Crypto World

Hybrid Crypto Exchange Solutions: Safer, Faster Trades 2026

The dominance of centralized exchanges in early crypto wasn’t accidental or irrational. It was a practical response to real constraints, technical, commercial, and user experience constraints that the alternatives of the time couldn’t adequately address.

Early crypto users needed somewhere to convert assets, discover prices, and execute trades with reasonable reliability.

Centralized exchanges provided all of this in a familiar package, an interface that looked and worked roughly like a traditional brokerage, custody handled by the platform, and liquidity sufficient for the asset range that existed at the time.

For users coming from traditional finance, the mental model translated. For new users, the learning curve was manageable. For a nascent market, it worked.

The centralized model also solved the bootstrapping problem that decentralized alternatives struggle with fundamentally, liquidity. A centralized exchange could onboard market makers, manage order books actively, and ensure that users could actually execute trades rather than posting orders into thin books and waiting.

In the early market, this wasn’t a minor convenience. It was the difference between a functional trading venue and an unusable one.

The Architectural Shifts That Followed

The response to centralized exchange limitations came in waves, each wave addressing specific failure modes of the centralized model, each wave introducing its own set of tradeoffs.

The response to centralized exchange limitations came in waves, each wave addressing specific failure modes of the centralized model, each wave introducing its own set of tradeoffs.

The first wave was technical hardening of centralized exchanges themselves. Better security practices, cold storage for user funds, proof-of-reserves mechanisms, improved audit procedures.

These improvements reduced but didn’t eliminate the structural risks inherent in centralized custody, because the fundamental architecture remained the same. A more secure centralized exchange is still a centralized exchange, with all the single-point-of-failure characteristics that implies.

The second wave was the emergence of decentralized exchanges, platforms where trading happened through smart contracts rather than centralized order books, where users retained custody of their assets throughout the trading process, and where no central operator could freeze accounts or misappropriate funds.

The promise was significant. The execution, particularly in early iterations, was uneven. A crypto exchange solution that emerged from this period of architectural experimentation looked quite different depending on when in the cycle it was built and what specific problems its designers prioritized.

Solutions built primarily in response to security concerns looked different from those built primarily in response to user experience concerns or liquidity concerns.

The diversity of approaches produced a rich ecosystem of alternatives, and, eventually, the conditions for a synthesis. The synthesis, what the market increasingly calls the hybrid model, didn’t emerge from a single design decision or a single team.

It emerged from accumulated recognition that centralized and decentralized approaches each had genuine strengths and genuine weaknesses, and that the most useful exchange infrastructure would find ways to combine the strengths while mitigating the weaknesses.

That recognition, translated into actual architecture, is what defines the current frontier of exchange infrastructure development.

The Cracks That Appeared – What Centralized Models Got Wrong?

The problems with centralized exchange infrastructure didn’t announce themselves dramatically at first. They accumulated, in security incidents, in operational failures, in the gradual recognition that certain structural characteristics of the centralized model created risks that couldn’t be engineered away.

Custody risk was the most consequential. Centralized exchanges hold user funds, which means they’re attractive targets, and when security fails, user funds disappear.

The history of centralized exchange hacks is long and expensive. Mt. Gox. Bitfinex. Coincheck. FTX, in a different but related category of failure. Each incident represented real user losses and a real erosion of trust in centralized custody as a model.

The FTX collapse in particular clarified something that security-focused critics had been arguing for years, that centralized custody creates not just security risk but operational and governance risk that users have no visibility into and no control over.

Funds held on a centralized exchange are not your funds in any meaningful sense. They’re IOUs from an institution whose internal operations you can’t audit and whose solvency you can’t verify.

For users in jurisdictions with restrictive financial regulations, or users whose assets became politically inconvenient, the centralized model’s single point of control became a single point of failure for their access to the market. Opacity around fees, execution quality, and order flow created a third category of concern.

Centralized exchanges have information advantages over their users, they see order flow before execution, they can adjust fee structures in ways that aren’t always transparent, and they’re not subject to best-execution obligations that apply to regulated financial venues.

Whether these advantages were systematically exploited varied by exchange. That they existed at all was a structural feature of the model.

Decentralized Exchanges – The Promise, The Reality, And The Gap

Decentralized exchanges arrived with genuinely compelling architecture. No custody risk. No single operator to freeze accounts or misappropriate funds.

Decentralized exchanges arrived with genuinely compelling architecture. No custody risk. No single operator to freeze accounts or misappropriate funds.

Transparent execution through auditable smart contracts. Self-sovereign asset control throughout the trading process. On paper, these properties addressed precisely the failure modes that centralized exchange history had exposed.

The reality of early DEX experience was more complicated. Liquidity was thin outside major pairs on established networks. Slippage on anything beyond the most common swaps was significant enough to make execution economically unattractive.

Gas costs on Ethereum-based DEXs added a fee layer that made small transactions uneconomical entirely. The user experience, connecting wallets, approving transactions, managing gas, understanding slippage tolerance, assumed a technical sophistication that most users didn’t have and shouldn’t need.

Speed was the other gap. Blockchain transaction finality times meant that DEX execution was measured in seconds to minutes rather than milliseconds.

For users accustomed to centralized exchange execution speeds, this felt like regression. For use cases requiring time-sensitive execution during volatile markets, it was a genuine functional limitation.

AMM-based DEXs improved on some of these dimensions – providing passive liquidity through pooling mechanisms that didn’t require active market making. But AMMs introduced their own set of issues. Impermanent loss for liquidity providers.

Sandwich attacks and MEV extraction that reduced execution quality for traders. Price impact curves that made large trades expensive relative to centralized alternatives.

None of this made DEXs without value. For specific use cases, privacy-sensitive transactions, access from jurisdictions where centralized options were unavailable, trading of assets not listed on centralized platforms, DEXs provided genuine utility that centralized alternatives couldn’t match.

The point is that DEXs as a complete replacement for centralized infrastructure faced real obstacles that pure decentralization couldn’t fully resolve.

The Hybrid Model – Combining The Best Of Both

The hybrid exchange model didn’t emerge from a manifesto or a whitepaper. It emerged from practitioners recognizing specific combinations of centralized and decentralized characteristics that produced better outcomes than either approach alone.

The core insight is straightforward: custody and execution are separable. A centralized exchange bundles them together, the platform holds your assets and executes your trades. But there’s no technical reason these functions need to be coupled.

Non-custodial architecture keeps assets under user control throughout the exchange process, while centralized infrastructure handles the rate aggregation, liquidity matching, and execution optimization that decentralized systems struggle with at scale.

This separation produces something genuinely useful. The user retains asset control – reducing custody risk to near zero – while getting execution quality and speed that DEX-only infrastructure can’t match.

The platform handles the operational complexity of liquidity aggregation and routing without ever touching user funds in a custodial sense. Both parties get the properties they most care about without accepting the downsides of either pure model.

Order matching in hybrid systems varies by implementation. Some use centralized order books with on-chain settlement, the speed and depth of centralized matching with the transparency and finality guarantees of blockchain settlement.

Others use aggregated liquidity across both centralized and decentralized sources, routing to whichever provides better execution for a specific transaction.

The architectural choices at this layer significantly affect the rate quality and execution reliability that users experience. The regulatory positioning of hybrid models is also more tractable than pure DEX architecture in many jurisdictions.

Non-custodial infrastructure reduces the regulatory surface area associated with holding user funds, while the presence of identifiable operating entities, unlike fully decentralized protocols, provides regulatory counterparties that can engage with evolving compliance requirements.

This isn’t a complete regulatory solution, but it’s a meaningfully better starting position than either extreme.

What Modern Hybrid Infrastructure Actually Looks Like?

Theory is useful. What hybrid exchange infrastructure looks like in actual production deployments is more instructive.

Theory is useful. What hybrid exchange infrastructure looks like in actual production deployments is more instructive.

LetsExchange operates as a practical example of what mature hybrid architecture delivers at scale, non-custodial exchange across hundreds of cryptocurrency pairs, with liquidity aggregated across multiple sources to produce competitive rates without requiring users to surrender asset custody at any point in the transaction flow https://letsexchange.io/.

Assets move directly between user wallets. The platform handles rate discovery, liquidity routing, and execution optimization in the middle. No funds held, no custody risk, no single point of failure for user assets.

The breadth of asset coverage in modern hybrid systems reflects the aggregation architecture underneath them. Single-source systems are limited to whatever their one liquidity provider supports.

Aggregated hybrid infrastructure can support the union of all supported assets across all connected sources, which in practice means hundreds of tradeable pairs including assets that no individual centralized exchange lists.

For users with diverse portfolio needs, this coverage breadth has real practical value. Transaction speed in hybrid systems has converged toward centralized exchange performance for most use cases.

The multi-minute execution times of early DEX infrastructure are not characteristic of well-built hybrid systems, rate confirmation and transaction initiation happen in seconds, with settlement times determined by the underlying blockchain networks involved rather than by the exchange infrastructure itself.

Fee transparency in hybrid architecture tends to be cleaner than in centralized alternatives. No hidden order flow revenue, no opaque spread manipulation, no custody-related fee structures.

What the user sees in the rate quote is what the transaction costs. For businesses with margin calculations that depend on accurate exchange cost modeling, this transparency has operational value beyond the immediate transaction.

Where The Evolution Goes Next?

The trajectory from centralized to hybrid is clear in retrospect. Where the evolution goes from the current hybrid frontier involves more uncertainty, but the directional forces are identifiable.

Cross-chain hybrid infrastructure is the most significant near-term development. Current hybrid systems generally operate within chain boundaries, aggregating liquidity on a specific network or between networks through defined bridge infrastructure.

Truly seamless cross-chain hybrid execution, where the user requests a swap and the system routes across chain boundaries as naturally as it routes within them, is technically achievable and commercially compelling. The infrastructure complexity is substantial. The user experience improvement it enables justifies that complexity.

Regulatory clarity will shape hybrid architecture development significantly over the next several years. Jurisdictions that develop clear frameworks for non-custodial exchange infrastructure will see hybrid platforms optimize for compliance within those frameworks.

Jurisdictions that remain ambiguous will see hybrid platforms designed for maximum flexibility. The regulatory environment is a design constraint that the best hybrid infrastructure builders are already building around rather than ignoring.

The US government has transferred about 8.2 Bitcoin, valued at over $606,000, to Coinbase Prime. The funds are linked to assets seized from the 2016 Bitfinex hack. Blockchain data tracked the movement and confirmed the destination.

The transfer is part of a broader restitution process approved by a federal court. Authorities are returning seized Bitcoin to Bitfinex instead of selling it. This move follows earlier transfers made in March and April 2026.

Bitcoin Transfer Linked to Restitution Process

The transaction was split into two parts, with 7.999 BTC and 0.197 BTC sent in sequence. Both amounts were directed to the same Coinbase Prime address. On-chain data confirmed the movements and timing.

This transfer follows a legal order issued in early 2025. The ruling required that recovered Bitcoin be returned directly to Bitfinex. The court recognized the exchange as the sole victim in the case.

Exchange transfers often raise concerns about possible selling. However, this case differs due to legal restrictions. The transferred Bitcoin is not intended for open market liquidation.

Federal authorities continue to manage a large Bitcoin reserve. As of April 2026, government wallets hold about 328,361 BTC. The latest transfer represents only a small portion of that total.

Background of the 2016 Bitfinex Hack

The Bitfinex hack occurred in August 2016 and significantly impacted the cryptocurrency market at the time. Hacker Ilya Lichtenstein exploited a system weakness and stole over 119,000 BTC. The stolen assets were worth $72 million then.

Over several years, Lichtenstein and Heather Morgan attempted to move the funds through layered transactions. Their actions aimed to hide the origin of the Bitcoin. Authorities tracked the activity over time.

In February 2022, the US government seized about 94,636 BTC. Investigators accessed private keys stored in cloud files. These keys allowed direct control of the stolen assets.

Lichtenstein later received a five-year prison sentence in November 2024. Morgan was sentenced to 18 months. Both had pleaded guilty to money laundering charges earlier.

Bitfinex Plans for Returned Bitcoin

Bitfinex has outlined how it will use the returned Bitcoin. The exchange plans to redeem its Recovery Right Tokens fully. These tokens were issued after the 2016 hack.

In addition, Bitfinex will allocate at least 80 percent of remaining proceeds. The funds will go toward buying back and burning UNUS SED LEO tokens. This plan follows commitments made in its recovery framework.

A statement tied to the plan noted that the process would follow existing agreements. It said, “the funds will be used according to the recovery commitments already defined.” This reflects a structured use of the returned assets.

The recent transfer marks another step in the restitution timeline. While the amount moved is small, it aligns with court directives. Further transfers may follow as the process continues.

Summary

- Coinglass data show about $1.044 billion of Ethereum longs would be exposed to forced liquidations on major centralized exchanges if ETH drops below $2,323.

- On the upside, a clean move above $2,563 would flip pressure onto bears, with roughly $531 million of short positions at risk of liquidation across the same venues.

- The new band extends an April pattern in which more than $1.8 billion of leverage has repeatedly clustered in tight ranges, turning 5–7% moves into outsized liquidations for over‑levered traders.

Fresh Coinglass heatmap data suggest Ethereum is again sitting between two sizeable liquidation walls, with leverage stacked just below and above spot. According to the latest read‑out, if ETH slides below $2,323, cumulative long liquidation intensity on mainstream centralized exchanges would reach around $1.044 billion, while a break above $2,563 would trigger up to $531 million in short liquidations.

Coinglass maps new ETH liquidation corridor

Coinglass describes its liquidation heatmaps as tools to “estimate price ranges where large‑scale liquidation events may occur,” aggregating futures and perpetual swap data from venues such as Binance, OKX and Bybit. The platform notes that liquidations can “cause sharp price movements and significantly impact traders’ positions,” as forced selling or buying cascades once price crosses dense clusters of leverage.

This latest corridor sits on top of an already crowded derivatives tape. Earlier this month, Coinglass data relayed in a crypto.news story showed $1.414 billion of ETH longs at risk below $2,040 and $889 million of shorts exposed above $2,253, with nearly $1.8 billion of combined leverage packed between roughly $1,952 and $2,154. In that earlier setup, even a 5–7% move was enough to threaten a “trapdoor” cascade as price collided with stacked liquidations in both directions.

The updated $2,323–$2,563 band suggests the same basic dynamic is creeping higher as ETH grinds up the chart. Coinglass’ Ethereum dashboard shows current open interest around $32.8 billion and notes that roughly $111.6 million of ETH futures positions have been liquidated over the past 24 hours, a reminder that even smaller intraday moves continue to flush over‑levered traders.

A separate Coinglass analysis highlighted another danger zone at $2,451, estimating that a decisive break above that level would put about $1.473 billion of short positions at risk, while a drop below $2,220 could trigger $1.10 billion in long liquidations. In that note, the firm warned that dense bands of leverage “create mechanical selling or buying” once price crosses key thresholds, amplifying what might otherwise be modest spot moves.

For ETH traders, the message is clear: the next few hundred dollars in either direction sit atop hundreds of millions of dollars in forced‑flow risk. Those running high leverage into the $2,323 downside level or the $2,563 upside pocket are effectively betting they can front‑run a billion‑dollar liquidation wave rather than be crushed by it.

Additionally, recent Ethereum liquidation setups include pieces on the near‑$2,000 “trapdoor” heatmap, the $2,057–$1,863 liquidation walls flagged in February, and this week’s deep‑dive on the looming $2,451 liquidation band.

Bitcoin price prediction turns cautious as BTC failed to sustain its third breakout attempt above $76,000, repeatedly touching the level only to reverse, while 46 consecutive days of negative funding rates on Binance have created the most compressed short positioning since the FTX crash bottom of late 2022.

Summary

- BTC briefly cleared $76,000 before reversing in the most prominent bearish pin bar on the daily chart since the March rejection at $74,500, keeping the asset in the $60K-$75K consolidation range it has occupied for over ten weeks.

- Binance perpetual funding rates have remained negative for 46 straight days even as open interest rises, a combination K33 Research’s Vetle Lunde called historically consistent with “attractive entry points” for contrarian longs.

- Three catalysts will resolve the range over the next two weeks: the Iran ceasefire expiry April 22, the FOMC meeting April 28-29, and any CLARITY Act markup announcement from Senator Tim Scott.

Bitcoin (BTC) price prediction now hinges on whether the third rejection at $76,000 is the final compression before a short squeeze or evidence that a sustained break higher requires a macro catalyst that has not yet arrived. BTC slid back below $74,000 after briefly clearing the resistance level, extending a ten-week consolidation in the $60K-$75K corridor.

The rejection printed a textbook bearish pin bar on the daily chart, with price spiking above $76,000 before closing well inside the range — the same pattern that produced the prior three failed breakouts in 2026.

The most technically significant signal in the current setup is the 46-day streak of negative perpetual funding rates on Binance, even as open interest in BTC futures has been rising throughout the same period. Negative funding means that short sellers are paying long holders to maintain their positions, a reliable indicator that the market’s speculative lean is heavily skewed toward expecting a price decline.

K33 Research head of research Vetle Lunde flagged the dynamic in a recent report, noting the 30-day average funding rate has now run negative longer than at almost any point in BTC’s history outside of the FTX crash bottom in November 2022. That regime also featured rising open interest alongside negative funding, and it resolved with a sharp upside move once sellers exhausted themselves.

The pattern does not guarantee a rally. But the math is simple: the longer shorts remain crowded below $76,000 with no follow-through to the downside, the more compressed the eventual move becomes in either direction.

Three Catalysts That Could Break the Range

BTC is 42% below its October 2025 all-time high of $126,198. The $60K-$75K consolidation has now held for the third consecutive month. Breaking out in either direction requires one of three near-term events.

The Iran ceasefire expires April 22. A credible extension or diplomatic breakthrough toward a permanent deal would likely replicate the 5% BTC surge that followed the original ceasefire announcement, as the asset has been trading as a high-beta geopolitical barometer throughout the conflict. A full resumption of fighting would likely push BTC back toward the $68,000 structural support floor.

The FOMC meets April 28-29. Bitcoin performs best in easing liquidity environments, and a dovish signal from Chair Powell’s final meeting would lower the opportunity cost of holding risk assets.

A confirmed CLARITY Act markup date from Senate Banking Committee Chair Tim Scott would add a third potential catalyst, with JPMorgan estimating such a development as a standalone positive trigger for digital assets.

Below $68,000, ETF inflows would likely need to accelerate substantially to prevent a test of $65,000, the lower bound analysts have identified as the next structural support. A confirmed close above $76,000 targets $80,000 as the next resistance.

Crypto World

Bitcoin Price Prediction: Pepeto Passes $9.13 Million as Morgan Stanley ETF Hits $100M and BNB Holds Support

The bitcoin price prediction picked up momentum after Morgan Stanley’s MSBT spot Bitcoin ETF pulled in more than $100 million in its first six trading days according to CoinGecko. But many people searching for the bitcoin price prediction are looking for more than a 12% recovery on a $1.48 trillion asset.

Pepeto is the presale drawing capital right now. The exchange has raised more than $9.13 million in presale, SolidProof audited every contract before the first round opened, and the Binance listing is getting closer with projections at 100x from the current price.

Morgan Stanley ETF Hits $100M in Week One as Bitcoin Price Prediction Models Move Higher

Morgan Stanley’s MSBT spot Bitcoin ETF drew over $100 million during its first week, the fastest ETF launch in the firm’s history, with the lowest fee structure among all competing products according to CoinGecko. Total spot Bitcoin ETF assets sit at $95 billion, covering 6.4% of Bitcoin’s $1.48 trillion market cap.

The growth arrived as Bitcoin climbed above $74,400 following a ceasefire between the US and Iran, and funding rates on Binance perpetuals stayed negative for 46 straight days, a setup that K33 Research says has historically come before sharp upside moves.

The outlook gains strength from record institutional flows, but presale entries with verified exchange tools are where the returns that change portfolios are being built.

Where the Bitcoin Price Prediction Lands and Where the Real Opportunity Lives

Pepeto: The Exchange Where $9.13 Million in Committed Capital Proves Informed Money Already Moved

The real signal is not that Morgan Stanley broke records with a Bitcoin ETF. It is that more than $9.13 million flowed into Pepeto while fear gripped the market while the market sat frozen. That pattern shows who is building positions and what they expect once trading opens.

Pepeto is the exchange built to protect your full balance before you risk it anywhere. PepetoSwap processes every swap without charging a fee. When you move tokens between networks, the bridge sends the full amount with nothing deducted. And the screener scans every contract and tells you clearly if it is clean or risky, all verified by SolidProof.

The creator who took the original Pepe to an $11 billion valuation designed the full product lineup and added a former Binance listing lead for the debut.

At $0.0000001865, BTC targets $80,000 for a 7% move over months while analysts project 100x from the Pepeto listing alone. Staking at 183% APY compounds your position every day, and the wallets moving in now already ran the numbers.

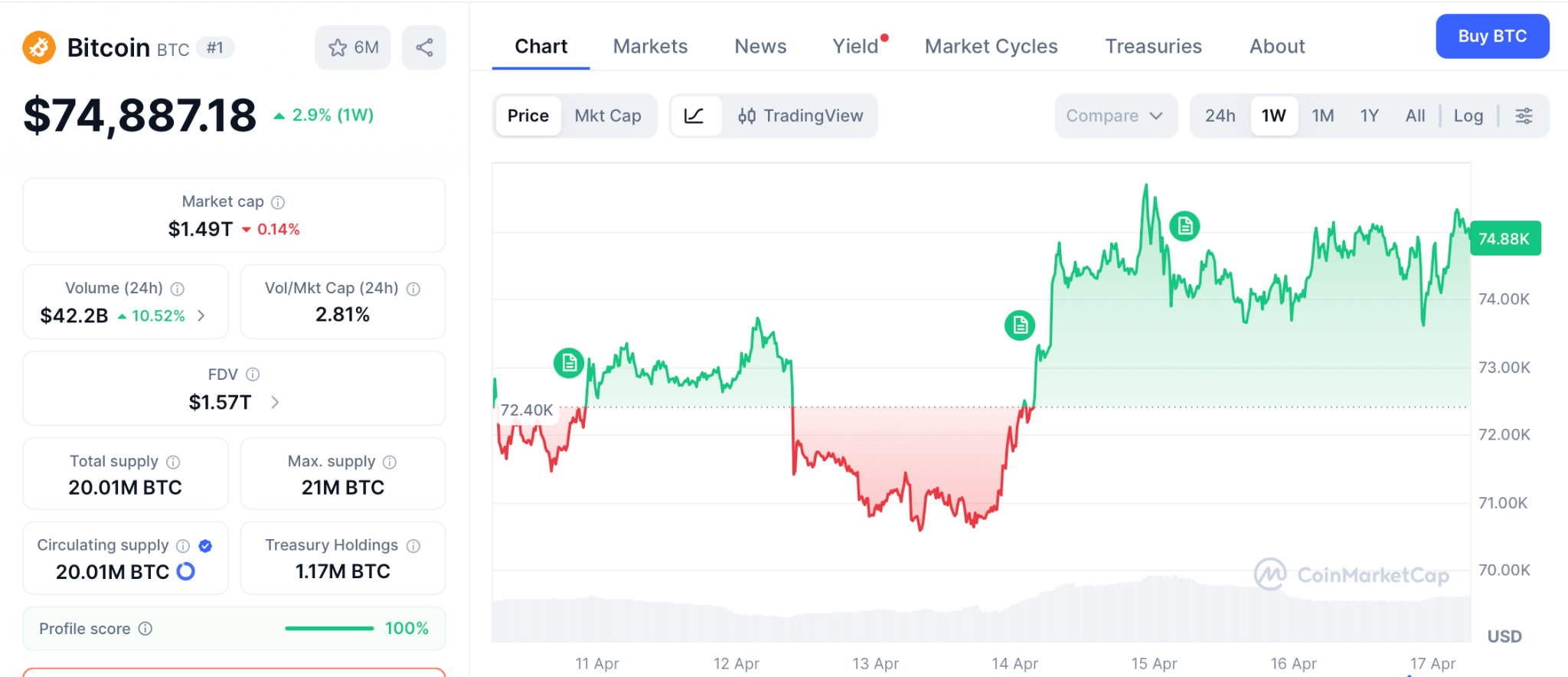

Bitcoin (BTC) Price at $74,887 as Morgan Stanley ETF Breaks Records and Funding Rates Signal a Bottom

Bitcoin (BTC) trades at $74,887 according to CoinMarketCap, up 0.89% on the day as Morgan Stanley’s MSBT drew over $100 million in its first week and total spot ETF assets held at $95 billion.

Funding rates on Binance perpetuals have stayed negative for 46 days according to CoinDesk, a setup K33 Research says has come before every major rally since 2023.

Analysts target $80,000 near term for a 7% return over months. Record institutional demand is bullish for the bitcoin price prediction. But Pepeto at presale holds the kind of multiplier that a $1.48 trillion asset cannot generate.

Binance Coin (BNB) Price at $619 as BNB Chain Zero Fee Program Holds Through April

Binance Coin (BNB) trades at $619 according to CoinMarketCap, down 0.76% as BNB Chain continued its fee-free stablecoin initiative through April 30. BNB dropped 21% from its January high near $780 but outperformed Bitcoin’s drawdown from its October all-time high.

Support holds at $583 with resistance at $650. A breakout to $700 gives 13% over months, while Pepeto at presale pricing carries the same setup BNB had when it traded at $0.15.

Conclusion

While the bitcoin price prediction points to steady recovery and BNB grinds against resistance over months, Pepeto continued attracting capital because $9.13 million raised while fear peaked is not accidental. It is informed money that already ran the numbers.

The same cofounder who built Pepe to $11 billion with nothing behind it created a full exchange this time, the SolidProof audit cleared every contract, and the Binance listing unlocks the return. Days after launch, presale buyers will face just one choice: sell on the 50x or hold for more. Everyone who missed it will carry the same feeling as those who passed on DOGE and Shiba Inu early.

Click To Visit Pepeto Website To Enter The Presale

FAQs

What is the bitcoin price prediction after Morgan Stanley’s ETF broke records in week one?

Bitcoin targets $80,000 near term after Morgan Stanley’s MSBT pulled in $100 million in six days and total spot ETF assets held at $95 billion. Pepeto at presale carries the 100x projected from the Binance listing.

How does Binance Coin compare to Pepeto for returns at BNB’s current price?

Binance Coin (BNB) trades at $619 with a $700 target for 13% over months from an $83 billion cap. Pepeto through the Pepeto official website offers presale entry and 100x listing returns that BNB at this size cannot match.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

Bitcoin technical analysis turned decisively bullish Thursday as BTC cleared $77,000 and climbed above its 100-day moving average for the first time since the early February selloff, triggering a 12%+ surge in Strategy shares as the company’s 780,897-BTC treasury gained roughly $1.6 billion in value in a single session.

Summary

- BTC absorbed $450 million in sell orders stacked between $75,900 and $76,300, breaking through resistance that has rejected price three times over the prior two months.

- Strategy jumped over 12% on the BTC move, extending a run since the company’s April 13 disclosure that it purchased 13,927 BTC for $1 billion at $71,902 per coin using proceeds from its STRC preferred stock ATM program.

- Derivatives data show a 140% jump in liquidations alongside rising open interest, signaling forced short covering rather than primarily new long buying, consistent with the squeeze thesis K33 Research had flagged.

Bitcoin (BTC) technical analysis produced a breakout signal Thursday as BTC cleared $77,000 and reclaimed its 100-day moving average, a threshold that has acted as resistance since the early February decline from above $90,000. The move marks BTC’s first decisive close above $77,000 since that selloff and represents the resolution, at least temporarily, of the ten-week $60K-$75K consolidation range that had defined the chart.

Strategy, the largest publicly traded corporate Bitcoin holder, surged over 12% in Thursday trading. The company holds 780,897 BTC acquired for approximately $59.02 billion at an average cost of $75,577 per coin.

The $76,000 level had capped four separate BTC rally attempts in 2026 before today. CoinGlass data showed $450 million in sell orders stacked between $75,900 and $76,300 as of Thursday morning, placed by traders either shorting the range high or defending against a short squeeze with liquidation risk overhead. Price chipped through the wall across the morning session, triggering a cascade as liquidation levels were breached.

Derivatives data confirmed the mechanical nature of the move: liquidations jumped 140% compared to recent sessions, and open interest continued to rise throughout the advance. Rising open interest alongside rising liquidations indicates forced short covering rather than new speculative buying, the exact setup K33 Research’s Vetle Lunde described last week when he flagged 46 consecutive days of negative funding as an “attractive entry” for contrarians.

Why Strategy Moved So Sharply

Strategy’s 12%+ gain amplified BTC’s move through its leveraged capital structure. The company holds 780,897 BTC worth roughly $1.6 billion more at $77,000 than at $74,000, with every dollar of BTC appreciation flowing directly through to the balance sheet under FASB’s fair-value accounting rules now governing digital assets.

On April 13, Strategy disclosed its latest purchase: 13,927 BTC for approximately $1 billion, funded entirely through sales of its STRC preferred shares. The company’s STRC volume has surged to roughly 20% of total MSTR trading volume from essentially zero earlier in 2026, reflecting a shift in how institutional capital is accessing the company’s Bitcoin exposure.

The company’s average cost basis of $75,577 per BTC means Thursday’s move above $77,000 pushed its entire treasury back into a small unrealized gain for the first time since early April, a shift that reduces near-term balance sheet pressure and may support continued STRC issuance.

Bitcoin reclaiming the 100-day moving average is a structural signal that technical traders track carefully. A sustained daily close above it would target $80,000 as the next resistance, with the 200-day SMA at $87,519 as the larger trend line that needs to be reclaimed for a full trend reversal. The BTC ETF inflow picture from the past week, which showed $597.5 million in two-day institutional buying, suggests demand is present to absorb further supply if the macro backdrop cooperates.

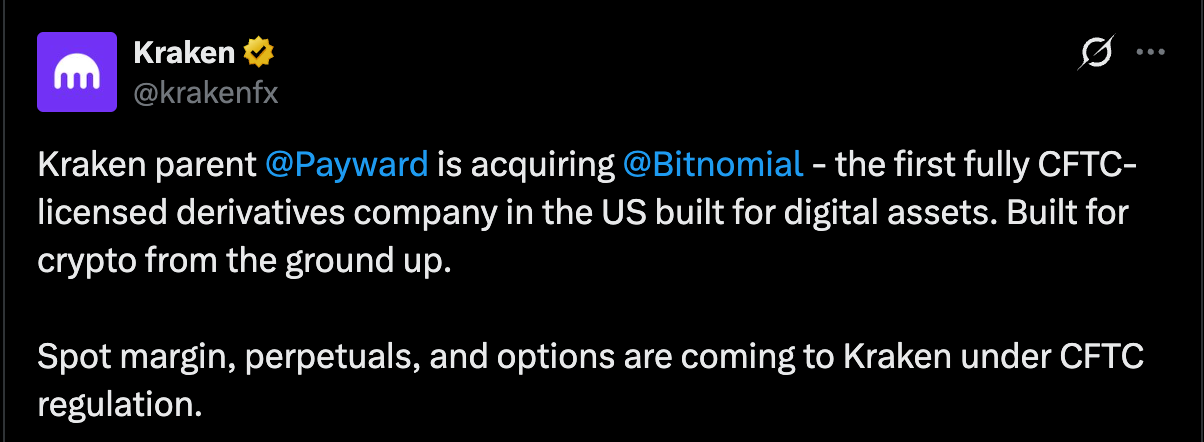

Payward, the parent company of the Kraken cryptocurrency exchange, announced on Friday that it has entered into a “definitive agreement” to acquire Bitnomial, a US-licensed cryptocurrency and derivatives exchange; the deal values Bitnomial’s equity at $20 billion.

Bitnomial is the “first” crypto-native exchange in the United States to hold all three regulatory licenses from the Commodity Futures Trading Commission (CFTC), including exchange, clearinghouse, and brokerage permits, according to Payward’s announcement.

“Settlement mechanics, margin models, and contract structures define what products can exist and who can access them. The US has had no clearing infrastructure built for digital assets,” Arjun Sethi, Co-CEO of Payward and Kraken, said. He added:

“Bitnomial spent a decade building it: crypto settlement, crypto collateral, continuous 24/7 markets. These are capabilities that cannot be retrofitted onto legacy systems. They have to be built natively.”

Payward will use Bitnomial’s infrastructure to offer spot margin trading, perpetual futures contracts and options trading for US clients, the company said.

Payward’s business clients can also integrate crypto services for their users, including spot crypto trading, tokenized stocks, crypto derivatives and fiat onramps through Payward Services, an application programming interface (API).

The announcement follows Kraken’s expansion into tokenized stocks, tokenized perpetual futures trading and the company securing a limited-purpose account with the United States Federal Reserve, a first for the crypto industry.

Related: Deutsche Börse invests $200 million in Kraken parent Payward

Kraken secures Federal Reserve limited-purpose master account

In March 2026, Kraken became the first crypto company to gain approval for a limited-purpose master account, which was issued by the Federal Reserve Bank of Kansas City, one of the US central bank’s 12 regional districts.

The account gives Kraken access to the Federal Reserve’s central payment system used by banks, credit unions and other traditional financial institutions, so it can settle transactions directly through the Fed’s Fedwire platform.

However, the limited-purpose master account has a term of one year and features some restrictions.

Kraken’s limited-purpose account is similar to the ‘skinny’ Federal Reserve master accounts proposed by Federal Reserve Governor Christopher Waller and promoted by Wyoming Senator Cynthia Lummis in 2025.

Magazine: Robinhood’s tokenized stocks have stirred up a legal hornet’s nest

TLDR:

- Bitcoin trades below key moving averages, indicating weak momentum and reduced support for altcoin growth.

- Rising Bitcoin dominance shows capital concentration, limiting liquidity flow into altcoins during this phase.

- Historical patterns suggest altcoins perform best when Bitcoin trends steadily above major moving averages.

- Current market structure reflects a defensive phase, with traders favoring Bitcoin over higher-risk altcoins.

Bitcoin’s recent price action has drawn attention as traders reassess altcoin exposure during a shifting market cycle.

A widely shared market chart now signals caution, suggesting current conditions may not favor altcoin accumulation amid weakening momentum and declining trend strength.

Market Structure Signals Shift in Momentum

A recent post by Our Crypto Talk outlines a structured approach to identifying favorable altcoin conditions. The framework relies on two moving average signals that define market phases.

These include price positioning above the 20-day moving average and the 20-day remaining above the 50-day moving average.

According to the shared chart, these conditions are not currently met. Bitcoin is trading below both moving averages, while the short-term average is trending downward toward the long-term line.

This configuration reflects weakening short-term momentum within the broader market structure.

The chart also maps historical cycles, showing how similar setups aligned with previous market phases. During 2021, price action remained above key averages, coinciding with strong altcoin rallies.

However, the current setup resembles earlier correction periods where capital shifted away from altcoins. At the same time, Bitcoin dominance stands near 57%, indicating capital concentration in the leading asset.

This level often coincides with reduced appetite for higher-risk altcoin exposure. As a result, traders appear to favor defensive positioning during this phase.

Historical Cycles Guide Altcoin Timing

The chart divides market behavior into green and red zones, each representing distinct trading environments. Green zones indicate favorable altcoin conditions, typically forming during controlled Bitcoin uptrends. Red zones, however, align with corrections or late-cycle phases where altcoins tend to underperform.

Historical data within the chart shows that green zones appeared during the 2020–2021 expansion and the 2023–2025 recovery period.

These phases saw Bitcoin rise steadily while liquidity expanded into altcoins. In contrast, red zones marked the 2022 bear market and the current correction phase.

Price levels further support this interpretation. Bitcoin recently pulled back from highs above $120,000 to a range near $70,000–$80,000.

This movement places the asset near a key support zone between $74,000 and $77,000. Meanwhile, resistance remains near $96,000 and extends toward previous cycle highs.

The post also stresses that timing altcoin entries requires patience rather than precision. Waiting for confirmed trend alignment may reduce exposure to prolonged drawdowns. Attempting to identify exact bottoms, on the other hand, often carries a higher risk during unstable phases.

Looking ahead, market participants are watching whether Bitcoin stabilizes within its current range. A sustained recovery above key moving averages could signal the return of favorable conditions.

Until then, the chart suggests a continued defensive phase where capital preservation remains a priority.

Two Tether-related entities, German former crypto miner Northern Data and US-based video streaming service Rumble, are set to begin the merger process, with Rumble offering equity for shares of Northern Data.

The merger, which was announced in November of last year, will end with Rumble taking over data center sites and receiving thousands of GPU servers. Tether owns a majority of Northern Data and 30% of Rumble.

Shareholders in Northern Data will receive 2.0281 shares of Rumble stock for each share they hold. Northern Data is currently trading at $13 a share and Rumble is trading at $6.41 a share.

A strange merger that’s good for Tether

From an outside perspective, a defunct mining company and a video streaming service merging doesn’t make a lot of sense. However, in November Christ Pavlovski, the CEO of Rumble, said, “Northern Data. Tether. Rumble. This is how we build the AI ecosystem for the future, from the ground up.”

It’s unclear what Tether or Rumble have to do with AI.

What’s more clear is that the merger will ultimately benefit Tether, which has already committed to purchasing $150 million in compute from Rumble over the next two years and will have a $610 million unsecured debt financing facility provided to Northern Data now reassessed and altered.

Financial Shenanigans

The merger of the two Tether-related companies required little agreement from minority shareholders due to Tether’s strong influence, Rumble’s executive equity structure, and Northern Data’s financial struggles over the past several years.

Both Northern Data and Rumble have seen the price of their stocks slide post-Tether investment, with Rumble trading near all-time lows as of recent.

Since the merger has begun the stock has rallied 20%.

The financial shenanigans involved in the Tether-related deal is nothing new for the company, which has been dogged by a long list of controversies around audits, hacks, and scams.

Read more: Tether-owned Northern Data considers ditching bitcoin mining

Since the collapse of FTX and the election of Donald Trump, Tether has attempted to present itself as transparent and safe, and has made a massive push into the US market. This includes lobbying efforts that saw CEO Paulo Ardoino visit the White House multiple times.

US Secretary of Commerce, Howard Lutnick, used to run Cantor Fitzgerald, which purchased US treasury notes for the company and previously said he was “a big fan of the company.”

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

Bitcoin (BTC) rallied above $78,000 to hit another 10-week high on Friday as crypto and equity markets reacted to cooling tensions in the US and Israel war in Iran. The rally above range highs also resulted in a large liquidation of leveraged Bitcoin positions.

More than $660 million in short positions were liquidated, with Bitcoin accounting for $353 million of that total. Ether (ETH) followed with $160 million in short liquidations.

Related: Three things Bitcoin must do to hold highs above $76K: Analysts

Across the board, $826 million was wiped from the futures market over the last 24 hours.

The single biggest liquidation occurred on Hyperliquid, where a $15.75 million BTC-USDT short position was closed.

Large clusters of short liquidations typically amplify the reach of asset rallies and data from CoinGlass showed a 13% rise in Bitcoin’s aggregate futures open interest (OI) over the last 24 hours.

Even though futures longs (buyers) and shorts (sellers) are always matched, rising OI suggests greater leverage and market participation, which, in this case, appears to be on the side of bulls.

Hyblock data showed ask liquidity sitting between $77,500 and $78,000 being absorbed as BTC rallied to its intra-day highs on Friday.

Bitcoin MACD forecasts a “big move“

Bitcoin’s moving average convergence divergence (MACD) indicator has signaled a buy on its weekly chart, a pattern that has historically preceded sharp price rallies.

The MACD is a popular momentum indicator used in technical analysis that helps traders identify the strength, direction and duration of a trend of an asset’s price.

The indicator reached its lowest level in history and has formed a bullish cross on the weekly chart, as shown in the figure below.

“Not only do we have a 1W MACD bullish cross and break of trend, we have it from the lowest point the MACD has ever dropped to,” analyst Sykodelic said in a recent post on X, adding:

“We are at a very important level here, and the weekly close will be very important.“

Previous instances show that Bitcoin tends to rise sharply when the MACD line (blue) crosses above the signal line (orange). The last time this happened was at the bottom of the 2022 bear market, which preceded a 376% increase in BTC price.

“A big move usually follows whenever this weekly MACD bullish cross happens,” analyst Mikybull Crypto said in a recent post on X.

Fellow analyst The Chart Report told their followers that previous crossovers have “historically produced a 93% win rate with a median 12-month return of +195%.”

Other Bitcoin analysts suggest that the altcoin could continue its recovery to retest higher resistance levels, with BTC price targets set at $90,000 and above.

This article is produced in accordance with Cointelegraph’s Editorial Policy and is intended for informational purposes only. It does not constitute investment advice or recommendations. All investments and trades carry risk; readers are encouraged to conduct independent research before making any decisions. Cointelegraph makes no guarantees regarding the accuracy or completeness of the information presented, including forward-looking statements, and will not be liable for any loss or damage arising from reliance on this content.

Pi Mainnet is moving toward Protocol 22, with April 27 set as the deadline tied to node readiness. The update puts fresh attention on Pi Node, which supports network security and transaction flow on desktop devices.

The move also renews focus on Pi’s long-running node plan. Pi’s own notice says parts of its early node document may not be up to date, yet the role of nodes remains clear.

Pi Node Remains Central to the Network Design

Pi Node is the fourth role in the Pi ecosystem.

It runs on laptops and desktops, while mobile users keep using the Pi app.

The system does not use proof of work like Bitcoin. Instead, Pi says it uses a model based on the Stellar Consensus Protocol.

Under that design, nodes form trusted groups called quorum slices. They agree on transactions only when trusted nodes reach agreement.

Pi says this trust model connects with security circles from mobile miners. Those circles help form a wider trust graph for validation.

Protocol 22 Deadline Brings Node Readiness Into Focus

With the April 27 deadline now in focus, node reliability becomes a key part of the discussion. Pi has said nodes help validate transactions and submit them to the blockchain.

SuperNodes carry a larger role in the network. They reach consensus, write transactions to the ledger, and keep other nodes updated.

Pi also says selected node operators must meet technical and account checks. These include uptime, internet stability, hardware capacity, and KYC after invitation.

The project has also said one account should run only one node. That rule links node participation to the same account used on the mobile app.

Pi Keeps a Phased Path for Node Development

Pi’s node plan has followed a staged testnet path. It began with a selection stage, then moved into revision work, and then live testnet activity.

In the selection stage, Pi assessed devices, connection quality, and software setup. The aim was to learn what was needed for a stable and secure network.

During the revision stage, Pi used a centralized layer for faster testing. The company said this helped it simulate many network conditions and stress the consensus model.

Pi has also said that this layer would be removed for mainnet after testing. That point matters as the network now moves around the Protocol 22 deadline.

Pi’s notice also says mainnet nodes are under a firewall during the Enclosed Network period. It adds that broader community access is planned for the Open Network period.

These Are The US’ Fastest-Selling Lexus Models In 2026 (So Far)

US Shifts Seized Bitfinex Hack Bitcoin Worth $606K to Coinbase Prime

Akon Talks Gender Roles, Polygamy & More

-

Business7 days ago

Business7 days agoTesla Model Y Tops China Auto Sales in March 2026 With 39,827 Registrations, Beating Cheaper EVs and Gas Cars

-

Politics5 days ago

Politics5 days agoWorld Cup exit makes Italy enter crisis mode

-

NewsBeat5 days ago

NewsBeat5 days agoPep Guardiola and Gary Neville agree over Arsenal title problem that benefits Man City

-

Crypto World4 days ago

Crypto World4 days agoThe SEC Conditionalises DeFi Platforms to Be Avoided for Broker Registration

-

Crypto World4 days ago

Crypto World4 days agoSEC Signals Exemption for Crypto Interfaces From Broker Registration

-

News Videos3 days ago

News Videos3 days agoSecure crypto trading starts with an FIU-registered

-

Sports11 hours ago

Sports11 hours agoNWFL Suspends Two Players Over Post-Match Clash in Ado-Ekiti

-

Crypto World4 days ago

Crypto World4 days agoSEC Proposes Certain Crypto Interfaces Don’t Need to Register as Brokers

-

Business6 days ago

Business6 days agoIreland Fuel Protests Enter Day 5 as Blockades Spark Shortages and Government Prepares Support Package

-

NewsBeat3 days ago

NewsBeat3 days agoTrump and Pope Leo: Behind their disagreement over Iran war

-

Crypto World7 days ago

Crypto World7 days agoFederal judge blocks Arizona from bringing criminal charges against Kalshi

-

NewsBeat6 days ago

NewsBeat6 days agoJD Vance announces ‘no agreement’ with Iran over nuclear weapons fear

-

Business7 days ago

Business7 days agoIMF retains floor for precautionary balances at SDR 20 billion

-

Sports6 days ago

Dexter Lawrence, Stefon Diggs, Trading for De’Von Achane

-

Business7 days ago

Business7 days agoFormer Liverpool CEO eviscerates FIFA for World Cup ticket pricing

-

Crypto World5 days ago

Sei Network Enters Quiet Reset Phase as On-Chain Metrics Signal a Slowdown in 2026

-

Crypto World5 days ago

Crypto World5 days agoTrump whales load up ahead of Mar-a-Lago luncheon.

-

Business7 days ago

Coreweave CSO Venturo sells $5.5m in class a common stock

-

Sports7 days ago

1st-Round WR Enters Vikings Mock Draft Orbit

-

Business5 days ago

Kering slides after Morgan Stanley downgrade, Gucci woes loom

You must be logged in to post a comment Login