Crypto World

Why India’s Central Bank Wants Crypto Out of the Banking System?

India’s central bank wants lawmakers to wall off the banking sector from crypto. The Reserve Bank of India (RBI) told a parliamentary panel that digital assets should not serve as payment instruments.

The Parliamentary Standing Committee on Finance heard the testimony for its study on virtual digital assets. Lawmakers plan to table the report during the monsoon session.

Central Bank Pitches Crypto Containment in India

Committee members said the RBI argued for a containment strategy, not a conventional rulebook. The central bank believes formal regulation could legitimize speculative assets. It warned that clear rules might give retail investors a false perception of safety.

Officials repeated long-standing concerns about illicit finance. They cited risks tied to drug trafficking and terror funding. Similar central bank warnings have appeared in other emerging markets this year.

The stance revives a fight the RBI lost in 2020, when the Supreme Court struck down its banking ban. This time, the central bank wants Parliament to write the separation into law.

No Payments and No Direct Bank Exposure

The RBI advised lawmakers to prohibit crypto for payments and settlements. The bank wants tight limits on direct banking-sector exposure to digital assets. The advice mirrors the caution found in several global regulatory frameworks, although most jurisdictions now prefer licensing over isolation. Washington set its own boundary in June, when senators passed a US CBDC ban lasting through 2030.

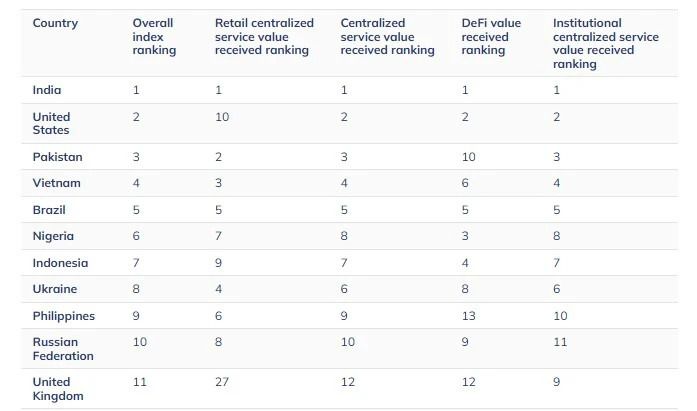

Committee members pushed back during the hearing. They questioned how India can ignore capital flight while Indonesia, Hong Kong, and the UAE regulate the sector. India ranked first in the 2025 Global Crypto Adoption Index, ahead of the US and Pakistan.

However, the officials offered a blunt reply.

“Not having a policy is also a policy,” RBI officials said, according to a committee member quoted by Business Standard.

Meanwhile, the Securities and Exchange Board of India (SEBI) earlier signaled it could regulate tokens classified as securities. The RBI declined to answer that question and promised a written response.

Tokenized Bonds Stay on a Separate Track

The proposal draws a line between cryptocurrencies and tokenized government securities. Growing tokenized bond markets would keep room to develop on a regulated infrastructure. The restriction targets speculation, not blockchain technology itself.

Still, India’s crypto investors face a 30% tax and a 1% levy on every trade. Industry voices keep lobbying for a softer line, including a domestic Bitcoin mining push as an alternative to gold imports.

The panel meets the Department of Economic Affairs on July 15 before it finalizes recommendations. The coming weeks should reveal whether Parliament backs isolation or an EU-style framework such as MiCA.

The post Why India’s Central Bank Wants Crypto Out of the Banking System? appeared first on BeInCrypto.

Strategy’s corporate approach to Bitcoin is evolving in a way that signals the industry’s broader shift from ideology to balance-sheet realism. This week, the company authorized up to $1.25 billion in Bitcoin sales under a new capital framework—explicitly designed to support dividends, strengthen cash reserves, and fund buybacks while keeping its long-term commitment to Bitcoin.

At the same time, the rest of crypto business news points to a more pragmatic era: stablecoin issuers are racing to capture reserve-driven yield, Fidelity is disputing the idea that Bitcoin’s security will deteriorate as halvings reduce rewards, and political spending by crypto firms is climbing ahead of the 2026 US midterm elections.

Key takeaways

- Strategy authorized up to $1.25 billion in Bitcoin sales to fund shareholder dividends, cash reserves, and buybacks—despite years of “never sell” messaging.

- The company outlined a formal Bitcoin monetization program under its “Digital Credit Capital Framework,” alongside additional capital return measures.

- Open USD (OUSD) is positioning as a yield-enabled dollar stablecoin, backed by payments and crypto firms, in an effort to challenge USDT and USDC.

- Fidelity argues Bitcoin’s security economics extend beyond block subsidies, citing rising miner revenue from fees and market incentives.

- Public Citizen reports $189 million in crypto-related spending for 2026 elections, with major PACs again driving influence.

Strategy’s “never sell” era meets capital allocation reality

Strategy disclosed that it has authorized up to $1.25 billion in Bitcoin sales under a new capital framework called the “Digital Credit Capital Framework.” The stated objective is to preserve Strategy’s long-term Bitcoin exposure while creating a structured path to monetize Bitcoin to support shareholder payments and corporate liquidity.

The framework increases the annual dividend on Strategy’s STRC preferred stock from 11.5% to 12% and sets out additional capital return mechanisms. Strategy also said its dedicated cash reserve has reached $2.55 billion, which management described as sufficient to cover roughly 17 months of preferred dividends and interest obligations.

Just as importantly, the authorization marks a change in how Strategy talks about Bitcoin. According to earlier reporting by Cointelegraph, the company had already disclosed its first-ever Bitcoin sale of 32 BTC in June. With this new framework, monetization is no longer an isolated event—it is now formalized as a program.

Strategy also indicated it did not purchase additional Bitcoin last week, leaving its holdings unchanged at 847,363 BTC. That detail matters because it underscores the logic behind the new approach: the company is trying to balance continued accumulation with practical liquidity management rather than relying solely on uninterrupted buy-and-hold behavior.

A new stablecoin backed by major payments firms targets “reserve yield”

While corporate Bitcoin holders reassess capital flexibility, stablecoin innovation is pushing in the opposite direction—toward feature competition. More than 140 financial and crypto companies have come together to launch a new US dollar-backed stablecoin designed to allow participants to retain yield generated by its reserves.

The project, Open USD (OUSD), is supported by large payments players including Visa and Mastercard, alongside crypto and trading ecosystem firms such as Coinbase, Ripple, OKX, and Bybit. Its positioning is straightforward: unlike many traditional stablecoin models that route reserve earnings to the issuer, OUSD aims to route those reserve earnings to token holders or businesses, according to the project’s supporters.

Open USD’s design also includes operational choices that proponents say could help it compete for market share. The initiative plans to let businesses mint tokens without fees or volume limits while keeping reserve earnings. Backers frame the offer as a direct alternative to incumbents, referencing Tether’s USDT and Circle’s USDC as competitors.

Timing and regulation are part of the pitch. Cointelegraph reported that the launch comes as US policy has moved toward a more favorable stance after the passage of the GENIUS Act. According to the reporting, Open Standard intends to roll out OUSD later this year, entering a market analysts expect to keep expanding, with the article noting the sector is already worth more than $300 billion.

Fidelity challenges the claim that halvings erode Bitcoin security

One of Bitcoin’s most persistent debates—especially after each halving—is whether lower block subsidies will eventually undermine miners’ incentive to secure the network. Fidelity Digital Assets is pushing back against the notion that Bitcoin’s long-term security is threatened by reward reductions.

In a research report, Fidelity argued that Bitcoin’s economic model extends beyond block subsidies. The central claim is that the network’s security incentives can be maintained through rising transaction fees, broader market incentives, and Bitcoin’s own price appreciation.

Cointelegraph’s summary of Fidelity’s analysis cites research analyst Daniel Gray, who points to miner revenue growth over time. The report’s figures, as quoted in the coverage, show average daily miner revenue increasing from $1.3 million during 2012–2016 to $40.2 million today. The implication is that while subsidies shrink mechanically, the overall economic picture for miners can improve through other revenue streams.

The timing also matters for the real-world mining industry. As halvings reduce block rewards, publicly traded mining firms have faced renewed pressure. Cointelegraph noted that many miners are seeking diversification—such as expanding into AI and high-performance computing—to offset the squeeze. Fidelity’s stance, however, is that those pressures do not automatically translate into a long-run weakening of Bitcoin’s programmed security.

Crypto’s political footprint expands ahead of the 2026 midterms

Beyond market structure, crypto’s business influence is increasingly visible in politics. A report by consumer advocacy group Public Citizen says crypto companies have contributed roughly $189 million to the 2026 US election cycle so far—about 37% of all corporate political spending, according to the figures cited in Cointelegraph’s coverage.

Public Citizen’s findings also suggest that crypto-backed PACs are again the key engine behind political leverage. Cointelegraph reports that Fairshake has spent more than $82 million this cycle, while the pro-Trump MAGA Inc. Super PAC—described as heavily backed by Crypto.com—has spent more than $56 million.

The report frames the strategy as consistent with 2024: supporting candidates from both major parties that align with the industry’s policy agenda. Public Citizen also notes that crypto election spending has already surpassed roughly $170 million deployed during the 2024 election cycle, with more than four months remaining before the November elections, based on the coverage’s description.

For investors and builders, this matters because policy outcomes can shape stablecoin rules, disclosure requirements, and enforcement priorities—areas that directly affect how crypto firms operate and compete.

What to watch next

The key question now is whether Strategy’s monetization framework becomes a template for other major Bitcoin holders—and how quickly stablecoin competitors like OUSD can translate “reserve yield” features into real usage. In parallel, the ongoing debate over Bitcoin security economics and the industry’s political momentum will likely define how both networks and regulations evolve as 2026 approaches.

US President Donald Trump has pushed back against criticism of his latest financial disclosures, telling CNBC that there was “nothing illegal” and “nothing wrong” about earning income tied to his crypto investments while in office. The remarks came shortly after the US Office of Government Ethics (OGE) released his 2025 financial disclosure report, which advocacy groups say highlights troubling conflicts of interest.

In a Thursday interview with CNBC’s Joe Kernen, Trump argued that others were responsible for his crypto-related investments and that he did not “even know who they are,” without directly addressing concerns about whether his position could influence policy affecting the digital asset industry. The disclosures reportedly show Trump’s businesses and investments generated more than $2 billion during 2025, with about $1.4 billion linked to crypto ventures.

Key takeaways

- Trump said on CNBC there was “nothing illegal” about profiting from crypto investments while president, following the release of his 2025 OGE financial disclosure.

- The filing reportedly attributes roughly $1.4 billion of Trump’s 2025 income to crypto-related activities, including his memecoin and the family platform World Liberty Financial.

- Trump did not provide specific answers about who managed the investments, saying he did not “even know who they are.”

- Advocacy groups argue the scale of crypto-linked earnings raises conflict-of-interest concerns as Congress considers digital asset legislation.

- Crypto political spending appears to be ramping up ahead of the 2026 elections, according to Public Citizen.

Trump denies wrongdoing after crypto-linked disclosures surface

Trump’s defense centered on the idea that profiting from digital assets while holding the presidency is not inherently improper. Speaking to CNBC’s Joe Kernen, he maintained that his crypto holdings did not involve wrongdoing and suggested he was not directly involved in the investment management decisions.

That response came after reporting on the contents of Trump’s 2025 financial disclosure. According to coverage referencing the OGE filing, Trump reported taking in more than $2 billion from his businesses and investments during 2025. Within that total, roughly $1.4 billion was described as connected to crypto projects, including his memecoin and activities tied to World Liberty Financial, a platform associated with his family.

According to the same reporting, Trump’s disclosed crypto-related earnings included:

- About $636 million from his memecoin

- About $588 million from World Liberty sales

- $197 million from equity in a stablecoin venture

Trump has previously criticized Bitcoin during his first term, calling it a “scam.” However, in the lead-up to the 2024 election he reportedly increased engagement with prominent figures in crypto, including Gemini co-founders Cameron and Tyler Winklevoss, as well as executives from mining companies and crypto exchanges. He has also launched an Official Trump memecoin and has remained closely associated with World Liberty and American Bitcoin.

Conflict-of-interest concerns keep pressure on US crypto policy

Trump’s remarks are likely to intensify a dispute that has been playing out across US politics: whether leaders can personally profit from industries while also participating in government actions that shape the regulatory environment for those same industries.

Several advocacy organizations have characterized the disclosed crypto earnings as a “grift,” pointing to the possibility that personal financial ties could affect legislative outcomes. In particular, critics have flagged the Digital Asset Market Clarity (CLARITY) Act as an example of the kind of policy initiative they believe could benefit from a more transparent and strictly separated approach.

Trump’s CNBC comments did not directly resolve those concerns. Instead, he emphasized that other parties were responsible for his investments and that he did not know the individuals involved. For critics, that stance may not address the core issue: whether the presidency creates an inherently asymmetric influence over markets and legislation even when day-to-day decisions are delegated.

Beyond Trump himself, his family has also become a focal point for commentary. In a Friday interview with CNN’s Anderson Cooper, Mary Trump—the president’s niece—argued that the political system enables people to “get away with” serious financial wrongdoing, adding that investors may have been harmed by trusting Trump’s businesses. Her comments did not cite new details from the OGE filing, but they align with the broader line of criticism that seeks more accountability and clearer separation between political power and private crypto interests.

What changes: from “scam” rhetoric to industry engagement

One of the more striking dynamics in this story is how sharply Trump’s posture toward crypto appears to have shifted over time. In his first term, he publicly derided Bitcoin. But leading into the 2024 election—and continuing since—he has moved closer to influential crypto personalities and industry players.

The new disclosure-related controversy comes against that backdrop. If 2025 earnings are indeed as large and as closely tied to crypto-specific ventures as the filing descriptions indicate, the question for investors and builders is not only whether regulations will change—but whose incentives are most aligned with those changes.

This matters beyond politics because crypto markets respond quickly to expectations about rules, enforcement posture, and legislative clarity. When a head of state is personally linked to crypto outcomes—whether through tokens, platforms, or stablecoin-related equity—participants may reassess the probability that policy will be aligned with industry interests rather than general consumer protection.

Crypto spending looks set for another election-cycle push

Trump’s crypto-related disclosure debate is unfolding as the industry prepares for more political contests. After digital asset companies reportedly spent $170 million to support candidates they considered “pro-crypto” during the 2024 cycle, political action committees and related organizations appear to be following a similar approach for 2026.

In a report cited by Cointelegraph, Public Citizen said that companies and figures linked to the crypto industry contributed $189 million toward the 2026 election cycle as of June. That figure is presented as the bulk of $294 million in spending so far across crypto, AI, Big Tech, and online betting companies to support or oppose politicians.

With Trump’s term running until January 2029, the timing of 2026 elections is still crucial: all 435 seats in the US House of Representatives and 35 in the Senate will be contested. For digital asset policy, those races could shape committee leadership and the legislative momentum behind bills that attempt to clarify how different parts of the market should be regulated.

For traders and long-term participants, political funding and lobbying activity can act as early signals for where the policy debate is moving—even when the market seems focused on immediate price action. However, disclosures like Trump’s add a separate layer of scrutiny: not just how much money crypto firms spend to influence policy, but whether government officials’ financial incentives complicate the regulatory process.

As these issues move forward, readers should watch for how lawmakers address conflict-of-interest concerns and whether any additional scrutiny from ethics or oversight bodies changes how crypto-linked disclosures are interpreted in practice.

U.S. Securities and Exchange Commission is advancing SEC Project Crypto as Chairman Paul Atkins outlines plans for blockchain-based financial markets. The initiative focuses on modernizing securities rules, improving token classification, and supporting market systems that can operate on-chain. Atkins said the agency has spent the past year adjusting its approach after President Donald Trump called for U.S. leadership in cryptocurrency. The SEC expects several rulemaking steps to continue through mid-2026.

Sec Sets Direction For On-Chain Markets

Atkins said SEC Project Crypto marks a broad effort to prepare existing market rules for blockchain infrastructure. He described the agency’s work as “historic steps” toward modernizing regulations for on-chain market activity. The plan aims to help issuers understand whether a token falls under securities laws before they launch a project. That clarity could reduce legal uncertainty for crypto startups, token issuers, and regulated trading platforms.

The SEC chairman said the initiative does not give the digital asset industry special treatment. Instead, he said the agency wants clear regulations that allow markets to operate under known rules. This approach places disclosure, investor protection, and market integrity at the center of the SEC’s digital asset agenda. It also signals that the agency wants blockchain finance to fit within regulated market structures.

Sec And Cftc Work On Joint Framework

The SEC also plans deeper coordination with the Commodity Futures Trading Commission. Under the current timeline, both agencies expect a Memorandum of Understanding by March 2026. The agreement should help classify digital assets that do not qualify as securities. It also aims to reduce overlap between the two regulators.

Atkins said the goal is to replace a “fragmented regulatory environment” with a more coordinated structure. This matters because many crypto products combine trading, custody, payments, and derivatives features. Clearer coordination could help firms understand which regulator oversees each product. It may also reduce delays for platforms that want to offer compliant digital asset services.

Rule Changes Target Custody And Trading

SEC Project Crypto also includes updates to market structure rules, including Regulation NMS. The SEC wants pathways that allow blockchain-based trading systems to operate alongside traditional exchanges. These changes could affect tokenized securities, settlement systems, and digital asset trading venues. The agency expects key rule updates by mid-2026.

Custody rules remain another major focus for the commission. Updated standards could determine whether banks can hold tokenized securities for clients. The SEC-CFTC framework may also shape crypto derivatives that now operate in a less settled legal environment. As a result, SEC Project Crypto could influence how on-chain markets connect with U.S. financial institutions.

URLS:

https://x.com/SECGov/status/2072745983088160996?s=20

Early in Donald Trump’s term, his then-advisor David Sacks announced the administration’s intention to pass a stablecoin regulatory bill and a cryptocurrency market structure bill.

The White House missed its deadline on both of those bills but did eventually pass a stablecoin regulatory bill in the form of the GENIUS Act.

However, the market structure bill hasn’t yet been signed into law, and tomorrow is the White House’s new July 4 deadline for this legislation.

Read more: Crypto Czar and Republican Congressmen hope for legislation

Patrick Witt, one of Trump’s current advisors, previously stated the White House was targeting July 4 for the signing, saying, “I think that would be a tremendous birthday present for America, celebrating our 250th.”

He further added that should the act fail to reach this deadline, “we are going to be a rule follower, and we’re going to be following somebody else’s rulebook on this. And God forbid it’s China that’s ultimately writing those rules.”

Unfortunately for Witt’s natural paranoia, it seems extraordinarily unlikely that this bill will be passed today and signed tomorrow.

For one thing, the Senate isn’t meeting for floor proceedings today, making it impossible to pass a bill.

This Trumpian crypto failure was easily foreseen; Republicans are unwilling to place in an ethics provision that would limit Trump’s ability to profit from cryptocurrency, and Democrats have no incentive to bend on ethics rules when they can use it to tar Republicans as corrupt.

Moreover, the Senate cannot even pass important bills like the National Defense Authorization Act, which makes it even more hilarious that the White House was willing to publicly deceive the public into believing it was plausible that this bill would pass.

Even the Democrats who voted to move this bill out of the Banking Committee, Ruben Gallego and Angela Alsobrooks, have both stated that they have yet to determine their final vote on this act.

Other Trump cryptocurrency failures

This isn’t the only embarrassing miss when it comes to crypto for this administration.

Despite throwing the federal government, in the form of the Strategic Bitcoin Reserve, and his social media company/ETF provider, Trump Media and Technology Group, behind BTC, its value has plummeted during Trump’s administration.

Its price has fallen from approximately $106,000 to less than $62,000 now.

During Trump’s campaign he also insisted that all BTC should be “made in the US.”

However, there’s no substantial evidence that large amounts of BTC mining have relocated to the US, and some US-based miners have pivoted to providing infrastructure at their data centers to artificial intelligence.

When Trump created the Strategic Bitcoin Reserve, he also promised that it would include “XRP, SOL, and ADA.”

He later added ETH to the list as well.

These assets weren’t included in the strategic reserve, though they may be part of the US Digital Asset Stockpile, which holds the non-BTC digital assets that have ended up in the possession of the US government.

It’s hard to say with a high degree of certainty what assets may be included in there, as there’s very little transparency, and the reports that were demanded within 30 or 60 days have not been made public, so we’re left to speculate.

Had the reserve included these assets, it would have lost money on every single one since the stockpile was announced.

Some, like Cardano, have lost truly incredible amounts of value, plummeting by more than 80%.

Despite these problems, Trump has still been able to personally make billions of dollars from the crypto industry during these plunges.

Read more: ANALYSIS: Eric and Donald Trump Jr. are cashing in on crypto

World Liberty Financial, where he’s co-founder, passed its first governance proposal nearly 600 days ago. Despite that it’s failed to launch the Aave instance promised in that.

Trump Media and Technology Group filed for crypto exchange traded funds and then abandoned the idea.

Even his eponymous memecoin has suffered, dropping by more than 96% from its peak.

However, despite these failures, Trump has grown ever more wealthy; Indeed, his fortune is now many billions larger than it was when he became president.

Everyone else in the crypto ecosystem may be suffering, but perhaps that’s because they have yet to fully embrace the cartoonish corruption.

Sure, the bills aren’t being passed, the reports aren’t being published, and the prices are plummeting, but at least the president is able to get richer.

What could be more appropriate for the first crypto president than someone who’s far better at extracting money than advancing the industry?

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

Solana now beats Ethereum on trading volume, active users, and fee revenue. Ethereum still holds the money. Halfway through 2026, the question is no longer who is faster. It is whether the two chains are even running the same race.

Summary

- Solana has overtaken Ethereum in Layer 1 activity with higher transaction volume, more active users, stronger DEX trading, and greater fee revenue.

- Ethereum continues to dominate in total value locked, stablecoin liquidity, institutional adoption, and developer activity despite losing ground in onchain usage.

- The rivalry has shifted from a direct competition into two distinct models, with Ethereum focused on settlement and custody while Solana leads in trading and execution.

There was a time when the Ethereum versus Solana debate could be settled with a smirk and an outage screenshot. Solana was the chain that went down. Ethereum was the chain that mattered. Then Solana stopped going down, its trading volume flipped Ethereum’s, its ETF launched to institutional inflows while Ethereum funds bled for seventeen straight days, and the smirk changed sides.

Halfway through 2026, both tokens are deep in a bear market. ETH trades near $1,714 after a brutal second quarter that included a 29.5% thirty-day drawdown at the June lows, its worst quarterly stretch in years. SOL trades near $81, down roughly 78% from its cycle high, hit even harder in raw percentage terms. Price settles nothing here. The interesting story is underneath, in the on-chain data, where the two networks have diverged so completely that comparing them now requires deciding which metrics count.

So: is Ethereum losing the L1 race to Solana? The honest answer is that Solana has already won several of the events, Ethereum still owns the ones with the most prize money, and the race itself has split into two different sports.

How we got here: a short history of a long feud

The rivalry has run through three distinct acts, and the current one makes no sense without the first two.

Act one, 2021 through 2022, was Solana as the venture-backed challenger: a chain built for speed, championed by Sam Bankman-Fried, and dismissed by Ethereum partisans as a centralized science project. The dismissal briefly looked like prophecy. Solana suffered repeated full-network outages, including the infamous February 2024 halt that lasted nearly five hours after a legacy loader bug forced a coordinated validator restart, and when FTX collapsed in November 2022, SOL crashed toward single digits as the market priced in guilt by association. Obituaries were published. Several were smug.

Act two, 2023 through 2024, was the resurrection nobody ordered. Solana’s developer community kept shipping through the winter, the Jupiter and Jito ecosystems matured, memecoin mania found its natural home on the only chain where a thousand trades cost less than a sandwich, and DEX volume began the climb that ended with the flip of Ethereum in late 2024. Ethereum spent the same period executing its own plan flawlessly and discovering the plan had a hole in it: the Dencun upgrade in March 2024 introduced blob space and cut L2 costs by an order of magnitude, which supercharged rollup adoption while gutting the fee burn that had underwritten the ultrasound money narrative. Activity exploded across the Ethereum stack, and ETH the asset captured almost none of it.

Act three is now: both chains institutionally legitimate, both tokens deep underwater, and the argument relocated from architecture threads to fund flow tables. Uniswap founder Hayden Adams warned back in 2025 that Ethereum’s confused scaling identity could hand DeFi leadership to Solana; in 2026 that warning reads less like a hot take and more like a memo the market already acted on.

The scoreboard, metric by metric

Start with what Solana has flatly won: activity.

On a representative day in late June, Solana processed 127 million transactions from more than 2 million active addresses. Ethereum mainnet processed 2.8 million transactions from roughly 512,000 active addresses. That is not a gap. That is a different order of magnitude. Solana sustains 600 to 700 real transactions per second on average against Ethereum L1’s 15 to 20, at a cost of roughly $0.00025 per transaction against Ethereum’s dollars-per-swap mainnet pricing.

Trading volume tells the same story. Solana’s weekly DEX volume hit $11.49 billion in April against Ethereum’s $7.62 billion, a 51% lead. In February the monthly gap was wider still: $117 billion on Solana against $52 billion on Ethereum, more than double. Jupiter, the aggregator that routes the overwhelming majority of Solana order flow across Raydium, Orca, Phoenix, and Meteora, alone processes $2 billion to $4 billion in daily volume. Solana flipped Ethereum on DEX volume in late 2024 and has held the lead through every market condition since.

Then comes the metric that should worry Ethereum researchers most: revenue.

Solana generates over $1 million in chain fees per day. The major Ethereum L2s, where most Ethereum user activity now lives, generate under $200,000 combined, because blob-based data posting after the Dencun upgrade pushed L2 costs, and therefore L2 fee revenue, toward zero. Ethereum deliberately commoditized its own execution layer to win the rollup war. The result is a settlement layer with shrinking direct income and a rival that monetizes every swap on a single unified ledger.

Now flip the card, because Ethereum’s wins are just as lopsided.

Total value locked

Ethereum L1 holds roughly $55.6 billion in DeFi deposits, around 68% of the entire global DeFi market, and the combined L1 plus L2 figure exceeds $80 billion. Solana holds between $8 billion and $12 billion depending on the week and the methodology, a figure that took a $270 million hit in April when the Drift Protocol exploit tore through its perps ecosystem. The deepest protocols in the industry, Lido at $27.5 billion, Aave at $27 billion, EigenLayer at $13 billion, all live on Ethereum, and Aave V4 launched on Ethereum mainnet in April to reinforce the point.

Stablecoins

Ethereum hosts roughly 70% of all on-chain stablecoin supply, around $32 billion in USDC and $60 billion in USDT, and remains the venue where BlackRock, Franklin Templeton, and JPMorgan build tokenized products first. Solana carries about $14 billion in stablecoins, though each of those dollars turns over roughly six times faster than its Ethereum counterpart.

Developers

Ethereum counted 31,869 active developers against Solana’s 17,708 at the latest Electric Capital reading, and added more new developers over the trailing year than any other ecosystem. Solana ranked second.

One chain has the users, the volume, and the revenue. The other has the money, the institutions, and the builders. Losing, it turns out, depends entirely on where you point the camera.

How the race split in two

The reason the comparison keeps producing contradictory answers is that the two chains stopped competing on the same terms years ago, a divergence we chronicled when the ecosystems first collided in early 2025.

Ethereum abandoned the monolithic race on purpose. Its roadmap treats the base layer as settlement infrastructure while execution migrates to rollups: Base, Arbitrum, Optimism, and a long tail of zk systems that post proofs and data back to mainnet. Base alone captures nearly half of all L2 DeFi value, Arbitrum another 31%, and the top three rollups process close to 90% of all L2 transactions. Measured as a stack, the Ethereum ecosystem still dwarfs Solana on almost every capital metric. Measured as an L1, Ethereum mainnet is a slow, expensive chain that its own designers no longer intend retail users to touch.

Solana made the opposite bet: one ledger, one global state, sub-second finality at 400 milliseconds, and a relentless engineering campaign to make the single chain fast enough that nothing else is needed. The Firedancer validator client built by Jump Crypto, rolling toward full deployment late this year, is the endgame of that bet, with a theoretical ceiling measured in the hundreds of thousands of transactions per second. The network reliability problem that defined Solana’s reputation in 2022 and 2023 has largely disappeared; outages went from routine to rare, and the chain has traded its crash-prone image for something closer to an execution monopoly on retail flow.

The philosophical split produces the statistical one. Capital sits and compounds on Ethereum because that is what the architecture rewards: deep pools, long-duration lending, staking layered on restaking. Capital churns on Solana because sub-cent fees make churning free: high-frequency trading, memecoin rotation, dollar-cost-average bots, payments. Ethereum became the deposit ledger. Solana became the trading floor.

Follow the fees: two broken business models, one working one

The revenue gap deserves its own examination, because it is the metric where architecture decisions turn into economics, and where both chains have problems they rarely advertise.

Ethereum’s fee engine used to be the envy of the industry. EIP-1559 burned base fees, high demand made ETH deflationary, and the ultrasound money framing wrote itself. The rollup migration dismantled the machine step by step. Execution moved to L2s, whose sequencers keep the margin between what users pay and what blob posting costs, and Dencun made blob posting cost next to nothing. The result in 2026: mainnet burns a fraction of its former fee load, L2s pay Ethereum pennies for security worth billions, and the value accrual question, what does ETH earn when Base wins, has replaced scaling as the ecosystem’s defining unsolved problem. Ethereum built a settlement business and priced its product like a public good.

Solana’s engine is simpler and currently stronger: one chain captures every fee at every layer. The base fee is fixed at 5,000 lamports per signature, roughly a hundredth of a cent, while priority fees let users bid during congestion, and stake-weighted quality of service plus local fee markets keep hot accounts from clogging the scheduler. On top of the protocol fees sits the Jito MEV economy, where searcher tips flow to validators and stakers, turning order-flow chaos into staking yield. Over $1 million in daily chain revenue against sub-$200,000 for the entire major L2 basket is the visible output.

The caveat is concentration of source. A large share of Solana’s fee revenue traces to speculative trading, memecoins above all, which makes the revenue line high-beta to the exact market segment least likely to survive a deep winter. Ethereum’s fee problem is structural but its demand is diversified; Solana’s fee machine works beautifully and runs on the most flammable fuel in crypto. Neither model is finished.

Fusaka and the second-half Ethereum upgrade path aim at scaling data further without answering value capture, while Solana’s validator economics, where thin margins already pushed the validator count down 68% from its 2023 peak, depend on fee and MEV income holding up.

The other front: stablecoins, payments, and tokenized everything

DEX volume gets the headlines, but the war’s second front may matter more by 2027, because it is the one institutions actually fund: who carries the tokenized economy.

Ethereum’s position is incumbency at scale. Roughly 70% of stablecoin supply, the deep USDC and USDT float that institutional desks require, and essentially the entire first generation of tokenized funds. When Ondo debuted its SEC-aligned tokenized stock model with BlackRock ETF shares this week, the underlying rails were Ethereum-ecosystem by default. Stablecoin legislation cleared the path for bank issuance and for the consortium models now emerging among major institutions, and banks build where the auditors already have coverage, which is one more network effect compounding for the incumbent.

Solana’s position is velocity and consumer reach. Its $14 billion stablecoin float turns over roughly six times faster than Ethereum’s, because sub-cent fees make stablecoins usable as money instead of just collateral. USDC settles on Solana in under a second for a fraction of a cent, which is why Visa chose it for settlement pilots, why payment processors keep adding it, and why the Solana Developer Platform launched with Mastercard, Worldpay, and Western Union rather than with hedge funds. Solana is also mounting a genuine RWA challenge through Token-2022, whose compliance extensions target exactly the issuer requirements Ethereum handles with bespoke contracts, and both chains now face a third competitor for the same institutional flow in the compliance-native stack being assembled on the XRP Ledger.

The stakes here dwarf the DEX war. Stablecoins are a $320 billion asset class growing through legislation, and tokenized funds are the institutional product with the steepest adoption curve. If Ethereum keeps the float while Solana takes the flow, the split-decision structure of this whole rivalry repeats at a much larger scale, with Ethereum as the vault and Solana as the checkout lane of tokenized finance.

The institutional tiebreaker

For most of crypto history, the institutional column belonged to Ethereum without argument. That is the column where 2026 has produced genuine movement.

The regulatory sequence mattered first. The SEC’s March 2025 classification of sixteen digital assets including SOL as commodities dissolved the securities overhang that had kept allocators away, and spot Solana ETFs began trading on October 28, 2025, making SOL the third asset after BTC and ETH with U.S. spot fund access. The flows since then have been small next to Bitcoin’s but directionally embarrassing for Ethereum: through the spring drawdown, Solana ETFs crossed $1 billion in cumulative inflows while Ethereum funds posted a seventeen-day outflow streak that stripped hundreds of millions, and July has opened with ETF flow reports showing ETH and SOL products gaining together while Bitcoin funds bleed. Goldman Sachs disclosures showed over $100 million in SOL exposure, and CalPERS entered the asset class the same quarter.

Solana’s institutional push went beyond funds. The Solana Foundation launched its Developer Platform in March with Mastercard, Worldpay, and Western Union among early adopters, shipped a quantum-readiness plan built on the NIST-standardized Falcon signature scheme in April, and rolled out on-chain, stake-weighted validator governance this week. Token-2022 extensions gave the chain the compliance hooks, confidential transfers, transfer restrictions, interest-bearing instruments, that enterprise issuers require. The pitch that Solana is a casino chain unsuitable for serious money has aged badly.

Ethereum’s institutional position remains the stronger one on stock rather than flow. It custodies the tokenized funds, hosts the deep stablecoin float, and runs the staking infrastructure through which more than 35 million ETH, nearly 29% of supply, secures the network across a million-plus validators. When a treasury desk needs to move nine figures with minimal slippage, Ethereum’s depth is still the only game available. BitMine Immersion bought its way past 5 million ETH this spring precisely on that thesis. But stock is what you accumulated yesterday. Flow is what you are winning today, and the flow has been tilting one direction for over a year.

The uncomfortable items on both ledgers

Neither chain gets to run its highlight reel without the blooper file.

Solana’s validator count has collapsed to roughly 795 active validators from more than 2,500 in 2023, a 68% decline that concentrates block production and hands critics a decentralization argument with real teeth. Its DeFi remains thin and concentrated: one aggregator with 95% market share is a single point of failure wearing a market structure costume, and the $270 million Drift exploit showed what happens when a load-bearing protocol breaks. Its volume mix still leans on memecoin speculation, the most cyclical demand source in the industry, and February’s $117 billion month can become a $40 billion month without a single thing going wrong technically.

Ethereum’s problems are quieter and arguably deeper. Lido alone controls roughly 24% of staked ETH, a concentration risk of its own. The rollup roadmap solved scaling and created a value-capture puzzle nobody has answered: if execution fees accrue to Base and Arbitrum while blobs cost pennies, what exactly does ETH the asset earn from Ethereum the ecosystem’s growth? Retail has already voted, migrating to L2s so completely that mainnet active addresses look like a ghost town next to Solana’s. And the fragmentation tax is real: liquidity split across a dozen rollups with seven-day optimistic exits is a worse user experience than one chain with 400-millisecond finality, no matter how elegant the settlement theory. The KelpDAO exploit this spring, which erased $13 billion of TVL in 48 hours of contagion, showed that composability depth cuts in both directions.

Both assets, meanwhile, have been terrible investments this year, a market-wide condition tied to the macro regime we examined in the context of Bitcoin’s liquidity dependence. Fee revenue and active addresses have not protected SOL holders from a 78% peak drawdown, and settlement supremacy has not protected ETH holders from underperforming Bitcoin for most of the cycle. Whatever race is being run, neither token’s chart looks like a victory lap, and on-chain fundamentals have been decoupled from price across the majors for much of 2026.

So who is actually winning?

Frame the question three ways and you get three defensible answers.

If the L1 race means base-layer usage, Solana won it, and the margin is no longer close. Two hundred times Ethereum’s L1 throughput, forty times its transaction count, five times its daily fee revenue, and a lead in DEX volume that has survived every market regime since late 2024. By the definition of Layer 1 that existed when the rivalry started, the contest is over.

If the race means where value lives, Ethereum is not losing and may never lose within this cycle. A 68% share of global DeFi TVL, 70% of stablecoin supply, the institutional tokenization pipeline, and the largest developer base in the industry constitute a network-effect fortress that Solana’s growth has dented but nowhere near breached. Capital has inertia, and inertia compounds.

If the race means trajectory, the tape favors Solana with an asterisk. It is winning new users, new listed products, new enterprise integrations, and the ETF flow battle. The asterisk is that trajectory arguments assume the current regime persists, and Solana’s flow-heavy economy is more exposed than Ethereum’s stock-heavy one to the next collapse in speculative appetite. Ethereum’s Fusaka upgrade cycle and the second-half protocol roadmap that all major chains have queued for late 2026 could reshuffle the technical comparison again.

The most likely outcome is also the least satisfying for partisans: permanent coexistence with divided territory. Ethereum settles and custodies. Solana executes and trades. Builders already behave as if this is settled, deploying on both by default. The 2025 framing of an L1 war with a single survivor has quietly died, not with a bang but with two chains discovering they are optimized for markets the other cannot serve.

What could flip the board before December

Split decisions invite the obvious follow-up: what would actually change the standings? Four live catalysts carry enough weight to move the argument rather than the noise.

Ethereum’s upgrade cycle is the first. The Fusaka window and the broader second-half protocol roadmap target another step-change in data capacity, and the ecosystem’s real prize sits next to it: any credible mechanism that routes L2 economic success back into ETH, whether through based sequencing, native rollup designs, or fee-market reform, would repair the value-capture hole that has haunted the asset since Dencun. Markets have front-run Ethereum upgrades before; a roadmap that finally answers the accrual question would be the first fundamental ETH catalyst in two years.

Firedancer completion is the second. Solana’s independent validator client moving to full deployment removes the single-client risk that institutions cite most, and its throughput headroom opens application categories, full order-book markets, high-frequency payment networks, that no chain currently serves. If even one breakout consumer or enterprise application lands on that capacity, Solana’s volume base diversifies away from memecoins, which neutralizes the strongest bear argument against its fee economy.

ETF mechanics are the third. Staking-enabled fund structures, under active regulatory discussion for both assets, would transform the flow picture: a spot product yielding 3% to 7% natively changes the allocator pitch entirely, and the asset that gets staking approval first inherits a durable flow advantage. Watch the filings, not the influencers.

Treasury companies are the fourth and strangest. BitMine’s multimillion-ETH accumulation and the emerging class of SOL treasury vehicles mean corporate balance sheets now sit inside both ecosystems as permanent, price-insensitive holders. The Strategy playbook applied to ETH and SOL is small today; its growth rate through a recovering market could make treasuries the marginal buyer that decides which token outperforms, independent of every on-chain metric in this article.

The verdict for the second half

Ethereum is losing the L1 race as originally defined, and it forfeited that race by choice when it went all-in on rollups. Solana is winning everything measurable at the base layer while still trailing badly where the institutional money actually sits. Watch three numbers through December: whether Ethereum ETF flows recover once its next upgrade lands, whether Firedancer’s full rollout converts Solana’s throughput ceiling into new categories of application, and whether Solana DeFi TVL can hold above $12 billion without memecoin volume subsidizing it. The chain that answers its own weakness first will own the 2027 narrative. Until then, the war everyone expected has settled into something stranger: two winners, two different games, and one increasingly obsolete question.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Digital asset markets are volatile, and you can lose your entire investment. Always do your own research. Information current as of July 3, 2026.

Bitcoin is attempting to build a short-term recovery after weeks of sustained selling pressure. Although buyers have defended a key support zone, the broader trend remains fragile as price continues to trade beneath major technical resistance levels that must be cleared first to expect a genuine recovery.

Bitcoin Price Analysis: The Daily Chart

The daily chart continues to reflect a bearish market structure, with BTC trading around $62.1K. The price remains well below both the 100-day and 200-day moving averages, which are now acting as dynamic resistance around the $71K to $75K region. As long as BTC remains beneath these averages, sellers are likely to maintain control.

Following the sharp breakdown below the 100-day moving average near $72K earlier this month, the market found demand within the $60K support zone. This area has once again prevented a deeper decline and is currently fueling a modest rebound. The RSI has also formed a bullish divergence, with higher lows while price recorded lower lows, indicating that bearish momentum is fading and a short-term recovery is possible.

However, the broader trend remains bearish. Even if buyers extend the current bounce, the first major obstacle lies between $72K and $75K, where previous support has turned into resistance alongside both moving averages. A successful recovery above this region would improve the medium-term outlook, while rejection could expose the $60k support once again. Losing that area would likely open the door toward the next major demand zone around $55K.

BTC/USDT 4-Hour Chart

The 4-hour timeframe presents a more constructive picture. Bitcoin has been trading inside a broad falling wedge following the sharp June sell-off, a pattern that often precedes bullish reversals when confirmed by a breakout.

Price has recently rebounded from the wedge’s lower boundary and the $60K support zone. At the same time, the RSI has produced another bullish divergence, reinforcing the idea that selling pressure is gradually weakening.

The next important hurdle lies near the wedge’s descending upper trendline, which currently aligns with the $62K level. A breakout above this resistance could trigger a stronger recovery toward the $66K to $68K supply zone. Beyond that, the much larger resistance area between $72K and $74K remains the key barrier to any meaningful trend reversal.

Failure to break the wedge would keep the broader bearish structure intact and increase the probability of a drop below the $60K support.

Sentiment Analysis

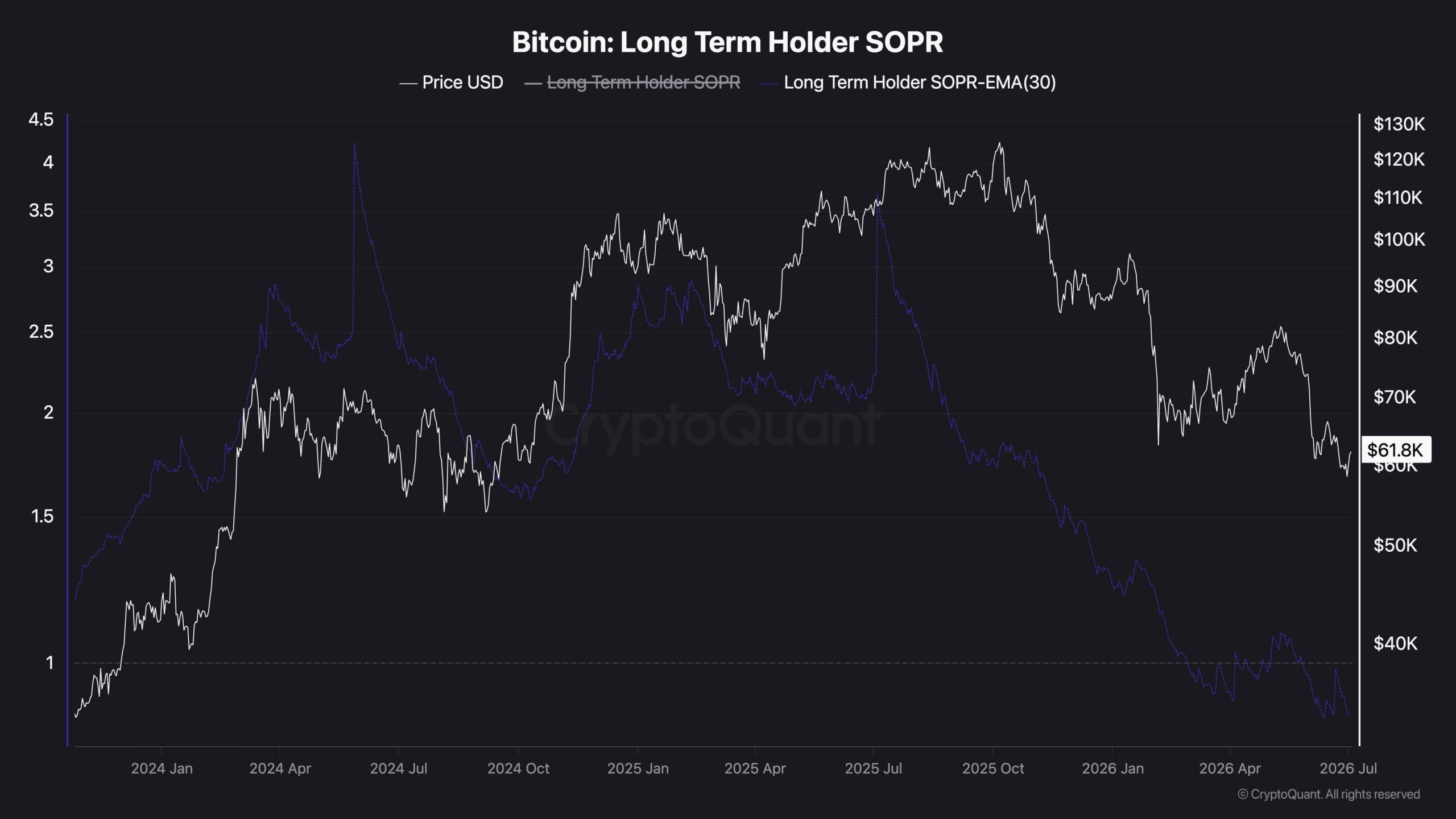

The Long-Term Holder SOPR (Spent Output Profit Ratio) continues to trend below the critical 1.0 threshold, indicating that long-term holders are, on average, realizing losses when spending their coins. Historically, sustained readings below 1.0 reflect periods of market stress, where even experienced investors begin distributing coins at a loss rather than taking profits.

The 30-day EMA of the metric has continued to weaken and now sits below the neutral level, suggesting this behavior has become persistent rather than temporary. This points to subdued investor confidence and confirms that long-term holders have yet to return to meaningful profit-taking.

While this reflects ongoing bearish sentiment, prolonged periods of LTH SOPR below 1.0 have often coincided with the later stages of market corrections, as weaker conviction is gradually exhausted. A recovery of the metric back above 1.0 would signal that long-term holders are once again spending coins in profit, a shift that has historically aligned with improving market conditions and a healthier uptrend. Until then, the on-chain data suggests the broader market remains in a phase of capitulation and recovery rather than a confirmed bullish reversal.

The post Bitcoin Recovery Hinges on Breakout Above $72K Resistance (BTC Price Analysis) appeared first on CryptoPotato.

Crypto World

Bitcoin Recovers Toward $62K as ETF Inflows Return and Trump’s BTC Holdings Make Waves: Weekly Crypto Update

Although July has only just begun, the past seven days brought some much-needed and long-awaited relief to the cryptocurrency market, even if the overall sentiment remains nothing but fragile.

Last week at this time, Bitcoin was still struggling around the $60,000 mark after the painful correction that was charted in June. The cryptocurrency spent the weekend moving mostly sideways, as neither bulls nor bears managed to take control.

The real action only started at the beginning of the business week. BTC attempted to recover, but was quickly rejected near $60,700, which allowed the sellers to push it lower. The pressure intensified on Tuesday, when Bitcoin, alongside the majority of the broader market, including the S&P500, the Nasdaq, as well as major tech stocks, took a beating. BTC dumped below $59,000 and slipped toward $58K on some exchanges, marking its intraweek low.

However, that support held firm. The cryptocurrency bounced back and quickly reclaimed $60,000. Later, it pushed toward $62,000 as buyers returned and spot Bitcoin ETFs finally saw renewed inflows after a brutal streak of outflows.

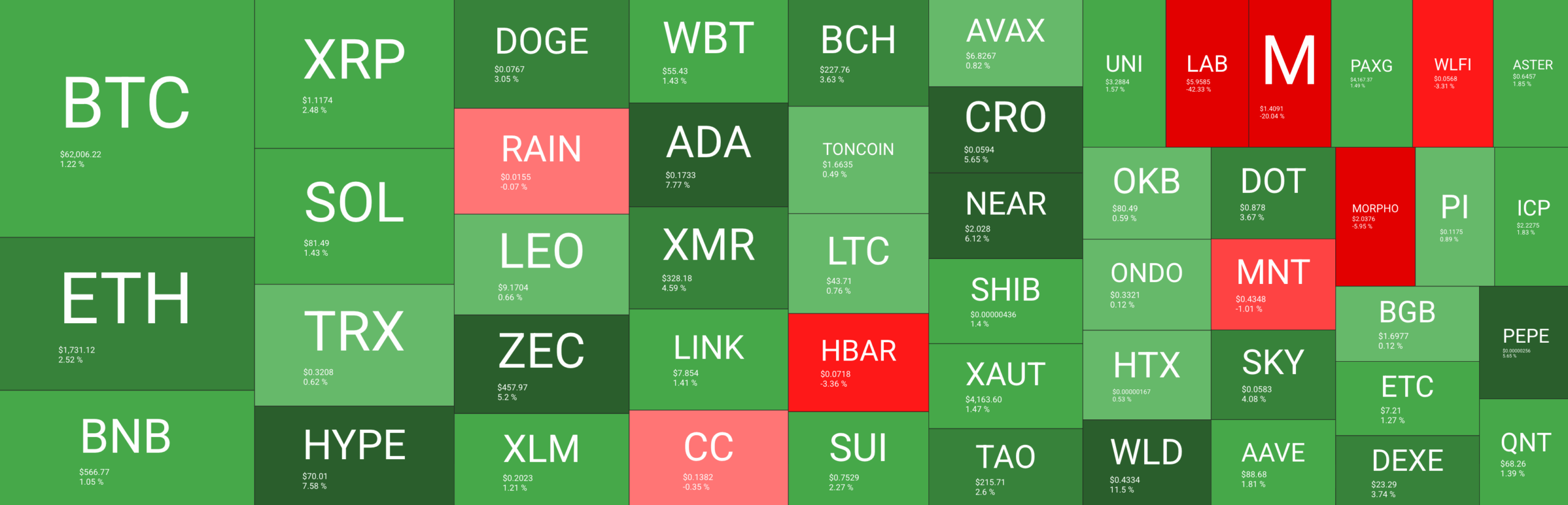

Altcoins were also able to follow, and some of them even marked sharper increases. ETH recovered strongly and moved back toward $1700, while SOL was among the best performers with a double-digit weekly jump. XRP, DOGE, ADA, XLM, and HYPE also joined the rebound, helping the total crypto market cap recover some of its recent losses.

The week was also packed with some major headlines. Donald Trump’s latest financial disclosure showed that he holds more than $50 million in Bitcoin, reigniting strong debates. FBI Director Kash Patel also amended a disclosure that was associated with Strategy’s stock, while Securitize made its NYSE debut and launched tokenized shares on Solana and Avalanche.

Overall, the bulls were finally able to stop the bleeding. However, this doesn’t mean that the worst is over. BTC still needs a decisive breakout above pivotal levels around $70K to prove that this was more than just a slight dead cat bounce.

Market Data

Market Cap: $2.22T | 24H Vol: $66B | BTC Dominance: 56%

BTC: $62,000(+2.7%) | ETH: $1,731 (+9.6%) | XRP: $1.12 (+7.2%)

This Week’s Crypto Headlines You Can’t Miss

Tokenized Stocks Emerge as Altcoin Lifeline Amid Crypto Market Reset. A new report argued that tokenized stocks are becoming one of crypto’s few bright spots, as persistent token unlocks and weak altcoin narratives continue to wear speculative assets down. The analyst also outlined that Solana is currently dominating tokenized equity trading alongside Hyperliquid’s HIP-3.

Why Bitwise’s Matt Hougan Thinks Strategy’s Bitcoin Era Is Fading. The CEO of Bitwise, Matt Hougan, said that Strategy’s role as one of the largest corporate buyers of Bitcoin is likely going to fade, especially as the next cycle could be led by institutions such as banks, asset managers, pension funds, and sovereign wealth funds.

Standard Chartered Becomes First Major Bank to Offer Direct Stablecoin Services. Standard Chartered became the very first major global bank to offer direct USDC minting and redemption services to institutional clients through its banking platform. The service was launched with Circle in Dubai’s DIFC.

Can Circle Defend Its Stablecoin Lead Against OpenUSD? Experts Weigh In. Experts, on the other hand, warned that Circle itself might be facing one of its toughest challenges yet from OpenUSD – a new stablecoin backed by major financial and payments firms such as Visa, Mastercard, BlackRock, and Coinbase.

UK Investors Sue Binance and Former CEO Changpeng Zhao for $200M. A group of 1,700 UK investors sued Binance and its former CEO – Changpeng Zhao – in London’s High Court. The plaintiffs seek roughly $200 million in damages, claiming that the exchange sold unauthorized derivatives products.

The Vanishing Bitcoin Bid: Where Are the ETF Billions Going? HashKey research Tim Sun told us that Bitcoin’s recent ETF outflows may reflect capital rotating into AI, semiconductors, and GPU-related stocks rather than a complete collapse in risk appetite.

Charts

This week, we have a chart analysis of Ethereum, Ripple, Cardano, Binance Coin, and Hyperliquid – click here for the complete price analysis.

The post Bitcoin Recovers Toward $62K as ETF Inflows Return and Trump’s BTC Holdings Make Waves: Weekly Crypto Update appeared first on CryptoPotato.

Bitwise has strengthened its proposed spot NEAR ETF with a staking feature in a new SEC filing, helping drive NEAR nearly 12% higher as the token broke above a multi-week downtrend.

Summary

- Bitwise has updated its proposed spot NEAR ETF, adding staking while naming NYSE Arca, BNY Mellon, and Coinbase Custody in the filing.

- NEAR jumped nearly 12% as the ETF amendment coincided with a breakout above multi-week descending resistance and improving momentum indicators.

- Analyst Michaël van de Poppe expects further upside if key support holds, while Grayscale has also advanced its own NEAR ETF proposal.

According to a revised S-1 registration statement submitted to the U.S. Securities and Exchange Commission, Bitwise has amended its proposed spot NEAR ETF for a second time, adding staking as a source of potential rewards alongside the fund’s primary objective of tracking the value of NEAR held by the trust.

The filing also confirms that the ETF is intended to list on NYSE Arca, while The Bank of New York Mellon will act as cash custodian, administrator and transfer agent, with Coinbase Custody safeguarding the fund’s digital assets.

The amendment also expands disclosures covering staking-related tax treatment, redemption liquidity and cryptocurrency market risks. Bitwise has not yet disclosed the ETF’s ticker symbol or management fee, and the proposal remains subject to SEC approval.

ETF filing coincides with a technical breakout

The revised filing arrived as NEAR staged one of its strongest rallies in weeks.

According to data from crypto.news, NEAR Protocol (NEAR) climbed nearly 12% to around $2.04 on July 3, extending a recovery that began earlier in the week. While the ETF amendment alone cannot be credited for the move, it arrived as the token was testing a critical technical level, providing a catalyst that coincided with a bullish breakout already taking shape.

On the four-hour chart, NEAR broke above a descending trendline that had capped every rally since the token peaked near $2.56 in mid-June. The breakout also carried price back above the 61.8% Fibonacci retracement level at roughly $2.04, a level many traders monitor for confirmation that buyers are regaining control after a prolonged correction.

Momentum indicators also turned more constructive. The Moving Average Convergence Divergence indicator maintained a bullish crossover with a rising positive histogram, while the Aroon indicator showed Aroon Up at 100 and Aroon Down near 14, signaling that buyers currently dominate the short-term trend.

If the breakout holds, the next resistance levels lie around $2.14 and $2.24, followed by the $2.36 region. A successful move through those levels could open the way for a retest of the June high near $2.56, while the former breakout area around $1.90 has become the first key support.

Analysts see improving market structure

Adding to the bullish technical picture, analyst Michaël van de Poppe said he increased his NEAR position around $1.82, describing the recent weakness as an attractive accumulation opportunity.

According to van de Poppe, NEAR is “clearly breaking back into an uptrend” after defending support near €1.70 (around $2.00). He added that holding this area could pave the way for a rally toward €2.20-€2.30 (roughly $2.58-$2.70), which he said would strengthen the case for new highs later in the summer.

The improving chart structure broadly aligns with that outlook. After several weeks of setting lower highs, NEAR has now established a higher low, reclaimed a key Fibonacci level and broken through descending resistance.

Although continued buying volume will be needed to confirm the reversal, the combination of Bitwise’s updated ETF filing, strengthening momentum indicators and renewed institutional interest has improved the token’s near-term technical outlook.

Institutional demand for NEAR investment products has also been building elsewhere. Earlier, crypto.news reported that Grayscale filed an amended registration statement for its own proposed spot NEAR ETF, adding another issuer to the growing race to launch regulated investment products tied to the network.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Bitget, the world’s largest Universal Exchange (UEX), has published CEO Gracy Chen’s mid-year address, outlining the company’s long-term vision for a more connected financial system powered by tokenization, artificial intelligence, and universal market access.

The leadership’s insights come as trading behavior continues to evolve beyond crypto alone. During the first half of 2026 the platform witnessed the shift, about 52% Bitget users now hold both stocks and crypto, 35% hold gold and other precious metals while 51% users use AI-powered tools. This highlights the growing demand for platforms that bring global markets together leveraging emerging tech.

Rather than becoming an “asset supermarket,” Bitget aims to remove the friction that separates financial markets. The letter outlines four principles guiding that strategy: improving capital efficiency, delivering global assets through a crypto-native experience, expanding financial access through products such as tokenized assets and pre-IPO investing, and simplifying trading through AI-powered automation.

“Our focus has pivoted from being a crypto exchange to a holistic universal provider,” said Gracy Chen, CEO of Bitget. “Our platform removes barriers that divided financial markets for decades. Users can now access crypto, stocks, CFDs, gold and do more with their capital 24/7.”

Bitget’s conviction on tokenization reshaping capital markets is based on Chen’s 10% tokenization vision, while highlighting products such as Stock+ and Reality as early examples of how blockchain infrastructure can make investing more accessible and efficient.

Artificial intelligence forms the second major pillar of the vision. As AI evolves from analysis toward execution, Chen described a future where users define investment goals and risk parameters while intelligent systems handle market monitoring and trade execution. Bitget now serves more than one million AI trading users alongside more than one million copy trading users, following the rollout of products including GetClaw and the GetAgent Playbook.

Closing the address, Chen described Bitget’s broader mission as extending financial opportunity beyond traditional institutional channels, calling it the shift from banking the unbanked to brokering the unbrokered.

Read the full “Break the Unbreakables” address here, or watch the address on Bitget’s X.

About Bitget

Bitget is the world’s largest Universal Exchange (UEX), serving over 125 million users and offering access to over 2M crypto tokens, 500+ tokenized stocks, ETFs, commodities, FX, and precious metals such as gold. The ecosystem is committed to helping users trade smarter with its AI agent, which co-pilots trade execution. Bitget is driving crypto adoption through strategic partnerships with LALIGA and MotoGP™. Aligned with its global impact strategy, Bitget has joined hands with UNICEF to support blockchain education for 1.1 million people by 2027. Bitget currently leads in the tokenized TradFi market, providing the industry’s lowest fees and highest liquidity across 150 regions worldwide.

For more information, visit: Website | X | Telegram | LinkedIn | Discord

Risk Warning: Digital asset prices are subject to fluctuation and may experience significant volatility. Investors are advised to only allocate funds they can afford to lose. The value of any investment may be impacted, and there is a possibility that financial objectives may not be met, nor the principal investment recovered. Independent financial advice should always be sought, and personal financial experience and standing carefully considered. Past performance is not a reliable indicator of future results. Bitget accepts no liability for any potential losses incurred. Nothing contained herein should be construed as financial advice. For further information, please refer to our Terms of Use.

The post Bitget CEO Gracy Chen Shares H1 2026 Remarks Highlight Company’s Strategy appeared first on BeInCrypto.

The European Securities and Markets Authority (ESMA) has warned that many prediction market contracts may already fall under existing restrictions on binary options, saying companies cannot avoid financial regulations simply by marketing them as “event contracts.”

In a public statement on Friday, the regulator reminded companies that event contracts meeting the definition of financial instruments are already prohibited from being marketed, distributed or sold to retail investors under national measures implementing ESMA’s 2018 binary options restrictions.

ESMA said the assessment depends on a contract’s characteristics rather than how it is marketed, adding that event contracts with binary outcomes and fixed payouts are likely to qualify as financial instruments subject to the restrictions.

The regulator also told companies that offering qualifying event contracts to professional or institutional clients still requires authorization under the EU’s Markets in Financial Instruments Directive, or MiFID II, regardless of whether retail investors are excluded.

Excerpt from ESMA’s July statement on event contracts. Source: ESMA

The statement does not introduce new restrictions. ESMA said it issued the reminder after observing increased offerings of event contracts and the rapid growth of prediction markets, noting that qualifying binary options have already been subject to national restrictions across the EU since 2018.

Related: StanChart joins ESMA’s first MiCA register update since deadline

US prediction markets face growing legal battle

In the United States, a regulatory battle over prediction markets is unfolding, pitting state gaming regulators against the Commodity Futures Trading Commission (CFTC) over whether event contracts should be treated as gambling or federally regulated derivatives.

By March, authorities in 11 states had taken legal or regulatory action against platforms including Kalshi and Polymarket. Nevada became the first state to temporarily block Kalshi’s operations, while Arizona brought criminal charges alleging the company was operating an illegal gambling business.

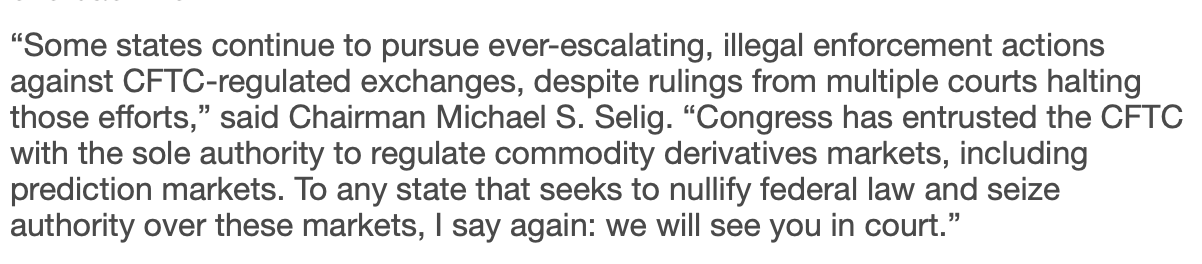

The following month, the CFTC asserted “exclusive jurisdiction” over prediction markets, saying Congress had entrusted the agency with sole authority to regulate commodity derivatives markets, including event contracts. The regulator also said it had sued several states and filed court briefs supporting platforms, including Kalshi.

The CFTC’s April announcement defending its authority over prediction markets. Source: CFTC.gov

The legal battle has continued to escalate. On June 30, a Massachusetts judge allowed state authorities to file an amended complaint against Kalshi in an ongoing lawsuit alleging that the company’s sports-event contracts constitute illegal gambling under state law.

The dispute has also prompted calls for congressional action. Last month, the Indian Gaming Association and American Gaming Association, joined by tribal and labor groups, urged lawmakers to amend the CLARITY Act to explicitly prohibit sports-related event contracts on prediction market platforms, arguing they fall outside the CFTC’s authority and should remain subject to state gambling laws.

Some legal experts believe the growing conflict between federal and state regulators over prediction markets could ultimately be decided by the US Supreme Court.

Magazine: Bitcoin slides to $58K, XRP hits $1 but onchain data promising: Market Moves

Why Pope Leo has excommunicated a group of conservative Catholics

England’s 1am World Cup match: unions urge employers to allow flexible working

Bitcoin Maximalism Faces Capital Market Realities, Crypto Biz Notes

-

Tech6 days ago

Tech6 days agoClaude Code turned every engineer into three. Now companies need more product thinkers

-

Crypto World4 days ago

Crypto World4 days agoStrategy authorizes up to $1.25B in Bitcoin sales under new capital plan

-

Politics6 hours ago

Politics6 hours agoThe House | “Reframing the debate from a binary discussion of winners and losers”: Yuan Yang reviews ‘We Are Not Machines’

-

News Videos5 days ago

News Videos5 days agoMAJOR BITCOIN & MARKET UPDATE!!!! (MUST WATCH ASAP!!!)

-

Tech4 days ago

Tech4 days agoAnonymous researcher drops 0-day ‘exploitarium’ repo

-

Crypto World6 days ago

Crypto World6 days agoCoinbase, Circle Deepen Crypto Stock Losses Despite Resilient S&P 500

-

Business4 days ago

Business4 days agoAustralia treasurer says alleged access of prime minister’s bank data ’incredibly concerning’

-

Crypto World7 days ago

Crypto World7 days agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Sports7 days ago

Sports7 days agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Tech6 days ago

Tech6 days agoBluekit phishing kit adopts browser-in-the-middle for login theft

-

Tech6 days ago

Tech6 days agoRussian hackers now target Signal backup recovery keys

-

Business4 days ago

Business4 days agoThe AI boom won’t burst all at once. It will pop in ‘rolling bubbles’: Macquarie

-

Sports2 days ago

Sports2 days agoBroncos roster: OL Ben Powers (No. 74) entering final year of contract

-

Tech6 days ago

Tech6 days agoSilicon Valley paid to kill AI regulation, now it wants the rules back

-

NewsBeat3 days ago

NewsBeat3 days agoPresenter Caroline Flack’s brother Paul Flack dies aged 55

-

Crypto World2 days ago

Crypto World2 days agoBinance stock trading tops $1B in first month after launch

-

NewsBeat1 day ago

NewsBeat1 day agoNew exhibition reflects five decades of movement between island of Ireland and GB

-

Tech6 days ago

Tech6 days agoOpenAI mulls delaying IPO over valuation concerns

-

Crypto World2 days ago

Crypto World2 days agoAlibaba-affiliate Ant Group enters the humanoid robot market with 12 deals

-

News Videos3 days ago

News Videos3 days agoHow to Build INSANE Live Financial Dashboards With Claude

You must be logged in to post a comment Login