Crypto World

United Parcel Service (UPS) Stock: $100M Taiwan Facility Targets Semiconductor Logistics

Key Highlights

- United Parcel Service inaugurated a $100 million distribution facility in Taoyuan, Taiwan — marking its biggest Asia Pacific investment

- The facility sits adjacent to Taiwan’s primary international airport, optimized for technology-related shipments

- Approximately 80% of cargo flowing through the center consists of high-technology products

- Applied Materials (AMAT) has designated this location as its primary Asian distribution point

- The company is exploring potential flight operations to Kaohsiung, near TSMC’s emerging manufacturing complex

United Parcel Service (UPS) has inaugurated a state-of-the-art $100 million distribution facility in Taoyuan, Taiwan, representing the company’s most significant infrastructure investment across the Asia Pacific region. This strategic facility aims to support surging requirements from technology manufacturers, especially within Taiwan’s globally dominant semiconductor sector.

United Parcel Service, Inc., UPS

Positioned strategically adjacent to Taiwan’s busiest international airport, the Taoyuan location offers optimal access for time-sensitive, high-value technology shipments. According to Lauren Zhao, who leads UPS Asia Pacific Supply Chain Solutions and Freight Forwarding operations, approximately 80% of cargo processed through this facility falls within the high-technology category.

Applied Materials (AMAT), America’s leading semiconductor equipment manufacturer, has selected this facility to serve as its central Asian distribution hub. Shares of AMAT climbed 3.37% following the announcement.

“Taiwan’s semiconductor sector stands unrivaled globally in terms of technological advancement,” Zhao stated during the facility’s opening ceremony. She emphasized that manufacturing capabilities associated with this industry represent areas where Taiwan maintains worldwide leadership.

TSMC, recognized as the planet’s leading contract chipmaker, serves as a primary catalyst for regional logistics demand. The company’s processors are integral to AI infrastructure development occurring across the globe, establishing Taiwan as an indispensable link in international supply networks.

Southern Taiwan Expansion Under Review

Sam Hung, who directs UPS operations across Japan, South Korea, and Taiwan, revealed that the logistics provider is evaluating flight service expansion to Kaohsiung in Taiwan’s southern region. This potential expansion hinges on demonstrated client requirements.

Kaohsiung hosts TSMC’s ongoing construction of a substantial new manufacturing facility, forming part of an expanding semiconductor industrial zone in Taiwan’s southern territory. Should this industrial cluster develop as anticipated, UPS may find compelling business justification for establishing operations there.

The substantial $100 million capital commitment demonstrates the extent to which logistics infrastructure is being developed to support Taiwan’s chip manufacturing ecosystem. With TSMC functioning as the nexus of AI hardware supply chains, rapid movement of equipment and materials has emerged as a strategic imperative for companies like Applied Materials.

Strategic Partnership with Applied Materials

Applied Materials selecting the Taoyuan center as its Asian operational headquarters provides UPS with a foundational client deeply embedded in chip production. AMAT produces the sophisticated machinery that fabricates semiconductors — meaning its logistics requirements directly correlate with semiconductor manufacturing timelines.

The UPS installation enables both organizations to react more rapidly to fluctuations in chip production requirements throughout the region. Such responsiveness proves critical when equipment delivery delays can potentially halt entire fabrication operations.

Currently, UPS maintains operations exclusively through Taoyuan airport within Taiwan. The Kaohsiung service expansion remains under active evaluation as of March 25, 2026.

The American Bankers Association (ABA) is mounting an aggressive lobbying push against portions of the Senate’s Digital Asset Market Clarity Act ahead of a scheduled Banking Committee markup on Thursday, warning lawmakers that stablecoin provisions in the updated bill could still undermine bank deposits and weaken financial stability.

In a call-to-arms circulated to bank executives nationwide, the ABA petitioned banks and their employees over the weekend to contact senators immediately to push for tighter restrictions on payment stablecoins in the crypto market structure bill. The group said the latest version of the legislation — after months of bank lobbying, meetings and input — still leaves room for crypto firms to offer interest-like rewards that may encourage consumers to move money out of traditional bank accounts.

The Senate Banking Committee is expected to release updated legislative text as soon as Monday, with comments and amendments from lawmakers likely to emerge Tuesday before Thursday’s committee vote on the Clarity Act.

“We need your help to drive this message home before senators consider this legislation,” ABA president Rob Nichols said in the request.

The ABA’s campaign follows a joint letter sent last week with other banking trade associations that outlined proposed edits to the bill. The groups argued lawmakers need to close what they describe as a loophole around stablecoin yield before advancing the legislation.

The dispute has become one of the defining battles in Washington’s crypto policy debate. Bank executives and trade groups have argued that yield-bearing stablecoins could function as substitutes for insured deposits, draining funding that banks rely on to make mortgages, business loans and other forms of credit.

Supporters of stablecoins, including many crypto firms and fintech companies, argue the products offer consumers faster payments and new ways to move money online. Critics in the crypto industry say banks are trying to preserve their dominance by limiting how digital dollar products compete for users.

“The banking cartel is in full panic mode,” U.S. Senator Bernie Moreno, an Ohio Republican who has been staunchly pro-crypto, posted on social media site X.

The fight previously delayed legislative progress, and lawmakers eventually negotiated a compromise that would prohibit stablecoin yield resembling deposit interest while allowing activity-based rewards programs similar to credit-card points. Even after those changes, major banking groups have continued pressing Congress for stricter guardrails.

While the White House Council of Economic Advisers had released an analysis on stablecoins that suggested their deployment wouldn’t damage the banking system, ABA economists answered with their own study in April. The banking group argued the administration focused on the wrong policy question by analyzing the effects of banning stablecoin yield rather than the consequences of allowing it. According to the ABA, permitting yield-bearing stablecoins could rapidly scale the market from roughly $300 billion today to as much as $2 trillion, increasing pressure on bank funding.

The longer negotiations drag on, lawmakers and industry participants warn, the harder it may become to move comprehensive crypto legislation through the Senate and onto the floor for a final vote. About 10 weeks of Senate floor time remain before the midterm elections, according to the current Senate calendar, and there are a lot of competing interests for that legislative bandwidth.

UPDATE (May 11, 2026, 14:55 UTC): Adds response from Senator Bernie Moreno.

Key takeaways

- XRP slipped below $1.50 as renewed Middle East tensions weakened broader crypto sentiment.

- XRP investment products saw nearly $40 million in inflows last week, while futures open interest climbed to $2.87 billion.

XRP tests key $1.45 support despite strong ETF and futures inflows

Ripple’s XRP retreated from highs near $1.50 and hovered around $1.46 on Monday as renewed geopolitical tensions in the Middle East pressured broader crypto markets and cooled recent bullish momentum.

The pullback followed comments from US President Donald Trump, who reportedly rejected Iran’s latest proposal aimed at ending the ongoing conflict in the region, calling the offer “totally unacceptable.”

The proposal included conditions tied to Iran’s sovereignty over the Strait of Hormuz alongside demands for compensation related to war damages.

Iranian Foreign Ministry spokesperson Esmail Baghaei defended the proposal, describing it as “reasonable” and “generous” for both Iran’s national interests and regional stability.

The renewed uncertainty rattled risk assets, including cryptocurrencies, which had recently rallied on hopes of a lasting ceasefire agreement between the US and Iran. XRP is up by less than 1% today as traders reassessed the broader macro outlook.

Despite the market weakness, capital inflows into XRP investment products remained resilient last week.

According to CoinShares, XRP-related digital investment products attracted nearly $40 million in inflows, with total assets under management averaging $2.5 billion, ranking fourth among crypto investment products.

Spot XRP exchange-traded funds (ETFs) accounted for approximately $34 million of those inflows, while cumulative ETF inflows climbed to $1.32 billion. Net ETF assets under management currently stand at around $1.12 billion, according to CoinGlass data.

Meanwhile, derivatives activity suggests retail traders continue positioning for further upside. XRP futures Open Interest (OI) surged to $2.95 billion from $2.65 billion a day earlier, indicating growing participation and investor conviction despite the recent pullback.

XRP technical outlook: bulls defend key EMA support zone

The XRP/USD 4-hour chart remains bullish as Ripple continues to trade above key levels. XRP is currently trading above the 50, 100, and 200 Exponential Moving Averages (EMAs) on the 4-hour chart clustered between $1.40 and $1.42, reinforcing a constructive short-term bias.

However, the $1.50 area remains a major resistance barrier after acting as a double-top ceiling during the recent rally.

Momentum indicators suggest bullish momentum is cooling rather than reversing entirely. The Relative Strength Index (RSI) remains in the high-50s, while the Money Flow Index (MFI) has eased from overbought territory, signaling a pause in buying pressure.

If the selloff persists, XRP could encounter a support level near the 50 EMA around $1.42, followed by stronger support around the 100 EMA at $1.41 and the 200 EMA near $1.40.

However, if the bulls regain control and XRP’s daily candle closes above the $1.50 resistance zone, it could pave the way for a more extended bullish move in the sessions ahead.

We fed Grok AI a carefully engineered prompt about XRP price action to find out what it predicts.

What came back was not a cautious hedge. It was a number that would make most analysts uncomfortable putting their name on.

The AI did not blink. By the end of 2026, it sees XRP printing somewhere between $4 and $7, with an optimistic run potentially pushing past that entirely if the right conditions stack up.

Grok’s AI reasoning is not random. It anchors the call on 3 converging factors that are already in motion.

The SEC case is resolved, regulatory clarity no longer hangs over the asset, and XRP ETFs are now attracting real institutional money.

That alone changes the demand equation. Layer on Ripple’s expanding On-Demand Liquidity partnerships, driving actual XRPL volume, and you have utility backing the speculation rather than speculation alone.

The macro setup adds to it: rate cuts, RWA tokenization momentum, and XRP’s structural advantage in cross-border payments put it directly in the path of capital that is actively looking for somewhere to go.

The base target Grok lands on is $3.50 to $5. The optimistic scenario is $7 or higher by year-end, representing a 3 to 5x move from current levels.

That is the kind of setup that only works if institutional demand shows up consistently and ETF inflows do not stall.

The bear case is real, though. If ETF momentum slows or stablecoin competition starts eating into XRP’s payments niche, the more likely outcome is a prolonged grind between $1.50 and $2.50. Not a collapse, but not the breakout either.

The prediction is high conviction, not guaranteed.

Is Grok AI XRP Price Prediction Realistic? Here Is What the Chart Says About his Predicts

XRP is trading at $1.45 on the daily, sitting inside a descending wedge that has been tightening since the February lows around $1.20.

The pattern is textbook. Lower highs, higher lows, price coiling toward the apex. A descending wedge is a bullish reversal structure by nature, and the chart has it drawn out clearly with the breakout projection pointing toward the $3.73 area, roughly a 164% move from the current XRP USD price.

Resistance sits at $1.55 to $1.60, which is where the upper trendline of the wedge is currently pressing down.

That zone has rejected price multiple times since February, and it is the level that matters most right now. Support is $1.30, the floor that has held through every flush since the wedge formed. Lose that, and the bullish structure breaks down.

RSI on the daily is at 51.21, sitting just above the midline. That is neutral, not extended, and actually leaves room for a real move without hitting overbought territory immediately.

The signal line is tracking above at 58.08, which suggests the momentum side of the indicator is tilting bullish even if the XRP price has not confirmed yet.

The wedge breakout would need a clean daily close above $1.60 with volume behind it. If that happens, $2.00 is the first target, and the path toward Grok’s base case starts looking a lot less speculative.

Discover: The best crypto to diversify your portfolio with

Grok Projects That Bitcoin Hyper Could Outperform Them All

Some traders rotating between cycles are already looking past large caps entirely.

Bitcoin Hyper is positioning itself for that rotation. The project is building the first Bitcoin Layer 2 with Solana Virtual Machine integration, claiming sub-Solana latency while keeping Bitcoin’s security layer intact. Fast, low-cost smart contracts on Bitcoin without abandoning its trust model. That is a gap neither Ethereum nor Solana fills directly.

The presale has raised $32 million at $0.013679 per token with high APY staking available for early participants.

The risk profile is different here. Higher upside potential, earlier entry, and significantly more execution risk than anything trading on major exchanges. That tradeoff is the whole point.

The post Elon Musk New Grok AI Predicts the Price of XRP by The End of 2026 appeared first on Cryptonews.

Key takeaways

- Solana surged nearly 15% last week as spot SOL ETFs attracted $39.23 million in inflows — the strongest since January.

- Solana surged nearly 15% last week as spot SOL ETFs attracted $39.23 million in inflows — the strongest since January.

Solana (SOL) is trading just above $95 on Monday after rallying nearly 15% over the past week, with bullish momentum supported by strong institutional demand, improving on-chain activity, and rising derivatives participation.

Institutional demand pushes SOL above $90

Institutional appetite for Solana strengthened sharply last week, with spot Solana Exchange Traded Funds (ETFs) recording net inflows of $39.23 million, according to CoinGlass data.

The figure marked the strongest weekly inflow since mid-January, signaling renewed investor confidence in the asset. Continued inflows could provide additional upside support for SOL in the near term.

On-chain and derivatives metrics also point to a constructive outlook. CryptoQuant data indicates cooling conditions across both spot and futures markets while showing buy-side dominance in futures activity — a combination that often precedes further upside.

Although several metrics remain neutral, overall sentiment has improved considerably compared to previous weeks.

In the derivatives market, Solana’s funding rates turned positive on Sunday before climbing to 0.0067% on Monday, showing that long traders are now paying shorts to maintain positions.

Historically, similar flips from negative to positive funding rates have coincided with strong upward price moves for SOL.

Open Interest (OI) in Solana futures has also surged. CoinGlass data shows total OI rising to $6.46 billion on Monday from $4.83 billion on May 5.

The steady increase since early May suggests fresh capital continues to enter the market, reinforcing bullish momentum and signaling growing trader participation.

Solana technical forecast: Bulls target the $100 psychological level

The SOL/USD 4-hour chart is bullish thanks to Solana’s recent rally. SOL is now trading above both the 100-day Exponential Moving Average (EMA) at $93.87 and the 50-day EMA at $87.51, strengthening the bullish case.

Momentum indicators also remain supportive. The Relative Strength Index (RSI) sits at 69, reflecting strong but not yet overextended momentum.

Meanwhile, the Moving Average Convergence Divergence (MACD) indicator remains firmly positive and continues to rise.

If the rally persists, immediate resistance is seen near the 38.2% Fibonacci retracement level at $98.53.

A daily candle close above this resistance could open the door toward the $108.12–$110.62 range, where the 50% retracement level and the 200-day EMA converge.

Additional resistance levels stand near $117.71 and $120.00, while an extended rally could target the 78.6% retracement level around $131.35.

However, if the market undergoes a correction, immediate support sits near the former channel resistance around $92.11, followed by the 100-day EMA at $93.87 and the 50-day EMA at $87.52.

Losing these levels could expose the support near $86.67, while deeper pullbacks could revisit the channel floor around $77.12 and the broader cycle low area near $67.50.

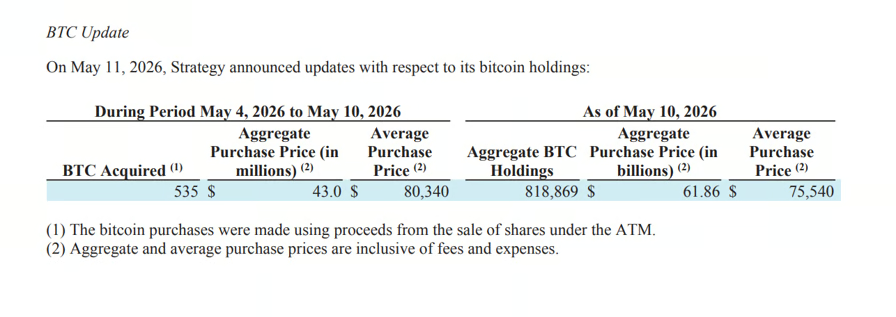

Strategy bought 535 Bitcoin for $43 million last week, resuming its accumulation strategy days after its chairman, Michael Saylor, said the company may sell some of its holdings to fund dividend payments.

The world’s largest corporate Bitcoin holder acquired the Bitcoin (BTC) between May 4 and May 10 at an average price of $80,340 per BTC, according to a Monday filing with the US Securities and Exchange Commission.

The purchase lifted Strategy’s total holdings to 818,869 BTC, acquired for about $61.86 billion at an average price of $75,540 per coin, including fees and expenses.

The acquisition was Strategy’s first since April 27, when the company bought 3,273 BTC for $255 million. It also followed the company’s first-quarter earnings call, where Saylor said Strategy would “probably sell some Bitcoin” to fund a dividend and show that a sale would not undermine the company or the broader Bitcoin market.

On Sunday, Saylor hinted that the company would resume BTC purchases after the prior week’s pause.

Strategy Bitcoin acquisition, 8-K filing. Source: SEC

The Bitcoin purchase was made using proceeds from share sales. The majority of the acquisition, or $42.9 million, was funded through the sales of Class A common stock (MSTR), while another $100,000 was funded through the issuance of Stretch (STRC) stock, the filing shows.

Related: Capital B raises $17.8M to expand its Bitcoin treasury

Strategy shares gain in pre-market, despite Bitcoin sales concerns

Strategy shares rose in premarket trading on Monday after the company disclosed the Bitcoin purchase.

Its shares rose 4.3% to change hands above $187.50 at the time of writing, according to Yahoo Finance.

Strategy’s shares are up 23% year-to-date despite Bitcoin’s 7.2% decline during the same period, data from TradingView shows.

MSTR/USD, 1-day chart. Source: Yahoo Finance

Still, investor concerns persist following Strategy’s first quarter earnings call, when Saylor said Strategy may periodically sell portions of the company’s Bitcoin holdings to fund dividends and to “inoculate the market.”

While some investors feared that a Strategy sale could create more cascading liquidations, others, such as Bitcoin advocate Samson Mow, said that Strategy’s potential sales can give it greater room to maneuver in the market.

Strategy investor Adam Livingston argued that periodic sales may allow the company to finance more Bitcoin purchases in the future.

Magazine: Strategy reveals why they would sell BTC, Trump Media posts loss: Hodler’s Digest, May 3 – 9

Solana developer Anza said Monday that Alpenglow, the network’s biggest proposed consensus overhaul to date, is live on a community test cluster, marking a major step toward a potential mainnet rollout.

The update means validator operators can now test software designed to move Solana from its current consensus system, which combines Proof-of-Stake with TowerBFT and Proof-of-History, toward a new architecture intended to dramatically reduce finality times and improve network responsiveness.

“Alpenglow is live on the community test cluster,” Anza wrote on X. “The biggest consensus change in Solana’s history, now running on validator infrastructure ahead of mainnet.”

Today, Solana relies on Proof-of-History, a cryptographic clock that timestamps transactions, alongside TowerBFT, a voting mechanism validators use to agree on the state of the blockchain. While the design has helped Solana achieve high throughput and low fees, some have pointed to outages and network instability during periods of heavy demand.

Alpenglow proposes replacing major portions of that system with a redesigned framework centered around new components. In simple terms, the new model aims to let validators communicate and confirm blocks faster and more efficiently, potentially cutting transaction finality from several seconds to near real-time speeds.

The start of the community test cluster also suggests that validator software can successfully perform what developers are informally calling “Alpenswitch,” transitioning validator nodes from Solana’s existing process to Alpenglow in a live network environment.

The test milestone comes just days after Solana co-founder Anatoly Yakovenko said at Consensus Miami 2026 that Alpenglow could reach mainnet as soon as next quarter if testing continues smoothly.

Read more: Solana’s ‘Alpenglow’ upgrade could arrive next quarter, co-founder Yakovenko says

Crypto World

Sui Crypto Outpaces Market with 37% Surge as Institutional Staking TVL Hits New Milestones

Sui crypto posted a 37% gain in the last 7 days, decoupling sharply from the broader crypto market as Bitcoin briefly topped $82,000 on improving macroeconomic conditions.

The SUI price move is not a sympathy rally, it is driven by two distinct catalysts: a surge in institutional staking inflows that has pushed network TVL to fresh milestones, and a protocol-level upgrade enabling zero-fee stablecoin transfers that is reshaping DeFi liquidity dynamics on the network.

The tension at the center of this story is supply. Sui Group Holdings’ involvement has amplified buy pressure at a moment when the free float is constrained by aggressive staking lockups, and that combination is producing outsized price moves from relatively modest capital inflows.

— Noodles Finance

BULLISH: NASDAQ JUST REMOVED 108 MILLION SUI FROM CIRCULATION

BULLISH: NASDAQ JUST REMOVED 108 MILLION SUI FROM CIRCULATION

NASDAQ LISTED SUIG STAKED ITS ENTIRE 108.7M $SUI TREASURY pic.twitter.com/eeYKJd3KLX

(@NoodlesFi) May 11, 2026

(@NoodlesFi) May 11, 2026

Whether that dynamic can sustain new price levels – or whether it reverses sharply once staking incentives normalize, is the question this rally forces traders to answer.

Discover: The best pre-launch token sales

Can SUI Crypto Price Hold Above $1.20 After the 37% Breakout?

SUI is sitting at $1.2692 on the daily chart, and the move that just happened in the last couple of sessions is impossible to ignore, price launched from the $0.85 to $0.90 base and spiked all the way to $1.35 in what looks like a near vertical candle off months of low-level consolidation.

The broader context is brutal though. SUI dropped from $4.40 at the July peak all the way down to $0.63 in the February capitulation wick, losing over 85% of its value, and has been grinding in a tight range between $0.85 and $1.10 for most of March and April before this sudden breakout.

The $1.30 to $1.40 zone is now the immediate test because that was where prior support existed during the November to December breakdown, and price is sitting right at that level after the spike, which is exactly where sellers from that period would be looking to exit.

A hold above $1.30 and the next meaningful resistance is around $1.80 to $2.00, and above that $2.40 where the longer distribution zone begins.

The concern with a move this sharp and vertical is the same as always: it tends to need a cooldown and retest before continuing, and a pullback toward $1.00 to $1.10 on a retest would actually be healthy for the setup.

The base is solid, the breakout is real, but the speed of the move means chasing here carries risk and a retest of the breakout zone is the cleaner entry if the setup holds.

Discover: The best crypto to diversify your portfolio with

The post Sui Crypto Outpaces Market with 37% Surge as Institutional Staking TVL Hits New Milestones appeared first on Cryptonews.

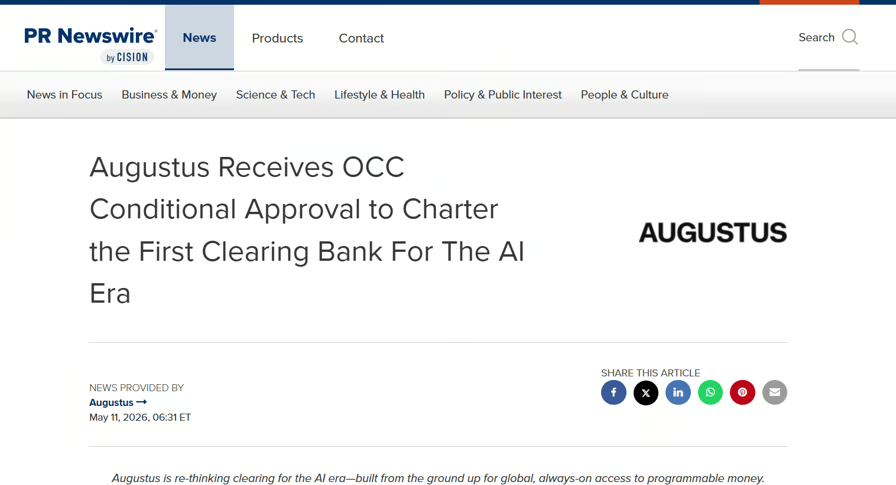

Peter Thiel-backed payments startup Augustus received conditional approval from the US Office of the Comptroller of the Currency (OCC) to establish a US national bank built around artificial intelligence and stablecoin-based payments.

The approval, announced Monday, would allow Augustus to expand its existing European banking operations into the US, as financial firms increasingly compete to modernize cross-border settlement infrastructure using tokenized dollars and blockchain-based payment systems.

The company describes Augustus National Bank as “the first clearing bank for the AI era,” built on an AI and stablecoin-native core designed to interact directly with machine agents at “the speed of compute,” rather than relying on batch processes and human clerks.

Founded in 2022, Augustus operates under European banking licences and says it already processes billions of dollars for institutional clients, including cryptocurrency exchange Kraken. Its proposed US national bank charter, however, is still at the conditional approval stage and will only become effective once the OCC’s pre-opening requirements are satisfied.

Augustus secures OCC conditional approval. Source: PR Newswire

Related: Stablecoin issuer Circle faces lawsuit over $280M Drift Protocol hack

While companies such as Ripple and Circle have pursued national trust bank charters under the OCC framework, only a limited number of digital asset firms have reached comparable advanced stages in the federal chartering process. The OCC approval places Augustus among a small group of companies that have progressed toward a national bank charter in recent years, according to the release.

Race to build the stablecoin bank

The move comes as competition intensifies to modernize cross-border payments and stablecoin settlement infrastructure in the US.

Under the Guiding and Establishing Innovation for US Stablecoins (GENIUS) Act regime for payment stablecoins, banks and trust companies can issue fully reserved dollar tokens, and a growing group of issuers and payments companies are testing ways to integrate tokenized dollar flows into regulated banking rails.

Circle’s collaboration with core banking provider Finastra in August 2025, for example, lets banks settle cross-border payments in USDC via Finastra’s Global PAYplus hub, and Citi and HSBC introduced live tokenized deposit services for 24/7 cross-border and interbank payments in November 2025.

Augustus, backed by Peter Thiel’s Valar Ventures, Creandum, and the founders of companies including Ramp and Deel, has raised about $40 million, according to the company. At 25, Dabitz would be the youngest chief executive of a federally chartered bank in over 100 years.

Cointelegraph reached out to Augustus for comment, but had not received a response by publication.

Asia Express: North Korea denies crypto hacks, Upbit’s bank tests Ripple

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Solana nears key resistance as cloud mining platforms like AJC Mining gain traction in crypto recovery phase.

Summary

- As Solana and major crypto assets rebound, interest in cloud mining platforms like AJC Mining is increasing among everyday users.

- AJC Mining offers simplified access to mining through professional data centers and managed hashrate systems.

- With rising market participation, AJC Mining attracts attention for its infrastructure, security focus, and user-friendly mining access.

As whale activity, ETF capital inflows, and bullish momentum in the derivatives market continue to build, Solana is preparing to challenge the key resistance level near $97.40.

For everyday users, this market rebound is not only a sign of Solana’s ecosystem recovery but also a clear indication that the digital asset market is entering a new phase driven by institutional capital, on-chain data, and global user participation.

Crypto market recovery makes cloud mining a new entry point for everyday users

As mainstream crypto assets such as Solana, Bitcoin, Litecoin, Dogecoin, and Bitcoin Cash regain market attention, more users are looking for easier ways to participate in the digital asset economy.

Compared with traditional mining, which requires expensive mining machines, electricity management, hardware maintenance, and technical knowledge, Cloud Mining is becoming a lighter and more accessible option. Users do not need to build their own mining farms or manage complex mining equipment. Instead, they can participate through a professional cloud mining platform and access mining power more conveniently.

Against this backdrop, AJC Mining is gaining attention as a cloud mining service platform. Through professional mining farm deployment, global hashrate management, and transparent system operations, AJC Mining aims to provide users with a more convenient and efficient Cloud Mining experience.

Register with AJC Mining now and receive a $15 new user bonus. Click to register and claim a free $15 bonus.

Real users share their views on Bitcoin cloud mining

Recently, AJC Mining conducted street interviews in the United Kingdom with real cryptocurrency users to understand how they view the current crypto market and the growing popularity of lower-barrier cloud mining.

One user from the UK said:

“I’m usually busy with work and don’t have time to study complicated mining equipment, so I prefer a simpler way to participate.”

Another user commented:

“Being able to check the system status and data changes in real time makes me feel more confident about the whole process.”

A third user said that the biggest value is “peace of mind”:

“I don’t want to watch the market every day. This allows me to focus on my own life instead of market fluctuations.”

Another user added:

“I used to think mining had a very high entry barrier, but after learning more about it, I found that ordinary users can also participate more easily.”

AJC Mining: Cloud mining is becoming a new choice for entering the crypto market

Why is traditional mining difficult for beginners?

Traditional crypto mining often requires expensive mining machines, high electricity costs, technical setup, equipment maintenance, and professional operational knowledge. These challenges make it difficult for many ordinary users to participate directly in mining.

Why Is Cloud Mining more suitable for everyday users?

With AJC Mining Cloud Mining, users do not need to purchase mining machines or handle technical issues. The platform manages mining resources in a centralized way, making it easier for users to participate in crypto mining.

For users searching for a reliable Bitcoin Cloud Mining Platform, AJC Mining provides a simpler way to access mining services without the complexity of traditional mining infrastructure.

How does AJC Mining help users start mining?

Users only need to select and purchase a cloud mining contract. AJC Mining manages the mining operations, allowing users to start mining easily, track income growth in real time, and participate without technical experience.

What data can users view?

AJC Mining provides users with access to mining status, system performance, and income updates. The process is designed to be transparent and intuitive, allowing users to monitor their cloud mining activity more clearly.

Core advantages of AJC mining cloud mining

AJC Mining offers several key advantages for users interested in Bitcoin Cloud Mining, LTC Cloud Mining, DOGE Cloud Mining, and BCH Cloud Mining:

- Professional data centers and standardized mining farm facilities designed to improve operational stability and efficiency.

- Security technologies associated with McAfee® and Cloudflare® to help protect user accounts and digital assets.

- Global mining farm deployment to reduce the impact of single-region fluctuations.

- A professional engineering team that conducts regular inspections and maintenance to support long-term platform stability.

Join AJC Mining and start a more efficient cloud mining journey

Step 1 — Create an Account

Complete registration in just a few seconds and receive a $15 new user bonus.

Step 2 — Choose a Plan

Select from popular cloud mining contracts with flexible cycles ranging from 1 to 50 days.

Step 3 — Start Earning

Once the contract is activated, the system runs automatically, helping users begin daily income generation more easily.

AJC Mining cloud mining contract examples

| Contract Name | Price | Daily Profit | Number of Days | Principal + Total Return |

| New User Experience Contract | $100 | $4 | 2 Days | $100 + $8 |

| Avalon Miner A15 | $500 | $6.25 | 5 Days | $500 + $31.25 |

| Litecoin Miner L9 | $1,000 | $13 | 10 Days | $1,000 + $130 |

| Bitcoin Miner S21 XP Imm | $5,000 | $70 | 25 Days | $5,000 + $1,750 |

| Bitcoin Miner S21e XP Hyd | $10,000 | $150 | 35 Days | $10,000 + $5,250 |

| ANTSPACE HW5 | $50,000 | $900 | 45 Days | $50,000 + $40,500 |

According to the contract descriptions, all contracts follow a “daily profit + principal return” model. Profit distribution is presented transparently and is open to all users.

(Click here to view more contract details.)

AJC Mining supports multiple cloud mining options

AJC Mining is not only focused on Bitcoin Cloud Mining. The platform also provides access to several popular cloud mining options, including:

LTC cloud mining

Litecoin remains one of the most established digital assets in the crypto market. AJC Mining offers users a convenient way to participate in LTC Cloud Mining.

DOGE cloud mining

Dogecoin continues to attract global attention because of its strong community and market popularity. Through DOGE Cloud Mining, users can participate in Dogecoin-related mining more easily.

BCH cloud mining

Bitcoin Cash also maintains a presence in the digital asset market. AJC Mining provides BCH Cloud Mining options for users interested in Bitcoin Cash mining services.

By supporting Bitcoin, Litecoin, Dogecoin, and Bitcoin Cash, AJC Mining is positioning itself as a multi-asset Cloud Mining platform for users who want flexible access to mining opportunities.

Conclusion: AJC Mining is becoming a popular Bitcoin cloud mining platform

As high-performance blockchain ecosystems such as Solana continue to expand, the crypto market is attracting renewed attention from ordinary users. The recent street interviews conducted by AJC Mining in the United Kingdom show that many users prefer a simpler and more transparent way to participate in mining, especially when compared with the technical complexity of traditional mining.

Through professional mining farm deployment, global hashrate management, and transparent system operations, AJC Mining is working to provide a more stable and efficient Cloud Mining experience. For users looking for an easier way to participate in the crypto market, cloud mining is becoming an increasingly popular choice.

For those searching for AJC Mining, Cloud Mining, Bitcoin Cloud Mining, Bitcoin Cloud Mining Platform, LTC Cloud Mining, DOGE Cloud Mining, or BCH Cloud Mining, AJC Mining offers a convenient platform to explore multiple cloud mining opportunities.

For more information, visit the official website or download the mobile app.

Disclosure: This content is provided by a third party. Neither crypto.news nor the author of this article endorses any product mentioned on this page. Users should conduct their own research before taking any action related to the company.

Circle Internet Group agreed to sell 740 million ARC tokens for $222 million in a private placement led by a16z Crypto, valuing the Arc blockchain network at $3 billion on a fully diluted basis.

The New York Stock Exchange-listed issuer of the USDC stablecoin disclosed the token presale Monday alongside its first-quarter 2026 results, which showed higher revenue and reserve income but lower net income.

The round was led by a16z Crypto and backed by a consortium including BlackRock, Apollo Funds, ARK Invest, Bullish, General Catalyst, Haun Ventures, Intercontinental Exchange, IDG Capital, Janus Henderson Investors, Marshall Wace, SBI Group and Standard Chartered Ventures.

Circle entered into the token purchase agreements on Friday, agreeing to sell the ARC tokens at $0.30 each in a private placement exempt from registration under the US Securities Act of 1933.

The sale marks a major step in Circle’s effort to expand beyond stablecoin issuance into blockchain infrastructure, as the company seeks to build Arc into a settlement layer for stablecoin finance, tokenized assets and programmable financial markets.

Circle first introduced Arc in August 2025 as an open layer-1 blockchain focused on stablecoin finance. It also published a whitepaper on Monday, describing ARC as a “native coordination asset” designed to support governance, security and network operations on the system.

ARC token powers Circle’s “Economic OS” blockchain

Circle’s Arc whitepaper describes ARC as the native token of its layer-1 “Economic OS” blockchain built for stablecoin-based finance and tokenized markets.

The network uses a hybrid consensus approach, combining permissioned validators with a planned shift toward proof-of-stake (PoS) from the proof-of-authority (PoA) consensus model.

ARC’s five interconnected functions. Source: ARC

Circle said ARC has a fixed initial supply of 10 billion tokens allocated across three buckets, with about 60% going to the ecosystem for developers, grants and network growth, while 25% is reserved for Circle to support development, staking and governance participation.

The company said the remaining 15% is set aside as a long-term reserve to provide flexibility and stability during market stress or future network needs.

Related: Canton Network creator targets $300M in capital raise: Report

Circle’s Q1 revenue rises as USDC growth offsets higher costs

Circle’s financial performance in the first quarter was driven primarily by continued growth in USDC circulation and transaction activity.

USDC in circulation rose 28% year over year to $77.0 billion at quarter end, while onchain transaction volume surged 263% to $21.5 trillion. Total revenue and reserve income, which includes earnings from USDC reserves and other business lines, rose 20% to $694 million.

Source: Circle

Net income fell 15% to $55 million, as higher costs outweighed revenue growth. Operating expenses rose 76% to $242 million, driven mainly by post-IPO stock-based compensation and related payroll taxes, along with continued investment in product, distribution and infrastructure.

Even so, Circle’s underlying business performance improved, with adjusted EBITDA rising 24% to $151 million.

Circle (CRCL) stock price chart year-to-date. Source: Yahoo Finance

Circle (CRCL) shares were up around 3% in premarket trading to $116.7, extending recent gains, according to Yahoo Finance. The stock is up around 12.2% over the past month and more than 40% year to date.

Magazine: XRP ‘probably going to $12,’ Bitcoin ETFs add $1B: Market Moves

Politics Home Article | Rebel MP To Canvass MPs For September Labour Leader Election

Ref Daniel Siebert gets PSG vs. Arsenal final after being left off World Cup list

Why Changing Passwords Doesn’t End an Active Directory Breach

Manchester United reach agreement with Casemiro over contract clause amid transfer speculation

US brings back mandatory military draft registration

Steven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

$10K Bitcoin Crash Imminent? (Weekend Warning!)

senior citizen card benefits #viral #kannada #facts #finance #education #shorts #governmentbenefits

Stellar Lumens XLM And An Institution That Enables 11.5% of *ALL* Financial Assets…. BIG NEWS

-

Crypto World3 days ago

Crypto World3 days agoHarrisX Poll Found 52% of Registered Voters Support the CLARITY Act

-

Crypto World4 days ago

Crypto World4 days agoUpbit adds B3 Korean won pair as Base token gains Korea access

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: Marianne Dress

-

Tech7 days ago

Tech7 days agoImage AI models now drive app growth, beating chatbot upgrades

-

NewsBeat4 days ago

NewsBeat4 days agoNCP car park operator enters administration putting 340 UK sites at risk of closure

-

Politics2 days ago

Politics2 days agoPolitics Home Article | Starmer Enters The Danger Zone

-

Tech1 day ago

Tech1 day agoAuto Enthusiast Carves Functional Two-Stroke Engine from Solid Metal

-

Business2 days ago

Business2 days agoIgnore market noise, India’s long-term story intact, say D-Street bulls Ramesh Damani and Sunil Singhania

-

Crypto World6 days ago

Crypto World6 days agoUAE Free Zone Deploys Blockchain IDs to Verify Registered Firms

-

Tech8 hours ago

Tech8 hours agoGM Agrees To Pay $12.75 Million To Settle California Lawsuit Over Misuse Of Customers’ Driving Data

-

Crypto World4 days ago

Crypto World4 days agoRobinhood says Wall Street is building onchain

-

Crypto World5 days ago

Crypto World5 days agoBlackRock CEO Larry Fink Discusses a New Asset Class

-

Entertainment7 days ago

Serena Williams hits Met Gala in metallic dress after GLP-1 reveal

-

Tech6 days ago

Tech6 days agoApple and Samsung are dominating smartphone sales so thoroughly that only one other company makes the top 10

-

Tech5 days ago

Tech5 days agoI tested the Xiaomi 17 Ultra’s camera and I don’t think I’ll ever go back to an iPhone

-

Politics6 days ago

Politics6 days agoMet Gala 2026: Madonna’s Dramatic Red Carpet Look Steals The Show

-

Fashion5 days ago

Fashion5 days agoThe Best Work Pants for Women in 2026

-

Sports7 days ago

Sports7 days agoEverton v Man City LIVE: Haaland’s two-word response as visitors collapse to hand Arsenal advantage in Premier League title race

-

Crypto World4 days ago

The FOMO Is Back: Why Bitcoin’s Latest Rally Has Analysts Flashing Warning Signs

-

Tech4 days ago

Tech4 days agoAI agents are missing all the discussions your team is having. SageOX has an answer: agentic context infrastructure

You must be logged in to post a comment Login