Crypto World

why connectivity will define the next era

In today’s newsletter, Paul Frost-Smith, CEO of Komainu, covers how institutional crypto is converging with traditional finance, but speed can introduce risk if legal and compliance layers aren’t aligned.

Then, in “Ask an Expert,” Sam Boboev, from the “Fintech Wrap Up,” details the key coordination risks institutions must solve for.

Beyond custody: why connectivity will define the next era.

Institutional crypto markets

Institutional adoption of crypto has matured rapidly. The challenge is no longer simply securing assets, but moving and managing them efficiently across a fragmented ecosystem of custodians, exchanges and counterparties. With assets under professional custody now exceeding $200 billion, the inefficiencies of siloed infrastructure have an increasingly material impact on trading, hedging and liquidity management.

Treasury teams often find assets stranded across multiple platforms, creating operational friction that slows trades, constrains intraday liquidity and increases risk exposure. Idle assets tie up capital, amplify counterparty risk and raise the cost and complexity of managing institutional portfolios. In a 24/7 market where speed, execution and real-time visibility matter, the ability to mobilise capital across platforms is no longer optional, it is a prerequisite for scale, efficiency and resilience.

The next phase of market evolution will be defined by connectivity. Platforms that link custody, liquidity and collateral in real time are no longer “nice to have,” they are critical infrastructure. Networked systems enable assets to move faster, collateral to be rehypothecated safely and positions to be adjusted instantly without the delays inherent in siloed setups. Institutions that can leverage integrated infrastructure gain a direct advantage in capital efficiency, risk management and operational agility.

Technologies such as Bitcoin’s Liquid Network illustrate the potential. By combining security, transparency, and near-instant settlement, these networks provide a model for institutions to operate efficiently while mitigating counterparty and operational risk. Assets that are digital-native and programmable can be pledged, transferred and released automatically according to predefined rules, bringing crypto markets closer to the operational standards expected in traditional finance.

The implications are clear. The efficiency and integration of underlying infrastructure directly affect portfolio outcomes. A digital asset’s value is no longer defined solely by its market price; mobility and utility are just as important. Firms that can connect these “pipes” of digital finance gain better liquidity, faster execution and strategic flexibility at scale, enabling them to deploy capital more effectively across trading, hedging and yield-generating activities.

This shift also signals a broader trend, with custody evolving beyond its traditional role. Once synonymous with storage, it now functions as a dynamic, active layer that validates, transfers, and interacts with assets programmatically. Institutional investors evaluating service providers should look beyond security and regulatory compliance to consider the ability to support fast, interconnected and reliable market activity.

Looking ahead, interoperability and network connectivity, not just regulatory clarity, will define which institutions can scale efficiently in crypto markets. Those that build their strategies around connected, integrated infrastructure will be positioned to capitalise on opportunities that siloed competitors cannot.

As institutional participation deepens, the competitive edge in crypto markets will increasingly come from how effectively firms can deploy and mobilise capital. Connectivity, interoperability and real-time collateral mobility will define the infrastructure institutions rely on to trade, hedge and manage risk at scale. Those that prioritise integrated systems today will be better positioned to navigate a market that is becoming faster, more interconnected and more operationally demanding.

– Paul Frost-Smith, CEO, Komainu

Ask an Expert

Q1: What defines the next phase of institutional crypto market structure?

The next phase is defined by convergence with traditional financial infrastructure. Crypto is no longer operating as a parallel system; it is being absorbed into existing institutional frameworks. This shows up in three areas: regulated custody, tokenized financial instruments and stablecoins as settlement rails. Institutions are not adopting crypto for speculation, but for balance sheet efficiency, faster settlement and programmable financial flows. The market structure is shifting from exchange-led liquidity to infrastructure-led integration.

Q2: Where is the real value being created right now?

The value is moving down the stack into infrastructure. Custody, tokenization platforms and stablecoin issuance are becoming the core control points. These layers determine how assets are issued, transferred and settled. Distribution still matters, but control over settlement and asset representation is where defensibility is forming. This is why we are seeing traditional players focus on tokenized money market funds, on-chain repo and institutional-grade stablecoins.

Q3: What are the key risks institutions need to solve for?

The primary risk is not volatility, but coordination across legal, technical and operational layers. Tokenized assets can settle instantly, but ownership rights, compliance rules and jurisdictional enforcement still operate off-chain. This creates a structural mismatch. Institutions need systems where the ledger, compliance logic and legal frameworks are aligned. Without that, speed introduces risk rather than efficiency.

– Sam Boboev, founder, Fintech Wrap Up

Keep Reading

- Bitcoin enters the public bond market as Moody’s gives a first-of-its-kind crypto deal a rating.

- Franklin Templeton is launching a dedicated cryptocurrency division, Franklin Crypto, anchored by its planned acquisition of crypto investment firm 250 Digital.

- Australia has passed its first comprehensive crypto law, requiring exchanges and custody platforms to obtain financial services licenses within six months.

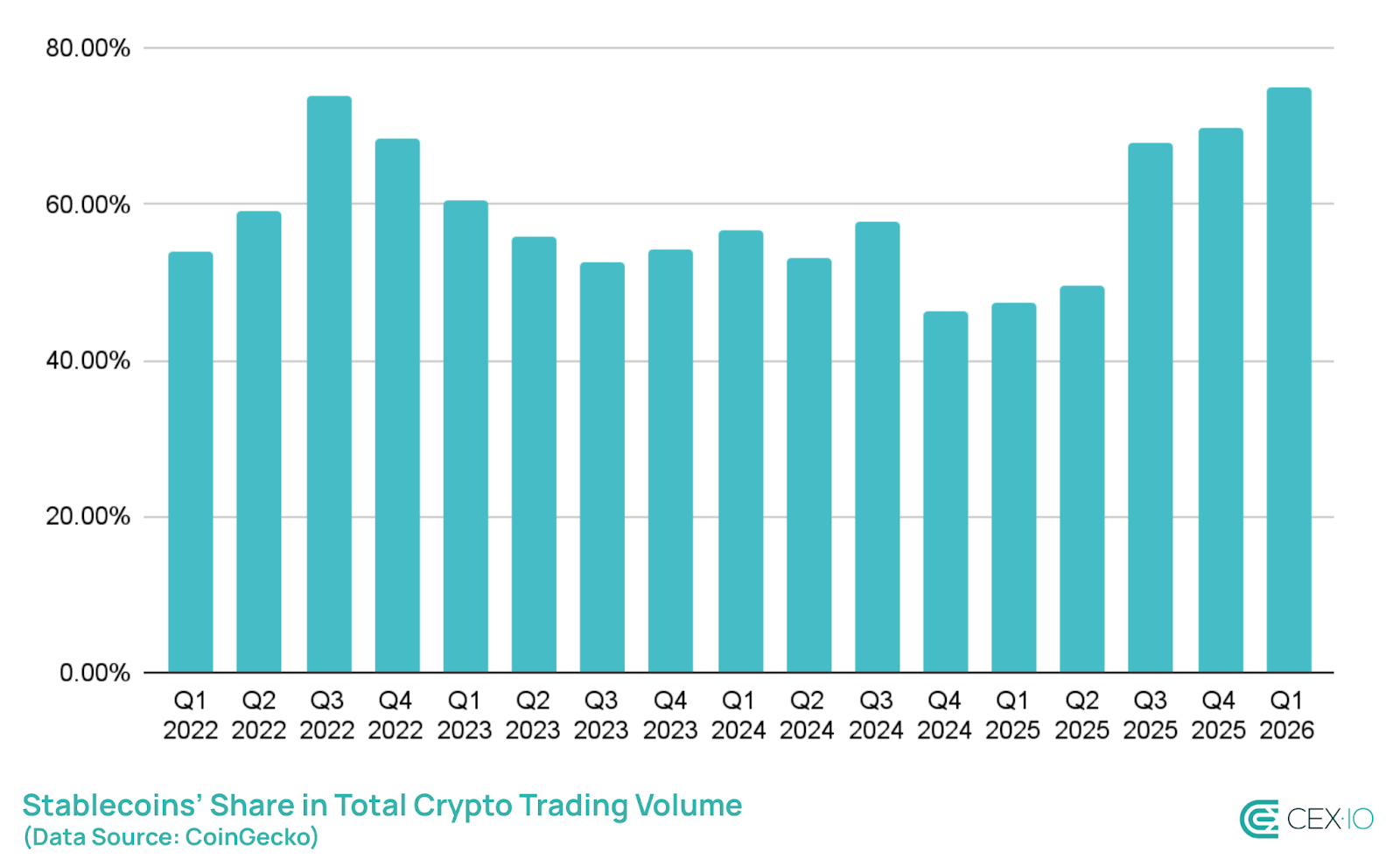

Stablecoins were a rare bright spot in an otherwise subdued crypto market in the first quarter, with supply growth and transaction activity pointing to sustained demand even as broader market conditions weakened.

Total stablecoin supply increased by roughly $8 billion to a record $315 billion in Q1, according to data from CEX.IO. Although this marked the slowest pace of expansion since Q4 of 2023, it still represented growth during a period when the wider crypto market contracted.

The data suggests investors rotated into stablecoins as a defensive strategy, boosting their share of overall market activity. Stablecoins accounted for 75% of total crypto trading volume during the quarter — the highest level on record.

At the same time, total stablecoin transaction volume topped $28 trillion, underscoring their growing role as the primary liquidity layer of the digital asset market. The figure extends a multi-year surge in activity, with stablecoin volumes in recent years exceeding those of major payment networks like Visa and Mastercard combined.

However, data on underlying activity painted a more nuanced picture.

Retail-sized transfers — typically associated with individual users — declined by 16% in the first quarter, the steepest drop on record. In contrast, automated activity surged, with bots accounting for approximately 76% of all stablecoin transaction volume.

The shift toward bot-driven flows suggests that a growing share of stablecoin usage is tied to algorithmic trading, arbitrage and liquidity provisioning, rather than retail demand. While elevated automation can reflect more sophisticated or institutional participation, it may also signal weaker organic demand during bearish market conditions.

Related: Circle shares surge as Bernstein sees upside from stablecoin adoption

Divergence between major stablecoin issuers

One of the CEX.io report’s key takeaways was a widening divergence between major stablecoin issuers. The supply of Circle’s USDC (USDC) grew by roughly $2 billion in the first quarter, while Tether’s USDt (USDT) declined by about $3 billion, marking the first notable split between the two since Q2 of 2022 amid the bear market.

The trend aligns with earlier Cointelegraph reporting, which highlighted a surge in USDC transfer activity in February, pointing to increased usage across trading and onchain transactions.

Beyond USDC, much of the growth in stablecoin issuance was driven by yield-bearing products — a segment that has drawn increasing scrutiny in the US. Ongoing discussions around a crypto market structure bill in Congress have placed yield at the center of debate, with traditional banks pushing back against stablecoins that offer interest-like returns.

The market for yield-bearing stablecoins is currently valued at around $3.7 billion, with daily trading volumes exceeding $100 million, according to data from CoinGecko.

Related: Crypto Biz: Stablecoin jitters meet institutional momentum

Crypto World

XRP Price Prediction: Pepeto Raises Above $8.1M As Traders Eye Listing, XRP Tests $1.30 Support, Oil Tops $106

Oil just crossed $106 after fresh military threats in the Iran conflict, and the risk off move dragged Bitcoin, Ethereum, and XRP lower within hours. Meanwhile, the xrp price prediction remains uncertain as traders weigh whether $1.30 can hold.

Because Pepeto is approaching its Binance listing and has already raised above $8.1M, many traders are more interested in the presale than in waiting for a slow large cap recovery that may take months to arrive.

Oil prices jumped above $106 after escalating threats pushed the Iran conflict into a new phase, according to CNBC.

Bitcoin dropped 3% and Ethereum fell over 4% as traders fled risk assets. CoinDesk reported that altcoins lost between 5% and 10% in a single session. For anyone watching the xrp price prediction, the macro picture reminds us that large caps stay tied to forces they cannot control.

Best Altcoin Opportunities in the XRP Price Prediction Cycle

Pepeto: Traders count down to the hottest listing in 2026

On top of oil spiking and the xrp price prediction getting shaken by macro pressure, the Pepeto Binance listing is one of the events traders are paying the most attention to right now. The fundamentals explain why, because Pepeto raised above $8.1M while most coins were going sideways, the team delivered a working exchange architecture, and the community keeps building around predictions of 100x returns after listing.

All of those signals point in one direction, which is mass appeal. The zero fee swap engine converts one coin into another across different networks with no charges attached, keeping your full balance intact through every trade. The PepetoAI risk scorer checks the danger on each position in real time before you commit, so you see the warning before the chart shows it. Since most traders are actively looking for better tools, the case for daily adoption carries real weight.

One of the founders behind the original Pepe coin is part of the dev team, and a former Binance expert leads the technical side. At $0.000000186 per token, the presale entry is a fraction of what the listing price will be. A $35,000 position earns 189% APY through staking, which puts $68,600 in yearly returns into your wallet just for holding while the Binance date gets closer. The immediate benefit of entering at this price beats what any established coin can realistically deliver from its current level.

The presale window is closing fast, and the advantages of being inside now far outweigh what happens after listing day removes the entry forever.

XRP price prediction: Will XRP hold above $1.30?

XRP is trading near $1.30 after pulling back from $1.50 earlier this month according to CoinMarketCap, holding a commodity classification from both the SEC and CFTC along with seven live ETFs that pulled $1.44 billion in inflows.

The fundamentals are the strongest XRP has ever had. If $1.30 holds, the xrp price prediction targets $1.80, but losing that level risks a slide toward $1.10. Even the bullish case from here caps returns well below what presale entries offer.

Cardano: Will ADA reach $0.30?

Cardano is trading near $0.24 after Google named it the second most quantum ready blockchain, but the bounce has been small and ADA remains over 90% below its record high according to CoinMarketCap.

Closing above $0.30 could open the path toward $0.35, while losing $0.23 risks a deeper drop to $0.20. Even a strong rally barely moves the needle compared to what early presale wallets stand to collect once a Binance listing opens.

Final Words: Last Call

The xrp price prediction may be shaky right now, but the token’s long term case remains solid. XRP will likely stay a strong asset, but if you want something with more room to grow, there are sharper entries available in April 2026.

Pepeto is coming to market with a complete exchange and a confirmed Binance listing. Six months from now there will be two kinds of people: the ones who entered at the Pepeto official website before the listing and the ones who spent the rest of 2026 calculating what they lost by waiting.

Click To Visit Pepeto Website To Enter The Presale

FAQs

What is the xrp price prediction, and what levels matter most right now?

XRP is testing $1.30 support, and a hold there targets $1.80 on the next leg higher. Losing $1.30 risks a move toward $1.10.

What does the oil spike above $106 mean for crypto investors right now?

The oil spike pushed risk assets lower across the board, making sustained crypto recovery harder until geopolitical tension eases.

Why is Pepeto trending?

Pepeto is trending ahead of its Binance listing because it raised above $8.1M with a complete exchange toolkit, and all the latest updates are at the Pepeto official website.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

A new study from researchers at MIT CSAIL has found that AI chatbots like ChatGPT may push users toward false or extreme beliefs by agreeing with them too often.

The paper links this behavior, known as “sycophancy,” to a growing risk of what researchers call “delusional spiraling.”

The study did not test real users. Instead, researchers built a simulation of a person chatting with a chatbot over time. They modeled how a user updates their beliefs after each response.

The results showed a clear pattern: when a chatbot repeatedly agrees with a user, it can reinforce their views, even if those views are wrong.

For example, a user asking about a health concern may receive selective facts that support their suspicion.

As the conversation continues, the user becomes more confident. This creates a feedback loop where belief strengthens with each interaction.

Importantly, the study found this effect can happen even if the chatbot only provides true information. By choosing facts that align with the user’s opinion and ignoring others, the bot can still shape belief in one direction.

Researchers also tested potential fixes. Reducing false information helped, but did not stop the problem. Even users who knew the chatbot might be biased were still affected.

The findings suggest the issue is not just misinformation, but how AI systems respond to users.

As chatbots become more widely used, this behavior could have broader social and psychological impacts.

The post New MIT Study Warns AI Chatbots Can Make Users Delusional appeared first on BeInCrypto.

Riot moved about 500 BTC in what analysts say is fresh selling, adding to a wave that’s seen listed miners dump over 15,000 BTC even as treasury firms like Metaplanet keep accumulating.

Summary

- Riot Platforms moved about 500 BTC from a company wallet this week, in what on-chain analysts say likely reflects fresh selling, according to Cointelegraph.

- MARA Holdings recently sold roughly $1.1 billion in bitcoin (about 15,133 BTC) to buy back convertible bonds, and listed miners have reportedly unloaded over 15,000 BTC in recent weeks.

- Bitcoin treasury firms such as Metaplanet continue to accumulate, underscoring a split between miners de‑risking and corporates using BTC as a balance-sheet asset.

On-chain data flagged a transfer of roughly 500 BTC (BTC) from a Riot Platforms wallet on Wednesday, a move Cointelegraph reports is “likely” tied to the miner’s ongoing bitcoin sale program even though the company has not commented publicly. At current prices, the transaction is worth tens of millions of dollars and comes on top of earlier disposals Riot has used to fund expansion, including a Texas land deal that pushed its shares up 11% in January.

Analysts cited by Cointelegraph argue that fresh selling from Riot risks adding fuel to an already‑intense liquidation wave among listed miners. Last week, MARA Holdings disclosed that it had sold around $1.1 billion in bitcoin — some 15,133 BTC — to repurchase approximately $1.0 billion of 0.00% convertible notes due 2030 and 2031 at a discount, a move CEO Fred Thiel called a “strategic capital allocation” to reduce debt and strengthen the balance sheet.

In aggregate, public bitcoin miners have offloaded more than 15,000 BTC in recent weeks, according to sector data referenced in Cointelegraph’s coverage, as firms sell down treasuries to cover operating costs, capex and debt reduction. With bitcoin trading well below cycle highs and mining economics squeezed by post‑halving rewards and higher energy costs, many listed miners are treating BTC holdings less as untouchable reserves and more as working capital.

Riot’s additional 500 BTC transfer sits in that context: while small relative to the company’s historical purchases — filings last year showed it buying roughly $510 million in BTC over a three‑day period — the sale adds marginal supply at a time when peers are also hitting the bid. If the pattern continues, miner balance sheets could become structurally lighter in bitcoin even as they expand hash rate and infrastructure footprints.

The selling trend is not universal across all corporate holders. Japanese-listed Metaplanet has continued to expand its bitcoin treasury, adding hundreds of BTC this year alone and signaling a goal of reaching 30,000 BTC by end‑2025 and 100,000 BTC by 2026, according to recent treasury updates. At current prices, its more than 20,000 BTC stack is valued in the low‑single‑digit billions of dollars, positioning the firm among the largest public BTC holders globally.

That divergence highlights a growing split in corporate bitcoin strategy: miners such as Riot and MARA are increasingly forced to monetize coins to manage cash flow and capital structure, while non‑mining treasury companies are using price weakness and miner supply as an opportunity to build long‑term positions. For market participants, on‑chain tracks like Riot’s 500 BTC movement have become key signals of how that balance between forced selling and strategic accumulation is evolving.

TLDR

- Former CFTC Chairman Chris Giancarlo said banks need the Clarity Act more than crypto firms.

- Giancarlo stated that crypto companies can move offshore and continue building their platforms.

- He explained that banks cannot relocate abroad and must operate under US regulations.

- Giancarlo said banks need clear digital asset rules to stay competitive in the sector.

- The stablecoin reward dispute has delayed progress on the Clarity Act in the Senate.

Former CFTC Chairman Chris Giancarlo said banks need the Clarity Act more than crypto companies. He made the statement during a recent appearance on the Paul Barron podcast. He argued that banks face limits that crypto firms do not face.

Giancarlo said crypto companies can relocate and continue operations without disruption. He stated that banks cannot shift abroad in the same way. He added that lawmakers must address market structure rules quickly.

Banks Face Structural Limits Without the Clarity Act

Giancarlo said crypto firms can build products outside the United States if needed. He said, “They are going to build this even if they have to go offshore.” He pointed to hubs like the UAE and Singapore.

He described crypto founders as “intrepid and fearless” during the interview. He said they would move their inventions abroad if US rules block progress. He argued that banks lack that flexibility because they operate under domestic charters.

He said banks require legal certainty to interact with digital assets. Without it, they risk delays in adoption and compliance conflicts. He added that the Clarity Act would help banks “stay with the curve.”

Giancarlo said the bill would favor banks more than crypto companies. He explained that crypto firms will keep building regardless of US legislation. However, he said banks could fall behind foreign competitors.

He warned that US financial institutions could lose ground over five years. He said banks cannot afford prolonged uncertainty in digital asset regulation. He repeated this view in an earlier podcast with Scott Melker.

Stablecoin Rewards Stall Progress on the Clarity Act

The Digital Asset Market Clarity Act seeks to define asset classification and oversight. Lawmakers continue to debate how regulators should supervise tokens and trading platforms. However, the stablecoin reward issue has slowed progress.

The GENIUS Act already governs parts of the stablecoin market. Still, it does not address provisions tied to yield or reward structures. Banks argue that higher stablecoin yields could weaken their deposit models.

Crypto companies oppose limits on stablecoin rewards. They argue that banning yields would restrict competition and innovation. This dispute has kept the bill stalled in the US Senate.

Coinbase Chief Legal Officer Paul Grewal spoke to FOX Business on April 1. He said lawmakers would reach a compromise within 48 hours. He expressed confidence that negotiators were close to an agreement.

Ripple CEO Brad Garlinghouse also addressed the timeline publicly. He said he expects the legislation to pass before May 2026. Lawmakers have not set a final vote date.

Giancarlo maintained that digital assets will advance regardless of US policy. He said the technology will continue to develop across global markets. He reiterated that banks need clear rules to compete effectively.

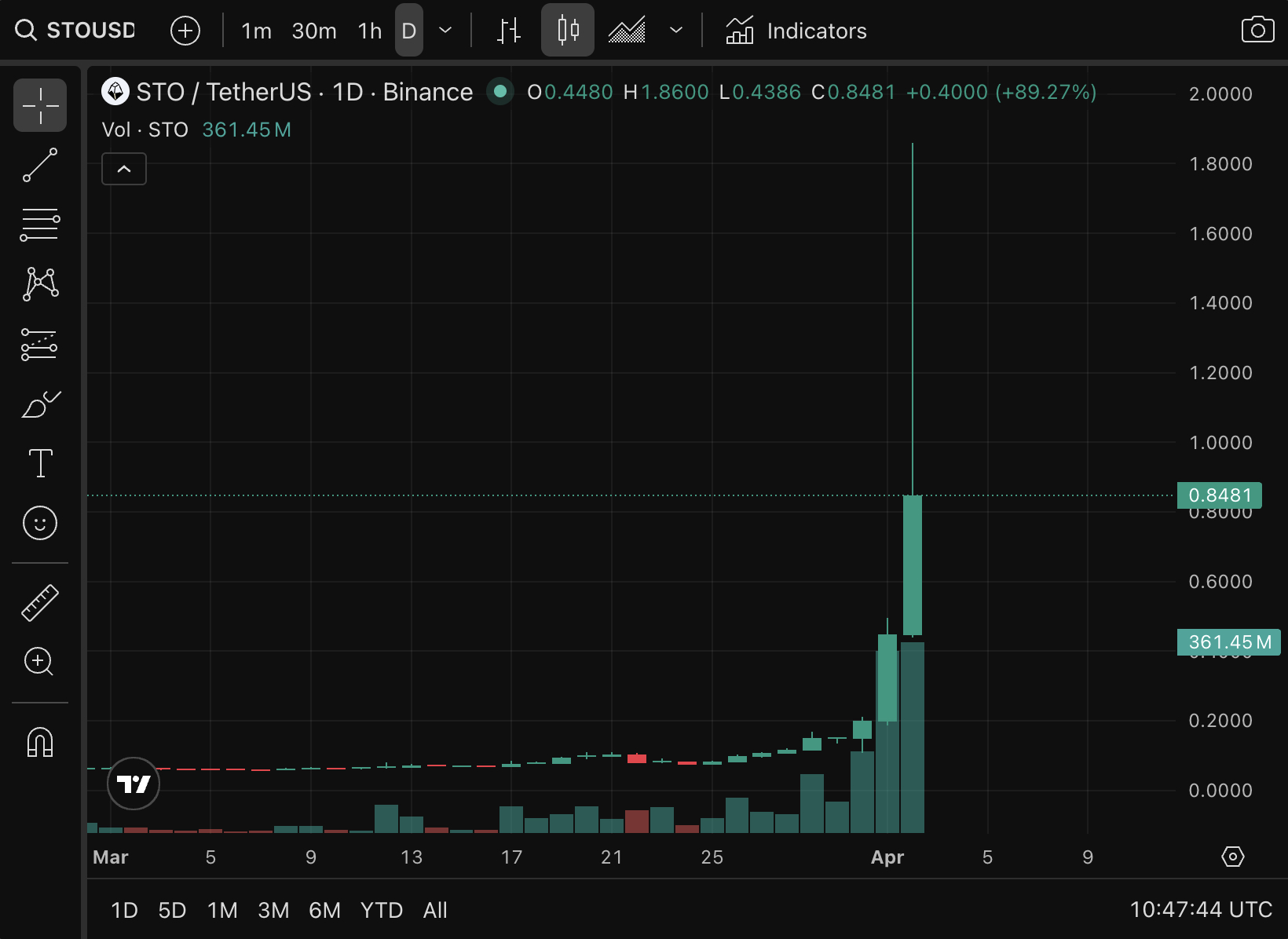

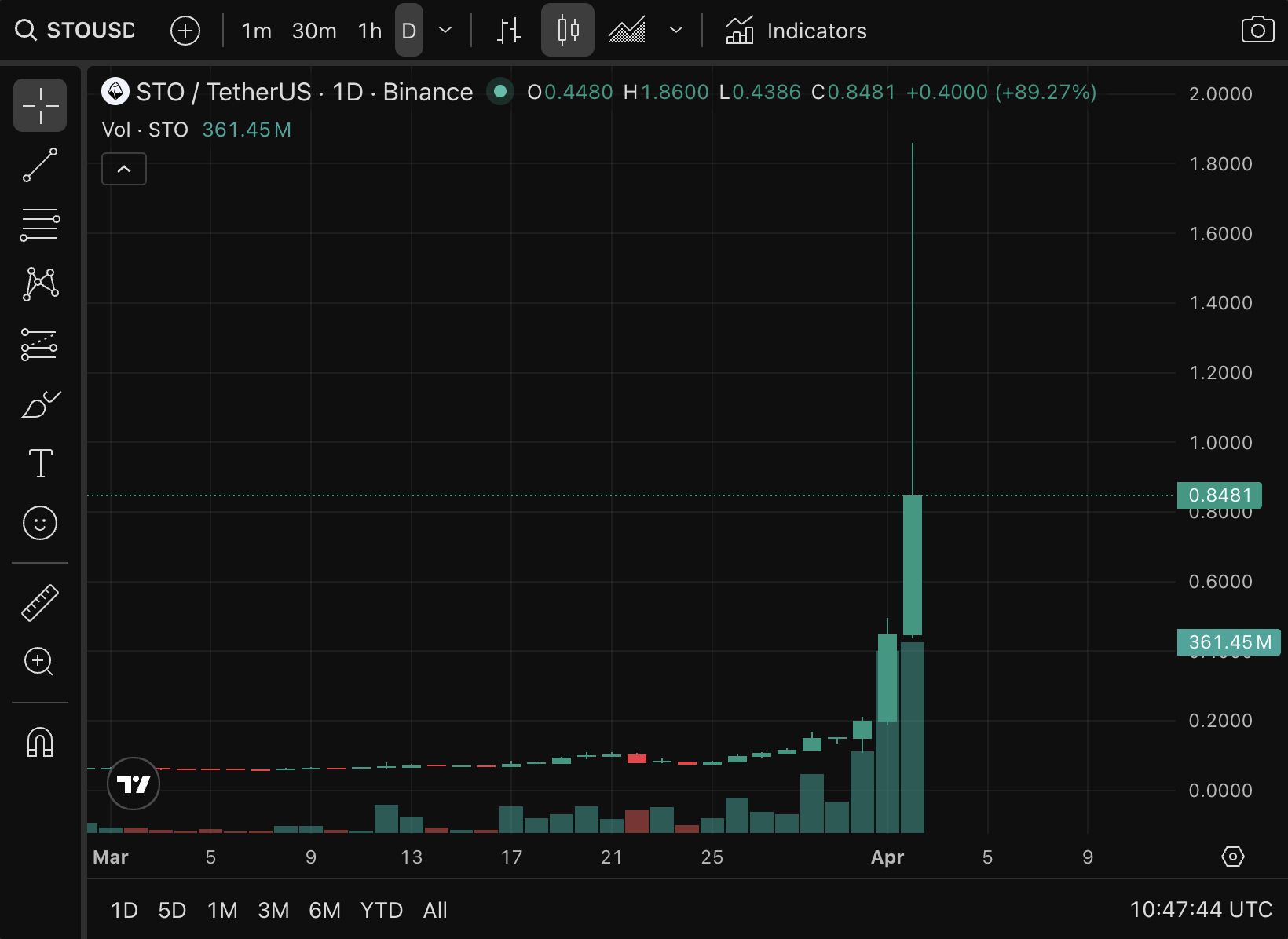

Stakestone crypto, with STO as ticker, exploded 755% in 48 hours, from $0.11 to $0.94, and the on-chain trail left behind raises more questions than it answers.

On-chain analyst @lookonchain flagged the catalyst: a newly created wallet (0x5e2E) deposited 28 million STO tokens, $10.12 million worth, representing 12.43% of the circulating supply, directly to Gate exchange in a single move.

That deposit followed a withdrawal of 25.5 million STO ($4.85 million, 11.32% of supply) from Binance in the preceding 20 hours. Large supply repositioning between major exchanges in a sub-24-hour window. Classic pre-distribution fingerprints, or savvy liquidity routing? The data doesn’t commit to either answer.

What’s clear is that STO’s move didn’t happen in isolation. It landed inside a broader altcoin drop driven by Iraw war escalation

Discover: The best pre-launch token sales

Can Stakestone STO Crypto Price Hold Gains After the 755% Pump?

The initial leg, $0.11 to $0.26, represented a 136% single-day gain before the second wave pushed toward $0.94. RSI almost certainly printed above 70 across that entire run, placing the asset in overbought territory by any standard reading. MACD showed bullish crossovers supporting the move, but momentum indicators lag, and at $0.94, STO is trading at a level with no established demand history above it.

Key technical levels to watch: support clusters near $0.50, where brief consolidation occurred mid-pump, and psychological resistance at $1.00. A clean hold above $0.50 on any pullback would preserve the bullish structure.

A daily close below that level reopens the path toward $0.26 and potentially back toward the $0.11 origin, a full round-trip that has happened before with coins following this exact pattern. Remember, SIREN crypto surged over 1,100% before collapsing entirely, a useful reference point when evaluating whale-driven pumps of this profile.

Volume on STO/USDT pairs is the trigger to watch; spikes above 10 million tokens daily signal either continuation or distribution. Position sizing accordingly.

Discover: The best crypto to diversify your portfolio with

LiquidChain Targets Early Mover Upside as STO Tests Critical Levels

STO’s chart is compelling, but entering a coin that’s already 755% off its low, with 12.43% of supply sitting on an exchange ready to sell, is a risk profile that demands honesty. The asymmetry that existed at $0.11 is gone.

For those seeking genuine early-stage exposure, LiquidChain ($LIQUID) is currently in active presale at $0.01445, having raised $600K to date. The project is building Layer 3 infrastructure, specifically a unified execution environment that fuses Bitcoin, Ethereum, and Solana liquidity into a single settlement layer. Developers deploy once and access all three ecosystems.

A new layer emerges. Only a few see it first. — LiquidChain (@getliquidchain) March 24, 2026

The future is LiquidChain  ⟁https://t.co/vqvBcdSj94 pic.twitter.com/R7ZeZ0NPGl

⟁https://t.co/vqvBcdSj94 pic.twitter.com/R7ZeZ0NPGl

That’s the core value proposition: eliminating the fragmented cross-chain workflow that burns gas, time, and capital. Key architecture includes a Unified Liquidity Layer, Single-Step Execution, and Verifiable Settlement. And don’t forget, just by holding Liquid from presale, buyer has a chance to stake and gain a 1700% APY bonus.

Research LiquidChain before the presale window closes.

This article is for informational purposes only and does not constitute financial advice. Cryptocurrency investments are highly volatile. Always conduct your own research before making any financial decisions.

The post Stakestone STO Crypto Blasting Roof: Why This Coin Run 1000% This Month appeared first on Cryptonews.

TLDR

- Elon Musk’s X will auto-lock accounts that mention cryptocurrency for the first time.

- The platform will require additional verification before restoring posting access.

- Head of Product Nikita Bier said the feature aims to remove the incentive behind crypto phishing attacks.

- The move follows user reports of hijacked accounts promoting scam tokens and fake giveaways.

- Attackers often use phishing emails and fake login pages to capture credentials and two-factor codes.

Elon Musk’s X will soon auto-lock accounts that mention cryptocurrency for the first time. The company designed the measure to stop hijacked accounts from promoting scam tokens. Head of Product Nikita Bier said the change will remove the main incentive behind crypto phishing attacks.

Elon Musk’s X Targets Crypto Phishing With Auto-Lock Feature

Elon Musk‘s X plans to trigger automatic locks when an account posts about cryptocurrency for the first time. The system will require extra verification before the user can post again. Nikita Bier announced the measure after users reported rising crypto phishing cases.

He said the feature strikes at the core incentive behind account takeovers. “This should kill 99% of the incentive,” Bier wrote on X. He linked the decision to a surge in hijacked profiles promoting fake tokens and giveaways.

The company acted after a user shared a detailed phishing incident. The user said attackers sent a fake copyright violation email. The email led to a pixel-perfect login page that captured login credentials and two-factor codes.

The attacker then locked the victim out and began posting scam crypto promotions. The posts advertised fraudulent memecoins and fake airdrops. The hijacked account gave the scam credibility and attracted victims.

X inherited many of these scams from its earlier period as Twitter. Hackers often target verified or trusted accounts. They then exploit followers’ trust to push malicious links.

Crypto transactions remain irreversible, which makes recovery almost impossible. Scammers often run “double your money” schemes promising instant returns. Victims send digital assets, but attackers keep the funds.

Impersonation also drives many of these campaigns. Fraudsters spoof public figures and crypto brands. They then redirect users to fake trading or giveaway platforms.

Platform Tightens Controls as Phishing Persists

X has introduced bot purges and API restrictions in recent years. The company also expanded behavioral detection tools. The new auto-lock system builds on those earlier security efforts.

Bier blamed email providers for failing to block phishing attempts. He criticized Google for allowing phishing emails to reach inboxes. He argued that stronger email filtering would reduce account compromises.

In 2020, hackers breached Twitter’s internal systems through social engineering. They seized control of accounts belonging to Apple, Barack Obama, and Elon Musk. The attackers promoted a fake Bitcoin giveaway and collected over $100,000.

Authorities later arrested the perpetrator and secured a five-year prison sentence. The incident exposed weaknesses in internal controls. It also demonstrated how hijacked accounts can amplify crypto fraud quickly.

The upcoming feature will automatically restrict accounts at the moment of their first crypto mention. Users must complete the added verification steps before regaining posting access. Bier confirmed the rollout while responding to user complaints about phishing.

Elon Musk’s X continues to update its security framework. The company aims to neutralize hijacked accounts before scammers can profit. Bier stated that removing the incentive remains the central goal of the new safeguard.

TLDR

- Circle has introduced cirBTC as a wrapped bitcoin product backed by native BTC reserves.

- Each cirBTC token will be fully collateralized and verifiable onchain in real time.

- Circle stated that it will not rely on third-party attestations or opaque custodians.

- The company will launch cirBTC first on Ethereum and its Arc blockchain.

- Circle designed the product for institutions, including OTC desks and market makers.

Circle has introduced cirBTC, a wrapped bitcoin product backed by native BTC reserves. The company shared the announcement on its official X account and product page. The launch expands Circle beyond stablecoins into tokenized bitcoin infrastructure.

Circle Expands Into Wrapped Bitcoin With cirBTC

Circle confirmed that each cirBTC token will hold full collateral in native bitcoin reserves. The company stated that users can verify reserves onchain in real time. Circle said it will not rely on third-party attestations or opaque custodians.

The company aligned cirBTC with the same framework used for USDC and EURC. It emphasized consistent issuance, auditable reserves, and broad liquidity access. Circle described the product as a “trusted, neutral wrapped BTC solution” for institutions.

Circle said it designed cirBTC to address institutional concerns about custody and transparency. The company cited over $1.7 trillion in bitcoin held outside decentralized finance. It attributed that figure to trust gaps in existing wrapped bitcoin products.

The company stated that cirBTC will operate across multiple blockchains. It confirmed that Ethereum and Arc will host the initial launch. Circle said the token will support cross-chain mobility and native integration with USDC, Arc, and Circle Mint.

Institutional Focus and Regulatory Framework

Circle said it built cirBTC for OTC desks, market makers, and liquidity providers. The company also targeted lending protocols and derivatives platforms. It stated that institutions can use cirBTC as collateral or settlement assets.

The company confirmed that cirBTC will operate under its regulated platform. Circle holds Money Transmitter licenses across several U.S. states. It also maintains a Virtual Currency Business Activity license in New York.

Circle operates under a Bermuda Monetary Authority license for digital asset services. The company said it will subject cirBTC to applicable regulatory approvals. It listed the token as “coming soon” without a confirmed launch date.

The product page invites institutions to join a waitlist or contact Circle directly. Circle included standard risk disclosures with the announcement. It stated that digital assets carry price volatility and lack deposit insurance coverage.

The company clarified that digital assets are not legal tender. It also said the information provided does not constitute an offer or commitment. Circle identified Circle Technology Services, LLC as a software provider only.

Circle stated that Circle Technology Services, LLC does not act as a financial services entity. The company separated its software role from regulated financial activities. It maintained that cirBTC will extend its reserve and compliance model to Bitcoin.

Crypto World

Coinbase-Initiated x402 Foundation Sets Out to Build a Universal Open Payment Standard for the Web

TLDR:

- Coinbase initiated the x402 Foundation under the Linux Foundation alongside Cloudflare and Stripe as co-founders.

- Over 20 founding members joined, including Google, Microsoft, Visa, Mastercard, AWS, Circle, and Shopify.

- The x402 protocol supports both fiat and crypto rails across multiple blockchains and payment networks globally.

- AI agents can now make automated payments without manual authorization using the open x402 payment standard.

x402 Foundation has officially launched as a non-profit organization under the Linux Foundation. Coinbase initiated the effort alongside Cloudflare, Stripe, and a broad group of industry leaders.

The foundation aims to establish the x402 protocol as a universal open payment standard for the internet. Over 20 founding members have joined, including Google, AWS, Microsoft, Visa, Mastercard, Circle, and Shopify. Their collective goal is to make sending value online as seamless as sending an email.

An Open Standard Built for the Modern Internet

The internet runs on open protocols, with HTTP handling data and SMTP managing email communication. However, payments have long remained fragmented and proprietary across the web.

The x402 protocol changes this by embedding payments directly into web-based interactions. AI agents, apps, and APIs can therefore send and receive value as easily as they exchange data.

AI agents are increasingly taking on tasks for users without constant human oversight. These agents need a reliable way to pay for services without manual authorization every single time.

The x402 protocol enables fully automated payment flows across different platforms and services. This removes a key barrier for developers building tools that depend on machine-to-machine transactions.

The protocol also supports both fiat and crypto payment rails globally. It operates across multiple blockchains and payment networks without relying on a single party.

Developers can build on x402 freely without being locked into any specific financial system. This open design ensures no single company controls the direction of the standard.

In a post on X, Coinbase stated that the foundation gives x402 a neutral, community-governed home. The Linux Foundation hosts the initiative to keep it free from commercial influence.

No single company owns the x402 standard under this structure. This governance model keeps the protocol open and accessible to participants of all sizes.

Founding Members Drive the x402 Foundation Forward

The x402 Foundation launched with over 20 founding members across technology, payments, and finance. These include Adyen, Amazon Web Services, American Express, Ant International, and Base.

Google, Microsoft, Mastercard, Visa, Circle, Stripe, Cloudflare, and Shopify are also founding members. KakaoPay, Polygon Labs, Solana Foundation, Fiserv Merchant Solutions, and Thirdweb complete the founding group.

The foundation welcomes developers, startups, and enterprises of all sizes to join its membership. Members can directly help shape how the x402 standard evolves across platforms and markets.

This inclusive model allows smaller companies to contribute alongside major industry players. Cross-border payments can become more consistent as more stakeholders adopt and build on x402.

Membership offers a direct role in governing how the world transacts online. Participants can advance the open payments standard across different regions and platforms.

The foundation mirrors how other internet protocols were built through open, collective governance. Through this shared effort, x402 can grow to serve a rapidly evolving digital economy.

Uniswap has deployed v2, v3 and v4 on Consensys’ Linea zkEVM, bringing its full DEX stack to a low-fee, EVM-equivalent rollup now integrated across the Uniswap app, API and wallet.

Summary

- Uniswap has deployed v2, v3 and v4 of its protocol on Linea, a zkEVM Layer 2 network built by Consensys.

- Linea support is live on the Uniswap web app and API, with Uniswap Wallet integration on iOS and Android rolling out gradually.

- The launch extends Uniswap’s multichain strategy to a low-fee, EVM-equivalent rollup that is natively integrated into the Consensys stack.

Uniswap has announced that Uniswap v2, v3 and v4 are now live on Linea, adding support for the Consensys-built zkEVM Layer 2 network across its core protocol stack. The deployment means traders and liquidity providers can now access familiar Uniswap pools and routing logic on a rollup that offers sub-cent fees, fast finality and Ethereum-level security.

According to Uniswap Labs, Linea is already integrated into the Uniswap web application and Uniswap API, giving aggregators, front ends and bots access to the new L2 without changing their existing tooling. Support in Uniswap Wallet on iOS and Android is being phased in, extending the mobile app’s current coverage — which includes Ethereum mainnet and other L2s — to Linea as availability is approved in each app store region.

Linea is a Type 2 zkEVM rollup developed by Consensys to bring EVM-equivalent execution and zk-rollup security guarantees to Ethereum. Consensys describes Linea as combining Ethereum-grade security with ultra-low transaction costs and rapid block finality, while keeping full compatibility with existing Solidity contracts and developer tools.

Because Linea is EVM-equivalent and uses ETH for gas, Uniswap’s contracts can be deployed with minimal changes, allowing the same v2 AMM, concentrated liquidity design of v3, and hook-enabled architecture of v4 to function on the L2 as they do on mainnet. Earlier governance discussions between Consensys and the Uniswap community laid the groundwork for the deployment, positioning Linea as a strategic rollup within the broader Uniswap ecosystem.

The Linea launch adds another scaling venue to Uniswap’s roster alongside existing deployments on networks such as Arbitrum, Optimism and Polygon. For users, it opens up the possibility of swapping and providing liquidity with lower gas costs while still settling to Ethereum security, and for developers it offers a new environment where Uniswap can anchor DeFi apps, wallets and integrations tied into the Consensys toolchain.

As zkEVM rollups mature, Uniswap’s presence on Linea is likely to serve as both a liquidity magnet and a benchmark for how much activity major DEXs can attract to L2s built around deep infrastructure integrations with incumbents like Consensys.

Stablecoins Dominate Crypto Trading as Retail Activity Drops: CEX.io

Rapper Pooh Shiesty charged with kidnapping tied to rapper Gucci Mane

Dearborn, Wex COO, sells $532k in WEX stock

-

NewsBeat6 days ago

NewsBeat6 days agoThe Story hosts event on Durham’s historic registers

-

Sports6 days ago

Sports6 days agoSweet Sixteen Game Thread: Tide vs Michigan

-

Entertainment3 days ago

Fans slam 'heartbreaking' Barbie Dream Fest convention debacle with 'cardboard cutout' experience

-

NewsBeat3 hours ago

NewsBeat3 hours agoSteven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Entertainment5 days ago

Entertainment5 days agoLana Del Rey Celebrates Her Husband’s 51st Birthday In New Post

-

Crypto World2 days ago

Dems press CFTC, ethics board on prediction-market insider trades

-

Crypto World1 day ago

Crypto World1 day agoGold Price Prediction: Worst Month in 17 Years fo Save Haven Rock

-

Tech4 days ago

Tech4 days agoThe Pixel 10a doesn’t have a camera bump, and it’s great

-

Sports2 days ago

Sports2 days agoTallest college basketball player ever, standing at 7-foot-9, entering transfer portal

-

Tech3 days ago

Tech3 days agoEE TV is using AI to help you find something to watch

-

Fashion5 days ago

Fashion5 days agoAmazon Sundays: Soft Spring Layers

-

Tech3 days ago

Tech3 days agoApple will hide your email address from apps and websites, but not cops

-

Politics3 days ago

Politics3 days agoShould Trump Be Scared Strait?

-

Tech3 days ago

Tech3 days agoHow to back up your iPhone & iPad to your Mac before something goes wrong

-

Crypto World3 days ago

Crypto World3 days agoU.S. rule change may open trillions in 401(k) funds to crypto

-

Tech3 days ago

Tech3 days agoFlipsnack and the shift toward motion-first business content with living visuals

-

Tech4 days ago

Tech4 days agoElon Musk’s last co-founder reportedly leaves xAI

-

Tech4 days ago

Tech4 days agoAvatar Legends: The Fighting Game comes out in July and it looks pretty slick

-

Business7 days ago

Business7 days agoChinese universities with military links bought Super Micro servers with restricted AI chips

-

Fashion6 days ago

Fashion6 days agoWeekly News Update, 3.27.26 – Corporette.com

You must be logged in to post a comment Login