Business

SpaceX Stock Edges Higher Today Just Days Before Historic Nasdaq-100 Entry as Musk Denies AI Phone Report

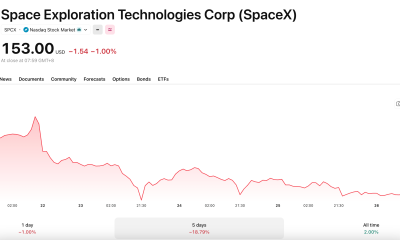

SpaceX shares stabilized Thursday after recovering from a sharp intraday drop Wednesday, with the stock edging higher as investors focused on the company’s imminent entry into the Nasdaq-100 index on Monday rather than dwelling on the whipsaw created when founder and chief executive Elon Musk denied a Wall Street Journal report suggesting SpaceX had built a prototype artificial intelligence device using Qualcomm’s Snapdragon chips.

Shares of Space Exploration Technologies Corp., trading under the ticker SPCX, were at $159.23 as of 10:39 a.m. EDT, up $1.69, or 1.07%, on the day. The gain follows a wild Wednesday session during which the stock initially surged on the WSJ report that SpaceX was developing a smartphone-like AI device featuring Snapdragon chips before Musk flatly denied the story on his social media platform X, calling it “utterly false” and sending the stock down roughly 7% to close at $157.54. Thursday’s tentative recovery reflects investors refocusing on the company’s Nasdaq-100 inclusion, now just three business days away.

Nasdaq officially confirmed that SpaceX will be added to the Nasdaq-100 index before the market opens on Monday, July 7, just 25 days after the company completed its initial public offering on June 12. That timeline makes SpaceX one of the fastest companies ever added to the benchmark index following a public market debut, a distinction made possible by a Nasdaq rule change implemented in May that shortened the waiting period for newly listed companies from several months to just 15 days, provided the company ranks among the top 40 Nasdaq-100 constituents by market capitalization. Given SpaceX’s market capitalization of approximately $2.25 trillion as of Thursday, it qualified easily.

Analysts at BNP Paribas have estimated that the Nasdaq-100 inclusion alone could generate approximately $4.3 billion in passive buying from index funds and exchange-traded products that are legally required to hold SpaceX shares in proportion to its index weighting once it enters the benchmark. The QQQ fund, the most heavily traded ETF tracking the Nasdaq-100, will be among the vehicles required to purchase SPCX shares, and the forced mechanical buying associated with index inclusion events has historically provided meaningful short-term price support for newly added companies regardless of their immediate fundamental performance.

In a separate development that could add additional forced demand, SpaceX may also eventually enter Russell 1000 and other FTSE Russell benchmark indexes, a separate process from the Nasdaq inclusion that would trigger another round of index-tracking purchases. That potential additional demand has been cited by some analysts as a further tailwind for the stock’s post-inclusion trading dynamics.

The Wedbush analyst team, which has been among the most prominently bullish voices on SpaceX since the IPO, maintained an Outperform rating and a $190 price target on the stock this week, framing the company as an AI-driven infrastructure play rather than simply a rocket and satellite company. The firm’s analysis emphasized SpaceX’s position at the intersection of three major structural technology trends, including satellite connectivity, launch vehicle economics and artificial intelligence, and described the stock as one of the most compelling long-term holdings available to investors seeking exposure to all three simultaneously.

Daiwa Securities initiated coverage of SpaceX Thursday morning with a Neutral rating, adding a relatively cautious voice to the analyst community even as the broader consensus remains skewed toward Buy. According to data from Investing.com, seven of the eight analysts currently covering SpaceX recommend buying the stock, with one recommending selling, and the average 12-month price target sits at $188.17 per share, implying upside of roughly 18% from Thursday’s trading levels. The high estimate of $310 and the low of $62 reflect the extraordinary spread of opinion surrounding a company that went public just three weeks ago and whose valuation remains deeply unsettled across the professional investor community.

Much of that valuation debate centers on three distinct business segments that SpaceX has consolidated under a single public entity. The Connectivity segment, built around Starlink’s satellite broadband network, is the most immediately visible and financially productive of the three, generating $11.4 billion in revenue and roughly $4.4 billion in operating profit in 2025, with approximately 10.3 million subscribers as of the end of March. The Space segment encompasses the company’s rocket launch operations, including Falcon 9, Falcon Heavy and the still-developing Starship system, while the AI segment, formed around the early 2026 acquisition of xAI from Musk himself, brings the Grok large language model, the Colossus gigawatt-scale data center and the social platform X under the SpaceX corporate umbrella.

SpaceX also announced this week that it is offering discounts to Starlink customers in the Memphis, Tennessee, area, according to a Bloomberg report, a move consistent with a broader strategy of using pricing flexibility to accelerate subscriber growth in markets where internet service provider competition is particularly intense. Analysts following the company have pointed to the U.S. consumer and enterprise subscriber market as an underappreciated growth vector given how much of the current Starlink narrative centers on international and rural deployment.

On the litigation front, Musk and OpenAI chief Sam Altman were reported Thursday to be heading toward mediation in their ongoing legal dispute, a development that could eventually clarify a complicated set of legal relationships involving Musk, xAI, SpaceX and OpenAI that have raised governance questions about potential conflicts of interest among the various technology ventures Musk oversees.

The stock’s current position, roughly 29% below its all-time intraday high of $225.64 reached on June 16 but still above its IPO price of $135 and meaningfully above its all-time closing low of $147.11 hit on June 23, reflects an ongoing process of price discovery for a company that has attracted both extraordinary enthusiasm and substantial skepticism from market participants attempting to determine what one of the most complex and ambitious technology businesses ever taken public is actually worth at this stage of its development.

What History Tells Us About SpaceX Joining The Nasdaq-100

Perth’s northern and south-eastern suburbs have been identified as small business hotspots, with the increased activity linked to population growth.

Moody’s places South32 on downgrade watch after $5.6 bln Alcoa asset sale

EU trade with US hits record despite tariff tensions, study shows

Business

Kawhi Leonard Returns to Toronto in Blockbuster Trade That Mirrors the 2018 Deal That Won Raptors a Title

TORONTO — Seven years after leading the Toronto Raptors to the first and only NBA championship in franchise history, Kawhi Leonard is going back to Canada in a blockbuster trade that has reshaped the Eastern Conference landscape and given Toronto the most compelling storyline in the NBA heading into the 2026-27 season.

The Los Angeles Clippers agreed to send Leonard to the Toronto Raptors in exchange for All-Star forward Brandon Ingram, guard Gradey Dick, unprotected first-round picks in 2031 and 2033, a 2027 first-round pick swap and two second-round picks in 2030 and 2033, according to ESPN’s Shams Charania, who first reported the deal Tuesday.

The transaction ends a seven-year Clippers tenure that produced three All-Star appearances, four All-NBA honors and a career-high 27.9 points per game last season but never came close to delivering the championship that both the team and Leonard sought when he chose Los Angeles over a return to Toronto in free agency in 2019. The Clippers, who went 42-40 and lost in the play-in tournament to the Golden State Warriors last season, now begin a full teardown.

The symmetry with 2018 is striking enough that analysts and commentators have noted it repeatedly since the deal became public. Eight years ago, Toronto was a strong regular-season team that could not break through in the playoffs. It traded its leading scorer, DeMar DeRozan, a recent lottery pick in Jakob Poeltl and draft capital for Leonard in the final year before his free agency. The result was an NBA title. Now, in 2026, Toronto is again a strong regular-season team that made noise before losing in the first round to the Cleveland Cavaliers. It has traded its leading scorer in Ingram, a recent lottery pick in Dick and draft capital for Leonard, again in the final year before his free agency.

Whether history repeats is an open question, but the personnel case for a strong Toronto team is real. The Raptors improved by 16 wins last season in their best offensive and defensive efficiency season in six years. Leonard, who maintained a career-high usage rate at 34 years old while playing 65 regular-season games, brings a scoring profile of the kind that Toronto has consistently lacked since the second iteration of the franchise’s championship window.

Leonard agreed to this deal for reasons ESPN sources described as grounded in familiarity and genuine competitive belief. The city of Toronto itself was a draw, as was the Raptors’ front office stability under executive vice president Bobby Webster. Most importantly, Leonard believes the Raptors can contend in the Eastern Conference. He will be eligible to sign up to a two-year, $123.7 million extension with his new team, according to ESPN’s Bobby Marks.

That extension eligibility was the single most critical variable shaping the entire trade. Leonard’s representatives had communicated to teams across the league that he was only willing to sign a contract extension with the Raptors, among teams outside Los Angeles, effectively collapsing his trade market down to one serious bidder. That leverage worked in Toronto’s favor in one sense, giving the Raptors a cleaner path to the deal without competition, but also created pressure to surrender meaningful assets since the Clippers knew Toronto was the only realistic taker willing to pay a full price.

Clippers president of basketball operations Lawrence Frank had said publicly in April, after his team’s early playoff exit, that the plan was to build around Leonard. “Our plan is to win with Kawhi,” he said at his end-of-season news conference. “At the appropriate time, we’ll sit down with Kawhi, and very similar to 2024, lay out our plan.” That plan unraveled when the Clippers made no long-term commitment to Leonard this offseason, sources told ESPN, leading Leonard’s camp to formally signal his openness to a Toronto return.

A separate but significant complication surrounds Leonard and the Clippers organization. The NBA has been investigating whether the Clippers circumvented the salary cap by channeling money to Leonard through a $28 million endorsement deal with green banking company Aspiration, which simultaneously held a $300 million, 23-year endorsement deal with the Clippers themselves. The outcome of that investigation could have implications for Leonard’s contract, though no formal ruling has been announced and the trade appears to have proceeded with full league awareness of the pending review.

For the Clippers, the Leonard trade is the final, formal acknowledgment that the organization is resetting. The franchise’s roster has been dramatically remade in a matter of months: James Harden and Ivica Zubac were moved at the trade deadline, Paul George left in free agency last summer, and now Leonard is headed to Toronto. Of the seven notable players assembled a year ago as part of an all-in championship attempt, only Brook Lopez remains. The Clippers now hold Ingram, a 28-year-old All-Star whose $40 million annual contract and recovery from a heel injury will shape what they can do next, alongside a collection of draft assets they hope to use in building a new core.

Toronto, meanwhile, wasted no time adding around Leonard’s return. The Raptors signed veteran forward Kyle Anderson, a former teammate of Leonard’s with the San Antonio Spurs, to a one-year deal. The team also confirmed a contract extension for head coach Darko Rajaković, ensuring coaching continuity as the franchise makes what is explicitly a win-now push with a player who will turn 35 during the coming season.

Scottie Barnes, Toronto’s rising young star, and Leonard together give the Raptors a forward pairing with the defensive versatility and offensive skill to compete with any team in the Eastern Conference. Whether Leonard’s body cooperates across a full playoff run, a concern that has shadowed every chapter of his career since his 2021-22 ACL season, remains the central risk in Toronto’s gamble. If he stays healthy, the Raptors have acquired one of the five best players in the NBA at a price that, relative to other recent superstar trades, analysts have described as closer to a bargain than an overpay.

A GOF Distribution Cut Is Likely Coming

In total, about 30 unique adverts appeared promoting child sexual abuse, although some of these were shared by multiple accounts.

The alias account was also shown about 20 ads featuring adult pornography.

The distribution of both child sexual abuse material and adult pornography are criminal offences in India, while Meta’s policy states that ads must not contain adult nudity, genitals or content that sexually exploits or endangers children. The BBC has reported all of the ads and the Telegram channels to the Indian authorities.

One ad showed a boy and girl, both of whom appeared to be about 12 years old, engaging in a sexual act.

Another showed a man with his arm around a girl, with text saying he was 52 and the girl was 12. “Click to watch more,” it said, linking out to a Telegram channel.

The BBC reported an advert to Instagram showing a very young girl in tears, with wording indicating that she had been sexually assaulted.

But 24 hours later, Instagram replied saying it hadn’t removed the advert because “our review team found that the advertiser’s ad does not go against our community standards”.

Meta later told the BBC that “no system is perfect, and our review process may not detect all policy violations”.

“We continue to run proactive detection technology on ads once they’re live, and anyone can report an ad to us that they think breaks our rules,” Meta said.

It added that when it becomes aware of apparent child exploitation it reports it to the National Center for Missing and Exploited Children (NCMEC), in compliance with the law. The NCMEC is the centralised global reporting system for the online sexual exploitation of children.

We reported two channels to Telegram for selling child sexual abuse videos.

One of them was subsequently taken down and replaced with a message saying: “This group can’t be displayed because it violated Telegram’s Terms of Service,” but the other continued to post new videos for sale.

Critics have previously accused the platform of not doing enough to prevent the sharing of criminal content.

The Dubai-based company is not a member of either the NCMEC or the Internet Watch Foundation, which also works with most online platforms to find, report and remove such material.

Telegram told the BBC that the company uses both automated and human moderation to eradicate child sexual abuse material (CSAM) from the app, and as a result it says it has “virtually eliminated the public spread of CSAM from its platform”.

Narendra Solanki from Anand Rathi Shares & Stock Brokers believes the upcoming results will largely reinforce the strength of domestic-facing sectors, while export-oriented industries like IT may continue to face pressure.

IT Likely to Remain Under Pressure

The IT sector is expected to remain in focus this earnings season as investors assess the impact of artificial intelligence-led disruption, delayed client spending and global uncertainty on growth prospects.According to Solanki, caution remains warranted despite attractive valuations.

“Results are around the corner, and the first results will start coming from the 9th. Coming to the IT sector, our positioning is neutral to cautious, especially in this quarter. The sector is currently facing multiple headwinds, right from AI disruption to the West Asia crisis. We are also seeing deals being delayed, with clients not committing upfront, so deal closures are not happening at the pace we used to see. These factors are likely to continue impacting the IT sector in the near term,” he said.

While near-term challenges remain, he believes the second half of the financial year could witness an improvement.

“One thing is certain: the second half is going to be better than the first half. However, one key risk remains whether there is any possibility of trimming the FY27 growth guidance, especially at the higher end. That is something the market should watch carefully in the management commentaries this quarter. The top-end guidance of around 2.5% to 3.5% now looks difficult, especially after recent commentary from Accenture. That is why our stance remains neutral to cautious in Q1,” he said.

FMCG May Spring a Positive Surprise

While markets have largely been optimistic on sectors such as auto ancillaries, manufacturing and power transmission & distribution, Solanki believes the biggest surprise could emerge from FMCG and discretionary consumption.

He points to easing inflation, lower crude oil prices and resilient demand trends as factors that could support stronger-than-expected earnings.

“Broadly, sectors like auto ancillaries, manufacturing and power T&D should continue to perform well. The surprising factor may come from the FMCG pack, where markets are currently cautious. However, there have been decent price hikes in the FMCG space, overall inflation has come down, crude oil prices have softened, and both rural and urban demand have shown resilience. So, there can be a positive surprise, especially in the FMCG or discretionary space,” he said.

He also expects domestic manufacturing, healthcare and banking to remain strong performers.

“Auto and auto ancillaries should continue to perform well. The hospitals segment within healthcare should also perform well. Banks are expected to remain strong, with overall credit growth at around 7.7%. Industrial growth data is also promising, so overall the domestic manufacturing sector should continue to perform well,” he said.

PSU Banks Continue to Outshine

Among financials, Solanki continues to favour public sector banks over their private-sector counterparts, citing consistent earnings growth, improving profitability and healthy asset quality.

“Compared with private banks, we remain committed to public sector banks because they have continuously posted better growth over the last seven straight quarters, and there is no reason for that momentum to stop. Return ratios are improving, asset quality continues to remain good, and provisioning has been very healthy, with more than an 80% provisioning run rate. We do not see any near-term risk and continue to favour public sector banks over private banks,” he said.

Real Estate Rally May Be Nearing a Pause

Although real estate stocks have staged a sharp recovery, Solanki believes much of the optimism has already been reflected in valuations. Rising inventory levels could begin to weigh on the sector in the coming quarters.

“Most of the rally has already been done. If you look at inventory build-up, it has risen from 14 months to 18 months, which is the first alarming sign. The good part of the rally is behind us, and after one or two quarters we could start seeing some consolidation or slack in the sector. Unsold inventory is steadily rising and now stands at around 18 months, which could impact the second quarter,” he said.

Management Guidance Will Be the Biggest Trigger

Beyond the headline earnings numbers, Solanki believes management guidance will play a decisive role in shaping investor sentiment, particularly in the IT sector where expectations may still be too optimistic.

“As I mentioned earlier, IT may be trading at historically lower valuations in terms of price-to-earnings ratios, but any cut in guidance by companies, especially in the first half, may not yet be fully priced in by the market. That will remain one of the key things to watch in the management commentaries,” he said.

The Bottom Line

The Q1 earnings season is shaping up as a test of sectoral divergence rather than broad-based strength. Domestic themes—including PSU banks, manufacturing, healthcare and auto ancillaries—are expected to remain resilient, while FMCG could emerge as an unexpected outperformer. In contrast, IT companies face heightened scrutiny, with investors closely tracking demand commentary and any revisions to growth guidance that could influence market sentiment in the months ahead.

Indonesia recovers body of American pilot killed by rebels in Papua, military says

The Cook Government has known for more than a year this moment might arrive.

When former AFL star Nicky Winmar was charged over an alleged assault last May, a political risk emerged alongside the criminal proceedings.

Winmar is not just another sporting great; He is the only individual honoured with a permanent statue at Optus Stadium, a monument supported by the State Government to commemorate his defining stand against racism in Australian football. It was unveiled by then-Premier Mark McGowan.

Now that Winmar has been convicted of assault offences against a female, the government can no longer avoid the question.

Does the statue stay?

Whatever answer it gives will come with political consequences.

If the government leaves the statue in place, critics will ask why Western Australia’s premier sporting venue continues to honour a man convicted of assaulting a woman.

Ministers regularly speak about respect for women and the importance of tackling family and domestic violence. Those statements will inevitably be measured against the decision they make about Winmar.

But removing the statue presents an equally difficult political challenge.

Winmar remains one of Australia’s most significant Indigenous sporting figures. His stand against racism in 1993 changed Australian football and became part of the nation’s broader story about race and reconciliation.

Imagine, for a minute, Winmar’s became just the second statue to be taken down in Western Australia because of the poor behaviour of the subject. The first featured Captain James Stirling, who led the 1834 Pinjarra Massacre for which Governor Chris Dawson has recently apologised.

Statues of John Septimus Roe (a member of the massacre party who didn’t fire a shot and also the surveyor-general charged with carving up land stolen from the Indigenous people) and the Explorer’s Monument at Fremantle that commemorates Maitland Brown (who led a punitive raid in which up to 40 Indigenous people were killed in retribution for the murder of three explorers) are still standing.

And that is where the Cook Government finds itself wedged.

This is a government that has already discovered how politically volatile Indigenous issues can become. The Aboriginal Cultural Heritage Act remains one of the defining political failures of its time in government, leaving ministers understandably cautious about decisions that intersect with Indigenous recognition and symbolism.

Against that backdrop, removing one of the city’s most prominent statues of an Indigenous person would be politically risky.

Leaving it untouched may prove no less so, and doubtless they will wait for the appeal period to expire before making the call.

Meanwhile, the AFL is no less wedged. The country’s highest-profile sporting body commissioned the statue and, presumably, still has a stake in its appearance at the stadium. Its position on this matter, given the slew of issues it has had with the poor behaviour of men, deserves scrutiny.

What History Tells Us About SpaceX Joining The Nasdaq-100

More bitcoin is now held at a loss than at a profit

Politics Home Article | The Lords should not be able to block legislation backed by MPs

-

Fashion7 days ago

Fashion7 days agoWeekend Open Thread: Staud – Corporette.com

-

Crypto World3 days ago

Crypto World3 days agoStrategy authorizes up to $1.25B in Bitcoin sales under new capital plan

-

Business7 days ago

Business7 days agoAsia stock markets slide as tech shares slump

-

News Videos4 days ago

News Videos4 days agoMAJOR BITCOIN & MARKET UPDATE!!!! (MUST WATCH ASAP!!!)

-

Tech3 days ago

Tech3 days agoAnonymous researcher drops 0-day ‘exploitarium’ repo

-

Crypto World6 days ago

Crypto World6 days agoCoinbase, Circle Deepen Crypto Stock Losses Despite Resilient S&P 500

-

Business3 days ago

Business3 days agoAustralia treasurer says alleged access of prime minister’s bank data ’incredibly concerning’

-

Crypto World6 days ago

Crypto World6 days agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Sports6 days ago

Sports6 days agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Tech5 days ago

Tech5 days agoBluekit phishing kit adopts browser-in-the-middle for login theft

-

Tech6 days ago

Tech6 days agoRussian hackers now target Signal backup recovery keys

-

Crypto World7 days ago

Crypto World7 days agoTether (USDT) Passes Ether in Market Cap as ETH Drops Toward $1.5K

-

Crypto World7 days ago

Crypto World7 days agoHyperliquid Named on Singapore MAS Investor Alert Register

-

Crypto World7 days ago

Crypto World7 days agoRTX holders must register wallets before token distribution begins

-

Sports2 days ago

Sports2 days agoBroncos roster: OL Ben Powers (No. 74) entering final year of contract

-

Business4 days ago

Business4 days agoThe AI boom won’t burst all at once. It will pop in ‘rolling bubbles’: Macquarie

-

Tech5 days ago

Tech5 days agoClaude Code turned every engineer into three. Now companies need more product thinkers

-

Crypto World7 days ago

Crypto World7 days agoSpaceX Called a Market Top Signal Just 2 Weeks After Its $86 Billion IPO

-

Tech6 days ago

Tech6 days agoSilicon Valley paid to kill AI regulation, now it wants the rules back

-

NewsBeat2 days ago

NewsBeat2 days agoPresenter Caroline Flack’s brother Paul Flack dies aged 55

You must be logged in to post a comment Login