Business

Zendaya Shines in Uneven, Noir-Tinged Return After Four-Year Wait

LOS ANGELES — HBO’s long-awaited “Euphoria” Season 3 finally arrives Sunday, delivering a visually stunning but uneven evolution of its raw teen drama into a darker, more adult crime saga. Premiering April 12 at 9 p.m. ET on HBO and streaming on Max, the eight-episode final season jumps five years forward, trading high school chaos for the messy realities of young adulthood, faith, redemption and evil. Zendaya once again anchors the series with a magnetic, layered performance as Rue Bennett, but creator Sam Levinson’s ambitious shift leaves some characters and plotlines feeling disjointed.

The season opens with Rue in an interrogation room, casually recounting her post-high school life south of the border in Mexico. Deep in debt to the menacing drug dealer Laurie (Martha Kelly, now a series regular), Rue has turned to smuggling as one of her “innovative ways” to settle scores. The trailer’s glimpse of this new direction sets a gritty, almost noir tone that permeates much of the early episodes, blending Levinson’s signature stylized visuals with crime-thriller elements reminiscent of “Fargo” or “Breaking Bad” filtered through a Gen-Z lens.

A major time jump allows the East Highland High School alumni to grapple with life beyond prom and parties. Cassie Howard (Sydney Sweeney) has pivoted to adult content creation, including an OnlyFans account, to fund an extravagant wedding to Nate Jacobs (Jacob Elordi), now an entrepreneur with his own ambitions and demons. Maddy Perez (Alexa Demie) navigates a Hollywood-adjacent lifestyle that feels both glamorous and hollow. Jules Vaughn (Hunter Schafer) explores art school and more complicated relationships, while Lexi Howard (Maude Apatow) continues observing the chaos from a safer distance.

The official logline — “A group of childhood friends wrestle with the virtue of faith, the possibility of redemption, and the problem of evil” — signals Levinson’s intent to deepen the show’s philosophical undercurrents. Religious imagery, moral dilemmas and consequences of past actions take center stage, moving away from the hormone-fueled intensity of Seasons 1 and 2. Colman Domingo returns as Ali, offering Rue moments of grounded wisdom, while Eric Dane’s Cal Jacobs marks his final appearances before his real-life passing earlier in 2026, adding an unintended layer of poignancy.

New series regulars bolster the ensemble. Adewale Akinnuoye-Agbaje and Toby Wallace bring fresh intensity, while a large supporting cast including Natasha Lyonne, Danielle Deadwyler and others expands the world into adult spheres of crime, Hollywood and personal reckoning. Martha Kelly and Chloe Cherry have been promoted to regulars, giving Laurie and Faye more narrative weight.

Visually, “Euphoria” remains unmatched. Cinematographer Marcell Rév’s work is hypnotic, with neon-drenched nights, dreamlike sequences and intimate close-ups that make every frame feel like a fashion editorial crossed with a fever dream. Labrinth’s score pulses with emotional weight, elevating even slower moments. Levinson’s direction leans into excess — long tracking shots, bold color palettes and unfiltered nudity or violence — but the style sometimes overshadows substance in the season’s more meandering stretches.

Zendaya delivers what many critics call her career-best work as Rue. Now in her early 20s, the character carries the scars of addiction and loss with a jittery vulnerability that feels lived-in. Her scenes in Mexico crackle with tension, blending quiet desperation and dark humor. Sweeney and Elordi bring commitment to their roles, with Cassie’s cam-girl storyline and Nate’s evolution providing provocative if polarizing material. Schafer’s Jules remains a highlight of emotional authenticity amid the ensemble’s larger-than-life arcs.

Yet the season struggles with cohesion. Early episodes juggle multiple storylines — drug smuggling, adult content entrepreneurship, fractured friendships and budding criminal enterprises — sometimes at the expense of deeper character development. Some reviewers describe it as “entertaining but disjointed fan fiction,” with tonal shifts that veer from poignant to absurd. The move away from high school allows for maturity, but the show occasionally feels like it’s chasing relevance in a post-pandemic cultural landscape where its once-shocking elements have become more normalized.

Critics are divided. Early reviews give the season mixed scores, with some praising the bold evolution and Zendaya’s anchoring presence while others call it indulgent or unhinged. One outlet labeled it an “unhinged disaster” that sacrifices depth for absurdity, while others hail the noir pivot as a refreshing reset that lets characters confront real adult stakes. Rotten Tomatoes and Metacritic scores reflect the polarization, hovering in the mixed-to-positive range after initial critic screenings.

The four-year gap since Season 2’s February 2022 finale tested fan patience but allowed real-world aging that benefits the story. The cast, now in their mid-to-late 20s, convincingly portray characters navigating quarter-life crises rather than teenage rebellion. Production delays, creative shifts and Levinson’s meticulous process contributed to the wait, but the result feels like a deliberate maturation rather than a rushed cash-in.

Themes of redemption resonate strongly. Rue’s journey toward accountability, however halting, carries emotional heft, especially in scenes with Ali or when confronting the consequences of her actions. The show continues tackling mental health, addiction, sexuality and toxic relationships with unflinching honesty, though some storylines risk veering into exploitation territory. Levinson’s writing remains provocative, sparking conversations about consent, ambition and the blurred lines between performance and reality in the social media age.

For longtime viewers, familiar Easter eggs and callbacks provide satisfaction, while newcomers may struggle with the dense backstory. The season’s eight-episode run keeps pacing brisk, with weekly Sunday drops building anticipation through May 31. A Coachella screening of the premiere added to the cultural buzz, echoing the show’s history of intersecting with music and fashion moments.

“Euphoria” Season 3 may not recapture the lightning-in-a-bottle shock of its debut, but it offers something more ambitious: a meditation on growing up when the stakes are no longer detention but real-world ruin or redemption. Zendaya’s performance alone makes it essential viewing, carrying the series through its uneven patches with quiet power.

Whether the season sticks the landing in its later episodes remains to be seen as critics and audiences watch weekly. For now, the return of HBO’s stylish, controversial drama reminds viewers why it became a cultural phenomenon — flawed, excessive and undeniably compelling.

As Rue asks in voiceover what she’s been up to since high school, the answer unfolds in neon-soaked moral gray areas that feel both timeless and very much of this moment. “Euphoria” may have aged, but its ability to provoke and mesmerize endures.

The ranch dressing marks the first condiment launched by the company.

Twix Bits are bite-size varieties of the classic candy bar.

NEW YORK — Alphabet Inc. Class C shares edged lower in early trading Wednesday, dipping 0.47 percent to $329.01 as investors paused ahead of the company’s first-quarter earnings later this month while weighing heavy artificial intelligence investments against broader market optimism over potential de-escalation in the Middle East.

At 9:41 a.m. EDT, GOOG had fallen $1.57 from Tuesday’s close. The modest decline contrasted with gains in the broader Dow Jones Industrial Average, which rose on hopes that President Donald Trump’s comments signaling the Iran conflict is “very close to over” could ease energy price pressures and support global advertising spending.

Alphabet, parent of Google, has been navigating a complex environment. Strong momentum in Google Cloud and Gemini AI advancements have driven optimism, yet concerns over soaring capital expenditures — projected between $175 billion and $185 billion for 2026 — continue to pressure near-term margins and free cash flow.

Earnings Preview

Alphabet is scheduled to report first-quarter 2026 results after the market close on April 29. Analysts expect revenue around $106-107 billion and earnings per share near $2.60, building on the robust Q4 2025 performance that saw revenue hit $113.8 billion and EPS reach $2.82.

Google Cloud remains a standout, with recent quarters showing accelerating growth fueled by AI infrastructure demand from hyperscalers. The segment’s backlog has swelled, reflecting strong enterprise adoption of Gemini-powered tools. However, the massive AI-related buildout has raised questions about profitability timelines.

Search advertising, still the company’s core engine, benefits from AI Overviews and Gemini integration, though shifts in user behavior and competition from OpenAI and others create ongoing dynamics. YouTube advertising and subscription services also provide diversified revenue streams.

AI Leadership and Gemini Momentum

Alphabet has aggressively pushed Gemini models throughout 2026. Recent updates have expanded capabilities, with user growth reaching hundreds of millions and deeper integration across Google products. The company’s heavy CapEx reflects ambitions to maintain leadership in the generative AI race, including data centers, custom chips and model training.

While some investors worry about the short-term financial burden, others see it as necessary spending to capture long-term market share. Google Cloud’s growth rate is expected to be a key focus on the upcoming earnings call, with analysts viewing it as the primary driver for potential stock upside.

Market and Geopolitical Context

Wednesday’s trading comes as markets broadly advance on Middle East developments. Reduced fears over prolonged disruption to oil supplies from the Strait of Hormuz have lifted risk assets, benefiting advertising-dependent companies like Alphabet. Digital ad spending tends to correlate with economic confidence and corporate budgets.

Alphabet shares have shown resilience in 2026 despite volatility tied to AI spending concerns and earlier geopolitical shocks. The stock has traded in a range, pulling back from highs earlier in the year amid broader tech sector rotation but remaining well above longer-term averages.

Regulatory and Antitrust Backdrop

Ongoing U.S. Department of Justice actions and potential appeals continue to loom over the company. Any resolution or clarity on remedies could influence investor sentiment, though the immediate focus remains on operational execution and AI progress.

Internationally, Alphabet navigates varying regulatory environments, from European privacy rules to competition probes in multiple jurisdictions. These factors add layers of uncertainty but have not derailed core business growth.

Analyst Perspectives

Wall Street remains generally bullish on Alphabet’s long-term prospects. Several firms highlight the company’s undervaluation relative to growth potential in cloud and AI, with price targets often exceeding current levels. However, execution on cost management and returns on AI investments will be closely scrutinized.

Some analysts recommend buying ahead of earnings, citing strong fundamentals and the possibility of positive surprises in cloud metrics. Others advise caution given high expectations and the risk of margin compression from elevated spending.

Broader Tech Sector Outlook

Alphabet’s performance mirrors trends across big tech. Peers face similar pressures balancing innovation spending with profitability. Yet demand for AI infrastructure remains robust, supporting valuations even as near-term costs mount.

Retail and institutional investors continue monitoring Alphabet as a core holding for exposure to digital advertising, cloud computing and artificial intelligence — three secular growth areas expected to shape the economy for years.

Looking Ahead

As the April 29 earnings approach, investors will seek details on cloud growth trajectory, Gemini adoption metrics, advertising trends and updated guidance on capital expenditures. Management’s tone on balancing growth and efficiency could sway sentiment significantly.

In the meantime, external factors like Middle East developments, Federal Reserve signals and overall market risk appetite will influence trading. Wednesday’s slight pullback appears more like profit-taking or positioning than a fundamental shift.

Alphabet’s massive scale, financial strength and technological moat position it well for continued leadership. Whether the current AI investment cycle delivers outsized returns remains the central debate, but the company’s track record of innovation suggests it is well-equipped to navigate the challenges.

For now, the modest decline in GOOG shares reflects a cautious pause in an otherwise optimistic market environment. As global tensions ease and earnings season intensifies, Alphabet stands ready to demonstrate why it remains one of the most important technology franchises in the world.

NEW YORK — IonQ Inc. shares have delivered explosive gains for early believers but remain a high-stakes bet heading deeper into 2026, with Wall Street analysts largely urging investors to buy the dip while cautioning that the quantum computing pioneer’s path to profitability is long and volatile.

Trading around $35–$40 in mid-April 2026, IONQ stock has pulled back from earlier highs amid broader tech sector rotation and lingering concerns over execution risks. Yet the company’s fundamentals tell a compelling growth story: 202% revenue increase in 2025 to $130 million, a robust $370 million backlog, and ambitious 2026 guidance of $225 million to $245 million in revenue.

Analysts maintain a consensus “Moderate Buy” to “Strong Buy” rating. The average 12-month price target sits near $65–$69, implying roughly 80–100 percent upside from current levels, with some optimistic forecasts reaching $100. No major brokerage currently carries a Sell rating.

Strong Commercial Momentum

IonQ has transitioned from pure research to a full-stack quantum platform provider faster than many competitors. Its trapped-ion technology has achieved industry-leading fidelity metrics, including 99.99% two-qubit gate fidelity on systems like Tempo. The company recently hit key milestones such as photonic interconnect breakthroughs and expanded collaborations with institutions including the University of Maryland and DARPA.

Enterprise and government adoption is accelerating. Major customers across finance, pharmaceuticals, logistics and defense are using IonQ systems for complex optimization, simulation and machine learning tasks that classical computers struggle with. The $370 million remaining performance obligations provide strong revenue visibility into 2026 and beyond.

CEO Niccolo de Masi described 2025 as an “inflection point,” with the company scaling production, improving manufacturing yields and positioning itself as the only full-stack quantum player with vertically integrated hardware, software and cloud access.

Financial Position and Path Forward

IonQ ended 2025 with a fortress-like balance sheet — roughly $3.3 billion in cash, cash equivalents and investments and no debt. This war chest funds aggressive R&D and potential acquisitions while shielding the company from near-term dilution pressures that have plagued smaller quantum peers.

Still, the company remains deeply unprofitable. Gross margins are negative as it invests heavily in scaling systems and cloud infrastructure. Analysts expect continued cash burn in 2026, though improving commercial mix and higher utilization rates should gradually narrow losses. Earnings growth estimates for 2026 sit around 65 percent on top of triple-digit revenue expansion.

Risks That Could Derail the Bull Case

Quantum computing is still an emerging field with significant technical and commercial hurdles. Error correction, scalability to thousands of logical qubits, and real-world advantage over classical systems remain years away for most applications. IonQ faces stiff competition from IBM, Google, Rigetti, Quantinuum and others pursuing different technological approaches.

Valuation remains stretched. Even after the recent pullback, shares trade at enormous multiples of current sales. Any delay in hitting 2026 guidance, slower customer ramp or negative clinical trial outcomes for quantum use cases could trigger sharp sell-offs. The stock’s beta above 2.7 underscores its volatility.

Broader market sentiment toward high-growth tech also matters. Geopolitical tensions, interest rate shifts or another AI-related rotation could pressure speculative names like IonQ.

Why Many Analysts Still Say Buy

Supporters argue IonQ is uniquely positioned. Its technology has demonstrated superior performance on key benchmarks, and the company is shipping systems and cloud access today while competitors remain further from commercialization. Government contracts, including recent DARPA awards, provide stable revenue and validation.

Longer-term forecasts are even more bullish. Some models see IonQ capturing a meaningful slice of a quantum market projected to reach tens of billions by the early 2030s. For patient investors with high risk tolerance, the current valuation may represent an entry point before the next leg of commercial scaling.

Recent sector catalysts — including Nvidia’s quantum-related AI announcements — have lifted the entire quantum basket, with IonQ often leading gains on positive news flow.

Investment Considerations for 2026

For growth-oriented portfolios, IonQ offers asymmetric upside if it executes on its roadmap and quantum advantage materializes in the coming years. Position sizing should remain modest given volatility and binary outcomes typical of frontier technology.

Conservative investors or those seeking near-term profitability may prefer to wait for clearer signals of sustained positive gross margins and consistent earnings beats. Dollar-cost averaging on dips could mitigate timing risk for believers in the long-term thesis.

Bottom Line

IonQ enters the heart of 2026 as a leader in a transformative but immature industry. Strong revenue momentum, technical progress and a rock-solid balance sheet support the bullish analyst consensus. Yet sky-high expectations, ongoing losses and execution challenges mean the stock will likely remain a roller-coaster ride.

Investors considering IonQ must weigh its enormous potential against substantial risks. For those with long time horizons and conviction in quantum’s future, the data leans toward buying on weakness. For others, it may be prudent to monitor from the sidelines until more commercial proof points emerge.

As quantum computing inches closer to practical utility, IonQ’s ability to convert its technology leadership into durable profits will ultimately decide whether today’s buyers become tomorrow’s winners.

Business

Trump administration ends lease for consumer protection bureau’s headquarters, records show

Trump administration ends lease for consumer protection bureau’s headquarters, records show

Nu Holdings: Not Waiting On The U.S. Market

USBC announces departure of Ronald P. Erickson and related compensation terms

Rachel Reeves touched down in Washington on Tuesday carrying an unwelcome piece of luggage: the International Monetary Fund’s verdict that Britain is the biggest economic casualty of the Iran war among the world’s wealthiest nations.

The Fund’s spring forecast, delivered as the Chancellor arrived for the IMF and World Bank meetings, trimmed 0.5 percentage points from the UK’s 2026 growth projection, the steepest cut handed to any G7 economy since its January outlook. Inflation is now expected to push towards 4 per cent, while unemployment is heading for its highest rate in more than a decade.

For the small and medium-sized businesses that power two-thirds of the UK’s private sector workforce, the numbers translate into a grim set of pressures: softer consumer demand, stubborn cost inflation and a Treasury with precious little headroom to soften the blow.

The UK entered the conflict already on the back foot. Growth was sluggish well before the first missiles flew, with firms and households hunkering down ahead of last autumn’s Budget amid a fog of tax speculation that dampened activity across the high street and the boardroom alike.

Pierre-Olivier Gourinchas, the IMF’s economic counsellor, pointed to what he called a “shadow effect” lingering from that weaker momentum, a drag the Fund believes will bleed into next year’s performance. It is a diagnosis the Chancellor firmly rejects, arguing that Labour inherited a damaged economy from the Conservatives and has since set firmer foundations. Yet the data is unsympathetic: British households were already wrestling with the G7’s highest inflation rate before a single Iranian oil facility was struck.

The deeper problem is energy. The Iran conflict has delivered the sharpest shock to global supplies since the oil crises of the 1970s, and Britain’s gas-heavy power mix leaves it unusually exposed. Although much of the country’s gas is produced domestically, imported cargoes are being bought at sharply elevated wholesale prices, and because gas sets the marginal price for UK electricity, the pain travels quickly from the terminal to the meter.

“There is more of a pass through, if you want, of gas prices into wholesale prices of energy,” Gourinchas observed, noting that household bills were being cushioned only temporarily by existing government measures.

Reeves has used her Washington platform to push for de-escalation while sharpening her criticism of Donald Trump’s decision to prosecute the war on Iran. The political calculus is plain enough. With the public finances squeezed by elevated debt and stubbornly high borrowing costs, her fiscal room for manoeuvre is wafer-thin, and Labour is trailing in the polls as it approaches a testing set of May local elections.

Treasury insiders expect short-term, narrowly targeted relief measures rather than a broad spending splurge, precisely the prescription the IMF itself has endorsed. Anything more expansive risks spooking the gilt market and undoing the hard-won credibility Reeves has spent the past year trying to bank.

For Britain’s business community, the more consequential question is what happens once the immediate crisis fades. Insulating the country against the next energy shock will demand a far more aggressive push into domestic renewable generation, grid reinforcement and the kind of supply-side reforms that unlock private investment at scale.

SME owners hoping for relief will be watching two pressure points closely: whether the promised targeted support reaches smaller firms exposed to soaring input costs, and whether the long-promised industrial strategy finally delivers the cheaper, home-grown power that British manufacturers have been demanding for the best part of a decade.

Reeves returns from Washington with the IMF’s blessing for her fiscal restraint, but also with its unvarnished warning that, on current trajectory, Britain will spend 2026 at the bottom of the G7 league table. For a Chancellor already short on political capital, that is a verdict she can ill afford to let stand.

Amy Ingham

Amy is a newly qualified journalist specialising in business journalism at Business Matters with responsibility for news content for what is now the UK’s largest print and online source of current business news.

Meta faces potential EU ban on WhatsApp AI policies

IRS CEO Frank Bisignano discusses a report regarding staffing, higher refunds and the Trump Accounts on Varney & Co.

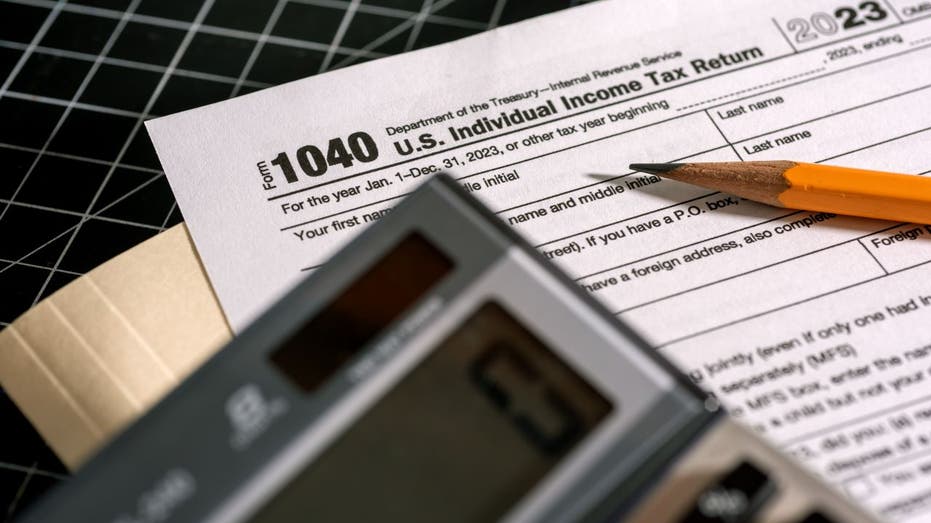

The tax filing deadline for 2025 tax returns is here, with taxpayers having until just before midnight on April 15 to file their returns or request an extension.

Last-minute tax filers racing against the clock to get their return filed ahead of the IRS deadline will want to be systematic in ensuring they have everything they need to file their return accurately when they get started, according to a tax expert.

“Gather all your documents in one place,” said Lisa Greene-Lewis, CPA and TurboTax expert, in an interview with FOX Business. “Documents that report your income like your W-2s, 1099s, and then don’t forget about any forms or receipts for anything that can be deductible.”

She noted that the process of gathering those documents may be more extensive than in years past due to changes from last year’s One Big Beautiful Bill Act, which created new provisions extending tax relief to income from tips, overtime and Social Security.

HOW TO FILE A TAX EXTENSION BEFORE THE APRIL 15 DEADLINE

Taxpayers can get refunds faster by e-filing their returns. (Timothy Fadek/Bloomberg via Getty Images)

Other provisions affected the child tax credit and created a deduction for auto loan interest on some new U.S.-made cars, while businesses are able to depreciate equipment for the year purchased instead of amortizing it over several years.

Taxpayers who anticipate getting a refund back from the IRS can get their refund the fastest by e-filing their return.

“Go online and e-file with direct deposit – that’s the fastest way to get your refund,” Greene-Lewis recommended. “If you mail your return, you don’t know when the IRS is going to get it. If you e-file, you get a message that they’ve accepted it.”

BEWARE OF THESE TAX SCAMS AS THE FILING DEADLINE APPROACHES, CONGRESS WARNS

Taxpayers who file a paper return and mail it on Wednesday should request a physical “round-date stamp” to ensure it’s postmarked in time. (Michael Bocchieri/Getty Images)

Greene-Lewis said that taxpayers who plan to mail their return should keep in mind that the U.S. Postal Service changed how it postmarks mail.

Starting in late December, USPS changed its rules to postmark parcels when processed at a facility, rather than when they’re dropped off at a post office, which can delay the postmark by 24 hours or more in some cases.

That means taxpayers who want to mail their return should either mail early, use certified mail or request a “round-date stamp” be applied manually when dropping it off at the retail counter.

IRS REFUND TRACKER EXPLAINED: WHAT YOU NEED TO KNOW BEFORE THIS YEAR’S TAX FILING DEADLINE

E-filing will allow taxpayers to have their returns processed more quickly, which means that any tax refund they are owed will hit their accounts via direct deposit sooner.

“The majority of people do get a refund, and we are seeing that refunds will be up this year,” Greene-Lewis said. “I would definitely try to make the deadline with all the deductions and credits available. Especially if you’re thinking you might owe, you may be able to get a refund.”

The IRS’ tax filing deadline is on April 15, just before midnight. (J. David Ake/Getty Images)

Taxpayers can request an extension to file their 2025 tax return through the IRS website and third-party tax preparation services, though they should be aware that if they owe the IRS money they will need to pay that amount or set up a payment plan by the deadline.

GET FOX BUSINESS ON THE GO BY CLICKING HERE

“One thing to remember is that it is an extension to file, and not an extension to pay. So you do need to try to pay what you owe by the deadline, even if you’re filing an extension,” Greene-Lewis added.

Adobe Is Working With Anthropic to Bring a Creative AI Agent to Claude

4-Hour War Countdown. Bitcoin Sphere Of Control

Martin Lewis reacts as ‘aggressive’ council tax rules end

-

Politics5 days ago

Politics5 days agoUS brings back mandatory military draft registration

-

Sports5 days ago

Sports5 days agoMan United discover Nico Schlotterbeck transfer fee as defender reaches Dortmund agreement

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Veronica Beard

-

Politics5 days ago

Politics5 days agoMalcolm In The Middle OG Turned Down ‘Buckets Of Money’ To Appear In Reboot

-

Politics3 days ago

Politics3 days agoWorld Cup exit makes Italy enter crisis mode

-

Crypto World6 days ago

Crypto World6 days agoCanary Capital Files SEC Registration for PEPE ETF

-

Business5 days ago

Business5 days agoTesla Model Y Tops China Auto Sales in March 2026 With 39,827 Registrations, Beating Cheaper EVs and Gas Cars

-

Crypto World2 days ago

Crypto World2 days agoThe SEC Conditionalises DeFi Platforms to Be Avoided for Broker Registration

-

Crypto World2 days ago

Crypto World2 days agoSEC Signals Exemption for Crypto Interfaces From Broker Registration

-

Crypto World7 days ago

Crypto World7 days agoBitcoin recovers as US and Iran Agree a Ceasefire Deal

-

News Videos6 hours ago

News Videos6 hours agoSecure crypto trading starts with an FIU-registered

-

NewsBeat3 days ago

NewsBeat3 days agoPep Guardiola and Gary Neville agree over Arsenal title problem that benefits Man City

-

Business5 days ago

Business5 days agoOpenAI Halts Stargate UK Data Centre Project Over Energy Costs and Copyright Row

-

Business4 days ago

Business4 days agoIreland Fuel Protests Enter Day 5 as Blockades Spark Shortages and Government Prepares Support Package

-

Politics5 days ago

Politics5 days agoLBC Presenter Mocks Trump Over Iran War Failures

-

Crypto World5 days ago

Crypto World5 days agoFederal judge blocks Arizona from bringing criminal charges against Kalshi

-

NewsBeat3 days ago

NewsBeat3 days agoJD Vance announces ‘no agreement’ with Iran over nuclear weapons fear

-

Tech6 days ago

Tech6 days agoA version of Windows 10 released a decade ago is now eligible for additional security patches

-

NewsBeat1 day ago

NewsBeat1 day agoTrump and Pope Leo: Behind their disagreement over Iran war

-

Crypto World1 day ago

Crypto World1 day agoSEC Proposes Certain Crypto Interfaces Don’t Need to Register as Brokers

You must be logged in to post a comment Login