Business

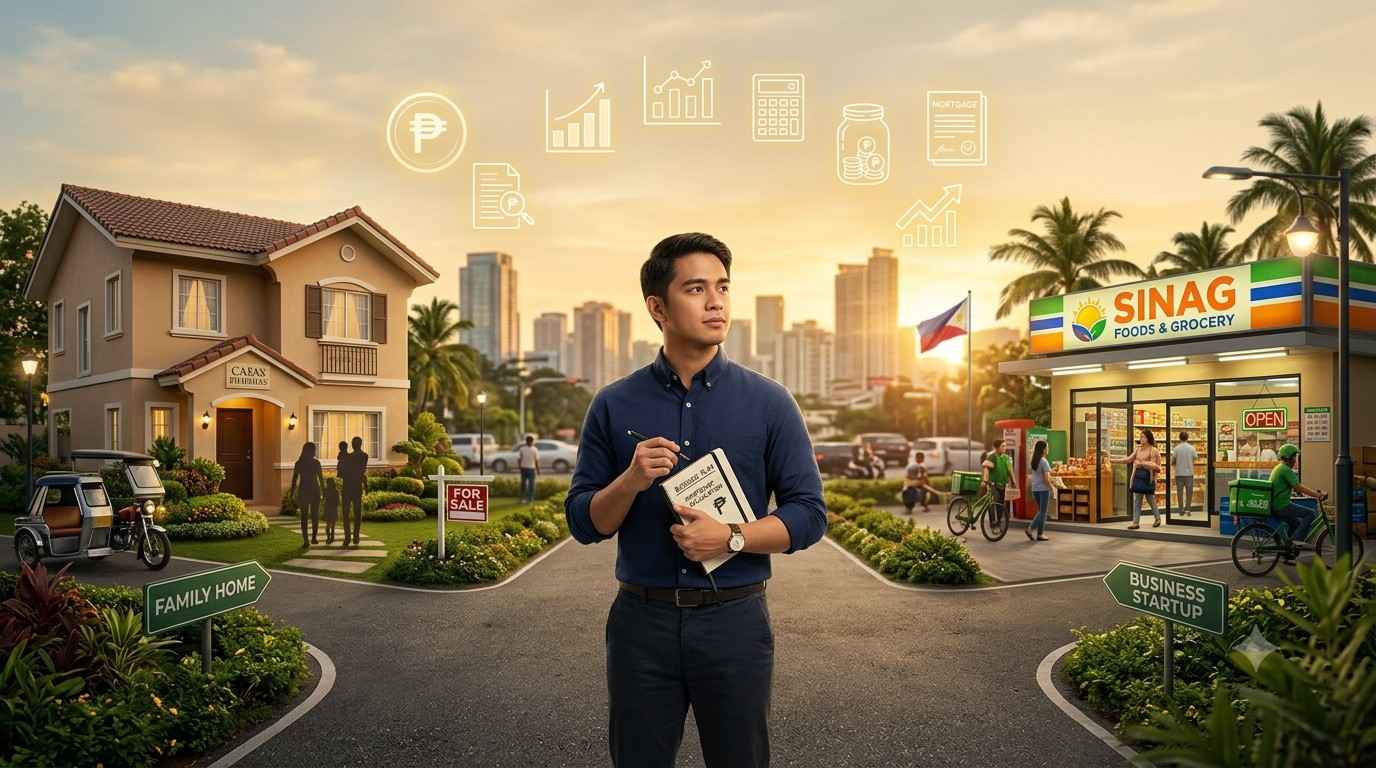

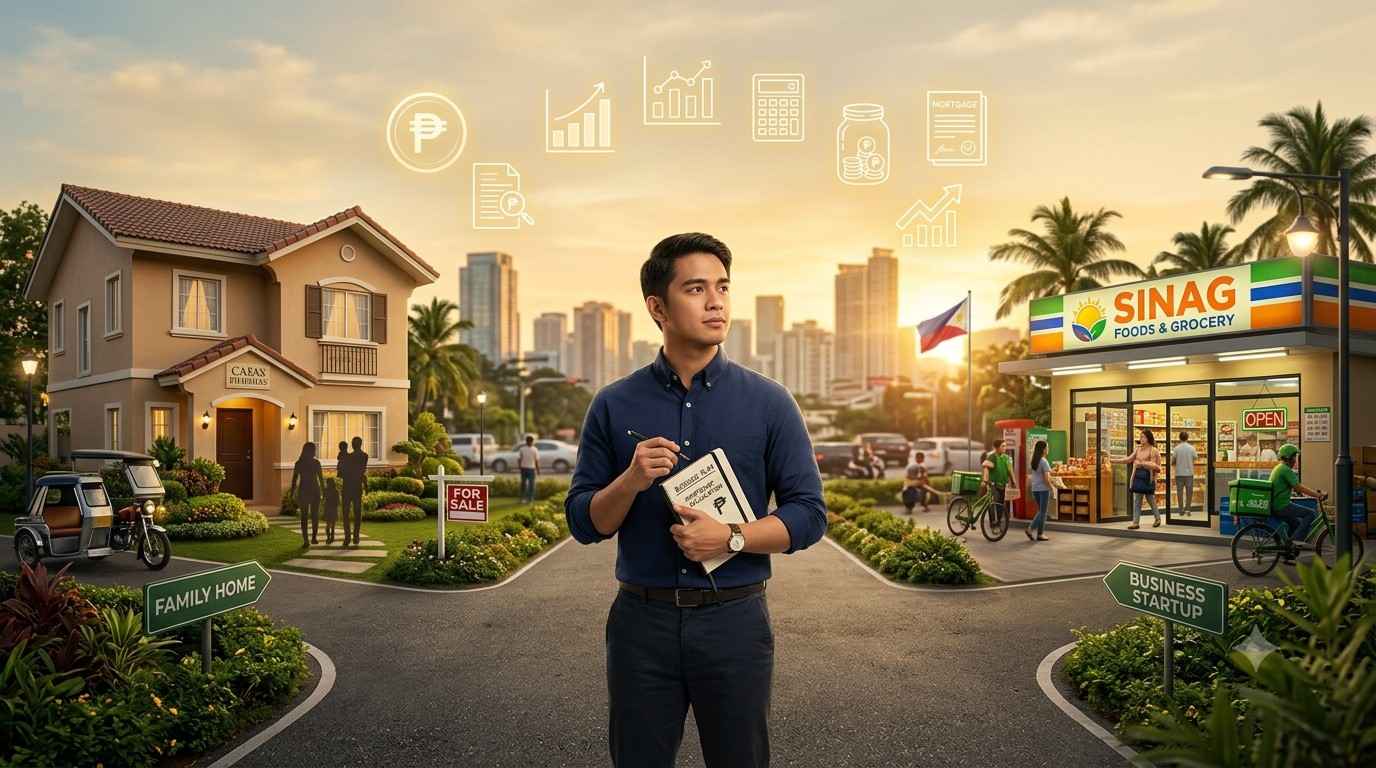

House Or Business First? A Smart Financial Guide To Building Wealth

One of the biggest financial decisions many people face is this: Should you buy a house first or start a business? There is no universal answer because every person’s financial situation, career goals, family responsibilities, and risk tolerance are different.

Some people believe that owning a home provides security and stability before taking entrepreneurial risks. Others argue that building a successful business first creates income that can later make buying a dream home much easier.

If you’re asking yourself, “Should I prioritize a house or a business?”, this guide will help you evaluate both options, understand their advantages and disadvantages, and make a smarter financial decision.

Why This Decision Matters

Both buying a house and starting a business require a significant financial commitment. In many cases, you may not have enough capital to do both at the same time.

Your choice today can influence your financial future for years, even decades. That’s why understanding the long-term impact is more important than simply following what friends or relatives recommend.

When Buying a House First Makes Sense

Purchasing a home is often viewed as a major life milestone. It provides stability and can become a valuable long-term asset.

Advantages of Buying a House First

- Stable Living Situation

You no longer worry about rising rental costs or frequent moves. - Build Home Equity

Instead of paying rent every month, your payments help build ownership in your property. - Potential Property Appreciation

Real estate often increases in value over time, especially in growing cities and developing communities. - Greater Family Security

A permanent home offers emotional stability, especially for families with children. - Easier Financial Planning

Fixed mortgage payments can be easier to budget than fluctuating rental expenses.

Disadvantages

- Large down payment requirements

- Monthly mortgage obligations

- Property taxes and maintenance costs

- Less available capital for investments

- Reduced financial flexibility

If most of your savings go toward buying a home, you may have little remaining capital to invest in business opportunities.

When Starting a Business First Makes Sense

A successful business can generate income that far exceeds what traditional employment offers. Many entrepreneurs choose to invest in their businesses first before purchasing real estate.

Advantages of Starting a Business First

- Higher Income Potential

A profitable business may generate significantly more income than your regular salary. - Creates Multiple Income Streams

Business profits can later fund investments, retirement savings, and property purchases. - Greater Financial Growth

Businesses have the potential to scale, increasing profits over time. - Tax Advantages

Depending on your country’s tax regulations, business owners may qualify for deductible business expenses. - Future Home Purchase Becomes Easier

A thriving business may allow you to purchase a home with less financial stress.

Disadvantages

- Higher financial risk

- Income may not be stable during the early years

- Long working hours

- Possible business losses

- No guarantee of success

Unlike real estate, businesses can fail if they are poorly managed or if market conditions change dramatically.

Consider Your Personal Financial Situation

Before deciding, honestly evaluate your finances.

Ask Yourself These Questions

- Do I have emergency savings?

- How stable is my current income?

- Do I have existing debts?

- Can I handle financial risks?

- Do I have dependents?

- How much capital do I have?

- Do I have entrepreneurial experience?

Your answers can reveal which option better aligns with your current financial position.

Business First: Who Is It Best For?

Starting a business before buying a house may be a good choice if you:

- Are young and have fewer financial obligations

- Already have a validated business idea

- Possess industry knowledge or experience

- Can tolerate financial uncertainty

- Want to build wealth faster

- Already have affordable housing arrangements

Many successful entrepreneurs rented modest homes while investing heavily in growing their businesses.

House First: Who Is It Best For?

Buying a house first may be more appropriate if you:

- Have a growing family

- Need housing stability

- Prefer lower financial risk

- Have a steady long-term career

- Already have sufficient savings

- Do not yet have a proven business concept

Can You Do Both?

Yes—but it requires careful planning.

Instead of making an all-or-nothing decision, many financially successful individuals gradually build both assets.

For example:

- Build an emergency fund.

- Start a small side business.

- Grow business profits.

- Save for a house down payment.

- Purchase a home when business income becomes stable.

This balanced approach reduces financial stress while allowing both goals to progress.

Common Mistakes to Avoid

1. Buying an Expensive House Too Early

A large mortgage can limit your ability to invest in opportunities that could grow your wealth.

2. Starting a Business Without Research

Never invest simply because others are doing it. Conduct market research and prepare a business plan.

3. Ignoring Emergency Savings

Unexpected expenses happen. Maintain at least three to six months of living expenses before making major financial commitments.

4. Depending on Debt

Borrow responsibly. Excessive debt can create financial pressure whether you buy a home or start a business.

Questions to Help You Decide

Consider these practical questions:

- Will this investment generate income?

- Can I comfortably afford the monthly payments?

- What happens if my income decreases?

- Am I financially prepared for unexpected emergencies?

- Will this decision improve my financial future?

The Best Strategy for Long-Term Wealth

For many people, the smartest strategy isn’t choosing one forever—it is choosing the right priority at the right stage of life.

If you have a profitable business opportunity with strong potential, investing in that business first could create the income needed to buy a better home later.

If your family urgently needs stability and your finances are secure, purchasing a home first may provide peace of mind while you slowly build a business on the side.

The key is avoiding decisions based solely on emotion or social pressure. Your financial goals should reflect your own circumstances—not someone else’s timeline.

So, should you buy a house first or start a business?

The answer depends on your income, financial stability, family responsibilities, risk tolerance, and long-term goals.

If your objective is maximizing wealth, many financial experts encourage investing in income-producing assets before acquiring lifestyle assets. A successful business can eventually pay for the home you truly want.

However, if stability, security, and family needs are your highest priorities, buying a home first may be the better decision.

Ultimately, the best investment is the one that moves you closer to financial freedom while allowing you to sleep peacefully at night.

Take time to evaluate your options, create a realistic financial plan, and remember that building wealth is a marathon—not a sprint.

Business News Philippines was launched in October 2015 as a portal for readers to learn more about operating a business in the Philippines.

Yes. Corporate subscriptions are available for teams and organisations, with discounted rates as user numbers increase. Pricing starts from $1,625 + GST per user.

Get in touch

to discuss the right option for your organisation.

Business News subscriptions are used by executives, investors, consultants and professionals who need to stay informed and make better decisions about the WA market. When you subscribe you’ll get

- Unlimited access to WA’s most trusted business journalism

- Data & Insights — detailed profiles of WA companies, people, projects and deals

- MyBN — a personalised feed based on the companies, people and sectors you follow

- Special publications and industry reports

- Daily and weekly email newsletters

Data & Insights is a research tool built specifically for the WA market. It draws on more than 30 years of Business News reporting, updated regularly to reflect what’s happening now. Use it to:

- Look up detailed profiles of WA companies, including financials, directors and ownership

- Find decision-makers and track their career movements

- Research live and completed projects across WA industries

- Monitor deals, appointments and market activity

- Access industry rankings and league tables

Data & Insights is updated daily by our dedicated research team, which uses the latest announcements, ASX filings and editorial coverage to keep our person, company, list and project records up to date.

Business News welcome all opportunities to make our dataset accurate, complete and current, so if you have an update request, please email the team at

general@businessnews.com.au, and we’d be happy to assist.

MyBN

is part of every subscription. It’s your personalised view of Business News. You can follow the companies, people, sectors and projects that matter to you, and get a news feed and alerts tailored to your interests. You can save articles to read later and retain only what you need.

Only subscribers have full access to all content on the Business News website.

If staying informed about the WA economy is part of your job, and/or you’re looking for networking opportunities in WA, Business News is built for you.

Business News subscribers are:

- Executives and directors tracking competitors, clients and market movements

- Investors and advisers researching companies, deals and industry trends

- Consultants and professionals staying across sectors relevant to their clients

- Business owners looking for leads, context and market intelligence

Most Business News publications cover national or global markets. Business News is focused entirely on Western Australia, which means the journalism, the data and the intelligence are all built around WA companies, people and projects — not adapted from a national feed. Data & Insights, included with every subscription, combines more than 30 years of WA-specific editorial research with live business data. There’s no comparable product for the WA market.

The Morning Digest Email provides a comprehensive wrap of the major headlines, relevant to WA business, and includes with a snapshot of the overnight news covering oil, gold and ASX-listed companies.

The Afternoon Wrap Email focuses on the news covered by our team of journalists during the course of the working day, including exclusive stories and analysis, all of which relates to WA business and the local economy.

The BN Weekender Email contains a wrap of the Business News from the week that was, highlighting the top stories in each area of WA business.

Sign up for free.

We’re happy to help.

Get in touch

and our team will come back to you.

Business

Sam Altman Draws Online Backlash for Suggesting Parents Use ChatGPT to Make Morning Podcasts for Kids

OpenAI CEO Sam Altman drew widespread criticism online this week after suggesting that parents use the company’s new ChatGPT Work product to generate a personalized morning podcast for their children ahead of the school-day commute, with critics arguing the idea encroaches on one of the few remaining stretches of uninterrupted time parents have to talk with their kids.

In a post on X on Friday, Altman described what he called a “cool use case” for the product. “connect your family calendars and explain your kids’ interests,” he wrote, in lowercase, before adding that parents could then have ChatGPT “make a podcast that talks about one kid’s soccer game that afternoon, one kid’s upcoming birthday, some news, etc.” every morning for the drive to school.

The suggestion quickly generated significant pushback. Alex Hirsch, creator of the animated series “Gravity Falls,” offered one of the most widely shared responses, replying simply, “What if you just talked to your children?” Other commenters described the proposal as reflecting “a very low bar for what counts as a good use case of this technology,” while still others argued that ordinary, unstructured conversation during the school commute holds inherent value that an AI-generated podcast could not replicate. Not all reactions were negative; some social media users suggested AI-generated podcasts could prove useful specifically on longer car trips, or that the format could help present information to children in a more engaging way without necessarily replacing genuine conversation between parents and kids.

The backlash to Friday’s post revived scrutiny of comments Altman has made previously about the role of AI in parenting. Speaking on “The Tonight Show Starring Jimmy Fallon,” Altman said, “I cannot imagine having gone through figuring out how to raise a newborn without ChatGPT,” describing how the chatbot had helped calm his anxiety when his child had not yet begun crawling by six months of age, reassuring him that the delay was normal. Altman did add a caveat during that same appearance, acknowledging, “Clearly, people did it for a long time, no problem.”

Altman has continued discussing AI’s role in his own parenting experience in subsequent public appearances. In the debut episode of the new OpenAI Podcast, hosted by Andrew Mayne, Altman was asked how ChatGPT has helped him as a new parent and offered a striking, matter-of-fact assessment of his children’s future relationship with artificial intelligence. “My kids will never be smarter than AI,” Altman said. “But also they will grow up vastly more capable than we were when we grew up. They will be able to do things that we cannot imagine and they’ll be really good at using AI.” Altman went on to say he did not believe his children would be bothered by growing up alongside systems more capable than themselves in certain respects, though he also acknowledged potential downsides later in the same conversation, saying he suspected “this is not all going to be good, there will be problems and people will develop these problematic, or somewhat problematic, parasocial relationships.”

Altman addressed the broader online reaction to his ChatGPT Work post in a follow-up statement on X on Saturday, writing that OpenAI employees themselves report discomfort when ChatGPT asks them for things, even when they would be “perfectly happy doing the same work” if a human coworker made the identical request. “reinforces how much people care about human relationships and helping each other, and want AI to give time back — or enhance time together — rather than become a layer separating people,” Altman wrote, again in lowercase.

Not every parent has reacted negatively to the broader concept of AI-assisted parenting. Hally Peck, a mother of two, told Business Insider that she relies on an AI agent to help manage her family’s work calendars, school schedules, activities, birthdays and childcare logistics. “I have two kids, and my husband also works full-time,” Peck said. “We’re both in very demanding jobs, which means time is our most critical resource.”

Getting parents comfortable with AI-assisted tools appears to be a genuine priority for OpenAI. The company recently posted a job listing seeking a product manager with specific experience building trust-sensitive consumer experiences for parents and families, according to TechCrunch. Rival technology company Meta has separately been testing an AI-powered app designed to tell children bedtime stories.

The scrutiny of Altman’s parenting-related comments comes as OpenAI continues facing significant legal exposure tied to how ChatGPT has interacted with younger and vulnerable users. The company faces multiple lawsuits from parents and families alleging the chatbot played a role in loved ones’ delusions and suicides, including a wrongful-death lawsuit filed by the parents of 16-year-old Adam Raine, who died by suicide in April after months of conversations with ChatGPT that his parents allege included the chatbot providing detailed information on self-harm methods and offering to draft a suicide note. OpenAI has said it is “continuously improving how our models respond in sensitive interactions” and has introduced new parental control features allowing adults to link accounts with their children’s, manage feature access, and receive notifications if the system detects a teen may be in acute distress.

If you or someone you know is struggling with thoughts of suicide, the 988 Suicide and Crisis Lifeline is available around the clock by calling or texting 988.

Liontown managing director Tony Ottaviano says he’s open to growing his company’s lithium portfolio and would look at Rio Tinto’s Mt Cattlin mine if approached.

Gina Rinehart-backed Liontown ended last financial year with more than $560 million in the bank, riding the wave of positivity in the lithium market to generate $137 million over three months.

The company is planning towards an expansion call at its sole Kathleen Valley mine this quarter and hopes to achieve a mining run rate of 2.8 million tonnes per annum by the end of next year.

But with the market for the battery metal resurgent compared with 12 months ago, Mr Ottaviano said the company was looking at different avenues to growth.

“We’re good at exploration, and that’s why we’ve instigated, now that we’ve got a little bit of money, our growth options from exploration,” he said.

“The second area is shovel-ready operations – these are things that are permitted, ready to go, should we build? But that’s a three-to-five-year journey.

“And then there’s … operating assets, but they take a lot more risk. They take a lot more due diligence and a lot more understanding.

“I think a portfolio that has a mixture of all that is what you should be preparing for, and that’s what we’re doing.”

Mr Ottaviano said Liontown would “probably stay within brief” when it came to its commodity focus, with lithium the most likely target.

Questioned specifically about the mine, he said Rio Tinto’s mothballed Mt Cattlin asset near Ravensthorpe could come under consideration if an approach was made.

“If they approach us, we’ll look at it,” Mr Ottaviano said.

“But it’ll depend on the quality of the resource, and where it sits on the cost curve.”

Mt Cattlin was closed in July 2025, having come onto the books of Rio via its acquisition of $10.7 billion Arcadium Lithium acquisition months earlier.

Rio boss Simon Trott flagged the potential for the global mining giant to sell the asset last week, when he declared it was not a focus for the company’s lithium division.

Liontown’s changing fortunes have been propelled by exposure to spodumene markets, which have evolved in recent years and allowed the company to access more dynamic pricing for its spodumene product.

The miner initially sold its product under offtake contracts signed in 2022 to help it secure funding as it developed Kathleen Valley, but Mr Ottaviano said they were being slowly unwound.

“Two thirds of our book by the end of the calendar year will be on the spodumene index,” he said.

Liontown raised $316 million in August last year, in a move to secure its balance sheet amid a challenging macroeconomic environment.

Liontown shares closed 2.5 per cent higher at 99c today.

Business

Tata Motors CV shares rise 4% as July sales jump 37% YoY. Nomura expects Iveco to support earnings recovery; check target price

Domestic sales increased 28% to 33,876 units from 26,432 a year earlier, while international volumes more than doubled, rising 128% to 5,765 units.

Nomura highlighted that Tata Motors’ management lowered its LCV industry outlook to flat in 2026 while MHCV demand remained unchanged at 5% year-on-year (YoY). Bus demand is likely to be slightly lower in the EU and South America.

The company maintained its top position in the European bus market and second overall with more than 25% market share. It expects a gradual recovery in profitability in the second half of the calendar year 2026, impacted by weak LCV demand and macro uncertainties offset by cost efficiency programs, Nomura noted.

Also read | Tata Motors CV can cross 1 million vehicles after Iveco deal: N Chandrasekaran at AGM

The international brokerage believes that while weak LCV industry outlook remains a demand headwind, Iveco’s focus on cost efficiencies, low-cost sourcing advantages post TMCV integration, and new launches will support an earnings recovery over the next two years, which remains a key monitorable.

Nomura has a ‘Neutral’ call for the shares of Tata Motor CV, with a target price of Rs 402 apiece. This implies a downside potential of nearly 8% from the stock’s previous closing price of Rs 436.95 apiece on BSE.

Tata Motors CV share price

Tata Motors CV shares have gained more than 10% in a week and 5% in a month. The stock is overall up around 6% in 2026 so far.

The company currently has a market capitalisation of nearly Rs 1.67 lakh crore.

Also read | Tata Motors CV bets on global expansion, EVs and digital businesses for next phase of growth

(Disclaimer: Recommendations, suggestions, views and opinions given by the experts are their own. These do not represent the views of The Economic Times)

Rates Spark: Rates Are Seeking New Levels To Settle

In a filing with the exchange, the company reported a consolidated net loss of Rs 791 crore for the first quarter of FY27, marking nearly a 34% year-on-year decrease from the Rs 1,197 crore net loss reported in the year-ago period.

Also Read | Swiggy shares plunge 6% even as losses narrow. Should investors buy, sell or accumulate?

The company’s revenue from operations, meanwhile, increased more than 37% YoY to Rs 6,812 crore during the April-June quarter of FY27, from Rs 4,961 crore reported in the corresponding quarter of the previous financial year.

Instamart, the company’s quick commerce arm, also saw losses contract to Rs 651 crore in Q1 FY27 from Rs 797 crore in the year-ago period. Its revenue from operations meanwhile soared nearly 53% YoY to Rs 1,232 crore. Instamart’s GOV rose nearly 40% YoY to Rs 7,907 crore, while contribution margin improved 440 bps to 0.2%.

“In a period where quick commerce competition has only intensified, we prioritised improving unit economics over fleeting headline growth. Our efforts over the last few quarters to reset our user base, economics and experience have together made the business much stronger and increased the staying power,” said Sriharsha Majety, founder and group CEO of Swiggy.

Instamart’s contribution margin for the quarter stood at -0.2% of gross order value (GOV), a 4.4% improvement from a year earlier, while adjusted Ebitda losses narrowed to Rs 778 crore from Rs 896 crore a year ago.

What should investors do?

Motilal Oswal has maintained its Buy rating on Swiggy with a target price of Rs 350, implying an upside of around 18%. The brokerage largely retained its estimates, saying food delivery execution remains steady with expanding margins, while Instamart has largely addressed concerns around contribution margins.

It believes the focus will now shift to sustaining GOV growth through higher monthly transacting users, better customer retention and monetisation, while moving closer to EBITDA profitability. Motilal continues to see long-term value in Swiggy’s food delivery franchise and brand, although it believes a clear path to quick commerce EBITDA profitability will be key for a meaningful re-rating.

Nuvama has maintained its Buy rating on Swiggy with a target price of Rs 444. The brokerage highlighted that management follows a conservative accounting approach, with no capitalization of employee costs or new-store ramp-up expenses and no payable securitization.

It noted that quarterly margins were impacted by seasonal cost pressures, including annual salary revisions, minimum wage hikes for dark store operations and higher delivery partner costs. Nuvama expects the profitability of the food delivery business to increasingly offset cash burn in the quick commerce segment over the coming quarters.

Also Read | Swiggy contra view: Why JM Financial downgraded the stock to Sell despite strong Q1 results

Domestic brokerage JM Financial turned more cautious, downgrading the stock to Sell from Reduce.

With a target price of Rs 250 per share, analysts forecast over 15% downside from current market levels. The contrarian view comes after a host of international and Indian brokerages issued bullish calls on the counter following the Q1 print.

JM Financial says Swiggy’s Q1FY27 results reinforce its view that meaningful profitability improvement in the Instamart business will require greater scale. The brokerage noted that after prioritising contribution margins over the past few quarters, the company has shifted its focus back to accelerating growth.

It highlighted that Instamart’s contribution margin was only marginally above break-even in Q1 despite muted quarter-on-quarter NOV growth and expects the metric to remain in negative territory, between 0 and -100 basis points, over the next two quarters.

According to JM Financial, Swiggy has once again shifted its Instamart strategy from improving profitability to accelerating growth after nearly reaching contribution-level break-even. It says the management now aims to deliver at least double-digit sequential NOV growth in Q2FY27 while operating within a 0% to -1% contribution margin range, indicating that elevated investments will continue and adjusted EBITDA losses are likely to remain in the Rs 750-800 crore range in the near term.

(Disclaimer: Recommendations, suggestions, views and opinions given by the experts are their own. These do not represent the views of Economic Times)

Yes. Corporate subscriptions are available for teams and organisations, with discounted rates as user numbers increase. Pricing starts from $1,625 + GST per user.

Get in touch

to discuss the right option for your organisation.

Business News subscriptions are used by executives, investors, consultants and professionals who need to stay informed and make better decisions about the WA market. When you subscribe you’ll get

- Unlimited access to WA’s most trusted business journalism

- Data & Insights — detailed profiles of WA companies, people, projects and deals

- MyBN — a personalised feed based on the companies, people and sectors you follow

- Special publications and industry reports

- Daily and weekly email newsletters

Data & Insights is a research tool built specifically for the WA market. It draws on more than 30 years of Business News reporting, updated regularly to reflect what’s happening now. Use it to:

- Look up detailed profiles of WA companies, including financials, directors and ownership

- Find decision-makers and track their career movements

- Research live and completed projects across WA industries

- Monitor deals, appointments and market activity

- Access industry rankings and league tables

Data & Insights is updated daily by our dedicated research team, which uses the latest announcements, ASX filings and editorial coverage to keep our person, company, list and project records up to date.

Business News welcome all opportunities to make our dataset accurate, complete and current, so if you have an update request, please email the team at

general@businessnews.com.au, and we’d be happy to assist.

MyBN

is part of every subscription. It’s your personalised view of Business News. You can follow the companies, people, sectors and projects that matter to you, and get a news feed and alerts tailored to your interests. You can save articles to read later and retain only what you need.

Only subscribers have full access to all content on the Business News website.

If staying informed about the WA economy is part of your job, and/or you’re looking for networking opportunities in WA, Business News is built for you.

Business News subscribers are:

- Executives and directors tracking competitors, clients and market movements

- Investors and advisers researching companies, deals and industry trends

- Consultants and professionals staying across sectors relevant to their clients

- Business owners looking for leads, context and market intelligence

Most Business News publications cover national or global markets. Business News is focused entirely on Western Australia, which means the journalism, the data and the intelligence are all built around WA companies, people and projects — not adapted from a national feed. Data & Insights, included with every subscription, combines more than 30 years of WA-specific editorial research with live business data. There’s no comparable product for the WA market.

The Morning Digest Email provides a comprehensive wrap of the major headlines, relevant to WA business, and includes with a snapshot of the overnight news covering oil, gold and ASX-listed companies.

The Afternoon Wrap Email focuses on the news covered by our team of journalists during the course of the working day, including exclusive stories and analysis, all of which relates to WA business and the local economy.

The BN Weekender Email contains a wrap of the Business News from the week that was, highlighting the top stories in each area of WA business.

Sign up for free.

We’re happy to help.

Get in touch

and our team will come back to you.

PhD in Law & Economics with a dissertation on corporate wrongdoing, paired with an accounting background and a lifelong interest in markets.I write almost exclusively about undercovered small and mid-cap names, currently concentrated in fintech and consumer lending, where legal, regulatory, and governance risk routinely moves the stock more than anything on the sell-side’s model. Value, growth, secular trends, accounting shenanigans: if it fits that lens, I’m interested.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of ECPG either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Torsten Asmus/iStock via Getty Images

Dear Partners & Friends:

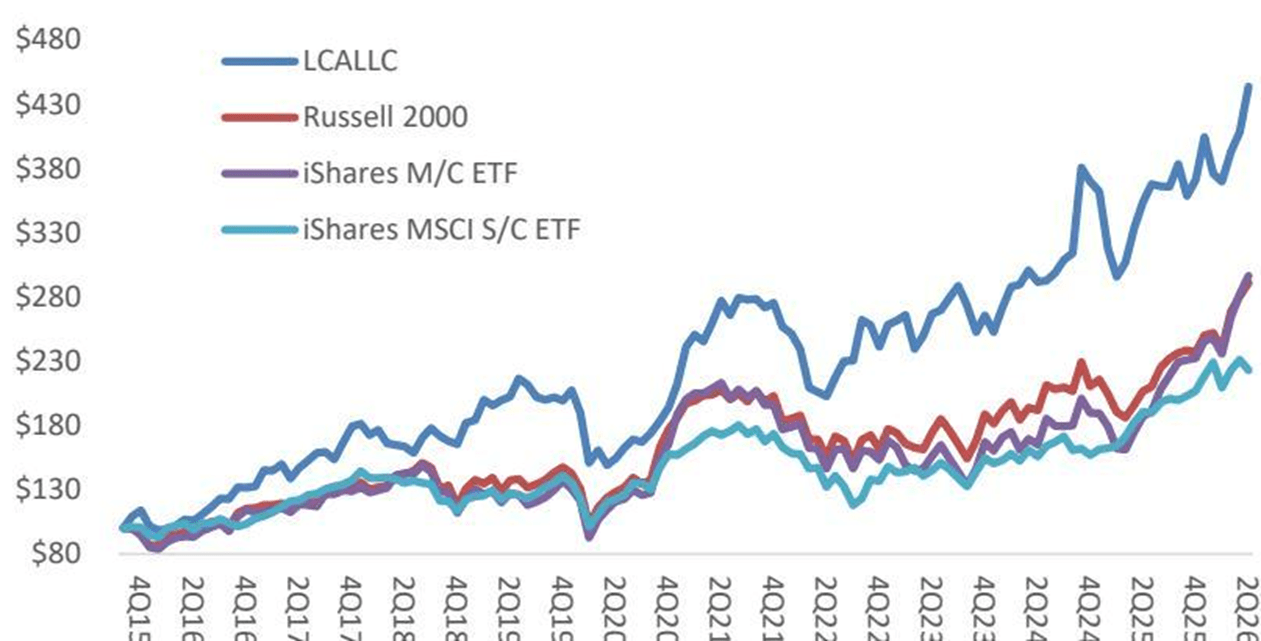

For the 2Q26 quarter ((ended June 30, 2026)), cumulative net returns improved 20%, lifting year-to-date returns to +19%, in both cases trailing the Russell 2000 and the iShares US MicroCap ETF (IWC) but well ahead of the iShares SmallCap EAFE (SCZ) ((ex-N. Am)) ETF. Returns were generated with little direct exposure to any of the themes du jour ((AI, hyperscalers, cyclical semis, etc)) that drives flows at passive funds. Since inception in November 2015 through quarter end, LCA has returned a cumulative 343% net of fees, or 15% CAGR, ahead of those indices. Past performance is no guarantee of future results. Individual account returns may vary. ¹

Long Cast was founded in 2015 on the principles of long-term and patient investing in well-researched small- and micro-cap companies. It was conceived as a “food truck version of a hedge fund”, a nod to its SMA structure, low overhead and Brooklyn base, backed by +12-years of institutional equity-research experience. It takes concentrated positions and aims for 15% annualized returns, operating as an alternative to passive investing, with more transparency than a fund and without using leverage.

Portfolio Update

In 2Q26, PDEX (PDEX), PESI (PESI) and MTRX (MTRX) were the largest contributors. There weren’t any significant decliners. We substantially added to NRC (NRC) and exited CCRN (CCRN), which was acquired, returning a solid after-tax IRR despite the unavoidable short-term treatment.

At quarter end the top five positions represented 62% of the portfolio. I am patiently putting available cash to work, recently adding to QRHC (QRHC), which has lapped negative revenue comps, and may benefit from stabilization in industrial manufacturing as well as new contracts announced earlier in the year.

It is our goal and intention to own large percentages of fewer companies over time, but we start small, continue researching and adjust as warranted. One new small position is a chemical company in turnaround, that offers the virtues of sound management, a strong balance sheet and fully depreciated assets. I am weighing if it should be a larger position, but probably not at current prices.

Since 2023, management and the Board have been excellent strategic and financial stewards. Previously an undercapitalized mini conglomerate, non-core assets have been sold off and there’s over $40M of net cash on the balance sheet. The business is built around three chemical plants, each over 50-years old, in TN, VA and SC, that supplied the once abundant carpet and textile manufacturers in the area, and now produce lubricants, surfactants, coatings, and other mixed and reacted chemicals for a variety of end markets.

From this point forward, the opportunity is improving on low-capacity utilization and “sales people who waited for the phone to ring”. It’s a solvable problem, but it’s not an easy path. This business is all about manufacturing with quality and consistency. A former HB Foster plant engineer explained to me that the chief sales people in this area are the process engineers and the plant managers with demonstrated capabilities around scheduling, batching, minimizing turnarounds and safety. These are manufacturing culture type things and culture takes time to change.

Meanwhile, our CEO and CFO’s prior successful exit was in pool chemicals, ie branded bleach, which is to say, wholly driven by sales and marketing. I’m not sure if what’s needed here from this point forward overlaps with any of their prior experiences. And that leads to questions around the intentions of the Board, some of whom are long time shareholders and possibly looking for the next fool to buy these old assets an exit.

I like a long and wide opportunity pathway, and this seems constrained and restricted. The underlying capacity puts a cap on revenues and the factories require regular maintenance and CAPEX. The industry operates in oversupply and peer group multiples are in the single digits. Meanwhile, to achieve our 15% hurdle rate at current prices would require multiple expansion into the double digits. Under certain conditions – higher-margin end-markets or faster growth – a premium multiple may be justified, but given the hill to climb, I think it pays to wait. I’ll continue to monitor it and continue to look for other ideas.

As I indicated in my mid-June email, I did a 15-minute set on the Vegas Strip by way of a “pitch session” at the Microcap Club / Planet Microcap conference, where I offered brief high-level thoughts on what makes stocks attractive, and then shared two stocks, PDEX and NRC that I think indeed are attractive.

The PDEX pitch offered an attempt to quantify the anticipated incremental benefits to operations if Zimmer (ZBH) succeeds with the mBos robot commercialization (a corrected version of the slide is below). The milestones, prices and margins are all derived from public filings and we assume four effectors per system sale, as an informed estimate.

Zimmer’s purchase of Monogram (MGRM) last year included “contingent valuation rights” (CVRs) that pay out $3.41 / share in each year from 2028 to 2030 that mBos gross revenues exceed certain hurdles. Based on these estimates, we calculated the number of systems needed to achieve those revenues, and it triangulates to a capital sale in the range of ~$1M per machine, in line with the cost of Stryker (SYK)’s Mako platform. Stryker sold 860 units, in its first three years so the forecast 609 units to trigger the final CVR seems achievable. And even if the timing is wrong or our estimates imprecise, as long as the direction is right – and Zimmer is putting significant resources behind the launch – once the system launches, PDEX could experience an exceptional transformation in operating cash flow that would justify a substantially higher corporate value. This is why it remains a top position.

On NRC, our newest investment, I discussed the company’s evolution from owner / operator to professionally led management team, and the expected benefits from putting a growth focused, incentivized and entrepreneurial executive suite behind this strong and recognizable brand, in a business with strong FCF generation and in a market where the two leading competitors just merged in a PE backed $6.5B deal.

Quantitative evidence that supports our optimism includes the recently announced largest contract in company history leading to the highest 12-mos backlog in history. Deferred revs are also growing and this typically leads sales. Furthermore, management indicated that the second year of the aforementioned contract is materially larger than the first, which infers that in one year’s time, 12-mos backlog could be even larger, and with capacity to do more. We continue to add opportunistically.

Among our other large holdings, PESI recently preannounced 2Q26 earnings indicating continued weak profitability but strong backlog growth on expanding processing at Hanford. There is potential for significantly more waste volumes if a decision is made to grout ((embed in concrete)) up to 9M gallons of low-level tank waste by 2030. This recent GAO report illustrates how large that opportunity could be and how favorable the government is in pursuing it.

Two other large holdings, MTRX and RSSS (RSSS), are on June 30 fiscal years and won’t report earnings until late August or possibly September. Given their weighting, results may be impactful to the portfolio. I think in both the cases, cash earnings will prove better than market expectations, especially MTRX, which all but guided to record profitability.

In Conclusion: On AI, Entrepreneurship and Investing

In our 1Q26 letter, I discussed my perspective of AI as a tool that’s creating a wonderful environment for entrepreneurs. Evidence is emerging along those lines, with growth in business formation and in new sole proprietorships exceeding $10M in revenues. And while the media focuses on layoffs at tech companies, evidence suggests that it’s creating ample work elsewhere, and not just for electricians and hvac installers.

Meanwhile, in the investing world, an AI-focused fund called “Situational Awareness”, led by a former Open AI (OPENAI) employee, recently blew up over $40B in capital. The fund strategy was to buy AI-related companies and short the disrupted software businesses, and use significant leverage in the process. It was recently forced to sell off its entire portfolio at a discount to meet margin calls. It puzzles me how someone so smart can be so unaware of the risks associated with using leverage in investing. Prior to its demise, returns were reportedly up 270% ytd and had been up 1,000% since inception.

It takes effort to resist the notion that we know how this is going to turn out. Our minds enjoy closure and sometimes even grope for conclusions, no matter how illogical, with a bias towards consensus.

Long Cast has experienced large drawdowns in the portfolio, and given our concentrated positioning, may well again in the future. But we operate under the premise that investing is a practice of patience and endurance, not a sprint. This is intended as a durable business that grows capital well into the future. In order to do that, we need to survive. We don’t use margin. We don’t seek out volatility. With rising rates, an expanding war and global constraints on a most a critical energy input, I’m comforted by our non-consensus portfolio.

As always, I remain committed to building a durable and sustainable business based on a repeatable investment process and intelligent capital allocation. I remain grateful to have clients ((by design)) aligned with my long term, small company centric and research-intensive focus. I welcome the continued interest from individuals and institutions as I patiently grow the business.

Sincerely / Avi

References

1. Performance data is based on Interactive Brokers “Portfolio Reports” function; shown net of management fees, expenses, and commissions; unaudited; and unless otherwise noted, since inception in Nov. 2015. Past performance is not a guarantee of future results. Individual account performance may vary. Any investment entails a risk of loss including the total loss of capital. ADV form available through Broker Check; CRD # 175005

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Business

Jonah Hill Says His Years of Jiu-Jitsu Training Have Him Ready to Take on Anyone Stuck in 2007 Still

Jonah Hill has made clear he has little patience left for people who still see him as the awkward teenage version of himself from “Superbad,” pointing to years of Brazilian jiu-jitsu training as evidence he is done being defined by a role from nearly two decades ago.

The comments came during a taping of the “SmartLess” podcast, recorded earlier this year in Los Angeles, where Hill appeared alongside hosts Jason Bateman, Will Arnett and Sean Hayes. Clips from the episode resurfaced widely online this week, reigniting conversation around Hill’s remarks about his physical transformation and his frustration with how audiences continue to perceive him nearly 20 years after “Superbad” made him and co-star Michael Cera household names.

Speaking on the podcast, Hill said he had grown tired of being reduced to the character of Seth from the 2007 comedy, telling the hosts he would “f— annihilate” anyone who continued to see him that way, and that he was not exaggerating. The comment drew immediate laughter from Bateman, Arnett and Hayes, though Hill did not walk back the remark, instead doubling down on the sentiment.

Hill’s confidence traces directly to his years of Brazilian jiu-jitsu training, a pursuit he first took up in late 2018 at age 35. He began training at Clockwork Jiu-Jitsu in New York City, where he reportedly trained four to five sessions per week to build his skills in the discipline. According to other reporting on his fitness journey, Hill has also trained under Josh Griffiths, a third-degree black belt who has competed at Abu Dhabi World Pro events and worked alongside top UFC fighters.

Before delivering his more pointed warning to critics, Hill leaned into the humor of the moment, joking that his body had begged him not to fall so deeply in love with the sport, and that his wife regularly reminds him he is a comedian rather than a professional fighter. When Bateman jokingly suggested the two of them settle things physically, Hill claimed without hesitation that he could take on all three podcast hosts simultaneously, further building the bit before pivoting to his more serious message about the lingering “Superbad” comparisons.

This is not the first time Hill has spoken candidly about how public perception of his body has affected him over the years. He has previously discussed how comments about his weight impacted him significantly during his rise to fame in his late teens and early 20s, and has been open in past interviews about how those experiences shaped both his relationship with exercise and his broader sense of self-image throughout his career.

Now settled in San Diego with his wife and their two young sons, Hill appears to occupy a markedly different place in his life than the young actor first introduced to audiences through “Superbad” in 2007. His jiu-jitsu practice appears to function as more than a simple physical outlet, instead serving as a genuine source of personal confidence that stands in direct contrast to how strangers online continue to characterize him nearly two decades later.

Hill’s frustration with being permanently associated with a single early role reflects a broader pattern common among performers whose breakout parts came relatively early in their careers, particularly in comedic roles that lean on physical characteristics for humor. “Superbad,” directed by Greg Mottola and produced by Judd Apatow, became a defining touchstone of mid-2000s teen comedy, launching both Hill and Cera into leading roles across film and television in the years that followed.

Since “Superbad,” Hill has built a considerably more varied career, earning two Academy Award nominations for best supporting actor, for “Moneyball” in 2012 and “The Wolf of Wall Street” in 2014, while also moving behind the camera as a writer and director with projects including the documentary “Stutz” and the film “Mid90s.” That range stands in contrast to the persistent public shorthand that continues to reduce him to his breakout comedic role from nearly 20 years ago.

Whether anyone actually takes Hill up on his tongue-in-cheek challenge remains to be seen, but the resurfaced clip has clearly struck a chord with fans and commentators reacting online this week. The moment underscores how even beloved, culturally resonant comedic performances can leave behind lasting assumptions about an actor that don’t always keep pace with how much that person’s career, and life, has evolved in the years since.

At Close of Business podcast August 3 2026

Coldcard pushes bitcoin back to exchanges: the anti-self-custody trade

15 Sci-Fi Movies Like ‘Interstellar’

-

Business5 days ago

Business5 days agoWhy Trees Belong on the Risk Register

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: Wit & Wisdom

-

Politics3 days ago

Politics3 days agoMeta enters AI-training agreement with far-right ‘propaganda rag’ Newsmax

-

Entertainment6 days ago

Entertainment6 days ago‘Stargate’ Creator’s New Sci-Fi Series Returns for Season 3 Tomorrow

-

Politics7 days ago

Politics7 days agoLuke Littler dismantles Gerwyn Price to retain title in Blackpool

-

Crypto World2 days ago

Crypto World2 days agoMicroStrategy Post-Earnings CLARITY Act Push Could Add New Catalyst for Its Stock

-

Politics6 days ago

Politics6 days agoThe Part of the Electric Transition Nobody Wants to Discuss

-

Business5 days ago

Business5 days agoMajor shareholder moves on Canyon

-

Crypto World2 days ago

Crypto World2 days agoXRP Ledger v3.3.0 brings five institutional features

-

News Videos4 days ago

News Videos4 days agoBitcoin Enters the 3rd Stage of the Bear Market

-

Crypto World5 days ago

Crypto World5 days agoKraken Enables Retail Access to Jersey Mike’s IPO via Tokenized Shares

-

Tech6 days ago

Tech6 days agoNew macOS Sequoia & Sonoma security updates for older Macs

-

News Videos6 days ago

News Videos6 days agoClaude: Build Financial Dashboards in Minutes (2026)

-

Politics4 days ago

Politics4 days agoLuke Littler’s dominance sparks GOAT debate

-

Business5 days ago

Business5 days agoJohnson & Johnson agrees to $5.5B settlement over talc cancer claims

-

Sports3 days ago

Sports3 days agoSeema Kaliramna Wins Discus Throw Bronze, Takes India’s CWG Medals Tally To 17

-

Crypto World23 hours ago

Crypto World23 hours agoCrypto PAC spending tops $2M in Michigan House race

-

Business3 days ago

Business3 days agoTrump Announces Hamas Disarmament Agreement as Iran Strikes Kuwait Air Base and US Attacks Pause Overnight

-

Tech5 days ago

Tech5 days agoGemini can now summarize the messiest comment threads in Google Docs

-

Tech1 day ago

Tech1 day agoESET tracks rise in malicious AI skills and adaptable malware

You must be logged in to post a comment Login