Crypto World

Bitcoin Sees New Monthly Low, Ethereum Dips to $2K: Weekend Watch

After it was rejected at $78,000 earlier this week, bitcoin’s troubles worsened with a nosedive to a monthly low of just over $74,000, where it finally found some support.

Most altcoins have followed suit on the way down, with ETH dipping to $2,000 today, BNB going down to $640, and XRP sliding to $1.31.

BTC Charts Monthly Low

The progress made on the CLARITY Act at the end of the previous week resulted in an impressive but short-lived BTC price pump that drove the asset to $82,000. However, it was almost immediately rejected at that level for the second time that week, but this correction has been a lot more painful.

The cryptocurrency first slipped to $79,000 by that Friday before it dropped to $78,000 during the weekend. The business week began on the wrong foot with a nosedive to $76,000. After it bounced to $78,000 on Tuesday and Wednesday, the bears stepped up on the gas pedal once again and didn’t allow a more impressive rebound.

Just the opposite; bitcoin dropped to $76,000 yesterday evening and kept plunging on Saturday to $75,000 at first and then to $74,200 minutes ago. The latter became BTC’s lowest price point in just over a month. Here are some possible reasons for its $8,000 drop in less than 10 days.

For now, its market capitalization has dumped below $1.5 trillion on CG, while its dominance over the alts has retreated slightly to 58%.

Alts Bleed Out

As mentioned above, bitcoin’s correction is not an isolated case. Essentially, the entire larger-cap altcoin field is in the red today. Ethereum dipped to $2,000 earlier today before it jumped slightly to $2,025 as of now. BNB is down to $640, XRP struggles to remain above $1.30, while SOL has plunged by over 6%.

Similar or more painful declines come from DOGE, HYPE, ZEC, ADA, BCH, LINK, SUI, and many others.

The cumulative market cap of all crypto assets has shed $100 billion since Thursday and is down to $2.570 trillion on CoinGecko.

The post Bitcoin Sees New Monthly Low, Ethereum Dips to $2K: Weekend Watch appeared first on CryptoPotato.

It’s hard to believe that it has been less than a year since Ripple’s cross-border token was riding high and tapped a new all-time high of $3.65. That was last July. A lot has changed since then, and the current landscape shows little to no indication that the bulls will reemerge and push XRP back to its former glory.

That’s why we decided to ask three of the most popular AI chatbots about their opinion on whether the token will ever go back even above $2, let alone $3 or higher.

Yes, but Not That Easy

ChatGPT’s most likely answer was ‘yes, but not anytime soon.” It believes that going beyond $2 is definitely possible, especially since the asset spent more than a year there before it lost that level several months ago. However, it’s not guaranteed in the short-term as the broader market conditions remain underwhelming, to say the least.

The AI model predicted a more “gradual and uncertain path” heavily dependent on external factors rather than pure hype. ChatGPT outlined what needed to change:

Strong overall crypto market (led by bitcoin), clear regulatory environment (such as the passing of the CLARITY Act), and sustained institutional demand.

Interestingly, Gemini’s factors for a future XRP bull run were rather similar. The only difference is that the Google AI believes XRP would need more real-world settlement involving the network behind it. As such, it also concluded that XRP still has the “structural foundation” to jump past $2. However, the days of “rocketing upward purely on legal drama and speculative frenzy are over.”

Perplexity, the last AI that we asked, shared the common opinion above, suggesting that going beyond $2 is “far from certain and may require better market conditions than investors are currently seeing.”

“The worrying path is not that $2 is impossible, but that the token seems to need a lot of help to get there, and that makes the move feel fragile rather than inevitable.”

Why $2 Matters So Much

Perplexity and Gemini answered in tandem that the psychological level of $2 is “more than just a round number.” They believe it has become a massive threshold that “traders watch closely because breaking above it would suggest stronger momentum and renewed confidence in the token.”

However, they outlined a significant problem, which has been more than evident for months: XRP has been rangebound since the February crash, and every breakout attempt has been halted at $1.6 or lower. This usually means that “the market is waiting for a major driver before making a decisive move,” which seems to be lacking at the moment.

The post We Asked 3 AIs: Will XRP Ever Break Above $2? The Answers Were Not What We Expected appeared first on CryptoPotato.

Key Takeaways

- Zoom shares surged over 9% following a Q1 fiscal 2027 earnings beat

- The company reported $1.24 billion in revenue, reflecting 5.5% growth year-over-year, while enterprise revenue expanded 7.2%

- A $51 million stake in Anthropic acquired in 2023 has ballooned to approximately $1.3 billion

- Full-year outlook upgraded with revenue projected at $5.08–$5.09 billion and adjusted EPS reaching up to $6.00

- Several Wall Street firms increased their price targets, including Rosenblatt to $130 and Benchmark to $125

Zoom shares opened dramatically higher on Friday, surging more than 9% to approximately $105.55, following the video conferencing giant’s impressive first-quarter performance and the disclosure of a remarkably profitable investment in artificial intelligence startup Anthropic.

The financial results exceeded expectations on multiple fronts. Revenue totaled $1.24 billion, marking a 5.5% increase compared to the same period last year and surpassing Zoom’s own forecast of $1.22 billion. Adjusted earnings per share reached $1.55, up from $1.43 in the prior-year quarter. The company generated $500.5 million in free cash flow, representing an 8% increase.

Enterprise segment revenue climbed 7.2% to $755.7 million, now representing 61% of Zoom’s total revenue. The number of customers with annual spending exceeding $100,000 expanded 8.2% to 4,534.

The net dollar expansion rate improved to 99% from 98%, indicating that current customers are gradually increasing their expenditures.

CEO Eric Yuan attributed the strong performance to artificial intelligence initiatives. Paid users of AI Companion experienced 184% year-over-year growth. The company’s newer AI-powered note-taking feature, My Notes, attracted 1.5 million licensed users in just four months following its debut.

“Customers are increasingly adopting Zoom as an AI-first system of action for modern work,” Yuan said.

The Anthropic Investment Windfall

The earnings narrative gained additional momentum on Friday when a regulatory disclosure unveiled the remarkable appreciation of Zoom’s Anthropic investment.

Zoom invested approximately $51 million in Anthropic during May 2023 via its Zoom Ventures investment arm. That position has appreciated to nearly $1.3 billion — representing a gain exceeding $1 billion. The initial investment was designed to facilitate integration of Anthropic’s Claude language models into Zoom’s artificial intelligence offerings.

Anthropically is reportedly nearing completion of a massive funding round potentially reaching $30 billion at a $900 billion valuation, with Sequoia Capital, Dragoneer, Altimeter, and Greenoaks each expected to invest $2 billion. Should that valuation materialize, Zoom’s stake could appreciate further.

Cantor Fitzgerald analysts observed that if the Anthropic position, estimated at $1.5 billion of Zoom’s aggregate $1.88 billion strategic investment portfolio, achieves the $900 billion valuation benchmark, Zoom’s share price could reach $116.

Updated Guidance and Wall Street Response

Management increased its full-year projections. Zoom now anticipates revenue between $5.08 and $5.09 billion, adjusted EPS ranging from $5.96 to $6.00, and free cash flow of $1.7 billion for fiscal 2027.

The company also approved a fresh $1 billion share repurchase authorization.

Wall Street analysts responded swiftly. Morgan Stanley increased its price target to $105 from $92. Rosenblatt elevated its target to $130 from $115. Benchmark raised its outlook to $125 from $121. Mizuho adjusted upward to $120, and Needham also increased to $130. Bank of America moved to $105 while maintaining a Neutral rating.

Cantor Fitzgerald, which kept its Neutral rating, raised its target to $104 from $87, pointing to growing adoption of Zoom’s CX, Phone, and AI products.

Zoom’s 52-week peak of $113.73 was achieved during Friday’s trading session.

Key Takeaways

- Ford shares surged more than 9% on May 22, reaching a 52-week peak of $14.94

- Ford Energy secured a five-year agreement with EDF Power Solutions for up to 20 GWh of battery storage capacity

- The agreement leverages underutilized EV manufacturing capacity to meet surging AI data center energy storage demands in a market valued near $10 billion

- Ford recorded a $1.3 billion noncash benefit from tariffs following a Supreme Court decision

- Morgan Stanley maintained its Equalweight rating with a $14.00 price target on Ford

Ford Motor (F) shares rallied more than 9% during Thursday’s trading session on May 22, reaching a 52-week peak of $14.94 before closing near $14.93. The dramatic surge followed the automaker’s announcement of a significant battery storage partnership that captured investor attention.

The driving force: Ford Energy entered into a five-year partnership with EDF Power Solutions to deliver up to 20 gigawatt-hours of battery energy storage systems throughout the United States. Initial shipments are scheduled to commence in 2028.

What makes this agreement particularly interesting is Ford’s strategic approach to fulfilling it. Rather than constructing new production facilities, the automaker intends to leverage spare capacity at its existing electric vehicle manufacturing plants — facilities currently operating below maximum output — to manufacture battery storage units.

This represents an efficient deployment of underperforming assets. Industry observers believe the timing aligns well with escalating demand from artificial intelligence data centers, which require substantial power storage infrastructure to maintain continuous operations.

Financial Impact of the Partnership

Industry analysts project the battery storage sector that Ford is targeting could reach approximately $10 billion in value. Should Ford Energy achieve the complete 20 GWh capacity specified in the EDF partnership, some financial models indicate it could contribute around $0.10 to Ford’s earnings per share.

While this figure alone won’t revolutionize Ford’s bottom line, it represents a meaningful strategic pivot. Market watchers are anticipating potential additional customer partnerships that could emerge following this EDF arrangement.

The stock received an additional lift from a $1.3 billion noncash benefit related to tariffs stemming from a recent Supreme Court decision. Although this doesn’t represent actual cash flow, it enhances Ford’s reported financial statements and added to Thursday’s positive market sentiment.

Speculation also emerged regarding Ford potentially pursuing new defense sector contracts, though the company hasn’t officially confirmed these reports. Market participants appeared to factor in some optimism regarding these possibilities as well.

Wall Street’s Perspective

Morgan Stanley maintained its Equalweight rating on Ford following the announcement, keeping its price target unchanged at $14.00. Notably, this target actually sits below Thursday’s closing price — suggesting some Street analysts remain cautious about whether the rally is fully warranted.

Ford’s underlying financial metrics tell a complicated story. The automaker posted a negative EPS of -$1.56 for the trailing twelve months. Its Piotroski F-Score registers at 3 out of 10, indicating some areas of financial concern. However, the price-to-sales ratio of just 0.3 appears attractive given total revenue of $189.86 billion.

The stock has delivered approximately 37% returns over the past twelve months and currently provides shareholders with a dividend yield of 4.39%.

Additionally, Ford recently completed a $1 billion note offering maturing in 2036, and conducted its annual shareholder meeting where the board was re-elected and executive compensation packages received approval. On the management front, Chief Marketing Officer Lisa Materazzo will depart on June 1, with Dean Stoneley assuming interim responsibilities.

As of Thursday’s market close, Ford commanded a market capitalization of roughly $59.25 billion.

The European Central Bank warned EU finance ministers on Friday that proposals to expand euro stablecoin issuance could weaken bank lending and complicate monetary policy, according to three sources cited by Reuters.

The pushback came in response to a policy paper prepared by Brussels-based think tank Bruegel, whose authors presented their proposals at the two-day informal meeting of the Economic and Financial Affairs Council in Nicosia, Cyprus. The paper called for easing liquidity requirements for stablecoin issuers and potentially granting them access to ECB funding, arguing that these measures were necessary if the euro stablecoin market was to compete with dollar-backed rivals.

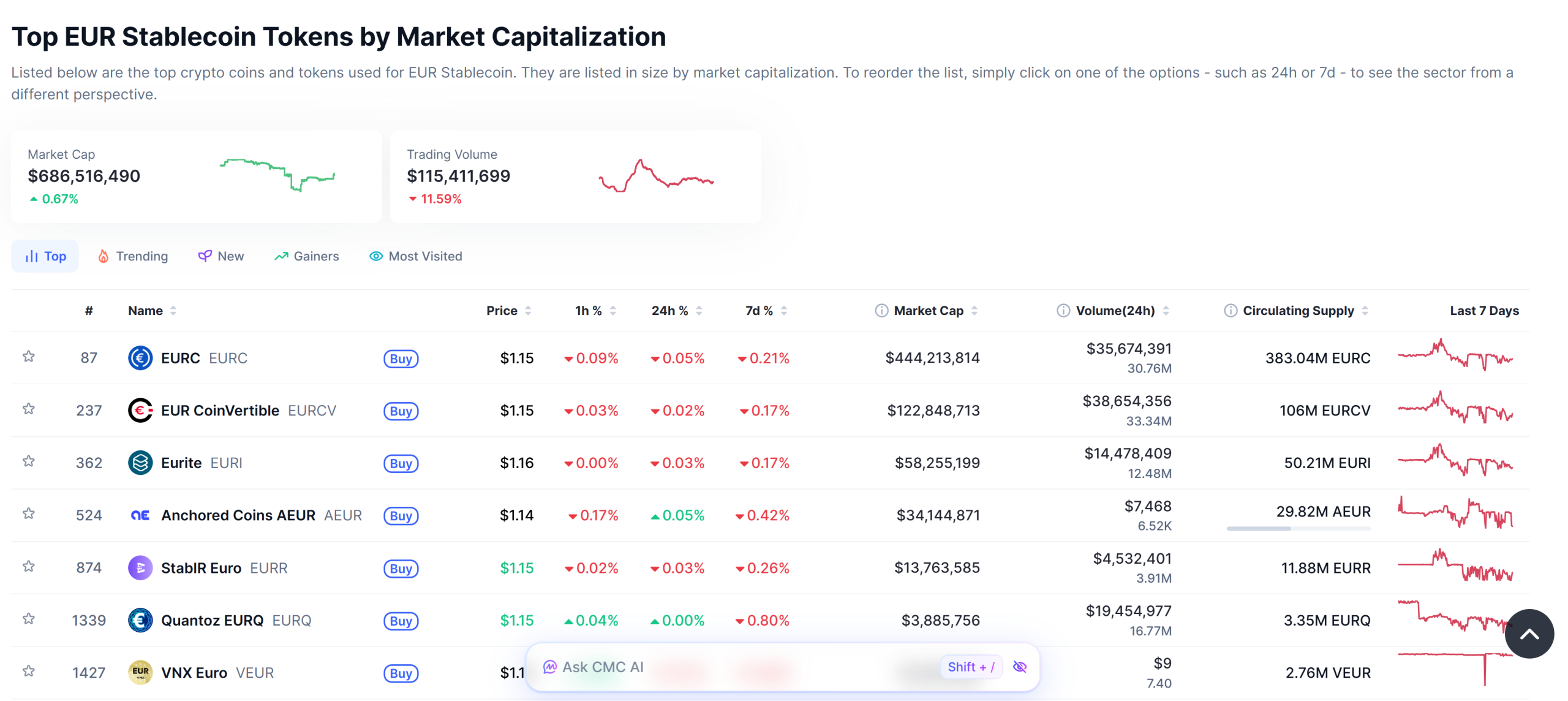

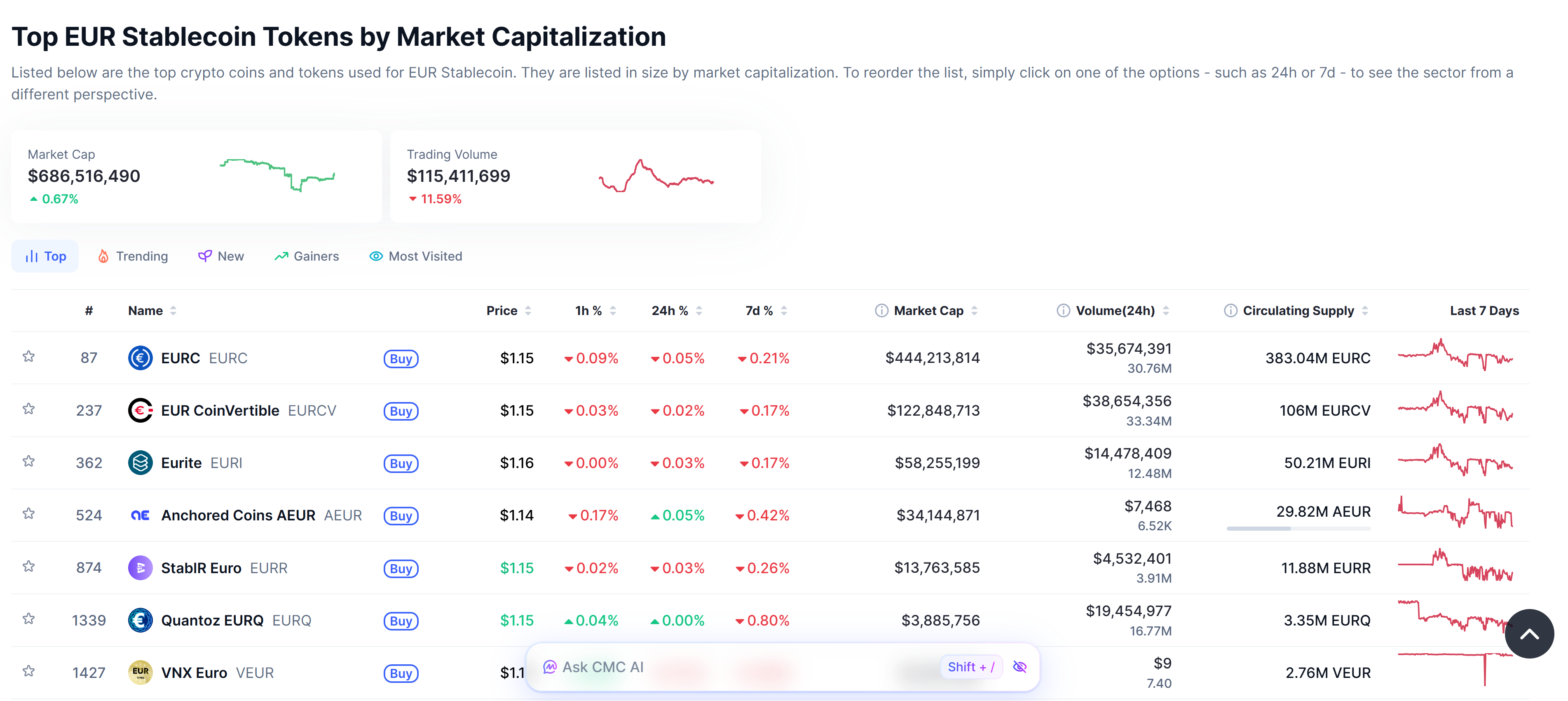

Europeans conduct 38% of global stablecoin transactions, yet euro-denominated tokens account for just 0.3% of total supply, per the policy paper. Circle’s EURC (EURC), the largest euro stablecoin, ranks only 12th globally, according to CoinMarketCap.

Top euro stablecoins. Source: CoinMarketCap

The question at the heart of the Nicosia meeting was whether Europe wants to close that gap badly enough to extend central bank-style support to stablecoin issuers. However, the ECB’s answer, for now, appears to be no.

Related: MiCA Made Euro Stablecoins Safe but Too Small, Report Says

Euro stablecoins could destabilize banks

ECB President Christine Lagarde led the resistance, warning that stablecoin issuance makes bank deposits less stable by transferring buyers’ funds to issuers’ accounts, according to Reuters. At scale, policymakers fear this accelerates disintermediation, raises bank funding costs and erodes the ECB’s ability to manage interest rates.

Several central bankers at the meeting also openly questioned the Bruegel proposal to position the ECB as a lender of last resort for stablecoin firms, an arrangement currently reserved for regulated banks, per the report.

In a speech at the Banco de España LatAm Economic Forum in Spain earlier this month, Lagarde argued that euro stablecoins could generate additional demand for euro-area safe assets but warned that the trade-offs, including financial stability risks, redemption pressures and weaker monetary policy transmission, outweigh the benefits.

Instead of stablecoins, Lagarde pointed to tokenized financial infrastructure anchored by central bank money as Europe’s preferred path, citing the Eurosystem’s Pontes project for wholesale settlement and the Appia roadmap for interoperable tokenized finance.

Related: European Banks Back MiCA Euro Stablecoin to Rival Dollar Tokens

EU central bankers shrug off digital dollarization fears

The Bruegel authors warned that stricter EU rules compared to the US risked accelerating digital dollarization, pushing activity outside the bloc. However, central bankers at the meeting largely dismissed that concern, with several calling instead for restrictions on European redemptions of both US and EU-issued stablecoins to guard against reserve runs, according to the Reuters report.

The debate comes as the EU reviews its Markets in Crypto-Assets (MiCA) regulation, which requires stablecoin issuers to hold large reserves in liquid assets, in contrast to the lighter-touch US GENIUS Act.

Market Moves: Why is Ethereum Foundation selling? BTC futures warning signs

Key Highlights

- Shares of NVTS climbed nearly 20% following investor conference announcements and sustained earnings-driven momentum

- First-quarter revenue reached $8.6M, exceeding forecasts; second-quarter outlook of approximately $10M surpassed Street projections by more than 11%

- Baird increased its price target from $9 to $20; Needham upgraded from $13 to $21

- Elevated short interest at 21% intensified the rally as bearish traders scrambled to exit positions

- Company secured a GaN technology licensing agreement with Cyient Semiconductors to produce India’s inaugural domestically branded GaN IC portfolio

Shares of Navitas Semiconductor (NVTS) reached a 52-week peak of $28.85 during Thursday’s trading session, climbing nearly 20% as several positive developments converged simultaneously.

Navitas Semiconductor Corporation, NVTS

The upward momentum accelerated following the company’s announcement that CEO Chris Allexandre and CFO Tonya Stevens will participate in the Craig-Hallum Institutional Investor Conference scheduled for May 28 in Minneapolis, along with the Evercore Global TMT Conference set for June 3 in San Francisco.

This conference participation news built upon recent earnings results that exceeded Wall Street projections. First-quarter revenue totaled $8.6M, surpassing analyst forecasts, while earnings per share registered at -$0.04 compared to the consensus estimate of -$0.05.

Management’s second-quarter fiscal 2026 revenue projection of roughly $10M exceeded the Street’s $8.93M estimate, suggesting sequential revenue expansion exceeding 16% alongside enhanced gross margin performance.

Wall Street analysts moved swiftly to adjust their outlooks. Baird elevated its price objective from $9 to $20, highlighting three secular expansion drivers connected to 800V AI data-center power infrastructure.

Needham subsequently increased its target from $13 to $21, emphasizing the quarterly earnings outperformance and above-consensus forward guidance as key justifications.

The semiconductor company had already established itself as one of the sector’s more notable recovery narratives. Through the current year, NVTS has advanced more than 241%.

Short Covering Intensifies Upward Movement

With short interest representing 21% of available shares as of mid-April, Thursday’s positive catalysts didn’t merely draw in fresh buyers — they compelled short sellers to unwind positions.

When heavily-shorted securities experience rapid price appreciation, forced covering can drive valuations significantly beyond what fundamental factors alone might justify, a pattern that clearly manifested in this situation.

Strategic GaN Partnership Expands Market Reach

Navitas simultaneously unveiled a licensing arrangement with Cyient Semiconductors to create India’s first domestically branded 650–700V gallium nitride integrated circuit product line.

These semiconductor components target AI data center applications, telecommunications infrastructure, rapid charging solutions, industrial power systems, and electric mobility sectors. Cyient will additionally serve as an alternative manufacturing source for selected Navitas GaN products.

This partnership introduces an expanded geographical element to NVTS’s expansion narrative and reflects increasing global appetite for its gallium nitride semiconductor technology.

From a financial position standpoint, NVTS maintains negligible debt obligations while holding cash reserves exceeding $220M, providing sufficient capital to support its gallium nitride and silicon carbide transformation without requiring external financing in the near term.

Broader equity markets contributed supportive conditions as well, with the S&P 500 advancing 0.6%, the Dow Jones climbing 0.8%, and the Nasdaq gaining 0.6% during the session.

Industry competitors including Wolfspeed and Marvell Technology continue operating within the AI power semiconductor landscape, sustaining investor focus on the broader GaN and SiC technology ecosystem.

NVTS’s current market capitalization stands at approximately $5.37B, with typical daily trading volume approaching 29 million shares. The stock concluded trading on May 22 at its 52-week peak of $28.85.

GameStop (GME) CEO Ryan Cohen publicly questioned eBay’s spending efficiency after the e-commerce platform posted a Senior Manager of Marketing Effectiveness role, citing the company’s $2.4 billion marketing budget.

The remarks extend a running public dispute between the two companies. It began with GameStop’s rejected $56 billion acquisition offer and escalated after eBay suspended Cohen’s seller account.

Cohen Questions Where the Money Goes

In response to a seller’s thread about eBay’s support failures and account access problems, Cohen posted on X that a company with $2.4 billion in marketing spend should be able to handle basic platform functions.

When a separate post flagged eBay’s new Toronto-based marketing effectiveness role, Cohen quote-tweeted it with a pointed observation that the position’s responsibilities include finding out where the money is going.

The role, listed under job code R0074539, sits within eBay’s Marketing & Communications division and reports to the Head of Marketing Efficiency. eBay’s fiscal 2025 sales and marketing spend totaled $2.4 billion.

GameStop – eBay Takeover Feud Behind the Jabs

Cohen’s efficiency critique ties to the ongoing GameStop acquisition bid. GameStop offered $56 billion in cash and stock, or $125 per share. TD Securities provided a highly confident letter backing up to $20 billion in financing.

eBay’s board reviewed the proposal and rejected the bid as neither credible nor attractive after consulting independent advisors.

Shortly after the feud became public, eBay permanently suspended Cohen’s seller account. The company said the activity posed a risk to its community.

Cohen had listed GameStop-branded items on the platform, including store signs and a square of branded carpet. The Cohen account suspension drew substantial public attention and was widely viewed as a deliberate publicity move.

With the acquisition rejected and his account banned, Cohen has turned to publicly scrutinizing eBay’s operations. The marketing effectiveness hire gives him a ready-made target.

The post GameStop CEO Questions eBay’s $2.4 Billion Marketing Spend appeared first on BeInCrypto.

Bitcoin ETF outflows reached $1.26 billion over six sessions, but Santiment says the streak signals a buying opportunity.

Summary

- US spot Bitcoin (BTC) ETFs recorded net outflows in each of the six trading sessions from May 15 through May 22, totalling $1.26 billion across 11 funds.

- Santiment says ETF flows reflect retail investor sentiment rather than institutional positioning, calling the outflow streak a contrarian accumulation signal.

- Bitcoin was trading at $75,410 when Santiment published its report, down from a May high of $79,052 reached on May 16.

The 11 US-listed spot Bitcoin ETFs have recorded net outflows in each of six sessions from May 15 through May 22, totalling $1.26 billion according to Farside data.

“Sustained ETF outflows have historically correlated with conditions favorable for patient accumulation rather than panic,” Santiment said in a published report. The analytics firm argued that ETFs disproportionately reflect retail conviction rather than smart money positioning, making large outflows a counter-signal.

Why Santiment reads outflows as a buying signal not a warning

Santiment’s analysis rests on a historical pattern: Bitcoin’s strongest rallies have followed periods of heavy ETF withdrawals. The firm said retail investors grew less patient after Bitcoin failed to hold $80,000, with the current streak resembling a healthy market reset.

ETF analyst James Seyffart noted that Bitcoin ETFs have clawed back most of the $9 billion in outflows seen between October 2025 and February 2026. Crypto.news has reported on the first May outflow event, which reversed the early-month inflow trend.

What the Farside data shows across the 11 funds

Fidelity’s Wise Origin Bitcoin Fund led individual redemptions within the streak. BlackRock’s IBIT saw outflows on multiple sessions, and Morgan Stanley’s MSBT attracted positive flows on some days during the period.

Crypto.news has tracked Bitcoin ETFs ending Q1 2026 with net outflows of approximately $500 million, showing the current six-session streak continues a broader 2026 pattern of intermittent redemptions.

Santiment’s contrarian framing does not eliminate further downside risk. If Bitcoin breaks below $74,000, the outflow streak would need reassessment as a buy signal.

Key Takeaways

- BB shares reached a 52-week peak at $6.64, surging approximately 19% in one trading session

- Fourth quarter fiscal 2026 earnings exceeded projections: EPS of $0.06 versus consensus of $0.05, revenue of $156M compared to $142.55M forecast

- QNX business unit posted 20% annual growth, achieving record revenue of $78.7M

- Company executives announced at CIBC Technology and Innovation Conference that BlackBerry is transitioning into a phase of profitable expansion

- InvestingPro data suggests potential overvaluation; Baird maintains $5.00 target, Canaccord sets $4.40 price objective

Shares of BlackBerry soared approximately 19% to reach a 52-week peak of $6.64, extending a rally that has propelled the stock more than 75% higher year-to-date.

The dramatic upswing followed executive presentations at the CIBC Technology and Innovation Conference 2026, where company leadership informed investors that BlackBerry has entered a phase of profitable growth driven by its QNX software platform and physical AI initiatives.

The announcement resonated strongly with market participants who have been increasingly receptive to the company’s transformation toward software-centric operations.

Additional momentum came from the renewal of a critical U.S. FedRAMP cybersecurity authorization for the AtHoc platform. The Class D (High) recertification maintains BlackBerry‘s qualification for federal government contracts, providing important support for its Secure Communications division.

A reinstated share repurchase authorization, encompassing up to 26.8 million shares, further bolstered investor sentiment by demonstrating management’s conviction in the strategic direction.

Fourth Quarter Results Surpass Forecasts

BlackBerry’s fiscal 2026 fourth quarter performance exceeded analyst expectations across key metrics. The company delivered adjusted earnings per share of $0.06, topping the $0.05 consensus estimate, while revenue reached $156 million—significantly above the projected $142.55 million.

The revenue figure marked a 10% year-over-year expansion, reflecting the type of sustained top-line momentum the organization has been pursuing through its strategic transformation.

The QNX division, which develops embedded software solutions for automotive and industrial applications, delivered particularly strong results. Revenue in this segment increased 20% to an all-time high of $78.7 million. Meanwhile, the Secure Communications unit expanded 8% to $72.5 million.

Wall Street Price Targets Lag Stock Performance

Notwithstanding the market’s enthusiasm, Wall Street analyst price objectives haven’t kept pace with the stock’s ascent.

Baird maintained its Neutral stance with a $5.00 valuation target. Canaccord revised its objective downward to $4.40 while retaining a Hold recommendation.

Both price targets remain substantially beneath current trading levels, suggesting potential concerns about whether market valuations have outpaced underlying business fundamentals.

InvestingPro’s analytical framework identifies the stock as potentially trading above its Fair Value estimation, including BB among its most overvalued securities.

During the preceding six-month period, shares have appreciated nearly 49%. For the current year, gains exceed 75%. The company’s market capitalization currently stands at roughly $3.62 billion.

Daily trading volume averages approximately 15.9 million shares, while technical momentum indicators presently generate buy signals.

The primary recent catalyst continues to be the CIBC conference presentations coupled with robust QNX performance, the FedRAMP recertification achievement, and the buyback program announcement.

TLDR:

- Bloom Energy posted $751M in Q1 2026 revenue, a 130% year-over-year jump driven by AI data center demand.

- Bloom deploys fuel cell systems in 90 days versus the two-to-five years a standard grid connection typically requires.

- Oracle has committed to procure up to 2.8 gigawatts of Bloom’s systems, with 1.2 gigawatts already under contract.

- Bloom projects 30% of all data center sites will rely on onsite power as a primary energy source by 2030.

Bloom Energy is gaining ground as one of the most closely watched names in AI infrastructure. The company posted $751 million in revenue in Q1 2026, a 130% increase year over year.

Product revenue alone grew 208% in that single quarter. With full-year 2026 guidance now set at $3.4 billion to $3.8 billion, Bloom Energy is moving well beyond the margins of the AI buildout conversation.

Rapid Deployment Solves the AI Power Problem

Bloom Energy addresses a bottleneck that is slowing down data center construction across the sector. A traditional utility grid connection for a large data center typically takes two to five years to complete.

Bloom can deploy its fuel cell systems in as little as 90 days, scaling from 20 megawatts up to 500 megawatts per site.

That speed is one of the key reasons major cloud and infrastructure operators are turning to Bloom. Oracle has committed to procure up to 2.8 gigawatts of Bloom’s fuel cell systems, with 1.2 gigawatts already under contract.

Equinix, CoreWeave, and AEP — which supplies power to Amazon Web Services — are also confirmed customers.

The reliability figures are also notable. Bloom’s systems operate at up to 99.999% availability. That number exceeds what most utility grid connections can guarantee, making it a compelling option for workloads that cannot tolerate downtime.

Milk Road AI, an industry analyst account, described the investment case in a recent post: Bloom solves the single biggest problem in data center development right now — getting power fast.

Analysts at Milk Road Pro flagged Bloom Energy early. Their central thesis was that the AI energy bottleneck would become just as large an investment opportunity as the chip bottleneck. That view has since been validated by the company’s financial results and contract pipeline.

Institutional Deals and Production Expansion Signal Long-Term Growth

The scale of Bloom’s commercial agreements suggests this is not a temporary cycle. Bloom has signed a $5 billion strategic AI infrastructure partnership with Brookfield Asset Management.

Under that agreement, Bloom becomes the preferred onsite power provider across Brookfield’s $1 trillion infrastructure portfolio.

This week, a supplier to Bloom received what it described as the largest single contract in its company’s history. The contract covers switchgear manufacturing in support of a large-scale AI data center project.

On the production side, Bloom is on track to double its annual manufacturing capacity to 2 gigawatts by the end of 2026. Further scaling is planned beyond that point.

The company’s own research projects that approximately 30% of all data center sites will rely on onsite power as a primary energy source by 2030.

That market barely existed three years ago. The shift toward continuous computing — where AI models run around the clock rather than on demand — is what is driving the structural change.

Jensen Huang, CEO of Nvidia, has noted that AI computing requires up to 1,000 times more energy than traditional on-demand computing, and has acknowledged that estimate could move in either direction by another order of magnitude.

Bloom Energy’s stock has risen 1,231% over the past twelve months and is up more than 130% year to date. Those figures reflect a broader market recognition that the energy layer of AI infrastructure carries just as much value as the hardware layer above it.

Michael Saylor says a Strategy Bitcoin sale before year-end is ‘not unlikely’ in a Coin Stories podcast interview.

Summary

- Saylor told Natalie Brunell it was “not unlikely” Strategy would sell some Bitcoin before year-end, softening his long-held never-sell position.

- He said any model relying solely on equity, credit, or Bitcoin sales underperforms, and that Strategy uses a mixed capital management approach.

- Strategy holds 818,334 BTC worth approximately $65 billion and aims to maximise Bitcoin per share over a seven-year horizon to 2033.

Strategy executive chairman Michael Saylor told the Coin Stories podcast it was “not unlikely” the company would sell some Bitcoin before year-end. The comment softens his long-standing public position that Strategy would never sell.

“I think it’s not unlikely that we’ll sell some Bitcoin between now and the end of the year,” Saylor said. “Any model that we put together that’s limited only to equity or only to credit or only to Bitcoin always underperforms.”

Why Saylor says Strategy might sell Bitcoin in 2026

The comments follow Strategy’s Q1 earnings call, where Saylor said the company raised the possibility of selling Bitcoin to fund dividends, saying it would “inoculate the market.” Crypto.news has reported on that call and the $12.54 billion Q1 net loss that preceded it.

Saylor described Strategy’s capital management as programmatic and data-driven, with liabilities evaluated against a mix of cash, equity, credit and Bitcoin. Strategy holds 818,334 BTC acquired for approximately $61.6 billion at an average price of $75,527.

Saylor also confirmed Strategy does not plan to retire its STRF, STRD, and STRK preferred products, calling them useful parts of the capital structure while convertible bonds remain senior liabilities to be retired over time.

What a Strategy Bitcoin sale would mean for markets

Saylor said any sale would be small relative to Bitcoin’s daily market liquidity, estimated at $20 to $50 billion. He argued Strategy could buy roughly 20 Bitcoin for every one sold if dividends were fully funded through BTC sales.

Crypto.news has noted Saylor’s framing of Strategy’s three-layer capital structure, with Bitcoin as digital capital, STRC as digital credit, and MSTR as leveraged equity. The firm’s seven-year goal is to maximise Bitcoin per share by 2033.

Saylor said this long-term lens makes 2026 Bitcoin sales a capital allocation decision, not a reversal of conviction.

We Asked 3 AIs: Will XRP Ever Break Above $2? The Answers Were Not What We Expected

Lucknow Super Giants’ Top-Scorer Ruled Out Of Crucial IPL 2026 Match vs Punjab Kings

Is The Google Pixel 9 Still A Good Buy In 2026?

-

Crypto World2 days ago

Crypto World2 days agoBlockchain.com files with SEC for U.S. IPO

-

Fashion17 hours ago

Fashion17 hours agoHoliday Weekend Open Thread – Corporette.com

-

Crypto World6 days ago

Crypto World6 days agoIntesa Sanpaolo’s crypto holdings jump to $235M as XRP enters

-

Business21 hours ago

Business21 hours agoDell Technologies DELL Stock Surges 15% on AI Server Momentum and Analyst Upgrades in 2026

-

Crypto World21 hours ago

Crypto World21 hours agoSpace X IPO Is ‘Bad News’ for Tech Stocks: But What About Bitcoin?

-

Fashion6 days ago

Fashion6 days agoOn the Scene at Gucci’s Cruise Show in New York City: Mariah Carey, Kim Kardashian, Lindsay Lohan, Iman, and More!

-

Fashion7 days ago

Fashion7 days agoTrending Western Style Vests Perfect for Summer

-

Politics17 hours ago

Politics17 hours agoMakerfield: a tale of two social-media histories

-

Crypto World1 hour ago

Crypto World1 hour agoRobinhood crypto COO Tanya Denisova exits

-

Fashion6 days ago

Fashion6 days agoAmazon Sundays: Memorial Day Hosting

-

Tech23 hours ago

Tech23 hours agoA 0.12% parameter add-on gives AI agents the working memory RAG can’t

-

Entertainment6 days ago

Entertainment6 days agoOff Campus Easter Eggs Explained: Characters, Stories, More

-

Crypto World5 days ago

Revolut Launches Dogecoin Debit Card Across UK and EU

-

Crypto World22 hours ago

Crypto World22 hours agoAI infrastructure race heats up as IREN pitches full-stack strategy, WhiteFiber lands $160M deal

-

Crypto World1 day ago

Crypto World1 day agoBitcoin Accumulation Weakens as BTC Realized Losses Hit $600M

-

NewsBeat2 days ago

NewsBeat2 days agoCharity run by Reform leader Malcolm Offord accused of ‘law breaking’ over Scottish registration

-

Tech2 days ago

Tech2 days agoWhatsApp ads could make Irish debut after discussions with DPC

-

Sports1 day ago

Sports1 day ago2026 CJ Cup Byron Nelson leaderboard: Brooks Koepka finds putting stroke in Round 1

-

Business6 days ago

Australia defends property tax changes designed to fix ‘broken’ housing

-

Crypto World1 day ago

Crypto World1 day agoTrump Media’s Bitcoin Stash Shrinks Again as 2,650 BTC Lands on Crypto.com

You must be logged in to post a comment Login