Crypto World

Did L2s break Ethereum’s ultrasound money?

Ethereum’s best marketing line was that using it destroyed it, that every transaction burned ETH and shrank the supply. Then the network solved its scaling problem, activity fled to layer 2s, and the burn collapsed. The scaling worked. The scarcity did not survive it.

Summary

- Ethereum’s “ultrasound money” thesis held that EIP-1559 fee burning would outpace new issuance, making ETH deflationary and a superior store of value to Bitcoin.

- It worked briefly after the 2022 Merge. Then the March 2024 Dencun upgrade moved activity to layer-2 rollups paying near-zero fees, and the daily burn collapsed from thousands of ETH to as low as 50 to 70.

- ETH has since been mildly inflationary, with net supply growth around 0.2% to 0.8% annually depending on the period, reversing the deflation the thesis promised.

- The December 2025 Fusaka upgrade added EIP-7918, a blob fee floor designed to restore a minimum burn. Fidelity modeled it would have added roughly $78.6 million in burn across 93% of days since 2024.

- The deeper tension is unresolved: a cheap, scaled Ethereum burns less than a congested, expensive one, so the network’s success as infrastructure works against its scarcity as an asset.

For about eighteen months, Ethereum had the best story in crypto, and the story was a paradox: the more people used the network, the rarer its token became. Every transaction burned a little ETH, and when the network was busy enough, it burned more than it created. Supply went down. The community called it ultrasound money, a deliberate jab at Bitcoin’s “sound money,” complete with a bat emoji and a movement.

For a while, the data backed it up. Then Ethereum did the thing it had promised to do for years, which was to scale, and scaling broke the story. Activity moved to layer-2 networks that pay almost nothing to the base chain, the burn collapsed, and ETH quietly went inflationary again. This is the story of how Ethereum’s greatest technical success dismantled its best economic narrative, and whether a December upgrade can put the pieces back.

What ultrasound money actually meant

The mechanism is worth getting exactly right, because the whole debate turns on it.

In August 2021, Ethereum activated EIP-1559, which changed how transaction fees work. Instead of paying miners directly, every transaction now pays a base fee that is burned, permanently removed from circulation. The busier the network, the higher the base fee, and the more ETH destroyed. On its own, that is just a fee-burning mechanism. It became a monetary thesis when Ethereum switched from proof-of-work to proof-of-stake in the September 2022 Merge, which cut new ETH issuance by roughly 90%, because the network no longer had to pay energy-intensive miners.

Put the two together, and you get the ultrasound thesis. Issuance dropped to a trickle after the Merge. Burning continued with every transaction. If burning exceeded issuance, total ETH supply would shrink over time, making the asset deflationary. And a deflationary asset with growing demand should, in theory, appreciate. Ethereum would become harder money than Bitcoin, whose supply still grows, hence “ultrasound.” The tracking site ultrasound.money existed to display exactly this: supply ticking down, day by day.

For a stretch after the Merge, it happened. Supply fell back toward and below the level it sat at during the Merge itself. Burns outpaced issuance. The narrative was not hype; it was, for that window, an accurate description of the data. That is what made it powerful, and what made its reversal so awkward.

How scaling broke it

The break came from Ethereum solving its most famous problem, and the irony is total.

Ethereum’s scaling strategy is to push transactions off the expensive base layer and onto layer-2 rollups, networks like Arbitrum, Optimism, and Base that process transactions cheaply and then post compressed data back to Ethereum for security. The base layer becomes a settlement and data-availability layer; the rollups handle the actual activity. This is the roadmap Ethereum has pursued for years, and it works.

The March 2024 Dencun upgrade was the pivotal moment. It introduced EIP-4844, “blob” transactions, a separate and far cheaper data channel for rollups to post their data. Costs for layer 2s dropped by a factor of 10 to 100. Activity that used to happen on mainnet, paying mainnet fees and burning mainnet ETH, moved to rollups paying blob fees that were, in practice, close to zero because blob space was massively oversupplied relative to demand.

The effect on the burn was immediate and severe. Before Dencun, Ethereum burned thousands of ETH per day during busy periods. After Dencun, daily burn dropped to as low as 50 to 70 ETH. The base layer had lost its primary fee source. With issuance running around 1,700 ETH per day and burn collapsing well below that, the equation flipped: Ethereum began creating more ETH than it destroyed. By various measures across 2025 and into 2026, net annual inflation ran somewhere between roughly 0.2% and 0.8%, depending on the window. ETH supply crossed back above its Merge-era level. The deflation was over.

The mechanism that made ultrasound money true, EIP-1559 burning at scale, had not been removed. It had been bypassed. The activity simply moved to a layer where the burn does not happen in any meaningful amount. Ethereum scaled successfully and, in doing so, severed the link between usage and scarcity that the entire thesis depended on.

The bull case: it still works, just differently

The response from Ethereum’s defenders is not denial. It is reframing, and parts of it are genuinely strong.

The first point is that elastic scarcity is the actual feature, not permanent deflation. Ethereum was never designed to deflate forever at a fixed rate. It was designed to burn in proportion to demand, which means it becomes deflationary when the network is busy and mildly inflationary when it is quiet. During periods of high mainnet activity, above roughly 16 gwei average gas, burn still exceeds issuance, and ETH still goes net deflationary, temporarily. The mechanism works exactly as designed; it is just that a scaled network spends more time in the quiet regime. In this reading, ultrasound money was always conditional, and the condition is demand, not a promise.

The second point is that issuance is still radically lower than before. Even mildly inflationary, Ethereum issues roughly 90% less ETH than it did under proof-of-work. Compared to Bitcoin, which currently inflates at around 0.8% annually on a fixed schedule, Ethereum’s roughly 0.2% net inflation in calmer periods is actually lower. Both assets inflate in 2026; Ethereum, by some measures, inflates less. The “harder than Bitcoin” claim survives in a narrow, technical form even without net deflation.

The third point is that the supply figure overstates the sell pressure. Roughly 28% to 30% of all ETH is locked in staking, earning yield and not circulating. The tradeable float, ETH actually available on exchanges, is meaningfully smaller than the headline supply number, and it shrinks as more ETH is staked. A modestly inflating total supply with a large and growing staked portion is a very different pressure than the raw inflation number suggests. Demand from ETFs, treasury companies, and staking can absorb 0.2% inflation without difficulty.

And the fourth point is simply that the store-of-value case never rested on deflation alone. As long as demand for Ethereum’s blockspace, its role as settlement for stablecoins, tokenization, and DeFi, grows faster than supply, price can rise regardless of whether supply ticks up 0.2% a year. Scarcity was a nice story. Utility is the real thesis.

The bear case: the narrative was load-bearing

The skeptical reading is that the ultrasound story was not just marketing, that it was doing real work in the investment case, and that losing it matters more than the reframing admits.

The blunt version comes from the on-chain data and the people watching it leave. Daily network fee revenue on Ethereum fell from near $40 million in early 2025 to a local low around $10 million in 2026. That is not just a burn problem; it is a value-accrual problem. If the base layer captures little fee revenue because activity happens on rollups that pay it almost nothing, then holding ETH is a bet on an asset whose own network is monetizing its users poorly. Some analyses have tied this directly to developer attrition and reduced whale support, framing the end of ultrasound money as the end of a period when ETH had a clean, quantifiable reason to appreciate.

The deeper problem is structural and hard to argue away: a scaled, efficient Ethereum is less deflationary than a congested, expensive one. This is the tension at the center of the whole debate. The very thing that makes Ethereum better as infrastructure, cheap transactions, more capacity, activity on fast rollups, is the thing that reduces the burn. Ethereum cannot simultaneously be the cheap, high-throughput settlement layer it wants to be and the fee-burning deflationary asset the ultrasound thesis needed. Those are in direct conflict, and the roadmap chose scaling. The asset thesis was, in a real sense, sacrificed to the technology roadmap.

Then there is the value-capture question that rollups sharpen. Layer 2s use Ethereum for security and pay it a pittance for the privilege. Robinhood’s own chain is an example: analyses of corporate L2s show the base layer capturing a rounding error of the economics while providing the security that makes the whole arrangement credible. If Ethereum’s future is thousands of rollups settling to it cheaply, then Ethereum is providing enormous value and capturing little of it, and no amount of narrative reframing fixes a value-capture problem that lives in the fee structure.

The fix nobody is talking about

Which brings us to December 2025, and the upgrade that was designed, in part, to address exactly this, and that most of the market ignored.

The Fusaka upgrade activated on December 3, 2025. Its headline features were about scaling further, PeerDAS and expanded blob capacity. But buried in it was EIP-7918, the “blob base fee bound,” which is the most direct attempt yet to repair the burn. The problem Dencun created was that blob fees could collapse to near-zero, one wei, when execution costs dominated and blob demand was soft, which meant rollups consumed Ethereum’s capacity almost for free and burned almost nothing. EIP-7918 sets a floor: it ties the minimum blob fee to the execution base fee, roughly the execution base fee divided by 16, so that even in quiet periods rollups pay a meaningful minimum, and a minimum stream of ETH gets burned.

The modeling is striking. Fidelity Digital Assets analyzed what would have happened if EIP-7918 had been active since blobs launched, and found that on 93% of days since the 2024 Dencun upgrade, the adjusted fee would have exceeded the actual fee, generating an estimated additional $78.6 million, roughly 24,641 ETH, in cumulative blob-fee revenue. Blockworks noted that had the mechanism been introduced in June 2025, burnt blob fees would have been nearly 8x higher. The intent is explicit: restore a floor under the burn so that as stablecoins, DeFi, and tokenization migrate to rollups, ETH still captures value from that activity instead of subsidizing it.

The honest caveat is that this is a floor, not a restoration. EIP-7918 prevents the burn from collapsing to zero; it does not recreate the thousands-of-ETH-per-day burn of the congested mainnet era. Whether it produces measurable, sustained deflation depends on how much activity flows through blobs and how high execution base fees run, and the market is still watching. It is a serious, well-designed attempt to reconnect usage and scarcity. It is not a return to 2022.

Sound money versus ultrasound money, honestly compared

Because the entire thesis was built as a shot at Bitcoin, it is worth putting the two monetary models side by side without the tribalism, since the comparison is more interesting than either camp admits.

Bitcoin offers fixed scarcity. The supply schedule is written into the protocol, capped at 21 million coins, and halves on a predictable timetable roughly every four years. A holder knows today, with certainty, what Bitcoin’s issuance will be in 2030 and 2040. That certainty is the entire product. Bitcoin does not react to demand, does not burn, does not adjust; it simply issues on schedule toward a hard cap, and its current inflation runs around 0.8% annually, trending toward zero over decades. The trade-off Bitcoin holders accept is that the base layer offers little native utility and no yield. You hold it for the certainty, and you give up productivity in exchange.

Ethereum offered, and to a degree still offers, elastic scarcity. Supply responds to network demand: high usage burns more and can push ETH net deflationary; low usage burns less and lets mild inflation through. The appeal was a token that becomes scarcer precisely when it is most used, tying the asset’s scarcity to the network’s success. The trade-off, which the L2 era exposed, is that elasticity cuts both ways.

A demand-responsive supply is only deflationary when demand is high on the layer that burns, and Ethereum deliberately moved demand to layers that do not burn. Bitcoin’s rigidity, often criticized as inflexible, turned out to be the thing that made its monetary promise keepable. Ethereum’s flexibility, often praised as sophisticated, turned out to be the thing that made its monetary promise conditional.

The honest scorecard is that these are different products for different buyers, not better and worse versions of the same thing. Bitcoin sells certainty and asks you to forgo utility. Ethereum sells utility and asks you to accept that its scarcity depends on how that utility is used. The ultrasound-money era was the brief window when Ethereum appeared to offer both, certainty of deflation and utility of a working network, and that window closed not because Ethereum failed but because it succeeded at scaling.

A holder choosing between them in 2026 is really choosing between guaranteed scarcity with no yield and demand-driven scarcity with staking yield and network utility. Framed that way, the loss of ultrasound money is less a defeat than a clarification: Ethereum was never going to be Bitcoin, and the burn was hiding how different the two bets actually are.

What this means for holding ETH

Strip away the narrative fight and the practical question is whether the ultrasound story mattered to the price, and the uncomfortable answer is that it is hard to tell, because ETH has underperformed through the entire period regardless.

The clean way to see it: the ultrasound thesis was strongest right after the Merge, and it has been dismantled steadily since Dencun in March 2024. Over that same window, ETH has been a persistent underperformer against both Bitcoin and its own former highs. Either the market was pricing the loss of the deflation narrative, or the market never cared about the narrative and ETH’s problems lie elsewhere, in L2 value leakage, in competition from Solana, in the sheer difficulty of the modular roadmap. Both readings are defensible, and they point to different conclusions about whether fixing the burn fixes the price.

The most honest framing is that ultrasound money was a proxy for a real question that has not gone away: does Ethereum capture value from its own success? When the network was congested and expensive, the answer was visibly yes; the burn made it legible. When the network scaled and cheapened, the answer became murky, and the burn stopped telling the story. EIP-7918 is an attempt to make the answer legible again by putting a floor under value capture.

Whether it works will show up not in the marketing but in two numbers over the next year: net ETH supply, and base-layer fee revenue. If both turn up meaningfully, the thesis has a second life. If they do not, then ultrasound money was a phase, not a property, and Ethereum’s investment case has to stand on utility alone, which is a harder, slower, less tweetable argument than the one that shrank the supply.

Frequently Asked Questions

What is Ethereum ultrasound money?

It is the thesis that Ethereum’s ETH token would become deflationary and a superior store of value to Bitcoin. It rests on two mechanisms: EIP-1559, activated in 2021, which burns a portion of every transaction fee, and the 2022 Merge, which cut new ETH issuance by roughly 90%. When burning exceeds issuance, total supply shrinks. The term was a play on Bitcoin’s “sound money” branding.

Is Ethereum still deflationary in 2026?

Not on a net basis, in normal conditions. After the March 2024 Dencun upgrade shifted activity to cheap layer-2 rollups, the burn collapsed, and ETH became mildly inflationary, with net supply growth around 0.2% to 0.8% annually depending on the period. During bursts of high mainnet activity, it can still turn temporarily deflationary, but the sustained deflation of the immediate post-Merge period ended.

Why did layer 2s break the burn?

Because they moved activity off the base layer, where transactions burned meaningful ETH, onto rollups that pay near-zero fees. The Dencun upgrade introduced cheap “blob” transactions for rollups, cutting their costs 10 to 100 times. Blob space was oversupplied, so blob fees fell close to zero, and the daily burn dropped from thousands of ETH to as low as 50 to 70. The activity continued; the burn did not follow it.

Does this mean ETH is a worse investment?

Not necessarily, and defenders make several counterpoints: issuance is still about 90% lower than under proof-of-work, roughly 0.2% net inflation in calm periods is actually below Bitcoin’s, nearly a third of ETH is locked in staking and off the market, and the real case rests on demand for blockspace rather than deflation. Critics counter that base-layer fee revenue collapsed too, raising a genuine value-capture problem.

What is EIP-7918?

A change introduced in Ethereum’s December 2025 Fusaka upgrade that sets a minimum price for blob transactions, tied to the execution base fee, roughly that fee divided by 16. It prevents blob fees from collapsing to near-zero during quiet periods, ensuring a minimum stream of ETH is burned. Fidelity modeled that it would have added roughly $78.6 million in cumulative burn across 93% of days since 2024 had it existed earlier.

Did Fusaka restore ultrasound money?

No, it put a floor under the burn rather than restoring the deflation of the post-Merge era. EIP-7918 stops the burn from collapsing to zero and improves value capture as activity migrates to rollups, but it does not recreate the thousands-of-ETH-per-day burn of the congested mainnet period. Whether it produces sustained net deflation depends on blob activity and execution fees, and remains to be seen.

Is Ethereum still harder money than Bitcoin?

In a narrow technical sense, sometimes. In calm periods, Ethereum’s roughly 0.2% net inflation can run below Bitcoin’s roughly 0.8% fixed-schedule inflation. But Bitcoin offers predictable, protocol-guaranteed scarcity indefinitely, while Ethereum’s supply is elastic and responds to demand, so it can inflate more during quiet, scaled periods. They offer different kinds of scarcity: fixed and certain versus elastic and demand-driven.

What should I watch to know if the thesis recovers?

Two numbers over the next year: net ETH supply growth, and Ethereum base-layer fee revenue. If EIP-7918 and rising rollup activity push net supply back toward flat or negative while base-layer revenue climbs from its roughly $10 million lows, the value-capture story recovers. If supply keeps growing and fee revenue stays depressed, ultrasound money was a temporary phase, and ETH’s case rests on utility and demand alone.

Disclaimer: This article is for information and educational purposes only and does not constitute financial or investment advice. It describes monetary mechanics and network upgrades whose effects are uncertain and still developing. Nothing here is a recommendation to buy or sell any asset. Always do your own research. Figures on supply, burn, and inflation move continuously and are accurate as of July 17, 2026.

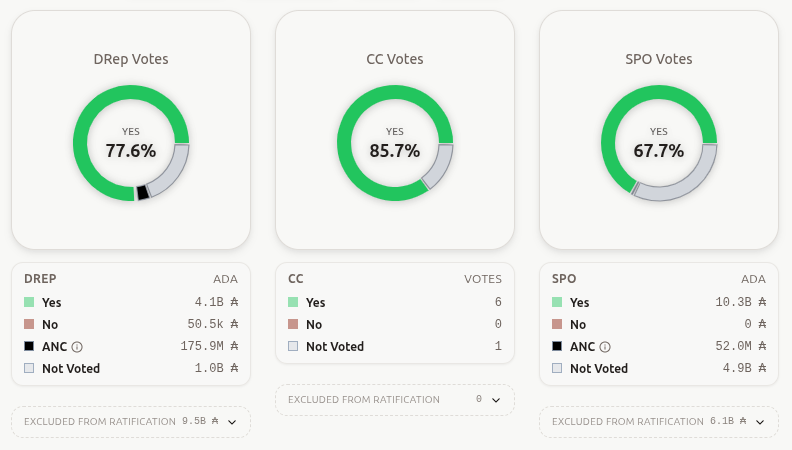

Cardano activated its Van Rossem hard fork on July 18, upgrading the network to Protocol Version 11 with faster, cheaper smart contracts and stronger node security.

The transition was smooth, but the real question is whether ADA can turn the milestone into lasting price gains.

What the Van Rossem Hard Fork Brings to Cardano

A hard fork is a permanent protocol change that updates a blockchain’s core rules for everyone at once. Van Rossem, named after contributor Max van Rossem, went live around 21:45 UTC.

The upgrade caused only a brief ten-minute block gap, with no disruption to users or holdings. It marks the first major upgrade fully approved through Cardano’s Voltaire governance system.

The improvements target smart contracts directly: faster Plutus execution, new built-in functions, updated cost models, and stronger node security.

Those changes aim to make decentralized application development cheaper. Lower costs and stronger scripting could accelerate DeFi, NFT, and real-world asset activity.

Unlike previous era-changing forks, Van Rossem is an intra-era upgrade. It keeps the network inside the Conway governance framework while delivering immediate efficiency gains for developers.

Intersect, coordinating Cardano’s development, framed the event as proof of maturing decentralized governance.

More than 77% of delegated representatives (DReps) and 52% of stake pool operators backed it.

“The best part: it was ratified on-chain by delegated community reps before activation. Upgrades by governance, not decree,” Cardano DRep Jason Appleton said on X.

Follow us on X to get the latest news as it happens.

The upgrade also arrives alongside a broader shift. Input Output will hand over core infrastructure, including the Plutus platform and Daedalus wallet, to external firms from August.

Can Van Rossem Deliver a Sustained ADA Rally

As expected with major upgrades, ADA saw short-term momentum. The token trades near $0.1663, up roughly 1.2% in 24 hours, according to BeInCrypto data. Still, the critical question remains whether Van Rossem can deliver a sustained rally. History urges caution.

Cardano hard forks have often generated initial excitement followed by consolidation, unless paired with real ecosystem growth. The lasting impact depends on several factors.

Rising developer activity, new dApp deployments, and growing total value locked in DeFi all matter. So does integration with upcoming upgrades like Ouroboros Leios, built for higher throughput.

Whale behavior adds another layer. Wallets holding 100,000 to 100 million ADA have accumulated over 25.6 billion tokens, their highest level since February 2023.

Analysts stay cautiously optimistic. The upgrade improves fundamentals, but price gains will ultimately depend on user adoption and capital inflow rather than the technical milestone alone.

Van Rossem represents another step in Cardano’s research-driven roadmap.

Whether ADA competes harder against Solana and newer Layer-1s now hinges on real on-chain growth in daily addresses, volume, and developer activity ahead.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights.

The post Cardano Activates the Van Rossem Hard Fork: Will It Boost ADA Price? appeared first on BeInCrypto.

The spot exchange-traded funds tracking the performance of Ripple’s cross-border token took their first hit last week in over two months, but net inflows have returned.

However, there’s still an evident investment exodus that we need to discuss, as the financial vehicles had no reportable data for too many days.

XRP ETFs Are Back

For roughly two months, during which the spot Bitcoin and Ethereum ETFs bled heavily, with billions of dollars leaving both, the XRP counterparts enjoyed investors’ attention by gathering fresh capital. In fact, as we repeatedly reported, they set a 9-week green-only streak, in which they attracted almost $200 million.

This all changed during the second week of July when data from SoSoValue showed that investors pulled out just over $7 million from the funds for the first time in over two months.

However, green is back on XRP’s street as the past week almost offset all the losses from the previous one. The net inflows for the five-day trading period stand at $6.78 million. This means that the cumulative total net inflow is back to its ATH levels of almost $1.5 billion.

Bitwise’s XRP ETF continues to increase the gap between itself and the first such fund to reach Wall Street – Canary Capital’s XRPC. The former now holds almost $500 million in AUM, while the latter is below $470 million.

The Big Catch

Although the week as a whole was indeed in the green, all $6.78 million in net inflows came in just one day: July 16. The rest (four) trading days saw no reportable action, according to SoSoValue. Although the XRP ETFs have seen many such days in the past, there were never four in the same week.

Moreover, seven of the last 10 business days have seen net flows of $0.00. This is a rather concerning trend, clearly showing that interest and demand for the financial products have declined significantly.

Perhaps a portion of the blame can be put on the overall sluggish summer season, in which trading volumes traditionally drop, as investors wait for better times. XRP’s sluggish price performance might also turn investors away, as the asset has failed to break out above the $1.10 resistance despite a few attempts. It remains down by 3% monthly, with a market cap of well under $70 billion.

The post Ripple (XRP) ETFs Resume Inflow Streak, but There’s an Elephant in the Room appeared first on CryptoPotato.

Strategy executive chairman Michael Saylor took to social media on Sunday to detail his “110 reasons” why a proposed temporary fork to limit non-monetary transactions on the Bitcoin network, or BIP-110, is a bad idea.

Bitcoin Improvement Proposal-110 was introduced in December 2025 to stop nonfungible token-like Ordinals inscriptions and other arbitrary data from spamming the network and to preserve BTC’s main use as a peer-to-peer cash system.

In a roughly 3,700 word post on X.com, the man in control of the largest Bitcoin (BTC) corporate treasury made a case for what he said are “neutral rules, hard consensus, open markets, and permissionless innovation.”

Source: Michael Saylor on X.com

“Many Bitcoiners I respect support BIP 110. They want to keep validation accessible, protect node operators from unwanted costs and content, preserve affordable payments, and keep Bitcoin focused on sound money rather than general-purpose data storage. Those are serious concerns. I share the objectives. I disagree about the remedy,” Saylor said. He added:

“This article critiques the proposal, not the people behind it. I assume good faith. Bitcoin is strongest when we can disagree vigorously without mistaking allies for enemies.”

As of 12 p.m. ET, on Sunday, the post had been viewed 879,000 times, with 692 replies and 852 retweets.

BIP-110 is one of the more notable protocol-level disputes in the Bitcoin development community since the Blocksize Wars between 2015 and 2017, when ecosystem participants debated whether it was worth risking a chain split to raise the block size limit for scalability.

The proposal was introduced by pseudonymous Bitcoin developer “Dathon Ohm” with the support of Ocean protocol founder Luke Dashjr. Opponents include Blockstream CEO Adam Back.

Related: Bitcoin nodes running BIP-110 crosses 2% as spam wars heat up

Little certainty on BHP-110 approval

To be sure, BIP-110 won’t be activated unless 55% of Bitcoin nodes validating blocks are in support of the proposal across a Bitcoin block “period.”

In the last period, period number 475 between block 955,584 and 957,599, only 1% of blocks were in support.

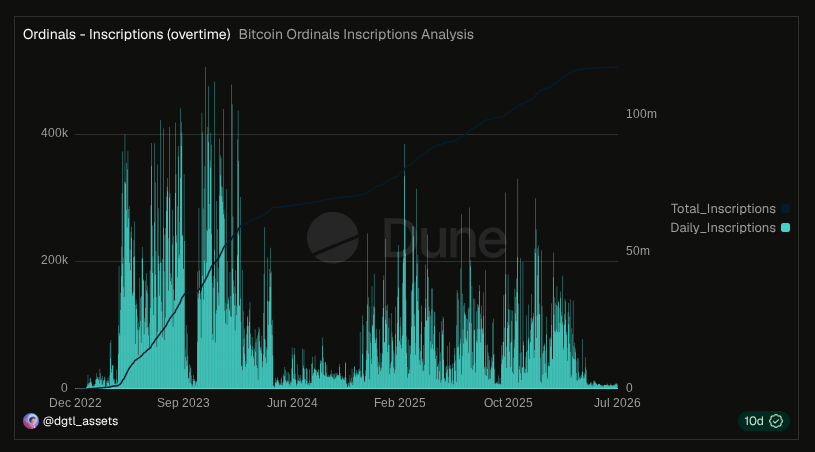

The dispute comes at a time when Ordinals activity is at near all-time lows, with fewer than 10,000 Ordinals inscribed into the Bitcoin blockchain on a daily basis over the last month, down from the more than 400,000 seen during its peak in August 2023.

Change in daily Ordinals inscriptions since December 2022.

Source: Dune Analytics

Bock has previously criticized BIP-110, describing it as a “quest to police other people.”

He said Bitcoin’s decentralization should mean “you can’t impose your views on others,” calling it incompatible with BTC’s cypherpunk ethos of permissionless, censorship-resistant money.

Dashjr and other BIP-110 supporters have called Ordinals-driven bloat a “serious threat” to the network, prompting the need for an imminent fix.

They have also argued BIP-110 wouldn’t cause a chain split, as many fear, while adding that the BIP-110 fork imposes a temporary one-year limit and thus wouldn’t invalidate fee-paying transactions over the long term.

Features: From Bitcoin critics to blockchain believers: The 5 biggest crypto backflips

Michael Saylor, executive chairman and co-founder of Strategy, has come out swinging against a new proposal to clean up Bitcoin’s ‘spam,’ arguing that it could fundamentally alter how the world’s largest blockchain operates.

The Bitcoin Improvement Proposal (BIP) 110, aimed at temporarily restricting arbitrary data to focus on the core monetary functions, is a threat to the main principles of the network, Saylor explained in a comprehensive critique published on X, titled “110 reasons BIP-110 is a bad idea.”

“The proposed cure is more dangerous than the condition,” Saylor said in the recent detailed analysis. “BIP 110 would use consensus to narrow valid activity, constrain future options, complicate deployment, and establish a precedent it cannot later erase.”

Saylor’s primary objection is based on the “no-questions-asked” nature of money. “Bitcoin cannot read intent,” Saylor writes. “The network cannot know whether bytes represent an image, a proof, a contract, metadata, an authentication record, or a future application,” argued.

By banning “spam,” the protocol would effectively elevate human judgment into protocol law, effectively turning Bitcoin’s conservatism upside down.

‘Too aggressive’

Saylor is the latest bitcoin executive to weigh in on this highly debated topic among the Bitcoin community.

Pi Network’s native token has stolen the show in the cryptocurrency markets with a massive price surge that drove it to a weekly high of roughly $0.10.

This is rather unexpected given the asset’s latest price performance, which included dumping to several consecutive all-time lows. The question is whether this is a profound recovery or another dead-cat bounce.

PI Pumps Hard on Sunday

CryptoPotato has repeatedly reported over the past week or so the adverse price developments around Pi Network’s PI token. The asset broke below the key $0.10 support last weekend, and the bears took complete control of the market. In the following days, they pushed it below $0.09 and $0.08.

PI rebounded only after it dumped to $0.07, which turned out to be a strong support. The token marked a new all-time low, which meant that it had plunged by over 97% since its ATH over a year ago, but rebounded immediately.

As reported yesterday, it showed some resilience and climbed above $0.08. It remained there for about 24 hours before it went on the aforementioned rally today. It skyrocketed by almost 20% and is now close to $0.10 for the first time in a week. This has become a key resistance level, which has to be reclaimed before the asset has any chance of a bigger rebound.

Recovery or Dead-Cat Bounce?

Although today’s rather unexpected but impressive surge has given some hope to the bulls, PI’s history has repeatedly shown that it’s not that simple, and the hype could come to an end soon.

The asset has posted similar gains on numerous occasions in the past, especially after prolonged downturns. Once it becomes the top performer, though, it crashes and burns to its starting level or even lower within days. The latest such example was in mid-March when it rocketed from $0.20 to $0.30 during the Kraken-listing hype.

It was rejected immediately and slumped below $0.20 within 72 hours. It has been unable to reclaim its former glory since then, and the recent crash to $0.07 only proved that. The Pi Network investors and believers would have to wait and see if this rally now is any different.

The post Pi Network’s PI Suddenly Explodes by 20%: Recovery or Dead-Cat Bounce? appeared first on CryptoPotato.

Thirty days is a short window to ask for anything, which makes Grok AI predicts that XRP is almost restrained by comparison to the usual end-of-year moonshots. From $1.08, it wants $1.25 to $1.35 by mid August.

The setup leans on five things happening together rather than one big catalyst. Spot ETF inflows keep showing up. Ripple’s full MiCA license opens the door to regulated European expansion.

XRPL network activity is surging in the background. Whales are accumulating instead of distributing. Exchange balances are dropping as coins move into cold storage.

Grok also points to something almost calendar-based. July has historically been a strong month for XRP, and that seasonal pattern is landing right on top of a market that just deleveraged hard.

The $1.00 to $1.05 zone has held firm through that deleveraging, which Grok reads as buyers defending a line rather than just drifting sideways. Clear resistance at $1.18 to $1.22, and Grok sees a confident push toward $1.25 to $1.40, with $1.30 to $1.35 as the realistic high if momentum and any regulatory tailwind cooperate.

The bear case stays narrow here, too. Broader market weakness or delays to the CLARITY Act could cap gains and force consolidation, with a retest of $0.95 to $1.00 support if the round number breaks.

Grok’s own base scenario without fresh catalysts is a flat $0.95 to $1.10, basically where XRP sits right now. The whole prediction hinges on new news arriving, not on existing momentum carrying itself.

Discover: The Best Token Presales

XRP Price Prediction: Has Traded In A Shrinking Box For Six Months And Grok Wants The Top Broken

The chart tells a quieter story than the prediction does. XRP closed at $1.08468, down 0.14%, in a session ranging between $1.07840 and $1.09495.

Zoom out from February, and this is not a downtrend anymore; it is a fading range. The February crash from above $2.30 down toward $1.20 was the violent part, and everything since has been a series of lower highs inside a slowly compressing box.

April topped near $1.55. May topped near $1.55 again. July’s bounce topped near $1.20 and already rolled over.

That is three failed attempts at reclaiming higher ground, each one weaker than the last. Support sits at $1.00, the level Grok specifically flagged as defended, then $0.95 below that.

Resistance stacks at $1.12, then $1.18, then the stubborn $1.20 ceiling that keeps rejecting every bounce. The RSI panel shows momentum at 44.55 with the signal line at 47.03, a small negative gap that has been narrowing over the past week.

That narrowing gap is the one mildly encouraging detail on this chart. It suggests selling pressure is easing rather than building, even if it has not flipped positive yet.

For Grok’s $1.25 target to happen in 30 days, XRP needs to do something it has failed to do three times since February, actually clear $1.20 and hold above it. Until that happens, this range keeps compressing rather than breaking.

Discover: The best crypto to diversify your portfolio with

Here is what Grok AI Predicts For LiquidChain’s Near Future

Every cycle has a moment where waiting becomes the most expensive decision you can make. That moment is now.

Bitcoin, Ethereum, and XRP are all pinned under the same resistance they have been testing for weeks. The macro unlock is perpetually one data point away. The institutional money keeps arriving next quarter. Large-cap traders waiting for a breakout are queuing for a decision that belongs to someone else entirely.

Grok AI has identified what experienced cycle traders already act on. Capital that registers as statistical background noise at Bitcoin’s market cap can completely reprice a small, undiscovered project.

The asymmetry is not complicated. It lives in the distance between what something is genuinely worth and what the market has currently assigned it. The moment that distance gets noticed, it collapses. Before that moment, it is fully open.

Cross-chain fragmentation has been quietly taxing every DeFi participant since the first bridge went live. Bitcoin, Ethereum, and Solana were engineered independently with zero shared infrastructure and no design intent to communicate. Every transaction crossing those ecosystem boundaries absorbs the cost of that decision in fees, failed execution, and slippage that hits before settlement even begins. The bridge industry did not fix this problem. It built a business model on top of it.

LiquidChain removes the business model entirely. Three networks unified inside a single execution layer. One deployment reaches all of them simultaneously. No cross-chain tax is extracted from any interaction anywhere.

Grok AI predicts it as a worth watching coin. The presale sits at $0.01454 with just over $860,000 raised.

Execution is unproven. Adoption is an open question. Established assets offer a smoother path toward a ceiling that the entire market can already see. LiquidChain is the entry point that stops existing once the market finds it.

Don’t Miss Out on Our $1,000 USDT Airdrop on ByBit

The post Elon Musk Grok AI Predicts XRP Will Do This by Next 30 Days, and Nobody Is Ready appeared first on Cryptonews.

The Electronic Transactions Association (ETA) is signaling a more constructive stance toward Bitcoin, with CEO Jason Oxman saying the group does not oppose the network and is open to partnerships—especially when customer demand and merchant needs point that way. Speaking in an interview with CoinDesk, Oxman framed the ETA’s position as technology-neutral, while pointing to recent activity with BitPay as evidence that Bitcoin-related innovation is on the table.

The shift is also reflected in the ETA’s membership changes: on August 6, the trade group announced BitPay—an Atlanta-based Bitcoin payments provider—as the first virtual currency company to join the ETA. The association represents major players in electronic payments, including Visa, MasterCard, Amazon, and PayPal, and said the addition underscores its intent to engage with emerging technologies as the payments industry evolves.

Key takeaways

- ETA CEO Jason Oxman said the organization does not advocate for Bitcoin and has not taken a position against other technologies; it treats electronic transactions as the common denominator.

- BitPay joining the ETA on August 6 marks the first virtual currency company membership, suggesting traditional payments groups may be willing to cooperate with Bitcoin processors.

- Oxman cited the Bitcoin Foundation’s role in educating ETA members—dating back to an ETA event in 2013—as part of why members began viewing Bitcoin as “an interesting development.”

- In discussing New York’s BitLicense proposal, Oxman argued regulators should avoid reflexive rules for “something new” and instead conduct deeper research into how Bitcoin systems and consumer protections work.

Why the ETA is talking more openly about Bitcoin

Oxman’s comments emphasize that the ETA’s mandate is broader than any single payment network. In the CoinDesk interview, he said the association’s stance is centered on facilitating electronic transactions, which means the transaction format ultimately follows what merchants and customers choose.

That framing matters because it positions Bitcoin less as an “alternative” and more as another option within the payments stack—one that may be integrated if it demonstrates value and operational safety. Oxman specifically pointed to the ETA’s partnership with BitPay as a concrete example of how the group approaches innovation without automatically dismissing new models.

By describing the ETA as “open to work with emerging tech startups, including Bitcoin-related companies,” Oxman also made demand the deciding factor. In other words, the ETA’s engagement appears less like advocacy for a particular technology and more like an attempt to stay relevant as customers and merchants experiment with Bitcoin payments.

BitPay membership and what it signals to traditional payments

The ETA press release introducing BitPay as a member described the decision as part of the group’s commitment to embrace new technology. BitPay’s entrance into an association that includes payment giants is significant, even if it does not automatically translate into endorsement of Bitcoin across the entire membership.

Oxman suggested the ETA’s outlook has changed as members gain more practical context. He referred to an earlier event in 2013 where Bitcoin Foundation general counsel Patrick Murck discussed Bitcoin in business-focused terms. Oxman said Murck’s presentation helped ETA members see Bitcoin as a relevant development for the industry, adding that at least one ETA member proceeded to strike a deal with a Bitcoin processor.

That historical detail points to a wider dynamic: partnerships in payments often come after repeated exposure to regulatory and operational questions. The ETA’s decision to bring BitPay in—and Oxman’s explanation of why—implies that Bitcoin’s perceived legitimacy is improving among mainstream payment stakeholders, at least in the context of how Bitcoin processing can fit into established transaction workflows.

The BitLicense debate: consumer protection vs. innovation

Oxman also addressed New York’s BitLicense proposal and the regulatory scrutiny surrounding it. He acknowledged that regulators’ concerns are understandable, particularly around consumer protection in novel payment systems. In his view, when alternative payment options are not well established and widely deployed, regulators feel more compelled to step in to protect consumers where those protections are not already present.

That stance reflects a tension at the heart of Bitcoin policy discussions: overly strict rules can raise compliance barriers and slow experimentation, while weak oversight can leave users exposed. Oxman argued that the ETA had previously worked through regulatory uncertainty when new payment methods—such as PayPal—arrived, spending significant time ensuring government action did not constrain innovation.

But he said New York should not treat Bitcoin as a special case that must be regulated using reflexive logic. Instead, he urged the NY Department of Financial Services (NYDFS) to conduct a more in-depth examination of Bitcoin’s technical operation and the additional measures that Bitcoin providers—including Bitcoin processors—take to protect both consumers and merchants.

Importantly, Oxman’s position is not a call to ignore regulation; it is a call for regulation built around how Bitcoin works in practice, rather than rules applied because the technology is new.

Regulatory timeline shifts in New York

Meanwhile, New York’s BitLicense review process is still moving. According to earlier coverage from Cointelegraph, the NYDFS superintendent Benjamin Lawsky extended the public comment period on the BitLicense proposal by 45 days, pushing the deadline to October 21. The extension followed a joint letter in which BTC China, Huobi, and OkCoin—referred to by Cointelegraph as the “Big three”—outlined concerns and requested changes to the proposal.

For investors and market participants, these procedural updates can be as important as the policy itself. Longer comment windows often indicate that regulators are weighing industry feedback more deliberately—potentially affecting how strict compliance obligations are ultimately framed. It also means companies preparing for the BitLicense regime may face shifting expectations as regulators refine their approach.

As the ETA continues building relationships with Bitcoin-focused firms like BitPay and New York’s BitLicense review proceeds through an extended comment period, the key question for the market is how regulators will translate concerns about consumer protection into rules that reflect Bitcoin’s actual system design—and whether mainstream payment stakeholders continue to increase engagement as compliance certainty improves.

Japanese logistics group AZ-COM Maruwa Holdings plans to introduce the yen-backed JPYC stablecoin for payments to about 2,300 partner carriers and independent drivers, according to a Nikkei report cited by Crypto Briefing.

Summary

- AZ-COM Maruwa plans JPYC payments for 2,300 logistics partners in Japan’s first large corporate rollout.

- The logistics group will invest ¥1 billion in JPYC while forming a business partnership directly.

- JPYC is gaining wider use through retail trials, lending projects, and emerging payment infrastructure nationwide.

The move is “expected to become Japan’s first large-scale corporate use of JPYC.”The company also plans to invest ¥1 billion in JPYC and form a business partnership with the stablecoin issuer. The rollout would move JPYC beyond retail tests and crypto services into routine business payments across a large logistics network.

AZ-COM Maruwa brings JPYC into logistics payments

AZ-COM Maruwa Holdings operates third-party logistics, transportation, warehousing and delivery services in Japan. Its planned use of JPYC would cover outsourcing and other payments made to a broad network of transport partners, including individual truck drivers.

The reported ¥1 billion investment also ties the logistics group directly to JPYC’s growth. The companies have not yet disclosed a detailed rollout schedule or explained how each partner will receive, hold or convert the tokens. Those operating details will determine how widely drivers and carriers use JPYC instead of immediately redeeming it for yen.

JPYC began issuing its regulated yen-backed stablecoin on October 27, 2025. The token maintains a one-to-one link with the yen and uses bank deposits and Japanese government bonds as reserve assets. It operates on public blockchain networks and can be issued or redeemed through JPYC EX.

The AZ-COM Maruwa plan follows other attempts to move JPYC into daily payments. As reported by crypto.news, Lawson plans to test JPYC payments at a Tokyo convenience store in August through a point-of-sale system. The trial will let customers pay using a smartphone-linked payment system.

Japan’s stablecoin market adds more use cases

JPYC is also expanding into financial products. As reported by crypto.news, Metaplanet and JPYC recently began studying Bitcoin-backed credit products that could use JPYC for lending and settlement. The project is examining how Bitcoin collateral and yen-denominated stablecoin liquidity could work together. Payment infrastructure is developing at the same time.As reported by crypto.news, LINE NEXT plans to support JPYC through Unifi Pay, a stablecoin payment service scheduled for a wider launch in the third quarter. The service is designed to let users in Japan top up local stablecoins from bank accounts after identity checks.

The logistics rollout would differ from smaller consumer pilots because it involves thousands of businesses and independent drivers receiving payments through the same stablecoin system. If implemented at the reported scale, it would test JPYC’s ability to handle regular corporate settlement rather than isolated retail purchases.

Japan is also tightening rules around stablecoin reserves as adoption grows.Japanese regulators have set conditions for government bonds held as reserve assets. JPYC has said it plans to keep most reserve proceeds in Japanese government bonds and the remainder in bank deposits.

AZ-COM Maruwa’s planned rollout therefore arrives as JPYC moves into retail payments, lending experiments and broader payment infrastructure. The ¥1 billion investment adds a direct corporate commitment, while the proposed payments to 2,300 logistics partners would provide one of the clearest tests yet of whether a regulated yen stablecoin can work in everyday business settlement.

The rise of autonomous AI agents necessitates the utilization of zero-knowledge proofs, argues Brian Trunzo, chief growth officer at Succinct Labs.

Michael Saylor rattled the community cages on X once again with a cryptic post containing a graph showcasing his company’s countless BTC purchases completed over the past six years, with the text “What’s next?”

Although many translated this message as a new hint that Strategy has made a new bitcoin purchase, the reality from the past several weeks tells a different story.

What’s next? pic.twitter.com/bNl0xX0obw

— Michael Saylor (@saylor) July 19, 2026

Buy or Sell Next?

The firm’s co-founder and former CEO has been publishing such posts for years. We didn’t pay much attention to them before, as they were always followed by a major purchase announcement on the next business day. However, this all changed a few weeks ago when, instead of bragging about the latest bitcoin acquisition, Strategy announced its biggest BTC sale to date by disposing of over 3,500 units.

The perception changed immediately. It came just a week after the firm had launched the Digital Credit Capital Framework to enhance liquidity and long-term BTC exposure. The idea was simple – the firm had a USD reserve of $2.55 billion, which was enough to cover 17.4 months of dividend payments. However, it wanted to raise that, and included potential BTC sales of up to $1.25 billion to expand the dividend payment period to over 25 months.

Saylor published a similar hint last weekend, which led to no bitcoin move. Instead, Strategy increased its USD reserve to $3 billion by raising funds via an at-the-market common stock offering. All eyes have now turned to the world’s largest corporate holder of BTC, and speculation is running wild about what tomorrow’s announcement will be.

113 Purchases

We called them countless above, but in fact the actual number of purchases is 113 (we counted them slowly; hopefully we are not wrong). They began almost six years ago, and the firm has accumulated 843,775 BTC since then after it ramped up its efforts following the 2024 US presidential elections and the promise of a friendlier regulatory environment.

Despite the DCA strategy, the company remains down on its major bitcoin bet, given the asset’s price correction over the last 9 months or so. The firm has spent roughly $64 billion to accumulate its stash, but its current value is nearly $10 billion lower. This means that the company’s unrealized loss stands at around 15%.

The post Buy or Sell? What Michael Saylor’s Cryptic New Tweet Means for Bitcoin appeared first on CryptoPotato.

Smoke seen for miles around as firefighters tackle huge blaze at industrial estate

4 Top Stocks In A Technical Bear Market

Cardano Activates the Van Rossem Hard Fork: Will It Boost ADA Price?

-

NewsBeat3 days ago

NewsBeat3 days agoLondon Mayor Sadiq Khan handed a peerage by Keir Starmer alongside 15 other Labour figures… just days before the PM leaves No10

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread – Corporette.com

-

Politics1 day ago

Politics1 day agoThe House | The City of London can help the new chancellor deliver growth in every postcode

-

Politics4 days ago

Politics4 days agoYoung campaigners urge incoming PM to act on outdoor junk food ads

-

Crypto World4 days ago

Crypto World4 days agoCFTC blocks Kalshi from unwinding Michigan trades after court order

-

Business4 days ago

Business4 days agoNvidia Stock Slips After Big Tuesday Rally as Huang Confirms Vera Rubin Chip Is Now in Production Today

-

Crypto World1 day ago

Crypto World1 day agoRipple Payments Joins MiCA With 14 Firms, Does It Mean Anything For XRP?

-

Politics3 hours ago

Politics3 hours agoDemocrats look to World Cup watch parties to register thousands of voters

-

Entertainment4 days ago

Entertainment4 days agoDisney’s Most Ambitious Failed Star Wars Attraction Is Coming to SDCC

-

Crypto World2 days ago

Crypto World2 days agoRipple wins EU-wide access as ESMA adds it to MiCA register

-

Crypto World2 days ago

Crypto World2 days agoTwo July Windows Left: The CLARITY Act’s Senate Fight and What Failure Means

-

Business4 days ago

Business4 days agoPalantir Shares Rise After Expanded Nvidia Partnership and Fresh Analyst Upgrades Ahead of Earnings Day

-

Crypto World3 days ago

Crypto World3 days agoInjective Submits SEC Transfer-Agent Registration to Onchain Ownership Records

-

Tech5 days ago

Tech5 days agoGet Your ESP32 Sunny Side Up With This Solar Dev Board

-

News Videos5 days ago

News Videos5 days agoXRP BOMBSHELL… XRP OMBOARDED FOR TRANSACTIONS!!!

-

NewsBeat2 days ago

NewsBeat2 days agoRegistration is now open for March for Men with Kev 2026

-

Tech5 days ago

Tech5 days agoDark Secrets Emerge When Jailbreaking LLMs

-

Sports4 days ago

Sports4 days agoNew Cornerback Enters Vikings Trade Rumor Mill

-

News Videos2 days ago

News Videos2 days agoMoney | Class 12 Economics | CBSE Board Exam 2026-27

-

Business3 days ago

Business3 days agoBanco Bilbao Vizcaya Argentaria, S.A. (BBVA) Discusses Global Macro Environment and Economic Outlook for Core Markets Transcript

You must be logged in to post a comment Login