Crypto World

Bitcoin’s Key Resistance Stall Could Send it Tumbling Much Lower: Analysts

Bitcoin has hit resistance at its 200-day moving average and is showing signs of a trend reversal, according to CryptoQuant on Wednesday. The move closely mirrors a March 2022 pattern where a 43% rally stalled at the same level before prices declined further.

“Overall, Bitcoin demand has flipped into contraction,” the analyst wrote.

The platform’s “Bull Score Index” has declined from 40 back to extreme bearish territory at 20, “as stalling stablecoin liquidity, and negative price momentum simultaneously eroded the composite signal.”

This score is consistent with the deep bear market readings of February and March, when prices declined to $60,000, and historically “has preceded either further price weakness or extended consolidation,” they added.

Bitcoin Correction Likely to Continue

If the correction continues, the $70,000 level represents the primary on-chain support target, the traders’ on-chain realized price. The analysts noted that this level has functioned as a “precise inflection point” throughout the current bear market cycle.

A break below this back into the $60k zone could result in new bear market lows, however. Meanwhile, Glassnode reported on Wednesday that Bitcoin has reclaimed the True Market Mean at $78,300 but failed to sustain above it. However, it also noted that the correction from recent highs is likely to continue if previous cycle patterns repeat.

“Any deeper correction from current levels would therefore reframe the recent rally as a local top within the ongoing bear market, a structure that has recurred multiple times in prior cycles and remains the higher probability outcome until price demonstrates sustained follow-through.”

Bitcoin momentum has faded from full max momentum, reported Swissblock on Thursday. It remained cautiously bullish, stating that as long as momentum does not degrade significantly, “the base case is consolidation, not breakdown.”

Bitcoin momentum has faded from full max momentum.

But as long as it does not fall below -0.5, this does not imply breakdown.

What usually follows is consolidation.

The key reference is June–July 2025.

Momentum faded from full strength, but the indicator never broke below… https://t.co/QkVFmMTReb pic.twitter.com/ZarKY77Bx3

— Swissblock (@swissblock__) May 21, 2026

Crypto Market Outlook

Bitcoin has climbed steadily over the past 24 hours, gaining 1.7% from $76,600 to tap $78,000 twice during the Thursday morning Asian trading session.

However, this level is also a resistance zone that needs to be overcome quickly for BTC to reach $80,000 again. Volumes and sentiment suggest it will be thwarted here again.

Ether prices have mirrored the move, but it remains bearish under $2,150 at the time of writing, while the altcoins were notching larger gains. Hyperliquid and Zcash had exploded with double-digit gains on the day.

The post Bitcoin’s Key Resistance Stall Could Send it Tumbling Much Lower: Analysts appeared first on CryptoPotato.

Since 2024, Bitcoin (BTC) has posted four major corrections after interest rate hikes by the Bank of Japan (BOJ), with declines ranging from 18% to 28%. This dynamic places renewed attention on the BOJ’s June 16 policy decision.

Data currently point to a variety of pressures on BTC, with BTC whale distribution and exchange inflows possibly carrying more weight than Japanese monetary policy.

BOJ hikes and Bitcoin drawdowns: Will history repeat?

The relationship between BOJ policy and Bitcoin has gained attention because each rate increase since Japan ended its negative interest rate policy has been followed by a sizable correction.

Following the March 19, 2024, hike, Bitcoin corrected by 18%. The July 31, 2024, increase preceded a 18.5% decline.

After the Jan. 24, 2025, hike, Bitcoin fell nearly 25%, while the Dec. 19, 2025, decision was followed by a 28% drawdown.

Across the four events, Bitcoin’s average decline was 22.4%.

BTC/USD, one-week chart. Source: Cointelegraph/TradingView

The sell-offs did not occur under identical conditions. The March 2024 correction followed Bitcoin’s breakout to new all-time highs during the spot Bitcoin exchange-traded fund (ETF) cycle. The July 2024 decline followed months of consolidation below peak levels and coincided with the sharp unwind of the yen carry trade, which affected global markets.

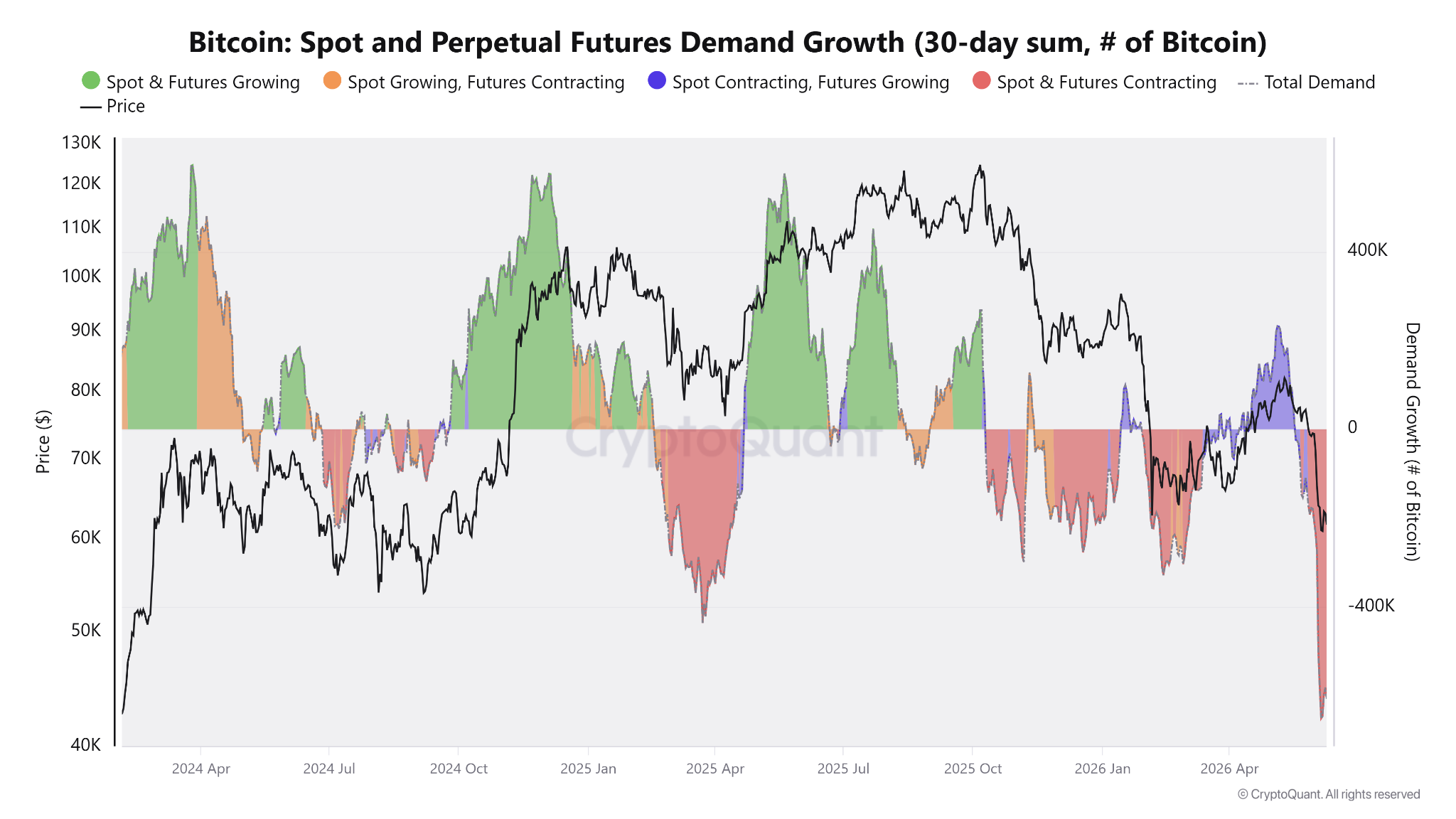

The January and December 2025 drawdowns followed extended rallies and periods of contraction for both BTC spot and futures 30-day demand.

BTC: spot and perpetual futures demand growth contraction. Source: CryptoQuant

The relationship between BOJ policy and Bitcoin is often linked to the yen carry trade. For years, investors borrowed yen at low rates and deployed that capital into higher-yielding assets, including stocks and cryptocurrencies.

When the BOJ raises rates, some of those positions can be reduced, weighing on risk assets. The July 2024 hike coincided with one of the largest carry-trade unwinds in recent years and a sharp sell-off across global markets, not only BTC.

The influence of that particular condition appears smaller today. The BOJ has already raised rates to 0.75% from -0.1% in March 2024, while Japan’s 10-year government bond yield climbed to 2.68% from 0.63% over the same period.

Japan’s 10-year bond yield increase since 2024. Source: TradingEconomics

With Japan’s borrowing costs already higher than during the negative-rate era, each additional hike represents a smaller policy shift than the BOJ’s initial move away from ultra-loose monetary policy. The June 16 meeting would extend an existing tightening cycle rather than introduce a new one.

Likewise, market analyst Cryptic Trades noted that concerns about a renewed yen carry-trade unwind are overblown, arguing that Japan has effectively moved away from its deflationary policy framework in 2024. The analyst added,

“The Yen Carry Trade has been dead ever since 2024. It is also a BIG nothing burger for the markets.”

Related: Bitcoin price may slide toward $30K as institutions dump 450% of daily BTC supply

BTC whales add to the pressure

While the BOJ meeting is a macro event that traders may monitor, onchain data points to a more immediate source of pressure.

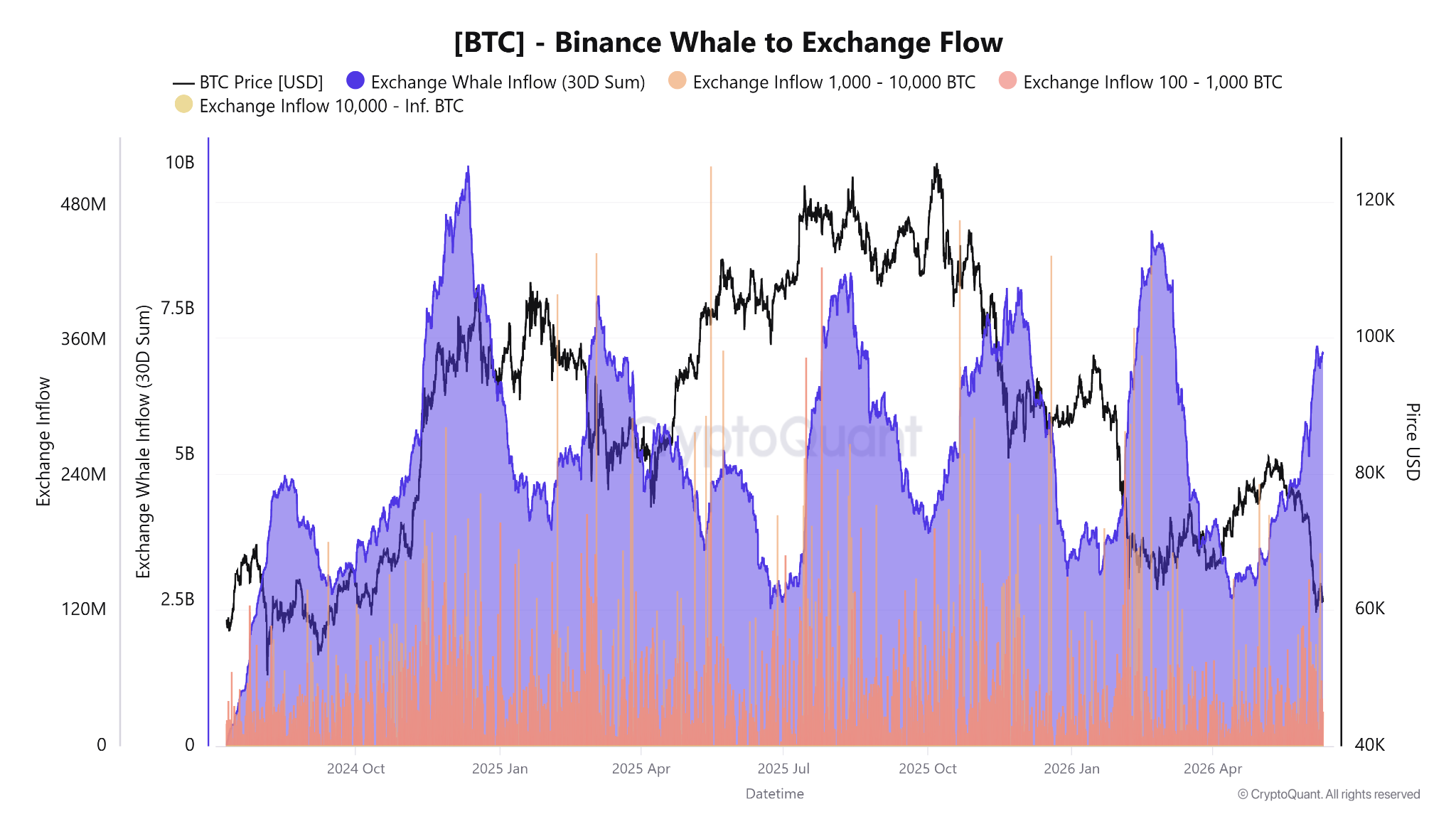

Crypto analyst MorenoDV noted that Binance has recorded rising BTC inflows from wallets holding 100–1,000 BTC and 1,000–10,000 BTC since the sell-off began in early June. As a result, the exchange’s 30-day whale inflow sum has climbed to $6.6 billion.

Bitcoin whale to exchange flow. Source: CryptoQuant

The pressure is already visible in realized activity. Short- and long-term whales have collectively locked in more than $2.5 billion in losses during the decline, indicating that some large holders have actively reduced exposure.

Short-term whales appear particularly vulnerable. The cohort is carrying roughly $16 billion in unrealized losses after briefly returning to profit for around 10 days in early May. Those positions now sit close to break-even levels, creating a potential source of supply during rebounds. MorenoDV said,

“Taken together, these three readings describe the stress profile of a late-stage bear market: capitulating whales, distribution into weakness, and a fragile short-term cohort with its finger on the trigger.”

Related: Bitcoin may act as a ‘canary in the coal mine’ as risk-off pressure spreads: Bitwise

Venture capitalist Tim Draper says fears that quantum computing will break Bitcoin (BTC) are misplaced, arguing that traditional banks and the dollars held within them face a bigger security risk.

In comments published by Benzinga and amplified in an X post on June 9, Draper said he considers his BTC holdings safer than cash sitting in a bank account.

Draper Says Banks Face Greater Quantum Risk Than Bitcoin

Responding to concerns that quantum computers could eventually crack BTC’s cryptography, Draper pointed out that financial institutions rely on older infrastructure that would be easier to compromise than the Bitcoin network.

“Quantum will crack the banks long before it touches the blockchain,” he wrote on X. “Everyone’s panicking about quantum breaking Bitcoin’s encryption while banks are running on legacy infrastructure that makes Bitcoin look like Fort Knox.”

He also argued that even if something did happen to the Bitcoin network, full node operators could roll back to the last secure block. Banks, as he put it, “don’t have that option.”

The rollback point is worth examining carefully. While that type of fork is technically feasible, it needs consensus from many node operators and miners, and it is usually only resorted to in extreme circumstances. Additionally, it would contradict Bitcoin’s claim of immutability, a tension that Draper did not address.

BTC investor Lark Davis backed Draper’s broader framing, saying that if people used “basic security hygiene,” then their holdings would be safer than cash in the bank, unless their keys got stolen. He also insisted that quantum technology will break all legacy security, so people need to stop singling out the cryptocurrency.

Draper also repeated a long-held prediction that Bitcoin will one day eclipse the dollar. He broke down the mechanism for that in a Crunchbase interview earlier in the year, where he said a time will come when retailers will “only take Bitcoin,” and were that to happen, he believes there would be a run on the dollar. Such is his confidence in the asset that in April this year, he reiterated an old bet that BTC could hit $250,000, this time giving it 18 months to do so.

A More Complicated Picture From Security Researchers

The quantum threat to Bitcoin has been analyzed in detail by several researchers, including on-chain analyst James Check, who in April argued that the commonly cited figure of 6.3 million BTC with exposed public keys overstates the actual risk.

According to him, active institutions such as exchanges and custodians, which face most of that exposure, are already working on solutions to mitigate that risk, meaning the genuinely high-risk portion is the roughly 1.716 million BTC in early-era Pay-to-Public-Key addresses, most of which he said are assumed to be permanently lost coins from Bitcoin’s earliest blocks.

Meanwhile, Draper’s infrastructure argument is directly counter to security expert Jameson Lopp’s. According to the Casa co-founder, who co-authored the BIP-361 proposal to freeze quantum-vulnerable addresses, banks can upgrade to counter quantum threats “orders of magnitudes faster” than Bitcoin, given that the cryptocurrency needs broad decentralized consensus before any protocol change can be made.

He estimated that it could take as much as a decade for a full Bitcoin upgrade to quantum-resistant cryptography, and that is the core difference. Draper is betting that banks will fail first, but Lopp thinks that Bitcoin’s slowness to upgrade will be the harder problem to solve.

The post Tim Draper Explains Why Bitcoin Is Safer Than Banks in the Quantum Era appeared first on CryptoPotato.

Crypto World

Mastercard prepares agentic commerce platform for a future where AI agents make payments

Mastercard (MA) is betting that AI agents will soon become active participants in the economy and wants its payments network to sit at the center of that shift.

The payments giant on Tuesday unveiled Agent Pay for Machines (AP4M), a service enabling AI agents and software systems to make payments to each other securely and at scale. The platform supports automated transactions across cards, bank accounts and stablecoins, while providing identity verification, spending controls and guaranteed settlement through Mastercard’s network.

The service comes as companies across technology, payments and crypto race to build infrastructure for what many are calling agentic commerce, where AI systems complete tasks, purchase services and coordinate transactions on behalf of users. Agents could be involved in trillions of dollars worth of transactions by the end of the decade, according to some estimates.

“We are already seeing a number of services and agents popping up to provide a range of products and services,” Raj Dhamodharan, Mastercard’s executive vice president of blockchain and digital asset products and partnerships, told CoinDesk. Those services range from booking travel and building websites to creating artwork and completing other digital tasks.

Dhamodharan said the next challenge is creating trust between those systems.

Businesses and consumers need confidence that agents are interacting with legitimate counterparties and operating within authorized spending limits. Service providers, meanwhile, need assurance that they will be paid.

“These are problems that we’ve solved before in the B2B world and the carded world for decades,” Dhamodharan said. “We’re bringing the same level of trust and ability to find the right set of agents, ability to convey that you’re actually going to complete the payment and to make sure that people can get paid.”

The platform is designed to address those concerns through credentialing, permissioning and settlement services. The company said the system can authenticate agents, enforce spending rules and settle payments across multiple payment methods, including stablecoins.

More than 30 companies have joined the initiative, including Coinbase (COIN), Stripe, Adyen, Checkout.com, Cloudflare, RippleX, Polygon Labs, Solana Foundation and OKX. Mastercard said permissions and credentials associated with AI agents will initially be recorded on the Polygon, Solana and Base blockchains.

Although large-scale machine-to-machine commerce remains nascent, Dhamodharan said Mastercard is already seeing signs of demand. He pointed to increasing activity around HTTP 402, an emerging internet payment standard, where automated transactions often fail because no payment method is available.

“There are already transactions happening,” he said. “There are already many declines happening because there is no payment option available. That is a leading indicator in our view.”

Mastercard said it plans to expand access to Agent Pay for Machines later this year.

If bitcoin and Ethereum had been invented on the same day, nobody would have heard of bitcoin. I sold every bitcoin Bit Digital held and deployed the proceeds into Ethereum. I have built one of the largest corporate Ethereum treasury positions in the world and said, on the record, that we will never sell it. People have asked me to articulate the single strongest argument for that conviction. On March 30, 2026, that argument arrived. Last month, Citi confirmed it.

In a research note published on May 18, Citi analysts warned that quantum computing advances have shortened the timeline for practical attacks on digital assets, and reached a conclusion that should give every institutional bitcoin holder pause: bitcoin faces significantly greater quantum risk than Ethereum, and the gap between them comes down not just to technology but to governance.

That finding echoes the landmark paper released in late March by Google Quantum AI in collaboration with Stanford University and the Ethereum Foundation, which found that the computing resources required to break bitcoin’s foundational cryptography are approximately 20 times lower than previously estimated. A sufficiently advanced quantum computer, operating with fewer than 500,000 physical qubits, could derive a bitcoin private key from its public key in roughly nine minutes. That machine does not exist today. But the window to act responsibly is narrowing faster than most institutions realize. When Google raises the alarm, and Citi confirms it in the same quarter, this is no longer a fringe concern. This is the silver bullet. And it points directly at bitcoin.

Why bitcoin is exposed

Bitcoin’s security rests on elliptic curve digital signature algorithms. When you spend bitcoin, your public key is briefly exposed onchain. Under classical computing, reversing that to obtain a private key is infeasible. Quantum computers running Shor’s algorithm can, in principle, do exactly that during the brief window a transaction is broadcast. The Google paper doesn’t merely confirm this theoretically; it quantifies it with a precision that removes comfortable ambiguity.

Nic Carter, co-founder of Coin Metrics and one of the sharpest minds in digital assets, has been sounding this alarm for months. In a series of essays beginning in October 2025, Carter called quantum computing “the biggest long-term risk to bitcoin’s core cryptography” and accused developers of “sleepwalking towards collapse.” He estimates a quantum computer could meaningfully break elliptic curve cryptography as early as 2028. Approximately 6.9 million BTC could be vulnerable at a sufficient quantum scale, including legacy wallets and Taproot outputs, which already represented more than 21% of all bitcoin transactions in 2025.

Bitcoin’s governance problem

One might ask: can’t bitcoin simply upgrade? Yes, in theory. In practice, this is where the risk compounds.

Bitcoin’s governance is intentionally conservative and consensus-driven, which makes it extraordinarily slow. SegWit took roughly 8.5 years from conception to widespread adoption. Taproot took approximately 7.5 years. The current quantum proposals, BIP-360 and BIP-361, are still at the draft or early testnet stage as of 2026. A full base-layer transition to post-quantum signatures would be the most contentious change bitcoin has ever attempted. As Carter documented, most bitcoin Core developers have expressed limited concern about urgency, a disposition that is, at minimum, a serious governance liability for any institution holding bitcoin in treasury. A quantum breakthrough does not politely wait for committee consensus.

Ethereum has already acted

This is where the picture diverges sharply. Ethereum’s approach to quantum resistance is not a reactive scramble. It is a structured road map already in execution, built on the NIST post-quantum cryptography standards finalized in August 2024.

The Pectra upgrade, which shipped on Ethereum mainnet in May 2025, introduced EIP-7702, a critical stepping stone toward full account abstraction. Rather than requiring a single network-wide hard fork, Ethereum’s architecture allows individual accounts to choose their own signature verification and switch to quantum-safe signatures voluntarily. The upcoming Hegotá hard fork, planned for the second half of 2026, embeds this further at the protocol level. The Ethereum Foundation has set structured milestones targeting completion of core post-quantum infrastructure by approximately 2029, with active interop devnets already running across multiple clients.

The contrast with bitcoin’s governance paralysis could not be more stark. Ethereum was designed, in ways bitcoin simply was not, to accommodate exactly this kind of foundational upgrade. That is not an accident. It is architecture.

The institutional calculus

For corporate treasurers and sovereign wealth managers, quantum risk is no longer a tail scenario to be footnoted and dismissed. Governments are already treating it as operational. U.S. federal agencies faced an April 2026 deadline to submit post-quantum cryptography transition plans under National Security Memorandum 10. The EU has set a 2030 quantum-resistance target for critical infrastructure. The G7 Cyber Expert Group published a coordinated financial sector road map in January 2026. This compliance architecture will, over time, extend to digital asset treasury holdings.

The question for any institution holding bitcoin is whether they are comfortable with an asset whose quantum-resistance road map is still in draft, whose governance moves at geological speed, and whose developer community is divided on whether urgency is even warranted.

The question for any institution considering Ethereum is whether they want the asset with a structured, transparent, and already in motion upgrade path.

Ethereum is the more adaptive, more capable, and more durable asset. I have put the balance sheet of a Nasdaq-listed company behind that conviction. The Google paper is what finally gives that conviction a single, undeniable, technically grounded answer to the hardest question in digital asset treasury strategy: which asset is built to last?

Ethereum is not a perfect asset. No asset is. But in the context of quantum risk, it is the asset whose architecture was built to survive what is coming. If Carter and Google are right, that distinction will matter enormously, and sooner than most people expect.

TLDR

- RippleX launched the XRP Ledger AI Starter Kit on June 10.

- The kit enables autonomous payments for AI agents on XRP Ledger.

- XRPL now supports the X402 protocol for web-based software payments.

- AI agents can pay for APIs, model inference, and digital services using XRP and RLUSD.

- Ripple-backed startup t54 helped integrate XRPL into X402.

Ripple Labs moved to link blockchain payments with the fast-growing AI economy through a new developer release. The company introduced the XRP Ledger AI Starter Kit on June 10 to support autonomous transactions. The rollout aligns with efforts to connect software agents with direct web payments.

XRP Ledger integrates X402 for autonomous web payments

RippleX launched the XRP Ledger AI Starter Kit to help developers build agent-powered applications. The first phase supports tools that enable autonomous payments on the XRP Ledger network. RippleX said the network design supports fast settlement and predictable costs.

“The XRP Ledger was built with many of these qualities in mind,” the announcement stated. It added that agentic payments now require speed and low transaction fees. The release supports X402, an open protocol that enables software to send payments without human approval.

Through support from t54, XRPL now operates as a supported chain on X402. Ripple backed t54 during a seed funding round to expand payment infrastructure. As a result, AI agents can use XRP and RLUSD for web-based transactions.

The system allows AI agents to pay for API calls and model inference services. It also enables payments for other digital services across web platforms. Developers can integrate these features into applications that require automated billing.

The starter kit also provides tooling for AI coding agents. A dedicated Model Context Protocol server supports queries to XRPL documentation. Clients, including Claude Code, Claude Desktop, and Cursor, can access the documentation directly.

XRP and RLUSD power Mastercard’s agent payment framework

The launch occurred on the same day Mastercard Inc. introduced Agent Pay for Machines. Mastercard designed the framework to support autonomous payments across digital services. More than 30 partners joined the initiative, including Ripple and t54.

RippleX senior vice president Markus Infanger outlined the role of XRPL and RLUSD. He said the network provides a settlement layer that clears in seconds. He added that the system offers predictable costs and built-in compliance.

“XRPL and RLUSD give Mastercard’s framework a settlement layer that clears in seconds,” Infanger said. He also referenced programmable compliance and a full audit trail. Mastercard listed Ripple as one of the core blockchain partners.

The framework supports high-volume and low-value transactions between software agents. It enables machine-to-machine settlements without manual approval. RippleX confirmed that XRP and RLUSD serve as payment rails within the system.

Ripple Labs continues to expand infrastructure through RippleX initiatives. The XRP Ledger AI Starter Kit now rolls out in stages across developer channels. The company released the tools on June 10, alongside Mastercard’s AP4M framework.

The past few weeks have been devastating for the cryptocurrency market, with Solana (SOL) being hit especially hard.

And while some analysts expect further losses in the near future, certain indicators signal that a much-needed recovery could be knocking on the door.

Buy Now?

Earlier this month, SOL collapsed to around $60, the lowest level since the end of 2023. As of this writing, it trades at roughly $63 (according to CoinGecko), which is a 33% monthly drop, while its market capitalization has fallen well below $40 billion.

According to Ali Martinez, though, the current bottom might present an excellent opportunity for investors to jump on the bandwagon. He revealed that the TD Sequential indicator has flashed a buy signal on SOL, meaning the price could soon head north to $77.

Another technical analysis tool that suggests a resurgence might be on the way is Solana’s Relative Strength Index. Its ratio (on a daily scale) recently dipped to approximately 15, its lowest mark ever. The index ranges from 0 to 100, and readings below 30 indicate that the asset is oversold and on the verge of a potential rebound. On the other hand, anything above 70 is a warning for a possible pullback ahead.

X user Henry supported the optimistic outlook. They noted SOL’s recent decline but argued that it looks “absolutely bullish” at the moment, predicting a W-shaped recovery beyond $88, assuming bulls reclaim $79.9. At the same time, the analyst warned that losing the major support level at $60 could be catastrophic.

More Pain Ahead?

Despite the positive signals, the bearish market conditions remain an obstacle, with some industry participants expecting a further price crash for SOL. X user cyclop envisioned a short-term plunge to the $30-$40 range, a level last visited in October 2023. Nevertheless, the analyst is optimistic for the long term, forecasting a pump to $300 in the next 1-2 years.

Lately, many investors have transferred their holdings from self-custody to centralized exchanges: a development that intensifies fears of an additional correction by increasing immediate selling pressure.

Another worrying factor is the waning interest from institutional investors. Over the past few days, outflows from spot SOL ETFs have exceeded inflows, indicating that pension funds, hedge funds, and other market players have reduced their exposure to the asset. This, in turn, has required the products’ issuers, including Bitwise, Fidelity, Grayscale, Invesco, and others, to sell real SOL to properly back the shares.

The post Solana (SOL) Bleeds Heavily, Yet Key Indicator Flashes a Buy Signal: Details appeared first on CryptoPotato.

Stand With Crypto UK, representing about 286,000 crypto enthusiasts and professionals, is pressing its network to challenge banks that block or restrict transfers to cryptocurrency exchanges. The campaign cites a UK Cryptoassets Business Council report indicating that 40% of crypto transactions are blocked or restricted by banks, with many restrictions applying to exchanges registered with the Financial Conduct Authority and not accounting for individual customer risk profiles.

The campaign outlines that one exchange recorded nearly £1 billion in declined transfers over a 12-month period, and 80% of surveyed platforms reported an uptick in blocked or restricted transfers. To push the issue forward, Stand With Crypto UK has launched a complaint-tool on its website that auto-generates letters challenging these restrictions; the organization says bank responses will help shape the next steps. Their tagline captures the spirit of the effort: “Your money. Your choice.”

Key takeaways

- According to the UK Cryptoassets Business Council, around 40% of crypto transactions are blocked or restricted by banks in the United Kingdom.

- One exchange reported nearly £1 billion in declined transfers over a year, illustrating the scale of friction for on-ramps and off-ramps.

- Approximately 80% of surveyed exchanges and platforms said they have seen higher rates of transfer blocking or restriction.

- The Stand With Crypto UK tool enables supporters to generate complaint letters to banks, with regulator-facing responses expected to influence the campaign’s next moves.

- Policy context in the UK centers on stabilizing and regulating stablecoins, with ongoing scrutiny of how such assets fit into the domestic financial system.

Bank access under scrutiny and the push for targeted risk controls

The campaign argues that blanket transfer bans hinder access to digital assets and stifle competition in a sector that is increasingly regulated. By urging members to file complaints, Stand With Crypto UK aims to convert anecdotal friction into formal regulatory and industry dialogue. In its public communication, the group emphasizes that many restrictions appear to apply broadly, regardless of a customer’s risk profile or the specific platform involved.

Industry voices calling for risk-based solutions

Industry observers have long warned that broad prohibitions can hamper legitimate crypto activity. In commentary to Cointelegraph, Mark Fairless, CEO of UK clearing bank ClearBank, underscored the need for a risk-based approach to crypto-related payments rather than sweeping blocks across the sector. “Interventions should be targeted and proportionate, as broad blocks risk undermining competition and the ability of regulated firms to operate effectively in the UK,” Fairless said.

Regulatory backdrop: UK stablecoins and the broader digital asset framework

The Stand With Crypto UK initiative arrives amid a wider regulatory effort to shape the UK’s stablecoin regime. In early May, a House of Lords committee examined proposed stablecoin regulations, questioning industry executives about bank-run risks, anti-money laundering controls, and the potential impact on traditional banking. Later in May, the Bank of England signaled a softer stance on proposed caps and reserve requirements as part of its review of the pound-denominated stablecoin framework. The objective is to foster a domestic stablecoin market while limiting risks to bank funding and financial stability; non-dollar stablecoins currently account for a small share of the global market. In June, the Lords committee warned that certain proposed stablecoin requirements could limit the viability of pound-denominated tokens and urged regulators to avoid measures that would hinder sector growth.

Beyond stablecoins, broader digital-asset initiatives are gaining momentum. In May, the central bank floated extending operating hours for settlement infrastructures to support tokenized markets, while the Financial Conduct Authority proposed on June 8 allowing some retail-focused investment funds to allocate up to 10% of their portfolios to crypto exchange-traded products.

What to watch next

As the UK weighs its stablecoin framework and the broader integration of digital assets into mainstream finance, the outcomes of this campaign could influence how banks calibrate risk and how regulators balance access with safety. The coming weeks will clarify whether targeted interventions replace blanket blocks and how exchanges and users adapt to evolving policy expectations.

Stand With Crypto UK is urging its 286,000 members to challenge British banks restricting transfers to cryptocurrency exchanges, arguing that blanket limits on transactions to regulated platforms are restricting access to digital assets.

The new campaign cites a report from the UK Cryptoassets Business Council that found 40% of crypto transactions are blocked or restricted by UK banks. The group argues that many of the restrictions apply to transfers involving exchanges registered with the country’s Financial Conduct Authority and do not account for individual customer risk profiles.

According to the report, one exchange recorded nearly 1 billion British pounds in declined transactions over a one-year period due to bank-side rejections, while 80% of surveyed platforms reported an increase in blocked or restricted transfers.

Stand With Crypto said members can submit complaints through a tool on its website that generates letters challenging transfer restrictions, with responses from banks expected to inform the campaign’s next steps.

“Your money. Your choice.” is the tag line of Stand With Crypto UK’s advocacy campaign.

Source: Stand With Crypto UK on X.com

Mark Fairless, CEO of UK clearing bank ClearBank, told Cointelegraph that banks should take a risk-based approach to crypto-related payments rather than imposing broad restrictions across the sector.

“Interventions should be targeted and proportionate, as broad blocks risk undermining competition and the ability of regulated firms to operate effectively in the UK,” Fairless said.

Related: EU proposes ban on 11 crypto platforms in Russia sanctions push

Stablecoin rules remain focus for UK policymakers

The campaign comes amid ongoing efforts by regulators to develop a UK-wide framework for stablecoins.

At the beginning of May, a House of Lords committee examined proposed stablecoin regulations, with lawmakers questioning industry executives on bank-run risks, anti-money laundering controls and the potential impact of stablecoins on traditional banking.

Later that month, the Bank of England said it was reconsidering proposed caps on stablecoin holdings and reserve requirements as it reviewed its framework for pound-denominated stablecoins.

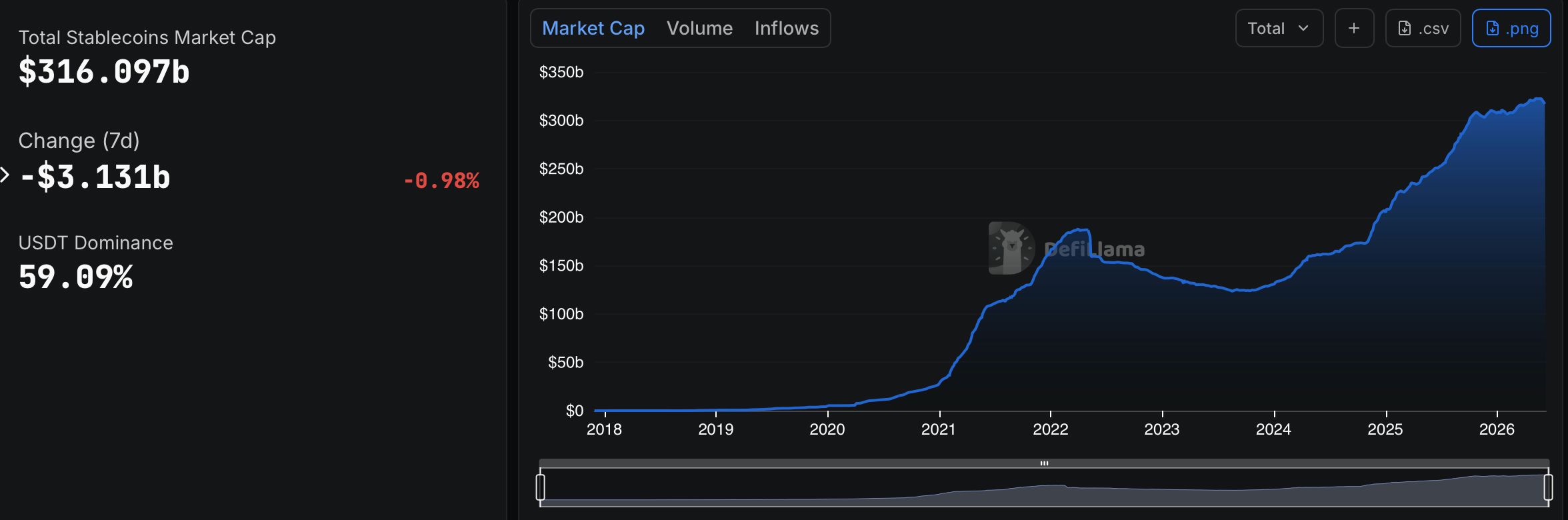

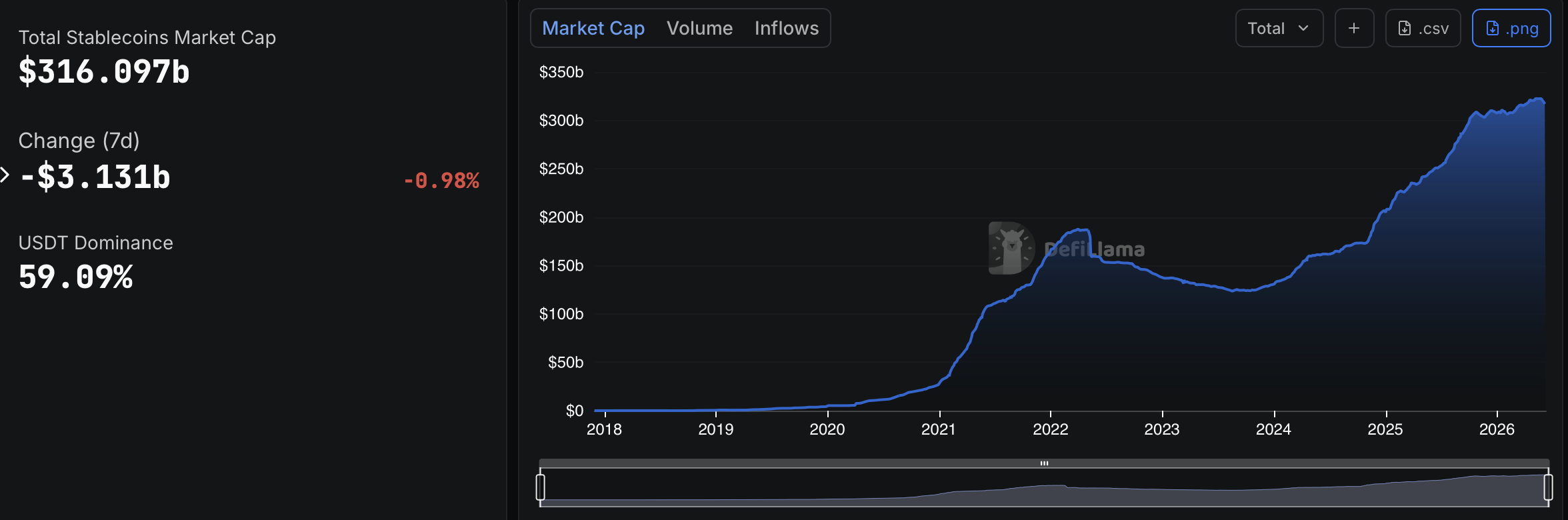

The review comes as regulators seek to support the growth of a domestic stablecoin market while limiting potential risks to bank funding and financial stability, with non-dollar stablecoins currently accounting for only a small fraction of the global market.

Total stablecoin market cap. Source: DefiLlama

In June, a House of Lords committee said certain proposed stablecoin requirements, including reserve and holding rules, could limit the viability of pound-denominated tokens. The committee urged regulators to avoid measures that could inhibit the growth of the sector while finalizing the country’s stablecoin framework.

Beyond stablecoins, regulators have also advanced broader digital asset initiatives. In May, the central bank proposed extending operating hours for the country’s settlement infrastructure to support tokenized markets, while the Financial Conduct Authority proposed on June 8 allowing certain retail-focused investment funds to allocate up to 10% of their portfolios to crypto exchange-traded products.

Magazine: Does ‘Paper Bitcoin’ mean there’s an unlimited supply of BTC?

Ripple on Wednesday released the XRPL AI Starter Kit, a developer toolkit for building AI-agent payment applications on the XRP Ledger, positioning XRPL and its RLUSD stablecoin as settlement infrastructure for autonomous software. The company published a blog post announcing the launch alongside… Read the full story at The Defiant

For months, Strategy (formerly MicroStrategy) founder Michael Saylor frequently reposted news about DeFi protocols using a variety of tokens and blockchains backed by Strategy’s STRC.

Now that their stablecoins and other yield farming tokens have wobbled, he wants everyone to know he was only sharing news, not endorsements.

STRC is one of Strategy’s stocks. It usually trades near $100 and pays a variable, 11.5% annualized dividend. Due to its high current rate of payouts, DeFi yield farmers find STRC appealing to tokenize through a variety of protocols, proprietary tokens, and blockchains.

Saylor took to social media today to clear up any misunderstanding about his frequent and prominent reposts about these non-bitcoin (BTC) tokens.

In his view, the free publicity he gave them was merely a series of non-endorsement “notifications.”

Saylor isn’t a BTC maximalist by the strictest of definitions. Indeed, despite Bitcoin branding and orange coloring across his company, website, and even attire, Saylor has spoken positively about alternative blockchains such as Ethereum and BNB Chain, so long as their utility improves adoption of BTC or Strategy’s securities like MSTR and STRC.

At altcoin conferences, he acknowledges the work of alternative blockchains in distributing proxies for BTC and Strategy exposure.

The timing is his disclaimer wasn’t subtle. In recent days, STRC-backed stablecoins like apxUSD and sUSDat started trading well below their prior $1 targets.

Within the last week, the STRC-backed sUSDat on Ethereum traded 9.5% below its $1 target, and apxUSD similarly traded below $0.91.

Both mirrored a crash in STRC, a stock that Strategy tries to keep trading near $100 despite it hitting $90.38 on Friday.

DeFi protocols Saylor ‘notified’ everyone about

In addition to social media reposts, Saylor named DeFi builders himself on stage at the Bitcoin 2026 conference, presenting three projects using STRC powered by a variety of altcoins: Apyx, Saturn, and Hermetica.

For example, Apyx uses DeFi protocols to transform STRC exposure into a type of synthetic dollar, apxUSD.

Saturn does roughly the same through its sUSDat token while another protocol, Pendle, slices STRC-backed tokens into ostensibly stable tokens as well as yield tokens like apyUSD.

Traders then loop their assets to borrow and re-borrow, manufacturing leveraged yields atop STRC that can reach higher than 38%.

Saylor didn’t merely tolerate this machinery, he repeatedly amplified these DeFi projects through reposting “notifications.”

For example, when STRC slipped, Saylor reposted Apyx declaring, “We just bought the $STRC dip.”

Saylor reposted Saturn touting its increasing STRC exposure.

He reposted Pendle celebrating roughly half a billion dollars in STRC-linked deposits.

Although Saylor claims he never endorsed them, the protocols themselves never hid their devotion.

Indeed, Saturn’s account describes its team as “Disciples of @Saylor” while Strata, another builder in the convoluted stack of STRC-backed DeFi, used Saylor’s own terminology, “The Bitcoin Credit flywheel is spinning.”

Read more: Strive’s $50M STRC bet is already underwater

The most prominent bitcoin buyer sells

During the last week of May, Strategy sold 32 BTC, its first sale since 2022. The price of BTC immediately crated.

Saylor had spent years swearing he had no intention to sell Strategy’s BTC. Nonetheless, after the world’s most prominent buyer turned into a seller, BTC dropped from above $73,000 to near $62,000 within the month of June alone.

Unfortunately, the typically stable STRC fell with it, and the DeFi tokens that used STRC as backing inherited that volatility. A synthetic dollar is no more stable than the asset backing it.

The DeFi protocols Saylor broadcast to millions of his followers on X and other media appearances are declining in value along with STRC, so now he insists his reposts were only ever harmless notifications.

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

Bitcoin Price Drops Follow BOJ Rate Hikes: Is Another Crash Developing?

Doctor Who Is Officially Dead, With No Regeneration In Sight

New Broadway Cast of Cabaret (1998), Alan Cumming, Cabaret Ensemble (1998) – Money (Official Audio)

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Evereve – Corporette.com

-

Crypto World5 days ago

Crypto World5 days agoJensen Huang Approves Samsung, SK Hynix, and Micron for NVIDIA (NVDA) HBM4 Memory Supply

-

Crypto World3 days ago

Crypto World3 days agoAnatomy of the June crypto crash: Fed, Iran, Saylor

-

Entertainment4 days ago

Entertainment4 days agoThe Best Mystery Series of All Time Is Surging on Streaming 30 Years After It Ended

-

NewsBeat3 days ago

NewsBeat3 days agoAlexander Zverev wins the French Open to finally earn a 1st Grand Slam title

-

Tech5 days ago

Tech5 days agoSuspicious Polyfill login prompts pop up on Toshiba, Muji websites

-

Crypto World4 days ago

Senator Cynthia Lummis Calls CLARITY Act the Most Consequential Financial Legislation of This Generation

-

Tech5 days ago

Tech5 days agoMicrosoft launches MXC, an OS-level sandbox for AI agents, with OpenAI and Nvidia already on board

-

Tech3 days ago

Tech3 days agoMicrosoft unveils seven homegrown AI models in new bid for ‘long term self-sufficiency’

-

Business5 days ago

Business5 days ago(VIDEO) Justin Bieber Delivers Surprise Happy Birthday Serenade to Diners at Los Angeles Mexican Restaurant

-

Business4 days ago

Business4 days agoThe Pain Points Taking a Fragile Tech Rally Down a Notch

-

Crypto World2 days ago

Crypto World2 days agoEli Lilly (LLY) Stock Surges 4% Following Breakthrough Sleep Apnea Trial Results

-

Crypto World5 days ago

LBank Surpasses 25 Million Users Worldwide as AFA Partnership Continues to Drive Global Growth

-

Tech5 days ago

Tech5 days agoVon der Leyen’s AI envoy pick draws conflict-of-interest fire

-

Crypto World3 days ago

Crypto World3 days agoTrump’s AI Ownership Plan Could Benefit Anthropic at OpenAI’s Expense

-

Tech5 days ago

Tech5 days agoMeta steals a tactic from Tesla and builds data centers in tents

-

Sports1 day ago

Sports1 day agoBangladesh beat Australia after 20 years in ODIs, register only their second win over six-time world champions | Cricket News

-

Business3 days ago

Business3 days agoHigh Stakes for Wembanyama as New York Pushes for 3-0 Lead

-

Tech5 days ago

Tech5 days agoHackers now exploit SolarWinds Serv-U flaw to crash servers

-

Tech3 days ago

Tech3 days agoNotion restores access to Anthropic after service disruption

You must be logged in to post a comment Login