Crypto World

Warsh Testifies to Congress Today: Will He Bring a Rate Hike in July?

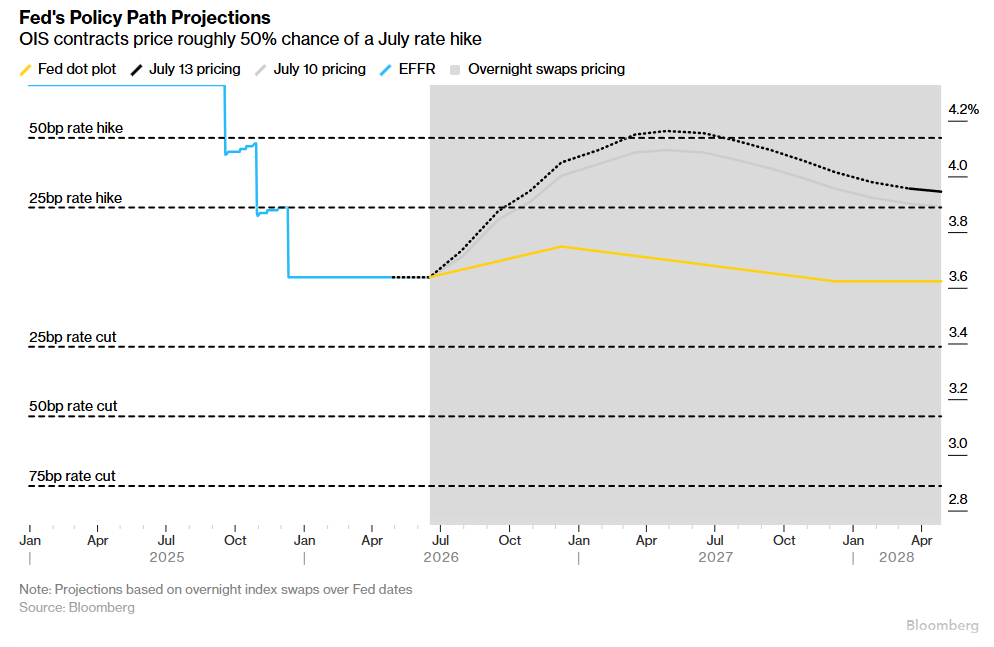

Federal Reserve Chairman Kevin Warsh testifies before Congress Today, July 14, and tomorrow. Bond traders increasingly bet the week will confirm what markets already suspect. A rate hike is coming in July.

The testimony lands alongside fresh inflation data and a wave of bank earnings. That makes this one of the most consequential weeks for anyone with a mortgage, a savings account, or a credit card balance.

Why Rate-Hike Odds Have Jumped

Traders have pushed the market-implied chance of a quarter-point hike this month to about 50%. Just weeks ago, that number sat under 10%. Two-year Treasury yields, which track Fed policy expectations closely, have stayed above 4.25%.

Fed Governor Christopher Waller triggered the shift. Markets had viewed him as one of the central bank’s most dovish officials. Waller said policymakers should consider a hike soon if upcoming data show another “hot reading” on core prices.

June’s Consumer Price Index, also releasing Tuesday, should show headline inflation easing to around 3.8% from May’s 4.2%. Falling gas prices are driving that drop.

Core inflation, which strips out food and energy, should tick down only slightly, to around 2.8% from 2.9%. That keeps it well above the Fed’s 2% target. This stickiness is exactly why rate-sensitive chip stocks still face CPI risk.

Don’t Expect Warsh to Tip His Hand

Warsh took office in May and he has already built a reputation for avoiding forward guidance. He made that clear this month at a central-bank symposium in Portugal.

“I want us to have a good family fight. When we get into that room and shut the door, we’re going to have a good debate, but I don’t have much more for you than that.”

So the testimony itself likely won’t confirm a hike. Instead, expect lawmakers to press Warsh on Fed independence from the Trump White House.

They’ll also ask whether AI-driven demand is adding to inflation, and how tariffs and Middle East oil disruptions keep filtering into consumer prices.

The real decision arrives at the Fed’s July 29 meeting, not this week’s hearings.

What a Hike Would Mean for Regular Households

A hike would raise rates on credit cards, home equity lines, and adjustable mortgages. That’s unwelcome news for borrowers already stretched by elevated inflation. Savers benefit more directly. Banks typically raise yields on savings accounts and CDs when the Fed hikes.

The post Warsh Testifies to Congress Today: Will He Bring a Rate Hike in July? appeared first on BeInCrypto.

ZachXBT says an old iPhone beats any hardware wallet for storing crypto. Tornado Cash developer Roman Storm agrees, but says one missing feature breaks the whole iPhone wallet plan.

That feature is the BIP39 passphrase. It is a secret extra word that hides your real wallet behind an empty one.

The One Feature the iPhone Wallet Plan Is Missing

The on-chain investigator’s frustration has a track record behind it. Bybit lost $1.5 billion in February 2025 after attackers tricked its signers into approving a bad transaction. The keys stayed safe. The money is still left.

“All hardware wallets are complete garbage and I do not advise using them for important tasks like signing transactions or storing funds. Much better to have a separate iPhone with its only purpose being to use as your hardware wallet,” ZachXBT noted.

Follow us on X to get the latest news as it happens

Storm liked the idea. However, his reply comes with a warning.

“I’d agree – if there were actually a mobile app with BIP39 passphrase support.”

Here is why that matters. Your seed phrase is 12 or 24 words, usually written on paper. Add a passphrase, and those same words open a completely different wallet.

So a thief who finds the paper sees an empty account. One UK holder lost roughly $172 million after his Trezor recovery phrase appeared on home CCTV. A passphrase would have made that recording worthless.

The threat is growing, too. Chainalysis logged 158,000 personal wallet compromises in 2025, nearly triple 2022’s count. Those attacks hit 80,000 victims for $713 million. Moreover, one seed phrase vulnerability alone drained $3.1 million this month.

Hardware Wallets Have It. Mobile Wallets Don’t

Storm listed the split. Trezor, Ledger, Coldcard, Keystone, and BitBox all support passphrases. Meanwhile, MetaMask has ignored requests since 2021. Trust Wallet skips it, too. Rabby only offers it on desktop, leaving AirGap Vault as the lone mobile option.

His fix is simple. Mobile wallets should support passphrases and air-gapped signing, so the phone never connects to the internet. Trail of Bits research backs the same principle of capping losses when keys leak.

There is a downside, though. Casa co-founder Jameson Lopp warned in an interview that people often lose their passphrases and lock themselves out forever.

The threat is not just thieves. Hong Kong can already force travelers to unlock phones and wallets at the border.

Trezor Pushes Back on the Phone-as-Vault Plan

Trezor is not conceding the point. Like Storm, Danny Sanders, the company’s chief commercial officer, praised ZachXBT’s detective work but rejected the swap.

Sanders argued that phones are general-purpose devices with too many doors. Zero-click exploits are a documented reality, he noted.

A hardware wallet also acts as an independent second screen. If a phone is compromised, nothing separates checks from what you sign.

He added that creating seed words on a phone risks iCloud backups and clipboard leaks. Even the battery works against the plan. An iPhone stored for years can degrade, and reviving it needs Apple’s activation servers and an Apple ID.

Storm, who awaits a retrial in his Tornado Cash case, put the ball in wallet makers’ court. If MetaMask or Trust Wallet adds the field, millions of old phones could become real crypto vaults.

The post Using an iPhone as Crypto Wallet? ZachXBT and Roman Storm Weigh In appeared first on BeInCrypto.

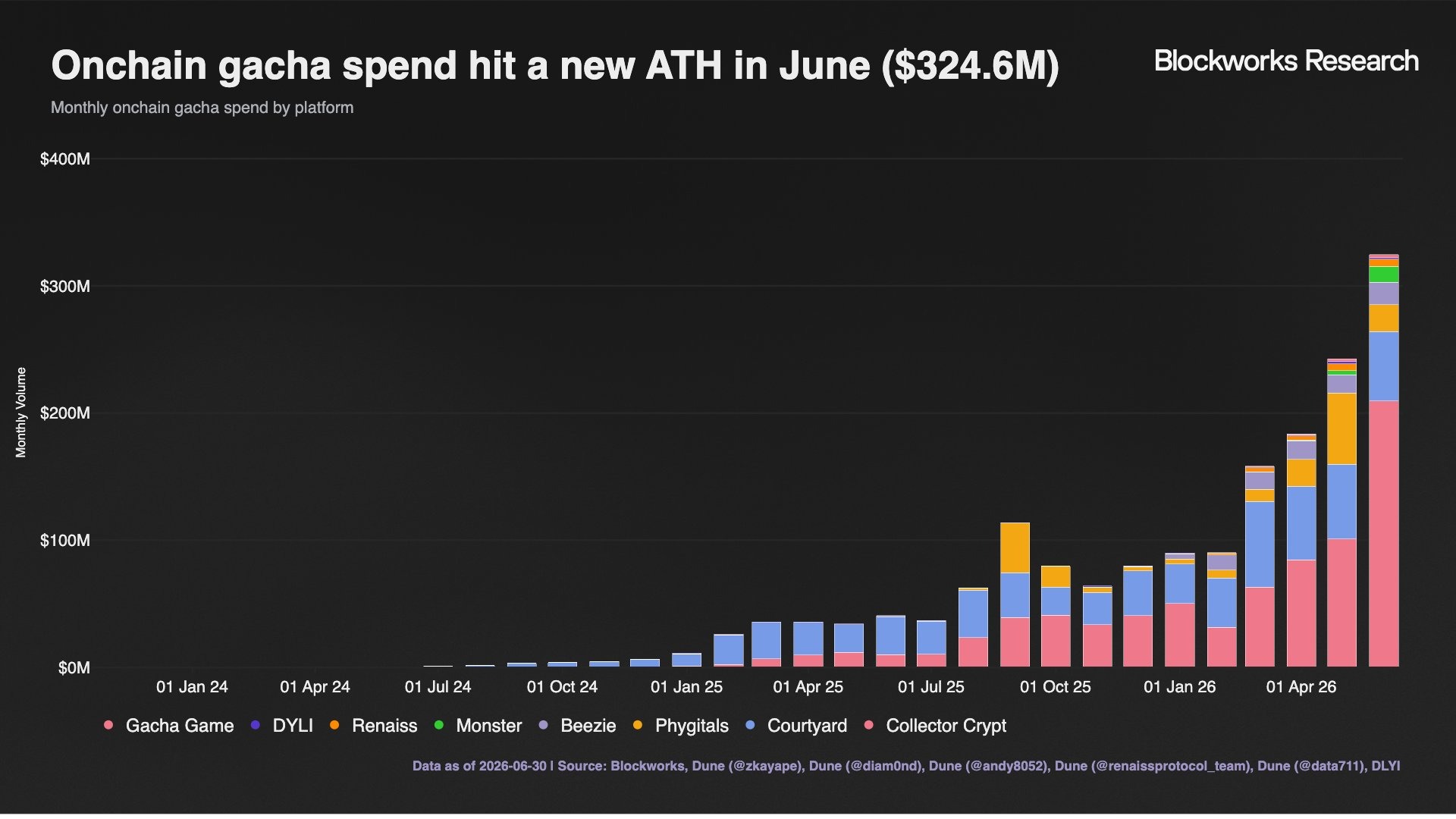

Crypto prices may have been in freefall in June 2026, but a niche corner of the tokenization boom is showing just how resilient consumer demand can be. Bitcoin dropped more than 20% and traded near a 21-month low, while spot Bitcoin exchange-traded funds recorded their worst stretch on record with $4.5 billion in outflows, according to Cointelegraph coverage.

At the same time, Blockworks Research reported that users spent a record $324 million on onchain gacha—an enormous jump from roughly $50 million in the same month a year earlier. The activity underscores how “randomized” collectibles mechanics, now tokenized and accelerated on blockchain rails, are drawing attention even during broader market stress.

Key takeaways

- Onchain gacha spending hit $324 million in June 2026, per Blockworks Research—up sharply from about $50 million a year earlier.

- Tokenized trading cards rely on physical custody and grading assumptions, shifting risk from buyers of cards to users of NFTs.

- Instant buyback and rapid trade cycles mimic gacha/loot-box behavior while compressing the time required to sell offchain.

- Collectors still participate in real-card redemption, including NFT burns that represent claims to physical assets on platforms like Courtyard, based on Dune.

From booster packs to blockchain packs

Gacha traces its roots to Japanese vending machines: pay a fixed amount and receive a randomized item. In traditional trading card games, this typically takes the form of sealed booster packs that contain an unpredictable assortment. The value of the cards inside can vary dramatically based on rarity, condition, print run, and the year of release—creating a market where prices can span from very small amounts to prices that reach the hundreds of thousands of dollars for pristine copies.

Because condition and authenticity matter so much at the high end, grading has become central to how these collectibles trade. Independent graders such as PSA, Beckett, or CGC evaluate attributes like centering, wear on corners and edges, and surface imperfections, then encapsulate the card in a sealed holder (“slab”). Two visually similar cards can command very different prices once graded.

That is the gap blockchain projects aim to bridge. According to the article, platforms such as Collector Crypt and Courtyard tokenize real collectibles by accepting physical cards (often already graded), storing them in vaults, and issuing NFTs tied to specific cards and stated grades. When a user opens a pack, the system delivers a token backed by a corresponding physical asset held in custody. Users can keep the NFT, trade it on marketplaces, sell it back to the platform, or redeem it for the physical card.

The core dependency is straightforward but important: the NFT value depends on whether the vault truly holds the exact card in the claimed condition. That places custodial and integrity risk on platform operators—risk that the article notes is not theoretical, as grading companies themselves report fraud and counterfeits.

What drove the June surge

Tokenized gacha’s rise is unlikely to be explained by one variable. The report points to several converging factors, including strong brand momentum in Pokémon and an onchain infrastructure that makes buying, trading, and verification feel immediate.

On the consumer side, the article cites Circana research saying Pokémon became the most popular toy brand in the U.S. in 2025, generating $2.5 billion in sales—up 87% year over year. It also points to interest from older collectors, not just children, alongside heightened demand for card grading.

That grading demand appears to have spilled into operations. In June, PSA reportedly suspended new submissions across four basic service levels while working through a backlog of nearly 10 million cards, according to the service-level update referenced in the article. Tokenization, in this framing, plugs into a market where collectors want liquidity and frictionless access, but where traditional channels can be slow and expensive.

The article also draws a direct line between tokenized packs and mainstream excitement around trading cards, noting that high-profile buyers such as Logan Paul have helped keep Pokémon in the public spotlight.

The mechanics: speed, buybacks, and speculation

While the collectibles are physical, the market behavior is increasingly shaped by how fast users can cycle positions. A major friction in the traditional offchain trading-card market is liquidity. Selling a card often requires finding a counterparty, confirming authenticity and grade, and arranging shipping.

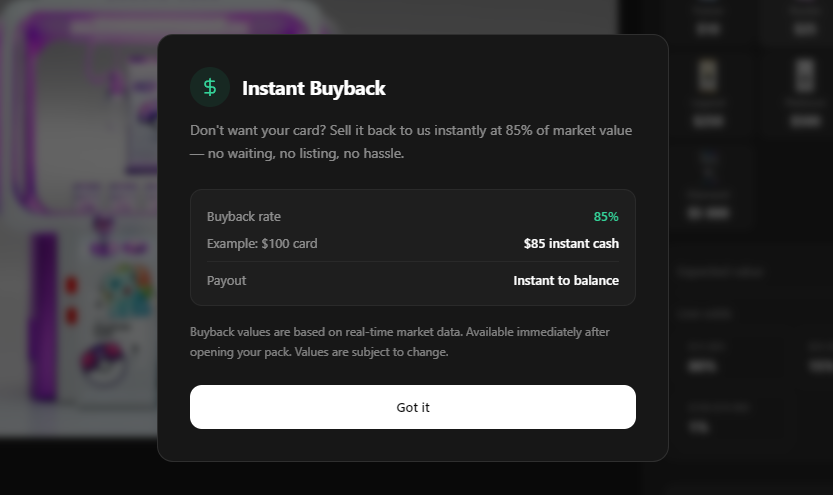

Onchain tokenized trading cards can reduce that friction by offering built-in pathways for trading. The article specifically describes an “instant buyback” mechanism: many platforms allow users to sell packs/cards back shortly after opening—so if the outcome disappoints, users can cash out quickly (for example, at a discount such as 85% of value in the article’s description) and open another pack. If the card is desirable, users can list it or hold it.

This creates a “gacha loop” that compresses what can take weeks offchain into minutes or seconds onchain. The article compares the effect to loot boxes in video games—where users pay for randomized outcomes and the appeal often includes the dopamine and uncertainty around rare pulls.

There are regulatory implications in the background. The article notes that some jurisdictions have tried to bring loot boxes under gambling frameworks. Whether tokenized TCG mechanics fall into similar categories could depend on how large the sector becomes and how platforms structure odds, marketing, and redemption terms. For now, the key operational difference highlighted is tempo: the same gacha logic plays out faster in the onchain environment.

Collectors haven’t disappeared—redemption still exists

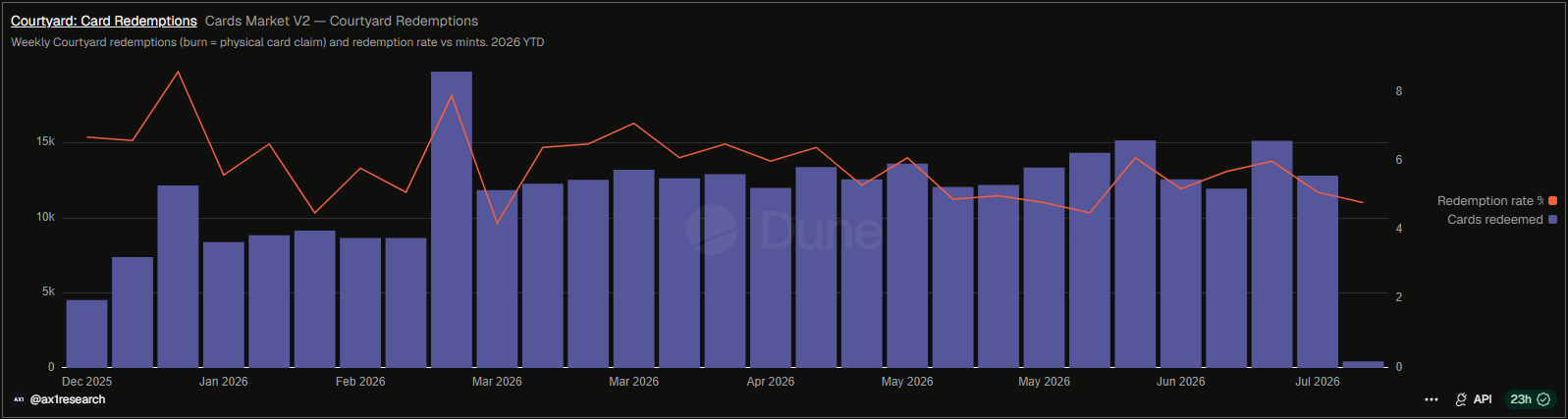

Despite the gambling-like loop, tokenized trading cards also serve a less flashy purpose: enabling real collectors to hold and redeem physical assets. According to Dune data cited in the article, users burn 5% to 8% of NFTs issued on Courtyard each week, with each burn representing a claim to a physical card.

Collector Crypt’s head of marketing, Dakota Campbell, is cited as saying that around 30% of its users eventually redeem a card. He also claims that many users choose to hold rather than constantly flip, often beyond the 72-hour buyback window described in the article.

Campbell further reports that, in the prior 30 days referenced in the piece, 5,400 assets were shipped to 634 unique users with a total insured value of $3.29 million. That detail matters because it anchors the story in actual custody and logistics, not only trading behavior.

Why this matters beyond one record month

Blockchain startups are essentially taking an established collectibles playbook—tokenizing and routing demand through faster rails. But the sustainability of onchain gacha is an open question. The article emphasizes that inflows can reverse quickly, since the gacha loop runs in both directions and user engagement can be sensitive to broader sentiment.

For readers and market participants, the key thing to watch next is whether platforms can maintain trust and real-world custody at scale—especially as counterfeit risk and consumer protection concerns remain persistent themes in graded-card markets—while also building durable collector communities that go beyond short-term speculation.

On August 26-27, Belgrade’s Sava Centar will host Solana Summit Serbia, bringing together financial regulators, banks and fintech, major tech companies, investors, academia, and the Solana ecosystem for a two-day summit expected to draw 1,000+ attendees, 50+ speakers, and around 50 companies.

“For the first time ever, we’re putting local government officials, finance executives, university professors and entrepreneurs together with the Solana ecosystem under one roof,” said Marko Djurdjevic, co-founder & CEO of Superteam Balkan. “Belgrade is becoming a key regional hub for innovation at the intersection of fintech and AI startups built on Solana.”

Finance, Tech, and the Solana Ecosystem Under One Roof

The two-day program brings together senior government officials, financial regulators and policymakers, banks and fintech, global technology companies, investors, and professors from the University of Belgrade and the University of Novi Sad, alongside the Solana ecosystem. Speakers and guests include Microsoft, Raiffeisen Bank, a16z, Chainalysis, ChainSecurity, Electrocoin, ECD.rs, Monri Payments, Solana Foundation, Solflare, Kamino, Jito, Arcium, Streamflow, BlastCtrl, and over 40 others.

What’s on the program

The agenda spans keynotes, panel discussions, an expo zone, workshops, and a startup pitch competition. Topics include the implementation of Serbia’s Capital Markets Development Strategy, digital assets regulation, payments infrastructure, security and compliance, venture capital in the Balkan region, and Solana ecosystem topics including company tokenization, emerging opportunities, and more.

Registration is free and open now via the official event website.

About Solana Summit Serbia

Solana Summit Serbia takes place August 26-27 at Sava Centar in Belgrade. The two-day event convenes financial regulators, banks and fintech leaders, global technology companies, investors, and academia alongside the Solana ecosystem, with 1,000+ attendees, 50+ speakers, and around 50 participating companies expected. More information is available at solanasummit.rs.

About the Organizer

Solana Summit Serbia is organized by Superteam Balkan, Solana’s official chapter for the Balkan region, active across 11 countries. Superteam Balkan has distributed over $500,000 in non-equity grants, supported regional startups in raising more than $10 million from investors, and grown to over 2,000 members across the region.

About Solana

Solana is a high-performance blockchain network, processing over $2 trillion in quarterly stablecoin transfers and $300 million in monthly payments volume.

Live since 2020, it has become the infrastructure of choice for payments companies, financial institutions, and startups building at the intersection of traditional finance and onchain technology.

The post Belgrade to Host Solana Summit Serbia, a Major European Solana Event appeared first on BeInCrypto.

BlackRock’s BUIDL looks like a stablecoin, pays interest like a bond fund, and is legally neither. Tokenized money market funds are the fastest-growing real-world asset in crypto, and almost nobody who talks about them can explain what you actually own.

Summary

- A tokenized money market fund is a regulated fund holding short-term instruments such as Treasury bills, repo, and cash, whose shares circulate as tokens on public blockchains instead of sitting only in a traditional register.

- They look like stablecoins and are legally the opposite. Payment stablecoins are barred from paying holders interest; tokenized money market funds are securities that distribute money market returns.

- Tokenized Treasury products grew from under $1 billion in early 2024 to more than $15 billion by April 2026, led by BlackRock’s BUIDL at roughly $2.5 to $3 billion.

- Access is permissioned. Wallets must be allow-listed by a transfer agent after identity checks, and transfers to unapproved addresses fail at the contract level. This is not a permissionless crypto asset.

- The uncomfortable data: roughly 90% of BUIDL and WisdomTree’s WTGXX sits in about four wallets each, and the main holders are DeFi protocols using the tokens as collateral, not retail savers.

For a decade, crypto’s answer to the question of where to park idle dollars was a stablecoin, and stablecoins had one glaring flaw as a savings instrument: they paid you nothing while the issuer collected the interest on the reserves. Tokenized money market funds are the industry’s response, and they have quietly become the most successful real-world asset category in existence. BlackRock, JPMorgan, Franklin Templeton, and Circle all now run one. The category went from essentially nothing to over $15 billion in about two years. And yet the basic question of what a holder actually owns, and what rights come with the token in the wallet, is answered wrong constantly, including by people trading them. This guide covers the structure, the mechanics, the major products, and the concentration problem sitting underneath the growth story.

What a tokenized money market fund is

A money market fund is one of the oldest and dullest products in finance. It pools money, invests it in very short-term, very low-risk instruments, and pays out the interest those instruments generate. Treasury bills with weeks to maturity, overnight repurchase agreements secured by Treasuries, and cash. The fund targets a stable value per share, conventionally one dollar, and the return comes from the underlying yield.

A tokenized money market fund is that same product with one change: the shares are represented as tokens on a blockchain, and the ownership record is maintained on-chain through a permissioned system rather than solely in traditional book-entry form. The fund still holds the same T-bills. The manager still runs the same mandate. The custodian bank still holds the underlying securities. What changes is the settlement rail.

That change is smaller than the marketing suggests and more consequential than the skepticism allows. It is not a reinvention of the product. It is a decades-old instrument moved onto infrastructure that settles in minutes instead of on a T+1 or T+2 cycle, operates continuously, and lets the share itself be programmable. Managers cut operational cost, holders gain around-the-clock mobility, and regulators get an auditable real-time record. Nobody involved is promising a revolution. They are removing settlement friction from cash management, which is a real if unglamorous prize.

Legally, these are securities. They are regulated and supervised by securities authorities, and the classification is what separates them from the thing they resemble.

Why they are not stablecoins

This is the distinction everything else depends on, and it is a legal one rather than a technical one.

A payment stablecoin such as USDC is designed as a settlement asset: a token that holds a dollar and moves. Under the GENIUS Act, US payment stablecoin issuers must hold full reserves in liquid assets, and they are prohibited from paying interest to holders. The issuer earns the yield on the reserves. You get the dollar.

A tokenized money market fund is designed as an investment: a token representing a share in a regulated fund that distributes returns in line with money market rates. Holders receive the yield. BlackRock’s OnChain Shares filing disclosed a 3.61% seven-day yield as of the end of 2025, which gives a concrete sense of the difference between holding a share and holding a stablecoin.

The odd part is that the two instruments are often backed by nearly identical assets. Both hold short-term Treasuries and cash. The economic substance is close to the same, and the legal classification is completely different, which determines who receives the interest and what rules apply. As one analyst framed it, these are essentially the same asset with different legal classifications and limitations.

The categories are also converging from both directions. The GENIUS Act permits eligible reserve assets, including money market funds, to be held in tokenized form, which means a tokenized fund can sit inside a stablecoin’s reserves. USDS, the third-largest stablecoin globally, reportedly holds BUIDL and JTRSY among its reserves, and Mountain Protocol’s stablecoin and frxUSD have done the same. JPMorgan launched JLTXX in May 2026 explicitly engineered as a GENIUS-compliant reserve asset for stablecoin issuers, seeded with $100 million alongside Anchorage Digital. The tokenized fund is becoming the thing that backs the stablecoin.

How one actually works

The operational flow has five steps and is considerably more controlled than a typical crypto transaction.

Step one: identity. The investor completes know-your-customer and sanctions screening with the transfer agent or an authorized platform. There is no anonymous participation.

Step two: allow-listing. The investor’s wallet address is added to an on-chain allow list maintained by the token contract. This is the critical departure from permissionless assets. An unapproved wallet cannot receive or hold the token, and a transfer to a non-approved address reverts at the contract level. The BIS has noted that these products rely on wallet allow-listing to constrain peer-to-peer trading and meet compliance requirements.

Step three: subscription. The investor sends cash, stablecoin, or another approved instrument. Payment methods vary: some funds accept only fiat wires, some accept USDC, some accept both. For BUIDL, investors wire dollars to the fund’s bank account at BNY Mellon.

Step four: issuance. The transfer agent confirms the subscription and the smart contract mints tokens to the whitelisted wallet, while the official ownership record is updated. The trade settles in minutes, bypassing the traditional clearing cycle.

Step five: yield. The interest earned by the underlying assets flows to holders through one of two designs. Accruing tokens hold price at $1.00 and pay rewards by minting additional tokens into holder wallets on a daily or monthly cadence, which is BUIDL’s model. Rebasing tokens grow the balance in each wallet automatically, so a wallet holding 1,000 tokens might hold 1,003.5 a month later.

Redemption reverses the path. Tokens go to the issuer’s contract, the contract burns them, and the administrator pays out dollars or, increasingly, a regulated stablecoin.

Four parties make this work, and it is worth naming them because the marketing tends to omit most. On the traditional side: a manager running the portfolio, a custodian bank holding the underlying securities, and a transfer agent keeping the official ownership record. On the tokenization side: a platform such as Securitize or Tokeny operating the smart contracts, and an oracle, typically Chainlink, publishing the fund’s net asset value on-chain so the token reflects its price.

What you actually own

Here is the part that gets stated backwards most often. The token in your wallet is not the ownership record.

The beneficial ownership of the fund shares remains recorded in the transfer agent’s official register. The token functions as a digital receipt that enables on-chain mobility. When a token moves between two authorized wallets, the system updates the off-chain ownership record to match. JPMorgan, among others, retains the authority to correct discrepancies between the on-chain ledger and the legal record, so that the technological holding never diverges from the legal reality.

Read that again, because it inverts the usual crypto assumption. In Bitcoin, the ledger is the truth. Here, the ledger is a mirror of the truth, and if the two disagree, the off-chain register wins and the chain gets corrected. Holding the token does not by itself prove ownership. Your rights flow from the fund documents, the transfer agent’s register, and the product’s redemption terms.

Access rules vary by product and are restrictive almost everywhere. BUIDL is a Securities Act Rule 506(c) private fund limited to qualified purchasers, with subscriptions starting around $5 million. USYC is available only to non-US persons. Some products carry institutional minimums far above any retail threshold. Acquiring exposure through a secondary market or an unapproved wallet may not carry the same rights as subscribing directly.

Legal structures differ too, in ways that matter. Some tokenized funds are digital representations of shares in a conventional US government money market fund, which allows broader participation but imposes strict liquidity constraints, including the requirement that 99.5% of assets sit in cash, government securities, or repo collateralized by them. Others are not money market funds at all in the regulatory sense, but private funds for accredited investors, exempt from many of the disclosure and liquidity risk management requirements that apply to registered funds. Treating BENJI, BUIDL, USYC, and WTGXX as interchangeable is a mistake, because their legal wrappers are not the same.

The major products

BUIDL is the BlackRock USD Institutional Digital Liquidity Fund, launched on Ethereum on March 20, 2024, with Securitize as transfer agent. It sits around $2.5 to $3 billion across at least eight networks, making it the largest single tokenized Treasury product. Each token targets $1.00, dividends accrue daily and pay monthly as newly minted BUIDL, and holders can custody at Anchorage, Coinbase Custody, Fireblocks, BitGo, Komainu, Copper, or their own multisig provided the wallet is whitelisted. Major derivatives platforms including OKX and Deribit accept it as collateral.

BENJI is the Franklin OnChain US Government Money Fund, the first tokenized money market fund, launched in 2021 on Stellar and since expanded to Polygon, Canton, Ethereum, Arbitrum, Base, Aptos, Avalanche, and Solana. One FOBXX share equals one BENJI token, with the transfer agent maintaining the official record through the Benji platform.

USYC was launched by Hashnote and later folded into Circle. It briefly overtook BUIDL on January 22, 2026 at roughly $2.98 billion, helped by deep integration as collateral on crypto-native venues.

OUSG and USDY, both from Ondo, show the structural creativity. OUSG is a fund-of-fund whose underlying allocation flows substantially through BUIDL, letting an issuer market a token under its own brand with its own fee and minimum structure. USDY is a reward-bearing note for non-US holders.

JLTXX and MONY are JPMorgan’s entries, with MONY launching on Ethereum in December 2025 and JLTXX following in May 2026 as a purpose-built stablecoin reserve asset.

WTGXX is WisdomTree’s Government Money Market Digital Fund, and USTB is Superstate’s short-duration Treasury product.

BlackRock also filed a registration statement in May 2026 for a fund whose OnChain Shares would have their official ownership record maintained through Securitize Transfer Agent using a permissioned system connected to multiple public blockchains. That filing was subject to completion, and the securities cannot be sold until it becomes effective.

What the tokens are used for

Demand does not come from savers. It comes from three institutional use cases.

Collateral. This is the largest driver. A tokenized fund share earns yield while sitting as margin, which a stablecoin cannot do. Crypto prime brokers allow clients including hedge funds to post BUIDL as collateral for derivatives trading, and DeFi protocols such as Aave’s Horizon accept tokenized funds as collateral against stablecoin borrowing. Capital that would otherwise sit idle in USDC now earns Treasury yield without leaving the trading system.

Stablecoin reserves. As covered above, tokenized funds are moving into the reserve baskets of stablecoins, a structural linkage that barely existed two years ago.

Fund-of-fund wrappers. OUSG is the model: build a product on top of another issuer’s fund, tailor the fees and minimums, market it under your own brand.

Notice what is absent from that list. Nobody is buying these to save for retirement. The BIS found that companies operating DeFi protocols are the main investors in BUIDL, and that fact explains the concentration data below.

How the yield actually reaches you

The yield mechanics deserve their own walkthrough, because they are where the tokenized wrapper does something a traditional fund share cannot, and where most confusion about these products lives.

Start with the source. The fund holds Treasury bills, overnight repo, and cash. Those instruments pay interest. That interest accrues to the fund and raises the value of the portfolio. In a conventional money market fund, the manager either lets the share price float slightly or, far more commonly, holds the share at a constant dollar and distributes the accrued income to holders on a schedule. Nothing about tokenization changes this part. The yield comes from short-term government debt, and it is whatever short-term government debt happens to pay.

Now the delivery, which is where the designs diverge. Accruing token models keep the token price pinned at $1.00 and pay rewards by minting additional tokens into holder wallets. BUIDL works this way: dividends accrue daily based on the fund’s net yield and are distributed monthly as freshly minted BUIDL. Your token count rises; each token stays worth a dollar. Rebasing models take the other route, growing the balance in each wallet automatically as rewards accrue, so a wallet holding 1,000 tokens at the start of a month might hold 1,003.5 by the end without any transaction appearing.

The distinction sounds cosmetic and is not, for two reasons. First, integrations break differently. A DeFi protocol that assumes a fixed balance will mishandle a rebasing token, and one that assumes a fixed supply will mishandle an accruing one. Second, the tax and accounting treatment of receiving new tokens is not obviously the same as the treatment of a balance silently increasing, and that difference belongs to the holder.

Then the part that has no traditional analogue at all: the share keeps earning while it works. This is the entire commercial case for the category, and it is worth stating precisely.

In the old arrangement, capital posted as margin sat idle. You wanted yield, so you held a money market fund; you wanted to trade, so you posted cash; you could not do both with the same dollar without a settlement cycle standing between them. A tokenized share collapses that. BlackRock structures BUIDL so exchanges including OKX and Deribit accept it as collateral for derivatives trades, and DeFi lending markets accept tokenized funds as collateral against stablecoin borrowing. The same dollar earns roughly the Treasury rate and backs a leveraged position at the same time.

That is not a marketing flourish. It is a genuine improvement in capital efficiency, and it explains the growth curve better than any narrative about democratized access.

Institutions did not adopt these products because they are on a blockchain. They adopted them because the blockchain let a yield-bearing security move at the speed of collateral, and collateral that earns is strictly better than collateral that does not.

It also explains the concentration. If the product’s killer feature is posting yield-bearing margin against derivatives positions, then the natural buyer is a trading desk or a protocol treasury, not a saver. The design selected its holders. Four wallets is not an accident of a young market; it is the predictable result of building an institutional collateral instrument and describing it as a savings revolution.

The concentration nobody advertises

The growth chart is genuinely impressive: under $1 billion in early 2024 to more than $15 billion by April 2026, with Boston Consulting Group and Standard Chartered projecting the broader tokenization market could reach $16 trillion by 2030. Set against a stablecoin market above $300 billion, tokenized funds are roughly 5% of the on-chain dollar economy, which is small but no longer trivial.

Now the part that appears in the BIS data and almost nowhere in the promotional material. For BUIDL, and also for WTGXX, around 90% of total holdings sit in the hands of only four wallet holders each, according to blockchain data. Demand from DeFi protocols has produced high concentration and limited trading activity.

That is a different product from the one being described in press releases. A category marketed as democratizing access to institutional cash management is, in practice, a handful of protocols and trading desks using an instrument that retail cannot legally touch. The allow-list model guarantees it: if wallets require qualified-purchaser status and $5 million minimums, the holder base will be institutional by construction.

The concentration has a practical consequence beyond optics. Four holders means redemption risk is lumpy. If one of four wallets holding a quarter of a fund decides to exit, the fund must liquidate a meaningful share of its portfolio at once. Money market funds are built for diversified redemption patterns, and a book with four holders does not have one. That risk has not been tested, partly because, as the ECB has observed, the tokenization market is still young enough that stress behavior has not yet been observed.

There is also a regulatory gap worth naming. In the EU, tokenized money market funds fall within the existing Money Market Fund Regulation, but whether they are permitted under MiCA is unclear, since the relevant implementing regulation has not been adopted. And the largest product by assets, BUIDL, is a private fund, which means it is exempt from many of the disclosure and liquidity risk management requirements that registered money market funds must meet. Regulators and the public have limited visibility into whether private tokenized funds have adopted the same liquidity tools, such as portfolio maturity maximums and liquid asset minimums, that registered funds are required to run.

The honest assessment

Tokenized money market funds are the clearest example in crypto of tokenization doing something real. They are not a narrative waiting for adoption. They hold actual Treasuries, pay actual yield, settle faster than the traditional rail, and have found genuine product-market fit as yield-bearing collateral. Compare that to most real-world asset projects, and the difference is stark.

The honest caveats are equally clear. This is not decentralized finance in any meaningful sense: access is permissioned, the ledger defers to an off-chain register, and an intermediary can correct your balance. The holder base is four wallets deep on the largest products. The retail access the category is marketed on does not exist for most of these funds. And the newest use case, sitting inside stablecoin reserves, quietly builds a linkage between the tokenized fund market and the $300 billion stablecoin market that regulators have not yet stress-tested.

The right way to hold both thoughts is this: tokenization worked here because it was applied to a product that did not need reinventing, only rewiring. That is the lesson, and it is a rebuke to every project trying to tokenize something that has no settlement problem to solve.

Disclaimer: This article is for information and educational purposes only and does not constitute financial or investment advice. Tokenized money market funds are securities subject to access restrictions, and eligibility, minimums, and terms vary by product and jurisdiction and can change at the manager’s discretion. Nothing here is a recommendation to buy any product. Always do your own research. Figures are accurate as of July 16, 2026.

Frequently Asked Questions

What is a tokenized money market fund?

It is a regulated fund holding short-term, low-risk instruments such as Treasury bills, overnight repo, and cash, whose shares are issued and recorded as tokens on public blockchains instead of only in a traditional register. Legally the shares are securities. The fund holds the same assets and follows the same mandate as a conventional money market fund; what changes is the settlement infrastructure.

How is it different from a stablecoin?

Legally and economically. Payment stablecoins are settlement assets and, under the GENIUS Act, US issuers are prohibited from paying interest to holders, so the issuer keeps the reserve yield. Tokenized money market funds are securities that distribute money market returns to holders. Both are often backed by nearly identical assets, which is why the distinction is legal classification instead of substance.

What is BUIDL?

The BlackRock USD Institutional Digital Liquidity Fund, launched on Ethereum in March 2024 with Securitize as transfer agent. It is the largest tokenized Treasury product at roughly $2.5 to $3 billion across at least eight networks. It is a Rule 506(c) private fund limited to qualified purchasers, with subscriptions starting around $5 million, targeting $1.00 per token with daily accrued yield paid monthly as new tokens.

Can anyone buy one?

Generally no. Access is permissioned and varies by product. BUIDL is limited to qualified purchasers with multi-million dollar minimums. USYC is restricted to non-US persons. Wallets must pass identity screening and be added to an on-chain allow list before they can hold the token, and transfers to unapproved addresses fail at the contract level.

Do I own the fund shares if I hold the token?

Not by itself. The authoritative ownership record is the register maintained by the transfer agent. The token acts as a digital receipt enabling on-chain mobility, and when it moves between approved wallets the off-chain record updates to match. Some administrators retain authority to correct discrepancies between the chain and the legal record. Your rights flow from the fund documents and the register.

How big is the market?

Tokenized US Treasury products and similar money market funds grew from under $1 billion in early 2024 to more than $15 billion by April 2026. For scale, the stablecoin market sits above $300 billion, making tokenized funds roughly 5% of the on-chain dollar economy. Boston Consulting Group and Standard Chartered project the broader tokenization market could reach $16 trillion by 2030.

Who actually holds these tokens?

Overwhelmingly institutions, and very few of them. The BIS found that companies operating DeFi protocols are the main investors in BUIDL, and blockchain data indicates roughly 90% of BUIDL and WisdomTree’s WTGXX holdings sit with about four wallet holders each. The dominant use is as yield-bearing collateral for derivatives and lending, not as a savings product.

What are the risks?

Concentration is the most immediate: a handful of holders creates lumpy redemption risk that diversified money market funds do not carry. The largest products are private funds exempt from many disclosure and liquidity requirements that registered funds must meet. Regulatory treatment is unsettled in the EU under MiCA. And the growing use of these funds inside stablecoin reserves creates linkages between two markets that have not been stress-tested together.

June 2026 was brutal for the crypto market. Bitcoin (BTC) fell more than 20%, hitting a 21-month low, while spot Bitcoin ETFs saw a record $4.5 billion in outflows.

That did not stop users from spending a record $324 million on onchain gacha during the month, according to Blockworks Research. A year earlier, the monthly figure was closer to $50 million.

Spending hit a new all time high in the depths of a bear market. While crypto prices were tanking, people were opening more and more packs of tokenized Pokémon cards — driven by the thrill, the hope of a profit or the urge to expand a collection.

It’s an entire randomized Real World Asset (RWA) sector that’s flown under the radar… until now.

Onchain gacha spending hit an all-time high in June 2026. Source: Blockworks.

Booster packs, grades and slabs

Gacha is a mechanism borrowed from Japanese vending machines, where a fixed payment yields a random item. In the trading card game (TCG) market, it usually works through booster packs: sealed packs holding a random assortment of cards. The buyer does not know in advance what they will get.

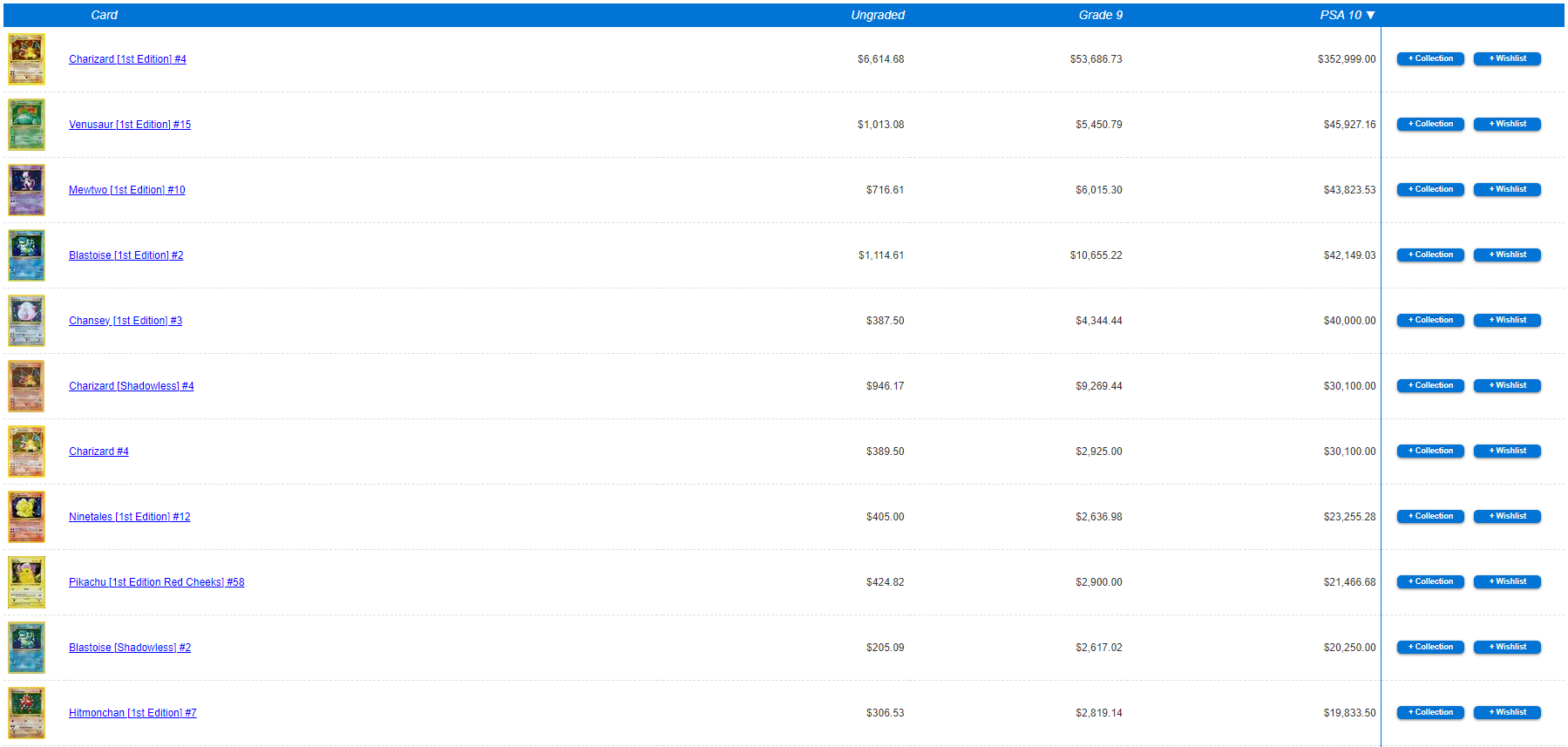

The cards inside a booster are not created equal. Print run, rarity, condition and year of release drive prices orders of magnitude apart: from cents for an ordinary card, to hundreds of thousands of dollars for a rare copy in pristine condition. A market has grown up around those collectibles, which Global Market Insights values at $9.2 billion and Mordor Intelligence at $15.11 billion.

Some cards can fetch several hundred thousand dollars. Source: PriceCharting.

When a card can cost as much as a car, its authenticity and condition have to be assessed.

Related: Logan Paul sells Pokémon card for $16.5M, years after fractional NFT row

That is what grading is for — a process in which an independent company such as PSA, Beckett or CGC checks a card against several criteria. The card is inspected for image centering, the condition of its corners, edges and surface, and for scratches and stains, after which it is assigned a grade and sealed in a plastic case known as a slab.

The grade directly affects the price: two identical cards can be worth completely different amounts, while a raw, ungraded card sells as a riskier asset.

A Pokémon card sealed in a PSA slab. Source: eBay.

Projects such as Collector Crypt and Courtyard are moving these real world assets onto the blockchain. They accept physical cards — usually ones that have already been graded — hold them in vaults and issue NFTs tied to a specific copy.

When a user buys and opens a pack, they receive a token backed by a real card in a real vault. The token can be kept, listed on a marketplace, sold back to the platform or redeemed for the physical card.

Crucially, the value of these NFTs rests on the assumption that the partner vault really does hold that exact card in the stated grade. The user takes on custodial risk — the safety of the asset, the integrity of the authentication and the durability of the platform itself — and with grading companies themselves reporting a rise in counterfeits, that assumption is far from trivial.

Why now?

The growing popularity of onchain gacha, and of TCG-focused blockchain platforms more broadly, is probably down to several factors.

Pokémon cards are the core product for many of these projects, and the franchise is on a roll right now.

According to research firm Circana, Pokémon became the most popular toy brand in the US in 2025, with $2.5 billion in sales, up 87% from a year earlier.

The interest is not coming from children alone. Wealthier members of Generations Y and Z sometimes prefer cards to expensive paintings. Demand for grading is so high that in June, PSA temporarily suspended card submissions across four basic service levels as it tried to work through a backlog of almost 10 million cards.

Tokenization simply plugged into this frenzy by providing a useful service and removing friction.

High-profile buyers like Logan Paul have helped push Pokémon cards into the spotlight. Source: Logan Paul.

The real world trading card market suffers from a problem common to all collectibles markets: the absence of instant liquidity. To sell a card offchain, the owner has to find a counterparty, verify its authenticity and grade, and ship the item.

Related: The 5 types of real world assets being tokenized fastest onchain

“Traditional marketplaces are slow and expensive,” Dakota Campbell, head of marketing at Collector Crypt, told Cointelegraph. “With tokenized trading cards, collectors can buy, sell, trade, and verify ownership instantly while the physical asset remains securely vaulted until they want it shipped.”

Collector Crypt has tokenized roughly $40 million worth of cards and comic books, according to Campbell. About $23 million of that inventory belongs to the platform itself, while the rest sits in user wallets or has already been redeemed. To keep up with demand, the company buys around $2 million worth of cards every week.

Gambling on collectibles

As with the NFT boom, it’s hard to deny that price speculation and gambling-style dopamine hits from the random prizes are part of the appeal.

The instant buyback mechanism, available on most platforms, creates an almost perfect “gacha loop”: Buy a pack, and if the card is unappealing or not worth much, sell it back for, say, 85% of its value and go open the next one. Pull something rare, and either list it on a marketplace or keep it. Unlike with physical cards, there’s no searching for a buyer, no shipping, no waiting.

The “instant buyback” option is available on nearly all TCG platforms. Source: Phygitals.

The gagcha mechanism is similar to loot boxes within video games: The user pays for a random outcome, knowing only the odds. Some jurisdictions have already tried to bring loot boxes under gambling regulations. Whether that logic will reach tokenized TCGs probably depends on how big the sector grows.

Either way, this is exactly how the traditional TCG market works. The only difference is speed: Offchain, closing the gacha loop takes weeks. Onchain, it takes a few seconds.

Sometimes users are driven by nothing more than the desire to “try their luck.” Source: X.

“There is always speculation in an emerging market, especially in the crypto sector,” Campbell said, while arguing that the platform benefits most from committed collectors hunting for their next “grail.”

No country for collectors?

Genuine collectors of physical cards still make up a proportion of the market. According to Dune, users burn 5% to 8% of the NFTs issued on Courtyard each week, with each burn representing a real physical claim.

Users burn 5% to 8% of Courtyard’s issued NFTs each week for physical cards. Source: Dune.

Collector Crypt reports that around 30% of its users eventually redeem a card, according to Campbell, and many more hold their cards in their onchain inventory past the 72-hour buyback window rather than flipping them.

“In just the last 30 days, 5,400 assets shipped to 634 unique users at $3.29 million insured value,” he said.

New tracks for an old train

Essentially, blockchain startups are running the classic tokenization play: moving a proven business model onto more efficient rails and removing some of the friction.

Concerns about the speculative nature of this market, or the role of gambling in it, are warranted to the extent that platforms build their marketing around this aspect.

Beyond that, this is simply how gacha works. People sift through the “junk” in pursuit of a rare card. And if there are complaints to be made, they should be addressed to the entire TCG industry, not just its onchain segment.

As for June’s records, they are the result of several factors converging. The traditional card market is booming, tokenization has proved mature enough to plug into it, and the gacha mechanic sits neatly on blockchain rails.

How sustainable that is remains an open question. The gacha loop runs fast in both directions, and record inflows can reverse just as fast.

Features: Will the crypto lobby’s $189M campaign get CLARITY over the line?

Crypto spent fifteen years arguing the ledger is the truth. Tokenized securities quietly reversed it. The token in your wallet is a receipt, and a company you have never heard of keeps the record that actually decides who owns what.

Summary

- A transfer agent maintains the official register of who owns a security, processes subscriptions and redemptions, issues and cancels shares, and pays out distributions. In the United States they must register with the SEC.

- In tokenized securities, the transfer agent’s off-chain register remains the authoritative legal record of ownership. The token is a digital representation that enables on-chain mobility, not the source of truth.

- If the blockchain and the register disagree, the register wins. Administrators including JPMorgan retain authority to correct the on-chain ledger against the legal record.

- Transfer agents run the allow-list. They screen identity, add approved wallets to an on-chain list, and the token contract blocks transfers to any address that is not on it.

- This inverts crypto’s founding assumption. Whether that is a betrayal or the precise reason institutions will tokenize anything at all is the argument worth having.

Every crypto explainer starts from the same premise: the blockchain is the record, possession of the key is ownership, and no intermediary can reverse it. That premise is true for Bitcoin. It is false for essentially every tokenized security in existence, including the ones BlackRock and JPMorgan are issuing right now. In those products, the authoritative record of who owns what is a database maintained by a company called a transfer agent, and the token in your wallet is a mirror of that database. If the two diverge, the database is right, and the chain gets corrected. Understanding this is not a technicality. It is the difference between understanding what tokenized securities are and repeating a marketing claim about them.

What a transfer agent does

The transfer agent is one of the least glamorous and most load-bearing roles in traditional finance. It exists because a company issuing shares needs someone to answer a deceptively hard question: who owns them right now?

The core functions are these. The transfer agent maintains the register of security holders, the official list of names and balances. It processes transfers when securities change hands, updating that register. It issues new shares when investors subscribe and cancels them when investors redeem. It distributes dividends, interest, and other payments to the holders on the register. And it handles corporate actions, communications, and the reconciliation that keeps everything consistent.

In the United States, transfer agents must register with the SEC under the Exchange Act and operate under its rules. This is not an informal bookkeeping role. It is a regulated function with legal consequences, because the register the agent maintains is what a court would consult to determine ownership.

Traditionally, shares in most listed securities are recorded through a central securities depository, with the Depository Trust and Clearing Corporation performing that function in the US. Each institution keeps its own books, and post-trade steps such as confirmation, clearing, and settlement require multiple intermediaries and repeated reconciliation between those books. The transfer agent sits inside that architecture as the issuer’s official record-keeper.

What changes when a security gets tokenized

The pitch for tokenization is that a shared, consensus-validated ledger replaces fragmented books and eliminates the reconciliation. Instead of every institution maintaining a separate record that must be checked against every other record, all participants read one ledger.

In practice, tokenized securities did not do that. They did something more modest and more interesting.

Tokenized funds use distributed ledger technology to issue and maintain their shares instead of recording them solely through a central depository. That is a real change: settlement collapses from a T+1 or T+2 cycle to minutes, and the share becomes programmable. But the transfer agent did not disappear. It moved.

The structure now looks like this. The transfer agent still maintains the official ownership record. A tokenization platform, most prominently Securitize and also Tokeny, runs the smart contracts that mint tokens on subscription and burn them on redemption. An oracle, typically Chainlink, publishes the fund’s net asset value on-chain. And the token contract enforces the transfer restrictions that the transfer agent’s compliance rules require.

Securitize Transfer Agent LLC is the reference example. It is an SEC-registered transfer agent and broker-dealer, and it maintains the official record for BlackRock’s BUIDL fund. BlackRock’s filing for its OnChain Shares describes Securitize Transfer Agent as maintaining the official record through a permissioned system connected to multiple public, permissionless blockchains, with wallets linked to off-chain identity records.

Franklin Templeton’s structure works the same way: one FOBXX share links to one BENJI token, while the transfer agent maintains the official ownership record through the Benji platform.

Read those descriptions carefully and the architecture becomes clear. A permissioned system, connected to public blockchains, with wallets linked to off-chain identity. The chain is a distribution and mobility layer bolted onto a conventional register. It is not the register.

The token is not the record

This is the single most important idea here, and it is stated backwards in most coverage.

The beneficial ownership of tokenized fund shares remains recorded in the transfer agent’s official register. The token acts as a digital receipt that enables on-chain movement. When a token transfers between two authorized wallets, the system updates the off-chain ownership record to reflect the change. The chain does not replace the register; it triggers an update to it.

And when they disagree? The register wins. JPMorgan, among others, retains the authority to correct discrepancies between the on-chain ledger and the legal record, so that the technological holding never diverges from the legal reality. There is a company with a button that can change what your wallet says, because your wallet was never the authority.

Holding the token does not, by itself, prove ownership. The exact rights depend on the fund’s legal documents, the official ownership record maintained by the transfer agent, and the product’s wallet and transfer rules. The official record is generally the authoritative source.

Consider what that means for a scenario crypto users take for granted. You send tokens to a friend’s wallet. In Bitcoin, that is final and your friend owns them. In a tokenized security, either the transfer fails because the wallet is not allow-listed, or it succeeds and the transfer agent updates the register to reflect the new holder, which happens only because the wallet was pre-approved and identity-linked. There is no version of that transaction where a stranger acquires the security by receiving the token.

Who controls the allow-list

The transfer agent’s most consequential power in tokenized securities is not record-keeping. It is the gate.

Before any subscription, the transfer agent runs know-your-customer and sanctions screening on the wallet owner. The wallet address is then added to an on-chain allow list maintained by the token contract. Smart contracts enforce restrictions from that list: any transfer to an address that is not allow-listed reverts. The BIS has noted that these products rely on the allow-listing of blockchain wallets to constrain peer-to-peer trading and meet regulatory compliance requirements.

The enforcement lives in the token standards. Where stablecoins typically use plain fungible standards such as ERC-20 with unrestricted transfers, tokenized securities often employ security token standards such as ERC-1400 or ERC-3643. Under ERC-3643, a function called isVerified confirms that a recipient appears in the register of allow-listed investors, and canTransfer enforces any additional conditions required before a transfer proceeds. As compliance needs evolve, programmable checks let more complex rules be applied in code.

That is the whole architecture in one sentence: compliance rules, written by a regulated intermediary, enforced automatically by a smart contract, on a public blockchain that anyone can read and almost nobody can transact on.

The practical consequences are worth spelling out. Moving a token to a wallet not on the allow list may be blocked at the protocol or transfer agent level, which is why verifying transfer eligibility before attempting to move a position is not optional. Access through secondary markets or unapproved wallets may not carry the same rights as subscribing directly through the fund or its authorized platform. And restrictions vary sharply by product: some funds are limited to qualified purchasers, some exclude US persons entirely, some impose institutional minimums.

Why this exists

It would be easy to read all of this as institutions gutting the point of a blockchain. The steelman is stronger than that, and it deserves stating properly.

Securities law does not care what technology you use. If an instrument is a security, then rules about who may hold it, how ownership is evidenced, what disclosures are owed, and how sanctions screening works all apply regardless of whether the record sits in Oracle or Ethereum. A tokenized fund that let anonymous wallets hold shares would not be an innovation. It would be an unregistered securities offering with an anti-money-laundering failure attached.

The allow-list model is what makes tokenized funds work inside existing securities and AML frameworks. Without it, none of these products would exist, because no regulated manager would issue them and no regulator would permit it. The choice was never between a permissioned tokenized fund and a permissionless one. It was between a permissioned tokenized fund and no tokenized fund.

And the benefits are real even with the gate in place. Settlement in minutes instead of days. Around-the-clock operation. Shares usable as collateral without leaving the fund, which is why crypto prime brokers accept BUIDL as margin. Real-time auditable records for regulators. Programmability that lets a share do things a book entry cannot. None of that requires the ledger to be the final authority. It only requires the ledger to be fast, shared, and honest about what it is.

The counterargument is equally real. If an intermediary maintains the authoritative record, screens participants, and can reverse the chain, then the blockchain is performing the role of a message bus, and a permissioned database could deliver most of the benefits with less complexity. The transparency argument weakens too, since the interesting record is off-chain. What you are left with is faster settlement and composability with other on-chain assets, which is genuinely valuable but a long way from disintermediation.

Where the two worlds are colliding

The most interesting developments sit exactly at this seam.

The DTCC, the central node in US securities infrastructure, ran its Smart NAV pilot with Chainlink, showing how mutual fund net asset value data can be published on-chain using cross-chain interoperability infrastructure, with multiple global asset managers participating. It has also unveiled a platform for real-time tokenized collateral management. The depository is not being disintermediated. It is tokenizing.

Meanwhile some tokenized funds are pushing the other way. Products including Superstate’s short-duration government securities fund and Franklin’s OnChain US Government Money Fund enable peer-to-peer transactions among approved holders, and BUIDL has been listed on Uniswap’s decentralized exchange for eligible traders. Each step widens the set of things an allow-listed holder can do without going through the issuer, which is a slow migration of function toward the chain without ever surrendering the register.

The tension shows up plainly in retail products. Robinhood’s Stock Tokens are structured as tokenized debt securities that track a stock’s economic performance but confer no voting rights, no shareholder rights, and no direct legal ownership claim on the shares, and they are unavailable to US persons. That is a different structure from a tokenized fund share, and it exists because building a token that conveys actual equity ownership across borders runs straight into the transfer agent and registrar architecture that governs real shares. It is easier to issue a derivative of a stock than to tokenize the stock.

What a failure would look like

A useful way to test whether you understand an architecture is to ask how it breaks, and the transfer agent model has failure modes that differ sharply from the ones crypto users are trained to watch for.

The register and the chain diverge. This is the mundane one and it will happen. A subscription is recorded off-chain but the mint fails. A transfer succeeds on-chain but the register update does not process. For a period, the two records disagree about who owns what. In a permissionless system this would be a crisis with no resolution path. Here it is a reconciliation task, because the hierarchy is defined in advance: the register is authoritative, the chain gets corrected, and administrators such as JPMorgan hold explicit authority to do exactly that. The failure is contained precisely because the system is not decentralized. That is the trade in one sentence.

The transfer agent itself fails. This is the interesting one, and it has no on-chain answer.

If the entity maintaining the register suffers an outage, an insolvency, or a compromise, the authoritative record of ownership is impaired. The tokens still sit in wallets, still display balances, still move between allow-listed addresses. And none of that settles what anyone owns, because the record that decides ownership is the impaired register. Traditional finance has procedures for transfer agent succession, because this risk predates blockchains by a century. But the crypto instinct, which is to point at the chain and say the record is right there, is precisely wrong here. The chain is a mirror. A mirror does not help when the original is gone.

The allow-list becomes the attack surface. Whoever controls which addresses may hold the token controls the asset in a way no key holder does. A compromised allow-list could add unauthorized addresses or, more disruptively, remove legitimate ones, freezing holders out of transfers they are entitled to make. The smart contract will faithfully enforce whatever the list says, because faithful enforcement is its only job. Decentralization does not protect you here; it is what is being enforced against.

Composability breaks at the edge. Tokenized fund shares are increasingly used as collateral across DeFi. But a permissioned token cannot be liquidated to an arbitrary buyer, because arbitrary buyers are not allow-listed. A lending protocol that accepts BUIDL as collateral must have a liquidation path that terminates in an approved wallet, which means its liquidation mechanism depends on a whitelist maintained by a company that has no obligation to that protocol. The composability that makes these tokens attractive is conditional on a permission layer sitting outside the protocol using them, and that dependency has not been tested during a genuine stress event.

None of these are arguments against the model. They are the actual risk register, and it is a different register from the one crypto is used to reading. Nobody is going to lose a tokenized fund position because they mismanaged a seed phrase. They would lose it because an intermediary’s database, an approval list, or a reconciliation process failed, which are exactly the risks tokenization was supposed to have removed and instead relocated.

The question underneath

Strip away the mechanics and one question remains, and it is the one that decides whether tokenization matters.

If the transfer agent’s register is the truth, and the token is a receipt, what exactly has been tokenized? The optimistic answer: the settlement layer, and that alone is worth billions in operational savings and unlocks collateral mobility that did not previously exist. The skeptical answer: nothing important, because the trust assumptions are identical to the ones we had, and we added a blockchain to a system that already worked.

The honest answer is probably that this is a transitional architecture. Right now the register is authoritative and the chain is a mirror, because the law requires a registered intermediary to keep the record and the law has not changed. If it ever does, if a properly regulated on-chain register were permitted to be the record itself, the transfer agent function would not vanish. It would become code plus a compliance oracle, and something would be genuinely different.

Until then, the useful discipline for anyone touching tokenized securities is to hold the correct mental model. The wallet shows you a balance. The register decides whether that balance is yours. Those are two different claims, and only one of them is enforceable in a courtroom.

Disclaimer: This article is for information and educational purposes only and does not constitute financial, investment, or legal advice. Tokenized securities are subject to access restrictions and securities regulation, and eligibility, rights, and terms vary by product and jurisdiction. Nothing here is a recommendation to buy any product. Always do your own.

Frequently Asked Questions

What is a transfer agent?

A transfer agent maintains the official register of who owns a security, processes transfers between holders, issues shares on subscription and cancels them on redemption, distributes dividends and interest to registered holders, and handles corporate actions and reconciliation. In the United States, transfer agents must register with the SEC and operate under its rules, making it a regulated function rather than informal bookkeeping.

What does a transfer agent do in tokenized securities?

The same things, plus two more. It maintains the authoritative off-chain ownership register that the tokens mirror, and it controls the allow-list: screening investor identity, adding approved wallets to an on-chain list, and thereby determining which addresses can legally hold the token. The smart contract enforces those decisions automatically, blocking transfers to addresses that have not been approved.

If I hold the token, do I own the security?

Not by itself. The authoritative record is the register maintained by the transfer agent. The token functions as a digital receipt enabling on-chain mobility, and when it moves between approved wallets the off-chain record updates to match. Your actual rights flow from the fund’s legal documents, the register, and the product’s transfer and redemption rules.

What happens if the blockchain and the official record disagree?

The official record wins. Administrators including JPMorgan retain authority to correct discrepancies between the on-chain ledger and the legal record, so the technological holding never diverges from the legal reality. This inverts the usual crypto assumption that the ledger is the final source of truth, and it is the defining characteristic of tokenized securities as currently structured.

Why can I not send tokenized fund shares to any wallet?

Because the token contract enforces an allow-list maintained by the transfer agent. Security token standards such as ERC-1400 and ERC-3643 build the restrictions into the token itself. Under ERC-3643, isVerified checks whether a recipient appears in the register of allow-listed investors and canTransfer enforces additional conditions. A transfer to an unapproved address reverts at the contract level.

Who are the major transfer agents in tokenization?

Securitize is the most prominent. Securitize Transfer Agent LLC is an SEC-registered transfer agent and broker-dealer and maintains the official record for BlackRock’s BUIDL and its OnChain Shares filing. Tokeny is another tokenization platform operating in this space. Franklin Templeton maintains the official record for BENJI through its own Benji platform.

Does this defeat the purpose of using a blockchain?

That is the genuine argument. Critics note that if an intermediary keeps the authoritative record, screens participants, and can reverse the chain, a permissioned database could deliver similar benefits more simply. Supporters note that securities law requires a registered record-keeper regardless of technology, that the allow-list is what makes these products legal at all, and that faster settlement, continuous operation, and collateral mobility are real gains that do not require the ledger to be authoritative.

How does this differ from Robinhood’s Stock Tokens?

Considerably. Robinhood’s Stock Tokens are structured as tokenized debt securities that track a stock’s economic performance but confer no voting rights, no shareholder rights, and no direct ownership claim on the underlying shares, and they are unavailable to US persons. A tokenized fund share represents an actual registered fund position recorded by a transfer agent. It is easier to issue a derivative referencing a stock than to tokenize the stock itself, precisely because of registrar architecture.

The BNP-backed brokerage infrastructure provider is expanding into tokenized markets and AI-native financial services as both DeFi and TradFi companies pursue onchain business.

ARK Invest has challenged a16z crypto’s view that traditional financial institutions will mainly adopt controlled blockchain systems rather than decentralized finance.

Summary

- ARK argues public blockchains will win institutional adoption as tokenized assets increasingly connect with DeFi.

- A16z expects banks to adopt blockchain primitives while keeping compliance, governance and operational control centralized.

- Standard Chartered forecasts mature DeFi protocols could capture much of the future tokenized asset activity.

ARK director of research Lorenzo Valente called the argument “overly bearish and simplistic” in a response on X. He argued that public blockchains have already gained more traction than earlier private blockchain projects and that institutional finance will increasingly depend on infrastructure created by crypto-native companies.

A16z sees institutions choosing control over open access

The debate began after a16z crypto published an essay titled “TradFi doesn’t want DeFi. It wants blockchains.” The firm argued that banks and asset managers will adopt blockchain features when they reduce costs, improve settlement or expand distribution without giving up control.

Under that model, institutions may use tokenization, programmable money and atomic settlement while limiting open access and pseudonymous participation. A16z described the emerging system as “programmable financial infrastructure” built around regulatory, risk and governance requirements rather than today’s fully permissionless DeFi model.

The firm did not argue that open networks will disappear. Its thesis says institutional blockchain systems and crypto-native DeFi can develop in parallel, with open networks continuing to create technology that regulated firms later adopt.

ARK argues public networks have already proved their value

Valente’s counterargument centers on adoption already taking place on public blockchains. Tokenized funds, stablecoins and other financial assets increasingly operate on networks such as Ethereum rather than isolated private systems.

As previously reported, tokenized real-world assets had crossed $29 billion by April 2026. Tokenized US Treasury products alone reached about $13.4 billion, while more than 40 major financial institutions had launched or developed products using public blockchain infrastructure.

That growth supports part of ARK’s case, although institutional projects are not purely permissionless. Products can use public networks while placing restrictions on investors, wallets, custody and transfers. This allows firms to use shared blockchain infrastructure without adopting every feature associated with open DeFi.

DeFi protocols are gaining institutional connections

Recent institutional activity also shows that the dividing line between DeFi and traditional finance is becoming less clear. Standard Chartered has forecast that $4 trillion in stablecoins and tokenized assets could move onchain by the end of 2028, with established DeFi protocols handling much of that activity.

As reported by crypto.news, the bank identified Aave, Compound and Morpho as potential beneficiaries as institutions move more assets onto blockchain networks. BlackRock’s BUIDL fund has also gained DeFi utility by serving as collateral and connecting with onchain markets.

Other blockchain ecosystems are adding controls directly to decentralized infrastructure.However, XRP Ledger developers have been working on permissioned trading and lending features designed for regulated institutions while maintaining onchain settlement.

Permissioned networks remain a competing model

Traditional finance is also putting capital into systems designed specifically around institutional privacy and control. Canton Network has attracted banks and market infrastructure companies by offering permissioned access and privacy-focused settlement tools.

A crypto.news analysis previously examined the growing competition between Canton’s institution-focused model and Ethereum’s open infrastructure. The two approaches show that financial firms are testing both controlled systems and public blockchain rails rather than following one clear model.

The dispute between ARK and a16z therefore centers less on whether traditional finance will use blockchain and more on which infrastructure will carry the activity. A16z expects institutions to reshape blockchain technology around existing controls. ARK argues that public networks and DeFi protocols have already built liquidity and infrastructure that financial firms will find increasingly difficult to avoid.

Tokenized stock products are continuing to gain traction even as wider crypto markets fluctuate. According to data aggregator Token Terminal, the total market capitalization of tokenized stocks climbed to a record $2.3 billion on Wednesday, reflecting renewed demand for blockchain-based access to equities.

The Ethereum ecosystem led the distribution of tokenized-stock market value with a 34% share, followed by BNB Chain at 30% and Solana at 23%, Token Terminal said in an X post. As more platforms expand “multi-asset” offerings, the shift highlights how tokenized equities are increasingly being treated as a mainstream bridge between traditional finance and onchain infrastructure.

Key takeaways

- Tokenized stocks reached a record $2.3 billion market capitalization, signaling stronger institutional-style exposure to equities onchain.

- Ethereum remains the largest venue for tokenized stocks by share (34%), with BNB Chain (30%) and Solana (23%) close behind.

- Kraken’s xStocks and Binance’s bStocks are among the biggest contributors to tokenized-stock market value, while Ondo Finance remains the top issuer.

- Despite rapid growth in tokenized real-world assets (RWAs), stocks still represent only about 5.5% of the overall tokenized RWA market.

Tokenized stocks hit a new high as access expands

The record figure—$2.3 billion—adds to a broader pattern of capital moving into tokenized versions of traditional financial instruments. Token Terminal’s breakdown points to a multi-chain race for distribution, with Ethereum still setting the pace for market share.

The issuer landscape also shows where liquidity is concentrating. Token Terminal data indicates Ondo Finance is the largest tokenized stock issuer, with $955 million in onchain equities. Two other large products—Kraken exchange’s xStocks and Binance’s bStocks—account for substantial portions of tokenized-stock market value, at $507 million and $334 million respectively, according to Token Terminal’s figures.

For investors, the practical appeal of tokenized stocks is often tied to two features: fractional ownership and the potential for faster, more continuous trading compared with traditional market schedules. For platforms and developers, these same characteristics support a broader product strategy—bringing familiar asset classes onto blockchain networks without requiring users to interact directly with settlement layers.

Which chains and products are driving tokenized-equity adoption

Token Terminal’s chain-level shares show a distribution that is increasingly difficult to ignore. Ethereum’s 34% share underscores that tokenized equities still find deep liquidity on the network with the longest track record for onchain asset issuance and trading. However, BNB Chain’s 30% share indicates that large centralized exchange ecosystems are successfully positioning themselves as distribution channels for tokenized financial products.