Business

Giannis Future, Star Shifts and Draft Buzz

As the 2026 NBA playoffs continue with the Western Conference Finals between the Oklahoma City Thunder and San Antonio Spurs, trade speculation has intensified for the upcoming offseason and 2026 NBA Draft.

League executives and analysts have highlighted several major storylines as teams evaluate rosters following the February 2026 trade deadline. Here are the three most prominent NBA trade rumors circulating as of May 23, 2026.

1. Giannis Antetokounmpo Trade Possibilities

Milwaukee Bucks forward Giannis Antetokounmpo remains the most discussed name in trade rumors. After the Bucks missed the 2026 playoffs, the organization has fielded inquiries about the two-time MVP, who is under contract through the 2027-28 season.

Teams including the Miami Heat, New York Knicks, Minnesota Timberwolves and Oklahoma City Thunder have been mentioned as potential suitors. Executives believe Antetokounmpo’s trade value could increase due to his matchup potential against players like Victor Wembanyama of the Spurs.

NBA executives have noted that teams are considering how to build rosters capable of competing against dominant Western Conference teams. One source told Sam Amick that Giannis is viewed as a potential solution against emerging stars.

The Golden State Warriors have expressed interest in keeping their 2026 draft pick rather than using it aggressively in a Giannis pursuit, according to reports. Warriors general manager Mike Dunleavy Jr. has emphasized flexibility with future assets.

2. Warriors Roster Reconstruction Plans

The Golden State Warriors have been active in trade discussions as they look to build around Stephen Curry in the win-now window. The team traded for Kristaps Porzingis at the 2026 deadline and continues exploring options.

Golden State holds the No. 11 pick in the 2026 NBA Draft and multiple future first-round selections. Reports indicate the franchise is open to trades involving young talent and picks to improve the roster.

Dunleavy stated after the deadline, “We’re willing to do whatever it takes to improve this team, whether it’s young players, first-round picks. We always have been, we always will be, as long as we’re in this win-now window.”

Potential targets include veterans who fit alongside Curry, Draymond Green and the team’s younger core. Salary constraints have limited some larger pursuits, but the Warriors maintain trade flexibility.

3. Lakers and Other Contender Moves

The Los Angeles Lakers have been linked to several trade targets as they seek to bolster their roster around LeBron James and Anthony Davis, though Davis was traded to the Washington Wizards earlier in the season.

Los Angeles has shown interest in centers and wing defenders. Names such as Jalen Duren, Jarrett Allen and Walker Kessler have surfaced in connection with the Lakers. The team holds future first-round picks in 2031 and 2033 that could be used in deals.

Broader offseason rumors include potential availability of players like Lauri Markkanen from the Utah Jazz, Michael Porter Jr. from the Brooklyn Nets and Trae Young from the Atlanta Hawks. These names have been discussed as possible targets for contenders seeking upgrades.

The 2026 NBA Draft features top prospects such as AJ Dybantsa, with teams like the Utah Jazz reportedly inquiring about trading up to the No. 1 pick held by the Washington Wizards.

Offseason Context

The NBA offseason will include the 2026 draft in June and free agency beginning in early July. Teams eliminated from the playoffs have begun internal evaluations of potential trades, extensions and draft strategies.

Several franchises face key decisions. The Memphis Grizzlies have been linked to discussions involving Ja Morant, though no resolution has been reported. Other teams are monitoring salary cap situations and asset accumulation.

League sources indicate that while major superstar trades are possible, many moves will involve role players and future picks as teams position themselves for the 2026-27 season.

Broader League Landscape

The Oklahoma City Thunder, currently leading the Western Conference Finals, have built a strong young core and could be active in future trades. The San Antonio Spurs, featuring Victor Wembanyama, have emerged as a formidable opponent.

Eastern Conference teams such as the Boston Celtics, who acquired Nikola Vucevic at the deadline, and the Cleveland Cavaliers, who added James Harden, continue refining their rosters.

Analysts expect a busy summer with draft-night deals and sign-and-trade possibilities. Teams with available cap space and draft assets hold advantages in negotiations.

The 2026 free agent class includes several notable names, though restricted free agents like Jalen Duren could complicate plans for suitors. Trade assets remain central to roster construction strategies.

Business

FIIs sell over Rs 30K crore worth of Indian equities in May as outflows swell to Rs 2.22 lakh crore. What lies ahead?

On Friday, FIIs sold domestic shares to the tune of Rs 4,440.47 crore while domestic institutional investors (DIIs) were net buyers at Rs 6,003.53 crore.

DIIs throwing around their weight on Friday, helped the benchmark indices end with gains though they were capped amid strong selling pressure in pharma & health stocks while financials helped bulls to ride the tide. While Nifty gained 64.60 points or 0.27% to close at 23,719.30, the BSE Sensex settled at 75,415.35, up 231.99 points or 0.31%.

Commenting on the current FII trends, Pabitro Mukherjee, Associate Vice President – Research at Bajaj Broking said the investor sentiment remains cautious due to persistent geo-political tensions, which continued to keep crude oil prices elevated.

“The Indian Rupee further weakened during the week, slipping to a fresh all-time low against the US Dollar. Meanwhile, a sharp rise in bond yields, driven by concerns over rising inflation and the possibility of prolonged higher interest rates, kept investors on edge. Overall, global uncertainty and macroeconomic headwinds led to cautious trading activity across the markets. Looking ahead, institutional flows are likely to remain sensitive to developments around US–Iran tensions, oil-price movement,” he said.

Outlook

Bajaj Broking has said institutional activity is expected to be largely driven by global developments, going forward. The progress or deterioration of the U.S.–Iran negotiations will remain a key factor to monitor, he said, outlining significant implications for geopolitical stability and the potential impact on crude oil price volatility.

FIIs in 2026

War-induced sell-off in March made it the worst month this year, witnessing an exodus worth Rs 1,17,775 crore. April was not kind too, with outflows of Rs 60,847 crore. Foreign investors turned net buyers in February, buying shares worth Rs 22,615 crore in the domestic markets so far. In January, they sold Rs 35,962 crore worth of shares.

In 2025, the FIIs buying trends remained patchy, but the overall trend was bearish. They took Rs 1,66,286 crore from Indian markets as trade deal delay and premium valuations weighed on the sentiments.

(Disclaimer: Recommendations, suggestions, views and opinions given by the experts are their own. These do not represent the views of Economic Times)

Business

Navitas Semiconductor NVTS Stock Jumps Nearly 20% on AI Power Demand and Analyst Upgrades in 2026

TORRANCE, Calif. — Navitas Semiconductor Corporation shares surged 19.98% to close at $29.25 on May 22, 2026, as the gallium nitride and silicon carbide power semiconductor specialist continued to benefit from momentum in artificial intelligence infrastructure and multiple analyst price target increases.

The stock traded as high as $29.54 during the session before pulling back slightly in after-hours trading to around $29.01. The move extended recent gains tied to the company’s pivot toward high-power markets.

Recent Analyst Actions

Several firms raised price targets in early May 2026. Needham increased its target to $21 from $13. Baird raised its target to $20 from $9. Morgan Stanley lifted its target to $12.50 from $4.20, and Rosenblatt moved to $13 from $7.

The company is scheduled to participate in upcoming investor conferences, contributing to positive sentiment.

Q1 2026 Financial Results

Navitas reported first-quarter 2026 revenue of $8.6 million on May 5, up 18% sequentially from $7.3 million in the fourth quarter of 2025 but down from $14.0 million in the year-ago period. The sequential increase was driven by higher contributions from high-power markets, including AI data centers, grid and energy infrastructure, and industrial electrification.

Non-GAAP gross margin expanded to 39.0%. The company reported a GAAP net loss of $33.8 million, or $0.15 per share, compared with a $16.8 million loss, or $0.09 per share, in the prior-year quarter. On a non-GAAP basis, the loss per share was $0.04, beating consensus estimates of $0.05.

For the second quarter of 2026, Navitas guided revenue to $10.0 million, plus or minus $0.5 million, representing sequential growth of over 16% at the midpoint. Non-GAAP gross margin is expected at 39.25%, plus or minus 75 basis points.

Strategic Shift to High-Power Markets

Navitas has focused on its “Navitas 2.0” strategy, emphasizing high-power GaN and SiC solutions for AI data centers and energy infrastructure while reducing exposure to lower-margin consumer and mobile segments. High-power markets represented a larger portion of revenue in the first quarter.

The company highlighted new 800V solutions for AI data centers and grid infrastructure at PCIM 2026. These include SST solutions for medium-voltage to high-voltage DC conversion and power delivery boards.

Partnerships and Product Developments

Navitas has secured design wins and partnerships supporting AI power efficiency. A partnership with Cyrient in India for GaN-based products targeted next-generation power applications, including AI infrastructure and industrial systems.

The company continues to advance its GeneSiC silicon carbide platform alongside GaNFast gallium nitride technology for data center and electrification needs.

Capital Markets Activity

In May 2026, Navitas completed a $122 million ATM equity offering and launched a new $125 million ATM program. It also filed a $250 million mixed securities shelf.

The company ended the first quarter with approximately $223.4 million in cash, cash equivalents and restricted cash.

Market Position

Navitas operates in the power semiconductor sector, competing in high-growth areas driven by AI power demands. The company’s technology focuses on efficiency improvements critical for data centers and renewable energy applications.

Shares have shown significant volatility in 2026, with strong year-to-date performance reflecting investor interest in AI-related power solutions. The stock has traded well above prior-year levels amid sector tailwinds.

Analyst Consensus

As of mid-May 2026, analysts maintained a range of ratings with upward revisions. Price targets varied widely, reflecting differing views on execution of the high-power strategy and revenue ramp.

Revenue forecasts for 2026 were upgraded by an average of 12% in recent weeks, according to some tracking services.

Broader Industry Context

Demand for efficient power semiconductors has risen with AI data center expansion. Navitas has positioned itself through product launches and customer engagements in energy infrastructure and performance computing.

The company added Gregory M. as a veteran independent director in early May to support its transformation.

Navitas plans to report second-quarter 2026 results in early August. Management has emphasized disciplined spending and R&D investment in high-power initiatives.

This report compiles information from company announcements, financial filings and market data available through May 22, 2026. Stock prices and projections remain subject to market conditions and future results.

NEW YORK — Intel Corp. and International Business Machines Corp. showed contrasting performances through mid-2026 as investors compared Intel’s semiconductor recovery efforts against IBM’s steady software, infrastructure and quantum computing progress.

As of May 22, 2026, Intel shares closed at $118.50. IBM shares closed at $252.97.

Intel reported first-quarter 2026 revenue of $13.6 billion, up 7% year-over-year. The Data Center and AI segment grew 22% to $5.1 billion. The company posted a GAAP net loss of $3.7 billion, or $0.73 per share, due to restructuring charges. Non-GAAP earnings per share were $0.29.

Intel guided second-quarter 2026 revenue between $13.8 billion and $14.8 billion. The company highlighted progress on its 18A process and AI CPU sales.

IBM posted first-quarter 2026 revenue of $15.9 billion, up 9% year-over-year, or 6% at constant currency. Software revenue reached $7.05 billion, up 11%. Infrastructure revenue increased 15% to $3.33 billion. Consulting revenue grew 4% to $5.27 billion.

IBM reported GAAP net income of $1.2 billion, or $1.28 per share. Operating non-GAAP earnings per share were $1.91. Free cash flow reached $2.2 billion. The company reiterated full-year 2026 expectations for more than 5% revenue growth at constant currency.

Valuation and Analyst Consensus

Analysts assigned Intel a consensus Hold rating with average price targets in the $70 to $81 range in some reports, though recent momentum pushed shares higher. Intel shares showed strong recovery from 2025 lows.

IBM carried a Moderate Buy consensus with an average 12-month price target near $294, suggesting potential upside. Some targets reached $360.

IBM showed higher revenue, earnings and net margins than Intel in the most recent quarter. IBM’s net margin was 15.61% compared to Intel’s negative figures in the period.

Business Strategies

Intel focused on regaining AI server share and advancing its foundry business under CEO Lip-Bu Tan. The company reported sold-out AI CPU capacity and explored partnerships, including with Tenstorrent. Challenges persisted in foundry profitability.

IBM emphasized hybrid cloud, Watsonx AI tools and quantum computing. The company announced plans for a U.S. quantum chip foundry and reported strong mainframe performance with the z17 model. Software and infrastructure drove growth.

Financial Metrics

Intel’s stock exhibited high volatility with a significant rebound in 2026. Operating cash flow in Q1 was $1.1 billion, with adjusted free cash flow negative due to capital expenditures.

IBM maintained stable financials with consistent profitability. Operating gross profit margin reached 57.7% in Q1 2026, up 110 basis points year-over-year.

Dividend and Returns

Both companies maintained dividends. IBM offered a yield around 3% with a history of consistent payments. Intel’s dividend faced scrutiny amid earlier losses but continued.

Risks and Outlook

Intel projected sequential revenue growth in client and data center segments for Q2, driven by supply and pricing. Risks included foundry execution and AI chip competition.

IBM projected continued software acceleration and free cash flow growth. Risks involved consulting execution and broader AI commercialization timelines.

Intel showed higher cyclical exposure compared to IBM’s enterprise focus. Stock movements in 2026 reflected these differences, with Intel displaying sharper rebounds.

Upcoming earnings include Intel in late July 2026 and IBM around July 22, 2026. Supply chain developments, AI adoption and quantum initiatives will influence both stocks through the remainder of 2026.

This comparison draws from company reports, analyst consensus and market data available through May 23, 2026. Investment decisions require individual assessment and professional advice. Actual results may vary based on economic conditions and execution.

A rebrand of the junction 32 retail park off the M62 has gone down poorly with some locals in Castleford.

Death toll in student dorm strike rises to 10, Russian-installed official says

The Barnacle is a quantitative analyst and has been in and out of the investing business since 2003. He is a former member of Marketocracy’s M100 Club. He has a degree in mathematics and believes that mathematics is the root of all success. If the numbers tell one to do something, then do it. When one reads his posts, one will realize that. Consequently, he does not put much stock in sell-side analysis, since most of it is pretty bad. he will share posts about value stocks that still have growth potential. This is not limited to large caps, but will also include midcaps, small caps, international stocks, gold miners, and REITs. Recently, his focus has been on ETF strategies that could potentially outperform the market’s overall return or provide better risk protection. He no longer focuses on individual stocks.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Weekly Commentary: The Warsh Fed

Business

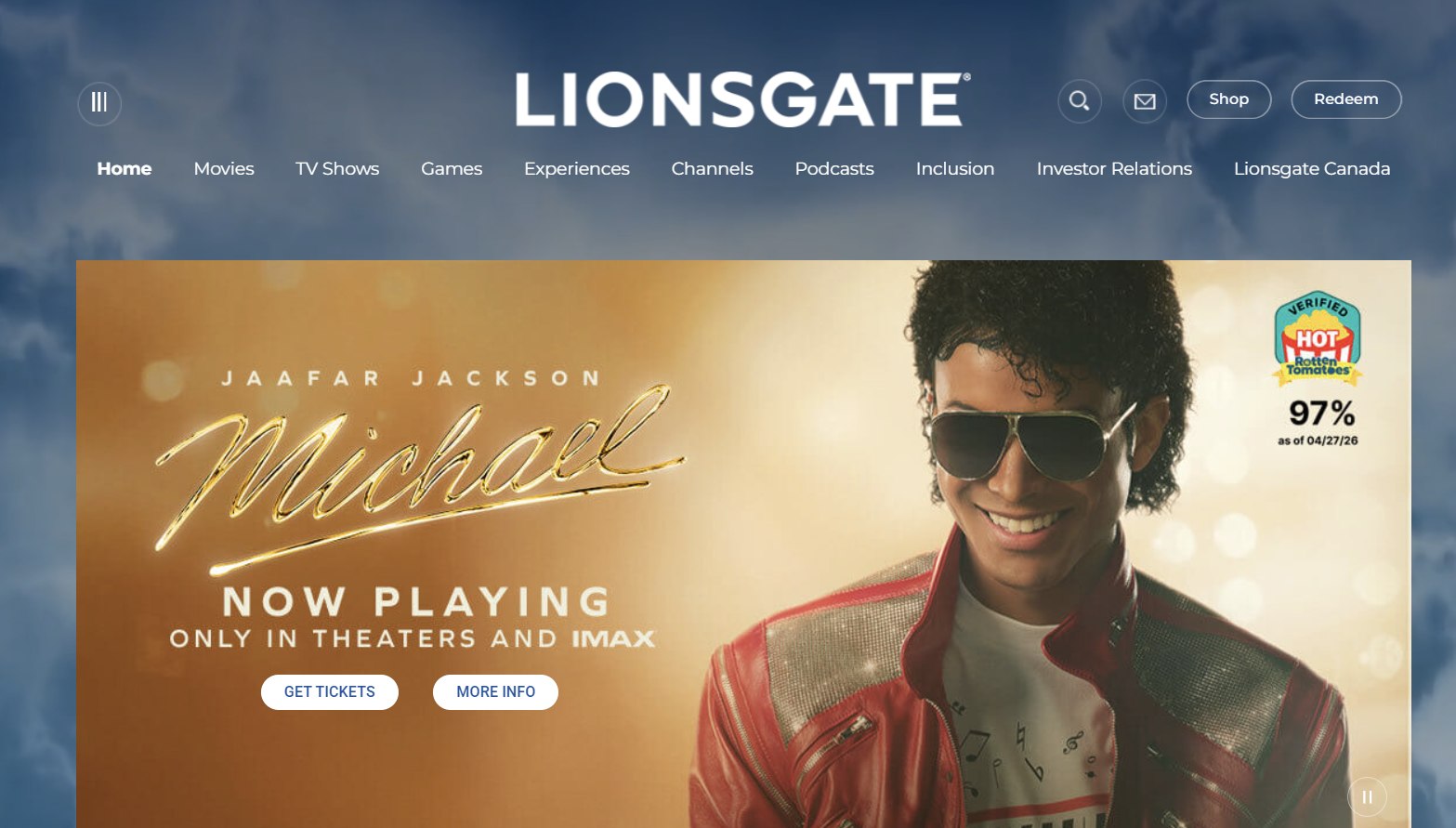

Lionsgate Studios LION Stock Rises 16% After Strong Q4 Earnings Beat and Film Slate Momentum

SANTA MONICA, Calif. — Lionsgate Studios Corp. shares climbed 15.80% to close at $14.95 on May 22, 2026, following the release of fiscal fourth-quarter 2026 results that exceeded analyst expectations on revenue and profitability.

The company reported revenue of $906.5 million for the quarter ended March 31, 2026, compared with $865.6 million in the year-ago period. Non-GAAP net income reached nearly $112 million, or $0.37 per share, more than tripling from the prior-year quarter.

Both figures surpassed consensus estimates of $809 million in revenue and $0.24 per share in adjusted net profit. Operating income totaled $117.5 million, up 52% year-over-year. Adjusted OIBDA stood at $165.4 million.

Motion Picture Segment Performance

The Motion Picture segment generated revenue of $651.9 million and segment profit of $187.1 million, increases of 23% and 39% respectively from the prior year. Performance was driven by the theatrical and ancillary results of “The Housemaid,” which grossed nearly $400 million worldwide, along with strong library sales.

“The Housemaid” also set records on premium video-on-demand and became the top Pay One title ever on STARZ.

Library and Other Metrics

Trailing 12-month library revenue topped $1 billion for the third consecutive quarter, rising 5% year-over-year. More than half of the company’s film, television and live entertainment slates consist of branded, repeatable properties.

CEO Jon Feltheimer stated, “All of the pieces of our business are coming together – our library has achieved a billion dollars in trailing 12-month revenue for three quarters in a row, more than half of our film, television and live entertainment slates are comprised of branded, repeatable properties, and massive hits like The Housemaid and Michael are strengthening our brand and increasing our forward visibility.”

Analyst Reactions

Benchmark maintained a Buy rating and raised its price target on Lionsgate Studios. Other firms including Baird and Morgan Stanley had issued upward target revisions in the weeks leading into earnings. Consensus price targets ranged from approximately $12 to $16 following recent updates.

Recent Film Success

Earlier in 2026, the Michael Jackson biopic “Michael” opened to $217 million globally in its first weekend, exceeding expectations and marking Lionsgate’s biggest opening since the pandemic.

Financial Position

The company reported improvements in free cash flow and adjusted OIBDA. Year-end leverage improved to 6.1 times. Lionsgate continues to focus on its library value and upcoming slate that includes multiple tentpole films.

Market Context

Lionsgate Studios operates as a standalone public company following its separation from Lions Gate Entertainment. The stock reached an all-time high during the May 22 session amid elevated trading volume. Shares have shown strong year-to-date performance in 2026, reflecting investor confidence in its content pipeline.

The company’s strategy emphasizes branded franchises and library monetization across theatrical, streaming and ancillary channels. Upcoming releases and television deliveries are expected to contribute to fiscal 2027 results.

Broader Industry Trends

Lionsgate competes in a dynamic entertainment landscape with major studios and streaming platforms. Its focus on mid-budget films and strong library has supported revenue stability amid industry shifts. Analysts project earnings growth in coming years tied to slate execution.

Lionsgate management will host its fiscal 2026 fourth-quarter earnings conference call on May 21, with a replay available afterward. Further details on fiscal 2027 guidance and film slate will be monitored in upcoming updates.

The May 22 stock movement reflected positive reaction to the earnings beat and optimism around recent box office results. Trading activity remained active into after-hours with shares around $14.91.

Business

(PHOTO) Meghan Markle Shares Unseen 2018 Wedding Photos on 8th Anniversary with Prince Harry

LOS ANGELES — Meghan Markle posted multiple never-before-seen photographs from her 2018 wedding to Prince Harry on May 19, 2026, to mark the couple’s eighth wedding anniversary.

The Duchess of Sussex shared two carousel posts on Instagram featuring previously unpublished images from the ceremony at St. George’s Chapel in Windsor and the reception. The photos included moments of the couple embracing, their first dance, Prince Harry toasting, and Elton John performing.

One post was captioned “Eight years ago today…☀️” with photo credit to royal photographer Chris Allerton. Markle did not include images of other members of the royal family such as King Charles III or Prince William in the shared collection. She did post a photo with her mother, Doria Ragland.

The couple married on May 19, 2018. The anniversary posts came amid reports of ongoing distance between the Duke and Duchess of Sussex and the British royal family. Prince Harry and Meghan Markle stepped back as working royals in 2020 and relocated to the United States.

Social Media Reactions

The anniversary posts drew a range of responses on social media platforms, including Reddit. Some users described the volume of photos — more than 20 across the posts — as notable for a non-milestone anniversary.

One Reddit user wrote, “She kept all the internal pics private and now, in a moment of desperation, unloads them all to get attention.” Another commented, “This is so beyond pathetic.” A third added, “She also posted SO MANY pictures. Feels desperate.”

Loyal fans of the couple praised the intimate glimpses into the 2018 ceremony and reception. The posts quickly gained significant engagement across Instagram.

Anniversary Details

Additional posts from Markle showed the couple celebrating with their children, Prince Archie and Princess Lilibet. Images included cutting a lemon elderflower cake. Prince Harry reportedly gifted Markle a bronze penguin sculpture, referencing an element from their early relationship.

The 2018 wedding was watched by hundreds of millions worldwide. Meghan Markle wore a minimalist Givenchy gown designed by Clare Waight Keller with a 16-foot veil. The ceremony featured notable guests including Elton John and other celebrities.

Recent Context

Reports in May 2026 indicated Prince Harry has expressed interest in reconciling with his family while Markle has focused on her lifestyle brand “As Ever” in the United States. The couple has maintained a private life in California with their two children.

This marked one of the first times Markle shared such a large collection of intimate, previously unseen wedding images publicly. The timing coincided with ongoing public interest in the couple’s life post-royal duties.

Public Interest

The anniversary posts generated widespread coverage across entertainment and royal news outlets. Discussions focused on the couple’s continued use of social media to share personal milestones despite previous requests for privacy.

Markle has maintained an active Instagram presence. The wedding anniversary content aligned with her pattern of occasional personal posts mixed with promotional activity for her brand initiatives.

The Duke and Duchess of Sussex have not issued additional joint statements on the anniversary beyond the shared photographs. Buckingham Palace has not commented on the posts.

Background on the Couple

Prince Harry and Meghan Markle met in 2016 and announced their engagement in 2017. Their wedding in 2018 was a global event broadcast live. The couple welcomed Archie in 2019 and Lilibet in 2021. They relocated to Montecito, California, after stepping back from senior royal roles.

Since leaving the United Kingdom, they have pursued media projects, including a Netflix series and Prince Harry’s memoir “Spare.” Markle has launched lifestyle ventures including the brand “As Ever.”

The couple has faced ongoing public scrutiny regarding their relationship with the royal family. Reports of internal differences have circulated periodically but remain unconfirmed by official statements from either side.

Broader Royal Developments

As of May 2026, King Charles III continues public duties following his cancer diagnosis and treatment. Prince William and Catherine, Princess of Wales, have maintained their schedule of royal engagements. The Sussexes have operated independently from the main royal household.

The anniversary posts highlighted the couple’s focus on their own family narrative eight years after the highly publicized royal wedding. The images provided fans with new perspectives on the event while avoiding direct references to other royal family members.

Williams Companies’ SWOT analysis: midstream stock eyes power growth

Every Financial Trap You’ll Face As Your Net Worth Grows

How to live Harry Styles’ low key London life

FIIs sell over Rs 30K crore worth of Indian equities in May as outflows swell to Rs 2.22 lakh crore. What lies ahead?

-

Crypto World2 days ago

Crypto World2 days agoBlockchain.com files with SEC for U.S. IPO

-

Fashion16 hours ago

Fashion16 hours agoHoliday Weekend Open Thread – Corporette.com

-

Crypto World6 days ago

Crypto World6 days agoIntesa Sanpaolo’s crypto holdings jump to $235M as XRP enters

-

Business19 hours ago

Business19 hours agoDell Technologies DELL Stock Surges 15% on AI Server Momentum and Analyst Upgrades in 2026

-

Crypto World19 hours ago

Crypto World19 hours agoSpace X IPO Is ‘Bad News’ for Tech Stocks: But What About Bitcoin?

-

Fashion6 days ago

Fashion6 days agoOn the Scene at Gucci’s Cruise Show in New York City: Mariah Carey, Kim Kardashian, Lindsay Lohan, Iman, and More!

-

Politics7 days ago

Politics7 days agoWatch: far-right flag-fanatics run over victim, attack locals – Setup By the Left wing for your entertainment

-

Fashion7 days ago

Fashion7 days agoTrending Western Style Vests Perfect for Summer

-

Politics15 hours ago

Politics15 hours agoMakerfield: a tale of two social-media histories

-

Fashion6 days ago

Fashion6 days agoAmazon Sundays: Memorial Day Hosting

-

Entertainment6 days ago

Entertainment6 days agoOff Campus Easter Eggs Explained: Characters, Stories, More

-

Tech21 hours ago

Tech21 hours agoA 0.12% parameter add-on gives AI agents the working memory RAG can’t

-

Crypto World5 days ago

Crypto World5 days agoRevolut Launches Dogecoin Debit Card Across UK and EU

-

Crypto World20 hours ago

Crypto World20 hours agoAI infrastructure race heats up as IREN pitches full-stack strategy, WhiteFiber lands $160M deal

-

NewsBeat2 days ago

NewsBeat2 days agoCharity run by Reform leader Malcolm Offord accused of ‘law breaking’ over Scottish registration

-

Sports1 day ago

Sports1 day ago2026 CJ Cup Byron Nelson leaderboard: Brooks Koepka finds putting stroke in Round 1

-

Crypto World1 day ago

Crypto World1 day agoBitcoin Accumulation Weakens as BTC Realized Losses Hit $600M

-

Business6 days ago

Australia defends property tax changes designed to fix ‘broken’ housing

-

Crypto World1 day ago

Crypto World1 day agoTrump Media’s Bitcoin Stash Shrinks Again as 2,650 BTC Lands on Crypto.com

-

Tech1 day ago

Tech1 day agoWhatsApp ads could make Irish debut after discussions with DPC

You must be logged in to post a comment Login