Crypto World

Nike Stock Hits a 12-Year Low as an Earnings Loophole Masks Weak Sales

Nike (NKE) stock slid about 1% on Wednesday, briefly trading at $40, its lowest level in about 12 years. The fall came despite an earnings beat, because most of the profit came from a one-time tariff refund.

That refund flattered the headline number and did nothing to fix Nike’s shrinking sales. Wall Street responded by trimming price targets, and the charts now point to more downside.

Why the Earnings Beat Triggered Target Cuts

Here is the earnings loophole the title promised. Nike reported a profit of $0.20 per share and beat the $0.13 that Wall Street expected. But most of that profit did not come from selling shoes.

About $0.52 per share (a large part of the $0.72 EPS) came from a $986 million tariff refund, money the government returned after the Supreme Court struck down many of the levies. That is a one-time payment, not a recurring business model.

Take the refund away, and Nike still looks weak. Sales slipped to $10.97 billion, and sales in China fell 12%.

Want more insights like this? Sign up for Editor Harsh Notariya’s Daily Newsletter here.

The market response shows how little faith investors have. A monthly chart from earlier shows Nike has now given back its entire pandemic-era run and sits back at prices last seen in early 2014.

Because the profit was a one-off, analysts cut their price targets instead of raising them. Goldman Sachs trimmed its target to $42 from $46 post-results, and JPMorgan cut to $47 from $52.

UBS stayed the most constructive at $48. Jefferies remains the lone bull among these analysts at $90.

Even so, most reduced targets sit only slightly above the last close near $41. In other words, the Nike stock price upside is not what analysts are betting on right now.

The soft outlook has therefore shifted attention to traders’ positioning.

Bearish Bets Are Building Against Nike Stock

Options traders turned defensive fast. The put-call ratio, which compares bearish put bets to bullish call bets, jumped to 1.14 on June 30 from 0.53 on June 26.

A ratio above 1 means puts now outnumber calls. That marks a sharp swing toward hedging and downside bets around nike earnings.

Meanwhile, volume tells the same story. Nike traded 73.89 million shares, its second-heaviest session since early April, and it came on a down day.

Additionally, Chaikin Money Flow (CMF), a proxy for institutional buying and selling pressure, sits at -0.29. The deep negative reading suggests big money is not stepping in to catch the fall.

More so when the Nike price chart clearly shows a bearish head-and-shoulders pattern with a 14% potential dip.

With flows and positioning aligned bearishly, the price chart becomes the decider.

Nike Stock Price Levels to Watch

The daily chart shows a head-and-shoulders pattern. Nike’s head formed near $47, with a right shoulder around $42.

The neckline now sits near $39, roughly 3% below the last close. A clean break there would confirm the pattern and open the door toward $38 as the first bearish target.

Below that, the measured move points to about $34, with $33 as the deeper extension target. That path frames the dramatic downside now in play.

The bulls still have a case, but it needs work. Nike must reclaim $41 quickly, and a daily close above $42 would signal real strength, the same level analysts already expect the stock to prove.

A push over $43 would improve the tone, while a move above $46 would weaken the bearish setup. Moreover, a clean daily break above $47 cancels the pattern entirely. Traders should note that head-and-shoulders patterns only confirm once the neckline breaks on volume, and failed breakdowns are common.

For now, the $39 neckline separates a slow base-building recovery from a deeper slide toward $34.

The post Nike Stock Hits a 12-Year Low as an Earnings Loophole Masks Weak Sales appeared first on BeInCrypto.

The primary cryptocurrency has staged a minor resurgence over the past week, with its valuation briefly rising to nearly $67,000 and now hovering around $65,000.

However, some analysts warn that this is unlikely to mark the start of a new bull run, envisioning a major collapse in the near future.

Same as 2022?

BTC, which plunged below $58,000 at the end of June, has rebounded by double digits in the following several weeks. And while bulls eagerly await the end of the bear market, the analyst who uses the X moniker BATMAN shut down that optimism.

They believe the cryptocurrency’s recent price increase mirrors the one from the autumn of 2022, which was followed by a massive crash to roughly $16,000.

“Side by side, this level looks concerning. It mirrors a similar bullish pump from 2022 that led to nothing afterward. History might not repeat itself, but it sure does rhyme,” they stated.

Of course, one should keep in mind that the drop below $20K at that time was driven largely by the meltdown of the once-prominent crypto exchange FTX: something that sent shockwaves through the entire digital asset sector.

For their part, X user Kabuki believes that the latest price setup represents a classic bull trap. They think BTC could dump to as low as $47,000 by August before starting a major uptrend move that could take it to over $200,000 by the start of next year.

Monitoring These Vital Levels

X user Ted also gave his two cents, noting the decline from the local high of almost $67K to the current $65K. At the same time, he emphasized the importance of the lower target, arguing that BTC could surge to $67,500-$68,000 if it stays above.

Meanwhile, Bitfinex’s analysts pointed to a key reaction zone between $67,900 and $68,300, where the short-term holder realized price and the second-quarter opening level have lined up. They believe a decisive breakout above or below that range could determine the asset’s direction in the near future.

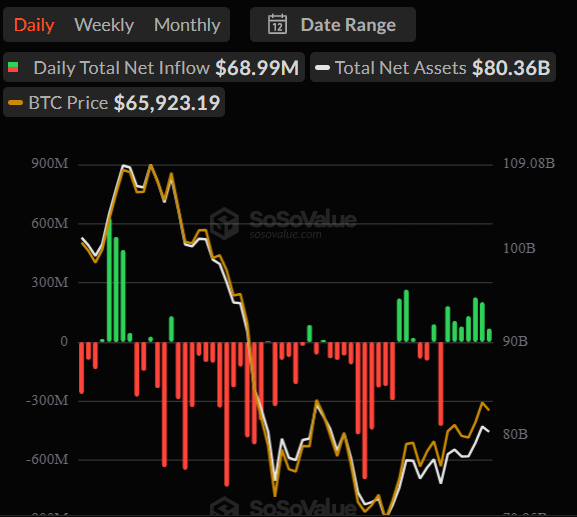

It is important to note that the renewed institutional interest gives hope that Bitcoin hasn’t completely lost its momentum and might soon post fresh gains. According to SoSoValue, the inflows into spot BTC ETFs have surpassed outflows in the past seven consecutive days, something unseen since April.

The development shows that pension funds, hedge funds, and other conservative investors have increased their exposure to the asset, prompting BlackRock, Fidelity, and many other financial giants that have launched such products to purchase Bitcoin, thereby backing their shares. The situation was much different toward the end of June, when spot BTC ETFs saw a weekly outflow of around $1.8 billion.

The post 2022 vs. 2026: Analyst Warns Bitcoin’s Recent Rally Could End in a Massive Crash appeared first on CryptoPotato.

Senate Republicans circulated a revised 616-page Crypto Bill draft on July 22 that includes a White House-backed ethics provision, but no Democrat has publicly endorsed the latest text. Senate Majority Leader John Thune said he wants to move the bill to the Senate floor before the August recess, although it remains unclear whether Republicans can secure the 60 votes needed to advance the legislation.

- The ethics provision bars the president, vice president, members of Congress, senior executive branch officials, and their spouses from issuing or sponsoring certain digital assets while in office.

- The provision designates the U.S. attorney general as the primary enforcement authority and does not authorize state attorneys general to enforce the ethics rules.

- The ethics restrictions would expire in 2029 unless extended by Congress.

- Republicans hold 53 Senate seats, meaning they would likely need support from at least seven Democrats if all senators vote.

The ethics language was negotiated between Senate Republicans and the White House and reflects a compromise the Trump administration was willing to support.

Under the proposal, crypto platforms could be required to avoid listing digital assets issued or sponsored in violation of the ethics rules, while the attorney general could pursue civil enforcement against officials and parties that knowingly violate the provision.

For many Democrats, however, the enforcement structure remains the central concern. They argue that relying solely on the Department of Justice provides insufficient independent oversight, particularly given President Donald Trump’s crypto-related business interests. Those concerns intensified after Trump’s annual financial disclosure reported substantial income tied to crypto ventures, including World Liberty Financial and his memecoin-related businesses.

Discover: The Best Token Presales

Alsobrooks Calls DOJ Only Enforcement ‘An Unserious Offer’

Sen. Angela Alsobrooks (D, Md.), one of the Democrats who has participated in negotiations on crypto legislation, said this week that any enforcement mechanism limited to the Department of Justice is “an unserious offer.” She added that she could not support the bill under its current ethics language while leaving room for further negotiations before a floor vote.

— Coin Bureau (@coinbureau) July 21, 2026

UPDATE: Sen. Angela Alsobrooks said that the White House proposal to have the DOJ enforce the CLARITY Act’s ethics provisions is an “unserious offer.”

UPDATE: Sen. Angela Alsobrooks said that the White House proposal to have the DOJ enforce the CLARITY Act’s ethics provisions is an “unserious offer.”

She also said she will not support the bill if it is the only enforcement option, per Eleanor Terrett. pic.twitter.com/Cb0TwfACeR

The main disagreement is over enforcement. Democrats have repeatedly sought to give state attorneys general independent authority to enforce the ethics provisions. The revised Republican draft instead reserves enforcement authority to the U.S. attorney general, preventing states from bringing their own actions under that section of the bill. Democratic lawmakers have argued for months that stronger and more independent oversight is necessary.

A group of Democratic senators, including Alsobrooks, Cory Booker, Ruben Gallego, and Mark Warner, has also said the current CLARITY Act draft remains inadequate on ethics, consumer protection, illicit finance, and market integrity. Their support could prove critical if Republicans hope to advance the legislation.

Discover: The Best Crypto to Diversify Your Portfolio

Thune’s Floor Timeline Puts Pressure on Both Sides of the Crypto Bill

Thune’s plan to pursue a floor vote before the August recess appears designed to increase pressure on negotiators rather than signal that the bill already has sufficient bipartisan backing. When asked whether the legislation was ready, Thune said he was hopeful but acknowledged that further discussions and possible revisions could still be necessary.

— Coin Bureau (@coinbureau) July 23, 2026

UPDATE: The CLARITY Act is heading toward a Senate vote, even without Democratic support.

UPDATE: The CLARITY Act is heading toward a Senate vote, even without Democratic support.

Senate Majority Leader John Thune plans to bring the crypto bill to the floor as soon as next week, even if no deal is reached with Democrats, per Bloomberg.

The Senate now has just 12… https://t.co/smqbz9EhuQ

The strategy could force lawmakers to either reach a compromise quickly or publicly demonstrate that bipartisan support remains out of reach. If the bill fails to advance before the Senate leaves for the August recess, negotiations could resume later in the year, although the legislative timeline would become less predictable.

The broader crypto regulation package would establish clearer jurisdiction between the SEC and CFTC, create a regulatory framework for digital assets, and include provisions affecting decentralized finance developers and blockchain infrastructure participants. While Republicans hoped the revised ethics language would attract Democratic support, negotiations remain ongoing, and the bill’s prospects are still uncertain.

Trade Crypto Before The Crypto Bill Passes on Bybit and Get a Chance to Win Our $1,000 USDT Airdrop

The post Crypto Bill Stalls as Democrats Reject DOJ-Only Ethics Enforcement appeared first on Cryptonews.

Cointelegraph is committed to providing independent, high-quality journalism across the crypto, blockchain, AI, and fintech industries.

All news, reviews, and analyses are produced with full journalistic independence and integrity. For more details on our standards and processes, please read our Editorial Policy.

Crypto World

BlackRock, Coinbase, Strategy pledge $15 million to prepare Bitcoin for quantum threats

A total of nine companies have formed a consortium pledging a combined $15 million over three years to support Bitcoin security research and open-source development.

Companies in the newly formed Bitcoin Security Consortium include major crypto market participants including BlackRock, Coinbase, Strategy, Anchorage Digital, ARK Invest, Block, Blockstream, Fidelity Digital Assets and Galaxy.

The group will focus partly on preparing Bitcoin for advances in quantum computing and will publish material tracking the state of Bitcoin security work for investors and the public.

The $15 million will not be held or allocated by the consortium, but instead member will choose which developers, researchers or organizations it funds. The group said it will not direct Bitcoin development or take positions on proposed protocol changes.

“Bitcoin Core developers do incredibly important work,” BlackRock digital assets head Robert Mitchnick said, adding that the group would make additional funding available for Bitcoin’s long-term security.

The announcement did not disclose individual contributions, initial recipients or how much of the funding represents new commitments.

Michael Saylor’s Strategy announced the launch of the Bitcoin Security Consortium, a group of financial institutions and Bitcoin companies supporting the long-term quantum security of the Bitcoin network.

The consortium pledged an aggregate $15 million over the next three years to support developers securing the Bitcoin network against the threat of a quantum computing breakthrough, Strategy announced in a Thursday press release.

Other founding members include Anchorage Digital, ARK Invest, BlackRock, Block, Blockstream, Coinbase, Fidelity Digital Assets and Galaxy. The consortium’s day-to-day work will be coordinated by Mike Schmidt, who serves in a volunteer capacity and is the executive director of Brink, a non-profit that supports Bitcoin open-source developers.

On Wednesday, Galaxy Digital pledged up to $5 million in grants for developers working on Bitcoin’s quantum security and elected a council of quantum-advisory experts to research quantum-resistant migration solutions.

Bitcoin’s quantum security is a growing concern in the community, though the timeline of a quantum breakthrough remains hotly debated. In November 2025, Blockstream CEO Adam Back said that Bitcoin faces no meaningful quantum threat for at least the next 20 to 40 years.

In contrast, an April report from investment manager Bernstein said that Bitcoin has about three to five years to prepare for a post-quantum security upgrade.

BlackRock’s global head of digital assets, Robert Mitchnick, said that Bitcoin core developers do “incredibly important work” and that the asset management company was pleased to make “significant additional funding available to support Bitcoin’s long-term security needs.”

Magazine: Bitcoin’s quantum upgrade path: What BIP-360 changes and what it does not

The European Union agreed on Thursday to its 21st sanctions package against Russia. EU persons are now barred from transacting with 11 unnamed crypto operators and 94 banks and financial institutions.

While names of the 11 crypto platforms have been withheld, the EU has revealed that they mostly operate in Belarus and Nigeria, acting as conduits to funnel money between Russia and countries blocked from doing business with it.

Previously, Brussels was limited to sanctioning individual firms. It now has the power to bar crypto services from an entire nation or jurisdiction if it is viewed as a hub for laundering Russian financial transactions, an unprecedented development in the battle against sanctions evasion.

Stablecoins and The Garantex Trail

This package is the latest in a series of moves to tighten the net on crypto services tied to the ruble. Earlier this year, the A7A5 stablecoin, which acted as a bridge between sanctioned exchanges Garantex and Grinex, was designated, followed by the RUBx token and digital ruble.

The UK moved in parallel, sanctioning the HTX (formerly Huobi) exchange in May over alleged ties to A7 and Garantex. A Global Ledger report found HTX had processed around $21 billion in ‘high-risk’ crypto transactions over the last 5 years, with almost $8 billion of it tied to Russian actors and darknet markets.

Broad Scope: Banks, Oil And The Shadow Fleet

The package designates 94 financial institutions, including 32 banks and the Moscow stock exchange, freezing their EU-held assets and banning transactions with them. It also targets vessels in Russia’s shadow fleet for the first time.

I welcome the agreement on the 21st sanctions package against Russia.

At a time when Ukraine has built military momentum, our sanctions continue to weaken the economic foundations of Russia’s war effort.

We’re adding 32 more Russian banks to our transaction ban list.

As well…

— Ursula von der Leyen (@vonderleyen) July 23, 2026

European Commission President Ursula von der Leyen confirmed a freeze on oil cap prices at $44.10 a barrel ‘so that the Russian war machine does not benefit from market shocks,’ adding that Brussels also plans on banning Russian combatants from entering the EU.

The post EU Hits Russia With Toughest Crypto Crackdown Yet appeared first on CryptoPotato.

An ongoing hacking spree has claimed another three victims in the past 24 hours, with a total of over $35 million lost.

Verus bridge has lost over $7.5 million, just two months after being hit by a similar hack which claimed $11 million. Proceeds of the May exploit were partially returned following a 25% bounty offer.

Now, AFX is offering a 30% bounty in response to losing $24 million USDC from its Arbitrum bridge.

In an increasingly bleak landscape for legitimate security researchers, such generous offers are, at best, insulting, and, at worst, may even tempt those with such skills to the dark side.

Read more: Across, Allbridge, TeleSwap lost $5.7M to bridge hacks in past week

Verus bridge hacked again

Following the return of 75% of the funds lost in May’s hack, the assets were sent from the recovery address back into the Verus bridge just 14 days ago.

In the early hours of Thursday, a wide range of assets (tBTC, ETH, USDC, scrvUSD, MKR, USDT and EURC) totaling $7.5 million were withdrawn from the bridge in a single transaction.

According to blockchain auditor SlowMist, both exploits share a root cause of “flawed cross-chain import validation,” though with slightly different attack vectors.

This time it looks much less likely that Verus will see the money again, however. The attacker has since deposited a total of 3,916 ETH (over $6.6 million) to Tornado Cash.

Read more: Bridge hacks back in vogue as Verus exploit brings 2026 total to $329M

AFX’s USDC bridge drained of $24M

Late on Wednesday, AFX’s USDC custody bridge on Arbitrum was drained of over $24 million. Security firm BlockSec believes this to be a “malicious use of authorized validator keys,” which were used to sign “the bridge’s 5-of-7 validator quorum.”

Responding to the incident, AFX stated it had suspended bridge operations and is “investigating the root cause.”

It reassured users that its “AFX trading infrastructure, mainnet, and the Arbitrum network itself have not been compromised.”

AFX has also offered a 30% bounty, worth $7.2 million, for the return of the remaining funds, “as a white hat bounty.” Security expert Taylor Monahan, again, questions the wisdom of such a move.

Read more: More oracle exploits as Ostium loses over $20M

Another audit firm, Peckshield, notes that the exploiter has since swapped the funds for over 12,000 ETH, worth approximately $24 million. Funds remain in the attacker’s address on Ethereum.

Since the beginning of last week, bridge exploits have claimed at least $40 million.

BSquared staking contract emptied

Finally, BTC-for-AI-agents project BSquared was hacked for almost $4 million due to “unauthorized access to the staking contract’s upgrade authority.”

The team has promised affected B2 stakers will be fully compensated, and is offering the standard 10% bounty.

Read more: Supra patched oracle on 11 other chains before $9M Hedera exploit

The contract was drained of $3.86 million worth of B2 tokens on BNB Chain. According to blockchain investigator Specter, which flagged the theft, the tokens were swapped to WBNB, bridged to Ethereum and moved to privacy protocol Zcash.

They claim that the privileged role has been active for over a year, which may point to an inside job.

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

XRP price climbed from around $1.11 to $1.14 during the past week, briefly testing resistance near $1.16 before easing back despite its bullish prediction. The move looked constructive, but buyers are now facing a key ceiling. A decisive break above recent highs could open the door toward $1.32. Otherwise, the rally risks fading as short-term traders lock in profits.

The latest advance follows nine consecutive weeks of net inflows into XRP investment products, totaling about $17.2 million. However, the pace of fresh inflows has slowed. The most recent weekly figure fell to roughly $12 million, suggesting institutional demand remains positive but is no longer accelerating.

Price can lead fund flows for a while, yet that relationship becomes less reliable when inflows begin to cool. As a result, traders chasing strength should watch whether demand catches up. If it does not, momentum could fade even if the technical picture still appears healthy.

Meanwhile, the CLARITY Act and the U.S. regulatory outlook remain important catalysts for XRP. Clearer rules could strengthen institutional conviction and support another leg higher. On the other hand, delays or weaker-than-expected progress may encourage investors to stay cautious despite the recent price recovery.

Discover: The Best Token Presales

XRP Price Prediction: Push to $1.65? Or is the Handle Getting Too Long?

XRP is working through a potential cup-and-handle pattern that has been developing since early July. However, the neckline now sits closer to the $1.16 to $1.17 area. The recent consolidation since July 21 still resembles the handle, provided buyers defend the current support. Meanwhile, lighter selling volume during the pullback suggests profit-taking rather than aggressive distribution.

Support is clustered around $1.12 to $1.13, where recent lows have attracted buyers. A stronger floor sits near $1.05 if selling pressure increases. On the upside, immediate resistance stands between $1.16 and $1.18, followed by $1.32. A breakout above that level could expose the next resistance near $1.46.

The earlier breakout from the $1.14 area came with a noticeable jump in trading volume. That move established a benchmark for meaningful market participation. As a result, traders will likely watch for another volume spike before treating any breakout as sustainable.

The bullish case calls for XRP to reclaim and hold above $1.18 on a daily close. If buying momentum strengthens, the price could revisit $1.32 before testing $1.46. The base case keeps XRP trading between $1.12 and $1.18 as traders wait for fresh regulatory or macro catalysts.

The bearish prediction emerges if XRP price closes below $1.12 on rising volume. That would weaken the handle setup and increase the risk of a move toward $1.05. MVRV data also adds an interesting twist. Negative 30 day and 365 day MVRV readings suggest many holders remain underwater, a condition some contrarian investors see as an opportunity rather than a warning.

Trade XRP on Bybit and Get a Chance to Win Our $1,000 USDT Airdrop

LiquidChain Eyes Early-Stage Entry as XRP Tests Resistance Ceiling

XRP at $1.50 is a different bet than XRP at $1.10. The asymmetry has compressed. That’s exactly when traders with a higher risk appetite start looking at earlier-stage setups where the entry price hasn’t already priced in the narrative. ETF inflow dynamics benefiting established assets don’t always filter down to infrastructure plays at presale prices, which is partly the point.

The next generation of infrastructure won't stand alone. — LiquidChain (@getliquidchain) July 21, 2026

It'll connect everything around it.  ⟁https://t.co/vqvBcdSQYC pic.twitter.com/mWc9fGndPd

⟁https://t.co/vqvBcdSQYC pic.twitter.com/mWc9fGndPd

LiquidChain ($LIQUID) is a Layer 3 infrastructure project positioning itself as a unified execution environment that merges Bitcoin, Ethereum, and Solana liquidity into a single settlement layer.

The architecture powers Unified Liquidity Layer, Single-Step Execution, Verifiable Settlement, and Deploy-Once Architecture, which targets the fragmentation problem that makes multi-chain DeFi operationally expensive. Current presale price is $0.01482. Total raised stands at $915K.

DYOR applies harder here than on a liquid mid-cap. For traders who’ve done the work, the LiquidChain presale details are worth reviewing directly.

Discover: The Best Crypto to Diversify Your Portfolio

The post XRP Price Breaks Resistance, But ETF Flows Warn Bulls appeared first on Cryptonews.

Dogecoin is trading under $0.073, moving little over the past 24 hours after another quiet session. Even so, the meme coin remains under pressure from last week’s pullback. Still, TD Sequential buy signals have appeared consecutively on the weekly chart, a setup that analyst Ali Martinez says has often preceded strong rallies.

The pattern has caught traders’ attention because consecutive weekly buy signals are rare. Martinez noted this type of cluster has historically come before major directional moves. Whale activity and derivatives data also remain mixed. Open interest has eased slightly, while spot taker CVD briefly favored buyers before that momentum faded.

Elon Musk liking a DOGE-related memecoin post created fresh headlines, but little changed on the chart. Price barely reacted, leaving technicals as the main focus. For now, traders appear more interested in whether the weekly signal confirms than in social media-driven speculation.

Meanwhile, the wider crypto market has offered little support. Bitcoin failed to hold above $66,500, keeping risk appetite in check across major altcoins. Dogecoin also remains below the $0.088 area, which previously acted as an important support level. Until that zone is reclaimed, bulls still have work to do.

Discover: The Best Token Presales

Can Dogecoin Price Break $0.075 Resistance This Week?

Dogecoin is consolidating in a tight range near $0.073 after several quiet sessions. Short-term forecasts still point to limited movement, with the price expected to remain inside a narrow band through this week. Even if buyers regain control, the projected upside remains modest unless trading volume picks up.

Support sits around $0.0722, followed by $0.0712 and the stronger floor near $0.0705. Meanwhile, resistance stands at $0.0740, $0.0746, and $0.0757. Those levels could slow any recovery before DOGE challenges the $0.088 area that previously acted as key support.

Technical indicators still lean cautiously. The 50-day moving average continues to slope lower, reflecting the recent downtrend. Even so, the weekly TD Sequential buy signal remains active, giving bulls a reason to watch for a reversal instead of chasing momentum too early.

The bullish case is straightforward. Dogecoin needs to defend $0.0705, attract stronger volume, and close the week above $0.0754. That could open the door toward $0.0793. Otherwise, the base case remains sideways trading between $0.0705 and $0.0755, while a break below support would leave sellers firmly in control.

Trade Memecoins like DOGE on Bybit and Get a Chance to Win Our $1,000 USDT Airdrop

Maxi Doge Eyes Early-Stage Upside as DOGE Tests Critical Resistance

DOGE at $0.074 with a $1 billion OI overhang is a trade, not a position. The asymmetry that existed at lower prices has compressed. Even a successful squeeze to $0.076 represents roughly 4% upside from here, meaningful on leverage, limited in spot. Traders looking for a larger risk-reward multiple are scanning earlier on the curve.

Maxi Doge ($MAXI) is an ERC-20 meme token built around a trading community thesis: the 240-lb canine juggernaut persona embodies 1000x leverage culture, and the project channels that into structured community mechanics.

The presale has raised closer to $5 million at a current price of just $0.000283, with a dynamic staking APY live for holders. Differentiating features include holder-only trading competitions with leaderboard rewards, a Maxi Fund treasury allocated to liquidity and partnerships, and meme-first marketing that leans into gym-bro culture without apology.

Research Maxi Doge before the next stage reprices.

Discover: The Best Crypto to Diversify Your Portfolio

The post Dogecoin Flashes Heavy Buy Signals, Price Yet to Move appeared first on Cryptonews.

Ethereum price has remained trapped below $2,000 as rising oil prices, renewed interest-rate concerns and BitMEX’s planned shutdown have tempered bullish sentiment despite continued spot ETF inflows.

Summary

- Ethereum price remains below $2,000 as higher oil prices revive Federal Reserve rate-hike concerns.

- Spot ETF inflows and positive capital flows continue to support ETH above $1,900.

- A break above $1,955 could target $2,030, while losing $1,860 would weaken the recovery.

According to data from crypto.news, Ethereum (ETH) price traded near $1,927 on July 23 after reaching an intraday high of $1,941. The token has recovered more than 27% from its June low near $1,514, but repeated failures around $1,955 have kept the psychological $2,000 level beyond buyers’ reach.

Oil supplied the latest macro pressure as Middle East tensions pushed crude prices higher for a fifth consecutive session. West Texas Intermediate rose above $90 a barrel after attacks by Iran-aligned Houthis on Saudi oil tankers raised concerns about regional supplies. Higher energy costs could feed inflation and reduce the Federal Reserve’s room to keep monetary policy unchanged.

Rate traders have already adjusted their positions. The probability of a September Fed hike rose to 79% from 68% per data from the CME FedWatch tool. Expectations for the July meeting remain centered on no change, but another oil-led inflation increase could lift Treasury yields and pressure risk assets such as Ethereum.

U.S. equities also weakened after Alphabet raised its 2026 capital-spending forecast to between $195 billion and $205 billion. The company recorded negative free cash flow of $5.9 billion as quarterly expenditure doubled to $44.9 billion, while its shares fell in premarket trading.

A retreat across technology stocks could limit speculative demand in crypto markets because both sectors remain sensitive to interest-rate expectations.

ETF demand has kept Ethereum above its rising support structure

Institutional flows have provided a counterweight to the macro uncertainty. U.S. spot Ethereum ETFs recorded $72.64 million in net inflows on July 22, according to SoSoValue. BlackRock’s iShares Ethereum Trust accounted for $53.47 million, showing that regulated products continued to attract capital even as ETH struggled below $2,000.

BitMEX added a separate source of uncertainty after announcing that it would cease operations on Sept. 23 following a strategic review by parent company HDR Global Trading. The exchange told customers to close positions and withdraw funds before the deadline. BitMEX helped popularize perpetual swaps and has served more than 2 million professional and institutional traders since its 2014 launch.

Position transfers and forced closures at BitMEX could temporarily reduce liquidity or move leverage to rival exchanges. However, the announcement does not mean Ethereum’s global perpetual market will close, because Binance, Bybit, OKX and other venues operate larger derivatives businesses.

Ethereum’s daily chart remains constructive above the Supertrend support at $1,744.73. The indicator has stayed green during the July advance, while the Chaikin Money Flow reading of 0.12 shows that buying volume has exceeded selling volume over the indicator’s measurement period. Price must still close above the nearby $1,941–$1,955 ceiling before the daily structure opens a route toward $2,000.

According to analyst Ted Pillows, spot-market demand has protected the recovery’s main support zone.

“Spot demand is strong and the key support zone hasn’t been lost. IMO, Ethereum could begin its next move up in a few days.”

Pillows placed $2,030 as the first major upside barrier, followed by $2,179 and a heavier supply zone near $2,400. His chart also identified support between roughly $1,834 and $1,897, with lower demand areas around $1,730 and $1,540.

The 4-hour chart shows ETH compressing beneath $1,955.40 while holding an ascending trendline drawn from the June 26 low. Buyers have also defended the 78.6% Fibonacci retracement at $1,860.86, leaving the sequence of higher lows intact. A 4-hour close above $1,955 would clear the recovery high and place $2,000–$2,030 within reach.

Momentum has weakened before that test. The 4-hour Relative Strength Index has fallen to 57.46 from its recent highs and sits below its signal average of 63.30. MACD has also registered a bearish crossover, with the MACD line at 13.48 beneath the 15.94 signal line and the histogram at minus 2.46. Neither indicator confirms a trend reversal, but both show that buyers have lost speed near resistance.

Break below $1,860 would invalidate the immediate breakout setup

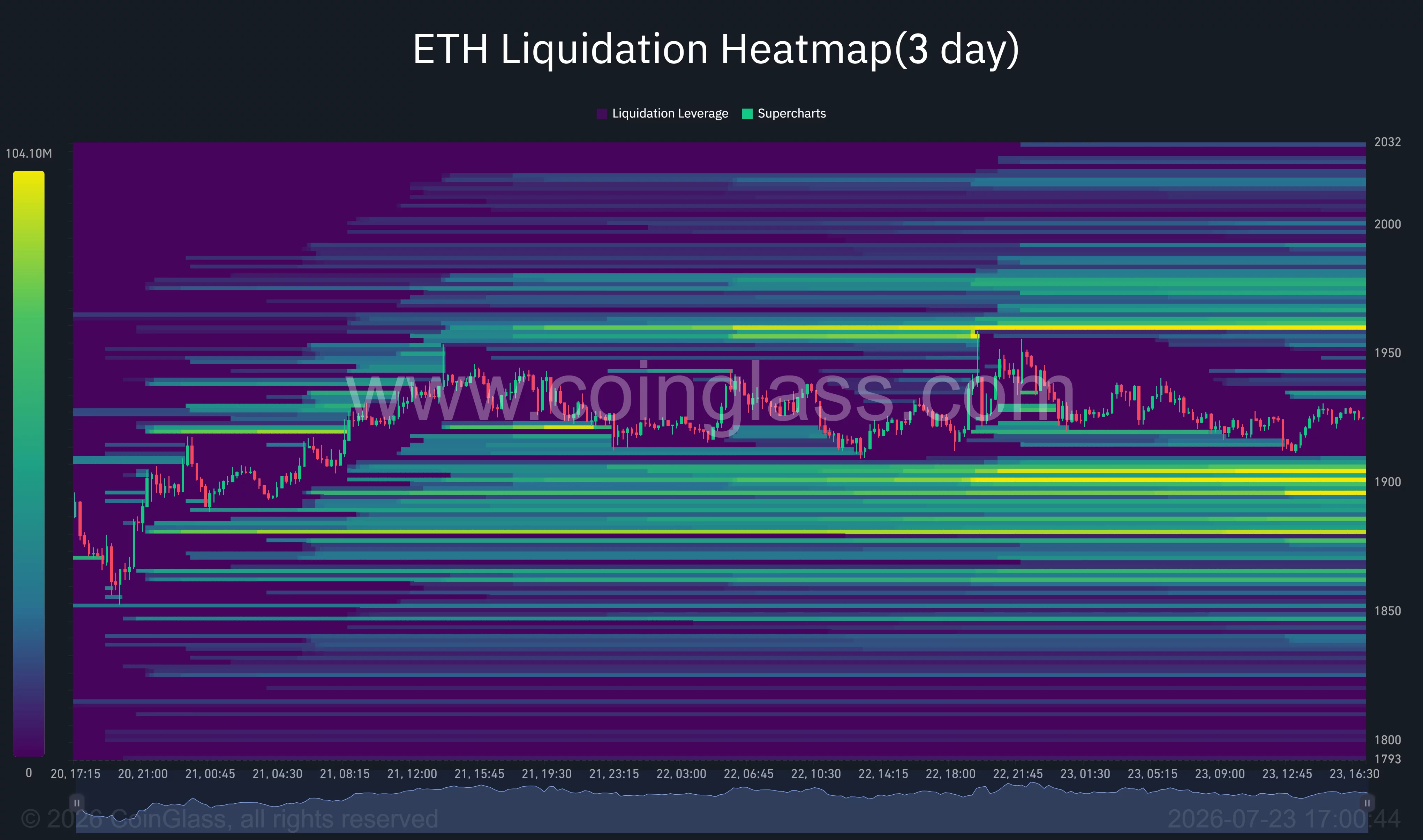

CoinGlass’s three-day liquidation heatmap places the largest nearby short-liquidation concentration around $1,958–$1,965. A move through that band could force bearish positions to close and accelerate a test of $2,000. The strongest downside liquidity sits near $1,895–$1,905, with another dense pocket around $1,875.

Failure to hold the rising 4-hour trendline would expose the $1,860 Fibonacci level first. A close below that support would weaken the higher-low structure and raise the risk of a decline toward $1,786.63, followed by daily Supertrend support near $1,745. Losses below $1,745 would invalidate the current recovery thesis and reopen $1,682.

Oil supply disruptions, a higher September rate-hike probability, and forced position reductions before BitMEX closes remain the main external risks. Ethereum needs sustained spot volume above $1,955 to confirm a breakout; without it, liquidity around $1,900 may continue to pull price back into the established range.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Jennifer Lopez Still Can’t Escape Ben Affleck After Split

The House Opinion Article | Are we really considering a bin for Clacton?

Q and A: Hockey Canada’s Scott Salmond talks CHL, world juniors, goaltending

-

NewsBeat7 days ago

NewsBeat7 days agoLondon Mayor Sadiq Khan handed a peerage by Keir Starmer alongside 15 other Labour figures… just days before the PM leaves No10

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread – Corporette.com

-

Politics5 days ago

Politics5 days agoThe House | The City of London can help the new chancellor deliver growth in every postcode

-

Crypto World5 days ago

Crypto World5 days agoRipple Payments Joins MiCA With 14 Firms, Does It Mean Anything For XRP?

-

Crypto World6 days ago

Crypto World6 days agoTwo July Windows Left: The CLARITY Act’s Senate Fight and What Failure Means

-

Politics4 days ago

Politics4 days agoDemocrats look to World Cup watch parties to register thousands of voters

-

Crypto World6 days ago

Crypto World6 days agoRipple wins EU-wide access as ESMA adds it to MiCA register

-

Crypto World2 days ago

Crypto World2 days agoGrayscale Files For Worldcoin ETF, WLD Registers Sharp Rise

-

NewsBeat3 days ago

NewsBeat3 days agoUnregistered fitter used Gas Safe logo on business flyers

-

Tech3 days ago

Tech3 days agoSail Virtually Aboard The “Itanic” With IA-64 Emulator

-

Crypto World7 days ago

Crypto World7 days agoInjective Submits SEC Transfer-Agent Registration to Onchain Ownership Records

-

Tech2 days ago

Tech2 days agoTurtle Beach Command Series KB7 review: a nifty screen-equipped gaming keyboard

-

NewsBeat6 days ago

NewsBeat6 days agoRegistration is now open for March for Men with Kev 2026

-

Business1 day ago

Business1 day agoNew Jersey voter registration controversy explained: How 6,600 noncitizens got on the rolls, and what happens next

-

Crypto World7 days ago

Crypto World7 days agoClaude Fable 5 Slips to Second in AI Coding Leaderboard

-

News Videos6 days ago

News Videos6 days agoMoney | Class 12 Economics | CBSE Board Exam 2026-27

-

Business7 days ago

Business7 days agoBanco Bilbao Vizcaya Argentaria, S.A. (BBVA) Discusses Global Macro Environment and Economic Outlook for Core Markets Transcript

-

Crypto World5 days ago

Crypto World5 days agoKaspersky exposes OkoBot’s 20-module crypto wallet attack

-

News Videos4 days ago

News Videos4 days agoBig Money Is Entering XRP

-

Business6 days ago

Business6 days agoAirlines warn Sunshine Protection Act could disrupt flight scheduling

You must be logged in to post a comment Login