Business

Night Watch Investment Management Q2 2026 Investor Letter

Jacob Wackerhausen/iStock via Getty Images

Performance

During the second quarter of 2026, Night Watch Investment Management LP appreciated by 12.80% net of fees.

Last quarter, we mentioned that our shareholding in Marex (MRX) had grown to be an outsized position in our portfolio, at 14.5%. This paid off this quarter, with the stock up 37% in the quarter and 230% since we bought our first shares around the IPO two years ago. The company is benefitting from high market volatility, while simultaneously showing great execution on their M&A playbook, most notably by continuing to grow their prime brokerage business. At 10x 2026 P/E and >30% ROE, this remains a compelling long.

Performance this quarter was further aided by strong performance of names such as Watches of Switzerland Group (WOSG LN) and Silicon Motion (SIMO). We owned two noticeable detractors: FUTU (FUTU) and Sanuwave (SNWV). We have been adding aggressively to FUTU while we are waiting for improving data points before risking more capital on SNWV.

Portfolio

Night Watch manages a global value strategy that differentiates on the following points:

Catalyst – We predominantly buy value companies with an identifiable catalyst for a rerating. Catalysts can include industry tailwinds or company-specific events (e.g., earnings inflection, CEO changes, refinancing).

Inside Ownership – We aim to find companies where management has considerable ownership in the company. We consider this alignment of interest to be an important determinant of share price performance.

Unique Names – To differentiate from a long list of other value strategies, we seek unique portfolio holdings that have little overlap with a typical wealth management portfolio. We aim to provide our LPs with diversification from their other investments in addition to strong performance.

The portfolio as of June 30th, 2026, is as follows:

Largest positions:

- Marex (13.7%)

- AAR Corp (7.3%)

- Remitly (6.2%)

- Distribution Solutions Group (5.8%)

- Universal Technical Institute (5.8%)

- Adyen (5.6%)

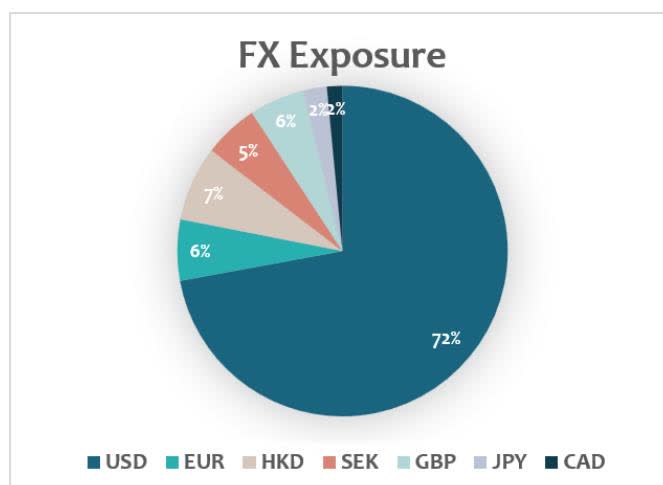

FX Exposure

Pie chart showing FX Exposure by currency: USD (72%), EUR (6%), HKD (7%), SEK (5%), GBP (6%), JPY (2%), CAD (2%).

Market Update

The first half of the year has been unusually volatile, and the market has been even more bifurcated than usual. On the one hand, you have got businesses that touch AI, whose stocks keep going up daily to what we believe to be unsustainable levels. We are not complaining. We were early on Western Digital Corp (WDC) and we still own Silicon Motion (SIMO). Both benefitted from the shortage in memory caused by strong demand from AI data centers. But we are not blind to the cyclical nature of those businesses, and we have been early in taking some chips off the table.

On the other hand, you have got everything that is not AI. If your business is a quality compounder with a decade-long history of providing your shareholders with 10-15% earnings growth, your stock got sold off because why would anyone care about 15% per year if you can earn that in a day by holding AI stocks!?

Naturally, we are buyers of such businesses. If we can find low-risk ways to lock in 15% earnings growth, and if we might even get some multiple expansion on top when markets normalize, we are happy to move up on the quality spectrum. We added quality names including Stryker (SYK), Adyen (ADYEN NA)(ADYYF) and Booking.com (BKNG).

Finally, there were the companies that, rightly or wrongly, were viewed as AI losers. We were reminded once again that valuation in today’s market does not provide a floor to stock prices. Especially software and payment related companies saw their shares freefall during the first half of 2026.

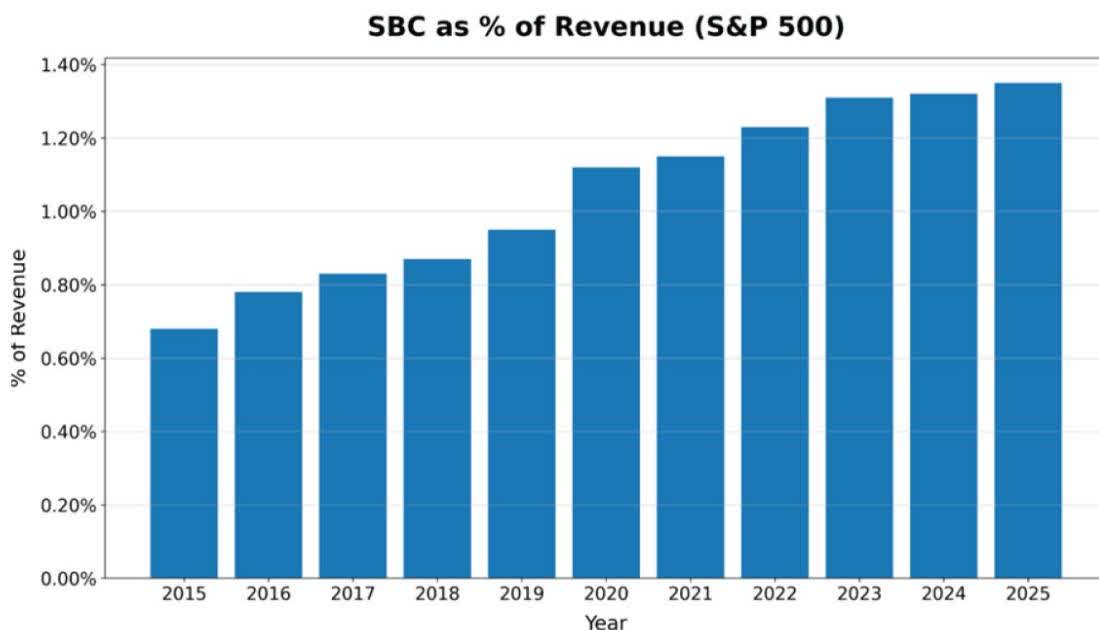

We have a differentiated view on this sell-off. Over the last few years, we have seen an increasing reliance of companies on Stock-Based Compensation (SBC). Growing a business requires capital. Wall Street’s greatest trick was to convince the markets that this growth could be funded without running the costs through the P&L. If you simply paid employees through stock options or stock grants, they argued, it’s not a real expense, and analysts ought to exclude it from their model.

For some reason, Wall Street obliged. SBC took on excessive levels as companies were keen to exploit this newly found loophole.

Source: KEDM.com – Companies taking Wall Street for a ride by excluding from earnings all salaries paid out in options and stock grants.

It isn’t hard to see the reflexive nature of this setup. Paying in SBC and excluding those costs is all fun and games when share prices go up. But when share prices go down, the dilution caused by the SBC goes up. 3% dilution per year can quickly become 10% dilution. On top of that, your employees are seeing the value of their stock options dwindle and might be quick to start thinking about updating their resumes.

Now that the market has finally started caring about SBC, it seems wise to buy companies with real earnings.

Historically, Dutch companies have paid out little to no SBC. This is not by accident. Stock options or grants in The Netherlands are taxed excessively, making this not a viable option for companies. While that’s a shame for Dutch employees, it benefits shareholders of those companies.

Companies with international operations, who have a large portion of their employees in places like Amsterdam, have a comparative advantage. BKNG and ADYEN fit that bill. For the first time since inception, Night Watch is going Dutch. We added BKNG and ADYEN to the portfolio.

Position Highlights

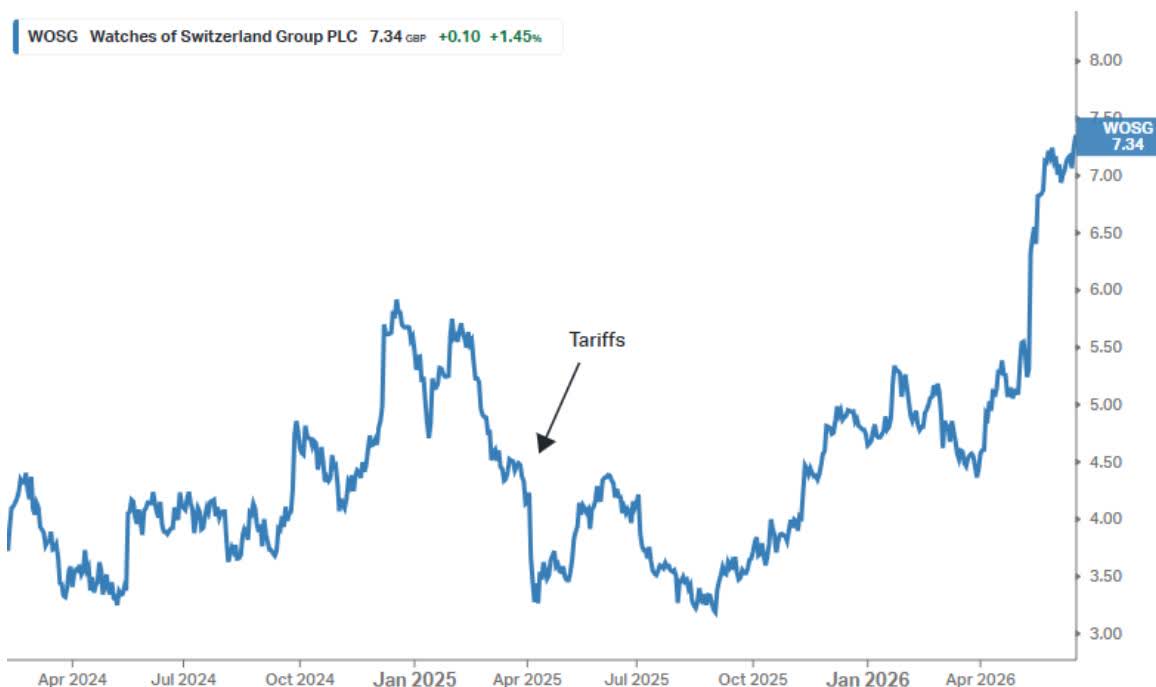

Watches of Switzerland Group (WOSG LN)(WOSGF) has been a core position since our inception in 2024. It has been a somewhat frustrating investment for the first two years, but more recently the stars have started to align.

WOSG is a retailer of luxury watches, most notably an authorized dealer of Rolex and Patek Philippe. This business is considerably higher quality than ordinary retailing because it is supply-constrained rather than demand-constrained. Prospective buyers often have to join waiting lists for popular models, and the number of watches a retailer sells is determined largely by the allocation it receives from Rolex rather than by end-market demand. Rolex, in turn, is owned by the Hans Wilsdorf Foundation, a non-profit organization that appears to be at least as interested in preserving its Swiss legacy as it is in maximizing profits.

The business model over the last few decades has been straightforward. Rolex consolidated the sale of its watches among a small group of trusted partners with the financial strength to invest millions in dedicated Rolex stores and the ability to provide a consistent customer experience across locations.

WOSG was the consolidator in the UK. In exchange for accepting slightly lower gross margins, it received larger allocations from Rolex. Higher volumes per store more than offset the lower margins.

Following its success in the UK, WOSG replicated the model in the United States, which today accounts for roughly 50% of revenue.

Luxury watch sales peaked in 2021, and demand for brands other than Rolex and Patek Philippe slowed. We initiated a position in early 2024 after the resulting decline in the share price.

Unfortunately, WOSG faced another setback when the United States imposed 39% tariffs on Swiss imports. We feared the economics of the business could deteriorate sharply. Rolex boutiques are difficult to repurpose, and passing through a 39% price increase, even in the luxury segment, seemed like a tall order.

We were patient. Switzerland was unlikely to be singled out as the root-cause of the US trade imbalance forever. And in a worst case, the tariffs would likely accelerate the consolidation in the industry, benefiting the strongest players.

With tariffs now finally in the rear-view mirror, WOSG is finally back to executing its proven playbook. US growth re-accelerated to 24%. The UK is steady at 5% growth. The balance sheet is underleveraged. Despite the strong move-up, shares are trading at 13x next year’s earnings. WOSG remains a conviction long.

Conclusion

The market has become a one-trick pony with many quality companies being sold off in favor of anything that touches the AI trade. We are happy to buy quality companies at depressed valuations. Meanwhile we are doing our own thing, allocating to sectors with structural tailwinds that are largely overlooked, including the aerospace aftermarket, futures commission merchants, and various payment companies.

By following this disciplined strategy, we have been compounding capital at well over 20% since inception while providing good diversification to anyone who is invested in the major indices. This has also resulted in very low volatility, and we have not seen any major drawdowns in our portfolio to date.

On behalf of the Night Watch team,

Roderick van Zuylen, Chief Investment Officer

Eileen Ke, Chief Operating Officer

Night Watch Investment Partners LP – Net Performance (in USD)

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Compass Point reiterates Applied Digital stock rating on data center milestone

Rosenblatt reiterates CoreWeave stock Buy rating amid Meta cloud reports

Dollar eases as yen gains ahead of US payrolls, chipmaker stocks struggle

OPINION: Michael Chaney and the board of Northern Star are pushing back as a US corporate raider raises the stakes.

For months, policymakers, businesses and trade watchers in Washington had been bracing for a turbulent spring and summer around the future of the USMCA, the trade pact binding the United States, Canada and Mexico.

But, to quote former UK Prime Minister Harold Macmillan, “Events, dear boy, events.” The war with Iran has dominated Washington’s attention, stripping away much of the political heat that was expected to surround the pact’s renewal.

Instead of a noisy fight over the agreement’s future, the USMCA has slipped into the background. The Iran conflict has absorbed the White House’s attention and, in practical terms, has become one of the best developments for keeping the trade pact out of the headlines.

Earlier this year, there were concerns the US might use the renewal window to force a confrontation with Canada and Mexico, or even threaten withdrawal. President Trump had already cooled on the deal he once signed, raising questions about how aggressively Washington would approach the next phase.

But with foreign policy dominating the administration’s agenda, the US has taken a more measured approach. It has confirmed it will not extend the agreement for another 16 years, while stopping short of more dramatic action.

Part of that restraint reflects a belief inside the administration that the trade relationship has already been reshaped.

US Trade Representative Jamieson Greer argues the White House’s tariff strategy has fundamentally altered North America’s economic ties, changing the balance with Canada and Mexico in ways that make a more confrontational approach unnecessary. But if trade does become more politically driven, the US auto industry could be the biggest loser.

Inside the Egg Price-Fixing Scandal That Spiked American Grocery Bills

British households have taken the heaviest hit to their wealth of any advanced economy since the pandemic, a sobering benchmark for a country that once prided itself on rising prosperity.

The average Briton is now more than a fifth poorer than five years ago, according to UBS. Of the 37 countries the Swiss bank surveyed, none has seen a steeper decline.

Typical individual wealth has dropped by roughly £28,500 since 2020 once inflation is stripped out, leaving the median adult with assets of just over £95,500 last year. That makes the British marginally better off than the French, but poorer than the Dutch and the Italians, a ranking that would have seemed improbable a decade ago.

Wealth here is measured by the value of assets such as property and shares, and it has been eroded at pace after inflation surged in the wake of the pandemic and Russia’s invasion of Ukraine. Britain absorbed a worse inflation shock than most of its peers as energy costs jumped, a squeeze that continues to shape the wider picture on living standards.

A cooling housing market has deepened the slump. Remarkably, British families have fared worse over the past five years than households in Turkey, Bulgaria, Mexico and Kazakhstan.

The UBS findings underline the scale of the task facing Andy Burnham as he prepares to become the next prime minister. In his first major speech since returning to the Commons, the MP for Makerfield said this week: “We cannot go through another decade like the one we have just had. We need a new determination to raise the living standards of every person in this land.”

Separate figures from the Office for National Statistics, published on Tuesday, showed that Sir Keir Starmer had failed to deliver on his pledge to improve living standards, with families now worse off than they were before he entered Downing Street.

The UBS data show the wealth of a typical individual has tumbled by more than 23 per cent on both the mean and median measures since 2020, ground down by a spike in inflation that peaked at 11.1 per cent in October 2022.

Paul Donovan, chief economist at UBS Global Wealth Management, said: “The UK had a brief period of notably higher inflation than Europe did, and that has distorted the real numbers. You had a couple of years of quite high inflation, partly because of the various peculiarities of our energy pricing structure.”

The housing market has added to the strain. UK house prices have risen by 26 per cent since the start of 2020, according to the ONS House Price Index, but consumer prices have climbed by 32 per cent over the same stretch, meaning the real value of the money tied up in the typical home has been quietly whittled away.

Donovan added: “There is a considerable weight to real estate as a form of wealth because it is the largest asset that most people own. A change in the relative performance of your local real estate market can have a notable bearing on, in particular, the median wealth level over time.”

The fall in wealth has landed alongside incomes that have struggled to keep up with prices, a double squeeze on households. At the same time, the tax burden is set to climb to its highest level since the Second World War, driven in part by the long freeze in income tax thresholds, an issue explored in Business Matters’ coverage of Britain’s record property tax burden.

The picture is not uniformly bleak across the globe. The biggest gains came in South Korea, where average wealth rose 55 per cent, along with Russia and Croatia. Among G7 economies, the largest rise was in Japan, where median wealth climbed 51 per cent.

The data arrived as the Institute of Directors said business confidence fell again in June. Anna Leach, the group’s chief economist, said it pointed to an urgent need for ministers to back economic growth.

“Businesses need to see meaningful improvements in areas like regulatory cost, tax complexity and swiftness and consistency of government decisions to fundamentally unlock spending and get growth going,” she said.

A Treasury spokesman was more upbeat: “We have the right economic plan. Inflation is holding steady, the UK led G7 growth at the start of the year, and the IMF and OECD have both upgraded growth forecasts. Real wages have risen more in the last year than in the first ten years of the previous government.” That claim of steadier prices chimes with the latest ONS inflation reading, though for many households the damage to accumulated wealth has already been done.

Jamie Young

Jamie is Senior Reporter at Business Matters, bringing over a decade of experience in UK SME business reporting.

Jamie holds a degree in Business Administration and regularly participates in industry conferences and workshops.

When not reporting on the latest business developments, Jamie is passionate about mentoring up-and-coming journalists and entrepreneurs to inspire the next generation of business leaders.

European stocks rise following Lagarde comments; U.S payrolls on tap

Form 144 RISKIFIED LTD. For: 2 July

Property heavyweights Dale Alcock and Garry Brown-Neaves have launched legal actions against their accountant and tax agent HLB Mann Judd over alleged contractual breaches.

Ethereum Price Prediction: Lubin, Bitmine, and Sharplink Launch Independent Non-Profit Institution to Bring Institutional Wealth Onchain

Taylor Swift’s Wedding Brings Major Name Change

North East TG Jones stores at risk of closing as 150 to be axed

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Staud – Corporette.com

-

Politics6 days ago

Politics6 days agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Crypto World2 days ago

Crypto World2 days agoStrategy authorizes up to $1.25B in Bitcoin sales under new capital plan

-

Politics6 days ago

Politics6 days agoPotential 2028er World Cup attendee leaderboard

-

Business6 days ago

Business6 days agoAsia stock markets slide as tech shares slump

-

News Videos4 days ago

News Videos4 days agoMAJOR BITCOIN & MARKET UPDATE!!!! (MUST WATCH ASAP!!!)

-

Tech7 days ago

Tech7 days agoA Look At A Gaggle Of Transputer Boards

-

Crypto World7 days ago

Crypto World7 days agoDell (DELL) Shares Tumble Over 5% Following Analyst Downgrade to Hold

-

Crypto World5 days ago

Crypto World5 days agoCoinbase, Circle Deepen Crypto Stock Losses Despite Resilient S&P 500

-

Business2 days ago

Business2 days agoAustralia treasurer says alleged access of prime minister’s bank data ’incredibly concerning’

-

Crypto World5 days ago

Crypto World5 days agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Sports6 days ago

Sports6 days agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Tech2 days ago

Tech2 days agoAnonymous researcher drops 0-day ‘exploitarium’ repo

-

Crypto World6 days ago

Crypto World6 days agoBitcoin Sparks $600M Hourly Liquidations With $65,000 Set To Become Resistance

-

Tech4 days ago

Tech4 days agoBluekit phishing kit adopts browser-in-the-middle for login theft

-

Tech5 days ago

Tech5 days agoRussian hackers now target Signal backup recovery keys

-

Crypto World6 days ago

Crypto World6 days agoHyperliquid Named on Singapore MAS Investor Alert Register

-

Crypto World6 days ago

Crypto World6 days agoRTX holders must register wallets before token distribution begins

-

Sports23 hours ago

Sports23 hours agoBroncos roster: OL Ben Powers (No. 74) entering final year of contract

-

Business3 days ago

Business3 days agoThe AI boom won’t burst all at once. It will pop in ‘rolling bubbles’: Macquarie

You must be logged in to post a comment Login