Crypto World

Aave’s WETH unfreeze hands leverage to whales and illiquidity to everyone else

Spark’s MonetSupply says Aave’s decision to unfreeze its Core WETH market lets LST/LRT whales farm ~45% weETH loops while aEthWETH sits at 100% utilization, trapping regular users.

Summary

- Spark strategy director MonetSupply says Aave’s decision to unfreeze its Ethereum Core WETH market is “ill-considered” under current liquidity conditions.

- With aEthWETH utilization at 100%, he warns that high‑leverage weETH loops chasing ~45% APY will trap normal depositors and stablecoin borrowers trying to exit.

- The move, he argues, hands out arb opportunities without fixing aEthWETH liquidity, further degrading conditions for regular users already struggling to refinance.

Aave (AAVE) has decided to unfreeze its Ethereum Core WETH market just as liquidity is at its tightest, drawing sharp criticism from Spark’s strategy director MonetSupply. In a post on X, he called the move “quite ill‑considered,” arguing that under the current interest rate model, LST and LRT holders can spin up aggressive circular leverage loops using assets like weETH while ordinary users are effectively locked in.

High-octane loops on a dry WETH market

According to his calculations, traders can exploit roughly a 0.5% discount on weETH’s secondary‑market price relative to ETH and an Aave ETH borrowing rate capped around 5.15% to construct recursive long ETH positions with an annualized return profile near 45% when stacked on top of the base staking yield. With the aEthWETH market already sitting at 100% utilization, every fresh loop tightens the squeeze on exit liquidity for plain‑vanilla depositors and borrowers.

The problem, MonetSupply argues, is that unfreezing WETH under these conditions does nothing to relieve the liquidity stress facing aEthWETH users. “This decision provides arbitrage opportunities without addressing the liquidity tension of aEthWETH,” he wrote, warning that users trying to withdraw WETH or roll over leveraged stables are discovering there is simply no buffer left in the pool.

Recent comments from the Spark strategist on related ETH‑market fragilities flagged how similar dynamics can spiral: once utilization is pinned at 100%, suppliers lose incentives to stay, while borrowers lose room to deleverage, raising the risk of stuck positions and cascading liquidations if rates or collateral prices move against them. Combined with post‑Kelp DAO nerves and elevated demand for on‑chain ETH liquidity, Aave’s decision to reopen the throttle on WETH looks, in his view, less like restoring normalcy and more like inviting sophisticated loopers to farm a basis trade atop an already strained market.

If those incentives persist, the likely outcome is a familiar split: whales and structured funds capturing leveraged carry via weETH loops, while retail depositors and stablecoin borrowers face rising odds of being trapped in a market where the exit door is technically open—but functionally blocked by 100% utilization.

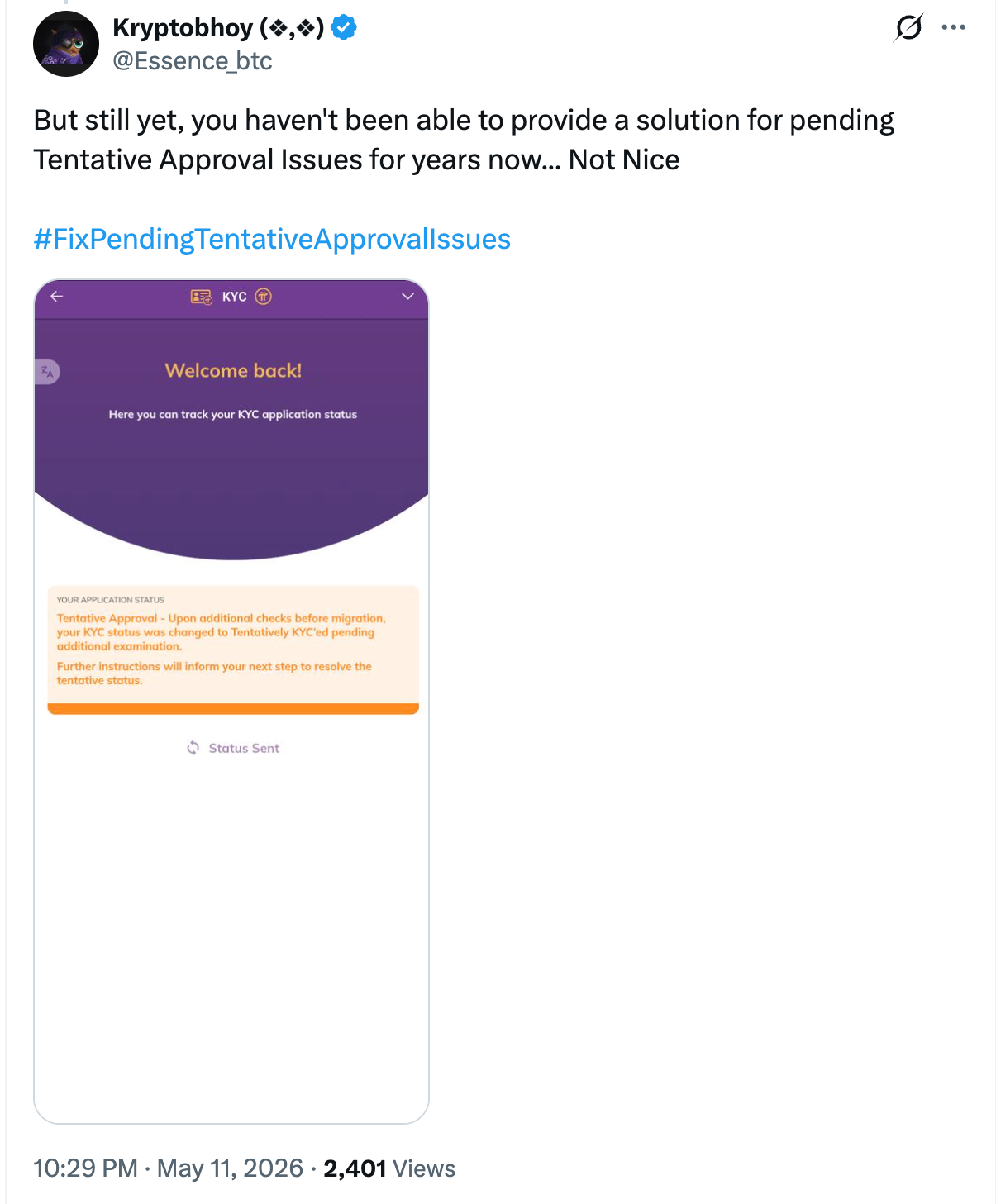

Pi Network’s April 2026 progress update revealed that the network has now surpassed 18.1 million fully verified users and completed over 16.72 million mainnet migrations.

According to the update, April alone saw more than 100,000 KYC approvals and 30,000 mainnet migrations.

Follow us on X to get the latest news as it happens

Pi Network’s KYC Update Triggers Pioneer Backlash

The latest figures come after the Pi Core Team explained that its in-app Know Your Customer (KYC) system combines human reviewers with AI-powered fraud detection.

The network stated that over 1 million individuals have collectively processed around 526 million verification tasks, helping confirm nearly 18 million unique identities.

Each application reportedly undergoes roughly 30 separate verification checks before approval, in an effort to reduce the number of duplicate or fraudulent accounts.

Nonetheless, Pioneers flooded the announcement with complaints. Commenters said tentative approvals had remained pending for extended periods.

“The @PiCoreTeam promised a decentralized revolution, but for millions of Pioneers, the only thing ‘decentralized’ is the hope of passing KYC. It’s been 7 years down the line with no hope in sight,” one user wrote.

Pi Core Team Responds to Pioneer Concerns on KYC

Nonetheless, the Pi Core Team told BeInCrypto that Pi’s KYC review process is intentionally conservative. The team said effective KYC should not allow every account to pass easily, which is exactly the intent of running a strong KYC process in the first place.

They added that if applications were approved without sufficient verification, it would:

• Duplicate accounts could migrate to Mainnet, harming the ecosystem

• Rewards and participation would become distorted, creating unfairness

• Applications and services would not be able to rely on user authenticity, diluting this Pi resource.

“Maintaining a verified, one-person-per-account structure ensures that Pi Network remains fair, secure, and usable. Since Pi rolled out a system process upgrade in October 2025, more than 3.36 million Pioneers have moved from Tentative to fully approved KYC,” the team said.

The team mentioned that resolving user concerns remains “a priority.” The outlined three steps that Pioneers who remain in Tentative status can take:

• Complete any available liveness checks in the Pi app

• Ensure all submitted information is accurate and clear

• Continue actively mining, which may trigger the system process checks

Pi explained that stuck Pioneers fall into different corner cases, each requiring a custom technical fix before that group can be unblocked.

“Overall, having a ‘Tentative KYC’ status does not mean rejection. It means additional verification is required before final approval. The Tentative KYC status helps ensure the integrity of the network by cautiously allowing as many real human Pioneers as possible to pass KYC, while catching and preventing as many fake and bot accounts as possible,” PCT told BeInCrypto.

Pi Coin (PI) Faces Headwinds in May

Meanwhile, amid growing user complaints, Pi Network is also facing pressure on the price front. While many altcoins have rallied with double digits in May, Pi Coin has lagged.

Its price has declined 2.6% so far this month. PI traded at $0.17 at press time, up 1.3% over the past day.

Still, a potential catalyst sits days away. Pi Network has set May 15 as the deadline for mainnet nodes to complete the Protocol 23 upgrade. Previously, Protocol 22 lifted PI nearly 9% before the rally faded.

Whether Protocol 23 produces durable price action remains to be seen. About 174.2 million PI tokens will enter circulation over the next 30 days, which could weigh on any rally.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Pi Network Shares KYC Update But Community Backlash Floods In appeared first on BeInCrypto.

Crypto World

Trump Just Flew to China With Elon Musk, Larry Fink, and Jensen Huang: Is a Trade Deal News About to Send Bitcoin to $90,000?

Bitcoin price climbed to a 24-hour high of $81,000 as Trump-China trade news pushed BTC toward its most structurally significant resistance in months.

The question now is whether the geopolitical narrative has enough legs to carry BTC through $90,000, or whether the move is front-running an outcome that hasn’t materialized yet.

What Is the Trump-China Trade Driving Bitcoin Toward $90k?

President Donald Trump’s state visit to China, the first U.S. presidential trip to the country in nearly a decade, landed with immediate market impact.

Trump boarded Air Force One with a delegation of over a dozen U.S. executives, including Tesla’s Elon Musk, Apple’s Tim Cook, BlackRock’s Larry Fink, and, confirmed as a last-minute addition on May 13, Nvidia CEO Jensen Huang.

Markets are pricing in a specific scenario: a framework agreement between Trump and Xi Jinping that eases tariffs on semiconductors and electronics, tariffs that peaked at 60% on Chinese goods in late 2025, alongside potential deals on rare earths and aviation.

US Treasury Secretary Scott Bessent began preparatory talks with Chinese officials in South Korea ahead of the summit, with meetings scheduled with Chinese Vice Premier He Lifeng on Wednesday. Successful outcomes could stabilize global supply chains and directly reduce one of the key macro headwinds suppressing risk appetite.

Bitwise strategist Juan Leon framed the stakes precisely, stating that “reduced tariff risks could unlock $1 trillion in sidelined capital for crypto.”

Near-term, if the Trump-Xi summit produces even a preliminary trade framework by May 15, Bitcoin’s path to $88,000–$90,000 opens quickly.

If talks stall, the unwinding of the Trump trade could be sharp. BTC already dipped to $79,832 when US CPI came in hot at 3.8%, demonstrating how quickly macro data can cut through geopolitical optimism

Can Bitcoin (BTC) Break $90,000 Upon the News?

Bitcoin price is trading above $81,000 after printing a session high of $81,248, recovering from a $79,832 low set earlier when CPI data disappointed.

The first meaningful resistance cluster sits at $82,500 to $83,500, a zone that has capped multiple recovery attempts over the past 2 weeks.

Above that, $88,000 to $90,000 is the decisive range. The 200-day SMA sits in that vicinity, and $90,000 has become a magnet for stop orders and institutional limit sells.

Clearing $90,000 on above-average volume opens the door to $93,000 to $95,000, the range where BTC traded post-election in November 2024. The SMA-50 at $84,500 needs to flip to support before a clean $90,000 test becomes structurally sound rather than just a spike.

On the downside, $79,500 to $80,000 is the line that must hold. A daily close below $79,500 breaks the current higher-low structure and reopens the $75,000 to $76,000 support band.

The bull structure is intact above $80,000, but not yet confirmed as a trend resumption. That confirmation requires a clean close above $84,500.

2 external variables are in play this week. Kevin Warsh’s expected confirmation as Fed Chair and the CLARITY Act markup are scheduled for Thursday. Both are net positive for BTC if they land clean. Both could introduce volatility that resets the setup if they do not.

The chart needs a daily close above $84,500. Everything else is noise until that print.

The post Trump Just Flew to China With Elon Musk, Larry Fink, and Jensen Huang: Is a Trade Deal News About to Send Bitcoin to $90,000? appeared first on Cryptonews.

The Ethereum Foundation unveiled Clear Signing, an open standard that makes transaction approvals human-readable. The release targets blind signing, a flaw the foundation said has fueled billions in user losses.

Built around ERC-7730, the framework lets wallets display plain-language descriptions of each transaction before users approve it. The Ethereum Foundation’s One Trillion Dollar Security Initiative will steward the underlying infrastructure as a credibly neutral host.

Why Blind Signing Has Become a Costly Default

In many crypto exploits, the final step is not a software bug but a user approving a transaction. The Foundation’s announcement framed that approval gap as the core problem. Even after phishing or infrastructure compromise begins a breach, the last action typically falls to the wallet holder. Clear Signing aims to make that defense hold.

Approvals today often appear in low-level machine code that requires technical expertise to interpret. Some users rely on a separate device to double-check transaction details when the application could be compromised. The foundation cited the Bybit incident among recent cases where signed transactions drained user wallets.

How Clear Signing Works

ERC-7730 introduces a shared format that turns transaction data into clear, human-readable descriptions. Instead of being stored on-chain, these descriptions are kept in a decentralized off-chain registry and distributed to wallets.

Another standard, ERC-8176, allows independent auditors to verify and cryptographically confirm that these descriptions are accurate. Based on these verifications, wallets can decide which sources they trust.

Because the system works off-chain, existing apps don’t need to change their smart contracts to support Clear Signing. The Ethereum Foundation says this approach fits into its broader plan to improve privacy and security across the network.

Wallet providers will ultimately choose which descriptor sources to display, relying on reputation and audit attestations.

Multi-Party Push as Institutions Expand Ethereum Exposure

Ledger originated ERC-7730. The working group now spans MetaMask, Trezor, Fireblocks, WalletConnect, Cyfrin, Sourcify, and Zama, alongside independent contributors. Rust and TypeScript libraries funded by the 1TS program are hosted on clearsigning.org.

The release lands as institutions expand their Ethereum footprint, including JPMorgan’s recent launch of JLTXX, a tokenized treasury product. Vitalik Buterin has previously flagged transaction transparency as a critical blind spot for the network’s next phase of adoption.

Developers said the project remains active. Contributors are expanding wallet compatibility, audit tooling, and adoption across decentralized applications. Whether issuers, custodians, and wallet vendors converge on shared descriptors will determine how quickly Clear Signing becomes the default across DeFi and institutional flows.

The post Ethereum Foundation Launches Clear Signing Standard to End Blind Wallet Approvals appeared first on BeInCrypto.

Key Highlights

- Sixt SE delivered Q1 pre-tax earnings of €2.1 million, significantly outperforming consensus forecasts of a €1.5 million loss

- Quarterly revenue reached €928.9 million, representing a 12.6% increase on a currency-adjusted basis and surpassing the €911 million estimate

- Corporate EBITDA surged 40.2% compared to the prior year, reaching €67.7 million

- The company returned to profitability with net income of €1.5 million, a sharp contrast to the €12.6 million loss recorded in Q1 2025

- Management reaffirmed 2026 full-year targets: €4.45–€4.60 billion in revenue with approximately 10% pre-tax profit margin

Shares of Sixt SE (ETR: SIXG) rallied 4.93% during Wednesday trading after the German mobility services provider delivered first-quarter financial results that exceeded market expectations on multiple fronts.

The company reported pre-tax earnings of €2.1 million for the first quarter. This marked a significant outperformance versus the consensus forecast, which had called for a €1.5 million loss, and represented a dramatic improvement from the €17.6 million loss recorded in the corresponding quarter of the previous year.

Quarterly revenue totaled €928.9 million, climbing 12.6% on a currency-adjusted basis and exceeding analyst projections of €911 million.

Net income turned positive at €1.5 million, reversing from a €12.6 million deficit in Q1 2025. This improvement highlights the company’s enhanced operational efficiency and more strategic fleet utilization.

Corporate EBITDA climbed 40.2% year-over-year to €67.7 million, also beating analyst forecasts. The company’s fleet expanded 8.4% to 182,900 vehicles, not including franchise partner operations.

Co-CEO Alexander Sixt attributed the performance to disciplined execution: “a tight, demand-oriented fleet, sustained strong investments in premium vehicles, brand, network, and above all technology.”

Performance Across Key Markets

European markets outside Germany delivered the most robust growth, with revenue climbing 16.2% to €344.7 million. The German domestic market posted solid gains as well, with revenue increasing 11.5% to €271.2 million.

Revenue from North America declined 1.9% to €310.3 million, though this decrease was primarily attributable to currency translation effects. According to Jefferies analysis, the region actually expanded 9.2% on an organic constant-currency basis.

While the foreign exchange headwind in North America warrants monitoring, the fundamental demand trends in the region remain positive.

2026 Outlook Maintained

Sixt retained its full-year 2026 financial guidance without modification. Management continues to project revenue in the range of €4.45 billion to €4.60 billion, accompanied by a pre-tax profit margin “in the area” of 10%.

The midpoint of this revenue guidance stands at €4.525 billion, closely aligned with the €4.54 billion consensus estimate. The implied pre-tax earnings of approximately €453 million exceed the consensus forecast of €446.9 million.

CFO Franz Weinberger emphasized the company’s confidence in maintaining its targets “despite increased geopolitical and macroeconomic uncertainty.”

The first-quarter performance represents a complete turnaround from the losses sustained twelve months earlier. With guidance unchanged and demand remaining resilient across most major markets, these results provide investors with greater visibility as Sixt approaches the peak summer travel period.

Senate Banking Committee members have reportedly filed more than 100 amendments to the CLARITY Act, with Senator Elizabeth Warren alone submitting over 40 proposals ahead of Thursday’s markup vote.

The flood of filings follows the committee’s release of a 309-page draft on Tuesday, expanded from January’s 278-page version.

Warren Files 40+ Amendments as Senate Preps Crypto Bill Markup

According to POLITICO, the list features dozens of amendments put forward by Democrats on the Banking Committee, along with a handful of revisions from the bill’s Republican sponsors.

Follow us on X to get the latest news as it happens

Crypto In America host Eleanor Terrett reported that one of Senator Warren’s amendments would block the Federal Reserve from granting master accounts to crypto companies.

Senator Jack Reed’s amendment “prohibits crypto from being used as legal tender, for example, to pay taxes.”

Committee members filed 137 amendments before the planned markup in January. The current tally signals continued resistance as the bill nears a committee vote.

Meanwhile, the American Bankers Association has sent more than 8,000 letters to Senate offices since last Friday, according to a source cited by Terrett. The campaign focuses on the stablecoin yield compromise brokered by Senators Thom Tillis and Angela Alsobrooks.

The Banking Committee will meet on Thursday morning in Washington to vote on the bill.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post CLARITY Act Hit With 100+ Amendments Ahead of Senate Banking Markup appeared first on BeInCrypto.

Key Takeaways

- SoftBank’s fourth-quarter net income reached $11.6 billion, representing a three-fold increase year-over-year

- A $45 billion valuation increase in its OpenAI holdings fueled the profit surge

- The company’s OpenAI stake was valued at $79.6 billion at the end of March

- Total OpenAI investment stands at $34.6 billion, with commitments exceeding $60 billion

- S&P Global Ratings downgraded SoftBank’s outlook to “negative” citing debt levels and portfolio concentration risks

SoftBank Group announced net income of 1.83 trillion yen (approximately $11.6 billion) for the quarter that concluded on March 31, 2026. This figure represents a substantial increase compared to the 517 billion yen profit recorded during the corresponding quarter of the previous year.

The performance significantly exceeded Wall Street expectations, with analysts having projected earnings of 295.2 billion yen, based on Bloomberg’s consensus estimates.

The dramatic earnings increase was primarily attributed to a 3.043 trillion yen investment gain recorded during the quarter. The majority of these gains originated from the Vision Fund, SoftBank’s primary investment arm.

The standout performer in the portfolio was OpenAI, the artificial intelligence company responsible for developing ChatGPT. As of March 31, SoftBank’s ownership position in OpenAI reached a valuation of $79.6 billion, marking a cumulative gain of $45 billion on the investment.

To date, SoftBank has deployed $34.6 billion into OpenAI. The Japanese conglomerate has pledged to invest over $60 billion in aggregate, which would secure approximately 13% equity ownership in the AI pioneer.

During February, OpenAI completed a funding round that assigned the company an $890 billion valuation. A subsequent financing round in March, which SoftBank co-led, valued the startup at $852 billion.

The Vision Fund alone recorded gains of approximately $20 billion during the three-month period from January through March, with OpenAI accounting for nearly the entire amount.

Significant Losses Beyond OpenAI Holdings

However, SoftBank’s investment portfolio showed mixed results elsewhere. The company experienced losses across multiple other holdings, including positions in Coupang, DiDi Global, and Klarna.

When excluding Vision Fund performance and accounting for currency fluctuations and operational expenses, SoftBank recorded an investment income deficit of 472.1 billion yen for the complete fiscal year.

Financing expenses during the fourth quarter climbed to 229.4 billion yen, compared with 148.9 billion yen in the prior-year period, demonstrating the increased borrowing costs associated with financing its artificial intelligence investments.

The company maintains $17.5 billion in outstanding obligations from a $40 billion bridge financing facility utilized to fund its OpenAI investment.

Credit Rating Concerns Intensify

To finance its aggressive OpenAI investment strategy, SoftBank has been divesting stakes in portfolio companies. The firm liquidated positions in Nvidia and T-Mobile, generating proceeds of 218.1 billion yen from these asset sales throughout the fiscal year.

S&P Global Ratings adjusted its outlook on SoftBank from “stable” to “negative” in March. The ratings agency expressed concerns that SoftBank’s asset quality and financial flexibility would likely decline due to its substantial OpenAI capital commitment.

According to S&P, SoftBank could mitigate these risks through additional asset monetization.

For the complete fiscal year, SoftBank reported net income of 5 trillion yen. Both the Vision Fund and its telecommunications business segment served as primary profit contributors.

Chief Executive Officer Masayoshi Son has positioned artificial intelligence as the central pillar of SoftBank’s long-term strategic vision. OpenAI continues to face intensifying competition from technology giants including Google and emerging players like Anthropic.

TLDR:

- Compound governance approved an oracle tweak that enabled liquidation of stolen rsETH collateral.

- The attacker used 116,500 rsETH as collateral to borrow ETH and wstETH across Compound v3.

- DeFi United seized nearly $30M after temporary oracle bounds forced undercollateralization.

- The recovered rsETH was redeemed into ETH to help restore KelpDAO’s damaged bridge reserves.

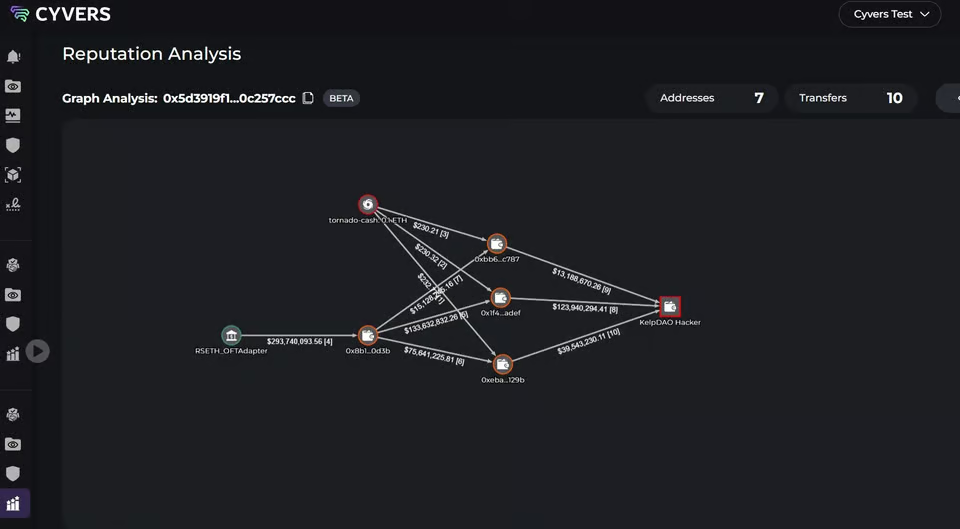

DeFi governance proved capable of acting as an emergency recovery mechanism after the April 2026 KelpDAO exploit. Roughly 116,500 rsETH worth $292 million were stolen and deployed as collateral on Compound v3.

Standard liquidation rules offered no path to recovery, since the stolen rsETH still priced normally. A governance-approved oracle adjustment changed that, eventually enabling DeFi United to seize roughly $30 million. The recovery marked one of the most coordinated on-chain interventions in DeFi’s history.

Why Standard Liquidation Rules Could Not Touch the Attacker’s Position

On April 18, 2026, attackers exploited a vulnerability in KelpDAO’s LayerZero bridge infrastructure. About 116,500 rsETH worth $292 million were released illegitimately from the Ethereum-side escrow.

The attack was widely attributed to North Korea’s Lazarus Group. Rather than selling, the attacker deployed them as collateral across multiple lending protocols.

On-chain data shows the attacker opened a Compound v3 position within minutes of the exploit. ETH and wstETH were borrowed in tranches against the stolen rsETH tokens.

Partial withdrawals helped manage the collateral ratio in the same window. The position was active and borrowing real assets before the protocol could respond.

In the weeks that followed, the position remained technically healthy at market prices. Compound’s rsETH markets were frozen, and loan-to-value ratios were set to zero.

The stolen rsETH still priced normally despite having no legitimate backing. Automated liquidation mechanisms therefore had no grounds to trigger.

DeFi lending liquidations depend on collateral value falling below set thresholds. Because rsETH had not dropped in price, the attacker’s position stayed above water.

There was no admin key or circuit breaker available to freeze the account. DeFi governance was therefore the only available instrument to act.

How a Governance Proposal Triggered Liquidation and Recovered the Collateral

The Compound Foundation engaged risk partners, including Gauntlet, to find a resolution pathway. Gauntlet submitted a proposal for a modified oracle for Compound’s rsETH markets.

The new oracle kept the Kelp DAO exchange rate feed as its primary source. It also added configurable price bounds operable by the Compound multisig.

Santiment Intelligence noted that an oracle adjustment pushed the attacker’s position into liquidation. This allowed DeFi United to seize roughly $30 million in collateral.

Temporarily setting the price floor below market value triggered undercollateralization. A DeFi United Recovery Guardian multisig then repaid the borrowed assets and seized the collateral.

Santiment data recorded $29,044,839 in Compound v3 liquidations on May 9th at 02:30 UTC. The event covered 12,426.70 rsETH at a price of $2,337.29 per token.

Notably, rsETH showed no meaningful price distress during the event. The collateral was removed cleanly without triggering a broader market selloff.

The seized collateral was redeemed through KelpDAO’s system and converted back to ETH. Those funds helped refill the damaged bridge lockbox that backed rsETH.

After completion, the oracle was restored to normal market levels. No persistent changes were made to the Compound protocol.

Members of the US Senate Banking Committee have filed more than 100 amendments to a crypto market structure bill set for markup on Thursday, with the proposed changes mostly related to stablecoins, software developers and ethics.

According to a list obtained by Politico, Democratic senators have proposed dozens of changes, while Republicans are seeking slight adjustments to the bill.

It is not clear what the specific details of each amendment are, but some concern issues the committee has been seeking to solve for months, including stablecoin yield, crypto software developer protections and ethics provisions.

The list offers insight into the issues the committee will likely debate at the bill’s markup on Thursday as it seeks to advance the measure to the Senate floor. The Senate Banking Committee indefinitely delayed a previous markup in January after major crypto lobbyist Coinbase withdrew support for the bill.

The legislation aims to divide how US market regulators oversee crypto, with the House passing a version of it in July called the CLARITY Act. Crypto and banking lobbyists, along with lawmakers, have fought over provisions on stablecoins and whether government officials should be barred from involvement in crypto.

Further restrictions on offering stablecoin yields have been the bill’s most contentious provision, with banking and crypto lobbyists failing to reach an agreement after months of negotiations.

A version of the bill released on Monday banned third-party platforms like crypto exchanges from offering yield on stablecoins in a way that is “functionally equivalent” to the payment of interest on an interest-bearing bank deposit.

The list shows Democratic Senators Jack Reed and Tina Smith introducing an amendment to “strengthen [the] prohibition on interest/yield by using a ‘substantially similar’ test rather than an ‘equivalence’ test.”

An excerpt of the leaked list showing amendments for debate by Senator Jack Reed, with one supported by Senator Tina Smith. Source: Politico

Another planned amendment from Democratic Senator Chris Van Hollen pitches an ethics provision that Democrats and some Republicans have supported, which would bar the president, vice president, senior officials, members of Congress and their families from owning, promoting or being affiliated with crypto.

Related: Seven Democrats seen as ‘key’ to advancing CLARITY Act: Galaxy

Democratic Senator Catherine Cortez Masto also plans an amendment protecting software developers by “creating a safe harbor from criminal liability for not registering as a money transmitter,” a provision that is supported by many crypto groups.

Other amendments concern sanctions, institutions engaging in crypto, and one from Democratic Senator Andy Kim that seeks to reestablish the Justice Department’s National Cryptocurrency Enforcement Team, which the department dismantled in April last year.

Republicans have a majority on the Banking Committee and in the Senate, but some party members, such as Senator Thom Tillis, have said they won’t support the bill without certain provisions.

Republicans also control the Senate, but will need some Democrats onside to pass it with a three-fifths majority to end any potential debate on the bill.

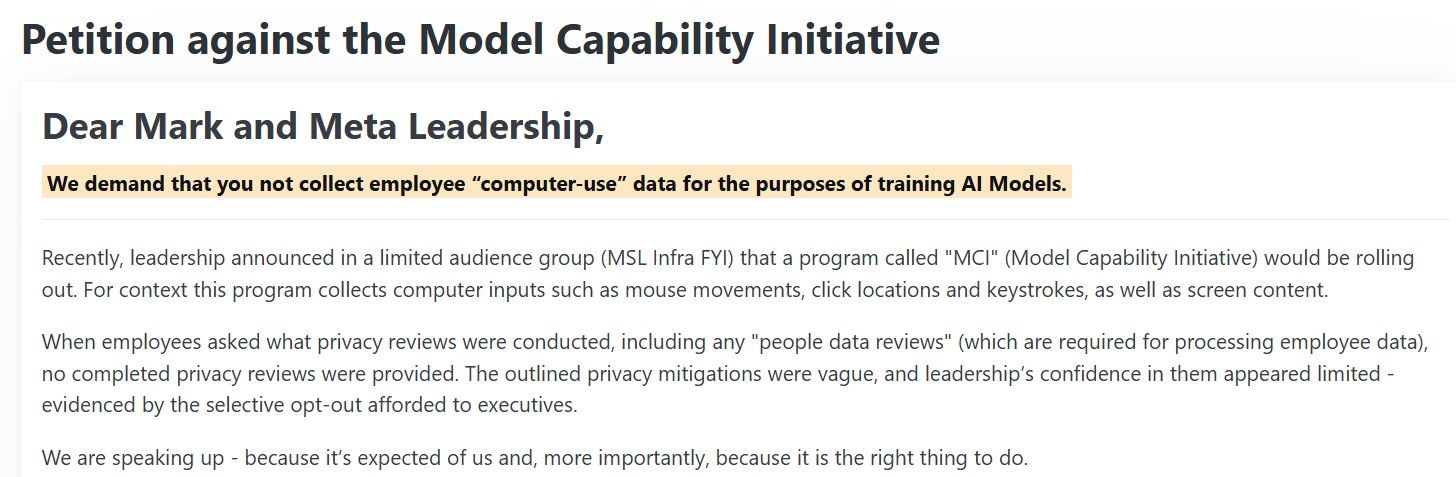

Meta employees at multiple U.S. offices distributed protest flyers. The action targets an internal tool that records mouse movements and keystrokes to train Meta’s AI models.

The flyers appeared in meeting rooms, on vending machines, and atop toilet paper dispensers. They direct staff to a petition demanding Meta withdraw the tool, called the Model Capability Initiative.

Mouse-Tracking Tool Collects Data Across Hundreds of Sites

Meta installed the Model Capability Initiative on U.S. employees’ work computers. The software captures clicks, keystrokes, and periodic screenshots. It runs across hundreds of applications, including Google, LinkedIn, and Wikipedia.

Meta says the data trains AI agents to mimic real human behavior on the web. According to a spokesperson, the models need real examples of how people use software. The company cited button clicks and dropdown menus as key inputs.

Several Meta employees called the program “dystopian” in interviews last month. Workers fear the tool could expose passwords and unreleased product details. They also flagged concerns about personal information, including immigration status, health records, and family details.

Petition Lands Days Before 8,000-Job Layoff

The petition builds on internal opposition that has grown since the April rollout. The flyer campaign on May 12 marked the first coordinated public action by U.S. staff against the program.

Pressure on Meta’s workforce is compounding. Chief people officer Janelle Gale said in late April that the company will cut 8,000 roles on May 20. The move is part of an efficiency drive tied to AI spending. Another 6,000 open positions will go unfilled.

Across the Atlantic, Meta employees in the United Kingdom announced a separate organizing effort this week. They are partnering with the United Tech and Allied Workers union.

Privacy Trade-Off Sits at AI Training Frontier

Meta says safeguards prevent the capture of certain sensitive content. However, it has not detailed the technical scope of those filters. Affected employees argue that consent terms are coercive, given the impending layoffs.

The dispute highlights a wider problem for large AI developers. Quality human behavioral data is increasingly scarce, and companies are turning to their own workforces to fill the gap.

Whether the May 12 protest pressures Meta to alter the program remains unclear. The outcome may signal how much leverage employees retain in an AI-driven cost-cutting cycle.

The post Meta Employees Protest Mouse-Tracking Tool Built to Train AI Models appeared first on BeInCrypto.

Ethereum liquid restaking platform Kelp and decentralized lending protocol Aave have completed a series of steps to restore rsETH backing, including burning the exploiter’s rsETH tokens.

Kelp DAO detailed a post-exploit recovery for its liquid staking token rsETH on Tuesday, confirming that the hacker’s tokens were burned on the layer-2 Arbitrum network.

The 117,132 rsETH — worth about $278 million at current prices — will be progressively restored over two weeks using funds from the Aave Recovery Guardian multisignature wallet, which is controlled by the DeFi United recovery group and Kelp’s own recovery safe.

The funds will be routed through the LayerZero OFT adapter, the smart contract responsible for locking, minting, burning and releasing rsETH during cross-chain transfers.

Kelp DAO confirmed that rsETH on mainnet and layer-2 networks, which has a market capitalization of $1.5 billion, remains fully backed at all times.

The move to recover the liquid staking tokens will bring users impacted by one of this year’s largest DeFi exploits one step closer to recovery.

Kelp was hacked in April when attackers widely attributed to North Korea’s Lazarus Group exploited its rsETH adapter bridge contract, the software that manages the platform’s liquid restaking token, and drained about $293 million.

Blockchain security firm OpenZeppelin reported at the time that no smart contract bug had been publicly identified, adding that “the system failed operationally,” and this is a category of risk the DeFi industry has “consistently underweighted.”

Tracking the exploited funds. Source: Cyvers

Withdrawals will resume within 24 hours

Kelp said it will unpause withdrawals, “tentatively within 24 hours,” after the first tranche is returned to the smart contract. All rsETH operations, including deposits, redemptions, bridging and claims, will resume as usual after the contracts are reactivated.

The protocol has also completed a “security hardening pass,” and bridging security now requires four independent attestors and 64 block confirmations, while it has deprecated some layer-2 routes.

Related: At least a dozen crypto entities attacked since Drift Protocol hack

It is also in the process of migrating to Chainlink’s Cross-Chain Interoperability Protocol (CCIP) for “further strengthened cross-chain bridging.”

Derivatives traders undeterred by DeFi hacks

Kelp is a prominent liquid restaking protocol on Ethereum, primarily built on top of EigenLayer, where users deposit ETH or other supported liquid staking tokens for additional yields.

The protocol’s total value locked hit an all-time high of just over $2 billion in September 2025 but has since declined by about 26% to $1.55 billion, according to DefiLlama.

Cointelegraph reported this week that ETH derivatives traders have largely remained unfazed by the recent wave of DeFi exploits, with professional sentiment holding steady despite elevated security concerns.

Magazine: DeFi’s billion-dollar secret: The insiders responsible for hacks

Disney’s $1 Billion Sci-Fi Sequel Officially Becomes New Late-Night Watch

Buttigieg picks sides in Iowa

iPhone & Android interoperability enhancements highlighted at Google I/O preshow

Manchester United reach agreement with Casemiro over contract clause amid transfer speculation

US brings back mandatory military draft registration

Steven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Crypto World5 days ago

Crypto World5 days agoHarrisX Poll Found 52% of Registered Voters Support the CLARITY Act

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Marianne Dress

-

Crypto World6 days ago

Crypto World6 days agoUpbit adds B3 Korean won pair as Base token gains Korea access

-

NewsBeat6 days ago

NewsBeat6 days agoNCP car park operator enters administration putting 340 UK sites at risk of closure

-

Fashion2 days ago

Fashion2 days agoCoffee Break: Travel Steam Iron

-

Fashion2 days ago

Fashion2 days agoWhat to Know Before Buying a Curling Wand or Curling Iron

-

Tech3 days ago

Tech3 days agoAuto Enthusiast Carves Functional Two-Stroke Engine from Solid Metal

-

Politics1 day ago

Politics1 day agoWhat to expect when you’re expecting a budget

-

Business4 days ago

Business4 days agoIgnore market noise, India’s long-term story intact, say D-Street bulls Ramesh Damani and Sunil Singhania

-

Politics4 days ago

Politics4 days agoPolitics Home Article | Starmer Enters The Danger Zone

-

Crypto World7 days ago

Crypto World7 days agoBlackRock CEO Larry Fink Discusses a New Asset Class

-

Tech2 days ago

Tech2 days agoGM Agrees To Pay $12.75 Million To Settle California Lawsuit Over Misuse Of Customers’ Driving Data

-

Sports7 days ago

Sports7 days agoNBA playoff winners and losers: Austin Reaves is not loving Lakers vs. Thunder matchup, but Chet Holmgren is

-

Entertainment6 days ago

Entertainment6 days agoSarah Paulson Called Out For Met Gala ‘Hypocrisy’

-

Entertainment6 days ago

Entertainment6 days agoGeneral Hospital: Ric & Ava Bombshell – Ric’s Massive Secret Exposed!

-

Politics6 days ago

Politics6 days agoSimon Cowell Says He Was ‘Horrible’ To Susan Boyle During BGT Audition

-

Crypto World6 days ago

Crypto World6 days agoRobinhood says Wall Street is building onchain

-

Sports6 days ago

Sports6 days agoUEFA Champions League final schedule, teams, venue, live time and streaming | Football News

-

Entertainment7 days ago

Entertainment7 days agoBold and Beautiful Early Spoilers May 11-15: Steffy Revolted & Liam Overjoyed!

-

Entertainment6 days ago

Entertainment6 days agoWhy David Letterman Called CBS ‘Lying Weasels’

You must be logged in to post a comment Login