Crypto World

What is tokenomics? Supply, FDV, Unlocks, and Vesting explained

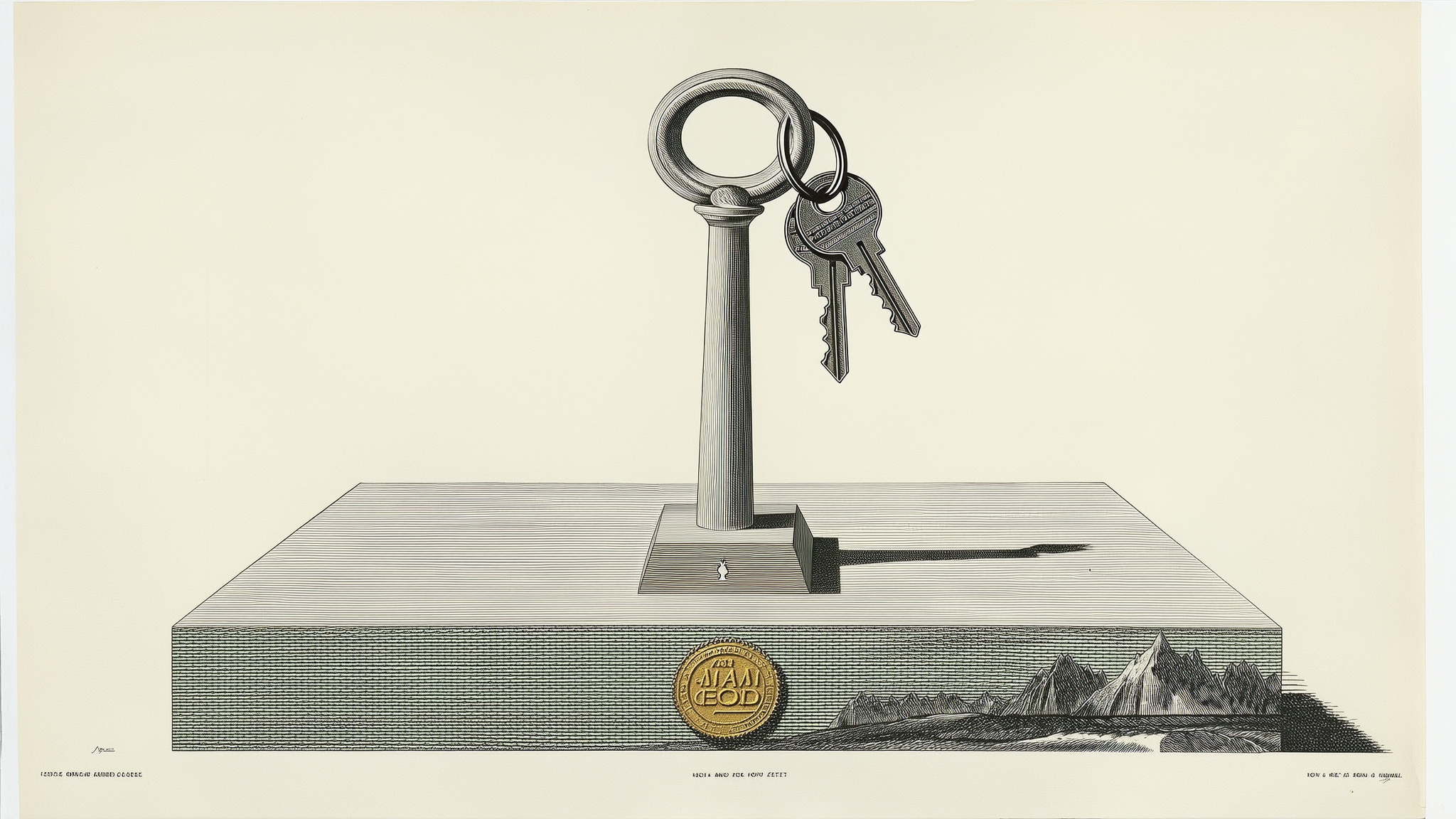

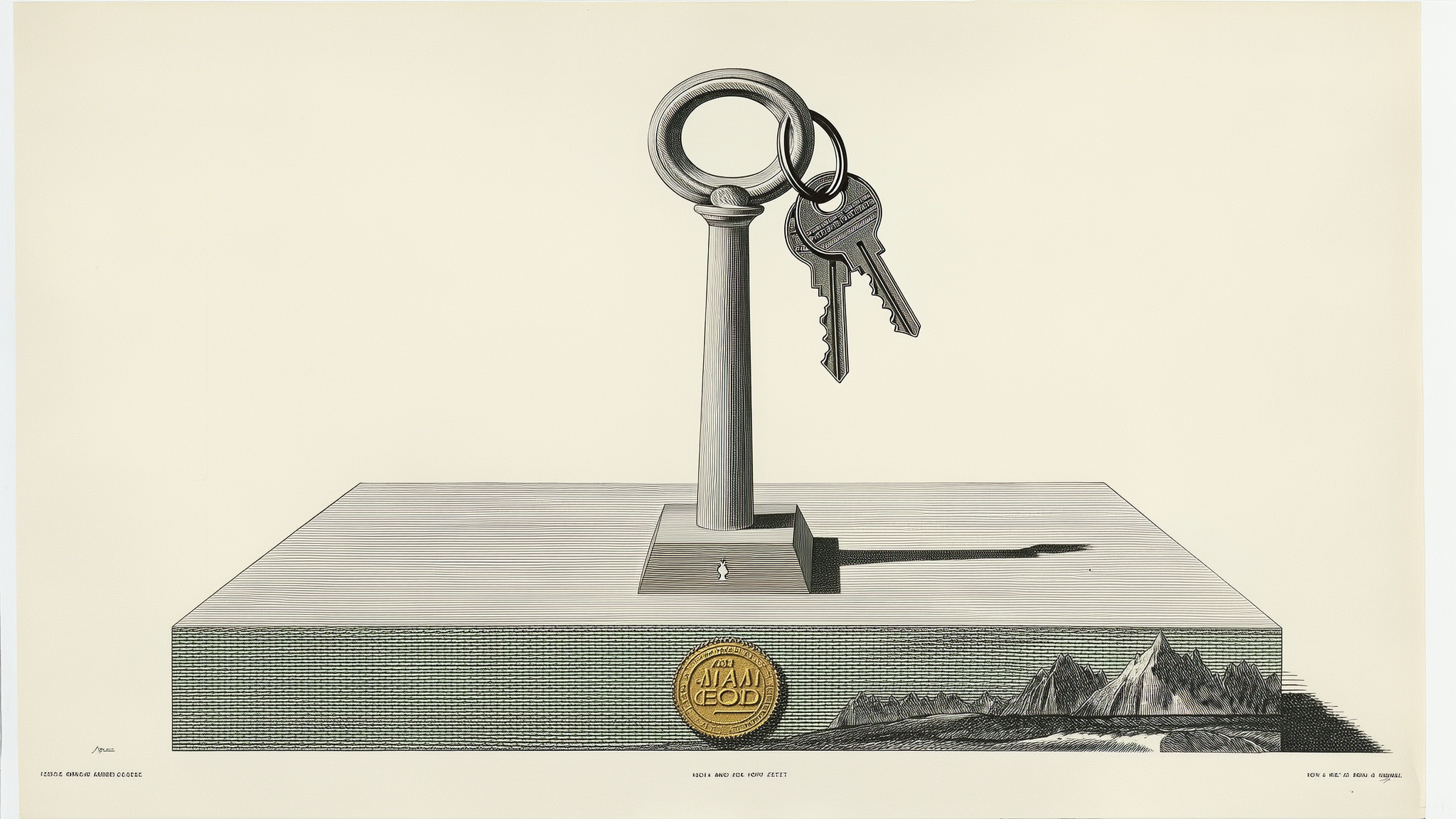

Tokenomics is the study of how a crypto token’s supply, distribution, and incentives are designed, and it is the single most useful lens for telling a serious project from a trap. Once you can read a token’s supply schedule and unlock calendar, a lot of crypto stops being mysterious.

Summary

- Tokenomics determines how a crypto token’s supply, distribution, utility, and release schedule are structured, making it a key factor in assessing long term risk and value.

- Large gaps between circulating supply and fully diluted valuation can signal significant future dilution as locked tokens enter the market through vesting and unlock schedules.

- Insider allocations, token emissions, burn mechanisms, and real world utility often reveal whether a project’s token economy is built for sustainability or faces ongoing selling pressure.

Tokenomics is the design and study of a cryptocurrency token’s economy: how many tokens exist, how new ones are created or destroyed, who holds them, how they are released over time, and what they are actually used for. The word is a blend of “token” and “economics,” and it matters because a token’s price is driven not only by demand but by the supply mechanics baked into its design, mechanics that are written into code and published in advance. Two projects with identical hype can perform very differently because one releases its tokens slowly to aligned long-term holders while the other dumps a flood of unlocked tokens onto the market every month. Learning to read tokenomics is how you tell those two apart before you buy, not after.

This guide breaks tokenomics into the pieces that actually move prices, with no finance background assumed. It covers the different kinds of token supply and why the distinction matters, the difference between market capitalization and fully diluted valuation, how token distribution reveals who really controls a project, the vesting and unlock schedules that quietly determine future selling pressure, the supply mechanics like burning and emissions that expand or shrink a token over time, what gives a token actual utility, and a worked example that ties it all together. By the end you will be able to look at a token’s supply page and unlock calendar and form a grounded view of its risks, which is a skill that protects you from a large share of crypto’s most common traps.

The three kinds of supply

The first thing to understand is that “how many tokens are there” has three different answers, and confusing them is one of the most common and costly mistakes new buyers make. Circulating supply is the number of tokens actually available and trading on the market right now. Total supply is the number that exists today, including tokens that are locked, reserved, or otherwise not yet circulating. Maximum supply is the absolute ceiling, the most tokens that will ever exist. Bitcoin, famously, has a maximum supply of twenty-one million coins, a hard cap that can never change. Many tokens have no maximum at all, meaning new units can keep being created indefinitely.

The gap between these numbers is where danger and opportunity hide. A token might have a small, healthy-looking circulating supply that makes its price seem reasonable, while a vast reserve of locked tokens waits in the background, scheduled to flood the market over the coming years. When those locked tokens release, they add selling pressure that can crush the price even if nothing about the project has changed, simply because supply expanded. So the question is never just “what is the price.” It is “what is the price, how many tokens circulate now, how many will exist eventually, and how fast does the gap close.” A token where circulating supply is close to total supply has most of its dilution behind it. A token where circulating supply is a small fraction of the total has most of its dilution still to come, and that pending supply is a headwind every future buyer inherits.

Market cap versus fully diluted valuation

This brings us to two numbers that beginners constantly mix up, with expensive consequences: market capitalization and fully diluted valuation. Market capitalization, or market cap, is the token’s price multiplied by its circulating supply. It tells you what the market currently values the actively trading tokens at, and it is the right number for comparing the present size of two projects. A token priced at one dollar with one hundred million tokens circulating has a market cap of one hundred million dollars.

Fully diluted valuation, or FDV, is the token’s price multiplied by its total or maximum supply; in other words, what the project would be worth if every token that will ever exist were already trading at today’s price. The gap between market cap and FDV is the single most revealing ratio in tokenomics. Imagine that same one-dollar token has a market cap of one hundred million dollars but a maximum supply of one billion tokens, giving it an FDV of one billion dollars. That means ninety percent of the eventual supply is not yet circulating, and as it unlocks, either the price must fall to keep the valuation steady or new demand must absorb every one of those tokens just to hold the price flat. A low ratio of market cap to FDV is a flashing warning that enormous future supply is coming, and many tokens that look cheap by market cap are quietly expensive once you account for the dilution baked into their FDV. Always check both numbers, never just the one the project prefers to show you.

Distribution: who actually holds the tokens

Numbers about supply mean little without knowing who controls it, which is why token distribution, the breakdown of who received the tokens at launch, is so important. A typical allocation divides the supply among several groups: the team and founders, early investors such as venture funds, a treasury or foundation reserve, rewards for the community, and the portion sold or distributed to the public. The percentages and the conditions attached to each tell you how fairly a project is structured and where future selling pressure will come from.

The warning signs are recognizable once you know to look. If insiders, meaning the team and early investors, hold a very large share of the supply, they have the power to overwhelm the market when their tokens unlock, and their interests may not align with ordinary buyers who paid far higher prices. A project where eighty percent of the supply sits in a single wallet, or where private investors bought in at a fraction of the public price, is structurally tilted against late buyers. The opposite end is a fair launch, where no insiders get a privileged early allocation, and the tokens are distributed broadly from the start, an approach common among community-driven tokens. Most projects sit somewhere in between, and the goal is not to demand perfection but to understand the structure: a heavy insider allocation is not automatically fatal, but it is a risk you should price in, especially when combined with the unlock schedule that decides when those insiders can sell.

Vesting and unlocks: the calendar that moves prices

If there is one section of this guide to internalize, it is this one, because vesting and unlock schedules quietly determine a token’s future supply pressure more than almost anything else. Vesting is the practice of locking up tokens allocated to insiders and releasing them gradually over time, rather than all at once, so that the team and early investors cannot dump their entire allocation the moment trading begins. A vesting schedule typically has two features: a cliff, an initial period during which nothing unlocks at all, and a release schedule, the rate at which tokens drip out afterward. A common structure might be a one-year cliff followed by tokens releasing monthly over the next two or three years.

The reason this matters so much is that every unlock is a scheduled, predictable increase in circulating supply, and large unlocks often coincide with price weakness as newly freed tokens hit the market. A project might trade calmly for months and then face a “cliff unlock,” a single date when a huge tranche of team or investor tokens becomes sellable all at once, which can swamp demand and drive the price down regardless of how the project is doing. Because these schedules are published in advance, often tracked on dedicated unlock-calendar tools, you can see the supply waves coming. Before buying a token, checking its unlock calendar is as important as checking its price: you want to know whether a large unlock is days away, who it benefits, and how big it is relative to the circulating supply. A ten percent supply unlock landing next week is a very different proposition from a token whose insiders are already fully vested with no major unlocks left. Smart buyers treat the unlock calendar as a core part of the decision, not an afterthought.

Supply mechanics: burning, emissions, and inflation

Beyond the initial design, tokens have ongoing mechanics that expand or shrink the supply over time, and these determine whether a token is inflationary or deflationary. Emissions are newly created tokens released as rewards, for instance to stakers, liquidity providers, or miners. Emissions are how many networks pay for their own security and growth, but they are also a form of inflation: if a protocol mints lots of new tokens to hand out as rewards, the supply grows, and unless demand keeps pace, each token is worth proportionally less. A high-yield farm paying out in a freely inflating token is often quietly diluting the very holders it is paying.

The counterweight is burning, the permanent removal of tokens from circulation by sending them to an address no one can access. Projects burn tokens for several reasons: to offset emissions, to return value to holders, or as a built-in feature of the network. Ethereum, for example, burns a portion of the fees paid on every transaction, which means heavy network usage can shrink supply and partly or fully offset the new ether created for validators. When you assess a token’s long-term supply trajectory, the question is the net balance: are tokens being created faster than they are destroyed, or the reverse. A token with high emissions and little burning faces persistent inflationary pressure, while one with modest emissions and meaningful burning can hold or even reduce its supply. Neither is automatically good or bad, but the direction matters: inflation that outruns demand erodes price, while a credibly shrinking supply supports it.

Utility: what the token is actually for

All the supply analysis in the world cannot save a token that has no reason to exist, which is why utility, what the token actually does, sits at the foundation of sound tokenomics. A token’s utility is the set of real uses that create demand for holding or spending it. Strong forms of utility include paying for transaction fees on a network, staking to secure a blockchain and earn rewards, granting governance rights to vote on a protocol’s decisions, or serving as the required medium of exchange within a particular application. The more essential a token is to using something people genuinely want to use, the more durable the demand for it.

The weak case is a token with little purpose beyond speculation, where the only reason to buy it is the hope that someone else will pay more later. Many tokens are designed so that their utility is thin or circular, for example, a governance token for a protocol no one uses, or a reward token whose only function is to be farmed and sold. This does not mean such tokens never rise; plenty do, driven by narrative and momentum, and memecoins openly embrace having culture rather than utility as their value. But for a project presenting itself as serious infrastructure, the honest question is whether removing the token would break the system or merely remove a speculative chip. Real utility ties the token’s demand to the success of the product, aligning holders with usage. Thin utility leaves the price floating on sentiment alone, which is a far more fragile foundation, especially when the unlock schedule starts adding supply.

Red flags: tokenomics warning signs to watch

Once you can read the individual pieces, certain combinations should make you pause, and learning to spot them quickly is what turns tokenomics from theory into protection. The clearest warning sign is a very low ratio of market cap to fully diluted valuation paired with heavy insider ownership. A token where only a small fraction of the supply circulates and most of the rest sits with the team and early investors is a structure where enormous future supply is coming and the people who control it bought in cheaply. That does not doom the token, but it stacks the deck against anyone buying at the current price, because the insiders can profit handsomely while late buyers absorb the dilution.

A second red flag is a large unlock arriving soon. A token that has traded calmly can face a “cliff” date when a big tranche of insider or investor tokens becomes sellable all at once, and that wave of new supply can overwhelm demand regardless of how the project is doing. Because unlock schedules are public, a buyer who fails to check the calendar is choosing not to see a risk that is sitting in plain view. Pair a looming unlock with insiders sitting on large paper gains, and the incentive to sell into that unlock is obvious. A third sign is high emissions with little or no burning, which means the supply is inflating steadily; a juicy advertised yield paid in a freely inflating token can quietly dilute you faster than the yield enriches you.

The subtlest red flag is thin or circular utility. If you cannot answer the simple question “why would anyone need to hold or use this token,” the price is floating on sentiment alone, which is a fragile foundation, especially when the supply schedule is adding tokens. Watch for governance tokens attached to protocols nobody uses, reward tokens whose only purpose is to be farmed and sold, and projects whose pitch is all narrative with no mechanism that ties demand to real activity. None of these signs is automatically fatal on its own, and plenty of tokens with imperfect structures still rise on momentum. The point is not to find a flawless project but to see the structure clearly and price the risk, so that a token’s design informs your decision instead of ambushing you after you have bought.

A worked example: reading a token at a glance

Put the pieces together with a hypothetical token, and you will see how quickly the picture forms. Suppose a new project’s token trades at two dollars. Its circulating supply is fifty million tokens, giving a market cap of one hundred million dollars, which sounds like a modest, mid-sized project. But its maximum supply is five hundred million tokens, so its fully diluted valuation is one billion dollars, and right away you know that ninety percent of the eventual supply is not yet circulating. That single ratio reframes everything: the token is far more expensive than its market cap suggests once dilution is accounted for.

Now look deeper. The distribution shows that forty percent of the supply went to the team and early investors, who bought in at twenty cents, a tenth of the current price, so they are sitting on large paper gains and have strong incentive to sell. The vesting schedule reveals a one-year cliff that ends in two months, after which those insider tokens begin unlocking at five percent of total supply per month. Putting it together: a token trading at a rich fully diluted valuation, with most of its supply still locked, held heavily by insiders who are about to start unlocking large monthly tranches at a tenth of their cost basis. None of that guarantees the price will fall, but it tells you exactly where the pressure will come from and when, and it lets you weigh that against the token’s actual utility and demand. A buyer who checked only the one-hundred-million-dollar market cap would have missed all of it. A buyer who read the tokenomics sees the whole board. That is the entire value of this skill: it turns a token from a price on a screen into a structure you can actually evaluate.

Frequently Asked Questions

What does tokenomics mean?

Tokenomics is the design and study of a crypto token’s economy: how many tokens exist, how they are created or destroyed, who holds them, how and when they are released, and what the token is used for. It blends “token” and “economics.” Tokenomics matters because price depends not just on demand but on supply mechanics written into a project’s code, so reading them helps you judge a token’s risk before buying rather than after.

What is the difference between market cap and FDV?

Market capitalization is the token’s price multiplied by its circulating supply, the value of the tokens trading right now. Fully diluted valuation, or FDV, is the price multiplied by the total or maximum supply, the value if every token that will ever exist were already trading. A large gap between them means much of the supply is not yet circulating and will dilute holders as it unlocks. A token can look cheap by market cap yet be expensive once FDV reveals the pending supply.

Why do token unlocks affect price?

An unlock releases previously locked tokens, usually held by the team or early investors, into the circulating supply. That increases the number of tokens available to sell, and large unlocks often coincide with price weakness because the new supply can overwhelm demand. Because unlock schedules are published in advance, you can see these supply waves coming. Checking a token’s unlock calendar before buying tells you whether a big release is imminent and how large it is relative to the circulating supply.

What is vesting in crypto?

Vesting is the gradual release of tokens allocated to insiders such as the team and early investors, instead of giving them everything at launch. A typical schedule has a cliff, an initial period when nothing unlocks, followed by a steady release over months or years. Vesting is meant to align insiders with the project’s long-term success and to prevent them from dumping their entire allocation immediately. The schedule also tells future buyers when supply pressure from insider selling is likely to arrive.

What makes tokenomics good or bad?

Healthier tokenomics generally feature a circulating supply close to the total, a reasonable gap between market cap and FDV, broad distribution without excessive insider concentration, gradual vesting without enormous looming cliffs, a sustainable balance between emissions and burning, and genuine utility that ties demand to real usage. Riskier tokenomics show the opposite: heavy insider holdings, a tiny circulating fraction with huge pending unlocks, high inflation, and thin or speculative utility. The goal is to understand and price these traits, not to demand perfection.

What is the difference between inflationary and deflationary tokens?

An inflationary token has a supply that grows over time, usually through emissions that reward stakers, miners, or liquidity providers; unless demand keeps pace, each token’s share of value falls. A deflationary token has a supply that shrinks, typically through burning, the permanent removal of tokens from circulation. Many tokens combine both, creating and destroying units at the same time, so what matters is the net balance. Bitcoin is disinflationary with a hard cap, while some tokens burn enough to offset or exceed their emissions.

This guide is educational information, not financial advice. Tokenomics helps you assess risk but does not predict price, and supply figures, schedules, and valuations vary by project and change over time, as of June 24, 2026. Always verify a token’s current supply and unlock data from primary sources before relying on it.

Bitcoin dropped to the $60,000 area on Wednesday for the second time this month, continuing its poor price action in the face of risk market rallies elsewhere.

Also continuing to lose ground on Wednesday were gold and oil, each falling below key levels — gold $4,000 per ounce and oil $70 per barrel.

Read more: Gold, silver and bitcoin tumble as ‘debasement’ trade unwinds

The declines in crypto, precious metals, and oil came as tech stocks rebounded following Tuesday’s modest one-day slump, with the AI trade continuing to draw investor interest and dollars.

South Korean memory chip giant SK Hynix on Wednesday filed to raise nearly $30 billion in a U.S. share offering, in what would be the overseas company capital raise since Saudi Aramco’s mammoth $26 billion sale in 2019.

The Nasdaq at midday Wednesday was up 0.8% against bitcoin’s 3.2% slump.

Bitcoin has lost the plot

Billionaire hedge fund manager Philippe Laffont succinctly summed up investor sentiment Tuesday, telling CNBC he has become “a little bit more worried” about bitcoin’s future, arguing that investors now have a wider range of opportunities to choose from than in previous years.

LastPass, the password manager that inadvertently facilitated the theft of $150 million in crypto from Ripple co-founder Chris Larsen, is now warning users that their personal information was stolen via an attack on third-party market firm Klue.

The company emailed its customers this week to inform them that Klue was breached on June 11 and that data including customer names, phone numbers, email addresses, and physical addresses, as well as support case data and sales-related data, had been stolen.

Despite this, LastPass stressed that the incident affects only Klue-integrated systems and that “LastPass products, services, and infrastructure were not impacted in any way and customer vaults remain secure.”

Multiple cybersecurity firms reliant on Klue have also seen customer data leaked.

The cybercrime group Icarus claimed responsibility for the breach and is reaching out to users and threatening to leak their data.

LastPass users have been warned to stay vigilant about social engineering and phishing attacks that may attempt to swindle them out of more information and funds.

LastPass’s 2022 breach lost Ripple co-founder $150M

LastPass suffered multiple major breaches in 2022 that saw sensitive data stolen from customers’ password vaults.

Crypto sleuth ZachXBT noted in 2024 that a threat actor was able to use data from this breach to steal $5.4 million worth of crypto from over 40 addresses.

Prior to this, in 2023, ZachXBT also reported that roughly $4.4 million was drained from over 25 victims because of the 2022 breach.

Possibly the biggest theft from LastPass involved Ripple co-founder Chris Larsen, who lost $150 million worth of crypto after his private keys were leaked in the 2022 breach.

Read more: ‘AudiA6’ crypto laundering suspects face extradition to US

Two people behind a $389 million cryptocurrency laundering service dubbed “AudiA6” have also, according to ZachXBT, helped launder stolen funds from LastPass users.

LastPass was fined £1.2 million by the UK’s Information Commissioner’s Office last year over the 2022 data breach.

The body claimed it impacted 1.6 million UK users, and that LastPass “failed to implement sufficiently robust technical and security measures, which ultimately enabled a hacker to gain unauthorised access to its backup database.”

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

Today’s blockchains already treat consensus as a matter of two properties: nodes must agree on the same history (consistency) and the system must keep processing transactions (liveness). But that framing leaves a crucial gap—what users ultimately care about is not only whether transactions get confirmed, but whether their relative ordering is meaningfully fair when multiple parties submit transactions that can interact economically.

A new line of research is trying to formalize “transaction order fairness” and map out what is possible under real-world networking constraints. The core takeaway: perfect “first-come, first-served” ordering is mathematically out of reach in asynchronous distributed systems, even before considering adversaries. The practical question becomes how to approximate fairness while keeping liveness and minimizing opportunities for extractive behavior.

Key takeaways

- Perfect receive-order fairness (“first-seen, first-executed”) cannot be guaranteed on public networks because messages arrive at different times and there is no shared clock.

- Even when each node has a clear local arrival order, group preferences can conflict—captured by the Condorcet paradox—making a single linear order impossible to satisfy.

- Hashgraph’s fairness model uses a DAG of events with median timestamps to respect causal relationships while bounding how far adversarial influence can shift ordering.

- BOF-style protocols (from the Aequitas/Themis line of work) relax fairness by ordering transaction “batches” derived from Condorcet cycles, enabling stronger liveness guarantees.

Why “fair ordering” is harder than it sounds

In public blockchains, ordering isn’t just an implementation detail—it can decide who captures value and who pays. When privileged roles like block builders or sequencers determine execution order, they can potentially exploit that power through strategies that front-run, back-run, or sandwich transactions. Research on maximal extractable value (MEV) describes this as a direct consequence of who can influence ordering.

To counteract this, some proposals treat transaction ordering fairness as a third consensus objective alongside consistency and liveness. The general idea is to constrain the block producer’s ability to bias ordering beyond what the network conditions and protocol rules imply—making execution more predictable and less vulnerable to systematic exploitation.

But the most intuitive fairness notion runs into a structural limitation. In an asynchronous distributed system, there is no globally defined reception order because different nodes observe transaction messages at different times. Without a shared clock and with arbitrary message delays, no protocol can ensure that every node’s “arrival order” maps perfectly onto a single network-wide execution order.

The Condorcet paradox: why majority “first” can loop

The strongest form of fairness is often described as Receive-Order-Fairness (ROF): if most nodes receive transaction A before transaction B, then A should be processed before B. ROF sounds straightforward, but the network reality undermines it. Nodes see messages at different speeds, so different nodes can legitimately observe different pairwise “firsts.” Even if those local observations are consistent for each node, the collective can still become inconsistent.

This is where the Condorcet paradox comes in from voting theory, and it translates cleanly to distributed ordering. Even when each participant has an internal preference for which of two items comes first, the majority preference across multiple pairs can form a cycle:

- Most nodes see A before B

- Most nodes see B before C

- Most nodes see C before A

When that happens, there is no single linear ordering that satisfies all majority pairwise preferences. The implication for blockchain consensus is direct: if fairness is defined too strictly in terms of majority “first-seen” comparisons, the protocol may be unable to produce any ordering that matches the majority view across all pairs.

Because of this impossibility, systems aiming for “fairness” must adopt weaker—but more achievable—guarantees.

Hashgraph’s approach: DAG causality plus median timestamps

Hedera’s hashgraph algorithm tackles transaction ordering fairness through a leaderless, event-driven model. According to the described model, transactions are transformed into cryptographically linked events inside a directed acyclic graph (DAG). Consensus ordering then emerges from how nodes collectively observe and sign those events, rather than from a single proposer unilaterally choosing a sequence.

Operationally, when a node receives a transaction, it creates an event and gossips it to peers. Subsequent events record hashes of earlier events they have seen, and nodes digitally sign the result. This creates a provable causal structure: if one event is an ancestor (direct or indirect) of another, the protocol provides a cryptographic guarantee about which event was created first by some node.

The ordering logic then distinguishes between events with causal relationships and those that are concurrent. Events connected by DAG ancestry are ordered according to their causal dependencies. For concurrent events (those without ancestor relationships), the protocol resolves relative ordering using a “round-received” concept and then refines that using median timestamps.

Median timestamps, as described, are derived from a set of node-reported local receive times, but constrained by the hashgraph’s ancestry. That constraint matters: nodes cannot claim to have observed an event before its causal predecessors without creating detectable inconsistency in the DAG. Under the standard assumption used in Byzantine fault tolerance—fewer than one-third of nodes are Byzantine—the median timestamp should remain within a bounded range of honest timing reports, limiting adversarial ability to arbitrarily skew ordering.

However, hashgraph’s fairness is not infinite. The described research emphasizes that fairness is bounded by an adversarial “surface” where a node can still influence its gossip behavior: which events it relays first and whether it delays relaying. While the DAG cannot fabricate a false causal history, strategic propagation patterns can reshape the inputs that ultimately feed into median timestamp computation.

There is also the Condorcet paradox risk for concurrent events. The DAG eliminates ambiguity for causally linked events because the ancestry is fixed at creation. But concurrent events can still be observed in different orders by different nodes, leaving some ordering tension that is then handled by the protocol’s round and median mechanisms.

BOF protocols: fairness by collapsing Condorcet cycles

Another line of work frames fairness differently—by explicitly embracing cycles. BOF (Batch-based Order Fairness) protocols define “blocks” as sets of transactions that form a Condorcet cycle, then enforce fairness at the level of how those blocks relate, while allowing arbitrary internal ordering inside each block.

In the BOF formulation described, fairness is controlled by a parameter γ: if a sufficient fraction γ of nodes observe block b before block b′, then honest nodes cannot output b after b′. When fairness constraints induce a cyclic relation, the protocol collapses the strongly connected component (SCC) into a single batch/block, because no linear order can satisfy all the directed constraints simultaneously.

A key practical point is that this approach relaxes strict ROF requirements. When a cycle occurs, internal ordering becomes irrelevant to the fairness guarantee, since the protocol treats the entire cycle participation as atomic at the batch level. The research description notes that deterministic rules (such as a hash-based rule) may then sort transactions within the batch, but the fairness criterion does not attempt to make those internal orders correspond to any global first-seen preference.

The Aequitas protocol line is described as having weaker liveness: its strict fairness constraints require waiting for complete Condorcet cycles, and if cycles can chain indefinitely, finalization delays could grow without bound—creating a “freeze” risk.

Themis is introduced as a refinement intended to preserve γ-BOF while improving liveness. As described, Themis also builds a dependency graph and collapses SCCs during a “FairFinalize” stage, but it avoids waiting for the full cycle to close. Instead, it uses deferred ordering and “batch unspooling” so SCCs can be output incrementally while new transactions keep flowing. The result, as presented, upgrades Aequitas’ weak liveness into standard liveness with a delay bound.

Themis also addresses communication scaling concerns. In its basic form, participants exchange messages with most other nodes, leading to communication growth roughly proportional to the square of the network size. An optimized variant, SNARK-Themis, replaces much of that direct exchange with succinct cryptographic proofs, so verification can scale more efficiently as the node count increases.

Finally, the protocol design includes a mechanism to prevent denial-style manipulation. If a malicious proposer tries to exploit the system by proposing an empty block, Themis’s deferred ordering accepts a partially ordered batch and leaves exact finalization to a subsequent honest proposer, based on verifiable transaction relationships rather than discretionary choices by the current proposer. This is framed as a way to tie finalization to bounded network delay rather than arbitrary proposer behavior.

What to watch next

The central unresolved question across these approaches is how to balance fairness guarantees against the operational costs—especially complexity, communication overhead, and the practical handling of concurrency. As more consensus designs incorporate formal ordering fairness ideas, investors and builders should watch for implementations that demonstrate bounded delays in real network conditions while maintaining robustness against adversarial reordering.

Kalshi has expanded its CFTC-regulated crypto perpetuals lineup to 13 digital assets after launching new contracts tied to Zcash, Near Protocol, and Shiba Inu, while legal battles over the platform’s products continue to intensify.

Summary

- Kalshi expanded its CFTC-regulated crypto perpetuals lineup with Zcash and Near contracts, while Dogecoin and Shiba Inu perpetuals are also live.

- The rollout comes as CME Group challenges the CFTC’s approval of similar products and the regulator fights Kentucky over market oversight.

- Traditional finance firms, including CBOE and Charles Schwab, are increasingly exploring perpetual and prediction-style trading products.

According to Kalshi’s latest listings, the prediction market operator has expanded its “American Perpetuals” lineup with contracts tied to Zcash (ZEC) and Near Protocol (NEAR), while Dogecoin (DOGE) and Shiba Inu (SHIB) perpetuals are also now available for trading. The additions bring the total number of supported crypto assets to 13, alongside Bitcoin and other altcoins.

The contracts are available through a structure approved by the U.S. Commodity Futures Trading Commission and do not carry expiration dates.

Recent filings submitted by Kalshi show the platform sought regulatory clearance for the new products on Tuesday. Zcash perpetuals are being offered with up to 2x leverage, while Near contracts allow leverage of up to 2.6x. Shiba Inu’s perpetual contract, listed under the ticker KSHIB, also carries a maximum leverage ratio of 2x. Dogecoin perpetuals are also listed on the platform as part of the latest wave of CFTC-approved crypto contracts.

The additions follow an earlier wave of filings covering assets including XRP, Solana, Dogecoin, Chainlink, Litecoin, Bitcoin Cash, Sui, Hyperliquid, Polkadot, Hedera, and Stellar. Kalshi has already secured approval for most of those products, though contracts linked to Stellar, Polkadot, and Hedera remain under review by the CFTC.

Legal scrutiny has grown around perpetual contracts

While Kalshi continues adding crypto products, regulatory questions surrounding the structure of perpetual contracts have become more prominent. As previously reported by crypto.news, CME Group filed a lawsuit against the CFTC and Chairman Michael Selig, arguing that certain contracts approved by the agency should be classified as swaps rather than futures products.

The debate has expanded beyond crypto markets. Earlier today, the CFTC sued Kentucky in federal court after the state sought to enforce gaming laws against Kalshi, Polymarket, and brokerage partners connected to Coinbase, Robinhood, and Webull.

In its complaint, the regulator argued that designated contract markets operating under federal oversight fall under the Commodity Exchange Act rather than state gaming regulations. Kentucky, however, maintains that sports-linked event contracts meet the state’s definition of sports wagering and should remain subject to local licensing requirements.

At the same time, regulators are seeking public feedback on how derivatives products should be classified. The SEC and CFTC have jointly requested comments on definitions involving swaps and related instruments, an issue that has gained urgency as event-based trading products become more common.

Traditional exchanges are moving toward similar products

Interest in perpetual-style contracts has also spread across traditional financial markets. As reported by crypto.news, CBOE Global Markets has begun evaluating whether its continuous Bitcoin and Ether futures could be converted into perpetual contracts after crypto perpetuals generated more than $8.5 billion in trading volume on Kalshi within weeks of launch.

Charles Schwab has likewise entered the prediction-markets segment through a partnership with CBOE, introducing all-or-nothing contracts tied to the performance of the S&P 500. The brokerage joins firms including CME Group and Interactive Brokers that have recently expanded into event-driven trading products.

Outside the United States, Kalshi is facing a different challenge. An updated members’ agreement published on Wednesday shows the company has added India to its list of restricted jurisdictions.

Indian authorities have classified prediction-market platforms under the Promotion and Regulation of Online Gaming Act 2025, arguing that products involving real-money speculation on uncertain outcomes can fall within prohibited betting activity regardless of how operators describe them.

Crypto World

Cardano wallet SecondFi hit by $2.4 million exploit, up to $20 million in user funds at risk

SecondFi, the Cardano wallet formerly known as Yoroi, says it has patched a major exploit that drained roughly 16 million ADA, worth approximately $2.4 million, from 374 user wallets across three separate attacks.

The root cause was a flaw in SecondFi’s proprietary wallet generation software. The vulnerability sits at the address level, meaning simply moving a seed phrase to another wallet offers no protection. “The security risk occurs when an affected user signs a transaction,” the team said on X.

Before attackers could reach a further 129 million ADA, SecondFi said it triggered emergency rescue measures, routing the funds to an independent third-party custodian. An external accounting firm has been engaged to verify those holdings and affected users can submit claims to SecondFi.

Blockchain security firm SlowMist estimates total losses could exceed $20 million when accounting for the full range of compromised wallets and tokens, a figure that remains unconfirmed pending an independent audit.

Cardano founder Charles Hoskinson acknowledged the incident but noted the dollar amount was modest relative to other crypto hacks, though he stressed that offered little consolation to those affected. “It hurts them whenever they lose anything,” he said. “This is the unfortunate reality of crypto.”

ADA is currently trading around $0.15, its lowest level since 2020.

Key takeaways

- The Ethereum Foundation has reduced its workforce by 20% following the completion of a major reorganization.

- ETH is up by 1% and is now trading above $1,650.

The Ethereum Foundation (EF) has completed a broad organizational restructuring that includes reducing its workforce by approximately 20%, affecting 54 employees across multiple teams.

In a blog post published Tuesday, the Foundation said the changes conclude a months-long reorganization process tied to the implementation of its updated mandate and treasury management strategy.

Ethereum Foundation introduces new organizational structure

As part of the overhaul, the EF has reorganized its operations into five core clusters: Protocol Layer, Access Layer, User Layer, Community Layer, and Institutional Layer. Two additional clusters will oversee management and operational functions.

According to the Foundation, each cluster has been designed with specific responsibilities, accountability frameworks, and internal structures tailored to its objectives.

“Each domain of work requires a different approach, is held accountable for different kinds of results, and has a different internal structure tailored to the work that needs to be done,” the EF stated.

Ethereum co-founder Vitalik Buterin revealed in a post on X that the workforce reduction comes as the Foundation pursues a significant spending reduction strategy.

The EF plans to lower annual spending from approximately 15% of its remaining treasury before 2026 to a long-term target of 5% after 2030. As part of this effort, the Foundation is reducing its budget by roughly 40% this year.

Buterin acknowledged the human cost of the restructuring, rejecting the notion that the layoffs were simply an efficiency exercise.

“Often, when an organization goes through something like this, people try to pretend that nothing of great value was lost,” Buterin wrote. “I will not try to pretend this. I respect my EF colleagues far too much to pretend that there was not much that is lost.”

The Foundation said affected employees will receive severance packages and transition assistance, similar to support provided to previous departing team members.

Ethereum price forecast: ETH risks further decline below key support

Ethereum continues to face downside pressure, with liquidation data highlighting persistent weakness in market sentiment.

On the 4-hour timeframe, ETH continues to trade below its 20-day, 50-day, and 100-day Exponential Moving Averages (EMAs), located near $1,753, $1,901, and $2,064, respectively.

The cryptocurrency also remains below a previously broken descending trendline around $1,729 and a key horizontal resistance zone near $1,741. These technical barriers suggest the broader bearish structure remains intact.

Ethereum is now approaching the important support level at $1,611 after being rejected near the convergence of the descending trendline and the 20-day EMA.

A decisive break below $1,611 could expose the next major support zone at $1,524. If selling pressure intensifies, additional downside targets emerge at $1,404 and potentially $1,155.

Unless buyers reclaim key resistance levels, Ethereum’s price action remains vulnerable to further losses in the near term.

Australian lawyer and prominent XRP community commentator Bill Morgan has been in the news headlines as he called on Ripple to relock less of its monthly 1 billion XRP escrow release. According to Morgan, accelerating the path to full circulating supply would establish XRP as a credible hard money asset and eliminate the supply overhang that continues to weigh on sentiment.

The argument is not new in outline, but the specifics of Morgan’s framing push it into sharper territory, and Ripple’s own CTO Emeritus has already drawn a clear line on how far the company is willing to go.

— XRP GURU

LEGAL EXPERT BILL MORGAN URGES RIPPLE TO UNLOCK XRP TOKENS FASTER

LEGAL EXPERT BILL MORGAN URGES RIPPLE TO UNLOCK XRP TOKENS FASTER

32.74 BILLION XRP STILL LOCKED IN ESCROW

"THE SOONER IT IS ALL RELEASED FROM ESCROW + CIRCULATING SUPPLY IS 100% — THE QUICKER XRP WILL BECOME THE BEST HARD MONEY"

CURRENT PACE COULD TAKE NEARLY 9 YEARS pic.twitter.com/J7KGnmRcy7

(@Xrp_Guru1) June 24, 2026

(@Xrp_Guru1) June 24, 2026

With 32.74 billion XRP still locked in escrow and the current release pace stretching the full-circulation timeline to roughly nine years, the structural math gives Morgan’s argument its weight. The question the XRP community is now openly debating is not whether the overhang is real, but whether Ripple has both the incentive and the flexibility to compress that timeline.

Discover: The Best Crypto to Diversify Your Portfolio

Ripple Supply Overhang

Ripple established its escrow system in 2017, placing 55 billion XRP into 55 separate on-ledger contracts, each releasing 1 billion XRP on the first of every month. The mechanism was designed to create a predictable, auditable supply and avoid an unannounced dump from a centralized treasury.

However, what it also created, by design, was an indefinitely extendable schedule: Ripple takes what it needs for operations and institutional distribution, then relocks the remainder into new contracts, effectively rolling the timeline forward month after month.

Morgan’s position, stated publicly on X, is direct:

The logic is three-layered. First, relocking less shortens the nine-year horizon. Second, full circulation removes the psychological shadow supply that suppresses valuation. Third, a fixed, fully-circulating crypto supply is structurally more credible for institutional participants who price assets on known fundamentals rather than unknowable future release schedules.

It is worth noting that Morgan is looking for an argument. He has previously defended the escrow mechanism itself against claims that it is a deliberate price-suppression tool. He also pointed out that XRP ran from roughly $0.50 to above $3.00 between November 2024 and January 2025 while monthly releases continued uninterrupted. His current call is for faster completion of a process he considers legitimate.

Discover: The Best Token Presales

David Schwartz Draws the Line

Ripple CTO Emeritus David Schwartz has not endorsed acceleration, and he has flatly rejected the most radical version of the proposal circulating in the XRP community: burning the escrowed supply outright.

Schwartz cited Stellar’s token burn as his primary cautionary reference. He argues that supply destruction produced a short-lived market reaction rather than a durable valuation re-rating. His broader defense of the current model is that Ripple voluntarily relocks whatever XRP it does not immediately need.

On the timeline question specifically, Schwartz acknowledged the inherent uncertainty:

“It’s hard to predict because you have to make assumptions about how much XRP Ripple uses and how much gets put back into subsequent escrow months.”

Schwartz’s position is structurally consistent with how Ripple has managed the escrow since inception. The company has positioned measured, predictable distribution as a feature, not a constraint. Changing that calculus would require Ripple to decide that the reputational and institutional benefits of acceleration outweigh the risks of increased near-term sell pressure. Basically, a trade-off that the company has not yet indicated it is willing to make.

Ripple’s recent MiCA regulatory approvals in Europe reinforce the pattern: the company is building compliant infrastructure, and supply stability is part of that institutional pitch.

Don’t Miss Out on Our $1,000 USDT Airdrop on ByBit

What the Community Debate Actually Reveals About XRP Beyond the News Headlines

Beyond the news headlines, the split inside the XRP community maps cleanly onto two different theories of what XRP is supposed to be. The pro-acceleration camp, aligned with Morgan, treats the hard money narrative as the primary long-term value proposition. A fixed, fully-circulating supply that can be evaluated on demand fundamentals alone. The pro-current-pace camp treats Ripple’s controlled distribution as an asset for institutional credibility, not a liability.

A third concern runs underneath both camps: if Ripple releases more net XRP per month without a corresponding increase in demand, the additional supply hits the market as sell pressure. XRP’s current price action does not obviously signal that the market is capacity-constrained on the demand side in a way that would absorb larger monthly net releases cleanly.

The token burn option, meanwhile, is effectively closed. Schwartz’s Stellar reference reflects a settled internal view that destroying escrow reserves would produce noise and would permanently eliminate the optionality Ripple currently holds.

Discover: The Best Crypto to Diversify Your Portfolio

The post XRP News: Why Ripple’s 9-Year Clock Divides the Community appeared first on Cryptonews.

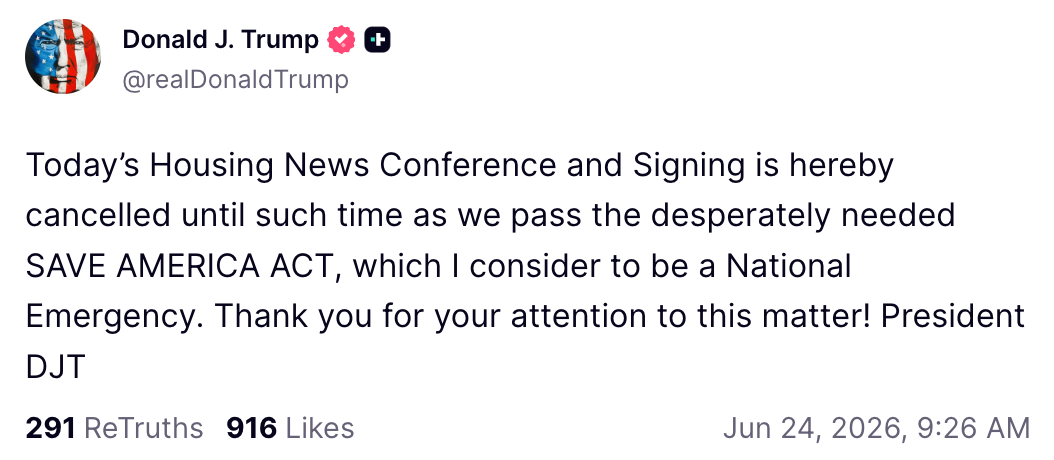

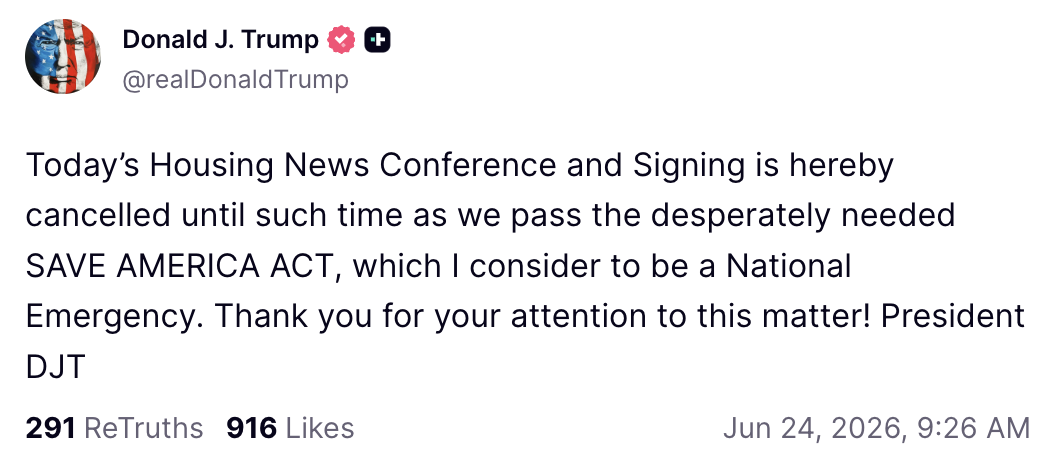

US President Donald Trump cancelled the signing ceremony for a housing bill containing a ban on a central bank digital currency (CBDC) as he looked for Republicans in Congress to prioritize a controversial voting bill.

In a Wednesday morning Truth Social post, Trump said that the signing for the 21st Century ROAD to Housing Act, passed by the US Senate and House of Representatives, would be cancelled “until such time as we pass the desperately needed SAVE America Act.”

Source: Donald Trump

The housing bill, passed by the House on Tuesday, included a provision barring the US Federal Reserve from issuing or creating a CBDC “or any digital asset that is substantially similar” until the end of 2030. However, the legislation also included a carve-out for stablecoins, allowing “dollar-denominated currency that is open, permissionless and private.”

Many had expected Trump to sign the bill, aimed at tackling housing affordability, into law on Wednesday without issues. However, the president said in March that he would “not sign other bills” until the SAVE America Act was passed.

The legislation would require voters to provide proof of US citizenship in person to register.

Related: US Senate passes housing bill with CBDC ban until 2030

Senate Republicans largely supported the housing bill, which passed the chamber in a 85-5 vote on Monday. Tim Scott, the Republican who chairs the Senate Banking Committee, expressed support for the legislation as recently as Wednesday morning before Trump’s announcement.

Could Trump’s position also impact crypto market structure?

Given the president’s opposition to signing any bill into law other than the SAVE America Act, it’s unclear whether Trump also intends to veto or delay signing of crypto-related bills.

As of Wednesday, the US Senate was still waiting to potentially vote on the Digital Asset Market Clarity (CLARITY) Act, a bill expected to change the roles of financial regulators in overseeing and enforcing digital asset laws. However, Trump said in May that he intended to codify a “future-proof digital asset market structure,” likely referring to CLARITY.

Magazine: AI is banking the unbanked in Africa… faster than crypto

This is a developing story, and further information will be added as it becomes available.

DeFi has long promised open and self-custodial finance. But for most users, actually using it still means juggling through wallets, dApps, bridges, pools, approvals, and risks that are very hard to understand in real time, especially for someone who’s relatively new to the industry.

CoinFello believes that the experience is ready for a major shift. With Fello 1, the company is building a self-sovereign AI agent designed to help users interact with DeFi through plain language while keeping complete control over their wallets and keys.

In the following interview with the founder, we go through why agents could become the primary interface for onchain finance, how controlled delegation can make automation a lot safer, and why liquidity provision is one of the first major frontiers for agent-powered decentralized finance.

CoinFello is positioning itself as a self-sovereign AI agent for DeFi. In simple terms, what problem are you trying to solve that wallets and dapps have not solved yet?

CoinFello is a completely new way to understand, use, and automate smart contracts.

The previous paradigm required users to create a wallet, navigate many disjointed websites, connect that wallet to a website, and then almost blindly trust that the smart contracts on that website do what the website promises they do. This made DeFi inaccessible, extremely complicated, and dangerous, and was one of the primary barriers to broader DeFi adoption.

CoinFello’s approach is to give users an agent that can interface directly with the smart contracts through a Claude-like user experience that people are familiar with. The agent isn’t just easier to use, it also opens up new frontiers of automation, where agents can act on behalf of users to accomplish virtually anything in DeFi: batch swap multiple tokens and bridge them across networks, discover advanced yield strategies, optimize existing deposits, take out a loan and automate payments, and a whole lot more. CoinFello makes doing these things super simple.

Fello 1 is described as a general-purpose DeFi agent rather than a narrowly integrated assistant. Why is general-purpose execution important, and what does it unlock for users that protocol-specific interfaces cannot?

DeFi is not one app or use case.

DeFi is an ecosystem of contracts, protocols, pools, vaults, bridges, and networks that constantly change.

Unfortunately, most of the crypto AI agent products on the market are just trading bots connected to some centralized API. If an agent only works through narrow integrations, it will always be limited to a few narrow use cases. That’s not how people use the internet (web browsers), their phones (extensible smartphones), AI agents, or even Ethereum itself. All of the great innovations were fundamentally extensible.

General-purpose execution means Fello 1 can reason about and interact with EVM-compatible smart contracts more broadly, instead of being locked into a small set of pre-built workflows. That unlocks all kinds of use cases that we ourselves never anticipate or integrate with. New pools, new protocols, and new opportunities can become accessible faster, without waiting for a dedicated front end or a code release for every specific action.

For the user, the benefit is simple: they do not need to jump between ten different interfaces to complete one DeFi strategy. They can describe what they want, review the steps, and execute across protocols from one agentic interface.

One of CoinFello’s core promises is that users can interact with DeFi through plain language while keeping custody of their wallets and private keys. How do you balance ease of use with the security expectations of self-custody?

We’ve tried to bring self-custody principles to the agentic era. This means that funds must remain in a self-custodied wallet, and agents should have guardrails enforced on them that define what funds they can access, in what ways those funds can be used, and for how long that agent has access to those funds.

With Fello 1, users keep their wallets and private keys. The agent operates through limited permissions that the user chooses to grant, and users review and approve transactions before execution. Plain language is the interface layer, not a replacement for consent. We fundamentally disagree with the approach of transferring funds to a centralized trading bot and hoping for the best.

The goal is to reduce cognitive overload without reducing user sovereignty. Fello can do the math, explain the route, surface the risks, prepare the transaction, and monitor positions, but the user remains in control of what permissions exist and what actually gets executed.

The Fello 1 launch puts a lot of emphasis on liquidity provision, including Uniswap V2, V3, and V4 positions, fee tiers, impermanent loss, and live position monitoring. Why did you choose LP management as such an important use case for the product?

Liquidity provision is one of the best examples of DeFi’s promise and its complexity. Concentrated liquidity can be a powerful yield opportunity, but it asks a lot from the user. You need to understand price ranges, ticks, fee tiers, pool selection, position sizing, impermanent loss, and when your liquidity is in or out of range.

That is exactly the kind of experience where an AI agent can create real value. Fello 1 can handle the mechanical and analytical parts: identifying LP strategies, doing the math, monitoring the position, explaining whether it is in range, showing the real return, and helping the user understand the trade-offs.

We chose LP management because it is not just a button-clicking problem. It is a decision-support problem. If we can make LPing understandable and manageable for more users while keeping them self-custodial, that is a major step toward making DeFi more mainstream.

AI agents in crypto are often associated with automation, but CoinFello says Fello 1 is not designed as an autonomous trading bot and that users still review and approve transactions. Where do you draw the line between helpful automation and too much delegation?

To be clear, we are building for automation, and we deeply believe users should be able to delegate approval for tightly defined automations to their agent. These are very complex problems to solve, so we’ve been working to expand the agent’s capabilities and the kinds of automation the user can create through the permissions and delegations we’ve been championing.

You previously led operations at MetaMask, one of the most important wallet products in crypto. What did that experience teach you about user behavior, wallet UX, and self-custody that directly shaped CoinFello?

MetaMask had a very radical vision in the early days of Ethereum. Most people at the time were building “use case wallets” with a handful of brittle integrations. MetaMask sought to do something else: create a permissionless and extensible wallet that could be used with any smart contract protocol.

We’ve brought the same radical values and vision to CoinFello that we previously used to build MetaMask. While most in the agent space are building narrow “use case bots,” our goal is different: to bring users onchain, and give them access to the entire decentralized web.

We also learned about the limitations of trying to solve the safety and user experience problems at the wallet layer. Wallets are forced to maintain endless integrations with third party protocols, and these integrations make their products slow to innovate, highly prone to bugs, and generally dangerous because the wallet still can’t understand what a smart contract *actually does.*

CoinFello is how we will solve these problems for the next wave of on-chain innovation.

CoinFello relies on a delegation model where users grant agents limited permissions that can be modified or revoked. What does a safe permission system for onchain AI agents need to look like as these tools become more powerful?

A safe permission system needs to be specific, limited, transparent, and revocable.

Users should not have to grant broad, unlimited authority over funds to an agent. Permissions should be scoped by action type, asset, protocol, amount, duration, and any other relevant rule the user cares about. The user should be able to see what permissions exist, understand what they allow, and revoke or modify them at any time.

As agents become more powerful, permission design becomes one of the most important parts of the stack. The future is not giving the AI your keys. The future is controlled delegation, where the agent can help execute within boundaries that the user defines. That is how we get the benefits of automation without sacrificing self-sovereignty.

Looking ahead, do you think the future of DeFi will still be built around users manually navigating dapps, or will agents become the primary interface for onchain finance?

I think dapps will still matter, but agents will become the primary interface for most users.

Today, DeFi still looks like the early internet in some ways. Users manually navigate different websites, learn different interfaces, and stitch together actions themselves. That works for power users, but it does not scale to broader adoption.

Agents change the interface from navigation to intent. Instead of asking users to know exactly which protocol to use and which buttons to click, they can say what they want to accomplish, compare options, understand risks, and approve execution.

The future of on-chain finance will still be open, composable, and self-custodial. But the way users access it will become much more conversational, automated, and personalized. Our view is that agents will become the execution layer that makes DeFi usable for the next wave of users.

Disclaimer: The content shared in this interview is for informational purposes only and does not constitute financial advice, investment recommendation, or endorsement of any project, protocol, or asset. The cryptocurrency space involves risk and volatility. Readers are encouraged to conduct their own research and consult with qualified professionals before making any financial decisions. This interview was conducted in cooperation with CoinFello, who generously shared their time and insights. The content has been reviewed and approved for publication in mutual understanding. Minor edits have been made for clarity and readability, while preserving the substance and tone of the original conversation.

The post From Wallets to Agents: CoinFello’s Bet on the Future of DeFi (Interview) appeared first on CryptoPotato.

Andrew Cuomo will co-chair a joint venture between OKX and Intercontinental Exchange, the parent of the New York Stock Exchange, the companies disclosed Monday. The former New York governor takes the role as ICE's strategic push into crypto markets reaches its highest-profile political appointment… Read the full story at The Defiant

The Official 2026 USA Income Classes Were Announced! #fyp #facts #usa #money

The Cure at Blackweir Live updates as fans head into Cardiff, roads close and red weather warning in place

Could Nike Get the Boot from the Dow? Why Berkshire Hathaway Might Take Its Place.

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Miami – Corporette.com

-

Entertainment4 days ago

Entertainment4 days agoRenter of Home in Anne Heche Crash Denies Settlement With Son

-

Tech2 days ago

Tech2 days agoMicrosoft accidentally kills epic Outlook email threads

-

Sports21 hours ago

Sports21 hours agoTwo goals and an assist by sheer aura: Cristiano Ronaldo just entered the World Cup chat

-

Business4 days ago

Business4 days agoSoccer-U.S. defends Iran World Cup travel restrictions, says discussions ongoing

-

Crypto World13 hours ago

Bitcoin (BTC) Dips Below $62K, Ethereum (ETH) Plunges 6% Daily: Market Watch

-

Politics6 days ago

Politics6 days agoBBC Reporter Discusses Cross Party Criticism Of Trumps Iran Deal

-

Crypto World10 hours ago

Crypto World10 hours agoSecuritize Wraps Roubini's SEC-Registered ETF as Dubai VARA Digital Security

-

Business15 hours ago

Entergy settles forward sale agreements, raises $672 million in cash proceeds

-

Business5 days ago

Business5 days agoWall Street Week Ahead: Investors see Micron earnings as pulse check of AI rally momentum

-

Politics4 days ago

Politics4 days agoAndy Burnham and the meaning of Makerfield

-

Tech6 days ago

Tech6 days agoAWS enters the context layer race with a graph that learns from agents, not manual curation

-

Crypto World4 days ago

Crypto World4 days agoCan Charles Hoskinson Really Rescue Cardano?

-

NewsBeat5 days ago

NewsBeat5 days agoKeir Starmer Allies Question His Chances For No 10

-

Crypto World5 days ago

Crypto World5 days agoHIVE shares jump as $220M AI deal speeds Bitcoin mining pivot

-

Crypto World4 days ago

Crypto World4 days agoJake Chervinsky accuses CME of protecting derivatives monopoly

-

Tech2 days ago

Tech2 days agoNearly 7,000 fake Amazon domains registered ahead of Prime Day 2026, researchers warn

-

Entertainment5 days ago

Entertainment5 days agoJose Alvarado Wants Taylor Swift at More Knicks Games

-

Tech3 days ago

Tech3 days agoSignal’s Meredith Whittaker says AI chatbots ‘are not your friends’ and calls Copilot agents a backdoor

-

Business6 days ago

Business6 days agoBrexit cost 6% of UK economy, Bank of England company data suggests

You must be logged in to post a comment Login