Crypto World

Why Australia’s $17B Crypto Opportunity Depends on Regulation

Key takeaways

-

Australia could generate A$24 billion, or about $17 billion, annually from digital assets and tokenized finance. But that opportunity depends on whether policymakers establish clear and supportive regulatory frameworks.

-

Tokenization could transform financial markets by improving liquidity, automating settlement processes and expanding investor access to assets such as foreign exchange, equities, government debt and investment funds.

-

Tokenized money, including CBDCs and stablecoins, could significantly reduce the cost and time of cross-border payments by minimizing reliance on traditional banking networks.

-

Regulatory uncertainty remains the biggest barrier to growth, as financial institutions hesitate to commit capital without clear rules on licensing, custody standards and compliance for digital asset businesses.

Australia is widely regarded as one of the most technologically advanced financial markets in the Asia-Pacific region. However, in the area of digital assets and tokenized finance, the country faces a critical choice.

The Digital Finance Cooperative Research Centre (DFCRC) and the Digital Economy Council of Australia published a report titled “Unlocking Australia’s $24b Digital Finance Opportunity.” It warns that the country will capture only a small portion of these gains unless its regulatory framework is updated swiftly.

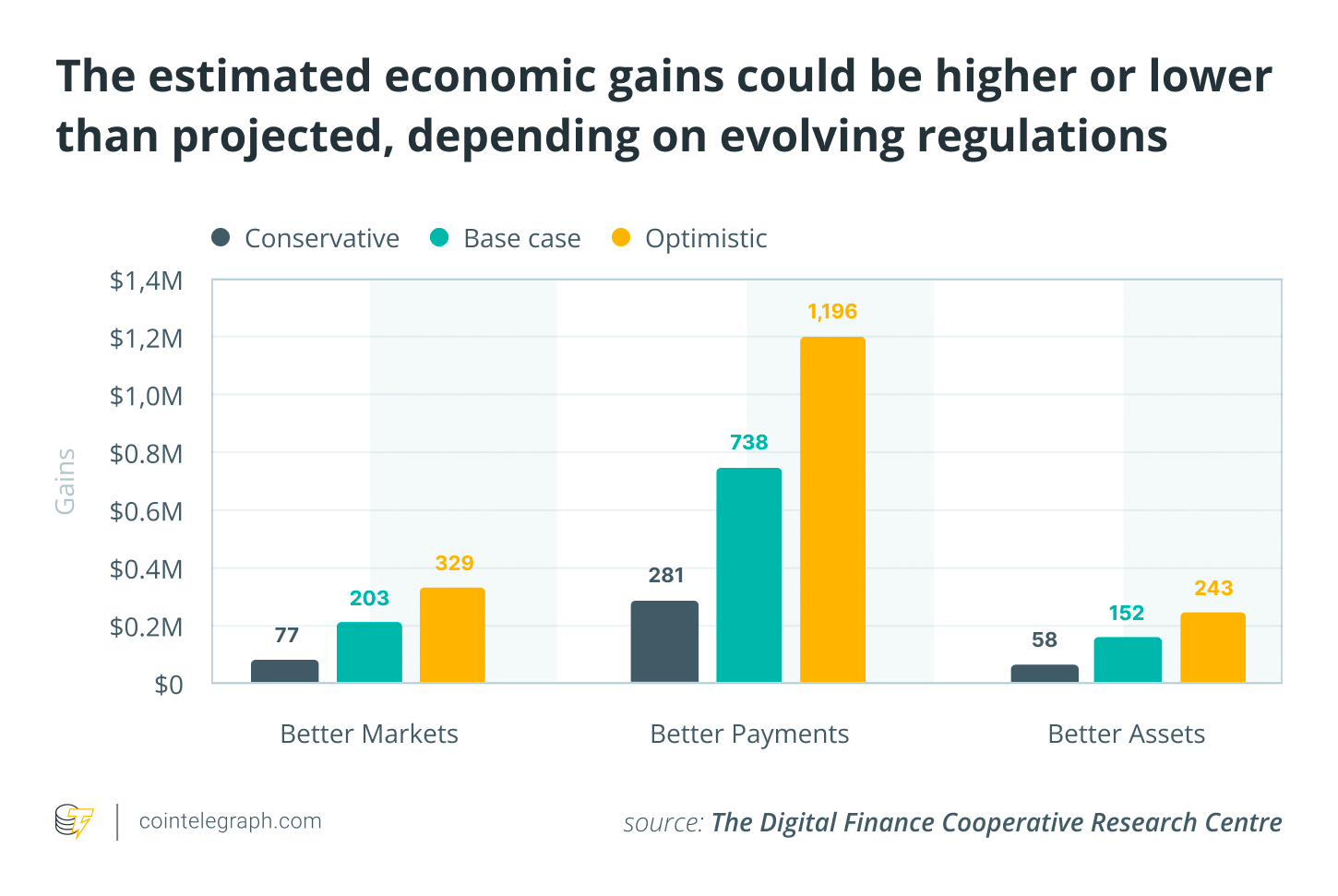

The report emphasizes that tokenized markets and digital finance could deliver around A$24 billion (approximately US$17 billion) in annual economic benefits for Australia, provided lawmakers move forward with regulation.

The scale of Australia’s digital finance opportunity

The DFCRC analysis indicates that tokenization and digital asset infrastructure could significantly improve several parts of Australia’s financial system. These improvements are expected to create economic value by making markets more efficient, increasing liquidity and allowing more investors to participate.

The report highlights three main sources of value that together represent an estimated A$24 billion opportunity.

Improved financial markets

Tokenized financial markets are likely to deliver significant economic benefits. By recording traditional securities such as shares or bonds on blockchain-based systems, markets can automate settlement processes, lower operational costs and open participation to a wider range of investors.

Tokenized infrastructure can also bring greater transparency and efficiency to assets including:

-

foreign exchange

-

investment funds

-

public equities

-

government debt

Improved liquidity and easier access for investors can lead to higher trading volumes and less friction throughout the financial system.

Improved payments

Tokenized forms of money such as stablecoins, bank deposit tokens and central bank digital currencies (CBDCs) could make both domestic and international payments faster and cheaper.

At present, many cross-border payments depend on correspondent banking networks, which are often slow and costly. Tokenized payment systems could enable near-instant transfers between institutions, shortening settlement times and reducing fees.

Better use of digital assets

Tokenization allows financial assets to become more programmable and easier to use in digital financial services. Smart contracts can automatically manage tasks such as margin calls, collateral handling and settlement, which are currently manual and time-intensive processes.

According to the DFCRC report, almost half of the gains related to assets could come from enabling new activities on tokenized infrastructure, including collateralized lending, repo markets and invoice financing.

Did you know? Australia was among the earliest countries to explore blockchain for financial market infrastructure. In 2017, the Australian Securities Exchange (ASX) began a project to replace its decades-old clearing system with blockchain technology before later reconsidering the plan.

Why regulation is the primary obstacle

While digital asset markets show great promise, the DFCRC report identifies regulatory uncertainty as the main factor holding back growth in Australia.

Large financial institutions generally avoid investing significant capital in new technologies until clear legal frameworks are established. Without specific rules on licensing, asset custody and compliance, many firms are hesitant to launch major tokenized products.

Key structural challenges include:

-

Vague licensing: It is currently unclear how digital asset businesses should obtain official permits.

-

Poor collaboration: There is a lack of communication between regulatory bodies and the industry.

-

Limited trials: A shortage of large-scale pilot programs limits practical testing.

-

Legal ambiguity: The status of tokenized financial products remains undefined.

These issues hinder progress even when the necessary technology is already available. Institutional investors need a well-defined regulatory foundation to enter the market with confidence.

The high cost of regulatory inaction

Continued delays in modernizing Australia’s regulatory framework could severely erode the country’s potential gains from digital finance.

If policy stagnation persists, Australia may capture only around A$1 billion (approximately US$710 million) from digital assets and tokenized finance by 2030. This figure represents only a small fraction of the A$24 billion in potential benefits that could be realized under a more supportive and predictable regulatory environment.

This massive shortfall highlights how regulatory hurdles can alter the future path of financial innovation. In the absence of clear, enabling policy settings, several damaging consequences could follow:

-

Pilot programs find it difficult to scale into live, production-grade systems.

-

Institutional capital stays on the sidelines, unwilling to take meaningful risks.

-

Cutting-edge innovation and talent increasingly relocate to jurisdictions offering regulatory clarity and predictability.

-

Australia’s domestic financial infrastructure modernizes more slowly than that of global peers.

Ultimately, prolonged regulatory uncertainty does not merely slow progress but may actively divert economic value and opportunity to other countries that have established favorable frameworks for digital finance.

Did you know? Australia hosts one of the densest networks of crypto ATMs in the Asia-Pacific region. It is also one of the largest markets for crypto kiosks outside North America.

What the industry is asking for in regulation

Australia has made initial strides toward establishing a regulatory framework for digital assets. However, industry stakeholders stress that more needs to be done to unlock meaningful institutional participation:

-

Clear licensing regimes for digital asset platforms: Trading venues, exchanges and other digital asset service providers urgently need well-defined licensing pathways. These include precise rules on permissible activities, operational requirements, capital standards and ongoing compliance obligations.

-

Modern, fit-for-purpose custody rules: Digital assets introduce distinct risks around security, segregation and operational resilience. Regulators should set clear, risk-based custody standards that safeguard client assets.

-

A coherent framework for stablecoins: Stablecoins are widely viewed as foundational infrastructure for tokenized markets and efficient on-chain payments. Industry participants are calling for clarity on issuance, reserves, redemption rights, supervision and cross-border rules to remove legal and operational uncertainty.

-

Balanced and proportionate consumer and investor protections: Strong safeguards against fraud, misconduct and loss are essential. But they must be designed carefully to avoid stifling legitimate innovation.

When addressed together, these regulatory building blocks would provide the clarity financial institutions need before committing significant capital and infrastructure to tokenized finance in Australia.

Why regulatory sandboxes are important

The DFCRC report recommends creating regulatory sandboxes tailored specifically for tokenized financial markets.

These sandboxes allow companies to test new financial technologies under close regulatory oversight before obtaining a full license. This approach lets regulators see how the innovations perform in practice while keeping risks under control.

Australia already has an Enhanced Regulatory Sandbox (ERS) managed by the Australian Securities and Investments Commission (ASIC). It permits eligible firms to trial certain financial services for a limited period without holding a full financial services license.

However, industry groups argue that more specialized sandboxes would speed up testing and development in key areas such as tokenized securities and digital settlement systems.

Targeted sandboxes would also improve dialogue between regulators and the industry, enabling policymakers to shape better rules based on actual testing outcomes.

The role of tokenized government bonds and CBDCs

The DFCRC report proposes that tokenized government bonds and a central bank digital currency (CBDC) could form essential infrastructure for digital financial markets.

Government bonds are already widely used as collateral in financial markets. Tokenizing them would allow for automated collateral management, faster settlement and improved transparency.

A CBDC designed for use by financial institutions rather than the general public could provide secure final settlement for tokenized assets. Together with stablecoins and bank deposit tokens, it would help build a flexible and efficient system for digital financial transactions.

These tools would create the reliable settlement infrastructure institutional markets need to operate at scale.

Did you know? Australia’s central bank was among the first to experiment with central bank digital currency trials. Earlier projects explored how a wholesale CBDC could help automate bond settlement and other complex financial transactions between institutions.

Project Acacia and Australia’s experimentation with digital money

Australia is already exploring these concepts through initiatives such as Project Acacia. This collaboration examines how digital money could work in tokenized wholesale markets.

The project tests how different forms of digital settlement, including CBDCs and stablecoins, can support financial market infrastructure.

Pilot programs like these can play an important role. They allow policymakers and financial institutions to test technical designs, operational risks and regulatory issues before moving to large-scale systems.

Real-world experimentation helps regulators create rules based on practical experience rather than theory alone.

Technological ability alone is not enough

A central finding of the DFCRC report is that technology alone is not enough to create new financial markets.

For institutions to adopt tokenized finance, the following are required:

-

clear legal frameworks

-

reliable settlement infrastructure

-

proper custody standards

-

effective risk management protocols

-

appropriate regulatory oversight

Together, these elements build the trust financial institutions need to commit to new technologies.

Without that trust, tokenized finance is likely to remain confined to small pilot projects rather than becoming part of mainstream financial systems.

Australia’s competitive challenge

The global competition to develop digital asset infrastructure is accelerating. Many jurisdictions are already building regulatory frameworks for tokenized securities, stablecoins and digital payment systems.

If Australia delays, it risks losing talent, investment and innovation to countries that provide regulatory clarity sooner.

In this sense, digital asset regulation is not just a financial policy issue. It is also a question of competitiveness for Australia’s broader economy.

Countries that put credible frameworks for digital finance in place are better positioned to attract capital and technology firms seeking stable regulatory settings.

Cointelegraph maintains full editorial independence. Guides are produced without influence from advertisers, partners or commercial relationships. Content published in Guides does not constitute financial, legal or investment advice. Readers should conduct their own research and consult qualified professionals where appropriate.

Crypto World

Bitcoin Rallies on Aggressive Spot Demand as Market Absorbs U.S. Economic Data: Bitfinex

Following a period of speculation-driven surges, bitcoin (BTC) appears to be rallying due to spot demand. Within a short time, spot demand metrics have shifted from contraction to growth. This development comes as the crypto market digests U.S. economic data.

According to the latest Bitfinex Alpha report, the ongoing bitcoin breakout reflects a widening gap between historical information about the U.S. economy and rapidly deteriorating sentiment evident in consumer data. This macro dynamic is significantly affecting risk assets like BTC and driving their prices higher.

BTC Sees Structural Improvement

Since the beginning of April, the crypto market capitalization has risen by $200 billion, following a 12% BTC rally that led to the strongest monthly performance in a year. By early May, BTC had broken above $80,000 – a level not touched since January 31. The move cleared the $78,000–$79,000, which had a dense overhead supply zone. Although the digital asset traded around $80,900 at the time of writing, the rally pushed it close to $83,000.

Bitfinex analysts have stated that the move marked a structural improvement and shifted BTC above a major aggregate cost-basis level near $79,800. This price doubles as the True Market Mean, which BTC has now reclaimed.

The most interesting part of this rally is that it was driven by aggressive spot demand. CryptoPotato reported last week that the market was not positioned for a surge above $80,000 due to weak demand.

Spot Demand Recovers

On-chain data shows that spot Cumulative Volume Delta (CVD) rose sharply after May 8, reflecting buyers absorbing supply at premium levels. Additionally, order books moved from bid-skewed to more neutral. Spot demand has stemmed from exchange-traded funds (ETFs) and from open-market accumulation.

As of two weeks ago, Michael Saylor’s Strategy was also a major driver of spot demand. However, there is less momentum from the company’s end because the purchases have been linked to the yield-bearing product, STRC. Unfortunately, the stock has not traded at or above its $100 par value, which is a threshold required for Strategy to purchase more BTC. In fact, the business intelligence entity is even looking to sell some of its bitcoins.

Nevertheless, conviction buyers, who are entities that accumulate BTC and rarely sell regardless of price, have increased their holdings. Analysts say they currently hold roughly 4 million BTC, following their largest surge since the COVID-19 crash. Historical data show that such growth from this cohort often precedes major price recoveries.

The post Bitcoin Rallies on Aggressive Spot Demand as Market Absorbs U.S. Economic Data: Bitfinex appeared first on CryptoPotato.

JPMorgan has filed to launch the JPMorgan OnChain Liquidity-Token Money Market Fund (JLTXX), a tokenized Treasury vehicle on Ethereum powered by Kinexys Digital Assets.

According to the filing with the US Securities and Exchange Commission (SEC), under normal conditions, the fund invests only in US Treasury securities and Treasury-collateralized overnight repurchase agreements.

JPMorgan Files To Launch A Second Tokenized Treasury Fund on Ethereum

The prospectus further says the fund will invest in a manner that satisfies eligible reserve requirements under the GENIUS Act, the US stablecoin law passed in July 2025.

“The Fund invests in a manner intended to satisfy the requirements for eligible reserve assets that stablecoin issuers are required to maintain under the Guiding and Establishing National Innovation for U.S. Stablecoins Act (otherwise referred to as the GENIUS Act) and regulations adopted thereunder, to support investment in the Fund by stablecoin issuers seeking to comply with such requirements,” the filing reads.

Follow us on X to get the latest news as it happens

JPMorgan’s prospectus signals that JLTXX will start on Ethereum but may expand to other networks. The launch deepens the bank’s tokenization push, alongside similar initiatives from institutional players such as BlackRock.

JLTXX would be JPMorgan’s second tokenized money market fund on Ethereum after My OnChain Net Yield Fund (MONY). The bank launched it in December 2025 with an initial investment of $100 million.

Why Ethereum, Again

Ethereum hosts the majority of distributed tokenized real-world asset (RWA) value tracked by RWA.xyz. The network currently accounts for more than 53.99% of the distributed RWA market share and supports around 846 tokenization projects,

The chain has become the leading settlement layer for institutional issuance, including funds from BlackRock and Franklin Templeton. Insights from BeInCrypto’s Expert Council indicated that institutional preference for Ethereum is less about ideology and more about institutional risk management, comfort, and defensibility.

“I think Ethereum probably wins for the next little while on the back of TradFi getting involved. As banks and other build stuff on blockchain space, it’s almost all going to happen on Ethereum for the next couple of years, I think,” Geoff Kendrick, Global Head of Digital Asset Research at Standard Chartered, told BeInCrypto.

Kendrick expects Ethereum to win the bulk of TradFi flows over the next couple of years.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post JPMorgan Picks Ethereum Again in New Money Market Fund Filing appeared first on BeInCrypto.

Crypto World

Solana price retreats from $100 after rejection, will upcoming SMA crossover trigger rebound?

Solana price pulled back on Monday after facing rejection near the key $100 psychological level, though traders continue watching a potentially bullish moving average crossover that could support another upside attempt.

Summary

- Solana price pulled back toward $95 after facing rejection near the key $100 psychological resistance zone.

- SOL continues trading above its 20-day, 50-day, and 100-day SMAs, with a bullish crossover now approaching.

- A breakout above $100 could open the door toward the $112–$115 region, while $85 remains key support.

According to data from crypto.news, Solana (SOL) traded around $95 at press time on May 12 after briefly climbing as high as $97.6 earlier in the session. The token remains up sharply from its April lows near $80 despite the latest rejection from the upper resistance zone.

The recent cooldown comes as broader crypto market sentiment weakened following Bitcoin’s retreat below the $82,000 level amid rising geopolitical uncertainty tied to renewed U.S.-Iran tensions. Risk appetite across altcoins also softened after investors began locking in profits from last week’s rally.

Despite the pullback, Solana continues to show signs of improving technical structure after reclaiming several important moving averages over the past two weeks.

Market sentiment around the Solana ecosystem has also remained relatively stable as on-chain activity gradually recovers. While decentralized application volumes remain below peak levels seen earlier this year, network usage and validator participation have stopped deteriorating at the same pace witnessed during the first quarter correction.

At the same time, derivatives positioning has started improving modestly, with futures activity stabilizing after weeks of subdued participation. Traders now appear focused on whether Solana can establish support above the mid-$90 region before another breakout attempt toward $100.

Solana price analysis

On the daily chart, Solana recently broke above the important resistance cluster near $92 before rallying toward the $97–$100 region, where sellers quickly stepped back in.

However, the broader structure still appears constructive as SOL continues trading above its 20-day, 50-day, and 100-day simple moving averages, which are now tightly compressed between roughly $85 and $88. The close convergence between these moving averages often signals that momentum is preparing for a larger directional move.

Notably, the 20-day SMA is now approaching a bullish crossover above the 50-day SMA, which could strengthen short-term bullish momentum if confirmed over the coming sessions.

The Supertrend indicator has also flipped green for the first time since January, suggesting that buyers may gradually be regaining broader trend control after months of bearish pressure.

Still, the higher timeframe trend remains somewhat cautious as Solana continues trading below its downward-sloping 200-day SMA near the $113 region, which remains a major long-term resistance barrier overhead.

If bulls manage to reclaim momentum and push above the recent high near $97, the next major upside target could emerge at the psychological $100 level. A successful breakout above that region may then open the door toward the $112–$115 resistance area near the 200-day SMA.

On the downside, failure to hold above the moving average cluster near $85–$88 could weaken the bullish setup and potentially trigger a pullback toward the $80 support region, where buyers previously stepped in aggressively.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

BlackRock has filed a second Securitize‑powered tokenized fund with the SEC, signaling BUIDL’s $2.3B success is becoming a repeatable on‑chain RWA product line, not a pilot.

Summary

- BlackRock has submitted a new tokenized fund application to the SEC, again tapping Securitize as its on-chain infrastructure partner, marking the asset manager’s second move into the tokenized fund space.

- The filing builds on the success of BUIDL, BlackRock’s first Securitize-powered tokenized fund launched in 2024, which has grown to roughly $2.3 billion in assets under management.

- The new application signals that BlackRock is treating tokenized funds as a repeatable product line rather than a one-off experiment, accelerating the broader race among traditional asset managers to bring regulated on-chain investment products to institutional clients.

BlackRock has filed a new tokenized fund application with the U.S. Securities and Exchange Commission, once again choosing Securitize as the infrastructure provider, according to reporting by The Defiant. The filing has not yet been approved, and details on the fund’s target asset class, chain deployment and fee structure remain limited in the public record, but the move confirms that the world’s largest asset manager — overseeing more than $11.5 trillion in assets — is moving from pilot to product line in the tokenized fund space.

The new application leans on a relationship that has already produced one of the most successful tokenized fund launches in history. BlackRock and Securitize co-launched BUIDL, the BlackRock USD Institutional Digital Liquidity Fund, in March 2024 on Ethereum, initially targeting accredited investors with a $5 million minimum and a focus on short-term U.S. Treasury exposure. BUIDL has since grown to approximately $2.3 billion in assets, making it the largest tokenized Treasury fund globally and the clearest proof point that institutional demand for on-chain, yield-bearing dollar instruments is real and scalable.

Securitize, which serves as BUIDL’s transfer agent and tokenization platform, has built its business around being the regulated middleware between traditional fund structures and public blockchains. The firm is registered with the SEC as a transfer agent and operates a broker-dealer, giving it the compliance infrastructure that large asset managers need before they can list tokenized products to institutional clients. By returning to Securitize for a second filing, BlackRock is effectively endorsing that compliance stack as fit-for-purpose and signaling that it does not intend to build its own on-chain fund infrastructure from scratch.

Tokenized funds as a product line, not a pilot

The broader context matters here. BlackRock’s second filing arrives as the tokenized asset market is accelerating across multiple fronts simultaneously. A recent crypto.news story on Ondo Finance’s tokenized stock bridge detailed how the RWA tokenization market has scaled past $1.5 billion in TVL for equities alone, while a separate story on DTCC’s tokenized securities platform showed how post-trade infrastructure giants are now building the settlement rails that would make multi-billion-dollar tokenized fund flows operationally viable at scale.

For BlackRock, the strategic logic of a second tokenized fund is straightforward: BUIDL proved the model works for short-duration Treasury exposure, and a second product allows the firm to test a different asset class, duration profile or investor base on the same regulatory and technical architecture. The move also puts competitive pressure on Franklin Templeton, whose BENJI tokenized money market fund was an early BUIDL rival and whose XRPZ ETF recently led XRP spot inflows, and on Fidelity and State Street, both of which have filed or hinted at tokenized product ambitions of their own.

At a policy level, the filing lands in the same week that the CLARITY Act is heading to Senate Banking Committee markup and the White House is pushing for Trump to sign a crypto market structure bill before July 4, a convergence that turns BlackRock’s SEC submission into more than a routine product launch. As a crypto.news story on BNY’s Abu Dhabi digital asset custody expansion illustrated, the largest names in traditional finance are no longer hedging their blockchain bets — they are building production infrastructure and filing with regulators, treating tokenization as the next decade’s core product category rather than an emerging technology experiment.

JPMorgan Chase has filed with the U.S. Securities and Exchange Commission to launch a tokenized money market fund on Ethereum. The vehicle aims to hold reserves backing stablecoins in a regulated, cash-like structure while earning interest for investors.

The OnChain Liquidity-Token Money Market Fund, ticker JLTXX, would invest in US Treasury bills and overnight repurchase agreements collateralized by US Treasuries or cash, according to the SEC filing. The fund is designed to comply with the GENIUS Act, a stablecoin-focused law signed in July.

Investors would face a $1 million minimum investment, and the fund carries a 0.16% annual fee after waivers. JPMorgan’s blockchain unit, Kinexys Digital Assets, would manage the strategy. The filing indicates the regulatory filing becomes effective on Wednesday, though a formal launch date was not disclosed.

Tokenization has drawn increasing attention from Wall Street executives in recent months, who see on-chain structures as potentially improving the efficiency of trading and settlement compared with traditional systems. Data from RWA.xyz shows more than $32.2 billion of real-world assets tokenized on-chain, excluding stablecoins, across asset classes such as commodities, equities, bonds, and real estate. The platform notes that nearly every major asset class has been tokenized to some degree.

Bloomberg analyst Eric Balchunas described JPMorgan’s JLTXX as a “big deal” due to its 0.16% fee for a money market fund with a stable asset value, highlighting the potential for cost-efficient on-chain reserve management.

Key takeaways

- JPMorgan is pursuing a regulated, cash-like tokenized money market vehicle on Ethereum to back stablecoin reserves, via the JLTXX fund.

- The fund targets a 0.16% annual fee after waivers, a historically low fee for stable-value money market products, according to market commentary.

- The project aligns with the GENIUS Act, signaling ongoing regulatory engagement with tokenized financial assets and stablecoin ecosystems.

- This filing follows JPMorgan’s broader tokenization experiments, including the MONY product and related blockchain experiments, underscoring a continuing corporate push into tokenized yields.

- The momentum in asset tokenization is evidenced by industry data showing hundreds of billions in real-world assets on-chain, while regulators warn about risks around ownership clarity, settlement finality, and market fragmentation.

JPMorgan’s tokenization playbook expands

The JLTXX filing adds to JPMorgan’s growing roster of blockchain-enabled products. The bank’s earlier tokenized offering, the My OnChain Net Yield Fund (MONY), launched in December and also operates on Ethereum. MONY holds short-term debt securities intended to deliver returns that exceed typical bank deposit rates, with interest and dividends accruing daily. The SEC filing for JLTXX suggests an intent to broaden the range of on-chain, cash-like investment options available to stablecoin issuers and other on-chain actors seeking regulated yield.

In a related development, JPMorgan participated in a pilot transaction last week that demonstrated the movement of a tokenized US Treasury fund from the United States to a JPMorgan account in Singapore. The transfer leveraged XRP Ledger and interbank rails to complete in seconds, illustrating how tokenized assets can traverse traditional borders with improved settlement speed.

Industry peers have also advanced tokenized reserve strategies. In April, Morgan Stanley unveiled the Stablecoin Reserves Portfolio, a facility allowing stablecoin issuers to park reserves in a bank money market fund and earn interest. The juxtaposition of these initiatives underscores a broader trend: financial institutions experimenting with on-chain representations of real-world assets to enhance liquidity, yield, and settlement efficiency.

Regulatory and market context

While the rapid pace of tokenization activity attracts bullish sentiment around efficiency gains, major international bodies have sounded cautions. The International Monetary Fund, in a recent report, warned that tokenization can shift certain risk exposures from traditional banking systems to shared ledgers and smart-contract code, complicating interventions during stress events. The IMF stressed that without clear legal ownership records and settlement finality, tokenized markets risk becoming fragmented or peripheral.

Industry observers remain attentive to governance and legislative developments designed to address these gaps. Prominent voices, including investor Kevin O’Leary, have argued that comprehensive crypto market-structure legislation—often discussed under frameworks like the CLARITY Act—will be necessary to clarify ownership, settlement, and regulatory expectations as tokenized finance evolves.

Beyond regulatory framing, the market is watching how tokenized assets scale. The RWA.xyz data cited above indicates substantial on-chain tokenization across asset classes, suggesting meaningful adoption potential. Yet observers emphasize that standards, interoperability, and robust risk controls will determine whether these tokenized vehicles can become mainstream tools for investors, stablecoin issuers, and financial institutions alike.

Source material and context for these developments reflect filings with the SEC, industry commentary, and market data aggregators tracking tokenized real-world assets and cross-border settlement initiatives. The evolution of JPMorgan’s on-chain offerings, alongside peers’ initiatives, points to a broader shift in how traditional finance interfaces with blockchain-enabled infrastructure.

As the JLTXX filing moves through regulatory review, market watchers will be keen to see whether the fund gains a launch timeline, how its reserve strategy performs in varying market regimes, and what additional tokenized products emerge to complement on-chain yield and liquidity solutions.

What remains uncertain is how rapidly stablecoin issuers will adopt on-chain reserve vehicles at scale and how policymakers will balance innovation with resilience and investor protection. The coming months will indicate whether JPMorgan’s approach signals a durable path toward on-chain money markets or if regulatory and technical hurdles will slow the rollout.

Dogecoin sits near $0.195, 70% below its 2025 peak, as altseason signals from SUI and ETH collide with Musk‑driven sentiment and a fragile path toward the $0.50 level.

Summary

- Dogecoin is trading around $0.195, down roughly 70% from its 2025 peak, even as altseason momentum and rising open interest across the top-10 begin to suggest a broader rotation out of Bitcoin dominance.

- SUI’s 31% single-day surge to $1.40 and Ethereum’s push toward a “parabolic” breakout on some timeframes are being cited on Crypto Twitter as early altseason signals that historically precede DOGE’s most explosive moves.

- Elon Musk’s continued dominance of X — now a tradeable data point on Polymarket’s tweet-count markets — keeps Dogecoin tied to one of crypto’s most unpredictable sentiment catalysts, even as its on-chain fundamentals slowly mature.

Dogecoin (DOGE) is currently trading around $0.195, a level that places it roughly 70% below the $0.65 peak it reached during the 2025 rally and well below the $0.50 psychological threshold that permabulls have flagged as the first real target in any sustained recovery. The drawdown is steep even by crypto standards, but it is also consistent with DOGE’s historical pattern: the token tends to underperform Bitcoin and large-cap altcoins for extended periods before compressing years of gains into weeks of vertical price action when sentiment flips.

That sentiment flip may be starting to take shape elsewhere in the market. A previous crypto.news story on SUI’s 31% single-session surge to $1.40 noted how open interest across derivatives venues jumped from roughly $450 million to over $620 million in a single day as traders rotated into high-beta altcoins following a supply shock from Nasdaq-listed SUI Group Holdings. That kind of move — a top-10 token exploding on a combination of fundamental catalyst and short squeeze — is exactly the precursor pattern that has historically preceded broader DOGE runs, as capital flows down the risk curve from large-caps to mid-caps and eventually into meme coins once speculative appetite is fully engaged.

Ethereum is adding another data point. Analysis circulating on X describes ETH as forming a “parabolic” breakout structure on the weekly chart, with Ethereum’s recent upgrade roadmap — detailed in a crypto.news story on the Glamsterdam devnet going live and the Hegotá scalability roadmap advancing — giving the second-largest asset a fundamental narrative to match its technical setup. When ETH leads, DOGE has historically followed with a lag of days to weeks, as retail traders who miss the Ethereum move look for the next high-leverage, high-beta play with name recognition and exchange liquidity.

The Musk variable and the road back to $0.50

No DOGE forecast is complete without addressing Elon Musk, and in May 2026 that variable is stranger than ever. As covered in a recent crypto.news story on Polymarket’s Elon Musk tweet-count contracts, Musk’s posting behavior is now literally a tradeable market, with millions of dollars wagered on whether he will post between 100 and 139 times in a given week. That financialization of Musk’s X activity is a two-edged sword for DOGE: it keeps him in the daily conversation of crypto traders, maintaining the ambient association between Musk and Dogecoin that has driven some of the token’s most violent pumps, but it also means any single pro-DOGE tweet now lands in a market that is already pricing his behavior probabilistically rather than reacting to it as a pure surprise.

On the fundamental side, DOGE’s case for a recovery is thin but not nonexistent. Daily transaction counts on the Dogecoin network have held above 50,000 in recent months even during the price drawdown, and the token continues to be accepted as payment by a small but growing list of merchants enabled through integrations that X’s payments infrastructure could eventually formalize. None of that is a near-term price catalyst on its own, but it does mean DOGE is not quietly dying during the bear phase — it is maintaining a baseline of utility that gives it a platform to rally from when conditions improve.

The price prediction range most consistent with the current setup runs something like this: in a base case where altseason continues to build off SUI and ETH momentum but does not fully ignite, DOGE could push toward $0.25 to $0.30 in the next four to six weeks as Bitcoin consolidates above $80,000 and capital continues rotating. In a bull case where the CLARITY Act passes committee this week, the stablecoin bill clears the House on May 14, and Bitcoin makes a clean break above $90,000, DOGE has historically traded at roughly 0.25% to 0.30% of Bitcoin’s price at peak altseason euphoria — a ratio that would put it between $0.225 and $0.27 at current BTC levels, and closer to $0.45 to $0.54 if Bitcoin reaches $150,000 to $180,000 by end of year in the most optimistic scenario. The bear case — a Wyckoff retest pulling Bitcoin back toward $60,000 and open interest liquidations cascading through altcoins — could drag DOGE back toward $0.12 to $0.14, erasing most of the recovery from last year’s lows and resetting the base for a later, larger move.

Coinbase now lets users borrow up to $100K against SOL via Morpho on Base, turning Solana into its third major collateral pillar as the token eyes a retest of $200.

Summary

- Coinbase has added Solana as a supported collateral asset in its on-chain lending product, letting users borrow up to $100,000 against SOL holdings via the Morpho protocol on Base, expanding a service that has already issued over $2.3 billion in cumulative loans.

- Bitcoin dominates Coinbase’s lending book with $2.17 billion in cumulative collateralized loans, followed by ETH at $110 million and XRP at $31.6 million, with SOL now joining that roster as Coinbase pursues its “Everything Exchange” strategy.

- The SOL addition lands despite Coinbase reporting a $394.1 million net loss in Q1 and cutting roughly 14% of its workforce, with CEO Brian Armstrong maintaining that “all finance will migrate on-chain” and multiple Wall Street desks keeping buy ratings on COIN stock.

Coinbase has expanded its on-chain crypto lending product to include Solana as collateral, allowing users to borrow up to $100,000 against SOL holdings through an integration with the Morpho lending protocol on the Base network, according to reporting by The Block.

Coinbase bets on SOL as its third major collateral pillar

The product previously supported Bitcoin and Ethereum as collateral assets, and the SOL (SOL) addition marks the first time a major non-BTC, non-ETH Layer 1 has been added to Coinbase’s lending stack, reflecting the exchange’s assessment that Solana has reached the liquidity depth and institutional acceptance needed to function as reliable loan collateral.

Ben Shen, Coinbase’s Head of Financial Services and Loyalty Products, framed the move explicitly around platform strategy, saying the addition of SOL collateral is “an important step for Coinbase to become the best platform for trading and holding Solana” and that it reflects the company’s broader push to build an “Everything Exchange” — a single venue where users can trade, hold, earn, borrow and settle across any major asset without leaving the Coinbase ecosystem. Since launching its crypto lending product last year, Coinbase has issued more than $2.3 billion in cumulative loans, with Bitcoin accounting for $2.17 billion of that total, ETH at roughly $110 million and XRP at $31.6 million, followed by smaller positions in cbETH, DOGE, ADA and LTC.

SOL is currently trading around $171, having pulled back from highs above $260 earlier in the cycle, and sits in a market where the addition of a major exchange’s collateral lending service has historically acted as a mild but persistent price support: users who might otherwise sell SOL to raise dollar liquidity can instead borrow against their position, reducing spot sell pressure while keeping exposure intact. That dynamic has been well-documented in Bitcoin’s lending market, where the growth of BTC-collateralized loans is cited as one structural reason why long-term holders have been able to extract liquidity without triggering the kind of forced selling that characterized earlier cycles.

“Everything Exchange” strategy survives a $394M quarterly loss

The SOL lending launch arrives in the same news cycle as Coinbase’s Q1 earnings disclosure, which showed a net loss of $394.1 million and a workforce reduction of approximately 14%. Those numbers reflect a broader revenue compression from lower trading volumes and the cost of Coinbase’s aggressive product expansion, but CEO Brian Armstrong has been consistent in framing near-term losses as the price of building infrastructure for what he calls the inevitable migration of “all finance on-chain.” Institutional analysts appear to agree with that framing: Bernstein, Benchmark and Rosenblatt have all maintained buy ratings on COIN stock, with Bernstein specifically noting that Coinbase is “gradually validating the feasibility of its Everything Exchange strategy” through cumulative data points like $2.3 billion in loans issued and the UK market expansion completed last month.

For Solana’s price trajectory, the Coinbase lending integration is one of several institutional signals converging this week. Huma Finance’s V2 PayFi platform, detailed in a recent crypto.news story, is built on Solana and recently survived a legacy Polygon exploit that underlined the architectural superiority of its Solana-native rebuild. Meanwhile, a crypto.news story on SUI’s 31% single-session surge showed how supply shocks and new institutional products can compress months of sideways price action into days of vertical movement for high-liquidity Layer 1 tokens.

At roughly $171, SOL would need a 17% move to retest $200 — a level it held briefly in early 2026 before the broader market correction — and a 52% recovery to challenge its cycle high above $260. The Coinbase collateral addition does not by itself generate that kind of move, but it does remove one structural friction point by giving large SOL holders a dollar-liquidity option that does not require selling, and it extends Coinbase’s institutional credibility to Solana in the same way that BTC and ETH lending helped normalize those assets as balance-sheet instruments. Combined with the altseason rotation signals flagged in a separate crypto.news story on Tuesday’s top-100 movers, a clear break above $180 to $185 in the near term looks more achievable than it did before Coinbase put SOL on the same collateral shelf as Bitcoin.

Coinbase CEO Brian Armstrong said the CLARITY Act gave banks their must-haves as the Senate released its 309-page bill text.

Summary

- Senate Banking Committee Chairman Tim Scott released the 309-page CLARITY Act substitute text on May 12, scheduling a markup for May 14.

- Brian Armstrong said in an X livestream that not everyone got everything they wanted, but the core priorities were preserved in the bill.

- Five major US banking groups jointly rejected the stablecoin yield compromise on the eve of the markup, calling the deal insufficient.

The Senate Banking Committee released the 309-page substitute text of the CLARITY Act on May 12, setting a committee markup for May 14 at 10:30 am. The bill defines which digital assets fall under the SEC and which belong to the CFTC, a question the US crypto industry has been pushing Congress to answer for years.

Coinbase CEO Brian Armstrong said in an X livestream on May 12 that the compromise preserved the industry’s core asks. “Not everyone got everything they wanted, but they got the must-haves,” he said, adding that Coinbase is working with at least five of the largest global banks on crypto integration.

Why banks are still pushing back

Five major banking groups, including the American Bankers Association and the Bank Policy Institute, issued a joint statement rejecting the stablecoin yield compromise brokered by Senators Thom Tillis and Angela Alsobrooks. The groups argued that Section 404 of the bill still permits yield-like rewards that compete with bank deposits.

“Research demonstrates that yield-earning stablecoins could reduce all consumer, small-business, and farm loans by one-fifth or more,” the coalition said. The compromise bans passive yield paid solely for holding stablecoins while permitting activity-based rewards tied to payments and platform use.

Senator Cynthia Lummis responded on X that the finalized text is “the culmination of months of hard work.” Senator Tillis went sharper, warning that certain factions in traditional finance may simply oppose any version of the CLARITY Act and are using the yield debate to stall it entirely.

The stakes around the May 14 markup

The CLARITY Act cleared the House 294 to 134 in July 2025 and passed the Senate Agriculture Committee in January 2026. The Banking Committee markup is the next required step before a full Senate floor vote, which needs 60 votes to advance.

Senators Lummis and Bernie Moreno have both warned that missing the May 21 Memorial Day recess window risks pushing comprehensive crypto legislation off the calendar entirely. Prediction markets currently price the bill’s odds of becoming law in 2026 at over 60%. The White House has set a July 4 target for a presidential signature.

The U.S. Senate is turning its attention to the Digital Asset Market Clarity Act (CLARITY) as an anticipated Thursday markup approaches, with lawmakers weighing a text that broadens the framework for crypto market structure while surfacing questions about unrelated policy provisions. The version released by three Republican senators—marking what they say is a product of ongoing negotiations with Democratic colleagues—follows earlier drafts from mid-2025 and represents a step in recent intensive discussions over stablecoin yield and market structure governance.

According to the U.S. Senate Banking Committee release, the text will guide committee deliberations on how digital assets are supervised and regulated in the broader financial system. The bill’s release came after negotiations that extended into fall 2025, with lawmakers signaling bipartisan momentum for a markup on the measure. In parallel, some Democrats have pressed for accompanying ethics provisions to address conflicts of interest, linking the crypto policy debate to wider concerns about governance and integrity in financial legislation. As reported, the dynamics remain delicate, with discussions framed by a balance between industry structure, investor protections, and legislative oversight.

Notably, the final pages of the draft contain a housing policy element—the Build Now Act—that would create a pilot program intended to incentivize housing development within select Community Development Block Grant participating jurisdictions. This inclusion has surprised some observers, given that the core text centers on market structure for digital assets rather than housing, and has sparked questions about Senate Democrats’ appetite for attaching broader policy measures to crypto legislation. The section-by-section summary indicates the housing provisions are designed to pilot development initiatives, which could influence the overall legislative package and its political reception.

Senators Tim Scott, Cynthia Lummis, and Thom Tillis have portrayed the text as a product of ongoing bipartisan talks with their Democratic colleagues, signaling a readiness to move toward a markup on Thursday. Yet, in public comment, some Senate Democrats, including Kirsten Gillibrand, have urged that the bill not reach the floor without explicit ethics language addressing potential conflicts of interest. The tension was summarized by party-line perspectives and positioned to shape the upcoming procedural path for CLARITY.

“We have worked too hard on this bill to give up now,” said Senator Angela Alsobrooks, who sits on the banking committee and helped broker a stablecoin yield compromise with Tillis. “My hope is to get to a bipartisan markup on Thursday with a compromise on ethics.”

In the broader policy conversation, the CLARITY Act is frequently described as a vehicle to clarify and potentially expand the Commodity Futures Trading Commission’s (CFTC) oversight role in the digital-asset space, a shift often discussed in relation to where the Securities and Exchange Commission (SEC) would or would not have jurisdiction. The legislative journey has included prior committee activity—most notably, the Senate Agriculture Committee’s January markup advancing its version of the bill—but full passage remains contingent on Banking Committee action, Senate floor votes, and eventual reconciliation with the House of Representatives. The cross-chamber process mirrors the complexity of other crypto-related legislation, including past bipartisan outcomes on related measures such as stablecoin infrastructure and cross-border policy alignment.

Key takeaways

- The CLARITY Act text has been released ahead of a scheduled Senate Banking Committee markup, signaling renewed bipartisan engagement on digital-asset market structure and regulatory oversight.

- A housing-related provision—the Build Now Act—appears in the later pages of the draft, introducing a pilot program to incentivize housing development in certain Community Development Block Grant jurisdictions. The policy’s inclusion in a crypto bill raises questions about legislative scope and sequencing.

- The bill explicitly prohibits paying interest or yield on payment-stablecoins, with narrow exceptions for bona fide activities or transactions that are not economically or functionally equivalent to interest-bearing deposits. This provision directly shapes how stablecoin models may be structured or marketed in the United States.

- Provisions drawn from the Blockchain Regulatory Certainty Act aim to shield software developers from traditional money-transmitter requirements, a topic closely watched by DeFi and open-source development advocates.

- Advocacy and enforcement dynamics center on the balance between empowering the CFTC and maintaining appropriate guardrails. Ethic provisions remain a point of contention among lawmakers, with some Democrats insisting on clear ethics language before advancing.

- The overall legislative path remains complex: Agriculture Committee approval has occurred, but the Banking Committee, Senate floor, and House reconciliation are still prerequisites for any final enactment. Previous crypto measures have demonstrated that bipartisan support can be achievable but not guaranteed on procedural or policy grounds.

CLARITY Act: structure, scope, and regulatory intent

At its core, the CLARITY Act seeks to redefine regulatory posture for digital assets by clarifying which agency takes primary supervisory responsibility and by spelling out market-structure rules that would govern issuance, trading, and settlement of crypto instruments. A central element, as outlined in the text, is a prohibition on paying interest or yield on payment stablecoins. The prohibition is not absolute, however; the text allows incentives or rewards that are based on bona fide activities or bona fide transactions and that are not economically or functionally equivalent to paying interest on an interest-bearing bank deposit. The structure of this prohibition will influence how stablecoins are designed and marketed, potentially shaping issuer strategies and user expectations for on-chain payments and settlements.

In addition, the bill incorporates language from the Blockchain Regulatory Certainty Act, a provision designed to shield developers of blockchain software from being treated as money transmitters under existing statutes. This element is of particular interest to DeFi ecosystems and other open-source projects, which have long argued that broad money-transmitter designations could chill innovation. Proponents argue that such protection helps maintain near-term operational viability for developers while still enabling appropriate regulatory oversight over the broader ecosystem.

Regulatory and enforcement implications extend beyond the CFTC’s jurisdictional purview. The measure is framed in a way that could influence how responsible actors—exchanges, issuers, and liquidity providers—structure products, comply with AML/KYC requirements, and interact with banking partners. The plan to tilt certain supervisory responsibilities toward the CFTC reflects ongoing debates about investor protection versus innovation, a dynamic that has repeatedly surfaced in discussions around MiCA-equivalent regimes and U.S. market architecture.

As part of the broader policy conversation, a number of lawmakers and advocacy groups have highlighted the need for practical guardrails. The DeFi Education Fund, for example, pointed to the software-developer protections as a meaningful step toward reducing friction for compliant developers. In public commentary, the organization noted that the protections align with a pragmatic approach to innovation while maintaining a clear regulatory boundary. The latest bill text and public discussion suggest a cautious but constructive path toward balancing innovation with supervisory clarity.

Ethics, governance, and the partisan friction

The ethics dimension remains a live issue in the currency of policy negotiations. Democrats have pressed for explicit ethics provisions to address potential conflicts of interest, a concern intensified by high-profile political discussions around cryptocurrency ventures connected to public figures and their families. The absence of ethics language in the released draft has drawn criticism from some quarters. Massachusetts Senator Elizabeth Warren publicly criticized the bill, arguing that it could undermine investor protection and national financial security by not addressing ethics standards. The exchange highlighted how the crypto policy debate intersects with broader governance concerns and national policy priorities.

On the other hand, proponents emphasize a pragmatic, bipartisan approach to market structure. Senator Scott, Senator Lummis, and Senator Tillis have framed the text as a product of ongoing negotiations with Democratic colleagues, signaling a potential path to bipartisan markup. As one takeaway, the willingness to consider a stablecoin-yield compromise with Senate Democratic leadership suggests a broader readiness to reconcile technical governance with concerns about conflicts of interest. The ongoing discussion underscores the delicate balance between advancing a cohesive regulatory framework and accommodating divergent views on ethics and governance.

In the political dynamics of the process, the Agriculture Committee’s January approval and the potential for a 60-vote threshold in a full Senate passage scenario are key procedural realities. The experience of earlier crypto legislation—such as the GENIUS Act, which passed the Senate with broad bipartisan support—demonstrates that consensus is possible but not guaranteed, especially when ethics and governance topics are front and center. Observers will be watching how Thursday’s markup addresses these policy tensions and whether a bipartisan compromise can survive to final passage.

For institutions and market participants, the evolving regulatory posture around CLARITY has practical implications. Compliance teams must monitor potential shifts in supervisory expectations—particularly any transition of primary oversight responsibilities to the CFTC—and assess how these changes could affect licensing, registration, and ongoing reporting requirements. Banks and payment networks, in turn, will need to align risk management and customer due diligence with a regime that may differentiate between stablecoin models and other digital assets, while also contemplating cross-border regulatory differences that may arise in analogous regimes abroad, such as MiCA in the European Union.

As observed, the text also implies ongoing considerations about stablecoin design, product rhetoric, and the permissible nature of yield-like features. The prohibition on paying yield on stablecoins, coupled with permitted bona fide activity-based rewards, may influence issuer business models, token utility, and marketing practices. These design constraints have direct consequences for liquidity providers, custodians, and wallet providers, all of whom must maintain alignment with evolving regulatory interpretations and enforcement expectations.

Regulatory context and what comes next

The CLARITY Act sits at the intersection of U.S. regulatory modernization efforts and evolving global frameworks for digital assets. Its progression touches on issues central to MiCA-like regimes, potential SEC/CFTC jurisdiction delineations, and the broader policy objective of preventing illicit finance while enabling legitimate financial innovation. Regulators and market participants alike are watching closely for how the bill’s structure could influence cross-border activity, licensing regimes, and the calculus of risk for institutions seeking to participate in regulated digital-asset markets.

To move from proposal to law, the bill must pass through the Banking Committee, clear the full Senate, and be reconciled with a version from the House of Representatives before any presidential sign-off. The legislative timeline remains uncertain, with procedural hurdles and political considerations continuing to shape the pace and substance of crypto regulation.

For now, the latest draft represents a meaningful consolidation of several policy threads: a clearer regulatory boundary for stablecoins, enhanced protections for developers, and a continued emphasis on market structure oversight. As coverage and commentary continue, observers should monitor not only the substantive provisions but also the ethics framework that many policymakers view as essential to a credible, sustainable regulatory regime. This frame is critical for institutions seeking to align operations with evolving rules and for analysts assessing the potential long-term impact on innovation, risk management, and financial stability.

As Cointelegraph observed in coverage surrounding the markup discussions, the ethics dimension and bipartisan dynamics will likely shape Thursday’s proceedings and the ultimate trajectory of CLARITY. The ongoing debate reflects a broader inquiry into how best to harmonize investor protection, regulatory clarity, and innovation in the United States’ rapidly evolving digital-asset landscape. See the committee’s posted text and related materials for the latest details and official documentation.

Related reporting and commentary continue to illustrate the evolving stance of lawmakers toward crypto market structure, ethics governance, and the role of regulators in a shifting financial ecosystem. For context, coverage of reactions, amendments, and subsequent developments remains essential for compliance and policy teams tracking regulatory risk and strategic planning in this space. Additionally, institutional readers may find it useful to benchmark these developments against existing or proposed international standards and cross-border policy initiatives.

Source notes and further reading: the text and summary materials linked by the Senate Banking Committee; press commentary on bipartisan negotiations and ethics considerations; coverage of related legislation and committee actions; and industry commentary on software developer protections and market structure considerations. For broader context, analyses and updates from specialized outlets continue to shape the interpretation of CLARITY’s regulatory implications.

Crypto World

Polygon CDK Unveils Institutional-Grade Privacy Chains With Full Access to Global Liquidity

TLDR:

- Polygon CDK’s validium config keeps raw transaction data sealed within institution-owned infrastructure.

- Settlement on Ethereum uses only a cryptographic commitment and a ZK proof, never exposing transactions.

- Five composable privacy levels let institutions scale confidentiality without migrating between configurations.

- Private CDK chains connect to Agglayer, preserving access to Ethereum, multi-chain liquidity, and fiat ramps.

Polygon CDK has announced a new privacy configuration for institutions building custom blockchains on its technology stack.

The upgrade keeps raw transaction data inside institution-owned infrastructure. At the same time, chains built on the configuration retain open access to global liquidity networks.

Powered by Succinct Labs’ SP1 Hypercube proving system, only a cryptographic commitment and a zero-knowledge proof settle to Ethereum.

The configuration primarily targets banks, payments companies, and asset managers that are moving onchain.

How the Privacy Configuration Works

Polygon CDK now offers a validium configuration developed in partnership with Succinct Labs. Transaction data stays within an institution-operated data availability environment.

Raw transaction data never reaches a public network. Ethereum receives only a cryptographic fingerprint and a validity proof for settlement.

The SP1 Hypercube proving system is already live in production on Katana Network. Settlement relies on validity proofs rather than a trusted operator with data access.

This approach means no single party holds visibility into the institution’s transaction data. The chain is verified publicly, but its transaction contents remain confidential.

@0xPolygon stated: “Ethereum confirms the chain is operating correctly. It never sees the transactions.” Role-based controls gate RPC endpoints and block explorers through enterprise systems like Okta and Azure AD. Policies apply at the contract and function level. Counterparties view only their own transactions.

Auditors receive scoped read access, while regulators get selective disclosure capabilities. Chain operators, by contrast, retain full visibility over all chain activity.

Even operational metadata — block contents, transaction counts, gas usage — can stay private. Institutions ultimately control what information is shared and with whom.

Five Privacy Levels and Cross-Chain Liquidity

Polygon CDK gives institutions five composable privacy levels with no migration required. The base level covers permissioned access through role-based RPC and private block explorers.

The newest tier is the confidential chain, keeping data within institution-owned infrastructure. A third level adds trusted execution environments for sealed workloads like dark-pool matching and sealed-bid auctions.

The fourth level applies fully homomorphic encryption to permissioned token rails. Balances and transfer amounts stay encrypted onchain throughout.

Apex Group’s T-REX Ledger with Zama on ERC-3643 already demonstrates this in production. The fifth level uses client-side zero-knowledge proofs through Hinkal to shield wallet-layer transactions from onchain visibility.

Despite the privacy architecture, Polygon CDK chains stay connected to Agglayer. Through this layer, private chains can access Ethereum, other L1s and L2s, and non-EVM networks like Miden.

A regional bank can settle with counterparties on other chains. Fiat ramps and stablecoin liquidity remain accessible through the Open Money Stack.

Target institutions include banks launching tokenized deposits and payments companies building stablecoin corridors. Asset managers issuing tokenized funds and crypto-native teams requiring enterprise SLAs also qualify.

Each deployment remains subject to applicable laws and regulations. Institutions can start at one privacy level and expand from there.

Nancy Guthrie's friend pleads for answers 100 days into her disappearance: 'It shouldn't take this long'

Women’s T20 World Cup: Sophie Molineux passed fit as Australia name squad

South Korea Floats ‘Citizen Dividend’ Using AI Profits

Manchester United reach agreement with Casemiro over contract clause amid transfer speculation

US brings back mandatory military draft registration

Steven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Crypto World5 days ago

Crypto World5 days agoHarrisX Poll Found 52% of Registered Voters Support the CLARITY Act

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: Marianne Dress

-

Crypto World6 days ago

Crypto World6 days agoUpbit adds B3 Korean won pair as Base token gains Korea access

-

NewsBeat6 days ago

NewsBeat6 days agoNCP car park operator enters administration putting 340 UK sites at risk of closure

-

Fashion1 day ago

Fashion1 day agoCoffee Break: Travel Steam Iron

-

Fashion2 days ago

Fashion2 days agoWhat to Know Before Buying a Curling Wand or Curling Iron

-

Tech3 days ago

Tech3 days agoAuto Enthusiast Carves Functional Two-Stroke Engine from Solid Metal

-

Politics1 day ago

Politics1 day agoWhat to expect when you’re expecting a budget

-

Politics4 days ago

Politics4 days agoPolitics Home Article | Starmer Enters The Danger Zone

-

Business4 days ago

Business4 days agoIgnore market noise, India’s long-term story intact, say D-Street bulls Ramesh Damani and Sunil Singhania

-

Crypto World7 days ago

Crypto World7 days agoBlackRock CEO Larry Fink Discusses a New Asset Class

-

Tech2 days ago

Tech2 days agoGM Agrees To Pay $12.75 Million To Settle California Lawsuit Over Misuse Of Customers’ Driving Data

-

Sports7 days ago

Sports7 days agoNBA playoff winners and losers: Austin Reaves is not loving Lakers vs. Thunder matchup, but Chet Holmgren is

-

Entertainment6 days ago

Entertainment6 days agoSarah Paulson Called Out For Met Gala ‘Hypocrisy’

-

Entertainment5 days ago

Entertainment5 days agoGeneral Hospital: Ric & Ava Bombshell – Ric’s Massive Secret Exposed!

-

Politics5 days ago

Politics5 days agoSimon Cowell Says He Was ‘Horrible’ To Susan Boyle During BGT Audition

-

Crypto World6 days ago

Crypto World6 days agoRobinhood says Wall Street is building onchain

-

Entertainment6 days ago

Entertainment6 days agoBold and Beautiful Early Spoilers May 11-15: Steffy Revolted & Liam Overjoyed!

-

Sports6 days ago

Sports6 days agoUEFA Champions League final schedule, teams, venue, live time and streaming | Football News

-

Entertainment6 days ago

Entertainment6 days agoWhy David Letterman Called CBS ‘Lying Weasels’

You must be logged in to post a comment Login