Crypto World

Senate Races Against August Deadline to Vote on Crypto CLARITY Act

Key Takeaways

- Senator Lummis characterizes the CLARITY Act as establishing the groundwork for modern financial infrastructure

- Despite House approval and Banking Committee clearance, the legislation awaits a complete Senate floor vote

- The critical date is August 7 — failure to vote before congressional recess could postpone the bill until 2027

- Democratic lawmakers insist on ethics provisions preventing presidential and congressional officials from cryptocurrency profiteering

- President Trump’s 2025 financial filings revealed approximately $1.4 billion in cryptocurrency-related earnings, intensifying ethics concerns

Senator Cynthia Lummis is calling on her colleagues to expedite action on the CLARITY Act, legislation designed to establish comprehensive regulatory guidelines for digital assets across America. She described it as a defining moment for financial policy and emphasized the urgency of completing the legislative process.

The legislation has successfully navigated the House of Representatives and obtained Senate Banking Committee approval. The remaining obstacle is securing a vote on the Senate floor. As of now, no voting session has been officially scheduled.

Time is rapidly running out. The Senate’s final session day before entering summer recess falls on August 7. Should voting fail to occur by that deadline, the earliest opportunity for reconsideration would be 2027.

Core Provisions of the Legislation

The CLARITY Act proposes dividing cryptocurrency regulatory authority between two federal agencies. The Securities and Exchange Commission would maintain jurisdiction over investment contract assets. Meanwhile, the Commodity Futures Trading Commission would gain expanded authority over spot markets for digital commodities.

Additionally, the legislation mandates that cryptocurrency platforms and brokerages maintain segregated accounts for client assets, keeping them separate from operational funds. This requirement directly addresses concerns stemming from previous exchange failures.

The bill allocates $150 million toward investigating cryptocurrency fraud and extends Bank Secrecy Act compliance requirements to certain digital asset businesses. Advocates argue this approach replaces ad-hoc enforcement with systematic regulation. Opponents counter that the legislation lacks sufficient consumer safeguards and fails to adequately address decentralized finance concerns.

Political Conflict Centers on Ethics Provisions

The primary obstacle currently isn’t regulatory complexity — it’s political disagreement. Democratic senators demand inclusion of ethics stipulations that would prohibit the president, vice president, high-ranking government officials, and congressional members from financially benefiting from cryptocurrency ventures.

This demand intensified following President Trump‘s submission of his 2025 financial disclosure documents. These filings revealed approximately $1.4 billion in cryptocurrency earnings during the previous year. Revenue sources included licensing fees from his memecoin venture, token transactions through World Liberty Financial, and asset sales to entities in Abu Dhabi.

Senator Elizabeth Warren advocated forcefully for robust ethics language, asserting the legislation “must prevent the president” and other officials from cryptocurrency profiteering. Senator Ruben Gallego, despite supporting the bill’s committee advancement, pledged to pursue measures to “crack down on corrupt crypto dealings” while withholding commitment on his eventual floor vote.

Negotiators must reach consensus on ethics language, and any agreement requires presidential approval.

The Path Forward

Behind closed doors, Senate staff members from both the Agriculture and Banking committees continue working to harmonize competing versions of the legislation. Individuals familiar with these discussions express measured optimism while recognizing the compressed timeline.

Following text finalization, Senate floor proceedings could advance rapidly — potentially achieving the necessary 60-vote supermajority within days.

The bill’s success may ultimately hinge on House dynamics. Publications including Politico and Punchbowl News have characterized the House as experiencing operational challenges, potentially complicating final passage even with Senate approval.

All eyes remain on August 7.

The biggest fight in American finance right now is over a single clause: whether digital dollars can pay their holders interest. Banks say yield-bearing stablecoins would drain trillions in deposits and break the lending machine. Crypto says the banks are defending a monopoly on other people’s money. The CLARITY Act is hostage to the answer, and this week the standoff escalated on every front.

Summary

- A battle over whether stablecoins should pay interest has become the biggest obstacle to advancing the CLARITY Act in the US Senate.

- Banks warn that yield bearing stablecoins could pull trillions of dollars from deposits while the crypto industry argues savers should receive the returns generated by reserve assets.

- As lawmakers remain divided, banks are also preparing for a future with stablecoins by investing in digital dollar infrastructure and settlement networks.

The week of June 29, 2026, was supposed to move the CLARITY Act toward the Senate floor. Instead, Coinbase publicly pulled its support for the bill it had spent two years championing, Senate Banking Committee chairman Tim Scott postponed the markup, and President Trump posted that the banks lobbying against stablecoin yield were threatening and undermining his own signature crypto law. The proximate cause of all three events was the same unresolved question: can a stablecoin pay interest?

The question sounds technical. It is not. It is a fight over roughly $6 trillion, which is the amount of deposit money that Bank of America chief executive Brian Moynihan has warned could migrate out of the banking system if digital dollars are allowed to pass their reserve earnings to holders. Behind the number sits the basic architecture of American credit: banks fund loans with deposits that pay savers little, and anything that gives savers a better default option attacks the cheapest funding source in finance.

Both sides understand the stakes with total clarity, which is why neither will yield. The banks have the oldest lobby in Washington and a century of regulatory capture to draw on. Crypto has the GENIUS Act already signed, a president publicly on its side, and products that customers demonstrably want. Between them sits a Congress trying to pass a market structure bill that both industries claim to support and each is willing to kill over this clause.

This is the anatomy of the standoff: where the yield actually comes from, what each side’s studies really say, how the fight broke into the open at Davos, why the CLARITY Act is stalled, and what the banks are quietly building in case they lose.

Where stablecoin yield comes from

A dollar stablecoin is a bearer claim on a reserve. The issuer takes a customer dollar, parks it in Treasury bills and repo and cash equivalents, and gives back a token redeemable at par. At 2026 short-term rates, that reserve portfolio throws off meaningful income: roughly four cents per year on every dollar, paid by the United States government to the issuer.

Under the GENIUS Act, the stablecoin framework signed in 2025, issuers keep that income. The law prohibits payment stablecoins from paying interest or yield to holders, a clause the banking lobby fought for and won. The result is one of the stranger economic arrangements in modern finance: tens of millions of stablecoin holders collectively finance a float measured in hundreds of billions of dollars, and the entire risk-free return on that float accrues to issuers and their distribution partners.

Tether’s profits, Circle’s revenue-sharing arrangement with Coinbase, and the business case for every new entrant described in the consortium stablecoin model behind Open USD all rest on that captured spread.

Crypto’s position is that the arrangement is indefensible on its own terms. If the token holder supplies the dollar, the token holder should be able to receive the yield, the same way a money market fund passes through its portfolio income. Exchanges already approximate this with rewards programs that pay users for holding certain stablecoins, a workaround the banks call interest by another name and want closed.

The banks’ position is that the arrangement is the only thing standing between the deposit system and a slow-motion run. A stablecoin that pays four percent, holds only Treasuries, settles instantly, and lives in a phone app is not a payment instrument, in their telling. It is a narrow bank, the exact institution American regulators have refused to charter for a century, because a narrow bank collects deposits and funds nothing.

Both descriptions are accurate. That is what makes the fight so hard to resolve. A product can be, simultaneously, a long-overdue transfer of interest income to the people who supply the money and a structural threat to the funding model of every lender in the country. The legislative machinery now stuck in the Senate exists precisely because Congress must pick which description governs, and there is no compromise text that makes both true halves false.

The dueling studies: $6.6 trillion or $2.1 billion

In early 2026 the American Bankers Association put a number on the threat. Its analysis warned that permitting interest-bearing stablecoins could trigger as much as $6.6 trillion in deposit flight from the banking system, a figure that would represent a structural repricing of bank funding. Moynihan carried the message personally, telling audiences that 30 to 35 percent of transactional deposits could leave banks if yield-bearing digital dollars became legal, and putting the Bank of America estimate in the $6 trillion range.

The mechanism behind the number is credit contraction. Deposits fund loans. A dollar that leaves a checking account for a stablecoin backed by T-bills stops funding a mortgage or a small business line and starts funding the federal government. Multiply by trillions and the banks’ model produces higher loan rates, reduced credit availability, and concentrated stress on community banks whose entire funding base is retail deposits. The ABA’s framing is not that banks would earn less, though they would; it is that the economy would lend less.

The White House Council of Economic Advisers looked at the same question and produced a number three orders of magnitude smaller. Its assessment put plausible deposit displacement in the low billions, around $2.1 billion in the scenario most cited, arguing that stablecoin demand comes overwhelmingly from crypto trading, cross-border flows, and dollar demand abroad, none of which is money sitting in a Kansas checking account today. In the CEA’s telling, the banks are counting every deposit that could theoretically move as a deposit that would move, ignoring deposit insurance, banking relationships, and the fact that money market funds have offered better rates than checking accounts for fifty years without ending bank lending.

The three-orders-of-magnitude gap is not really an empirical dispute. The two studies answer different questions. The ABA models the ceiling of a mature, frictionless, fully legal yield-bearing stablecoin market; the CEA models the floor of the current one. The honest answer, that displacement would start small and compound as the products improved, satisfies neither side, because the banks need the threat to be immediate and crypto needs it to be imaginary.

Davos, and the fight goes personal

The clearest public glimpse of how raw the conflict has become came at Davos in January, in an exchange between the two most powerful executives on either side.

JPMorgan chief executive Jamie Dimon, discussing stablecoin yield with Coinbase chief executive Brian Armstrong on a panel, dismissed Armstrong’s framing of deposit competition with a phrase that escaped the room within minutes: he told him he was full of s—, a vulgarity from the most measured banker of his generation that did more to reveal the temperature of the fight than any comment letter.

Armstrong’s argument, the one that drew the response, is the consumer-surplus case. American savers hold trillions in accounts paying a fraction of a percent while banks earn multiples of that on the float. Stablecoin yield, in his telling, is simply technology forcing banks to pay depositors something closer to the market rate for their money, and the deposit-flight studies are incumbents pricing their own margin as a systemic necessity. Coinbase has the most direct commercial stake of anyone in the room: its revenue share on USDC reserves is one of its largest income lines, and a world of legal yield pass-through is a world where its stablecoin business attacks bank deposits head-on.

Dimon’s counter is that payments and banking are different businesses with different risk, and that crypto wants banking economics without banking obligations: no lending mandate, no Community Reinvestment Act, no branch network, no discount window responsibilities, just the float. JPMorgan has hedged its own position, running deposit tokens and blockchain settlement internally while its chief executive argues against the retail version, a posture crypto reads as monopoly defense and banks read as prudence.

Then the President entered. In a late June post, Trump accused the banks of threatening and undermining the GENIUS Act, his own signed legislation, by lobbying to extend the yield ban and hobble stablecoin competition. A Republican president publicly siding against the banking lobby on a financial regulation fight is a genuinely new configuration in Washington, and it reshuffled assumptions on both sides about who holds the political high ground.

How the yield clause took CLARITY hostage

The CLARITY Act is a market structure bill. It assigns jurisdiction between the SEC and CFTC, defines when a digital asset is a security or a commodity, and creates the registration framework the industry has demanded for a decade. It is not, on its face, a stablecoin bill; the complete stablecoin framework already passed in GENIUS. But Washington does not respect bill boundaries, and the yield war has annexed it.

The banking lobby’s ask is straightforward: use CLARITY to close the loopholes GENIUS left open. That means extending the interest prohibition from issuers to exchanges and affiliates, killing the rewards programs that pay stablecoin holders today, and blocking any structure that passes reserve income to users. Bank trade groups have made support conditional on those provisions, and enough senators from both parties bank with them, figuratively and literally, to make the demand real.

Crypto’s response arrived the last week of June, when Coinbase announced it could no longer support CLARITY in its current trajectory, precisely because the yield restrictions being negotiated into it would, in the company’s view, entrench the ban permanently. The industry’s most important lobbying force turning against the industry’s most important bill was the loudest possible signal that the yield clause now outweighs the rest of the legislation for the companies whose business models depend on it.

Chairman Scott’s postponement of the markup followed within days. The delay was procedural on its face and structural in substance: there is no current text that both the banks and the crypto industry will accept, and members have little appetite to vote on a bill that one of the two richest lobbies in the country has promised to remember.

The market structure everyone claims to want is now collateral in a fight over a clause most voters have never heard of.

The political calendar sharpens everything. The window before the midterm campaign consumes Congress is measured in weeks, and both lobbies know that a bill that slips past the summer likely slips past the election, into a Congress nobody can predict.

The Regulation Q rhyme

The yield war has a nearly perfect historical precedent, and both sides quote it selectively.

From 1933 until its final repeal in 2011, Regulation Q capped or prohibited the interest American banks could pay on various deposits, a Depression-era rule justified in language strikingly close to today’s: unrestrained competition for deposits would push banks into risky lending and destabilize the system. For four decades the cap was mostly invisible, because market rates sat near the ceiling. Then came the inflation of the 1970s. Market rates ran far above what banks were legally allowed to pay, and savers found themselves holding accounts that lost purchasing power by regulatory design.

The market’s answer was the money market mutual fund, an instrument that did precisely what yield-bearing stablecoins propose to do now: pool customer cash, buy short-term government paper, and pass the interest through. Money funds grew from nothing in 1971 to hundreds of billions by the early 1980s, deposit flight became a named phenomenon, disintermediation, and the banking industry warned in congressional testimony that the funds would destroy community banking and starve the economy of credit. Congress ultimately responded not by banning money funds but by deregulating deposits, phasing out the caps and letting banks compete for money at market rates.

Both sides of the 2026 fight live inside this story. Crypto cites it as proof that yield restrictions always fall, that savers eventually get paid, and that the catastrophic credit predictions never arrived; the banking system that emerged from deregulation was different, and more expensive to fund, but intact. The banks cite the sequel: the savings and loan industry, built entirely on cheap capped deposits, could not survive paying market rates for money, and its collapse consumed a decade and roughly $124 billion of public funds. Deposit competition did not end banking, but it did end the banks whose models required the subsidy.

The rhyme suggests the real question is not whether stablecoin yield eventually becomes legal in some form; the historical base rate says restrictions on paying savers erode. The question is which institutions are the savings and loans of this cycle, funded so completely by the interest-free float that they cannot survive its repricing, and whether they are banks, or the stablecoin issuers whose entire margin is the yield they currently keep.

The banks’ quiet hedge

While the trade associations fight the public war, the banks themselves are behaving like institutions that expect to lose it.

Barclays made the most explicit move, taking a stake in Ubyx, the stablecoin clearing network built to let banks and fintechs redeem stablecoins at par across issuers, the plumbing a bank needs on the day it decides to issue or distribute digital dollars itself. It was the first direct stablecoin infrastructure investment by a major bank since the yield fight broke into the open, and it was not framed as an experiment. Bank executives have begun saying the quiet part in public: if Congress makes yield-bearing digital dollars legal, the banks will go into that business, at scale, the day the ink dries.

The logic is the same one that has played out in every disruption cycle in finance. Banks did not want money market funds in 1975 or online brokerages in 1995, and once each became inevitable, banks became the largest providers of both. A legal yield-bearing stablecoin issued by a money center bank, with deposit-adjacent branding, existing customer relationships, and a balance sheet behind it, is a formidable product, and arguably a more dangerous one to Tether and Circle than to the banks themselves. Consortium efforts like Open USD, whose members built a shared issuance model precisely so no single firm owns the float, exist in part because everyone can see the banks coming.

The infrastructure is converging from the other direction too. Payment-first blockchains designed for regulated issuers, the category examined in the rise of dedicated stablechains, are being built with bank compliance requirements as first-order design constraints, not afterthoughts. The technical gap between a bank deposit and a stablecoin narrows every quarter; the yield clause is the last load-bearing wall between the two products.

That is the tell in this fight. Institutions do not invest in the rails of a product category they expect to strangle. The banks are lobbying to delay the future and provisioning to own it.

What each side gets wrong

The banks’ deposit-flight case has a real weakness at its center: it treats the current deposit franchise as an entitlement. The spread between what banks earn on customer money and what they pay for it is not a law of nature; it is a price maintained by friction, and every prior technology that reduced the friction, from money funds to high-yield online savings, transferred some of that spread to savers without collapsing credit. The system adapted, banks paid more for funding, lending got marginally more expensive, and the economy survived. Framing the next step in that fifty-year process as a $6.6 trillion cliff requires assuming, without much evidence, that this time adaptation is impossible.

Crypto’s consumer-surplus case has a mirror-image weakness: it waves away the run problem. Bank deposits are sticky in a crisis partly because they are insured and partly because moving them is slow. A yield-bearing stablecoin is uninsured and moves at the speed of a tap. In a March 2023-style panic, the same properties that make stablecoins efficient make them the fastest exit door in the system, and a world where a meaningful share of transactional money can flee to tokenized T-bills in an afternoon is a world with a new, untested amplifier under every banking stress. The honest crypto answer is that this risk is manageable with reserve rules and redemption gates; the marketing answer, that it does not exist, is the one that gets said out loud.

There is also a shared blind spot. Both sides model the fight as domestic, and the stablecoin market is not. The majority of dollar stablecoin demand originates outside the United States, from savers and businesses in weak-currency economies for whom the yield question is secondary to the dollar itself. Whatever Congress decides about interest, the offshore float will keep growing, and the deposits it drains first are not in Kansas; they are in Buenos Aires and Lagos and Istanbul. The American fight over yield is, in part, a fight over who gets to monetize a global phenomenon neither side created.

The endgame scenarios

Three broad resolutions are visible from here, and each has a coalition behind it.

The first is the status quo hardened: CLARITY passes with the extended yield ban, rewards programs die, and issuers keep the float. This is the banks’ victory condition. Its weakness is that it is probably temporary, an attempt to legislate against a spread that technology keeps making easier to deliver, enforced against an industry with a sitting president publicly on its side. Prohibitions that fight both technology and the White House have a poor record.

The second is the pass-through world: yield becomes legal, the banks execute their hedge, and within a few years the largest stablecoin issuers in America are the same institutions that spent 2026 warning about them. Deposits reprice, weaker banks consolidate, and the credit system adjusts to more expensive funding, the way it adjusted to money market funds. This is where the investment behavior of the banks themselves suggests the smart money already sits.

The third is stalemate: CLARITY dies this Congress, GENIUS remains the only law, and the yield question migrates to regulators and courts, fought product by product through rewards programs, tokenized money funds, and offshore issuers that Congress never manages to reach. This is the default outcome if the next few weeks produce no text, and default outcomes in a midterm year are heavy favorites.

The watch list for the next few weeks is short and concrete. First, whether Scott reschedules the markup before the August recess, because a markup date means a text exists that leadership believes can survive both lobbies, and no date means the third scenario is winning. Second, the behavior of the pro-crypto Senate bloc, which has to decide whether a CLARITY with a hardened yield ban is worth passing over the industry’s objection, or whether half the coalition walks. Third, the regulatory perimeter fights already underway: how the Treasury implements the GENIUS provisions on affiliates, whether the rewards programs survive their first supervisory challenges, and how aggressively tokenized money market funds, which pay yield legally because they are securities, get marketed as the stablecoin alternative the ban cannot touch. Every one of those is a proxy battle in the same war, and each can move independent of Congress.

It is also worth naming the quiet incentive nobody in the fight advertises: the federal government is a beneficiary of the stablecoin boom regardless of who keeps the yield, because every reserve dollar is demand for Treasury bills at the exact moment deficits need buyers. A Washington that quietly likes the float’s growth has reasons to resolve the fight in whatever way grows it fastest, and that logic, unspoken, may ultimately weigh more than either lobby’s studies.

The $6 trillion number that anchors the fight will keep being quoted whichever path unfolds, and it is worth remembering what it actually is: not a measurement, but a boundary claim, the banks’ estimate of everything they could lose in the world their opponents want. The real number will be discovered the way these numbers always are, one repriced deposit at a time. The only certainty is the direction. Money has spent fifty years migrating toward whoever pays for it, and no clause has ever held that line forever.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Digital asset markets are volatile and you can lose your entire investment. Always do your own research. Information current as of July 6, 2026.

Crypto World

The AI vs. Crypto Tug-of-War for Capital: Why Today’s Competition Will Become Tomorrow’s Partnership

For nearly a decade, venture capital has chased one transformative technology after another. From mobile apps to cloud computing, from blockchain to generative AI, investment dollars have always followed the next big narrative. Today, that narrative belongs overwhelmingly to artificial intelligence.

In 2025 and into 2026, AI startups have secured some of the largest funding rounds in technology history. Companies developing frontier AI models have attracted tens of billions of dollars in fresh capital, while enterprises racing to integrate AI have become venture capital’s highest priority. In contrast, the once-explosive Web3 funding environment has become quieter, more disciplined, and far more selective.

To many observers, this appears to signal a clear winner. AI is booming, while crypto has faded into the background.

But that conclusion misses the bigger picture.

Rather than signaling the decline of blockchain, today’s capital migration is forcing the crypto industry to evolve beyond speculation. More importantly, it is laying the foundation for a future where AI and blockchain become deeply interconnected technologies rather than competing ones.

The real story isn’t AI versus crypto.

It’s AI because of crypto—and eventually, AI powered by crypto.

The Great Migration of Venture Capital

Venture capital has always been driven by two powerful forces: limited capital and unlimited fear of missing out.

Whenever a new technology demonstrates explosive growth potential, investors naturally redirect capital toward the highest perceived returns. Over the past two years, AI has become that destination.

Large Language Models, autonomous agents, enterprise AI platforms, robotics, and AI infrastructure have collectively absorbed billions that might once have flowed into decentralized finance, NFT ecosystems, or Layer-1 blockchain projects.

This migration has dramatically changed the investment landscape.

Where crypto startups once raised enormous seed rounds based largely on future potential, today’s investors demand measurable adoption, sustainable revenue, and realistic business models. Meanwhile, nearly every startup pitch deck now includes an AI strategy because founders recognize that artificial intelligence has become almost mandatory for attracting early-stage investment.

Crypto has effectively lost its speculative premium.

Instead of existing as a separate asset class driven primarily by narrative, blockchain projects are increasingly evaluated like traditional technology companies.

While painful for many projects, this transition may ultimately be one of the healthiest developments the industry has experienced.

Why AI Is Winning the Short-Term Investment War

The reasons behind AI’s dominance are surprisingly straightforward.

Immediate Utility Beats Long-Term Infrastructure

Artificial intelligence delivers value almost instantly.

A developer can purchase access to an AI API and automate software development within minutes. Businesses can deploy customer service agents overnight. Marketing teams can generate content at unprecedented speed.

The productivity gains are visible immediately.

Blockchain, on the other hand, operates differently.

Its value proposition isn’t instant automation—it’s rebuilding the infrastructure of digital trust.

Creating decentralized financial systems, secure identity networks, tokenized assets, or censorship-resistant infrastructure requires years of engineering, regulatory clarity, and user adoption. These projects solve foundational problems, but they often lack the immediate “wow factor” that attracts short-term investors.

Simply put:

- AI delivers productivity today.

- Blockchain builds infrastructure for tomorrow.

For venture capital seeking rapid returns, today’s value often outweighs tomorrow’s architecture.

The Valuation Gap

AI has also created an increasingly uneven investment environment.

Many venture firms now treat AI integration as a baseline requirement rather than a competitive advantage.

As a result, pure-play Web3 startups frequently compete for a shrinking pool of specialized blockchain investors, while AI startups enjoy broader access to general technology funds.

This has effectively created a two-tier venture ecosystem:

Tier One: AI-native companies attracting premium valuations.

Tier Two: Blockchain companies face significantly higher scrutiny before receiving funding.

The imbalance is substantial—but it is unlikely to remain permanent.

Faster Exit Opportunities

Investors also prefer AI because commercialization appears more predictable.

Enterprise software companies regularly acquire AI startups.

Major cloud providers continuously expand their AI capabilities.

Corporate demand already exists.

Crypto investments follow a different path.

Returns often depend on token launches, network adoption, evolving regulations, and volatile market cycles.

For venture capital firms measured on fund performance, AI currently offers a shorter and more visible path toward liquidity.

Crypto’s Evolution: From Hype to High-Beta Technology

Ironically, losing speculative capital may be exactly what blockchain needed.

The crypto industry has spent years funding countless variations of decentralized exchanges, yield farms, Layer-2 networks, and meme-driven ecosystems.

That era is fading.

Today’s investors increasingly demand fundamentals.

Projects are expected to generate revenue.

Tokenomics must align with sustainable economic models.

Communities alone are no longer enough.

This shift has given rise to what many describe as Tokenomics 2.0.

Modern blockchain projects increasingly emphasize:

- Revenue-linked token value

- Fee-sharing mechanisms

- Token buyback programs

- Treasury sustainability

- Real protocol cash flows

Instead of rewarding speculation, markets are beginning to reward measurable utility.

Crypto is becoming less of an isolated financial experiment and more of a high-beta extension of the broader technology sector—still volatile, but increasingly tied to real economic activity.

The Turning Point: Where AI Meets Blockchain

The assumption that AI and crypto compete for the same future overlooks one fundamental reality:

Artificial intelligence cannot fully scale using traditional financial infrastructure.

As AI systems become autonomous, they begin encountering problems that existing payment systems were never designed to solve.

This is where blockchain re-enters the story.

The Machine-to-Machine Economy

Imagine an autonomous AI agent managing an international supply chain.

It needs to:

- Purchase satellite imagery.

- Rent cloud computing.

- Pay for API requests.

- Buy proprietary datasets.

- Hire another specialized AI agent.

Each transaction may cost fractions of a cent.

Traditional banking struggles with this model.

Credit cards require human identities.

Bank accounts require legal ownership.

International wire transfers take days.

Card networks charge fixed transaction fees that make micropayments economically impossible.

An AI agent cannot simply apply for a corporate credit card.

Nor should it.

Machines need a native digital payment infrastructure.

Blockchain as the Economic Rail for AI

Blockchain networks solve many of these challenges naturally.

Crypto wallets allow software agents to control digital assets independently through cryptographic signatures.

Stablecoins enable programmable global payments without relying on traditional banking hours.

Transactions settle within seconds.

Fees can be measured in fractions of a cent.

This creates entirely new possibilities.

An AI assistant reading premium research could instantly pay a publisher $0.001 for access.

A coding agent could purchase compute power by the second.

Autonomous robots could negotiate and pay one another for services without human intervention.

These tiny machine-to-machine payments are practically impossible using legacy financial systems.

On blockchain, they become routine.

Increasingly, blockchain ecosystems are building this infrastructure precisely through AI-focused development kits, agent frameworks, and stablecoin payment rails. As autonomous software becomes more common, decentralized networks may become the default settlement layer for machine commerce.

From “Vibes” to Value

Another important shift is occurring beneath the surface.

Global regulation is gradually pushing crypto beyond its speculative origins.

Frameworks such as Markets in Crypto-Assets Regulation are establishing clearer rules for digital asset markets, while regulators in the United States continue developing more standardized oversight for crypto businesses.

As legal uncertainty decreases, blockchain projects face increasing pressure to operate like mature financial infrastructure rather than experimental internet communities.

Ironically, AI’s dominance has accelerated this transition.

With speculative capital flowing elsewhere, blockchain builders have been forced to focus on products that solve real-world problems.

The industry has become leaner, more disciplined, and arguably stronger.

Is AI Becoming Overvalued?

History suggests that no investment narrative dominates forever.

Today’s AI market is attracting enormous amounts of capital, producing increasingly expensive funding rounds and premium valuations.

While artificial intelligence undoubtedly represents a transformative technology, concentrated investment can also create valuation risk.

If future funding becomes more selective or AI valuations begin normalizing, investors will naturally search for underpriced sectors with strong long-term fundamentals.

Blockchain infrastructure may become one of the most attractive destinations.

Especially projects enabling:

- AI payments

- Stablecoin infrastructure

- Decentralized identity

- Compute marketplaces

- Agent coordination

- Cross-chain settlement

Rather than competing with AI, these technologies enhance AI’s ability to operate autonomously.

The Future Is Convergence, Not Competition

The narrative that AI and crypto are enemies reflects a short-term investment mindset rather than a long-term technological reality.

Artificial intelligence may become the brain of tomorrow’s digital economy, making decisions, learning continuously, and performing increasingly sophisticated work.

But every brain requires a nervous system.

Blockchain provides that infrastructure.

It supplies programmable ownership, verifiable identity, decentralized coordination, and instant global settlement—the economic rails that autonomous machines will increasingly depend upon.

The future is unlikely to belong exclusively to AI or crypto.

It belongs to the intersection where intelligent agents transact securely, coordinate independently, and exchange value without friction.

Investors abandoning blockchain entirely in pursuit of AI’s latest megadeals may be overlooking the next major opportunity.

The smartest capital rarely chases yesterday’s headline.

It quietly positions itself where two transformative technologies begin to converge.

And that convergence—where autonomous AI meets decentralized economic infrastructure—could become the foundation of the next multi-trillion-dollar digital economy.

REQUEST AN ARTICLE

Key Highlights

-

Russia’s largest bank Sberbank will introduce cryptocurrency wallet services via its digital platforms.

-

New digital asset legislation in Russia may become active from September 1.

-

The bank intends to establish a digital depository for cryptocurrency custody by year-end.

-

Other major institutions including Moscow Exchange, VTB, and T-Bank are developing similar offerings.

-

Russia’s approach to digital assets is evolving from restriction toward licensed market participation.

Russia’s dominant banking institution Sberbank is preparing to enter the cryptocurrency sector with a digital wallet and custody solution as federal authorities advance comprehensive digital asset regulations. The financial giant intends to integrate licensed cryptocurrency functionality into its existing consumer-facing platforms. This strategic initiative represents a significant reversal in a market historically characterized by governmental constraints.

Banking Giant Develops Crypto Infrastructure Under Legislative Framework

The institution plans to roll out its cryptocurrency wallet functionality through both Sberbank Online and SberInvestments platforms following parliamentary approval of pending legislation. During remarks at the Bank of Russia Financial Congress, Kirill Tsarev, who serves as first deputy chairman at Sberbank, detailed the institution’s roadmap. He emphasized that consumer-facing services would be developed in alignment with evolving regulatory guidelines.

The legislative proposal, formally titled “On Digital Currency and Digital Rights,” is anticipated to enter into force on September 1. This implementation date was confirmed by Vladimir Chistyukhin, First Deputy Chairman at Russia’s central bank, according to RBC reporting. Sberbank awaits the publication of finalized legislative text to establish more precise operational timelines.

Beyond wallet services, Sberbank is developing comprehensive infrastructure to support cryptocurrency trading and digital asset record-keeping. The financial institution has set a December 1 target date for launching a digital depository designed to safeguard and track cryptocurrency holdings. Distribution through mobile app marketplaces could present challenges, particularly regarding platform-specific approval processes.

Federal Authorities Establish Licensed Digital Asset Ecosystem

The emerging regulatory structure will authorize licensed entities to provide various cryptocurrency-related financial services. These organizations may be permitted to facilitate trading operations, asset custody, fiat-to-crypto conversion, and international cryptocurrency settlement functions. Traditional banking institutions and established exchanges will gain market entry under direct oversight from financial authorities.

Sberbank is evaluating the possibility of serving as a domestic gateway for international cryptocurrency trading platforms. Such an arrangement would require compliance with Russian regulatory standards and acceptance of terms established by foreign exchanges. This intermediary model could enable Russian citizens to participate in global cryptocurrency markets through domestically approved channels.

Moscow Exchange has announced intentions to commence cryptocurrency trading operations before 2026 concludes. The exchange anticipates moving forward after legislative approval and subsequent regulatory guidance. Concurrently, VTB and T-Bank have disclosed plans to establish their respective digital custody solutions.

Russian Policy Evolves From Prohibition Toward Supervised Market Participation

For several years, Russian authorities maintained restrictive policies regarding cryptocurrency within the domestic financial ecosystem. The Bank of Russia advocated for extensive limitations in 2022, citing potential threats to financial system stability. The Finance Ministry, however, favored a regulatory approach rather than comprehensive prohibition.

President Vladimir Putin subsequently enacted regulations prohibiting cryptocurrency as a payment method for commercial transactions. Nevertheless, international sanctions created demand for alternative settlement mechanisms after Russian financial institutions encountered barriers in traditional payment networks. Consequently, Russia authorized cryptocurrency mining operations and pilot programs for cross-border crypto settlements during 2024.

The forthcoming regulatory framework will permit domestic cryptocurrency trading within experimental parameters and impose annual transaction limits for retail participants. Market participants will receive a transition window extending to July 1, 2027, to complete official registration procedures. Sberbank’s strategic initiative demonstrates how Russia’s leading financial institutions now anticipate the emergence of a supervised cryptocurrency marketplace.

Belgium’s financial markets regulator warned consumers against six crypto-asset service providers (CASPs) it said were operating in the country without authorization, days after the European Union’s Markets in Crypto-Assets (MiCA) licensing deadline took effect.

On Monday, the Financial Services and Markets Authority (FSMA) identified several CASPs active in Belgium without authorization under MiCA regulation. FSMA named Aurum Foundation, Bank Bit, Bithf Pro, Dxago, Global Dynamic Trade and ZeriaFunding. The regulator said it had added these entities to its list of fraudulent CASPs.

The warning indicates that national regulators are beginning to apply the MiCA licensing perimeter following the EU’s transitional period, which ended on July 1.

The Brussels-based regulator strongly advised consumers not to accept offers from the named companies and told users to check whether a provider is listed in its official CASP register. The FSMA also warned that crypto assets can be volatile, may suffer from liquidity limitations and are not covered by a compensation scheme that could reimburse users for potential losses.

Cointelegraph contacted FSMA for more information but did not receive a response by the time of publication.

List of unregistered CASPs. Source: FSMA

MiCA deadline starts enforcement phase across Europe

MiCA entered into force at the end of 2024, creating a harmonized EU framework for CASPs and issuers. Under Belgium’s FSMA guidance, only authorized CASPs are permitted to offer crypto asset services like custody, trading platforms, crypto-to-fiat exchange, crypto-to-crypto exchange, order execution, transfer services, advice and portfolio management.

Belgium’s transitional regime expired on July 1, the same date by which existing providers across the EU generally had to obtain authorization or stop offering crypto-asset services.

Related: Germany leads MiCA crypto authorization race as Europe’s deadline looms

The deadline has been a major pressure point for crypto companies operating in the bloc. On June 24, crypto exchange Binance withdrew its MiCA application filed in Greece and planned to seek authorization in another EU jurisdiction just days before the July 1 deadline.

At the time, the exchange said it was “not leaving Europe” but acknowledged some users could be affected as it worked to comply with applicable requirements.

Magazine: Bitcoin slides to $58K, XRP hits $1 but onchain data promising: Market Moves

Key Takeaways

- Shares of Intel began Monday’s session at $120.35, helping drive a semiconductor sector recovery following two weeks of declines in the SOX benchmark.

- Information technology earnings projections have jumped 10% throughout Q2; Intel and Sandisk show the strongest estimate growth.

- Wall Street now forecasts Intel’s Q2 earnings per share at $0.21, a significant increase from the $0.08 projection on March 31.

- Several institutional players expanded their INTC holdings during Q2, with institutions and hedge funds controlling 64.53% of shares outstanding.

- HSBC maintains a Buy rating with a $200 price target, while Goldman Sachs assigned a neutral stance with a $150 objective.

Intel shares opened Monday’s trading at $120.35 as semiconductor stocks recovered from back-to-back weekly declines that pressured the PHLX Semiconductor Index (SOX).

Sandisk (SNDK) and Western Digital (WDC) also experienced approximately 4% gains after suffering significant losses during Thursday’s selloff.

The semiconductor recovery materialized as market participants shifted focus toward the approaching earnings reporting period, where technology sector expectations have been strengthening.

FactSet data reveals that information technology sector earnings forecasts have advanced 10% since the second quarter’s April 1 start date. This positions IT just behind the energy sector, which has witnessed a dramatic 50% surge in estimates during the identical timeframe.

Intel and Sandisk are spearheading the technology sector’s earnings-per-share estimate improvements on a percentage basis since the end of March. Sandisk also appears near the top when measured in absolute dollar terms, alongside Micron (MU), Nvidia (NVDA), and Apple.

Regarding Intel’s specific outlook, Wall Street analysts currently project Q2 EPS of $0.21, representing a substantial increase from the $0.08 forecast that existed at the quarter’s beginning. Intel’s management has issued Q2 guidance calling for $0.20 EPS.

Institutional Ownership Continues Growing

Numerous institutional investment firms expanded their Intel holdings during the second quarter. Walkner Condon Financial Advisors established a fresh position valued at approximately $224,000 through the purchase of 5,068 shares. Sivia Capital Partners expanded its Intel stake by 271.7%, bringing its total to 34,201 shares valued at $766,000. NewEdge Advisors increased its position by 29.6%, now holding 158,277 shares.

In total, hedge funds and institutional investors maintain ownership of 64.53% of Intel stock.

On the insider transaction front, Executive Vice President April Miller divested 40,256 shares on May 1 at an average price of $99.53 per share, generating proceeds exceeding $4 million. This transaction decreased her ownership percentage by 27.7%.

Street Price Targets Show Wide Dispersion

Analyst price objectives for Intel demonstrate considerable variance across Wall Street. HSBC elevated its target to $200 while maintaining a Buy recommendation, citing advancement in Intel’s foundry operations and possible collaborations with Apple, Nvidia, and Amazon.

Goldman Sachs launched coverage on June 25 with a neutral assessment and a $150 price objective. Mizuho established a $135 target on June 21. TD Cowen maintains a Hold rating with a $75 price goal. Rosenblatt carries a Sell rating alongside a $50 target.

The aggregate consensus among 49 Wall Street analysts establishes a “Hold” rating with an average price target of $96.69.

Intel’s latest quarterly results, disclosed on April 23, revealed Q1 EPS of $0.29, surpassing the $0.01 consensus estimate by $0.28. Revenue totaled $13.58 billion, exceeding the $12.32 billion projection and representing a 7.4% year-over-year increase.

The stock’s 52-week trading range spans from $18.97 to $142.35. Its 200-day moving average stands at $71.20, considerably below current trading levels. Intel maintains a market capitalization of $604.88 billion with a beta coefficient of 2.18.

Strategy (MSTR) sold 3,588 bitcoin for approximately $216 million last week, reducing its total holdings to 843,775 BTC, according to a Monday SEC filing.

The company said proceeds from the bitcoin sales will be used to fund distributions on its preferred stock and replenish the portion of its U.S. dollar reserve used for those payments. As of July 5, the USD reserve totaled $2.55 billion.

The latest sales were executed at an average price of roughly $60,000 per bitcoin and are dramatically higher than the 32 bitcoin sold by the company about one month ago, which sent crypto prices plunging. Strategy currently holds 843,775 BTC acquired for approximately $63.69 billion, or an average purchase price of $75,476 per bitcoin.

Strategy also said it did not sell any shares under its at-the-market equity program during the week ended July, and did not repurchase any shares under its buyback programs. The company added that the full $1.25 billion capacity under its recently announced BTC Monetization Program remains available.

Strategy shares are down 2% in pre-market trading and bitcoin has given up much of its weekend gain, trading down to $61,900 from $62,900 prior to the announcement.

TLDR

- Solana added 1.60 million new addresses in two weeks, showing stronger network participation.

- SOL held its short-term uptrend as buyers defended key support levels.

- Analysts identified $85.81, $88.79, and $93.95 as the next upside targets.

- The $86 to $94 zone remains the main resistance area for Solana’s breakout setup.

Solana price prediction remains positive after on-chain activity strengthened and technical support stayed intact. Network data showed 1.60 million new addresses joined within two weeks. Meanwhile, SOL continued holding higher lows while resistance near $94 remained the next focus.

Network activity strengthens Solana’s market outlook

Solana price prediction gained attention after fresh on-chain data highlighted steady network expansion. Ali Charts reported 1.60 million new addresses during the past two weeks. The figures reflected stronger participation across the broader Solana ecosystem.

The total address count increased from about 6.8 million to 8.6 million during the measured period. That increase suggested rising activity beyond short-term market movements. Consequently, stronger network participation supported improving market conditions.

Solana price prediction also received support because expanding addresses often reflect growing ecosystem usage. However, address growth alone cannot confirm a sustained price breakout. Even so, consistent participation strengthened the broader bullish structure.

Price structure keeps the bullish trend intact

Solana price prediction remained constructive because SOL preserved its short-term upward trend. More Crypto Online said, “there is still no clear sign that a local top has formed.” The Elliott Wave structure continued pointing toward higher resistance levels.

The analyst identified immediate support near $80.38 for the ongoing structure. Additional support rested near $78.22 and $76.52. Therefore, holding those levels would preserve the current higher-low pattern.

Solana price prediction continued favoring upside targets while buyers defended key support levels. The chart highlighted resistance near $85.81, $88.79, and $93.95. Those levels represented the next technical objectives if momentum continued.

Resistance near $94 remains the next target

Solana price prediction focused on the $86-$94 resistance area as buying pressure persisted. Market structure remained positive because price respected higher lows. Consequently, traders monitored resistance without disrupting the prevailing trend.

A deeper decline could return the $71.17-$64.68 region into focus. That move would weaken the current short-term technical picture. However, it would still fit a broader corrective structure.

Solana price prediction continued to rely on network growth and stable price action together. Strong address creation supported the technical outlook during recent sessions. Therefore, sustained participation and higher lows kept the $94 breakout scenario active.

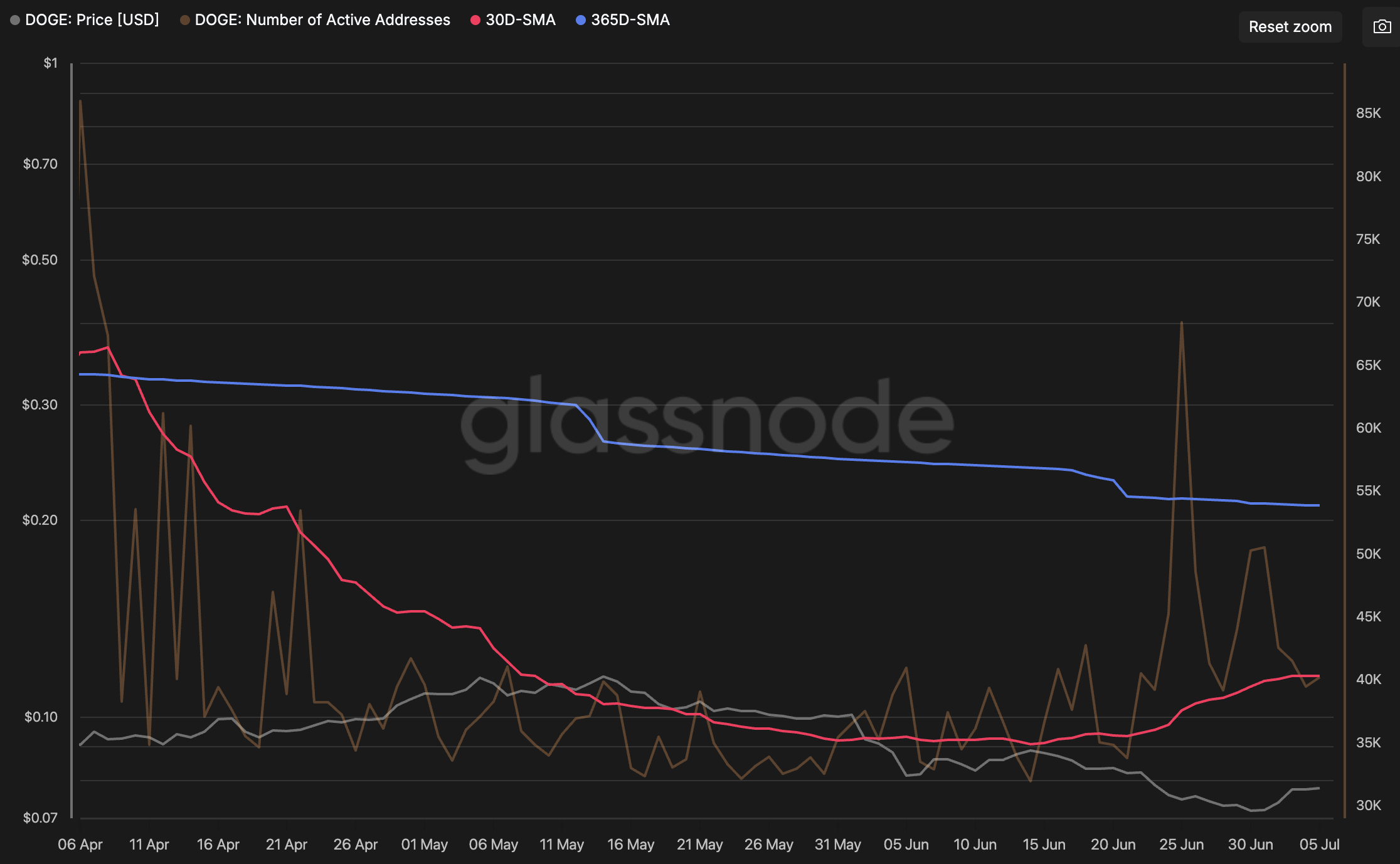

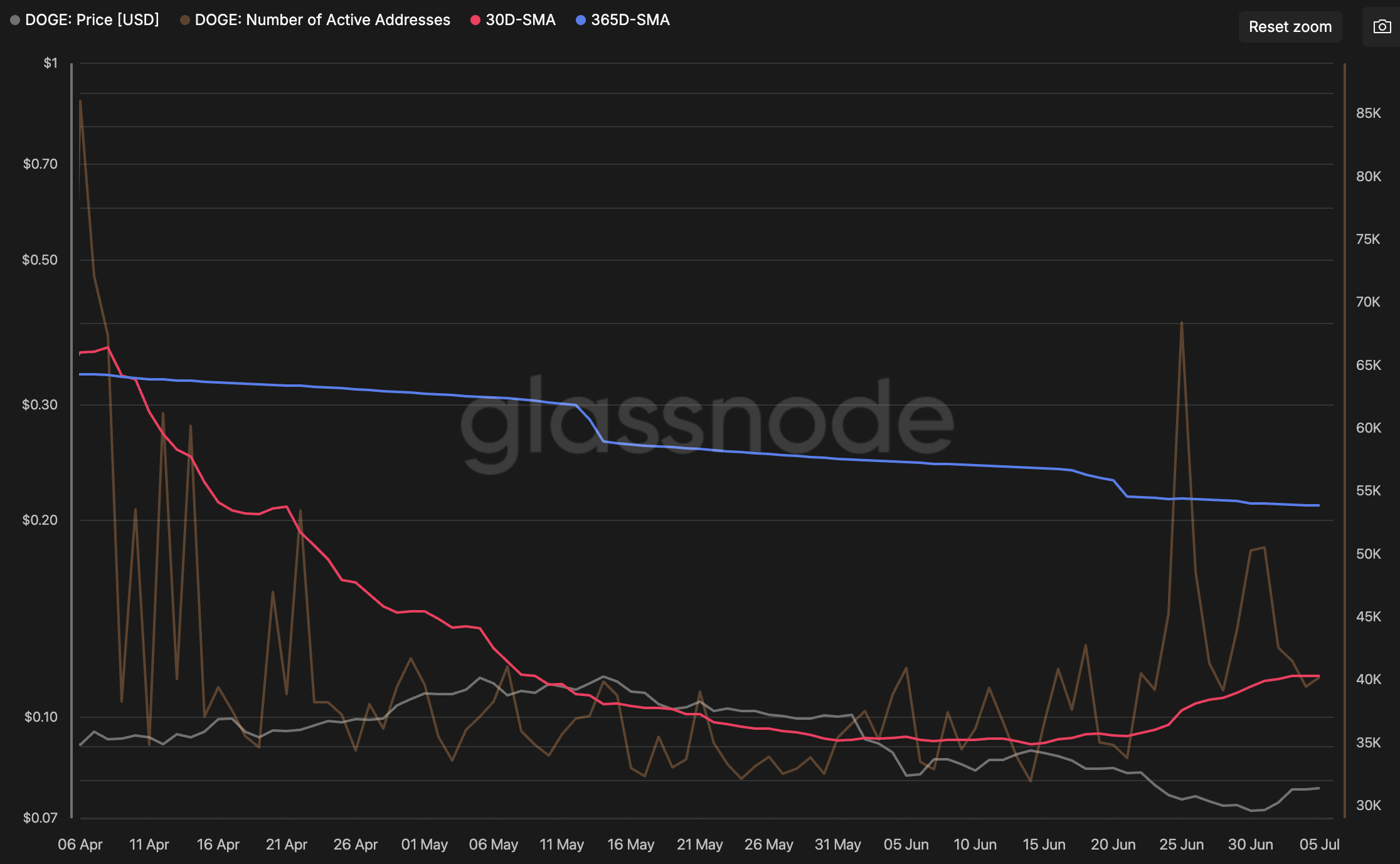

Dogecoin network is suddenly buzzing again. Active addresses have surged to nearly 50,000 since early July, fueling speculation that a bigger move could be around the corner despite muted price action.

Ali Martinez pointed to the jump on X, citing Glassnode data that showed active addresses reaching a multi-month high. His verdict was simple: “Something is brewing.” A day earlier, he also spotted a TD Sequential buy signal, suggesting momentum could be shifting.

Meanwhile, technical indicators are starting to lean bullish. TradingView’s summary shows the MACD flashing a Buy signal, adding weight to the growing optimism. Still, charts only tell half the story. Buyers now need to show up with real volume, or this setup could fizzle out as quickly as it appeared.

Dogecoin is also following Bitcoin’s lead, just as it often does. If Bitcoin keeps pushing higher, DOGE could finally break out of its recent range. However, if Bitcoin loses steam, Dogecoin may stay stuck despite the spike in network activity. Sometimes the chain speaks first, while the price takes its sweet time catching up.

Discover: The Best Token Presales

Can Dogecoin Price Reach $0.12 Before the Breakout Stalls?

DOGE is trading near $0.076, keeping the $0.075-$0.077 area in focus after several sessions of choppy action. Buyers are still defending this zone, but they have not shown much urgency. It feels more like a waiting game than a tug-of-war.

Volume remains light compared with previous rallies, which explains why upside momentum has struggled. Futures open interest is also relatively muted, showing traders are not rushing into leveraged bets. Sometimes the quietest charts make the loudest moves, but that part still needs proof.

The first hurdle sits around $0.081, followed by stronger resistance near $0.09. If DOGE clears those levels with stronger volume, the next area to watch comes in around $0.10. Until then, long-term holders appear patient while short-term traders continue swapping seats.

If support around $0.075 holds, buyers could slowly regain control and push toward $0.081-$0.09. Otherwise, DOGE may stay stuck in its current range for a while longer. A decisive break below $0.075 could open the door to the $0.070-$0.072 area, giving bulls another headache they did not order.

Discover: The Best Crypto to Diversify Your Portfolio

Maxi Doge Eyes Early Mover Upside as DOGE Tests Key Levels

DOGE’s setup is compelling, but at an entry above $0.07, even a run to $0.135 is less than 2X on an asset with a multi-billion dollar market cap and significant overhead supply to absorb. Early-stage exposure to the meme coin narrative carries a structurally different risk-reward profile. That gap is where presales draw attention.

Maxi Doge ($MAXI) is a meme token built on Ethereum that leans hard into gym-culture trading energy, the 240-lb canine juggernaut framing is exactly as absurd as it sounds, and that is precisely the point for viral meme mechanics.

The project has raised somewhere close to $5 million at a current presale price of $0.0002827, with dynamic staking APY active for holders. Standout features include holder-only trading competitions with leaderboard rewards and a Maxi Fund treasury earmarked for liquidity and partnerships.

Research Maxi Doge before the presale ends.

Don’t Miss Out on Our $1,000 USDT Airdrop on ByBit

The post Dogecoin Price Prediction: Analyst Flags DOGE Exploding Network Activity appeared first on Cryptonews.

Bitcoin (BTC) starts the second week of June near two-week highs with traders keen to see bullish continuation.

Key points:

- BTC price action targets nearby liquidity as a trader names the “most important” support zone to hold next.

- US stock-market performance gives analysis reason to believe that the good times will continue amid “record” retail risk appetite.

- A stock-market correction is not out of the question, new warnings conclude, but Bitcoin should have already priced in the fallout.

- Exchange inflow data reveals cooling panic among both retail and whale investors.

- Crypto market sentiment is at monthly highs, on the cusp of exiting “extreme fear.”

Bitcoin key support emerges as bulls eye $64,000

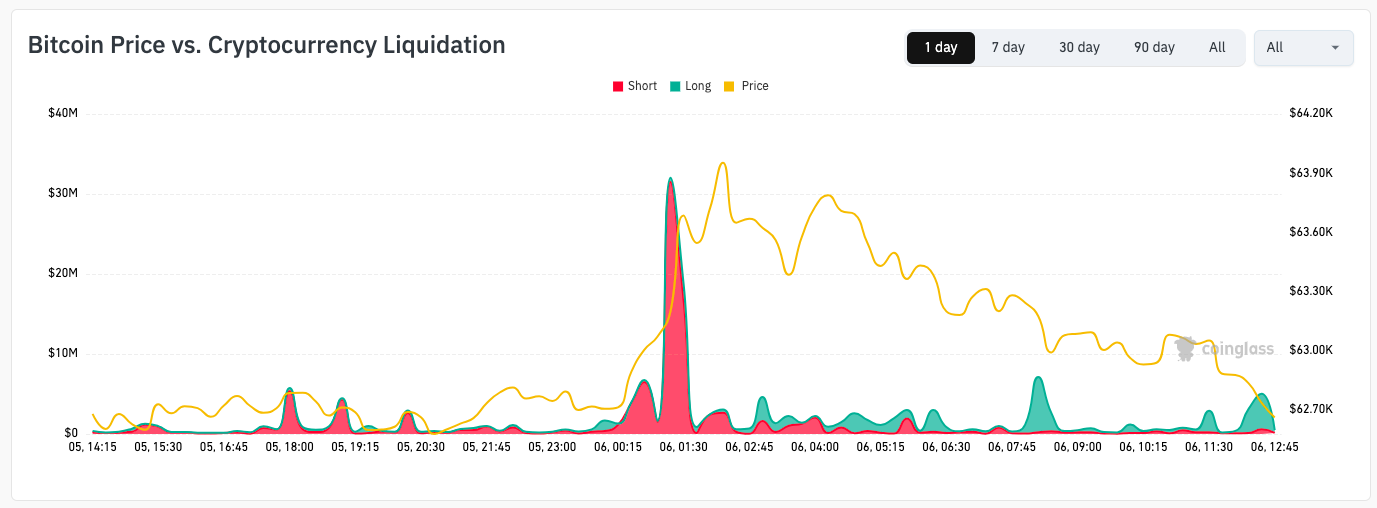

Bitcoin kept up pressure on short positions into the weekly close, hitting $63,960 — its highest levels since June 23, per data from TradingView.

BTC/USD four-hour chart. Source: Cointelegraph/TradingView

Total crypto short liquidations for the 24 hours to the time of writing were just over $100 million, CoinGlass reports.

BTC/USD vs. crypto liquidation history (screenshot). Source: CoinGlass

Commenting on low time frames, X account Exitpump was among those attributing the moves to liquidity hunts.

“Seeing aggressive selling from spot markets, spot CVD (yellow) trending down while perps CVD (blue) is flat,” they reported on Monday, referring to cumulative volume delta on exchange order books.

BTC/USD chart with order-book data. Source: Exitpump/X

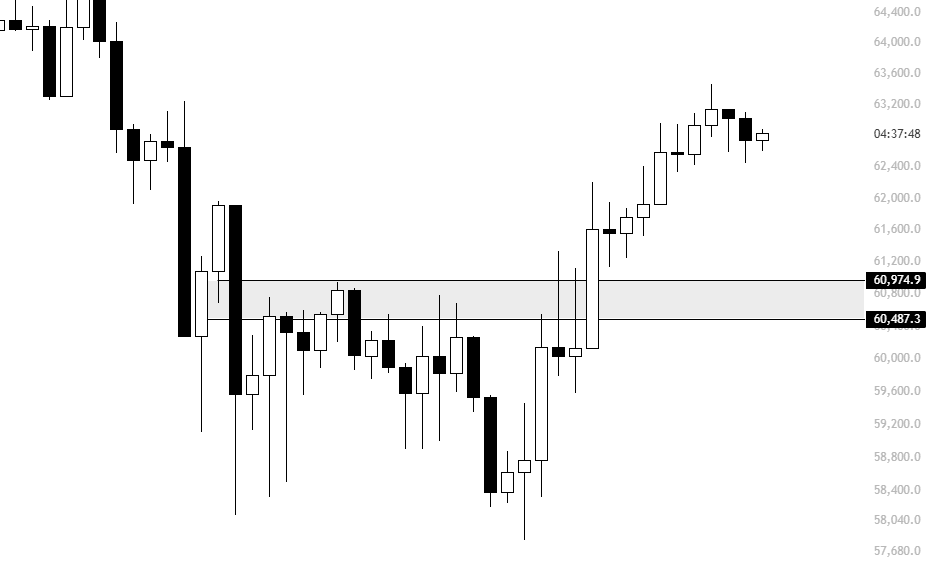

In the event of a reversal downward, trader Killa called the zone between $60,400 and $60,900 Bitcoin’s “most important.”

“If we cannot hold this price region on a revisit, I’m afraid we are going to trend directly to the lows again. Something to watch out for next week,” the analyst told X followers.

BTC/USD chart. Source: Killa/X

As Cointelegraph continues to report, market participants still see Bitcoin’s bear-market low as yet to come — despite a growing number of bullish trend reversal signals.

Trader Roman, who was long bearish on BTC/USD, stayed optimistic on longer time frames this week.

“Still looking excellent to continue our reversal to see higher prices in the interim,” an X post read.

“I still have a feeling we put in one more macro low before the bottom is officially in, but there are dozens of macro reversal signs all over HTF.”

BTC/USDT one-week chart. Source: Roman/X

Retail risk appetite hits record levels

Bitcoin’s waning ability to copy equities is under the microscope this week as US stock futures start higher after the holiday weekend.

While BTC/USD managed a trip to near two-week highs, Nasdaq 100 futures added 1% as analysts remain bullish on the broader US outlook.

“Although the S&P 500 is coming off a hot second quarter with a 15% gain, the index topped in early June and has yet to make a new high,” trading resource Mosaic Asset Company wrote in the latest edition of its regular newsletter, The Market Mosaic.

“But the S&P 500 trading within a bullish continuation pattern and has been finding support at a key level.”

S&P 500 market data. Source: Mosaic Asset Company

Mosaic added that the average stock “has been rallying to new record highs.”

“That includes the equal-weight S&P 500, small-cap stocks with the Russell 2000 Index, and the NYSE advance/decline line. New highs minus new lows across major exchanges are jumping higher as well,” it noted.

As Cointelegraph reported, recent US inflation and labor-market data helped soften markets’ hawkish expectations for Federal Reserve policy last week.

The latest data from CME Group’s FedWatch Tool sees the Fed holding interest rates at current levels in both July and September.

Fed target rate probabilities (screenshot). Source: CME Group

Another potential macro tailwind for Bitcoin comes in the form of retail investor demand for risk — despite the cohort’s crypto exodus this year. Analyzing options data, trading resource The Kobeissi Letter described retail risk appetite as being “at record levels.”

“Retail demand for short-term options has never been higher,” it reported on X.

This week, the Fed will release the minutes of its June meeting, where it likewise kept rates steady. Markets will also react to Purchasing Managers Index (PMI) numbers, along with more employment data releases.

“We expect another volatile week ahead as markets brace for earnings season,” Kobeissi added.

Warning over pre-midterm stock market correction

Looking ahead, not all market participants are convinced that the persistent stocks bull market will last. Among them is Andre Dragosch, European head of research at crypto asset manager Bitwise.

“What if there is a bigger stock market correction right before the Midterms?” he queried in X posts on Monday, referring to upcoming US elections.

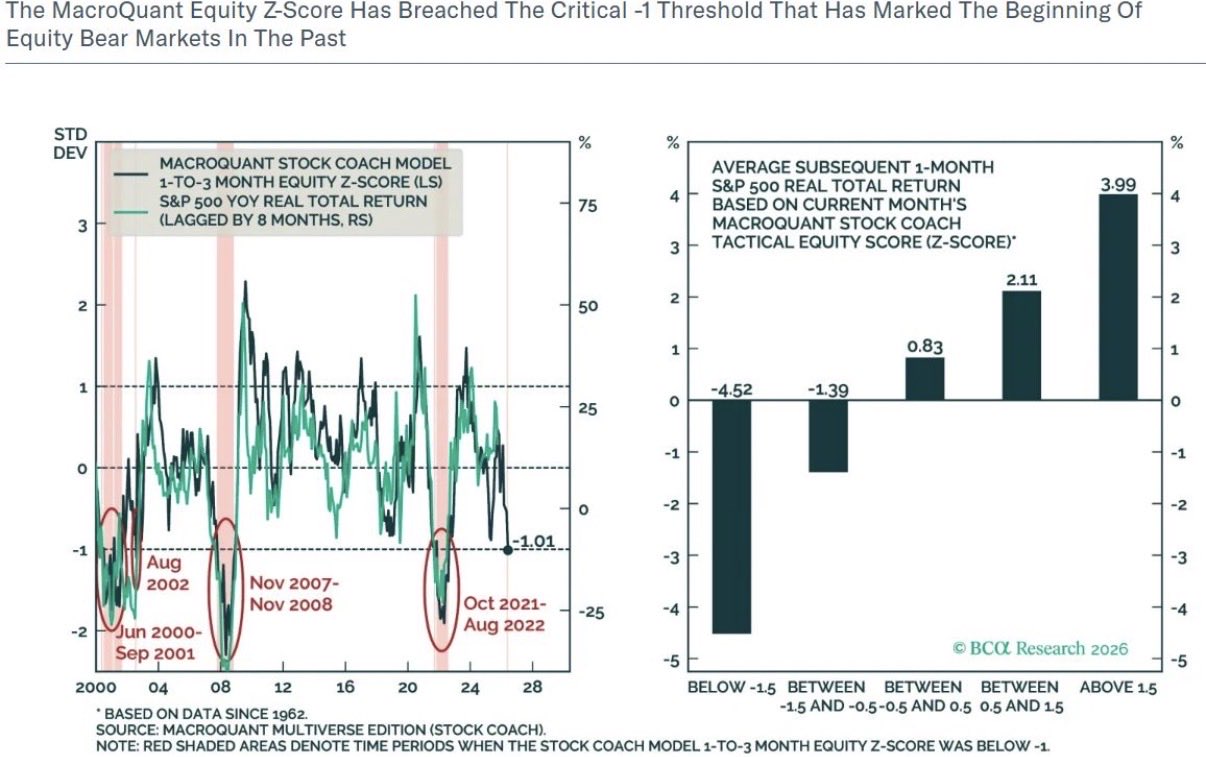

Dragosch flagged the latest data from the MacroQuant Equity Risk Model by macro analytics company BCA Research. This, he warned, was “flashing a bear market warning signal.”

An accompanying chart likened current readings to those last seen in late 2021, when Bitcoin saw the top of its previous bull market.

Source: Andre Dragosch/X

In an extended X post last week, Dragosch nonetheless reasoned that crypto markets had already priced in much of the worst-case scenario that could hit macro in the future: a stock market comedown and a US recession.

“In other words, even if a AI crash and a subsequent US recession materialized, much of that pain appears to be already reflected in Bitcoin prices, which points to reduced downside from here,” he summarized.

Dragosch gave Bitcoin a “decent chance” of outperforming the Nasdaq “on a relative basis over the coming months.”

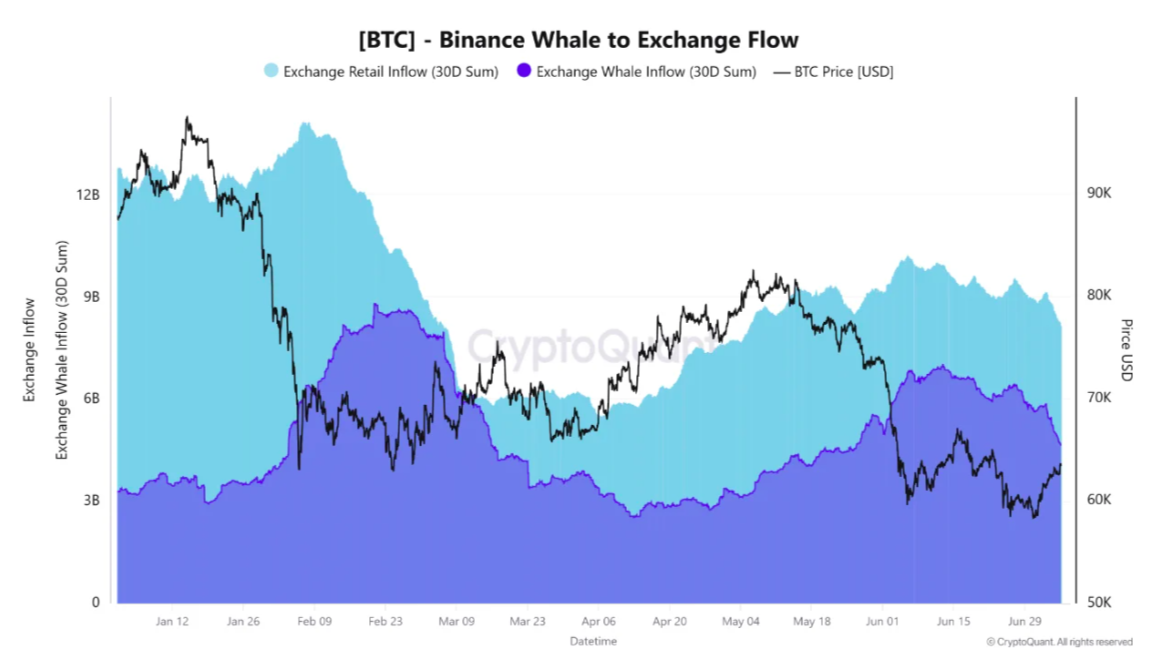

Whales lead exchange inflow drop

New data reveals that Bitcoin investors cooled selling significantly in the second half of June — even as price set new multi-year lows.

In a QuickTake blog post, onchain analytics platform CryptoQuant confirmed that inflows to exchanges had decreased from both retail and whale investors alike.

“Bitcoin whale activity on Binance has cooled sharply since mid-June, with the rolling 30-day value of whale inflows falling by nearly $2.4 billion,” contributor Amr Taha confirmed.

Retail investor inflows displayed a shallower rate of decline, falling from $10.02 billion on June 12 to $8.2 billion on July 6.

“Whale inflows fell at nearly twice the rate of retail inflows, reducing the relative role of large holders in exchange-bound Bitcoin supply. Meanwhile, the gap between retail and whale inflows widened from about $2.98 billion to $3.55 billion,” Taha continued.

Bitcoin whale exchange flows to Binance (screenshot). Source: CryptoQuant

Earlier, Cointelegraph reported on whales’ overall market conviction improving around the lows.

CryptoQuant notes that exchange inflows are not an infallible signal of investors’ intent to sell.

“The key question now is whether Binance whale inflows stabilize around the current $4.65 billion level or continue moving lower,” Taha concluded.

“A further decline would reinforce the view that large Bitcoin holders are becoming less active on the exchange compared with the retail cohort.”

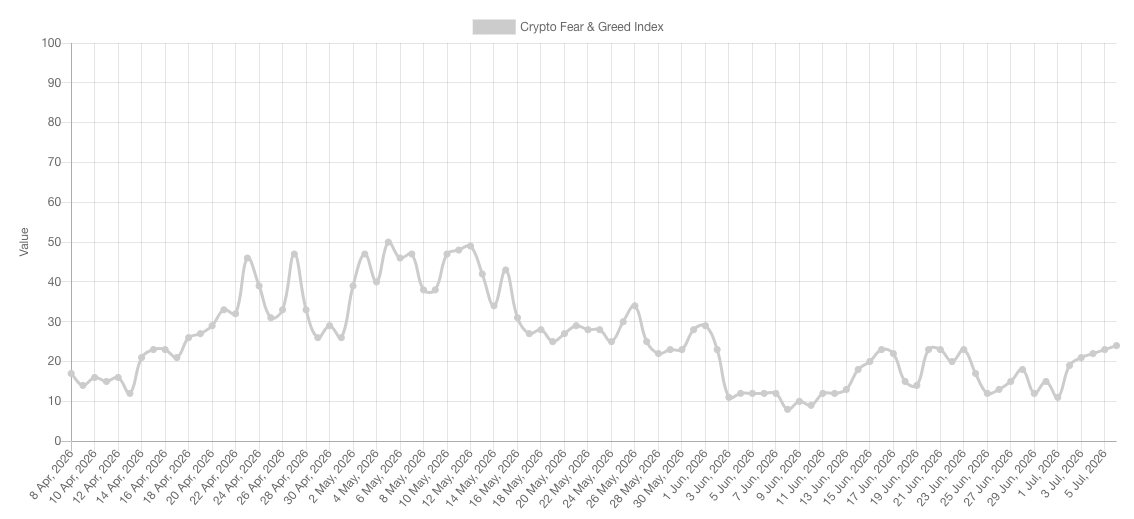

Crypto market fear “easing, not gone”

Bitcoin’s modest recovery was enough to boost crypto market sentiment considerably this week.

Related: Bollinger Bands creator eyes Bitcoin bear-market end, ‘W’-shaped reversal

The latest readings from the Crypto Fear & Greed Index show that aggregate sentiment is on the verge of exiting “extreme fear” for the first time in over a month.

Fear & Greed measured 24/100 on Monday, more than double its score at the start of July.

“That’s a clear improvement from recent lows. But the market is still in Extreme Fear,” trader Master of Crypto responded on X.

“Fear is easing, not gone.”

Crypto Fear & Greed Index (screenshot). Source: Alternative.me

As a lagging indicator, Fear & Greed tends to mirror existing shifts in market behavior post factum. While the Index is calculated based on a basket of factors, it lacks the ability to predict future trend continuation.

In his latest analysis published this week, commentator and blockchain advisor Anndy Lian argued that Bitcoin bulls needed to back up their optimism with tangible price moves.

“A successful breakout above that US$65,000 threshold would open the door to a broader test of the 100-day moving average, which currently hovers near US$69,500,” he wrote.

“Conversely, failing to sustain the current momentum carries severe downside risks.”

The German government has placed crypto taxation on its savings list for the 2027 federal budget. The move could end the crypto tax exemption that investors currently earn after a one-year holding period.

The Federal Ministry of Finance detailed the plan in its monthly report. An adjustment of cryptocurrency taxation for 2027 appears among the consolidation measures agreed by the governing coalition.

Crypto Taxes Join Germany’s Budget Consolidation List

The cabinet approved the key figures for the 2027 budget. The Ministry set a spending frame of €543.3 billion, with net borrowing of €110.8 billion.

Consolidation carries much of the load. The coalition agreed on structural savings of roughly €4 billion per year, alongside a package of revenue measures. That package includes new plastic and sugar levies, higher alcohol and tobacco taxes, a tougher fight against tax crime, and a change to how cryptocurrencies are taxed.

Why the Crypto Tax Exemption Is Under Pressure

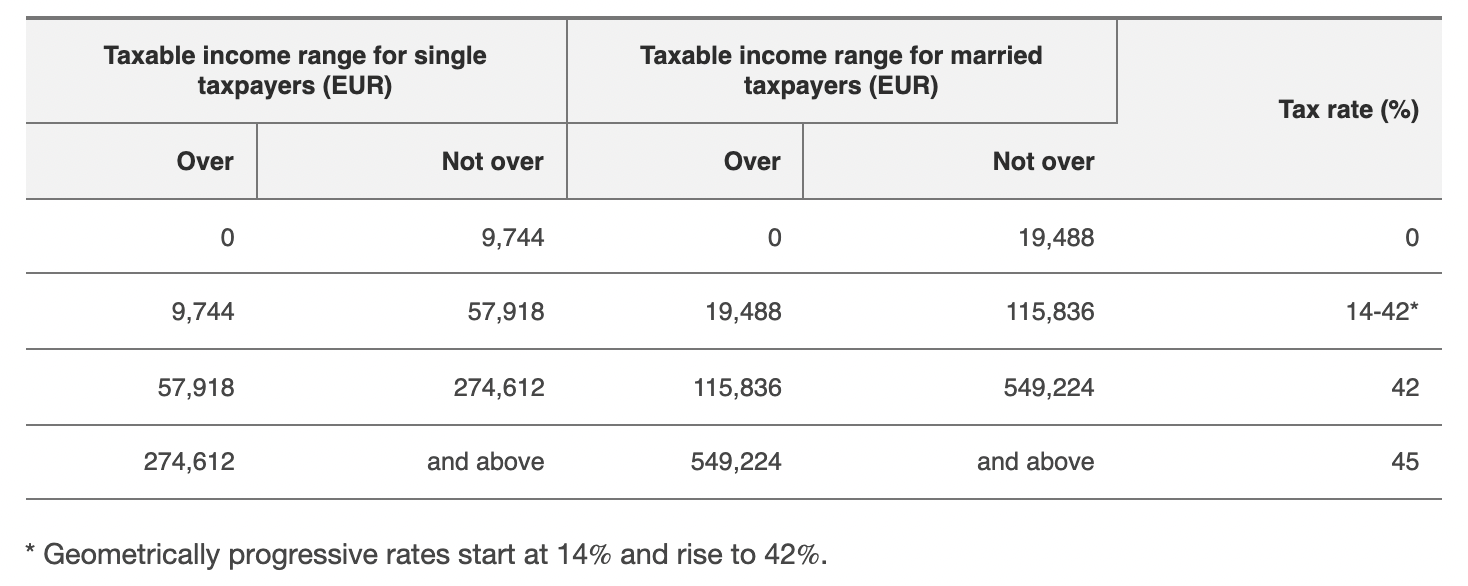

German law treats crypto as a private asset under Section 23 of the Income Tax Act. Gains become tax-free once coins have been held for more than 12 months. Sales within a year face personal income tax rates of up to 45%, while total annual gains below €1,000 stay untaxed.

Calls to scrap the rule have grown louder since late 2025.

“in future, capital gains should be taxed uniformly regardless of the holding period,” The SPD’s Seeheimer Kreis demanded in a position paper, cited by the Bitcoin Bundesverband.

Industry voices pushed back hard. Bundesverband board member Matthias Steger warned that taxing every disposal would turn each everyday payment into a tax event and push firms to friendlier countries such as Portugal.

Parliament has resisted similar moves before. In May 2026, the Bundestag Finance Committee rejected a comparable bid by the Green Party to abolish the exemption.

A Signal for the Rest of the EU

Germany is not the only EU country with such a rule, but it is close. Portugal is the sole other member state that fully exempts crypto gains after a one-year holding period. Austria, by contrast, scrapped its holding period in 2022 and now taxes new holdings at a flat 27.5%.

The stakes reach beyond national borders. As the EU’s largest economy and its leader in MiCA license approvals, Germany often sets the template that other member states follow.

That influence matters now more than ever. Because one in four European investors has invested in cryptocurrency, and new tax reporting rules under CARF and DAC8 are already in force. If Germany exits the exemption, it could reshape the debate in Brussels and beyond.

Whether the rule survives should become clearer once the Bundestag takes over the draft. A regime that made Germany one of Europe’s friendliest places to hold Bitcoin (BTC) long term now depends on how much revenue lawmakers believe they can raise from it.

The post Germany’s 2027 Budget Targets the Crypto Tax Exemption appeared first on BeInCrypto.

Banks vs crypto over stablecoin yield

Fresh twist in Folarin Balogun row: Belgium allowed to appeal FIFA’s suspension decision before USA World Cup clash – what it means | Football News

Avoid entering in FOMO #bitcoin #cryptocurrency #trading #scalping

No Jackpot Winner as $257 Million Prize Rolls Over to $269 Million Monday Draw

Renter of Home in Anne Heche Crash Denies Settlement With Son

Weekend Open Thread: Staud – Corporette.com

Avoid entering in FOMO #bitcoin #cryptocurrency #trading #scalping

Have a Billionare Mindset! She a Night Life Financial Literacy Coach and Dancer. Match her hustle!

money making process lets see whts the fact of money ! #money #viral #shorts

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: High Hopes

-

Politics3 days ago

Politics3 days agoThe House | “Reframing the debate from a binary discussion of winners and losers”: Yuan Yang reviews ‘We Are Not Machines’

-

Crypto World6 days ago

Crypto World6 days agoStrategy authorizes up to $1.25B in Bitcoin sales under new capital plan

-

News Videos6 days ago

News Videos6 days agoHow to Build INSANE Live Financial Dashboards With Claude

-

Tech6 days ago

Tech6 days agoAnonymous researcher drops 0-day ‘exploitarium’ repo

-

Business6 days ago

Business6 days agoAustralia treasurer says alleged access of prime minister’s bank data ’incredibly concerning’

-

NewsBeat1 day ago

NewsBeat1 day agoTaylor Swift and Travis Kelce wedding staffer hilariously struggles to keep her cool while checking in megastars

-

Crypto World5 days ago

Airdrop Registration Becomes Key Focus For Remittix As RTX Launch Updates Approach

-

Sports5 days ago

Sports5 days agoBroncos roster: OL Ben Powers (No. 74) entering final year of contract

-

Business7 days ago

Business7 days agoThe AI boom won’t burst all at once. It will pop in ‘rolling bubbles’: Macquarie

-

Crypto World4 days ago

Crypto World4 days agoBinance stock trading tops $1B in first month after launch

-

NewsBeat6 days ago

NewsBeat6 days agoPresenter Caroline Flack’s brother Paul Flack dies aged 55

-

Crypto World4 days ago

Crypto World4 days agoAlibaba-affiliate Ant Group enters the humanoid robot market with 12 deals

-

NewsBeat4 days ago

NewsBeat4 days agoNew exhibition reflects five decades of movement between island of Ireland and GB

-

Crypto World23 hours ago

Crypto World23 hours agoSouth Africa proposes crypto tax guidance under existing rules

-

Crypto World3 days ago

Crypto World3 days agoStandard Chartered Secures MiCA License as ESMA Adds 37 New Crypto Firms

-

Business5 days ago

Business5 days agoMeta Platforms Stock Jumps 7% Today as Bloomberg Reports Company Plans to Enter the Cloud Business

-

Tech1 day ago

Tech1 day agoLenovo laptops are now shipping with YMTC SSDs, a sign of Chinese NAND entering the mainstream

-

Business3 days ago

Business3 days agoWhat a 10 Percent Drop Means for Buyers, Sellers and Renters

-

Crypto World4 days ago

Crypto World4 days agoBinance Re-Enters Philippines As EU MiCA Rules Restrict Access

You must be logged in to post a comment Login