Crypto World

MiCA Rules Tighten Compliance Burden on European Small Crypto Firms

The European Union’s Markets in Crypto Assets Regulation (MiCA) transition period is entering its final stretch, placing significant pressure on smaller crypto firms to secure authorization or winding down regulated services for EU clients. The deadline hits July 1, marking the end of the longest grandfathering window and triggering a hard stop for non-compliant providers across the bloc.

Industry early movers, such as United Kingdom–based CoinJar, have publicly noted MiCA’s maturation dynamics: obtaining authorization in Ireland in 2025, they view the regime as a necessary step toward a compliant, investor-protective market. Yet voices from markets like Poland caution that thousands of virtual asset service providers (VASPs) could face a regulatory cliff as deadlines approach, foreshadowing a period of rapid consolidation and market reconfiguration in Europe.

Under MiCA, the July 1 deadline represents decisive enforcement for the most capital-intensive and governance-heavy requirements. The regime includes an 18-month grandfathering period, but the window is uneven across member states, and several national regimes have already tightened or closed their doors to non-authorized operators. For smaller entities and hybrid projects, the regime is perceived as a potential breaking point rather than a gradual ramp-up.

The costs associated with authorization, governance upgrades, and ongoing reporting are raising the barrier to entry at a time when MiCA leaves a narrow lane for narrowly defined, fully decentralized services outside its scope. In practice, this is shaping a market where compliance-first players gain a competitive edge, and noncompliant actors either partner with regulated entities or exit the EU market altogether.

Regulators emphasize that MiCA aims to balance innovation with investor protection through proportionate obligations, but the policy’s ultimate effect on Europe’s crypto ecosystem remains uncertain. A statement from European Union supervisory bodies indicates that the transitional rules were designed to support innovation while preserving fair competition and investor safeguards. The question remains whether MiCA will underpin Europe as a trusted crypto hub or push parts of the sector toward offshore or offshore-like jurisdictions.

Key takeaways

- The MiCA transitional regime culminates on July 1; providers operating without a MiCA license must stop serving EU clients, regardless of size.

- The longest grandfathering window is 18 months, but national implementations and enforcement timing vary, increasing compliance complexity for smaller operators.

- Authorization costs, governance upgrades, and ongoing reporting obligations are creating a higher barrier to entry, incentivizing consolidation among EU VASPs and hybrids.

- MiCA’s scope excludes only a narrow band of fully decentralized services, leaving many DeFi projects in a regulatory gray area and prompting firms to adjust architectures and access points.

- Industry leaders anticipate a shift toward larger exchanges, custodians, and regulated gateways, with potential relocation of activity to more permissive jurisdictions outside Europe for smaller teams.

MiCA transition: implications for EU VASPs and market structure

Polish founders and market participants emphasize that MiCA’s cost and organizational demands leave limited room for smaller players. When Ari10 secured a MiCA license in the Netherlands in February, its founder noted that among roughly 2,000 registered VASPs in Poland, only his group had obtained MiCA authorization to date. The implication is clear: many local firms may be compelled to close or relocate activities to jurisdictions with more favorable regulatory environments. This pattern aligns with industry observations from other markets where licensing barriers have previously driven consolidation and exit of smaller operators.

Industry voices argue that the MiCA framework effectively channels activity toward larger, more capable entities capable of meeting governance, reporting, and capital requirements. This dynamic mirrors historical licensing waves in other jurisdictions, where rigorous post-licensing compliance has favored established custodians and large exchanges. At the same time, proponents contend the regime promotes a healthier market by encouraging credible actors and reducing the prevalence of opaque, undercapitalized ventures.

For those operating at the fringe of the regulated perimeter—hybrid models, experimental projects, or on-chain protocols—MiCA tests new approaches: how to deliver access for EU users through regulated intermediaries while preserving decentralization’s core design. Altura, a DeFi platform cited by industry participants, is exploring structures that keep core functionality on-chain while routing regulated access through compliant exchanges, custodians, and wallets. The practical challenge is how to classify and treat DeFi architectures once upgraded or modified to meet MiCA’s requirements, particularly where there is not an obvious operator or where upgradeability could influence control over outcomes.

DeFi in the gray zone: interpretation and risk

MiCA’s Recital 22 provides an exemption for fully decentralized services, but real-world application remains contested. Analysts argue that many DeFi systems operate as hybrids, with governance, upgradeability, and potential operator influence shaping outcomes. As such, DeFi projects face a spectrum of regulatory risk: some structures might sit outside MiCA’s scope in theory, but practical governance and on-chain dependencies could invite scrutiny. The debate underscores a broader risk: ambiguity surrounding what constitutes “decentralized enough” to avoid MiCA’s reach.

Industry practitioners assert that the current framework creates uncertainty for innovative models that prioritize user sovereignty and on-chain logic. If the landscape remains ambiguous, there is a clear incentive to centralize certain functions through regulated intermediaries or relocate development activities to jurisdictions with more permissive interpretations of decentralization. In this context, the decentralization exemption is a critical but unsettled hinge of MiCA’s long-term impact on innovation within Europe’s crypto ecosystem.

Regulators and the centralization debate

EU supervisors frame MiCA as a measure designed to enable a cohesive, risk-aware market that still supports innovation. An ESMA spokesperson stressed that the framework aims to ensure fair competition and robust investor protection, with the transitional period structured to give existing providers time to comply. The regulator also highlighted that obligations scale with risk, so smaller participants are not expected to meet the same standards as systemically important players. In this view, MiCA’s architecture reduces regulatory arbitrage and promotes a uniform standard across cross-border activities.

However, not all regulators share the same pace or approach. Malta’s Financial Services Authority (MFSA), for example, has warned against rushing toward centralized supervision of major cross-border crypto activities before MiCA’s practical implementation has fully matured in smaller markets. Local knowledge and proportionate oversight are cited as essential to effective supervision, particularly where market dynamics and consumer protection needs differ from larger, more integrated economies. These tensions reflect a broader debate about how to balance central oversight with the realities of diverse member states and emerging products.

In evaluating MiCA’s trajectory, observers note a tension between the desire for a unified, passportable regulatory regime and the risk of over-centralization that could stifle innovation or push activities offshore. The debate also intersects with cross-border regulatory differences, licensing regimes, and the evolving stance of EU authorities toward stablecoins, banking integration, and compliant on-ramps and off-ramps for crypto services.

MiCA as a filter, not a threat: practical consequences for firms

Some industry participants frame MiCA not as an existential hurdle but as a filter that raises the bar for quality, resilience, and investor protection. The path to scale in Europe is now clearly tied to a compliant, scalable, and auditable operation across the EU single market. For established players, MiCA offers a clear passport to grow across member states; for smaller teams, the regime signals a need to partner with regulated entities or migrate to jurisdictions with lighter or differently structured regimes. In this sense, MiCA’s design may concentrate market power toward those with the resources to meet the standards, while compelling experimentation and activity to seek alternatives elsewhere if the regulatory cost becomes prohibitive.

As regulatory monitoring intensifies, market participants should watch how national authorities implement the transition, how DeFi classifications evolve, and how cross-border supervision will interact with local licenses. The evolving policy environment will influence licensing pipelines, partner ecosystems, and the geographic distribution of crypto activities across Europe and beyond.

Closing perspective

With the July 1 deadline approaching, MiCA’s transitional framework is rapidly shaping Europe’s crypto market structure. Regulators emphasize proportionate requirements and investor protection, but the practical outcomes—consolidation, relocation, and evolving DeFi classifications—remain dynamic. For policymakers, market participants, and observers, the next phase will reveal how well a centralized supervisory approach can coexist with innovation-led growth, and whether MiCA’s balance of risk and opportunity will sustain Europe as a credible, globally integrated crypto hub.

As noted in discussions surrounding the regime, ongoing observations of enforcement, licensing activity, and cross-border supervision will be critical to assess MiCA’s real-world impact. Authorities and firms alike will be watching how the final transition unfolds, including the interpretation of decentralization exemptions and the practical application of proportionate requirements to a diverse ecosystem of players.

Key takeaways

- Bitcoin recovers slightly on Wednesday after finding support below $80,000.

- US-listed spot ETF saw outflows of $233 million on Tuesday,

Bitcoin finds support at a key level

Bitcoin (BTC) has slightly rebounded and is currently trading above $81,000 on Wednesday, following a retest of a critical technical support level the previous day.

The price surge is attributed to a recent correction and support found near the psychological $80,000 mark. As market participants await the Senate Banking Committee’s vote on the Clarity Act on Thursday, there are early indications that this could be a near-term catalyst for Bitcoin’s future price action.

Institutional demand appears to be showing some caution this week. Spot BTC Exchange-Traded Funds (ETFs) recorded a notable outflow of $233.25 million on Tuesday, after a modest inflow of $27.29 million the previous day, according to CoinGlass data.

If these outflows persist or intensify in the coming days, Bitcoin may experience a price correction. However, the focus remains on the Senate Banking Committee’s upcoming vote on the Clarity Act, which is anticipated to have a significant impact on the crypto market.

Bitcoin’s recent price action has lost momentum as it faces resistance around the 200-day Exponential Moving Average (EMA), hovering near $82,000.

The ongoing consolidation suggests that Bitcoin is taking a breather after a strong rally since early April. However, the outlook remains bullish, with the largest cryptocurrency by market capitalization potentially poised to resume its upward trend. Analysts are optimistic that the Clarity Act, which is expected to be voted on Thursday, could trigger a breakout for Bitcoin.

Bitcoin price forecast: BTC consolidating above key EMAs

Despite some caution in institutional demand, Bitcoin is showing a bullish near-term bias, with support holding above the 50-day and 100-day Exponential Moving Averages (EMAs).

These EMAs are clustered just below $76,800 and are part of a parallel channel, suggesting ongoing consolidation in the price action.

The Relative Strength Index (RSI) on the daily chart is near 61, indicating positive momentum without being overextended.

Meanwhile, a slightly negative Moving Average Convergence Divergence (MACD) reading points to moderating upside pressure, rather than a reversal, as Bitcoin remains below the 200-day EMA near $82,100.

If the rally persists, Bitcoin will face initial resistance at the 200-day EMA around $82,100, followed by the 61.8% Fibonacci retracement level near $83,440 and a horizontal barrier at $84,410.

A sustained break above this resistance zone could open the door for a run toward the January peak of around $97,925.

However, if the bears regain control, support is seen at the psychological $80,000 level, with further support zones near the 50% retracement at $78,960 and the 100-day and 50-day EMAs around $76,730 and $76,420, respectively.

Hyperliquid price extended its decline on Tuesday after failing to hold above a key resistance zone, raising concerns that a bearish double top pattern may now be forming on the daily chart.

Summary

- Hyperliquid price fell toward $39 after forming a potential bearish double top pattern near the $44–$45 resistance zone.

- Whale positioning on Hyperliquid reached $4.236 billion, with long and short exposure remaining nearly balanced at a 0.98 ratio.

- A bearish MACD crossover and weakening momentum indicators raised the risk of a deeper correction toward the key $35 support level.

According to data from crypto.news, Hyperliquid (HYPE) price dropped to around $39.2 at press time on May 13 after briefly trading above $44 earlier this month. Despite the recent pullback, the token still remains significantly above its April lows near the $35 region.

The latest correction comes as whale positioning on Hyperliquid reached roughly $4.236 billion in total exposure, with large traders showing an unusually balanced stance between bullish and bearish bets. Long positions accounted for around $2.099 billion, while short positions stood slightly higher near $2.137 billion, producing a near-neutral long-short ratio of 0.98.

The positioning suggests that institutional and high-net-worth traders remain uncertain on the market’s near-term direction despite elevated volatility across digital assets.

At the same time, investor sentiment surrounding the Hyperliquid ecosystem has remained relatively strong following the launch of the first U.S.-listed exchange-traded funds tied to the HYPE token by 21Shares. The products include a spot ETF with staking exposure alongside a leveraged fund linked to the decentralized derivatives platform.

The ETF launch further strengthened Hyperliquid’s growing institutional profile as the protocol continues dominating decentralized perpetual futures trading. The platform currently controls a substantial share of decentralized perpetual open interest while processing billions of dollars in daily trading volume.

However, traders appear to have started locking in profits after HYPE repeatedly failed to break above the key $44–$45 resistance zone over the past several weeks.

Hyperliquid price analysis

On the daily chart, Hyperliquid price appears to have formed a bearish double top pattern with two major peaks established near the $44–$45 region. Typically, a double top pattern signals weakening bullish momentum and often precedes a deeper correction once the neckline support breaks.

The neckline of the pattern currently sits near the $35.2 support zone, which also aligns with a major horizontal support area that buyers defended aggressively during the April consolidation phase.

A look at the MACD indicator reinforces the weakening momentum outlook. The MACD histogram has turned negative again, while the MACD line has crossed below the signal line, confirming a bearish crossover and suggesting that downside pressure may continue building in the short term.

Meanwhile, the Aroon indicator also points to fading bullish momentum. The Aroon Up indicator has declined toward the 50% level while the Aroon Down remains subdued near 7%, signaling that buyers are gradually losing control of the trend even though broader bearish dominance has not yet fully emerged.

If sellers manage to push HYPE below the neckline support near $35, the bearish double top setup could trigger a larger correction toward the $31–$32 region.

On the upside, bulls would likely need to reclaim the $44 resistance area to invalidate the bearish structure and restore momentum toward the psychological $50 level.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Crypto World

Brickken and Magma partner to deliver Net Asset Value (NAV) oracle for tokenized real estate

Built on Magma’s Digital Twin Token (DTT) and Brickken’s institutional tokenization infrastructure to close the data gap that has held tokenized real estate back.

Crypto World

Trump Crypto Project Just Burned $6.67 Million in Tokens: Is This Enough to Save World Liberty Financial (WLFI) From Its Downtrend?

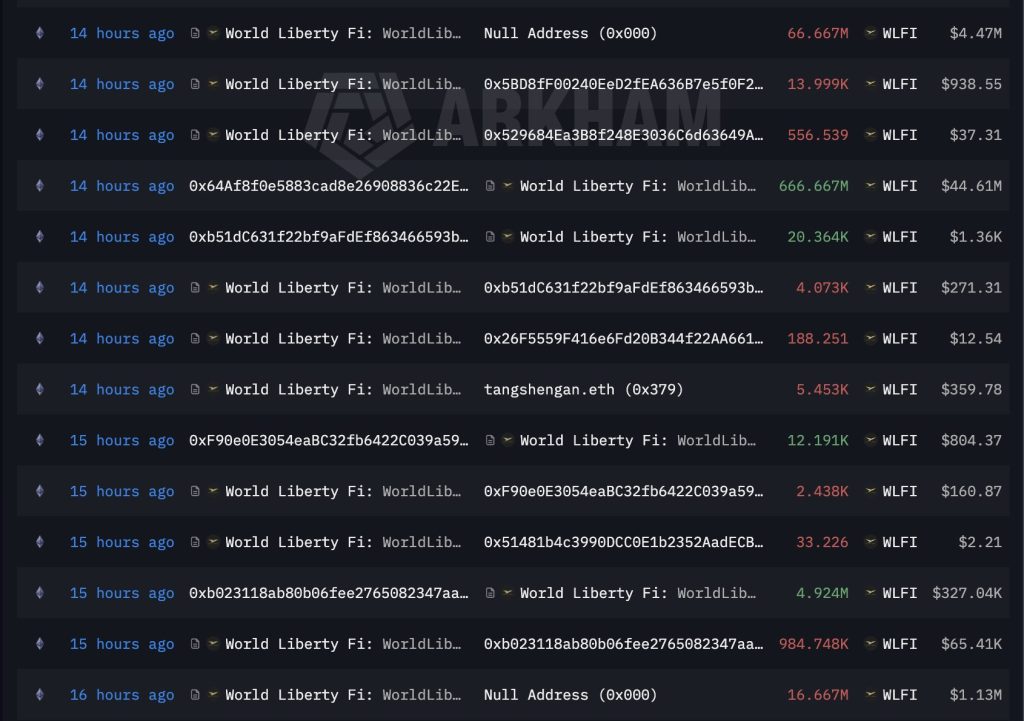

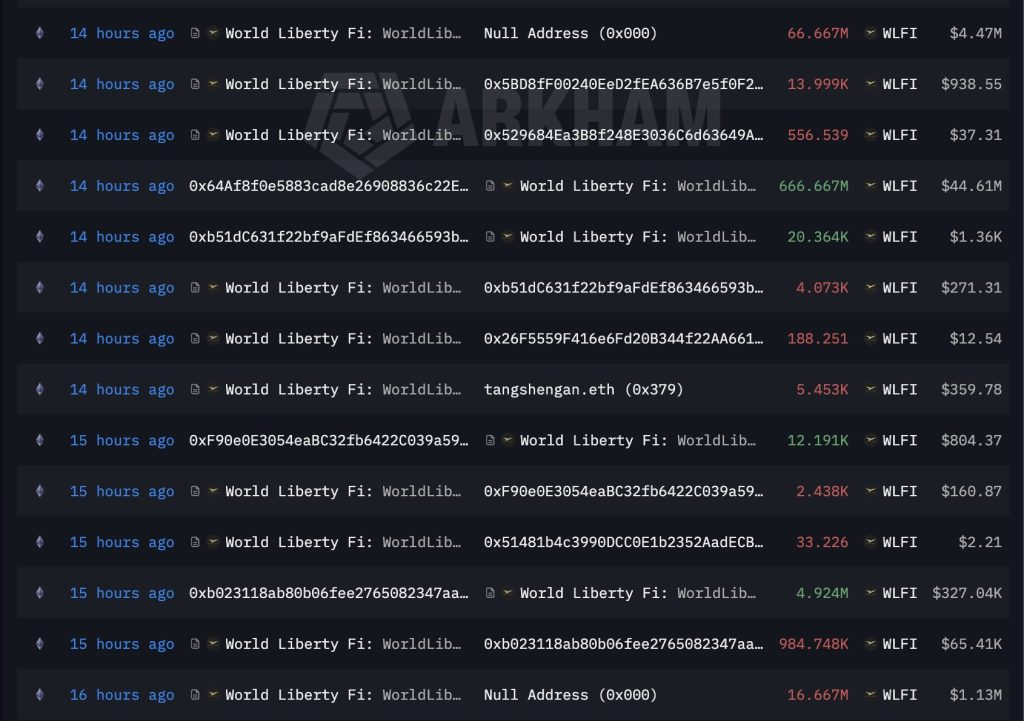

World Liberty Financial (WLFI) Crypto has torched $6.67 million worth of $WLFI tokens in under 24 hours, and the broader crypto market is watching.

The question is whether WLFI’s supply shock can cut through a market increasingly sceptical of politically connected DeFi projects.

Blockchain analyst EmberCN confirmed the burn: four team-linked addresses transferred one billion WLFI tokens into an unlocked vesting contract, then permanently removed 100 million, exactly 10%, via a burn mechanism.

The remaining 900 million tokens stay locked under a revised unlock schedule. This follows a plan announced last month to delay unlocks for contributors and founders, bundled with the commitment to burn a tenth of those allocations.

The move reduces near-term selling pressure from insiders, a signal of long-term alignment, or at least the appearance of it.

Can World Liberty Financial (WLFI) Crypto Reclaim $0.08 This Month?

WLFI is sitting at $0.0686 on the 4h chart, and this is a chart that tells a straightforward story of a coin that has been in a downtrend since launch, with no meaningful base built yet.

Price opened around $0.14 to $0.19 in early January and has been bleeding consistently lower ever since, hitting a recent low around $0.050 before a small bounce back to the current $0.068 level.

That bounce off $0.050 is the only remotely constructive thing on this chart, but it is too early to call it a base because price has not shown any ability to hold a level for more than a few sessions before continuing lower, and the overall structure is still a series of lower highs with no clear accumulation zone forming.

The $0.075 to $0.080 range is the first level of resistance from the most recent consolidation, and it is the level any recovery attempt needs to clear before the picture starts improving even marginally.

On the downside, the $0.050 low is the only real floor on the chart, and a break below it puts the price in completely uncharted territory with no support reference points below.

This is a high-risk chart with no confirmed bottom, no base structure, and a downtrend that has been intact since day one. The bounce from $0.050 could develop into something, but there is nothing here yet to suggest the selling is done.

Here is Why Bitcoin Hyper Could Outperform WLFI Next

With Bitcoin grinding at a key decision point and compressed upside at current market caps, rotation into early-stage infrastructure plays is picking up.

The WLFI burn itself underscores a broader theme: tokenomics discipline and genuine utility are separating credible projects from noise. Early-stage positioning, before price discovery, is where asymmetric returns historically originate.

Bitcoin Hyper (HYPER) is making a direct play on Bitcoin’s core limitations. It’s the first Bitcoin Layer 2 to integrate the Solana Virtual Machine (SVM), delivering sub-second finality and low-cost smart contract execution while inheriting Bitcoin’s security.

That’s a technically ambitious combination; SVM performance benchmarks have beaten Solana itself in early tests, which is either a bold claim or a genuine engineering leap (the on-chain data will settle that debate at launch).

The numbers are concrete: $HYPER is priced at $0.01368, with $32,676,096.88 raised to date. Staking rewards are live, with high APY available to current presale participants.

The project’s presale has already crossed $32M, meaningful traction for an infrastructure-layer bet. As with any presale, smart contract risk and execution uncertainty apply. Research the project independently before committing capital.

The post Trump Crypto Project Just Burned $6.67 Million in Tokens: Is This Enough to Save World Liberty Financial (WLFI) From Its Downtrend? appeared first on Cryptonews.

Key takeaways

- ATOM extends its gains, trading above $2.10 on Wednesday, up over 8% so far this week.

- The technical outlook suggests a further upward rally in the near term

ATOM trading volume hits multi-month highs

Cosmos Hub (ATOM) continues its bullish rally, currently trading above $2.10, up more than 8% this week.

On-chain data reveals a positive outlook, with ATOM’s trading volume surging to $120.74 million on Wednesday, marking the highest level since early February.

This surge in trading volume indicates growing trader interest and liquidity, further boosting ATOM’s upside momentum.

Santiment’s data suggests an increase in demand, with spot markets showing buy-side dominance and generally neutral conditions across other metrics, pointing to potential for continued upward movement.

The rally comes after Cosmos Hub announced a new partnership with Injective. Starting soon, the USDC stablecoin from Injective will be integrated into the Cosmos Hub ecosystem.

This integration ensures long-term support for USDC, solidifying the relationship for at least four years.

The partnership will enhance liquidity, cross-chain interoperability, and introduce a buyback mechanism for ATOM tokens.

The Cross-Chain Transfer Protocol (CCTP) will facilitate one-signature transfers, with the protocol fees used to buy back ATOM tokens programmatically.

This move is bullish for both Cosmos Hub and ATOM in the long term, as it strengthens the ecosystem and introduces new demand drivers.

Cosmos Hub price forecast: ATOM aims for $2.34

The ATOM/USD 4-hour chart is bullish and efficient as the coin is outperforming the broader crypto market.

ATOM is trading at $2.15 on Wednesday, marking a 8% increase this week. The token remains above key support levels, with the 50-day and 100-day Exponential Moving Averages (EMAs) at $1.90 and $1.97, respectively.

This keeps the near-term bullish trend intact as ATOM pushes further away from its broken descending trend line.

The Relative Strength Index (RSI) has surged into overbought territory, currently around 75, while the Moving Average Convergence Divergence (MACD) line stays above zero with a positive spread, suggesting strong bullish momentum but cautioning against overextension.

If the bullish trend continues, initial resistance is found at the 200-day EMA around $2.34, followed by the 38.2% Fibonacci retracement at $2.39.

A sustained break above this resistance zone could open the path to further gains, with potential targets at the 50% retracement near $2.63 and the 61.8% retracement level at $2.88.

However, if the market undergoes a correction, immediate support is seen at the 23.6% Fibonacci retracement at $2.09, followed by the 100-day EMA at $1.97 and the 50-day EMA near $1.90.

A deeper pullback could occur if these levels are lost, with further support near the former trendline break area at $1.75 and the lower horizontal support around $1.65.

Every market has its dominant players. In online sports betting, two names have occupied the top positions for long enough that most people stopped questioning them. DraftKings built the most recognisable betting brand in the United States. Bet365 built what many consider the definitive international sportsbook. Between them, they have set the terms for what online gambling looks like for a very large number of players.

But markets evolve. Player expectations shift. And in 2026, a new platform called ZunaBet is entering the conversation — not by trying to replicate what DraftKings and Bet365 do, but by building something specifically for the players those platforms have never fully served.

This article looks at all three. What the established platforms do well, where they fall short, and why ZunaBet is generating attention from a particular and growing segment of the market.

DraftKings: America’s Sportsbook

DraftKings did not come from nowhere. It started as a daily fantasy sports platform, spent years building an audience of sports-engaged, financially active users, and was positioned better than almost any competitor when the US Supreme Court’s 2018 ruling began opening state-by-state sports betting legalisation. The platform moved fast, spent heavily, and converted its fantasy user base into a sportsbook audience more effectively than traditional operators could manage.

Today DraftKings operates a full sportsbook and online casino across multiple licensed US states. The sportsbook covers NFL, NBA, MLB, and NHL in depth, with soccer, golf, tennis, and international markets expanding the offering. In-play betting is polished and the mobile app is among the most downloaded in the gambling category. The casino has grown across licensed states — slots, live dealer tables, and RNG games building out the product beyond its sportsbook origins.

Crypto is partially supported in some states, but the platform is fundamentally fiat-first. The payment infrastructure was built for traditional banking and cryptocurrency exists at the edges rather than forming the foundation. The Dynasty Rewards loyalty programme operates on a tiered points system — Dynasty Dollars earned through wagering, redeemable for site credits. The tiers are structured and the upper levels carry real benefits, but the actual return rate as a percentage is not stated plainly. Most players find the mechanics functional but not particularly transparent.

DraftKings is the right platform for the American sports bettor who wants a polished, mobile-first product built for US regulations and US sports culture. Its limitations — partial crypto support, complex loyalty mechanics, and a fiat-first infrastructure — are largely inherited from the environment it was built within.

Bet365: The International Standard

Bet365 has been building its sportsbook since 2000. Twenty-five years of focused product development, regulatory approvals across the UK, Malta, Gibraltar, Australia, and dozens of other jurisdictions, and a marketing presence that has made it one of the most recognised gambling brands in the world.

The sportsbook is where Bet365 earns its reputation. Football coverage is the benchmark — market depth, in-play quality, and live streaming across competitions from the top European leagues down to matches most operators do not bother covering. Tennis, cricket, basketball, American sports, horse racing, and golf are all present at the same depth. For a sports bettor in an international regulated market, Bet365 is the default recommendation for good reason.

The casino offers slots, live dealer games, and RNG table games as a solid secondary product. The platform is stable, the brand carries trust built across decades, and the regulatory standing is among the strongest of any operator in the industry.

Crypto is not supported at all. Cards, bank transfers, and e-wallets are the options. The loyalty programme accumulates points through wagering, redeemable for free bets and bonuses. It has operated in broadly the same form for years without meaningful structural change. The real return rate is not communicated plainly.

Bet365 serves its core audience — the international sports bettor in a regulated fiat market — better than almost anyone. Outside that profile, it has not moved to accommodate changing player expectations.

What Both Platforms Share

Looking at DraftKings and Bet365 together, two consistent limitations stand out.

The first is cryptocurrency. DraftKings has partial support in limited markets. Bet365 has none. In 2026, this is a more significant gap than it might appear. Crypto ownership has moved well past early adopter status into mainstream financial behaviour. A meaningful and growing portion of online gambling players holds and transacts in Bitcoin, Ethereum, USDT, Solana, or other currencies as a routine part of their financial lives. For those players, fiat-only or fiat-first platforms require conversion, fees, and engagement with banking infrastructure they have specifically moved away from.

The second is loyalty transparency. Both platforms run points-based programmes where the real return rate is embedded in mechanics that require effort to calculate. Players accumulate balances and redeem for bonuses without ever being told plainly what percentage of their wagering is coming back to them. This model has been the industry standard for so long that most platforms have never questioned it. But the players who have encountered rakeback-based systems — where a defined percentage is returned at a clearly stated rate — find it difficult to return to opacity.

These are structural gaps, not surface-level complaints. They define the audience that both DraftKings and Bet365 were never built to serve — and they define exactly who ZunaBet is building for.

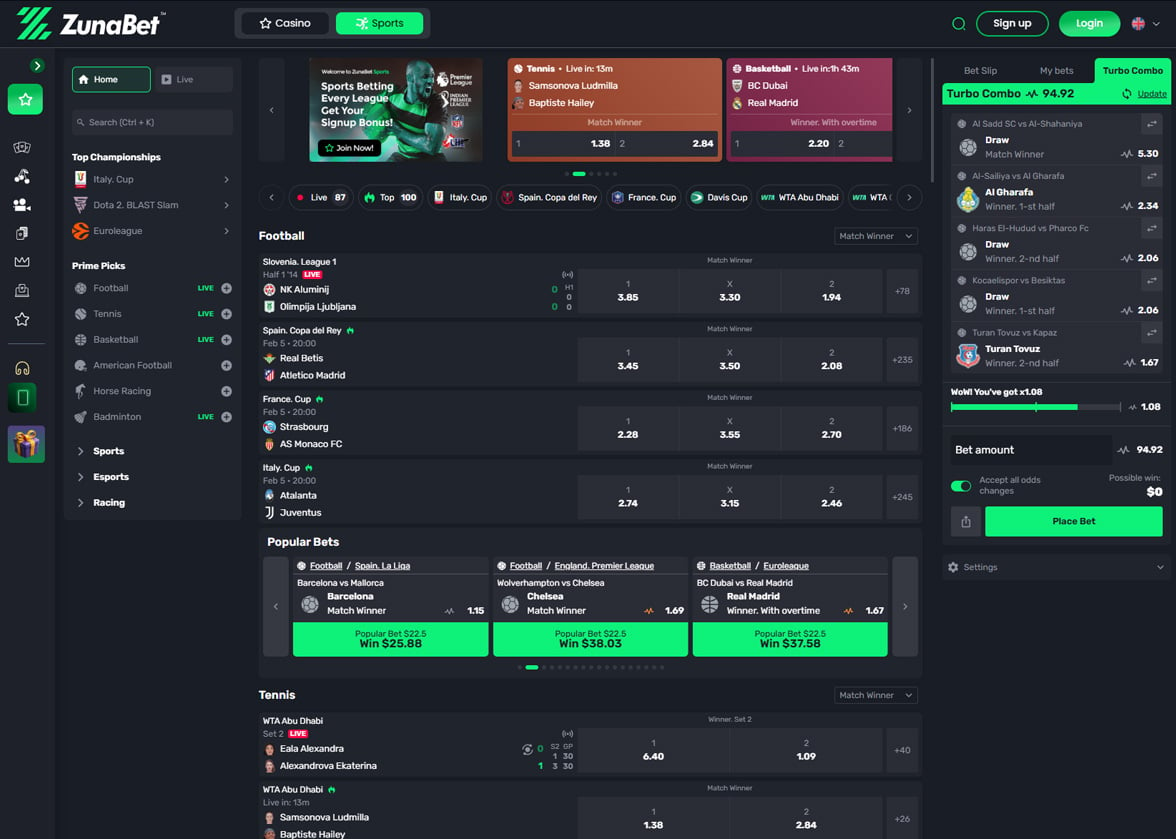

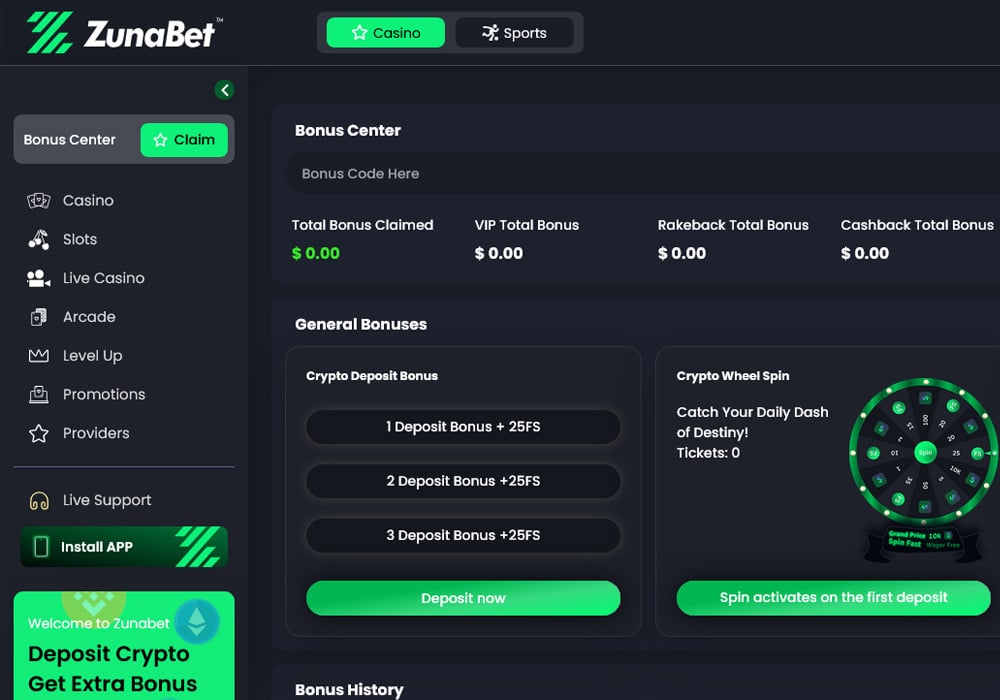

ZunaBet: The Platform Getting Attention in 2026

ZunaBet launched in 2026 under Strathvale Group Ltd with an Anjouan gaming licence. The team behind it brings over 20 years of combined industry experience. It did not inherit a fiat payment system, a loyalty programme designed in the early 2000s, or a regulatory geography that shapes product decisions. It built from scratch, in 2026, with a clear picture of the player it was designed to serve.

Crypto at the foundation. More than 20 cryptocurrencies are supported — Bitcoin, Ethereum, USDT across multiple chains, Solana, Dogecoin, Cardano, XRP, and others. No platform processing fees. Fast withdrawals. This is not a fiat platform with a crypto deposit option. Crypto is the infrastructure the entire platform is built on. For players who have been navigating workarounds to use traditional platforms, the experience is immediately different.

A game library that competes at the top level. Over 11,000 titles from more than 63 providers including Pragmatic Play, Hacksaw Gaming, Evolution, Yggdrasil, and BGaming. Slots account for the majority, but live dealer games and RNG table games are both substantively covered. By volume and provider depth this is one of the largest crypto casino libraries in the market — and it competes with the casino side of either established platform on content alone.

A sportsbook that is part of the platform. Football, basketball, tennis, NHL, and major global sports alongside esports markets for CS2, Dota 2, League of Legends, and Valorant. Virtual sports and combat sports included. Casino and sportsbook live in the same product — not linked, not adjacent, the same place. Players who move between casino and sports betting do so without switching platforms or managing separate experiences.

Technology built for modern usage. Dedicated apps for iOS, Android, Windows, and MacOS. Dark-themed HTML5 interface, fast-loading across devices. 24/7 live chat support always available.

The Welcome Offer: $5,000 and 75 Free Spins

ZunaBet welcomes new players with a bonus structured across three deposits.

First deposit: 100% match up to $2,000 plus 25 free spins. Second deposit: 50% match up to $1,500 plus 25 spins. Third deposit: 100% match up to $1,500 plus a final 25 spins.

Total value: up to $5,000 in matched funds and 75 free spins across the opening three deposits. Spreading the offer across multiple deposits keeps value active across the early experience on the platform and rewards players for continuing to engage rather than treating the welcome bonus as a single transaction.

The Loyalty Question: Where ZunaBet Pulls Ahead

The comparison between ZunaBet’s loyalty programme and those at DraftKings and Bet365 is the starkest illustration of the difference between old and new platform thinking.

Dynasty Rewards and Bet365 points both operate on the same core model: wager, earn points, redeem for bonuses. The rate of return is never stated as a plain percentage. Players trust the system without being shown the number behind it.

ZunaBet shows the number.

The dragon evolution loyalty system runs through six named tiers — Squire, Warden, Champion, Divine, Knight, and Ultimate. Each tier carries a defined rakeback percentage. Squire earns 1% of losses returned. Ultimate earns 20%. The rate is stated. It applies. It comes back to the player. No calculation required.

Alongside the rakeback, each tier adds benefits: free spins up to 1,000, VIP club access, double wheel spins, and a gamified identity built around a mascot called Zuno. The programme has both structure and personality — something traditional loyalty systems rarely manage simultaneously.

At 20% rakeback for the highest tier, ZunaBet returns one in every five dollars lost over time to its most engaged players. For regular, high-volume players that compounds into a substantial ongoing financial benefit that neither Dynasty Rewards nor Bet365 points can match in value or in the simple fact of being transparent about it.

Is ZunaBet the Alternative Players Are Watching?

The question in the headline has a straightforward answer: for a specific type of player, yes.

DraftKings is not losing its core US sports betting audience to ZunaBet. Bet365 is not losing its international regulated market players. Both platforms serve their audiences well and will continue to do so.

What ZunaBet represents is a new option for the player who sits outside both those profiles — the crypto user, the player who wants to know what their loyalty is worth, the person who expects casino, sportsbook, and esports to exist in one place without compromise. That player has existed for years without a platform built around them.

In 2026, they have one. And based on what ZunaBet has launched with — the game library, the sportsbook depth, the crypto infrastructure, and the most transparent loyalty programme in its class — the attention it is receiving is entirely justified.

The old names defined what online gambling looked like for one generation of players. ZunaBet is part of what it looks like for the next.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

Americans are sending Washington a clear message: the United States should lead the future of digital finance, not fall behind while other countries write the rules. A new national HarrisX survey of registered voters found that 70% say the U.S. should have already passed crypto legislation, 62% say it is important for America to set the global rules for digital finance, and 60% prefer clear federal legislation over case-by-case enforcement.

That makes the Senate Banking Committee’s decision to mark up the Clarity Act a critical next step toward giving the United States a workable framework for digital asset markets.

For years, Washington treated digital assets as a moving target. The technology evolved quickly, the market was volatile, and policymakers were still sorting out the risks and opportunities. That is no longer the case. Lawmakers, regulators and staff have now spent years studying these markets, engaging stakeholders and wrestling with difficult questions around consumer protection, market integrity, custody, trading and disclosure.

The industry has changed as well. A sector that once spoke in scattered, often conflicting voices has become more disciplined in its engagement with policymakers. That matters because durable legislation comes from sustained engagement, practical proposals and a willingness to work through tradeoffs.

The House made that much clear when it passed the CLARITY Act with strong bipartisan support. That vote did not resolve every outstanding question, but it established something important: digital asset market structure belongs squarely on Congress’s agenda. The Senate now has a chance to build on that foundation.

It is doing so with a stronger policy foundation than it had even a year ago. The SEC and the CFTC have taken steps to improve coordination and clarify how existing law applies to parts of the market. Those efforts are important, but they also underscore the limits of agency action. Only Congress can provide durable rules on regulatory boundaries, registration requirements, market oversight and the treatment of digital assets that do not fit neatly within older frameworks.

Meanwhile, the market has continued to move ahead. Following the signing of the GENIUS Act, stablecoins have grown rapidly and are becoming more connected to mainstream payments infrastructure. Tokenization is moving from concept to institutional experimentation. Major financial firms are testing blockchain-based systems for settlement and other market functions. Public blockchain networks are increasingly part of that activity.

Some of that development is taking place on networks like Solana. PayPal expanded PYUSD to Solana to support faster, lower-cost payment use cases. Visa has included Solana in its stablecoin settlement work. And SoFi, which launched SoFiUSD in December, has said parts of its broader digital asset banking platform are expected to leverage Solana alongside other networks. These examples show how digital asset markets are becoming more connected to real financial activity.

It’s clear: Digital assets are the next generation of financial infrastructure.

Congress should legislate with that reality in mind. A market structure bill has to do difficult, important work. It has to draw workable lines between regulators. It has to establish clear rules for market participants while ensuring robust consumer protections. And it has to account for the fact that blockchain networks and digital asset markets do not map neatly onto categories built for earlier generations of financial products.

That is precisely why markup matters. It requires lawmakers to engage real legislative text in public. Members debate substance, offer amendments, narrow disagreements and test whether a proposal is ready to move. On legislation this consequential, that process is where serious policymaking happens.

For digital asset legislation to last, it must be bipartisan. A framework written on a party-line basis will be fragile from the start. Rules that shape markets endure when both parties help write them. The good news is that more lawmakers on both sides of the aisle now understand the stakes. They understand the need for consumer protection, the importance of market integrity and the cost of leaving a growing sector trapped in legal uncertainty.

The United States has deep capital markets, strong institutions, world-class entrepreneurs and a long history of leading in financial innovation. It should bring those strengths to digital assets as well. Clear rules will protect consumers, strengthen markets and give responsible builders the confidence to operate and invest in the United States.

Digital asset markets will continue to grow. Capital will move. Infrastructure will be built. The question is whether the United States will shape that future with clear rules, credible oversight and the confidence to lead.

The Senate can help answer that question now by moving this legislation forward and closer to the President’s desk. It’s critical that it does.

Crypto World

Tower Semiconductor (TSEM) Soars 17% on Earnings Beat and Major AI Chip Contracts Worth $1.3B

Key Highlights

- Tower Semiconductor surpassed Q1 2026 earnings expectations with adjusted EPS of $0.65, topping the $0.55 Wall Street consensus

- First-quarter revenue reached $413.6 million, marking a 15% year-over-year increase and exceeding the $408 million projection

- Second-quarter revenue forecast of $455 million surpassed analyst expectations of $436 million — potentially setting a new company milestone

- The company secured $1.3 billion worth of silicon photonics agreements for 2027 delivery, with customers already providing $290 million in upfront payments

- TSEM shares skyrocketed more than 17%, reaching a 52-week peak of $267.42

Tower Semiconductor delivered an impressive performance on Tuesday. The Israel-based chip manufacturer reported solid earnings results, provided robust forward guidance, and unveiled $1.3 billion in artificial intelligence chip agreements — creating a trifecta of positive catalysts.

Tower Semiconductor Ltd., TSEM

TSEM shares surged over 17% during early U.S. market hours, climbing to a 52-week peak of $267.42. Meanwhile, broader market indices remained subdued, with the S&P 500 declining 0.11% and the Nasdaq essentially unchanged, highlighting that Tower’s rally was driven purely by company-specific developments.

First-quarter 2026 revenue totaled $413.6 million, representing a 15% climb compared to the prior-year period, and narrowly exceeding the Street’s $408 million projection. Adjusted earnings per share landed at $0.65, comfortably beating the analyst consensus of $0.55 by a dime.

Gross profit expanded 52% year-over-year to reach $111 million. Operating profit saw even more dramatic growth, nearly doubling with a 96% surge to $65 million compared to $33 million in the first quarter of 2025.

Looking ahead to Q2 2026, Tower projected revenue of $455 million, with a variance of plus or minus 5%. Wall Street analysts had penciled in $436 million. Successfully hitting this target would establish a new revenue record for the semiconductor manufacturer.

However, the most significant development centers around silicon photonics. Tower locked in $1.3 billion in agreements for 2027 revenue from its primary silicon photonics clients — specialized chips that utilize light instead of electrical signals for data transmission, making them particularly effective for AI data center applications.

Secured Revenue Stream of $1.3 Billion

Customers demonstrated serious commitment beyond mere paperwork — they’ve already transferred $290 million in advance payments to reserve manufacturing capacity. Furthermore, they’ve pledged to place even larger orders for 2028, with additional upfront payments scheduled for delivery by January 2027.

CEO Russell Ellwanger expressed confidence, stating the company is “confident in our path toward achieving our financial model targets of $2.8 billion in annual revenue and $750 million in net profit in 2028.”

These financial objectives now carry substantial weight. The order pipeline continues to strengthen.

Credit Rating Boost Reinforces Positive Trend

S&P’s Maalot maintained Tower’s “ilAA” credit rating while elevating its outlook from stable to positive — a subtle yet significant validation of the company’s business direction.

Tower’s semiconductor products support automotive, industrial, consumer electronics, and communications sectors, though current momentum stems primarily from AI data center requirements.

In March, competitor GlobalFoundries initiated legal action against Tower, claiming patent infringement on 11 patents associated with chip production for smartphones and related devices. This legal matter remains unresolved.

Tower concluded the trading day at a new 52-week high, with the stock’s appreciation stemming exclusively from company-specific announcements rather than broader semiconductor industry trends.

Reform UK leader Nigel Farage is reportedly facing a parliamentary standards inquiry over whether he failed to declare a 5 million pound ($6.7 million) gift from crypto billionaire Christopher Harborne.

The UK Parliamentary Standards Commissioner has opened an inquiry into whether Farage breached House of Commons rules by not registering the payment, the BBC reported Wednesday.

Farage said he was under “no obligation” to declare the gift from the Reform party backer, which he received before he was elected to the Commons in 2024. Critics argue he should have registered the payment after becoming a member of parliament.

The Conservatives wrote to the parliamentary standards watchdog asking it to investigate the matter, according to the BBC. The Conservatives also raised the issue with the Electoral Commission, which is reportedly deciding whether to launch a formal investigation into the donation.

The inquiry adds to scrutiny of Farage’s financial ties to crypto-linked backers and businesses, as UK lawmakers and regulators pay closer attention to the role of digital asset money in politics.

The development comes a month after the UK Liberal Democrats called on the Financial Conduct Authority to investigate whether Farage breached market rules by appearing in a promotional video for Stack BTC while holding a financial stake in the company.

Farage previously disclosed a $286,000 equity investment in the company after acquiring a 6.31% stake through his media vehicle Thorn In The Side in March.

Related: Revolut among 4 companies chosen to test stablecoins in UK sandbox

UK lawmakers mull halt to political crypto donations

Cryptocurrency donations to political parties have come under growing scrutiny in the UK.

Farage’s Reform UK was the first party to start accepting crypto donations in 2025. Reform recently disclosed a $4 million donation from Harborne in the fourth quarter of 2025, after receiving a record $12 million gift in the previous quarter.

Political cryptocurrency donations are currently legal in the UK, subject to permissible rules under the Electoral Commission guidance. However, some parliamentary committees have called for a halt.

On March 18, the Joint Committee on the National Security Strategy urged the UK government to impose an immediate moratorium on crypto donations to political parties until the Electoral Commission produces statutory guidance ahead of the next general election, which is due to take place by August 2029.

The committee also called for the creation of a Political Finance Enforcement Unit and for reducing the minimum declaration threshold of political donations from $14,900 to $668. It cited growing foreign-state threats and efforts to influence the UK’s positions on critical issues, including its relations with the US, the European Union and Ukraine.

Three weeks earlier, Matt Western, chair of the committee, urged the government to put a temporary halt on crypto donations to political parties, citing foreign interference risks, Cointelegraph reported on Feb. 26.

Magazine: Clarity Act risks repeat of Europe’s mistakes, crypto lawyer warns

U.S. President Donald Trump arrived in Beijing on May 13 for a formal state visit at the invitation of Chinese President Xi Jinping.

Summary

- U.S. President Donald Trump has arrived in Beijing for a state visit following an invitation from Xi Jinping.

- Markets are closely watching geopolitical sentiment, with prediction platforms pricing shifts in U.S.–China diplomatic expectations.

- Crypto traders are assessing whether renewed U.S.–China engagement could impact risk appetite and global liquidity flows.

The visit marks a renewed high-level diplomatic engagement between the world’s two largest economies amid ongoing strategic and economic competition.

The announcement has quickly drawn attention across financial markets, where geopolitical developments between the U.S. and China often influence risk sentiment, trade expectations and cross-asset volatility. Crypto traders, in particular, are watching for potential spillover effects into liquidity conditions and speculative positioning.

Prediction markets are also reacting to the development. Platforms such as Polymarket are tracking event-based probabilities tied to U.S.–China relations, including the likelihood of trade policy shifts, tariff adjustments, or formal agreements emerging from diplomatic meetings.

Geopolitics meets prediction markets and crypto sentiment

On Polymarket, traders typically express views on scenarios such as “U.S.–China trade deal probability,” “new tariff escalation risk,” or “high-level diplomatic agreement outcomes,” allowing sentiment to be priced in real time rather than through traditional polling or analyst forecasts.

These markets have become increasingly relevant to crypto participants because geopolitical risk is now tightly linked to digital asset volatility cycles. When tensions rise, liquidity often tightens and risk assets tend to experience sharper repricing, while diplomatic easing can trigger broad-based risk-on rotations.

In the current context, the Trump–Xi meeting is being interpreted less as a single political event and more as a signal node for global macro positioning. Traders are watching whether it leads to policy clarity, trade de-escalation, or further strategic uncertainty between the two nations.

Crypto markets watch macro signals for liquidity direction

Crypto investors are closely monitoring geopolitical developments like this because digital assets increasingly trade as high-beta macro instruments sensitive to global liquidity expectations.

Improved U.S.–China relations could support broader risk appetite by reducing tail-risk uncertainty in global trade, while escalation or breakdown in talks could have the opposite effect, tightening liquidity conditions and increasing volatility across speculative markets.

At the same time, prediction markets are amplifying the speed at which sentiment is priced in. Platforms like Polymarket allow traders to hedge or speculate directly on geopolitical outcomes, effectively turning diplomatic events into tradable macro signals.

As a result, the Trump visit to Beijing is being watched not only as a diplomatic milestone but also as a potential catalyst for shifts across prediction markets, equities, and crypto-linked risk assets, depending on how negotiations and messaging unfold in the coming days.

Bitcoin rebounds slightly above $81k amid institutional caution

Save the Children expose Israel’s sham ‘ceasefire’ as it keeps murdering kids in Lebanon

Teddy Atlas ranks one man above Mayweather and Crawford as the best welterweight of all time

Manchester United reach agreement with Casemiro over contract clause amid transfer speculation

US brings back mandatory military draft registration

Steven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Crypto World5 days ago

Crypto World5 days agoHarrisX Poll Found 52% of Registered Voters Support the CLARITY Act

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Marianne Dress

-

Crypto World6 days ago

Crypto World6 days agoUpbit adds B3 Korean won pair as Base token gains Korea access

-

NewsBeat6 days ago

NewsBeat6 days agoNCP car park operator enters administration putting 340 UK sites at risk of closure

-

Fashion2 days ago

Fashion2 days agoCoffee Break: Travel Steam Iron

-

Fashion3 days ago

Fashion3 days agoWhat to Know Before Buying a Curling Wand or Curling Iron

-

Tech3 days ago

Tech3 days agoAuto Enthusiast Carves Functional Two-Stroke Engine from Solid Metal

-

Politics2 days ago

Politics2 days agoWhat to expect when you’re expecting a budget

-

Business4 days ago

Business4 days agoIgnore market noise, India’s long-term story intact, say D-Street bulls Ramesh Damani and Sunil Singhania

-

Politics4 days ago

Politics4 days agoPolitics Home Article | Starmer Enters The Danger Zone

-

Tech2 days ago

Tech2 days agoGM Agrees To Pay $12.75 Million To Settle California Lawsuit Over Misuse Of Customers’ Driving Data

-

Entertainment6 days ago

Entertainment6 days agoSarah Paulson Called Out For Met Gala ‘Hypocrisy’

-

Politics6 days ago

Politics6 days agoSimon Cowell Says He Was ‘Horrible’ To Susan Boyle During BGT Audition

-

Entertainment6 days ago

Entertainment6 days agoGeneral Hospital: Ric & Ava Bombshell – Ric’s Massive Secret Exposed!

-

Crypto World6 days ago

Crypto World6 days agoRobinhood says Wall Street is building onchain

-

Entertainment7 days ago

Entertainment7 days agoBold and Beautiful Early Spoilers May 11-15: Steffy Revolted & Liam Overjoyed!

-

Sports6 days ago

Sports6 days agoUEFA Champions League final schedule, teams, venue, live time and streaming | Football News

-

Entertainment6 days ago

Entertainment6 days agoWhy David Letterman Called CBS ‘Lying Weasels’

-

Fashion7 days ago

Fashion7 days agoThe Best Work Pants for Women in 2026

-

Entertainment7 days ago

Entertainment7 days agoSister Wives: Tony Flings Shade at Robyn in New Post

You must be logged in to post a comment Login