Crypto World

Google Introduces Gemini 3.5 Flash for Smarter Search Results

TLDR

- Google introduced a redesigned Search experience powered by Gemini 3.5 Flash at I O 2026.

- The new interface supports longer and more conversational user queries instead of short keywords.

- Google added an AI-powered autocomplete that suggests refined and follow-up questions in real time.

- AI Overviews now appear more consistently and provide summarized answers at the top of results.

- Users can move between AI summaries and chatbot-style interactions without leaving the search page.

Google introduced a redesigned Search platform powered by Gemini 3.5 Flash at I/O 2026. The update blends traditional search with AI-generated responses and conversational features. The company confirmed that the rollout aims to shift user behavior toward natural language queries.

Google presented the updated interface as part of its broader Gemini strategy across products and Android systems. The company emphasized faster responses and improved context handling through the new model. Robby Stein said users will “reliably” see AI Overviews for conversational queries.

Google Expands Conversational Search and AI Summaries

Google redesigned the search box to support longer and more detailed user queries. The interface now encourages full questions instead of short keyword searches. As a result, users can ask complex queries like protocol explanations and receive structured answers.

The company also introduced AI-powered autocomplete that suggests refined questions in real time. This system builds on user intent and offers follow-up prompts during typing. Google stated that this feature helps guide users toward more complete and relevant searches.

AI Overviews remain central to the new experience and appear at the top of results pages. These summaries compile information from multiple sources into a single response. Stein explained that the system connects directly to AI Mode for extended conversations.

Users can now transition between summaries and chatbot interactions without leaving the search page. This integration allows continuous dialogue powered by Gemini 3.5 Flash. Google positioned the model as faster and more efficient than earlier versions.

Gemini Model Powers Deeper Integration Across Devices

Google confirmed that Gemini 3.5 Flash supports both cloud and on-device processing. Some AI tasks will now run locally on Android devices. This approach reduces latency and improves performance for certain features.

The company linked this update to its broader Gemini Intelligence initiative. It aims to embed AI capabilities across mobile ecosystems and services. Google also highlighted ongoing work on open models for developers.

The search redesign aligns with Google’s focus on unified AI experiences across platforms. The company plans to expand these capabilities in future updates. Current deployments began following the I/O announcement.

Google did not disclose exact rollout timelines for all regions. However, it confirmed gradual availability across devices and markets. The company continues to test features through limited releases.

Changes in Search Structure Affect Information Visibility

Google confirmed that AI Overviews synthesize content from multiple indexed sources. The system selects key data points and presents a summarized response. This process reduces reliance on traditional link-based navigation.

The company acknowledged that users may interact less with individual websites. AI-generated answers often provide direct responses without requiring clicks. Google did not provide specific metrics on traffic changes.

Platforms that provide structured data may still contribute to AI summaries. However, their visibility depends on how Gemini selects information. Google continues refining its ranking and synthesis systems.

Strike, the Bitcoin financial services firm led by Jack Mallers, has introduced a new “volatility-proof” Bitcoin-backed loan designed to reduce the risk of margin calls and forced liquidations during sharp market drops. The trade-off is cost and scheduling discipline: the program carries a higher interest rate, a shorter loan term, and an expectation that borrowers make payments on time.

In a Tuesday announcement, Mallers said the product was built in response to customer feedback on Strike’s earlier Bitcoin loan offering launched in May 2025—an initial rollout that coincided with a severe drawdown. During that period, Bitcoin fell 54% from peak to trough, and many borrowers were liquidated.

Key takeaways

- Strike’s new loans aim to remove margin calls and price-triggered liquidations, limiting forced selling during downturns.

- The mechanism requires borrowers to stay current; missed payments can still lead Strike to sell collateral.

- Terms are shorter than Strike’s standard product and the interest rate is higher—up to an APR range around 10.7% to 14.2% based on Strike’s disclosed structure.

- The maximum initial loan-to-value ratio is 45%, which lowers borrowing capacity relative to the collateral posted.

A product aimed at breaking the “volatility-to-liquidation” link

In his remarks, Mallers summarized the core design goal: “No margin calls. No price liquidations. No matter how far bitcoin falls, your bitcoin doesn’t move.” He emphasized that the protection comes with conditions—namely paying on time and accepting a higher cost and shorter term than Strike’s standard loans.

Strike’s pitch matters because the industry has spent years trying to broaden Bitcoin’s utility beyond holding and transfers. Yet adoption of crypto-backed lending has lagged, largely due to uncertainty around how quickly collateral can be liquidated when markets move. A June report from crypto lending platform Ledn—referenced in the announcement—found that 88% of surveyed crypto investors would consider crypto-backed loans, but only 14% actually use them, citing a “crypto collateral gap” driven by volatility and confidence issues.

Volatility has been a persistent challenge for Bitcoin loans. Mallers pointed out that Bitcoin has fallen by 30% or more in 10 of the past 12 years, and that drawdowns of 50% or more have occurred four times since 2014. The new loan structure attempts to address a key behavioral and structural concern: that borrowers can be forced to sell when prices drop, even if they would be able to manage debt payments under a different risk framework.

How Strike’s “volatility-proof” structure changes borrowing terms

According to Strike’s details, the volatility-proof loans have a maximum initial loan-to-value ratio of 45%. That means a borrower posting $100,000 in Bitcoin could borrow up to $45,000 under this framework. Strike also disclosed that the APR is meaningfully higher than for its standard Bitcoin loan product, with an additional charge intended to support extra hedging designed to protect the system.

Strike’s standard Bitcoin loans carry an annual percentage rate between 7.75% and 11.25%. The new product is described as 2.95 percentage points higher than the standard offering, putting the volatility-proof APR roughly in the 10.7% to 14.2% range. Mallers characterized the approach as an exchange: “If you’re OK with a slightly shorter term and a little bit higher of a fee, there is no price move that can liquidate you.”

The company also pointed to Bitcoin’s recent market backdrop to frame why the change was necessary. Over the past year, Bitcoin has dropped 54% from its all-time high of $126,080 in October to $58,190 on June 25, according to the figures cited in the announcement.

Other market participants highlighted the product’s potential benefit while still acknowledging the cost. Investor Fred Krueger, responding on X, said the loan model could address “one of Bitcoin’s biggest structural problems: forced selling during market crashes,” arguing that defaults would be tied more to borrowers’ ability to service debt rather than temporary price swings. Vibes Capital Management executive chairman Rob Topping also welcomed the liquidity angle for users who want near-term cash without liquidation risk, while calling the 14% APR expensive.

Payments still matter: the rules shift from price risk to default risk

Strike’s volatility-proof label is not absolute. The company’s approach redirects risk away from price-based liquidations and toward payment behavior. Mallers said that if a borrower misses a payment, they have 10 days to catch up or contact Strike to explain their financial situation.

If Strike does not hear from the borrower after that 10-day period, the company may begin liquidating the borrower’s Bitcoin collateral to cover the overdue amount. Mallers underscored this distinction by stating that the product is designed to be “volatility-proof,” not “liquidation-proof,” adding that if clients appear to be “doing a hit-and-run,” Strike may have to sell some collateral.

The loans are available in most U.S. states and can be taken out under both personal and business names. Strike’s disclosed minimums vary by state and by loan type, with personal loans offered from $10,000 and certain business loans available as low as $5,000. The company said the proceeds can be used for new borrowing, refinancing, or consolidating existing obligations.

Where this fits in a wider lending market

Strike is not alone in offering Bitcoin-backed loans; other participants mentioned alongside Strike include Binance, Coinbase, Nexo, and Xapo Bank. However, the central question for borrowers remains the same across providers: how to access liquidity without being forced to sell during sharp market declines.

By setting a lower maximum loan-to-value ratio (45%) and charging a higher APR to fund additional hedging, Strike is attempting to engineer a path where collateral value volatility does not automatically translate into liquidation. For investors and traders, this shift could be meaningful in managing cash-flow stress—especially during periods where paying down debt remains feasible, but the collateral drawdown would otherwise trigger margin calls.

Borrowers considering the new program should watch two things going forward: how consistently Strike enforces the payment schedule across cases, and whether the company’s higher APR and tighter loan framework materially improve outcomes relative to its first loan product during prolonged volatility. The effectiveness of a volatility-proof model ultimately depends on how well it balances hedging costs with real-world borrower repayment behavior.

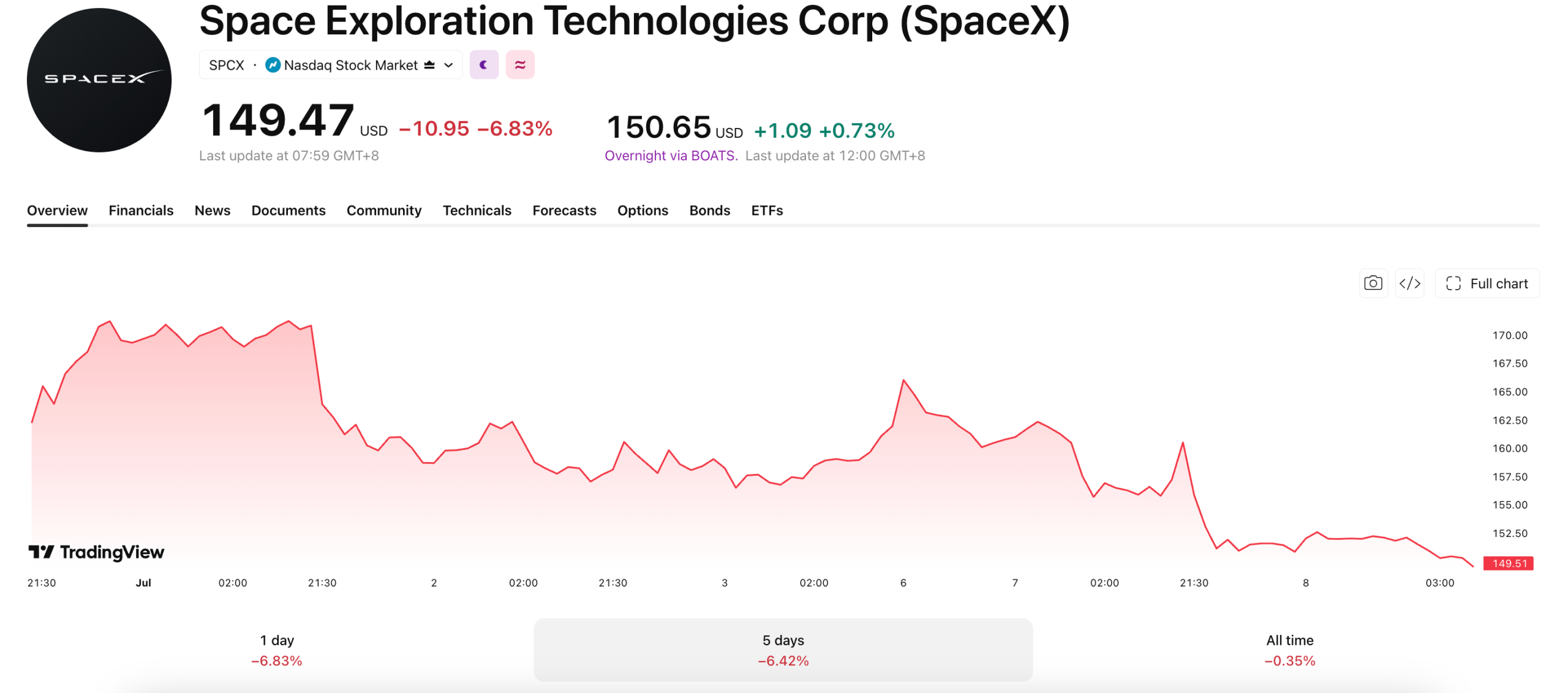

SpaceX’s price targets now span a massive range. Wall Street analysts set targets from $131 to $800 as the IPO quiet period ended.

Nineteen analysts published new ratings once the quiet period lifted for 23 underwriting banks behind SpaceX’s IPO. The moves coincided with SpaceX’s inclusion in the Nasdaq-100 index on Tuesday, July 7. The median target sits at around $250, a 56% jump from Monday’s closing price.

The High End of the Range

Raymond James analyst Brian Gesuale set the Street-high target at $800. He compared SpaceX to railroads and the internet as foundational infrastructure.

Citi’s John Godyn rated the stock a buy at $200. He called it a step toward a longer-term $900 target tied to Starship.

Deutsche Bank’s Edison Yu and J.P. Morgan’s Doug Anmuth issued buy-equivalent ratings at $255 and $225. Morgan Stanley’s Adam Jonas set a $300 base case. His range spans a $600 bull case and a $75 bear case.

Fourteen of the 19 targets clustered between $200 and $250. That optimism follows heavy institutional demand. BlackRock placed a $5 billion order ahead of the company’s $2 trillion debut last month.

The Low End of the Range

MoffettNathanson’s Julie Zhu set the Street-low target at $131, the sole holdout with a neutral rating that implies 18% downside. The firm called SpaceX’s $30 trillion addressable market estimate “absurd.” It also questioned Musk’s plan to deploy 100 gigawatts of orbital compute by 2029.

“There is simply no credible financial model that can support what is at the time of this writing a roughly $2 trillion valuation. Our own certainly does not.”

Zhu’s team stopped short of a sell rating. The analysts argue investors are pricing SpaceX as an option on businesses that don’t exist yet. It flagged regulatory scrutiny of SpaceX’s launch dominance as the bigger long-term risk. That risk remains years away, the firm said.

The nearly $700 gap between the highest and lowest targets leaves SpaceX’s volatile stock at a crossroads. Starship’s next test this month could sway which camp proves right.

The post SpaceX Price Predicted to Range Between $131 and $800. Where Will SPCX Land? appeared first on BeInCrypto.

The market capitalization of compliant euro stablecoins grew 128% in the year leading up to the end of the Markets in Crypto-Assets Regulation (MiCA) transition period, according to payments infrastructure firm Decta.

Decta said in a Sunday report that the combined market cap of eight MiCA-compliant euro stablecoins rose to $673.9 million on June 28, 2026, from $295.6 million on June 30, 2025. Trading volume rose 43.1% to $67.3 million from $47 million. The number of MiCA-compliant euro stablecoins tracked in the report also rose to eight from five over the period.

Decta tracked eight euro stablecoins that were actively issuing tokens and had market capitalization and trading volume during the study period. By contrast, the European Securities and Markets Authority interim MiCA register lists a broader set, including tokens that may not meet Decta’s activity criteria.

The report found that euro-denominated stablecoins are growing under MiCA but from a small base in a market still dominated by dollar-backed tokens. CoinGecko data shows US dollar-pegged stablecoins at about $300 billion in market capitalization. The combined market capitalization of Decta’s eight actively traded, MiCA-compliant euro stablecoins was 0.22% of the dollar stablecoin market.

From July 1, firms offering crypto-asset services in the European Union generally needed MiCA authorization. Decta’s data sample ends days before the close of MiCA’s crypto-asset service provider (CASP) transition period.

Market capitalization of the top eight euro-pegged stablecoins. Source: Decta

Euro stablecoin growth amid MiCA competitiveness debate

The report adds to a debate among policymakers and industry groups over whether MiCA’s stricter stablecoin rules are helping the euro ecosystem grow or limiting its competitiveness against dollar-backed tokens.

On April 27, a Blockchain for Europe report argued that MiCA had made euro stablecoins safer but commercially weaker. The report said MiCA’s reserve requirements and ban on interest payments left euro tokens at a disadvantage.

Related: EU crypto rulebook faces enforcement challenge as MiCA transition ends

The debate intensified in May after a policy paper from Brussels-based think tank Bruegel called for easing liquidity requirements for stablecoin issuers and potentially granting them access to European Central Bank funding. The paper argued that looser rules could help the euro stablecoin market compete with dollar-backed tokens.

However, the European Central Bank (ECB) pushed back. On May 23, the ECB warned EU finance ministers that expanding issuance of euro stablecoins could weaken bank lending and complicate monetary policy. The ECB also dismissed concerns that stricter EU rules would accelerate digital dollarization.

Magazine: Bitcoin slides to $58K, XRP hits $1 but onchain data promising: Market Moves

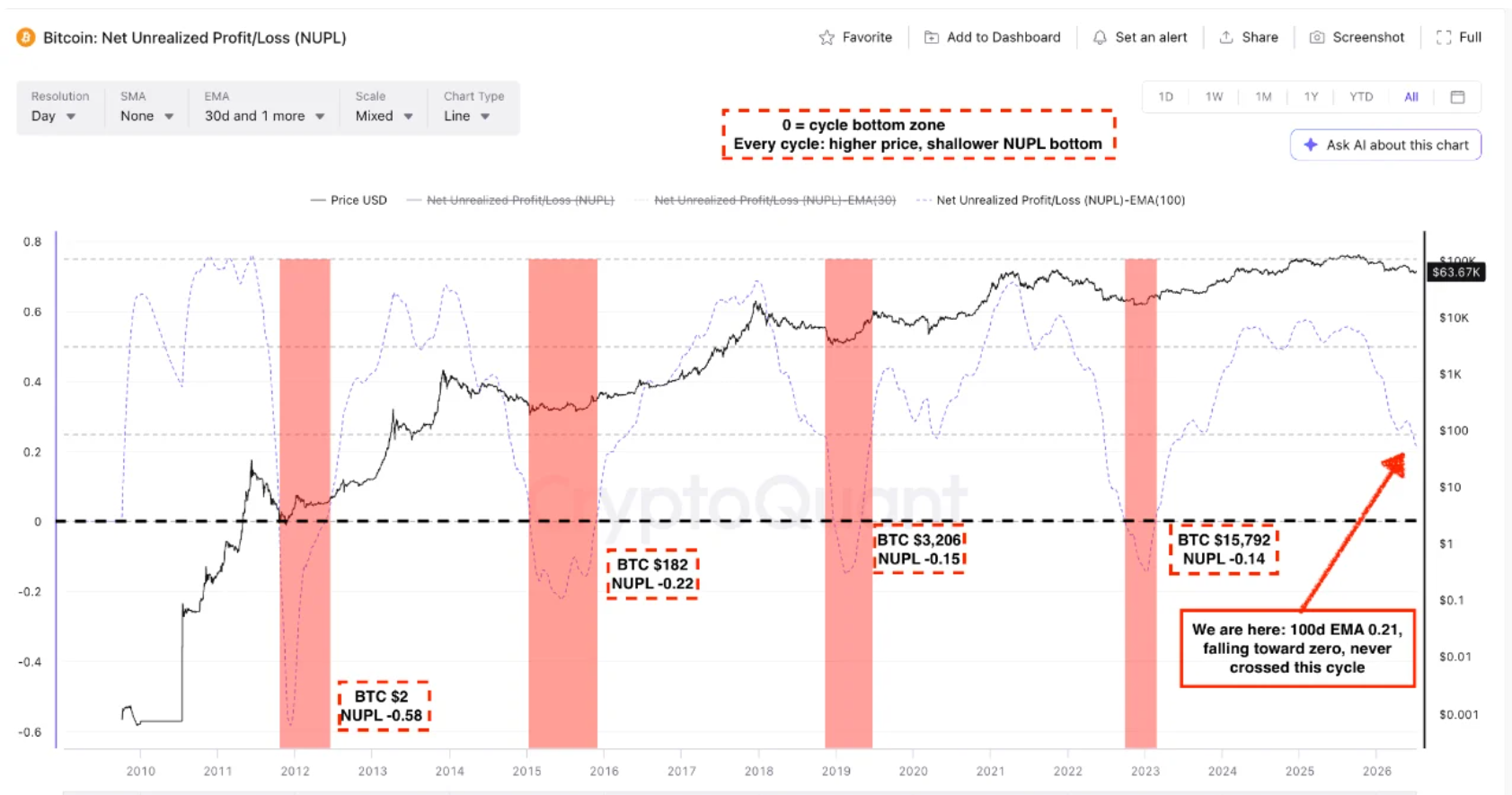

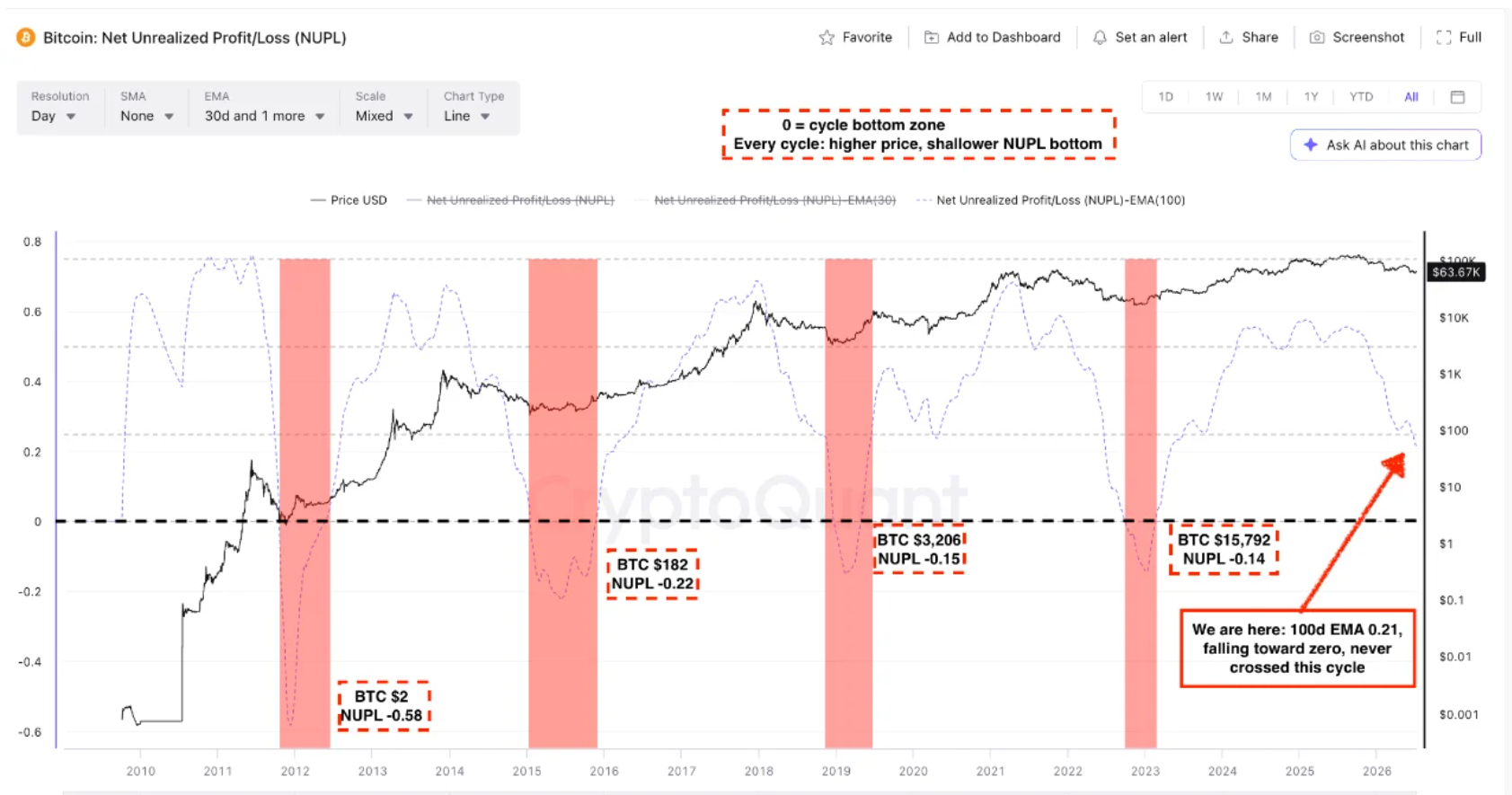

Bitcoin (BTC) has further to fall for one of its “cleanest cycle clocks” to signal a bear-market bottom, new analysis says.

Key points:

- One of Bitcoin’s “cleanest cycle clocks” suggests that new macro lows are needed this bear market.

- The NUPL metric is still in positive territory, setting it apart from previous bear markets.

- Analysis expects history to repeat with a higher low on a long-term NUPL moving average.

CryptoQuant: Bitcoin NUPL contains “level to watch”

In research published on Monday, onchain analytics platform CryptoQuant flagged an incoming profitability floor for the BTC supply.

The onchain metric involved was Net Unrealized Profit/Loss (NUPL), which measures the portion of the supply being held at a higher or lower price versus that at which it last moved. Its score is currently 0.158, a level last seen in early 2023.

“Smoothed into its 30 and 100-day exponential moving averages (EMAs), it becomes one of the cleanest cycle clocks on-chain,” contributor TheChessOnChain commented.

An accompanying chart shows the 100-day EMA of NUPL slowly trending toward cycle bottom levels below zero.

“Every time the 100-day EMA of NUPL fell below zero, Bitcoin was carving its cycle bottom: late 2011 (low near $2), January 2015 ($182), the 2018 bear ($3,206 in December 2018), and the 2022 FTX bottom ($15,792 in November 2022),” TheChessOnChain noted.

Bitcoin NUPL data (screenshot). Source: CryptoQuant

At just above $60,000, BTC/USD corresponds to an NUPL 100-day EMA of 0.215, signalling plenty of room left to drop in order to match previous bear-market lows.

CryptoQuant acknowledged that NUPL has put in higher lows throughout Bitcoin’s history, meaning that even a trip below the zero line may not be essential.

“That leaves two paths,” it continued, describing the four extant zero-line crosses as a “pattern, not a law.”

“Either the 100-day EMA crosses zero as it did at every prior bottom, or this becomes the first cycle to bottom without it, which would fit the shallower-each-time trend.”

No time frame was given for when the next bottom could occur, with CryptoQuant specifying the zero line as the “level to watch in the coming weeks.”

Bear market reversal signals copy history

As Cointelegraph reported, multiple bear-market reversal signals have come from onchain sources in recent weeks, echoing 2022.

Related: $60.4K Becomes ‘most important area’: Five things to know in Bitcoin this week

Despite these now locking in, market participants broadly expect new macro lows to enter before bulls regain the upper hand.

Last week, fellow CryptoQuant contributor Axel Adler Jr. highlighted other supply data presenting mixed signals over short and mid-term BTC price action. Supply in loss, Adler calculated, could still be two months off levels that traditionally correspond to the end of Bitcoin bear markets.

“Until then, it is more accurate to treat capitulation as a process rather than a completed fact,” he wrote.

Privacy-focused layer-1 blockchain Secret Network is proposing to move from its longtime home on Cosmos to Ethereum layer-2 Arbitrum, citing security risks from artificial intelligence, among other reasons.

Secret Network has been running privacy-preserving smart contracts on Cosmos since 2020, as the ecosystem had strong momentum back then, but the “environment has changed,” the team said Tuesday.

“The security risk is the part we take most seriously,” it said. “Old code is becoming dramatically easier to analyze … With AI, the cost of attacking stale code is falling across the board.”

The recent Axelar-Secret IBC bridge exploit highlighted growing security risk from aging, under-maintained code — a risk the team argues AI-assisted exploitation is making worse. The release of advanced AI models such as Anthropic’s Claude Mythos 5 has dramatically increased the capabilities for discovering and potentially exploiting code vulnerabilities.

Liquidity has thinned

The Secret team described Arbitrum as having “deep liquidity, tooling, wallet and exchange support, and thousands of builders composing with one another,” and said “liquidity has thinned” on Cosmos while builders have “drifted to other ecosystems.”

“The tooling you’d want to count on is shakier than it used to be, and a number of projects that once anchored Cosmos have migrated,” it added.

“Attacks that used to take deep manual effort are getting cheaper as models get better at reading contracts, tracing assumptions, and turning a forgotten edge case into a working exploit.”

The proposal, which requires a governance vote, follows a bridge exploit in June that resulted in the loss of $4.7 million in bridged assets but did not affect Secret’s native token, SCRT.

Related: Secret Network bridge exploited for $4.7M with ‘infinite mint’ bug

For SCRT to endure, it needs a new stable home, and the Ethereum ecosystem is that home, the team said.

The team is planning a one-time snapshot of SCRT balances on Sept. 1, which will be used to issue a new ERC-20 SCRT contract on Arbitrum.

Dwindling DeFi value locked

The total value locked in the Cosmos ecosystem is around $2 billion, down 88% from its peak during the 2021 bull market. Comparatively, Arbitrum is the leading layer-2 network by total value secured, which is $17.4 billion, according to L2Beat.

Secret Network has just $1.3 million in TVL on Cosmos, according to DefiLlama.

SCRT holders did not react well to the news, with the token tanking 24% over the past 24 hours to 4.1 cents, down more than 99% from its 2021 peak, according to CoinGecko.

Secret is not the only network to leave Cosmos. In February, privacy-focused blockchain NilChain, built with the Cosmos SDK, left the ecosystem in a move to Ethereum.

The Sei Network completed a full Cosmos-to-EVM transition in June, closing down its native Cosmos transaction layer entirely and becoming Ethereum-based.

Stablecoin blockchain Noble also announced it was moving from the Cosmos ecosystem to Ethereum in January.

Features: The biggest blockchain upgrades still to come in 2026

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

XRPPower integrates AI analysis, automated management, and risk monitoring as investors explore new digital finance solutions amid global market uncertainty.

Summary

- XRPPower highlights AI-powered digital asset management as investors seek alternatives amid market uncertainty.

- It promotes its AI intelligent system for automated digital asset services in the evolving fintech market.

- XRPPower introduces AI-driven asset management tools as global investors navigate changing market conditions.

Entering 2026, global financial markets remain highly focused on the Federal Reserve’s interest rate policy. In recent years, the Fed has maintained relatively high interest rates to combat inflation, and whether it will continue to cut rates or maintain high rates in the future will continue to influence global capital flows and remain a key focus for investors.

While the crude oil market presents investment opportunities, prices are often influenced by multiple factors, including the global economy, geopolitics, and supply and demand. A sudden event can disrupt the existing market rhythm.

Gold has long been considered a safe-haven asset, but its price can also experience corrections when the dollar strengthens or interest rates remain high.

While real estate possesses long-term investment value, it is easily affected by changes in loan interest rates, the economic environment, and market demand. It involves long capital ties and relatively limited liquidity.

For many investors, the real regret is not missing out on a price surge, but watching their assets shrink amidst market volatility, unable to find a more suitable investment approach.

With the continuous integration of AI and fintech, the digital finance industry in 2026 is entering a more intelligent and efficient development phase. More and more investors are beginning to pay attention to the new changes brought about by technological innovation. XRPPower, keeping pace with this trend, continuously upgrades its AI intelligent system, integrating intelligent analysis, automated management, and risk monitoring into platform operations. It constantly optimizes product experience and operational processes, making the platform safer, more transparent, and more convenient. Both new and long-term users can easily understand platform rules and experience more efficient digital asset services.

Join XRPPower and experience the long-term benefits of AI intelligence!

1. Free account registration

2. Choose contract options

The platform offers a variety of product periods and options. Before participating, users can view the product term, rules, settlement methods, and related instructions, and choose according to their needs.

3. Supports mainstream digital asset payments

Supports payments using mainstream digital assets such as BTC, ETH, XRP, USDT, and USDC. The process is simple and convenient.

4. Automatic profit settlement

During product operation, the system will automatically complete daily settlements according to product rules, and profits will be returned to the account balance. Users can choose to withdraw funds or continue participating in other products according to platform rules.

5. Invite friends to share platform rewards

Share a referral with friends using an exclusive invitation code or link. Subject to platform activity rules and receive a 3% + 2% referral reward. Depending on different products and activity rules, the cumulative reward can reach up to $100,000.

Popular earnings details

- Investment Amount: $1,000, Contract Period: 7 days, Daily Earnings: $13.2, Total Earnings: $92.4, Principal $1,000 returned upon maturity.

- Investment Amount: $5,000, Contract Period: 15 days, Daily Earnings: $70.50, Total Earnings: $1,057.5, Principal $5,000 returned upon maturity.

- Investment Amount: $10,000, Contract Period: 20 days, Daily Earnings: $153, Total Earnings: $3,060, Principal $10,000 returned upon maturity.

View more contracts with different yields

XRPPower security, compliance, and protection

XRPPower, headquartered in London, UK, adheres to a development philosophy of security, transparency, and standardization. It continuously references relevant international financial industry standards to improve its platform technology, risk management, and compliance operation system. All product rules, cycles, and settlement information are publicly displayed, and users can query and verify relevant information at any time.

The platform employs multi-layered security mechanisms, including SSL/TLS data encryption, two-factor authentication (2FA), separate storage of cold and hot wallets, multi-signature, and AI-powered intelligent risk monitoring, to comprehensively protect account, data, and digital asset security. Simultaneously, the platform continuously draws on risk management and internal control concepts widely adopted by international professional institutions such as PwC to continuously improve platform transparency, operational standardization, and long-term service capabilities, striving to create a safer, more stable, and transparent digital asset service platform for global users.

2026 investment summary

The financial market is always accompanied by both opportunities and risks. Whether choosing crude oil, gold, real estate, or focusing on digital asset services, investors should fully understand the product rules and risks, develop a reasonable asset allocation plan based on their own needs, and find a suitable long-term development direction in the ever-changing market environment.

With the continuous integration of AI technology and fintech, XRPPower is providing various product cycles and solutions through intelligent analysis and its platform to meet the short-term or long-term asset allocation needs of different users. Product rules, cycles, and settlement information are all open, transparent, searchable, and verifiable, helping users develop more reasonable investment strategies based on their own goals and explore a more stable development direction in long-term planning.

Learn more on the official website.

Disclosure: This content is provided by a third party. Neither crypto.news nor the author of this article endorses any product mentioned on this page. Users should conduct their own research before taking any action related to the company.

The US Commodity Futures Trading Commission has sued a North Carolina man, accusing him of operating a commodity pool featuring crypto that defrauded investors of more than $14 million.

The CFTC’s lawsuit, filed in federal court on Tuesday, alleged that Trevor Vernon and his company, Argent Capital Management, operated a commodity pool featuring equity index futures, options on equity index futures and crypto.

The agency alleged that from March 2022 to February 2026, Vernon solicited $14.8 million from at least 60 investors and falsely claimed he was a successful trader, even though his trading actually “resulted in consistent and catastrophic losses” for the pool’s investors.

The lawsuit is a rare crypto-related enforcement action from the CFTC, which is angling to oversee the crypto industry while facing questions from some lawmakers about whether it has the resources to police the complicated and rapidly growing sector.

The agency alleged that as part of the scheme, Vernon traded crypto, including Bitcoin (BTC) and Ether (ETH), which the CFTC asserted were commodities.

CFTC alleges Vernon ran pool “akin to a Ponzi scheme”

The CFTC alleged in its complaint that Vernon made false statements to existing and potential investors, including in quarterly account updates and monthly performance emails.

The agency claimed Vernon’s trading of crypto, as well as futures and options on stock indices, resulted in losses of more than $8.6 million.

Related: CME Group sues CFTC over crypto perpetual futures

The CFTC said Vernon never disclosed the losses to investors and alleged he misappropriated $3 million to pay investors “in a manner akin to a Ponzi scheme” to hide his losses. He also allegedly misappropriated $136,000 for private air travel, according to the lawsuit.

The CFTC accused Argent Capital Management of failing to register with the agency as required by federal commodities law, and claimed Vernon made false statements to the regulator in January about the issues alleged in its complaint.

The CFTC charged Vernon with seven counts related to fraud, failure to register and making false statements.

It asked the court to permanently ban Vernon from registration and trading, along with disgorgement, penalties and restitution.

Features: From Bitcoin critics to blockchain believers: The 5 biggest crypto backflips

The Federal Reserve releases the minutes from its June 16-17 policy meeting on Wednesday at 2 p.m. ET. Investors hoping for clarity on a September rate hike may come away with less than they expect.

Chair Kevin Warsh withheld his own rate projection this cycle. He also issued a policy statement of just 130 words that dropped forward guidance entirely. That leaves the minutes as the only detailed record of the committee’s internal debate.

A Committee Split Between Hawks and Doves

The FOMC held rates steady at 3.50% to 3.75% on June 17. That marked the fourth consecutive hold. Nine of 18 FOMC policymakers penciled in at least one 2026 hike. Warsh declined to submit a projection of his own.

The committee met before the Bureau of Labor Statistics released its June payrolls report. That report showed just 57,000 new jobs, the weakest reading in four months. Any hawkish language in the minutes reflects a labor market that still looked solid at the time. The softer picture came days later.

The CME FedWatch Tool now prices roughly a 50% to 55% chance of a September hike. That is down from 66% before a weaker-than-expected June jobs report. Warsh addressed the uncertainty directly at his press conference.

“We recognize that inflation has been running well ahead of the Fed’s long-stated inflation

goal of 2 percent that’s been going on for more than five years. Persistently high prices are a

burden for the American people. But the recent past need not be prologue.”

— Kevin Warsh.

Why the Silence Itself Is the Story

Warsh has pushed for a leaner communication style since taking office. He argues forward guidance entangles the Fed in markets that should react to data instead.

That approach puts unusual weight on Wednesday’s release. No accompanying statement language exists for comparison. Speaking at the Sintra policy forum in July, Warsh left little doubt about his inflation stance. he stated that people should not expect his Fed to be comfortable with inflation above 2%

The minutes could reveal how close the committee’s hawks came to pushing for a hike in June. Or they could leave the disagreement as vague as the statement did.

Either way, a chair who prefers silence may keep investors waiting past Wednesday for real clarity.

The post Markets Wait on Fed Minutes: What to Expect from Today’s Release appeared first on BeInCrypto.

Crinetics Pharmaceuticals shares nearly doubled on Monday, July 6 after Vertex Pharmaceuticals agreed to buy the company for $10 billion in cash.

Vertex will pay $85 a share. That is roughly double Crinetics’ closing price the day before Vertex announced the deal.

What Vertex Is Actually Buying

Crinetics makes Palsonify, a pill for acromegaly, a rare disorder that causes excess growth hormone. Patients previously relied on regular injections, so a once-daily pill is a real upgrade in convenience.

Vertex, known for its cystic fibrosis drugs, is betting big on that convenience. It has a second drug in late-stage trials for another rare hormone condition. Together, the two products could bring in more than $5 billion a year at their peak.

William Blair analyst Myles Minter said the price tag makes sense if that sales target holds up.

“Investors will debate this (stock was down 1.8% after hours), but we view this as reasonable if the peak sales number can be achieved.”

Retail sentiment on Crinetics flipped from bearish to bullish within a day. The GameStop eBay takeover saga shows how fast retail mood can swing on buyout news.

Is There Any Upside Left?

Once a company announces a cash buyout, its stock stops trading on its own business prospects. It trades toward the agreed price instead.

Crinetics is already close to that $85 target. The Riot Platforms Bitfarms takeover played out the same way, with shares settling near the offer price.

Most of the reward has already landed. What remains is a small gap, plus the risk that the deal falls through before it closes in the third quarter.

The post Why Crinetics Stock Doubled After Vertex’s $10 Billion Buyout appeared first on BeInCrypto.

Staking locks your crypto and earns yield. Liquid staking hands you a tradeable receipt for that locked position, so the same capital can earn twice. It is one of DeFi’s largest markets, and it comes with a specific danger most guides skip: the receipt can trade below what it represents. Here is how liquid staking tokens work, and where the risk actually lives.

Summary

- Liquid staking tokens let users keep earning staking rewards while using a tradeable token across DeFi without unlocking the original assets.

- The biggest risk comes when liquid staking tokens trade below the value of the assets backing them, especially during periods of market stress and heavy withdrawals.

- Higher yields from liquid staking strategies often involve leverage, increasing the risk of liquidations if the token temporarily loses its peg.

Staking a proof-of-stake asset like Ether involves a trade-off that used to be absolute: lock your tokens to help secure the network and earn rewards, and accept that the locked tokens are frozen and useless for anything else. Liquid staking removes the second half of that bargain. You deposit your tokens with a protocol, the protocol stakes them for you, and in return you receive a new token, a liquid staking token, that represents your staked position and can be freely traded, sold, or put to work elsewhere in decentralized finance. The original capital keeps earning staking rewards; the receipt token lets that same capital do a second job.

That double-duty is why liquid staking became one of the largest categories in all of DeFi, with tens of billions of dollars flowing into it. It is also why it carries a risk that plain staking does not. The receipt token is only useful if the market treats it as equal in value to the asset it represents, and there are moments, usually the worst possible moments, when the market does not. A liquid staking token can trade below the value of the staked asset behind it, an event called a depeg, and understanding when and why that happens is the difference between using this tool safely and being surprised by it.

This guide explains what liquid staking tokens are, the two designs they come in, how the peg is supposed to hold and how it breaks, the concentration risk hiding behind the biggest provider, the way these tokens get stacked into leverage across DeFi, and the practical questions to ask before holding one. The star example throughout is stETH, the largest liquid staking token, but the mechanics apply across the category, from Rocket Pool’s rETH on Ethereum to the staked-asset tokens on other proof-of-stake networks. The goal is to leave you able to hold one of these tokens understanding exactly what it is, what backs it, and under what conditions its price can part ways with the asset it represents.

The problem liquid staking solves

To see why liquid staking exists, start with the friction of ordinary staking. On Ethereum, running your own validator requires locking thirty-two ether, operating node software with constant uptime, and accepting that your stake is subject to exit queues when you want out. For most holders this is impractical: they lack thirty-two ether, do not want to run infrastructure, and dislike freezing capital they might need, especially as Ethereum reworks its staking and consensus layers in ways that will reshape validator economics for years.

Staking pools solved the first problems by letting many users combine smaller amounts under professional validators, but the funds were still locked. Liquid staking solves the last problem, the lock itself. When you deposit into a liquid staking protocol, it pools your tokens with everyone else’s, stakes them across a set of validators, and mints you a token representing your share of the staked pool plus its accruing rewards. You no longer need thirty-two ether, you never touch validator software, and, crucially, your position is now liquid: the receipt token sits in your wallet and can move freely while the underlying stake keeps earning.

A coat-check analogy captures it. You hand over your coat and receive a claim ticket. The coat stays safely in the cloakroom earning nothing, but the ticket is now in your hands, and while you cannot wear the ticket, you can hold it, hand it to a friend, or even sell it. Liquid staking works the same way: the staked asset stays locked and productive, while the token proving your claim to it circulates freely. Whoever holds the ticket holds the claim, so selling the token means selling the staked position along with it.

The result is capital efficiency that plain staking cannot match. A holder can stake, receive the token, and then lend it, use it as collateral, or provide it as liquidity, earning a second layer of return on top of the base staking reward, all without unstaking. That stacking is the appeal and, as later sections show, the source of the systemic worry.

Two designs: rebasing and value-accruing

Liquid staking tokens come in two flavors, and the difference matters for how rewards show up in your wallet and how the token behaves in DeFi.

A rebasing token keeps its price pegged to the underlying asset one to one and delivers rewards by increasing the number of tokens you hold. Lido’s stETH is the classic example: hold it, and your stETH balance grows a little each day, with each stETH meant to remain worth roughly one ether. The appeal is transparency, since your balance visibly climbs, but the growing balance complicates integrations, because many DeFi protocols were not built to handle a token quantity that changes on its own.

A value-accruing token keeps the token count fixed and delivers rewards by rising in value against the underlying asset. Rocket Pool’s rETH works this way, as does the wrapped version of stETH, wstETH. You hold the same number of tokens over time, but each one is redeemable for progressively more ether as rewards accumulate; stake when one token equals one ether and, a year later, that token might redeem for meaningfully more. This design integrates more smoothly across DeFi because the balance is stable, which is why wrapped, value-accruing versions dominate in lending and liquidity protocols and increasingly appear in the institutional DeFi rails being built on other ledgers too.

The distinction is easy to miss and important in practice. A rebasing token used as collateral can behave strangely because its balance shifts; a value-accruing token trades at a price that is intentionally above one-to-one and rising, so seeing rETH or wstETH quoted above the price of ether is normal and correct, not a premium to fear. Knowing which design you hold prevents misreading its price and misusing it in a protocol.

How the peg holds, and how it breaks

The entire usefulness of a liquid staking token rests on the market valuing it close to the staked asset it represents. That relationship is a soft peg, maintained by arbitrage and redemption instead of any hard guarantee, and understanding the mechanism explains exactly when it can slip.

In normal conditions the peg holds tightly because of a redemption path. A stETH is a claim on staked ether, and once the protocol’s withdrawal queue is functioning, that claim can be redeemed for actual ether. If stETH ever trades meaningfully below one ether on the open market, arbitrageurs buy the discounted stETH, redeem it for a full ether through the queue, and pocket the difference, and that buying pressure pushes the price back toward parity. Deep secondary-market liquidity reinforces this: research on stETH has found that most deviations beyond a small threshold correct within hours, because the arbitrage is reliable and the market is deep.

The peg breaks when the redemption path is slow and the market panics faster than arbitrage can act. Redeeming a liquid staking token for the underlying asset is not instant; it runs through the network’s validator exit queue, which can take days when many people withdraw at once. In a stressed market, holders who want out immediately cannot wait for the queue, so they sell on the open market instead, and a wave of forced selling can push the token below the value of the asset behind it. This is a depeg: not a loss of the underlying stake, but a temporary discount on the receipt.

The defining real-world case came in 2022, when stETH traded as low as roughly a nickel under parity during a broad market crisis. Large holders facing liquidation needed liquidity immediately, the withdrawal path at the time did not allow direct redemption, and the resulting sell pressure drove stETH to a visible discount to ether. Critically, the underlying staked ether was never lost or impaired; the discount reflected the mismatch between an instant desire to exit and a redemption process that could not move instantly. Once redemption became possible and panic subsided, the peg restored. The episode is the template: a liquid staking token depeg is almost always a liquidity-and-timing event, not a solvency event, but that distinction is cold comfort to someone forced to sell at the discount.

How the yield actually stacks

A concrete walk-through of the returns shows both why liquid staking is popular and where the layers of risk enter, because each layer of yield is also a layer of exposure.

Start with the base. Staking ether on Ethereum earns a network reward, a modest annual percentage that comes from new issuance and transaction fees paid to validators for securing the chain. A holder who simply stakes and holds a liquid staking token captures this base reward with almost none of the friction of solo staking: no thirty-two-ether minimum, no node to run, no direct exit-queue management. For many holders, that is the entire appeal, and it is a reasonable, relatively conservative use of the tool.

The second layer comes from putting the token to work. Because the liquid staking token is freely tradeable, a holder can deposit it into a lending protocol to earn interest, supply it to a liquidity pool to earn trading fees, or use it as collateral, each adding a return on top of the base staking reward. This is the capital efficiency that plain staking cannot match: the same underlying ether earns its staking reward and a second yield simultaneously. It is also where smart-contract risk begins to compound, because the token now passes through a second protocol’s code in addition to the staking protocol’s own.

The third layer, and the dangerous one, is leverage, described earlier: borrowing against the token to acquire more of it and repeating the loop. Each turn of the loop multiplies the base yield, which is why advertised returns on some liquid staking strategies look far higher than the underlying staking reward could ever justify. The arithmetic that produces those headline numbers is leverage, and leverage is precisely what converts a survivable depeg into a forced liquidation.

The practical takeaway is to read any liquid staking yield as a signal of how many layers are involved. A return close to the base staking reward is a plain, relatively safe position. A return well above it means the token is deployed into other protocols, adding smart-contract exposure. A return far above the base almost always means leverage, and therefore liquidation risk in a depeg. The yield number is not just a reward; it is a readout of the risk stack beneath it, and matching the layer you accept to the risk you understand is the whole discipline of using these tokens well. The same logic governs every layered yield strategy in DeFi: more yield is always more of something else at risk.

The concentration problem

Beyond the depeg risk sits a subtler, more structural concern: one protocol dominates Ethereum liquid staking to a degree that worries people who think about the network’s health.

Lido, the issuer of stETH, has for long stretches controlled roughly a third of all staked ether, a share large enough that Ethereum researchers openly discuss it as a risk to the network itself. The reasoning is about consensus: if a single staking entity controls too large a fraction of validators, it gains outsized influence over block production and could, in extreme scenarios, threaten the neutrality or censorship-resistance the network depends on. This is not an accusation that Lido would misbehave; it is a structural observation that concentration itself is a vulnerability, regardless of the operator’s intentions, and it is why parts of the community actively encourage stakers to choose smaller providers.

Concentration also compounds the token-level risks. When one liquid staking token is embedded as collateral across nearly every major lending protocol, a serious problem with that token, a smart-contract bug, a governance failure, or a severe depeg, is not one protocol’s problem but a shock that ripples through all of DeFi at once. The dominant token’s ubiquity, which is a convenience in calm markets, becomes a transmission channel in stressed ones. The same dynamic appears wherever a single asset becomes foundational infrastructure, from stablecoins to the restaking protocols that layer additional yield on top of staked positions: dominance buys efficiency and sells fragility.

For an individual holder, concentration risk is mostly about awareness. Using the largest, most liquid token gives the tightest peg and the deepest DeFi integration, which is a real benefit; it also means holding the asset most entangled with everything else, so a systemic event touches it first. Diversifying across providers reduces personal exposure and, in aggregate, improves the network’s health, at the cost of slightly thinner liquidity in the smaller tokens.

The leverage stack, and why it magnifies everything

The feature that makes liquid staking tokens powerful, their usability across DeFi, also enables a leverage loop that turns a modest depeg into a cascade. Understanding this loop is essential to understanding why depegs matter beyond the inconvenience of a discount.

The loop works like this. A user stakes ether and receives a liquid staking token. They deposit that token as collateral in a lending protocol and borrow ether against it. They stake the borrowed ether, receive more of the liquid staking token, deposit that as collateral, and borrow again. Repeated, this stacks several layers of leverage on a single underlying position, each layer amplifying the yield in calm markets. It is a popular strategy precisely because the base staking reward, multiplied by leverage, produces attractive returns.

The danger is what happens when the token depegs. Each borrowing position has a liquidation threshold tied to the value of the collateral, and a depeg lowers that value. As the token slips below parity, leveraged positions approach liquidation; liquidations force the collateral token to be sold; that selling deepens the depeg; the deeper depeg triggers more liquidations. In stressed markets this becomes a self-reinforcing spiral, a domino run dressed in yield-farm packaging. The 2022 depeg was made sharper by exactly this dynamic, as leveraged holders were forced to unwind into a falling market.

The lesson for holders is that a liquid staking token held plainly is a fairly conservative instrument: it earns staking yield and, absent a solvency failure in the protocol, its worst realistic outcome is a temporary discount that arbitrage eventually closes. The same token levered several times over is a very different risk, one where a discount that a plain holder could simply wait out becomes a forced liquidation. The token did not change; the leverage around it did. Anyone evaluating liquid staking yields that look unusually high should assume leverage is involved and price the liquidation risk accordingly.

What to check before holding one

Liquid staking is a genuinely useful tool, and using it well comes down to a handful of concrete checks, not blanket caution.

Confirm the token design. Know whether you hold a rebasing token, whose balance grows, or a value-accruing one, whose price rises, because the two behave differently in your wallet and in any protocol you deposit them into. Value-accruing wrapped versions are generally the smoother choice for DeFi use.

Assess the redemption path. The peg’s strength depends on being able to redeem the token for the underlying asset, so check that direct withdrawals are live and how long the exit queue runs. A token with a fast, functioning redemption path has a stronger peg than one where exit depends entirely on selling into secondary-market liquidity.

Gauge the liquidity and the provider. Deep secondary-market liquidity is what lets arbitrage defend the peg between redemptions, so a token with thin liquidity is more prone to slipping and slower to recover, the same slippage dynamics that govern any thinly-traded swap. Weigh the largest provider’s tight peg and deep integration against its concentration risk, and consider whether spreading across providers suits your risk tolerance and, incidentally, helps the network.

Respect the layered smart-contract risk. Your capital passes through the staking protocol’s contracts, and if you deploy the token into lending or liquidity protocols, through those as well. Each layer is code that can contain bugs, and stacking layers stacks the places something can break, the same concentration-of-risk lesson that runs through every major bridge exploit. Favor audited, long-lived protocols, and treat any strategy promising outsized yield as a signal that leverage, and its liquidation risk, is present.

Held with these checks in mind, a liquid staking token does what it promises: it unlocks the value of a staked position so the same capital can work twice, earning a base reward while remaining liquid and productive. The depeg risk that defines the category is real but specific, a timing-and-liquidity event instead of a loss of the underlying stake, and it is most dangerous not to plain holders but to those who lever the token into a stack that turns a temporary discount into a forced sale. Understand which of those two users you are, and the risk becomes something you can size instead of something that surprises you.

The broader significance is worth a closing thought. Liquid staking tokens have become foundational plumbing for proof-of-stake economies: tens of billions of dollars of staked value now circulate as these receipts, and they underpin lending, trading, and collateral across DeFi. That ubiquity is a genuine achievement, turning otherwise idle staked capital into productive infrastructure. It also means the health of a few dominant tokens matters to the whole system, which is why the concentration and depeg risks discussed here are not merely individual concerns but systemic ones.

Using these tokens knowledgeably, favoring strong redemption paths, deep liquidity, and audited protocols, and staying alert to the leverage hiding behind unusually high yields, is how an individual participates in that system without being surprised by its failure modes.

Frequently asked questions

What is a liquid staking token?

A liquid staking token is a tradeable token you receive when you stake a proof-of-stake asset through a liquid staking protocol. It represents your staked position plus its accruing rewards, and it can be freely sold or used in DeFi while the underlying asset stays staked and earning. stETH from Lido and rETH from Rocket Pool are the best-known examples on Ethereum.

How is liquid staking different from regular staking?

Regular staking locks your tokens, making them unavailable for anything else until you unstake through an exit queue. Liquid staking gives you a receipt token that keeps your capital liquid, so you can trade it or use it elsewhere in DeFi while the underlying stake continues to earn rewards. The trade-off is added smart-contract risk and the possibility that the receipt token depegs.

What does it mean when stETH depegs?

A depeg means the liquid staking token trades below the value of the staked asset it represents, such as stETH trading below one ether. It usually happens when many holders want to exit faster than the redemption queue allows, so they sell on the open market and push the price to a discount. Importantly, a depeg is generally a liquidity and timing event, not a loss of the underlying staked asset.

Is my staked asset lost if the token depegs?

No. A depeg reflects a temporary market discount on the receipt token, not destruction of the underlying stake. The staked asset remains intact and continues earning, and once the redemption path clears and panic subsides, arbitrage typically restores the peg. The real risk is being forced to sell at the discount, which mainly affects leveraged holders facing liquidation.

Are rebasing and value-accruing tokens different?

Yes. A rebasing token like stETH stays pegged one-to-one and pays rewards by increasing your token balance over time. A value-accruing token like rETH or wrapped stETH keeps the balance fixed and pays rewards by rising in value against the underlying asset. Value-accruing versions integrate more smoothly into DeFi because their balance does not change unexpectedly.

Why is Lido’s dominance considered a risk?

Lido has often controlled roughly a third of all staked ether, and Ethereum researchers worry that any single staking entity holding too large a share of validators could gain outsized influence over the network’s consensus. It also means the dominant token is embedded across most of DeFi, so a serious problem with it would ripple widely. The concern is structural rather than an accusation of misconduct.

Can I lose money with liquid staking tokens?

Yes, through several channels: a smart-contract bug in the staking or DeFi protocols you use, a severe depeg that forces you to sell at a discount, or liquidation if you lever the token in a borrowing loop. Held plainly in an audited, liquid protocol, the risk is relatively modest, but stacking leverage on top substantially raises the chance of a forced loss.

What is the leverage loop with liquid staking tokens?

The loop involves staking to get the token, using it as collateral to borrow the underlying asset, staking that to get more of the token, and repeating to stack leverage and amplify yield. It works in calm markets but is dangerous in a depeg, because falling collateral value triggers liquidations that force selling, which deepens the depeg and triggers more liquidations in a self-reinforcing cascade.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Digital asset markets are volatile and you can lose your entire investment. Always do your own research. Information current as of July 7, 2026.

10 Marvel Heroes Strong Enough To Stop Doom

‘Weak and inconsistent’ safeguarding of NI school funds, report finds

Maase Inc Shares Jump 16% as Speculative China-Based AI Pivot Stock Extends Its Volatile 2026 Rally Today

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: High Hopes

-

NewsBeat3 days ago

NewsBeat3 days agoTaylor Swift and Travis Kelce wedding staffer hilariously struggles to keep her cool while checking in megastars

-

Fashion1 day ago

Fashion1 day agoOpen Thread: What Great Books Have You Read Recently?

-

Crypto World7 days ago

Airdrop Registration Becomes Key Focus For Remittix As RTX Launch Updates Approach

-

Politics5 days ago

Politics5 days agoThe House | “Reframing the debate from a binary discussion of winners and losers”: Yuan Yang reviews ‘We Are Not Machines’

-

Crypto World4 days ago

Crypto World4 days agoStandard Chartered Secures MiCA License as ESMA Adds 37 New Crypto Firms

-

Business1 day ago

Business1 day agoAXT Shares Jump Nearly 14% as Semiconductor Materials Maker Rebounds on AI-Linked Indium Phosphide Demand

-

Sports7 days ago

Sports7 days agoBroncos roster: OL Ben Powers (No. 74) entering final year of contract

-

Crypto World6 days ago

Crypto World6 days agoBinance stock trading tops $1B in first month after launch

-

Crypto World1 day ago

SK hynix (000660.KS) Stock Dips as $28B Nasdaq ADR Offering Drives AI Memory Expansion

-

Crypto World6 days ago

Crypto World6 days agoAlibaba-affiliate Ant Group enters the humanoid robot market with 12 deals

-

Crypto World3 days ago

Crypto World3 days agoSouth Africa proposes crypto tax guidance under existing rules

-

News Videos2 days ago

News Videos2 days agoBest Time to Enter Small Caps Right Now? Another Bull Run? | Financially Free

-

News Videos1 day ago

News Videos1 day agoWhats Hidden Inside This Cash Register? #treasure #reselling #money

-

Tech3 days ago

Tech3 days agoLenovo laptops are now shipping with YMTC SSDs, a sign of Chinese NAND entering the mainstream

-

Business6 days ago

Business6 days agoMeta Platforms Stock Jumps 7% Today as Bloomberg Reports Company Plans to Enter the Cloud Business

-

NewsBeat6 days ago

NewsBeat6 days agoNew exhibition reflects five decades of movement between island of Ireland and GB

-

Business5 days ago

Business5 days agoWhat a 10 Percent Drop Means for Buyers, Sellers and Renters

-

Crypto World5 days ago

Crypto World5 days agoBinance Re-Enters Philippines As EU MiCA Rules Restrict Access

-

News Videos2 days ago

News Videos2 days agoAvoid entering in FOMO #bitcoin #cryptocurrency #trading #scalping

You must be logged in to post a comment Login