Crypto World

DoubleLine’s Jeffrey Gundlach sees no more Fed rate cuts under Jerome Powell

DoubleLine Capital CEO Jeffrey Gundlach said Wednesday he expects the Federal Reserve to stay on hold for the remainder of Jerome Powell‘s term as chair with a more balanced outlook for the economy.

“I think I would bet pretty heavily that there’s not another rate cut under Jay Powell,” Gundlach said on CNBC’s “Closing Bell.” “I think he’s going out of his way to emphasize that inflation is a little elevated, but not as bad as maybe it was feared a few months ago, that the unemployment rate is no longer separately rising in any kind of meaningful way.”

Powell has just two policy meetings left as chair — in March and April — before his term expires. A new chair would take the helm for the June meeting, assuming Senate confirmation.

On Wednesday, the central bank kept its overnight lending rate steady at a range of 3.5% to 3.75%. The post-meeting statement suggested that economic activity has been “expanding at a solid pace,” while policymakers also noted that the unemployment rate has shown some signs of stabilization.

“I think, and many of my colleagues think, it’s hard to look at the incoming data and say the policy is significantly restrictive at this time,” said Powell during his press conference.

Fed funds futures trading suggests two quarter percentage point cuts by the end of 2026, according to the CME FedWatch Tool.

“He’s talking about less tension between both sides of the mandate, and I really agree with that,” Gundlach said, referring to the Fed’s dual goals of price stability and maximum employment. “And I think he’s setting the stage.”

Gundlach reiterated his preference for international exposure, saying investors should consider allocating 30% to 40% of their portfolios to unhedged international equities. He said such positions could benefit from gains in local currencies against the U.S. dollar.

Welcome to our institutional newsletter, Crypto Long & Short. This week:

- Bob Williams on how stricter crypto regulations in Asia are putting more personal responsibility on senior leaders, making strong governance and D&O insurance essential.

- The FBI’s Haidy Grigsby on how crypto scams are increasingly targeting experienced investors by building trust and tricking them into making larger deposits until their money is gone.

- Top headlines institutions should pay attention to by Francisco Rodrigues.

- Hyperliquid’s TradFi bet is now 40% of its own volume in Chart of the Week.

Expert Insights

Asia’s digital asset crackdown: accountability gets personal

By Bob Williams, FinTech, digital assets, & blockchain advisory leader (Asia/Pacific), Lockton Companies

A new wave of digital asset regulations across Asia is increasing pressure on trading platforms and asset managers to strengthen governance — and to reassess their Directors’ and Officers’ (D&O) liability insurance arrangements.

In recent months, three leading digital asset hubs — Hong Kong, Singapore and South Korea — have announced plans to refine their respective regulatory frameworks. As regulatory expectations rise and senior management’s personal accountability becomes clearer, platform operators must stay informed of these developments and evaluate whether their existing risk transfer strategies remain fit for purpose.

Hong Kong: expanding accountability beyond governance

In August 2025, Hong Kong’s Securities and Futures Commission (SFC) issued a circular to licensed virtual asset trading platform operators clarifying senior management’s responsibilities regarding the custody of clients’ virtual assets. The circular reinforces expectations around governance, internal controls and effective oversight, signaling a continual shift toward personal accountability for directors and senior management.

An emerging consideration from the SFC’s consultation process is whether virtual asset management service providers should be permitted to rely on non‑SFC‑regulated or offshore custodians. From an insurance perspective, the availability of coverage for virtual asset risks is closely tied to the robustness of custody arrangements, including security controls, operational resilience and asset protection standards. To date, insurance capacity has largely been supported by the prescriptive requirements imposed on SFC‑regulated custodians and platforms.

If alternative custody models are permitted, ensuring that non‑regulated or offshore custodians are held to equivalent standards, including appropriate insurance coverage will be critical. Without alignment, firms that have invested heavily to meet Hong Kong’s regulatory and insurance expectations may face a competitive disadvantage, while the objective of enhancing investor protection and market integrity could be undermined.

Singapore: reinforcing senior management competency

In 2025, Singapore introduced licensing requirements for digital token service providers serving only overseas customers, bringing a broader range of firms within the Monetary Authority of Singapore’s regulatory perimeter.

Under the licensing guidelines, the competency and fitness of key individuals are core admission criteria. Senior management is expected to demonstrate a clear understanding of the regulatory framework and to exercise effective oversight and control over business activities and staff.

As regulatory expectations rise, so too does the personal exposure of directors and officers. In this context, D&O insurance remains a critical component of a firm’s overall risk management framework, helping to protect personal assets in the event of claims or regulatory actions arising from alleged governance or oversight failures.

South Korea: gearing up for Digital Asset Basic Act

South Korea is pursuing a more expansive regulatory overhaul through the proposed Digital Asset Basic Act, introduced to the National Assembly in June 2025. The bill seeks to formalize the digital asset market by regulating issuance, trading practices and distributions, while introducing new governance structures around asset listing and delisting decisions.

These imminent changes would significantly increase compliance obligations for trading platforms and related service providers. In this environment, D&O insurance plays an important role in protecting directors and officers from the financial consequences of legal actions, investigations or claims arising from alleged regulatory breaches.

Navigating regulatory complexity with D&O insurance

Across Hong Kong, Singapore and South Korea, regulators are refining already sophisticated frameworks to address the evolving risks of digital assets. These developments reflect a broader global trend toward intensified regulatory scrutiny and heightened expectations of senior management accountability.

For firms operating in the region, this means proactively reviewing governance structures, custody arrangements and insurance programs to ensure leadership is appropriately protected against emerging liabilities. D&O insurance is no longer a secondary consideration — it is a core element of responsible risk management in an increasingly regulated digital asset landscape.

Informed Perspectives

Crypto scams are not just targeting the uninformed

By Haidy Grigsby, special agent, cybercrime and digital evidence unit, Tennessee Bureau of Investigation

A common assumption is that crypto scams prey on the uninformed. While this is often true in financial fraud, crypto-related frauds are increasingly catching experienced investors, retired professionals and former market participants off guard with increasing frequency.

In my work at the FBI, I recently met with a retired trader who fit that profile exactly. He met a young woman online who claimed to know someone involved in crypto trading. He was told he had been selected as a consultant because of his experience. His case illustrates a strategy that we now see often.

Initial contact often begins with a wrong-number text, LinkedIn message or social media outreach. What starts as professional often turns personal or romantic, a tactic known as “pig butchering.” Scammers flatter expertise, create exclusivity and get the target to move the conversation to encrypted apps. In this case, “she” said WhatsApp was easier for her.

Exploiting familiarity with legitimate infrastructure, victims are instructed to open accounts on real exchanges, then use self-custody wallets to access external sites through built-in Web3 browsers. Because they click within a trusted app, they often don’t realize that they have left it.

These fraudulent markets mimic real ones with a twist: unlike real markets, these platforms allow one daily trade at a set time, ostensibly to capture optimal volatility. Victims choose long or short, allocate funds and confirm a brief trade lasting seconds or minutes. The scammer will often claim to contribute their own funds, reinforcing trust and the illusion of shared risk.

Balances grow and profits appear real. In truth, no trading occurs — the website is controlled by the operation, and the returns aresimply numbers entered by the scammer on their end.

To build credibility, victims are encouraged to withdraw a small amount after a “winning” trade. The withdrawal appears processed successfully, but is funded with cryptocurrency stolen from other victims and is meant to encourage larger future deposits. “I took profits. It had to be real,” the retired trader told me in frustration.

The websites change domains and branding frequently, with victims being told the company is merging, upgrading or rebranding. In reality these changes occur because of law enforcement takedowns, and victims are simply redirected to “new trading platforms.”

When victims attempt larger withdrawals, the narrative shifts: regulatory holds, tax prepayments, liquidity verification thresholds or tier upgrades. Each explanation is paired with urgent demands for more funds.

Convincing victims of the truth remains one of the greatest challenges. When I spoke with the retired trader, it was difficult to convince him I was law enforcement and that he had been dealing with a criminal organization, not one individual. No one wants to believe the person they built trust with and gave substantial sums of money to never existed. This retired trader was left to face his family, admit he had been defrauded and ask for help with basic living expenses. By the time he accepted reality, his retirement savings were already gone: assets had been transferred overseas, laundered and liquidated.

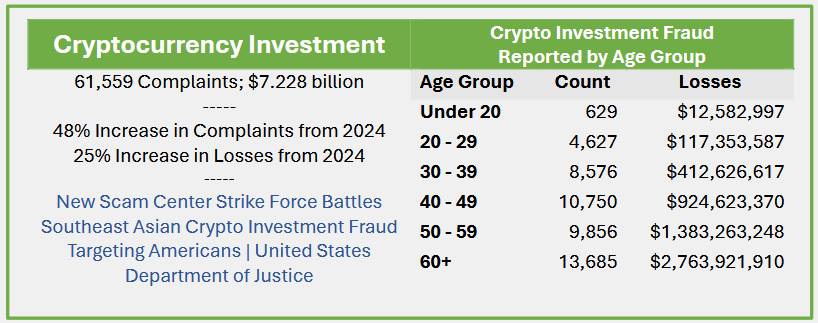

Source: FBI Internet Crime Complaint Center (IC3), 2025 Internet Crime Report, p. 53, https://www.ic3.gov/AnnualReport/Reports/2025_IC3Report.pdf

The FBI’s 2024 data show losses rising with age, likely reflecting the fact that older individuals have more accumulated wealth than those in their 20s.

Victims gather evidence: phone numbers, accounts, photos and websites — most of it turns out to be stolen, fake or AI-generated. Despite the difficulties in apprehending the perpetrators of these sophisticated schemes, law enforcement continues to pursue these cases. Anyone affected should cease all communication and report the incident to local law enforcement, IC3.gov and Chainabuse.com.

Headlines of the Week

– By Francisco Rodrigues

This week’s headlines show institutional adoption has kept on growing in the cryptocurrency space, yet old dangers remain. Protocol exploits, state-sponsored attacks, and technology disruption remain active threats.

Chart of the Week

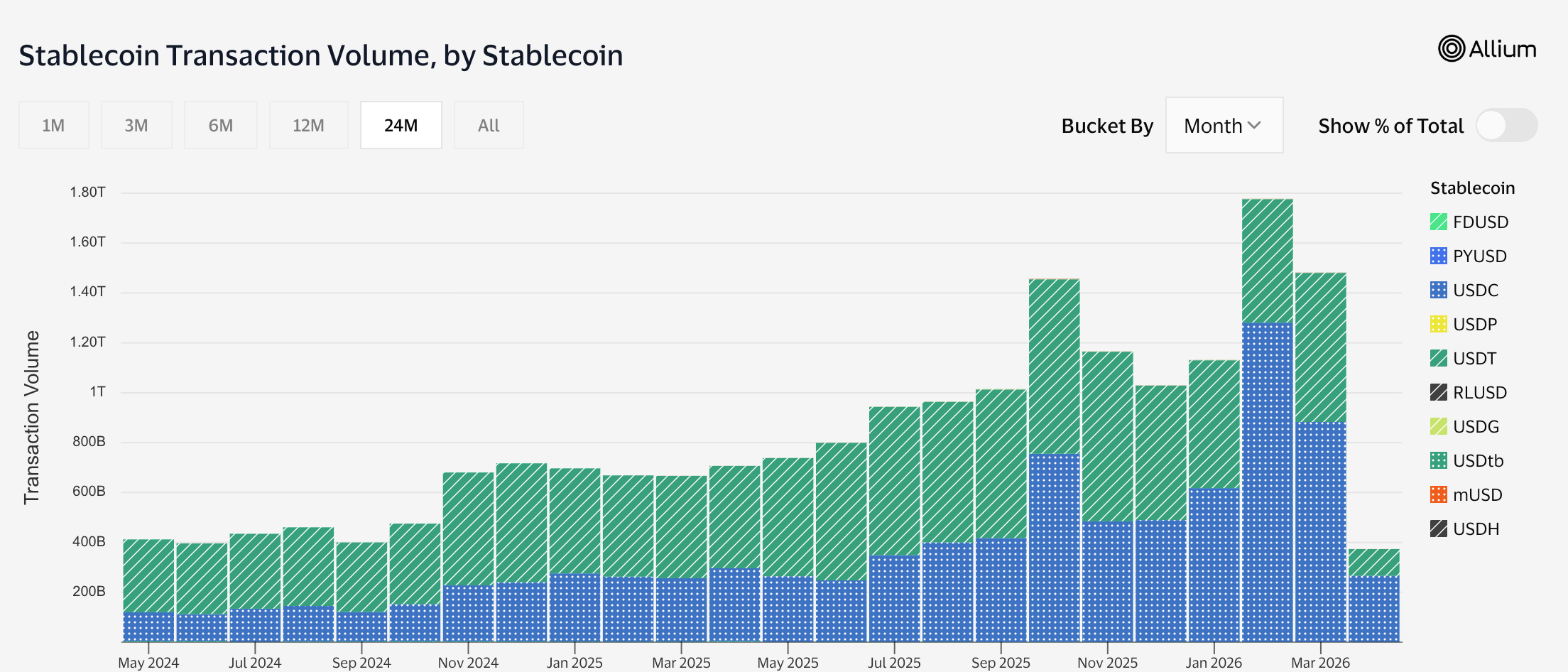

Hyperliquid’s TradFi bet is now 40% of its own volume

Hyperliquid’s HIP-3 has scaled from ~$115 million in its first week (Oct 2025) to a peak of $17.8 billion/week, now consistently representing 35–40% of total protocol volume. Despite launching as a crypto-adjacent product, HIP-3 is overwhelmingly a TradFi venue, with Commodities alone driving ~60% of volume and pure crypto categories accounting for just ~12%. The aggregate (core + HIP 3) volume continues to decline since the early March 2026 peak with the HYPE price now following the same trend.

Listen. Read. Watch. Engage.

- Listen: Jennifer Sanasie is joined by Bloomberg Intelligence Senior Analyst James Seyffart to break down what Morgan Stanley’s bitcoin ETF could mean for institutional flows, fee competition, and the next phase of crypto adoption.

- Read: In Crypto for Advisors, Paul Frost-Smith, CEO of Komainu, covers how institutional crypto is converging with traditional finance, but speed can introduce risk if legal and compliance layers aren’t aligned. Then, in “Ask an Expert,” Sam Boboev from the “Fintech Wrap Up,” details the key coordination risks institutions must solve for.

- Watch: Jennifer Sanasie hosts Public Keys from the NYSE. Christopher Perkins discusses the recent acquisition by Franklin Templeton and the new “Franklin Crypto,” Superstate CEO Robert Leshner and Invesco’s Kathleen Wrynn break down their partnership, and NYSE Senior Market Strategist Michael Reinking, CFA unpacks the macro environment.

- Engage: Have you bought tickets to Consensus Miami yet? More speakers have been added to the agenda! Surrounding Consensus is an institutional summit, an advisor-focused “Wealth Management Day,” 100+ ancillary events and much, much more.

Looking for more? Receive the latest crypto news from coindesk.com and market updates from coindesk.com/institutions.

Note: The views expressed in this column are those of the author and do not necessarily reflect those of CoinDesk, Inc., CoinDesk Indices or its owners and affiliates.

Federal Reserve Chair Jerome Powell speaks during a press conference following the Federal Open Markets Committee meeting at the Federal Reserve on March 18, 2026 in Washington, DC.

Anna Moneymaker | Getty Images

Federal Reserve officials at their March meeting still expected to lower interest rates this year, even with a high level of uncertainty from the Iran war and tariffs, according to minutes released Wednesday.

Most of the participants said the war could result in the need for easier monetary policy if rising gas prices hit the labor market and consumer wallets.

Policymakers said they would need to remain “nimble” as they weighed the impact the war had on inflation, which continued to hold above the Fed’s target, and hiring, which has been mostly flat over the past year.

“Many participants judged that, in time, it would likely become appropriate to lower the target range for the federal funds rate if inflation were to decline in line with their expectations,” the minutes said.

The consensus anticipated one cut this year, unchanged from the last update in December.

The summary then noted caution over “a further softening in labor market conditions, which could warrant additional rate cuts, as substantially higher oil prices could reduce households’ purchasing power, tighten financial conditions, and reduce growth abroad.”

Ultimately, the rate-setting Federal Open Market Committee voted 11-1 to keep the benchmark overnight borrowing rate targeted in a range between 3.5%-3.75%.

Possible hike?

The consensus was to keep rates steady as they observed conditions unfold, with officials also expressing concern that the Middle East hostilities could result in sustained inflation that could require rate hikes.

“Most participants commented that it was too early to know how developments in the Middle East would affect the U.S. economy and judged it prudent to continue to monitor the situation and assess the implications for the appropriate stance of monetary policy,” the minutes said.

The March 17-18 meeting came just a weeks after the U.S. and Israel launched an attack on Iran that triggered a surge in energy costs and renewed fears of a spike in inflation. A ceasefire announced Tuesday evening led to a sharp drop in oil, though the durability of the agreement is still highly in question.

In assessing conditions so far, meeting participants said they still expected inflation to continue moving toward the Fed’s 2% target, despite the tumult the war caused. They noted that tariffs remain a threat, though most see the impact of the duties as temporary when it comes to computing inflation.

Chair Jerome Powell said in a recent public appearance that raising rates now to stave off an inflation spike could have negative longer-term effects given the lagged impact of Fed rate moves.

At the same time, officials expressed concern about the labor market, which has been creating enough jobs to keep the unemployment rate steady. However, job growth has come almost exclusively from health care-related sectors, raising concerns about stability and potential for growth.

“The vast majority of participants judged that risks to the employment side of the mandate were skewed to the downside,” the minutes said. “In particular, many participants cautioned that, in the current situation of low rates of net job creation, labor market conditions appeared vulnerable to adverse shocks.”

Markets largely expect the Fed to remain on hold through the rest of the year. However, the ceasefire led traders to raise the odds for a potential cut.

Broadly speaking, the economy has showed signs of slowing, causing some on Wall Street to raise their expectations for a recession.

Gross domestic product rose at just a 0.7% pace in the fourth quarter of 2025 and is on track for just a 1.3% growth rate in the first quarter of 2026.

Network News

BERNSTEIN SAYS QUANTUM THREAT TO BITCOIN IS REAL BUT MANAGEABLE: Wall Street broker Bernstein said the rise of quantum computing poses a credible but manageable threat to Bitcoin and the broader crypto ecosystem, as recent breakthroughs compress timelines for potential attacks on modern cryptography. Advances such as Google Quantum AI’s reported reduction in qubit requirements suggest the risk is no longer a distant, decade-long concern, the broker noted. Still, the firm cautioned that scaling quantum systems to the level needed to break widely used encryption remains a complex, multi-step challenge. “Quantum should be seen as a medium to long term system upgrade cycle rather than a risk,” analysts led by Gautam Chhugani said in the Wednesday report. Quantum computing uses the principles of quantum mechanics rather than classical physics. Instead of binary bits, it relies on qubits that can exist in multiple states at once, a property known as superposition, allowing many possibilities to be processed simultaneously. Combined with entanglement, this enables quantum systems to solve certain problems, such as breaking encryption, far more efficiently than classical computers. Quantum computers could eventually weaken cryptographic systems like elliptic curve encryption, which underpin crypto wallets, by solving problems beyond the reach of classical machines. However, the report said the threat spans industries from finance to defense and should be viewed as a manageable, long-term risk rather than an existential one for Bitcoin. — Will Canny Read more.

EXPLOITS TO ESPIONAGE: DRIFT HACK REVEALS MORE COMPLEX OPERATIONS: When Drift disclosed the details behind its $270 million exploit, the most unsettling part wasn’t the scale of the loss — it was how it happened. According to the team behind the protocol, the attack wasn’t a smart contract bug or a clever piece of code manipulation. It was a six-month campaign involving fake identities, in-person meetings across multiple countries and carefully cultivated trust. The attackers, allegedly from North Korea, didn’t just find a vulnerability in the system. They became part of it. This new threat is now forcing a broader reckoning across decentralized finance. For years, the industry has treated security as a technical problem, something that could be solved with audits, formal verification and better code. But the Drift incident suggests something far more complex: that the real vulnerabilities may lie outside the codebase altogether. Alexander Urbelis, chief information security officer (CISO) at ENS Labs, argues the framing itself is already outdated. “We need to stop calling these ‘hacks’ and start calling them what they are: intelligence operations,” Urbelis told CoinDesk. “The people who showed up at conferences, who met Drift contributors in person across multiple countries, who deposited a million dollars of their own money to build credibility: that’s tradecraft. It’s the kind of thing you’d expect from a case officer, not a hacker.” If that characterization holds, then Drift represents a new playbook: one where attackers behave less like opportunistic hackers and more like patient operators embedding themselves socially before making a move onchain. — Margaux Nijkerk Read more.

SOLANA FOUNDATION NEW AD ‘DONT WASTE TIME ON CRYPTO’: The Solana Foundation is taking a deliberately contrarian approach to crypto marketing in San Francisco, rolling out a billboard campaign that reads: “Don’t waste time with crypto.” At first glance, the message may seem a bit confusing as a crypto foundation is saying not to waste time with crypto. But according to the Solana Foundation, it is a bullish bet on the future of crypto that intersects with agentic AI. Essentially, what this means is that rather than wasting your time executing transactions with crypto, which might be cumbersome and time-consuming, let your AI agents do the hard work. The ad directs passersby to the x402 account on X, a nod to a growing push within the Solana ecosystem to position blockchain not as a consumer-facing product, but as invisible infrastructure for the next phase of the internet. — Margaux Nijkerk Read more.

NEW ALCHEMY AI TOOL: Alchemy, a cryptocurrency infrastructure provider used by many blockchains and firms in the space, has released a new tool, AgentPay , that lets different AI payment systems, from companies like Coinbase, Stripe, Visa, Mastercard, and Circle, work together. The new tool addresses the problem that agentic payment systems currently coming online aren’t “interoperable,” or in other words, don’t talk to one another, meaning a merchant that wants AI agents as customers has to build a separate integration for every protocol. “That’s not sustainable, and it’s only going to get more fragmented as more systems launch,” said Alchemy CTO Guillaume Poncin in an email. “AgentPay fixes that. A merchant registers their existing API with us, we give them a new endpoint, and any agent on any supported protocol can pay them through it.” Alchemy is widely seen as the “AWS of Web3,” as it provides the infrastructure, developer tools, and node services needed to build blockchain applications. AgentPay promises one integration for every protocol, citing the likes of x402, MPP, A2P or L402. “We sit in the middle as the translation layer, where AgentPay routes instructions, and Alchemy never touches the funds,” Poncin said. — Ian Allison Read more.

In Other News

- Adam Back has denied claims that he is Satoshi Nakamoto after a New York Times story argued that the British cryptographer is the strongest candidate yet for Bitcoin’s pseudonymous creator. In a post on X after the article was published, Back said his long record in cryptography, privacy tools and electronic cash research explains why reporters keep finding links between his work and Bitcoin’s design. “I’m not satoshi,” Back wrote. He said he had been “early in laser focus on the positive societal implications of cryptography, online privacy and electronic cash,” and that his work from about 1992 onward, including discussions on the cypherpunks mailing list, led to Hashcash and other ideas later echoed in Bitcoin. Back, said NYT reporter John Carreyrou, had found “many interesting bitcoin analogs in early attempts to create a decentralized ecash,” adding that early researchers explored concepts such as peer-to-peer systems, proof-of-work, and routing models that looked like prototypes for Bitcoin. — Helene Braun Read more.

- Wall Street investment bank JPMorgan (JPM) said the pace of capital flowing into digital assets slowed markedly in the first quarter of 2026, with total inflows estimated at around $11 billion. That implies an annualized run rate of roughly $44 billion, about one-third of the pace seen in 2025, according to the report published last week. “Investor flows, either retail or institutional, have been small or even negative YTD with the bulk of the digital asset flow in Q1’26 stemming from Strategy’s (MSTR) bitcoin purchases and concentrated crypto VC funding,” wrote analysts led by Nikolaos Panigirtzoglou. Crypto markets had a volatile and broadly negative first quarter, with prices and market value retreating sharply amid a risk-off backdrop. Total crypto market capitalization fell roughly 20% over the period, while bitcoin dropped around 23% and ether (ETH) declined more than 30%, marking one of the weakest first-quarter performances in years. The selloff was driven by macroeconomic and geopolitical pressures, triggering liquidations and a broad pullback in risk assets, with altcoins hit even harder. — Will Canny Read more.

Regulatory and Policy

- Polymarket removed a betting market tied to the rescue of U.S. service members in Iran, after intense backlash and criticism from lawmakers this weekend. The market allowed users to wager on when the U.S. would confirm the rescue of two airmen after an F-15E fighter jet was shot down over Iran. The crew members have since been rescued. Rep. Seth Moulton, a Democrat from Massachusetts, criticized the listing in a post on X, calling it “disgusting” and arguing it reduced a military rescue effort to a financial trade. Moulton has taken a hard line on prediction markets, recently banning his staff from using platforms such as Polymarket and Kalshi over concerns that financial incentives could influence policy decisions. A Polymarket spokesperson said the listing did not meet its integrity standards and the contract was removed shortly after it appeared. The company added that it is reviewing how the market passed internal safeguards. — Francesco Rodrigues Read more.

- The U.S. Federal Deposit Insurance Corp. formally proposed its approach to stablecoin issuers as one of the federal financial regulators required to write and oversee rules under last year’s Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act. The FDIC’s proposal —meant to align closely with what its sister banking agency, the Office of the Comptroller of the Currency, proposed in February — will be open for a 60-day public comment period on the lengthy list of 144 questions posed Tuesday by the agency. The FDIC’s job is to police U.S. depository institutions, and under the GENIUS Act, its role is to regulate such institutions issuing stablecoins from their subsidiaries. To that end, it posed capital, liquidity and custody standards for those firms, though the details won’t be set in stone until the rule is finalized — not likely to occur until the agency spends further months reviewing input and writing the final language. This is the second GENIUS Act proposal from the banking agency after its December pitch on the issuer application process. As expected under the law, stablecoins won’t enjoy the deposit insurance that the banks maintain on traditional banking accounts, according to the proposal. — Jesse Hamilton Read more.

Calendar

- Apr.15-16, 2026: Paris Blockchain Week, Paris

- May 5-7, 2026: Consensus, Miami

- Sept. 29-Oct.1, 2026: Korea Blockchain Week, Seoul

- Oct. 7-8, 2026: Token2049, Singapore

- Nov. 3-6, 2026: Devcon, Mumbai

- Nov. 15-17, 2026: Solana Breakpoint, London

Crypto World

BTC’s next bull run to be driven by banking and digital credit, says Strategy’s Michael Saylor

Michael Saylor, executive chairman of Strategy (MSTR), believes bitcoin likely bottomed in early February at $60,000.

Speaking at a recent Mizuho event, Saylor reiterated his long-held view that bottoms aren’t necessarily about valuations but are driven by seller exhaustion, analysts Dan Dolev and Alexander Jenkins wrote.

Trend reversals, he added, are driven more by capital structure and liquidity than by investor sentiment.

Saylor now sees limited selling pressure amid growing demand from ETF inflows, which are absorbing daily supply, and companies shifting treasury assets into bitcoin.

Bitcoin and Strategy’s next drivers

As for the catalyst for the next bull market, Saylor believes it will be the formation of banking credit and digital credit on top of bitcoin. This will have bitcoin supporting more lending and credit activity beyond simple buy-and-hold demand.

Digital credit already exists, said Saylor, in the form of Strategy’s STRC preferred stock, whose beefy 11.5% yield remains well below the company’s expectation of BTC’s long-term appreciation. Strategy is “stretching” bitcoin “from a nonyielding asset into a capital markets engine,” he said.

On the recently hotly-debated topic of quantum computing, Saylor said the risks are overblown. The threat, he argued, is theoretical, likely decades away, and even then solvable.

Mizuho retained its outperform rating on Stategy and $320 price target, suggesting about 150% upside from the current $127.

Circle Payments Network (CPN) Managed Payments let financial institutions operate in fiat, while using crypto rails behind the scenes via Circle.

Circle today launched Circle Payments Network (CPN) Managed Payments, a stablecoin settlement solution designed to simplify stablecoin transactions for traditional financial institutions, according to a press release from the firm.

The new managed solution is aimed at mainstream TradFi firms, including payment service providers, fintechs, banks, and global enterprises, per the release. The product’s core pitch is simplicity: participating firms interact solely in fiat, while Circle handles the the crypto rails in the background, namely USDC minting and burning, payment orchestration, compliance, and blockchain infrastructure.

Use cases include cross-border settlement, merchant stablecoin acceptance, high-volume payouts, and FX cost reduction, according to the releae. At launch, partners include Thunes and Worldline, alongside payments company Veem.

In recent months, UDSC has overtaken Tether’s USDT, the largest stablecoin by market cap, in terms of monthly transaction volume, per data from Visa and Allium.

The launch comes as stablecoins cement their role as mainstream financial infrastructure. Total stablecoin supply surged 50% in 2025 as enterprise adoption accelerated, with the GENIUS Act creating the first federal U.S. regulatory framework for the sector.

Major institutions have moved quickly: Visa launched USDC settlement on Solana in December, and the same month, Intuit struck a multi-year deal with Circle to embed stablecoin capabilities across TurboTax, QuickBooks, and Credit Karma.

Meanwhile, last month, Mastercard acquired stablecoin infrastructure firm BVNK with aims to bridge on-chain and fiat rails within the network.

This article was written with the assistance of AI workflows. All our stories are curated, edited and fact-checked by a human.

Institutional money is rotating back in, and XRP is leading the rallies. XRP recorded $119.6 million in weekly fund inflows for the period ending last week, its strongest weekly haul since mid-December 2025, which occurred when XRP price prediction was running at rock bottom.

That single figure puts XRP ahead of every other digital asset for the week, including Bitcoin. The broader crypto market pulled in $224 million total, reversing a stretch of notable outflows and signaling a clear sentiment shift among institutional allocators.

Regulatory clarity and XRP’s entrenched position in cross-border payment infrastructure appear to be the twin catalysts. With macro conditions still turbulent, the price setup deserves a closer look.

Discover: The best crypto to diversify your portfolio with

XRP Price Prediction: $2.00 Before Year-End?

XRP’s 4.6–5.0% daily gain lands it at the $1.37–$1.38 range, but the technical picture remains cautious. The asset is holding above its short-term 10-day and 20-day exponential moving averages, a tentative green flag.

The problem? It still trades below the 50-, 100-, and 200-day EMAs, keeping the broader trend firmly in bearish territory. The 14-day RSI sits at 39.43, neutral but leaning toward oversold, which historically creates room for further upside before momentum stalls.

Support levels are stacked at $1.31, $1.29, and $1.27, with resistance clustered at $1.4, the exact range XRP is currently testing. A clean breakout above $1.38 with volume would open the door toward $1.50 and potentially $1.70 on a momentum extension.

The inflow data is bullish. The chart structure is still mending. Those two realities coexist, and neither cancels the other out.

Discover: The best pre-launch token sales

Bitcoin Hyper Targets Early Mover Upside as XRP Tests Key Resistance

XRP’s 50% projected upside is compelling, but at a $84B+ market cap, the runway to 10x returns requires a very specific set of conditions to align perfectly. Traders hunting asymmetric early-stage exposure are looking elsewhere without abandoning the Bitcoin ecosystem entirely.

Bitcoin Hyper ($HYPER) is positioned as the first Bitcoin Layer 2 with Solana Virtual Machine (SVM) integration, a combination that delivers sub-second transaction finality while inheriting Bitcoin’s security layer. The project targets Bitcoin’s three structural weaknesses directly: slow transactions, high fees, and the near-total absence of programmability.

The presale has raised $32 million at a current token price of $0.0136, with staking rewards already live for early participants. The Decentralized Canonical Bridge enables direct BTC transfers into the ecosystem, removing friction that has historically limited Bitcoin DeFi adoption.

The post XRP Price Prediction: Ripple Leads Crypto Inflows as Market Recovers appeared first on Cryptonews.

South Korea’s ruling Democratic Party proposed a “Digital Asset Basic Act” Wednesday that would establish a legal framework for digital assets, including issuance, trading, custody and supervision.

“Digital assets are emerging as a core medium connecting the real economy and financial markets,” the proposal states. It defines value-linked digital assets, including those tied to fiat currencies or real-world assets, as a category requiring issuer authorization, refund reserves and redemption obligations.

The new proposal comes amid stalled Digital Asset Basic Act negotiations since early this year when regulators clashed over who should be allowed to issue won-pegged stablecoins. The Bank of Korea insisted banks with 51% ownership should be the only ones authorized to issue stablecoins, while the Financial Services Commission warned this could hinder innovation.

The bill also said it aims to “establish a foundation for Korea to lead the global digital financial order.” Under the proposal, entities seeking to issue such assets must obtain approval and meet requirements including capital thresholds, operational capacity and reserve plans.

The legislation would introduce licensing, registration and reporting requirements for digital asset businesses, including trading, brokerage, custody and advisory services.

It would also establish rules on disclosures, internal controls and market conduct, including prohibitions on unfair trading practices such as market manipulation and use of non-public information.

The proposal calls for the creation of a digital asset committee to review and coordinate policy, as well as national basic and implementation plans for the sector.

It also noted that South Korea’s current system remains focused on investor protection and lacks a comprehensive framework covering issuance, disclosure and market structure.

The proposal follows the announcement of new rules Wednesday by the country’s Financial Services Commission and Financial Supervisory Service ordering all domestic cryptocurrency exchanges to adopt a single, strict system for delaying withdrawals. The aim is to block a surge in voice phishing scams that rely on speed.

Yuga Labs has settled its lawsuit against artist Ryder Ripps and Jeremy Cahen over their alleged copycatting of its non-fungible tokens (NFTs) from the Bored Ape Yacht Club collection.

The agreement ends a two-year dispute over whether the pair’s project, which reused Bored Ape imagery, crossed the line from satire into trademark infringement.

Proposed court orders would permanently bar Ripps and Cahen from using Yuga’s trademarks and imagery, according to a filing in California federal court. The terms of the settlement were not disclosed.

Yuga’s Bored Ape collection became one of the most recognizable NFT brands during the market’s peak. The firm sued in 2022, claiming Ripps and Cahen sold lookalike tokens in their RR/BAYC NFT collection and earned millions by confusing buyers. The defendants argued their work was a satirical response to the actual Bored Ape Yacht Club collection.

A district judge initially sided with Yuga and awarded nearly $9 million in damages and fees. But an appeals court later overturned that ruling, saying a jury should decide whether buyers were actually misled. The settlement avoids that trial.

Summary

- Ethereum Foundation will convert 5,000 ETH into stablecoins via CoWSwap’s TWAP feature to fund research, grants, and donations.

- The move follows earlier EF treasury conversions using DeFi rails as part of a broader diversification policy.

- Market watchers scrutinize EF sales as potential sentiment signals, even when the amounts are small relative to ETH’s total supply.

The Ethereum Foundation (EF) has announced it will convert 5,000 ETH into stablecoins using decentralized trading protocol CoWSwap’s time-weighted average price (TWAP) function, describing the move as routine funding for “R&D, grants and donations.” “Today, The Ethereum Foundation will convert 5000 ETH to stablecoins via @CoWSwap’s TWAP feature as a part of our ongoing work to fund R&D, grants and donations,” the foundation wrote on X, reiterating its commitment to using DeFi-native tools for treasury operations. At current prices, the sale is worth tens of millions of dollars but remains negligible versus Ethereum’s circulating supply and daily trading volume.

EF’s latest conversion echoes a similar move in October 2025, when it sold 1,000 ETH via CoWSwap TWAP “to fund R&D, grants and donations, and to highlight the power of DeFi,” a transaction then valued at roughly $4.5 million. The foundation has also previously outlined a plan to convert up to 10,000 ETH on centralized exchanges, positioning these sales as part of a diversification strategy that seeks “a middle ground between earning yields above standard benchmarks and serving as a responsible steward of Ethereum.” BeInCrypto noted that the new 5,000 ETH TWAP sale is “in line with its June 2025 treasury policy focused on DeFi and privacy,” framing it as policy execution rather than a directional bet on ETH.

While modest in size, EF treasury moves are closely watched as soft sentiment gauges around whether the organization views current levels as top-of-cycle or simply takes profit to extend runway. In a previous crypto.news story, Ripple’s Brad Garlinghouse argued that stablecoins and DeFi rails are becoming a primary “business entry point” for crypto, underscoring why Ethereum-native funding operations resonate far beyond the foundation’s own balance sheet. Another crypto.news story highlighted how 90% of financial institutions already use stablecoins in some form, and a third story on cross-border payments detailed how incumbents such as SWIFT are testing tokenized settlement, putting Ethereum-based infrastructure at the center of the next phase of global payments.

Anthropic has moved Claude Mythos Preview into a limited testing phase with a select group of enterprise partners after the model surfaced thousands of critical vulnerabilities across operating systems, web browsers and other software. The disclosure highlights both the immense potential of AI-powered security tools and the new, accompanying risks as capabilities proliferate in the wild.

The company described Mythos Preview as a general-purpose model that, during its internal evaluation, identified high-severity weaknesses across major platforms. Anthropic cautioned that such capabilities could spread rapidly if not managed responsibly, noting that adversaries may deploy these tools before safeguards are in place.

“Given the rate of AI progress, it will not be long before such capabilities proliferate, potentially beyond actors who are committed to deploying them safely.”

Security researchers have long warned that AI can accelerate cyberattacks by automating discovery and exploitation. In a broader landscape where AI-driven threats are increasingly common, Anthropic pointed to alarming trends. AllAboutAI reports a 72% year-over-year increase in AI-powered cyberattacks, and that 87% of global organizations experienced AI-enabled attacks in 2025. Against that backdrop, Anthropic emphasized the need for defensive AI tools to outrun the bad actors.

To shore up defenses, Anthropic announced Project Glasswing on the same day. The initiative unites more than 40 companies, including Amazon Web Services, Apple, Cisco, Google, JPMorgan, the Linux Foundation, Microsoft and Nvidia, with the goal of using Claude Mythos Preview’s capabilities to find bugs, share data with partners and patch critical vulnerabilities before criminals exploit them.

Key takeaways

- Claude Mythos Preview has identified thousands of critical vulnerabilities across operating systems, browsers and cryptography libraries, underscoring a broad surface area for potential exploitation.

- The majority of these flaws remain unpatched, with Anthropic noting that about 99% of the vulnerabilities it found have not yet been fixed.

- Project Glasswing mobilizes a cross‑industry coalition to operationalize AI-driven defense, aiming to accelerate bug discovery, disclosure and remediation across the software stack.

- The vulnerabilities span decades, hinting at long-standing fragility in widely used software and the persistent risk to critical infrastructure and crypto ecosystems.

AI-driven vulnerability discovery and decades‑old weaknesses

Anthropic’s early findings reveal a troubling reality: flaws that have lingered for years or even decades can still pose meaningful threats today. Among the examples cited were now-patched but historically significant bugs in OpenBSD—a 27-year-old vulnerability that resurfaced in testing—alongside a 16-year-old flaw in the FFmpeg library, and a 17-year-old remote code execution vulnerability in the FreeBSD operating system. The disclosures extended to multiple vulnerabilities within the Linux kernel, illustrating that even well-maintained open-source projects are not immune to latent risks.

Beyond operating systems, Mythos Preview flagged weaknesses in the cryptography landscape—areas that are foundational to secure communications and transactions. The model reportedly identified flaws in widely used libraries and protocols, including TLS, AES-GCM and SSH. Web applications emerged as a particularly fertile ground for vulnerability discovery, with a spectrum of issues ranging from cross-site scripting to SQL injection and cross-site request forgery, the latter often leveraged in phishing-style campaigns.

Anthropic stressed that many of these issues are subtle, context-specific or deeply embedded in complex code paths, making them hard to surface through traditional auditing alone. The implication for developers and operators is clear: even mature software stacks can hide critical flaws that AI could help uncover much faster than conventional methods.

The company also highlighted a stark statistic accompanying the findings: the majority of these vulnerabilities had not yet been patched, creating a window of exposure that could be exploited by opportunistic attackers if not addressed promptly.

Glasswing: a coalition for proactive defense

Project Glasswing is pitched as a proactive defense program rather than a retrospective analysis initiative. By pooling resources and expertise from participants across cloud providers, hardware developers, financial institutions and open-source ecosystems, Glasswing seeks to turn AI-driven vulnerability discovery into a learning loop that accelerates patch creation and deployment. The collaboration aims to share insights about emerging threats, coordinate disclosure with vendors and suppliers, and push for rapid remediation before exploitation becomes widespread.

Key participants span industry giants and pivotal security ecosystems: Amazon Web Services, Apple, Cisco, Google, JPMorgan, the Linux Foundation, Microsoft and Nvidia, among others. The initiative reflects a growing trend in which large technologist coalitions coordinate to harden software supply chains and reduce the window between vulnerability discovery and patching—an objective that is especially relevant to blockchain and crypto infrastructure, where security incidents can trigger cascading failures across networks and ecosystems.

What this shift means for crypto and cybersecurity ecosystems

For investors and builders in the crypto space, the Mythos Preview findings and Glasswing’s collaborative model lend a more nuanced view of risk and resilience. On the one hand, AI-assisted vulnerability discovery could markedly improve the security posture of crypto platforms, wallets, node software and smart-contract ecosystems by uncovering weaknesses that would have taken humans far longer to detect. On the other hand, early access to such powerful tools poses governance and safety questions: who controls the disclosure of findings, how quickly patches are issued, and how risk is priced for users in real-time markets?

From a market perspective, the activity around AI-enabled security tools could influence demand for security primitives, auditing suites and formal verification services within crypto infrastructure. It also underscores the importance of strong supply-chain security, given that a single zero-day in a widely used library or OS could ripple across decentralized networks, exchanges and custodial services.

Analysts note that the transition period for defense‑driven AI is likely to be fraught. In the long run, advocates expect defense capabilities to dominate, yielding a more secure software ecosystem, but the interim phase will be characterized by widespread misconfigurations, patch delays and evolving threat tactics as attackers adapt to new defensive technologies. Anthropic’s framing suggests that the shift toward AI-assisted defense will not be instantaneous; it will require sustained collaboration, standardized disclosures and rapid patch cycles to reduce the window of exploitation.

Beyond the immediate technical implications, industry observers are watching how policy and governance frameworks adapt to these capabilities. The balance between sharing threat intelligence and protecting sensitive vulnerability data will shape how quickly organizations can benefit from AI-driven defense, including in crypto-focused environments where liability, transparency and user trust are paramount.

As coverage in security circles notes, similar narratives have emerged around AI-enabled code security and the broader debate over how to regulate and deploy AI safely. The media and market response to these discussions has included volatility in cybersecurity equities, underscoring that investors are weighing the reliability of AI-driven defense against the risk of enabling more capable attackers.

In the near term, readers should watch how Glasswing translates the model’s findings into tangible patches and how quickly participating firms can operationalize the shared intelligence. The outcome will likely influence security budgets, developer workflows and incident-response readiness across both traditional tech and crypto-native ecosystems.

What remains uncertain is how quickly the industry can close the patch gap for the vast array of uncovered vulnerabilities and whether AI-assisted defenses can stay ahead of increasingly sophisticated exploitation techniques. The coming months will be telling for developers, operators and policymakers about the feasibility and effectiveness of large-scale, AI-enabled defense programs in reducing systemic risk.

For now, Anthropic’s disclosures reinforce a critical takeaway: as AI capabilities grow, so does the imperative to pair powerful discovery tools with disciplined, collaborative defense—especially in sectors where security is inseparable from trust and continuity.

Crypto Long & Short: Asia’s digital asset crackdown: accountability gets personal

Dow Jones And U.S. Stock Market Outlook – Bulls Are Back In Vengeance After The U.S.-Iran Ceasefire

PSL team owner contradicts Mohsin Naqvi on empty stands, says Pakistan was ‘busy driving global peace’ | Cricket News

-

NewsBeat6 days ago

NewsBeat6 days agoSteven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Business6 days ago

Business6 days agoNo Jackpot Winner and $194 Million Prize Rolls Over

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Spanx – Corporette.com

-

Crypto World7 days ago

Crypto World7 days agoGold Price Prediction: Worst Month in 17 Years fo Save Haven Rock

-

Business4 days ago

Business4 days agoExpert Picks for Every Need

-

Business3 days ago

Business3 days agoThree Gulf funds agree to back Paramount’s $81 billion takeover of Warner, WSJ reports

-

Sports4 days ago

Sports4 days agoIndia men’s 4x400m and mixed 4x100m relay teams register big progress | Other Sports News

-

Business7 days ago

Business7 days agoLogin and Checkout Issues Spark Merchant Frustration

-

Tech21 hours ago

Tech21 hours agoHow Long Can You Drive With Expired Registration? What Florida Law Says

-

Business3 days ago

No Jackpot Winner, Prize to Climb to $231 Million

-

Tech6 days ago

Tech6 days agoCommonwealth Fusion Systems leans on magnets for near-term revenue

-

Fashion2 days ago

Fashion2 days agoMassimo Dutti Offers Inspiration for Your Summer Mood Board

-

Crypto World7 days ago

Crypto World7 days agoRipple rolls out enterprise crypto treasury platform for corporates

-

Fashion1 day ago

Fashion1 day agoLet’s Discuss: DEI in 2026

-

Politics5 days ago

Wings Over Scotland | The quality of mercy

-

Sports7 days ago

Sports7 days agoSteal Gary Woodland’s subtle power move for longer drives

-

Sports7 days ago

Tom Pelissero Drives the Final Nail in the Coffin

-

Tech7 days ago

Tech7 days agoBattery Tester Outperforms Cheaper Options

-

Business4 days ago

Business4 days agoAkebia Therapeutics, Inc. (AKBA) Discusses Pipeline Progress and Strategic Focus on Kidney Disease Treatments at R&D Day – Slideshow

-

Tech7 days ago

Tech7 days agoFollowing Artemis II’s Journey Around The Moon

You must be logged in to post a comment Login