Crypto World

Pi Network Price Prediction: Can PI Reclaim $0.20?

Pi trades near $0.12, sitting on its all-time low, down roughly 95% from its peak. Getting back to $0.20 would take a 60% gain. This guide weighs the unlocks and thin liquidity dragging it down against the upgrades and the Pi2Day catalyst that bulls are counting on.

Summary

- Pi trades near $0.12-$0.13, sitting on or just below its all-time low near $0.13, down roughly 95% from its post-listing peak above $2.90.

- Reclaiming $0.20 would require a gain of roughly 60% from current levels, a large move against a year-long downtrend, and persistent selling pressure.

- The core drag is supply meeting weak demand: ongoing token unlocks add millions of coins while 24-hour volume sits below $10 to 26 million against a market cap over $1.3 billion, a sign of thin liquidity.

- The bull case rests on catalysts: the annual Pi2Day event, newly launched smart contracts, a growing app ecosystem, and the long-awaited possibility of a major exchange listing.

- Reclaiming $0.20 before year-end is possible but demanding, requiring real demand to finally outpace the unlocks, with the more likely path a continued grind unless a genuine catalyst lands.

Pi Network’s token trades near $0.12, sitting on or just below its all-time low, and the question for the rest of 2026 is whether it can claw its way back to $0.20, a level that would require a gain of roughly 60% from where it stands now. That framing matters because $0.20 is not an arbitrary target; it is the level Pi traded around as recently as late 2025 before its latest decline, a psychological and technical zone that, if reclaimed, would signal that the relentless downtrend has finally broken.

Getting there, though, means overcoming the forces that have driven Pi down roughly 95% from its post-listing peak above $2 and $0.90: a steady stream of token unlocks that keep adding supply, thin trading liquidity that makes the token fragile, weak real-world utility, and the conspicuous absence of a listing on a major tier-one exchange.

Against those headwinds stand a set of genuine catalysts that Pi’s large community is counting on, including the network’s annual flagship event, the recent arrival of smart contracts, a growing roster of ecosystem apps, and the ever-present possibility of a major listing. This piece weighs the two sides honestly to assess whether a move back to $0.20 is realistic before the year ends.

The reason to frame Pi’s prediction around the twenty-cent question, rather than the wildly divergent multi-year targets that fill most prediction pages, is that Pi’s situation is fundamentally a near-term contest between supply and demand, and $0.20 is the concrete level at which that contest would be visibly resolved in the bulls’ favor.

The wildly optimistic long-term forecasts that some sites publish, and the community calls for prices many multiples higher, are largely disconnected from the mechanics actually driving Pi’s price right now, which are the unlock schedule, the thin liquidity, and the search for real demand.

What follows traces how Pi reached its all-time low, maps the levels that matter, examines the supply problem that defines the token, weighs the catalysts that could spark a recovery against the forces holding it down, and lays out concrete bull, base, and bear scenarios for whether $0.20 is reachable before year-end.

A long way back to $0.20

Start with the distance Pi has to travel, because it frames everything. At roughly $0.20, Pi sits on or just beneath its all-time low near $0.13, having fallen relentlessly from a peak above $2 and $0.90 recorded shortly after its broader market availability. That is a decline of roughly 95%, the kind of drawdown that leaves a token searching for any sign of a floor.

To reclaim $0.20 from $0.12 requires a gain of around 60%, which in the context of crypto is far from impossible over a year, but which represents a major reversal for an asset that has done little but fall and that faces continuous selling pressure from new supply.

The $0.20 level is meaningful precisely because Pi traded around it as recently as the fourth quarter of 2025, before sliding below it and then below subsequent support levels through the first half of 2026, so reclaiming it would mark a genuine break from the established downtrend.

The path to $0.20 was a steady erosion rather than a single collapse. Pi traded in a higher range through much of 2025, with periods in the $0.30-$0.40, before momentum faded in the second half of the year and the price slipped into the twenties and then below.

In early 2026, it broke beneath the twenty-cent area that had served as support, and subsequent attempts to rally, often fueled by ecosystem announcements, failed to hold, with the price repeatedly rejected at higher levels before resuming its decline toward the all-time low.

The token now trades below all of its major moving averages with momentum indicators in or near oversold territory, the technical signature of a sustained downtrend that has not yet found its bottom. The 60% climb back to $0.20, in other words, would have to overcome both the weight of a year-long decline and the specific forces that have driven it, which is why the question is genuinely open rather than a foregone conclusion in either direction.

The levels: $0.097 below, $0.20 above

The technical map around Pi is worth laying out, because it defines how much room there is on each side. Immediately around the current price, support sits in the area of $0.130-$0.135, the zone of the all-time low, with a break below it pointing toward lower levels that some analysts identify near $0.10, and a deeper “ultimate support” flagged around $0.09-$0.10.

These are the downside markers: losing the all-time low would open the door to single-digit-cent territory, a prospect that underscores how fragile the current level is. The fact that Pi is testing its all-time low at all means there is little historical price structure beneath it to provide support, which is part of what makes the downside risk real.

On the upside, the resistance levels are stacked and meaningful, which is what makes the climb to $0.20 demanding. The first hurdle sits near $0.14, with a more significant barrier around $0.16, the level that has recently capped rallies. Above that, the seventeen-to-nineteen-cent zone represents further resistance, and then $0.20 itself, the target, sits at the top of this band as both a psychological round number and a former support-turned-resistance level.

For Pi to reclaim $0.20, it would have to break through this entire stack of resistance in succession, each level representing a point where sellers, including holders looking to exit losing positions and recipients of newly unlocked tokens, are likely to apply pressure.

The structure is therefore asymmetric in a worrying way for bulls: relatively little support beneath the all-time low, and multiple layers of resistance between the current price and the twenty-cent target. Climbing that wall requires sustained buying pressure that has been conspicuously absent, which brings the analysis to the core problem.

The supply problem nobody can ignore

The single most important factor weighing on Pi’s price is the imbalance between supply and demand, and it is worth understanding in detail because it defines the token’s predicament. Pi has a very large maximum supply, and a substantial portion of the total has yet to enter circulation, held back by lock-up mechanisms that release tokens on a schedule. As those unlocks occur, new supply enters the market, and in June alone, the network was set to unlock well over 170 million tokens worth tens of millions of dollars.

This is the crux of the problem: every unlock adds coins that can be sold, and unless demand grows fast enough to absorb them, the additional supply pushes the price down. For a token already in a downtrend, a steady stream of unlocks acts as a persistent headwind, continually replenishing the supply available to sell into any rally.

Compounding the supply pressure is the thinness of Pi’s trading liquidity, which is striking given its size. Despite a market capitalization above $1 billion, Pi’s 24-hour trading volume has at times fallen below $10 million and generally sits in the low tens of millions, an unusually small amount of trading for a token of that nominal value. Thin liquidity makes a token fragile in both directions, but especially on the downside, because relatively small amounts of selling can move the price significantly when there are few buyers, and the steady supply from unlocks meets a market without deep enough demand to absorb it.

This combination, ongoing unlocks adding supply into a thinly traded market with weak organic demand, is the fundamental reason Pi has ground lower, and it is the central obstacle to any recovery toward $0.20. Until demand grows enough to outpace the unlocks and deepen the liquidity, the supply problem will keep exerting downward pressure, which is why the bull case has to rest on catalysts large enough to change the demand side of the equation.

The bull case: catalysts that could spark a move

For Pi to reclaim $0.20, demand has to finally outpace the unlocks, and the bull case rests on a set of catalysts that could, in principle, drive that demand, several of which are concrete and near-term.

The most immediate is the network’s annual flagship event, held in late June, which has historically served as a moment for major ecosystem announcements, including new applications, developer initiatives, and feature launches. Because the community anticipates this event as a catalyst, it can drive a surge of engagement and speculative buying around the date, and a slate of well-received announcements could refresh the narrative around Pi and spark the kind of demand the price needs.

The event functions as a recurring opportunity for a positive surprise, and with it falling just days away from the current moment, it is the most time-sensitive catalyst on the horizon.

The deeper bull case rests on the network’s technical progress and ecosystem growth. Pi recently introduced smart contracts through a series of protocol upgrades, a significant capability that opens the door to decentralized finance, real-world asset tokenization, and more complex applications, potentially giving the token the genuine utility it has lacked.

The ecosystem has shown early signs of life, with new applications and games attracting tens of thousands of users in short periods, developer tools expanding, and initiatives to make it easier for builders to launch apps and reach Pi’s large user base.

If this ecosystem activity translates into real, sustained usage that creates organic demand for the token, it could begin to absorb the unlock supply and shift the supply-demand balance. And hanging over everything is the possibility, long rumored and long awaited, of a listing on a major tier-one exchange, which would dramatically expand access, liquidity, and visibility, and which many in the community view as the single catalyst most capable of driving a substantial repricing.

Each of these, the event, the smart contracts, the ecosystem, and a potential major listing, is a plausible source of the demand a recovery would require, which is what keeps the bull case alive despite the bearish chart.

The bear case: why $0.20 may stay out of reach

Honesty requires giving equal weight to the case that $0.20 stays out of reach, because the bearish argument is grounded in the same structural realities that have driven Pi to its all-time low.

The foundation is the supply problem: the unlocks are scheduled and will continue regardless of sentiment, so unless demand grows substantially and consistently, the steady addition of new supply will keep capping rallies and pressuring the price, making a 60% climb against that headwind genuinely difficult.

The thin liquidity reinforces this, because even if demand picks up, the shallow market can be overwhelmed by unlock-driven selling, and the absence of deep order books makes sustained rallies hard to hold.

The bearish case is reinforced by the demand side’s persistent weakness. Despite a large user base, Pi has struggled to translate that into real economic activity that creates organic token demand, with utility remaining limited and much of the trading driven by speculation instead of usage.

The much-anticipated catalysts have, in the past, repeatedly failed to produce sustained demand: ecosystem announcements have sparked brief rallies that faded, and the major exchange listing that the community counts on has not materialized despite years of anticipation, with no guarantee it ever will.

The risk around the annual event is that announcements fail to meet the community’s high expectations, which could trigger sell pressure instead of a rally. And Pi remains exposed to the broader crypto market, where a weak environment for altcoins provides little tailwind.

The bearish synthesis is that Pi’s problems are structural and have repeatedly defeated the same catalysts the bulls are counting on, so the most likely path is a continued grind near or below the all-time low, with $0.20 remaining out of reach unless something truly changes the demand side in a durable way.

One widely cited analysis has flagged a path toward $0.10 as a real possibility if unlocks keep outrunning demand.

The bull, base, and bear cases for year-end

Tying the scenarios to the supply-demand contest and the catalysts makes them concrete. These are conditional ranges, not predictions, and each depends on whether demand can outpace the unlocks.

- Bull case: a genuine catalyst lands, whether a strong slate of announcements at the annual event, real adoption of the new smart-contract capabilities, breakout ecosystem usage, or a long-awaited major exchange listing, and demand finally outpaces the unlock supply. Pi breaks through the stack of resistance from fourteen to $0.19 and reclaims $0.20 before year-end, with the upper end of optimistic ranges pointing toward the high $0.20-$0.40 if a major listing in particular materializes.

- Base case: Pi continues to grind in a low range near its all-time low, roughly $0.12-$0.18, as the unlocks and thin liquidity cap rallies while the ecosystem develops too slowly to generate the demand needed for a decisive breakout. In this scenario, the catalysts produce brief rallies that fade, $0.20 is approached at best but not reclaimed durably, and the token ends the year near where it began the second half.

- Bear case: the unlocks continue to outpace weak demand, the anticipated catalysts disappoint, no major listing arrives, and a soft broader market provides no support. Pi loses its all-time low and slides into single-digit-cent territory toward $0.10 or below, with $0.20 firmly out of reach and the structural supply problem dominating.

What to watch

For anyone tracking whether Pi can reclaim $0.20, the analysis points to a clear watchlist, and the first item is the annual event and its immediate aftermath. Because the late-June event is the most time-sensitive catalyst, the substance of its announcements and the market’s reaction will be an early and telling signal: a strong, well-received slate that drives sustained buying would support the bull case, while announcements that disappoint and a rally that fades would reinforce the bearish pattern of catalysts failing to produce lasting demand. Watching how Pi trades around and after the event is the most immediate test.

The second item is the perennial question of a major exchange listing, which remains the single catalyst most capable of a substantial repricing; any credible news of a tier-one listing would be a powerful bullish signal, while continued absence keeps a key source of liquidity and demand off the table.

The third item is the relationship between the unlocks and demand, which is the structural heart of the matter: watching whether trading volume and on-chain usage grow enough to absorb the scheduled unlock supply, or whether the unlocks continue to outpace demand, will indicate which direction the supply-demand balance is tipping. The fourth item is the adoption of the new smart-contract capabilities, and the ecosystem’s growth, since real, sustained usage is what would create the organic demand a durable recovery requires, as opposed to the speculative rallies that have repeatedly faded.

The honest synthesis is that reclaiming $0.20 is possible but demanding, requiring demand to finally and durably outpace the persistent unlock supply, and that, absent a genuine catalyst of sufficient size, the more likely path is a continued grind near the all-time low. The catalysts that could change this are real, and some are near-term, but Pi’s history is a string of catalysts that sparked brief hope and faded, so the burden of proof rests firmly on demand actually showing up this time.

Frequently Asked Questions

Why is Pi trading near its all-time low?

Because of a persistent imbalance between supply and demand. Pi has a very large maximum supply, much of it released gradually through scheduled unlocks, and in some months, well over 100 million tokens enter circulation. That steady new supply meets weak organic demand and unusually thin trading liquidity, with twenty-four-hour volume sometimes below $10 million despite a market cap of over 1 billion. The result is continuous downward pressure: new supply gets sold into a shallow market without enough buyers to absorb it, driving Pi down roughly 95% from its post-listing peak to its current all-time low area near $0.12-$0.13.

What would it take for Pi to reach $0.20?

Demand would have to finally and durably outpace the unlock supply, which requires a genuine catalyst. The most immediate is the network’s annual late-June event, which can drive engagement if its announcements are strong. The deeper drivers would be real adoption of Pi’s new smart-contract capabilities, breakout ecosystem usage that creates organic token demand, and, most powerfully, a listing on a major tier-one exchange, which would expand access and liquidity. Reclaiming $0.20 from $0.12 is a roughly 60% gain, achievable in crypto over a year but demanding against the unlock headwind, so it depends on demand truly showing up.

What is the supply problem with Pi?

Pi has a large maximum supply, and a substantial portion has not yet entered circulation, held back by lock-up mechanisms that release tokens on a schedule. As these unlocks occur, new coins enter the market and can be sold, and unless demand grows fast enough to absorb them, the added supply pushes the price down. For a token already in a downtrend with thin liquidity, this acts as a persistent headwind, continually replenishing the supply available to sell into rallies. The supply problem is the central obstacle to any recovery, because it must be outpaced by demand for the price to rise durably.

Why does Pi’s thin liquidity matter?

Because it makes the token fragile and amplifies the supply problem. Despite a market cap over $1 billion, Pi’s daily trading volume often sits in the low tens of millions or below, unusually small for a token of that size. Thin liquidity means relatively small amounts of selling can move the price significantly when buyers are scarce, so the steady supply from unlocks meets a market without the depth to absorb it smoothly. It also makes rallies hard to sustain, because shallow order books can be overwhelmed. Deepening liquidity, which a major exchange listing would help with, is part of what a durable recovery would require.

Could Pi fall below its all-time low?

Yes, that is the bear scenario, and it is a real risk. Because Pi is testing its all-time low, there is little historical price structure beneath it to provide support, so a decisive break lower could open the door to single-digit-cent territory, with analysts identifying levels near $0.10 and a deeper floor below that. This would happen if the unlocks continue to outpace weak demand, the anticipated catalysts disappoint, no major listing arrives, and the broader market stays soft. One widely cited analysis has flagged a path toward $0.10 as a genuine possibility if supply keeps overwhelming demand.

Are the bullish long-term Pi price predictions realistic?

Most of the very high long-term targets that circulate, including community calls for prices many multiples above current levels, are largely disconnected from the mechanics actually driving Pi’s price, which are the unlock schedule, thin liquidity, and weak demand. Reaching even $1, let alone the far higher figures some promote, would require a combination of full ecosystem adoption, sustained real usage, and much broader exchange access than exists today, and figures in the hundreds or thousands of dollars are not grounded in any realistic near or medium-term scenario. A disciplined view focuses on the near-term supply-demand contest instead of speculative long-range targets.

This article is information, not investment advice. The scenarios described are conditional ranges that depend on unresolved questions, not predictions, and Pi is highly volatile with thin liquidity. Prices, unlock schedules, and ecosystem developments reflect reporting available as of June 26, 2026, and can change quickly. Nothing here is a recommendation to buy or sell. Verify current data from primary sources and consider your own circumstances before making any decision.

Tether's USDT has drawn level with ether, narrowing the gap for the second-largest cryptocurrency by market capitalization to a fraction of a percent. The stablecoin briefly overtook ether earlier this month, the first time a dollar-pegged token has done so. USDT carried a market cap of about… Read the full story at The Defiant

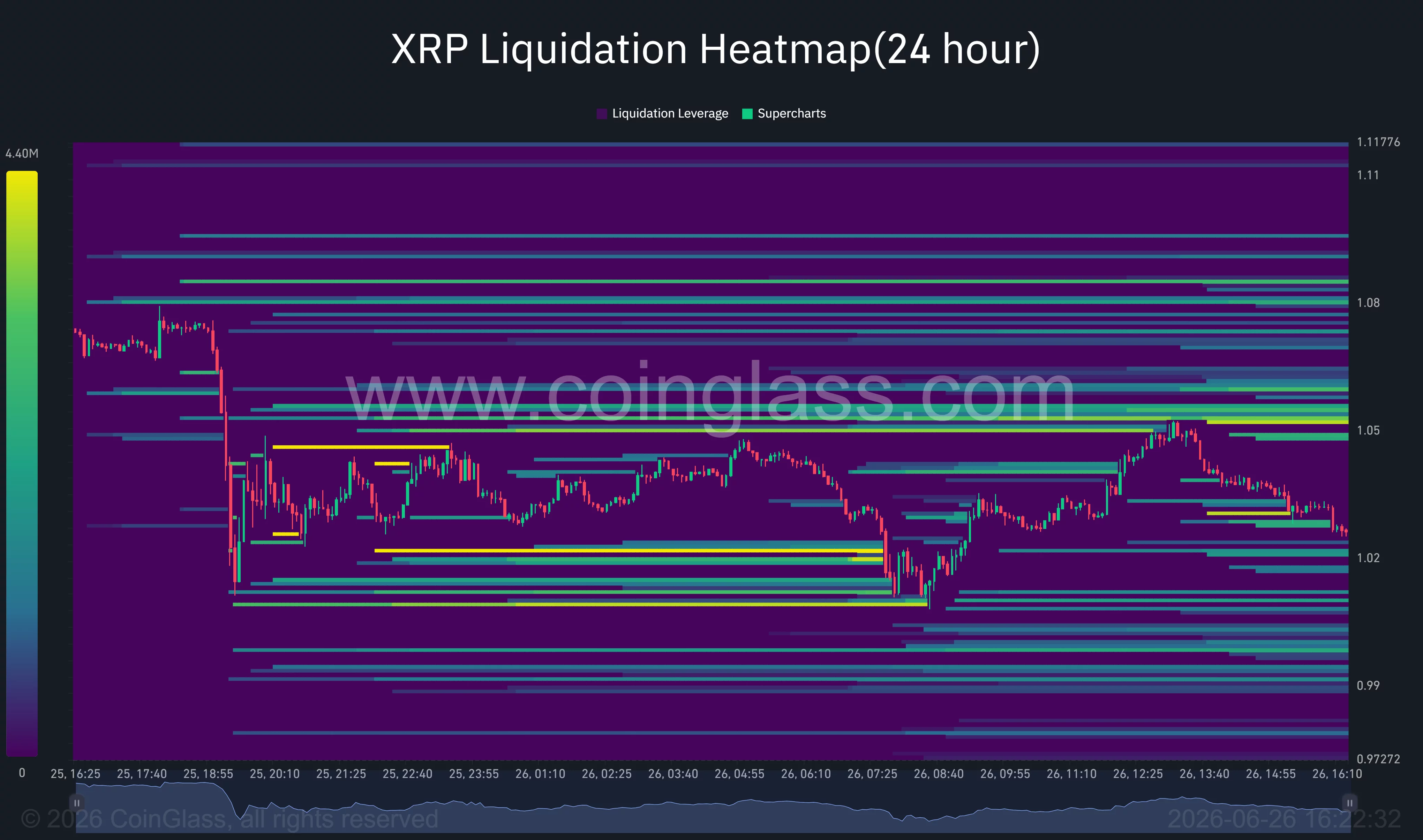

XRP has fallen to its lowest level in months after a sharp selloff driven by a major derivatives flush and fresh pressure across the crypto market, while technical charts now show the token testing the lower boundary of a long-term falling wedge.

Summary

- XRP has fallen toward the key $1 support after a $10.8 billion crypto options expiry triggered heavy market-wide selling.

- A multi-month falling wedge and oversold momentum indicators suggest the token is nearing a critical technical inflection point.

- Analysts warn a break below $1 could expose lower support zones, while reclaiming $1.10 would improve the bullish outlook.

According to data from crypto.news price, XRP (XRP) price dropped from around $1.07 on June 25 to $1.01 on June 26, extending its year-to-date decline to more than 40%. The decline accelerated as a $10.8 billion crypto options expiry triggered heavy volatility across digital assets and forced a wave of long liquidations.

At the same time, sentiment surrounding the XRP ecosystem weakened after decentralized finance protocol Strobe Finance abruptly announced it would shut down operations.

The selling pressure arrived as investors also reduced exposure to risk assets following stronger expectations that the U.S. Federal Reserve could keep interest rates higher for longer. Bitcoin’s slide below the $60,000 level removed another layer of support for altcoins, leaving XRP among the weaker large-cap tokens during Thursday’s session.

XRP approaches long-term support as liquidation clusters build overhead

The daily chart shows XRP trading at the lower edge of a falling wedge that has contained price action for almost a year. The pattern has compressed between descending resistance and gradually declining support, with the token now sitting close to the wedge’s lower boundary near $1.00.

Momentum indicators remain weak. The MACD has stayed below its signal line with histogram bars still in negative territory, while the Aroon indicator continues to favor sellers after Aroon Down climbed back toward 100 and Aroon Up remained subdued. Together, the indicators suggest bears still control the short-term trend even as XRP price approaches a historically important support zone.

The four-hour chart presents another important technical level. XRP has retraced almost the entire advance measured by the displayed Fibonacci range and now trades just above the 100% retracement near $1.01. Price also remains below the Supertrend resistance around $1.10, while the RSI has slipped to nearly 31, placing momentum close to oversold territory but without confirming a bullish reversal.

Derivatives positioning also highlights where volatility could increase next. CoinGlass liquidation heatmap data show large concentrations of leveraged positions clustered between roughly $1.05 and $1.08, while another sizable liquidity pocket sits around the $1.02 area. Those zones could attract price in either direction as traders compete for liquidity, increasing the likelihood of sharp short-term swings.

On-chain positioning has also drawn attention to nearby support. According to well-followed analyst Ali Martinez, UTXO Realized Price Distribution data identify $1.06 as a major accumulation level where more than 830 million XRP previously changed hands.

“XRP is testing a major volume block at $1.06…If the market drops below this level, the next core support targets are $0.80, $0.62 and $0.51.”

Bears retain control while lower demand zones come into focus

Several downside risks could still invalidate any recovery attempt. A sustained move below the wedge support around $1.00 would break one of XRP’s longest-running chart structures and could expose lower historical demand zones identified by both technical and on-chain data.

Commenting on the latest structure, crypto analyst ChartNerd noted that XRP has entered an area of interest after weeks of decline but warned that losing the current support would shift attention toward the $0.90-$0.70 range, where previous buying activity was concentrated.

$XRP has continued to decline into our area of interest since our last update two weeks ago. The deeper price retraces, the stronger the risk-reward setup becomes. If the new local $1.00 low is swept, the next major demand zone sits in the $0.90/$0.70 region. https://t.co/IzZZOIksTy pic.twitter.com/5K0KwKmTpr

— 🇬🇧 ChartNerd 📊 (@ChartNerdTA) June 26, 2026

Any recovery will also depend on conditions outside the XRP market. Additional institutional outflows from crypto investment products, another round of heavy derivatives liquidations, or stronger-than-expected U.S. economic data that reinforce expectations for restrictive Federal Reserve policy could extend pressure across digital assets.

Conversely, reclaiming the $1.10 region and breaking above the falling wedge resistance would be the first technical signal that buyers are regaining control.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

At least three Strategy officials published coordinated investor reassurances Friday morning, as bitcoin traded around $59,600 and the company's STRC preferred shares languished near record lows of $73-75. Executive Chairman Michael Saylor, bitcoin executive Chaitanya Jain and President and CEO… Read the full story at The Defiant

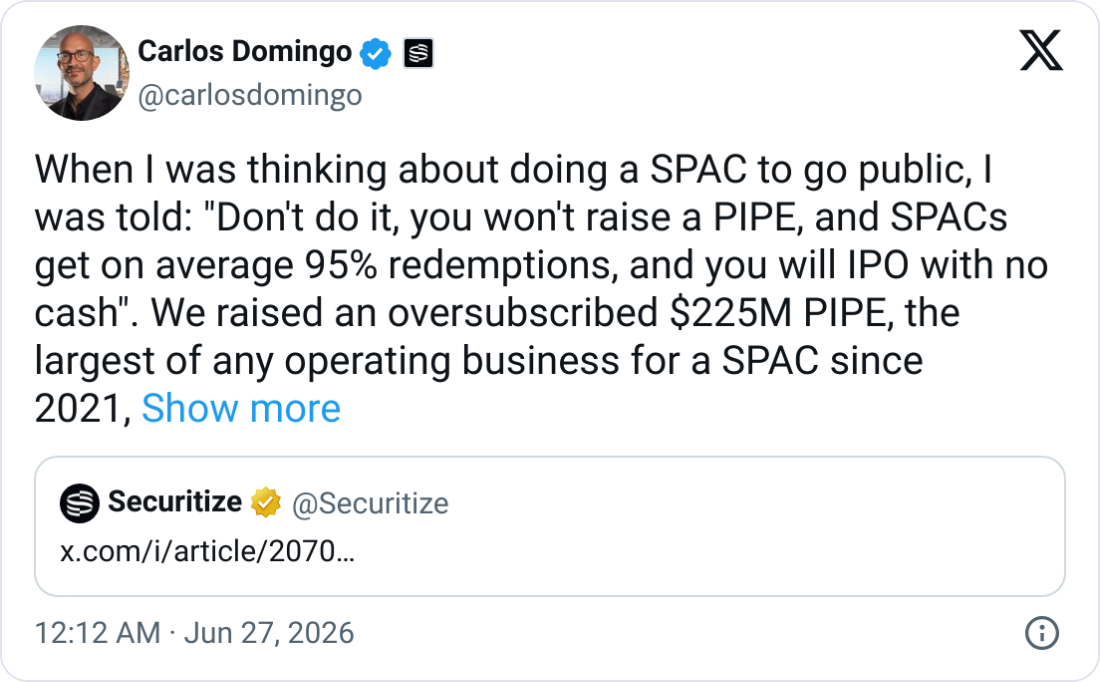

Tokenization platform Securitize says it expects to raise $400 million in its upcoming public debut through a merger with a company backed by Cantor Fitzgerald.

Securitize said on Friday that its final redemption results showed less than 30% of shareholders in Cantor Equity Partners II (CEPT), the special purpose acquisition company that will take Securitize public, had elected to redeem.

The company said it expects to receive approximately $400 million in gross proceeds from the merger, including related private investment in public equity, or PIPE, financings and excluding transaction-related expenses.

Securitize is set to be the latest buzzy crypto-related public debut as Wall Street seeks exposure to tokenization, an area that is seeing heightened investor interest and attention from US regulators.

Shares in Cantor’s acquisition vehicle rose on Friday, closing the trading day up 7% to $10.86 and continuing to rise after-hours to $11.

CEPT shares climbed on Friday as Securitize announced fewer shareholder redemptions than expected. Source: Google Finance

The merger between Securitize and CEPT is expected to close on Wednesday, July 1, subject to shareholder approval on Monday and other closing conditions, and the company will then trade under the ticker SECZ on the New York Stock Exchange on Thursday, July 2.

“Reaching the public markets is a significant milestone for Securitize and a reflection of the growing momentum behind tokenization,” said Securitize co-founder and CEO Carlos Domingo.

Source: Carlos Domingo

“When we started more than eight years ago, the idea that major institutions would embrace tokenized securities was still largely theoretical,” Domingo added. “Today, tokenization is moving into the mainstream.”

Related: Franklin Templeton, BNP Paribas see tokenization boosting EU’s capital efficiency

Securitize is backed by major institutions, such as BlackRock and Morgan Stanley, and crypto firms, including Coinbase and Circle, and has carved out a lead in the tokenization sector, where assets are represented on blockchains.

The company partnered with the New York Stock Exchange in March to create tokenized assets for the exchange’s upcoming tokenized securities platform,

Standard Chartered said earlier this month that it expects the amount of tokenized assets active in decentralized finance to grow 37-fold to $2.7 trillion by the end of 2030.

In mid-May, the US Securities and Exchange Commission was reportedly ready to allow trading of tokenized stocks, but delayed the plan later that month after stock exchange officials raised concerns over how it would be implemented.

Magazine: Bitcoin slides to $58K, XRP hits $1 but onchain data promising: Market Moves

Brad Garlinghouse has criticized Michael Saylor’s Bitcoin acquisition strategy, arguing that Strategy’s reliance on preferred stock financing has failed to create lasting value as its securities continue to weaken.

Summary

- Brad Garlinghouse criticized Strategy’s Bitcoin funding model, arguing long-term value should come from utility rather than financial engineering.

- Growing scrutiny of Strategy includes a shareholder investigation, insider share sales, and CryptoQuant’s call to preserve cash.

- Anchorage Digital said investors remain defensive, but options markets are not signaling expectations of a company-specific crisis.

According to comments made during a CNBC interview on Friday, Ripple CEO Brad Garlinghouse criticized Michael Saylor’s approach to financing Bitcoin purchases through Strategy’s capital markets program, saying long-term value in crypto should come from real-world utility rather than financial engineering.

Questioning whether the model can continue rewarding shareholders over time, Garlinghouse argued that issuing securities to fund additional Bitcoin purchases does not create sustainable value. He added that Strategy’s focus on financial structuring has had negative consequences for the digital asset market.

“Financial engineering does not drive long-term value … long-term value of any digital asset is going to be driven by utility.”

Although he challenged Strategy’s funding model, Garlinghouse maintained that he remains bullish on Bitcoin itself. His comments came as Bitcoin briefly traded below $60,000 on Friday, extending pressure across companies closely tied to the cryptocurrency.

Strategy’s preferred stock has come under pressure

Garlinghouse pointed to Strategy’s STRC preferred shares as evidence that investors are becoming more cautious about the company’s financing structure. He noted that the preferred stock has fallen roughly 25% below its $100 face value, describing the decline as a sign that investors are questioning the sustainability of the approach.

Strategy has spent roughly the past year raising capital through preferred securities, including STRC, to finance additional Bitcoin purchases. The instrument also carries an 11.5% cumulative annual dividend obligation, leaving the company with continuing dividend commitments alongside its expanding Bitcoin treasury.

At the same time, scrutiny has widened beyond Garlinghouse’s criticism. Earlier this week, on-chain analytics firm CryptoQuant recommended that Strategy pause further Bitcoin purchases and instead strengthen its cash reserves as market conditions remain difficult.

Additional pressure has emerged from legal developments. As crypto.news reported previously, Rosen Law Firm has opened an investigation into whether Strategy made materially inaccurate business disclosures to investors. According to the firm, it is evaluating potential securities claims and considering a possible class action lawsuit on behalf of shareholders who suffered losses.

Investor scrutiny has continued despite mixed market signals

Selling by company insiders has added another layer to investor concerns. SEC filings show Strategy director Jarrod Patten exercised options to acquire 1,500 Class A shares on June 23 before selling the entire position the same day at $106.08 per share, generating an estimated pre-tax gain of about $131,766.

The latest transaction extends a months-long selling streak. Regulatory filings indicate Patten has sold 55,750 Strategy shares over the past three months for roughly $9 million in proceeds, with the sales taking place as investors continue debating the company’s reliance on repeated share issuance and leveraged Bitcoin accumulation.

Even so, derivatives markets are not signaling expectations of an immediate company-specific crisis. According to new research from Anchorage Digital, traders continue paying elevated premiums for downside protection across Bitcoin, BlackRock’s iShares Bitcoin Trust and Strategy shares, but options pricing remains well below levels seen during previous periods of severe stress.

Anchorage Digital’s head of research, David Lawant, wrote that while defensive positioning has risen into the upper range of historical readings, Strategy’s options market has not reached the conditions normally associated with forced deleveraging or fears of a breakdown in the company’s business model.

A conditional national trust bank charter, a pending Federal Reserve master account, and a string of acquisitions in brokerage, payments, and treasury. Ripple is assembling a full regulated-finance stack. The benefits flow first to its stablecoin and the company itself. What is left for XRP is the question.

Summary

- Ripple has assembled a full regulated-finance stack: a conditional national trust bank charter, a pending Federal Reserve master account bid, and acquisitions in prime brokerage, payments, and treasury services.

- The charter and master account primarily benefit RLUSD, Ripple’s stablecoin, whose reserves would sit under federal and state oversight, not XRP directly.

- A national trust bank cannot take ordinary deposits or carry federal deposit insurance, so the real prize is direct access to Federal Reserve payment rails and custody of its own stablecoin reserves.

- For XRP, the benefit is indirect: a more legitimate, bank-grade Ripple strengthens the whole ecosystem and XRP’s role as a bridge asset, but it creates no direct token-demand mechanism.

- This is the same pattern that defined XRP through 2026, in which Ripple’s wins flow first to the company and RLUSD, with the token benefiting slowly, if at all.

Ripple is turning itself into a bank, or something very close to one, and it is doing it methodically.

Over the past year the company won conditional federal approval to operate a national trust bank, applied for a Federal Reserve master account that would give it direct access to the central bank’s payment systems, and bought its way into prime brokerage, payments, and corporate treasury services through a series of acquisitions.

Add the dollar stablecoin it already issues, the 70-plus regulatory licenses it holds around the world, and a fresh European license that lets it passport services across 30 countries, and the picture is unmistakable.

A company once known mainly for a cross-border payments network and a controversial token is assembling the full apparatus of a regulated financial institution.

For XRP holders, who have watched the token grind sideways near a dollar through a year of Ripple triumphs, the natural question is what all of this means for them.

The honest answer is more complicated, and more sobering, than the headlines suggest, because almost every piece of Ripple’s banking build benefits the company and its stablecoin first, and the token only indirectly.

This piece works through Ripple’s transformation into a regulated financial institution and what it actually delivers for XRP. It covers the banking stack Ripple is assembling, what a national trust bank can and cannot do, the real prize of a Federal Reserve master account, why the charter is mostly a stablecoin story, what genuinely accrues to XRP, the bull case within the bank build, and what holders should watch.

The goal is to separate the real significance of Ripple becoming a bank, which is considerable for the company, from the wishful assumption that everything good for Ripple is automatically good for the token, which 2026 has repeatedly shown to be false.

A payments company is turning into a financial institution

Take the full measure of what Ripple has built, because the strategy only becomes clear when you see the pieces together.

The foundation is a conditional charter to operate a national trust bank, granted by the Office of the Comptroller of the Currency, the federal regulator that supervises national banks. The OCC conditionally approved Ripple National Trust Bank alongside other crypto firms in a broader wave of national trust bank approvals.

That federal approval matters because it moves Ripple deeper into the regulated banking perimeter without turning it into an ordinary retail bank.

A subsequent rule expanded what such trust banks are allowed to do, turning what would have been a narrow custody license into something with real operational scope, including digital-asset custody, stablecoin reserve management, and certain payment services.

On top of the charter, a Ripple subsidiary applied for a Federal Reserve master account, the account that would connect Ripple directly to the central bank’s payment rails.

And around that regulatory core, Ripple has been buying capabilities: a prime brokerage, a payments business, and a corporate treasury-services firm, each acquisition adding a piece of the institutional-finance stack.

Layer in the rest and the ambition is obvious. Ripple issues a dollar-pegged stablecoin that has grown past $1 billion in market value.

It holds dozens of regulatory licenses across jurisdictions, and it recently secured preliminary European authorization that lets it offer regulated services across the entire European Economic Area.

That is where Ripple’s European license fits into the larger build. The company is not only chasing U.S. banking access; it is trying to make its regulated-finance stack portable across major markets.

Taken individually, any one of these is a notable corporate step. Taken together, they describe a single, coherent strategy: to become the institutional infrastructure layer for crypto-native finance.

Ripple wants to be a regulated entity that banks and corporations can trust to custody assets, manage stablecoin reserves, settle payments, and connect to both the traditional financial system and the blockchain world.

Ripple is not dabbling in banking. It is building a bank-grade financial institution deliberately, piece by piece.

The question for a token holder is where, in all of this carefully assembled machinery, XRP actually fits.

What a national trust bank is, and what it is not

Before assessing what the charter means for XRP, it is worth being precise about what a national trust bank actually is, because the word “bank” carries connotations the charter does not deliver.

A national trust bank is not a retail bank. It cannot take ordinary deposits, cannot offer checking or savings accounts, and does not carry federal deposit insurance, the protection that backs ordinary bank deposits.

What it can do is custody assets, provide fiduciary and trust services, manage reserves, and, under the expanded rule, handle digital-asset custody and certain payment-related functions.

Headlines that say “Ripple becomes a bank” are gesturing at something real, but they compress away an important distinction.

That distinction matters for understanding the charter’s purpose. Ripple’s trust bank exists primarily to serve Ripple’s stablecoin business.

Its core planned function is to custody and manage the reserve assets that back the stablecoin, which today are held through a separate trust entity, and to provide custody to institutional clients.

By bringing reserve management in-house under a federal charter, Ripple gains tighter control, removes reliance on third-party custodians, and obtains a regulatory standing that few stablecoin issuers can match: oversight at both the federal level, through the national chartering regulator, and the state level, through New York’s financial regulator.

That dual supervision is a genuine selling point to institutions weighing whether to trust Ripple’s rails.

This is also why the fight over trust charters matters. Senator Elizabeth Warren and banking groups have challenged the idea that crypto firms with OCC trust charters should be treated like bank-grade institutions, arguing that they could act like crypto banks without the same restrictions.

The crypto industry has pushed back. The Digital Chamber called on the OCC to uphold crypto trust bank charters for firms including Coinbase, Ripple, Circle, and BitGo, arguing that the charters are part of bringing digital assets into regulated finance rather than keeping them outside it.

But notice what the trust bank does not do. It does not custody XRP for the benefit of XRP holders, does not create any obligation to buy or hold the token, and does not make XRP a bank deposit or a regulated bank instrument.

It is, at its heart, infrastructure for the stablecoin, which is the recurring theme of Ripple’s entire banking build.

The real prize: a Federal Reserve master account

The most consequential piece of Ripple’s banking strategy is the one furthest from being secured: a Federal Reserve master account.

A master account is the account a financial institution holds directly with the central bank, and it is the gateway to the core of the financial system.

It allows direct settlement through the central bank’s payment networks, the same rails the largest banks use, and direct access to base money rather than balances held at a commercial bank.

For a stablecoin issuer, the prize is enormous. With a master account, Ripple could hold the reserves backing its stablecoin directly at the central bank, the safest possible place, eliminating the counterparty risk of relying on private banks and giving institutions far greater confidence in the stablecoin’s solvency and redemption safety.

That is why custody and reserve safety matters so much in this story. Stablecoins are only as trusted as the assets backing them, the institutions holding those assets, and the transparency around redemption.

The catch is that no crypto-native firm has ever received full access of this kind on ordinary terms, and the bar is extraordinarily high.

The central bank has historically been reluctant to extend master accounts to non-traditional institutions. Uninsured trust banks face the most stringent levels of review, and previous attempts by crypto-adjacent firms to win access have often failed or taken years.

Ripple’s subsidiary has applied, and the application remains pending, with no public timeline and no clear signal of when or whether the central bank will act.

Approval would be genuinely transformative. It would mark a deeper integration between a crypto-native company and the core U.S. financial system, and it would dramatically strengthen the institutional credibility of RLUSD.

But it is far from assured. Even in the optimistic case, the direct beneficiary is again the stablecoin and the company’s settlement capabilities, not the token.

A master account would let Ripple hold stablecoin reserves at the central bank and settle through its rails. It would not, by itself, create demand for XRP.

The prize is real, and the prize is mostly about everything except the token.

Why this is mostly a stablecoin story

Step back and a clear pattern emerges from every piece of Ripple’s banking build: it is, overwhelmingly, a stablecoin story.

The trust charter exists primarily to custody and manage stablecoin reserves. The master account, if granted, would primarily benefit the stablecoin by letting its reserves sit at the central bank.

The European license primarily expands where Ripple can offer regulated payment and stablecoin services. The acquisitions in brokerage, payments, and treasury primarily build out an institutional settlement and services business in which the stablecoin is the natural cash leg.

Ripple’s dollar stablecoin has grown past $1 billion, expanded across multiple blockchains, and won approvals in multiple jurisdictions. The banking apparatus is being constructed largely to support and legitimize it.

That is why the RLUSD the bank serves is the center of the story. A stablecoin is useful to institutions precisely because it is designed to hold a steady dollar value while moving across crypto rails.

Ripple’s own reserve-transparency page also shows why this matters. The company is trying to make RLUSD look less like an experimental crypto product and more like a regulated dollar instrument with transparent backing, regular attestations, and bank-grade custody.

This is the same dynamic that defined XRP through 2026, when Ripple’s marquee bank deals and settlement milestones ran through its stablecoin and ledger while the token captured little beyond a negligible network fee.

As previously reported, this is why Ripple wins bypass the token. Ripple can deepen its institutional footprint while XRP still waits for direct, measurable token demand.

The banking build is that dynamic taken to its logical conclusion. Ripple is constructing a regulated financial institution whose central purpose is to make its stablecoin the most trusted, most institutionally credible dollar token in the market, and to build a settlement and custody business around it.

XRP is part of the broader ecosystem, but it is not the thing the bank is for.

A holder hoping that the charter, the master account bid, and the acquisitions would translate into direct demand for the token is, once again, watching the wrong variable.

The value of all this machinery flows first to Ripple the company and to the stablecoin it is built to serve, exactly as Ripple’s own communications have acknowledged in noting that the banking progress is unlikely to move the token’s price directly or immediately.

So what do XRP holders actually get?

If the bank build is mostly about the stablecoin, the fair question is whether XRP holders get anything at all.

The honest answer is yes, but indirectly and slowly. The benefit to XRP runs through legitimacy and ecosystem strength rather than any direct mechanism.

As Ripple becomes a regulated, bank-grade financial institution, the entire ecosystem it anchors gains credibility in the eyes of the banks and corporations Ripple wants as customers.

A more trusted Ripple makes every part of its stack, including the ledger on which XRP lives and the role XRP can play, more palatable to institutional users.

The argument, which Ripple and many holders make, is that demand for one asset in an ecosystem can lift others in the same stack, and that a Ripple wired into the core of the financial system is a Ripple better positioned to drive real-world use of XRP as a bridge asset over time.

This indirect benefit is not nothing, and it would be a mistake to dismiss it. XRP’s most plausible long-term role is as a bridge asset that moves value between currencies in settlement.

A Ripple with a federal charter, a master account, and a credible institutional settlement business is a Ripple with more opportunities to route that kind of settlement in ways that touch the token.

But the benefit is conditional, gradual, and unguaranteed, three qualities that make it very different from the direct, immediate boost holders often hope for.

XRP does not become a bank deposit, a stablecoin, or a regulated instrument through any of this. It remains a separate, volatile asset whose demand depends on whether Ripple’s growing institutional infrastructure eventually channels real settlement volume through it.

The competing path is obvious: the same settlement volume could instead keep flowing through RLUSD, which is better suited to settlement precisely because it does not move in price.

The banking build improves the odds that Ripple can win regulated institutional business someday. It does not make that business flow through XRP now, and it does not create token demand on its own.

The bull case within the bank build

In fairness to the optimistic view, there is a coherent bull case for XRP buried inside Ripple’s banking transformation, and it deserves a clear statement.

The strongest version goes like this: Ripple is methodically removing every reason an institution might hesitate to build on its rails.

The charter answers the custody and reserve-management question. The master account, if granted, answers the reserve-safety question at the highest possible level.

The acquisitions answer the brokerage, payments, and treasury questions. The licenses answer the regulatory question across jurisdictions.

As those barriers fall one by one, Ripple becomes a place where serious institutions can conduct serious volume. In a world where Ripple is running large-scale regulated settlement, the case for using XRP as the neutral bridge asset between currencies strengthens, because the infrastructure to do it at scale finally exists and is trusted.

Pair that with the token’s other tailwinds, including the regulatory clarity from its resolved legal status, the spot exchange-traded funds gathering assets, and the prospect of federal legislation codifying its commodity classification, and the bull case becomes clearer.

That is where the legislation that could codify XRP fits in. If the CLARITY Act turns XRP’s commodity treatment into durable federal law, it could make institutions more comfortable using the token where it has a genuine settlement role.

In that version of the future, XRP sits inside a maturing, increasingly bank-grade ecosystem at exactly the moment that ecosystem becomes capable of institutional-scale activity.

If even a fraction of the settlement flowing through a fully built-out Ripple touches XRP as a bridge, the demand could be meaningful, and it would arrive on top of a token that has already cleared its regulatory hurdles.

This is a real argument, and it is why the banking build is truly good news for the long-term XRP thesis even though it is not a direct catalyst.

The caveat, as always, is the word “if.” The bull case depends on Ripple choosing and managing to route settlement through the token rather than through the stablecoin, and the entire pattern of 2026 suggests the stablecoin keeps winning that role.

The infrastructure being built is real. Whether XRP is wired into it is the open question.

What XRP holders should watch

For a holder trying to judge whether Ripple’s banking transformation will ever translate into token demand, the analysis points to a few specific signals worth tracking, none of which is another charter or acquisition headline.

The first is the Federal Reserve master account decision.

If granted, it would be a landmark for Ripple and the stablecoin, and it would mark the company’s deepest integration into the financial system. Over time, that expands the surface area where XRP could be used.

If denied, a key piece of the institutional thesis stalls.

Either way, it is the most consequential pending item, and its outcome shapes everything downstream.

The second and more important signal is whether XRP actually appears in the settlement flows of Ripple’s bank-grade business, as opposed to the stablecoin doing all the work.

This is the variable that decides the entire question. If Ripple’s institutional settlement increasingly routes through XRP as a bridge asset, generating real, recurring token demand, then the banking build will finally have reached the token.

If, as has been the pattern, the stablecoin carries the settlement while XRP captures only a fee, then the bank is a Ripple and stablecoin story with XRP riding the halo of legitimacy but not the flows.

The third signal is the broader regulatory picture, particularly whether federal legislation codifies XRP’s status, which would compound the legitimacy the banking build provides.

The honest synthesis is that Ripple becoming a bank is a major, genuine achievement that strengthens the company, the stablecoin, and the long-term credibility of the whole ecosystem.

For XRP specifically, it improves the odds without delivering the goods.

The token’s payoff depends on a future choice, to run regulated settlement through XRP, that Ripple has not yet shown it will make.

Until it does, the bank is being built for everything except the token, and the token, as it has all year, waits.

Frequently asked questions

Is Ripple actually becoming a bank?

Sort of, but with important caveats. Ripple won conditional federal approval to operate a national trust bank and applied for a Federal Reserve master account, and it has acquired prime brokerage, payments, and treasury businesses. But a national trust bank is not a retail bank: it cannot take ordinary deposits, offer checking or savings accounts, or carry federal deposit insurance. It is a specialized institution for custody, fiduciary services, and reserve management. So Ripple is building a bank-grade regulated financial institution, but one focused on custody and stablecoin reserves instead of traditional deposit-taking banking.

What is the Federal Reserve master account and why does it matter?

A master account is an account held directly with the central bank, giving direct access to its payment rails and to base money, the same access the largest banks have. For Ripple, it would let the company hold its stablecoin’s reserves directly at the central bank, the safest possible location, eliminating reliance on private banks and boosting institutional confidence in the stablecoin. No crypto-native firm has ever been granted full access of this kind on ordinary terms, the review is stringent, and Ripple’s application is pending with no timeline. Approval would be transformative for the company and stablecoin, though not a direct catalyst for XRP.

Does Ripple’s banking push help XRP?

Indirectly and gradually, not directly. The charter and master account primarily benefit Ripple’s stablecoin, whose reserves they would custody and secure. XRP does not become a deposit, a stablecoin, or a regulated instrument. The benefit to XRP runs through legitimacy: a bank-grade Ripple strengthens the whole ecosystem and improves the odds that XRP is eventually used as a bridge asset in regulated settlement. But that is conditional and slow, not the direct demand boost holders often hope for, and Ripple itself has acknowledged the banking progress is unlikely to move the token’s price immediately.

Why does the stablecoin benefit more than XRP?

Because the entire banking build is designed around the stablecoin. The trust charter exists mainly to custody and manage stablecoin reserves. The master account, if granted, would let those reserves sit at the central bank. The acquisitions build a settlement business in which the stablecoin is the natural cash leg. A stablecoin is suited to settlement precisely because it holds a steady value, while XRP’s volatility makes it less suitable for that role. So Ripple’s regulated infrastructure naturally channels value to the stablecoin, with XRP benefiting only as part of the broader, more credible ecosystem.

What is the bull case for XRP in all this?

The bull case is that Ripple is methodically removing every reason an institution might hesitate to use its rails, through the charter, the master account bid, the acquisitions, and the licenses. As those barriers fall, Ripple becomes capable of large-scale regulated settlement, and the case for using XRP as a neutral bridge asset between currencies strengthens because the trusted infrastructure to do it finally exists. Combined with XRP’s regulatory clarity, its ETFs, and possible federal legislation, the bull case is that XRP sits inside a maturing, bank-grade ecosystem just as that ecosystem becomes capable of institutional-scale activity. The caveat is whether settlement actually routes through XRP instead of the stablecoin.

What should XRP holders watch next?

Three things. First, the Federal Reserve master account decision, which would mark Ripple’s deepest integration into the financial system and expand where XRP could be used, or stall a key part of the thesis if denied. Second, and most important, whether XRP actually appears in the settlement flows of Ripple’s institutional business, generating real token demand, as opposed to the stablecoin doing all the work. Third, the broader regulatory picture, especially whether federal legislation codifies XRP’s commodity status. The token’s payoff depends on Ripple choosing to route regulated settlement through XRP, a choice it has not yet shown it will make.

This article is information, not investment advice. Cryptocurrency is volatile, and regulatory approvals, corporate plans, and figures reflect reporting available as of June 26, 2026, which can change quickly. Verify current data from primary sources before making any decision.

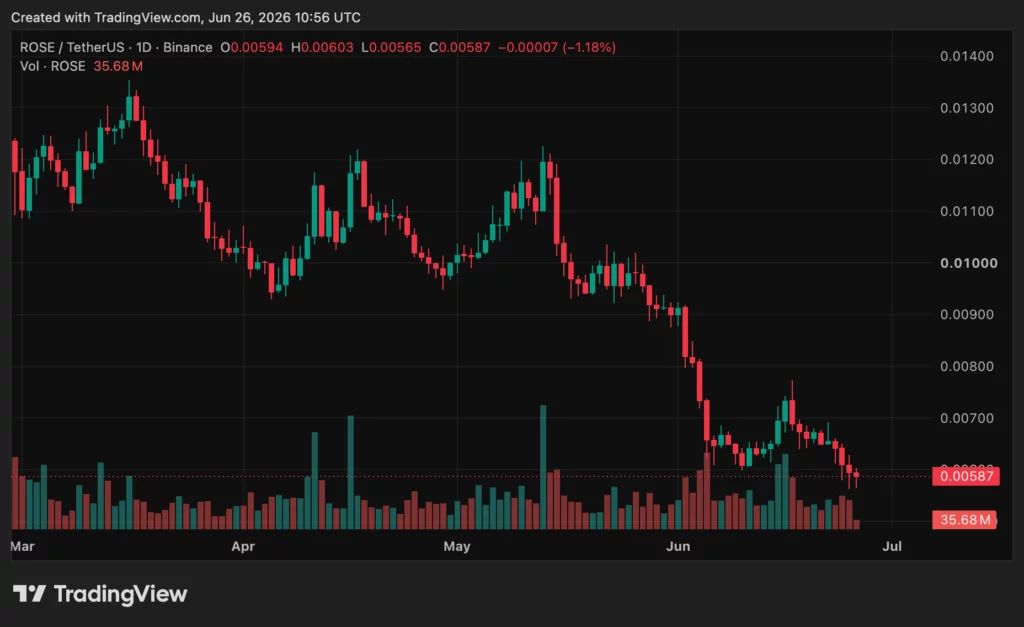

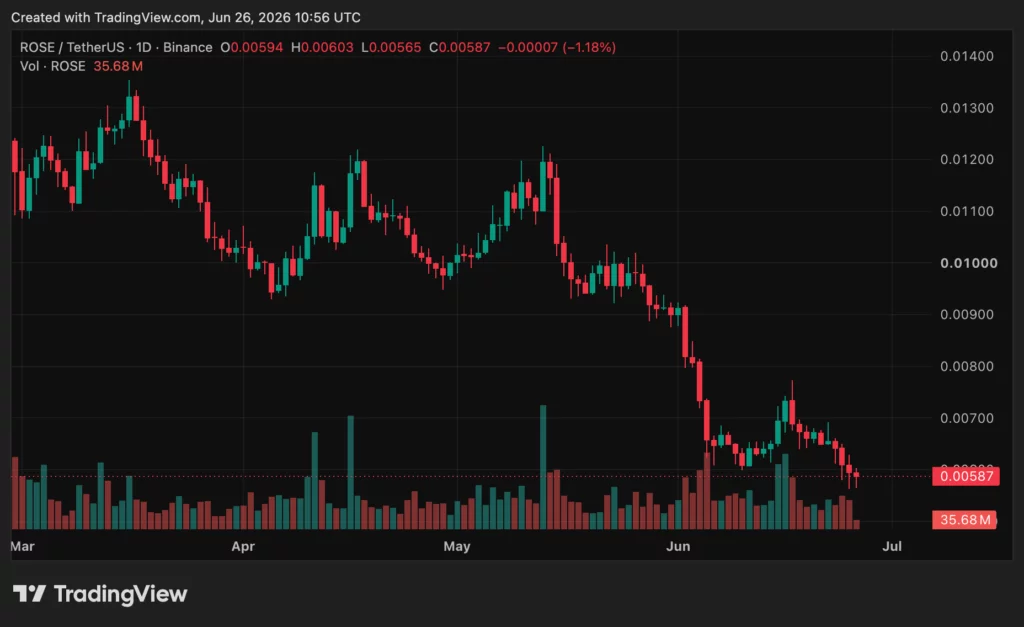

UC Berkeley professor and Oasis Labs founder Dawn Song has joined Meta Superintelligence Labs as vice president of AI research.

Summary

- Dawn Song joins Meta, bringing Oasis privacy experience to frontier AI safety and security work.

- Virtue AI members are joining Meta as MSL builds safety tools for agentic AI systems.

- ROSE remains near record lows, showing Song’s AI move has not revived Oasis token demand.

She said she will help lead Meta’s AI safety and AI security efforts. Song announced the move in a post on X. She said several members of the Virtue AI team will also join Meta. Axios also reported that Virtue AI co-founders Bo Li and Sanmi Koyejo are among the hires.

Song said her work at Meta will focus on frontier AI models and agentic AI systems. She wrote that AI must be “secure, trustworthy, and beneficial” if it is to reach its full use.

The move gives Meta more senior talent in AI security. It also brings a well-known blockchain privacy researcher into one of the world’s largest AI labs.

Virtue AI team moves to MSL

Virtue AI was founded in 2024 to build tools for trustworthy AI. Song said the team worked on AI security, agent security, benchmarks and open platforms before the Meta move.

According to Axios, Meta is hiring several Virtue AI leaders and team members. The report said the group worked on automated red teaming, runtime guardrails and AI governance.

Meta’s interest comes as AI labs put more attention on agent safety. AI agents can take actions, use tools and handle tasks across software systems. That makes security more important because errors or misuse can spread across real products.

As previously reported, Meta has been building a superintelligence AI team after its large Scale AI deal. The company wants to improve its AI models and ship them across Facebook, Instagram, WhatsApp and other products.

Oasis background adds crypto angle

Song is also known in crypto as the founder of Oasis Labs. The company raised $45m in 2018 to build privacy-first cloud computing on blockchain. Its backers included a16zcrypto, Accel and Binance Labs.

The Oasis project later became tied to the Oasis Network and the ROSE token. The network focuses on confidential computing, data privacy and privacy-preserving applications.

In a previous article, crypto.news discussed Oasis Protocol’s verifiable AI agents for crypto trading. The project used trusted execution environments to keep strategies private while giving users proof of how agents behave.

Previously, crypto.news explored Oasis-based AI and data services through Pontus-X, a platform built around privacy and data control. Song’s Meta role connects that same privacy and security theme to a much larger AI platform.

ROSE remains near record lows

The hiring news has not changed ROSE’s weak market setup. Oasis traded near $0.0059 on June 26, close to its intraday low. That is about 99% below its all-time high near $0.596.

ROSE has also struggled with the broader crypto market selloff. Its market value remains far below peak-cycle levels, even as AI and privacy remain active themes in the sector.

The move is still notable for the Oasis community because Song helped shape the project’s early research identity. Her work linked blockchain, privacy and security before AI safety became a major mainstream topic.

For Meta, the hire adds academic and startup experience to its AI safety push. For crypto, it shows how privacy and security talent from blockchain continues to move into frontier AI.

Long-dormant Ethereum (ETH) wallets dating back nearly eight years have begun moving funds again, according to on-chain monitoring shared by multiple crypto analytics sources. The activity has reintroduced additional ETH supply into the visible flow, coinciding with Ether trading slightly above the $1,500 mark. While some of these addresses have taken profits, other large holders appear to be continuing accumulation, resulting in a mixed ledger picture.

At the same time, analysts say long-term whale profitability has deteriorated across major ETH holder cohorts. This matters for compliance and institutional risk assessment because persistent unrealized losses can influence large-holder behavior, custody-related transfers, and the pace at which liquidity is redeployed across venues—factors that institutions often track when managing exposure and counterparty risk.

Key takeaways

- On-chain trackers reported activation of ETH addresses last used in 2017, with one group of wallets moving a combined 37,602 ETH after years of dormancy.

- Separately, large investors appear to be rotating into ETH through swaps involving BTC, while others have continued withdrawals from major exchanges.

- Analysts state that unrealized profitability for major ETH whale cohorts has turned negative for the first time since 2019, based on reported unrealized profit ratios.

- Institutional custody-related movements were also noted, including transfers involving Coinbase Prime, without confirmation of a market sale.

Eight-year-old wallets reactivate, bringing long-dated supply into motion

According to Lookonchain, four Ethereum wallets that collectively received 37,602 ETH nearly eight years ago—at an average price of about $830—became active after a prolonged period of dormancy. The same set of wallets reportedly held through multiple market cycles, including the 2021 and 2025 bull markets, when unrealized gains reached levels described as exceeding $150 million.

Lookonchain further reported that these wallets sold 33,623 ETH during Thursday’s activity at an estimated price near $1,560, with the realized profit now described as approximately $27.4 million. For compliance teams and market-structure monitoring, reactivation of long-dormant addresses can be a relevant signal: it may reflect liquidity management, tax or rebalancing actions, or simply opportunistic execution after extended inactivity—each with different implications for market integrity checks and risk controls.

Whales show mixed behavior: rotation into ETH alongside selective profit-taking

Beyond the reactivated wallet group, other large transactions were reported as continuing capital rotation into Ether. Lookonchain stated that one whale swapped 464 BTC, valued at about $27.6 million, for 17,750 ETH. Such cross-asset rotation can be meaningful in institutional workflows because it may affect spot liquidity dynamics and the timing of ETH supply relative to broader crypto market flows.

In a separate report, investor Chun Wang was described as acquiring 9,937 ETH and 147 wrapped Bitcoin. Lookonchain also cited recent behavior in which Wang withdrew nearly 87,000 ETH from Binance over the prior month, at an average purchase price reported as $1,749. Exchange withdrawals by large holders are often monitored for operational and counterparty risk reasons—particularly where trading activity, custody arrangements, or liquidity sourcing may change.

Institutional-related activity was also referenced. BlackRock was reported to have transferred 41,996 ETH and 4,577 BTC to Coinbase Prime. Movements to Prime are commonly associated with custody or operational management rather than an immediately confirmed spot sale. For regulated entities, the distinction matters: custody transfers can trigger reporting and monitoring workflows without implying directional market exposure.

Unrealized losses broaden across whale cohorts

Crypto analyst Darkfost highlighted that unrealized profit ratios for ETH whale cohorts—from 1,000 ETH up to more than 100,000 ETH—have turned negative. The analyst said this is the first time since 2019 that every major whale cohort is reported to be underwater on an unrealized basis.

While unrealized metrics are not guarantees of future behavior, they are frequently used by analysts as a proxy for risk posture and conviction. Darkfost added that when ETH prices test whale conviction historically, periods often align with long-term bottom zones. Even so, the current setup was framed as placing greater pressure on large holders in 2026, even as selective accumulation appears to persist.

For institutional compliance monitoring, this kind of broadening drawdown can be relevant when assessing the potential for forced selling, changes in collateralization behavior, or shifts in custody and transfer patterns—especially for firms with exposure to exchanges, OTC counterparties, or derivative counterparties whose operational decisions may be influenced by large-holder positioning.

ETH’s $1,500 area remains a focal point amid ongoing uncertainty

Separately from on-chain behavior, attention among market participants remains on Ether’s $1,500 level. The article sources cited that ETH fell to around $1,510 during Thursday’s sell-off, while not setting a new yearly low as Bitcoin moved to fresh 2026 lows.

Crypto trader Ardi characterized $1,500 as a key long-term support, arguing that daily closes below that region would undermine bullish assumptions formed since the 2022 bear market. Crypto investor Jelle similarly suggested that a sustained break could return ETH to a trading range last seen in early 2023, noting that the $1,500 zone has historically been defended during several major corrections since mid-2022.

Other participants pointed to the possibility of lower demand zones. Trader Cyclops identified a $1,070–$1,370 range as a potential accumulation area, describing it as a demand region established in early 2023. The same source noted that moving into that lower band would also mean ETH breaking below a multi-year ascending trendline—an outcome that could prolong uncertainty in market structure.

From a policy and risk perspective, the common theme is not price forecasting but the importance of clearly defined reference levels for institutional monitoring: support breaks can affect portfolio risk calculations, margin models, and liquidity planning. However, the unresolved question remains whether observed on-chain transfers reflect genuine distribution pressures or routine movements that do not necessarily translate into sustained sell-side flow.

Closing perspective

The reactivation of nearly eight-year-old ETH wallets, combined with reported negative unrealized profitability across major whale cohorts, underscores a market where long-dated holders are again participating in active liquidity. Watch for whether these movements translate into sustained net distribution or whether ongoing withdrawals and ETH-denominated swaps continue to offset the added supply. For compliance and institutional teams, tracking wallet reactivation, exchange withdrawal patterns, and custody-related transfers alongside regulatory monitoring frameworks remains a practical approach as crypto markets evolve.

Crypto users have reported difficulties withdrawing funds from the exchange AscendEX, renewing concerns about exchange liquidity and operational readiness during periods of customer demand. Blockchain investigator ZachXBT and multiple social-media accounts pointed to delays and apparent limitations in the exchange’s liquid reserves, framing the issue as a potential liquidity problem rather than an isolated technical glitch.

These allegations matter for institutional compliance and risk teams because withdrawal processing is a key stress indicator for trading venues. When withdrawals become stuck or support channels stop responding, regulators and auditors typically treat it as a potential sign of liquidity strain, inaccurate reserve management, or deficient contingency controls—issues that can quickly intersect with insolvency risk, consumer protection obligations, and AML/CTF expectations.

Key takeaways

- Multiple users reported delayed withdrawals from AscendEX, including at least one case where a USDT withdrawal remained in an “initiating” status for days.

- ZachXBT said AscendEX may have limited large-cap token reserves, citing purported low holdings of widely used assets such as ETH, USDT, and SOL.

- On-chain analytics referenced by Cointelegraph indicated AscendEX-tagged wallets were concentrated in smaller-cap tokens rather than major cryptocurrencies.

- The situation echoes post-FTX regulatory and industry emphasis on demonstrable liquidity and transparency, including proof-of-reserves approaches.

User complaints highlight potential withdrawal processing gaps

According to an X post by an account operating under the name Lorenzo Navarro Rodriguez, a 4,196 USDT withdrawal on AscendEX remained stuck in an “initiating” state since June 10. The same post alleged that repeated inquiries to customer support did not receive responses.

Following that initial report, at least five other users responded over subsequent days with similar claims about withdrawal delays. While social-media reporting does not, on its own, establish causality, repeated, independent user accounts can increase the likelihood that an operational or liquidity bottleneck is affecting customers—particularly when withdrawal requests do not progress and support fails to provide timely status updates.

From a compliance perspective, unresolved withdrawal delays can also complicate obligations related to customer asset safeguarding, dispute handling, and required communications to affected counterparties. If a venue cannot process withdrawals within expected service windows, risk teams generally consider whether internal controls for hot-wallet management, transaction monitoring, and escalation procedures are functioning as intended.

ZachXBT links the issue to liquidity concerns

ZachXBT said in a Telegram post on Friday that AscendEX lacked large-cap reserves for major assets, including ETH, USDT, and SOL, and suggested this may indicate “liquidity issues” on the platform. He urged the exchange to respond to reports of delayed withdrawal requests and to clarify why its hot wallets appeared to have low liquidity.

Hot wallets are central to withdrawal execution because they must hold sufficient balances to cover outgoing transactions without requiring time-consuming asset swaps or fund transfers from less liquid or less accessible accounts. If a platform’s operational liquidity is concentrated in illiquid holdings—especially small-cap tokens—withdrawals of major assets can become delayed, particularly if conversion routes are constrained by market depth, exchange limits, or internal custody flows.

However, unresolved details remain. Even when on-chain activity suggests reserve composition constraints, it does not automatically confirm whether the exchange can meet withdrawal demand through other mechanisms (for example, larger balances elsewhere under different wallet clusters, custodial arrangements, or internal transfer arrangements not visible to public labeling). As such, the legal and regulatory implications typically depend on verified asset custody, the completeness of reserve disclosure, and documented solvency and operational capacity.

On-chain data cited by Cointelegraph points to reserve concentration

Blockchain data on Arkham, reviewed by Cointelegraph on Friday, indicated that wallets tagged as AscendEX-held contained about $20.2 million in crypto. The same analysis described those Arkham-tagged wallets as being concentrated in smaller-cap assets, with comparatively limited holdings of major cryptocurrencies.

Cointelegraph reported that AscendEX-tagged wallets showed UNITE tokens as the largest holding at approximately $10 million. Other cited holdings included REUR at about $5.24 million, ASD at around $2.9 million, and roughly $600,000 in Reservoir rUSD stablecoins, among smaller positions.

Cointelegraph also reported that it had approached AscendEX for comment but did not receive a response before publication. The absence of an official explanation is consequential in both governance and compliance contexts. When liquidity concerns surface, institutional stakeholders typically expect timely disclosures covering withdrawal status, wallet and custody structure, and the operational steps being taken to clear pending requests—especially where customer communications appear inconsistent.

These issues are not occurring in a regulatory vacuum. Following the 2022 collapse of FTX, withdrawal behavior became a focal point for regulators and industry participants. In that case, customer withdrawal requests exposed a large shortfall, culminating in bankruptcy. The broader industry response included increased attention to reserve transparency and more intensive regulatory scrutiny of exchange solvency and custody practices.

Regulatory implications: liquidity, custody, and transparency expectations

Delays in customer withdrawals can trigger multiple regulatory and legal considerations across jurisdictions. While this article does not establish wrongdoing, it highlights a scenario regulators commonly scrutinize: whether an exchange holds sufficient liquid assets to meet customer redemption demands and whether custody arrangements and internal controls are capable of handling peak outflows.

In the European context, MiCA has increased the compliance and governance expectations for crypto-asset service providers, including requirements that can affect how firms manage customer assets, disclosures, and operational resilience. Even where MiCA applies differently depending on licensing status and activity type, the direction of travel is consistent: regulators are placing greater emphasis on risk controls and verifiable safeguards for customer funds.

In the United States, enforcement and regulatory focus from bodies such as the SEC and CFTC has historically centered on how crypto intermediaries structure operations, disclose risks, and manage custody and market integrity concerns. Separately, AML/KYC compliance obligations do not disappear during liquidity stress; in fact, heightened operational strain often increases the risk of compliance breakdowns, including failure to adequately screen counterparties, properly document investigations, or maintain auditable records of transactions during customer disputes.

Cross-border complexity also matters. Exchanges operating across multiple markets face different standards for reserve reporting, insolvency planning, and customer-protection requirements. Without verified and jurisdiction-appropriate disclosures, a venue may face challenges demonstrating compliance to regulators or to institutional counterparties—particularly banks and regulated financial firms evaluating counterparty risk exposure.

Finally, reserve claims and proof-of-reserves efforts, while helpful, can be incomplete if they do not reflect total customer entitlements, the accessibility of assets when withdrawals are requested, and the distinction between illiquid holdings and immediately usable liquidity. For institutional monitoring, the practical question is not only what assets are held, but how quickly and reliably they can be mobilized to honor withdrawal demands.

Closing perspective

For now, the core open issue is verification: whether AscendEX can process pending withdrawals at scale and whether its disclosed or accessible reserves align with customer redemption needs. Continued user reporting, any official exchange statements, and any regulator- or auditor-led assessments will be key to determining whether the incident reflects temporary operational constraints or a deeper liquidity and custody mismatch.

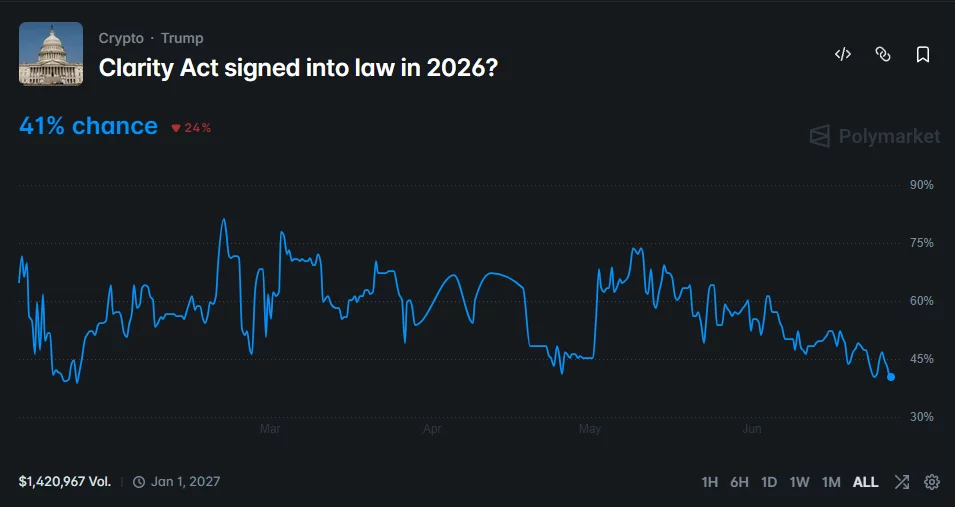

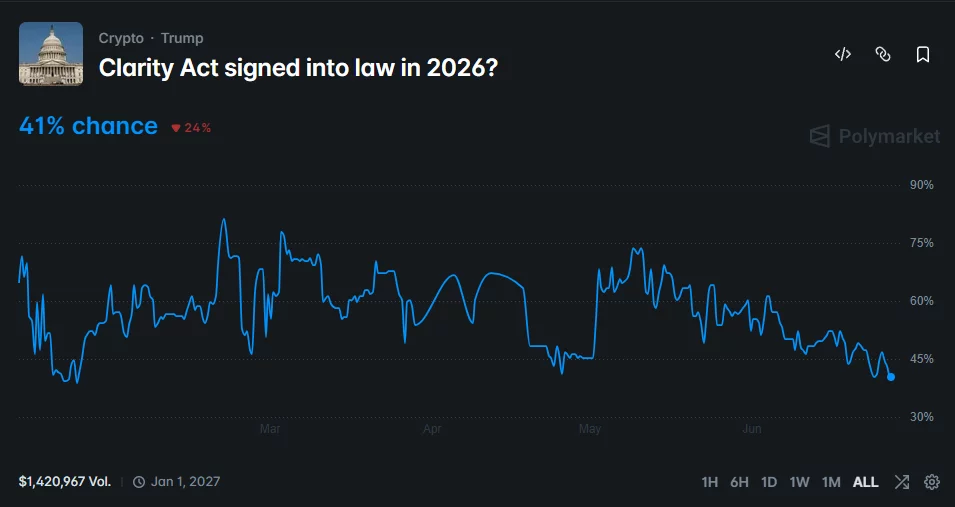

Galaxy Digital has lowered its estimated probability of the CLARITY Act becoming law in 2026 to 50%, citing a shrinking Senate calendar and the absence of visible legislative progress ahead of the August recess.

Summary

- Galaxy Digital has lowered its estimated odds of the CLARITY Act passing in 2026 to 50%, citing Senate scheduling delays rather than policy disagreements.