Crypto World

What is atomic settlement? Payment-versus-Payment and the and of settlement risk

Atomic settlement means both sides of a deal are complete at the same instant or neither does, removing the centuries-old danger that one party pays and the other fails to deliver. This guide explains payment-versus-payment, why blockchains make it natural, and how banks are now testing it for cross-border trades.

Summary

- Atomic settlement means both sides of a transaction complete at the exact same moment or neither does, removing the risk that one party pays and the other fails to deliver.

- It targets settlement risk, the danger that has haunted finance for decades, most famously when a bank’s collapse left counterparties paid on one leg but not the other.

- Payment-versus-payment (PvP) applies this to currency trades and delivery-versus-payment (DvP) to securities, ensuring the two legs are linked and simultaneous.

- Blockchains and smart contracts make atomic settlement natural, because a single transaction can be programmed to either execute both legs together or fail entirely.

- The shift promises to compress settlement from days toward instant, and bank-backed projects are now testing it for cross-border foreign exchange.

Atomic settlement is a way of completing a transaction so that both sides happen at the same instant or neither happens at all, with no possibility that one party fulfills its obligation while the other fails to fulfill theirs. The word “atomic” captures the essential property: the transaction is indivisible, an all-or-nothing event that cannot be split into a completed half and an uncompleted half. This may sound like an obscure technicality, but it addresses one of the oldest and most dangerous problems in finance, the risk that arises in the gap between agreeing to a trade and actually settling it, during which one party can pay or deliver while the other defaults, leaving the first party out of pocket.

Atomic settlement closes that gap entirely by binding the two sides of a transaction together so they succeed or fail as a single unit. Blockchains, as it happens, are unusually well suited to delivering this property, which is why atomic settlement has become a central promise of tokenized finance.

This guide explains what atomic settlement is, the settlement risk it eliminates, how it applies to payments and securities, why blockchains make it natural, and how banks are now testing it in the real world.

The reason this matters is that settlement risk, though invisible to most people, is a genuine systemic danger that has caused real crises, and the financial industry has spent decades and enormous resources trying to manage it. Atomic settlement offers something the traditional system has never quite achieved: the complete elimination of that risk, not its mitigation but its removal, by making it structurally impossible for one leg of a trade to settle without the other.

Combined with the ability to compress settlement times from days to near-instant, the implications for capital efficiency and financial stability are significant. This guide covers the meaning of atomicity, the nature of settlement risk and the famous failure that named it, the payment-versus-payment and delivery-versus-payment models, a concrete worked example, why blockchains make atomic settlement natural, the move from multi-day to instant settlement, the real-world bank projects now testing it, and the genuine hurdles that remain.

What atomic settlement means

Begin with the core property, because everything else follows from it. A transaction is atomic when it is indivisible: it either completes in full, with both sides fulfilling their obligations simultaneously, or it does not happen at all, with neither side committed. There is no in-between state in which one party has paid and the other has not.

The term is borrowed from computing, where an atomic operation is one that cannot be interrupted partway through, and it carries the same meaning in finance: an atomic settlement cannot be left half-done. If anything would prevent both legs from completing together, the entire transaction reverts, returning both parties to where they started as if nothing had happened.

This all-or-nothing quality is what makes atomic settlement powerful. In an ordinary transaction split across time, there is always a window during which one party has performed and is waiting for the other to perform, and in that window the first party is exposed to the risk that the second fails.

Atomic settlement abolishes that window by making the two performances a single, simultaneous, inseparable event. Neither party can find itself having given value without receiving it, because the giving and receiving are bound together and happen at once or not at all.

The significance is that a risk which traditional finance has always had to manage, monitor, and price, the risk lurking in the gap between the legs of a trade, simply ceases to exist under atomic settlement, because the gap itself is gone. Understanding that the entire benefit flows from this one structural property, indivisibility, is the key to understanding why atomic settlement matters.

The problem it solves: settlement risk

To appreciate atomic settlement, you have to understand the danger it removes, which is called settlement risk, and there is no better illustration than the event that gave one form of it its name. In 1974, a German bank named Herstatt was shut down by regulators in the middle of a business day. Earlier that day, counterparties had paid the bank in German marks as their side of foreign-exchange trades, expecting to receive United States dollars in return once the New York business day began. But the bank was closed before it made those dollar payments, so the counterparties had handed over their marks and received nothing back. They had performed their leg of the trade and were left exposed when the bank failed to perform its leg. This specific danger, where one party pays and the other fails before reciprocating, became known as Herstatt risk, a permanent reminder of what settlement risk can do.

Settlement risk, in general, is the risk that arises in any transaction where the two sides do not settle simultaneously. Whenever there is a gap between when one party performs and when the other does, the party that goes first is exposed to the possibility that the counterparty defaults, becomes insolvent, or simply fails to deliver in that interval. This is sometimes called principal risk, because the party can lose the entire principal amount it advanced, not merely the profit on the trade.

Across the global financial system, where trillions of dollars in currencies, securities, and other assets change hands daily, settlement risk is a pervasive and serious concern, and managing it requires extensive infrastructure, collateral, monitoring, and trust. Atomic settlement is so significant precisely because it does not merely reduce this risk through better management; it eliminates it structurally, by ensuring the two legs settle together so that neither party is ever exposed to the other’s potential failure. The problem that closed Herstatt and has haunted finance ever since simply cannot occur when settlement is atomic.

Payment-versus-Payment and Delivery-versus-Payment

The principle of atomic settlement shows up in finance under two main labels, depending on what is being exchanged, and knowing the difference clarifies the concept. When the exchange is one currency for another, as in a foreign-exchange trade, the atomic version is called payment-versus-payment, often abbreviated PvP.

Under PvP, the payment in one currency and the payment in the other currency are linked so that both happen simultaneously or neither does, ensuring that no party can pay in one currency without receiving the other. This is the direct answer to Herstatt risk: under true PvP, the situation that destroyed Herstatt’s counterparties, paying marks and not receiving dollars, becomes impossible, because the two payments are bound together.

When the exchange is an asset for a payment, as when securities are bought or sold, the atomic version is called delivery-versus-payment, abbreviated DvP. Under DvP, the delivery of the security and the payment for it are linked so that the asset changes hands at the same instant as the money, ensuring that no party delivers a security without receiving payment, and no party pays without receiving the security.

Both PvP and DvP are expressions of the same atomic principle applied to different kinds of trades, and both aim to eliminate the settlement risk that lives in the gap between the legs. The traditional financial system has built elaborate infrastructure to approximate these protections, such as specialized settlement institutions that hold both legs and release them together, but these systems are complex, do not cover every currency or market, and still leave gaps. Atomic settlement on a blockchain offers a way to achieve PvP and DvP more directly and more universally, which is a large part of why the technology has drawn such intense institutional interest.

A worked example: an FX trade with and without atomicity

To make settlement risk and its atomic solution concrete, walk through a single foreign-exchange trade both ways. Suppose a bank in Europe agrees to sell ten million euros to a bank in Asia in exchange for the equivalent in dollars. Under the traditional, non-atomic process, the two payments may not happen at the same moment, because the banks operate in different time zones and through different payment systems.

The European bank might send its euros during its business day, expecting the dollars to arrive later when the other party’s systems process the payment. In the interval between sending the euros and receiving the dollars, the European bank is exposed: if the Asian bank fails, defaults, or is shut down in that window, the European bank has paid ten million euros and may receive nothing, losing the entire principal. This is exactly the Herstatt scenario, and it is a real risk that institutions must monitor and manage on every such trade.

Now run the same trade with atomic settlement. The euro payment and the dollar payment are bound together into a single, indivisible transaction, structured so that both transfers execute at the same instant or neither executes at all. If for any reason the dollar leg cannot complete, the euro leg does not complete either, and both banks remain exactly where they started, with no exposure and no loss.

The European bank can never find itself having sent euros without receiving dollars, because the protocol makes that outcome structurally impossible. The risk window that existed in the traditional version is gone, not managed or reduced but eliminated, because the two legs are no longer separated in time. That is the difference atomicity makes: it converts a trade with an unavoidable risk window into a trade with no risk window at all, which is why the financial industry regards atomic settlement as a genuine advance rather than an incremental improvement.

Why blockchains make atomic settlement natural

Atomic settlement is not new as a concept, but blockchains make it dramatically easier to achieve, and understanding why reveals the deep fit between the technology and the problem. A blockchain transaction is, by its nature, atomic at the level of the ledger: it either executes completely and is recorded, or it fails and changes nothing. Smart contracts, the programmable agreements that run on many blockchains, extend this property to complex, multi-step transactions.

A smart contract can be written so that it performs two transfers, say, moving one asset from party A to party B and another asset from party B to party A, as a single operation that either completes both transfers together or reverts entirely, leaving both parties untouched. This is atomic settlement expressed directly in code, with the all-or-nothing guarantee enforced by the blockchain itself rather than by an external institution.

This is a profound fit, because the property that finance has always struggled to guarantee, that two legs of a trade settle together or not at all, is something a blockchain provides almost for free, as a basic feature of how it works. The earliest crypto version of this idea was the atomic swap, a way for two parties to exchange different cryptocurrencies such that the swap either completes for both or fails for both, with no possibility of one party absconding with the other’s coins.

The same principle now underpins the tokenization of traditional assets: if currencies and securities are represented as tokens on a blockchain, then trades between them can be settled atomically by smart contracts, achieving true PvP and DvP without the elaborate intermediary infrastructure the traditional system requires. The blockchain becomes the neutral venue where both legs settle simultaneously and trustlessly. This is why atomic settlement is so central to the institutional interest in tokenization: the technology delivers, as a native capability, the settlement guarantee that traditional finance has spent decades and fortunes trying to approximate.

From multi-day to instant settlement

Closely tied to atomic settlement is the compression of settlement time, and the two together explain much of the institutional excitement. In traditional markets, settlement often does not happen immediately after a trade is agreed; instead, it occurs after a delay, commonly a couple of business days for many securities, a convention referred to by labels like T plus two, meaning trade date plus two days.

This delay exists for historical and operational reasons, because the traditional system needs time to coordinate the many parties, records, and transfers involved in settling a trade. But the delay is costly: during the gap between trade and settlement, capital is tied up, positions carry risk, and the settlement exposure discussed above persists for longer. Shortening the cycle has been a long-running goal of market reform, with markets gradually moving from longer cycles to shorter ones over the years.

Atomic settlement on a blockchain points toward the logical endpoint of this trend: instant settlement, sometimes called T plus zero, where the trade settles the moment it is executed. Because a smart contract can bind and complete both legs simultaneously, there is no operational reason for a multi-day delay; the settlement can happen at the instant of the trade.

This collapses the settlement window from days to seconds, which has large benefits. Capital is freed immediately rather than tied up for days, settlement risk persists for moments instead of days, and the entire system becomes more efficient and less exposed. The combination of atomicity, which removes the risk in the gap between legs, and instant settlement, which removes the gap in time, is what makes blockchain-based settlement so attractive to institutions.

Together, they promise a financial system where trades settle instantly and with no settlement risk, a meaningful improvement over a status quo built around multi-day cycles and the risks they carry.

The real-world push: bank projects and tokenization

This is not merely theoretical, because banks and market infrastructures are actively testing atomic settlement, which signals that the technology is moving from concept toward production. A notable recent example is a bank-backed initiative bringing together a large group of international banks to study faster cross-border foreign-exchange settlement using atomic, payment-versus-payment swaps of compliant stablecoins, aiming to replace the multi-day settlement that currency trades often still require with simultaneous, same-instant settlement.

The design deliberately works with existing bank standards and messaging infrastructure instead of asking banks to abandon their systems, layering atomic settlement onto the rails they already use. The scale of such efforts, involving banks representing trillions of dollars in assets, shows that the institutional world takes atomic settlement seriously as a practical goal, not just a research curiosity.

The broader context is the tokenization of real-world assets, which is the larger movement that atomic settlement enables. As currencies, government bonds, equities, and funds are increasingly represented as tokens on blockchains, the trades between them can be settled atomically, achieving the simultaneous, risk-free settlement that has long been the ideal.

Major financial institutions and market infrastructures have been running pilots and building platforms for tokenized assets precisely because the settlement properties are so attractive, and the tokenized-asset sector has grown substantially as a result. The convergence of tokenized assets and atomic settlement is, in many ways, the heart of the institutional crypto thesis: not speculative tokens, but the use of blockchain technology to settle real financial transactions instantly and without settlement risk.

The bank projects testing it today are the early, concrete steps toward that future, and their progress is a useful signal of how quickly atomic settlement is moving from promise to practice.

Risks and open questions

For all its promise, atomic settlement carries real hurdles and risks that an informed reader should weigh instead of accepting the idealized vision. The first is a liquidity requirement: atomic settlement demands that both legs of a trade be available to settle at the same instant, which means the necessary assets or funds must actually be present on the settlement venue simultaneously. In a world where value is fragmented across many blockchains and traditional systems, ensuring that both legs are present and ready at the same moment is a genuine operational challenge, and a trade cannot settle atomically if one side’s liquidity is not there when needed.

Other open questions are significant. Legal finality is one: for atomic settlement to be trusted by institutions, the law must recognize a blockchain settlement as final and irreversible in the same way it recognizes traditional settlement, and the legal frameworks for this are still developing in many jurisdictions.

Fragmentation is another, because if assets are tokenized across many incompatible blockchains, achieving atomic settlement between them requires interoperability that does not always exist, and bridging between chains can reintroduce the very risks atomic settlement was meant to remove.

There are also operational demands, since instant, around-the-clock settlement requires institutions to manage liquidity continuously instead of within business-day cycles, a real change to how treasury operations work. And the technology itself must be secure, because a flaw in a settlement smart contract could undermine the guarantees the whole system relies on.

None of these hurdles is necessarily fatal, and the active bank projects suggest they are being worked through, but they are real, and atomic settlement should be understood as a powerful approach still maturing instead of a finished solution. As with any emerging financial technology, the gap between a successful pilot and universal adoption can be wide, and the risks in that gap are worth respecting.

Frequently Asked Questions

What is atomic settlement in simple terms?

Atomic settlement is a way of completing a transaction so that both sides happen at the same instant or neither happens at all. The word “atomic” means indivisible: the transaction cannot be left half-done, with one party having paid and the other not. If anything would stop both legs from completing together, the whole transaction reverts and both parties end up where they started. This removes the risk that one party performs while the other fails, which is the core danger in any trade where the two sides do not settle simultaneously.

What is settlement risk?

Settlement risk is the danger that arises in the gap between agreeing to a trade and actually settling it, during which one party can pay or deliver while the other defaults, leaving the first party exposed. It is sometimes called principal risk, because the exposed party can lose the entire amount it advanced. The classic example is Herstatt risk, named after a German bank shut down in 1974 after its counterparties had paid it in marks but before it paid them dollars, leaving them with nothing. Atomic settlement eliminates this risk by binding the two legs together.

What is the difference between PvP and DvP?

Both are forms of atomic settlement applied to different trades.

Payment-versus-payment, or PvP, applies to currency exchanges, linking the payment in one currency to the payment in the other so both happen together or neither does, which directly prevents Herstatt-style losses.

Delivery-versus-payment, or DvP, applies to securities, linking the delivery of the asset to the payment for it so the security and the money change hands at the same instant. Both express the same atomic principle, ensuring no party gives value without simultaneously receiving what they were promised.

Why are blockchains good at atomic settlement?

Because a blockchain transaction is naturally atomic: it either executes completely or fails and changes nothing. Smart contracts extend this to complex trades, allowing two transfers to be bound into a single operation that either completes both together or reverts entirely. This gives, as a native feature, the all-or-nothing settlement guarantee that traditional finance has spent decades trying to approximate with elaborate intermediary infrastructure. When currencies and securities are tokenized on a blockchain, trades between them can settle atomically through smart contracts, achieving true PvP and DvP directly.

What is the difference between T+2 and T+0 settlement?

T plus two means a trade settles two business days after it is agreed, a common convention in traditional markets that exists because the legacy system needs time to coordinate the many parties and records involved. During that delay, capital is tied up and settlement risk persists. T plus zero, or instant settlement, means the trade settles the moment it is executed, which atomic settlement on a blockchain makes possible because a smart contract can complete both legs simultaneously. Moving from T plus two to T plus zero frees capital immediately and shrinks the risk window from days to seconds.

Is atomic settlement actually being used?

It is being actively tested and piloted instead of universally deployed. Bank-backed initiatives have brought together large groups of international banks to study faster cross-border foreign-exchange settlement using atomic, payment-versus-payment swaps, working with existing bank standards instead of replacing them. The broader tokenization of real-world assets, which has grown substantially, relies on atomic settlement as a core benefit, and major institutions have run pilots and built platforms around it. So atomic settlement is moving from concept toward practice, though real hurdles around liquidity, legal finality, interoperability, and operations remain to be worked through.

This article is educational information, not financial or investment advice. The technology and the projects described are still developing, and details reflect reporting available as of June 26, 2026, which can change quickly. Verify current information from primary sources before relying on anything described here.

Bitcoin (BTC) dropped below $60,000, a key psychological support, on Thursday as losses in megacap technology stocks weighed on investors’ broader risk appetite, adding pressure to an already fragile crypto market.

BTC/USD vs. Nasdaq and S&P 500 daily performance chart. Source: TradingView

The decline has triggered a classic bearish reversal setup that may push the BTC price under the $54,000 mark in the coming days.

Key takeaways:

- Bitcoin’s break below $60,000 has erased its June gains and activated multiple bearish setups.

- Bitcoin’s rounded top and daily bear flag breakdowns are both projecting a downside target below $54,000.

BTC’s rounded top breakdown signals more pain ahead

The BTC/USD pair fell as much as 4.8% on Thursday, hitting an intraday low near $58,000 and erasing its entire June advance. The pullback also completed what appears to be a rounded top pattern on the four-hour chart.

BTC/USD four-hour chart tracking the rounded top bearish setup. Source: TradingView

In technical analysis, a rounded top forms when buying momentum gradually exhausts, shifting the asset from an uptrend to a downtrend in an inverse-U-shaped structure. The pattern officially resolves when the price breaks below the “neckline” or the structure’s base support.

By measuring the distance from the top of the dome to the neckline and projecting that same distance downward from the breakdown point, analysts calculate a clear target.

For Bitcoin, this measured downside target sits just under the $54,000 level, representing an approximate 8.9% drop from current prices.

On the daily chart, Bitcoin has simultaneously triggered a bear flag breakdown.

BTC/USD daily chart tracking the bear flag breakdown setup. Source: TradingView

This secondary pattern independently projects an identical move toward the $54,000 zone, adding substantial weight to the bearish case.

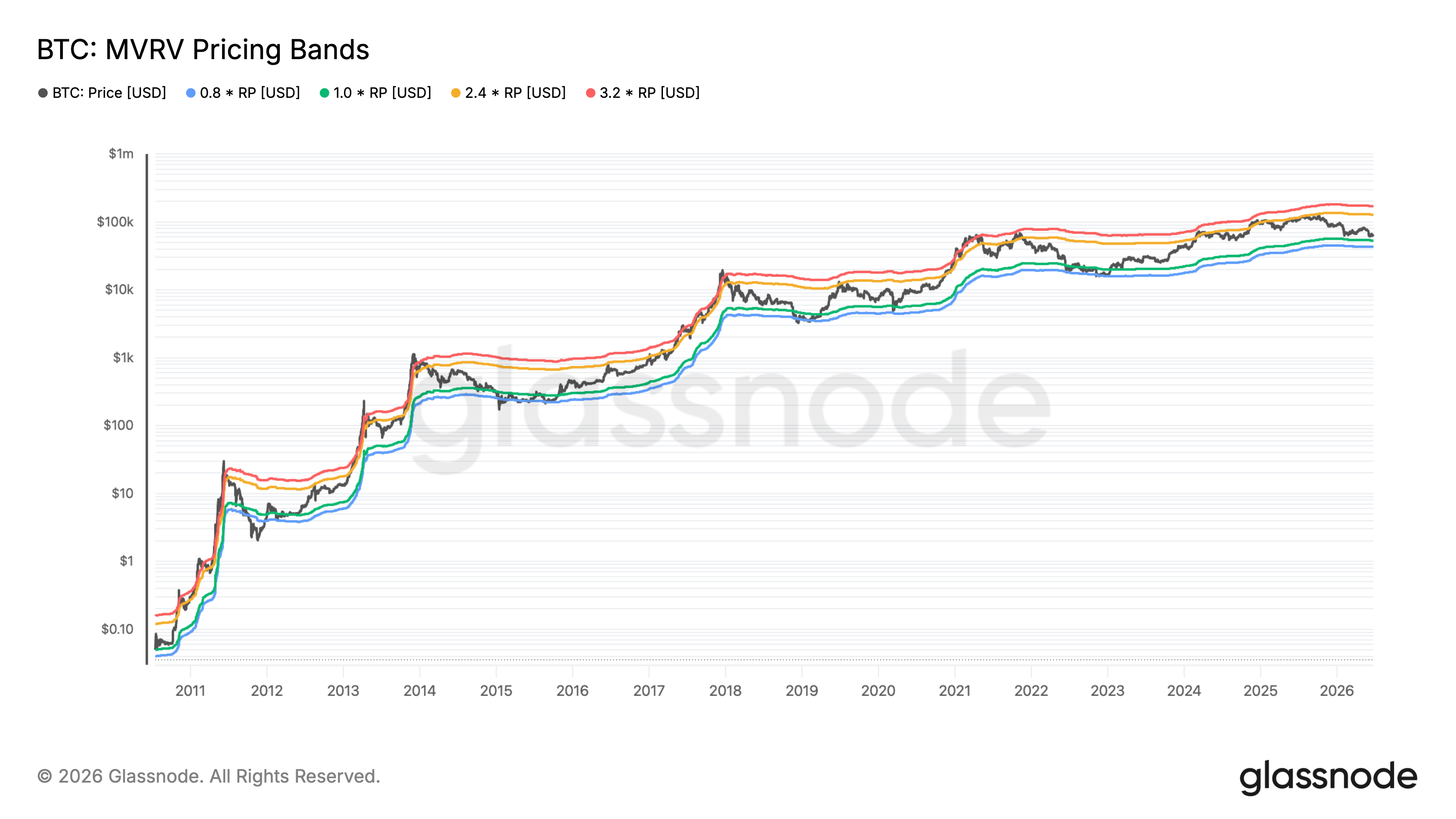

Bitcoin MVRV bands increase $54,000 target odds

Bitcoin’s on-chain price bands also point to the same downside area highlighted by the rounded-top and bear-flag setups.

Glassnode’s MVRV pricing bands compare Bitcoin’s market price with its realized price, or the average price at which coins last moved on-chain. In simple terms, they show whether the market is trading at unusually high profit or loss levels.

BTC MVRV pricing bands vs. price. Source: Glassnode

As of Wednesday, Bitcoin was trading near $60,997, while the 1.0 MVRV band, shown in green, sat around $53,390. That level closely matches the technical downside target near $54,000, making it an important support zone if BTC extends its decline.

Related: Bitcoin nearly loses $59K as DXY surges: Are traders bracing for more pain?

A deeper selloff, however, could push Bitcoin toward the 0.8 MVRV band, shown in blue, near $42,700. Historically, Bitcoin’s major bear-market bottoms have formed around this lower blue band, where unrealized losses become extreme, and capitulation risk rises.

XRP is trading near the $1.00 level, down about 9% in the last seven days and more than 52% over the past year.

But UK-based technical analyst ChartNerd is suggesting that the deeper the Ripple token falls from here, the better the potential risk-reward setup becomes, with a possible demand zone between $0.90 and $0.70 if $1.00 gives way.

What the Charts Are Saying

ChartNerd has been tracking this setup since at least June 12, when he published a thread laying out the macro picture. According to him, XRP spent most of 2023 and into late 2024, capped below $0.80/$0.70 resistance that acted as a ceiling up until there was a breakout in Q4 2024.

That breakout, he says, was what eventually pushed XRP to its all-time high of $3.65 in July 2025, and since then, the trend has gone the other way, with key moving averages lost and a weekly 20/50 EMA death cross confirming the structural change, and the asset dropping from its January 2026 peak of $2.40 all the way to where it is now.

Recall that in February, XRP hit a low of $1.12, after which it attempted a recovery, with a bunch of sideways trading eventually taking it near $1.55, where it was rejected. Per ChartNerd’s analysis, that rejection kick-started the current leg down to lows near $1.00 in June, putting it in what the market watcher called his “area of interest,” a zone where he has been keeping an eye out for a potential cycle bottom between now and Q4 2026.

In his view, the reason that zone matters is that the old resistance level from 2023 and 2024 could switch to support. And if XRP holds anywhere in the $0.90 to $0.70 range during any deeper market drop, the previous ceiling will become the floor.

“This is a high-interest support region, but confirmation still matters most, and we do not have it yet,” he wrote at the time.

But now, the analyst believes XRP’s decline is pushing it further into the area of interest, and the more it falls, “the stronger the risk-reward setup becomes.” He said that he’s also watching the 10-year Gaussian Channel, which, according to him, XRP is now entering, and which has not failed as a guardrail for as long as he has tracked it.

On the timing question, ChartNerd stated in a different post that there is a “very strong likelihood” that a market bounce could happen in the coming weeks as June ends, something that is consistent with what Bitcoin tends to do in midterm years. However, he added a caveat: it will probably be a relief rally that leads to a final drop in the last quarter of the year.

The On-Chain Picture

Elsewhere, analyst Ali Martinez said that XRP is testing a major volume block at $1.06, where on-chain data shows more than 830 million tokens changed hands. Below it, the next important clusters on the UTXO Realized Price Distribution are at $0.80, $0.62, and $0.51.

At the same time, another market watcher, CasiTrades, observed that XRP was at its “most critical moment” in the current cycle, with buy orders placed at $0.93 and a deeper Fibonacci level at $0.87, framing the current fear as part of how bottoms actually form, not as a reason to sell.

The post XRP’s Slide to Sub-$1.00 Could Set Up ‘Risk-Reward’ Zone: Analyst appeared first on CryptoPotato.

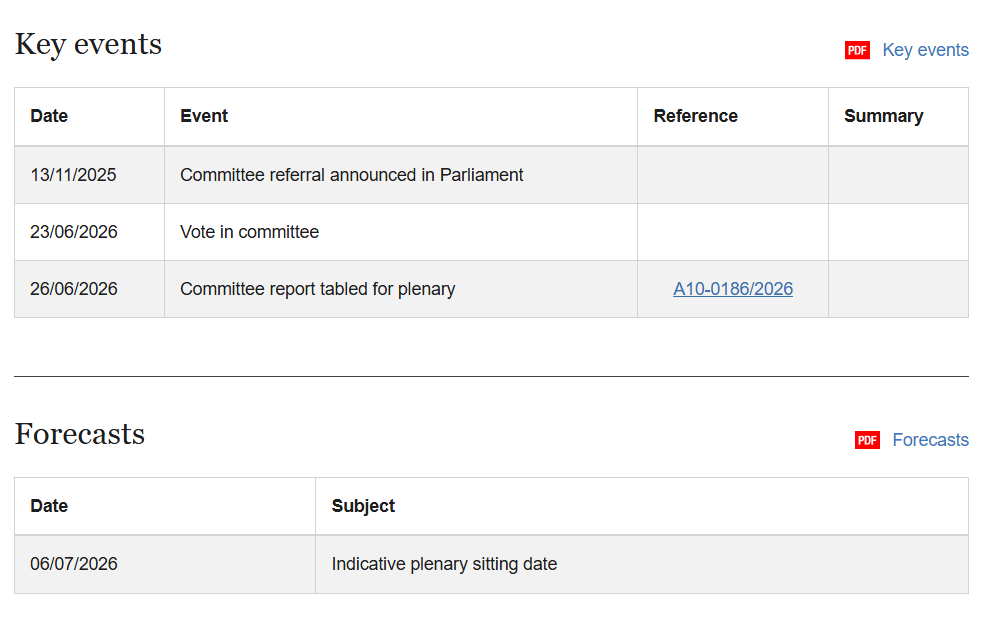

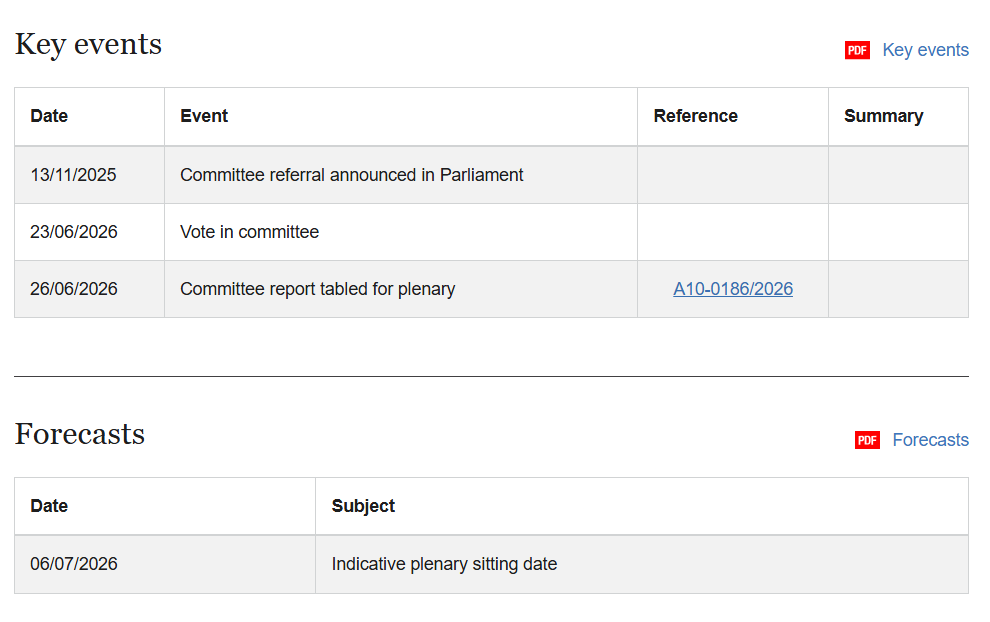

The European Parliament’s Committee on Economic and Monetary Affairs (ECON) has asked the European Commission to examine whether additional parts of the crypto sector—such as crypto lending and borrowing, staking, non-fungible tokens (NFTs), and decentralized finance (DeFi)—should be brought within the EU’s regulatory perimeter. The request is set out in an own-initiative resolution tabled for the Parliament’s plenary vote, where it is expected to be considered on July 7.

While the measure would not amend the EU’s Markets in Crypto-Assets Regulation (MiCA) or create new legal obligations, it signals how lawmakers may shape subsequent Commission proposals and supervisory priorities. For crypto-asset service providers, banks, and institutional investors, the resolution matters less for immediate enforceable change and more for how it could influence the direction of EU crypto policy—particularly around stablecoins and “tokenization” of traditional financial services.

Key takeaways

- ECON urges the European Commission to assess whether crypto lending/borrowing, staking, NFTs, and DeFi merit additional regulation beyond MiCA.

- The draft resolution supports the development of euro-denominated stablecoins within MiCA and frames them as potentially complementary to tokenized bank deposits and wholesale central bank digital currency models.

- ECON calls for consistent, EU-wide application of MiCA to avoid divergent national rules that could fragment the single market.

- If adopted, the resolution would become the Parliament’s official policy position, but it would not modify MiCA or impose new obligations.

ECON’s resolution: expanding the policy lens beyond MiCA

The recommendations were drafted by Belgian Member of the European Parliament Johan Van Overtveldt and advanced through ECON’s internal negotiations before being tabled for a plenary vote. According to the European Parliament’s procedure documents, the resolution is an own-initiative instrument designed to set out guidance for the Commission regarding the future shape of EU digital asset regulation.

ECON’s central request is forward-looking: the committee asks the Commission to evaluate regulatory coverage for activities that are not uniformly addressed by MiCA’s current scope. The resolution explicitly references crypto lending and borrowing, staking, NFTs, and DeFi—areas that, in practice, span multiple business models and may involve varying degrees of custody, asset pooling, market-making, governance structures, and cross-border service provision.

For compliance teams and regulated intermediaries, the key issue is not simply “whether” these activities should be regulated, but “how” and “under which regime.” MiCA already establishes licensing and authorization requirements for certain crypto-asset service providers, while other frameworks—such as rules on anti-money laundering (AML), consumer protection, and market conduct—may apply depending on structure and distribution. ECON’s call indicates lawmakers want clearer boundaries and regulatory coherence as these products evolve.

Stablecoins and tokenized finance: a more constructive regulatory stance

A major element of the ECON resolution relates to stablecoins, particularly those denominated in euros. The text frames euro stablecoins as potentially supportive of the EU’s payments ecosystem and encourages their development within MiCA’s framework.

That approach reflects a broader policy shift among some European institutions, including a recognition that stablecoins can operate alongside—rather than necessarily replace—existing money and payment rails. ECON links euro-denominated stablecoins to potential integration with tokenized commercial bank deposits and wholesale central bank digital currencies, suggesting that future EU financial infrastructure could incorporate multiple “digital money” channels.

The policy context is particularly sensitive given how stablecoin arrangements interact with banking liquidity and reserve management. In earlier discussions around the banking turbulence in the United States, concerns were tied to reserve custody and banking counterparties. For example, during the collapse of Silicon Valley Bank, USDC issuer Circle reportedly held a material portion of reserves at the bank, and USDC briefly lost its dollar peg. Although those events occurred outside the EU, they continue to influence how European policymakers evaluate reserve quality, redemption arrangements, and systemic risk controls for stablecoins.

ECON’s resolution also aligns with the committee’s parallel work on the euro’s digital future. It references legislative momentum supporting a “coexistence” model for a potential digital euro alongside private digital money solutions—an approach that suggests policymakers may view stablecoins and public digital currency designs as complementary components of a broader digital payments architecture.

MiCA implementation pressure and the question of national divergence

The resolution goes beyond new regulatory topics by focusing on execution and market structure. It urges consistent application of MiCA across member states to preserve a level playing field for crypto firms. This is a crucial compliance concern: when national regulators introduce additional or differing requirements, firms face increased operating cost, legal uncertainty, and fragmentation of distribution strategies within the EU.

ECON’s earlier draft, presented by Van Overtveldt in February, reportedly focused more tightly on MiCA’s existing framework—such as stablecoin classifications and legal certainty for multi-issued stablecoins. Over months of negotiation, the committee incorporated a broader set of policy questions, culminating in the current recommendation set that also calls for reconsideration of regulatory coverage for activities such as DeFi and staking.

At the EU level, the Commission is already working to reassess parts of MiCA’s scope. In May, the European Commission launched a public consultation seeking input on whether the framework should be expanded to cover areas that include DeFi, staking, lending, NFTs, and tokenized financial assets, while also revisiting debates around MiCA’s ban on interest-bearing stablecoins. Although consultations are not binding legislation, they typically shape the Commission’s next steps and can provide a timeline for future legislative proposals.

Implementation is also time-bound. MiCA’s transitional period is set to end on July 1, after which crypto-asset service providers generally need authorization under MiCA to continue operating across the EU. That deadline increases the practical stakes for firms regarding licensing strategy, supervision expectations, and product mapping—especially for services that may fall near the edges between crypto-asset activity and activities that regulators may treat differently under existing financial law.

Institutional implications: compliance, consumer protection, and legal clarity

For banks, payment firms, and institutional investors assessing crypto exposure, the resolution underscores that EU oversight is moving toward a more comprehensive assessment of how crypto activities affect market integrity and risk allocation. Even without immediate amendments to MiCA, the Parliament’s policy position can influence supervisory guidance, regulatory interpretation, and the Commission’s legislative drafting priorities.

Key open questions remain. ECON’s call does not specify a single mechanism for extending regulation, and the outcome of the plenary vote would only establish a non-binding political mandate for the Commission. In practice, the future direction could depend on how the Commission and co-legislators determine which activities are best addressed by MiCA extensions versus other EU regimes (for example, rules tied to financial services licensing, AML/KYC, consumer protection, or market abuse).

Cross-border coordination is also likely to remain a central theme. DeFi and tokenized asset activities often rely on service providers, intermediaries, or infrastructure operating across jurisdictions. As the EU considers regulatory scope expansion, compliance teams will need to monitor how authorization requirements, supervisory expectations, and governance standards may be applied to novel business models—particularly those with decentralized features that complicate “who is responsible” under traditional regulatory frameworks.

Closing perspective

As the July 7 plenary vote approaches, the resolution’s adoption would provide the European Parliament with an explicit mandate on crypto regulatory coverage, reinforcing pressure on the Commission’s ongoing MiCA review process. The central item for observers is how the Commission translates this political direction into concrete legislative options—if any—particularly for stablecoins, DeFi-adjacent services, and staking-related business models.

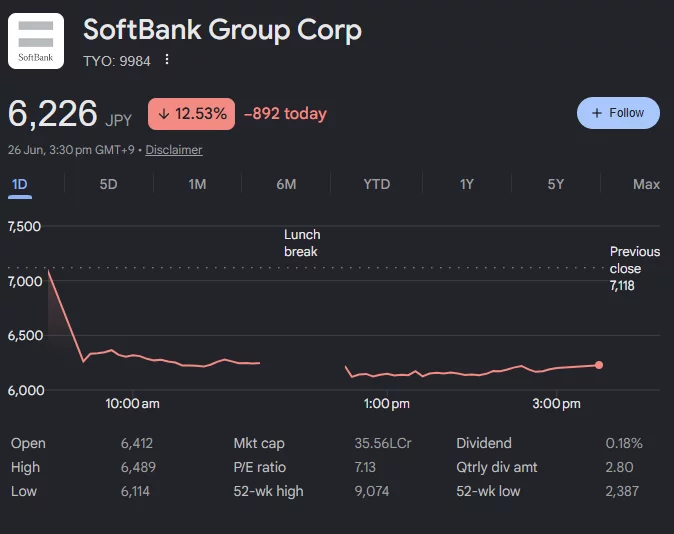

SoftBank Group shares have plunged more than 12% after reports suggested OpenAI is considering delaying its planned initial public offering until 2027 to preserve a potential valuation of up to $1 trillion.

Summary

- SoftBank shares fell 12.5% after reports suggested OpenAI may delay its IPO until 2027.

- OpenAI is reportedly weighing a lower-valued IPO this year against pursuing a $1 trillion valuation later.

- SoftBank’s $64.6 billion OpenAI commitment has made its stock increasingly sensitive to the startup’s listing plans.

According to reports, SoftBank shares dropped as much as 13% during trading in Tokyo on Friday before closing 12.53% lower, making the investment conglomerate one of the biggest contributors to the Nikkei 225’s roughly 4% decline.

The selloff followed reports that OpenAI executives are weighing whether to proceed with a lower-valued IPO this year or postpone the listing until 2027 while continuing to pursue a valuation approaching $1 trillion.

Reports indicated that OpenAI chief executive Sam Altman opposed reducing the company’s valuation simply to accelerate a stock market debut. Although the company confidentially filed a draft registration statement with the U.S. Securities and Exchange Commission earlier this month, OpenAI said at the time that no final decision had been made on the timing of an IPO and that it could remain privately held for longer.

OpenAI’s expanding business has increased investor focus

Pressure on SoftBank has intensified because of its growing financial commitment to OpenAI. The Japanese investment group agreed in February to invest another $30 billion into the artificial intelligence company. Once completed, the transaction will raise SoftBank’s total commitment to about $64.6 billion and give it an ownership stake of roughly 13%.

Because of that exposure, investors have increasingly treated SoftBank as one of the largest public proxies for OpenAI’s future value. A later public listing would not reduce SoftBank’s ownership, but it would postpone the first market-based valuation of its investment and delay any opportunity to monetize part of the stake.

The latest market reaction follows months of rapid expansion by OpenAI. Earlier this week, the company introduced its first custom-built artificial intelligence chip, Jalapeño, developed with Broadcom to support inference workloads powering ChatGPT, Codex, and future AI agents.

According to OpenAI, developing proprietary silicon forms part of its strategy to control more of the infrastructure behind its AI services while reducing dependence on third-party hardware providers.

OpenAI also unveiled its GPT-5.6 model family on Friday under the names Sol, Terra, and Luna. Although the names quickly drew attention across crypto communities because of their similarity to well-known blockchain projects, OpenAI said they represent capability tiers within the model lineup rather than any connection to digital assets.

Recent OpenAI developments have kept the company in focus

OpenAI has remained at the center of attention outside its product launches as well. Last week, reports said Amazon withdrew from distributing Artificial, a film centered on Sam Altman, while discussions continued with filmmakers about finding another distribution partner. According to the report, Amazon’s decision came as the company expanded its commercial relationship with OpenAI through a multi-billion-dollar investment commitment linked to future milestones, although Amazon has not publicly connected the two developments.

Meanwhile, SoftBank founder Masayoshi Son defended the company’s aggressive investment strategy only two days before Friday’s selloff. Rejecting concerns that heavy spending on artificial intelligence resembles a speculative bubble, Son maintained his confidence in long-term AI investment despite growing market volatility surrounding OpenAI’s expected path to the public markets.

With just a few days left in June, it’s safe to say that bitcoin would require nothing short of a miracle to end the month in the green, as current data show a substantial 18% decline.

On-chain data depicts a few key factors behind BTC’s latest nosedive and what has to change for a stronger July.

Demand Lacks

In a recent post on X, popular analyst Ali Martinez explained that bitcoin accumulation levels have stalled for the past seven months.

“Bitcoin apparent demand has remained negative for 208 consecutive days, recently dropping to a new low of -273,000 BTC.”

The evident decline in this metric indicates that real spot market demand has fallen, as it compares new BTC creation to the movement of existing inventory. The trend change came after the massive liquidation event in early October, when over $19 billion was wiped out in a single day.

From November 9, 2025, to May 31, 2026, this demand “hovered quietly in negative territory between 0 and -150,000 BTC, indicating a mild but steady distribution of supply,” Martinez added. However, the metric plummeted to -273,000 BTC following the early and late June crashes and has “flatlined around this level.”

The metric remaining in negative territory for so long means a significant amount of old supply is entering circulation faster than the spot market can absorb it. This substantial divergence suggests that selling pressure continues to outpace new capital inflows, which is the first crucial factor that has to change for BTC to have a more robust and favorable July.

Just a few days ago, Martinez pointed to another metric showing no real demand for BTC but primarily from US investors. The Coinbase Premium remains deep in the red for nearly two months. More specifically, it went into negative territory after BTC peaked at over $82,000 in mid-May and has remained there ever since.

US institutional demand is key to bitcoin’s price moves and ranks as the second factor that has to change in July.

ETF Outflows

Aligned with the aforementioned developments, the spot Bitcoin ETFs have been on a massive withdrawal streak for weeks. The past week was no exception, as red dominated all days. On Thursday, the day BTC plummeted to $58,000 for the first time in almost two years, investors pulled out nearly $700 million from the funds.

Bitget Wallet’s Research Analyst Lacie Zhang told CryptoPotato that ETF outflows have to stabilize, and volatility will normalize after the massive options expiry event of $11 billion that took place on June 26.

“If redemptions resume and post-expiry positioning remains defensive, the market may stay choppy around current levels. The key point is that Bitcoin’s July direction may be shaped less by last week’s PCE print and more by how flows, leverage, and on-chain accumulation behave in the 72 hours after expiry settles,” she concluded.

The post Bitcoin’s July Outlook Depends on These Key Factors appeared first on CryptoPotato.

Brad Garlinghouse, CEO of Ripple, labeled Michael Saylor’s leveraged Bitcoin model a “damning indictment”, pointing to MicroStrategy’s preferred stock, which is trading well below its $100 par value.

Garlinghouse reiterated his long-term bullishness on Bitcoin (BTC), but drew a clear line between his view on the asset and the financing structure Saylor has built around it.

Saylor’s Preferred Stock Under Pressure

Strategy’s STRC perpetual preferred stock traded around $74 at the time of Garlinghouse’s remarks. That placed it roughly 26% below its $100 par value. The discount has widened throughout 2026 as the market weighed Strategy’s growing financial obligations.

Annualized dividend payments tied to STRC have climbed to approximately $1.2 billion. More strikingly, Strategy’s dividend coverage window has narrowed from more than seven years to roughly 14 months.

Questions about whether STRC can remain viable under sustained pressure have intensified among investors.

Strategy also sold 32 Bitcoin in late May to fund STRC dividend payments. This marked the first time the company liquidated any BTC to service its financial obligations. The move drew scrutiny from analysts monitoring its capital structure.

Garlinghouse Argues Utility Drives Value

Garlinghouse’s critique targets the gap between financial engineering and long-term asset value. In his view, Saylor’s borrow-to-buy approach generates market pressure without creating the utility that sustains it.

“Financial engineering does not drive long-term value… long-term value of any digital asset is going to be driven by utility.”

Garlinghouse has consistently backed that argument with Ripple’s own positioning. He has cited XRP cross-border payment infrastructure as a contrast to leverage-driven accumulation strategies.

Ripple also released its 2025 impact report this week, showing more than $70 million donated during the year.

The company deployed RLUSD and XRP Ledger technology across small business lending, humanitarian aid delivery, and water access programs in multiple markets, with over $53 million in capital reaching underserved small business owners through its Accion Opportunity Fund partnership alone.

Ripple CEO Bullish on Bitcoin

Garlinghouse also noted that his bullish stance on BTC remains unchanged. He distinguished between the asset’s long-term potential and the risks introduced when companies borrow heavily to accumulate it.

The critique lands amid Bitcoin institutional treasury adoption becoming a dominant corporate trend in 2026. Strategy holds more than 843,000 BTC, roughly 76% of all Bitcoin on public company balance sheets.

Several other firms have followed a similar treasury model, though none approach Strategy’s scale or financial complexity.

Beyond STRC, Strategy also faces a securities investigation opened earlier in 2026, adding regulatory strain to its financial picture.

The post Ripple CEO Criticizes Saylor’s Bitcoin Strategy While Remaining Bullish on BTC appeared first on BeInCrypto.

The European Parliament’s Committee on Economic and Monetary Affairs (ECON) has formally pushed the European Commission to consider whether several fast-growing areas of the crypto market should fall under EU-wide rules. In an own-initiative resolution scheduled for a plenary vote, lawmakers ask the Commission to assess the regulatory perimeter for crypto lending and borrowing, staking, non-fungible tokens (NFTs) and decentralized finance (DeFi), while also encouraging broader tokenization across financial services.

The proposal, drafted by Belgian MEP Johan Van Overtveldt, will be submitted to the full Parliament for voting expected on July 7. If adopted, it would become the Parliament’s policy position—but it would not itself amend the existing Markets in Crypto-Assets Regulation (MiCA) or create new binding legal obligations.

Key takeaways

- ECON is urging the European Commission to evaluate whether lending/borrowing, staking, NFTs and DeFi should be regulated beyond MiCA’s current coverage.

- The draft strongly supports the development of euro-denominated stablecoins under MiCA to support payments and tokenized financial infrastructure.

- ECON wants consistent application of MiCA across EU member states, warning against national rule-making that could fragment the market.

- The resolution is set for a plenary vote around July 7 and would reflect Parliament’s stance without directly changing MiCA.

From MiCA scope to a wider policy checklist

MiCA already provides an EU framework for certain categories of crypto assets and sets licensing expectations for crypto-asset service providers. But ECON’s report signals that lawmakers are now looking past MiCA’s current boundaries. The resolution asks the Commission to assess regulatory needs for additional activity types, including staking and crypto lending and borrowing, as well as NFTs and DeFi.

The timing matters for investors and operators because the Commission is already in review mode. According to the report’s context, the European Commission launched a public consultation in May on whether MiCA should be expanded to cover DeFi, staking, lending, NFTs and tokenized financial assets, and whether the current ban on interest-bearing stablecoins should be revisited. ECON’s resolution effectively adds political weight to those questions, by asking the Commission to consider a broader regulatory scope rather than treating MiCA as a closed endpoint.

In addition, lawmakers stress the importance of a level playing field for firms operating across the EU. The draft encourages consistent MiCA implementation throughout member states, and warns against additional national requirements that could fragment regulation and force crypto businesses to navigate a patchwork of rules.

Stablecoins shift from suspicion to policy support

While the resolution opens the door to evaluating regulation for more crypto activity types, it also reflects an increasingly supportive stance toward euro-denominated stablecoins. ECON backs the development of regulated stablecoins under MiCA and ties that support to the bloc’s payments strategy and broader tokenization plans across financial services.

The report’s stablecoin emphasis also follows a notable change in tone from some senior crypto critics in recent weeks. The policy direction comes shortly after former Bank for International Settlements general manager Agustín Carstens softened his stance on stablecoins and highlighted a potential coexistence with fiat systems, according to earlier coverage referenced in the source material.

ECON’s stablecoin perspective is consistent with the idea that euro-backed tokens could complement existing financial rails. The resolution argues that euro-denominated stablecoins could complement tokenized commercial bank deposits and wholesale central bank digital currencies, while also enabling faster and cheaper cross-border payments. It further claims that wider use could strengthen EU financial markets’ competitiveness and support the euro’s international role.

Importantly for market participants, these points do not signal a standalone rule change by themselves. Instead, they serve as a political directive: policymakers appear increasingly willing to treat certain stablecoin use cases as strategically valuable—provided they operate within the EU’s regulatory framework.

Why this vote matters for the EU crypto market

The ECON report is an own-initiative resolution, meaning it is Parliament setting out recommendations for the Commission rather than directly legislating. Even so, a Parliament-backed position can influence how regulators prioritize consultations, drafting work, and the next round of policy decisions.

The filing process also underscores what is at stake. The text drafted by Van Overtveldt went through negotiations and amendments within ECON before receiving committee approval. An earlier draft, presented in February, focused more narrowly on MiCA’s existing framework, including stablecoin classifications and legal certainty for multi-issued stablecoins. Months later, the committee’s final version broadens the emphasis toward whether additional crypto sectors—particularly DeFi-like activity and token-driven financial primitives—should be pulled under a more explicit regulatory framework.

Meanwhile, MiCA’s implementation timetable is already moving. The transitional period for crypto asset service providers ends July 1, after which providers generally must hold authorization under the regulation to continue serving customers across the EU. For businesses watching for additional MiCA expansion, the July plenary vote on the resolution could be another step in shaping regulatory expectations—especially for models that don’t neatly fit within today’s MiCA categories.

A broader push for “digital money” coexistence

ECON’s approach aligns with a parallel strand of EU digital money policy. In the source context, the committee previously backed legislation for a digital euro, with lawmakers arguing that public and private forms of digital money should coexist rather than compete.

That political framing matters because it helps explain why stablecoins and tokenized deposits are treated as complementary tools instead of outright replacements. If the Parliament’s position is adopted and the Commission follows through during its MiCA review process, the next policy cycle could be defined less by whether crypto should exist, and more by how different digital money instruments should interact within an overarching EU framework.

Readers should watch the European Commission’s response to its May consultation and any follow-on legislative proposals once the July 7 plenary vote sets Parliament’s official stance. The key uncertainty is how the Commission will translate “assessment” questions—especially around DeFi, staking, lending/borrowing, and NFTs—into concrete regulatory boundaries without undermining the consistent MiCA implementation ECON says it wants across the EU.

A survey arranged by digital asset services provider CoinShares found that more than half of UK-based financial advisers reported the bulk of their clients’ crypto holdings were outside their oversight.

According to the results of a CoinShares survey released on Thursday, 52% of UK advisers in a group of 261 European wealth management professionals said that the majority of their clients’ digital assets exposure was essentially “invisible” to them. Among all the EU countries surveyed, including France, Germany, Italy and Switzerland, the number was 25%, with 61% of advisers saying that they worked in companies that explicitly restricted digital assets or provided no clear internal guidance.

“The capital has already been allocated,” said CoinShares co-founder and CEO Jean-Marie Mognetti. “The people entrusted with managing it simply cannot see it, and in most cases not because clients are unwilling to engage, but because firm policy prevents them from doing so. This is not a knowledge problem. It is not a demand problem. It is a firm-policy problem becoming a wrong-way risk.”

He added:

“[…] Visibility comes before advice. You cannot allocate, manage risk or earn trust over assets you cannot see.”

Source: CoinShares

The UK’s Financial Conduct Authority (FCA), the watchdog overseeing digital asset regulation, reported in December that about 8% of the country’s adults were invested in crypto. The group recently proposed allowing authorized investment funds to hold up to a 10% allocation of cryptocurrency exchange-traded notes.

Related: Bank of England eases stablecoin rules, introduces 40B pound issuance cap

Potential new leadership to shake up UK crypto policy?

UK Prime Minister Keir Starmer resigned as Labour leader on Monday amid pressure from many in his own party, opening the door to a recently elected member of parliament to take the reins.

In a recent by-election, former Mayor of Greater Manchester Andy Burnham won a seat as a member of parliament representing Makerfield, positioning him to be heavily favored by many in Labour to replace Starmer. While it’s unclear how Burnham may handle crypto policy on a national stage, as mayor, he supported the blockchain industry as a driver for economic development.

Magazine: AI is banking the unbanked in Africa… faster than crypto

The European Parliament’s economic affairs committee has urged the European Commission to assess whether crypto lending and borrowing, staking, non-fungible tokens (NFTs) and decentralized finance (DeFi) should be regulated.

The recommendations were part of a report tabled Friday for plenary vote. It also called for promoting tokenization across financial services, encouraging euro-denominated stablecoins and assessing whether additional crypto activities should be regulated under the European Union’s Markets in Crypto-Assets Regulation (MiCA).

Drafted by Belgian Member of the European Parliament Johan Van Overtveldt, the report is an own-initiative resolution by the Committee on Economic and Monetary Affairs (ECON) that outlines recommendations for the Commission on digital asset regulation.

It will next go before the European Parliament for a vote, expected July 7. If adopted, the resolution would become Parliament’s official position on digital assets policy but would not amend MiCA or create new legal obligations.

The legislative timeline shows the committee’s approval of the report and its referral for a plenary vote. Source: European Parliament

Related: European Parliament throws support behind digital euro

EU warms up to regulated stablecoins

The recommendations also reflect an evolving view of stablecoins among policymakers. Days after former Bank for International Settlements general manager and longtime crypto critic Agustín Carstens softened his stance on stablecoins, the report welcomed euro-denominated stablecoins under MiCA and encouraged their development to support the bloc’s payment sector.

In 2023, Van Overtveldt called for tighter restrictions on cryptocurrencies following the banking turmoil surrounding Silicon Valley Bank, Signature Bank and Silvergate Bank. The crisis was also closely tied to stablecoins, as USDC issuer Circle held roughly $3.3 billion of its reserves at Silicon Valley Bank when it collapsed, briefly causing USDC to lose its dollar peg.

Van Overtveldt likened cryptocurrencies to drugs during the 2023 banking crisis. Source:Johan Van Overtveldt

The report argued that euro-denominated stablecoins could complement tokenized commercial bank deposits and wholesale central bank digital currencies while enabling faster and cheaper cross-border payments. It also said broader adoption could strengthen the competitiveness of EU financial markets and the international role of the euro.

The stance also aligns with ECON’s broader vision for Europe’s digital money ecosystem. On Tuesday, the committee backed legislation for a digital euro, with lawmakers arguing that public and private forms of digital money should coexist rather than compete.

Related: Poland president vetoes MiCA bill again as crypto companies look to license abroad

Lawmakers look beyond MiCA’s current scope

Van Overtveldt first presented a draft of the report in February before months of negotiations and amendments by ECON members. The earlier version largely focused on MiCA’s existing framework, including stablecoin classifications and legal certainty for multi-issued stablecoins.

The committee-approved report urged consistent application of MiCA across the EU to preserve a level playing field for crypto firms. It also warned member states against introducing national requirements beyond MiCA that could fragment the bloc’s digital asset industry.

The Commission is already reviewing MiCA. In May, the Commission launched a public consultation seeking feedback on whether the framework should be expanded to cover areas including DeFi, staking, lending, NFTs and tokenized financial assets, while also reopening debate over the regulation’s ban on interest-bearing stablecoins.

Meanwhile, MiCA’s transitional period ends July 1, after which crypto asset service providers generally must hold authorization under the regulation to continue operating across the EU.

Magazine: AI is banking the unbanked in Africa… faster than crypto

Polymarket says a third-party vendor compromise discovered on Thursday enabled attackers to inject malicious code into its website interface, leading to a phishing campaign that targeted multiple users. According to blockchain analyst Specter, the injected script was used to drain an estimated $2.94 million from at least 11 Polymarket wallets.

Polymarket stated that the incident has been contained and that the compromised dependency has been removed. The platform also said affected users will receive full refunds. Cointelegraph contacted Polymarket for comment but did not receive a response before publication.

Key takeaways

- Polymarket reported a third-party vendor compromise that allowed attackers to inject a malicious script into its frontend.

- Analyst Specter linked the malicious code to phishing activity, estimating losses of about $2.94 million across at least 11 user wallets.

- Polymarket said the issue has been contained, a dependency has been removed, and users will be fully refunded.

- Blockchain security reporting data indicates the incident fits within a high volume of crypto breaches in the quarter.

- Separately, DefiLlama data shows private key compromise remains the dominant cause of reported exploit losses over the last 30 days.

Frontend compromise and phishing-driven wallet losses

The Polymarket incident centers on a supply-chain style failure rather than a direct smart contract exploit. Specter said the malicious script appeared to enable a phishing attack that redirected or induced users into compromising credentials or authorizations, culminating in unauthorized asset movement from user wallets.

In practice, this type of front-end compromise can be especially damaging for institutions and compliance teams because it shifts the risk profile away from on-chain mechanics alone. Even where contracts are unchanged, malicious web-layer code can manipulate user behavior, compromise session-related security assumptions, or trick users into signing harmful transactions. For regulated entities that integrate with or route user access to crypto services, incidents like this highlight the need for tighter vendor governance and continuous integrity controls over externally served dependencies.

Polymarket’s response suggests the affected component was identified and removed after discovery. Its commitment to fully refund users also raises operational and policy considerations: while refunds may mitigate user harm, they do not automatically address whether the underlying controls—such as third-party software update processes, dependency monitoring, and incident response playbooks—were sufficient to prevent reoccurrence.

DefiLlama breach reporting underscores a pattern of recurring exploit methods

The Polymarket case arrives as crypto security incident reporting remains elevated. DefiLlama data places the event within a broader timeline: the third quarter’s second quarter-to-date statistics indicate the quarter had its most-hacked period by incident count, according to Cointelegraph’s reference to DefiLlama and its reporting on Q2.

DefiLlama also reports that June saw reported crypto exploit losses of $74.9 million across 29 incidents, exceeding May’s $60.5 million total but remaining well below April’s $644 million peak.

Among the largest June incidents were a $36 million Humanity Protocol exploit, a $4.7 million Secret Network bridge exploit, two separate Aztec exploits valued at $2.1 million each, and a $1.7 million bridge exploit tied to Taiko. While each exploit involves different technical pathways, they collectively reinforce a key compliance reality: incident frequency and magnitude continue to stress operational risk management across exchanges, wallets, and service providers with protocol-level exposure.

DefiLlama’s breakdown of losses over the past 30 days points to private key compromise as the most common leading vector, accounting for 43% of reported exploit losses. Fake proof exploits made up 10%, and reverse MEV honeypots accounted for 8%. For risk teams, these categories matter because they indicate whether controls should prioritize key management, signature/authorization integrity, or transaction routing safeguards for automated systems and integrators.

Private key history at Polymarket highlights multiple threat surfaces

About a month before the reported Polymarket frontend incident, the prediction market disclosed an additional exploit traced to a six-year-old private key used for internal top-up operations. Cointelegraph previously reported that Polymarket said contracts and user funds remained safe in that earlier case and that all permissions associated with the compromised key were revoked.

Taken together, the two events underscore that Polymarket—or any crypto service with on-chain and off-chain touchpoints—can face multiple, distinct threat surfaces: backend key management for operational processes, and web-delivered dependencies for user-facing interactions. For institutional stakeholders, the combination can complicate assurance: even when one control area is remediated (for example, permissions revoked after a key issue), a separate control plane—like third-party dependency integrity—can still introduce new risk.

Polymarket’s scale also implies higher stakes for incident governance. DefiLlama reports that the platform holds more than $450 million in total value locked, up from $112 million a year ago.

Regulatory and compliance implications for crypto firms and integrators

Although Polymarket operates in a market with evolving regulation, incidents of this nature feed directly into compliance expectations for crypto businesses. Under frameworks such as the EU’s Markets in Crypto-Assets regulation (MiCA), firms are expected to meet governance and operational resilience obligations, while AML/CFT requirements under applicable regimes typically extend to “know your customer” processes and the protection of user funds. Supply-chain compromise and phishing-driven theft also raise questions for regulated counterparties about how customer asset protection claims are substantiated in practice.

For exchanges, wallet providers, payment processors, and institutional service providers, vendor-linked incidents may trigger additional internal review under third-party risk management policies. Common areas include: the lifecycle management of dependencies, auditability of frontend build and deployment pipelines, incident detection and containment procedures, and the adequacy of refund or restitution policies. Even if the theft originates outside on-chain code, user harms can still translate into regulatory scrutiny about consumer protection, disclosures, and operational risk controls.

Cross-border differences in enforcement priorities can further complicate response. In the United States, where crypto enforcement actions have frequently addressed security, consumer protection, and alleged failures in compliance controls, and where federal agencies coordinate through legal processes and subpoenas, a frontend-driven phishing incident can still be framed as a failure to maintain reasonable safeguards. Separately, AML/KYC obligations do not prevent phishing, but they can affect how stolen funds are identified, how affected users are supported, and how suspicious activity is triaged.

For institutional compliance monitoring, the most actionable element is the incident pattern itself: third-party compromise leading to user deception, alongside persistent exploit vectors such as key compromise. These themes suggest that governance should cover both technical controls (key management, permissioning, transaction integrity) and administrative controls (vendor oversight, software supply-chain assurance, and documented response measures).

Closing perspective

Polymarket says the compromised dependency has been removed and that affected users will be refunded. The next phase will likely involve detailed post-incident validation of the compromised supply chain, verification of residual exposure across its frontend delivery stack, and continued alignment of technical controls with the compliance expectations institutions apply to customer protection and operational resilience. Security incident reporting will remain a key reference point for assessing whether this case reflects a broader systemic risk pattern or an isolated vendor failure.

Bitcoin Below $59K Activates Multiple Setups With $54K BTC Price Target

Man City have agreed to sign a player that ‘Enzo Maresca will love’

How Much Money To Have With $60K Income?

-

Entertainment6 days ago

Entertainment6 days agoRenter of Home in Anne Heche Crash Denies Settlement With Son

-

Sports4 days ago

Sports4 days agoTwo goals and an assist by sheer aura: Cristiano Ronaldo just entered the World Cup chat

-

Tech5 days ago

Tech5 days agoMicrosoft accidentally kills epic Outlook email threads

-

Fashion16 hours ago

Fashion16 hours agoWeekend Open Thread: Staud – Corporette.com

-

Business6 days ago

Business6 days agoSoccer-U.S. defends Iran World Cup travel restrictions, says discussions ongoing

-

Politics1 day ago

Politics1 day agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Politics1 day ago

Politics1 day agoPotential 2028er World Cup attendee leaderboard

-

Business1 day ago

Business1 day agoAsia stock markets slide as tech shares slump

-

Tech2 days ago

Tech2 days agoA Look At A Gaggle Of Transputer Boards

-

Crypto World3 days ago

Bitcoin (BTC) Dips Below $62K, Ethereum (ETH) Plunges 6% Daily: Market Watch

-

Crypto World3 days ago

Crypto World3 days agoSecuritize Wraps Roubini's SEC-Registered ETF as Dubai VARA Digital Security

-

Crypto World2 days ago

Crypto World2 days agoDell (DELL) Shares Tumble Over 5% Following Analyst Downgrade to Hold

-

Business3 days ago

Entergy settles forward sale agreements, raises $672 million in cash proceeds

-

Crypto World7 days ago

Crypto World7 days agoCan Charles Hoskinson Really Rescue Cardano?

-

Sports13 hours ago

Sports13 hours agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Crypto World5 hours ago

Crypto World5 hours agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Crypto World17 hours ago

Crypto World17 hours agoRTX holders must register wallets before token distribution begins

-

Crypto World19 hours ago

Crypto World19 hours agoHyperliquid Named on Singapore MAS Investor Alert Register

-

Crypto World7 days ago

Crypto World7 days agoJake Chervinsky accuses CME of protecting derivatives monopoly

-

Sports2 days ago

Sports2 days agoIndia vs Bangladesh LIVE Score, Women’s T20 World Cup: Bangladesh Opt To Bat; India Enter ‘Do-Or-Die’ Stage As Semi-Final Race Heats Up

You must be logged in to post a comment Login