Crypto World

Chinese billionaire Miles Guo gets 30 years in $1B crypto fraud case

Self-exiled Chinese billionaire Miles Guo has been sentenced to 30 years in a U.S. prison after being convicted in a fraud scheme that prosecutors said stole more than $1 billion from investors through multiple ventures, including cryptocurrency.

Summary

- Miles Guo was sentenced to 30 years in a U.S. prison and ordered to forfeit $889 million after his fraud conviction.

- Prosecutors said the scheme raised more than $1 billion from investors through multiple ventures, including the Himalaya Exchange and Himalaya Coin.

- The sentencing comes as crypto related financial crime continues to face tighter enforcement in both the United States and China.

According to multiple media reports, U.S. District Judge Analisa Torres handed down the sentence on Monday and ordered Guo, also known as Guo Wengui, to forfeit $889 million in restitution.

The sentencing follows a July 2024 jury verdict that found Guo guilty on nine fraud and conspiracy charges after prosecutors accused him of raising money from hundreds of thousands of online followers through false investment promises tied to businesses under his control.

Crypto scheme formed part of fraud case

Federal prosecutors had alleged that Guo attracted investors by presenting himself as a critic of the Chinese Communist Party after fleeing China more than a decade ago, while using that reputation to promote fraudulent investment opportunities.

According to the U.S. Department of Justice, one of those ventures was the Himalaya Exchange, a cryptocurrency ecosystem that collected more than $262 million from victims. The department said Guo later spent investor funds on luxury assets, including a mansion and high end vehicles.

Earlier court filings from the DOJ said Guo orchestrated a scheme that defrauded thousands of investors of more than $1 billion after his arrest in March 2023.

At the sentencing hearing, the Associated Press reported that Guo told the court he came to the United States “to destroy the CCP.” AP also reported that Judge Torres said Guo had preyed on supporters seeking democracy in China and had continued to deny causing financial harm.

SEC case remains part of wider enforcement action

Separate from the criminal prosecution, the U.S. Securities and Exchange Commission charged Guo and his financial adviser, William Je, in March 2023 over an alleged fraud that raised hundreds of millions of dollars through an unregistered crypto asset known as H Coin, or Himalaya Coin.

According to the SEC complaint, Guo falsely claimed the token was backed by gold and assured investors they would be reimbursed for any losses. The regulator also accused Guo and Je of diverting investor funds to finance luxury purchases, including a mansion and a Ferrari, while seeking permanent injunctions, civil penalties and the recovery of alleged illegal gains.

The SEC and DOJ announced their actions on the same day in March 2023, with the Justice Department filing a 12-count indictment that included securities fraud, wire fraud, investment fraud and money laundering charges against Guo. William Je was also charged with obstruction of justice, while authorities said they seized about $634 million held across 21 bank accounts linked to the investigation.

Guo is also known for his association with former Donald Trump strategist Steve Bannon. In 2020, the pair announced the New Federal State of China initiative, describing it as an effort to overthrow the Chinese government.

Elsewhere, Chinese authorities have also stepped up enforcement against cryptocurrency-related financial crimes.

China’s Supreme People’s Procuratorate said on June 25 that prosecutors had charged more than 1,200 people for drug related money laundering cases between January 2025 and May 2026, including schemes involving cryptocurrencies.

The disclosure came as China announced a death sentence for a convicted drug trafficker found to have laundered more than 48 million yuan, or about $7 million, through cryptocurrency as part of a cross-border narcotics operation.

A routine filing crowned Goldman Sachs the largest institutional holder of XRP ETFs, and the market read it as Wall Street validating XRP. The next filing showed Goldman had quietly exited the entire position and rotated into crypto stocks instead. Here is what the round trip actually reveals about XRP, Ripple, and how Wall Street is really playing crypto.

Summary

- Goldman Sachs was crowned Wall Street’s biggest XRP whale after a December 31 filing showed a $153.8 million position across four XRP ETFs, roughly 73% of the top 30 institutions’ combined exposure.

- The market read it as a powerful institutional endorsement of XRP, arriving while retail sentiment was mired in extreme fear, the classic “smart money accumulating” narrative.

- A 13F filing is a rear-view mirror, and the catch was timing: the snapshot predated a roughly 40% drop in XRP, leaving open whether Goldman held through the decline.

- The next filing answered it: Goldman had completely exited its XRP and Solana ETF positions and rotated into crypto equities such as Circle, Galaxy Digital, and Coinbase, boosting some stakes by as much as 249%.

- The episode is a lesson in reading delayed filings and a window into how Wall Street is really playing crypto, often preferring the companies and infrastructure over the tokens, which echoes the core question hanging over XRP.

In March 2026, a routine regulatory filing handed XRP holders the kind of headline they had waited years for: Goldman Sachs, the most prestigious investment bank on Wall Street, had been revealed as the single largest institutional holder of XRP exchange-traded funds in the U.S., with a position worth $153.8 million spread across four separate funds. For a token whose entire bull thesis rests on institutional adoption finally arriving, this looked like the proof. The largest bank in the world had quietly loaded up on XRP while ordinary investors were selling in fear, the very picture of smart money moving ahead of the crowd. The crypto community celebrated, analysts framed it as validation that XRP had cleared Wall Street’s due-diligence bar, and the story spread as evidence that the institutional era for XRP had begun.

It was, for a moment, exactly the catalyst the narrative needed. Then the next filing arrived, and it told the opposite story. When Goldman disclosed its following quarter, the $153.8 million XRP position had vanished entirely. The bank had exited its XRP ETF holdings completely, exited its Solana ETF holdings completely, trimmed its Bitcoin and Ethereum exposure, and redirected capital into crypto-related equities instead, increasing stakes in companies like Circle, Galaxy Digital, and Coinbase by as much as 249%.

The biggest XRP whale on Wall Street had, by the time the market crowned it, already swum away. This article tells the full story of that round trip and, more importantly, what it reveals. It covers the filing that created the whale, why the market loved it, why filings are a rear-view mirror, the exit that followed, where Goldman actually moved its money, the retail reality behind the XRP ETF, and what the whole episode means for Ripple and XRP. The analysis is information, not advice, and the lesson is both practical and structural: delayed filings can mislead, and Wall Street may prefer crypto infrastructure over the tokens themselves.

The filing that crowned a whale

Start with what was actually disclosed, because the precision of it is part of why the market took it so seriously. In a quarterly 13F filing, the mandatory disclosure large institutions must make of their equity holdings, Goldman Sachs reported a position of $153.8 million spread across four spot XRP ETFs as of December 31, 2025. The breakdown, first surfaced by the journalist Eleanor Terrett and analyzed by Bloomberg Intelligence analyst James Seyffart, showed roughly $40 million in Bitwise’s XRP ETF, $38.5 million in the Franklin XRP Trust, $38 million in Grayscale’s XRP fund, and $36 million in the 21Shares product. That made Goldman the single largest disclosed institutional holder of XRP ETF shares in the country.

To put its dominance in context, Seyffart’s analysis found that the top 30 institutional holders collectively controlled just over $211 million in XRP ETF exposure, and Goldman alone accounted for roughly 73% of that total. It was not a marginal position; it dwarfed the rest of the institutional field. Two details made the disclosure especially compelling to observers. First, it was Goldman’s first disclosed crypto allocation beyond Bitcoin and Ethereum, which meant the bank was extending its digital-asset exposure into an altcoin for the first time, a meaningful step for an institution of its stature.

Second, the position was deliberately constructed rather than concentrated: Goldman spread its bet across four different issuers in roughly equal slices, the kind of diversified allocation that signals a considered, risk-managed decision rather than an opportunistic punt. When the largest investment bank in the world shows up in the filings of four separate XRP funds with a carefully distributed nine-figure position, it suggests the trade was intentional and institutional, not incidental. The regulatory clarity that followed the conclusion of Ripple’s legal battle, combined with the ETF approvals it enabled, had given an institution like Goldman a familiar, regulated wrapper through which to hold XRP exposure, and Goldman appeared to have used it decisively. On its face, this was the institutional validation the XRP thesis had always promised.

Why the market loved the story

It is worth dwelling on why this filing landed so powerfully, because the appeal reveals what the XRP community has been hungry for. The core of the XRP bull case has long been that the token’s real catalyst is institutional adoption: that once banks, asset managers, and other large players begin holding and using XRP, demand will arrive at a scale that retail speculation never could, and the price will follow. For years, that adoption was promised but rarely visible in a form retail holders could point to. A 13F filing showing the world’s most prestigious investment bank as the single largest institutional holder of XRP ETF shares was exactly the visible, concrete proof the narrative had been missing.

It was not a vague partnership announcement or a settlement that proved the plumbing worked; it was Goldman Sachs, by name, in the filings, with a nine-figure position. The timing amplified the effect. The disclosure landed during a period when retail sentiment across crypto was mired in extreme fear, with the broad market stuck in a pessimistic stretch lasting weeks. Against that backdrop, the revelation fit one of the most seductive patterns in investing: the contrarian “smart money accumulating while the crowd panics” story.

The interpretation almost wrote itself. While ordinary investors were selling XRP in fear, Wall Street’s most powerful bank was quietly buying, which implied that the people with the best information and the deepest resources saw value precisely where retail saw only losses. That framing is emotionally powerful because it offers reassurance to holders sitting on losses, recasting their pain as the entry point that institutions were exploiting. Commentators leaned into it, describing a wave of institutional “super fans” piling into XRP ETFs and treating Goldman’s position as the leading edge of a broader Wall Street embrace. The story was compelling, well-sourced, and emotionally satisfying; its only flaw was that it was already out of date.

The catch nobody priced in

Here is the structural problem that the celebration overlooked, and it is fundamental to how 13F filings work. A 13F is a rear-view mirror. It discloses what an institution held as of the end of a calendar quarter, but it is filed weeks later, which means that by the time the public sees the position, it reflects where the institution stood at the snapshot date, not where it stands when the filing becomes news. Goldman’s $153.8 million XRP position was a snapshot as of December 31, 2025.

The filing that revealed it became public in February and drove headlines into March, but the holding it described was already two to three months stale by the time the market reacted to it. Goldman could have trimmed, added to, or exited the position entirely in the intervening period, and the filing would say nothing about it. The market was celebrating a photograph of the past as if it were a live feed. That gap mattered enormously in this case because of what happened to XRP in the interim.

The snapshot captured Goldman’s position at the end of a quarter when XRP was trading materially higher; the token had peaked near $2.40 in early January 2026. Over the following weeks, XRP fell hard, declining more than 40% through the first quarter as the broader market weakened, the same drawdown that prompted Standard Chartered to cut its year-end XRP target from $8 to $2.80 in mid-February. So the celebrated Goldman position was struck before a major decline, and the obvious question, which the more careful analysts raised at the time, was whether Goldman had held through that drawdown or exited as XRP fell. The bullish crowd treated the position as current conviction; the careful reading treated it as an open question.

The next filing settled the matter, and it did not settle it in the bulls’ favor. That is why stale filing data needs to be read differently from live flow data. A 13F can prove that an institution held something at a point in time, but it cannot prove present conviction. In crypto, where a token can move 40% before the filing becomes public, that difference is not academic.

Then Goldman sold everything

When Goldman’s first-quarter 2026 13F filing arrived in May, it revealed that the bank had completely exited its XRP ETF position. The $153.8 million spread across four funds, the holding that had crowned Goldman the biggest XRP whale on Wall Street, was simply gone. And it was not only XRP: Goldman had also exited its Solana ETF holdings entirely, erasing positions it had previously held across multiple Solana products. The bank trimmed its Bitcoin and Ethereum ETF exposure as well, reducing those holdings rather than eliminating them.

In other words, the institution that the XRP community had celebrated as a marquee believer had, by the next available snapshot, removed XRP from its portfolio completely, alongside a broader pullback from altcoin ETF exposure. The whale had not merely trimmed; it had fully unwound the position that made the headlines. The implication reframes the entire earlier narrative. The story that spread in February and March, of Wall Street’s biggest bank accumulating XRP while retail panicked, was describing a position that Goldman was in the process of exiting, or had already decided to exit, even as the public celebrated it.

The “smart money accumulating” interpretation was, in hindsight, exactly backward: the smart money was on its way out, and the delayed nature of the filing meant retail was cheering an entry at almost the moment of the exit. This does not prove that Goldman timed anything perfectly or that its move was a verdict on XRP’s long-term prospects; a single bank’s quarterly allocation decisions reflect many factors, including risk management, mandate changes, and portfolio rebalancing, not necessarily a strong directional view. But it does demolish the specific bullish read that had been built on the earlier filing. The institutional validation that the XRP thesis leaned on turned out, in this instance, to be an institution heading for the door.

For a holder who had taken comfort in the Goldman headline, the follow-up filing was a cold lesson in how stale the comfort had been. The better takeaway is not that every institutional filing is meaningless, but that timing and persistence matter. A real institutional adoption story has to survive more than one delayed snapshot. It has to show up quarter after quarter, across more than one institution, and through drawdowns.

Where the money actually went

The most revealing part of the episode is not that Goldman sold XRP, but what it bought instead, because the rotation tells a story about how Wall Street is really approaching crypto. In the same first-quarter filing that showed Goldman exiting XRP and Solana ETFs, the bank substantially increased its equity stakes in crypto-related companies, boosting positions in firms such as Circle, the stablecoin issuer, Galaxy Digital, the digital-asset financial-services firm, and Coinbase, the exchange, by as much as 249%. So Goldman did not exit crypto. It rotated within crypto, moving out of direct token exposure through altcoin ETFs and into the equities of the companies that operate the crypto economy’s infrastructure.

This is a meaningful signal about institutional strategy, and arguably a more durable insight than the original whale headline. Buying the companies instead of the tokens reflects a particular thesis: that the reliable way to profit from crypto’s growth is to own the businesses that monetize the activity, the picks-and-shovels of the industry, instead of betting on the price of any individual asset. A stablecoin issuer earns on reserves and transaction volume, an exchange earns on trading fees, and a digital-asset financial-services firm earns across market conditions, whereas an altcoin ETF simply tracks a volatile token price. For a risk-managed institution, the equities can look like a steadier way to gain crypto exposure than a single token.

The rotation suggests that, at least for this quarter and this bank, Wall Street’s conviction was stronger in the crypto economy’s infrastructure than in the XRP token itself. That distinction, between the businesses that run on crypto and the tokens crypto runs on, is precisely the distinction that has haunted XRP, and it is why this episode matters far beyond a single bank’s trade. Goldman’s money went to the companies, not the coin. For XRP holders, that distinction is the uncomfortable heart of the story.

The retail reality behind the XRP ETF

The Goldman round trip also punctures a broader assumption about XRP’s ETFs, and the data here is clarifying. Despite the institutional framing that the Goldman headline encouraged, the XRP ETF complex is, in fact, overwhelmingly retail-driven. According to Ripple’s own data, around 84% of U.S. XRP ETF assets are held by retail investors, a striking figure that stands in sharp contrast to Solana ETF products, where institutional participation runs closer to half. So even at the moment Goldman was being celebrated as the face of institutional XRP adoption, the reality was that the ETFs were funded mostly by ordinary investors, with institutions like Goldman representing a smaller, and as it turned out, transient slice.

The institutional adoption story was at a far earlier and thinner stage than the marquee headline suggested. The flow data fills in the picture. XRP ETFs launched in late 2025 and accumulated assets quickly, crossing $1 billion in cumulative inflows by mid-December and surpassing $1.5 billion by early March 2026, a pace Ripple described as among the fastest institutional adoption curves in regulated ETF history. But that momentum did not hold.

By the middle of 2026, total XRP ETF assets under management had fallen back to roughly $1 billion, well below the peak, as inflows slowed dramatically and the token’s price decline eroded the value of the holdings. The retail base has shown genuine conviction, sustaining inflow streaks even through falling prices, which is a real and somewhat encouraging signal of grassroots demand. But conviction from retail is a different foundation than sustained institutional accumulation, and the Goldman episode laid bare how much of the institutional story was projection. The ETFs proved that regulated XRP access works and that demand exists, but the demand is mostly retail, the institutional participation is early and uneven, and the single biggest institutional holder turned out to be a seller.

That is a more sober picture than the one the original headline painted, and a more accurate one. It also makes the broader ETF flow picture more important than any single famous holder. ETF demand can matter for XRP, but it matters most when flows are persistent, diversified, and not merely the result of retail conviction in a falling market. Until institutional ownership broadens and holds through volatility, the ETF story remains real but incomplete.

What it means for Ripple and XRP

So what does the whole episode actually mean for Ripple and the token? The sobering read is that it exposes how thin the institutional-validation narrative was, and it reinforces the deepest concern about XRP. The pattern that has defined XRP through this period is that Ripple keeps winning, genuinely, in the institutional arena, while the token struggles to capture the value, because the market distinguishes between adoption of Ripple’s infrastructure and demand for XRP itself. Goldman’s rotation maps onto that distinction with uncomfortable precision: the bank moved out of the XRP token and into the equities of crypto companies, choosing the businesses over the coin.

If sophisticated institutions, when they want crypto exposure, increasingly prefer to own Circle, Coinbase, and Galaxy over holding XRP, that is the value-accrual problem expressed through a portfolio: Wall Street betting on the crypto economy without betting on the token. For a holder, the lesson is to treat institutional-adoption headlines with the same skepticism the Goldman story now demands, and to ask not whether institutions are touching the ecosystem but whether they are holding the asset. That is the value-accrual question in depth, and it keeps resurfacing across Ripple’s story. Ripple can win business while XRP still has to prove that those wins create direct token demand.

The fairer, more balanced read does not let the bears claim too much, though. One bank’s quarterly decision is not a referendum on XRP, and there are real counterpoints. Goldman exited Solana too, so the move looks more like a broad altcoin-ETF pullback amid a risk-off market than a targeted verdict on XRP specifically. The bank could re-enter; 13F filings capture a moment, and the next one could show a different posture.

The retail demand underpinning the XRP ETFs has been persistent, holding through the drawdown, which suggests a genuine base of conviction that does not depend on any single institution. And the structural supports for XRP remain in place: regulated ETF access exists, the legal status is clearer than for almost any major token, and the CLARITY Act, if it passes, could codify XRP’s commodity status into federal law and unlock the larger, more durable institutional buyers, pensions and asset managers, that cannot allocate to an asset until its status is settled in statute. That is the catalyst that could unlock real institutions, and it remains the most important distinction between today’s retail-heavy ETF demand and the institutional allocation XRP bulls still expect. In that reading, Goldman was simply early and tactical, not a leading indicator, and the real institutional money is still waiting on a catalyst that has not yet arrived.

Both readings are legitimate. What the episode settles is only that the institutional era for XRP had not, in fact, begun when the headline said it had. The Goldman headline was a sign of interest, not proof of durable adoption. The sellout was a warning about overreading a single filing, not proof that XRP has no institutional future.

What to watch from here

The productive way to carry this lesson forward is to track the signals that would actually indicate institutional conviction in XRP, instead of reacting to stale snapshots. The first is the sequence of upcoming 13F filings, watched not for a single marquee name but for whether institutional XRP ETF holdings broaden and persist across multiple players and multiple quarters, which is what real adoption would look like, as opposed to one bank’s transient position. A durable institutional base would show up as sustained, distributed holdings that survive drawdowns, not a one-quarter cameo. Whether Goldman itself re-enters in a later filing is worth noting too, though it should be read as one data point instead of a verdict.

The second signal is the trajectory of XRP ETF flows and assets: whether the retail-driven inflows that have sustained the funds continue, and whether institutional participation rises from its currently thin share toward the higher levels seen in some other products. The third, and most consequential, is the CLARITY Act, because the structural argument is that the largest institutions are not absent by choice but constrained by the lack of statutory clarity, and that legislation codifying XRP’s status is the catalyst that would unlock them. If that money arrives, it would be visible in exactly the filings this episode taught us to read carefully. And the fourth is whether Wall Street’s apparent preference for crypto equities over tokens, the Circle-and-Coinbase rotation Goldman exemplified, becomes a durable pattern.

If institutions keep choosing the companies over the coins, that is the value-accrual question answering itself in real time. The Goldman round trip was a single episode, but it handed XRP holders a durable framework: celebrate adoption when it is current, distributed, and sustained, not when it is a stale snapshot of a position already being unwound. Read that way, the whale that swam away taught a more useful lesson than the whale that was never quite there. For price-focused readers, where the token stands now is the next practical question, because ETF flows, regulation, and institutional ownership only matter if they eventually show up in the chart.

Frequently asked questions

Was Goldman Sachs really the biggest XRP holder?

It was the largest disclosed institutional holder of XRP ETF shares, based on its 13F filing for the quarter ending December 31, 2025, which showed a $153.8 million position spread across four spot XRP ETFs, roughly 73% of the top 30 institutions’ combined exposure. That made it the single biggest institutional name in the XRP ETF field at that snapshot. Importantly, this was a position in XRP ETFs, not direct token holdings, and it described where Goldman stood at year-end 2025, not necessarily where it stood when the filing became public news in early 2026. The next filing revealed Goldman had since exited the position entirely.

Did Goldman Sachs sell its XRP?

Yes. Goldman’s subsequent 13F filing, covering the first quarter of 2026 and disclosed in May, showed that the bank had completely exited its XRP ETF position; the entire $153.8 million holding was gone. It also exited its Solana ETF holdings entirely and trimmed its Bitcoin and Ethereum ETF exposure. So by the time the market was celebrating Goldman as the biggest XRP whale, based on the earlier year-end snapshot, the bank had already unwound the position. This is a direct consequence of how 13F filings work: they disclose holdings weeks after the snapshot date, so a celebrated position can already be sold by the time it makes headlines.

Why did Goldman exit XRP?

The filing does not state reasons, and a bank’s quarterly allocation decisions reflect many factors, including risk management, mandate changes, and rebalancing, not necessarily a directional verdict on XRP. Two contextual points stand out. First, Goldman exited Solana ETFs too and trimmed Bitcoin and Ethereum, suggesting a broad pullback from altcoin and crypto-ETF exposure during a risk-off, falling market instead of a targeted call against XRP. Second, and more tellingly, Goldman rotated into crypto-related equities instead, increasing stakes in companies like Circle, Galaxy Digital, and Coinbase by as much as 249%, which suggests a strategic preference for owning the businesses of the crypto economy over holding volatile tokens directly.

What did Goldman buy instead of XRP?

Goldman rotated into the equities of crypto-related companies. In the same filing that showed it exiting XRP and Solana ETFs, the bank substantially increased its stakes in firms such as Circle, the stablecoin issuer, Galaxy Digital, a digital-asset financial-services firm, and Coinbase, the exchange, raising some positions by as much as 249%. The logic this implies is a picks-and-shovels thesis: profiting from crypto’s growth by owning the businesses that earn revenue from the activity, issuers, exchanges, and financial-services firms, instead of betting on the price of any single token. It is a more risk-managed way to gain crypto exposure, and it reflects a preference for the infrastructure of crypto over the assets themselves.

Does Goldman’s exit mean XRP is a bad investment?

Not on its own, and the episode should not be over-read. One bank’s quarterly decision is not a referendum on XRP, especially since Goldman pulled back from altcoin ETFs broadly during a risk-off market and could re-enter later. The retail demand underpinning XRP ETFs has been persistent, holding through the drawdown, and the structural supports, regulated access, clearer legal status, and the potential of the CLARITY Act to unlock larger institutional buyers, remain in place. What the episode does establish is that the institutional-adoption narrative built on the original Goldman headline was premature, and that holders should treat such headlines cautiously. It is a caution about reading stale filings, not a verdict on the asset.

What does this mean for Ripple?

It reinforces the central tension in the Ripple and XRP story: the distinction between adoption of Ripple’s ecosystem and demand for the XRP token. Goldman rotating from XRP into crypto equities like Circle and Coinbase mirrors, at the portfolio level, the broader pattern in which value tends to accrue to companies and infrastructure instead of to the token. If institutions seeking crypto exposure increasingly prefer to own the businesses over the coins, that is the value-accrual question expressed through Wall Street’s choices. The counterweight is that the larger, more durable institutional money may still be waiting on statutory clarity from the CLARITY Act, which, if it passes, could change the calculus. For now, the episode is a reminder that institutional validation for XRP is thinner and more provisional than headlines suggest.

This article is information, not financial or investment advice. Details of Goldman Sachs’s filings, holdings, XRP ETF figures, and price levels reflect reporting available as of June 30, 2026, are point-in-time, and can change. 13F filings are delayed snapshots and may not reflect current positions. Cryptocurrency is volatile and you can lose money. Nothing here is a recommendation about XRP or any asset. Do your own research and consult a qualified financial professional before making any decision.

The White House invited law enforcement groups opposing the Digital Asset Market Clarity Act to a Monday meeting to resolve objections to Section 604, the provision drawn from the Blockchain Regulatory Certainty Act (BRCA) that shields software developers from money-transmitter classification.

Patrick Witt, the White House’s lead crypto adviser, is driving the engagement, but the bill still requires 60 Senate votes to pass, and roughly four weeks of floor time remain before the August recess.

Senate Majority Leader John Thune is reportedly prepared to bring the CLARITY Act to the floor in the coming weeks, regardless of whether Democrats are ready, according to Punchbowl News.

Banking Committee Chairman Tim Scott posted on X Monday that the Senate “should vote on crypto market structure legislation in July.” The urgency is real. The political math is harder.

The bill passed the House 294–134 on July 17, 2025, and cleared the Senate Banking Committee 15–9 on May 14, 2026. Those are comfortable margins in their respective chambers. The Senate floor is a different problem entirely.

Discover: The Best Token Presales

Section 604: The Provision That Stopped the Clock

Section 604 of the CLARITY Act, the BRCA provision, is where the legislative fight is concentrated. It would prevent software developers who do not exercise ultimate control over their tools from being classified as money transmitters under Bank Secrecy Act rules, a protection the crypto industry treats as foundational for continued DeFi development in the United States.

The National Sheriffs Association sent a May letter to Senate Banking Committee leaders stating: “No good reason supports giving mixers, tumblers, and DeFi a blanket exemption.

While some software developers are not engaged in money transmitting or other activity that should subject them to BSA regulation, plenty of others are.” The group was invited to a prior two-day White House session in June, but did not attend, which is why Monday’s targeted meeting exists.

The law enforcement argument is not that the BRCA protection is wrong in principle; it is that the current language is too broad. Investigators working on sanctions evasion and mixer-facilitated crime say the exemption, as written, blurs the enforcement boundary around developers whose tools are functionally indistinguishable from financial intermediaries.

That is not a fringe position; it is shared across multiple law enforcement organizations that attended the June White House sessions.

Patrick Witt’s counter-argument is that the bill adds new prosecutorial tools and that the current regulatory vacuum is itself the enforcement problem. “We’re putting real regulatory constraints on businesses and actors that currently live in a state of uncertainty,” Witt said at an industry event earlier this month.

To skeptical law enforcement officials, he argued they “should be the biggest cheerleaders for this bill, because this is really what is missing.” Whether that framing moves the National Sheriffs Association off its stated position is what Monday’s meeting is designed to test.

Three More Problems Beyond Section 604

The BRCA dispute is the most visible obstacle, but three additional issues remain unresolved. First, regarding the Commodity Futures Trading Commission staffing question, the bill’s provisions expand the CFTC’s jurisdiction over crypto market structure, and bringing the agency to full operational strength remains part of active negotiations.

Second, an ethics provision that would bar senior government officials, including the president, from holding personal crypto interests. Multiple lawmakers have stated explicitly that they will not vote for the bill without it, including the only Democrats who voted for the bill during the Senate Banking Committee markup.

That second point is the structural bind. The Democrats, whose votes the White House needs, are conditioning their support on a provision the White House may resist. Senators Catherine Cortez Masto and Mark Warner have both signaled that the ethics provision is a threshold requirement, not a negotiating chip. That is not resolved; it is deferred.

Third, Trump’s broader legislative posture adds a layer of uncertainty. His refusal to sign a major housing affordability bill, demanding a voter-identification bill first, has already disrupted one congressional timeline.

TD Cowen policy analyst Jaret Seiberg said Monday he expects the housing bill to become law through the constitutional ten-day automatic-passage window, projecting a Friday, July 10, effective date. Whether Trump applies the same resistance to the CLARITY Act is not yet clear, but the precedent is live.

Don’t Miss Out on Our $1,000 USDT Airdrop on ByBit

The post CLARITY Act Faces Senate Clock as Law Enforcement Pushes Back on DeFi Exemption appeared first on Cryptonews.

Ripple (XRP) is holding around $1.04–$1.06 with negligible 24-hour movement, while Stellar (XLM) is showing more immediate energy at $0.18 with a 3.91% gain on the day, a divergence that’s drawing relative-value traders back to the classic XRP vs XLM debate.

But how’s it looking in 2026? Well, both assets staged breakout attempts from multi-week consolidations, but neither has confirmed continuation. The question now isn’t whether momentum exists; it’s whether either coin has enough structural support to avoid a fade back into range.

Coinpedia described the recent move as “a massive upswing as bullish momentum revives after weeks of consolidation,” framing it as a technical breakout attempt rather than a confirmed trend shift.

XRP faces a significant resistance band at $1.30–$1.37, while XLM’s immediate test sits at $0.22–$0.23, a level that, if reclaimed cleanly, opens a path toward $0.26 and then $0.30. The XRPXLM rate sits at 7.59, up 2.15%, suggesting XRP is still holding relative value dominance in the pair even as XLM shows stronger short-term momentum.

What happens at these inflection points over the next few sessions will likely define whether traders are looking at a sustained move or a textbook bull trap in a headline-sensitive market.

Can XRP Break $1.30 or Is XLM Setting Up the Cleaner Trade?

XRP’s technical picture is a short-term correction inside a broader breakout attempt. TradingView’s live feed places XRP price at approximately $1.058, with the near-term support zone identified at $1.08–$1.10, the floor that needs to hold for any bull case to stay intact.

A confirmed bounce off that zone with volume would put $1.30 back in play, and some price models targeting far higher levels by end of 2026 assume that band gets cleared without significant rejection.

Bull case: XRP reclaims $1.10, consolidates briefly, presses $1.30–$1.37 on volume. A clean break above that band puts $1.45 and $1.60 on the board.

Base case: price grinds between $1.04 and $1.20 for another week, building a tighter base before any directional move.

Bear case (invalidation): a close below $1.04 with follow-through selling re-opens the sub-$1.00 range.

XLM’s setup is arguably cleaner in percentage terms. Starting from $0.18 with immediate resistance at $0.22–$0.23, a 22–28% move to the first key target is on the table if the breakout holds.

The Stellar network’s cross-border utility case gives it a macro narrative that can attract institutional flow when risk appetite returns, though at this stage, the chart is doing most of the talking.

Watch $0.18 as the line in the sand; a failure to hold it on any pullback would shift the read to “consolidation-continues” rather than “breakout-confirmed.” (Both setups have merit; XLM’s is just more binary right now.)

Can LiquidChain be The Better Option?

XRP at $1.06 and XLM at $0.18 are already reflecting significant market cap, even a clean breakout to $1.45 or $0.26, respectively, represents incremental gains from here.

Traders who caught these moves earlier are sitting on compressed upside relative to their entry risk. That reality is where early-stage infrastructure plays start making a different kind of sense.

LiquidChain ($LIQUID) is a Layer 3 infrastructure project positioning as a cross-chain liquidity layer, its stated USP is fusing Bitcoin, Ethereum, and Solana liquidity into a single execution environment, allowing developers to deploy once and access all three ecosystems.

According to the project’s presale data, $LIQUID is currently priced at $0.01475 with $880,132.41 raised to date. Key features include a Unified Liquidity Layer, Single-Step Execution, Verifiable Settlement, and a Deploy-Once Architecture, infrastructure-layer components that address a real fragmentation problem across the three largest ecosystems by liquidity depth.

The post XRP and XLM Are Both Testing Breakouts at the Same Time: Which One Actually Holds? appeared first on Cryptonews.

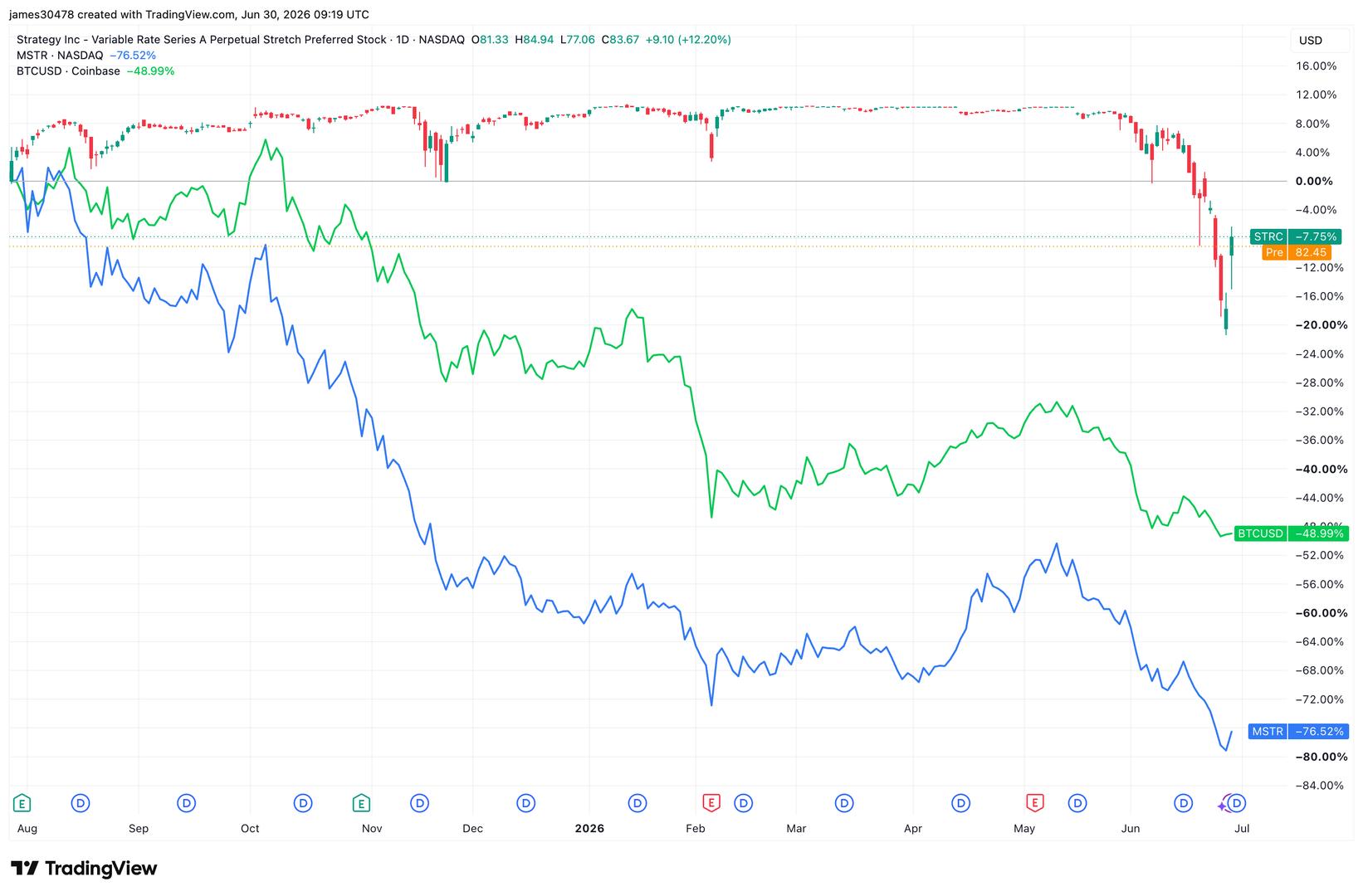

Strategy (MSTR) stock is set to end the month around 41% lower, its worst monthly performance since 2022, with one trading day remaining.

MSTR is on course to mark its eleventh negative month out of the last twelve. Shares traded as low as nearly $80 on Friday before rallying more than 12% on Monday following the company’s announcement of its new capital management framework.

The stock reached an all time high of $540 per share in November 2024, before a sustained decline began the following July, coinciding with the debut of its perpetual preferred security, STRC.

STRC sits above the common stock in the capital structure and so offered investors a lower volatility alternative to owning MSTR shares. At the same time, the need for continued issuance of common stock to help fund STRC’s dividend obligations increased dilution concerns, contributing to the stock’s prolonged underperformance.

Since STRC’s IPO, bitcoin has fallen by almost 50%, while MSTR has declined by roughly 77%.

Meanwhile, bitcoin is on track to post its third consecutive negative quarter and has fallen 20% in June.

Key Takeaways

- On June 29, Bank of America identified IBM as a quantum computing leader, highlighting its manufacturing capabilities and qubit advancement metrics.

- Shares increased 2.3% on Tuesday, opening at $277.83, within a 52-week trading band of $212.34 to $332.46.

- Approximately 30% of IBM’s consulting backlog now consists of generative AI projects, with total AI-related business expanding from $7.5 billion to $12.5 billion across three quarters.

- Simmons Bank expanded its IBM position by 16.7% during Q1, currently holding 15,660 shares valued at approximately $3.8 million.

- Analysts assign IBM a “Moderate Buy” consensus rating with a mean price target near $306.94, suggesting additional upside potential.

IBM shares advanced 2.3% during Tuesday’s trading session, reaching an opening price of $277.83. The upward movement reflects growing investor confidence driven by positive developments in both quantum computing capabilities and artificial intelligence adoption.

International Business Machines Corporation, IBM

On June 29, Bank of America designated IBM as a leading force in quantum computing development. The analysis highlighted IBM’s vertically integrated manufacturing infrastructure as a competitive advantage. Bank of America’s evaluation methodology includes tracking programming qubits, operational efficiency, and throughput metrics to benchmark performance against industry competitors.

IBM’s recent quantum computing showcase reportedly demonstrated superior research documentation compared to rivals. This recognition follows another significant achievement earlier this month when IBM unveiled what it describes as the industry’s first chip utilizing sub-1 nanometer technology.

Enterprise AI Implementation Drives Revenue Momentum

Unlike companies focused on developing consumer-facing AI models, IBM concentrates on enterprise AI integration—helping corporations deploy artificial intelligence within their established infrastructure, data environments, and regulatory frameworks.

This specialized strategy is producing measurable financial results. During Q1 2026, IBM delivered $15.9 billion in total revenue, representing 9% year-over-year growth. The software division posted 11% revenue expansion, while recurring software revenue reached $24.6 billion.

The company generated $2.2 billion in free cash flow during the quarter—its strongest first-quarter performance in ten years. Generative AI initiatives now represent roughly 30% of IBM’s complete consulting pipeline.

IBM’s cumulative AI business portfolio expanded from $7.5 billion to $12.5 billion within a three-quarter timeframe. Enterprise clients are transitioning from exploratory discussions to formal contract commitments.

The stock currently trades at a forward price-to-earnings ratio of approximately 26.41x. This represents nearly a 20% valuation discount relative to the sector median of 33.02x.

Institutional Ownership Continues Expanding

According to recent SEC disclosures, Simmons Bank increased its IBM holdings by 16.7% during the first quarter. The institution acquired 2,243 additional shares, elevating its total position to 15,660 shares valued at $3.8 million.

Numerous other institutional players executed comparable transactions. Family CFO Inc, Basepoint Wealth, Portus Wealth Advisors, Joseph Group Capital Management, and Cornerstone Financial Management all established new IBM positions during recent reporting periods.

Institutional investors and hedge funds collectively control 58.96% of IBM’s outstanding shares. This represents substantial institutional concentration for an organization of IBM’s market capitalization.

The company maintains its commitment to shareholder returns through consistent dividend payments. IBM increased its quarterly dividend to $1.69 per share, distributed on June 10th. This translates to an annualized dividend of $6.76 and a yield of 2.4%, extending the company’s dividend increase streak to 31 consecutive years.

IBM released quarterly results on April 22nd, reporting earnings of $1.91 per share versus the consensus forecast of $1.81. Revenue of $15.92 billion similarly exceeded analyst expectations of $15.60 billion.

The company achieved a return on equity of 37.23% alongside a net margin of 15.61%. Analysts project full-year 2026 earnings per share of 12.39 for IBM.

Multiple analyst firms have recently updated their positions on the stock. HSBC elevated IBM from “reduce” to “hold” in April. KeyCorp shifted to “sector weight” in June, while Wolfe Research adjusted its rating to “peer perform.”

Royal Bank of Canada maintained an “outperform” rating, and Wall Street Zen upgraded IBM from “sell” to “hold.” The current analyst breakdown includes one Strong Buy rating, seventeen Buy ratings, and nine Hold ratings.

The overall consensus stands at “Moderate Buy,” with a mean price target of $306.94. This target suggests meaningful appreciation potential from Tuesday’s opening price of $277.83.

The U.K.’s Financial Conduct Authority (FCA) reduced the proposed capital requirements for stablecoin issuers as it set out its formal guidance for cryptocurrency regulations.

The financial services regulator cut the amount of financial backing that needs to be set aside to 1% of the total value of the stablecoins they issue. It was previously 2%.

The change “makes the prudential framework more proportionate for larger issuers while maintaining the robustness of the overall regime,” the FCA said in a new framework document published Tuesday.

The proposed requirement is lower than the 2% equivalent stipulation under the European Union’s Markets in Crypto Assets (MiCA) regulation.

The FCA’s aim is to simplify key elements of the regime to make it more workable in practice, it said in a statement.

The loosening follows the Bank of England’s (BOE) reversal of its proposal to limit the value of stablecoins an individual can hold, abandoning plans to impose a 20,000-pound ($26,500) cap.

Major financial markets around the world have been setting out formal regulatory regimes for the oversight of crypto assets in recent years, with stablecoins emerging as one the most significant areas of interest.

The FCA also aims to simplify the framework for crypto exchanges. Under the new rules, they will need to set aside 40% of their trading capital to cover potential losses and apply a 40% potential loss to the value of their collateral when lending or trading with other parties.

Key Takeaways

- Apple stock closed at $281.74 on Monday following news of a significant data breach.

- Confidential iPhone 18 Pro documentation, including supplier data and testing images, appeared on the dark web.

- The security incident originated from Tata Electronics, a crucial Apple manufacturing partner in India.

- Ransomware collective World Leaks has claimed the attack, though verification remains pending.

- Analysts maintain a Moderate Buy stance with an average target price around $324.40.

Shares of Apple (AAPL) experienced a decline on Monday, settling at $281.74, following revelations that confidential materials related to the upcoming iPhone 18 Pro had been published on the dark web. The compromised materials allegedly contain detailed component specifications, supplier identification, and imagery from physical durability testing performed at a Tata Electronics facility in India.

Tata Electronics represents a cornerstone of Apple’s diversification strategy beyond Chinese manufacturing. The firm functions as both a component provider and final assembly operator, positioning it as essential to Apple’s expanding production footprint in India.

The cybercriminal organization World Leaks has claimed responsibility for the security breach. This collective previously orchestrated another attack on Tata that resulted in more than 200,000 files being compromised, some containing references to Tesla, Taiwan Semiconductor Manufacturing, and Qualcomm.

Reuters examined a minimum of six newly surfaced documents that detail precise iPhone 18 Pro components alongside their corresponding suppliers. The documentation encompasses semiconductor chips for the primary logic board, as well as power cell and imaging system components.

Apple guards its supplier network information with extreme secrecy. The corporation avoids disclosing vendor-part relationships publicly, meaning this breach provides rivals and counterfeit operations with unprecedented insight into Apple’s production ecosystem.

The leaked imagery depicts iPhones undergoing physical stress testing, with timestamps indicating early 2026. The photographs show a grey, rectangular device featuring three rear-mounted cameras and Apple’s signature branding, although Reuters could not authenticate the specific model designation.

Both Apple and Tata have declined to issue public statements regarding the security incident. Reuters noted it was unable to independently authenticate the leaked materials.

Implications for the Apple-Tata Manufacturing Alliance

Tata’s significance within Apple’s production network has expanded rapidly. According to Counterpoint Research projections, India is expected to manufacture 26% of global iPhone units in 2026, representing a substantial increase from merely 6% four years earlier.

This manufacturing shift aligns with Prime Minister Narendra Modi’s strategic initiative to establish India as a dominant force in electronics production. A cybersecurity incident of this magnitude may influence Apple’s confidence in its partnership with Tata moving forward.

Tata has implemented immediate restrictions on employee access to critical systems during its internal investigation. The company has additionally engaged external cybersecurity specialists to conduct a comprehensive forensic examination of the breach.

Unfortunate Timing for Apple’s Product Cycle

The data breach emerges at a particularly sensitive moment as Apple prepares for the iPhone 18 Pro and Pro Max debut, anticipated in September. Market observers are already monitoring potential price increases driven by escalating costs for memory and storage components.

Apple implemented price adjustments for iPad and MacBook products last week citing identical component cost pressures. A comparable pricing strategy for iPhones would align with current market dynamics affecting component procurement this year.

In parallel developments, Apple has accelerated its security update deployment schedule as artificial intelligence technologies enable threat actors to identify software weaknesses more efficiently. Instead of bundling security patches with major iOS releases, Apple now distributes critical fixes independently on an expedited timeline.

The company has stated that currently available evidence suggests the recently patched vulnerabilities were not actively exploited. While this security initiative operates separately from the Tata incident, it demonstrates Apple’s broader commitment to enhanced security responsiveness.

Wall Street analysts have maintained their outlook on Apple. The stock carries a Moderate Buy consensus derived from 30 analyst evaluations published within the last three months, breaking down to 18 Buy ratings, 11 Hold recommendations, and one Sell rating. The consensus price target stands at $324.40, representing approximately 15% upside from present trading levels.

Singapore court has awarded more than $3 million in damages to 40 investors after finding Terraform Labs and co-founder Do Kwon liable for fraudulent misrepresentations tied to the 2022 TerraUSD collapse.

Summary

- Singapore court awarded more than $3 million to 40 investors after finding Terraform Labs and Do Kwon liable for fraudulent UST claims.

- The ruling followed earlier court findings and used a revised UST valuation that increased compensation for eligible claimants.

- Terraform’s legal troubles continue as bankruptcy proceedings and other lawsuits linked to the 2022 Terra collapse remain ongoing.

According to the June 29 judgment from the Singapore International Commercial Court (SICC), the award concludes the second tranche of a representative fraud action brought by 275 investors who sought compensation for losses suffered during the collapse of the TerraUSD (UST) algorithmic stablecoin in May 2022.

The latest ruling follows the court’s first-tranche decision in 2025, which found that Terraform Labs Pte Ltd and Do Kwon made actionable fraudulent representations. It also incorporates guidance from the Singapore Court of Appeal’s March 2026 decision, which revised the method for calculating damages by adopting a higher cut off value of about $0.60485 per UST.

Court finds investors relied on false UST claims

In its ruling, the SICC found that Terraform and Kwon falsely represented UST as a stablecoin capable of reliably maintaining its one dollar peg through its algorithm, reserves, and LUNA-based arbitrage mechanism. According to the court, those statements appeared on Terraform’s website, white papers, and public communications despite being false or made with reckless disregard for their accuracy.

The court held that some investors relied on those claims when buying or continuing to hold UST, leading to financial losses after the stablecoin lost its peg. Damages were therefore calculated on a reliance basis for holdings up to May 12, 2022, while losses after that date were treated as too speculative for compensation.

The Court of Appeal’s earlier decision to increase the UST cut off valuation resulted in higher compensation for eligible claimants than under the original damages model.

Bankruptcy cases continue as legal pressure grows

The Singapore judgment adds to Terraform’s expanding legal challenges after the company entered Chapter 11 bankruptcy proceedings in the United States. Claims reconciliation for creditors is ongoing, and any further recoveries for investors are expected to depend largely on distributions from the bankruptcy estate, alongside the outcome of other pending litigation.

Earlier this year, Terraform’s court-appointed bankruptcy administrator also sued market maker Jane Street, alleging the firm used confidential information and manipulated markets to profit during the Terra ecosystem’s collapse. Jane Street denied the allegations, calling the lawsuit an attempt to extract money and maintaining that Terra investor losses resulted from fraud committed by Terraform’s own management.

Do Kwon, who was sentenced to 15 years in prison after pleading guilty to fraud charges in the United States, also continues to face criminal proceedings in South Korea alongside other legal actions connected to the collapse.

According to the SICC ruling and related court proceedings, the case adds to a series of legal actions examining how crypto projects communicated risks to investors before major failures. The court’s findings may also influence future representative actions involving digital asset projects, while regulators in several jurisdictions continue to push for stronger disclosure standards for stablecoin and decentralised finance products.

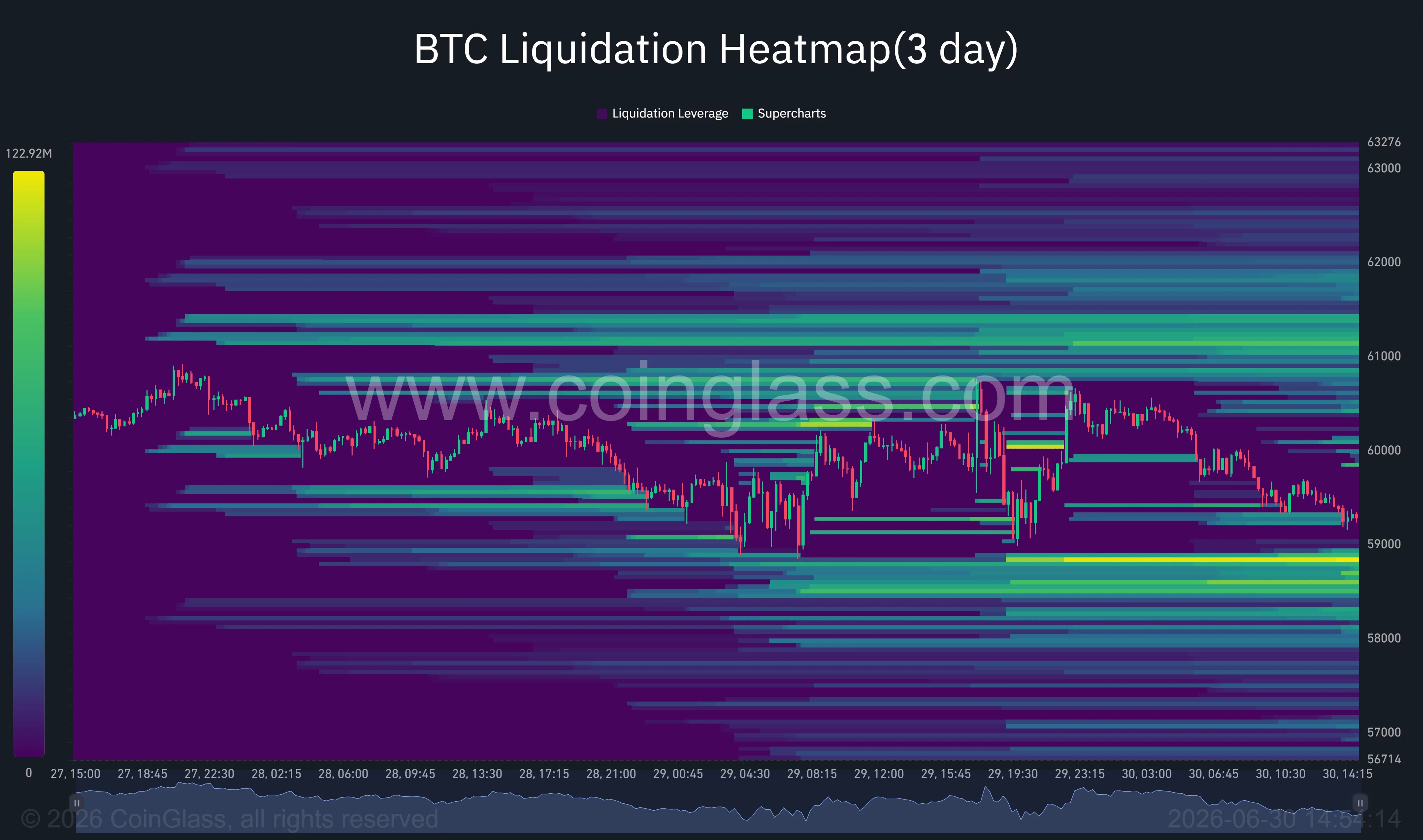

Bitcoin price has slipped back below $60,000 after another failed breakout attempt, as weak stablecoin inflows have reinforced concerns over a lack of fresh buying demand.

Summary

- Bitcoin price has failed to hold above $60,000 since June 25 as weak stablecoin inflows limit buying demand.

- Record spot Bitcoin ETF outflows and Strategy’s potential BTC sales continue to weigh on market liquidity.

- Analysts see $58,000-$59,000 as key support, with a break lower increasing the risk of another selloff.

According to data from crypto.news, Bitcoin (BTC) traded near $59,300 on June 30 after briefly reclaiming the psychological $60,000 level before slipping back below it, extending a series of failed breakout attempts since falling under the mark on June 25.

Market sentiment remained fragile as traders weighed shrinking liquidity, record spot ETF outflows, and a challenging macro backdrop. According to CryptoQuant analyst Sunny Mom, the latest on-chain data suggests the market lacks the fresh capital typically needed to support a sustained breakout.

“New money has stopped coming in,” Sunny Mom wrote, adding that “any bounce that does appear is more likely a short-term technical reaction than the beginning of a trend reversal.”

The analyst based that view on the 30-day stablecoin market capitalization growth rate. USDC issuance has turned negative, while Ethereum-based USDT growth has also weakened.

Stablecoins often serve as the primary source of buying power for crypto markets, making slower issuance a sign that fewer investors are converting cash into digital assets.

Institutional selling and macro headwinds continue to cap Bitcoin

Fresh institutional data has reinforced the liquidity concerns. U.S. spot Bitcoin exchange-traded funds recorded nearly $1.79 billion in net outflows during the final full week of June, the largest weekly withdrawal this year. Because fund managers must sell Bitcoin to meet investor redemptions, those outflows have removed one of the market’s strongest sources of spot demand.

As reported earlier by crypto.news, Strategy recently unveiled its Digital Credit Capital Framework, authorizing up to $1.25 billion in potential Bitcoin sales to meet interest and dividend obligations. The announcement arrived alongside quarter-end portfolio rebalancing by institutional investors, adding another source of supply after months in which the company had consistently accumulated Bitcoin.

Economic conditions have further reduced appetite for risk assets. A stronger-than-expected U.S. Core PCE inflation reading weakened expectations for Federal Reserve rate cuts, while higher Treasury yields encouraged investors to rotate toward fixed-income assets.

At the same time, Brent crude slipped toward $73 per barrel as attention shifted to renewed U.S.-Iran negotiations in Doha after an interim agreement reduced the immediate risk of disruptions through the Strait of Hormuz. Still, geopolitical uncertainty has remained part of the market backdrop.

Technical structure keeps downside risks in focus

Bitcoin’s 1-day USDT chart continues to favor sellers after price failed to reclaim the descending trendline drawn from the May highs. The cryptocurrency is trading just above the key support zone around $58,169, which coincides with the 100% Fibonacci retracement of the recent decline. A decisive move below that level could expose the mid-$50,000 region.

Momentum indicators have yet to confirm a durable reversal. The daily RSI has slipped to around 32, placing Bitcoin close to oversold territory, while the MACD remains below the zero line despite flattening after the recent selloff. Those readings suggest selling pressure has slowed but buyers have not yet regained control.

Derivatives positioning also points to heightened volatility around current prices. CoinGlass liquidation data shows one of the largest downside liquidity clusters between $58,800 and $59,000, while another concentration of leveraged positions sits near $61,000 to $61,500. Either zone could attract price if momentum accelerates.

According to analyst Ted Pillows, Bitcoin’s immediate outlook depends on whether support between $58,000 and $59,000 can hold.

“The key level for Bitcoin here is $58,000-$59,000 which should hold for any bounceback.”

A successful defense of that area could trigger a relief rally toward the low-$60,000 range and potentially $61,500, where liquidation pressure increases.

However, if Bitcoin fails to hold support, it would strengthen the bearish case, particularly if stablecoin issuance remains weak, ETF redemptions continue, and macro conditions keep institutional capital away from risk assets.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

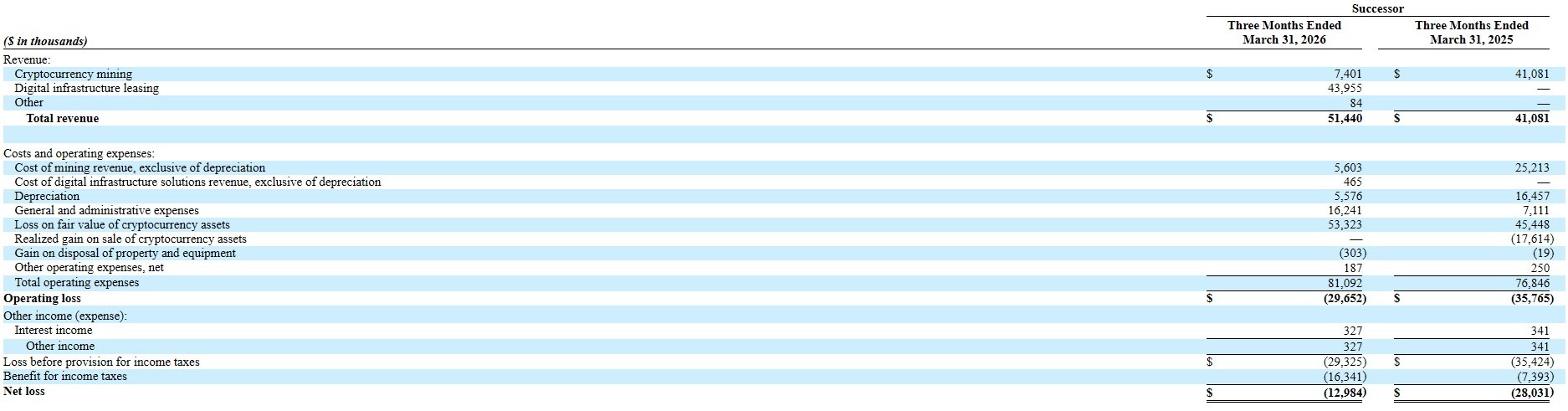

Bitcoin miner-turned-AI infrastructure company Ionic Digital has filed for a Nasdaq direct listing that could give former Celsius creditors a public market for shares they received through the bankrupt lender’s restructuring.

Registered stockholders may sell up to 10.8 million Class A shares under the proposed IOND ticker, according to a registration statement filed with the US Securities and Exchange Commission on Monday.

Ionic was formed in 2024 to acquire Celsius Mining’s assets through the bankrupt lender’s restructuring. In the filing, Ionic said it started repositioning itself in 2025 from a pure-play Bitcoin miner into a broader digital infrastructure company serving artificial intelligence and high-performance computing (HPC) workloads.

The proposed direct Nasdaq listing will not raise new capital for Ionic, according to the filing. Instead, the listing will establish a public market for existing shareholders, including former Celsius creditors who received Ionic shares through the bankruptcy plan.

Ionic repurposes Bitcoin mining site for AI

Ionic’s AI pivot revolves around its 234-megawatt Ward County property in Texas, originally developed for Bitcoin mining. In October 2025, the company leased the site to AI infrastructure provider Nscale under a 126-month agreement representing nearly $2 billion in contracted revenue.

Ionic said the agreement could be expanded to include an additional 89 MW if the company secures the required capacity and approvals. This potentially increases its contracted revenue to about $2.6 billion, according to the company.

Related: Celsius’ Mashinsky gets permanent trading ban in CFTC settlement

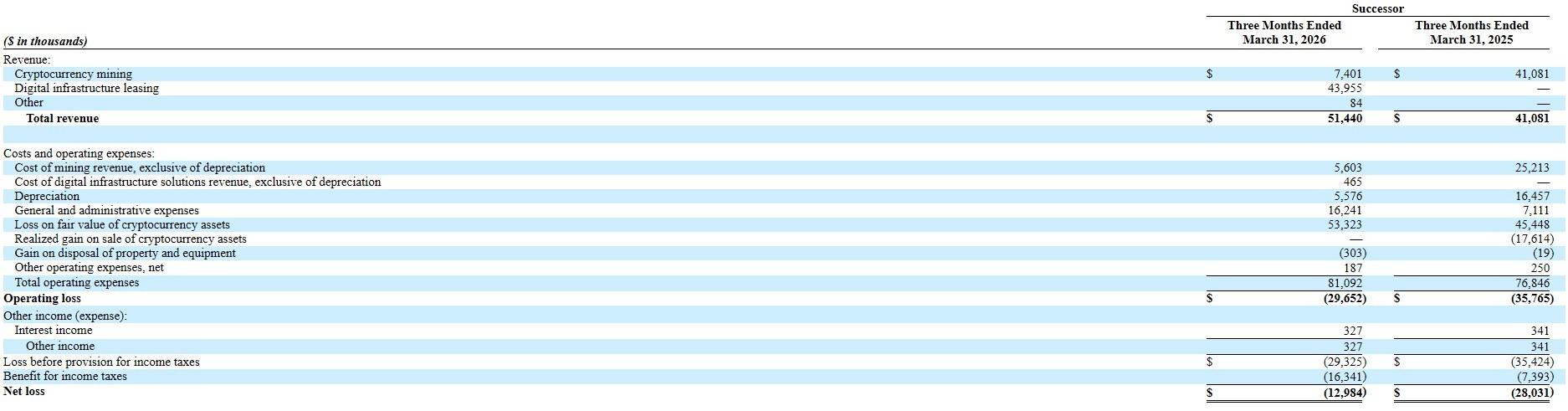

The shift has started to appear in Ionic’s financial results. The company recorded $44 million in digital infrastructure leasing revenue in the first quarter of 2026, while Bitcoin mining revenue fell 82% year over year to $7.4 million as it repurposed Ward County and reduced the number of active miners, according to its SEC filing on Monday.

Ionic Digital’s reported revenue. Source: SEC filing

The filing follows Ionic’s completion of a $400 million equity private placement on Friday. Ionic said the proceeds would be used for general corporate purposes, while its CEO, Andy Stewart, said the funds would support the continued development of its digital infrastructure assets.

Magazine: Bitcoin decouples from tech stocks, Ether eyes ‘selling wave’: Market Moves

Pictured: Ukrainian oligarch’s wife ‘whose legs were blown off in bomb blast’ as couple and their son are placed under guard by French special forces in hospital

Aussie shares fall as gold drops to eight-month low

Goldman Sachs was the biggest XRP whale, then it sold

-

Sports7 days ago

Sports7 days agoTwo goals and an assist by sheer aura: Cristiano Ronaldo just entered the World Cup chat

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: Staud – Corporette.com

-

Politics4 days ago

Politics4 days agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Politics4 days ago

Politics4 days agoPotential 2028er World Cup attendee leaderboard

-

News Videos2 days ago

News Videos2 days agoMAJOR BITCOIN & MARKET UPDATE!!!! (MUST WATCH ASAP!!!)

-

Business4 days ago

Business4 days agoAsia stock markets slide as tech shares slump

-

Tech5 days ago

Tech5 days agoA Look At A Gaggle Of Transputer Boards

-

Crypto World6 days ago

Crypto World6 days agoSecuritize Wraps Roubini's SEC-Registered ETF as Dubai VARA Digital Security

-

Crypto World6 days ago

Bitcoin (BTC) Dips Below $62K, Ethereum (ETH) Plunges 6% Daily: Market Watch

-

Crypto World5 days ago

Crypto World5 days agoDell (DELL) Shares Tumble Over 5% Following Analyst Downgrade to Hold

-

Crypto World3 days ago

Crypto World3 days agoCoinbase, Circle Deepen Crypto Stock Losses Despite Resilient S&P 500

-

Business6 days ago

Entergy settles forward sale agreements, raises $672 million in cash proceeds

-

Crypto World3 days ago

Crypto World3 days agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Sports4 days ago

Sports4 days agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Tech2 days ago

Tech2 days agoBluekit phishing kit adopts browser-in-the-middle for login theft

-

Crypto World4 days ago

Crypto World4 days agoBitcoin Sparks $600M Hourly Liquidations With $65,000 Set To Become Resistance

-

Tech3 days ago

Tech3 days agoRussian hackers now target Signal backup recovery keys

-

Crypto World4 days ago

Crypto World4 days agoHyperliquid Named on Singapore MAS Investor Alert Register

-

Crypto World4 days ago

Crypto World4 days agoRTX holders must register wallets before token distribution begins

-

Crypto World5 days ago

Crypto World5 days agoRipple and SBI launch RLUSD in Japan after JFSA approval

You must be logged in to post a comment Login