Crypto World

Binance Adds Anchorage Digital Off-Exchange Settlement

Anchorage Digital has integrated its off-exchange settlement platform with Binance, allowing institutional clients to trade on the exchange while keeping their crypto and cash in qualified custody at the federally chartered US crypto bank rather than depositing assets directly onto Binance.

Under the arrangement, institutions can use crypto assets or US dollar deposits held with Anchorage as collateral to meet Binance’s margin requirements without first transferring those assets onto the exchange. The companies said the model separates custody from trade execution, allowing assets to remain with an independent custodian until settlement.

The service is initially available to select institutional clients and marks the first off-exchange settlement implementation for Anchorage Digital’s Atlas platform, which the company said is designed to support institutional trading, settlement, lending and collateral management through custody-based infrastructure.

The collaboration addresses one of the biggest obstacles keeping institutional capital on the sidelines of crypto markets: exchange counterparty risk. By eliminating the traditional requirement to pre-fund trades, this could bring crypto trading closer to the custody-and-execution model long used in traditional financial markets.

Financial terms of the partnership were not disclosed.

Related: ESMA MiCA warning puts Binance EU service changes under scrutiny

Crypto exchanges expand off-exchange settlement offerings

Off-exchange settlement has gained traction among institutional crypto trading platforms in 2026.

In April, BitMEX partnered with Zodia Custody to let institutional clients trade derivatives while keeping collateral in segregated custody rather than on the exchange. Under the BitMEX integration, traders can access perpetual swaps and futures while collateral remained in Zodia’s custody and was mirrored for trading.

BitMEX said the structure eliminated the need to prefund exchange accounts while improving capital efficiency and reducing operational risks associated with moving assets between custody and trading venues.

Source: BitMEX

Bitget adopted a similar model in June by integrating Fireblocks Off Exchange. The integration allows institutional clients to execute trades from MPC-based wallets while keeping assets in trader-controlled collateral vaults rather than transferring them onto the exchange. According to Bitget, the platform can verify that trading accounts are fully collateralized in real time without taking custody of client assets.

KuCoin Institutional also expanded its institutional custody offering earlier in the year, integrating Ceffu’s MirrorX platform in January. The system allows institutional clients to trade while keeping digital assets in third-party custody, with funds mirrored for trading and settled offchain every four hours.

Magazine: Bitcoin slides to $58K, XRP hits $1 but onchain data promising: Market Moves

Crypto World

ENS Community Member Proposes Dissolving DAO After Founder Blocks Security Council Renewal

Christoph Jentzsch proposed on X that ENS DAO dissolve itself rather than continue operating under what he called a broken governance structure. "As it seems, the ENS DAO is broken," he wrote. "I would propose turning this into a win, by actually dissolving it. Its goals have been accomplished, the… Read the full story at The Defiant

Solana Foundation has introduced Solana Governance Proposals, a new onchain process for validators to move major network questions into stake-weighted votes.

Summary

- Solana validators can now move core governance questions into stake-weighted onchain votes through SGPs directly.

- A proposal needs 15% active stake support before it can enter formal network voting period.

- Validators need at least 100,000 SOL delegated to take an SGP onchain under current rules.

The system gives validators a formal route to submit, support, and decide governance items that may shape Solana’s future protocol direction.

Meanwhile, the Solana Governance Proposals repo says SGPs are documents proposed by Solana validators for stake-weighted, onchain voting through the svmgov program. The process is for high-level questions that ask whether the network should move in a certain direction, rather than detailed technical changes. This keeps SGPs focused on broad network direction only.

A validator vote account needs at least 100,000 SOL staked to take an SGP onchain. The proposal then needs support from at least 15% of active stake before it can enter voting. The Solana Governance documentation says validators create proposals, other validators support them, and voting weight is proven through Merkle proofs against an onchain stake snapshot.

The process separates signals from code

The SGP process sits beside Solana Improvement Documents, which cover detailed protocol design. In simple terms, SGPs ask whether Solana should pursue a direction, while SIMDs explain how a change would be built. The repo says, “A ‘yes’ on an SGP is a mandate to proceed.”

The lifecycle moves from idea to draft, support, voting, acceptance, and activation. Once a proposal reaches the 15% support threshold, it enters a fixed 11-epoch process. That includes seven epochs for discussion, one epoch for a Node Consensus Network snapshot, and three epochs for voting.

There is no quorum rule. A proposal passes only if “For” votes reach at least 66.67% of “For” plus “Against” stake. The repo also says SGPs are not mandatory for every technical change. If validators do not reach support, developers can continue through normal SIMD review.

Governance arrives as upgrades continue

The launch comes as Solana continues to test large infrastructure changes. As previously reported, the Alpenglow upgrade entered community validator testing in May. Alpenglow aims to cut confirmation times to about 150 milliseconds and remove Proof of History and onchain vote transactions from Solana’s core process.

The new SGP route could give validators a clearer way to request network-wide direction before developers prepare technical work. The GitHub repo uses Alpenglow as an example of a proposal that could have first taken a directional vote before later SIMDs defined the build path. That example shows how Solana may use SGPs when validator input is needed before engineering details are complete.

Recent Solana activity adds context

Solana’s validator set has also been tied to other recent network tools. As crypto.news reported, DoubleZero launched Edge in April with 379 validators publishing shreds and about 43% of Solana’s total stake covered at launch. The project aims to deliver Solana block data through private fiber paths.

Solana has also seen renewed market activity around network use. Crypto.news reported that Solana’s tokenized stock activity helped drive an 18% weekly SOL rebound in late June. Earlier, crypto.news reported that Galaxy Digital proposed a voting model for Solana inflation, showing that validator voting design has already been part of the network’s policy debate.

Türkiye-based digital asset platform Paribu has launched DeFi access inside its main app, adding DEX trading, perpetual contracts through Hyperliquid, and Polymarket-linked option markets.

Summary

- Paribu now offers Hyperliquid perpetuals and Polymarket markets through its main self-custodial DeFi app section.

- The platform opened a waitlist for NYSE, Nasdaq, and Borsa Istanbul stock trading access soon.

- Paribu says users can trade DeFi products without separate wallet apps, seed phrases, or transfers.

The company also opened a waitlist for stock trading as it works to combine crypto, DeFi, yield products, and equities in one app.

Paribu said it is the first regulated exchange to offer both Hyperliquid perpetuals and Polymarket option markets through a centralized exchange interface. Users can access the DeFi section with their existing balance, without a separate wallet app, seed phrase, or new account. The company said each DeFi position remains self-custodial, while trades settle onchain through linked protocols.

DeFi access targets Türkiye’s retail market

Paribu framed the launch around Türkiye’s active crypto market. The company cited TRM Labs data showing Türkiye ranked fifth globally in retail crypto activity, with $40 billion in volume in Q1 2026. The figure rose 7% year over year while global retail crypto volume fell 11%.

The company said many local retail users keep their main crypto holdings inside one app and have not used DeFi wallet tools. Paribu’s DeFi access is designed to let these users reach onchain markets without switching platforms. Its blog post on DeFi access says the wallet setup uses passkeys and recovery tools instead of seed phrases.

Hyperliquid and Polymarket enter the app

The Hyperliquid integration lets Paribu users trade perpetual contracts from the DeFi section of the app. Trades route to Hyperliquid’s decentralized blockchain, while positions remain in users’ self-custodial wallets. Paribu said Hyperliquid has processed more than $4 trillion in cumulative trading volume.

The launch follows wider activity around Hyperliquid. As reported by crypto.news, Kalshi launched CFTC-regulated HYPE perpetual futures, lifting HYPE futures open interest to $2.48 billion. Moreover, crypto.news reported thatHyperliquid added validator-settled outcome markets under HIP-4, expanding beyond perpetual futures.

Paribu also added access to Polymarket markets through the same DeFi section. The company said it will list curated markets only, with each contract reviewed for integrity, liquidity, and risk profile before appearing in the app. Paribu serves as the interface, while execution and settlement happen onchain through Polymarket infrastructure.

The rollout comes as prediction markets face closer review in several jurisdictions. As crypto.news reported, the CFTC is preparing new rules that could affect Polymarket and Kalshi. Crypto.news also reported that the CFTC sued Kentucky to block state action against Kalshi, Polymarket, and related partners.

Stock trading remains pending

Paribu is also preparing to offer equities. Its brokerage arm has received establishment authorization from Türkiye’s Capital Markets Board and is waiting for an operating license. The company said NYSE, Nasdaq, and Borsa Istanbul stocks will become tradable after the license process is complete.

For now, users can view real-time market data for U.S. and Turkish stocks inside the app. Paribu said the stock waitlist is open before trading goes live. Founder and CEO Yasin Oral said, “Paribu is becoming a single app for all of finance: crypto, DeFi, equities, and yield.”

The expansion follows other Paribu moves. Previously, crypto.news reported that Paribu’s $240 million CoinMENA acquisition led a weekly crypto funding period in December 2025. The company has also said Clave joined Paribu in 2026 to support passkey-based account abstraction and self-custody tools.

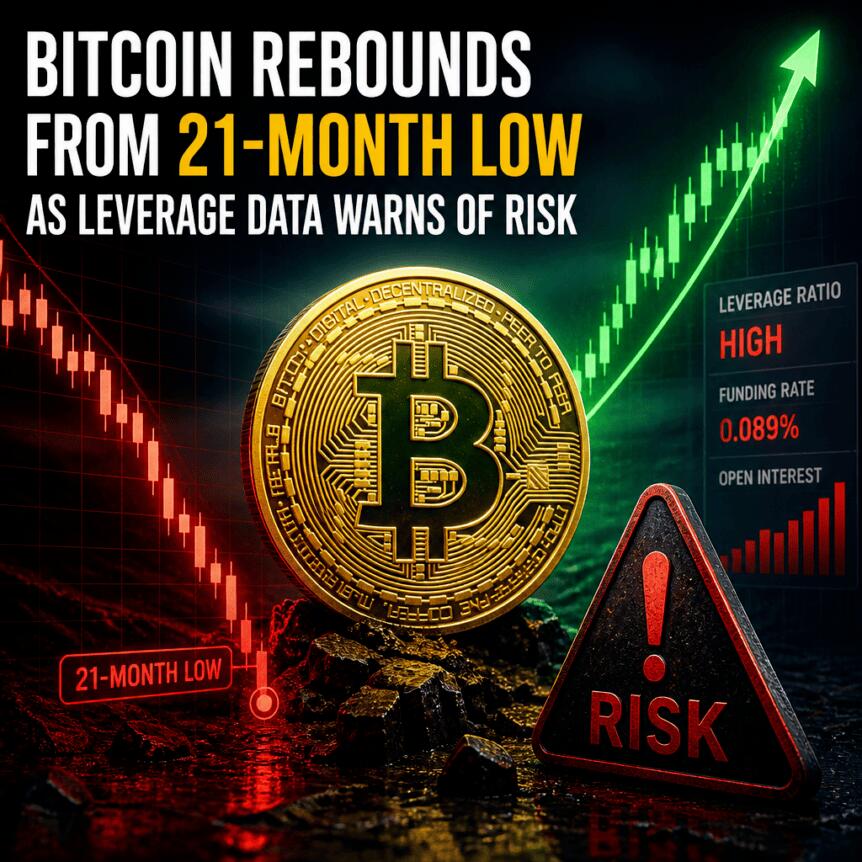

Bitcoin rebounded on Wednesday after tagging a 21-month low, with BTC rising as high as $60,200 and gaining roughly 2.7% over the past 24 hours from earlier losses. The bounce lifted major alternatives as well: Ether (ETH) rose about 3%, while Solana (SOL) climbed roughly 4.85%.

Still, the recovery is happening against a backdrop of persistent caution. According to the Crypto Fear & Greed Index maintained by Alternative.me, sentiment is around 11 out of 100—an “Extreme Fear” reading—suggesting many market participants remain nervous about what comes next. Even with today’s uptick, Bitcoin is still down about a third since the start of the year.

Key takeaways

- Bitcoin’s intraday bounce followed a fresh 21-month low near $57,737, but broader confidence remains weak with the Fear & Greed Index in “Extreme Fear.”

- US spot Bitcoin ETF flows have been net negative recently, including a reported $4.5 billion outflow in June—the largest since the funds launched—indicating cautious institutional positioning.

- On-chain data points to strength from long-term holders, with an estimated addition of roughly 270,000 BTC over the past two weeks.

- Funding rates have stayed positive for three straight days, implying leverage is still leaning toward long exposure even as price remains under pressure.

- Liquidation risk appears heaviest in the $57,000 to $60,500 band, meaning sustained moves beyond roughly $61,000 or below $56,000 could accelerate volatility.

Fear remains elevated even after the rebound

Market pricing today reflects a tug-of-war between dip-buyers and the fear of further downside. The latest sentiment readings underline that many traders are still operating defensively, despite Bitcoin’s recovery attempt from the yearly low area.

This matters because fear can shape how quickly the market absorbs negative news. When sentiment is extremely negative, rebounds often face selling pressure not just from those who missed the decline, but from participants who are using rallies to reduce risk. The result is a market that can rally sharply—then struggle to build follow-through.

ETF outflows versus long-term accumulation

One of the clearest contrasts in the data is between institutional product flows and on-chain holder behavior.

US spot Bitcoin exchange-traded funds (ETFs) have seen more money leaving than entering in recent weeks, including a reported total outflow of $4.5 billion in June, described as the largest since the funds began launching. That pattern typically suggests that, at least for now, some traditional investors are not convinced enough to add exposure during a drawdown.

At the same time, on-chain indicators show long-term holders accumulating. According to the on-chain data referenced in the analysis, long-term wallets added about 270,000 BTC over the past two weeks. In crypto market interpretation, that kind of accumulation is often read as evidence that bigger investors view the recent decline as an opportunity rather than a prompt to sell.

The tension between these two signals—net outflows from ETFs versus accumulation by long-term holders—helps explain why the market can bounce without fully transitioning into a sustained uptrend. Flows may stay cautious while deeper capital continues to build positions more quietly.

Funding rates stay positive as leverage crowds in

Another point to watch is leverage. The analysis highlights that Bitcoin’s funding rate has remained positive for three consecutive days. In practical terms, that means the prevailing derivatives positioning has continued to lean toward bets that prices will rise.

Positive funding while spot prices are weak can be a volatility risk. When one side of the market becomes overcrowded with leveraged longs, a further downside move can force liquidations that amplify the drop—especially if price breaks key support levels. Conversely, if the market stabilizes or turns upward while longs remain funded, the same mechanism can also support rallies through short-covering and stop-trigger effects.

As of now, the key point is that leverage appears active, but price confirmation has not yet clearly followed through in a way that would suggest the market has fully flipped from fear to conviction.

Liquidations cluster around current trading levels

Where liquidation risk sits is often central to understanding how quickly price can move during stressful periods. Using a three-exchange, three-day liquidation heatmap (as cited in the analysis, sourced from Hyblock), the highest concentration of leveraged positioning appears roughly between $57,000 and $60,500. That zone closely overlaps with the trading range Bitcoin has held since late June.

Above that area, the density of liquidation risk thins out noticeably between approximately $61,000 to $62,000. Below, a similar reduction appears around $55,000 to $56,000. This distribution suggests that a move breaking out of the present range could encounter less immediate “magnet” pressure from nearby liquidations—while a move that stays within or slightly beyond the clustered zone could lead to sharper, more abrupt price reactions.

In the near term, the analysis argues that most forced unwind potential sits close to current prices rather than far away. That is why decisive movement beyond roughly $61,000 to the upside—or below about $56,000 on the downside—could create room for accelerated liquidation-driven volatility.

Looking ahead to the next 24 hours, the outlook described here is neutral. A meaningful change would likely require stronger evidence that leveraged positioning is both rising and aligning with a rising spot price—an interaction the analysis notes has not clearly emerged yet.

Traders and investors should monitor whether ETF flow weakness persists alongside continued long-term accumulation, and whether derivatives conditions evolve—particularly funding rate direction and liquidation clustering—as these factors together will determine whether this bounce becomes a trend or fades back into range-bound action.

Venice AI, the privacy-focused AI platform founded by Erik Voorhees, has raised $65 million in Series A funding at a $1 billion valuation, bringing the company to “unicorn” status. The round—led by Dragonfly and backed by Coinbase Ventures, F-Prime, North Island Ventures, Morgan Creek and others—was announced on Wednesday, and represents Venice AI’s first outside capital raise since it launched in 2024.

The funding arrives as privacy concerns around mainstream AI services are drawing renewed attention. Earlier this month, Anthropic cut off foreign access to two of its latest models, and in the broader public debate over AI data handling, a class-action lawsuit recently accused OpenAI of sharing ChatGPT data with third parties. Against that backdrop, Venice AI positions itself as a layer between users and model providers, designed to reduce what third parties can see about user activity.

Key takeaways

- Venice AI reached unicorn status after closing a $65 million Series A round at a $1 billion valuation, led by Dragonfly.

- The platform claims 3.5 million users and routes traffic through a proxy that can obscure IP address and user/account/session data from model providers.

- Venice AI says the new capital will fund more of its own infrastructure, including owning GPUs via data center expansion rather than relying entirely on rental capacity.

- The announcement lands amid heightened scrutiny of AI data privacy, including legal claims involving tracking technologies and alleged sharing of user information.

Unicorn funding for a privacy-first AI delivery layer

Venice AI’s Series A funding was announced by the company in a blog post published Wednesday, with Erik Voorhees describing the company’s mission in constitutional terms in a separate X post. Voorhees said the funding will be used to uphold the First and Fourth Amendments “as they relate to mankind’s interaction with AI.” In the U.S. legal framework, the First Amendment protects core freedoms including speech, while the Fourth Amendment restricts unreasonable government searches and seizures.

While the fundraising headlines focus on valuation and total capital, the more meaningful detail for potential users is the product model: Venice AI’s platform is built to act as an intermediary between a user and over 200 AI models. According to the company, users can choose the level of privacy they want, with different models routed through different privacy protections.

How Venice AI says it protects user data

Venice AI claims it has 3.5 million users. For models associated with OpenAI, Anthropic, xAI and Google, Venice AI says its proxy obscures users’ IP address as well as account and session data. The company also claims “other models offer higher levels of privacy,” indicating that its approach is not one-size-fits-all and may vary depending on which model is being accessed.

The core premise is that owning (or controlling) the “delivery stack” matters: if the intermediary is the part that can see traffic patterns and data flows, then that component can potentially reduce exposure to outside entities that operate the underlying model endpoints. Dragonfly managing partner Haseeb Qureshi framed the strategic stakes in those terms, arguing that whoever runs the AI delivery layer can see more about users’ behavior and ultimately influences the conditions under which users get access to powerful systems.

Where the $65 million will go

Voorhees said the Series A funding will be used to continue building Venice AI’s data center infrastructure. A central element of that plan is ownership of the compute resources—specifically, owning GPUs that power the platform—rather than renting them at higher costs.

Beyond infrastructure, Voorhees said remaining capital will support growth initiatives including expanding the customer base, entering new markets, hiring talent, and acquiring what he described as “additive businesses.” The acquisition language suggests Venice AI may be looking to broaden capabilities around its platform, though no specific targets were named in the materials provided.

Privacy scrutiny pushes privacy-focused AI into focus

Venice AI’s funding timing underscores how quickly privacy questions have become a defining topic for AI adoption. Earlier coverage from Cointelegraph reported that a user who consults an AI for legal matters could face the risk of chat logs being used against them in court. The broader theme is that AI interactions can generate sensitive records—even if users are not providing personal data intentionally.

In parallel, researchers and industry figures have proposed technical approaches to limit exposure. For example, the Ethereum Foundation’s AI lead Davide Crapis and Ethereum co-founder Vitalik Buterin proposed using zero-knowledge proofs and other techniques to help ensure that a user’s interactions with large language models are kept private.

Legal concerns have also intensified. In May, a proposed class action was filed in California federal court accusing OpenAI of disclosing private ChatGPT user data to third parties including Google and Meta. The complaint alleged that Meta Pixel and Google Analytics were embedded into ChatGPT.com, so that when users send queries, duplicate data is allegedly sent to Meta and Google along with advertising cookies and personally identifiable information—information that could then be used for targeted advertising.

These developments highlight a tension for users: modern AI platforms often involve multiple layers of data collection, analytics, and third-party integration, which can be difficult to disentangle from “model inference” itself. Venice AI’s proxy concept is an attempt to restructure that data path by introducing a dedicated intermediary that can obscure certain identifiers from model providers.

The recent industry shifts also reinforce why an intermediary approach is gaining attention. Anthropic’s sudden reduction in foreign access to two of its latest AI models earlier this month served as another reminder that availability and access controls can change quickly—while privacy-focused architectures aim to give users more predictable control over how their data is handled.

What to watch next

With Venice AI scaling its infrastructure and expanding adoption, the key question for investors and users will be how effectively its proxy-based design delivers measurable privacy protections across a wide set of models and real-world integrations. Readers should watch for more transparency around which metadata is obscured under each privacy mode, and whether Venice AI’s compute buildout translates into faster, more consistent performance without sacrificing its stated privacy goals.

The Erik Voorhees-founded Venice AI has achieved unicorn status after raising $65 million in Series A funding at a $1 billion valuation.

Led by Dragonfly and with backing from Coinbase Ventures, F-Prime, North Island Ventures, Morgan Creek and others, the funding round announced on Wednesday marks the company’s first external capital raise since launching in 2024.

The fundraising came in the same month Anthropic was forced to suddenly cut foreign access to two of its latest AI models, and comes just weeks after OpenAI was accused in a class-action lawsuit for sharing ChatGPT data with third parties, highlighting the potential appeal of privacy-focused AI platforms.

“This capital will be used to uphold the First and Fourth Amendments to the Constitution as they relate to mankind’s interaction with AI,” Voorhees said in an X post on Wednesday.

The First Amendment is part of the United States Constitution protecting five essential freedoms including the freedom of speech. The Fourth Amendment protects people from unreasonable searches and seizures by the government.

Venice AI courts privacy-focused users

Venice AI, which claims to have 3.5 million users, offers access to over 200 AI models but adds a proxy between the user and the models and allows users to choose the level of privacy they want.

For models from OpenAI, Anthropic, xAI and Google, the proxy obscures users’ IP address, account and session data. Other models offer higher levels of privacy.

Source: Erik Voorhees

“Control over intelligence is the defining fight of the coming decade,” Haseeb Qureshi, managing partner at Dragonfly, said on Wednesday.

“Whoever owns the AI delivery stack owns a direct window into your interior life. They log all your chats, train on them, and will hand them over when asked. And in the end, they decide the terms on which you’ll get to access the most powerful systems humankind has ever built.”

Voorhees said the capital will be used to further build out its own data center infrastructure, owning the GPUs that power its platform rather than being forced to rent them at higher costs.

The remaining capital will be used to grow its customer base, enter new markets, hire talent and acquire “additive businesses,” he added.

Venice Token rose 6% on Wednesday. Source: X

AI privacy concerns in spotlight

The capital raise comes amid mounting concerns over user privacy when using AI models.

Earlier this year, lawyers told Cointelegraph that a user consulting an AI for legal matters could have their chat logs used against them in court.

Related: AI’s power crunch turns Bitcoin miners’ grid access into an asset

In February, Ethereum Foundation AI lead Davide Crapis and Ethereum co-founder Vitalik Buterin proposed a way to use zero-knowledge proofs and other methods to ensure that a user’s interactions with large language models are private.

Conversations about privacy when using AI were stirred again in May, when a proposed class action was filed in California federal court accusing OpenAI of disclosing private ChatGPT user data to Google and Meta.

The complaint alleged that OpenAI embedded Meta Pixel and Google Analytics into the ChatGPT.com website, so that when a user sends a query, the website allegedly sends duplicate data to Meta and Google alongside advertising cookies and personally identifiable information, which is then used to target advertisements to the user.

Magazine: Bitcoin slides to $58K, XRP hits $1 but onchain data promising: Market Moves

Meta’s plan to sell surplus computing power hit chip stocks hard on Wall Street. Meta’s own shares climbed nearly 9% on the news.

The announcement flipped years of assumed AI compute scarcity into a supply warning. It erased billions in semiconductor and neocloud value in a single session.

A Supply Signal Rattles Wall Street

Meta is building a business called Meta Compute. The unit will lease idle data center capacity to outside clients. The approach mirrors SpaceX’s model. SpaceX has rented spare capacity to firms including Anthropic.

For years, investors rewarded chip suppliers on one premise. They believed AI demand always outstripped supply. Meta’s admission of excess capacity broke that premise. Recent Nvidia institutional money flow data already show large investors pulling back.

Micron sank more than 10% on July 1. SanDisk, Intel and AMD each lost between 6.9% and 10.6%. Nvidia slipped just 1.25%, a modest decline that stood out against the broader rout.

Neoclouds and Big Tech Diverge

CoreWeave and Nebius rent GPU capacity to AI developers and saw their stocks fall 14% and 17% respectively on fears that Meta will undercut their pricing.

Meta has paid for similar cloud services before, but its shift into the same business now puts it in direct competition with its own vendors.

Other Magnificent 7 members gained ground. Apple, Microsoft, Amazon, Alphabet and Tesla all closed higher as some strategists link the split to AI spending cycle winners rotating away from pure hardware plays.

South Korea Feels the Spillover

The sell-off spread to Asia as Samsung and SK Hynix memory stocks fell more than 7% and 9% respectively in early trading and the KOSPI triggered another trading halt. The move extended a pattern from a prior Big Tech selloff spillover that hit Asian chipmakers earlier this year.

The post Meta Compute Launch Sends AI Compute Stocks Tumbling Globally appeared first on BeInCrypto.

Modern day crypto trading has become a deeply fragmented battleground that favors the institutional algorithms and punishes the retail trader. On one hand, there are high-frequency funds exploiting total visibility over public order books; on the other hand, ordinary market participants are forced into transparent matching pools where their pending stop-losses are openly hunted. Ouinex, a community-backed multi-asset platform, is trying to eliminate this structural asymmetry to shield retail orders from predatory manipulation.

Summary

- Ouinex says its Fair Execution Engine separates retail orders from institutional liquidity providers to reduce exposure to predatory trading strategies.

- The platform combines crypto markets with stock indices, commodities, forex, and equities through one interface with leverage of up to 500x.

- Ouinex says its OUIX token excludes venture capital allocations and uses trading based incentives instead of early institutional distribution.

For retail crypto traders, the core operational hurdles boil down to having to pit their personal portfolios against institutional-grade execution power, which creates a highly uncompetitive scenario where the everyday investor is structurally outmatched from the start. That’s the technological disparity Ouinex is trying to address.

“If I’m an institution that has 20 traders working around the clock with a trading infrastructure that is worth multi-million dollars with low latency, and I’m trading against the retail guy that’s sipping a coffee at Starbucks on his Wi-Fi, who do you think is going to win the battle? It’s a little bit like you’re swimming in a pool and you’re the little fish and there are sharks,” Ouinex CEO Ilies Larbi told crypto.news during an interview.

Professional trading venues typically rely on what is called a Central Limit Order Book, or CLOB. What this does is it matches bids and offers systematically to execute transactions.

On traditional platforms like Nasdaq or NYSE, retail investors are structurally insulated from the raw matching engine. Regular retail orders are typically routed through intermediary brokers or internalized by market wholesalers, meaning everyday retail capital rarely interacts directly with predatory institutional algorithms on the public book.

However, when this same methodology is transplanted across crypto trading venues, that protective buffer disappears. Most crypto platforms force everyday retail accounts and hyper-capitalized automated market makers onto the exact same matching engine, creating what Larbi calls an “absolutely unfair environment” for the retail trader.

This has been the core structural friction that has led Larbi and his team to come up with their proprietary Fair Execution Engine, which, simply said, drops the central limit order book for a more isolated, retail-protected matching model.

“We have built this Chinese wall between retail clients and institutions,” Larbi said, trying to explain the technology in layman’s terms.

What the Fair Execution Engine does is continuously scan and filter incoming institutional quotes in real time, thereby creating the hypothetical Chinese wall that keeps sensitive retail order details safely hidden on internal servers. As a result, the external trading algorithms cannot query a public order book to map out pending positions, and artificial liquidation hunts become mechanically impossible.

“Our retail users are fully protected because institutions cannot take liquidity on our platform, they’re only allowed to make markets, and that’s it. They don’t have access to things like stop losses or limit orders, because everything is sitting on our servers, and orders only get sent for execution once the market reaches that level.”

More than just crypto trading

Neutralizing predatory execution solves only half the equation for a modern brokerage, as sustaining active trader volume requires looking beyond a purely digital asset class. The modern day trader is always looking out for diverse financial instruments that can be accessed directly on a single platform without having to move capital in and out every time an opportunity arises outside the crypto arena.

We have already seen this structural integration materialise across several digital asset platforms that now offer traditional financial instruments like commodities, stock indices, and fiat pairs alongside native tokens.

Larbi agrees that “mixing” the two landscapes is the correct approach, especially with how recent geopolitical events have boosted traditional financial volumes while crypto activity has remained sidelined.

However, Ouinex is taking a different approach compared to what most crypto exchanges do when introducing traditional assets through a perpetual framework, which, according to Larbi, “doesn’t offer much liquidity” in most cases because they synthesize entirely new contracts rather than tapping into mature and established markets.

“What we’ve done is used traditional financial infrastructure to provide these instruments through a system that has existed for the last 50 years. On Ouinex, for example, when you trade TradFi, you’re basically trading at a cost that is about seven times cheaper than anything related to perpetuals, in a market that is approximately 20 times more liquid.”

Citing Hyperliquid as an example, Larbi noted that utilizing traditional financial plumbing makes trading the euro-dollar pair roughly seven times cheaper on Ouinex.

Furthermore, the executive pointed out that this infrastructure secures approximately $5 million in top-of-the-book liquidity, which represents a significantly deeper pool of available capital when compared to the mere $100,000 in depth of market on the competing venue.

As of publication time, besides the multiple crypto native instruments, Ouinex offers traditional instruments like stock indices, commodities, foreign exchange, and equities. Users can navigate all these asset classes through a unified interface that supports up to 500x leverage.

Eliminating predatory venture capital allocations

It’s not just market execution pipelines where Ouinex is taking a defensive posture to safeguard retail participants. Larbi also drew attention to token launch dynamics, flagging structural allocation manipulation as a serious issue fueling the “pump and dump schemes” that has been rampant throughout the ecosystem, especially during the years lacking clear crypto regulation.

“Exchange gets an allocation, VC gets an allocation, the founder spends money on marketing to hype the project, retail clients come in and buy, buy, buy, buy, buy. Once the market goes up, the exchange or the VC just dumps. They make millions. Retail people just lose money, right? That’s just the reality of 90% of what’s been happening in the crypto market.”

Addressing this structural misalignment required rewriting the tokenomics architecture for the platform’s native utility token, OUIX ($OUIX), from scratch. According to Larbi, Ouinex has completely excluded venture capital funds from the token’s distribution ledger, thereby preventing early-stage institutional dump pressure post-listing.

“We decided not to include any type of VCs in any of our token allocations, so no VC has a token allocation,” Larbi stated.

Additionally, operating a native trading ecosystem allows the firm to host its own token listing, bypassing the extortionate, unvested supply demands typically levied by third-party centralized exchanges. Retaining the asset entirely within its internal ecosystem forces the management team to assume full accountability for market stability, ensuring retail users are never treated as corporate exit liquidity.

“Because we are an exchange, we don’t need to actually go to another exchange to list the token… we make ourselves responsible fully for the performance of the token,” he added.

Instead of relying on traditional, one-off marketing promotions that attract temporary speculative hype, the exchange structures its token distribution through an active incentive model tied directly to network usage.

Participants can complete basic social tasks and accumulate NEX Points by engaging in either demo or live trading environments and then claim campaign payouts in OUIX or other supported cryptocurrencies at the end of each recurring campaign.

Targeting a lean ecosystem of dedicated traders

In his concluding remarks, Larbi said that Ouinex does not plan on competing against mass-market exchange giants that have already accumulated millions of casual, low-volume retail accounts. Instead, the platform wants to prioritize building a highly concentrated user base composed entirely of dedicated market participants.

“My goal is to go after 50,000 or 100,000 of the right users, people that are true traders that trade the market, and that’ll be enough for me to do right. So, if in two years we’re able to accomplish this, I’ll be absolutely happy. It’s a leaner operation, more quality traders, more revenue with less obviously operational cost, and that’s where you know we were trying to position, that’s how we’re trying to position Ouinex.”

According to company documents shared with crypto.news, Ouinex has raised over $9 million through a combination of community-equity financing and pre-sale rounds, establishing a base of over 5,000 retail and professional community investors with zero VC capital involved.

The platform is operated by an executive team averaging more than 25 years of experience in legacy financial systems and brokerage markets. It currently operates across multiple jurisdictions, with active compliance entities maintained in South Africa, Australia, Poland, and Saint Vincent and the Grenadines.

The architecture of the native OUIX ($OUIX) token introduces a deflationary mechanism sustained by trading fees generated across more than five asset classes. To safeguard the asset’s long-term market health, the tokenomics framework places over 50% of the pre-sold supply under a strict three-year cliff lockup schedule.

A record run of mega-listings is pulling hundreds of billions in fresh equity supply into the market. The fear is that the money to buy it comes partly out of crypto. The truth is more tangled than the timeline suggests.

Summary

- SpaceX completed the largest IPO in history in June 2026, and anticipated listings from OpenAI and Anthropic could bring the wave of new equity supply above $240 billion by year-end.

- The core worry is mechanical: an IPO does not create new money, so investors sell existing holdings to fund allocations, and crypto is among the easiest assets to liquidate quickly.

- The evidence for a drain is real: Bitcoin fell hard around the SpaceX listing, spot Bitcoin ETFs posted a record $4.5 billion of outflows in June, and higher-beta altcoins took the most damage.

- The evidence against a simple story is just as real: the same weeks brought a sharp equity selloff, geopolitical shocks, and a hawkish Fed, so macro, not the IPOs alone, drove much of Bitcoin’s drop.

- The likely answer is that the wave is a genuine short-term headwind that competes with macro forces, and whether it becomes a lasting drain depends on flows reversing once the deals are digested.

There is an obvious villain in crypto’s rough summer. SpaceX carried out the biggest IPO ever, OpenAI and Anthropic are lining up behind it, and Bitcoin fell through the same window. The story writes itself: the mega-IPO wave is a giant vacuum, sucking capital out of digital assets to fund the hottest listings in a generation. The mechanism is plausible, the timeline lines up, and the fear is widespread.

But correlation this clean often hides a messier truth, and the question deserves more than a chart with two lines pointing opposite directions. This piece lays out the scale of the wave, the mechanism behind the drain thesis, the evidence for it, the macro confound that complicates it, and what would tell us which force is really in control. It also looks at the strange counterpoint that the same IPO wave pulling liquidity from crypto is also pushing equity-like speculation onto crypto rails. The result is not a clean bullish or bearish answer, but a liquidity map.

The scale of the wave

Start with the numbers, because they are genuinely large. SpaceX went public around June 12, 2026, targeting roughly $75 billion at a valuation near $1.75 trillion, the largest listing in history, with reported demand exceeding $250 billion. Behind it sit two of the most anticipated technology debuts in years, OpenAI and Anthropic, whose listings and fundraising are expected to pull in tens of billions more. One estimate puts the combined new equity supply from this cluster above $240 billion by year-end.

That figure is what makes the drain thesis credible. Markets absorb new supply by finding buyers, and buyers need cash. When the supply arriving is measured in hundreds of billions and concentrated in a short window, the question of where the money comes from stops being academic. The wave is not one event but a sequence, which is why the concern is less about any single listing and more about the cumulative pull of several mega-deals stacking up across the same months.

For crypto readers, SpaceX’s Bitcoin position on public markets matters because it complicates the simple drain story. SpaceX did not only pull money from risk assets; it also brought 18,712 BTC onto the balance sheet of a public-market giant. That makes the listing both a competitor for crypto liquidity and a legitimizing event for Bitcoin as a corporate asset. The tension between those two effects is the core of the debate.

The mechanism: an IPO does not create new money

The heart of the drain argument is a simple truth that is easy to forget in a rally. An IPO does not print new money into the system. It transfers existing capital from investors into a newly public company and its early backers. To buy into a hot offering, investors free up cash, and they free up cash by selling something they already own.

Crypto is a prime candidate for that selling, because it trades around the clock and can be liquidated fast when someone needs capital in a hurry. The mechanism has several strands. Retail overlap is one: a large share of the SpaceX allocation targeted retail investors, a group that overlaps heavily with active crypto participants, so some of the money chasing shares comes straight out of crypto positions. Index-fund mechanics are another: once a giant company enters the indices, funds tracking those benchmarks are forced to buy billions of its shares, and because they hold little spare cash, they raise it by selling existing positions.

Institutional rebalancing is the third: funds holding Bitcoin through ETFs face a choice about trimming crypto to fund IPO allocations. Each strand points the same way, toward selling pressure on liquid risk assets, with crypto near the front of the line. That is why how ETF flows move the market matters in this context. When crypto ETF shares are sold to raise cash, the effect is not abstract; it removes a real bid from the market.

The evidence for a drain

The tape offers real support for the thesis. Around the SpaceX filing and listing, Bitcoin fell roughly 20% and slipped under $60,000, and the broader crypto market bled with it. The clearest institutional signal came from the funds: U.S. spot Bitcoin ETFs recorded about $4.5 billion of net outflows in June 2026, the worst month since the products launched, removing the steady bid that had cushioned earlier drops. Crypto ETFs had already seen billions in outflows the month before.

Analysts explicitly cited capital rotation and the SpaceX IPO among the drivers of the redemptions. The pattern extended beyond Bitcoin. Space and hard-tech stocks rallied in the same weeks that crypto slid, a visual rotation from digital assets into aerospace and AI exposure. And altcoins fared worse than Bitcoin, consistent with the idea that investors raising cash sell their highest-beta positions first.

Taken together, the outflows, the rotation into listing-adjacent equities, and the outsized altcoin damage form a coherent picture of capital leaving crypto as the IPO wave built. It does not prove the IPO wave caused all of the selloff, but it proves the drain thesis has more than vibes behind it. The timing, the flow data, and the asset-performance pattern all point in the same direction. The next question is whether they point only to the IPO wave or to a broader risk-off event that happened to arrive at the same time.

The evidence against a simple story

Here is where the clean narrative frays. The same weeks that saw Bitcoin fall also delivered a broad risk-off shock that had nothing to do with any IPO. Equity markets sold off sharply, with the Nasdaq posting one of its worst single days of the year and AI bellwethers dropping as bubble fears flared. Geopolitics piled on, with missile exchanges in the Middle East pushing oil higher and stoking the inflation fears that keep the Fed hawkish.

Under a hawkish Fed, with markets pricing a strong chance of a December rate hike as inflation drifts back up, risk assets were under pressure across the board. Bitcoin, which trades far more like a high-beta risk asset than like digital gold, did what every speculative position did in that environment: it got sold. When it recovered, it recovered on macro news, not on IPO mechanics. That sequence exposes the flaw in blaming the listings alone.

The IPO wave competed with genuine global risk-off conditions, and it is close to impossible to cleanly separate how much of Bitcoin’s drop came from capital rotating into SpaceX versus capital fleeing risk in general. Correlation with the IPO timeline is not proof of causation when a dozen other bearish forces arrived at once. That is why the Bitcoin market backdrop still matters more than any single listing. If macro remains hostile, even a completed IPO wave will not automatically restore crypto liquidity.

The rotation-back case

The drain thesis also has a time limit that its loudest versions ignore. An IPO is a one-time reallocation, not a permanent siphon. Once allocations are funded and the deals are digested, the selling pressure fades, and the capital that rotated out can rotate back. If the listings price well and risk sentiment improves, the same investors who sold crypto to fund IPO positions may redeploy into digital assets, turning a short-term headwind into a medium-term tailwind.

There is a structural sweetener too. SpaceX carried a multibillion-dollar Bitcoin position onto public markets, so every new shareholder gained indirect exposure to the asset, and a successful debut could encourage other pre-IPO companies to hold and disclose Bitcoin to court crypto-friendly investors. In that scenario, the IPO wave ends up expanding the base of Bitcoin holders rather than shrinking crypto’s capital. The drain, if it is one, may be the front end of a cycle that feeds back into the asset it briefly pulled from.

This is why the rotation-back case should not be dismissed, even if it is slower than the drain. Liquidity can leave quickly and return gradually. The first leg shows up as selling pressure, ETF outflows, and weaker altcoins. The second leg would show up later, through renewed ETF inflows, higher risk appetite, and capital moving back down the crypto risk curve once the IPO allocations have settled.

Why altcoins bear the brunt

If there is a drain, its incidence is uneven, and that unevenness is itself informative. Bitcoin is the deepest, most liquid crypto asset and the one institutions hold through ETFs, so it absorbs pressure but also attracts the first capital back. Altcoins are higher-beta and thinner, which means investors raising cash tend to liquidate them first and rebuild them last. That dynamic delays any altcoin season and concentrates the pain in the long tail of the market, even when Bitcoin itself is only mildly affected.

For readers trying to gauge the wave’s impact, the altcoin-versus-Bitcoin spread is a useful tell. If the drain is real and ongoing, altcoins keep underperforming as capital stays parked in equities. If the pressure is easing, the higher-beta names are where the recovery shows up first once risk appetite returns. The brunt falling on altcoins is both a symptom of the drain and an early indicator of its reversal.

The reason is behavioral as much as mechanical. In a cash-raising event, investors usually sell what is liquid, volatile, and easiest to replace later. That puts altcoins near the front of the liquidation queue. It also means a later altcoin rebound would be meaningful, because it would suggest the market has moved from forced cash-raising back into risk-taking.

What to watch

The debate does not resolve with a single number, but a few signals will show which force is winning. ETF flow direction is the clearest: a return to sustained net inflows would signal the drain is over and capital is coming back, while continued outflows would confirm the pressure persists. The timing of the OpenAI and Anthropic listings is the second: if they cluster into the same window, the cumulative supply shock intensifies, whereas spacing them out softens it. The third is whether post-deal capital actually rotates back after SpaceX is digested, the test of the rotation-back thesis.

The fourth is Bitcoin’s behavior around its support in the high $50,000s to $60,000 range, since holding there through the wave would suggest the selling is absorbable, while breaking down would suggest the drain is compounding other bearish forces. And the fifth is the macro backdrop, because as long as the Fed stays hawkish and risk-off conditions dominate, it will be hard to blame crypto weakness on the IPOs alone. Watched together, these signals separate a temporary reallocation from a structural outflow, which is the distinction that actually matters. One rough rule: if ETF flows turn positive while altcoins stop underperforming, the IPO drain is probably fading.

The harder signal is whether the IPO wave changes investor preference, not just investor positioning. A temporary drain means investors sold crypto to fund new listings and later returned. A structural drain would mean they now prefer listed AI and hard-tech exposure over crypto as their main risk-on trade. The first is a headwind; the second would be a deeper challenge.

The pre-IPO perps signal

One of the most revealing threads in this story has nothing to do with the drain itself and everything to do with where financial infrastructure is heading. Before SpaceX shares ever reached Wall Street, crypto exchanges rolled out pre-IPO perpetual futures tied to the expected listing, letting traders bet on the valuation through crypto rails. The activity was substantial, and the price action was wild: one pre-IPO SPCX perpetual fell sharply from its listing high as speculation swung, showing both the demand for the exposure and its volatility. Crypto venues, in other words, became the first place retail could trade SpaceX at all.

That detail reframes the whole liquidity question. The same infrastructure that the drain thesis says is losing capital to equities is simultaneously absorbing equity-style trading onto crypto rails. If pre-IPO perps on tokens and stocks become a durable product, then crypto exchanges are not just donors of liquidity to the IPO wave; they are also venues capturing a slice of the speculative interest the wave generates. The relationship between crypto and the mega-listings is more two-way than a one-directional siphon, which complicates the simple picture of capital flowing out and not coming back.

It also hints at a longer arc. As tokenized and pre-IPO markets mature, the line between trading a stock and trading a token blurs, and the platforms that started in crypto are positioned to sit in the middle of that convergence. The IPO wave may pull spot capital out of Bitcoin in the near term while pushing trading volume and relevance toward crypto-native infrastructure at the same time, a nuance the drain narrative misses entirely. For readers new to the product, the pre-IPO perps market sits inside the broader world of perpetual futures, where traders can take synthetic exposure without owning the underlying asset.

Lessons from past capital events

History offers a rough template for how these episodes resolve, even if no two are identical. Large capital events that pull attention and money toward a specific opportunity tend to produce a front-loaded effect: the pressure is heaviest in the run-up and immediate aftermath, when investors are raising cash and reallocating, and it eases once the event is digested and positions settle. The reallocation is a one-time transfer, not a permanent change in how much capital exists, so the assets that gave up liquidity often see some of it return once the opportunity is fully priced. The variable that decides whether the return happens quickly is the macro environment.

In a risk-on backdrop with ample liquidity, a big IPO gets absorbed with little lasting damage to other assets, because there is enough capital to fund the new supply without deep selling elsewhere. In a tight, risk-off backdrop like mid-2026, the same IPO bites harder, because investors are already defensive and more willing to sell liquid positions to raise cash. The current wave is landing in the harder version of that setup, which is part of why its effect on crypto feels sharp. The same deal that might have been absorbed cleanly in a looser market becomes a visible drain when liquidity is already scarce.

The practical lesson is to separate the temporary from the structural. A front-loaded drain that reverses once the deals clear is a headwind to trade around, not a reason to abandon the asset class. A structural shift, where capital permanently prefers listed innovation stocks over crypto, would be a bigger deal, but it requires evidence beyond a few months of correlated moves. So far, the pattern looks more like a large, concentrated reallocation arriving into an already-weak market than proof of a lasting migration, which is why the flows in the months after the listings matter more than the drawdown during them.

Who actually gets drained, and who does not

A subtlety the blunt drain thesis misses is that not all crypto capital is equally at risk of being pulled into an IPO. The money most likely to rotate out is the marginal, liquid, opportunistic kind: leveraged traders, short-term speculators, and investors who hold crypto as one line in a broader risk portfolio and will happily sell it to chase a hot listing. That is exactly the capital that flows through the venues showing the most stress, and its exit shows up fast in falling open interest and higher volatility.

The capital least likely to leave is the opposite: long-term holders, self-custody accumulators, and conviction buyers who treat Bitcoin as a multi-year position instead of a source of dry powder for equities. The exchange-outflow data discussed above suggests this cohort has been buying weakness even as the speculative money leaves, which means the drain is concentrated in the flighty end of the market and cushioned at the sticky end. That split matters for how deep and how lasting any drain can be, because a market losing its weak hands while its strong hands accumulate is behaving very differently from one where everyone is heading for the exits.

There is a geographic and structural layer too. The retail overlap that funds IPO allocations is heaviest in the markets and platforms where the same investors trade both stocks and crypto, so the drain is not uniform across the world or across venues. Institutions holding Bitcoin through ETFs face a cleaner rebalancing decision than a self-custody holder in a jurisdiction with limited access to the SpaceX offering, who may have no easy way to swap one for the other even if they wanted to. The result is that the drain is real but uneven, biting hardest where crypto and equity trading overlap and barely at all where they do not. For anyone trying to size the effect, the question is not whether capital is leaving, but which capital, and the answer, that it is mostly the liquid and opportunistic kind, is part of why the impact may prove more temporary than the headline drop suggests.

Frequently asked questions

How big is the IPO wave?

SpaceX completed the largest IPO in history in June 2026, targeting roughly $75 billion at a valuation near $1.75 trillion, with reported demand above $250 billion. Anticipated listings and fundraising from OpenAI and Anthropic could push the combined new equity supply from this cluster above $240 billion by year-end, concentrated into a relatively short window. That is why the drain thesis is being taken seriously: the scale is too large to ignore. The issue is whether the money comes mainly from crypto, from broader equities, or from cash and other liquid holdings.

Why would an IPO drain crypto liquidity?

Because an IPO does not create new money. Investors fund allocations by selling assets they already own, and crypto is easy to liquidate quickly. Retail buyers overlap with crypto holders, index funds are forced to buy the new shares by selling other positions, and institutions may trim Bitcoin ETF holdings to raise cash. Each channel points to selling pressure on liquid risk assets. Crypto sits near the front of that line because it trades 24/7, has deep venues, and is often held by investors who also chase high-growth tech listings. That does not mean every dollar funding the IPO wave comes from crypto. It means crypto is one obvious source of dry powder when investors need cash quickly.

Is there proof the drain is happening?

There is supporting evidence, not proof. Bitcoin fell around the SpaceX listing, spot Bitcoin ETFs saw a record $4.5 billion of outflows in June 2026, space stocks rallied as crypto slid, and altcoins underperformed. Analysts cited capital rotation and the IPO among the drivers. But the same period brought a broad risk-off shock, so the IPO cannot be cleanly isolated as the cause. The cleaner way to frame it is that the IPO wave was one headwind among several. It likely added pressure at the margin, especially through ETF outflows and altcoin selling. But macro conditions, Fed expectations, equity weakness, and geopolitical stress were also moving risk assets at the same time.

What else could explain Bitcoin’s drop?

Macro forces that arrived at the same time. Equity markets sold off sharply, AI stocks fell on bubble fears, geopolitical tension pushed oil higher, and a hawkish Fed pricing a likely December rate hike pressured risk assets broadly. Bitcoin trades like a high-beta risk asset, so it got sold in that environment regardless of the IPO wave. Macro and the listings are hard to separate. This matters because blaming only the IPO wave can lead to the wrong read. If the drop was mainly macro, then even after the listings clear, crypto can stay weak until risk appetite improves. If the drop was mainly IPO funding pressure, flows should recover once the deals are digested. The market’s next move depends on which force dominates.

Could the IPO wave actually help crypto later?

Yes, potentially. An IPO is a one-time reallocation, not a permanent siphon. Once deals are funded and digested, capital that rotated out can rotate back, especially if listings price well and risk sentiment improves. SpaceX also carried Bitcoin onto public markets, giving new shareholders indirect exposure and possibly encouraging other pre-IPO firms to hold and disclose Bitcoin. That is where the corporate-Bitcoin angle becomes relevant. If large public companies normalize holding BTC, the long-term adoption signal can offset some of the near-term liquidity drain. The question is whether that normalization is strong enough to matter for flows, not merely for narrative.

Why do altcoins get hit harder than Bitcoin?

Altcoins are higher-beta and less liquid, so investors raising cash tend to sell them first and rebuild them last. Bitcoin is deeper and held through ETFs, so it absorbs pressure but also draws capital back first. That dynamic concentrates the pain in altcoins and delays any altcoin season, which is why the altcoin-versus-Bitcoin spread is a useful gauge of the drain. If altcoins keep underperforming after the IPO allocations settle, the pressure is probably not over.

What signals show whether the drain is easing?

The clearest is ETF flow direction: a return to sustained inflows would signal capital coming back, while continued outflows would confirm ongoing pressure. Also watch the timing of the OpenAI and Anthropic listings, whether capital rotates back after SpaceX is digested, Bitcoin’s behavior around its support, and the macro backdrop, since a hawkish Fed keeps risk assets pressured independently. The altcoin-versus-Bitcoin spread is another useful tell. If higher-beta crypto starts recovering first, the forced cash-raising phase may be ending.

Does an IPO wave always pull money from crypto?

Not necessarily. The effect depends on overlap between IPO buyers and crypto holders, the size and timing of the deals, and the macro environment. In a risk-on market with ample liquidity, large IPOs can be absorbed without much crypto selling. In a tight, risk-off market like mid-2026, the overlap and the cash needs make crypto a more likely source of funding, amplifying the effect. The SpaceX, OpenAI, and Anthropic wave is unusual because the listings are large, concentrated, and aimed at the same risk-seeking investor base that often owns crypto. That makes the drain plausible. It still does not make it the only driver of crypto weakness.

Disclaimer: This article is for information purposes only and does not constitute financial, investment, or trading advice. Cryptocurrency prices are highly volatile, and market analysis is speculative and can change quickly. Nothing here is a recommendation to buy or sell any asset. Always do your own research and consider consulting a licensed professional before making financial decisions. Figures are accurate as of July 1, 2026, and will change.

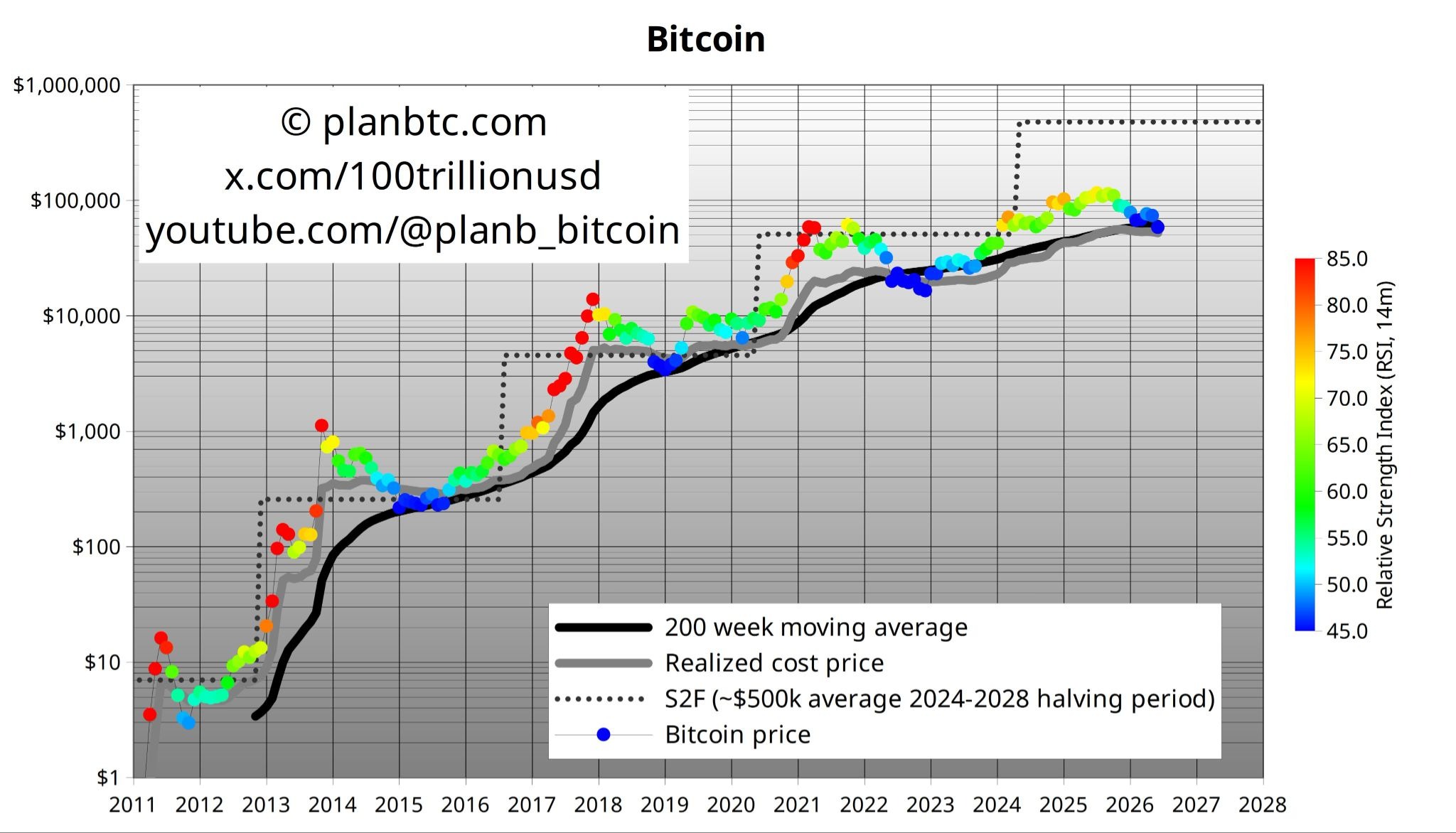

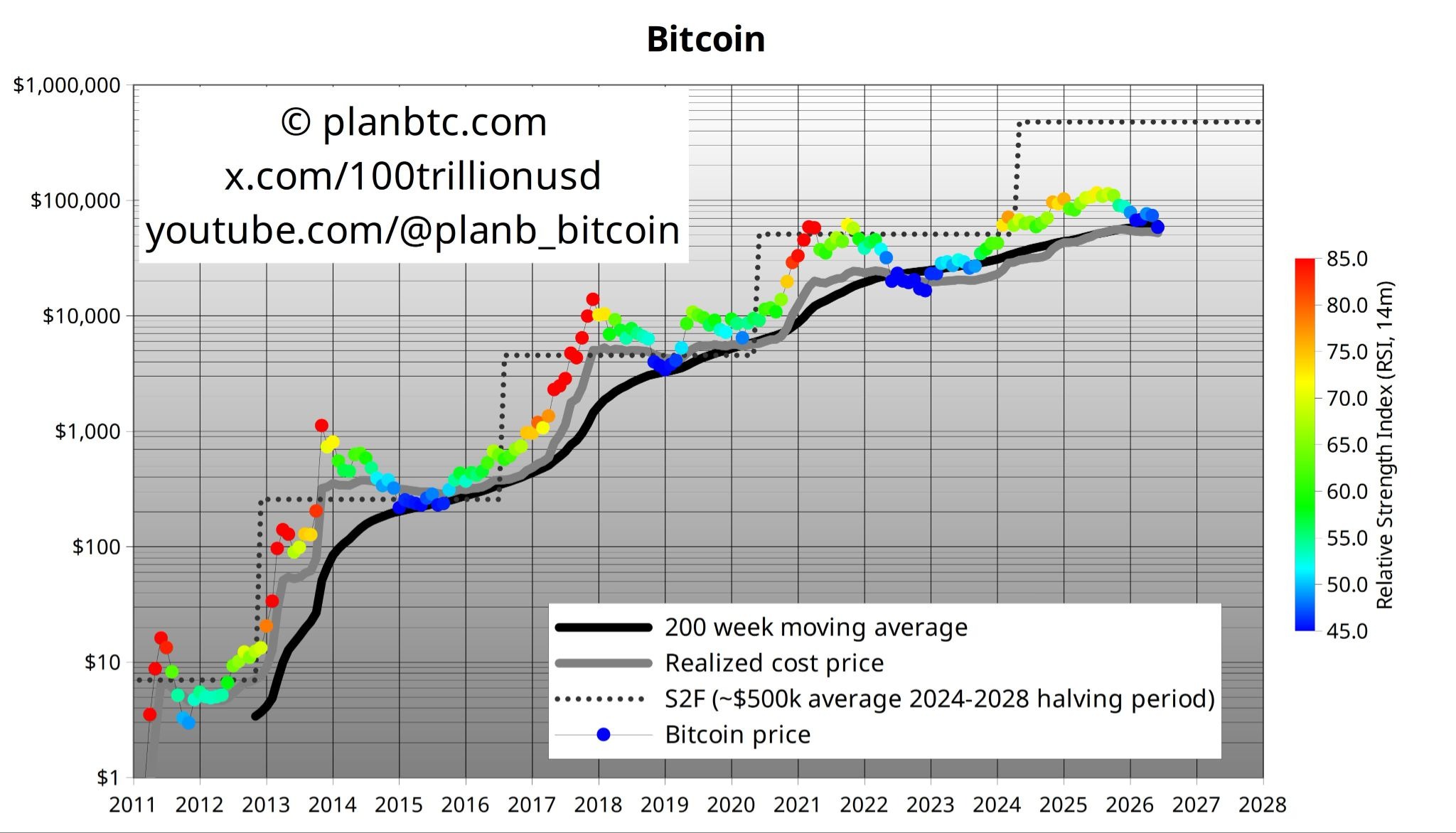

Bitcoin could face further downside pressure after ending June below its 200-week moving average but above its realized price, a combination that crypto analyst PlanB says suggests the market has yet to reach a bear market bottom.

Bitcoin fell 20.5% in June to close the month at $58,526 — its worst monthly performance since June 2022 — below its 200-week moving average of $62,000 but above its realized price of $52,000.

“ALL previous bear market bottoms were below realized price,” said PlanB, the creator of the stock-to-flow pricing model, on Wednesday, adding in a separate post that Bitcoin could drop to $52,000.

The price move would mean Bitcoin falling about 60% from its all-time high of $126,000 in October. The dip could be even deeper, as previous bear markets have seen Bitcoin fall even further, such as 83% in 2018 and 76% in 2022.

BTC is undervalued but can still go lower

“Right now, price is much lower than value and indeed might go lower from here (below realized),” PlanB said. “So, Bitcoin is undervalued but can still go lower.”

BTC is trading between the 200-week moving average and the realized price. Source: PlanB

Bitcoin’s realized price is the aggregate cost basis of all coins in circulation, calculated by valuing each unspent transaction output (UTXO) at the price when it last moved on-chain. It represents the average price at which holders acquired their coins, serving as a key onchain metric for support levels during bear markets.

Related: Bitcoin bounces off 21-month low, but leverage data signals caution: Was $57K the bottom?

Andri Fauzan Adziima, research lead at Bitrue Research Institute, told Cointelegraph that the June close above realized price but below the 200-week moving average “signals the bear bottom is still ahead per prior cycles.”

“I’m eyeing late-2026 capitulation there before the next leg up, though shallower this cycle due to institutions,” he said.

Lacie Zhang, research analyst at Bitget Wallet, told Cointelegraph that the current consolidation near $60,000 is “approaching a potential bottom zone, with strong historical and technical support likely forming around the $55,000 level if further downside occurs.”

Midterm year market bottom

ITC Crypto founder Benjamin Cowen also speculated there could be a cycle bottom for Bitcoin this year, given it is a US midterm election year. This has previously coincided with bear market bottoms in 2018 and 2022.

“The second half of midterm years usually marks the accumulation zone/market cycle bottom,” he said.

The US midterms are scheduled for Nov. 3, when all House of Representatives seats and about a third of Senate seats are up for election.

Magazine: Bitcoin slides to $58K, XRP hits $1 but onchain data promising: Market Moves

Medtronic notifies customers impacted by ShinyHunters data breach

Furious USA boss Mauricio Pochettino’s immediate reaction to World Cup red card

SoftBank’s LY, Bain raise Kakaku bid again with $4.1 billion valuation

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Staud – Corporette.com

-

Politics6 days ago

Politics6 days agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Crypto World2 days ago

Crypto World2 days agoStrategy authorizes up to $1.25B in Bitcoin sales under new capital plan

-

Politics6 days ago

Politics6 days agoPotential 2028er World Cup attendee leaderboard

-

Business6 days ago

Business6 days agoAsia stock markets slide as tech shares slump

-

News Videos3 days ago

News Videos3 days agoMAJOR BITCOIN & MARKET UPDATE!!!! (MUST WATCH ASAP!!!)

-

Tech6 days ago

Tech6 days agoA Look At A Gaggle Of Transputer Boards

-

Crypto World6 days ago

Crypto World6 days agoDell (DELL) Shares Tumble Over 5% Following Analyst Downgrade to Hold

-

Crypto World5 days ago

Crypto World5 days agoCoinbase, Circle Deepen Crypto Stock Losses Despite Resilient S&P 500

-

Business2 days ago

Business2 days agoAustralia treasurer says alleged access of prime minister’s bank data ’incredibly concerning’

-

Crypto World5 days ago

Crypto World5 days agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Sports5 days ago

Sports5 days agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Crypto World6 days ago

Crypto World6 days agoBitcoin Sparks $600M Hourly Liquidations With $65,000 Set To Become Resistance

-

Tech4 days ago

Tech4 days agoBluekit phishing kit adopts browser-in-the-middle for login theft

-

Tech2 days ago

Tech2 days agoAnonymous researcher drops 0-day ‘exploitarium’ repo

-

Tech5 days ago

Tech5 days agoRussian hackers now target Signal backup recovery keys

-

Crypto World6 days ago

Crypto World6 days agoHyperliquid Named on Singapore MAS Investor Alert Register

-

Crypto World5 days ago

Crypto World5 days agoRTX holders must register wallets before token distribution begins

-

Sports16 hours ago

Sports16 hours agoBroncos roster: OL Ben Powers (No. 74) entering final year of contract

-

Business2 days ago

Business2 days agoThe AI boom won’t burst all at once. It will pop in ‘rolling bubbles’: Macquarie

You must be logged in to post a comment Login