Crypto World

Farage crypto gift prompts regulatory questions after property purchase

London’s political-finance landscape is sharpening its focus on crypto-enabled gifts as scrutiny tightens around donations and personal gifts to public figures. Nigel Farage, the leader of the Reform Party, received a £5 million personal gift from crypto entrepreneur Christopher Harborne, which was used to acquire a property valued at £1.4 million. The deal closed in May 2024, several weeks before Farage announced his candidacy for the general election. Critics and opposition figures have raised questions about whether the gift should have been disclosed and registered under political-finance rules after he assumed office. Farage and his party deny any wrongdoing, arguing the gift predated his formal entry into Parliament and thus was not subject to the same reporting requirements.

According to Sky News, the property transaction was completed in May 2024, and the gift was part of the broader discussion surrounding Farage’s parliamentary bid. The case has since become a focal point in debates over crypto-enabled political donations and the evolving regulatory framework governing political financing in the United Kingdom. Cointelegraph reported that Farage is facing a UK parliamentary probe over the £5 million gift, signaling the potential for formal inquiries that could affect the party’s fundraising practices and compliance posture.

The broader context includes a growing push among UK lawmakers to curb crypto political donations amid concerns about ethics, transparency, and foreign influence. The Reform Party’s stance, which includes resistance to bans on crypto political contributions, is juxtaposed with regulatory-driven efforts to impose stricter controls on such donations. The dynamic underscores a key regulatory tension: balancing the use of digital assets in political philanthropy with robust governance and enforcement mechanisms.

Nigel Farage said the Reform Party will fight back against bans or temporary moratoriums on crypto political donations. Source: Sky News

The developing narrative extends beyond Farage’s case. In February 2025, Matt Western, chair of the United Kingdom’s Joint Committee on the National Security Strategy, urged lawmakers to temporarily ban crypto donations to political parties and figures. Western argued that tightening controls is warranted given concerns about foreign governments seeking to influence UK elections through political finance channels that include cryptocurrency donations. “As the security environment worsens and the UK’s military role in Europe grows, the value of influencing the UK’s political positions, for example, on Ukraine, or US-EU relations, is likely to increase,” he said in a parliamentary document.

The government has moved, in parallel, to advance a legislative proposal to temporarily ban political crypto donations, following Western’s recommendations and an independent inquiry into the threats posed by foreign political donations. Although the proposal reflects heightened regulatory intent, it still requires passage through both houses of Parliament and royal assent before becoming law. Prime Minister Keir Starmer emphasized a decisive approach to protecting democratic processes, stating that the government will act to curb crypto political donations if legislation progresses to enactment.

Against this backdrop, regulatory and policy implications are becoming more pronounced for a range of actors—political parties, donors, financial institutions, and crypto firms. The Farage matter has amplified discussions about disclosure obligations, pre-office gifts, and how such transfers should be treated under existing rules governing political financing. It has also elevated the importance of robust AML/KYC controls, due-diligence standards for political donors, and the potential need for licensing or heightened oversight for entities that facilitate large crypto gifts to political actors.

Key takeaways

- A £5 million personal gift from crypto entrepreneur Christopher Harborne to Nigel Farage is the subject of a UK parliamentary probe, spotlighting the governance of crypto-backed political donations.

- The associated property purchase, valued at £1.4 million, closed in May 2024, weeks before Farage publicly announced his election bid. Farage contends the gift predated his official office entry and thus falls outside post-office reporting requirements.

- There is growing legislative and regulatory attention on crypto contributions to political campaigns in the UK, including calls for a temporary ban on such donations.

- In February 2025, Matt Western urged a temporary ban on crypto political donations, arguing foreign influence risks and national security considerations. The proposed policy is progressing through the legislative process but has not yet become law.

- The government’s March proposal to curb crypto political donations represents a broader effort to align political finance rules with emerging crypto-regulatory standards, raising implications for compliance programs, financial institutions, and political actors.

Gift receipts and disclosure: legal and regulatory implications

The Farage case foregrounds a critical question for UK political finance law: how gifts and donations that involve digital assets or crypto-linked funds should be disclosed and recorded, especially when transfers occur before an individual assumes public office. The existing framework in the UK requires certain gifts and donations to be declared to ensure transparency and prevent undue influence. If the gift predates official office, as Farage contends, regulators and oversight bodies may view the reporting thresholds and timelines differently. The ongoing parliamentary inquiry will likely examine whether any disclosure requirements were met or could have been triggered under applicable rules at the time of receipt and subsequent use.

Regulatory filings and parliamentary records show a deliberate push to scrutinize crypto-donation pathways used by political actors. The case has catalyzed discussions about whether amendments to the Political Parties, Elections and Referendums Act, or related guidance, are warranted to close potential gaps in reporting, especially for non-traditional funding mechanisms. While the gift itself is not a direct financial transaction from a political party to a candidate, the transparency framework surrounding personal gifts to politicians in the context of campaign activities remains an active area of regulatory assessment.

Regulatory push: crypto donations in UK politics

The UK’s policy environment for crypto donations is evolving on multiple fronts. The Joint Committee on the National Security Strategy’s inquiry into foreign influence, combined with broader ethics and democratic-resilience concerns, has spurred regulatory interest in strict limits or temporary prohibitions on crypto donations. The February 2025 letter from Matt Western exemplifies a growing chorus among lawmakers advocating precautionary measures as a safeguard for national security and political integrity.

In March, the government introduced a legislative proposal aimed at temporarily banning political crypto donations. The aim is to address recommendations from Western and an independent inquiry into foreign donations, while acknowledging that the proposal must navigate parliamentary approval and constitutional processes, including assent by the sovereign. The steps underscore how quickly policy can evolve in response to perceived regulatory risks associated with crypto contributions to public life.

From a compliance perspective, the evolving regulatory stance has material implications for entities involved in processing or facilitating crypto gifts to political actors. Crypto firms, exchanges, and payment service providers may face enhanced due diligence, anti-money-laundering checks, and reporting obligations if crypto contributions become subject to stricter licensing, oversight, or even restricted access to political channels. Banks and traditional financial institutions, increasingly engaged in crypto-related banking relationships, will be attentive to any shifts that could affect cross-border fund flows, reporting requirements, and customer onboarding protocols tied to political donors.

At the margin, the regulatory discourse resonates with broader developments in international crypto policy, including how MiCA (Market in Crypto-Assets) and related frameworks interact with national approaches to political financing and banking integration. While the UK has not adopted MiCA wholesale, the policy direction—emphasizing transparency, supervision, and risk mitigation for crypto-enabled activities—frames the context in which UK regulators are refining how political gifts are treated in practice.

Policy implications for institutions and market structure

Beyond the immediate political-finance questions, the Farage matter spotlights practical implications for institutions interfacing with crypto donations and political funding. For political parties, tighter rules could necessitate enhanced donor screening, more rigorous record-keeping, and clearer guidance on the timing and manner of disclosures. For financial institutions and crypto service providers, the case reinforces the imperative to align client onboarding, sanctions screening, and transaction monitoring with evolving regulatory expectations. In a new normal where crypto gifts intersect with public financing, firms must anticipate potential licensing or registration requirements and heightened regulatory scrutiny.

From a policy design perspective, the UK’s approach may influence cross-border regulatory dynamics and the future stance toward crypto fundraising and political engagement. The conversation around foreign influence, transparency, and the security implications of crypto-based donations remains unsettled in the short term, with the risk of policy changes that could reorder how donors participate in political campaigns.

Analysts and compliance teams will be watching how the government balances democratic safeguards with the practicalities of fundraising and political expression in a digital age. The pace and direction of legislative progress, as well as the outcomes of parliamentary scrutiny, will shape the regulatory baseline for political crypto donations in the UK for years to come.

In sum, the Farage gift case serves as a bellwether for how crypto philanthropy and political finance will be governed moving forward. It highlights the need for clear disclosure standards, robust enforcement, and an adaptable regulatory framework that can address both national-security concerns and the realities of digital asset markets.

Closing perspective: As Parliament weighs temporary restrictions and potential reforms, observers should monitor the legislative timeline, the outcomes of the ongoing probe, and the broader regulatory alignment with international standards on crypto assets and political finance. The coming months will reveal how aggressively the UK intends to constrain crypto contributions—and what that means for political actors, financial institutions, and the evolving crypto market ecosystem.

Source lines and attribution: The property transaction and timing were reported by Sky News. The political-probe context and related developments have been covered in Cointelegraph, including reports on regulatory discussions around crypto donations and related parliamentary activity. The parliamentary and government actions cited reflect ongoing UK oversight and policy reform discussions surrounding crypto-enabled political contributions.

SIREN price crashed 51.36% on May 14, closing at $0.5574 after opening above $1.14.

Summary

- SIREN price collapsed 51.36% on the daily chart on May 14, closing at $0.5574 after hitting an intraday high of $1.1619.

- The daily MACD histogram is rolling over sharply, with the MACD line curling toward an imminent bearish crossover below the signal line.

- If $0.50 fails to hold as daily support, the next meaningful demand zone does not appear until the $0.13 to $0.15 range from the March crash.

SIREN price dropped 51.36% on the daily chart on May 14, opening at $1.1455 and collapsing to a low of $0.5041 before closing at $0.5574 on the MEXC spot market.

The selloff pushed the BNB Chain token decisively below its SMA 20 at $0.8549 and SMA 50 at $0.8256, two levels that had held as dynamic support throughout late April and early May.

Volume on the session reached 6.03 million tokens, a significant spike relative to the muted candles that characterised the prior consolidation.

Heavy-volume breakdowns that close near the session low typically reflect motivated selling rather than thin-market noise, and the absence of any meaningful intraday recovery attempt reinforces that bear thesis.

MACD histogram rollover signals momentum shift

The daily MACD (12, 26, 9) is printing a clear warning. The MACD line sits at $0.0058 against a signal line at $0.0503, with the histogram contracting sharply from its mid-May peak.

A bearish crossover, where the MACD line crosses below the signal line, appears imminent on the current trajectory. As crypto.news documented in its May 8 coverage, SIREN’s chart had already printed upper wick distribution and lighter follow-through volume, an early warning that buying conviction was fading before this daily breakdown.

Analyst @SteveHODLs had warned on X that a failed breakout structure could send SIREN toward $0.60 and then $0.30, calling the setup a “fast unwind.” That target now looks relevant again given Thursday’s close.

Key levels, support, and price targets

The immediate support sits at the $0.50 round number, which aligns with the session low of $0.5041. A daily close below $0.50 would confirm the breakdown and open the door to the next structural demand zone in the $0.13 to $0.15 range, established during the March collapse from SIREN’s all-time high of $3.61. That level also represents the bull case invalidation for any near-term recovery.

On the upside, the former SMA cluster at $0.82 to $0.85 now acts as the first meaningful overhead resistance. Reclaiming the SMA 50 at $0.8256 on a daily close is the minimum requirement to shift structure back to neutral.

A close above the SMA 20 at $0.8549 would be needed to confirm the May 14 move as a temporary deviation rather than a structural breakdown.

On-chain context and supply risk

SIREN’s fragility has a documented structural cause. As crypto.news reported, one wallet cluster holds an estimated 88% of total supply at an average entry well below current prices,

creating asymmetric downside risk for other holders every time price recovers toward a profitable exit range. The same concentration that drove the March parabolic move is the structural overhang suppressing any sustained recovery.

SIREN markets itself as an AI agent protocol on BNB Chain, but its core products, including a DEX and a trading agent, remain listed as coming soon. Until delivery materialises, price action will continue to be driven by speculative positioning rather than protocol fundamentals.

If $0.50 fails to hold on a daily close, the path of least resistance points toward the $0.30 level, with the March low near $0.13 as the extended downside target.

Fuutura unveils non-custodial multi-asset trading protocol with identity attestation

Fuutura has launched a non-custodial trading protocol designed to support multiple asset types while incorporating identity attestation at the protocol layer. The move signals a continued effort in the crypto industry to reconcile decentralized trading models with regulatory and compliance needs without returning custody of user funds to centralized intermediaries.

Non-custodial trading protocols remove the need for users to hand private keys or funds to a third party, a model preferred by traders and institutions seeking to reduce counterparty risk. By building identity attestation into the protocol itself, Fuutura aims to provide a mechanism for verifying participants in a way that can support compliance processes while preserving user control over assets.

What this means for DeFi and regulated markets

Embedding identity attestation at the protocol level reflects broader industry trends toward programmable compliance. For regulators and compliance teams, having an auditable way to link on-chain activity to verified identifiers can assist in anti-money laundering and sanctions screening. For market participants, protocol-level identity could enable institutional counterparties to interact with decentralized markets with clearer operational controls.

At the same time, adding identity features to trading rails raises questions about privacy, data protection, and the potential for surveillance. The approach chosen for identity attestation will determine how much personally identifiable information is exposed on-chain, how attestations are issued and revoked, and who can verify those attestations. Balancing transparency for regulators with privacy for users remains a central design challenge.

Technical and operational considerations

Non-custodial, multi-asset trading involves smart contracts that manage order matching, settlement, and asset transfers while keeping private keys in users’ control. Layering identity attestation on top of that requires secure, verifiable credential systems and well-audited smart contracts to prevent new attack vectors.

Industry implementations of on-chain identity typically rely on cryptographic attestations, decentralized identifiers, or off-chain verifiers that attest to a user’s status. The precise implementation details will dictate interoperability with wallets, custody solutions and compliance tooling. Any protocol-level identity system must also account for key recovery, credential rotation and dispute resolution processes, which are critical for institutional adoption.

Market implications

If Fuutura’s protocol gains traction, it could appeal to institutional traders and liquidity providers who have been wary of purely permissionless venues. Protocol-level attestations may lower onboarding friction for counterparties that need to prove regulatory compliance while still wanting to retain custody of assets.

However, the success of such an approach depends on network effects and standards. For identity attestations to be useful across markets, they must be accepted by a range of counterparties and verifiers. That will likely require collaboration with identity providers, compliance vendors and other protocol teams to create interoperable attestations and common verification flows.

Risks and challenges

Adding identity features increases the protocol’s attack surface. Smart contract vulnerabilities, poorly designed attestation schemes, or insufficient privacy protections could expose users to new risks. Robust security audits and transparent governance will be important to build trust.

There is also regulatory uncertainty. Different jurisdictions have varying rules on identity verification, data retention and privacy. A protocol designed to be compliant in one market may face legal friction in another, complicating cross-border trading and liquidity aggregation.

Industry context and outlook

The launch of an identity-enabled, non-custodial trading protocol follows a wave of experimentation in decentralized finance where builders seek to make DeFi more palatable to traditional finance while retaining decentralization benefits. Firms and protocols are exploring hybrid models that combine cryptographic attestations with off-chain compliance checks to meet institutional requirements.

For market participants, the next questions are practical: will such protocols attract sufficient liquidity, how will they integrate with existing custody and prime brokerage services, and can they offer competitive fees and execution quality compared with centralized venues? The answers will determine whether identity-attested protocols become a niche compliance play or a mainstream market infrastructure innovation.

Fuutura’s announcement adds to an evolving debate about how to scale decentralized trading for a broader set of users. The coming months will show whether protocol-level identity attestation can deliver a workable compromise between regulatory expectations and the privacy and autonomy that underpin the decentralized finance movement.

Key takeaways:

- Fuutura launched a non-custodial, multi-asset trading protocol that integrates identity attestation at the protocol layer.

- Protocol-level identity can lower onboarding friction for regulated counterparties but raises privacy and security design challenges.

- Interoperability, strong security audits and cross-jurisdictional legal clarity will be critical for adoption.

Crypto World

BNB Chain Publishes Research Report Exploring Post-Quantum Cryptography Migration Path for BSC

[PRESS RELEASE – Dubai, UAE, May 14th, 2026]

14th of May, Dubai: BNB Chain, the leading L1 blockchain ecosystem, has published a new research report evaluating how BNB Smart Chain (BSC) could migrate core cryptographic systems to post-quantum alternatives in the future.

The report explores the implementation and performance implications of replacing traditional blockchain cryptography with quantum-resistant approaches, including ML-DSA-44 transaction signatures and pqSTARK aggregation for validator consensus.

While quantum computing is not yet capable of breaking production blockchain cryptography in real-world systems, the research reflects a forward-looking approach to infrastructure resilience and long-term network security.

The report evaluates several core areas of the BSC stack, including:

- Post-quantum transaction signature schemes

- Validator signature aggregation

- Transaction verification flows

- Public key storage

- Cross-region network performance under increased data loads

One of the key findings was that post-quantum readiness is technically achievable today, but comes with significant scalability trade-offs.

In testing:

- Transaction size increased from 110 B to ~2.5 KB

- Block size increased from ~110 KB to ~2 MB

- Native transfer TPS decreased from 4,973 to 2,997

The report found that the primary bottleneck was not signature verification performance itself, but the increase in transaction and block sizes, which created additional network propagation overhead across regions.

At the same time, pqSTARK aggregation remained highly efficient. Validator signatures were compressed at roughly 43:1, helping keep consensus-layer overhead manageable despite larger signature sizes.

The report also notes that several areas remain outside the current scope of evaluation, including post-quantum replacements for P2P handshakes and KZG commitments, both of which would require broader ecosystem coordination and additional research.

BNB Chain stated that the work is intended as research and evaluation, rather than a response to any immediate security threat.

The full report is available by clicking this link HERE.

About BNB Chain

BNB Chain is one of the largest and most active blockchain ecosystems in the world, supported by a global community of developers and users. With high throughput, low transaction costs, and full EVM compatibility, BNB Chain powers scalable applications across finance, gaming, and the broader Web3 economy. For more information, users can visit www.bnbchain.org.

The post BNB Chain Publishes Research Report Exploring Post-Quantum Cryptography Migration Path for BSC appeared first on CryptoPotato.

President Donald Trump logged 3,642 stock trades during Q1 2026, according to a 113-page OGE Form 278-T disclosure released this week. The filing reveals a sharp pivot away from the bond-heavy posture seen in earlier 2026 reports.

The volume averages roughly 60 trades per session. That pace breaks with a near-unbroken stretch of blind-trust arrangements stretching back to Lyndon B. Johnson.

A Break From Decades of Blind-Trust Practice

Most U.S. presidents since Johnson placed personal holdings into qualified blind trusts to limit conflicts. Jimmy Carter went further and liquidated his peanut farm. Barack Obama held Treasury notes and index funds. Joe Biden used a blind-trust arrangement during his term.

The current filing covers 113 pages. It lists individual purchases of Nvidia (NVDA), Microsoft (MSFT), Broadcom (AVGO), Amazon (AMZN), and Apple (AAPL).

Each fell in the $1 million to $5 million range. Hundreds of separate sales range from $15,000 up to $25 million per line item.

Treasury Secretary Scott Bessent has publicly backed a ban on congressional stock trading. Lawmakers in both parties have echoed that position.

The same arguments increasingly apply to executive-branch trading. The 2012 STOCK Act requires officials to disclose such trades but does not forbid them.

Holdings Mirror Administration Priorities

The portfolio leans toward sectors that have benefited from administration actions. Semiconductor positions in Nvidia, Broadcom, and AMD align with the White House push on domestic chip capacity.

The buys also overlap with a year of shifting tariffs aimed at Asian supply chains. Financials including JPMorgan, Goldman Sachs, and Visa overlap with the deregulatory posture pursued through 2026.

Buys of Coinbase (COIN), Robinhood (HOOD), and SoFi (SOFI) sit inside an active pro-crypto policy window. That window has seen executive orders, a federal Bitcoin reserve, and a Trump Accounts retirement program.

Robinhood serves as the program’s initial trustee. Critics flag the overlap as a conflict risk. The White House has defended the filings as full STOCK Act compliance.

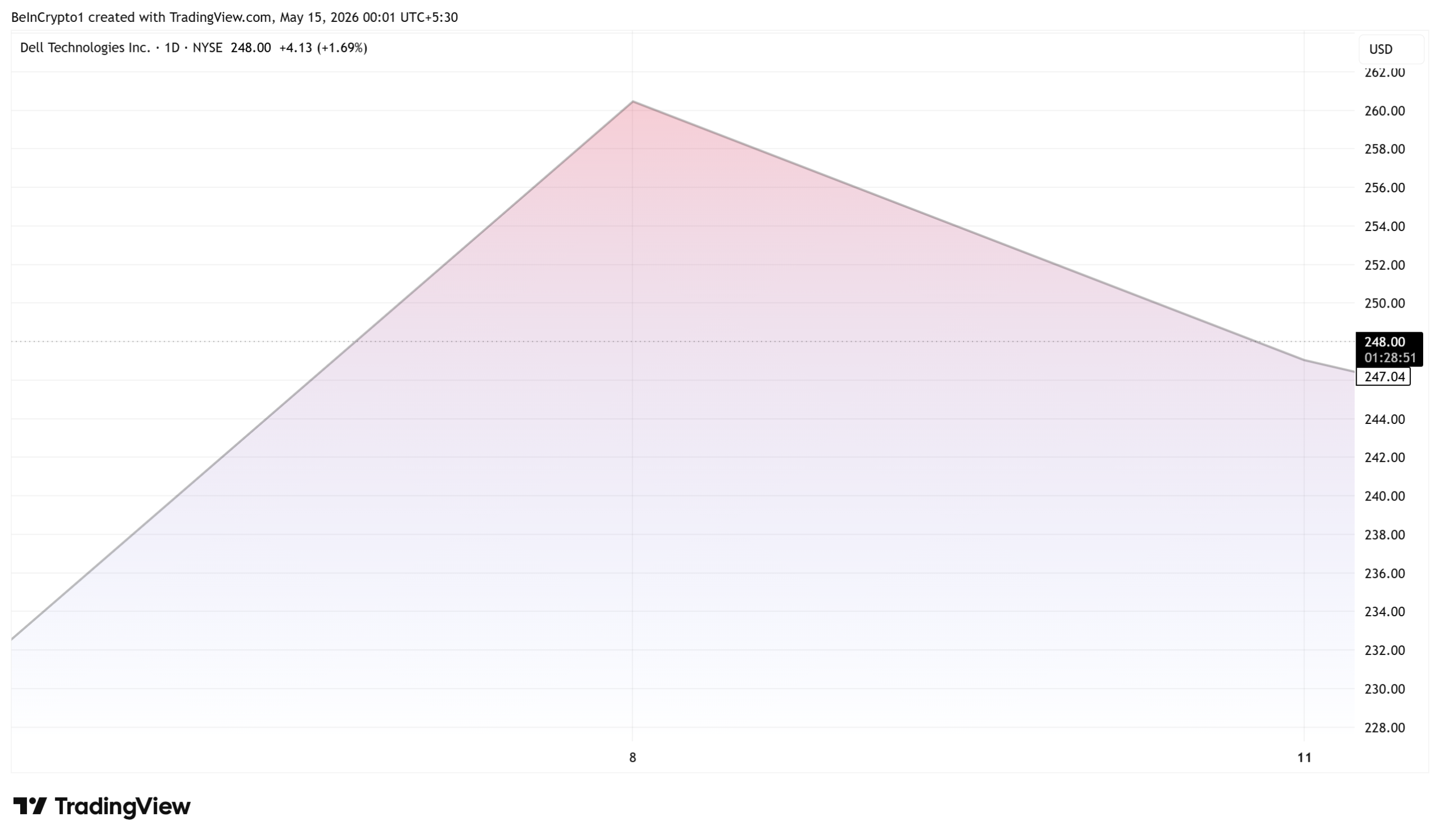

The most contested example involves Dell Technologies (DELL). Filings record multiple seven-figure DELL purchases beginning February 10. On May 8, the president publicly praised the company at a White House event.

The stock rose roughly 12% the same day. The Dell family separately pledged $6.25 billion to the Trump Accounts program in December 2025.

Whether the pattern triggers a formal review will depend on House and Senate ethics committees and the OGE.

The disclosure satisfies current reporting law, yet it widens an already active debate over executive-branch trading rules.

That debate gained urgency after years of scrutiny aimed at congressional portfolios.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Trump Logs 3,642 Stock Trades in Q1, Breaking Decades of Blind Trust Norms appeared first on BeInCrypto.

The U.S. Commodity Futures Trading Commission (CFTC) issued no-action relief from certain swap-related reporting and recordkeeping requirements for fully collateralized event contracts, easing compliance for prediction market venues and their clearing counterparts. The move aims to reduce administrative burden on designated contract markets (DCMs) and derivatives clearing organizations (DCOs) that list and clear such contracts, while preserving regulatory oversight where appropriate.

The CFTC’s market and clearing divisions stated they would not recommend enforcement against DCMs, DCOs, or their participants for not adhering to specified swap-related recordkeeping or for reporting covered transactions to swap data repositories. The agency framed event contracts on prediction markets as binary-outcome swaps in theory, yet described them as instruments that often resemble futures or futures options in practice, suggesting they may be reported to the CFTC in a manner akin to futures. The agency also named 19 platforms—including Kalshi, Polymaket, and Gemini Titan—and indicated that other firms seeking to list similar contracts could request a no-action letter.

The no-action relief responds to multiple requests from market operators that list and clear event contracts and the CFTC indicated it expects additional similar requests in the future. The relief could meaningfully reduce compliance complexity for CFTC-regulated prediction-market venues as the agency continues to defend its jurisdiction in the face of state-level gambling regulation challenges.

According to Cointelegraph, the move arrives amid a broader federal–state dispute over how these markets should be regulated—whether as derivatives under federal law or as gambling products regulated by state authorities. The CFTC has been advancing its view of exclusive federal jurisdiction in several high-profile matters, underscoring the tension between federal regulation and state laws on prediction markets.

Key takeaways

- No-action relief: The CFTC will not pursue enforcement against DCMs, DCOs, or their participants for certain swap-related recordkeeping and swap-data-reporting obligations in relation to fully collateralized event contracts.

- Scope and reporting: Event contracts—though binary by design—are treated as swaps in theory, but the CFTC indicates they can be listed and reported with mechanisms similar to futures and futures options.

- Platform coverage: The relief names 19 platforms, including Kalshi, Polymaket, and Gemini Titan, with the option for others to seek no-action from the agency.

- Regulatory posture: The relief reflects ongoing efforts to reconcile federal derivatives regulation with state gambling authorities, a conflict that includes lawsuits and amicus filings in federal courts.

No-action relief: scope and rationale

The CFTC’s writedown of enforcement risk centers on fully collateralized event contracts listed on designated markets. By carving out a relief path, the agency acknowledges that many of these contracts function in ways more akin to futures and options than to traditional swaps, despite their binary-event underpinnings. The relief allows listing venues and clearinghouses to maintain listing and clearing operations without triggering automatic enforcement for specific swap-recordkeeping deficiencies or for failing to report certain events to swap data repositories.

Key platforms identified by the agency—such as Kalshi, Polymaket, and Gemini Titan—are included in the relief’s scope, which also clarifies that other platforms seeking to list similar contracts may apply for no-action relief. The intent appears to be reducing administrative friction for CFTC-regulated prediction-market operators while preserving the agency’s oversight posture should issues arise in the future.

The development is framed as a practical accommodation in response to a wave of compliance requests from DCMs and DCOs that list and clear event contracts. The CFTC signaled it expects further such requests, suggesting a continued alignment between enforcement discretion and market development in the prediction-market space.

Regulatory context and enforcement posture

At a broader policy level, the no-action relief sits within a contentious regulatory landscape where the CFTC seeks exclusive jurisdiction over prediction markets, but state authorities have pursued gambling-regulation actions against the same platforms. The agency has engaged in high-stakes litigation and court filings to defend its authority, including an amicus brief in the Sixth Circuit aimed at limiting state actions perceived as intruding on federally regulated markets. Ohio’s attempts to regulate or restrict sports-event contracts have been a focal point of these disputes, resulting in Kalshi pursuing a federal court challenge that has progressed through the courts with varying outcomes.

The CFTC’s March staff advisory that categorized event contracts on prediction markets as a distinct financial asset class adds another layer to the regulatory framework, signaling that the agency views these instruments through a broadly defined, potentially cross-cutting lens. In parallel, the agency’s forthcoming rulemaking—shortly after soliciting public comments—has drawn a wide range of responses. The agency reported receiving more than 1,500 comments in May on a March-published rule proposal intended to modify or introduce new regulations for event contracts. Reactions have been mixed: some state regulators pressed for stronger enforcement or tighter controls, while notable investors and industry participants—including venture firms—argued that federal regulation is essential to preserving market access and preventing a patchwork of state rules from undermining the sector’s integrity and liquidity.

In this climate, the CFTC’s no-action relief represents a tactical element of a broader federal strategy to codify a predictable regulatory baseline for prediction markets, even as jurisdictional debates persist across the states and the courts. The agency’s actions are being watched by market operators, financial institutions, and compliance teams for how future no-action letters may shape listing, clearing, licensing, and cross-border operations in a space that remains subject to evolving regulatory interpretation.

Operational implications for platforms and market participants

For prediction-market venues and their banking and clearing partners, the relief could lower the ongoing compliance overhead associated with swap-data reporting and recordkeeping. By differentiating event contracts from conventional swaps in practical reporting terms and pointing to futures-like treatment for listing and reporting, the CFTC signals a potential path to streamlined regulatory oversight without loosening safeguards around market integrity, transparency, or customer protection.

For operators like Kalshi, Polymarket US, and Gemini Titan, the development underscores the importance of clear regulatory delineations between federal derivatives law and state gambling statutes. The relief could influence licensing strategies, reporting frameworks, and the design of collateral requirements, all within the context of a broader push for consistent enforcement and improved market access across jurisdictions. The agency’s emphasis on prospective no-action letters suggests operators should anticipate further regulatory interactions as the rulemaking process unfolds and as states sharpen their policy positions on prediction markets.

From a compliance standpoint, firms should monitor the evolving guidance around what constitutes a reportable event, how event contracts should be classified for filing to swap-data repositories, and what documentation supports a no-action determination. The evolving posture of enforcement discretion—paired with ongoing litigation and rulemaking—implies that firms must maintain robust internal governance, particularly around data retention, event-logging, and cross-border operational risks that arise when state and federal authorities diverge in their regulatory expectations.

Closing perspective: The CFTC’s no-action relief for fully collateralized event contracts marks a deliberate attempt to balance market development with regulatory oversight. As federal and state authorities continue to navigate the jurisdictional questions surrounding prediction markets, market participants should prepare for evolving requirements, potential licensing changes, and continued policy debate that will influence how these platforms operate within the U.S. financial-legal framework.

Update May 14, 2:45 pm UTC: This article has been updated to include comments from Katie Haries, head of policy for Europe at Coinbase.

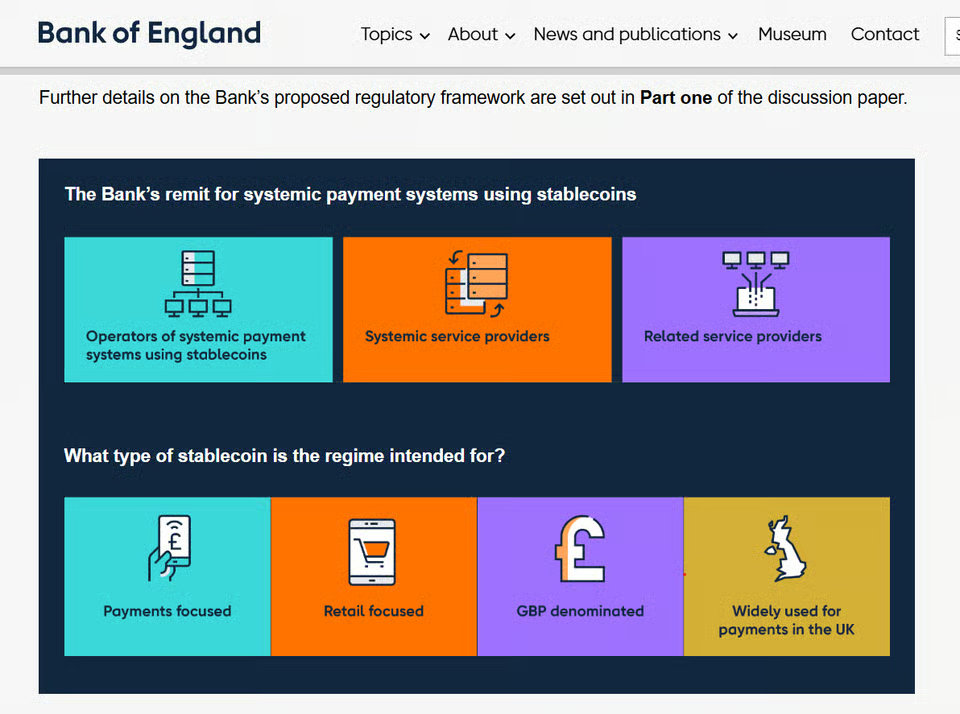

The Bank of England (BoE) is reconsidering parts of its proposed regime for pound sterling stablecoins after digital asset companies warned that holding caps and reserve requirements could stifle adoption and make UK-issued tokens uneconomic.

The central bank is looking at alternatives to temporary caps on how many stablecoins individuals and businesses can hold, and is examining whether its requirement that at least 40% of backing assets be held as non-interest-bearing deposits at the BoE is overly conservative, Deputy Governor Sarah Breeden told the Financial Times.

The rethink comes as the UK government and regulators try to position Britain as a competitive hub for digital assets while containing risks to bank funding and financial stability. Sterling-pegged tokens currently make up a tiny fraction of the roughly $300 billion global stablecoin market, which remains dominated by dollar-based issuers.

The BoE set out detailed ownership limits in its November 2025 consultation paper on a proposed regulatory regime for sterling-denominated systemic stablecoins, building on options first aired in a 2023 discussion paper.

Under that proposal, individuals would be restricted to holding up to 20,000 pounds (roughly $27,000) of a given UK stablecoin, while businesses would be capped at roughly $13.5 million, at least during an initial transition period.

Stablecoins Discussion Paper, 2023. Source: Bank of England

The central bank argued that limits were needed to avoid a sudden outflow of deposits from commercial banks into new forms of “tokenised” money if a large stablecoin were rapidly adopted for payments.

Related: Bank of England chief says global stablecoin rules will ‘wrestle’ with US

Industry groups and prospective issuers countered that the caps were operationally cumbersome, hard to supervise across platforms, and could deter serious institutional use of regulated UK stablecoins in areas like corporate treasury, payroll and settlement.

BoE rethinks stablecoin caps after pushback

Breeden has been one of the most cautious voices on stablecoins within the BoE. In November 2025, she warned that diluting the rules too far could damage financial stability, stressing that stablecoins are money-like instruments that must be at least as safe and robust as existing payments infrastructure.

At the time, she backed stringent liquidity requirements that would force stablecoin issuers to park large portions of their reserves at the central bank and hold the rest in high-quality liquid securities such as UK government bonds.

Law firms and potential issuers argue that such a structure would significantly compress margins and make UK stablecoin issuance far less attractive than operating under the United States or European Union regimes.

UK hunts for middle ground on stablecoins

The shift in tone highlights how UK policymakers are still feeling their way toward a middle ground on stablecoins as global approaches diverge.

In January, UK lawmakers opened an inquiry into how best to oversee fiat-backed tokens, taking evidence from industry participants such as Coinbase and Innovate Finance, while the BoE and Treasury continue to refine a framework intended to sit alongside broader crypto rules and potential digital pound plans.

Katie Haries, head of policy for Europe at Coinbase, told Cointelegraph it’s an important signal the BoE is prepared to revisit its stablecoin proposals.

“We’ve said for a long time that a cap on stablecoin holdings is a cap on innovation,” she said, with “real and significant risks for UK competitiveness.” She added that creating a regime where stablecoins can succeed and benefit users is “exactly the right ambition,” and something the crypto industry and everyday people are asking for.

A more flexible approach to caps and backing requirements could determine whether systemic GBP stablecoins emerge as serious competitors to dollar-pegged rivals in cross-border payments and onshore crypto markets, or whether activity remains concentrated in jurisdictions seen as more accommodating.

Magazine: Singapore isn’t a ‘crypto hub’ — it’s something better: StraitsX CEO

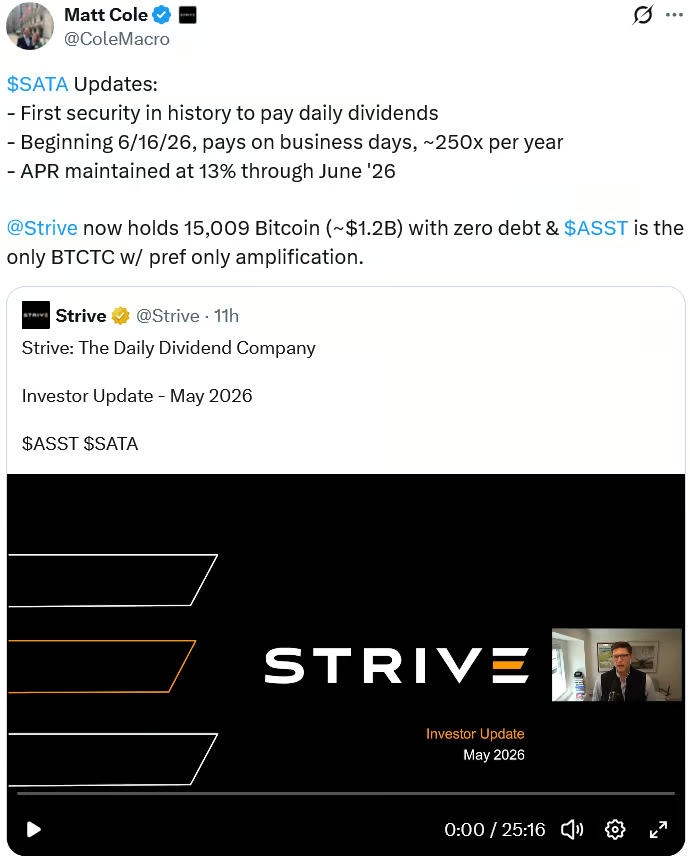

Shares in Bitcoin-focused Strive closed 5.8% higher on Thursday after the company said it will become a “Daily Dividend Company” and revealed it eliminated all debt in the first quarter of 2026.

The Vivek Ramaswamy-founded company said the Variable Rate Series A Perpetual Preferred Stock, ticker SATA, will start paying dividends every business day beginning June 16 at a current annual dividend rate of 13%. The payouts are funded by income generated from the company’s Bitcoin treasury strategy.

Strive CEO Matt Cole said the move will make it the first public company to offer daily dividends, expanding on a similar playbook adopted by Michael Saylor’s Strategy, which has relied on perpetual preferred stock offerings such as Stretch (STRC) to fund its Bitcoin purchases while paying investors every two weeks.

“The rate at which innovation is happening in the digital credit space is fascinating to behold,” said Bitcoin For Corporations contributor Adam Livingston. Strategy executive chairman Michael Saylor called the daily dividends “impressive.”

Strive’s daily dividends mark another example of a Bitcoin treasury firm moving beyond a simple buy-and-hold strategy to remain competitive in the bear market.

This comes as Strive reported an unrealized net loss of $265.9 million for Q1. The company attributed the loss to a decrease in the fair market value of its Bitcoin holdings as Bitcoin fell 23% during the quarter.

Source: Matt Cole

Strive is now operating debt-free

Strive said it ended the quarter with no outstanding debt after buying back the remainder of its long-term notes.

“Today, Strive stands debt-free, with zero margin requirements, and zero encumbered Bitcoin; a balance sheet purpose-built to thrive through Bitcoin volatility.”

Strive shares flip to positive year-to-date

Strive (ASST) shares rose 5.8% to $17.70 Thursday following the company’s earnings statement and gained another 0.73% in after-hours trading.

The company is now up 2.43% year to date but still down more than 81% over the past year.

Related: Bitcoin trades at a ‘discount’ on Coinbase: Is a $76K retest next?

Strive ended Q1 with 13,628 Bitcoin, including 5,048 Bitcoin acquired through its purchase of Semler Scientific during the quarter. It has since added another 1,381 Bitcoin, bringing its total to 15,009 Bitcoin worth $1.22 billion at current prices.

On Wednesday, another Bitcoin company, Nakamoto, rose 2.7% after reporting that its revenue increased 500% quarter-on-quarter in Q1 to $2.7 million, with $1.1 million of that coming from a new strategy of using its Bitcoin holdings as collateral to earn yield.

Meanwhile, Q1 results from some of the larger players in the crypto industry were a mixed bag.

Stablecoin issuer Circle rallied 15% after reporting its revenue rose 20% quarter-on-quarter to $694 million, beating estimates, while crypto exchange Coinbase’s shares slid after it reported a steep first-quarter loss with a 21% fall in revenue to $1.4 billion. Robinhood also dipped 9.4% after its Q1 revenue also missed analyst expectations.

Magazine: eToro founder timed Bitcoin top perfectly due to belief in 4 year cycles

Dune Analytics is cutting 25% of its workforce as cofounder Fredrik Haga restructures the platform around AI agents and institutional adoption of onchain finance.

The May 14 post from Haga also drew a sharp reply from Surf cofounder Ryan Li, who argued crypto research now demands infrastructure built for AI agents rather than human-operated dashboards.

Restructure Targets AI and Institutional Clients

Haga said Dune is preserving its end-to-end data stack while letting go of strong performers he is openly recommending to other hiring firms.

The company has raised roughly $79 million in total funding, including a $69.4 million Series B in 2022, and Haga said it remains well capitalized.

The pivot leans on Dune MCP, an open-standard server launched in March 2026 that lets AI agents query the platform’s data warehouse through natural language.

Twelve tools cover table discovery, query execution, and visualization across more than 100 chains. Dune also recently released a dbt Connector for teams building on-chain data pipelines.

Haga said Dune already powers most leading crypto companies and is now expanding white-glove service to financial institutions tokenizing stocks, bonds, and commodities.

Surf Challenges the Dashboard Era

Li, who said he was previously a heavy Dune user, used his reply to position Surf as a purpose-built alternative.

“However, crypto research has evolved and operating in the AI era demands infrastructure built for agents, not humans clicking through dashboards. We need fast query engines, reliable SQL, structured outputs. At Surf, we’ve spent Q1 building an end-to-end crypto data stack purpose-built for AI agents,” he stated.

Surf raised $15 million in December 2025 from Pantera Capital, Coinbase Ventures, and DCG.

The exchange marks an escalation in the crypto data race as established platforms compete with agent-native entrants for AI research workflows.

The post Dune Cuts 25% of Staff to Focus on AI Agents and Institutional On-chain Data appeared first on BeInCrypto.

Bitcoin mining has always been a margins business, now more so than ever. The difference between profit and loss can come down to electricity prices, machine performance, pool fees, or even how many shares get rejected before they reach the network.

That pressure became more serious after the 2024 Bitcoin halving. The block reward dropped, while mining difficulty in 2026 has stayed above 135T. For many miners, the electricity cost alone to mine one Bitcoin has moved above $74,000.

That leaves less room for waste, and a business can quickly become unprofitable. This is the problem EMCD and Vnish are trying to address.

The new partnership brings together EMCD’s mining pool infrastructure with Vnish’s firmware technology, which holds a 26.4% global market share.

The goal is to help miners find where they are losing money and improve profitability without simply buying more machines.

At Consensus 2026 in Miami, EMCD founder and CEO Michael Jerlis described a market where miners need more practical support from infrastructure providers.

“Before, pools and machine manufacturers were just service providers,” Jerlis said. “Now, it looks like they became more partners with the miners.”

Where Bitcoin Miners Are Losing Money

The losses often start at the machine level.

Factory firmware usually applies the same voltage settings across ASIC chips. The problem is that chips do not perform equally. Stronger chips may be held back, while weaker chips can overheat. According to the partnership materials, this can leave up to 25% of potential hardware performance unused.

Then come pool-related costs. A pool fee difference between 1.5% and 4% may seem small, but over a year, that gap can eat into a meaningful share of a miner’s gross output.

Rejected shares create another quiet drain. When the latency to pool servers is high, miners still spend electricity on calculations that do not get accepted.

EMCD and Vnish estimate that this can possibly reduce monthly income by another 2% to 5%.

Jerlis summed up the pressure clearly.

“All miners have the same troubles,” he said, pointing to operating costs, electricity prices, software providers, and equipment sellers.

How the Partnership Helps

The EMCD–Vnish service focuses on practical fixes rather than broad promises. It includes hashboard diagnostics, tuning, network-loss reduction, mining optimization steps, and audits from EMCD and Vnish experts.

In simple terms, the service looks at where a miner’s setup is leaking performance, then gives them clear steps to improve it.

Firmware is a major part of that. Vnish can help tune ASICs more precisely, improve hardware performance, and reduce wasted power. For miners operating close to breakeven, even small gains can matter.

“Custom firmware helps to cut power consumption,” Jerlis said.

The pool side matters too. Jerlis said EMCD is working on ways to improve how miners connect to pool servers, including better routing and tools to reduce rejected shares.

That matters because mining rewards depend on accepted work. Electricity spent on rejected work is simply lost money.

Jerlis said the partnership is designed to improve miner profitability from several angles at once.

“Together we will cut our fees and give miners more profitability,” he said.

A More Hands-On Mining Model

After the halving, miners are under pressure to operate with more discipline. Cheaper power still matters, but it is no longer enough by itself. Machine tuning, firmware, pool reliability, latency, and support all affect the final result.

Jerlis said EMCD was built around this need for direct miner support. When the company started, many miners struggled to reach pool operators when something went wrong.

EMCD’s early advantage was 24-hour support. The Vnish partnership extends that same approach into optimization.

“We need to help them to acquire more Bitcoins, to tune their machines, to spend less money,” Jerlis said.

That is the core story. The EMCD–Vnish partnership is about helping miners survive a market where small inefficiencies now have a much higher cost.

The post EMCD CEO: Bitcoin Miners Can Become Profitable Again appeared first on BeInCrypto.

The US Commodity Futures Trading Commission’s (CFTC) market and clearing divisions issued no-action relief for fully collateralized event contracts, easing certain swap data reporting and recordkeeping obligations for prediction market operators and clearing organizations.

The divisions said Wednesday that they will not recommend enforcement against designated contract markets (DCMs), derivatives clearing organizations (DCOs), or their participants for failing to comply with specified swap-related recordkeeping requirements or for failing to report covered transactions to swap data repositories.

Event contracts on prediction markets technically qualify as “swaps” as they are based on binary events. However, the letter argued that similar contracts are listed for trade by DCMs and have more similar characteristics to futures and options on futures, hence enabling firms to report certain events contracts directly to the CFTC.

The letter listed 19 platforms, including Polymaket, Kalshi and Gemini Titan. It added that companies seeking to list similar contracts may request a no-action letter from the CFTC.

The CFTC said the no-action letter comes in response to numerous requests from DCMs and DCOs that list and clear event contracts and said it anticipates more similar requests.

The move could reduce compliance complexity for CFTC-regulated prediction market venues, including Kalshi and Polymarket US as the agency continues to defend its jurisdiction against state gambling regulators.

The no-action letter comes as prediction markets sit at the center of a widening federal-state fight over whether sports and other event contracts should be regulated as derivatives by the CFTC or as gambling products by state authorities. The agency filed an amicus brief in the Sixth Circuit Court of Appeals on Tuesday, arguing that Ohio’s actions intrude on federally regulated markets after it ordered Kalshi to halt sports event contracts in the state last year.

Kalshi sued Ohio lawmakers in October 2025, requesting that the federal court stop the Ohio Casino Control Commission and state attorney general from taking action, but the motion was denied in court in March, leading Kalshi to appeal the decision.

CFTC no-action letter on prediction markets. Source: CFTC.gov

CFTC pushes for exclusive jurisdiction over prediction markets

The CFTC has multiple ongoing disputes with state lawmakers over prediction market jurisdiction. It sued five states in a bid to cement its authority over prediction markets, including lawmakers in Wisconsin, New York, Arizona, Connecticut and Illinois.

Earlier in May, the CFTC said it received over 1,500 responses on a rule it proposed in March that would allow it to amend or issue new regulations for event contracts on prediction markets.

The responses were mixed, with some state regulators calling for a stricter crackdown on prediction markets, while others, such as venture capital firm a16z, sided with the CFTC, arguing that state crackdowns on these platforms conflict with federal law and damage market access for ordinary users.

Related: Kalshi, Polymarket face trading halt in Nevada after court rulings

On March 12, the CFTC issued a staff advisory classifying event contracts on prediction markets as a “financial asset class,” Cointelegraph reported.

Earlier in February, CFTC Chair Michael Selig publicly reiterated claims that the CFTC had “exclusive jurisdiction” over prediction markets.

Magazine: Inside a 30,000 phone bot farm stealing crypto airdrops from real users

Sony shows off AI-touched Xperia 1 VIII camera samples. It’s an epic self-own that I can’t digest

Forget Nolan’s The Odyssey, We Already Have A Killer Greek Epic

Netflix’s The Crash: Inside Mackenzie Shirilla’s ‘posessive’ romance with boyfriend before murder

Manchester United reach agreement with Casemiro over contract clause amid transfer speculation

US brings back mandatory military draft registration

Steven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Crypto World7 days ago

Crypto World7 days agoHarrisX Poll Found 52% of Registered Voters Support the CLARITY Act

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Marianne Dress

-

Fashion3 days ago

Fashion3 days agoCoffee Break: Travel Steam Iron

-

Fashion4 days ago

Fashion4 days agoWhat to Know Before Buying a Curling Wand or Curling Iron

-

Tech5 days ago

Tech5 days agoAuto Enthusiast Carves Functional Two-Stroke Engine from Solid Metal

-

Politics3 days ago

Politics3 days agoWhat to expect when you’re expecting a budget

-

Business6 days ago

Business6 days agoIgnore market noise, India’s long-term story intact, say D-Street bulls Ramesh Damani and Sunil Singhania

-

Politics6 days ago

Politics6 days agoPolitics Home Article | Starmer Enters The Danger Zone

-

Tech4 days ago

Tech4 days agoGM Agrees To Pay $12.75 Million To Settle California Lawsuit Over Misuse Of Customers’ Driving Data

-

Crypto World6 days ago

Crypto World6 days agoPROS explodes 48% as Upbit and Bithumb listings ignite demand

-

Crypto World5 days ago

Crypto World5 days agoCZ says US crypto rivals tried to block Trump pardon

-

Entertainment6 days ago

Entertainment6 days agoYNW Melly Denied Bond Again Ahead Of Double Murder Retrial

-

Tech3 days ago

Tech3 days agoGM agrees to $12.75M California settlement over sale of drivers’ data

-

Sports7 days ago

Sports7 days agoBayern Munich vs PSG UEFA Champions League SF2 live match time, streaming | Football News

-

Tech7 days ago

The Most Exciting Apple Products In The Pipeline For 2026 And Beyond

-

Crypto World6 days ago

The Hantavirus Danger: Can a Potential Outbreak Spark a New Meme Coin Frenzy?

-

Crypto World6 days ago

Crypto World6 days agoKraken Parent Seeks OCC Charter, Signaling Regulated Banking Access

-

Politics7 days ago

Politics7 days agoDavid Attenborough ‘Overwhelmed’ By Love Shown Ahead Of 100th Birthday

-

Sports6 days ago

Sports6 days agoAfter Waka Waka, Shakira now drops first teaser for FIFA WC 2026 song | FIFA World Cup 2022

-

Entertainment7 days ago

How “Grey's Anatomy” bid farewell to Owen and Teddy — and whether they end up together

You must be logged in to post a comment Login