashdex prospectuses point to it as the basis on which their index constituents are not securities. Accredited investors and fund managers could reclassify holdings and adjust compliance programs without waiting for the GENIUS Act’s full implementation in November 2026. Exchanges listing named assets shed a category of risk they had carried since 2018. A framework that private capital has already built products on top of is considerably harder to unwind than a memo, because unwinding it now means breaking live registered products.

There is a political durability argument too. Reversing the classification of Bitcoin, Ether, and XRP would require a future Commission to explain why a functional ledger’s token became a security again, against its own recent 68-page reasoning, in the face of litigation from every issuer relying on it. Agencies can do that. They rarely enjoy it.

Why it is weaker than a law

Now the other side, and it is the reason this piece exists. Everything above describes strength within the executive branch. None of it describes permanence.

The interpretation is administrative action. It is not a statute. Any future administration can direct its agencies to reinterpret, and no congressional vote is required to do it. The current regulatory floor under XRP was created by two agency chairs and can be lifted by two different agency chairs. The industry spent 2018 through 2025 learning what it feels like when a Commission decides that the previous Commission’s posture was wrong, and nothing in the March release prevents that from happening again. It simply raises the cost.

The release also does not supersede Howey. Norton Rose Fulbright made the point plainly: the joint interpretation does not replace the Supreme Court’s test. It cannot, because an interpretive release cannot overrule the Court. What the agencies did was explain how they will apply existing law. A court hearing a private securities claim is not bound by the agencies’ view of the statute, and the security status of any specific asset still turns on the facts and circumstances of its offer and sale. The SEC said as much: an asset may cease to be linked to an investment contract as the relevant facts evolve, which is the same sentence read backwards.

That leaves a gap that matters for XRP specifically. The 2023 ruling in the Ripple case drew a line between programmatic sales on exchanges and institutional sales, treating them differently. The March interpretation classifies the asset. It does not immunize every transaction in that asset. An aggressive future enforcement posture would not need to declare XRP a security to cause problems. It would only need to find managerial effort in a particular offering.

And there is the awkward provenance question. The framework XRP holders are now relying on was produced by the same agency that spent four years litigating against Ripple and collected a $125 million penalty. That agency did not change its mind because the law changed. It changed its mind because its leadership changed. Which is precisely the argument for wanting something more permanent.

The ladder

The useful way to hold all of this is as a hierarchy of durability, because XRP’s status is not binary. It sits on a specific rung.

Staff guidance is the bottom. Non-binding, reversible by a memo, worth roughly what the issuing staff’s tenure is worth. This is what crypto had for years.

Commission-level interpretation is where XRP sits today. Binding on the SEC and CFTC, reasoned in public across 68 pages, relied upon in live registration statements. Reversible by a future Commission through the same instrument that created it, with no involvement from Congress and no notice-and-comment obligation.

A formal rule is the next rung, and it is the one currently in motion. The SEC’s Regulation Crypto proposal sits in the agency’s July 2026 rulemaking slot, under review at the White House Office of Information and Regulatory Affairs. Rules go through notice and comment, which is slow and irritating and precisely why they are hard to unwind. Reversing a final rule generally requires another full rulemaking, with a reasoned explanation that survives judicial review. Bankless made the observation that most outlets missed: the SEC has leaned on staff guidance and its taxonomy so far, but formal rules are far harder for a future commission to undo.

A statute is the top. The CLARITY Act would put the taxonomy into law, at which point unwinding it requires Congress, which is a body that struggles to pass anything at all. That difficulty is the feature.

So XRP holders currently occupy rung two of four, with rung three under White House review and rung four stuck on the Senate calendar with no floor vote scheduled and roughly three working weeks left before the August recess. That is the actual position, and it is neither the triumph nor the mirage that the two loudest camps describe.

The four years everyone forgot to price

There is a piece of history worth putting next to the March release, because it explains why the classification felt like an ending and why it is not one.

The SEC sued Ripple in December 2020, alleging XRP had been sold as an unregistered security. The case ran four years and produced a split ruling in 2023: sales to institutional buyers were investment contracts, while programmatic sales on exchanges were not, because anonymous buyers on an order book could not know whose effort they were relying on. Ripple ultimately paid a $125 million penalty and the litigation wound down in 2025. Exchanges delisted XRP for American users during the case and relisted after it. Billions in market value moved on procedural filings.

Notice what that outcome did and did not settle. It resolved claims against one company. It did not classify XRP for anyone else, which is why the question survived the case that was supposed to answer it. Every other market participant was left reading a district court opinion about someone else’s conduct and guessing. That guessing is what ended in March, and it ended not because a court ruled or Congress voted, but because agency leadership changed and the new leadership read the same statute differently.

That is the part worth sitting with. The law did not change between 2020 and 2026. The Securities Act of 1933 reads the same. Howey reads the same. The XRP Ledger runs the same consensus it ran when the lawsuit was filed. What changed was who occupied the chairs, and the outcome flipped from four years of litigation to a 68-page release naming XRP as a commodity in the first category.

Anyone who believes that dynamic runs in only one direction has not been paying attention. The same mechanism that delivered the win is the mechanism that could withdraw it, and it requires nothing more dramatic than another election and another appointment. This is exactly why the ladder matters, and exactly why the industry pushed for statute instead of settling for the agency’s blessing. A framework that can be reversed by a personnel change is not a framework. It is a truce.

The counterpoint, and it is a fair one, is that this cuts against the doom case too. If a hostile Commission could reclassify XRP tomorrow, it could also have done so at any point in the past decade and largely did try. The industry survived. Exchanges relisted. The asset persisted through the worst enforcement posture the SEC could produce, which suggests the practical downside of reinterpretation is a repeat of a period XRP already lived through and outlasted, not an existential event. The market has already stress-tested the bear case, and XRP is still here.

What this means for the price nobody wants to hear

XRP trades around $1.10 to $1.15, having reclaimed that support after a macro-driven rally cooled. A year ago it traded near $3.65. Analysts note that regulatory risk on Ripple has fallen to a multi-year bottom following the end of the SEC litigation, and demand from domestic funds has stabilized accordingly.

Both of those sentences are true simultaneously, and their coexistence is the most instructive fact about this market. The single largest overhang on XRP for seven years was legal uncertainty. That overhang has been removed more decisively than the most optimistic holder could have scripted in 2022: named, in writing, by both agencies, at Commission level. And the token is down roughly 70% from a year ago.

The honest conclusion is that legal clarity was necessary and is not sufficient. It removed a reason not to own XRP. It did not create a reason to own it. Those are different things, and the market has now run the experiment. Anyone still arguing that the next regulatory milestone is the catalyst has to explain why the biggest regulatory milestone in the asset’s history produced a lower price.

Which loops back to the ladder, and to why the rung matters even in a market that appears not to care. The value of moving from interpretation to rule to statute is not that it triggers a rally. It is that it removes the tail. As long as XRP’s classification rests on administrative action, an unknown future Commission holds an option to reopen a question that took seven years and $125 million to close the first time. Codification does not make XRP go up. It makes the worst case go away. In an asset that has spent a decade pricing legal risk, retiring the possibility of its return is worth something, and it is worth it quietly, over years, in the form of institutions that will hold it because they no longer need a legal opinion to do so.

What to watch

Three things, in order of how much they would change.

Regulation Crypto clearing OIRA and reaching public comment. The proposal is slotted for July. If it publishes and survives comment substantially intact, XRP moves from rung two to rung three, and the classification gets meaningfully harder to reverse. Watch whether the decentralization off-ramp language stays intact, since that is the provision doing the same work the taxonomy does.

The CLARITY Act reaching a floor vote before August 7. If it passes and is signed, the taxonomy becomes statute and the question closes permanently. If it dies, the entire American crypto framework rests on one agency’s interpretation and one agency’s pending rule, which is the outcome the industry spent a year lobbying to avoid.

Any enforcement action that tests the edges. The interpretation classifies assets. It does not classify transactions. The first case that alleges a specific XRP offering carried managerial effort, notwithstanding XRP’s commodity status, will show how much the March release actually protects. Until that happens, its practical strength is theoretical.

XRP won its argument. It won it in the weakest venue that could have delivered the win, from an agency that could deliver it because its leadership changed and could withdraw it for the same reason. Whether that victory is permanent is being decided right now, in a rulemaking review and on a Senate calendar, and almost none of it is being decided by anything Ripple does.

Disclaimer: This article is for information and educational purposes only and does not constitute financial, investment, or legal advice. It describes regulatory interpretations and pending rulemaking, both of which can change, and it is not a legal opinion on the status of any asset. Nothing here is a recommendation to buy or sell anything. Always do your own research. Information is accurate as of July 17, 2026.

Frequently Asked Questions

Is XRP a security?

No, according to the SEC and CFTC. On March 17, 2026, the two agencies jointly issued a 68-page interpretive release classifying XRP as a digital commodity, meaning it is not a security under federal law. The classification also covers Bitcoin, Ether, Solana, and roughly a dozen other named assets. The release is binding on both agencies.

Why does XRP qualify as a digital commodity?

Because the test asks whether an asset derives its value from the programmatic operation of a functional crypto system and from supply and demand, instead of from the expectation of profits from the essential managerial efforts of others. The XRP Ledger operates without Ripple’s managerial effort determining the token’s value, which is the argument holders made for years and which became the basis of the classification.

Can the SEC reverse this?

Yes, without asking Congress. It is administrative action, not statute. A future Commission could issue a new interpretation. What makes reversal costly rather than trivial is that this is a Commission-level interpretation binding on both agencies, publicly reasoned across 68 pages, and already relied upon in live registration statements filed by fund issuers, so unwinding it would mean disrupting registered products and inviting litigation.

Does the interpretation replace the Howey test?

No. An interpretive release cannot overrule a Supreme Court decision. The agencies explained how they will apply existing law, and the SEC noted that an asset’s security status still depends on the facts and circumstances of its offer and sale. A court hearing a private claim is not bound by the agencies’ view. The release classifies assets; it does not immunize every transaction in them.

How is this different from the Ripple lawsuit outcome?

The lawsuit resolved claims against one company and produced a split ruling distinguishing programmatic exchange sales from institutional sales, plus a $125 million penalty. It did not settle XRP’s classification for anyone else. The March 2026 interpretation classifies the asset itself, applies to all market participants, and comes from both agencies jointly.

What would make XRP’s status permanent?

Two things, in ascending order of durability. The SEC’s Regulation Crypto proposal, currently in the agency’s July 2026 rulemaking slot and under White House review, would convert interpretation into a formal rule, which requires another full rulemaking to reverse. The CLARITY Act would write the taxonomy into statute, which would require an act of Congress to undo.

If the legal question is settled, why is XRP down?

Because legal clarity removed a reason not to own XRP without creating a reason to own it. Regulatory risk on Ripple has fallen to a multi-year bottom and the token still trades near $1.10 against roughly $3.65 a year ago. The market has effectively run the experiment: the largest regulatory milestone in the asset’s history did not produce a higher price, which suggests the price is being set by broader market conditions instead of by classification.

Through an introduction with a “reputable third-party service provider,“ the company took on a developer who, as part of an investigation, was revealed to be tied to North Korea.

No. There is no official Robinhood Chain token, there is no airdrop, and there is no snapshot. Every token currently claiming that association is either a joke that admits it or a trap that does not.

Summary

- Robinhood has not issued a native token for Robinhood Chain. The network runs on ether for gas, which removes the main technical reason a chain needs a token of its own.

- Robinhood Markets trades as HOOD on Nasdaq. That equity is the only official way to own a piece of the company, and it is a stock, not a crypto asset.

- CASHCAT, the chain’s best-known token, is a community project with no affiliation to Robinhood. Its own website describes itself as fan fiction with a ticker.

- New tokens keep launching into the branding gap. STONKCAT opened a presale on July 16, and others are running alongside it.

- The absence of a token is the scam surface. Treat any airdrop claim, snapshot rumor, or official-looking token as false unless Robinhood confirms it through its own channels.

Ask the internet whether Robinhood Chain has a token and you will get a hundred confident answers, most of them wrong and several of them designed to be. The correct answer is short: no. Robinhood launched its blockchain on July 1, 2026 and did not issue a native token with it. What exists instead is a chain that runs on ether, a company stock that trades on Nasdaq, and a growing crowd of community tokens borrowing Robinhood’s branding without permission. Understanding why the chain has no token, and why that absence is precisely what makes the question dangerous, is worth more than any list of tickers.

The direct answer

Robinhood Chain has no official native token. There is no RHC, no HOODCHAIN, no chain coin.

The network is an Ethereum layer 2 built on Arbitrum’s Orbit stack, and it uses ether for gas. When you transact on Robinhood Chain, you pay fees in ETH, the same asset that secures Ethereum. That is a deliberate design choice and it is the single most important fact in this article, because gas is the primary reason most chains issue tokens at all. For readers new to the network, crypto.news has also explained the chain itself and its Stock Tokens.

The company’s only official tradable instrument is HOOD, the common stock of Robinhood Markets on Nasdaq. That is an equity: it carries shareholder rights, it is regulated as a security, and it is bought through a brokerage account. It is not a crypto token and it does not live on the chain.

Two other tickers cause confusion and neither is what people mean. USDG is the stablecoin used across Robinhood’s on-chain products, including as collateral for perpetual futures. It is not a Robinhood Chain token; it is a dollar stablecoin. LIT is the token of Lighter, the perpetuals exchange that partners with Robinhood Chain. Robinhood Ventures invested in Lighter and Lighter committed $11 million of LIT to the Robinhood community, which is a partner incentive and not a chain token.

So: ETH for gas, HOOD for equity, USDG for stable value, LIT for a partner protocol. No chain token.

Why the chain does not have one

Blockchains issue native tokens for three reasons, and Robinhood Chain has an answer for each.

Gas. A chain needs a unit to pay for computation. Most layer 1 networks mint their own. Robinhood Chain uses ether instead, inheriting Ethereum’s asset and its liquidity on day one. No new token required.

Governance. Some networks distribute tokens so holders can vote on protocol changes. Robinhood is a publicly listed brokerage running a chain as corporate infrastructure. It has shareholders and a board. It does not need a governance token, and issuing one would create an awkward second constituency with unclear legal standing next to the one that already owns the company.

Incentives. Chains hand out tokens to bootstrap usage. Robinhood has roughly 28 million customers across 38 countries and a distribution pipeline no new chain can match. It ran a 90-day gas fee subsidy instead, which achieves the same bootstrapping without issuing a security-shaped asset.

There is a fourth reason, unstated and probably decisive. Robinhood is a regulated broker with securities licenses in multiple jurisdictions. Issuing a token would invite an immediate question about whether that token is a security, from the same regulators who supervise its core business. The company has spent years building the relationships that let it offer Stock Tokens abroad and lending products at home. A native token would put all of that on the table in exchange for benefits it can already obtain without one.

The precedent supports the read. Coinbase’s Base, the most successful corporate chain to date, has no native token either, and Coinbase has repeatedly said it has no plans to issue one. Corporate chains built by regulated financial companies tend not to mint coins. That is the pattern, not the exception.

What CASHCAT actually is

CASHCAT is the token everyone means when they ask this question, so it deserves a direct treatment.

It is a community memecoin deployed on Robinhood Chain shortly after mainnet. It has a fixed supply of one billion tokens and its contract address is 0x020bfC650A365f8BB26819deAAbF3E21291018b4. It reached a market capitalization near $156 million within days and, at its peak, was worth roughly twelve times every tokenized real-world asset on the chain combined.

It has no affiliation with Robinhood. Not a partnership, not an endorsement, not a corporate project. The token’s own website says as much, disclaiming any connection to Robinhood Markets or to Vlad Tenev, and describing the project as fan fiction with a ticker. Asked what the utility is, the site answers that the utility is cat.

The name is where the confusion comes from, and it is a genuinely good story. Before Robinhood was Robinhood, Tenev and co-founder Baiju Bhatt called their company CashCat. The detail comes from a New Yorker profile and had been sitting in startup lore for years until someone realized it made a perfect memecoin. The token resurrects a discarded company name. That is the whole connection, and it is a connection of trivia, not of ownership.

What complicated matters is that on July 8, Tenev posted that while the company is building the chain to be the best for real-world assets, it works great for memes too, and he followed the token’s account. That is a CEO acknowledging something visible on his own network. It is not an endorsement, an affiliation, or a claim of ownership. But it is exactly the kind of signal that makes a retail buyer assume otherwise, which is why the disclaimer matters more than the follow.

The tokens filling the gap

The absence of an official token has not produced an absence of tokens. It has produced the opposite.

Within days of launch, Robinhood Chain hosted Cash Dog in Hood, Little John, Hoodrat, and Arrow, none of which existed before July 1. Noxa, the chain’s dominant launchpad, was averaging roughly 18,600 new token launches per day before it stopped accepting launches on July 11 and went dark two days later. Pump.fun added Robinhood Chain support on July 8, letting Solana’s memecoin crowd deploy without bridging. Crypto.news covered how memecoins took over the network as Robinhood’s RWA chain became dominated by speculative tokens.

The wave has not stopped. On July 16, STONKCAT opened a presale for $SCAT, pitching a community called The Litter and a running joke about a cat that never sells. A separate MemeToro presale is running alongside it, promising staking, AI-assisted launch tools, and prediction markets after the ecosystem expands.

Read the pattern rather than the individual tokens. Each new project borrows Robinhood’s branding, gestures at the chain’s legitimacy, and sells the association. None of them have the association. The branding gap that CASHCAT discovered is now a repeatable business model, and presales are where it converts fastest, because a presale asks for money before there is a market price to check.

How the scam works

This is the part worth internalizing, because the mechanics are predictable.

The airdrop rumor. New chains often reward early users with retroactive token distributions. Robinhood Chain will not, because there is no token to distribute. But the expectation exists, and it is exploited: posts claiming a snapshot has been taken, a claim window is open, or eligibility depends on connecting a wallet. Every one of those is false by construction. There is nothing to claim.

The official-looking token. A token deploys with Robinhood branding, a plausible ticker, and a website that mimics corporate design. It buys visibility. Retail buyers who have heard that Robinhood launched a chain assume this is the asset. It is not, and no amount of visual polish changes that.

The unaudited contract. CASHCAT itself illustrates the deeper problem: security audits of its contract were not possible because Robinhood Chain is too new for the tooling to have caught up. That applies across the chain. Tokens launching today are deploying into an environment where standard verification infrastructure does not yet exist, which removes the check that would normally catch a malicious contract.

Thin liquidity. CASHCAT’s trading pool has been worth far less than the token’s market capitalization, which means large trades swing the price hard in both directions. A nine-figure market cap sitting on a shallow pool is not a nine-figure asset. It is a small pool with a large number attached.

The defense is unglamorous and it works. Verify the contract address against a source you trust before buying anything. Assume any claim of official Robinhood affiliation is false unless Robinhood says otherwise on its own channels. Treat presales with more suspicion than listed tokens, since presales take money before price discovery. And accept the base case: there is no token, so there is nothing to be early to. That is also why understanding how token scams are structured matters before interacting with any new chain asset.

Why the question keeps getting asked

It is worth understanding why this particular question generates so much search traffic, because the answer explains the risk better than any warning does.

Crypto spent roughly four years training people that a new chain means a new token, and that being early to the token is where the money is. That training was accurate. Solana, Avalanche, Arbitrum, Optimism, and dozens of others issued native assets, and early participants in several of them did extraordinarily well. Airdrops turned unpaid testnet activity into five-figure windfalls. An entire behavioral pattern formed around it: hear about a new chain, find the token, get in before everyone else.

Robinhood Chain arrives carrying every signal that pattern responds to. It is new. It launched with a keynote. It is backed by a company with roughly 28 million customers and a Nasdaq listing. It has partners with real names, real volume, and real integrations. Every heuristic a crypto user has says there is a token here and being early to it matters.

There is not, and the mismatch between the expectation and the reality is the entire exploit surface. Scammers do not need to be clever when the audience has already convinced itself the thing exists. They only need to supply it. A token appears, the branding is close enough, and buyers who arrived expecting to find an official asset find something that looks like one. The pattern completes itself. That is why these tokens appear on new chains so quickly after launch.

The same dynamic explains why presales cluster here. STONKCAT opened a $SCAT presale on July 16 and a MemeToro presale is running alongside it, both pitching future products, staking, and ecosystem participation. A presale is the purest expression of the be-early instinct: it asks for money before there is any market price, any liquidity, or any way to verify what you bought is what was described. On a chain where audit tooling has not caught up, the ordinary checks that would flag a problem are also unavailable.

Notice too what the corporate structure means for anyone hoping the policy changes. If Robinhood ever issued a token, it would be a decision made by a listed company with a board, disclosed through filings and official channels, and scrutinized immediately by the regulators supervising its brokerage business. It would not leak through a countdown site or a Telegram group. The manner of any announcement would itself be evidence of whether it was real, and that is a more reliable filter than any list of red flags.

The uncomfortable framing worth sitting with: the reason there is no official token is the same reason the chain has institutional credibility at all. A regulated broker that minted a coin would be a different kind of company, facing a different set of questions, offering a different product. The absence people are searching for is not an oversight waiting to be corrected. It is the design.

What to watch instead

If the interest behind the question is genuine exposure to what Robinhood is building, three things are real and none of them are memecoins.

HOOD equity. The company’s stock is the direct instrument. Its crypto business is under real pressure, with transaction revenue down 47% year over year to $134 million in the first quarter of 2026 and native-app crypto volume down 48% to $24 billion. The chain is the response. Second-quarter earnings on July 29 are the first look at whether Stock Tokens are converting.

The chain’s real-world asset figure. This is the metric that matters and almost nobody quotes it. Tokenized real-world assets on Robinhood Chain total roughly $12.8 million against a network holding around $312 million in total value. If that number grows substantially while memecoin activity fades, the strategy is working. If it does not, the traffic never converted.

Whether the policy changes. Companies reverse themselves. If Robinhood ever does issue a token, it will announce it through its own channels, in filings and official communications, not through a countdown site. Until that happens, the answer to the question in the headline is the same as it was on July 1.

The honest summary is that the most valuable thing about Robinhood Chain having no token is that it tells you what kind of chain it is. Networks that mint coins are asking you to fund them. A network built by a listed brokerage running on someone else’s gas asset is asking you to use it. Those are different propositions, and only one of them has a ticker to chase.

The one number that answers everything

If you take a single thing from this article, make it this: the chain’s own scoreboard tells you whether any of it is working, and it is not the number anyone quotes.

Robinhood Chain holds roughly $312 million in total value locked. That figure gets cited constantly and it is close to meaningless, because value locked counts stablecoins parked, lending positions open, and assets sitting in automated market makers. It measures presence, not purpose. Transaction counts are worse, because a 90-day gas fee subsidy has been paying for activity since launch, which inflates the count and makes comparisons with chains like Base unreliable until the subsidy expires.

The number that means something is tokenized real-world assets: roughly $12.8 million, of which about $10.68 million is stocks and around $410,000 is Treasuries. That is approximately 4.1% of activity on a chain built entirely for that category. Every other metric on the network is measuring something the chain was not designed to do.

So the honest scorecard reads: enormous traffic, negligible product-market fit for the actual product, and a subsidy propping up the headline. That is not a verdict, because two weeks is not a verdict. It is a baseline. If tokenized assets grow well past $13 million while the memecoin volume fades, the speculation was the ignition sequence and Robinhood was right. If the assets stay flat while the traffic rotates to whichever chain is paying attention next, the chain attracted a crowd that was never going to convert.

Second-quarter earnings on July 29 are the first genuine look, because they will show Stock Token adoption from the company’s own books rather than from chain-level metrics that a subsidy is distorting. Watch that, and watch whether liquidity persists after the subsidy expires. Those two data points will tell you more than any token ever could, and neither of them requires you to buy anything.

Frequently asked questions

Is there an official Robinhood Chain token?

No. Robinhood has not issued a native token for the chain, which launched its public mainnet on July 1, 2026. The network uses ether for gas, which removes the primary technical reason a blockchain needs its own token. The only official way to own a stake in the company is HOOD, its common stock on Nasdaq, which is an equity and not a crypto asset.

Is CASHCAT the Robinhood Chain token?

No. CASHCAT is a community memecoin with no affiliation to Robinhood, no endorsement, and no partnership. Its own website disclaims any connection to Robinhood Markets or Vlad Tenev and describes the project as fan fiction with a ticker. The name references CashCat, the working name Tenev and co-founder Baiju Bhatt used before the company became Robinhood, which is a piece of trivia rather than a relationship.

Will there be a Robinhood Chain airdrop?

There is nothing to airdrop, because no token exists. Claims of a snapshot, a claim window, or eligibility requirements are false by construction and are a common scam pattern on new chains. If Robinhood ever changed this policy, it would be announced through official company channels and filings, not through a third-party claim site.

Why does Robinhood Chain not have a token?

Three technical reasons and one strategic one. Gas is paid in ether, so no new unit is needed. Governance runs through a listed company with shareholders and a board. Incentives come from roughly 28 million existing customers and a 90-day gas subsidy instead of a token distribution. Strategically, a regulated broker issuing a token would invite securities questions from the regulators supervising its core business.

Do other corporate chains have tokens?

Generally no. Coinbase’s Base, the most successful corporate chain to date, has no native token and Coinbase has repeatedly said it has no plans to issue one. Chains built by regulated financial companies tend not to mint coins, because the legal cost of doing so exceeds the benefit when the company already has distribution and a balance sheet.

What are USDG and LIT then?

USDG is a dollar stablecoin used across Robinhood’s on-chain products, including as collateral and quote asset for perpetual futures. LIT is the token of Lighter, the perpetuals exchange partnered with Robinhood Chain, in which Robinhood Ventures invested. Lighter committed $11 million of LIT to the Robinhood community as a partner incentive. Neither is a Robinhood Chain native token.

How do I avoid Robinhood Chain token scams?

Start from the base case that no official token exists, so any claim of one is false. Verify contract addresses against a trusted source before buying. Treat presales with extra caution, since they take money before any market price exists. Be aware that security audits are difficult on Robinhood Chain because the network is new enough that verification tooling has not caught up, which removes a check that would normally catch malicious contracts. Crypto.news has also explained verifying contracts before you transact as part of broader self-custody safety.

What should I look at instead?

If the interest is exposure to Robinhood’s strategy, HOOD equity is the direct instrument. If the interest is whether the chain is working, watch the tokenized real-world asset figure, which sits around $12.8 million against roughly $312 million in total value locked. Robinhood’s second-quarter earnings on July 29 are the first meaningful look at Stock Token adoption.

Disclaimer: This article is for information and educational purposes only and does not constitute financial or investment advice. Memecoins are highly speculative, frequently trade on thin liquidity, and most participants lose money. Token affiliations, contract addresses, and project claims change and should be verified independently before any transaction. Nothing here is a recommendation to buy any token or security. Always do your own research. Information is accurate as of July 17, 2026.

Augur has returned with a proposed resolution system and a two-month token migration test as prediction markets draw increased institutional scrutiny.

Summary

- Augur has returned with a decentralized layer for resolving disputed prediction-market outcomes.

- REP holders are testing the system through a two-month Moon Fork migration.

- Wall Street banks are tightening employee rules as insider-trading concerns grow.

According to a press release shared with crypto.news, the Lituus Foundation announced the relaunch alongside the Augur Lituus whitepaper, which outlines a settlement layer for prediction markets facing disputed outcomes. Under the proposed system, markets could resolve contested events without depending on a company, committee, multisignature wallet, or governance council.

Rather than opening another trading platform, the foundation plans to offer the resolution layer as infrastructure that other prediction markets and protocols could use. Its design separates the process of determining an outcome from services such as trading, liquidity management, user interfaces, and customer distribution.

The whitepaper also compares several decentralized oracle systems, focusing on how each one may perform when participants have a financial reason to influence a result. According to the foundation, Augur Lituus uses economic incentives intended to make support for an accurate outcome more rational than backing a false one.

“Prediction markets are only as credible as their resolution process,” Lituus Foundation co-founder Phill said.

“As markets become larger and more influential, the question isn’t whether they can predict the future. It’s whether they can determine what actually happened when billions of dollars depend on the answer.”

Augur is testing settlement through a live token fork

Alongside the whitepaper, Augur has started what it calls the Moon Fork, a public test of its dispute and algorithmic fork process. The exercise stems from a prediction market connected to NASA’s Artemis II mission, according to the foundation.

During the test, REP token holders must choose which version of the protocol to support by moving their assets within a two-month migration period. The foundation said tokens remaining in versions that participants abandon would lose their economic relevance.

Unlike an internal simulation, the Moon Fork involves financial incentives and public participation. The foundation said the process would test token migration, user coordination and behavior when competing versions of an event’s outcome exist.

Augur originally introduced its prediction-market model during Ethereum’s early development. Its system allowed users to create markets tied to real-world events, while REP holders participated in settling their outcomes through economic incentives.

The project’s renewed focus comes after prediction markets such as Polymarket and Kalshi attracted more users and attention. Many current platforms still depend on centralized operators or governance procedures to decide contested outcomes, according to the Lituus Foundation.

Institutional controls are increasing around event contracts

Prediction markets are also facing closer examination over how traders may use confidential information. As previously reported by crypto.news, Goldman Sachs, Morgan Stanley, JPMorgan Chase and Bank of America have introduced or revised employee policies covering event contracts.

Those restrictions are intended to limit insider-trading and conflict-of-interest risks on platforms including Polymarket and Kalshi, crypto.news reported. Employees may hold information about elections, economic releases, corporate decisions or geopolitical developments before it becomes public.

Goldman Sachs has prohibited staff from trading contracts connected to the bank, elections, financial markets, macroeconomic data and geopolitics. The bank adopted the rules as regulators and companies began paying closer attention to employee activity on prediction platforms.

While those controls concern who may trade and what information they possess, Augur’s proposed system addresses a separate part of the market: how a disputed contract is settled after the underlying event has occurred. The foundation has not provided a launch date for general use of the Lituus resolution layer.

SBI Holdings has acquired a majority stake in Coinhako after receiving regulatory approval for the Singapore transaction. The deal strengthens the Japanese financial group’s digital asset presence across Southeast Asia. Coinhako will operate as a consolidated subsidiary following the transaction’s completion on July 16.

Regulatory Approval Clears Coinhako Acquisition

The Monetary Authority of Singapore approved the acquisition before the companies completed the deal. SBI Holdings funded the transaction through its Singapore-based investment unit, SBI Ventures Asset Pte. Ltd. The group also purchased shares from several existing Coinhako investors as part of the transaction.

Neither party disclosed the investment amount, acquired ownership percentage, or Coinhako’s valuation. However, the majority position gives the Japanese financial group control over the exchange’s operations. Coinhako will retain its Singapore base while joining SBI Holdings’ consolidated financial network.

Coinhako operates through Hako Technology Pte. Ltd. and entered Singapore’s cryptocurrency market in 2014. The company holds a Major Payment Institution licence from the Monetary Authority of Singapore. Its affiliate, Alpha Hako Ltd., also maintains regulatory registration in the British Virgin Islands.

Singapore Exchange Expands Regional Crypto Network

SBI Holdings plans to combine Coinhako’s customers with its financial services and international digital asset operations. Singapore provides established regulations and direct access to expanding cryptocurrency markets across Southeast Asia. Coinhako also offers licensed infrastructure, local expertise, and an existing regional distribution network.

Chairman and President Yoshitaka Kitao linked the acquisition to plans for connecting exchanges across several countries. The proposed network could support cross-border trading and reduce restrictions caused by different national currencies. SBI Holdings expects Coinhako to hold a central position within that international exchange structure.

The companies plan services involving stablecoins, tokenized assets, cross-border trading, and on-chain finance. Coinhako co-founder Yusho Liu described the agreement as the company’s next stage after ten years in Singapore. The exchange gains access to SBI Holdings’ banking, securities, investment, and digital asset businesses.

Tokenized Products Support Wider Asia Strategy

SBI Holdings is also developing JPYSC, a yen-backed stablecoin, with blockchain company Startale. The group may connect the stablecoin with Coinhako’s services and established regional customer network. This integration could support payments, settlements, and transactions involving tokenized financial instruments.

SBI Holdings has also partnered with Ondo to distribute tokenized investment products through its customer network. Separately, SBI Global Asset Management launched the JX token with regulated real-world asset exchange DigiFT. The Solana-based product gives eligible investors exposure to a Japanese high-dividend equity strategy.

Coinhako adds a regulated Singapore platform to SBI Holdings’ expanding digital asset infrastructure across Asia. The exchange complements the group’s stablecoin development and recently launched tokenized investment products. SBI Holdings now controls a regional gateway linking Singapore customers with its wider financial network.

Digital asset and AI infrastructure company Galaxy Digital has signed a 15-year naming rights agreement with Texas Tech, renaming the university’s football stadium Galaxy Stadium beginning with the 2026 season.

The partnership also makes Galaxy the official data center and digital assets partner of Texas Tech Athletics, with the companies planning to collaborate on student-athlete name, image and likeness opportunities, artificial intelligence initiatives and workforce development programs.

According to Friday’s announcement, the stadium will debut under its new name on Sept. 5, when Texas Tech opens its season against Abilene Christian. Financial terms of the agreement were not disclosed.

The deal expands Galaxy’s footprint in West Texas, where it operates the Helios data center campus in nearby Dickens County, about 60 miles east of Lubbock. The site has 1.6 gigawatts of approved capacity for artificial intelligence and high-performance computing (HPC).

Related: Bitdeer stock jumps 14% as company expands US mining hardware production

Texas strengthens its crypto industry footprint

The partnership comes as Texas strengthens its position as a hub for the crypto industry, combining major Bitcoin mining investment with growing political influence and pro-crypto legislation.

The state is already home to some of the industry’s largest Bitcoin (BTC) miners and digital infrastructure operators, including Riot Platforms, Cipher Mining, Core Scientific, CleanSpark, IREN and Hut 8.

In February, Bitcoin mining hardware maker Canaan acquired a 49% stake in three operating Texas mining facilities from Cipher Mining for nearly $40 million, while earlier this month, MARA Holdings announced plans to acquire a 2-gigawatt powered site in Texas to develop a digital infrastructure campus supporting both HPC and Bitcoin mining.

Recently, Texas has become a focal point for crypto-backed political spending. In May, industry-affiliated political action committees spent more than $10 million supporting candidates in Texas congressional primary runoffs, with all six backed candidates winning.

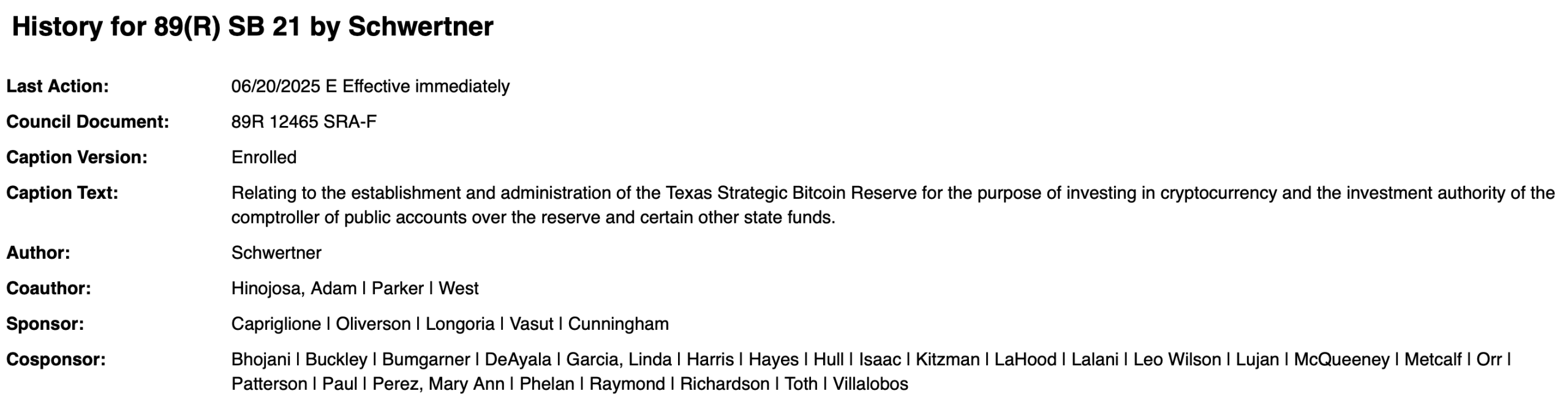

The state has also backed the industry through public policy. Last year, Gov. Greg Abbott signed legislation creating the Texas Strategic Bitcoin Reserve. In May, state officials began transitioning the reserve’s holdings from a spot Bitcoin ETF to directly custodied bitcoin.

Texas Senate Bill 21 established the Texas Strategic Bitcoin Reserve. Source: Texas Legislature

Magazine: Gambling on random Pokémon cards: Onchain gagcha hits record high as crypto sinks

Regulators are reportedly in talks with a former White House teleprompter operator as the U.S. probes whether nonpublic information was used to profit from political prediction markets. ABC News reported that Gabriel Perez—who has supported the Trump teleprompter since 2016—has been accused of betting on Kalshi markets tied to words and topics appearing in the president’s speeches.

According to ABC, Kalshi’s surveillance identified activity linked to more than a dozen speech-related contracts over roughly three months, with profits reportedly exceeding $100,000. The report adds a familiar but thorny issue to the growing prediction market sector: when real-time access and politically sensitive timing can create opportunities for alleged “insider” advantages.

Key takeaways

- ABC News says Gabriel Perez, the teleprompter operator since 2016, allegedly profited from Kalshi “Mentions” markets tied to Trump speeches.

- Kalshi reportedly detected the trades and referred them to the Commodity Futures Trading Commission, linking activity to more than a dozen speeches over about three months.

- ABC reports that Perez sometimes exited positions mid-speech when Trump skipped prepared passages containing wagered words.

- The White House placed Perez on unpaid administrative leave after the report, according to White House press secretary Karoline Leavitt.

- Congressional and regulatory attention has intensified as other prediction-market cases raised concerns about information timing and potential misconduct.

What ABC says happened on Kalshi

ABC News reported that Perez, a technical assistant who operated the president’s teleprompter, placed bets on Kalshi markets tied to phrases and topics expected to appear during Trump’s remarks. The contracts were part of Kalshi’s “Mentions” suite, which lets users trade on whether specific words, phrases, or topics will show up in public speeches.

Per ABC’s sources, the alleged conduct involved bets on more than a dozen markets associated with multiple speeches, including the State of the Union and remarks delivered at the World Economic Forum. The outlet also reported that the activity generated more than $100,000 in profits.

ABC further claims that Perez sometimes exited positions while speeches were underway, particularly when Trump skipped portions of prepared text that included words Perez had allegedly wagered would be mentioned. That detail—timing trades to the content that ultimately appears—could be central to how regulators evaluate whether the trades reflected privileged access or legitimate market behavior.

Kalshi’s surveillance and a CFTC referral

In ABC’s account, Kalshi detected the trades using its surveillance systems and referred the activity to the Commodity Futures Trading Commission. For prediction market participants, the practical implication is straightforward: platform monitoring may increasingly focus not only on trading volume or profit patterns, but also on whether trades cluster around sensitive events in ways that could indicate information advantages.

The case also underscores how prediction markets, even when they are built around public speech formats and verifiable outcomes, can intersect with regulatory scrutiny if trading appears coordinated with nonpublic material.

White House response and administrative leave

Following ABC’s report, the White House placed Perez on unpaid administrative leave, according to press secretary Karoline Leavitt. Leavitt said Trump called the alleged conduct a “disgrace.”

While the report describes accusations and an ongoing regulatory engagement, readers should note that administrative leave is not the same as a final finding of wrongdoing. Still, the action signals that the alleged behavior—if confirmed—would represent more than a routine market dispute, given Perez’s role in the teleprompter operation and the claimed linkage to politically sensitive communications.

Why this matters to prediction markets now

This development arrives as prediction markets have faced mounting attention over potential insider trading risks, particularly as activity and visibility grow. Cointelegraph previously reported that Polymarket traders earned roughly $1 million after correctly betting on a U.S. strike against Iran before the end of February, raising questions about whether some traders may have had access to information ahead of public reporting. Bloomberg, citing analytics firm Bubblemaps, was also reported to have identified wallets placing bets only hours before explosions were first reported in Tehran.

Other cases described by Cointelegraph have similarly involved timing concerns. Cointelegraph reported on instances where wallets earned more than $1.2 million by betting on an onchain investigation into DeFi platform Axiom shortly before blockchain investigator ZachXBT published allegations involving an employee. Separately, another trader was reported to have made about $400,000 by wagering on a Venezuelan political event shortly before news became public, with subsequent disappearance reported by Cointelegraph.

Taken together, these examples highlight a recurring asymmetry in prediction markets: while outcomes are ultimately verifiable, the period between a potentially market-moving piece of information and its public release can create incentives to seek advantages. That tension is especially acute for contracts that map closely to political messaging, breaking news, or other time-sensitive developments.

Beyond enforcement, lawmakers have also begun to weigh in. Cointelegraph reported that Republican Representative Bryan Steil, who chairs the House subcommittee on digital assets, introduced legislation intended to bar members of Congress and their immediate families from trading prediction market contracts tied to public policy and political outcomes.

Kalshi’s referral to the CFTC and the reported involvement of a White House insider adds another dimension to the debate: even without legislative restrictions, platforms and regulators may increasingly treat “who had access to what, and when” as central to market integrity.

What to watch next

For market participants, the next signals to monitor are whether the CFTC’s involvement leads to formal charges, and how Kalshi and other prediction platforms refine surveillance and compliance measures for politically related or otherwise sensitive events. The broader question remains whether regulators will draw clear lines between ordinary trading behavior and trading that plausibly depends on nonpublic access—lines that will shape how confident users can be in the fairness of future prediction market outcomes.

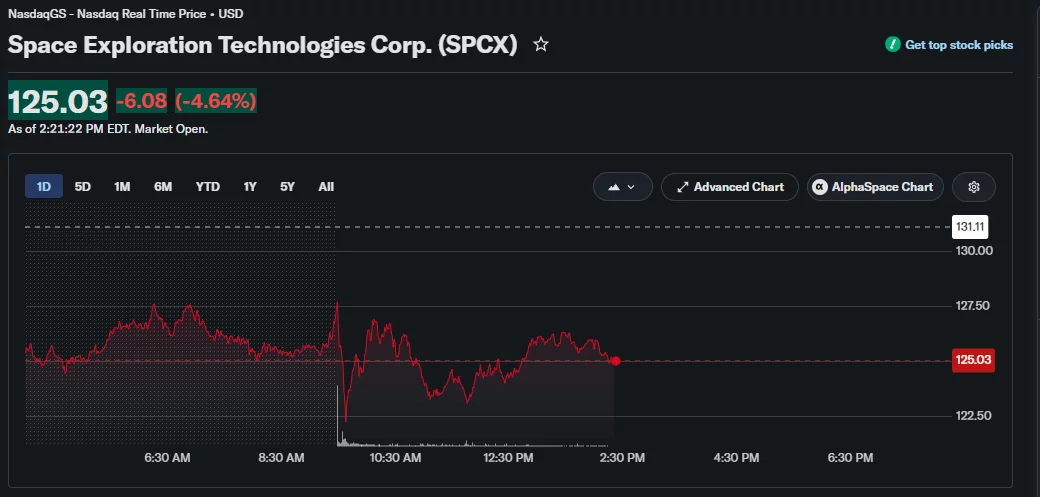

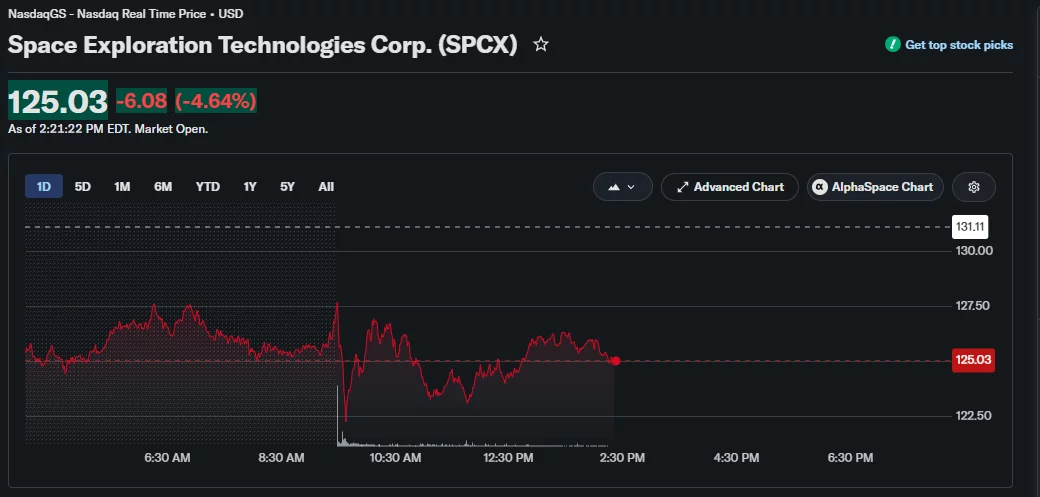

SpaceX stock has fallen nearly 5% to a post-IPO low of $125 after the company aborted Starship’s 13th test flight shortly before liftoff.

Summary

- SpaceX stock fell nearly 5% to $125, slipping below its $135 IPO price.

- SpaceX aborted the Starship launch after two Super Heavy booster engines failed to ignite.

- Elon Musk confirmed engine replacements ahead of another launch attempt scheduled for July 20.

SPCX has slipped below its $135 initial public offering price and lost about 35% over the past 30 days. The decline extends a losing streak that began after enthusiasm surrounding SpaceX’s public debut cooled and early investors started taking profits.

Selling accelerated after SpaceX halted its latest Starship launch during pre-flight procedures. According to the company, at least two Raptor engines on the Super Heavy booster failed to ignite, preventing the rocket from proceeding with the planned test.

CEO Elon Musk later confirmed that SpaceX would replace the affected engines before making another launch attempt. His update pushed the flight into the following week, adding a fresh setback for a stock already trading well below its post-IPO peak.

Starship engine failure adds pressure on SpaceX stock

SpaceX’s launch cancellation gave traders another reason to reduce their exposure after several weeks of falling prices. While the company did not link the stock decline directly to the failed ignition, market commentary on X focused heavily on the timing of the abort and the subsequent 5% selloff.

Author and cognitive scientist Gary Marcus suggested that the failed attempt could deepen concerns about investor confidence in Musk’s ability to execute SpaceX’s plans. Clarifying his view later, Marcus argued that another record low appeared more likely than a sudden collapse in the company’s shares.

Investor and longtime Tesla supporter Sawyer Merritt took the opposite position. Commenting on the selloff, Merritt argued that shareholders were placing too much weight on a launch delay expected to last only a few days.

Investors selling SpaceX shares for that reason “shouldn’t have been in the stock in the first place,” Merritt wrote on X. His comment framed the market reaction as excessive, although the shares remained under pressure following the postponement.

Before the recent decline, demand surrounding SpaceX’s IPO had driven SPCX as high as $225.64. The stock has since surrendered much of that advance and now trades about 8% below its offering price.

Revised Starship launch offers the next test for investors

SpaceX has rescheduled Starship’s 13th test flight for Monday, July 20, at 6:45 p.m. ET, according to the company’s latest announcement. The updated timetable gives engineers several days to replace the two engines and prepare the Super Heavy booster for another attempt.

Merritt pointed to the revised date as evidence that the interruption may be brief. Marcus, however, continued to focus on the stock’s deteriorating performance, leaving two sharply different readings of what the aborted launch means for shareholders.

A successful flight could influence sentiment around SPCX, but that possibility remains dependent on SpaceX completing the test without another technical delay. Until then, price data shows that the shares remain caught in a month-long decline despite the company providing a new launch schedule.

Separate from the test flight, Binance has introduced a perpetual futures product linked to SpaceX stock, according to the exchange’s announcement. The contract gives eligible traders derivatives-based exposure to SPCX, adding another venue through which market participants can take leveraged positions on the company’s price movements.

Anthropic has proposed leasing up to $10 billion of computing power from Meta Platforms over two years as the AI developer prepares for a possible October IPO.

Summary

- Anthropic has proposed leasing up to $10 billion of computing power from Meta over two years.

- Meta is reviewing the deal, which could create a new revenue stream from its AI infrastructure.

- Bloomberg reports Anthropic is preparing for a possible IPO as early as October.

According to Reuters, which cited The New York Times, Meta is reviewing the proposal after Anthropic presented the terms in June. The planned agreement would require Anthropic to make monthly payments for access to Meta’s computing capacity.

Both companies could end the contract before the two-year period expires, the report added. Meta and Anthropic have not finalized the arrangement, leaving its value and duration subject to the outcome of their talks.

For Anthropic, the lease would provide access to the processing capacity needed to train and operate advanced artificial intelligence models. AI developers depend on large numbers of specialized chips and data centers, making reliable computing access a central part of their expansion plans.

Meta, in turn, could earn revenue from infrastructure built primarily for its own AI products and services. According to the report, the proposed lease would give the social media company another way to generate returns from its computing investments beyond its advertising business.

Meta could enter the AI infrastructure market

A completed agreement would place Meta in competition with CoreWeave and Nebius, two companies that supply computing infrastructure for AI workloads. Reuters reported that the Anthropic proposal could turn Meta into a provider of capacity to an external AI developer while it continues building models and products of its own.

The talks have emerged as technology companies compete for chips, electricity and data center space. Under the reported structure, Anthropic would secure capacity from a company that has spent heavily on AI infrastructure, while Meta would add a potential customer for resources within its computing network.

Anthropic has also pursued separate long-term infrastructure arrangements. Earlier this month, the company signed a 20-year data center lease with Bitcoin miner TeraWulf. The agreement is expected to supply additional computing resources for Anthropic’s future AI development.

Taken together, the Meta discussions and TeraWulf lease show how Anthropic is assembling the infrastructure required to support its models. Any assessment of the scale or financial effect of those agreements, however, depends on their final terms and the amount of capacity Anthropic ultimately uses.

Anthropic could reach public markets in October

Bloomberg reported that Anthropic is moving forward with preparations for a possible stock market listing. Banks working on the offering have begun arranging meetings between company executives and prospective investors, according to the report.

Those meetings could support an IPO as early as October, although Bloomberg’s timeline remains subject to market conditions and the company’s final decision. An October debut would put Anthropic in the public market before OpenAI, which Bloomberg reported is considering a listing in 2027.

Chinese AI developer DeepSeek is also preparing for an eventual public offering, according to the original report. Anthropic could therefore become one of the first major companies from the latest generation of AI model developers to list its shares.

Before the IPO report emerged, Anthropic had received approval from the US government to restore access to its Mythos 5 model for selected companies and federal agencies last month. Combined with its infrastructure agreements and investor meetings, the decision adds another development for banks and potential shareholders to examine as preparations continue.

OKX Europe has introduced a “one-way conversion” tool that lets customers deposit Tether’s USDT and convert it into Circle’s MiCA-compliant USDC. The feature is aimed at clients who can no longer keep USDT supported on their accounts as European Union stablecoin rules tighten.

In an announcement shared with Cointelegraph, OKX Europe said the process is customer-controlled: users can deposit USDT into their OKX Europe account and convert it into USDC at their discretion, rather than being forced through a platform-imposed deadline. The exchange said the tool is meant to support customers whose existing venues no longer accept USDT or who plan to move balances automatically to compliant alternatives.

Key takeaways

- OKX Europe now supports conversion from USDT into MiCA-compliant USDC, without requiring a two-way transfer option.

- The feature targets customers affected by MiCA implementation, when many EU-facing platforms reduced USDT availability.

- OKX Europe positions the update as a migration path for users who want to preserve value continuity while shifting to USDC.

- Tether has not pursued MiCA authorization for USDT, which is central to why some platforms restrict or delist USDT in the EU.

- USDT remains the largest stablecoin by market share, according to DefiLlama, even as compliance-driven changes accelerate in Europe.

How OKX Europe’s one-way migration works

According to OKX Europe’s announcement, the new conversion feature allows customers to deposit USDT—Tether’s USDt—into their OKX Europe account and convert those tokens into USDC. USDC is described as one of the major stablecoins that fits the EU’s Markets in Crypto-Assets (MiCA) framework.

The “one-way” aspect matters: the workflow is designed to move balances toward a MiCA-aligned stablecoin rather than enabling conversion in both directions. OKX Europe also emphasized that conversions can be completed at the customer’s discretion instead of via a strict cutoff determined by the exchange.

OKX Europe operates under its MiCA license across 30 EU and European Economic Area countries, positioning the feature as a practical bridge for users navigating where USDT is no longer supported.

MiCA rollout forces stablecoin support to change

The timing aligns with the EU’s stablecoin regulatory rollout. Tether has not obtained authorization to issue USDT under MiCA, a status that has led many European platforms to restrict deposits, remove trading pairs, or convert client balances into compliant alternatives as MiCA rules took full effect on July 1.

That regulatory friction is not marginal. DefiLlama data cited in the report shows Tether accounts for about 59% of the roughly $310 billion stablecoin market, with USDT market capitalization around $184 billion. Circle’s USDC is much smaller by comparison, at about $73 billion, but still one of the largest compliant options for EU-based platforms.

For investors and traders, these shifts can change liquidity and execution. When a major venue restricts deposits or delists pairs, users who depend on a stablecoin—whether for trading, hedging, or moving between exchanges—can face friction even if the underlying stablecoin remains available elsewhere outside the EU.

Tether’s stance on MiCA authorization

Tether has defended its decision not to pursue MiCA authorization for USDT, and the approach has shaped the behavior of European market operators. Cointelegraph previously reported that Tether CEO Paolo Ardoino has criticized MiCA, arguing that reserve requirements could introduce unnecessary risk by requiring part of reserves to be held with European credit institutions.

Ardoino has also suggested that the regulatory tradeoffs are not favorable for stablecoin issuers. In a May 2025 interview with Cointelegraph, he characterized MiCA’s approach as “very dangerous when it comes to stablecoins,” noting Tether’s choice not to seek authorization despite expectations that USDT could lose support on European exchanges.

More recently, in a July 2025 post on X, Ardoino said Tether would reconsider pursuing MiCA authorization only “when MiCA becomes safer for consumers and stablecoin issuers.” The messaging indicates Tether sees no near-term reason to change course—an implication reinforced by the continuing migration efforts from EU-facing exchanges and other service providers.

Broader industry response: from exchanges to retail apps

OKX Europe’s conversion tool reflects a wider trend across Europe: when MiCA restricts USDT access, platforms often re-route customers toward compliant stablecoins or withdrawal pathways.

One example highlighted in the same material is Revolut, a digital banking platform that said it will stop supporting USDT for customers in the European Economic Area and Switzerland. Revolut reportedly gave users until Aug. 31 to sell or withdraw their holdings, with any remaining balances expected to be automatically converted into the base currency.

These actions underscore a key asymmetry for USDT holders in Europe. While USDT remains globally dominant, users in MiCA-regulated jurisdictions may experience forced transitions—either by changing what can be deposited and traded on exchanges or by shifting stablecoin exposure within retail financial interfaces.

For traders, this can affect strategy execution. Stablecoin pairs tied to USDT liquidity may shrink, and conversion paths could introduce operational steps or timing variability. For users focused on custody or settlement, the migration choice also becomes a matter of which compliant stablecoin is supported on the platform they use day to day.

What to watch next for EU stablecoin migration

As MiCA compliance keeps reshaping which stablecoins are usable on EU-facing platforms, customers should watch whether more exchanges adopt similar “migration” features and whether USDT support continues to narrow to withdrawals and conversions rather than active trading. The next turning point will likely be how quickly the market’s liquidity consolidates around MiCA-approved alternatives like USDC—and whether Tether’s position evolves if regulatory conditions change.

XRP is a commodity until the SEC changes its mind

Wings Over Scotland | These Words Are My Own

Everybody Rise chases fourth straight win at Ipswich 2024

-

Fashion7 days ago

Fashion7 days agoWeekend Open Thread: Nutriplenish Leave-In Conditioner

-

NewsBeat1 day ago

NewsBeat1 day agoLondon Mayor Sadiq Khan handed a peerage by Keir Starmer alongside 15 other Labour figures… just days before the PM leaves No10

-

Politics2 days ago

Politics2 days agoYoung campaigners urge incoming PM to act on outdoor junk food ads

-

Crypto World2 days ago

Crypto World2 days agoCFTC blocks Kalshi from unwinding Michigan trades after court order

-

Business2 days ago

Business2 days agoNvidia Stock Slips After Big Tuesday Rally as Huang Confirms Vera Rubin Chip Is Now in Production Today

-

Fashion3 hours ago

Fashion3 hours agoWeekend Open Thread – Corporette.com

-

Entertainment2 days ago

Entertainment2 days agoDisney’s Most Ambitious Failed Star Wars Attraction Is Coming to SDCC

-

News Videos3 days ago

News Videos3 days agoXRP BOMBSHELL… XRP OMBOARDED FOR TRANSACTIONS!!!

-

Tech4 days ago

Tech4 days agoGet Your ESP32 Sunny Side Up With This Solar Dev Board

-

Crypto World1 day ago

Crypto World1 day agoInjective Submits SEC Transfer-Agent Registration to Onchain Ownership Records

-

NewsBeat9 hours ago

NewsBeat9 hours agoRegistration is now open for March for Men with Kev 2026

-

Tech3 days ago

Tech3 days agoDark Secrets Emerge When Jailbreaking LLMs

-

Business2 days ago

Business2 days agoPalantir Shares Rise After Expanded Nvidia Partnership and Fresh Analyst Upgrades Ahead of Earnings Day

-

Sports2 days ago

Sports2 days agoNew Cornerback Enters Vikings Trade Rumor Mill

-

News Videos14 hours ago

News Videos14 hours agoMoney | Class 12 Economics | CBSE Board Exam 2026-27

-

Business19 hours ago

Business19 hours agoBanco Bilbao Vizcaya Argentaria, S.A. (BBVA) Discusses Global Macro Environment and Economic Outlook for Core Markets Transcript

-

Tech4 days ago

Tech4 days agoCloudflare Precursor Watches Your Mouse and Keyboard To Decide If You Are Human

-

News Videos4 days ago

News Videos4 days agohow to make coin bank box with cardboard #scienceproject #money #diy #shorts

-

Business2 hours ago

Business2 hours agoAirlines warn Sunshine Protection Act could disrupt flight scheduling

-

Entertainment2 days ago

Entertainment2 days agoVicki Gunvalson Defends Discussing Heather Dubrow’s Money

You must be logged in to post a comment Login