Crypto World

SBI bets $76M on EDX as institutional crypto race heats up

EDX Markets closed a $76 million Series C funding round led by Japan’s SBI Holdings. The Chicago-based company announced the deal on July 7, 2026. EDX said it will use the capital to expand trading, clearing, and settlement services. It also plans to speed up product development and grow its operations outside the United States.

Summary

- SBI led EDX Markets’ $76 million round to expand institutional crypto trading and clearing worldwide.

- EDX will fund product growth, global expansion, settlement services, and its planned national trust bank.

- Ripple Prime integration gives institutions unified access to EDX spot markets and perpetual futures liquidity.

SBI acted as the sole investor in the equity round, according to EDX chief executive Tony Acuña-Rohter. The company did not disclose its valuation or other deal terms. Earlier backers include Charles Schwab, Citadel Securities, Fidelity Investments, Sequoia Capital, Paradigm, and other market firms. This marks the first funding round whose size EDX has publicly disclosed. Acuña-Rohter said EDX was “pleased to welcome SBI as a strategic partner.”

Funding supports institutional crypto infrastructure

EDX runs an institutional-only crypto marketplace and a central clearinghouse. Its U.S. venue offers spot trading, while EDXM International provides perpetual futures to eligible non-U.S. institutions. The company follows a market structure used by traditional exchanges. It separates trading from some clearing and custody functions to reduce conflicts between service providers.

The new funding will support infrastructure for banks, trading firms, and other professional clients. EDX plans to improve its clearing process, settlement systems, and risk controls. The company also aims to add products as more institutions seek regulated access to crypto markets. SBI chairman Yoshitaka Kitao said “trusted market infrastructure will serve as a critical foundation for institutional adoption.” The SBI Holdings announcement described EDX as part of its wider digital asset strategy.

EDX expands products and seeks a trust bank charter

Earlier in 2026, EDX launched EDX FlowConnect, a crypto-as-a-service product. The service lets companies add digital asset trading for their customers without building a full exchange system. EDX provides tools for execution, liquidity access, clearing, settlement, and related market operations. The Series C capital will help the company expand this service and support more institutional clients.

EDX has also applied to the U.S. Office of the Comptroller of the Currency to form EDX Trust, National Association. The OCC listed the application as received on March 26, 2026. If approved, the national trust bank would provide custody, clearing, settlement, and risk management. It would operate alongside EDX’s trading venues as a separate regulated entity.

Crypto.news links funding to EDX’s wider expansion

A July 8 crypto.news report said the round follows EDX’s recent growth across spot trading, perpetual futures, clearing, and settlement. The report also linked the funding to EDX’s work with Ripple Prime. That integration gives institutional clients access to EDX spot liquidity and EDXM International perpetual futures through one prime brokerage system.

Ripple Prime announced the integration in May 2026. The companies also plan to use RLUSD for settlement and collateral on EDX. The arrangement has not placed XRP in the main settlement role. SBI’s own digital asset plans include the yen-based JPYSC and support for dollar stablecoins such as RLUSD and USDC in Japan.

The $76 million round gives EDX more capital as it targets large financial institutions. SBI gains a strategic position in a trading and clearing company built for professional clients. EDX will now focus on product delivery, international growth, its FlowConnect service, and the pending EDX Trust application.

A wallet last active when Bitcoin was trading near $6,500 transferred $188 million of its holdings in recent days, its first onchain movement in seven years.

With the biggest cryptocurrency now trading at around $64,000 apiece, the whale transferred 2,931 Bitcoin (BTC) from wallet “356my” to wallet address “bc1qn” on Sunday, according to blockchain data platform Arkham.

The whale is likely looking at a nearly 10-fold gain on the long-dormant holdings, according to blockchain analytics platform Onchain Lens.

The transaction comes during a period when whale transfers — those at a minimum of $10 million per Coinglass — are accounting for the majority of Bitcoin flowing to cryptocurrency exchanges. Large whale transfers to exchanges often precede sales, which can place additional pressure on Bitcoin’s price.

Crypto wallet address 356my, transactions and token balance history. Source: Arkham

Fast becoming year of the whale

Whales have been driving most of the Bitcoin inflows to cryptocurrency exchanges since the beginning of the year.

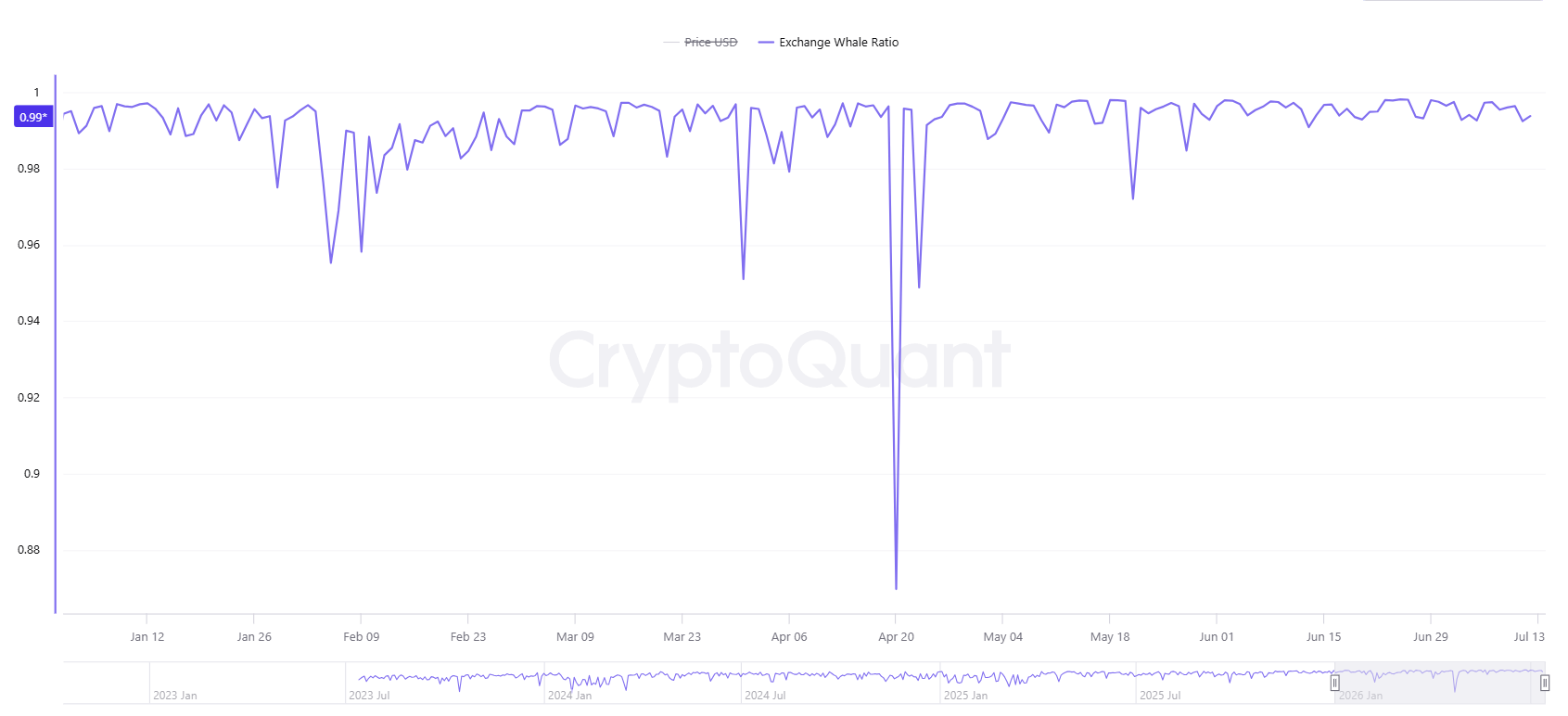

About 99% of BTC deposited to exchanges is currently from the 10 largest individual transfers, according to CryptoQuant’s chart tracking the ratio of whale transfers to exchanges, which stood at 0.99 at press time.

Bitcoin: Exchange Whale Ratio – all exchanges, year-to-date chart. Source: CryptoQuant

A high exchange ratio means that whales account for a disproportionate share of inflows, which is “historically a bearish signal” as these large deposits are more likely to precede significant sell orders than routine retail activity, according to the analytics platform.

Related: Strategy sells 3,588 Bitcoin for $216M to fund dividends, keeps $2.55B reserve intact

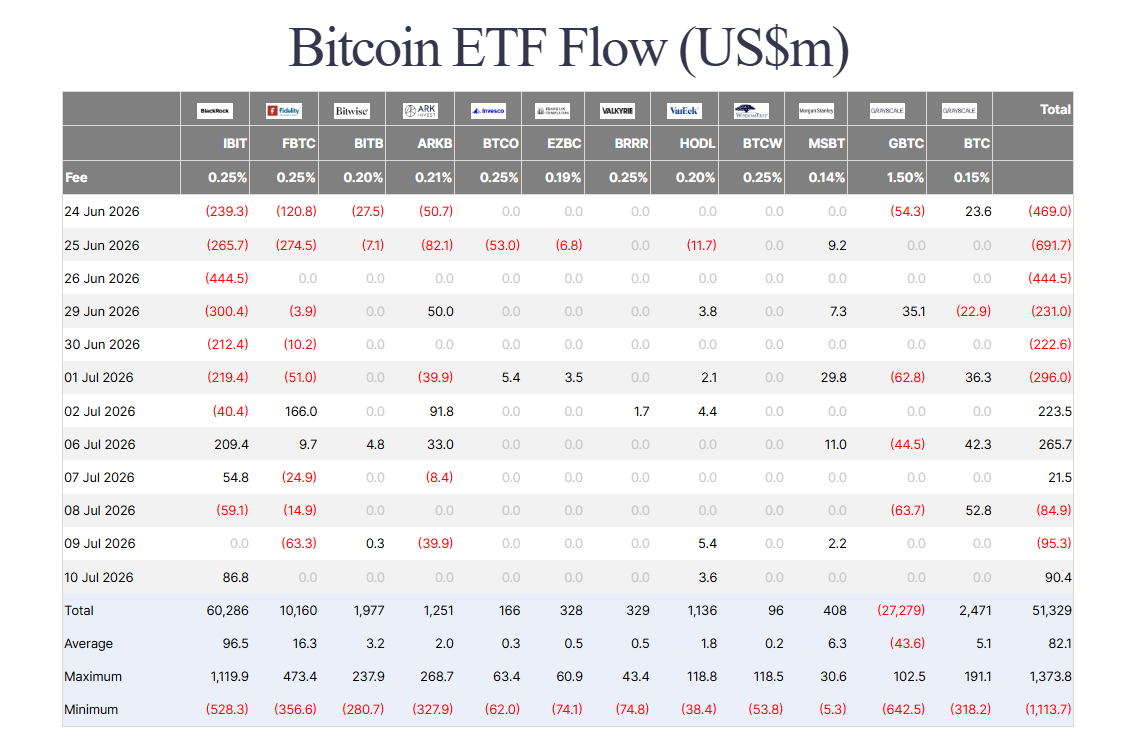

The whale transfers may add to the persistent Bitcoin selling pressure from spot Bitcoin exchange-traded fund (ETF) holders.

Bitcoin ETF Flow (USD, million). Source: Farside Investors

US-traded spot Bitcoin ETFs registered $197 million in net weekly inflows leading up to Friday, but saw $4.51 billion in net outflows in June, marking their worst month on record, according to Farside Investors data.

Magazine: Bitcoin nearing late stages of bear market: Jamie Coutts, Real Vision

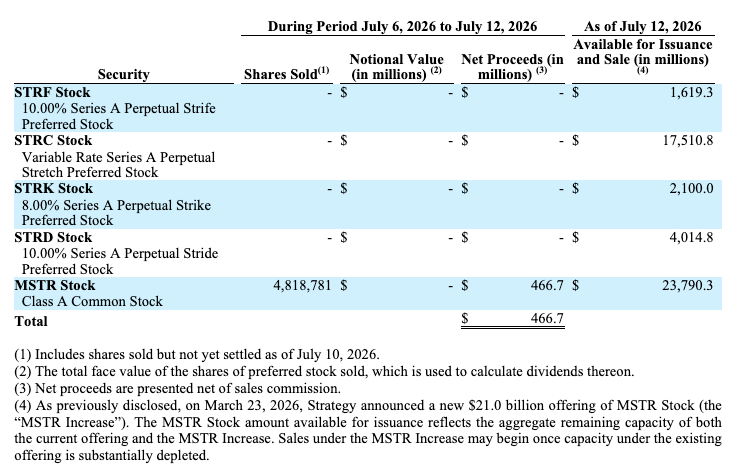

Strategy, the largest corporate holder of Bitcoin, has raised additional capital by selling shares under its at-the-market (ATM) program while keeping its Bitcoin treasury unchanged during the latest reporting window. In its most recent SEC update, the company detailed the size of the equity issuance and reaffirmed that no BTC trades occurred in the period.

According to an 8-K filing dated Monday, Strategy sold 4.8 million shares of its Class A common stock for $466.7 million between July 6 and July 12. The filing also states that Strategy held 843,775 BTC at an average purchase price of $75,476 per BTC, with no Bitcoin purchases or sales reported during the same timeframe.

Key takeaways

- Strategy raised $466.7 million by selling 4.8 million shares through its ATM offering from July 6–12, without altering its BTC holdings.

- The company reported 843,775 BTC at an average purchase price of $75,476 and disclosed no BTC transactions in the period covered by the filing.

- Strategy’s reported US dollar reserve increased to $3 billion as of July 12, supporting preferred dividends and debt interest obligations.

- The company continues to expand its equity-capacity runway, citing $23.8 billion of remaining ATM capacity, including capacity from a $21 billion additional offering announced earlier this year.

- Strategy is preparing its first semi-monthly dividend cycle for preferred shareholders, with near-term payment dates tied to new record-date rules.

Equity funding without touching the Bitcoin treasury

Strategy’s latest SEC filing highlights a deliberate split between raising fiat liquidity and managing its Bitcoin inventory. During the July 6–12 window, the company used its ATM program to issue shares and generate cash, but it reported no spot BTC activity.

The reported balance of 843,775 BTC suggests Strategy continues to treat its Bitcoin treasury as a long-horizon asset rather than a pool to be actively traded in response to short-term liquidity needs. That approach matters for investors watching whether Strategy’s BTC exposure remains steady while it scales the rest of its capital structure.

As investors monitor day-to-day market dynamics, the filing also landed while MSTR shares were reportedly down roughly 3% near the Nasdaq open to about $91.80 per share, according to Yahoo Finance. Bitcoin was trading around $62,580, down more than 2% over the prior 24 hours.

Cash buffer climbs to $3 billion

Beyond the share-sale figures, the 8-K update focused on Strategy’s liquidity position. The company reported its US dollar reserve at $3 billion as of July 12, up from $2.55 billion one week earlier.

Strategy said this cash reserve is used for operational obligations tied to its preferred stock dividends and interest payments on its outstanding debt. Importantly for readers tracking settlement mechanics, the reserve is also described as including expected proceeds from ATM share sales that had not yet settled as of the reporting date.

The update reinforces that Strategy’s financing strategy is not solely reliant on selling Bitcoin. Instead, the company is using equity issuance—at least in this period—to increase its USD buffer, potentially reducing the need for BTC sales to meet near-term payment requirements.

ATM capacity remains significant, with more runway available

Strategy also disclosed remaining capacity under its ATM framework. The company said it has $23.8 billion of available capacity, which includes capacity related to a new $21 billion offering announced on March 23. Strategy noted it may begin selling shares under this additional capacity once the existing offering has been substantially depleted.

That matters because the ATM program effectively functions as a flexible funding channel. For investors, the key question is how quickly Strategy can draw on this capacity while still maintaining its broader Bitcoin-oriented corporate posture.

In a separate development referenced in the update, Strategy previously sold BTC to replenish its US dollar reserve. The company announced it sold 3,588 BTC for about $216 million to fund preferred dividend payments, with the transactions described as:

- 1,363 BTC sold at an average price of $59,256 between June 29 and June 30

- 2,225 BTC sold at an average price of $60,773 between July 1 and July 5

In the same earlier June 29 8-K filing, Strategy reportedly stated it made no BTC purchases and disclosed the sale of 12.7 million shares through its ATM offering, generating $1.15 billion in net proceeds. Together, those disclosures show an ongoing balancing act between equity issuance and selective BTC sales to meet liquidity targets.

Earlier coverage from Cointelegraph discussed the rationale behind the company’s $216 million BTC sale, framing the decision in the context of Strategy’s preferred dividend obligations and its overall capital strategy.

Preferred dividends shift to a semi-monthly rhythm

Strategy’s equity and cash management also intersects with its dividend schedule. The company is preparing for its first semi-monthly dividend payment to holders of its STRC preferred stock on Wednesday.

In an announcement from June 8, Strategy said the new schedule would use record dates on the 15th and the last day of each month, with payments made on the following record date. The first semi-monthly record date was June 30, 2026, and the first payment date was scheduled for July 15, according to Strategy’s release.

With dividends arriving more frequently, the importance of Strategy’s updated cash reserve could rise. For preferred investors, the operational question becomes how consistently Strategy can fund distributions through a mix of ATM proceeds, reserve management, and—when necessary—BTC sales.

What to watch next

With Strategy now drawing on substantial remaining ATM capacity while preparing a more frequent preferred dividend timetable, market participants will likely focus on whether the company continues to keep BTC holdings static during future funding windows—and how quickly its USD reserve translates into predictable dividend coverage as semi-monthly payments roll forward.

BitMine Immersion (BMNR) added to its Ethereum treasury last week, bringing its total holdings to 5.77 million ether (ETH), or about 4.8% of Ethereum’s circulating supply of 120.7 million tokens, according to a Monday press release.

The company said nearly five million of its ETH holdings are staked, allowing it to earn staking rewards while maintaining one of the largest corporate Ethereum treasuries.

Beyond ether, BitMine’s balance sheet includes 206 bitcoin , a $180 million stake in Beast Industries, a $69 million stake in Eightco Holdings (ORBS) and about $482 million in cash and marketable securities.

Chairman Tom Lee pointed to growing activity on Ethereum’s layer-2 networks as a key reason for the company’s continued focus on ETH.

“One of the biggest crypto success stories in 2026 is the breakaway success of the Robinhood Chain L2 mainnet on July 1, built on Arbitrum,” Lee said in the release. “Already, dollar volumes have exceeded $1 billion, and Robinhood Chain now has more trading volume than any other decentralized exchange (DEX), demonstrating the outstanding utility and product market fit for Ethereum, which is the underlying chain.”

Strategy, the largest corporate holder of Bitcoin, raised fresh capital by selling MSTR shares through its at-the-market (ATM) offering last week while leaving its BTC treasury unchanged.

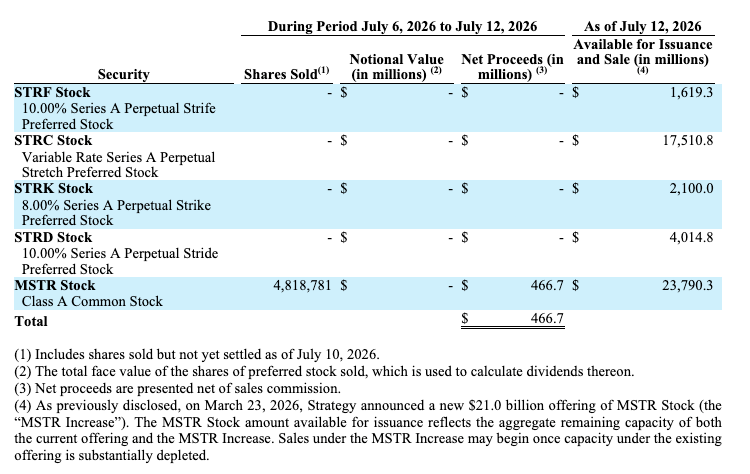

Strategy sold 4.8 million shares of its Class A common stock for $466.7 million between July 6 and July 12, according to a Monday 8-K filing with the US Securities and Exchange Commission.

The company did not buy or sell any Bitcoin during the period and reported holdings of 843,775 BTC at an average purchase price of $75,476 per BTC.

The update comes as investors continue to watch how Strategy balances equity issuance, Bitcoin accumulation and its growing preferred stock offerings as it expands its BTC-focused corporate strategy.

Ahead of Monday’s Nasdaq open, MSTR shares were trading down roughly 3%, to $91.80 apiece, according to Yahoo Finance. Bitcoin was trading at about $62,580, down more than 2% in the past 24 hours.

Cash buffer grows to $3 billion

Strategy increased its US dollar reserve to $3 billion as of July 12, up from $2.55 billion a week earlier. The reserve is used to fund dividend payments on its preferred stock and interest payments on its outstanding debt.

The reserve includes expected proceeds from MSTR shares sold through the company’s ATM offering that had not yet settled as of the reporting date.

Source: SEC

Strategy has $23.8 billion of remaining capacity under its MSTR ATM offering, including capacity from a new $21 billion offering the company announced on March 23. The company said it may begin selling shares under the additional capacity once the existing offering is substantially depleted.

Last week, Strategy announced it sold 3,588 BTC for about $216 million to replenish its US dollar reserve and fund preferred stock dividend payments.

Related: Lyn Alden says Bitcoin needs no savior as Strategy sells $216M of BTC

The transactions included the sale of 1,363 BTC at an average price of $59,256 between June 29 and June 30, followed by another 2,225 BTC at an average price of $60,773 between July 1 and July 5.

In the same June 29 8-K filing, Strategy also reported no BTC purchases, while disclosing the sale of 12.7 million MSTR shares through its ATM offering, generating $1.15 billion in net proceeds.

STRC moves to twice-monthly dividend schedule

Strategy is boosting its USD reserve as it readies its first semi-monthly dividend payment to its STRC preferred stock holders on Wednesday.

Under a new schedule announced on June 8, STRC will use record dates on the 15th and the last day of each month, with payments made on the following record date.

The first semi-monthly record date was June 30, 2026, with the first payment date scheduled for July 15.

Magazine: Bitcoin nearing late stages of bear market: Jamie Coutts, Real Vision

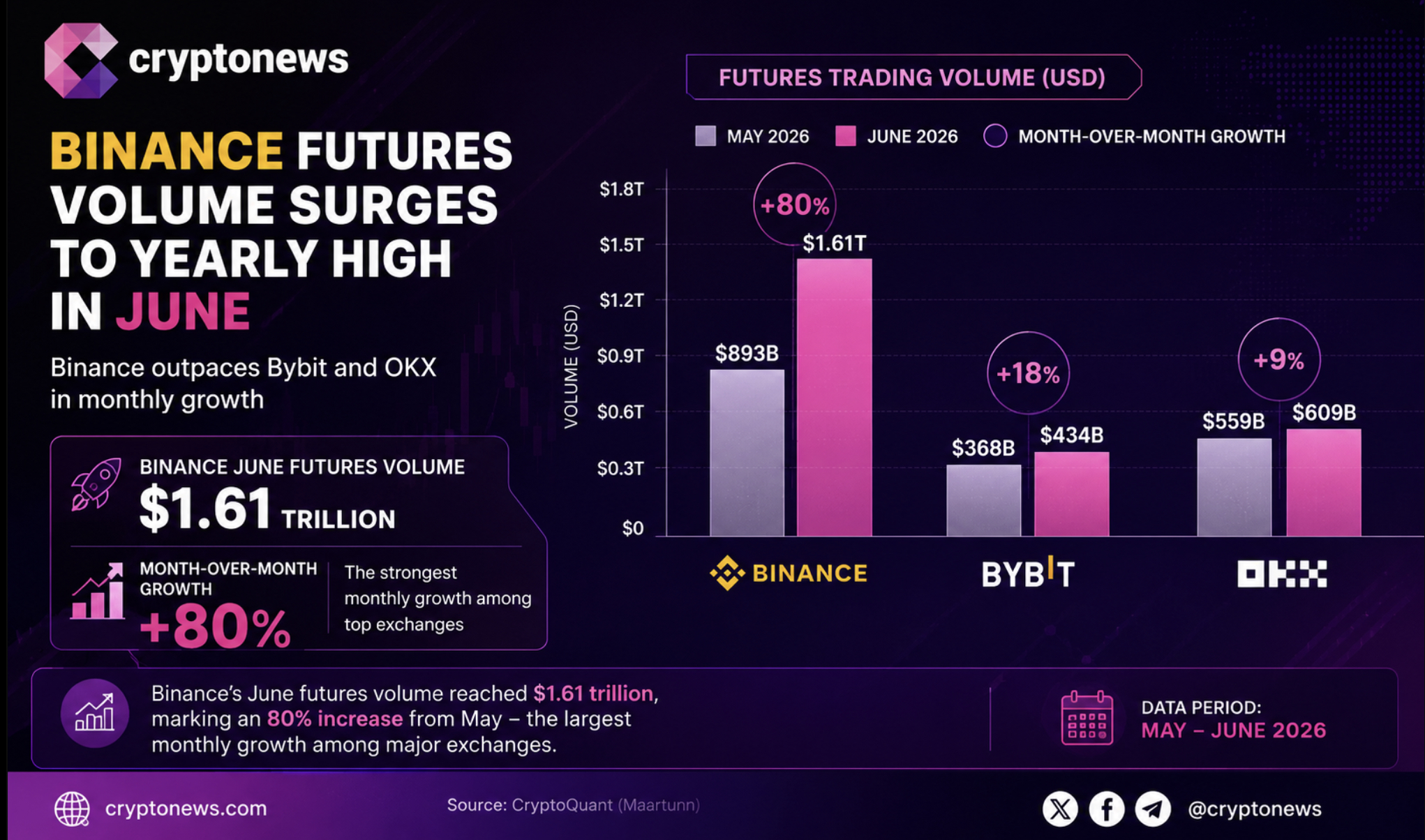

Binance reportedly saw a significant increase in futures trading volume last month, with figures suggesting an 80% jump from May’s volume and marking a high point for the year. This increase occurred while crypto spot markets were running at their weakest pace in two years.

CryptoQuant analyst commentary noted the surge arrives while Bitcoin’s price remains relatively stable, and a significant share of the market views conditions as bearish. The sharp monthly jump in futures volume compared to a stagnant spot market indicates a deliberate shift in trader positioning.

Don’t Miss Out on Our $1,000 USDT Airdrop on ByBit

Binance Futures Pulls Away From OKX and Bybit

The June futures figures positioned Binance ahead of its closest derivatives competitors. OKX and Bybit both reported increases in futures volume from May to June, but neither matched Binance’s growth or scale. Binance’s futures volume notably exceeded those of OKX and Bybit, according to data.

The last time these exchanges approached similar volume levels was in early 2026. June marked a return to, and in Binance’s case a surpassing of, that benchmark. However, the centralized exchange (CEX) futures market remained under pressure across the full second quarter.

Binance’s June futures volume increase came against a deteriorating quarterly backdrop. Total CEX futures volume across the market declined in Q2 2026 compared to Q1, marking a continued downtrend. The pace of decline slowed relative to earlier quarters, but the downward direction persisted

Spot markets faced deeper challenges. CEX spot volume dropped to a two-year low in Q2, with Binance remaining the largest spot venue but experiencing a slight decrease in market share. Binance maintained a steady share of the futures market for the quarter.

The gap between futures and spot markets underscores a structural shift in trading behavior. Derivatives-driven price action has characterized much of the 2026 market, with leverage washouts, basis trades, and hedging activity running hot while directional spot buying stalls. The June Binance data fits and amplifies this pattern.

What remains unclear is whether the futures surge reflects genuine directional conviction or primarily hedging and arbitrage flows-strategies that generate volume without necessarily indicating bullish or bearish bets. This distinction is crucial for interpreting the implications of the volume spike.

Discover: The Best Crypto to Diversify Your Portfolio

MiCA Transition: Early July Data Suggests No Disruption

Binance’s futures volume surge occurred just before Europe’s Markets in Crypto-Assets (MiCA) regulatory framework entered a new enforcement phase on July 1. Binance withdrew its application for a Greek license in late June, raising questions about European market access and potential impacts on derivatives volumes.

Early data from July suggests the regulatory transition has not materially disrupted Binance’s futures activity. Binance recorded substantial futures volume in the first 10 days of July, indicating continued trading momentum. However, the limited data period means future regulatory actions could still affect volumes.

The MiCA transition is significant as Europe is considered an important market for derivatives volumes on major centralized exchanges. Market patterns in July will clarify the extent to which June’s volume reflected front-running of regulatory deadlines versus durable shifts in demand.

In summary, Binance’s June volume increase is a notable data point signaling concentration of trading activity in derivatives on dominant venues amidst weaker spot volumes. Whether this concentration persists into the third quarter and how MiCA affects European-sourced volume will become clearer with forthcoming data.

Discover: The Best Token Presales

The post Binance Futures Surge 80% in June as Spot Markets Hit Two-Year Low appeared first on Cryptonews.

The report also noted a problem with permissionless chains: a confirmed transaction can, in theory, be reversed by a chain reorganization. That introduces a settlement-finality risk that traditional infrastructures do not encounter.

Nevertheless, the report said, established firms in traditional finance and crypto-native companies are converging.

As one example, it cited Ripple’s $1.25 billion purchase of prime broker Hidden Road. Hidden Road, now Ripple Prime, is listed among firms holding both an investment-firm license and cryptoasset registration covering spot and derivatives across forex and digital asset markets from the Financial Conduct Authority.

Santander U.K.’s use of Ripple’s blockchain for cross-border payments was named as a white-labeling example. The bank fronts the customer relationship while Ripple’s technology moves the money.

Woolard puts the U.S. and U.K. markets on similar timelines for stablecoin regulation, with both targeting full regimes in 2027. For wholesale policy, the U.K. is ahead of the U.S., where the Clarity Act remains stuck.

While the FCA is already authorizing crypto companies under money-laundering regulations, the regulator’s new regime under the Financial Services and Markets Act (FSMA) kicks in next year.

Applications under FSMA open on Sept. 30, ahead of an October 2027 launch date.

The report concedes that the industry still sees U.K. authorization as slower than the U.S., where the SEC’s December 2025 no-action letter handed the Depository Trust Company a three-year tokenization pilot that lets firms launch live rather than build for a test environment.

Bitcoin is trading around 62,700 dollars, and Jurrien Timmer, Fidelity’s director of global macro, is watching it drift toward a line he has tracked for more than a decade.

Summary

- Bitcoin is trading near Fidelity’s power law support zone, with the model’s lower boundary around 58,000 dollars.

- Jurrien Timmer views the area as an accumulation zone but is not calling a bottom without a clear catalyst.

- The power law support has aligned closely with major Bitcoin lows in 2015, 2018, and 2022.

- Bitcoin’s deviation from trend and its underperformance against gold now resemble prior cycle-bottom conditions.

- The main missing ingredient is liquidity, which has historically determined when accumulation zones turn into recoveries.

On his power law model, a logarithmic chart that bounds Bitcoin’s entire price history between an upper resistance curve, a middle trendline, and a lower support curve, the floor currently sits near 58,000 dollars. That lower line has caught every major Bitcoin bottom since 2015. Timmer’s label for the zone the market has now entered is unambiguous: accumulation. His caveat is just as unambiguous: he sees no catalyst for a reversal, and he is not calling a bottom.

That combination, a historically reliable floor approaching and a strategist refusing to ring the bell, is the most honest summary of the Bitcoin market in July 2026. The asset is coming off its worst quarter since the 2022 bear market, spot ETFs just recorded their largest quarterly outflow since launch, the speculative premium that carried the price past 120,000 dollars last year has evaporated, and the fast money has visibly rotated elsewhere, first into gold, then into semiconductor stocks. And yet the two quantitative measures Timmer trusts most, the deviation from the power law trendline and the Bitcoin-to-gold ratio, have both sunk to depths recorded at exactly two prior moments: the 2018 low and the 2022 low. Both of those moments were generational buying opportunities. Both also felt like the end of the world at the time.

This feature takes the model seriously in both directions: what the power law actually says, why its track record earns attention, and why the missing-catalyst objection is not a hedge but the core of the analysis.

What the power law model actually is

The power law framework treats Bitcoin’s price growth as a function that decays over time. Early in the asset’s life, prices could multiply a hundredfold in a cycle; as the network matures and the base grows, each cycle’s percentage gains shrink, and the whole price history, plotted on log-log axes, settles into a corridor that rises steadily but ever more slowly. Timmer’s version of the chart draws three curves through that corridor. The upper line marks the euphoria boundary, where prior cycles topped. The middle trendline marks something like fair value under the model. The lower line marks the floor where sellers have historically exhausted themselves.

The track record of that lower line is the reason the chart circulates every time the market bleeds. In the 2014 to 2015 bear market, the model’s support calculation stood near 252 dollars and the actual bottom printed at roughly 230. In 2018, the support line sat near 2,521 dollars against a low of 3,204. In the 2022 winter, the line read about 15,006 dollars and the market bottomed at 16,366. Three cycles, three bottoms, all landing within shouting distance of a curve drawn from math, not sentiment. In the current fit, that curve passes near 58,000 dollars, with some of Timmer’s postings citing figures around 58,237, and Bitcoin at 62,700 is trading roughly 8 percent above it.

Two companion indicators complete the picture, and both are flashing the same reading. The first tracks how far the price trades above or below the middle trendline. That deviation has swung to negative 56 percent, a depth the chart explicitly labels the accumulation zone and one that aligned with the 2018 and 2022 lows. The second is the 52-week z-score of the Bitcoin-to-gold ratio, which has collapsed to around negative 100 percent, meaning Bitcoin has underperformed gold over the trailing year to a degree seen only at prior points of maximal exhaustion. Historically, readings between negative 100 and negative 120 on that gauge, recorded in late 2014, 2018, and 2022, marked the moments when relative weakness against gold had run its course.

One underappreciated property of the setup: the price does not need to fall for the test to happen. The support curve rises over time, so a market that simply goes sideways will meet the floor from above. Stagnation and decline arrive at the same destination, which is partly why Timmer frames the coming months as a period of drift along support, not a decision point with a date.

The case for the accumulation zone

The bull argument starts with base rates. A signal that has fired three times in eleven years and preceded a major recovery all three times deserves weight, especially when two independent gauges, trendline deviation and the gold ratio, corroborate each other. Markets rarely hand out cleaner historical analogies than negative 56 percent deviation, a level with exactly two precedents, both of them cycle lows.

The structural context has also improved in ways the 2018 and 2022 comparisons undersell. In those winters, Bitcoin had no spot ETF complex, no corporate treasury cohort, and no legislative framework in motion. Today the ETFs exist and, after a June that ranked as their worst month on record, just snapped a ten-day outflow streak with a 221.7 million dollar single-day inflow, their largest daily haul in two months. The corporate treasury era is wobbling but not gone: Strategy has begun selling coins for the first time, a shift in the never-sell orthodoxy that crypto.news examined in depth, yet Grayscale mounted a public defense of that very sale as rational balance sheet management, a case crypto.news also covered. And beneath the visible institutional churn, the largest private holders have leaned in: whale wallets absorbed some 16.7 billion dollars in Bitcoin during the spring drawdown even as Wall Street vehicles bled, an accumulation wave crypto.news documented while it was happening. Deep-pocketed buyers behaving exactly as the accumulation zone label predicts is not proof of a bottom, but it is the pattern the model expects to see near one.

There is also the catalyst calendar, which is not empty. The CLARITY Act’s merged draft is due imminently, with Senate floor action targeted before the August recess, and the May committee vote already showed the reflex: Bitcoin jumped to 81,449 dollars within an hour of that 15 to 9 result. Citi and Standard Chartered carry six-figure targets, 143,000 and 150,000 dollars respectively, contingent on passage. A political catalyst is not the liquidity catalyst Timmer wants, but it is a scheduled, binary event with proven price sensitivity, sitting three weeks away, a countdown crypto.news has tracked through every procedural stumble.

Finally, the model’s own asymmetry favors patience over precision. Timmer’s floor is a zone, not a tripwire, and the historical bottoms landed both slightly above and slightly below the calculated line. For an allocator with a multi-year horizon, the question the chart answers is not whether 58,000 holds to the dollar. It is whether prices 8 percent above a three-times-validated floor represent better risk-reward than prices 90 percent above it did a year ago. Framed that way, the zone does most of the work regardless of where the exact low prints.

The other side of the corridor: what the model said at the top

The power law’s credibility does not rest on bottoms alone. The framework has a symmetrical claim about tops, and its record there is what separates it from the usual gallery of bull market curve-fitting.

When Bitcoin approaches the upper boundary of the corridor, the model labels the region a distribution zone, the mirror image of the current setup. Prior cycle peaks at 1,137 dollars, 19,042 dollars, and 64,337 dollars each printed as large positive deviations above the trendline, the same gauge that now reads negative 56 percent. Last year’s run past 120,000 dollars registered as another such excursion, and the model’s framing at the time, a speculative premium stretched far above structural value, was exactly the language skeptics dismissed as premature. In hindsight, the reading was the warning. Capital that bought the upper deviation is the capital now absent, and the round trip from positive extreme to negative extreme in roughly a year is, in the model’s terms, a complete emotional cycle compressed into twelve months.

That symmetry matters for how much trust the current signal deserves. A model that only ever says buy is marketing. A model that flagged distribution near the highs and now flags accumulation near a historically validated floor has at least earned the right to be argued with seriously. Fidelity’s own 2026 Periodic Table of Investment Returns makes the discomfort concrete: alternative assets including Bitcoin, gold, and long-duration Treasuries sit at the bottom of the annual performance ranking, beneath emerging markets, small caps, and Japanese equities. The model is asking investors to accumulate the asset class the scoreboard says has been the year’s worst idea. That is what the entries at 230, 3,204, and 16,366 dollars felt like too, which is either the entire point or the oldest trap in markets, depending on which side of the argument one occupies.

There is one further nuance in how Timmer talks about the line that deserves precision. He has described the mid-60,000s and the level around 60,000 as a line in the sand for the model, language that refers to where recalibration pressure begins, not where the thesis dies. The structural version of the power law, by his framing, would only be falsified by Bitcoin trading below roughly 17,000 dollars for more than a year, an outcome no serious participant currently prices. Between the tactical line at 58,000 and the structural line at 17,000 stretches an enormous gray zone in which the model can be wrong about timing, wrong about the exact floor, and still right about the destination. Critics call that unfalsifiability. Adherents call it the difference between a trading signal and a valuation framework. Both descriptions are accurate, which is why position sizing, not conviction, is where the argument actually gets settled.

The case for the missing catalyst

The bear argument does not dispute the chart. It disputes the physics behind it, and Timmer himself supplies most of the ammunition.

His stated reason for withholding a bottom call is that the drivers of every prior recovery are absent. Global money supply growth is decelerating, not accelerating. The speculative premium, the gap between price and the model’s structural floor that expands when fast money floods in, has been almost entirely erased, and the capital that produced it has left the building in a traceable sequence: out of Bitcoin, into gold, and now out of gold into semiconductor and AI equities. In Timmer’s framing, Bitcoin does not bounce because it reaches a line. It bounces when liquidity returns, and until it does, the base case is months of sideways drift along the floor instead of a V-shaped snapback. The accumulation zones of 2015 and 2018 were not quick either; both involved long stretches of dead money before the turn.

The demand infrastructure that was supposed to make this cycle different is, at the moment, cutting the other way. The ETF complex that absorbed supply on the way up distributed it on the way down, posting its worst month ever in June and its largest quarterly outflow since launch, a reminder that regulated wrappers transmit institutional risk appetite in both directions. The treasury company cohort has moved from pure accumulation to selective distribution, with Strategy selling coins and smaller vehicles like Empery Digital liquidating roughly half a Bitcoin stack to fund a pivot toward AI data centers. Each of these flows is individually explainable; together they describe a marginal buyer that has, for now, become a marginal seller.

The macro overlay is genuinely hostile. The United States has struck Iran three times in a single week, the Strait of Hormuz has reportedly closed again, oil holds above 100 dollars, and the Federal Reserve faces inflation pressure that keeps rate cuts off the table. Risk assets broadly are contending with the same liquidity drought, which is precisely why capital rotated to semiconductors, the one sector with an earnings story strong enough to ignore it. Bitcoin’s correlation regime matters here: in liquidity droughts it trades like a high-beta risk asset, not like gold, and the negative 100 percent reading on the gold ratio is the scar tissue of that regime. The same reading bulls cite as exhaustion, bears read as reclassification: the market spent a year deciding that in this environment, gold is the hedge and Bitcoin is the trade.

And the model itself deserves a dose of humility. Power law fits are parameterization-sensitive: Fidelity’s curve puts support near 58,000, while other published fits place the floor closer to 51,000, and at least one derivation cited in coverage runs as low as 56,488. A zone that moves by 10 percent depending on who draws it is a framework, not a law of nature. The model’s own authors concede the structural version only breaks if Bitcoin spends more than a year below roughly 17,000 dollars, which means the framework can absorb a decline of 70 percent from here without being falsified. A thesis that cannot be quickly proven wrong is comfortable to hold and dangerous to size.

Anatomy of the exodus: where the fast money actually went

The rotation Timmer describes is traceable in the flow data, and following it explains both why the drawdown was so orderly and why the recovery lacks an obvious buyer.

The first leg ran from Bitcoin to gold. As the speculative premium deflated through the winter, gold absorbed the store-of-value bid, and the Bitcoin-to-gold ratio began the slide that would eventually reach its negative 100 percent extreme. The second leg ran from gold into semiconductors, as the AI capital expenditure cycle gave momentum capital an earnings-backed home that neither metal nor token could match. Institutional surveys confirm the sequence: digital assets posted three consecutive quarterly losses, the longest streak since 2022, precisely as capital rotated into AI equities, and even crypto-native corporate stories, like the treasury company that sold half its Bitcoin stack to fund data centers, bent toward the same gravity.

What remained in the crypto market redistributed internally instead of leaving entirely. Bitcoin dominance held up because altcoins fell harder, with everything outside the top two losing roughly 23 percent in six months. Stablecoin capitalization, the market’s cash position, shrank by 10 billion dollars over two months, the largest contraction since the Terra collapse, though analysts read it as cyclical de-risking, not structural exit. And the transactional economy kept consolidating into the venues with real usage, from tokenization networks to the stablecoin rails where volume actually lives, a migration visible in the flippening of trading volume toward regulated dollar tokens that crypto.news charted this month.

The composite picture is a market that de-levered without panicking: no cascade, no exchange failure, no credit event, just a year-long transfer of coins from momentum hands to patient ones at steadily lower prices. That is, almost to the letter, the textbook description of an accumulation phase. It is also, and this is the uncomfortable part, indistinguishable in real time from the early innings of a longer decline. The difference between the two is supplied later, by liquidity, which returns the analysis to Timmer’s missing ingredient.

How the two cases actually reconcile

Strip the rhetoric and the disagreement is narrower than it looks. Both sides accept the same facts: the price is near a historically validated floor, the on-chain and whale evidence shows accumulation, the liquidity backdrop shows no fuel for a rally, and the one scheduled catalyst is political rather than monetary. The dispute is about sequencing and about what an investor should do during the gap.

History offers a specific answer about the gap. In each prior visit to the accumulation zone, the market spent between several months and more than a year grinding along the floor before the recovery began, and the recovery started when an external liquidity impulse arrived: the 2015 turn preceded the 2016 halving cycle and easing conditions, the 2019 recovery tracked the Fed’s pivot, and the 2023 exit from the zone rode the turn in global money supply and the ETF approval trade. The floor identified where the low formed. Liquidity decided when. There is no example of the zone producing a durable rally without the second ingredient, which is why Timmer’s refusal to call a bottom is not hedging. It is the model applied correctly.

That reconciliation also clarifies what the CLARITY Act can and cannot do. Legislative passage would be a demand catalyst, activating allocator categories that cannot currently hold the asset, and the market’s hair-trigger response to the committee vote suggests real convexity around the outcome. But a statute does not print money. If the bill passes into a liquidity drought, the plausible result is a strong repricing that then stalls at the trendline instead of reaching a new cycle high, the difference between closing the discount and starting a bull market. If it fails, the floor gets its stress test with no cushion, and the parameterization debate, 58,000 versus 51,000, stops being academic. Elsewhere in the market, the same liquidity question is being answered asset by asset: capital that stayed in crypto has crowded into the few networks with visible usage growth, a concentration visible across the tokenization trade, leaving Bitcoin to trade almost purely on macro.

What to watch while the market drifts

Before the gauges, a word on method, because the practical difference between the two camps is not belief but execution. The accumulation zone framework, taken seriously, argues for scaling over timing: building exposure in defined tranches as price approaches the floor, sized so that a breach of 58,000 is survivable and a visit toward the alternative fits near 51,000 is a continuation of the plan, not its failure. It argues for instruments matched to a months-long horizon, since the model’s own history says the zone can persist for two to four quarters before resolving, and leveraged expressions of a patient thesis are how correct analysis produces liquidated accounts. And it argues for treating a confirmed weekly close below the floor as a thesis review trigger, a scheduled reassessment, not a panic exit, because the difference between the tactical line and the structural one is 40,000 dollars wide. The missing-catalyst framework, taken equally seriously, adds only one amendment: let the macro data, not the price, decide when the accumulation window is closing. Buying the zone is a bet that liquidity returns eventually. Watching the liquidity gauges is how eventually gets a date. Neither camp needs to convert the other for both to be useful; one supplies the map of where value lives, the other supplies the clock that says when the market will agree.

Four gauges will signal the regime change before the price does. Global money supply growth is the master variable; Timmer’s entire framework waits on its second derivative turning positive, and any coordinated easing impulse, from the Fed or elsewhere, is the starting gun the model requires. ETF weekly flows are the institutional thermometer; one 221 million dollar day means nothing, but a month of sustained net inflows through a flat tape would mark the return of the allocator bid. The Bitcoin-to-gold ratio recovering from its negative 100 percent extreme would show relative capitulation has ended even before absolute prices move. And a confirmed weekly close below the 58,000 zone would be the model’s recalibration trigger, the signal to treat the floor as broken instead of tested, with the next published fits clustering around 51,000.

The honest conclusion is that the chart and the strategist are both right, and they are answering different questions. The power law says where: Bitcoin is entering the zone where every prior cycle’s sellers ran out, with corroborating exhaustion readings that have exactly two precedents, both of them bottoms. The catalyst analysis says when: not until liquidity returns, and possibly not for months. Accumulation zones are named for what disciplined capital does inside them, quietly and without confirmation. The word was never a promise that the bell rings at the low. It is a description of who is buying while everyone else waits for one.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

BlackRock and HSBC have joined a UK tokenization push projected to boost annual economic output by up to $44 billion, as 54 firms line up behind the plan.

The taskforce is led by Christopher Woolard, the British government’s wholesale digital markets champion and a former interim head of the Financial Conduct Authority. His first report to the Treasury, delivered in July 2026, maps a route from pilots to live markets.

A $44 Billion Bet on Tokenized Markets

Tokenization converts ownership of assets such as bonds, funds, and property into digital tokens that are recorded on a blockchain. Supporters argue it cuts costs, speeds settlement, and frees capital trapped in aging back-office systems.

The economic case comes from Barclays and PwC. Their study estimates that tokenization could add up to $44 billion (£33 billion) to UK output by 2035. Roughly two-thirds of that gain would fall outside financial services, in the wider economy.

That top figure is a ceiling, not a base case. It assumes the UK becomes a leading hub while the US and Europe adopt in parallel. A more cautious scenario points to about $29 billion (£22 billion) a year, plus $19 billion (£14 billion) in fresh annual tax revenue.

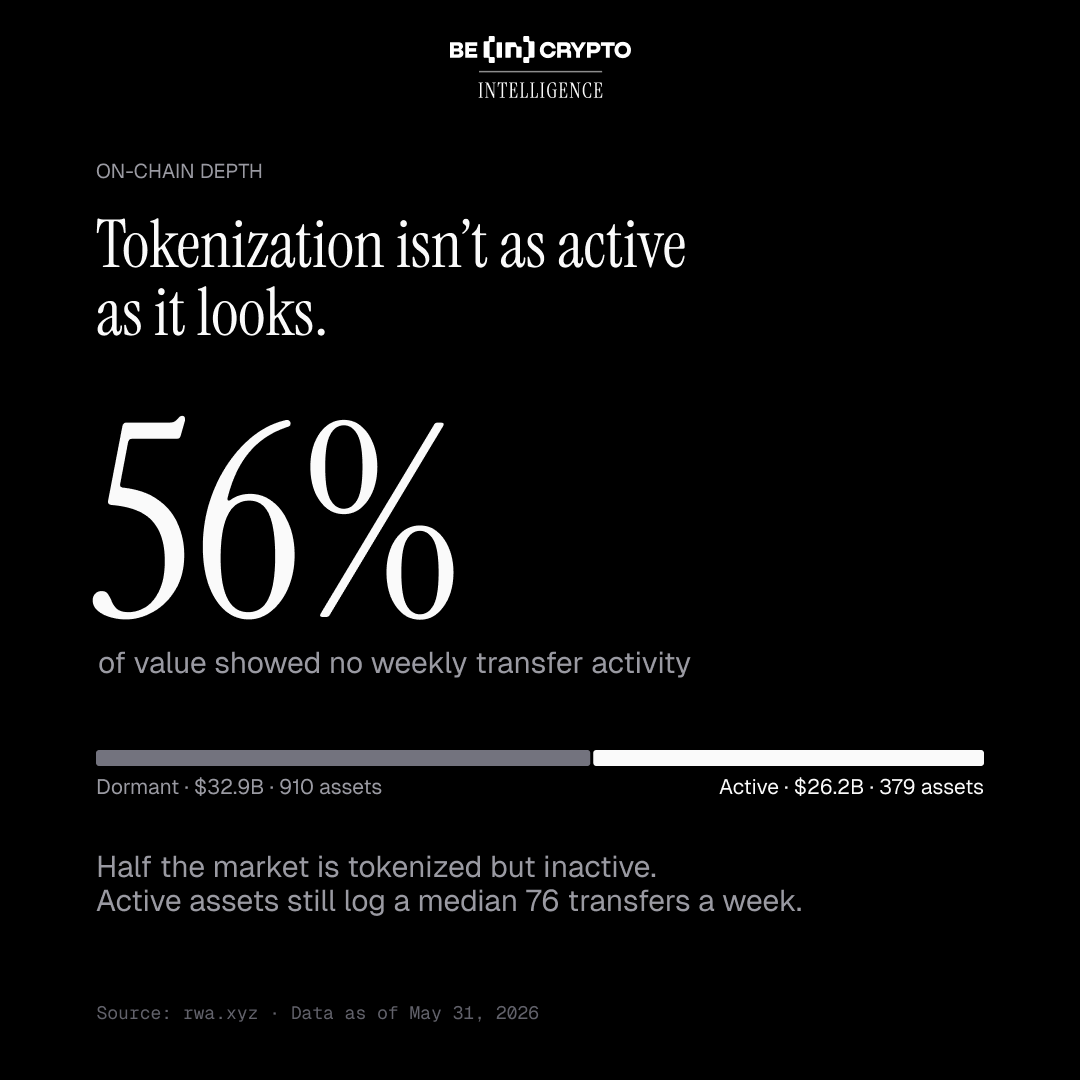

The prize reflects how early the market still is. Tokenized real-world assets (RWA) stood near $30 billion in 2025, a sliver of global markets. Yet that value jumped about 300% over the year. The latest on-chain tokenization data track the same climb.

Forecasters expect the base to expand fast. Consultancy BCG projects that tokenized assets could reach around $55 trillion by 2035. That gap is why the tokenized stocks and bonds wave now sits at the center of institutional strategy.

Note: Latest research from BeInCrypto found that more than 56% of the Tokenization market has zero activity on-chain.

Global Banks Back the UK Tokenization Push

BlackRock shows how far traditional finance has moved. The world’s largest asset manager runs BUIDL, the largest tokenized US Treasury fund, with about $2.4 billion in assets. It also registered as a UK cryptoasset firm in 2025, while HSBC has issued digital bonds through its Orion platform.

The taskforce reads like a roll call of global finance. Its 54 members include JPMorgan, Goldman Sachs, Morgan Stanley, Citi, Deutsche Bank, and UBS.

Asset managers Fidelity International, Schroders, and State Street also signed on. Market infrastructure firms DTCC, Euroclear, and the London Stock Exchange Group joined too. So did crypto-native players such as Circle, Ripple, and Coinbase.

The UK has already produced working proof points. Lloyds, Aberdeen, and Archax completed a UK-first tokenized foreign exchange trade collateralized in 2025. Baillie Gifford and BNY launched Britain’s first fully tokenized investment fund in June 2026.

That momentum has pulled established institutional tokenization platforms into regulated markets rather than sandboxes alone.

The taskforce plans to prove the technology one use case at a time. Its first target is the repo market, where firms borrow cash against securities for short periods. Woolard’s group wants a live tokenized repo trial by spring 2027, then work on fixed income and derivatives.

There is precedent to build on. In early 2026, Digital Asset ran a cross-border intraday repo trade using tokenized gilts on its Canton network.

UK Eyes First G7 Tokenized Government Bond

The boldest goal targets sovereign debt. The report urges an early pilot of a digital gilt instrument, known as DIGIT, no later than the first quarter of 2027. Success would make the UK the first Group of Seven nation to issue tokenized government debt.

Smaller jurisdictions moved first. Hong Kong sold the world’s first tokenized government green bond in 2023. It then priced a record multi-currency digital bond in 2025. Slovenia became the first European Union sovereign to issue debt on a distributed ledger in 2024. The European Investment Bank has run blockchain bonds since 2021.

That history sharpens the stakes. The UK is not inventing tokenized debt, but no major economy has issued it, and London wants to claim that ground first.

Regulators are moving in step. The Financial Conduct Authority will open applications for its cryptoasset regime on September 30, 2026. Full rollout follows in October 2027, alongside broader UK stablecoin plans due the same year.

Woolard cast the effort as a contest for the country’s place in global finance.

“Put simply, tokenised markets are fundamental to the future of financial services. What the UK does here determines our right to be at the heart of the next generation of financial markets,” read an excerpt in the report, citing Woolard.

The hard part is what follows the pilots. Analysts still flag thin trading and shallow tokenized market liquidity as the sector’s weak spot. The taskforce must close that gap as it scales.

The UK now has firm dates, heavyweight backers, and a clear target. The next year will show whether these trials can reach live markets before rival financial centers close the gap.

The post BlackRock Joins UK Tokenization Push to Deliver $44 Billion to the Economy appeared first on BeInCrypto.

Arguably the most popular UFC fighter of our time – Conor McGregor – returned to the octagon after a five-year absence during which he recovered from a severe leg fracture and dealt with personal and legal issues.

However, his long-awaited return was anything but successful, resulting in a notable financial loss for Canadian rapper Drake.

The Curse Strikes Again

This weekend, the Irish fighter faced Max Holloway at UFC 329 in Las Vegas. This was his first fight since 2021, but the highly anticipated comeback was surprisingly brief.

McGregor landed awkwardly on his right knee in the very first seconds, giving his opponent the upper hand. Just 1:09 into the fight, the referee called it off, handing Holloway the victory after he unloaded a barrage of punches on the Irishman.

Given his long absence from the octagon, McGregor was the underdog in this game and the odds for his win were quite high. The renowned Canadian musician Aubrey Drake Graham, better known as Drake, tested his luck at gambling again, wagering $1 million in Bitcoin (BTC) on “The Notorious” to emerge victorious.

A McGregor win would have earned him a massive $1.85 million profit, but instead the million-dollar bet vanished into thin air. Some might say Drake’s latest setback was expected, considering his consistently poor track record with high-stakes bets.

Over the years, the rapper has wagered substantial sums on athletes and sports teams, many of which ended up losing. This led to the creation of the so-called “Drake Curse,” and the examples are countless.

In 2024, for instance, the musician forfeited $700,000 in BTC on a UFC fight, while earlier this year he lost $1 million worth of the cryptocurrency after the New England Patriots were defeated by the Seattle Seahawks in the Super Bowl.

Better Luck With the World Cup

It is important to note that every now and then, Drake places a winning wager. Such was the case a couple of weeks back when he bet that Canada would eliminate South Africa in the FIFA World Cup 2026.

His homeland scored the winning goal at the very end of the game, and the rapper (who bet $770,000 in USDT) made approximately $230,000 in profit in the stablecoin.

The post ‘Drake Curse’ Is Back: Here’s How Much Bitcoin (BTC) He Lost Betting on Conor McGregor appeared first on CryptoPotato.

Crypto World

Newly launched 2026 cloud mining app with smart AI, unaffected by market swings, earning up to $67,000 daily

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

AI-powered cloud mining platforms are simplifying crypto participation by automating resource management, optimization, and daily operations for users.

Over the past few years, cloud mining has undergone several technological iterations, but the barrier to entry remains a significant hurdle for many ordinary users. From mining machine management and computing power configuration to profit monitoring, traditional cloud mining often requires a substantial amount of time to learn the relevant knowledge and even constant monitoring of market conditions and platform operations. For new users just starting out with digital assets, the complex operating procedures and technical jargon also deter many.

Entering 2026, the rapid development of artificial intelligence technology is propelling cloud mining into a new intelligent phase. The next generation of cloud mining applications deeply integrates AI intelligent systems with automated management, transforming the previously complex operating procedures into a simpler and more efficient user experience. Users do not need to configure equipment, learn complex technical knowledge, or perform frequent manual operations; they only need to complete simple registration and account setup to quickly start experiencing intelligent cloud mining services.

Compared to traditional cloud mining, the next-generation xrppower AI cloud mining is more intelligent, efficient, and easy to use. The intelligent system can automatically complete resource scheduling, operational optimization, and daily management without complex operations or frequent human intervention, allowing even inexperienced new users to quickly get started. With the continuous development of AI technology, cloud mining is evolving towards greater convenience, intelligence, and automation, bringing users a more relaxed experience.

How to Use XRPPower AI smart cloud mining

Step 1: Register an Account

Register using an email address. Creating an XRPPower account takes just a few minutes.

Step 2: Choose a Cloud Mining Contract

Choose a suitable cloud mining contract plan based on a specific financial plan and needs.

Step 3: Pay the Contract Fee

Pay the contract fee using a supported cryptocurrency. The system will automatically activate the selected contract upon confirmation.

Step 4: Earn Profits

After the contract takes effect, profits will be automatically credited to the account balance according to platform rules. Users can choose to withdraw funds or purchase new cloud mining contracts using the platform’s features.

Details of Some Popular XRPPower Cloud Mining Profit Contracts

Investment Amount: $5,000, Contract Period: 15 days, Daily Profit: $70.50, Total Profit: $1,057.50, Principal $5,000 Refunded Upon Maturity.

Investment Amount: $10,000 USD, Contract Period: 20 days, Daily Yield: $153 USD, Total Yield: $3,060 USD, Principal $10,000 USD Refund Upon Maturity.

Click to view more cloud mining yield contracts

XRPPower AI intelligent cloud mining security and compliance

AI-Driven, Continuously Optimized Platform Services

XRPPower continuously upgrades its AI intelligent system, integrating automation technology into platform operations. Through intelligent resource scheduling, system optimization, and automated management, it continuously improves platform efficiency and user experience. The platform provides digital services 365 days a year and continuously optimizes system performance and service processes to create a more efficient and convenient user experience for global users.

Global operations, robust platform governance

Headquartered in London, UK, XRPPower continuously monitors the development of the global digital finance industry, constantly improving its platform operation system, risk management mechanism, and internal governance processes. The platform is committed to continuously promoting compliance in accordance with applicable laws, regulations, and operational requirements, providing global users with more standardized, transparent, and stable digital financial services.

Multiple security measures to protect user assets and data

Regarding platform security, XRPPower employs technologies such as SSL/TLS data encryption, two-factor authentication (2FA), separate storage for hot and cold wallets, multi-layered security protection, and intelligent risk monitoring to provide multiple layers of security for user accounts, transaction data, and digital assets. Simultaneously, the platform continuously optimizes its internal controls, risk management, and security operations system, and draws on risk management concepts widely adopted by international professional institutions to continuously improve platform governance capabilities, operational transparency, and long-term service levels, creating a more reliable digital financial service environment for users.

Summary

In 2026, XRPPower completed a major upgrade, further integrating AI intelligent technology into its cloud mining services, providing a more intelligent and convenient digital experience to over 3 million users worldwide. Through automated management and continuously optimized platform services, users can more easily participate in cloud mining, using related functions without complex operations. The platform operates continuously 365 days a year, providing users with a stable service experience. Register for XRPPower now for free to learn more about the platform’s functions and operating model, explore digital asset management methods according to your needs, and rationally participate in related services.

For more information, visit the official website.

Disclosure: This content is provided by a third party. Neither crypto.news nor the author of this article endorses any product mentioned on this page. Users should conduct their own research before taking any action related to the company.

Kathryn Newton and Lana Condor Are Caught in the Maw of Prime Video’s Chilling Survival Thriller in New Look [Exclusive]

BIGGEST XRP NUKE OF THE CENTURY!?! (XRP $1000?)

What we know so far as three people found dead at Ballymena home

-

Fashion7 days ago

Fashion7 days agoOpen Thread: What Great Books Have You Read Recently?

-

News Videos6 days ago

News Videos6 days agoWhats Hidden Inside This Cash Register? #treasure #reselling #money

-

Fashion4 days ago

Fashion4 days agoLoro Piana Fall 2026 Enters Houston’s Art Scene

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: Nutriplenish Leave-In Conditioner

-

Crypto World7 days ago

Crypto World7 days ago$1,000 Credit Alert! BlockDAG X Exchange Pre-Registration Now Officially Open, Polkadot Dips & Zcash Rebounds

-

Tech6 days ago

Tech6 days agoAnthropic’s new “J-lens” reveals a silent workspace inside Claude that mirrors a leading theory of consciousness

-

News Videos7 days ago

News Videos7 days agoBest Time to Enter Small Caps Right Now? Another Bull Run? | Financially Free

-

Business7 days ago

Business7 days agoAXT Shares Jump Nearly 14% as Semiconductor Materials Maker Rebounds on AI-Linked Indium Phosphide Demand

-

Sports6 days ago

Sports6 days agoJoshua Pacio ‘more complete’ ahead of ONE rematch vs Malachiev

-

Sports4 days ago

Sports4 days ago2026 Genesis Scottish Open Thursday TV coverage: Round 1

-

Tech5 days ago

Tech5 days agoAnthropic brings Claude Cowork to mobile and web as usage data shows most users aren’t coding

-

Crypto World7 days ago

Crypto World7 days agoSK hynix (000660.KS) Stock Dips as $28B Nasdaq ADR Offering Drives AI Memory Expansion

-

Sports3 days ago

Sports3 days agoSuper Eagles star Moses Simon opens up on Liverpool transfer regret

-

Sports6 days ago

We have punished the disrespect

-

Crypto World6 days ago

Crypto World6 days agoBinance lists Strategy’s STRC stock as company expands Bitcoin funding

-

Tech4 days ago

Tech4 days agoCharacter.AI enters the microdrama arena with its own productions, but there’s a twist

-

Tech7 days ago

Tech7 days ago9 Best Keyboards (2025), Tested and Reviewed

-

Business6 days ago

Business6 days agoEnbridge: AI Tailwind Priced In (Rating Downgrade)

-

Crypto World6 days ago

Crypto World6 days agoClaude AI Created Something Anthropic Never Designed

-

Crypto World6 days ago

Crypto World6 days agoNasdaq arthritis company holding Moshe Hogeg crypto hits all-time low

You must be logged in to post a comment Login