U.S. stocks are set to close out a blockbuster quarter with fresh momentum.

Major indexes are marching toward their best quarterly gains in years. The S&P 500 was up 14% through Monday, and the Nasdaq had jumped 20%-the biggest quarterly rallies for both since the second quarter of 2020.

While up the headline confidence level for Wales is below the UK as a whole

09:01, 02 Jul 2026Updated 09:07, 02 Jul 2026

Lloyds Banking Group.(Image: PA)

Business confidence in Wales rose in June but remains below the UK as a whole, shows latest research from Lloyds Bank

Its business barometer shows companies in Wales reported higher confidence in their own trading outlook month-on-month, up 13 points at 48%. When taken alongside their optimism in the economy, up five points to 16%, this gives a headline confidence reading of 32% (up from 23% in May). For the UK as a whole overall confidence was down 3% to 44%.

Advertisement

elsh firms reported strong customer demand (89%) as the key driver of confidence in their own trading outlook A net balance of 20% of businesses in the country also expect to increase staff levels over the next year, up two points on last month. Business confidence in Wales now sits below the 12-month average of 42%, with its highest figure of 76% in July last year.

Looking ahead to the next six months, Welsh businesses identified their top target areas for growth as introducing new technology such as AI or automation (52%), entering new markets (36%) and investing in their team, for example through training (33%).

Nathan Morgan, area director for Wales at Lloyds, said: “It’s encouraging to see confidence among Welsh businesses rise this month, with firms feeling more positive about their own trading outlook and the wider economy.

“That optimism is being backed by clear plans for growth, with businesses looking to embrace new technology, enter new markets and invest in their teams.

Advertisement

“With hiring intentions also edging up, there are positive signs of momentum across Wales. We’ll continue to support Welsh businesses as they adapt and pursue new opportunities.”

Business confidence rose across six of the 12 UK regions and nations in June, with the south west of England seeing the biggest improvement on May, up 22% jump to 44%. The East Midlands had the highest headline confidence reading of 56%.

On the UK position, Amanda Murphy, chief executive for Lloyds Business and Commercial Banking, said: “Confidence has edged down this month, and that reflects what we’re hearing directly from businesses. Many are still dealing with a mix of higher costs, uncertain demand and a wider global backdrop that feels difficult to read. That is weighing on decision making, particularly for firms that are focused on the UK market and have fewer ways to offset those pressures.

“However, this is not a picture of businesses stepping back altogether. Trading outlook remains relatively steady and we continue to see firms looking for new opportunities, even if investment plans have become more cautious. Businesses have shown over time that they can adapt in tough conditions, but for many the priority is managing costs and maintaining stability rather than pushing for growth.

U.S. stocks advanced to close out a blockbuster quarter, marked by sharp gains in the technology sector on expectations for strong spending for artificial intelligence. The S&P 500 and Nasdaq logged their best quarterly performances since 2020.

The Dow Jones Industrial Average rose 136.46 points, or 0.26% to 52319.20 on Tuesday. The S&P 500 rose 58.93 points, or 0.79%, to 7499.36, while the Nasdaq Composite gained 393.58 points, 1.52% to 26213.72. According to preliminary data, there were 1285 advancing issues and 1477 declining issues on the NYSE.

During the second quarter of 2026, Night Watch Investment Management LP appreciated by 12.80% net of fees.

Last quarter, we mentioned that our shareholding in Marex (MRX) had grown to be an outsized position in our portfolio, at 14.5%. This paid off this quarter, with the stock up 37% in the quarter and 230% since we bought our first shares around the IPO two years ago. The company is benefitting from high market volatility, while simultaneously showing great execution on their M&A playbook, most notably by continuing to grow their prime brokerage business. At 10x 2026 P/E and >30% ROE, this remains a compelling long.

Performance this quarter was further aided by strong performance of names such as Watches of Switzerland Group (WOSG LN) and Silicon Motion (SIMO). We owned two noticeable detractors: FUTU (FUTU) and Sanuwave (SNWV). We have been adding aggressively to FUTU while we are waiting for improving data points before risking more capital on SNWV.

Advertisement

Portfolio

Night Watch manages a global value strategy that differentiates on the following points:

Catalyst – We predominantly buy value companies with an identifiable catalyst for a rerating. Catalysts can include industry tailwinds or company-specific events (e.g., earnings inflection, CEO changes, refinancing).

Inside Ownership – We aim to find companies where management has considerable ownership in the company. We consider this alignment of interest to be an important determinant of share price performance.

Unique Names – To differentiate from a long list of other value strategies, we seek unique portfolio holdings that have little overlap with a typical wealth management portfolio. We aim to provide our LPs with diversification from their other investments in addition to strong performance.

Advertisement

The portfolio as of June 30th, 2026, is as follows:

Theme

Weight

Positions

(Senior) Housing

7.0%

2

Aerospace / Defense

15.0%

4

Payments

14.8%

3

US Cyclicals

17.0%

5

US Counter-cyclicals

21.3%

3

US Defensive

12.9%

5

Europe

10.8%

2

Hong Kong

11.2%

4

Japan

7.4%

2

Brazil

5.6%

2

Event Driven

0.4%

Funding Shorts

-17.7%

Cash

-5.8%

Total

100%

32

Largest positions:

Marex (13.7%)

AAR Corp (7.3%)

Remitly (6.2%)

Distribution Solutions Group (5.8%)

Universal Technical Institute (5.8%)

Adyen (5.6%)

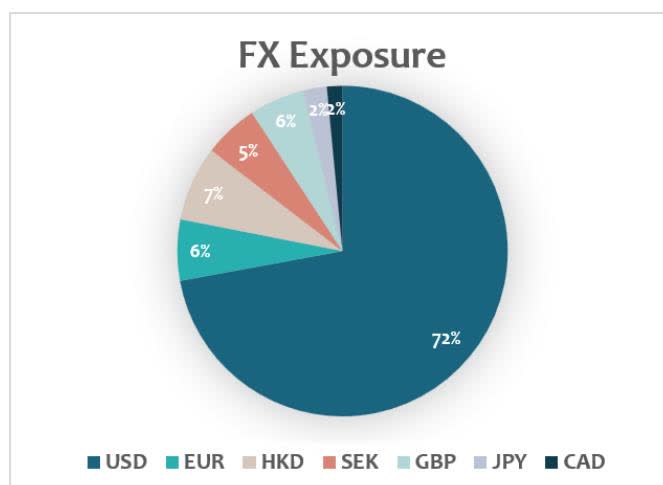

FX Exposure

Advertisement

Currency

Exposure (%)

USD

72%

EUR

6%

HKD

7%

SEK

5%

GBP

6%

JPY

2%

CAD

2%

Pie chart showing FX Exposure by currency: USD (72%), EUR (6%), HKD (7%), SEK (5%), GBP (6%), JPY (2%), CAD (2%).

Market Update

The first half of the year has been unusually volatile, and the market has been even more bifurcated than usual. On the one hand, you have got businesses that touch AI, whose stocks keep going up daily to what we believe to be unsustainable levels. We are not complaining. We were early on Western Digital Corp (WDC) and we still own Silicon Motion (SIMO). Both benefitted from the shortage in memory caused by strong demand from AI data centers. But we are not blind to the cyclical nature of those businesses, and we have been early in taking some chips off the table.

On the other hand, you have got everything that is not AI. If your business is a quality compounder with a decade-long history of providing your shareholders with 10-15% earnings growth, your stock got sold off because why would anyone care about 15% per year if you can earn that in a day by holding AI stocks!?

Naturally, we are buyers of such businesses. If we can find low-risk ways to lock in 15% earnings growth, and if we might even get some multiple expansion on top when markets normalize, we are happy to move up on the quality spectrum. We added quality names including Stryker (SYK), Adyen (ADYEN NA)(ADYYF) and Booking.com (BKNG).

Advertisement

Finally, there were the companies that, rightly or wrongly, were viewed as AI losers. We were reminded once again that valuation in today’s market does not provide a floor to stock prices. Especially software and payment related companies saw their shares freefall during the first half of 2026.

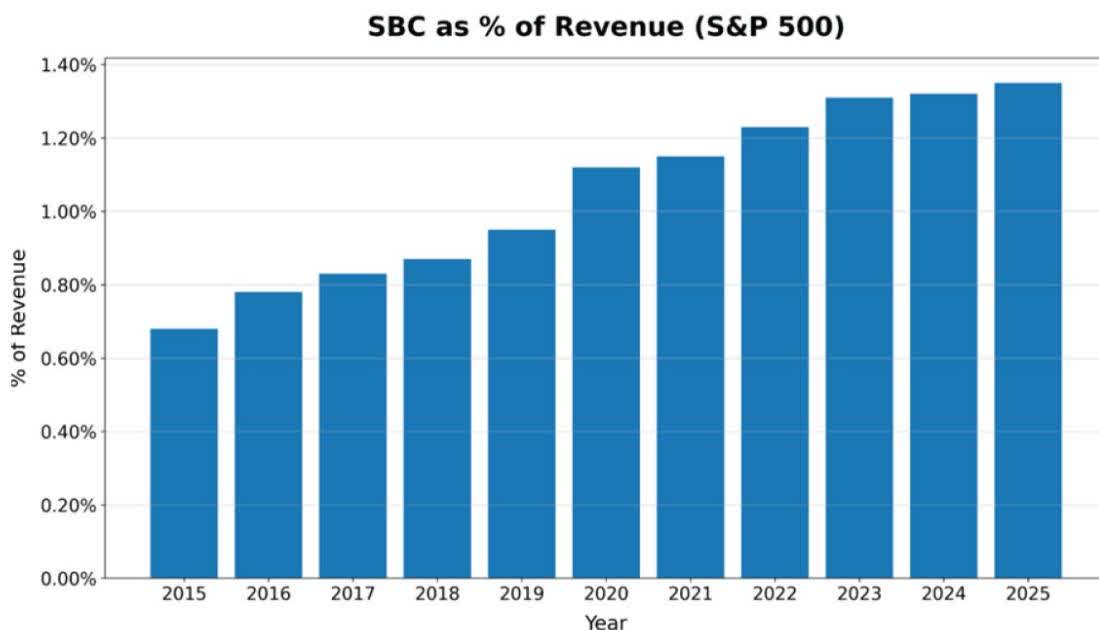

We have a differentiated view on this sell-off. Over the last few years, we have seen an increasing reliance of companies on Stock-Based Compensation (SBC). Growing a business requires capital. Wall Street’s greatest trick was to convince the markets that this growth could be funded without running the costs through the P&L. If you simply paid employees through stock options or stock grants, they argued, it’s not a real expense, and analysts ought to exclude it from their model.

For some reason, Wall Street obliged. SBC took on excessive levels as companies were keen to exploit this newly found loophole.

Source: KEDM.com – Companies taking Wall Street for a ride by excluding from earnings all salaries paid out in options and stock grants.

Advertisement

It isn’t hard to see the reflexive nature of this setup. Paying in SBC and excluding those costs is all fun and games when share prices go up. But when share prices go down, the dilution caused by the SBC goes up. 3% dilution per year can quickly become 10% dilution. On top of that, your employees are seeing the value of their stock options dwindle and might be quick to start thinking about updating their resumes.

Now that the market has finally started caring about SBC, it seems wise to buy companies with real earnings.

Historically, Dutch companies have paid out little to no SBC. This is not by accident. Stock options or grants in The Netherlands are taxed excessively, making this not a viable option for companies. While that’s a shame for Dutch employees, it benefits shareholders of those companies.

Companies with international operations, who have a large portion of their employees in places like Amsterdam, have a comparative advantage. BKNG and ADYEN fit that bill. For the first time since inception, Night Watch is going Dutch. We added BKNG and ADYEN to the portfolio.

Advertisement

Position Highlights

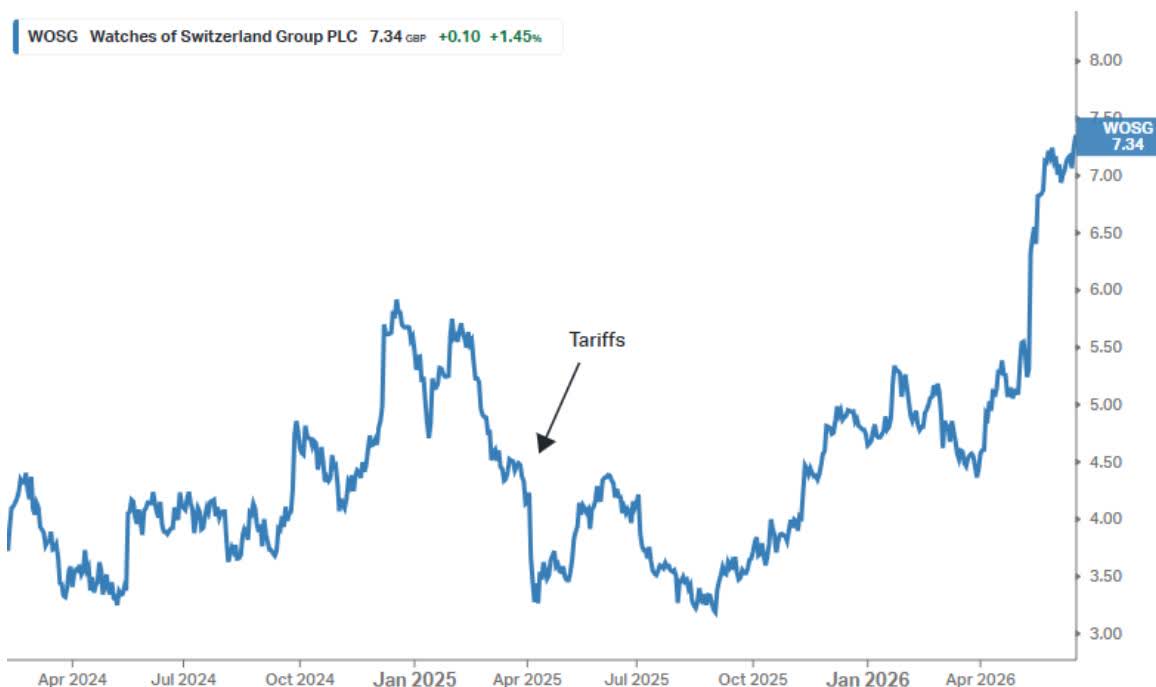

Watches of Switzerland Group (WOSG LN)(WOSGF) has been a core position since our inception in 2024. It has been a somewhat frustrating investment for the first two years, but more recently the stars have started to align.

WOSG is a retailer of luxury watches, most notably an authorized dealer of Rolex and Patek Philippe. This business is considerably higher quality than ordinary retailing because it is supply-constrained rather than demand-constrained. Prospective buyers often have to join waiting lists for popular models, and the number of watches a retailer sells is determined largely by the allocation it receives from Rolex rather than by end-market demand. Rolex, in turn, is owned by the Hans Wilsdorf Foundation, a non-profit organization that appears to be at least as interested in preserving its Swiss legacy as it is in maximizing profits.

The business model over the last few decades has been straightforward. Rolex consolidated the sale of its watches among a small group of trusted partners with the financial strength to invest millions in dedicated Rolex stores and the ability to provide a consistent customer experience across locations.

WOSG was the consolidator in the UK. In exchange for accepting slightly lower gross margins, it received larger allocations from Rolex. Higher volumes per store more than offset the lower margins.

Advertisement

Following its success in the UK, WOSG replicated the model in the United States, which today accounts for roughly 50% of revenue.

Luxury watch sales peaked in 2021, and demand for brands other than Rolex and Patek Philippe slowed. We initiated a position in early 2024 after the resulting decline in the share price.

Unfortunately, WOSG faced another setback when the United States imposed 39% tariffs on Swiss imports. We feared the economics of the business could deteriorate sharply. Rolex boutiques are difficult to repurpose, and passing through a 39% price increase, even in the luxury segment, seemed like a tall order.

We were patient. Switzerland was unlikely to be singled out as the root-cause of the US trade imbalance forever. And in a worst case, the tariffs would likely accelerate the consolidation in the industry, benefiting the strongest players.

Advertisement

With tariffs now finally in the rear-view mirror, WOSG is finally back to executing its proven playbook. US growth re-accelerated to 24%. The UK is steady at 5% growth. The balance sheet is underleveraged. Despite the strong move-up, shares are trading at 13x next year’s earnings. WOSG remains a conviction long.

Conclusion

The market has become a one-trick pony with many quality companies being sold off in favor of anything that touches the AI trade. We are happy to buy quality companies at depressed valuations. Meanwhile we are doing our own thing, allocating to sectors with structural tailwinds that are largely overlooked, including the aerospace aftermarket, futures commission merchants, and various payment companies.

By following this disciplined strategy, we have been compounding capital at well over 20% since inception while providing good diversification to anyone who is invested in the major indices. This has also resulted in very low volatility, and we have not seen any major drawdowns in our portfolio to date.

On behalf of the Night Watch team,

Advertisement

Roderick van Zuylen, Chief Investment Officer

Eileen Ke, Chief Operating Officer

Night Watch Investment Partners LP – Net Performance (in USD)

Advertisement

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

Nov

Dec

Year

2024

-0.82%

0.58%

7.09%

-0.24%

5.14%

-5.20%

9.11%

-0.23%

-1.34%

-2.40%

2.10%

-2.92%

10.30%

2025

2.56%

-0.45%

-4.12%

1.03%

8.94%

12.04%

0.14%

3.06%

1.04%

-4.46%

2.90%

-0.12%

23.61%

2026

6.44%

3.74%

-6.99%

9.69%

1.21%

1.61%

15.85%

Since Inception, Total:

57.96%

Since Inception, CAGR:

20.06%

Important Disclosures

This document was prepared by Night Watch Investment Management, LLC (“NWIM”) on July 1st, 2026, based on information available as of July 1st, 2026, and is subject to amendment. The information and opinions contained in this document (including information obtained from third-party sources) are for background purposes only and do not purport to be full or complete, and do not in any way constitute personalized investment advice or an investment recommendation on the part of NWIM. No representation, warranty, or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this document, and no liability is accepted as to the accuracy or completeness of any such information or opinions.

All investments involve the risk of a loss of capital. NWIM believes that its proprietary investment program, research and risk-management techniques moderate this risk through the careful selection of portfolio investments. However, no guarantee or representation is made that NWIM’s investment program will be successful, and investment results may vary substantially over time. Past performance is not a guide to future performance. This publication makes no recommendations whatsoever regarding buying, selling, or holding any specific security, class of securities, or securities of a class of issuers. You are required to conduct your own due diligence, analyses, draw your own conclusions, and make your own investment decisions. Commentary is provided without reference to any investment strategy or product offered by NWIM. NWIM or entities managed by NWIM may be invested in any of the industries or securities mentioned. They may trade in and out of those positions without providing any updates.

Certain information contained in this document constitute “forward-looking statements,” which can be identified by the use of certain terminology, such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue” or “believe” or the negatives thereof, or other variations thereon or comparable terminology. Any projections or other estimates in this document, including estimates of returns or performance, are “forward-looking statements” and are based upon certain assumptions that may change. Due to various risks and uncertainties, actual events or results, or the actual performance of any investment vehicle, portfolio or product described herein may differ materially from those reflected or contemplated in the forward-looking statements. Actual events are difficult to project and often depend upon factors that are beyond the control of NWIM.

Advertisement

TO THE FULL EXTENT PERMITTED BY LAW NEITHER, NWIM NOR ANY OF ITS AFFILIATES, NOR ANY OTHER PERSON OR COMPANY, ACCEPTS ANY LIABILITY WHATSOEVER FOR ANY DIRECT, INDIRECT, OR CONSEQUENTIAL LOSS ARISING FROM, OR IN CONNECTION WITH, ANY USE OF THIS PUBLICATION OR THE INFORMATION CONTAINED HEREIN. NWIM AND ITS AFFILIATES EXPRESSLY DISCLAIM ANY GUARANTEES, INCLUDING, BUT NOT LIMITED TO, FUTURE PERFORMANCE OR RETURNS.

Copyright 2026 Night Watch Investment Management, LLC. All rights reserved.

SLG Brands said the deal would allow it to focus on ‘the next era of beauty creation’

08:36, 02 Jul 2026Updated 08:42, 02 Jul 2026

SLG Brands has sold COLAB Dry Shampoo (pictured)(Image: SLG Brands)

A global beauty product incubator headquartered in Cheltenham has completed the sale of two of its flagship haircare brands to a US consumer goods company.

SLG Brands has sold Colab Dry Shampoo and Johnny’s Chop Shop to Thriving Brands – a consumer goods company in Cincinnati backed by Dallas-based private equity firm Trive Capital.

Advertisement

Following the deal, Thriving Brands – the owner of household names such as Right Guard – will use SLG’s existing distribution networks with UK and US retailers including Tesco, Boots, Target and Walmart.

SLG said the deal would allow it to focus on its core licensing business “while unlocking capital for future growth initiatives”.

Lucy Beresford, chief executive officer of SLG Brands, said: “We conceived and founded Colab Dry Shampoo and Johnny’s Chop Shop, and grew them into internationally recognised brands. Completing this transaction frees SLG to focus on the next era of beauty creation.”

SLG was established in 1985 and has developed its own portfolio of beauty and personal care products for domestic and international markets.

Advertisement

The business specialises in brand creation and licensing, having partnered with well-known high street names and celebrities for its beauty ranges including Paul Smith, Superdry, Sweaty Betty and White Fox Boutique. It is also backed by private equity firm BGF.

The deal was supported by FRP Corporate Finance’s team, led by partner Victoria Kisseleva with assistance from associate director Matthew Nolan.

Ms Kisseleva said: “In the beauty market we’re seeing continued interest in brands that can prove repeat purchase behaviour from their customers and offer the ability to scale internationally.

“Haircare in particular is one area where we’re seeing growth, which is what made these brands such an attractive prospect for acquisition on the international market.

Advertisement

“It was great to be able to help the team at SLG Brands secure this deal as it forms a key part of their future growth strategy.”

Netflix’s third installment in its popular Enola Holmes franchise arrived Tuesday with Millie Bobby Brown reprising her role as Sherlock Holmes’ younger sister in a sunnier, darker and more action-heavy chapter set against the backdrop of Malta, drawing a divided critical reception that praised Brown’s performance while questioning whether the series has begun to show signs of franchise fatigue.

“Enola Holmes 3,” rated PG-13 and running one hour and 45 minutes, begins on wedding day. Enola is about to marry Lord Tewkesbury, played again by Louis Partridge, in a ceremony set on the sun-drenched Mediterranean island. Before she can reach the altar, news arrives that her brother Sherlock, played by Henry Cavill, has been kidnapped, and Tewkesbury’s mother is taken shortly afterward. The wedding is indefinitely postponed, the mystery takes over, and Enola races through Malta with Dr. Watson, played by Himesh Patel, to find the kidnappers before the situation turns fatal.

The film is directed by Philip Barantini, best known for the critically acclaimed Netflix series “Adolescence,” who takes over the franchise from Harry Bradbeer, who helmed the first two entries. The screenplay was again written by Jack Thorne, who adapted Nancy Springer’s YA book series for all three films. The ensemble cast also includes Helena Bonham Carter as Enola’s bomb-throwing revolutionary mother Eudoria, Sharon Duncan-Brewster as the villainous Moriarty and Susan Wokoma as Enola’s mentor Edith.

Advertisement

The film includes a clue left by Sherlock before his abduction that becomes central to the plot.

“A Holmes does not disappear without leaving clues for a Holmes,” Enola observes in the film.

The shift to Malta gives the film its most visually distinctive look of the trilogy, trading London’s gloomy Victorian streets and fog for sparkling Mediterranean light and colorful architecture. Several critics noted the change of scenery as one of the film’s stronger decisions, lending the story a fresh visual energy that helps distinguish this installment from its predecessors.

Among the more enthusiastic reviews, Tom’s Guide described the third film as “easily” the reviewer’s favorite in the franchise, citing the emotional depth added to the story through Enola’s ambivalence about marriage and the fear of losing herself in the role of Victorian aristocratic wife alongside her fear of failing to save her brother. RogerEbert.com praised Brown as “ideally cast” and highlighted the film’s action sequences, puzzles and romance as dynamic and engaging elements, adding that “when she speaks directly to us, it feels good to be part of her story.”

Advertisement

MovieWeb similarly called the villain “deliciously fiendish” and praised the film’s ambition in raising the franchise’s stakes.

Critical reviews at the other end of the spectrum identified a set of recurring concerns about pacing, mystery quality and tonal inconsistency. Collider called the film “mostly forgettable,” arguing that while Brown continues to charm in the lead role, the mystery itself is lazy, largely predictable and telegraphed from early in the running time, a particular problem for a series built explicitly on the detective genre’s tradition of genuine puzzle-solving. IndieWire noted that while Barantini brings a more grown-up touch to the material, the choice doesn’t always mesh comfortably with the franchise’s characteristic exuberance, creating a film that feels caught between its desire to mature alongside its audience and its obligation to retain the playful energy that distinguished the original.

Gulf News offered perhaps the most pointed mixed assessment, describing the film as resembling banana bread: “Fine, but nothing to make a fuss about.” The review flagged the feminist and colonial commentary as clumsily integrated into the plot, suggested the villain lacked the nuance appropriate for a Holmes story and criticized a pattern in which Enola’s detective work increasingly gives way to action sequences.

Variety noted that while Enola’s fourth-wall breaks and deductive moments remain charming, some of the real-world social commentary about the suffrage movement and workers’ rights that made the earlier films feel particularly vital is largely absent here, replaced by plot threads about Maltese independence fighters and Dr. Watson’s military past that feel like afterthoughts.

Advertisement

Hollywood Reporter, in perhaps the most concisely worded verdict across the critical coverage, offered what it called a “bottom line” that the film was “elementary but enjoyable,” a play on Sherlock Holmes’ most famous phrase that captures the middling but watchable quality many critics identified.

Brown is again a producer on the film alongside Robert Brown, Michael Dreyer and Jack Thorne. The executive producer roster includes Joshua Grode and Jake Bongiovi. Director of photography Matthew Lewis shot the film on location in Malta and in studio, with production design by Gary Williamson and costumes by Consolata Boyle rounding out the period aesthetic.

The first Enola Holmes film, released in 2020 during the height of the pandemic, was watched by approximately 76 million households in its first four weeks on the platform, making it one of Netflix’s more successful original film launches and establishing Brown as a reliable franchise anchor for the streaming service alongside her work on “Stranger Things.” The sequel followed in 2022 with a broadly positive reception and solid viewership, setting up the third installment as the next test of whether the series can sustain long-term audience engagement.

Whether the franchise continues beyond this third film remains unclear. Some critics specifically called for a fourth entry if the creative team can sharpen the mystery writing, while others suggested the franchise has run its natural course and that Enola might be better served retiring gracefully rather than continuing in diminished form.

You must be logged in to post a comment Login