Crypto World

Analyst Sees Upside for ETH Ahead of Glamsterdam Upgrade

Ethereum (ETH) is trading at nearly 65% below its all-time high, with attention around the asset at an almost yearly low, even as its largest network upgrade since The Merge is due within weeks.

But an analyst tracking the setup says the gap between weak social interest and steady on-chain usage is the kind of divergence that has often come right before sharp moves for the cryptocurrency.

Glamsterdam Approaches as On-Chain Data Stays Firm

In a July 9 post on X, pseudonymous analyst Wise Crypto noted that the Ethereum network has been processing roughly 450,000 active addresses despite social media discussion sitting near yearly lows.

According to them, the upcoming Glamsterdam upgrade could become a major catalyst, considering that it could increase Ethereum’s gas limit by three times and cut transaction fees by about 78%. It has also been said that it could lift throughput to about 10,000 transactions per second.

“Major catalyst. Minimal attention,” the market watcher wrote, while naming $1,754 as the ETH level worth watching. A sustained move above that area, according to them, could open the way toward $2,440, while failure to hold support could send the world’s second-largest crypto asset back toward $880.

Looking at CoinGecko data at the time of writing, ETH was trading just a few dollars below Wise Crypto’s stated resistance level, having dipped slightly (about 1%) in 24 hours but still gaining nearly 7% during the past week and about 3% over 30 days.

That quiet backdrop is sitting alongside some unusual exchange data shared by CryptoQuant contributor Amr Taha, who said that Binance’s 30-day ETH open interest change fell to -594,000 ETH earlier in the week, marking its deepest contraction since August 2024. Around the same time, ETH spot volume on OKX climbed to $2.09 billion, 49% higher than its best reading of the year, which was recorded on February 5.

According to Taha, the pairing is notable because a leverage flush alongside rising spot volumes probably means that speculators are leaving the market while spot buyers are continuing to stack ETH and not that there’s a broad retreat from the asset.

Executives Talk Up the Cycle While Traders Stay Cautious

Ethereum has been rejected at $1,800 three times this week, but that didn’t stop Consensys co-founder Joseph Lubin from saying Wednesday that the “Summer of Ethereum Love is gaining steam,” pointing to newly launched steward groups like Ethlabs working alongside the Ethereum Foundation, and citing the network’s eleven years of uptime as a draw for institutions.

Analyst Michaël van de Poppe struck a similar tone over the weekend, arguing that “the worst period for ETH is over” after the token closed out its third straight quarterly loss of more than 20%, a first in its history. He called the odds of a fourth consecutive drop statistically low and pointed to the pending CLARITY Act as a potential liquidity driver.

The post Analyst Sees Upside for ETH Ahead of Glamsterdam Upgrade appeared first on CryptoPotato.

Strategy has increased its US dollar reserve and expanded its preferred-stock repurchases. The otherwise Bitcoin-focused company is moving to strengthen its balance sheet.

The firm added $250 million to its cash reserve, bringing the total to $4 billion. It also repurchased approximately $81 million worth of its Variable Rate Series A Perpetual Stretch Preferred Stock (STRC).

Strategy increased its USD Reserve by $250M and repurchased $81M of $STRC. This increased USD Duration by 57 days to 2.3 years and tightened STRC’s BTC Credit by 5 bps. As of 8/2/26, we hold ₿842,138 in our BTC Reserve and $4.0B in our USD Reserve. $MSTR https://t.co/t7bGZJ8Q3o

— Michael Saylor (@saylor) August 3, 2026

The transaction builds on the firm’s recently introduced Digital Credit Capital Framework. The company intends to use its dollar reserve primarily to cover preferred-stock dividends and debt interest, reducing the need to sell Bitcoin during periods of market stress.

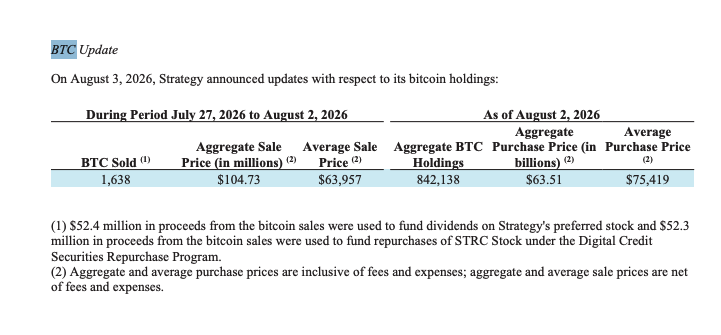

What Saylor failed to mention in the tweet was that the firm also sold some 1,638 BTC for approximately $105 million between July 27 and August 2 at an average price of $63,957 – according to the official filing.

The post Strategy Sold Over $100 Million in Bitcoin, Buys Back More STRC appeared first on CryptoPotato.

Ethereum price fell 2% to around $1,847 on Aug. 3 after another rejection near key moving averages left the $1,800 support zone exposed.

Summary

- Ethereum price fell 2.04%, reaching an intraday low of $1,828.

- ETH remains below its 50-day and 100-day moving averages at $1,889 and $1,927.

- 4-hour MACD and Chaikin Money Flow readings show weak momentum and continued selling pressure.

- A break below $1,800 could bring $1,785 and $1,700 into focus.

ETH slides after failing to reclaim $1,900

According to data from crypto.news, Ethereum (ETH) price traded at $1,847 at the time of writing, down 2.04% over the previous 24 hours. The token moved between an intraday high of $1,886 and a low of $1,829 on Binance.

The decline extended ETH’s retreat from its July 27 high near $1,975. Buyers have now failed several times to sustain a move above the resistance zone between $1,950 and $1,975.

ETH briefly rebounded after touching $1,828, but the recovery stalled around $1,850. That left the token near the lower end of its recent trading range and inside the closely watched $1,800–$1,850 support area.

The broader daily structure also remains defensive. Ethereum trades below its 50-day simple moving average at $1,889, its 100-day SMA at $1,927, and its 200-day SMA at $2,089.

Weak liquidity deepens Ethereum’s sell-off

The immediate pressure came from Ethereum’s failure to reclaim the moving-average resistance between $1,889 and $1,927. Sellers entered after the latest attempt faded, pushing ETH below $1,850 and toward its Aug. 3 low.

The 4-hour chart shows the price rolling over after forming a broad curved top below $1,975. Lower highs since late July suggest that buying demand has weakened, although ETH must still break below $1,800 to confirm a larger bearish continuation.

Momentum indicators support the cautious outlook. The 4-hour Moving Average Convergence Divergence remains below zero, with the MACD line near -10.46 and the signal line at about -9.92.

Chaikin Money Flow stands at -0.14. The negative reading indicates that selling volume has outweighed buying volume over the indicator’s measurement period.

Ethereum also faces broader liquidity pressure. A sharp weekly decline in Binance stablecoin netflows suggests less immediately available capital is entering the exchange, potentially reducing the buy-side liquidity available during market declines. However, exchange flows can change quickly and do not determine price direction alone.

Longer-term concerns include weaker institutional demand for Ethereum products relative to Bitcoin and lower mainnet fee revenue as activity shifts toward Layer-2 networks. These factors have weakened Ethereum’s investment narrative, but the current move remains primarily tied to the chart rejection and wider risk-off positioning.

Losing $1,800 could expose ETH to $1,700

The first support range sits between $1,828 and $1,800. ETH has already attracted buyers near the upper part of that zone, but repeated tests could weaken the remaining demand.

Ethereum’s lower daily moving-average ribbon stands near $1,785. A daily close below that level would strengthen the bearish setup and expose $1,700, followed by the June accumulation region around $1,550–$1,600.

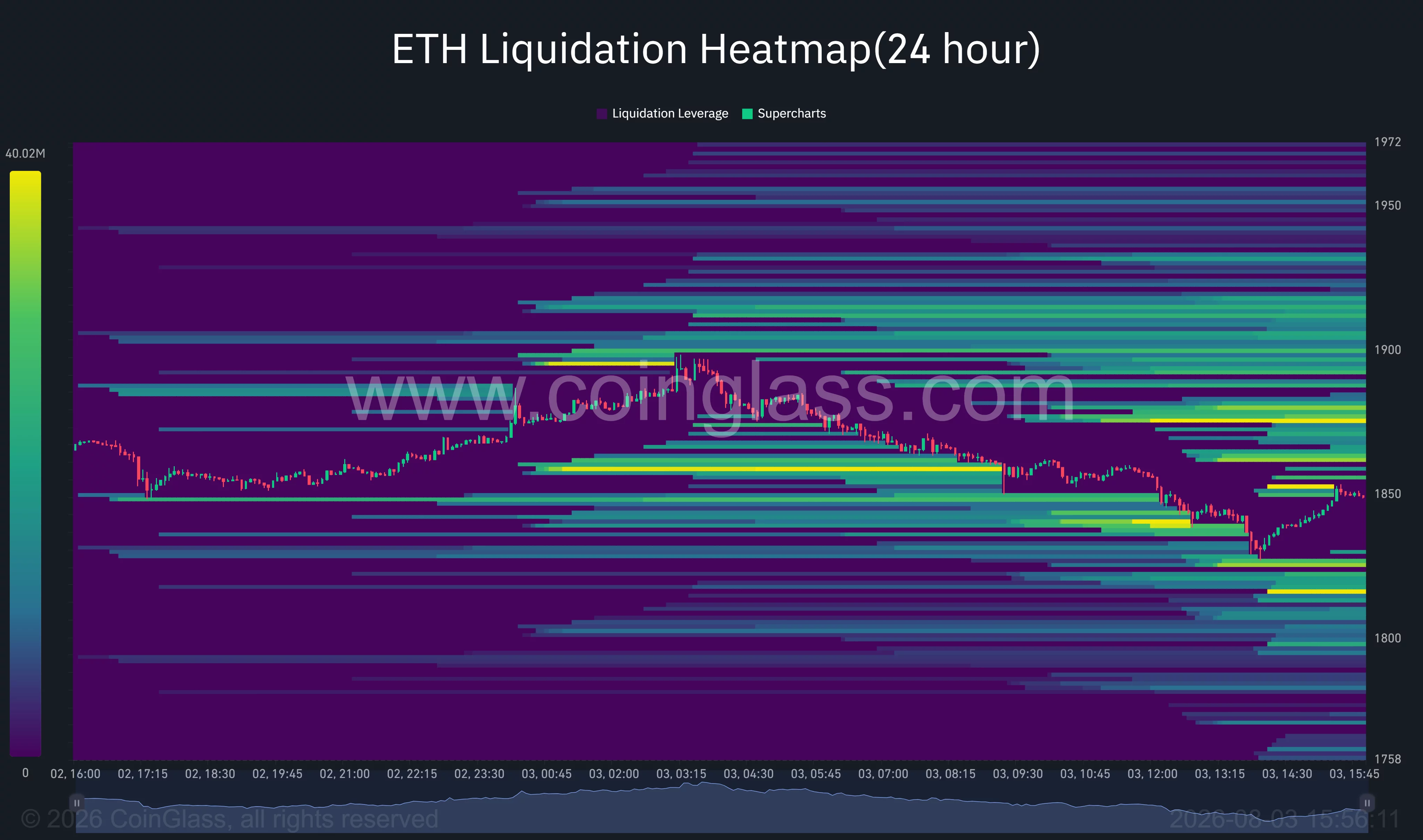

CoinGlass’ 24-hour liquidation heatmap shows nearby leveraged-position clusters around $1,840, $1,820 and $1,810. A move through those levels could liquidate leveraged long positions and accelerate short-term volatility.

The map also shows overhead liquidity around $1,860–$1,875. If ETH rebounds above that range, short liquidations could help drive the price toward $1,890 and $1,920.

On the upside, Ethereum must first reclaim its 50-day SMA at $1,889. A daily close above the 100-day SMA at $1,927 would improve the setup, while a breakout above $1,975 would invalidate the current sequence of lower highs and place $2,000 back in focus.

The daily Relative Strength Index stands at 48.81, below its signal average of 56.44. The reading points to weakening momentum but remains well above oversold territory, leaving room for further selling if $1,800 fails.

Analyst sees Ethereum at a critical support zone

Crypto analyst Ted Pillows described the current support range as decisive for Ethereum’s next move.

“ETH is currently in the $1,800–$1,850 support level,” Pillows said. “This is very crucial for Ethereum to hold, or else it could drop towards $1,700.”

His chart presents two potential paths. Holding the current zone could allow ETH to recover toward $1,950 and then $2,050, while a confirmed breakdown could send the price toward $1,700.

The forecast aligns with the support levels visible on the daily chart, but the $1,700 target would require ETH to lose both the psychological $1,800 level and support near $1,785.

Fed outlook adds pressure on US crypto investors

Changing expectations for US monetary policy remain an additional risk for Ethereum and other speculative assets. Higher Treasury yields and a stronger dollar can reduce investor demand for crypto by increasing the relative appeal of dollar-denominated assets.

Slower-than-expected Federal Reserve rate cuts would keep financial conditions tighter and could limit institutional risk-taking. Ethereum may therefore remain sensitive to upcoming US inflation, employment and Fed policy signals.

For US investors, the near-term setup depends on whether ETH can defend $1,800 as macro liquidity remains constrained. A recovery above $1,927 would improve the technical outlook, but a daily close below $1,785 would shift attention toward $1,700.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Solana price slipped below $73 on Aug. 3 as weak spot demand and sustained capital outflows raised the risk of a drop toward $70.

Summary

- Solana price fell 1.47% to $72.55, placing the token near its daily lower Bollinger Band.

- The 4-hour chart shows SOL below all four tracked moving averages, with the 200-period SMA at $76.79.

- Chaikin Money Flow dropped to -0.17, indicating that selling pressure continued to outweigh buying demand.

- Liquidation liquidity is concentrated near $73.50–$74.50, making that zone the first major upside test.

Solana price extends its decline below $73

According to data from crypto.news, Solana (SOL) price traded at $72.55 on Aug. 3, down 1.47% on the daily chart after moving between an intraday high of $73.67 and a low of $71.98.

The decline extended a broader pullback from the July high near $82.50. SOL has formed a sequence of lower highs since that peak, with sellers defending rebounds around $78 and then $76.

Price has now fallen below the daily Bollinger Band midpoint at $75.09. This level previously acted as support but has turned into the first major resistance area.

SOL briefly moved below the lower Bollinger Band at $71.49 before recovering above $72. That reaction shows buyers remain active around $71.50–$72, but the limited rebound suggests they have not regained control.

The Awesome Oscillator stood at -3.56, with its red bars expanding below zero. That reading points to strengthening bearish momentum on the daily timeframe rather than an immediate trend reversal.

Flat spot demand weakens SOL’s recovery

Solana attempted to rebound after falling toward $71 on Aug. 2, but spot demand failed to recover alongside price.

Analyst Ted Pillows described the divergence as a sign of weakness.

“$SOL is bouncing back. But spot demand is flat. Sign of weakness.”

The 4-hour Chaikin Money Flow reading supports that view. CMF fell to -0.17, meaning more capital was leaving SOL than entering it during the measured period.

Declining spot participation can leave a rebound dependent on leveraged derivatives positions. Such moves are more vulnerable to reversals because they lack the direct buying pressure needed to absorb new selling.

The weakness also comes as activity tied to speculative Solana tokens cools from previous peaks. Lower decentralized exchange activity and weaker fee generation would reduce one source of demand for SOL, which traders need to pay network fees and interact with on-chain applications.

Four-hour indicators keep sellers in control

Solana remains below every major moving average displayed on the 4-hour chart. The 20-period SMA stands at $72.96, followed by the 50-period SMA at $73.88 and the 100-period SMA at $75.06.

The 200-period SMA, currently near $76.79, represents the strongest overhead technical barrier. SOL would need to reclaim that level to weaken the current sequence of lower highs.

The moving averages are also bearishly ordered, with each shorter-term average sitting below the longer-term measures. That structure suggests the decline is established across several trading horizons.

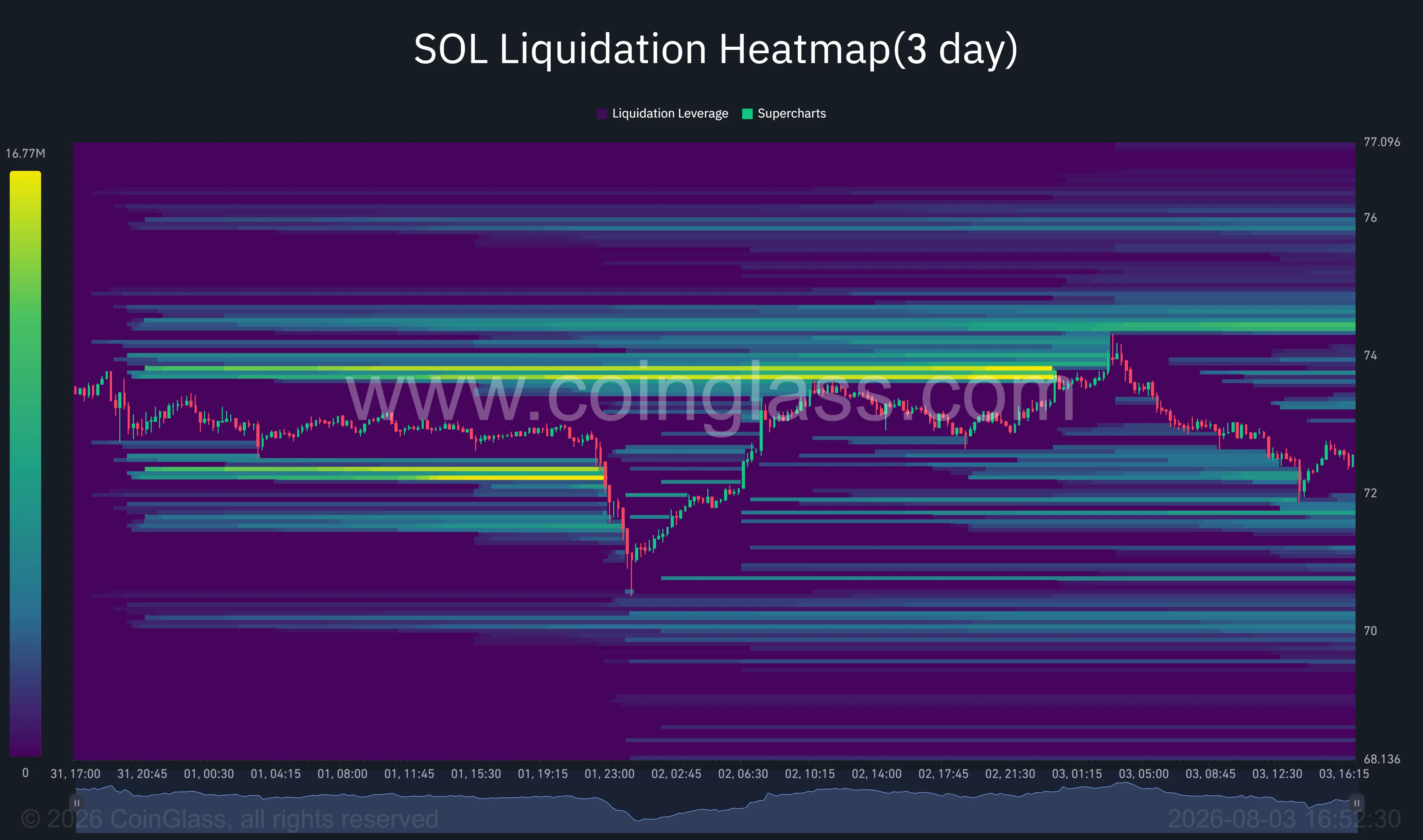

A move above $72.96 could open a retest of $73.88. The $73.88–$75.06 range is particularly important because it combines two moving averages with liquidity visible on the three-day liquidation heatmap.

Failure to reclaim that area would leave SOL exposed to another test of $71.50. A daily close below the lower Bollinger Band could bring $70 into focus, followed by the June support region near $67.50.

Liquidation clusters could increase volatility

CoinGlass’ three-day liquidation heatmap shows the largest nearby concentration of leveraged positions above the current price, particularly around $73.50–$74.

Additional liquidity appears near $74.50 and $76, creating potential targets if SOL begins a short-covering rebound. A move into these clusters could force bearish traders to close positions, accelerating the recovery.

However, liquidity also appears below the market around $71.50 and $70. These clusters could attract price if support near $72 fails.

This leaves SOL between competing liquidity zones. The closer upside concentration could produce a short-term bounce, but the weak CMF reading and bearish moving-average structure suggest any recovery must be confirmed by stronger spot buying.

Fee-burn vote offers Solana a potential catalyst

SolanaFloor reported that proposals addressing Solana’s fee burn and token disinflation were set to enter an initial vote on Aug. 3.

According to the report, the measures would double annual disinflation to 30%, remove about $1.36 billion in projected token issuance over six years and increase daily burns from roughly 650 SOL to 9,000 SOL.

Those figures remain projected outcomes rather than confirmed changes. The proposals must progress through governance before they can alter SOL’s supply dynamics.

For US investors, the immediate backdrop also remains tied to broader risk appetite. High-beta tokens such as SOL can face added pressure when elevated Treasury yields make lower-risk dollar assets more attractive. A shift in Federal Reserve expectations or US yields could therefore affect whether buyers return at the current support zone.

The short-term outlook remains bearish below $75.06. Reclaiming that level would improve the setup and expose $76.79, while a confirmed break below $71.49 would increase the risk of a move toward $70.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

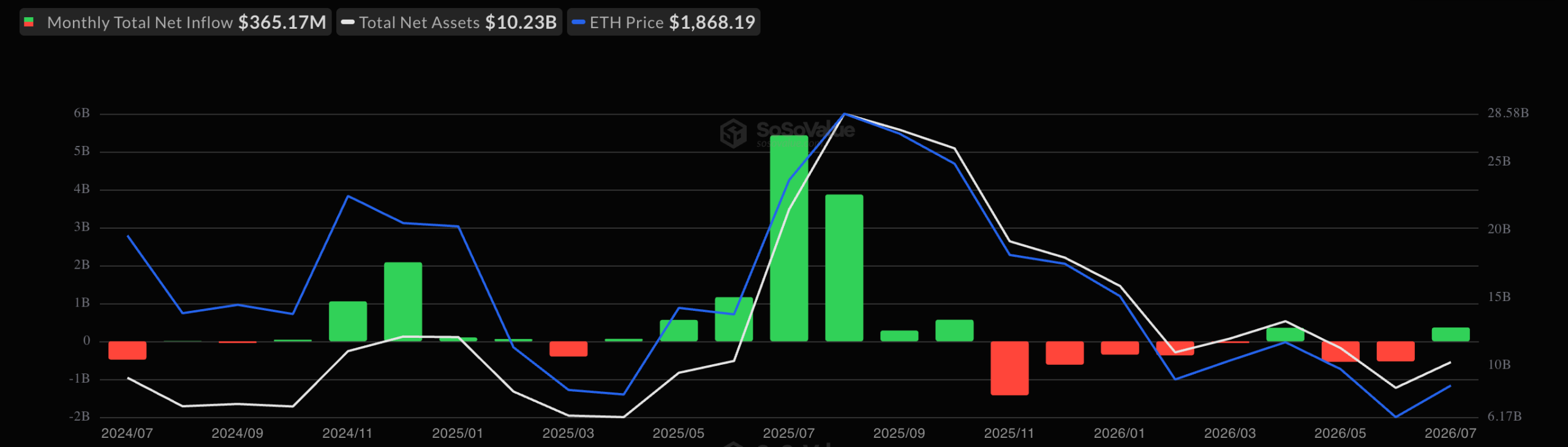

Ethereum (ETH) spot ETFs recorded their strongest month since October 2025. Yet the ending week of July raises concerns about whether institutional appetite is already fading.

Inflows dropped 74% in the final week as the Federal Reserve held rates steady. The pullback raises a key question over whether the demand will carry into August.

Ethereum ETF Inflows Hit 9-Month High Before Buyers Retreat

Ethereum funds attracted $365.17 million in July, their best showing in 9 months, per SoSoValue. The total came after back-to-back redemptions of $540.88 million in May and $528.99 million in June.

Follow us on X to get the latest news as it happens

The recovery lost steam fast, though. Weekly inflows collapsed from $103.9 million to $27.42 million in the week ending July 31.

Price action offered little help. ETH touched $1,967 on July 27, its highest level in nearly two months, before sliding to about $1,863 by Friday, CoinGecko data shows.

Demand also slowed across other ETF products. Bitcoin (BTC) funds shed $61.53 million during the week, snapping three straight weeks of net buying.

Hyperliquid (HYPE) products bled for a third consecutive week, losing $14.75 million. XRP (XRP) ETFs added $14.86 million, pushing cumulative inflows past $1.5 billion.

Fed Hold and Hike Odds Put August Demand in Question

Macro caution appears central to the retreat. The Federal Reserve voted 9-3 on July 29 to keep the interest rate at 3.50%-3.75%.

Three regional presidents, Beth Hammack, Neel Kashkari, and Lorie Logan, dissented in favor of a hike with inflation still above target. Markets now price in a 64% chance of a quarter-point hike in September, keeping tightening risk alive for risk assets.

“I want to stress, of course, that decisions by this committee matter a great deal, and where necessary and appropriate, we will not hesitate to act,” Fed Chair Kevin Warsh said.

If investors stay risk-off into August, the late-July slowdown may extend and erase the month’s progress. However, a revival in demand would confirm July’s rebound as the start of a broader recovery rather than a one-month bounce. The Fed’s Jackson Hole symposium in late August may offer the next signal.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Ethereum ETFs Post Best Month Since October 2025 but Fed Hold Chills Demand appeared first on BeInCrypto.

Strategy (MSTR) raised $104.73 million last week with the sale of 1,638 bitcoin, and raised an additional $290.6 million via the sale of common stock.

Alongside, the company repurchased 912,143 shares of its high-yielding preferred stock STRC for $81.2 million, according to an SEC filing Monday morning.

The bitcoin sales reduced Strategy’s holdings to 842,138 BTC, acquired for $63.51 billion at an average price of $75,419. The company lifted its USD reserve by $250 million.

The company announced over the weekend that it would maintain STRC’s annual dividend rate at 12%, saying it does not intend to recommend a reduction until the shares trade consistently near their stated $100 value.

In XRP news today, the XRP Ledger released xrpld 3.2.1 on July 31 after a validator manifest flood was detected hitting nodes that same day, with Ripple Director of Engineering Vijay Khanna issuing an urgent call on August 1–2 for all node operators to upgrade immediately.

The ledger continued closing normally throughout the incident, with no confirmed fund losses and no consensus failure, but unpatched nodes remain exposed to resource-exhaustion risk until operators complete the two-step upgrade process.

This news dropped as XRP USD fell 1.5% from $1.10 to $1.06 over the past 24 hours, with daily trading volume of $791M. This follows a worrying trend in which Ripple has crashed -4% over the past seven days.

XRP News: What the Manifest Flood Actually Did

The attack exploited a structural gap in how XRPL nodes handled validator manifests: before the patch, nodes would accept, cache, and rebroadcast an unlimited number of manifests tied to unknown validator keys with no ceiling on volume or storage.

An attacker could generate junk manifests at scale, forcing nodes to burn memory, disk space, and bandwidth processing data they would never act on.

The mechanism is closer to a denial-of-service resource drain than a consensus attack; the network’s transaction processing was never disrupted, but the exposure was real for any operator running unprotected infrastructure.

The development team confirmed the problem was specifically tied to how XRPLF nodes handled validator manifests, though as of publication the root cause and full exploitation details have not been publicly disclosed.

A technical post-mortem is forthcoming from XRPL Operations, which should clarify attacker behavior, traffic volumes, and any additional hardening steps.

For those tracking broader blockchain security vulnerabilities and attack vectors, the manifest flood fits a pattern where unbounded auxiliary data channels become leverage points even when consensus logic holds.

— Crypto Michael

Urgent XRPL Update: Node Operators Told to Install Critical Fix

Urgent XRPL Update: Node Operators Told to Install Critical Fix

Ripple engineering director Vijay Khanna is urging XRP Ledger node operators to upgrade to **xrpld version 3.2.1**, which includes a hotfix designed to prevent a manifest flood attack observed on the network.…

Dinarian888 (@Dinarian888) August 2, 2026

Dinarian888 (@Dinarian888) August 2, 2026

Discover: The Best Crypto to Diversify Your Portfolio

Four Safeguards Introduced in the Hotfix

The hotfix introduces four discrete protections targeting different points in the manifest handling pipeline. Oversized manifests are now rejected outright before full decoding. Incoming manifest batches per network message are capped.

The volume of manifest data shared with new peers is limited. And the unknown-key manifest cache is hard-capped at 100 entries, preventing unbounded growth from unrecognized validator identities.

Beyond those four caps, unknown validator manifests are no longer written to disk. That change means any pre-patch flood data is cleared on restart rather than persisting in storage, which is precisely why the upgrade requires a specific two-step sequence.

Firstly, install 3.2.1, let the server run for one to two minutes, then perform a second restart to purge any manifests retained from before the patch. Skipping the second restart leaves stale flood data in place. Operators should also verify their systems trust Ripple’s current GPG signing key, rotated February 18, 2026, or automatic upgrades may fail silently.

Trade XRP on Bybit and Get a Chance to Win Our $1,000 USDT Airdrop

Who Needs to Act and Why It Matters Now

—

$XRP's momentum fades, but the bullish structure holds firm: price is drifting back into 6YR support that guided all breakouts since 2020 — each green-arrow marked previously triggered expansion; compression within a falling wedge is setting the stage for a major repricing

$XRP's momentum fades, but the bullish structure holds firm: price is drifting back into 6YR support that guided all breakouts since 2020 — each green-arrow marked previously triggered expansion; compression within a falling wedge is setting the stage for a major repricing  pic.twitter.com/Es1Mae0poz

pic.twitter.com/Es1Mae0poz

ChartNerd

ChartNerd  (@ChartNerdTA) August 3, 2026

(@ChartNerdTA) August 3, 2026

In other XRP news, exchanges, custodians, wallet back ends, data providers, and any business running its own XRPL server must complete the node upgrade. Ordinary XRP holders do not need to move funds or change keys.

The urgency is compounded by upgrade adoption lag: xrpld v3.2.0, the larger June 15 release that renamed the reference server and required infrastructure config change, spread faster among validators than across the broader node network, meaning a cohort of operators may still be running older versions that are now doubly exposed.

The network security response here was operationally sound: a targeted hotfix, clear operator instructions, and a pending post-mortem that signals the team is treating this as a formal security incident rather than routine maintenance.

In the broader XRP ecosystem, the incident comes as the ledger scales; the network added nearly 490,000 new accounts in the first half of 2026, per supplementary data from Coinpaper, pushing total accounts past 8.4 million.

That growth trajectory makes robust infrastructure hardening a structural necessity, not an edge-case concern. Institutional developments, including Aviva’s tokenized liquidity fund on XRPL and growing enterprise adoption, raise the stakes for any operator still delaying the patch.

Discover: The Best Token Presales

The post XRP News: xrpld 3.2.1 Hotfix Patches Manifest Flood Draining XRPL Node Resources appeared first on Cryptonews.

Trump-linked Bitcoin miner produced a record 932 BTC in the second quarter, lifting mining revenue 8% as its net loss narrowed from the previous quarter.

South Africa has proposed new rules requiring cross-border crypto transfers to pass through authorized providers and be reported to the central bank, expanding the country’s effort to bring digital assets under its financial control framework.

Summary

- South Africa has proposed rules requiring cross border crypto transfers to go through authorized service providers and be reported to the central bank.

- The draft says only transfers to offshore providers or private wallets would qualify as regulated cross border crypto transactions.

- Individuals would be allowed to move crypto offshore only within South Africa’s existing foreign currency allowances.

- The proposal builds on earlier plans to bring crypto under the country’s foreign exchange control framework.

- Public comments on the draft Crypto Asset Manual will remain open until Sept. 30.

According to local media, South Africa’s National Treasury and the South African Reserve Bank (SARB) on Monday released a draft Crypto Asset Manual setting out when crypto transactions become regulated cross-border events and how they must be handled. The proposal forms part of the country’s ongoing overhaul of its capital flow rules first introduced in April.

South Africa has defined when crypto transfers become reportable

Under the draft, moving crypto offshore will only qualify as a cross-border transaction in specific situations. A report to the SARB’s Financial Surveillance Department (FinSurv) would be required when crypto assets move from a locally authorized Crypto Asset Service Provider (CASP) to an offshore CASP or into a privately controlled non-custodial wallet.

The proposal says people who wish to transfer crypto abroad would have to use an authorized provider instead of sending assets directly through unregulated channels. FinSurv would receive reports of those transactions as part of the country’s foreign exchange monitoring process.

Domestic crypto activity would remain outside those reporting requirements. Buying or selling crypto in South African rand through a local authorized provider would not be treated as a cross-border event under the proposed framework.

For now, the draft allows only individuals to move crypto assets offshore, and only within South Africa’s existing foreign currency allowances. The SARB also said the framework does not recognize crypto assets as legal tender and currently does not distinguish between different categories of digital assets because additional research is still underway.

Interested parties can submit comments on the draft until Sept. 30.

Crypto rules build on South Africa’s earlier capital flow proposal

The new manual follows South Africa’s Draft Capital Flow Management Regulations released in April, which proposed bringing crypto assets into the country’s foreign exchange control system for the first time.

The National Treasury and SARB said in April that crypto assets would be treated as a form of capital moving across borders, placing them alongside other regulated assets under the country’s capital flow regime. The proposal was also designed to replace South Africa’s Exchange Control Regulations dating back to 1961 while aligning the country’s framework with recommendations from the Financial Action Task Force and the Organisation for Economic Co-operation and Development.

The April proposal introduced the concept of authorized crypto service providers, transaction reporting, declaration requirements and administrative penalties for non-compliance. Treasury officials said at the time the policy would focus on reporting, traceability and risk-based oversight instead of relying only on transaction-by-transaction approvals.

The draft Crypto Asset Manual now explains how those principles would work in practice by defining the point at which crypto movements become cross-border transactions that fall under financial surveillance rules.

Authorities have linked the framework to financial crime controls

According to Reuters, the reporting framework is intended to stop crypto assets from being used to bypass South Africa’s existing financial controls while helping authorities identify illicit financial flows.

By limiting offshore transfers to authorized service providers, regulators would receive transaction data through FinSurv instead of relying on transfers conducted outside the regulated financial system.

The proposal arrives as crypto adoption continues to grow in South Africa. Reuters, citing blockchain analytics firm Chainalysis, said the country already has hundreds of licensed virtual asset service providers, while several major banks are developing crypto products for institutional clients.

South Africa has become one of Africa’s largest digital asset markets in recent years. Earlier industry estimates placed annual crypto transaction value in the country among the highest on the continent, while blockchain investment has continued to attract institutional interest.

Crypto oversight has expanded beyond capital controls

The latest consultation follows another crypto policy proposal published in July by the South African Revenue Service (SARS), which released draft guidance explaining how existing tax laws apply to digital assets.

Unlike the latest capital flow proposal, the SARS draft focused on taxation rather than foreign exchange regulation. It confirmed that crypto assets are treated as intangible assets instead of legal tender or foreign currency under existing tax law and explained how income tax and capital gains tax could apply depending on each taxpayer’s circumstances.

The tax authority also outlined how activities including crypto trading, token swaps, staking, mining, decentralized finance participation and crypto payments may trigger taxable events under current legislation.

At the same time, South Africa has begun implementing the Crypto-Asset Reporting Framework (CARF), under which crypto service providers will collect and report selected customer and transaction information to SARS. The first reporting period runs from March 1, 2026, through Feb. 28, 2027.

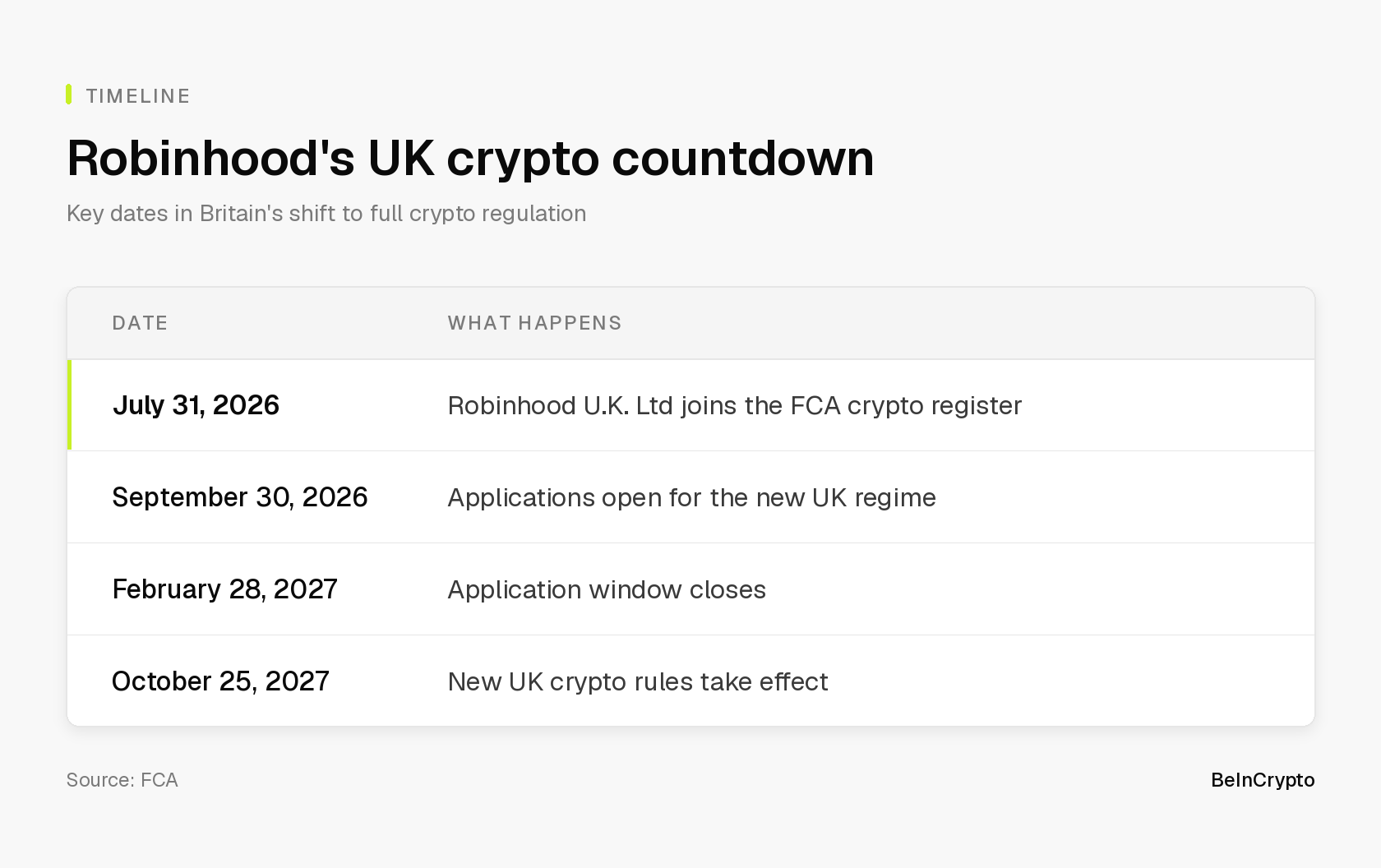

Robinhood Markets won UK crypto approval on July 31. The surprise is everything the approval does not allow.

The Financial Conduct Authority (FCA) added Robinhood U.K. Ltd to its crypto register. The company may pass customer orders to other firms. It cannot hold anyone’s coins.

What the FCA actually approved

Robinhood has been an FCA-approved stockbroker in Britain since August 2019. Crypto is new ground. The regulator added it to the crypto register on July 31, 2026.

Two limits took effect the same day, with the first one mattering most:

- Robinhood UK may only arrange crypto trades.

In plain terms, it takes your order and hands it to someone else to finish.

UK crypto rules cover two other jobs. One is running an exchange. The other is holding coins for customers. Robinhood got neither.

- The second limit bans crypto cash machines unless the FCA agrees in writing.

The register also says the firm cannot hold client money. Even this much is hard to win. FCA figures show 291 firms applied between January 2020 and October 2022. Only 38 made the register. Another 155 gave up before a decision.

One point matters for customers. Being on the register is not a safety net. The FCA warns that crypto services are unlikely to be protected if something goes wrong.

Britain’s compensation scheme rarely covers crypto losses. The financial ombudsman usually cannot help either.

Rivals Got There First, With More Freedom

Robinhood is late. The register opened in 2020.

Kraken’s UK arm, Coinbase, and Revolut are all on it. Several also hold e-money licences, which let them handle customer cash. Robinhood UK does not.

It already owns one company on the list. Bitstamp UK Ltd joined years earlier, and Robinhood bought its parent for $224 million in June 2025.

That makes Bitstamp the obvious place for UK orders to land.

Robinhood has also tried and failed here before. It agreed to buy British crypto app Ziglu in April 2022. Ten months later it walked away. The $12 million it had already sent Ziglu was written off.

So the new approval looks like housekeeping rather than a launch. Robinhood told investors in July it plans to start UK crypto soon.

Its own small print still says UK customers get no crypto trading or custody. Elsewhere the company keeps building, including its Robinhood Chain public testnet.

Why October 2027 Decides What Survives

This approval is temporary. Tougher UK crypto rules start on October 25, 2027.

Every firm on today’s register must apply again. Nothing carries over.

The window is five months long. Firms that miss it must stop most crypto work. The FCA has warned that today’s registration counts for nothing at that stage.

That deadline has driven Britain’s crypto policy debate all year, alongside UK stablecoin payment plans.

For investors, any reward is years away. Crypto revenue fell 38% to $100 million in Robinhood’s second quarter. Total revenue still hit a record $1.31 billion.

The market shrugged on Monday. HOOD closed Friday at $86.56, then traded at $87.22 before the bell, up 0.76%. Its 52-week high is $153.86.

The real test comes with that 2027 application. Robinhood sells trading, custody, and staking across Europe. An arranging license supports none of it.

What the company asks for will show how serious it is about Britain.

The post Robinhood Cleared for UK Crypto, But There Are Major Limits appeared first on BeInCrypto.

Crypto World

Solo Bitcoin (BTC) miner nets $200,000 as Coldcard wallet hack rocks sentiment: Crypto Daily

A solo miner scored a major win even as the broader market frets over a multimillion-dollar Coldcard hardware wallet exploit.

According to mempool data, an independent miner successfully packaged block 960,804 early Monday. The block reward of 3.157 BTC is valued at approximately $199,300. Details on the specific hardware used remain unknown.

The success came just three weeks after another solo miner, running a single hobbyist-grade Bitaxe device, struck block 957,382, pocketing 3.1382 BTC, worth roughly $200,000 at the time.

These back-to-back wins highlight a broader trend. Solo miners have already claimed 13 blocks this year. While individual operators continue to defy the odds with relatively modest setups, the wider Bitcoin mining sector has come under stress due to tight margins. That has prompted several large mining companies to pivot toward artificial intelligence data centers and related infrastructure in search of sustainability.

Meanwhile, small BTC holders continue to express frustration over the Coldcard incident, which has led to the loss of long-held Bitcoin savings. Over the weekend, onchain data showed signs of some BTC holders moving millions of dollars worth of coins to exchanges.

Wild-card contenders Diamondbacks, Padres clash in desert

Kenny Barron Trio’s Brilliant 1995 Welsh Jazz Festival Performance Arrives on Elemental Music 2CD and 2LP Sets

JIO FINANCIAL SERVICE NEWS | JIO FINANCIALS LATEST NEWS | Market support

-

Business5 days ago

Business5 days agoWhy Trees Belong on the Risk Register

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: Wit & Wisdom

-

Politics3 days ago

Politics3 days agoMeta enters AI-training agreement with far-right ‘propaganda rag’ Newsmax

-

Entertainment6 days ago

Entertainment6 days ago‘Stargate’ Creator’s New Sci-Fi Series Returns for Season 3 Tomorrow

-

Crypto World2 days ago

Crypto World2 days agoMicroStrategy Post-Earnings CLARITY Act Push Could Add New Catalyst for Its Stock

-

Politics6 days ago

Politics6 days agoThe Part of the Electric Transition Nobody Wants to Discuss

-

Business5 days ago

Business5 days agoMajor shareholder moves on Canyon

-

Crypto World2 days ago

Crypto World2 days agoXRP Ledger v3.3.0 brings five institutional features

-

News Videos4 days ago

News Videos4 days agoBitcoin Enters the 3rd Stage of the Bear Market

-

Crypto World6 days ago

Crypto World6 days agoKraken Enables Retail Access to Jersey Mike’s IPO via Tokenized Shares

-

Tech6 days ago

Tech6 days agoNew macOS Sequoia & Sonoma security updates for older Macs

-

Politics4 days ago

Politics4 days agoLuke Littler’s dominance sparks GOAT debate

-

News Videos6 days ago

News Videos6 days agoClaude: Build Financial Dashboards in Minutes (2026)

-

Business6 days ago

Business6 days agoJohnson & Johnson agrees to $5.5B settlement over talc cancer claims

-

Sports4 days ago

Sports4 days agoSeema Kaliramna Wins Discus Throw Bronze, Takes India’s CWG Medals Tally To 17

-

Crypto World1 day ago

Crypto World1 day agoCrypto PAC spending tops $2M in Michigan House race

-

Business3 days ago

Business3 days agoTrump Announces Hamas Disarmament Agreement as Iran Strikes Kuwait Air Base and US Attacks Pause Overnight

-

Tech5 days ago

Tech5 days agoGemini can now summarize the messiest comment threads in Google Docs

-

Tech1 day ago

Tech1 day agoESET tracks rise in malicious AI skills and adaptable malware

-

NewsBeat4 days ago

NewsBeat4 days agoFour people die trying to cross Channel in small boats

You must be logged in to post a comment Login