Crypto World

Binance Locked Out of Europe on July 1: What Happened

The world’s largest crypto exchange will suspend services for European Union users from July 1 after failing to secure a license under Europe’s new crypto rules. The headlines say Binance is leaving Europe. The reality is more precise, and more revealing: it was locked out, and the reason was not its paperwork but its past.

Summary

- From July 1, 2026, Binance will suspend most services for European Union residents, halting new orders, deposits, sign-ups, and staking products, after failing to obtain a license under the EU’s MiCA regulation by the June 30 deadline.

- This is a suspension, not a permanent exit: user funds remain safe and withdrawable, and Binance says it intends to secure an EU license and return in the coming months.

- Binance bet on Greece as its entry point, but on June 24, it withdrew its application one week after reports that the Greek regulator was preparing to reject it.

- The rejection reportedly turned on Binance’s past, not its paperwork, in particular its history of penalties and whether co-founder Changpeng Zhao could pass MiCA’s “fit and proper” test for owners and managers.

- The episode shows MiCA has teeth: of more than 3,000 crypto firms in Europe, only around 210 secured authorization, with rivals like Coinbase, Kraken, and OKX passing, while the largest exchange in the world was shut out.

On June 24, an email from Binance landed in the inboxes of millions of European users, and within hours, it had set off a wave of alarm across the continent’s crypto community. The message was blunt: starting July 1, the world’s largest cryptocurrency exchange would suspend much of its service for anyone residing in the European Union. The headlines that followed were predictably dramatic, declaring that Binance was shutting down in Europe, abandoning the region, or being expelled from the bloc.

The reality is both narrower and more revealing than any of those framings. Binance is not collapsing, it is not seizing anyone’s money, and it is not, in its own telling, permanently leaving Europe. What actually happened is that Binance failed to obtain the license it needed under the European Union’s new crypto regulation before a hard deadline, and as a result, it is being locked out of the EU market until it can secure that license somewhere else.

The distinction matters because the panic-inducing version of the story obscures both what users should actually do and the far more interesting question of why the largest exchange on earth could not get a license that its smaller rivals managed to obtain.

This piece lays out what actually happened, what changes and what does not, and what the episode reveals about the new rules now governing crypto in Europe.

The story is worth understanding precisely because it is a milestone, the moment when Europe’s comprehensive crypto framework showed that it would apply to everyone, including the biggest player in the industry, with no exceptions for size or market share. It is also a story with a specific and somewhat surprising cause, one that has less to do with Binance’s compliance systems or its application paperwork and more to do with the legal history of the company and its founder.

To make sense of it, this piece works through the precise facts of the suspension, the practical reality for users whose first instinct was to panic, the MiCA regulation and the deadline that forced the situation, the Greek gateway that collapsed, the deeper reason the application failed, Binance’s own account of events, the rivals who succeeded where it did not, the path Binance is now pursuing, and what the whole affair means for the future of crypto in Europe. The aim throughout is accuracy over drama, because the drama, while real, has obscured what is genuinely going on.

What actually happened

Strip away the alarmist framing, and the sequence of events is clear. Binance needed a license to operate legally in the European Union under a regulation called MiCA, the bloc’s new crypto framework, and the deadline to have that license was the end of June. Binance had pursued the license through Greece, filing its application there in January, but the process stalled, and in mid-June, reports emerged that the Greek regulator was preparing to reject the application.

Facing a likely formal rejection, Binance made a strategic choice on June 24: rather than wait to be formally refused, it withdrew its Greek application altogether, framing the move as a prudent decision to pursue authorization in another EU member state instead. Because withdrawing the application meant Binance would not hold a MiCA license by the June 30 deadline, it was obligated to stop offering regulated services to EU residents from July 1, and so it emailed its European users to tell them exactly that.

The crucial point that the dramatic headlines missed is what this suspension is and is not. It is a halt to Binance’s ability to offer new regulated services to EU residents, triggered by the absence of a license. It is not a shutdown of the company, a seizure of user assets, or, in Binance’s framing, a permanent departure from Europe.

Binance has stated clearly that it intends to remain in the European market, that it will seek a license through another member state, and that it expects to secure authorization in the coming months.

So the accurate description of what happened is this: Binance, unable to get the license it needed in time and facing a probable rejection in Greece, withdrew its application and is now suspending EU services until it can obtain a license elsewhere, while assuring users their funds are safe.

That is a serious setback and a significant moment for the industry, but it is a regulatory lockout with a stated path back, not the collapse or expulsion the headlines suggested.

What changes on July 1, and what does not

For the millions of European users who received that email, the most urgent question is intensely practical: what happens to their accounts and their money? Here, the gap between the panic and the reality is widest, and it is worth being precise, because the distinction between what stops and what continues determines what users should actually do.

What stops on July 1 is the set of active, regulated services that require a license. Binance will halt new spot trading orders for EU residents, stop accepting new deposits, end new sign-ups and onboarding, and suspend its yield-generating products such as staking and the various Earn offerings.

In effect, the ability to put new money in and to actively trade or earn on the platform as an EU resident comes to an end, because those are precisely the regulated activities MiCA requires a license to provide.

What does not change is just as important. User funds remain safe and accessible, and withdrawals stay active, which means no one’s assets are being seized, frozen, or automatically lost.

The orderly wind-down that EU rules require an exiting platform to provide is designed to guarantee exactly this: that users retain access to their assets and can move them elsewhere. Binance has said it is not instructing customers to remove their funds by a specific date and that user assets remain secure. To allow an orderly exit, it keeps certain features available in a limited form, such as a conversion function that can be used to sell positions so users can wind down in an orderly way.

The practical guidance that follows from this is the opposite of panic: EU users have time, their money is accessible, and the sensible course is to withdraw funds to another licensed platform or a self-custody wallet in an unhurried way, while being especially alert to scammers who exploit exactly this kind of confusion.

Binance has also said it will contact affected users directly with steps specific to their account and country, and that it will never call them by phone or ask for passwords or security codes, a warning worth heeding because moments of regulatory upheaval are prime opportunities for fraud.

The headline made it sound like an emergency. The reality is a wind-down with the safety nets that the regulation requires.

MiCA, and the deadline that forced this

To understand why any of this happened, you have to understand the regulation at the center of it, because the Binance situation is a direct consequence of a deliberate European policy choice.

MiCA, which stands for Markets in Crypto-Assets, is the European Union’s comprehensive framework for regulating crypto, designed to replace the patchwork of differing national rules that previously governed the industry across the bloc’s member states.

Before MiCA, a crypto company could operate in Europe by registering under the individual rules of various countries, and global operators often moved through the gaps and gray areas between those national regimes. MiCA ends that fragmented era by creating a single, unified system: to offer crypto services anywhere in the EU, a company must obtain authorization as a Crypto-Asset Service Provider, known as a CASP, from the regulator of one member state, after which a passport mechanism lets it operate across the entire bloc on the strength of that single license.

The deadline that forced the Binance situation is the end of a transition period built into the regulation. MiCA came into full effect at the end of 2024, but it included a grandfathering window that let firms operating under the old national registrations continue while they pursued a CASP license. That transition period closes on July 1, 2026, which is the hard enforcement date.

From that day forward, any firm offering crypto services in the EU without a CASP license is in breach of European law, and the prior national registrations that companies once relied on, in countries such as Spain, France, Italy, and Poland, carry no legal weight under the new framework. This is why the deadline was absolute for Binance: its old national registrations became void, and without a CASP license by June 30, it had no legal basis to serve EU customers.

The regulation makes no distinction between large exchanges and small ones; it distinguishes only between the licensed and the unlicensed. Binance, for all its size, fell on the wrong side of that line, and MiCA’s design left no room for a grace period or a special arrangement. The deadline was the deadline, and Binance did not meet it.

The Greek gateway that collapsed

Binance’s path to a license ran through Greece, and the choice was strategic rather than accidental. Because a single CASP license passport across the entire EU, a company can pick which member state to apply through, and the calculation involves speed, the competitiveness of the local process, and the regulator’s posture.

Binance filed its application with the Greek markets regulator in January, setting up a local holding entity to anchor its European operations there. The logic, by several accounts, was that Greece had granted few or no MiCA licenses at that point, which in principle might offer a faster and less crowded path than applying in a country like Germany or the Netherlands, which had already processed dozens of applications and built up queues.

Binance also cited the country’s local talent and other practical considerations, and it pursued the Greek approval for what it described as a lengthy engagement with regulators.

The plan collapsed. Although Binance filed in Greece, the application did not get reviewed in isolation, because under MiCA’s structure, the assessment was tracked alongside regulators in other member states, with authorities in Ireland and Latvia reportedly involved in the review, and oversight at the level of the EU’s central markets authority.

According to multiple press reconstructions, that joint review raised concerns about Binance’s legal history and its complex corporate structure, and in mid-June, reports indicated that the Greek regulator was poised to reject the application.

People familiar with the process described Binance making significant offers to win approval, including commitments to hire staff, open an office in Greece, and bring substantial investment into the country, the kind of inducements that signal how badly the company wanted the license and how much trouble it sensed.

None of it was enough. Faced with a likely formal rejection, Binance withdrew the application on June 24, pulling its bid before it could be officially refused. The Greek gateway, chosen for its supposed speed and openness, had become the place where Binance’s European ambitions stalled, and the reasons for the stall point to something deeper than any single country’s process.

The real reason: the fit and proper problem

Here is the heart of the matter, the part that the headlines about Europe and deadlines miss entirely: the rejection reportedly turned on Binance’s past, not its paperwork. MiCA, like most serious financial regulations, applies a standard known as the fit and proper test to the people who own and run a regulated firm, assessing whether an applicant’s management and significant shareholders are suitable to operate a licensed financial business.

This is where Binance ran into trouble, because the test put the spotlight on its co-founder and roughly 90% owner, Changpeng Zhao, and on the company’s documented history of legal problems.

According to people familiar with the review, the concerns that sank the Greek application centered on Binance’s anti-money-laundering controls and on whether Zhao could satisfy the fit and proper standard, given his record.

That record is substantial and a matter of public fact. In 2023, Binance pleaded guilty in the United States to anti-money-laundering and sanctions violations and paid penalties exceeding $4 billion, among the largest corporate penalties in American history.

Zhao himself stepped down as chief executive, pleaded guilty to a criminal charge, served a prison sentence of several months, and was later pardoned by the United States president in late 2025, though he retains his roughly 90% stake in the exchange.

Beyond the American case, Binance faces elevated pressure elsewhere in Europe: French authorities opened a judicial investigation into whether the company assisted money laundering, including possible links to drug trafficking and tax fraud, allegations Binance denies, and the exchange has been banned in the United Kingdom since 2021.

Stacked together, this history is exactly the kind of baggage that a fit and proper assessment is designed to scrutinize, and it gave regulators concrete grounds for concern about authorizing the firm and its dominant owner.

The significance of this cannot be overstated: Binance was not locked out because it filed a sloppy application or lacked the technical capacity to comply. By the available accounts, it was locked out because regulators looked at its past and the standing of the man who controls it and concluded they could not, in good conscience, hand it a license to operate across the EU. The obstacle was history, not paperwork.

Binance’s side of the story

Fairness requires giving Binance’s account, because the company disputes important parts of this narrative, and its perspective deserves a clear hearing.

Binance’s central contention is that its application was sound and that it never received a formal rejection. The company has stated that its understanding was that the Greek regulator completed its review and considered the application compliant with MiCA requirements, and that the application was also reviewed at the level of the EU’s central markets authority.

In Binance’s framing, it did not fail a clear test so much as run out of time within an ambiguous process: it received no formal decision before the deadline, and so it made what it called the prudent choice to withdraw the Greek application and pursue authorization in another member state rather than wait passively to be refused.

The company emphasizes that it engaged constructively with regulators for roughly eighteen months and believes it meets MiCA’s requirements, casting the outcome as a procedural and timing failure instead of a substantive rejection on the merits.

Binance has also worked hard to reassure users and to project continuity. It has stressed repeatedly that user funds remain safe and secure, that it is not instructing customers to rush their withdrawals, and that its ambition to operate in Europe under a clear and harmonized framework is unchanged. It has framed the entire episode as a setback on the path to a license instead of a defeat, expressing confidence that it will secure authorization in another EU member state in the coming months.

At the same time, the company’s handling of the situation has drawn criticism even from sympathetic observers, who argue that the weeks of ambiguity before the announcement, followed by an email that triggered panic, reflected poorly on a firm seeking to present itself as a mature, compliant financial institution.

Several commentators noted that a straightforward early acknowledgment of the Greek difficulty and a clear timeline could have spared users much of the confusion, and that in regulated finance, where transparency maps directly to trust, the murkiness of the process was itself a reputational cost.

Binance’s version, then, is of a compliant applicant caught in a slow and unclear process, choosing prudence over a formal refusal, while its critics see a company whose past caught up with it and whose communication compounded the damage.

The winners: who passed MiCA

Nothing illustrates the significance of Binance’s failure more sharply than the list of companies that succeeded, because the contrast turns the story from one exchange’s misfortune into a statement about the new shape of European crypto.

While Binance was being locked out, a number of its largest rivals secured the MiCA authorization it could not obtain. Major exchanges, including Coinbase, Kraken, OKX, and Crypto.com, all cleared the process and now hold licenses to operate across the bloc, giving them a significant competitive advantage heading into the second half of the year.

These are not minor players; they are among the most prominent exchanges in the world, and their success shows that the MiCA hurdle, while high, was clearable by serious firms willing and able to meet its standards. The fact that the largest exchange of all could not join them is what makes the moment so striking.

The broader numbers underline how selective the new regime is, and how much of an achievement a license represents. Of more than 3000 crypto firms operating across Europe, only around 210 secured full CASP authorization across roughly two dozen member states, a clearance rate in the single digits. Measured against the smaller universe of firms that had held national registrations before MiCA, the conversion rate was still well under a fifth.

In other words, the overwhelming majority of crypto firms that operated in Europe under the old patchwork did not make it through MiCA’s gate and were left to exit the market or scale back. This is the regime working as intended, filtering out firms unable or unwilling to meet a unified standard, and the licensed survivors now enjoy a meaningful moat.

Unsurprisingly, regulated rivals have moved quickly to capture the business Binance is vacating, with competitors publicly promoting their authorized status and their readiness to serve the users now looking for a licensed home. The competitive map of European crypto is being redrawn, and the redrawing favors those who got their license, with Binance, for now, on the outside looking in.

What comes next: the France gambit

Binance’s lockout is, by the company’s account, temporary, and the path it is pursuing back into the market is worth understanding, because it raises questions of its own.

Having withdrawn from Greece, Binance has signaled that it will seek a MiCA license through another member state, and according to reports citing people familiar with its plans, the chosen venue is France. This is a notable choice given that French authorities have an open judicial investigation into the company, which would seem to complicate an application there, and it suggests Binance believes it can satisfy the French regulator despite the scrutiny it faces in the country.

The more immediate problem is timing. Even if Binance applies promptly in France, any approval is likely to come after the July 1 deadline, which means there will be a gap, potentially of months, during which Binance remains locked out of the EU and unable to serve its European users with regulated services. The company’s confidence that it will secure a license in the coming months may prove justified, but the interim is real, and during it, the business migrates elsewhere.

The France gambit also surfaces a deeper tension within MiCA that the Binance affair has exposed. If Greece, working alongside regulators in Ireland and Latvia, found Binance unsuitable for a license, and France subsequently grants one, the episode would reveal inconsistencies in how different member states interpret and apply the same supposedly unified requirements.

That kind of divergence is precisely the regulatory arbitrage that MiCA was designed to eliminate, the practice of shopping for the most permissive regulator, and a high-profile instance of it involving the largest exchange in the world would raise uncomfortable questions about whether the framework is as harmonized as advertised.

Conversely, if France also declines, Binance’s path back into Europe narrows considerably, and the lockout could extend well beyond the coming months, the company has promised.

So the next chapter hinges on France: a relatively quick approval would vindicate Binance’s confidence while testing MiCA’s consistency, a slow process would prolong the lockout, and a refusal would turn a temporary suspension into something that looks more like a lasting exclusion. The one certainty is that the gap between July 1 and whatever comes next is a period in which Binance is genuinely shut out, and the European crypto market continues without it.

What it means: the end of crypto’s gray zone

Step back from the specifics, and the Binance affair marks a genuine turning point, the moment when Europe showed that its crypto regulation has real teeth and applies without exception.

For years, the crypto industry operated in a gray zone in Europe, with global exchanges moving through the gaps between national rules and the largest players seemingly too big and too important to be meaningfully constrained. MiCA was built to end that gray zone, to replace ambiguity with a single clear standard, and to subject every operator to the same requirements.

The fact that the framework’s first major casualty is the largest exchange in the world is the clearest possible proof that the regime means what it says. No firm, however dominant, is exempt from the fit and proper standard, the anti-money-laundering requirements, or the licensing process, and a company that cannot meet them is locked out regardless of its size.

That message will reverberate through the industry far beyond Binance, because if the biggest player can be shut out, everyone else is on notice that compliance is now the price of access to the European market.

The implications are double-edged, and an honest accounting acknowledges both sides. On one hand, the regime delivers what it promised: consumer protection, a level playing field of uniform rules, and the removal of operators unwilling or unable to meet serious standards, which many would call a healthier and safer market.

On the other hand, locking out the largest exchange carries real costs and risks. Liquidity and trading volume migrate, some of it to the licensed rivals who will consolidate the market, but some of it potentially to workarounds, as users turn to virtual private networks and offshore accounts to keep accessing Binance, which is exactly the kind of regulatory shadow activity that MiCA was meant to prevent.

The bloc may lose some of the investment, jobs, and tax revenue that a major exchange brings, a concern Binance itself has raised. And the France question hangs over everything, with the prospect that inconsistent application across member states could undercut the very harmonization MiCA was built to achieve.

What is not in doubt is that the era of crypto’s European gray zone is over. From July 1, the rule is simple and absolute: hold a license or do not operate, and even Binance is not big enough to be an exception.

That is what actually happened, and it matters far more than the headlines about an exchange leaving Europe, because the real story is that Europe decided who gets to stay, and for now, on its own terms, it said no to the biggest name in crypto.

Frequently Asked Questions

Is Binance actually leaving Europe?

Not permanently, despite headlines suggesting otherwise. Binance is suspending most regulated services for EU residents from July 1 because it failed to obtain the required MiCA license by the June 30 deadline. The company has stated clearly that it intends to remain in the European market, that it will seek a license through another member state, and that it expects to secure authorization in the coming months. So the accurate description is a regulatory lockout with a stated path back, not a permanent departure. Binance is being shut out until it can get a license elsewhere, not abandoning Europe by choice.

What happens to my funds on Binance if I am in the EU?

Your funds remain safe and accessible, and withdrawals stay active. Nothing is being seized, frozen, or automatically lost. What stops on July 1 is new activity: new spot trading orders, new deposits, new sign-ups, and yield products like staking and Earn. The orderly wind-down that EU rules require is designed to guarantee continued access to your assets, and Binance has said it is not instructing users to remove funds by a specific date. The sensible approach is to withdraw to another licensed platform or a self-custody wallet without panic, and to be alert to scammers, since Binance says it will never call you by phone or ask for passwords.

Why did Binance fail to get a MiCA license?

By the available accounts, the rejection turned on Binance’s past, not its paperwork. MiCA applies a “fit and proper” test to a firm’s owners and managers, and the concerns reportedly centered on Binance’s anti-money-laundering controls and on whether co-founder and roughly 90% owner Changpeng Zhao could satisfy that standard. Binance’s history includes a 2023 guilty plea in the United States to anti-money-laundering and sanctions violations with penalties over $4 billion, Zhao’s own criminal plea and prison sentence, an open French investigation, and a UK ban since 2021. Regulators looked at that record and the standing of its controlling owner and had grounds for concern.

What is MiCA and why does it matter?

MiCA, the Markets in Crypto-Assets regulation, is the European Union’s comprehensive framework for crypto, replacing the old patchwork of differing national rules with a single unified system. To offer crypto services anywhere in the EU, a firm must obtain authorization as a Crypto-Asset Service Provider from one member state’s regulator, after which a passport lets it operate across the bloc. MiCA came into full effect at the end of 2024 with a transition period that closes July 1, 2026, the hard enforcement date. After that, operating without a license breaches EU law, and prior national registrations carry no weight. It matters because it sets a single, serious standard for the entire European market.

Which exchanges did get a MiCA license?

Several of Binance’s largest rivals secured authorization, including Coinbase, Kraken, OKX, and Crypto.com, all of which can now operate across the bloc and hold a meaningful competitive advantage. The broader picture shows how selective the regime is: of more than three thousand crypto firms operating in Europe, only around two hundred ten obtained full authorization across roughly two dozen member states, a clearance rate in the single digits. The overwhelming majority did not make it through and must exit or scale back. That the largest exchange of all was locked out while these rivals passed is what makes the moment so significant for the industry.

Can Binance come back to the EU?

Yes, that is its stated plan, though the timing and outcome are uncertain. Having withdrawn from Greece, Binance intends to seek a license through another member state, reportedly France, and expects to secure authorization in the coming months. But any approval is likely to come after July 1, leaving a gap during which Binance remains locked out. France route also raises questions, both because French authorities have an open investigation into the company and because, if France grants what Greece would have refused, it would expose inconsistencies in how member states apply MiCA. A quick approval would bring Binance back; a refusal would turn the suspension into something more lasting.

This article provides information about a fast-moving regulatory situation, not legal or financial advice. Details of Binance’s licensing, the positions of regulators, and the timeline reflect reporting available as of June 26, 2026, and can change quickly as the situation develops. EU users with questions about their accounts should rely on official communications from verified sources and be alert to scams. Verify current developments through primary sources

Key Takeaways

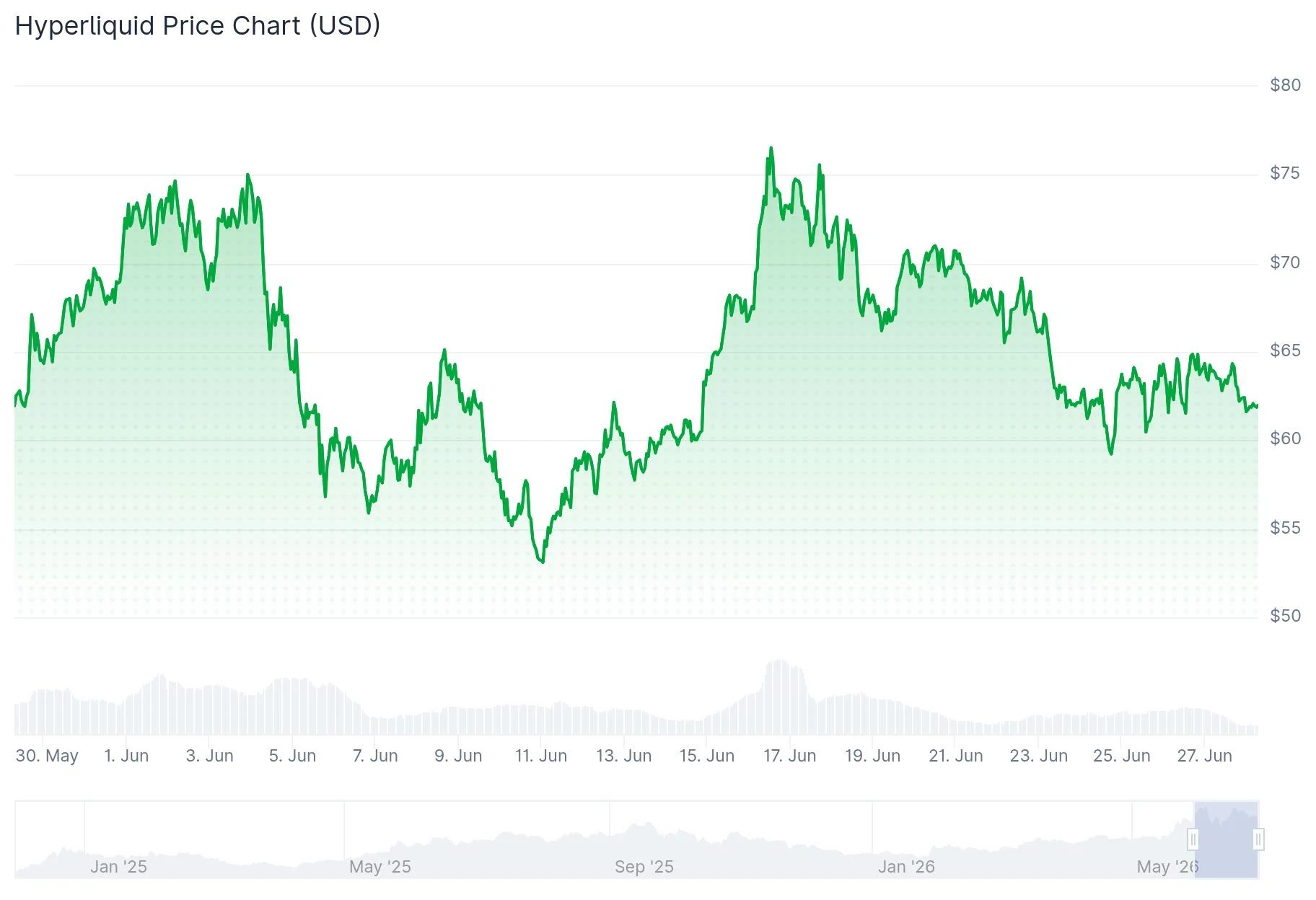

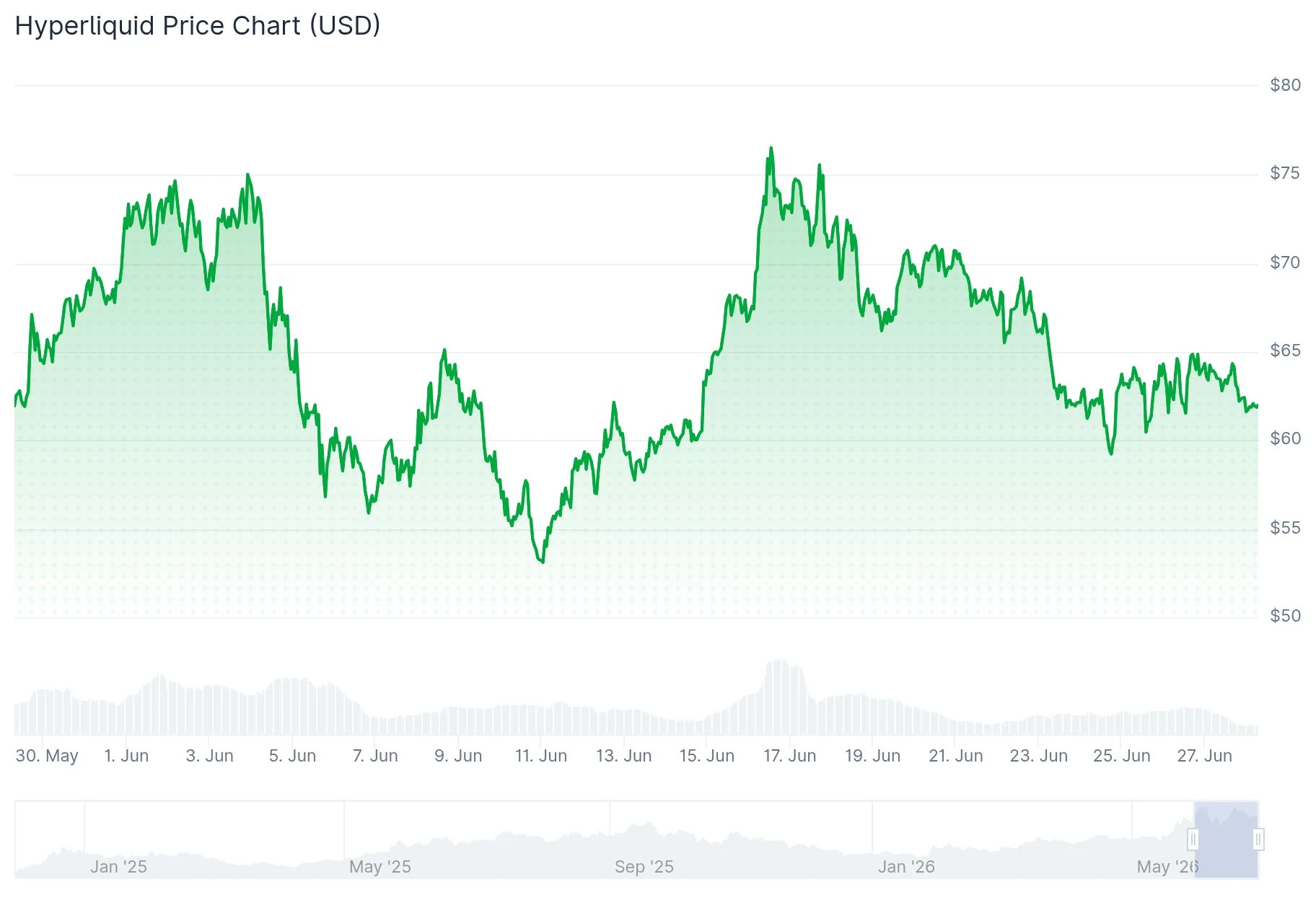

- HYPE is currently valued near $62 with a multi-billion dollar market capitalization

- Baseline scenario projects $100–$160, valuing HYPE as a decentralized exchange token

- Optimistic scenario envisions $250–$400 if Hyperliquid dominates on-chain derivatives trading

- Pessimistic scenario suggests $20–$35 amid competitive pressures, security incidents, and token dilution

- Weighted probability analysis points to approximately $145 by the year 2031

Hyperliquid stands out in a crowded cryptocurrency landscape by delivering tangible results. Unlike countless projects built purely on speculation, Hyperliquid has secured more than 40% of the decentralized perpetual futures market by mid-2026. This represents genuine market dominance backed by data.

Currently trading near $62, HYPE’s valuation fundamentally depends on transaction volume, fee generation, and platform liquidity rather than empty promises.

The protocol handled transaction volumes in the hundreds of billions throughout the first quarter of 2026, with daily figures consistently reaching into the billions. These metrics mirror those of established centralized exchanges.

This performance explains why market observers increasingly compare HYPE’s valuation framework to traditional exchange tokens rather than standard Layer 1 blockchain assets.

Baseline Projection: $100 to $160 Range

The baseline forecast assumes Hyperliquid maintains its leadership position within decentralized perpetuals throughout the coming half-decade.

This scenario requires continued migration of traders toward on-chain platforms, sustained growth in cryptocurrency derivatives markets, and Hyperliquid’s ability to defend its market share. A valuation range of $100 to $160 would translate to a fully diluted market cap between $100 billion and $160 billion, calculated against the maximum token supply of 1 billion HYPE.

While ambitious, these valuations become reasonable if Hyperliquid evolves into essential infrastructure for cryptocurrency trading.

Reuters coverage indicates that cryptocurrency exchanges are positioning themselves for expanded U.S. perpetual futures offerings as regulatory frameworks crystallize. This regulatory shift could significantly expand Hyperliquid’s addressable market.

Optimistic and Pessimistic Scenarios

The optimistic projection places HYPE between $250 and $400. Achieving this requires Hyperliquid to dominate decentralized derivatives, successfully launch spot trading markets, attract significant institutional capital, and transform into a comprehensive on-chain financial infrastructure.

This scenario demands multiple favorable outcomes aligning simultaneously.

The pessimistic forecast settles between $20 and $35. Trading platform markets are intensely competitive. Centralized exchanges, dYdX, GMX, Solana ecosystem protocols, and emerging perpetual DEXs all compete for identical liquidity pools.

Security vulnerabilities represent substantial threats. The Financial Times documented a $280 million security breach at Drift, a rival decentralized derivatives platform. Such incidents can undermine confidence across the entire sector.

Token supply expansion creates additional downward pressure. The current circulating supply represents only a fraction of the 1 billion maximum HYPE tokens. Future unlock events occurring during periods of weak demand could significantly depress prices.

The probability-adjusted five-year projection estimates approximately $145 by 2031.

Hyperliquid commands over 40% of decentralized perpetual futures volume as of mid-2026, with daily trading consistently reaching billions of dollars.

Key Takeaways

- ZEC is currently valued at approximately $388 with a total market capitalization approaching $6.7 billion

- The moderate scenario projects ZEC reaching $600–$1,000 by the end of 2031

- An optimistic scenario envisions $2,000–$3,500 should privacy features gain mainstream adoption

- A pessimistic outlook anticipates $120–$220 amid intensifying regulatory challenges

- Weighted average projection indicates approximately $850 as the target price for 2031

Introduced to the cryptocurrency ecosystem in 2016, Zcash emerged as a privacy-centric counterpart to Bitcoin. While Bitcoin operates with complete transaction transparency, Zcash enables users to conduct confidential transfers utilizing zero-knowledge cryptographic protocols.

This positions ZEC as a unique investment proposition. Rather than challenging platforms like Ethereum or Solana, it represents a strategic bet on whether financial confidentiality will resonate with cryptocurrency participants and corporate entities.

Presently trading at roughly $388, ZEC maintains a market valuation close to $6.7 billion, with approximately 16.7 million tokens currently circulating. Mirroring Bitcoin’s economic model, Zcash incorporates a maximum supply ceiling of 21 million coins alongside a halving mechanism that reduces mining rewards approximately every four years.

Industry observers from CoinDesk indicated that privacy-oriented cryptocurrencies such as Zcash and Monero were projected to maintain investor interest throughout 2026, despite ongoing challenges related to exchange removals and financial institution restrictions.

Moderate Projection: $600–$1,000 Range

The middle-ground forecast for ZEC through 2031 anticipates valuations spanning $600 to $1,000. This translates to a market capitalization between approximately $12 billion and $20 billion.

This pathway doesn’t demand that Zcash ascends into the top tier of cryptocurrency assets. It simply requires maintaining its status as the premier privacy-focused digital asset offering regulatory-compliant optional transparency features.

Three fundamental drivers support this trajectory: expanding privacy consciousness among users, sustained availability on major trading platforms, and robust technical foundations. Zcash’s Bitcoin-inspired monetary policy and proof-of-work consensus mechanism reinforce this projection.

Optimistic Projection: $2,000–$3,500 Range

Should privacy emerge as a central theme within cryptocurrency markets, ZEC could potentially climb to $2,000–$3,500. Such appreciation would elevate its market capitalization to the $40 billion–$70 billion territory.

Realizing this scenario requires widespread implementation of confidential transaction features, significant improvements in user interface design, and revitalized institutional participation in privacy-preserving technologies.

Additionally, Zcash would need market recognition as a “privacy-enhanced Bitcoin” rather than merely another aging alternative cryptocurrency.

Pessimistic Projection: $120–$220 Range

The downside scenario centers on regulatory enforcement. Privacy-focused cryptocurrencies currently face removal pressures across numerous jurisdictions, representing tangible rather than theoretical risks.

Should major exchanges impose restrictions or completely eliminate ZEC trading pairs, resulting in severely diminished liquidity, valuations could contract to $120–$220 by 2031.

Maintaining access to reputable trading venues constitutes one of the most significant threats to Zcash’s future market value.

Calculating probability-weighted outcomes across these three distinct scenarios yields an approximate target price of $850 for 2031.

Grayscale Research Head Zach Pandl has put Strategy’s Bitcoin treasury under fresh review. His comments focus on whether a larger BTC sale could ease investor concern better than another increase in STRC dividends.

Summary

- Pandl says a larger Bitcoin sale could clear doubts around Strategy’s cash obligations and dividends.

- STRC trading below $100 keeps pressure on Strategy’s preferred stock model and future funding choices.

- Crypto.news reports tied Strategy’s small BTC sale to wider concerns about leverage and liquidity risk.

Pandl said Strategy raising the STRC dividend by 50 basis points next week would add about $100 million in dividend obligations over the next two years. He said that move “would likely not restore market confidence” because it would not remove the question around future cash needs.

He argued that selling more than $3 billion in BTC could be more effective. In his view, such a sale could cover nearly all cash obligations over the next two years and give investors a clearer view of how Strategy plans to manage its preferred stock costs.

Strategy, formerly known as MicroStrategy, remains the largest corporate Bitcoin holder. The company built its public market identity around buying and holding BTC, while using equity, debt and preferred shares to fund the strategy.

STRC keeps pressure on the treasury model

The debate centers on STRC, Strategy’s variable-rate preferred stock. The company designed the product to trade near $100, and it currently pays an 11.5% annual dividend. Still, STRC has traded below its target level during recent market stress.

As crypto.news reported earlier, Strategy sold 32 BTC for about $2.5 million between May 26 and May 31. The sale was small compared with its Bitcoin treasury, but it drew attention because it was the company’s first reported BTC sale since December 2022.

That sale also changed how investors view the company’s funding model. Strategy had long acted as a steady Bitcoin buyer. Even a small sale raised doubts about whether the firm may need to sell more BTC if preferred stock costs keep rising.

Crypto.news also reported that STRC later fell as low as $82.50, while its effective yield moved near 13.2%. A higher yield can show that investors want more return to hold the stock.

Cash runway becomes the key question

CryptoQuant has estimated that Strategy’s annualized dividend obligations tied to STRC reached about $1.2 billion. The firm also estimated that dividend coverage fell to roughly 14 months as cash reserves declined during 2026.

Those figures explain why Pandl’s $3 billion sale idea has attracted attention. A planned BTC sale could raise cash before pressure grows. It could also show that Strategy can meet fixed obligations without depending only on new share sales or a higher Bitcoin price.

Recent market reports said Strategy later bought 520 BTC for about $34.9 million, bringing total holdings to 847,363 BTC. The company also raised cash reserves by about $300 million, which showed it had not stopped using capital markets to support both Bitcoin holdings and dividend needs.

For investors, the next focus is STRC’s price against the $100 level. If the preferred stock stays below that mark, Strategy may face more pressure to adjust payouts, raise cash or sell Bitcoin in a more planned way.

The evident divergence in how ETF investors behave toward the largest cryptocurrencies by market cap continues. The past week saw some record-setting withdrawals from the BTC funds, but those following HYPE and XRP have maintained their green dominance.

At the same time, the SOL funds have turned red after the previous week’s positive performance.

XRP and HYPE Still Dominate

CryptoPotato reported last week that the spot ETFs tracking HYPE, XRP, and SOL defied the trend set by the two largest digital assets and attracted notable capital. The trend extended in the past week for two of those assets, and one day was particularly positive for the HYPE funds.

Data from SoSoValue reveals that Thursday stands out with just over $108 million in net inflows, making it by far the best single-day performance from the funds. With a lot more modest $1.46 million on Tuesday and $1.82 million on Friday, the week ended with $111.36 million in net inflows. It also set the record for the most significant weekly inflows, surpassing the previous of $72.38 million marked during the funds’ second week of existence.

The spot XRP ETFs also ended the week strongly, albeit nowhere near HYPE’s Thursday inflows. They attracted $15.63 million on Friday, building on the $5.31 million on Monday and $2.05 million on Wednesday. With Tuesday and Thursday being $0.00 days, the week ended with $23 million in net inflows, the best in a month and a half.

The cumulative total net flows have risen to another all-time high of $1.47 billion. Moreover, both XRP and HYPE ETFs have been on a green-only weekly streak for 8 and 7 consecutive weeks now, respectively.

SOL Joins BTC and ETH

While the HYPE and XRP products have continued their impressive streak, SOL has fallen behind with a $3.8 million net outflow. Thus, the Solana ETFs have joined the two market leaders.

The spot Bitcoin ETFs registered another massive withdrawal in the past week, with nearly $1.8 billion leaving the funds. This was their second-worst weekly performance in their 2.5-year history. The Ethereum funds were also in the red, with more than $273 million withdrawn.

The post XRP and HYPE Keep Winning the ETF Race as SOL Joins BTC and ETH appeared first on CryptoPotato.

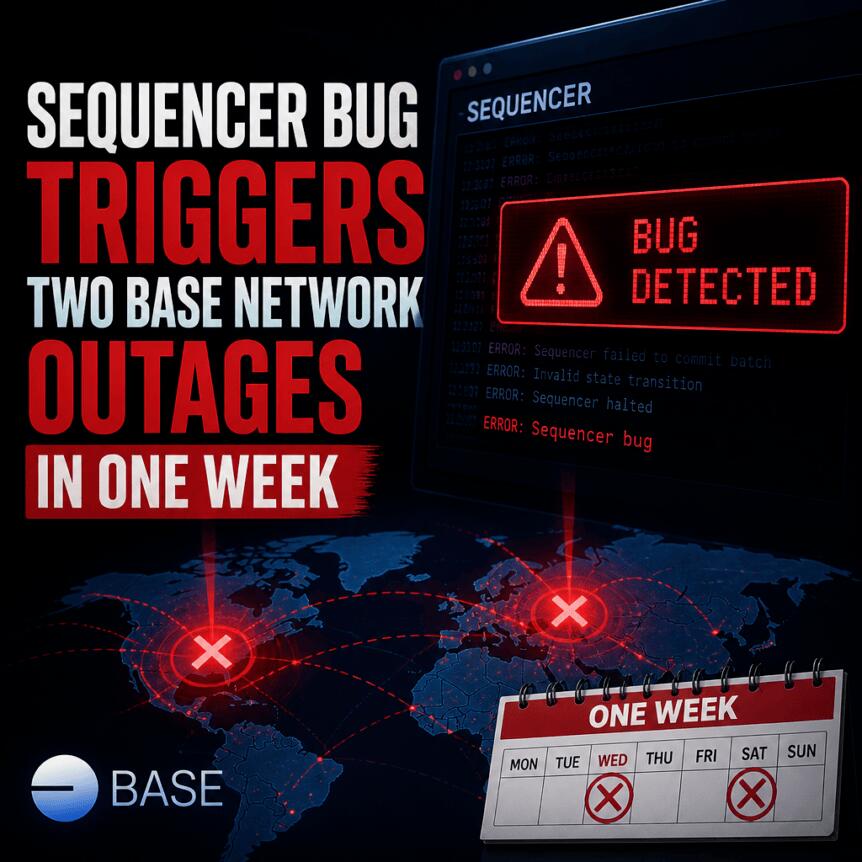

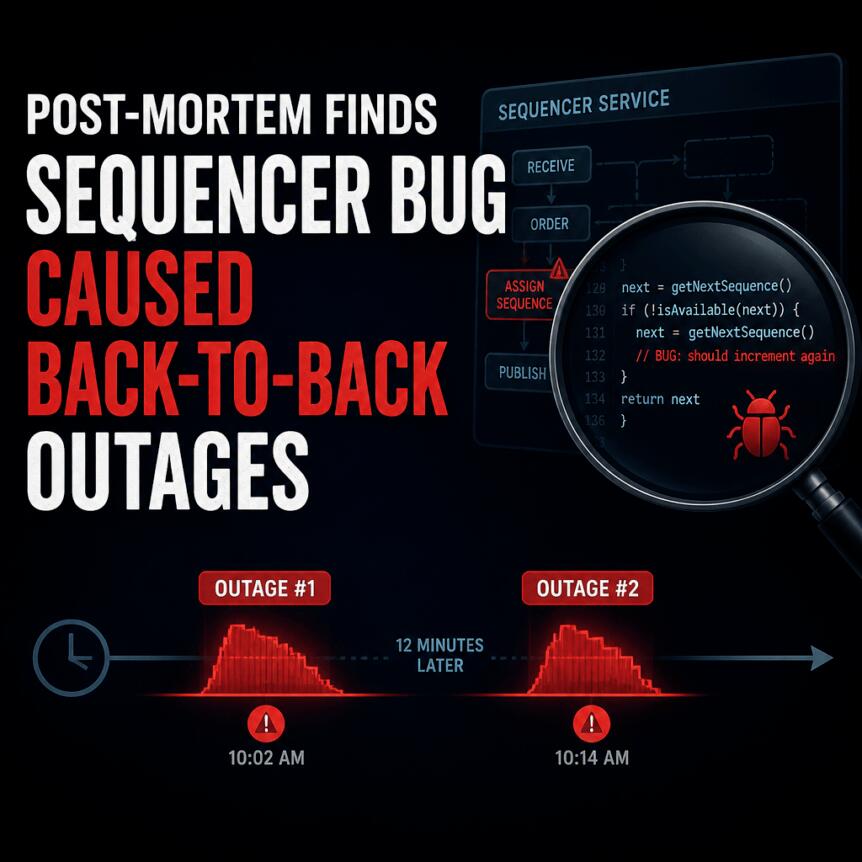

Coinbase’s Base layer-2 network suffered two block production outages last week, and the project’s engineering team has traced both issues to problems in its sequencer infrastructure. According to a Saturday post-mortem, a bug in the block-building process caused “stale journal state” to remain after an execution failure—preventing the network from progressing until operators applied fixes.

Because Base runs with a single sequencer, the incident underscores a structural risk familiar to many rollups: when sequencer logic fails, block ordering and forward progress can stall across the whole chain. Base experienced a first outage on Thursday lasting 116 minutes, followed by a second that lasted 20 minutes, with a complete halt of new layer-2 block production during both events.

Key takeaways

- Base’s engineering team linked the outages to sequencer block-building logic that left “stale journal state” after a transaction validation failure.

- Base operates a single sequencer, so a sequencer-level defect can halt the entire network’s block production.

- The second outage was worsened by a “race condition” after a system reset that prevented sequencers from catching up.

- Engineers say remediation took longer than expected due to infrastructure conditions, not the original bug.

- Planned follow-ups include more protocol “fuzz testing” and “graceful recovery” measures to reduce manual restarts.

What the post-mortem says went wrong

In the post-mortem, the Base engineering team explained that an invalid transaction reached the block builder and failed during execution—consistent with expected behavior. The failure, however, was followed by an unintended state-management outcome: the sequencer did not clear the journal state that records which accounts and storage slots were accessed during processing.

That journal state is critical to correct execution bookkeeping. If it persists when it should be cleared, later stages of block building can be forced into an inconsistent pathway, preventing the sequencer and validator nodes from moving past the problematic block. In this case, that’s what ultimately stopped progress on Base’s chain.

The post-mortem also points out why this is particularly disruptive on Base: the network uses a single sequencer. Unlike architectures that distribute sequencer responsibilities across multiple components, a single sequencer becomes a single point of failure for block production. The team’s analysis places the incident squarely in the sequencer layer, rather than the broader execution environment.

Two outages, one root process—and a second failure mode

Base mainnet halted block production twice over the Thursday–Friday window. The first incident lasted 116 minutes, while the second ran for 20 minutes. During both events, new layer-2 blocks stopped being produced, and the sequencer and validator nodes could not progress past the invalid block until sequencing was restored.

Engineers said they resolved the outages by patching the sequencers to ensure the journal state is properly updated during execution. However, they emphasized that the time required for mitigation exceeded expectations. The team attributed the delay to “infrastructure conditions unrelated to the original bug,” implying the remediation itself was more operationally complex than the underlying code fix.

Beyond the initial state-clearing issue, the post-mortem describes an additional complication after system reset: a “race condition” prevented the sequencers from catching up. This race condition, following the restart, is presented as the driver behind the second outage—meaning the chain did not simply fail once and recover, but experienced a follow-on stall tied to how components re-synchronized.

Why sequencer fragility matters to rollup users

While outages are never ideal, sequencer incidents carry a special weight for users because ordering is foundational to how rollups coordinate transactions. A centralized sequencer decides the order of transactions and packages them into blocks. When its block-building logic or recovery flow breaks, users can see cascading effects: delayed confirmations, stalled finality progress, and operational interruptions that can be difficult for end users to predict.

The Base team’s findings also resonate with a broader pattern across the rollup ecosystem. The post-mortem narrative aligns with earlier reporting that sequencer or sequencer-adjacent failures have triggered outages on other layer-2 networks as well, including Arbitrum, OP Mainnet, and zkSync Era. Those precedents help explain why developers and investors pay close attention to sequencer fault tolerance, restart behavior, and how systems handle invalid transactions under real-world conditions.

For Base specifically, the incident is likely to intensify scrutiny around resiliency and recovery mechanisms, given its “single sequencer” setup. In a centralized sequencer design, even small logical errors can have system-wide consequences if recovery pathways require manual intervention or are sensitive to timing.

What Base plans to do next

After identifying the immediate cause and applying patches, Base’s engineering team outlined improvements intended to reduce the likelihood of recurrence. Two steps are highlighted in the post-mortem: enhanced protocol “fuzz testing” and better “graceful recovery.”

Fuzz testing generally involves bombarding the system with large volumes of randomized inputs—including malformed or unexpected cases—to uncover edge-case failures that may not appear in standard testing. In this context, the goal is to better stress sequencer logic such that state-handling bugs—like improper journal state clearing—are caught earlier.

“Graceful recovery,” as described by the team, aims to ensure validator nodes don’t need manual restarts during future incidents. That matters because recovery time affects user experience and operational risk: the faster and more automatic the system can re-stabilize, the less time the network spends in a stalled state.

Base isn’t new to sequencer incidents

This isn’t Base’s first sequencer-related interruption. The post-mortem notes an earlier episode in September 2024 where block production stopped for 17 minutes, and another incident in August 2025 lasting around half an hour.

The network’s scale also makes these events more consequential. According to L2beat, Base is the second-largest layer-2 network by total value secured, just under $11 billion. With that level of capital and activity, sequencer reliability becomes more than a technical metric—it directly influences the perceived operational maturity of the chain.

As Base continues to grow, the industry will likely watch whether the promised improvements translate into faster, smoother recovery and fewer extended stalls. Even if the sequencer remains centralized, the fault-tolerance of its software pathways—especially around state management and reset behavior—can make a meaningful difference in how often outages cascade.

For now, Base users and builders should focus on how quickly engineering can validate the patched behavior under stress, and whether the planned fuzz testing and recovery upgrades reduce the chance of repeat failures—particularly those tied to invalid transaction handling and post-reset synchronization.

Bitcoin dipped below $60,000 over the weekend, trading around $59,940 on Sunday, down 0.6% over 24 hours and nearly 7% on the week, per CoinDesk data, as a quarter of selling neared its final days.

The altcoins again led the way down. Ether fell 9.5% on the week to about $1,567, dogecoin dropped 11.7% to $0.073, Hyperliquid’s HYPE lost 10.6% and XRP slid 8.7% to $1.04. Solana held up better at $70, off 3.5%, and tron was the most resilient, down 1.5%.

The market has spent the week leaning on bitcoin’s relative steadiness while everything riskier fell faster.

The weekend marks the end of a weak first half, with just two days to go. Bitcoin is on track to finish the second quarter down about 12%, after a roughly 22% drop in the first, according to data from Coinglass. Ether has fared worse, down about 25% in the second quarter following a 29% first-quarter fall.

Key Takeaways

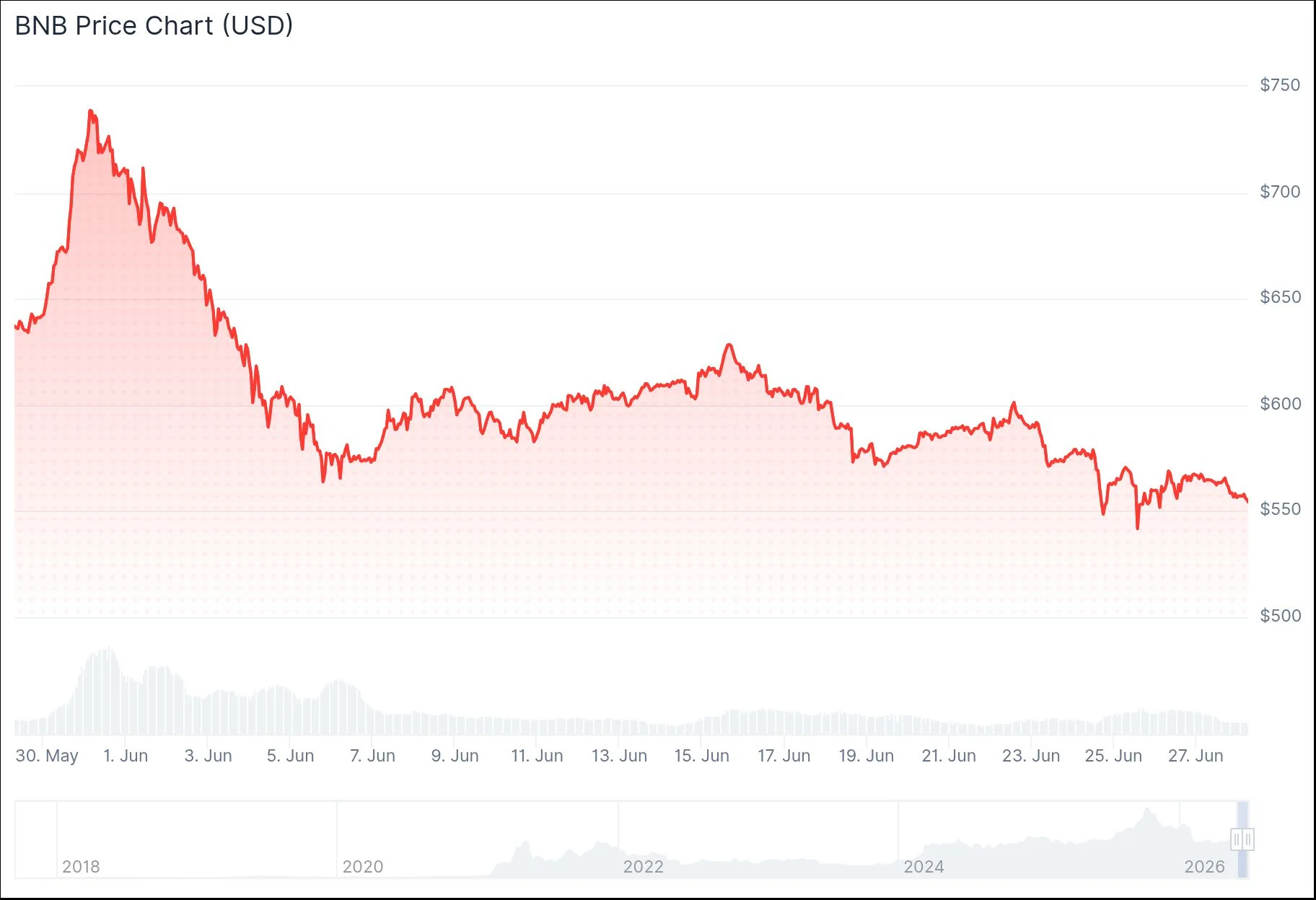

- BNB serves multiple functions including trading fee reductions, staking rewards, DeFi applications, gaming utilities, and payment solutions within Binance’s infrastructure

- Regular token burn events each quarter progressively decrease BNB’s circulating supply, aiming to halve the total from 200 million down to 100 million coins

- Conservative projections for 2031 place BNB between $1,200–$1,800, assuming steady market conditions without major disruptions

- Optimistic scenarios suggest $2,500–$4,000 valuations if BNB Chain gains widespread adoption and institutional interest accelerates

- Regulatory challenges pose the greatest threat, with pessimistic forecasts estimating $400–$600 price levels

Binance Coin has consistently ranked among the strongest-performing major cryptocurrencies in recent years. Projecting its value through 2031 requires examining several critical variables.

BNB maintains an intrinsic connection to the Binance platform. Countless traders hold the token to benefit from reduced transaction fees, participate in initial exchange offerings, cover network fees on BNB Chain, and utilize various Binance services.

This practical use case provides BNB with tangible value that distinguishes it from purely speculative digital assets.

Additionally, Binance implements a systematic quarterly burn mechanism. Every three months, a portion of tokens gets permanently eliminated from the available supply. The ultimate objective is reducing total token count by 50% — decreasing from 200 million to 100 million BNB.

This deflationary mechanism, combined with sustained market demand, forms the foundation of BNB’s long-term valuation thesis.

Moderate Scenario: $1,200 to $1,800

The most probable outcome for 2031 positions BNB trading within the $1,200 to $1,800 corridor. This forecast presumes Binance maintains its position among leading cryptocurrency exchanges worldwide while digital asset adoption continues expanding at moderate rates.

This valuation bracket corresponds to a market capitalization ranging from approximately $180 billion to $270 billion. Considering the trajectory of cryptocurrency markets, these figures remain achievable.

This scenario doesn’t demand extraordinary developments. It simply requires consistent user base expansion and ongoing supply reduction through burns.

Optimistic Scenario: $2,500 to $4,000

Under favorable conditions, BNB could climb to anywhere between $2,500 and $4,000. This projection assumes heightened institutional participation in cryptocurrency markets, BNB Chain establishing itself as a dominant infrastructure for decentralized applications and commerce, and continued aggressive token burning.

Such pricing would translate to market capitalization between $375 billion and $600 billion. While substantial, these figures don’t necessitate BNB surpassing Bitcoin or Ethereum in total value.

Primary Concern: Regulatory Pressure

BNB lacks the decentralized structure characteristic of Bitcoin. Its fortunes remain tightly bound to Binance’s corporate operations.

Should regulatory authorities impose restrictions on Binance across significant jurisdictions, exchange activity could decline substantially, pulling BNB demand downward correspondingly.

In a pessimistic scenario, BNB might trade between $400 and $600 by 2031.

The probability-adjusted price projection from this assessment centers around $1,650 for 2031. BNB’s future valuation depends more heavily on Binance’s operational success than on market speculation alone.

Coinbase and OKX are trying to win European crypto users after Binance moved to suspend several services in the European Union. The shift comes before the July 1 MiCA deadline, when crypto firms must hold approval from one EU state to keep serving the bloc.

Summary

- Coinbase and OKX moved fast as Binance prepared to restrict several EU services under MiCA.

- Transfer bonuses show licensed exchanges are competing for users before Europe’s crypto rulebook fully starts.

- Binance says assets remain accessible while it searches for a new EU authorization route elsewhere.

The campaigns add a commercial race to a regulatory deadline. Binance has told users that access to some services will change because it has not secured a MiCA license in time.

Rivals move with transfer offers

As reported, Coinbase is using the opening to court users in Germany, France, Italy, Belgium, Poland, Sweden and the U.K. The exchange says it holds MiCA approval and is offering a “5% transfer bonus” for users who move funds before July 13.

The offer puts Coinbase’s regulated status at the center of its pitch. It also gives affected users a time-limited reason to move funds before Binance fully adjusts its European services.

OKX has launched a similar push for eligible users in the European Economic Area. The exchange is offering welcome rewards and “deposit matching of up to 8%” as it promotes itself as a licensed platform for long-term access in Europe.

OKX Europe General Manager Erald Ghoos said the exchange saw record new customer sign-ups ahead of the MiCA transition deadline. The rise suggests some users are already moving before the new rules take full effect.

Binance keeps withdrawal access open

Binance has said it will restrict new registrations and certain services in the EU after missing the licensing deadline. The exchange has also told users that their assets “remain accessible at all times.”

The company withdrew its Greek MiCA application and said it would seek approval in another EU country. Binance also said its European goals “remain the same” and that it expects to secure a license in the coming months.

As previously reported, Binance had already been exploring another EU approval route before the cutoff. Reports said regulators had raised concerns tied to compliance history, corporate structure and executive oversight.

The service pause does not mean a full exit from Europe. It means Binance cannot keep offering the same range of services to EU users without MiCA approval after the transition period ends.

MiCA changes Europe’s exchange market

MiCA creates one rulebook for crypto service providers across the EU. From July 1, firms without approval must stop serving EU users or manage an orderly wind-down.

The rule gives licensed exchanges a clear marketing edge. Coinbase, OKX, Kraken and other approved firms can present themselves as stable routes for users who want to keep trading under EU rules.

Customers now have to check eligibility, fees, asset support and local rules before transferring assets. Campaign rewards can lower moving costs, but users still need to compare custody, trading pairs and withdrawal terms.

Data shared by OKX Europe earlier showed many European crypto users were still using unlicensed exchanges weeks before the deadline. That created a large pool of users who may need to review their platform choices.

Coinbase’s Base layer-2 network faced two block production outages last week, and a post-mortem published by the Base engineering team attributes both incidents to a bug in the chain’s sequencer block-building logic.

According to the report, the problem allowed “stale journal state” to persist after a transaction validation failure—meaning the system did not properly clear account and storage slot data after an invalid transaction failed during execution. Because Base uses a single sequencer, the defect had system-wide consequences.

Key takeaways

- Base’s post-mortem says a sequencer bug caused “stale journal state” to remain after an execution failure, contributing to two outages.

- Both incidents stopped new layer-2 block production; sequencer and validator nodes could not move forward past the invalid block until recovery steps completed.

- The engineering team applied a patch to update journal state correctly during execution.

- Mitigation took longer than planned, partly due to unrelated infrastructure conditions, and a follow-on “race condition” after a system reset delayed full recovery for the second outage.

- Base says it will strengthen testing through “fuzz testing” and work toward “graceful recovery” to avoid manual validator restarts in future incidents.

What went wrong in Base’s sequencer

In its Saturday post-mortem, the Base engineering team described how the system handled an invalid transaction received by the block builder. The transaction failed during execution “as expected,” the team said—but the sequencer did not clear the journal state associated with the accounts and storage slots that had been accessed.

That lingering state, the report explains, stemmed from sequencer logic that built blocks while leaving “stale journal state” intact. In typical operation, clearing or rolling back intermediate state is essential to ensure subsequent blocks are constructed from a clean execution context. Here, the failure to do so prevented normal progression.

Two outages, tied to the same failure path

Base mainnet suffered two separate block production outages on Thursday and Friday, according to the post-mortem. The first incident lasted 116 minutes, while the second was shorter at 20 minutes.

In both events, the practical outcome was the same: a complete halt in new layer-2 block creation. The sequencer and validator nodes were unable to progress past the invalid block until sequencing was restored, effectively freezing the chain’s ability to finalize new blocks.

The team implemented a fix by patching the sequencers so journal state is properly updated during execution. However, the report notes that the time required to mitigate the problem exceeded expectations “due to infrastructure conditions unrelated to the original bug.” That distinction matters for operators and builders watching for operational reliability, because it suggests the initial logic flaw was not the only factor affecting service restoration.

A follow-on “race condition” delayed full recovery

The post-mortem also points to additional complexity after a system reset. It states that a “race condition” occurred during recovery, which prevented the sequencers from catching up after the restart—contributing to the second outage.

This kind of sequencing delay is particularly important for layer-2 chains that rely on correct synchronization between components. Even after patching the underlying logic, if the system cannot re-align its execution pipeline cleanly, validators may remain blocked waiting for proper sequencer outputs. Base’s report indicates this is what happened in the follow-up period.

Sequencer centralization raises the stakes

Base is designed with a single sequencer, as the post-mortem and the team’s public communications emphasize. That architecture makes the sequencer a critical dependency: when the sequencer stalls or encounters a logic failure, the chain’s block production can stop.

This is not a theoretical risk. The report notes that outages tied to sequencer behavior have also affected other layer-2 networks, including Arbitrum, OP Mainnet, and zkSync Era. With Base, the single-sequencer model means a bug in block construction logic can become immediately visible to users across the network.

What Base plans to change next

Looking ahead, the engineering team outlined two forward-looking measures aimed at reducing the odds of similar incidents and improving recovery speed.

First, it plans to improve protocol “fuzz testing,” a technique that tests systems by generating large volumes of random, malformed, or unexpected inputs. For blockchain execution and sequencing code paths—where edge cases can trigger state inconsistencies—fuzzing is often used to uncover failure modes that normal testing may miss.

Second, the team intends to build “graceful recovery,” aiming to prevent validators from requiring manual restarts during future incidents. The operational goal is straightforward: even when something goes wrong, systems should return to service without extended human intervention or prolonged uncertainty.

Base has seen similar issues before

This week’s outages follow earlier sequencer-related disruptions on Base. The post-mortem indicates Base stopped producing blocks for 17 minutes in September 2024 and for around half an hour in August 2025—another reminder that sequencer reliability remains an ongoing focus area for the network.

In terms of scale, Base is described as the second-largest layer-2 network by total value secured, which is just under $11 billion, according to L2beat’s data. For investors and users, that positioning increases the significance of uptime and recovery mechanics: disruptions may affect activity and settlement on the network, especially during periods when other infrastructure remains stable.

As Base rolls out its planned testing and recovery improvements, the next key signal to watch is whether the fixes reduce both the likelihood of state-related sequencing failures and the time needed to fully recover after resets—particularly if future incidents still surface around tricky execution-state edge cases.

![]()

A sequencer bug was responsible for two outages of the Coinbase layer-2 network Base last week, according to a post-mortem.

The Base engineering team said in a Saturday post-mortem that they identified a bug in sequencer block-building logic that allowed “stale journal state” to persist after a transaction validation failure.

“An invalid transaction was received by the block builder and failed during execution, as expected, but erroneously did not clear the journal state that contained the accounts and storage slots that had been accessed,” said the team.

The Base layer-2 network runs a single sequencer, which means one bug can stop everything. It is a centralized blockchain component that decides the order of transactions and has been responsible for outages on other layer-2 chains, including Arbitrum, OP Mainnet and zkSync Era.

On Thursday and Friday, Base mainnet experienced two block production outages, the first incident lasted 116 minutes and the second lasted 20 minutes.

There was a complete halt of new layer-2 blocks, and the sequencer and validator nodes could not progress past the invalid block until sequencing was restored.

The team fixed the outages by applying a patch to the sequencers to ensure the journal state was properly updated during execution.

However, mitigation took longer than expected “due to infrastructure conditions unrelated to the original bug,” they said.

There was also a “race condition” after the system reset, which prevented the sequencers from catching up, causing the second outage.

Related: Coinbase’s Base resumes block production after 2-hour outage

Going forward, the Base engineering team plans to improve protocol “fuzz testing,” which involves bombarding the system with large volumes of random, malformed, or unexpected inputs to find bugs, and building “graceful recovery” so that validator nodes don’t need manual restarts during future incidents.

Not the first outage for Base

It is not the first sequencer-related outage for Base, which stopped producing blocks for 17 minutes in September 2024 and for around half an hour in August 2025.

Base is the second-largest layer-2 network by total value secured, which is just under $11 billion, according to L2beat.

Magazine: AI is banking the unbanked in Africa… faster than crypto

What time is the Wimbledon curfew and why does it exist?

Jason Statham’s Gritty $51M Action Hit Is Leaving Free Streaming Soon

#motivation #money #savings #finance #viralvideo #shorts #viralshorts #viral #youtube #trending

-

Sports5 days ago

Sports5 days agoTwo goals and an assist by sheer aura: Cristiano Ronaldo just entered the World Cup chat

-

Tech6 days ago

Tech6 days agoMicrosoft accidentally kills epic Outlook email threads

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Staud – Corporette.com

-

Politics2 days ago

Politics2 days agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Politics2 days ago

Politics2 days agoPotential 2028er World Cup attendee leaderboard

-

Business2 days ago

Business2 days agoAsia stock markets slide as tech shares slump

-

Tech3 days ago

Tech3 days agoA Look At A Gaggle Of Transputer Boards

-

Crypto World4 days ago

Bitcoin (BTC) Dips Below $62K, Ethereum (ETH) Plunges 6% Daily: Market Watch

-

Crypto World3 days ago

Crypto World3 days agoDell (DELL) Shares Tumble Over 5% Following Analyst Downgrade to Hold

-

Crypto World4 days ago

Crypto World4 days agoSecuritize Wraps Roubini's SEC-Registered ETF as Dubai VARA Digital Security

-

Business4 days ago

Entergy settles forward sale agreements, raises $672 million in cash proceeds

-

Crypto World1 day ago

Crypto World1 day agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Sports1 day ago

Sports1 day agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Crypto World2 days ago

Crypto World2 days agoRTX holders must register wallets before token distribution begins

-

Crypto World2 days ago

Crypto World2 days agoHyperliquid Named on Singapore MAS Investor Alert Register

-

Sports3 days ago

Sports3 days agoIndia vs Bangladesh LIVE Score, Women’s T20 World Cup: Bangladesh Opt To Bat; India Enter ‘Do-Or-Die’ Stage As Semi-Final Race Heats Up

-

Tech7 days ago

Tech7 days agoSignal’s Meredith Whittaker says AI chatbots ‘are not your friends’ and calls Copilot agents a backdoor

-

Crypto World2 days ago

The DATA Foundation Launches to Tackle AI’s Multi-Billion Dollar Training Data Bottleneck

-

Crypto World3 days ago

Crypto World3 days agoStrategy (MSTR) has a 10-month cash runway for dividends, but retail investors are losing faith

-

Crypto World2 days ago

Crypto World2 days agoAAVE price tests 9-month trendline after 17% rebound as breakout hopes build

You must be logged in to post a comment Login