Crypto World

Justin Sun Takes Legal Action Against World Liberty Financial Over Frozen Crypto Holdings

TLDR

- Justin Sun, founder of Tron, initiated legal proceedings against World Liberty Financial in California’s federal court system

- The lawsuit alleges WLFI improperly froze Sun’s token holdings, stripped voting privileges, and issued threats to destroy his assets

- Sun attempted private resolution before pursuing litigation

- A new governance measure would permanently lock tokens of holders who don’t consent to new terms

- Sun maintains his support for President Trump’s cryptocurrency initiatives despite the legal conflict

Justin Sun, the blockchain entrepreneur behind Tron, has initiated legal proceedings against World Liberty Financial—a cryptocurrency venture supported by the Trump family—in California’s federal court.

According to Sun’s complaint, the World Liberty Financial team improperly locked his token holdings, eliminated his governance voting capabilities, and issued threats to permanently destroy his investment without providing adequate justification.

Sun maintains he pursued private negotiation channels before resorting to legal action. When the WLFI management refused to restore access to his frozen assets, he determined that litigation was his only remaining recourse.

Previously recognized as World Liberty Financial’s most significant external investor, Sun has now emerged as the project’s most outspoken detractor.

On April 12th, Sun made public allegations that WLFI developers had secretly incorporated a blacklist mechanism within the project’s smart contract infrastructure. This hidden functionality, he asserts, grants the development team authority to freeze, limit, and essentially seize investor assets.

World Liberty Financial addressed these accusations on their social channels, dismissing them as “baseless allegations” and portraying Sun as someone “playing the victim.” The organization suggested imminent legal proceedings with the statement: “See you in court pal.”

The Governance Dispute

The situation intensified following World Liberty‘s April 15th release of a governance resolution. This measure proposes converting more than 62 billion WLFI tokens from unlimited lockup periods into predetermined vesting timelines.

The resolution establishes that founders, development personnel, and advisors would face a two-year token freeze, followed by incremental distribution across three additional years. Additionally, a 10% token destruction would occur upon proposal approval.

Investors declining to accept these revised conditions would see their holdings locked permanently under the current framework.

Sun characterized the resolution as “one of the most absurd governance scams” he’s encountered. He contends it masquerades as a governance initiative while actually functioning as an investor trap for those who don’t actively participate.

Due to his frozen token status, Sun reports he’s completely unable to participate in the voting process—neither in support nor opposition.

Sun Still Backs Trump Despite Legal Fight

Sun emphasized through his public statements that this legal action doesn’t represent opposition to President Trump or his administration’s initiatives.

“Unfortunately, certain individuals on the World Liberty project team have been operating the project in a manner that goes against President Trump’s values,” Sun wrote.

Sun reportedly ranks among the top holders of the TRUMP memecoin. This substantial investment secured him access to an exclusive cryptocurrency gala dinner in May 2025, where he received a commemorative watch during the event.

Analytical data from CoinCarp reveals 642,882 holders of the TRUMP memecoin currently exist. More than 91% of total supply concentration resides within the top 10 wallet addresses.

World Liberty Financial has not issued any official statement regarding the lawsuit when approached by journalists.

Laundering of the proceeds from Saturday’s $290 million rsETH hack is well and truly underway, and state-sponsored North Korean hacking collective Lazarus Group is suspected to be behind the theft, given the commingling of funds with other TraderTraitor-related hacks, BTC Turk and ByBit.

As with previous incidents, the culprits have taken to funneling vast volumes through blockchain bridges. The tools used so far even include LayerZero, the bridging protocol from which the $290 million rsETH were originally stolen.

Read more: DeFi sector in $14B meltdown as $290M rsETH hack fallout burns Aave

The efforts began shortly after Arbitrum’s Security Council rescued over 30,000 ether (ETH), slashing the hackers’ realized profit from $245 million to around $175 million.

One on-chain analyst, who goes by “Specter,” claims to have tracked over 1,600 transactions via 370 addresses in the first 12 hours of laundering. That’s an average of one transaction every 25 seconds.

As of Wednesday morning, they tallied $116 million as having been laundered to bitcoin (BTC), with another wallet currently holding $61 million still to go.

Read more: DeFi plays the blame game

Mixed reactions

The projects behind the bridges themselves have responded differently to the ill-gotten gains flowing through their tech.

Privacy protocol Umbra acknowledged that $800,000 worth of ETH had passed through its system. While the project underlined its inability to stop illicit use of its autonomous smart contracts, it did put its own hosted front end into “maintenance mode.”

THORChain, as usual, washed its hands of responsibility, with varying degrees of diplomacy.

Read more: Vultisig founder says DPRK-linked Bybit transactions are ‘legitimate’

Specter estimates that 99% of the laundered funds flowed through THORChain, whose dashboard shows over $100,000 of affiliate fees earned on Tuesday.

While THORChain’s bridging infrastructure is decentralized across a network of 95 active nodes, affiliate fees come from use of its front end. Blockchain investigator Tanuki42 puts the recent fees at more than double year-to-date revenue.

In attempting to defend THORChain’s inability to prevent illicit use, founder JP let slip that the protocol held an admin key for many years.

Read more: DeFi karma: Garden hacked for $11M after bridging Lazarus’ loot

No let up

The DeFi sector has faced two catastrophic hacks so far this month, with combined losses of well over half a billion dollars.

On top of this, a slew of smaller incidents also continue to batter community morale.

While DeFi users and developers alike are still reeling from the fallout of Saturday’s incident, just last night a further $3.5 million was lost.

Read more: Inside the $280M Drift hack: weeks of setup, minutes to drain

Since the hack, Volo has provided two separate updates, informing users it had recovered $500,000, and then 19.6 BTC ($1.3 million).

As if near constant multi-million dollar hacks weren’t enough to worry about, ongoing phishing campaigns continue to hook victims.

In a span of just 11 hours, four victims reportedly lost almost $600,000 to the same drainer contract.

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

Solana price has rebounded by 6% since its Monday drop as investor confidence returns to the market. It is in the process of forming a double bottom pattern, which could position it for a significant trend reversal in the coming sessions.

Summary

- Solana rose to $88.5 as market sentiment improved, supported by easing geopolitical tensions and rising trading volume.

- The token is forming a double bottom pattern, with a breakout above $97.8 potentially targeting $118.

- Liquidation data shows $20.5 million in short positions near $91, raising the likelihood of a short squeeze on further upside.

According to data from crypto.news, Solana (SOL) price rose 3% to $88.5 on Wednesday, bringing its market cap to over $50 billion. Its gains came amid its daily trading volume rising by 22% to $4.96 billion.

Solana price rose after U.S. President Donald Trump announced an extension of the Iran ceasefire, easing broader macro fears and leading to a relief rally across the entire crypto sector.

The token has also benefited from institutional players doubling down on the token. Notably, Goldman Sachs recently disclosed that it holds $108 million in spot Solana ETFs. At the same time, assets in Solana spot ETFs, including those from Bitwise and Fidelity, have now surpassed $1 billion.

Solana is now in the process of completing a double bottom pattern on the daily, a setup that typically signals a bullish reversal on breakout from the neckline of the pattern. For Solana price, the neckline stands at $97.8, just 10% above the current price.

A decisive breakout could position the token for an upside to $118 with no more major resistance levels on the way. The target is calculated by adding the height of the double bottom formed to the point at which the breakout occurs.

Meanwhile, the Solana weekly liquidation heat map shows a large cluster of dense liquidity at $91, where more than $20.5 million in short positions are currently sitting. If the price reaches this level, it could trigger a short squeeze that accelerates the move toward the neckline.

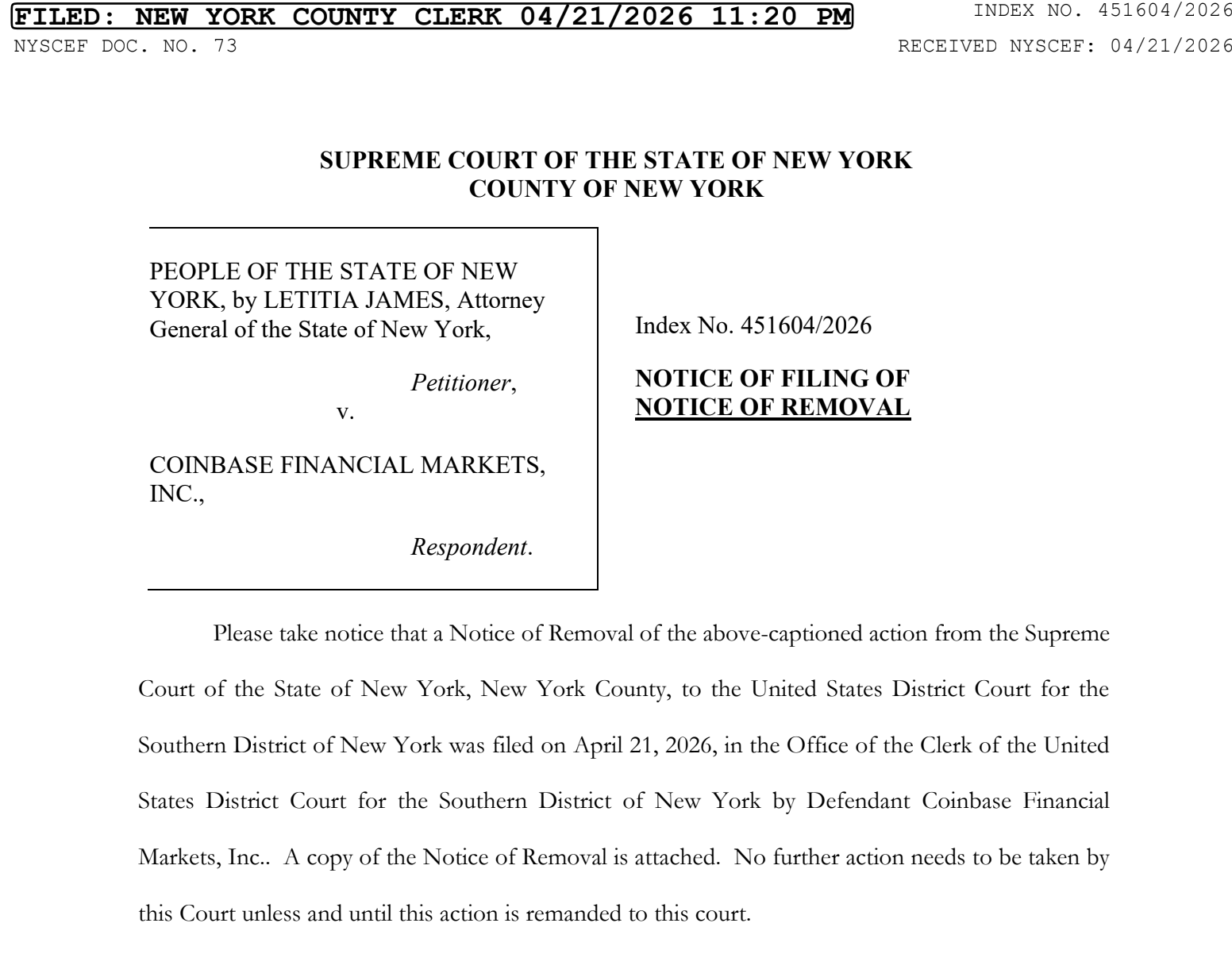

Coinbase’s chief legal officer, Paul Grewal, said Wednesday that the company had removed New York Attorney General Letitia James’ prediction markets lawsuit from state court to federal court, arguing that the case turns on disputed questions of federal law over how event contracts are regulated.

The move escalates a legal fight that could help define whether prediction markets fall under federal commodities regulation and the scope of the US Commodities and Futures Trading Commission’s (CFTC) or state gambling laws, with broader implications for the oversight of platforms like Coinbase and Gemini.

“We have removed this action to federal court,” wrote Grewal in a Wednesday X post, adding that New York’s claims raise “disputed and substantial questions of federal law” and are subject to “complete preemption.”

It comes in response to a Tuesday lawsuit filed by New York’s Attorney General Letitia James against Coinbase Financial Markets and Gemini Titan, alleging their prediction market offerings violate New York gambling law by allowing users to bet on sports, entertainment and elections without a state gaming license, including users between 18 and 20 years old.

Related: Kalshi, Polymarket face trading halt in Nevada after court rulings

The lawsuit seeks fines, forfeiture of alleged illegal profits and restitution for customers, while also asking the court to stop the companies from offering similar products in New York without complying with state law.

Cointelegraph has approached Coinbase for comment on the matter and a copy of the court filing.

State regulators battle for prediction markets jurisdiction

State regulators have stepped up pressure on prediction market platforms in recent months, with 11 states having pursued legal action against them, seeking to assert control over federal regulators.

Coinbase’s Grewal said in a Tuesday X post that prediction markets are “federally regulated national exchanges” under the CFTC and the company will continue to “fight for the federal oversight of these markets that Congress intended.”

Coinbase launched prediction markets across 50 US states, including New York, on Jan. 28, offering trades on “any real-world outcomes” across sports, politics, culture and more.

The New York Attorney General’s lawsuit is the latest sign that state regulators are seeking to assert their jurisdiction over emerging prediction markets, contradicting the CFTC’s stance, which said it has exclusive jurisdiction over prediction markets registered as designated contract markets, such as Polymarket and Kalshi.

On April 2, the CFTC filed three separate lawsuits against the gaming regulators of Illinois, Connecticut and Arizona, arguing that those states could not apply their gambling laws and licensing requirements to event contracts listed on CFTC-regulated platforms.

On April 8, the CFTC and US Department of Justice (DoJ) asked a federal court to block Arizona from enforcing state gambling law against Kalshi’s event contracts, arguing that they fall under the CFTC’s exclusive authority.

Memecoin season keeps printing life-changing trades for people willing to take a shot.

An anonymous wallet bought 2.79 billion ASTEROID tokens for $575 on April 17 and sold the entire position for 503 ETH on Tuesday, worth roughly $1.17 million, according to on-chain tracker Lookonchain. The round trip took five days and produced a return of more than 2,000x.

ASTEROID is an Ethereum-based memecoin branded as “First Shiba In Space.” It is themed after a Shiba Inu drawing by Liv Perrotto, a teenage cancer patient who died in January 2026 after a five-year battle with the disease.

Two years before her death, Perrotto sketched the dog while serving as a volunteer on SpaceX’s Polaris Dawn ground support team. The design, inspired by Musk’s own Shiba Inu named Floki, flew on the Polaris Dawn mission in September 2024 as the crew’s zero-gravity indicator.

Before she passed, Perrotto had written down eight questions she hoped to ask Musk. The final one asked whether Asteroid could become SpaceX’s official mascot. Her mother shared the list publicly after her death, and media personality Glenn Beck amplified it on April 16. The post went viral, reached Musk, and he said “ok” in response to making Asteroid the official SpaceX mascot.

That response ignited the token. ASTEROID’s market cap ran from roughly $50,000 to more than $20 million within hours of Musk’s reply, then pushed past $100 million over the following days on more than $100 million in 24-hour trading volume.

At its peak the token briefly entered the top 200 cryptocurrencies by market cap. As of European morning hours on Wednesday, it trades at $0.0004435 with a $186.5 million market cap and $24 million in 24-hour volume.

The token has no formal SpaceX endorsement, no licensing arrangement, and no confirmed Musk involvement beyond the social media replies.

It trades on Uniswap against wrapped ether with a market cap of $186.5 million and 24-hour trading volume of $24.3 million. Price is up 20.69% over 24 hours, 28.54% over six hours, and has climbed about 10x from the wallet’s entry point on April 17, according to DEX Screener data.

Crypto World

North Korean-backed hackers roll out new attack vector targeting crypto executives and firms

The North Korean state-run Lazarus Group is running a new campaign known as “Mach-O Man” that turns routine business communication into a direct path to credential theft and data loss, security experts warned Wednesday.

The collective, with cumulative loot estimated at $6.7 billion since 2017, is targeting fintech, cryptocurrency and other high-value executives and firms, Natalie Newson, a senior blockchain security researcher at CertiK, told CoinDesk on Wednesday.

In the past two weeks alone, the North Korean hackers have siphoned more than $500 million from the Drift and KelpDAO exploits in what appears to be a sustained campaign. The crypto industry needs to start viewing Lazarus the same way banks view nation-state cyber actors: “as a constant and well-funded threat, not just another news headline,” she said.

“What makes Lazarus especially dangerous right now is their activity level,” Newson said. “KelpDAO, Drift, and now a new macOS malware kit, all within the same month. This isn’t random hacking; it’s a state-directed financial operation running at a scale and speed typical of institutions.”

North Korea has turned crypto theft into a lucrative national industry, and Mach-O Man is just the latest product from that process, she said. While Lazarus created it, other cybercrime groups are also using it.

“It is a modular macOS malware kit created by Lazarus Group’s infamous Chollima division. It uses native Mach-O binaries tailored for Apple environments where crypto and fintech operate,” she said.

Newson said Mach-O Man uses a delivery method known as ClickFix. “It’s important to be clear because a lot of coverage is mixing up two separate things,” she noted. ClickFix is a social engineering technique where the victim is asked to paste a command into their terminal to fix a simulated connection issue.

It works by Lazarus sending executives an “urgent” meeting invite over Telegram for a Zoom, Microsoft Teams or Google Meet call, according to Mauro Eldritch, a security expert and founder of threat intelligence firm BCA Ltd.

The link leads to a fake, but convincing, website that instructs them to copy and paste one simple command into their Mac’s terminal to “fix a connection issue.” In doing so, the victims provide immediate access to corporate systems, SaaS platforms and financial resources. By the time they find out they were exploited, it is usually too late.

There are several variations of this attack, security threat researcher Vladimir S. said on X. There are already cases where Lazarus attackers have hijacked decentralized finance (DeFI) projects’ domains with this new malware by replacing their websites with a fake message from Cloudflare, asking them to enter a command to grant access.

“These fake ‘verification steps’ guide victims through keyboard shortcuts that run a harmful command,” said Certik’s Newson. “The page looks real, the instructions seem normal, and the victim initiates the action themselves — which is why traditional security controls often miss it.”

Most victims of this hack will not realize their security has been breached until the damage has been done, at which time, the malware will have already erased itself as well.

“They likely don’t know it yet,” she said. “If they do, they probably can’t identify which variant affected them.”

Bitcoin is showing short-term relief in price and sentiment metrics, but investors should stay wary of a potential relapse into the 2022 bear-market dynamics. New data from on-chain analytics firm CryptoQuant suggests that Bitcoin’s Bull Score Index (BSI) has moved into neutral territory for the first time in this bear market, even as BTC tries to push toward fresh highs. At the same time, broader market mood appears to be firming, with the Crypto Fear & Greed Index climbing back from extreme fear, hinting at a cautious but improving backdrop for traders and holders.

Key points:

- Bitcoin’s Bull Score Index has reached neutral territory (50) for the first time in this bear market, with BTC rallying toward $78,000.

- CryptoQuant cautions that the relief could be transient, echoing the pattern seen earlier in March 2022 when neutral readings preceded renewed price declines.

- The Crypto Fear & Greed Index has recovered to the 30s, marking the most bullish sentiment since January and signaling a shift, albeit from a still-fragile base.

Bitcoin Bull Score Index exits the “bearish” zone

CryptoQuant’s Bull Score Index, which aggregates nine price metrics to gauge overall momentum, shows Bitcoin entering neutral territory as the price tests the $78,000 level. This marks the first time the index has broken above the early-bear-market axis toward 50 since the downturn began. A CryptoQuant analyst highlighted the milestone in a recent post, noting that it represents a transition point rather than a signal of a lasting trend.

“First time in this bear market that the Bull Score Index enters neutral zone (50),” wrote Julio Moreno on X, underscoring that the shift is a notable, yet potentially fragile, moment. The caution mirrors a familiar pattern from the prior bear cycle, when the bull-score flickered into neutrality only to retreat as selling pressure resurfaced.

The historical context matters. In March 2022, the BSI briefly touched neutral territory for about a week before the price resumed its decline, reminding markets that a neutral reading does not guarantee sustained upside. As market participants monitor April’s monthly close, the key question remains whether BTC can sustain strength beyond a near-term range and break decisively out of a multi-month plateau noted by observers at times this year.

At present, traders are watching for catalysts that could lift the trajectory beyond the current range. CryptoQuant contributor Arab Chain described a balance in the near term, with price hovering around $74,000 and activity suggesting a tug-of-war between supply and demand. While the neutral reading of the BSI implies a more balanced dynamic than the steeply bearish readings of the past months, it does not remove the risk of renewed downside if demand cools or macro stress reasserts itself.

Sentiment steadies, though still cautious

Beyond on-chain momentum, sentiment indicators are painting a cautiously improving picture. The Crypto Fear & Greed Index has recovered to a reading of 32 out of 100, moving away from the previous week’s Extreme Fear readings near 23. Although still categorized in the Fear territory, this shift signals a softening of negative mood among market participants. The index has roughly tripled in a little more than a week, reflecting a notable swing in trader psychology amid the price action.

“This places the market in a transitional phase, as investors await new catalysts to determine the next direction.”

The Fear & Greed Index is a lagging measure that aggregates multiple factors to gauge overall investor mood. Its upward movement toward a neutral zone aligns with the improved technicals observed in the BSI and with reports that Bitcoin has regained some supply-demand balance in recent days. Still, the index remains below the level that would typically accompany strong bullish conditions, reinforcing the sense that a breakout remains uncertain and conditional on broader market drivers.

In addition to the fear-greed cycle, broader market commentary has cited the potential for renewed volatility tied to macro and sector-specific developments. Cointelegraph’s coverage this week highlighted the possibility of Bitcoin breaking out of a multi-month trading range, a development that would align with improving sentiment but could hinge on fresh liquidity, risk appetites, and systemic cues from traditional markets.

With BTC flirting with the $78,000 level and the BSI shifting into neutral territory, traders face a decision juncture. The immediate question is whether the balance between supply and demand can be maintained in the face of potential macro headwinds or if renewed selling pressure could reassert itself as the market digests upcoming catalysts.

Investors should pay particular attention to:

- April monthly close: A decisive move above or below key thresholds could recalibrate market expectations and alter positioning among traders who use the BSI and sentiment signals to time entries and exits.

- Resistance and liquidity dynamics: If the price breaks higher, traders will be watching for a sustained flow of bids and a shift in open interest that confirms conviction beyond a short-term squeeze.

- Correlation with broader risk assets: As global risk appetite evolves, Bitcoin’s performance often tracks or diverges from equities and macro risk proxies, potentially amplifying moves around upcoming data releases or policy signals.

The evolving picture is a reminder that a neutral or even bullish signal in one metric does not erase risk. The 2022 bear episode began with a period of moderation before renewed declines; today’s readings suggest a transitional phase rather than a clear, enduring uptrend. For investors, the prudent approach remains to balance on-chain signals with macro awareness and to watch how fresh catalysts influence both price and sentiment in the weeks ahead.

As the market weighs these readings, the next moves in Bitcoin will be closely watched by traders, institutions, and developers alike. Whether this neutral tilt is a prelude to a sustainable rally or a temporary pause before further volatility remains an open question, but the current data clearly signal a shift away from the most bearish extremes toward a more balanced, if fragile, footing.

Key takeaways

- Pepe extends gains on Wednesday, stretching its rally from the 50-day EMA.

- Derivatives data show heightened retail activity as risk-on sentiment returns to the market.

Pepe (PEPE) is experiencing a steady rally on Wednesday, trading in the green for the third consecutive day. The frog-themed meme coin is gaining traction as broader market sentiment improves, lifting retail demand for meme coins.

Market sentiment boosts meme coin demand

The broader market’s upside, despite ongoing geopolitical tensions surrounding the US-Iran blockade of the Strait of Hormuz and faltering peace talks, is boosting retail interest in meme coins.

According to CoinMarketCap, the Fear and Greed Index is at 62 on Wednesday, showing a consistent rise in risk appetite since the US-Iran ceasefire announcement.

On the derivatives side, the PEPE futures Open Interest (OI) stands at $213.25 million, with a 7% increase in the last 24 hours.

This surge in futures positions indicates growing participation from traders, aligning with the recovery in the spot price—further supporting a bullish outlook for PEPE.

Pepe tests breakout of key resistance level

The PEPE/USD 4-hour chart is bullish and efficient as Pepe’s short-term recovery remains intact, with a three-day rebound from the 50-day Exponential Moving Average (EMA) at $0.00000368.

However, PEPE is still trading below the 100-day and 200-day EMAs, which could cap the ongoing rally.

The Relative Strength Index (RSI) at 60 is edging higher from the midline, indicating mild positive momentum. Meanwhile, the Moving Average Convergence Divergence (MACD) remains above its signal line, keeping the histogram bars positive.

At press time, PEPE is trading at $0.00000393. If the rally should continue, PEPE must break above its descending trendline near $0.00000400, close to the 100-day EMA at $0.00000404.

A breakout above this level could pave the way for a rally toward the 200-day EMA around the $0.00000500 psychological resistance.

On the downside, the 50-day EMA at $0.00000368 provides immediate dynamic support, with further downside protection at the February 6 low of $0.00000311.

Bitcoin (BTC) could see further upside volatility as several technical indicators suggested the BTC price was due for a “powerful“ upward move.

Key takeaways:

-

Bitcoin’s Bollinger Bands indicator now sees the potential for a massive price breakout.

-

BTC price needs to overcome resistance at $80,000 for more upside.

Bollinger Bands suggest Bitcoin’s “bull run is next”

Bitcoin’s Bollinger Bands have reached their tightest point ever on the monthly time frame, signaling that volatility should be expected soon.

Related: Bitcoin ‘Bull Score’ hits six-month high as 2022 bear-market fears linger

Bollinger Bands (BB) is a technical indicator used by traders to assess momentum and volatility within a certain range.

The “tightest Bitcoin monthly Bollinger band squeeze, ever,” said analyst Cantonese Cat in an X post on Wednesday.

“This will lead to a very powerful move when it expands,” the analyst added.

The BTC/USD pair gained about 230% between December 2023 and August 2025 to its current all-time high of $126,000, after breaking above the upper boundary of the Bollinger Bands.

Similar occurrences in 2020 and 2016 triggered the previous bull runs that saw BTC price rally more than 520% and 4,400%, respectively.

Meanwhile, Coinvo Trading shared a chart showing that Bitcoin’s monthly RSI has dropped to its lowest level since late 2022.

This coincided with the BTC/USD drop to a multi-year support trend line, an occurrence that has previously marked Bitcoin’s macro bottoms.

The last time this happened was at the bottom of the 2022 bear market, preceding a 350% BTC price rally to its previous all-time high of $73,800, reached in March 2024.

“The same exact trendline, the same oversold RSI, the same outcome,” Coinvo Trading said, adding:

“Bull run is next in line.”

As Cointelegraph reported, several Bitcoin metrics, including a bullish MACD crossover on the weekly chart, suggest that a BTC price breakout is about to begin.

Bitcoin must reclaim $80,000 next

Bitcoin’s 6% rally over the last three days saw the BTC/USD pair fill the $74,000-$77,000 CME gap created over the weekend.

Traders are now looking at the next CME gap above $80,000, formed in early February.

MC Capital founder Michael van de Poppe said resistance at $79,000 could temporarily “stall” Bitcoin’s upward momentum

“Likely we’ll test it first, come back down for a little, find extra stamina, and then we’ll push through to $86K.”

Meanwhile, Bitcoin’s whale order book showed “heavy sell pressure” between $78,000-$80,000, reinforcing the significance of this resistance level.

As Cointelegraph reported, a close above the $76,000-$78,000 resistance zone would confirm that the buyers are in control, clearing the path for a potential rally to $84,000.

This article is produced in accordance with Cointelegraph’s Editorial Policy and is intended for informational purposes only. It does not constitute investment advice or recommendations. All investments and trades carry risk; readers are encouraged to conduct independent research before making any decisions. Cointelegraph makes no guarantees regarding the accuracy or completeness of the information presented, including forward-looking statements, and will not be liable for any loss or damage arising from reliance on this content.

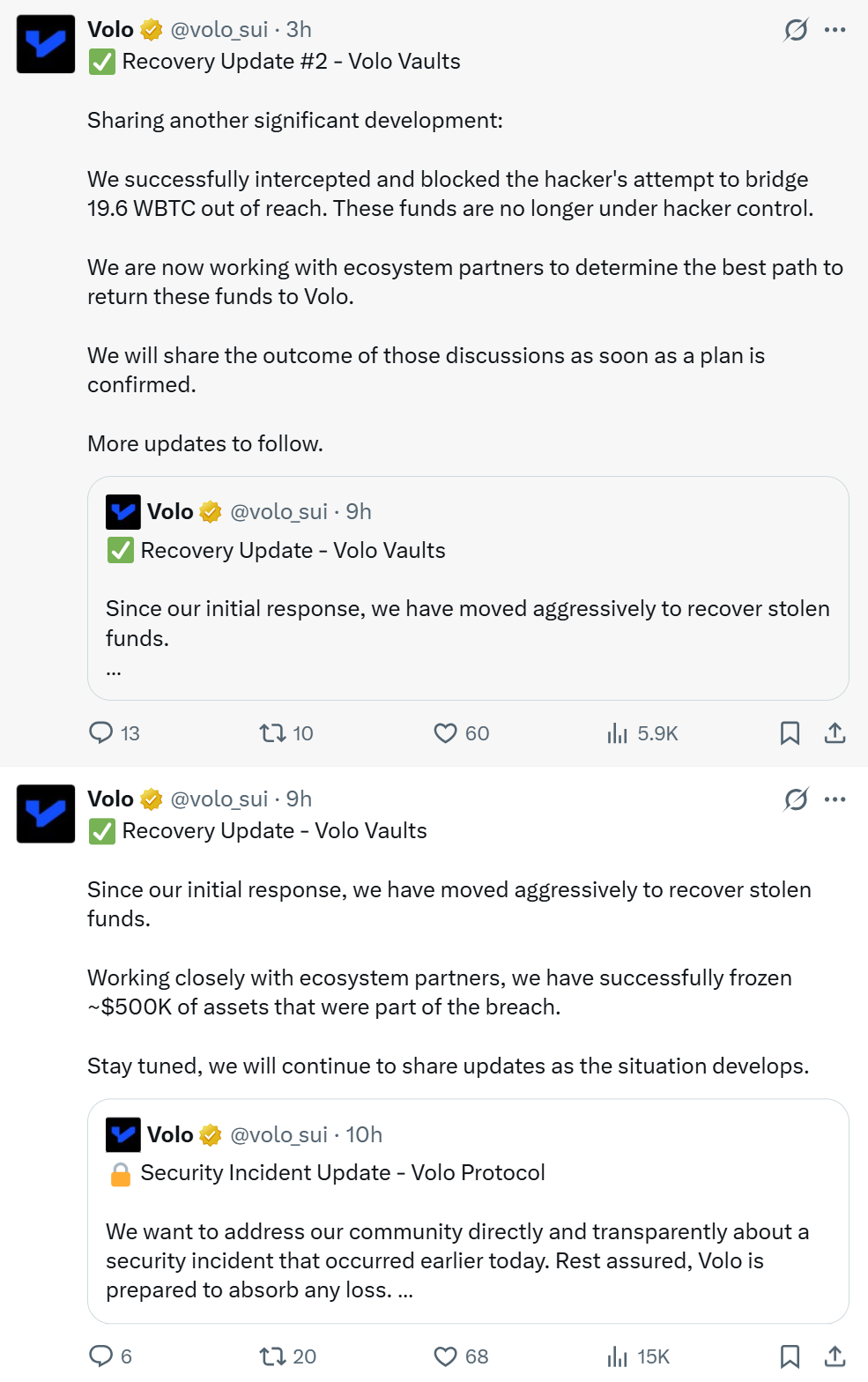

Decentralized finance (DeFi) protocol Volo has disclosed a security breach that resulted in the loss of approximately $3.5 million in digital assets, marking the latest incident in a series of exploits targeting DeFi platforms.

In a Wednesday post on X, the team said the attack affected select vaults and involved assets including Wrapped Bitcoin (WBTC), Matrixdock Gold XAUm and USDC (USDC). “We detected the attack, immediately notified the Sui Foundation and ecosystem partners to contain the damage, and froze the vaults to prevent any further exposure,” the team wrote.

The protocol added that around $28 million in total value locked across other vaults is safe, with the exploit limited to three isolated vaults and no shared vulnerability identified. It also revealed plans to absorb the losses rather than pass them on to users, though details of any remediation plan have yet to be finalized.

Volo is a liquid staking DeFi platform on the Sui blockchain, allowing users to stake their Sui (SUI) tokens and receive voloSUI (VSUI) in return. DeFi is already on edge, as the exploit comes as another liquid restaking protocol, Kelp, was hacked for approximately $293 million over the weekend, which has had a ripple effect across the broader ecosystem.

Related: Kelp DAO attacker moves $175M in Ether after exploit: Arkham

Volo freezes a portion of lost funds

In two separate updates, Volo said it has frozen or blocked roughly $2 million of the stolen funds so far. In the first update, the protocol said that roughly $500,000 linked to the breach has already been frozen. In a later update, the team claimed it had successfully blocked an attempt by the attacker to bridge 19.6 WBTC, effectively removing those funds from the hacker’s control.

“We are now working with ecosystem partners to determine the best path to return these funds to Volo,” the protocol wrote.

Crypto hacks claim $17 billion in 10 years

As Cointelegraph reported, more than $17 billion has been stolen in crypto over the past decade, with private key compromises identified as one of the major contributing attack vectors, according to DefiLlama.

Related: ZachXBT asks MemeCore to explain valuation and token supply

Roughly 22.3% of incidents are linked to brute-force key compromises, 18.2% to unknown methods and 10% to phishing attacks on multi-signature wallets. The findings show that many of the biggest losses stem from wallet security and user-side weaknesses rather than protocol bugs.

Magazine: 53 DeFi projects infiltrated, 50M NEO tokens could be ‘given back’: Asia Express

Crypto World

Tesla Reports Earnings After the Bell: Will Elon Musk’s AI Roadmap Trigger a Crypto Rally Before Midnight?

Tesla reports Q1 2026 earnings after market close today, and the AI roadmap update could move crypto markets before midnight.

The live Q&A webcast kicks off at 5:30 p.m. Eastern, with analysts watching every word on robotaxi expansion and Optimus progress.

Wall Street consensus sits at $0.30 EPS, a steep drop from Q4’s $0.50 beat, leaving the bar low enough that almost any positive AI catalyst could trigger a sharp move.

Cross-chain liquidity plays are already seeing elevated attention as institutional money rotates into infrastructure narratives ahead of the print.

Tesla’s April 2 production release confirmed 408,000+ vehicles built and 358,000+ delivered in Q1, alongside 8.8 GWh of energy storage deployed, steady numbers that kept the stock from collapsing pre-earnings.

The shareholder deck is expected to detail robotaxi expansion to nine cities in H1 2026, Cortex 2 compute buildout at the Texas Gigafactory, and a belated Optimus Gen 3 update after Q1’s promised unveil quietly didn’t happen.

A live earnings stream is already pulling significant viewer traffic ahead of the 4:30 p.m. CT call. The broader question isn’t whether Tesla beats — it’s whether the AI narrative holds up under analyst questioning. That answer will ripple well beyond TSLA.

Can TSLA’s AI Reveal Spark a Broader Risk Rally This Week?

With Q1 EPS projected at $0.30 against Q4’s actual $0.50 — a 25% beat over the $0.40 estimate, the year-over-year earnings compression is real.

The question is whether Tesla’s AI pipeline reframes the valuation story fast enough to matter. Robotaxi revenue is pre-commercial. Optimus is still pre-scale. Cortex 2 is burning capex. None of that is cheap.

Technically, TSLA has been consolidating in a wide range ahead of the print, with momentum indicators suggesting indecision rather than conviction.

The bull case: a strong AI update, new robotaxi city timelines, Optimus production numbers, or Cortex 2 milestones, pushes sentiment into breakout territory and drags high-beta tech and crypto assets with it. Spot Bitcoin ETFs have already recorded $1B+ weekly inflows, signaling institutional appetite that a TSLA AI pop could amplify.

Base case: Tesla meets the $0.30 EPS print, management delivers cautious optimism on robotaxi rollout, and markets grind sideways into the weekend.

Bear case, and the genuine invalidation, is any hint that Full Self-Driving timelines are slipping further, Optimus production targets are being walked back, or Cortex 2 costs are running over. That scenario pressures AI-adjacent assets across the board. Three numbers to watch at 5:30 Eastern: gross margin, energy storage revenue, and any hard robotaxi fleet figure.

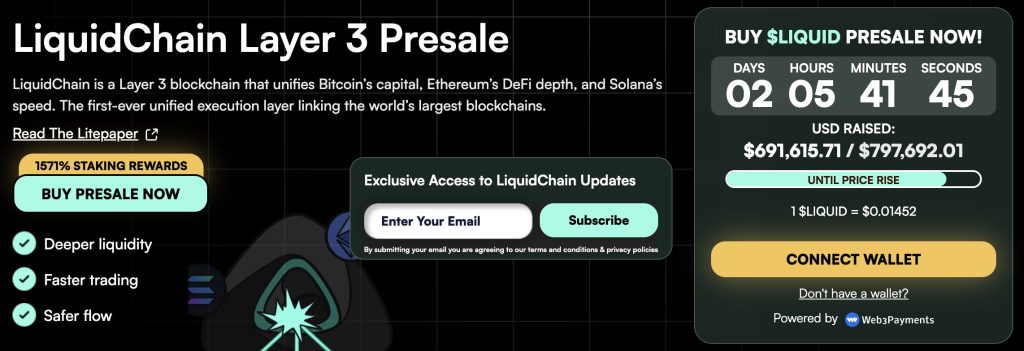

LiquidChain Targets Early-Mover Upside as TSLA Tests Key Catalyst Levels

Here’s the uncomfortable truth about chasing TSLA post-earnings: at any size, the asymmetric upside is gone before retail gets in.

The move happens in the first 90 seconds. On-chain liquidity signals are spiking ahead of tonight’s call, and that capital is increasingly looking for early-stage infrastructure plays where the entry point still exists.

LiquidChain ($LIQUID) is a Layer 3 infrastructure project built around a single proposition: fusing Bitcoin, Ethereum, and Solana liquidity into one unified execution environment. Developers deploy once, access all three ecosystems. The architecture includes a Unified Liquidity Layer, Single-Step Execution, Verifiable Settlement, and Deploy-Once infrastructure, targeting the fragmentation problem that costs DeFi protocols billions annually in lost efficiency.

The presale is currently priced at $0.01452, with $691,470.51 raised to date. That’s early by any measure.

Institutional narratives around BTC are accelerating, and a project merging BTC, ETH, and SOL liquidity rails is positioned directly inside that thesis. Risk is real — presales carry no liquidity guarantees, and token value is speculative until mainnet.

Research LiquidChain here before the next presale stage opens.

The post Tesla Reports Earnings After the Bell: Will Elon Musk’s AI Roadmap Trigger a Crypto Rally Before Midnight? appeared first on Cryptonews.

Mystery Deepens as 11 US Nuclear and Space Scientists Die or Vanish, Sparking Federal Probe

LayerZero among bridges Lazarus using to launder loot

17 Billowy Spring Dresses That Give Hamptons Energy From $7

Manchester United reach agreement with Casemiro over contract clause amid transfer speculation

Steven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

US brings back mandatory military draft registration

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Theodora Dress

-

Sports5 days ago

Sports5 days agoNWFL Suspends Two Players Over Post-Match Clash in Ado-Ekiti

-

Politics5 days ago

Politics5 days agoPalestine barred from entering Canada for FIFA Congress

-

Entertainment3 days ago

NBA Analyst Charles Barkley Chimes in on Ice Spice McDonald’s Fiasco

-

Business3 days ago

Business3 days agoPowerball Result April 18, 2026: No Jackpot Winner in Powerball Draw: $75 Million Rolls Over

-

Politics3 days ago

Politics3 days agoZack Polanski demands ‘council homes not luxury flats for foreign investors’

-

Crypto World5 days ago

Crypto World5 days agoRussia Pushes Bill to Criminalize Unregistered Crypto Services

-

Tech3 days ago

Tech3 days agoAuto Enthusiast Scores Running Tesla Model 3 for Two Grand and Turns It Into Bare-Bones Go-Kart

-

Politics2 days ago

Politics2 days agoGary Stevenson delivers timely reminder to register to vote as deadline TODAY

-

Tech7 days ago

Tech7 days ago‘Avatar: Aang, The Last Airbender’ Leaked Online. Some Fans Say Paramount Deserves the Fallout

-

Business6 days ago

Business6 days agoCreo Medical agree sale of its manufacturing operation

-

Business3 hours ago

Business3 hours agoRolls-Royce Voted UK’s Most Iconic Trade Mark as IPO Register Hits 150

-

Crypto World5 days ago

Crypto World5 days agoRussia Introduces Bill To Criminalize Unregistered Crypto Services

-

Crypto World3 days ago

Kelp DAO rsETH Bridge Hack Drains $292M as DeFi Losses Top $600M in Two Weeks

-

Sports6 days ago

Sports6 days agoBritish climbers complete new route in Swiss Alps

-

Tech6 days ago

Tech6 days agoFord EV and tech chief leaving automaker

-

Sports6 days ago

Sports6 days ago“Felt Much Better Today”: Josh Hazlewood Opens Up On His Recovery Win Over LSG

-

Entertainment7 days ago

Entertainment7 days agoRuby Rose Accuses Katy Perry Of Sexual Assault, Police React

-

Business6 days ago

Business6 days agoCheaper Doritos and Lays helps PepsiCo win back struggling snackers

-

Entertainment6 days ago

Entertainment6 days agoClavicular Says Streaming May Not Work Without Substances

You must be logged in to post a comment Login