Crypto World

What Is zkTLS? Web Proofs and How They Work

Blockchains are excellent at verifying what happens on-chain and nearly blind to everything else. zkTLS, a family of protocols also called web proofs, lets anyone prove facts from an ordinary HTTPS session, a bank balance, a driver rating, a loyalty tier, without revealing the underlying data or asking the website for permission. Here is how it works, who is building it, and where the trust assumptions hide.

Crypto has a data problem that predates every bull market narrative. Smart contracts can verify a token transfer with mathematical certainty, but they cannot see a payroll deposit, a university diploma, an Uber rating, or a frequent flyer tier. All of that information lives behind the login walls of Web2 platforms, reachable only through official APIs that are limited, revocable, and priced at whatever the platform decides. Oracles solved a narrow slice of this, mostly public price feeds, and were never designed to carry personal data.

zkTLS is the attempt to solve the rest of it. The idea is simple to state and hard to engineer: take the secure connection your browser already makes to any website, and turn what you see in that session into a cryptographic proof that anyone can verify, without exposing your password, your session, or the raw data itself. If it works at scale, every piece of information behind every login on the internet becomes portable, provable, and usable on-chain.

Start with TLS

Every website address that begins with https uses Transport Layer Security, or TLS. It is the protocol that secures roughly 95% of web traffic. When your browser connects to your bank, TLS performs a cryptographic handshake that does three things: it confirms you are talking to the real server, it encrypts the traffic so nobody in the middle can read it, and it guarantees the data was not altered in transit.

What TLS does not do is produce evidence. The encryption is symmetric, meaning your browser and the server share the same session keys. Once the session ends, you have no way to prove to a third party what the server sent you. You could screenshot your bank balance, but screenshots are trivially forged. You could hand over your login, but that exposes everything. You could share the session keys, but since the same keys both encrypt and authenticate, whoever holds them could fabricate any transcript they like. TLS was built for private communication, not for portable proof. That gap is what zkTLS fills.

What zkTLS actually is

zkTLS, short for zero-knowledge Transport Layer Security, is an umbrella term for protocols that make TLS sessions verifiable. The core output is a proof with two properties. Authenticity: the data genuinely came from a specific domain during a real TLS session, unaltered. Selectivity: the proof reveals only the specific claim being made, such as balance above $5,000 or rating above 4.8, while everything else in the session, including credentials, stays hidden.

One naming caveat worth knowing: the term is a misnomer. Not every implementation uses zero-knowledge proofs, and the emphasis is often verifiability first, privacy second. Many builders prefer the terms web proofs or TLS attestations. The industry has mostly settled on zkTLS anyway, so this guide uses it while flagging the imprecision.

The hard engineering problem is that TLS was never designed to admit a third-party verifier. Three architectures compete to solve it, each with different trust assumptions.

The three models

MPC-TLS. The oldest approach, pioneered by the nonprofit TLSNotary project, which dates back to 2013. Secure multi-party computation splits the TLS session keys between the user and a verifier node, so neither party ever holds the full keys. The verifier participates in the encrypted session cryptographically, using techniques like garbled circuits, and can attest to what the server sent without seeing the plaintext or being able to forge it. The security is the strongest of the three models, and the cost is overhead: MPC adds heavy network round-trips, which historically made proofs slow. Opacity Network builds on this model and has pushed hard on decentralizing the verifier set. Research directions like vector oblivious linear evaluation could cut MPC networking costs enough for one-second proofs.

Proxy witness. A proxy sits between the user and the website, forwarding the encrypted traffic and attesting that the recorded exchange really happened between that client and that domain. The user then proves claims about the decrypted contents, often with a zero-knowledge proof. This is the fastest model in production. Reclaim Protocol, its leading implementer, generates proofs from a phone in about two to four seconds with no app or extension, supports most major blockchains, and lists 889 community-built data sources. An academic paper titled Proxying is Enough put the probability of breaking Reclaim’s construction at ten to the power of minus forty. The trade-off is a trust shift toward the proxy layer and practical friction, since some platforms firewall known proxy traffic, which Reclaim works around with residential proxies.

TEE-based. Trusted execution environments, the tamper-resistant enclaves inside modern processors, handle the session inside sealed hardware. The enclave logs in, fetches the data, and signs an attestation about what it saw, with minimal performance overhead. The trust assumption moves to the chip: you are trusting the hardware manufacturer and the enclave’s resistance to side-channel attacks, a category with a documented history of breaks. zkPass began as an MPC project and now runs a hybrid, using a proxy witness model in production with MPC as backup, while other teams lean on TEEs for speed.

No model is strictly best. MPC maximizes cryptographic trust and pays in latency, proxies maximize speed and pay in trust assumptions, TEEs maximize convenience and pay in hardware dependence. Serious applications pick based on what breaks their use case first.

A worked example, start to finish

Abstractions aside, here is what a zkTLS flow looks like in practice for one concrete case: a borrower proving to a lending protocol that their bank balance exceeds $5,000, without sharing statements or credentials.

The borrower opens the lender’s app, which hands off to a zkTLS client, typically a lightweight mobile flow with no separate install. The client opens a normal TLS session with the bank’s website, and the borrower logs in exactly as they always do. Their password travels over the same encrypted channel as any ordinary login; the verifier never sees it, because depending on the model, the verifier either holds only a useless share of the session keys, or observes only ciphertext passing through a proxy.

The bank’s server returns the account page, oblivious to anything unusual. From its perspective, this is a routine customer session. The client then isolates the relevant response data, the balance field, and generates a proof of a narrow statement: this TLS session was with the bank’s real domain, the response was not altered, and the balance value in it exceeds $5,000. The actual number stays hidden. The account history stays hidden. The login stays hidden.

The proof lands on-chain or with the lender’s backend, where a verifier contract checks it in milliseconds. The whole round trip takes seconds on the proxy model, and the lender has learned exactly one bit of information: qualified. Compare that against the incumbent process, which involves uploading full statements to a stranger’s server and trusting their retention policy forever, and the appeal writes itself. The same skeleton, swap the bank for any website and the balance for any visible fact, is every zkTLS application in existence.

From 2013 curiosity to 2026 infrastructure

The idea is older than most of the industry using it. TLSNotary shipped its first construction in 2013, before Ethereum existed, as a way to notarize web pages for dispute resolution. For a decade it stayed a cryptographic curiosity: the MPC overhead made proofs slow, the tooling assumed expertise, and crypto had no application layer hungry for private off-chain data.

Three things changed. Zero-knowledge proving systems got fast and cheap on the back of the rollup boom, which industrialized zk engineering talent and libraries. Mobile-first implementations, led by Reclaim’s proxy design, collapsed proof generation from minutes on a desktop to seconds on a phone. And the application layer arrived: identity networks, points programs plagued by sybils, prediction markets processing tens of billions monthly, and AI agents that need to verify what they pay for. By the time Devconnect dedicated a full day to the technology, the question had shifted from whether web proofs work to which trust model wins each vertical.

What people are building with it

The use cases sort into a few families, and most of them were impossible before.

- Proof of personhood and identity. Humanity Protocol, the Worldcoin rival valued at $1.1 billion after a round co-led by Jump Crypto and Pantera, launched its mainnet with zkTLS at the center. Users link Web2 accounts, from airline loyalty programs to professional profiles, to a portable Human ID, proving who they are and what they have achieved without any central party seeing the underlying documents. It is identity verification without iris scans.

- Credit and undercollateralized lending. DeFi lending is overcollateralized because protocols cannot see income. With zkTLS, a borrower proves salary deposits, bank balances, or an off-chain credit score directly from the source, without handing over statements. Projects like Cr3dentials build income and KYC verification for lenders on this rail, and lending protocols use web proofs to unlock on-chain credit against Web2 financial reputation.

- Reputation portability. Opacity’s early demo let Uber drivers export their ratings to a rival platform. The same pattern applies to seller ratings, subscriber counts, and gaming achievements: reputations that platforms hold hostage become assets the user carries. This is the quietly radical part, because data lock-in is the moat under most large internet businesses.

- Marketplaces for gated goods. zkP2P uses web proofs to power a ticket marketplace where a seller proves they own a real ticket inside the vendor’s own system before the trade settles, collapsing the fraud problem that plagues secondary markets.

- Data for markets and AI agents. Prediction markets need trustworthy real-world data, and resolution disputes remain the sector’s biggest weakness. Web proofs offer a way to verify a source document cryptographically instead of arguing about it. The same applies to AI agents that buy data over protocols like x402: projects like MCPay use zkTLS to prove that an API response an agent paid for is authentic and untampered.

Why the timing is 2026

The technology is a decade old in concept, so the fair question is why it matters now. Three currents converged.

First, privacy became the sector’s active narrative. A16z crypto argued that privacy is the moat of crypto’s next phase, a thesis that has pulled privacy coins and privacy infrastructure back into focus. zkTLS is the consumer-facing end of that stack: it lets users prove things about themselves while revealing less, the exact inversion of how the data economy currently works.

Second, the tooling matured. Reclaim’s mobile-speed proofs, TLSNotary’s open-source verifier infrastructure, vlayer’s web proofs for Ethereum developers, and zkPass’s production deployments moved the field from papers to SDKs. Ethereum’s Devconnect conference now runs a dedicated zkTLS Day, with hands-on workshops across the competing implementations, a reliable sign that a primitive has crossed from research to developer adoption.

Third, adjacent security work made verifiable data legible to a mainstream audience. Ethereum’s push to end blind transaction approvals through the ERC-7730 Clear Signing standard trained the industry to ask what users can actually verify on their screens. zkTLS asks the same question about data instead of transactions.

How this differs from oracles, and why both survive

Because zkTLS moves off-chain data on-chain, it gets lumped in with oracle networks, and the comparison is worth drawing precisely. Chainlink, Pyth, and their peers are push systems: node networks fetch public data, mostly prices, aggregate it, and publish it continuously for every application to read. The economics amortize across all users of a feed, and the security model rests on the independence and stake of the node operators. This design is close to unbeatable for its job, which is why DeFi’s core money legos still run on it.

It also cannot do what web proofs do. An oracle network has no mechanism for data that requires logging in as a specific person, and no economics for data only one user will ever need. Nobody runs a Chainlink feed for your bank balance. zkTLS inverts every design choice: pull instead of push, per-user instead of shared, private data instead of public, generated on demand instead of streamed. The user is the oracle, and cryptography replaces the node network as the reason to believe them.

The mature stack will use both. Public market data flows through feed networks; personal, session-gated facts flow through web proofs; and the two already meet in places like prediction market resolution, where a price feed settles the objective markets and a verified source document could someday settle the contested ones.

The limits and the risks

An honest account has to include the ways this can disappoint.

Trust assumptions never disappear, they relocate. The proxy model trusts the witness layer not to collude with the user. The TEE model trusts silicon vendors. Even MPC, the most trust-minimized, typically relies on a verifier network whose decentralization is a work in progress. When a marketing page says trustless, the correct response is to ask which of the three models it runs and what breaks it.

Websites are not passive. Platforms change page structures constantly, which breaks data source integrations, and some actively resist automated access. A protocol whose data sources depend on scrapers dressed in cryptography inherits the fragility of scrapers.

Privacy cuts both ways. The same machinery that lets a user prove facts without exposure can help bad actors move value while revealing less to investigators. Wallet drainers adopting privacy tooling is not hypothetical, and regulatory attention on privacy-preserving infrastructure has a long track record.

And selective disclosure invites coercion. If proving your salary to a landlord becomes possible, it can become expected. A technology built to minimize disclosure can normalize new categories of demanded proof. That is a social risk, not a cryptographic one, and no protocol upgrade fixes it.

The quiet stakes: what happens to data moats

Zoom out from the cryptography and zkTLS is an economic weapon aimed at the deepest moat on the internet. Large platforms defend their positions with data lock-in: your ratings, your history, your follower graph, and your purchase record live on their servers, and leaving means starting from zero. That switching cost is why a five-star driver stays on one app, why a power seller cannot move marketplaces, and why challenger platforms die in the cold-start phase regardless of how good their product is.

Web proofs dissolve the lock without asking the incumbent’s permission. If a new ride platform can accept a cryptographic proof of a competitor’s rating, it inherits the trust the incumbent spent a decade accumulating, and the user carries their reputation the way they carry a passport. A lender can underwrite against a credit history it never stores. A social network can import proof of an audience without an API deal that the incumbent can revoke on a whim, which incumbents historically do the moment a client grows threatening.

Incumbents will not stay passive, and the countermeasure escalation is predictable: aggressive bot detection, page structures that shift weekly, legal pressure on proxy infrastructure, and terms of service amended to prohibit proof generation. None of those measures can break the cryptography, but all of them can raise the maintenance cost of data source integrations, and the protocols that win will be the ones that industrialize that maintenance. The fight over whether users own the facts about themselves is about to move from privacy policy debates into engineering, and for once the users’ side has tooling.

The bridge crypto kept promising

For years the industry described blockchains as a trust layer for the internet while the internet’s actual data sat somewhere the chains could not reach. zkTLS is the most credible attempt yet to close that gap without asking platforms for permission, and permissionlessness is the whole point: no API deal, no data-sharing agreement, no gatekeeper deciding which facts are exportable. Whether it becomes core infrastructure depends on the unglamorous work ahead, decentralizing verifier networks, surviving platform countermeasures, and proving the trust models under adversarial pressure. The primitive, though, is real, the proofs verify, and the fortress walls around Web2 data have their first practical siege engine.

Frequently asked questions

What is zkTLS in simple terms?

zkTLS is a set of protocols that turn an ordinary secure web session into cryptographic evidence. It lets you prove a specific fact you saw on a website, such as an account balance, a rating, or a membership tier, to any third party, without revealing your password, your full data, or anything beyond the claim itself, and without the website’s cooperation.

Is zkTLS the same as a zero-knowledge proof?

Not exactly. Zero-knowledge proofs are one ingredient, used to prove claims about session data without revealing it. zkTLS as a whole is a broader construction that also has to prove the data authentically came from a specific website, which involves MPC, proxies, or trusted hardware. Some implementations use little or no actual zk math, which is why many builders prefer the term web proofs.

What are the main zkTLS projects?

TLSNotary is the open-source pioneer of the MPC approach. Reclaim Protocol leads the proxy witness model with two-to-four-second mobile proofs and 889 data sources. zkPass runs a hybrid proxy and MPC design. Opacity Network builds a decentralized MPC verifier network. vlayer brings web proofs to Ethereum developers, and Humanity Protocol applies the technology to identity at network scale.

What can zkTLS be used for?

Proving identity and credentials without documents, unlocking undercollateralized DeFi loans with verified income, porting reputations like driver ratings between platforms, verifying tickets and gated goods in marketplaces, feeding verified real-world data to prediction markets, and letting AI agents confirm that data they purchase is authentic. Anything visible in a logged-in web session can, in principle, become provable.

Does the website need to approve or integrate anything?

No, and that is the point. zkTLS works from the user’s side of an ordinary TLS session, so no API access, partnership, or permission from the data-holding platform is required. The trade-off is fragility: platforms change their pages, throttle suspicious traffic, and firewall known proxies, so data source integrations require ongoing maintenance.

Is zkTLS private and safe to use?

The proofs themselves reveal only the claim being proven, and credentials never leave the user’s device in readable form. The real questions are about each model’s trust assumptions: proxy designs trust a witness layer, TEE designs trust chip vendors, and MPC designs trust a verifier network. Reputable implementations publish their assumptions; unaudited ones deserve skepticism.

How is zkTLS different from an oracle like Chainlink?

Traditional oracles publish public data, mostly asset prices, through node networks that fetch from APIs, and they scale poorly for personal information. zkTLS produces user-generated proofs about private, session-gated data, at per-user granularity, without the data source’s involvement. The two are complements: oracles for public market data, web proofs for everything behind a login.

Can zkTLS proofs be faked?

Forging a proof would require breaking the underlying model: defeating the MPC protocol, corrupting the proxy attestation, or compromising the hardware enclave. For the leading proxy construction, peer-reviewed analysis put the break probability at ten to the power of minus forty. The realistic risks are subtler: manipulated source pages, stale data, and poorly written claim logic, which is where audits matter.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Digital asset markets are volatile and you can lose your entire investment. Always do your own research. Information current as of July 3, 2026.

After two consecutive painful months in which they lost billions of dollars, the spot Bitcoin ETFs finally turned the page in July, but inflows were still modest.

Meanwhile, the exchange-traded funds tracking the performance of the largest altcoin enjoyed the month more, attracting over 2x more fresh capital.

Bitcoin ETFs in July

March and April were quite bullish for the spot BTC ETFs as the financial vehicles attracted well over $3 billion. However, the trend changed violently in May when they lost $2.43 billion. June became the worst month on record, as investors pulled out just over $4.5 billion. In total, the net outflows for May and June stood at nearly $7 billion, and the cumulative total flows dropped from over $58 billion to $51 billion.

July started more positively, with almost $200 million in net inflows during the first full week. Another $76 million followed during the second, and a more modest $34 million in the third. The trend was obvious as the initial high numbers gradually declined, aligning with the underlying asset’s controversial and sporadic price performance and ultimately leading to a very modest increase throughout the month.

The last week in July was once again in the red, with investors pulling $61.53 million out of the funds. Friday was the most painful day, as the total net outflows stood at over $265 million. As such, the month ended with $172.42 million. On one hand, green finally overcame the red wave, but on the other, the number was nowhere near enough to offset some of the recent losses.

ETH ETFs Do Better

The Ethereum ETFs entered July after a similarly painful two-month streak, in which they lost $541 million in May and another $529 million in June. However, investors were more persistent, and the actual net inflows for July were at a more respectable $365.17 million, thus outpacing the BTC ETF flows by over 2x.

Moreover, the ETH ETFs closed all four full weeks of July in the green, including the last one, which saw only one day in the red. Perhaps this investor behavior is among the reasons behind the underlying asset’s major resurgence in July. As reported earlier, ETH ended the month with a substantial 20% increase, making it the best in precisely a year.

All eyes are now on August, which hasn’t been ETH’s most favorable month historically, but there are some major double-digit exceptions.

The post Bitcoin vs. Ethereum ETF Battle: Who Won July? appeared first on CryptoPotato.

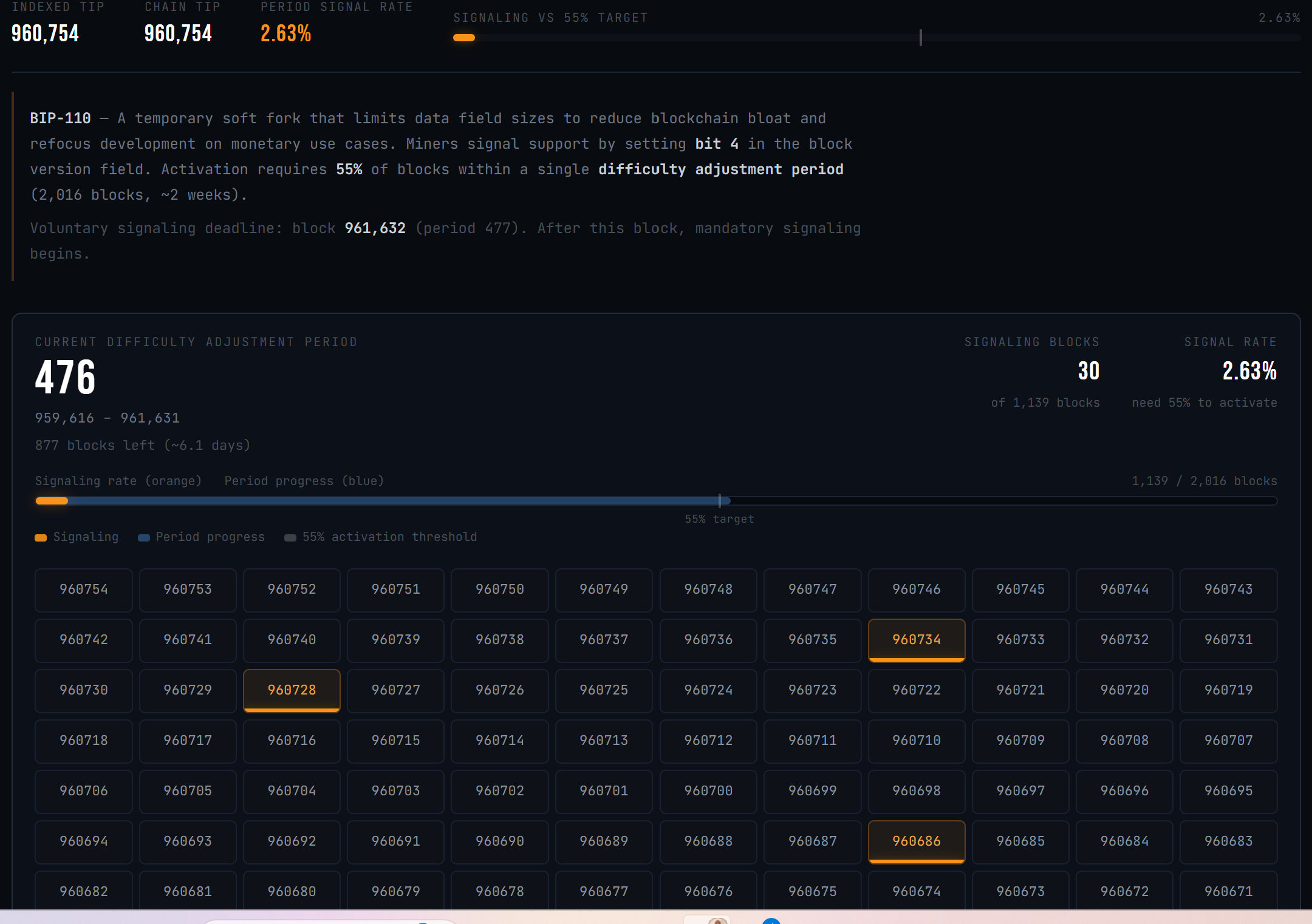

The developers pushing Bitcoin’s BIP-110 rule change have called off its launch. They blamed the industry response to a Coldcard wallet flaw that left user funds easier to steal.

Udi Wertheimer announced the delay, urging anyone running BIP-110 software to switch back to a normal Bitcoin (BTC) node. He gave no new date.

Why BIP-110 Activation Was Paused

BIP-110 is a temporary rule change, known as a soft fork. It would limit how much data people can pack into Bitcoin transactions.

Supporters say that data crowds out ordinary payments. Critics say Bitcoin should not police what users store.

The limits would last one year. Developer Dathon Ohm wrote the rules, and Bitcoin Knots software ships them.

Miners started voting on December 1, 2025. The Bitcoin blockspace spam debate had already split the community.

Then a separate problem landed.

Coinkite disclosed the bug on July 30. Its COLDCARD wallets built seed phrases, the master key behind a wallet, using far less randomness than promised. Roughly 72 bits instead of 128.

That gap makes a seed vastly easier to guess. Wallets running firmware released since March 2021 were hit hardest.

Updating the device does not fix a seed it already made. Coinkite is telling owners to move their money.

Thieves had already drained wallets tied to the flaw. The company has not said how much was lost.

Wertheimer called the delay a matter of timing, not doubt.

“…due to the coldcard incident, BIP-110 community leaders have decided to DELAY ACTIVATION. a new activation date will be announced at a later time,” he wrote.

Follow us on X to get the latest news as it happens

The Math Was Already Settled

Miners back a rule change by flagging their blocks. BIP-110 needed 55% of blocks in a two-week stretch. That means 1,109 blocks. The live monitor counted 30.

That is 2.63% of 1,068 blocks mined this period. It is the best BIP-110 has ever managed. It is still more than 20 times short.

Every earlier two-week stretch since December finished below 1.3%. Only 948 blocks are left. Even if every one voted yes, the total would reach about 48%. It could not pass this round.

That was already true days before anyone announced a delay.

Michael Saylor has warned about Bitcoin neutrality for weeks. He says almost every yes vote comes from one mining pool. Blockstream chief executive Adam Back has flagged chain split risk, calling the 55% bar too low to be safe.

A second phase was due at block 961,632, about six days away. It would reject any block that did not vote yes.

Nodes still running BIP-110 would enforce that on their own. That is why the warning to switch back matters.

No one owns Bitcoin’s rules. Nobody can flip a switch to start or stop a soft fork. This was a request, not a command.

Whether operators listen will say more about BIP-110’s support than any vote counter has.

The post BIP-110 Activation Frozen After Coldcard Exploit: Is the Soft Fork Dead? appeared first on BeInCrypto.

Senators Ruben Gallego and Thom Tillis sent a proposed revised ethics provision to the White House on Thursday, after drafting the compromise the day before, an industry source familiar with the talks told CoinDesk. As of midafternoon on Friday, the White House had not officially responded to the proposal.

Ethics remains the biggest outstanding issue to be resolved before the Clarity Act can advance. There are ongoing negotiations around other issues, including stablecoin reserves and yield, law enforcement authorities and some of the Agriculture Committee provisions addressing the Commodity Futures Trading Commission’s total remit, but these are relatively uncomplicated compared to ethics, two industry sources said. One added that they expected those other issues to be resolved relatively quickly should negotiators come to a deal on ethics.

If the White House signs off on the counter-proposal from Tillis and Gallego, that could speed the way to at least the first part of the cloture process, the other source told CoinDesk. The Senate would still need to follow the cloture process laid out in last week’s edition of this newsletter, but the timelines involved mean that it would be difficult to get the bill all the way through by the end of the week. Still, getting through that first procedural vote would be a visible win for the crypto industry, should it happen.

Strategy Inc. kept the annual dividend rate on its STRC preferred stock at 12% for August 2026, even though the Nasdaq-listed security ended July more than 10% below its $100 stated amount.

Summary

- 12% annualized dividend remains unchanged for August despite STRC closing July at $89.46 per share.

- $3.75 billion reserve covers roughly 2.1 years of preferred dividends and debt interest payments currently.

- Strategy repurchased 288,930 STRC shares below par while retaining $975 million in remaining authorization capacity.

The company’s official STRC information page confirms that the variable annualized rate for record dates beginning in August remains 12%. Executive Chairman Michael Saylor promoted the product on Aug. 1 as a way to “stretch your income,” emphasizing its twice-monthly payment schedule.

STRC closed at $89.46 on July 31, down $0.25 during the session. At that price, the $12 annualized payout based on the security’s $100 stated amount produces an effective yield of about 13.41%. Because Saylor announced the unchanged rate during the weekend, no post-announcement market reaction will be available until Nasdaq trading resumes.

Strategy’s STRC dividend no longer rises automatically

Strategy raised STRC’s annual dividend from 11.5% to 12% for record dates beginning in July. The increase followed a sharp June decline that took the shares as low as $71.25 and moved them far below the $100 level the company wants to maintain.

However, the company changed its rate-setting policy on June 29. Under the revised framework, management considers STRC’s market price, credit spreads, competing yields, Bitcoin volatility, cash-reserve coverage and the wider capital structure. The filing specifically states that Strategy will not necessarily raise the dividend solely because STRC trades below its stated amount.

That policy explains why July’s discount did not produce another 50-basis-point increase. Strategy instead said during its second-quarter results that it would maintain the 12% rate until STRC shows “sustained, healthy trading” near $100. The language describes management’s objective and does not guarantee that the shares will return to par.

The decision also prevents Strategy’s cash obligations from rising further while the company attempts to repair demand through other measures. Every additional 50 basis points would increase the annual cash cost across more than $10.46 billion in outstanding STRC stated value.

Buybacks now carry more of the price-support burden

Strategy has shifted part of its response from dividend increases to preferred-share repurchases. Between July 20 and July 26, the company bought back 288,930 STRC shares for approximately $25 million, paying an average of $86.53 per share. The purchase represented a 13.47% discount to the shares’ stated amount.

About $975 million remains under Strategy’s $1 billion preferred-securities repurchase authorization. Management said it intends to purchase more STRC at deeper discounts and reduce its activity as the security approaches $100. The authorization does not require Strategy to spend the remaining amount and has no fixed expiry date.

Repurchasing shares below par reduces the number of preferred shares requiring future cash distributions. It also lets Strategy retire $100 of stated value for less than $100. However, buybacks use capital that could otherwise remain available for dividends, debt interest or Bitcoin purchases.

As previously reported, Strategy funded its first $25 million STRC repurchase while increasing its U.S. dollar reserve and keeping Bitcoin purchases paused. The company raised much of that liquidity through sales of MSTR common stock rather than new STRC issuance.

The $3.75 billion reserve supports the 12% payout

Strategy reported a $3.75 billion U.S. dollar reserve as of July 26. The company said that amount covers approximately 2.1 years of expected preferred-stock dividends and interest on outstanding debt. The reserve can only be used for those obligations unless the board approves another purpose.

The cash cushion has become more important because Strategy’s preferred-stock commitments have expanded. The company recorded $400.7 million in preferred dividends during the second quarter, compared with $49.1 million one year earlier. It has paid or declared more than $1 billion in cumulative preferred distributions.

Strategy also reported an $8.22 billion second-quarter net loss, driven mainly by an $8.32 billion unrealized loss on its Bitcoin holdings. The accounting loss did not represent an equivalent cash outflow, but the preferred dividends must be paid in U.S. dollars.

The company has therefore authorized Bitcoin sales to refill the reserve, cover dividends and interest, or finance approved security repurchases. Strategy had sold approximately $218.4 million of Bitcoin during 2026 through July 26 to fund part of its preferred obligations.

As crypto.news reported, Strategy held 843,775 BTC at an average acquisition cost of about $75,476 as of July 26. The company valued that position at $54.77 billion using Bitcoin’s July 27 market price, compared with its $63.69 billion original cost.

STRC holders receive two payments each month

STRC moved from monthly to semi-monthly distributions after shareholders approved the change in June. Record dates now fall on the 15th and final day of each month, with payments generally following around 15 days later.

Strategy has already declared a payment of $0.50 per share for Aug. 15 to investors recorded as shareholders on July 31. The company’s website lists the 12% rate for August record dates, but future cash distributions still require board or committee approval and are not guaranteed.

For U.S. federal tax purposes, Strategy expects the current payments to be treated as returns of capital to the extent of an investor’s tax basis. That is the company’s expectation rather than a guarantee of each shareholder’s treatment, and Strategy advises investors to seek tax guidance based on their own circumstances.

STRC is also unsecured. Strategy states that its preferred securities are not collateralized by its Bitcoin holdings and only hold a preferred claim on the company’s residual assets. The company further warns that STRC is not a bank deposit, is not FDIC-insured and does not carry the same protections as Treasury securities or money-market funds.

What happens next for STRC and Strategy

Chief Executive Phong Le said management’s objective is for STRC to trade between $99 and $100 “over time.” Strategy has not provided a deadline for reaching that range, and the shares’ $89.46 closing price shows that the market continues to demand a yield above the stated 12% rate.

The next confirmed event is the Aug. 15 distribution. Investors will then watch Strategy’s next monthly rate decision, further STRC repurchases and weekly SEC disclosures covering common-stock sales, Bitcoin transactions and changes to the dollar reserve.

Saylor separately posted “Bitcoin Drive engaged” on Aug. 2 alongside the company’s treasury chart. The message may fuel expectations of a new purchase disclosure, but the post does not confirm that Strategy bought Bitcoin or reversed its recent pause. An SEC filing or company announcement would be needed to verify any transaction.

As of then, Strategy is relying on its existing 12% rate, twice-monthly payments, cash reserves and discounted repurchases rather than offering STRC investors another dividend increase.

The spot exchange-traded funds tracking Ripple’s cross-border token continue with their impressive performance in times of market uncertainty, and saw only one day of no reportable action in the past week, unlike the previous ones.

July also ended in the green for the funds, meaning that only one out of the nine months they have been active was in the red.

The Good Weekly and Monthly

Data from SoSoValue shows that Monday and Wednesday were quite modest in terms of net inflows. On both days, the ETFs attracted just under $600,000. However, the green streak continued and accelerated at the end of the business week, with $6 million in net inflows on Thursday and another $7.7 million on Friday.

Thus, the week ended with $14.86 million in the green, making it the best since the one that ended on July 2, when the funds attracted $17.19 million. On a monthly scale, investors poured in $27.29 million into the spot XRP ETFs.

What’s even better is that the funds have reached another all-time high in terms of cumulative total net inflows, at over $1.5 billion as of Friday’s close. Bitwise’s XRP has extended its lead over Canary Capital’s XRPC, with $511 million in net inflows compared to $467 million for the latter.

The Bad

Although July indeed ended in the green, the actual net inflows were not all that impressive. The $27.29 million places July as just the second-worst month, beating only January when investors inserted $15.59 million into the funds.

In contrast, June was a lot more positive, with the net inflows standing close to $60 million. May was even better, with almost $132 million. The all-time high from November at $666.61 million remains untouchable.

The Ugly

Although this improved at the end of the month, July saw the most days with no reportable action in terms of net flows. Precisely half of the trading days (11 out of the 22) saw no flows, according to SoSoValue, which, aligned with the more modest $27.29 million in net inflows, suggests dwindling interest in the funds.

Separately, the underlying asset’s price performance continues to disappoint despite the numerous positive developments in the broader Ripple ecosystem. Although it managed to defend the $1.05 support during the weekend, XRP is still below $1.10, and it’s down by more than 3% on a monthly scale. What’s even more worrisome is the fact that August has been a particularly painful month for the asset historically.

The post Ripple (XRP) ETF Monthly Recap: The Good, The Bad, and the Ugly appeared first on CryptoPotato.

Strategy’s preferred stock tracker, STRC, ended July trading well below its $100 par value, but management signaled that the company’s next preferred dividend rate will not rise. Executive chairman Michael Saylor said the August dividend will remain at 12%, continuing a payout level that was set after a June performance dip.

In a Saturday post on X, Saylor confirmed the dividend will hold at 12% for August. He also noted the company will keep its semi-monthly payment cadence for the second straight month after shareholders approved that change in June, following the earlier decision to increase the dividend by 50 basis points to 12%.

Key takeaways

- Strategy’s executive chairman said the August STRC dividend will remain at a 12% rate, not increase.

- STRC has continued to trade below its $100 par value throughout July, despite a monthly price rebound that began after the June dividend hike.

- Management reiterated a longer-term objective for STRC to trade near $99–$100, without specifying a timeline.

- Strategy reported building a large cash reserve—cited as $3.75 billion—to support preferred stock payouts and related obligations.

Dividend holds at 12% as preferred shares stay below par

Although STRC shares did not reach par in July, the stock did gain momentum over the month. The shares closed at $89.46 on Friday, up 5.42% for the month that started with the dividend adjustment.

Earlier, management had lifted the dividend rate in response to weak performance in June—raising it by 50 basis points to 12%. After that change, Strategy’s preferred payout strategy moved toward semi-monthly distributions, a structure that takes effect for the second month in August after the June shareholder vote.

Trading activity on Friday was also notably lighter than typical: volume was about two-thirds of the Nasdaq-listed shares’ daily average, according to the figures referenced in the report. That detail matters because it suggests the month’s rebound did not coincide with a surge in participation, even as investors processed the dividend update.

Management’s $99–$100 target meets a lower-than-par reality

Even as the next dividend stays flat, Strategy’s leadership continues to frame STRC around a valuation target. On Friday, CEO Phong Le reiterated that management’s “corporate objective” is for STRC to trade at $99–$100 over time, without adding specifics on when that goal might be reached.

That position is important to read in context: shareholders were told the dividend rate would not increase in August, even after the company adjusted payouts earlier in the quarter. Investors looking for signals that STRC might close the gap toward par have therefore had to balance two competing inputs—management’s longer-term pricing objective and the near-term decision to keep the dividend at the same level.

Cash reserve and buybacks aimed at supporting payouts

While the dividend rate message was unchanged, Saylor’s social-media activity pointed to continued capital management efforts tied to Strategy’s Bitcoin treasury strategy. On Sunday, he posted “Bitcoin Drive engaged,” accompanied by a familiar chart of Strategy’s BTC buying activity as tracked by Saylortracker.com.

The emphasis on liquidity and coverage aligns with what Strategy disclosed in its latest reporting. The company recently reported an $8.22 billion second-quarter net loss, driven primarily by an $8.32 billion unrealized loss on its Bitcoin holdings as the cryptocurrency’s price declined during the quarter.

Against that backdrop, Strategy said it has built a $3.75 billion cash reserve intended to support preferred stock payouts following the launch of its BTC monetization program. In the same vein, the company described a $3.75 billion U.S. dollar reserve sufficient to cover more than two years of preferred dividend payments and related interest obligations.

Strategy also disclosed that it repurchased $25 million of its STRC preferred shares at a discount to par and said it intends to keep buying the securities while they trade below $100. For investors, the practical takeaway is straightforward: management is pairing a coverage plan with an active buyback strategy, presumably to reduce pressure on valuation while the preferred shares trade under par.

However, the gap between par value and the prevailing market price remains the key issue. Management’s stated intent to buy more when the shares trade below $100 suggests the company believes the market offers an entry point—but without a near-term dividend increase, investors will likely focus on whether buybacks and reserve policy can translate into sustained movement toward the $99–$100 trading range.

What to watch next for STRC holders

With the August dividend rate confirmed at 12% and STRC still trading below $100 par, the next signal for holders will likely come from any further updates on Strategy’s Bitcoin treasury actions and whether cash-reserve coverage and buybacks continue at a pace that supports improving market pricing. Investors should also watch whether management provides clearer timing around its $99–$100 objective, since it currently remains framed as a long-term goal rather than a defined schedule.

Trump Media & Technology Group’s Truth API became available to institutional customers on Aug. 1, giving trading firms rapid, machine-readable access to posts from influential Truth Social accounts, including U.S. President Donald Trump’s account.

Summary

- August 1 launch gives institutions millisecond access to influential Truth Social posts with continuous coverage.

- Schiff and Warren asked the SEC to investigate whether the paid feed violates securities laws.

- Trump’s trust holds 41% of Trump Media, linking the product’s revenue directly to his wealth.

The launch followed a July 16 Form 8-K in which Trump Media said it had already signed customers and was onboarding additional partners. The company has not publicly identified those customers or disclosed how many subscriptions it has sold.

Truth API sells faster delivery of public posts

Trump Media describes Truth API as its first data-licensing product. The feed provides posts through a low-latency connection designed for high-frequency and algorithmic trading firms. It offers continuous coverage, delivery within milliseconds and a searchable archive dating to 2022.

Interim CEO Kevin McGurn said the service provides direct access to the platform’s “most market-moving Truths.” He also said Trump Media expects the product to become an ongoing, high-margin revenue source. Those revenue expectations remain forward-looking company claims rather than reported financial results.

The company has not published an official price list. Senators Adam Schiff and Elizabeth Warren cited reports placing subscriptions between $60,000 and $100,000 per month. Therefore, the widely repeated $100,000 price should be treated as a reported upper estimate, not a company-confirmed standard fee.

Trump Media says the underlying posts remain publicly available. However, automated customers can receive and process them faster than users who refresh the platform, rely on notifications or manually monitor accounts. That speed difference matters when algorithms can react to policy announcements within milliseconds.

Insider trading claims face an uncertain legal test

Writer James Surowiecki argued that the arrangement may involve government information being monetized for private benefit. Former SEC regional director Marc Fagel offered a more cautious assessment, calling insider-trading liability a “defensible argument” but “not slam-dunk.” Both comments are legal opinions, not findings by a regulator or court.

Federal insider-trading cases generally require more than an information advantage. Under the misappropriation theory recognized by the U.S. Supreme Court, prosecutors ordinarily must show that confidential information was taken for securities trading in breach of a duty owed to its source. SEC rules also focus on trading while aware of material nonpublic information.

That creates a key unresolved question. If a presidential post becomes publicly visible at the same time the API distributes it, Trump Media may argue that subscribers are paying for speed and formatting rather than nonpublic information. Many financial-data companies sell faster access to information that is technically public.

However, critics could examine whether paying customers ever receive a post before ordinary users can access it, whether unpublished policy information enters the feed or whether any subscriber knows information was obtained through a breach of duty. Purchasing a data subscription alone would not automatically establish insider trading.

Trump Media rejected the senators’ argument, saying they had created a new insider-trading theory based on publicly available information. That response states the company’s legal position. It does not prevent the SEC from reviewing the product’s design, timing records or customer communications.

Trump’s 41% stake sharpens the U.S. ethics dispute

Trump Media’s latest ownership disclosure says the Donald J. Trump Revocable Trust holds 114.75 million shares, equal to about 41% of the company. Donald Trump Jr. serves as sole trustee, while President Trump is the trust’s settlor and sole beneficiary.

The ownership structure means successful Truth API revenue could benefit the company and, indirectly, the value of the trust’s stake. It does not mean subscription payments go directly to the president. Share prices, operating costs, corporate decisions and other business results determine how product revenue affects shareholder wealth.

Schiff and Warren asked SEC Chair Paul Atkins to investigate whether the feed violates federal securities law or weakens market fairness. They argued that presidential posts may contain policy information capable of moving stocks, currencies and commodities while Trump retains a large financial interest in the platform distributing them.

The senators’ request also adds another political dispute to Trump Media’s expansion into financial and crypto-related services. As previously reported, the company posted a $405.9 million first-quarter loss after large unrealized markdowns on Bitcoin, Cronos and securities. Revenue for the quarter reached $871,200.

Meanwhile, Trump Media-linked wallets moved 2,650 BTC to Crypto.com in May. The company is also exploring wider financial products and a possible Truth Social corporate separation connected to its planned TAE Technologies transaction.

The SEC has not announced an investigation

The SEC acknowledged receiving the senators’ letter but had not publicly announced an investigation, subpoena, enforcement case or formal conclusion as of Aug. 2. SEC investigations are often confidential, meaning the absence of a public notice does not establish whether staff members are privately reviewing the matter.

The next verifiable developments could include an SEC response to Congress, a Trump Media filing describing customer numbers or revenue, or disclosures explaining whether API recipients receive posts simultaneously with ordinary Truth Social users.

Trump Media shares closed at $9.86 on July 31, down $0.52 from the previous close. That session occurred before the Saturday launch, so the move cannot be attributed to Truth API becoming available. U.S. markets were closed during the weekend criticism, leaving no verified post-launch stock reaction.

For now, the central dispute remains unresolved. Trump Media presents Truth API as a conventional paid data service that distributes public information more efficiently. Critics argue that the president’s ownership, government role and ability to move markets make the arrangement unlike an ordinary social-media feed.

Dogecoin community contributor Mishaboar urged Coldcard users on Aug. 1 to move their Bitcoin to wallets controlled by newly generated seed phrases.

Summary

- 1,367.05 BTC worth $88.6 million was drained from 4,585 addresses across three suspected attack waves.

- Coinkite says firmware updates protect new seeds but cannot repair seed phrases from vulnerable versions.

- Mishaboar advised users never to reuse affected seeds or enter recovery phrases into computers online.

The warning followed Galaxy Research’s estimate that three suspected attack waves drained 1,367.05 BTC, worth about $88.6 million, from 4,585 addresses.

Mishaboar wrote, “If you have ever used a COLDCARD device of any kind, migrate your funds to a new wallet immediately.” He also warned users not to reuse their existing Coldcard seed phrase or enter recovery words into an internet-connected computer. However, his reference to every Coldcard device is broader than Coinkite’s official security advisory, which identifies specific firmware versions and several exceptions.

Coldcard losses rise as attackers target smaller wallets

Galaxy Research’s latest on-chain estimate identified 1,367.05 BTC across three suspected attack waves. The research firm described $88.6 million as its “estimated observed size,” meaning the total has not been confirmed by Coinkite, law enforcement or every affected user.

The first wave removed 1,082.65 BTC from 1,196 addresses in about 41 minutes on July 30. A later third wave drained roughly 208 BTC from 1,912 addresses, with the average balance falling to slightly more than 0.1 BTC per address. The changing pattern suggests attackers moved from larger holdings toward smaller wallets.

Galaxy said each wave appeared internally consistent with one operator. However, it could not determine whether one attacker controlled all three waves. The third group used separate destination addresses, batched several victims into individual transactions and checked only the default derivation path, making it different from the earlier sweeps.

The research firm also warned that its known transaction patterns cannot identify every theft. A different attacker could generate valid transactions without repeating the fees, destination formats or collection methods seen in the first three waves.

Official Coldcard warning covers specific firmware

Coinkite said the problem affects seeds generated on Mk2 and Mk3 devices running firmware versions 4.0.1 through 4.1.9. Seeds created on Mk4 and Mk5 devices before standard version 5.6.0 or Edge version 6.6.0X are also covered. For Coldcard Q, the fixed releases are standard version 1.5.0Q and Edge version 6.6.0QX.

Coldcard Mk1 devices are outside the firmware regression identified by Block’s researchers. Coinkite also said TAPSIGNER, OPENDIME and SATSCARD are unaffected because they use different codebases. Therefore, the available technical evidence does not establish that every product ever made by Coinkite is vulnerable.

Block’s Bitcoin engineering and security team traced the flaw to a firmware integration error. The affected software used a deterministic MicroPython fallback instead of the intended STM32 hardware random-number generator when creating wallet secrets. On Mk2 and Mk3 v4 firmware, the affected path added no cryptographic entropy. Later models received a limited secure-element reseed.

Block cautioned that its analysis represented its current technical view and did not include complete empirical testing of every device. Coinkite has also said its investigation remains open and promised a formal technical report.

Firmware updates cannot repair existing seeds

Coinkite has released fixed firmware for every affected model and release track. The patches correct the seed-generation process for new wallets, but they cannot add randomness to a seed phrase created earlier. Moving the same vulnerable phrase into another hardware or software wallet also carries the weakness into the new device.

Affected users should install the correct fixed firmware before generating a replacement seed. Coinkite advises recording and verifying the new backup, checking a receiving address on the device screen and sending a small test transaction. Users should move the remaining balance only after confirming that the test funds reached the new wallet.

The company advises users to keep the old backup until the entire migration is confirmed. Mishaboar separately warned users never to type a seed phrase into a computer and recommended keeping offline copies in separate secure locations. That advice can reduce exposure to phishing, malware and cloud synchronization during a rushed migration.

Coinkite identified a limited exception for users who added at least 50 fair, independent and private dice rolls before the final seed words were produced. The company said those rolls contributed at least 128 bits of independent entropy. Users who entered fewer than 50 rolls, cannot remember the number or exposed the roll sequence should migrate.

A strong, unique BIP-39 passphrase creates an additional barrier, but Coinkite said it does not repair an affected seed. Short, reused or predictable passphrases may be guessable. Even users with strong passphrases are advised to replace the underlying seed as soon as practical.

Coldcard incident renews the self-custody debate

Bitcoin investor Anthony Pompliano said the losses showed how technically demanding self-custody can be, even though individuals retain the right to control their assets directly. He also stressed that Bitcoin itself was not hacked because the failure occurred in third-party wallet firmware rather than the Bitcoin protocol.

That distinction matters because an attacker reportedly reproduced weak wallet keys offline. The incident did not require changing Bitcoin transactions, breaking its cryptography or compromising the network’s consensus rules. Once an attacker obtains a valid private key, the resulting transaction appears on-chain like one authorized by the legitimate owner.

As previously reported, the observed loss estimate rose from an early 594.48 BTC calculation to 1,367.05 BTC as researchers found additional address groups. In related coverage, crypto.news examined how the firmware build error weakened seed generation for more than five years.

The case has also entered the U.S. institutional-custody debate.As crypto.news reported, Bloomberg ETF analyst Eric Balchunas argued that the losses strengthen the case for spot Bitcoin ETFs among investors seeking price exposure without managing private keys. ETFs remove personal seed-management duties, although they replace those risks with institutional custody and counterparty exposure.

Coinkite’s promised technical review and further Galaxy address analysis are the next expected updates. Until then, $88.6 million remains the latest public on-chain estimate rather than a final confirmed loss. Users covered by the official advisory face the more immediate task of installing fixed firmware and moving funds to a completely new seed.

Crypto World

A massive stablecoin fragmentation war is brewing between tech giants and a startup is aiming to capitalize on it

The stablecoin market is fragmenting, and onchain capital allocator Spark is betting it can capitalize on the split.

Fintechs, exchanges and banking groups are increasingly launching their own dollar-linked tokens. Each issuer wants to keep users, reserves and transaction activity inside its own network as competition ramps up.

The stablecoin landscape “is about to fragment more and more,” Sam MacPherson, CEO of Phoenix Labs, said in an interview with CoinDesk.

PayPal has PYUSD, Circle has USDC, and Tether has USDT. Robinhood has joined the Global Dollar (USDG) consortium and is building its own chain, while OpenUSD (OUSD) is another large consortium that includes Stripe and Coinbase.

Beyond these giants, there are hundreds of other stablecoins, including Ethena’s USDe, World Liberty Financial’s USD1 and Sky’s USDS.

The result is liquidity scattered across an expanding number of tokens and networks.

Spark is betting those networks will still need to connect. Its aim is to be the layer that moves money between them.

Spark is an affiliated lending and liquidity unit of Sky, the DeFi ecosystem formerly known as MakerDAO and the issuer of the USDS stablecoin. It is developed by Phoenix Labs and supported through Sky’s governance and capital.

Strategy CEO Michael Saylor told investors that the preferred dividend tied to Strategy’s STRC shares will stay at 12% for August, despite STRC trading well below its $100 par value through July.

In a Saturday post on X, Saylor framed STRC as an income-oriented vehicle that he says can help investors “stretch your income,” while indicating that the semi-monthly dividend schedule approved earlier this year will continue. Strategy’s chief then reiterated a longer-term target price range for the preferred shares, even as market pricing suggests investors are still demanding a discount.

Key takeaways

- Strategy’s STRC preferred dividend will remain at 12% for August, according to Michael Saylor.

- August will mark the second month in a row that STRC dividends are paid semi-monthly, following a June shareholder vote.

- STRC shares closed at $89.46 on Friday, trading below $100 par value throughout July.

- Management has continued to state a corporate objective for STRC to reach and hold around $99–$100 over time.

- Strategy says it has built a sizable cash reserve to fund preferred payouts as it monetizes Bitcoin.

Dividend guidance holds steady even as STRC trades at a discount

While Strategy’s STRC preferred shares ended July below their stated $100 par value, shareholders were told that the August dividend will not increase. Michael Saylor made that point in a Saturday X post, continuing the company’s pitch that STRC is designed to provide a steady income stream for investors.

The 12% dividend rate is not a one-off adjustment: it follows a dividend change earlier in the cycle. In June, Strategy shareholders approved changes that moved STRC to a semi-monthly payment cadence. As a result, August will be the second month that the dividend is paid on that more frequent schedule.

On the market side, STRC ended Friday at $89.46, up 5.42% for the month that began with a dividend increase. According to the article, the daily trading volume on Friday was about two-thirds of STRC’s usual daily average—suggesting participation was fairly active, but not at peak levels.

Management’s messaging has also stayed consistent with its longer-term plan. On Friday, Strategy CEO Phong Le reiterated that the company’s “corporate objective is for STRC to trade at $99-$100 over time,” without offering a specific timeline for when that target could be met.

Cash reserve strategy tied to Bitcoin treasury and preferred obligations

Beyond dividend arithmetic, the company’s stability message appears to be supported by its Bitcoin treasury and liquidity planning. Saylor posted on Sunday that “Bitcoin Drive engaged,” a phrase he used alongside a chart of Strategy’s BTC purchases from Saylortracker.com, signaling the company’s ongoing buying activity.

That matters because Strategy’s preferred dividend economics are linked to how it finances obligations while its Bitcoin holdings remain exposed to market volatility. Last week, Strategy reported an $8.22 billion second-quarter net loss, which the report attributed largely to an $8.32 billion unrealized loss tied to movements in the price of its Bitcoin holdings during the quarter.

Even with that drawdown, Strategy said it has built a cash reserve intended to help cover preferred stock payouts after the launch of its BTC monetization program. The figures cited in the article include a $3.75 billion U.S. dollar reserve. Strategy also stated that the reserve is enough to cover more than two years of preferred dividend payments and interest obligations.

In practical terms, that guidance is meant to reduce concerns that near-term Bitcoin price fluctuations could immediately disrupt the dividend. Traders may still price STRC based on expected returns and relative risk, but a defined liquidity buffer can influence how investors interpret the sustainability of the payout.

Discount-to-par repurchases and the $99–$100 over-time goal

Another point investors are watching is how Strategy manages the preferred share discount. The article says Strategy recently repurchased $25 million of its STRC preferred shares at a discount to par and intends to continue buying the securities while they trade below $100.

This approach aligns with management’s public objective for STRC to trade closer to par over time. However, the market continues to price the shares significantly lower: with Friday’s close at $89.46, the gap to $100 remains substantial. That spread reflects uncertainty about timing—how quickly any pathway to par could play out, and whether dividends alone are enough to close the valuation gap.

Le’s repeated comment that the objective is $99–$100 over time, without specifying when, highlights the central tension: Strategy is emphasizing financial buffers and ongoing BTC-driven support, while the preferred market is still setting prices around a discount that persists through July.

Investors therefore have two parallel items to track. First is the dividend rate itself—now confirmed to stay at 12% for August. Second is whether Strategy’s buybacks and any treasury policy changes translate into steady demand for STRC preferred shares that could narrow the discount.

What to watch next for STRC holders

Going forward, STRC investors should monitor the next dividend payment cycle for August and pay close attention to whether Strategy follows through on continued preferred repurchases while the shares remain below par. At the same time, any updates related to “BTC monetization” and treasury allocation could influence how markets assess the company’s ability to fund preferred obligations during periods of Bitcoin volatility.

Live Gold, Crypto Trading | 31 JULY | #goldtrading #cryptotrading #bitcoin – MANSI

Chelsea blamed for major Alejandro Garnacho issue as ex-Man United star starts again

Bitcoin vs. Ethereum ETF Battle: Who Won July?

-

Sports7 days ago

Sports7 days agoCommonwealth Games boxing: Jadumani Singh seals dominant 5-0 win over Pakistan’s Sumama Rehman to enter quarter-finals | Commonwealth Games News

-

Business4 days ago

Business4 days agoWhy Trees Belong on the Risk Register

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Wit & Wisdom

-

Tech7 days ago

Tech7 days agoIntel is reversing course and bringing hyper-threading back to its server chips

-

Politics2 days ago

Politics2 days agoMeta enters AI-training agreement with far-right ‘propaganda rag’ Newsmax

-

Politics6 days ago

Politics6 days agoLuke Littler dismantles Gerwyn Price to retain title in Blackpool

-

Crypto World1 day ago

Crypto World1 day agoMicroStrategy Post-Earnings CLARITY Act Push Could Add New Catalyst for Its Stock

-

Politics5 days ago

Politics5 days agoThe Part of the Electric Transition Nobody Wants to Discuss

-

Entertainment5 days ago

Entertainment5 days ago‘Stargate’ Creator’s New Sci-Fi Series Returns for Season 3 Tomorrow

-

News Videos7 days ago

News Videos7 days agoBITCOIN JUST ENTERED THIS CRITICAL ZONE…

-

Business5 days ago

Business5 days agoMajor shareholder moves on Canyon

-

News Videos3 days ago

News Videos3 days agoBitcoin Enters the 3rd Stage of the Bear Market

-

Crypto World2 days ago

Crypto World2 days agoXRP Ledger v3.3.0 brings five institutional features

-

Crypto World5 days ago

Crypto World5 days agoKraken Enables Retail Access to Jersey Mike’s IPO via Tokenized Shares

-

Tech6 days ago

Tech6 days agoNew macOS Sequoia & Sonoma security updates for older Macs

-

News Videos5 days ago

News Videos5 days agoClaude: Build Financial Dashboards in Minutes (2026)

-

Politics3 days ago

Politics3 days agoLuke Littler’s dominance sparks GOAT debate

-

Sports3 days ago

Sports3 days agoSeema Kaliramna Wins Discus Throw Bronze, Takes India’s CWG Medals Tally To 17

-

Business5 days ago

Business5 days agoJohnson & Johnson agrees to $5.5B settlement over talc cancer claims

-

Crypto World9 hours ago

Crypto World9 hours agoCrypto PAC spending tops $2M in Michigan House race

You must be logged in to post a comment Login