Crypto World

The AI vs. Crypto Tug-of-War for Capital: Why Today’s Competition Will Become Tomorrow’s Partnership

For nearly a decade, venture capital has chased one transformative technology after another. From mobile apps to cloud computing, from blockchain to generative AI, investment dollars have always followed the next big narrative. Today, that narrative belongs overwhelmingly to artificial intelligence.

In 2025 and into 2026, AI startups have secured some of the largest funding rounds in technology history. Companies developing frontier AI models have attracted tens of billions of dollars in fresh capital, while enterprises racing to integrate AI have become venture capital’s highest priority. In contrast, the once-explosive Web3 funding environment has become quieter, more disciplined, and far more selective.

To many observers, this appears to signal a clear winner. AI is booming, while crypto has faded into the background.

But that conclusion misses the bigger picture.

Rather than signaling the decline of blockchain, today’s capital migration is forcing the crypto industry to evolve beyond speculation. More importantly, it is laying the foundation for a future where AI and blockchain become deeply interconnected technologies rather than competing ones.

The real story isn’t AI versus crypto.

It’s AI because of crypto—and eventually, AI powered by crypto.

The Great Migration of Venture Capital

Venture capital has always been driven by two powerful forces: limited capital and unlimited fear of missing out.

Whenever a new technology demonstrates explosive growth potential, investors naturally redirect capital toward the highest perceived returns. Over the past two years, AI has become that destination.

Large Language Models, autonomous agents, enterprise AI platforms, robotics, and AI infrastructure have collectively absorbed billions that might once have flowed into decentralized finance, NFT ecosystems, or Layer-1 blockchain projects.

This migration has dramatically changed the investment landscape.

Where crypto startups once raised enormous seed rounds based largely on future potential, today’s investors demand measurable adoption, sustainable revenue, and realistic business models. Meanwhile, nearly every startup pitch deck now includes an AI strategy because founders recognize that artificial intelligence has become almost mandatory for attracting early-stage investment.

Crypto has effectively lost its speculative premium.

Instead of existing as a separate asset class driven primarily by narrative, blockchain projects are increasingly evaluated like traditional technology companies.

While painful for many projects, this transition may ultimately be one of the healthiest developments the industry has experienced.

Why AI Is Winning the Short-Term Investment War

The reasons behind AI’s dominance are surprisingly straightforward.

Immediate Utility Beats Long-Term Infrastructure

Artificial intelligence delivers value almost instantly.

A developer can purchase access to an AI API and automate software development within minutes. Businesses can deploy customer service agents overnight. Marketing teams can generate content at unprecedented speed.

The productivity gains are visible immediately.

Blockchain, on the other hand, operates differently.

Its value proposition isn’t instant automation—it’s rebuilding the infrastructure of digital trust.

Creating decentralized financial systems, secure identity networks, tokenized assets, or censorship-resistant infrastructure requires years of engineering, regulatory clarity, and user adoption. These projects solve foundational problems, but they often lack the immediate “wow factor” that attracts short-term investors.

Simply put:

- AI delivers productivity today.

- Blockchain builds infrastructure for tomorrow.

For venture capital seeking rapid returns, today’s value often outweighs tomorrow’s architecture.

The Valuation Gap

AI has also created an increasingly uneven investment environment.

Many venture firms now treat AI integration as a baseline requirement rather than a competitive advantage.

As a result, pure-play Web3 startups frequently compete for a shrinking pool of specialized blockchain investors, while AI startups enjoy broader access to general technology funds.

This has effectively created a two-tier venture ecosystem:

Tier One: AI-native companies attracting premium valuations.

Tier Two: Blockchain companies face significantly higher scrutiny before receiving funding.

The imbalance is substantial—but it is unlikely to remain permanent.

Faster Exit Opportunities

Investors also prefer AI because commercialization appears more predictable.

Enterprise software companies regularly acquire AI startups.

Major cloud providers continuously expand their AI capabilities.

Corporate demand already exists.

Crypto investments follow a different path.

Returns often depend on token launches, network adoption, evolving regulations, and volatile market cycles.

For venture capital firms measured on fund performance, AI currently offers a shorter and more visible path toward liquidity.

Crypto’s Evolution: From Hype to High-Beta Technology

Ironically, losing speculative capital may be exactly what blockchain needed.

The crypto industry has spent years funding countless variations of decentralized exchanges, yield farms, Layer-2 networks, and meme-driven ecosystems.

That era is fading.

Today’s investors increasingly demand fundamentals.

Projects are expected to generate revenue.

Tokenomics must align with sustainable economic models.

Communities alone are no longer enough.

This shift has given rise to what many describe as Tokenomics 2.0.

Modern blockchain projects increasingly emphasize:

- Revenue-linked token value

- Fee-sharing mechanisms

- Token buyback programs

- Treasury sustainability

- Real protocol cash flows

Instead of rewarding speculation, markets are beginning to reward measurable utility.

Crypto is becoming less of an isolated financial experiment and more of a high-beta extension of the broader technology sector—still volatile, but increasingly tied to real economic activity.

The Turning Point: Where AI Meets Blockchain

The assumption that AI and crypto compete for the same future overlooks one fundamental reality:

Artificial intelligence cannot fully scale using traditional financial infrastructure.

As AI systems become autonomous, they begin encountering problems that existing payment systems were never designed to solve.

This is where blockchain re-enters the story.

The Machine-to-Machine Economy

Imagine an autonomous AI agent managing an international supply chain.

It needs to:

- Purchase satellite imagery.

- Rent cloud computing.

- Pay for API requests.

- Buy proprietary datasets.

- Hire another specialized AI agent.

Each transaction may cost fractions of a cent.

Traditional banking struggles with this model.

Credit cards require human identities.

Bank accounts require legal ownership.

International wire transfers take days.

Card networks charge fixed transaction fees that make micropayments economically impossible.

An AI agent cannot simply apply for a corporate credit card.

Nor should it.

Machines need a native digital payment infrastructure.

Blockchain as the Economic Rail for AI

Blockchain networks solve many of these challenges naturally.

Crypto wallets allow software agents to control digital assets independently through cryptographic signatures.

Stablecoins enable programmable global payments without relying on traditional banking hours.

Transactions settle within seconds.

Fees can be measured in fractions of a cent.

This creates entirely new possibilities.

An AI assistant reading premium research could instantly pay a publisher $0.001 for access.

A coding agent could purchase compute power by the second.

Autonomous robots could negotiate and pay one another for services without human intervention.

These tiny machine-to-machine payments are practically impossible using legacy financial systems.

On blockchain, they become routine.

Increasingly, blockchain ecosystems are building this infrastructure precisely through AI-focused development kits, agent frameworks, and stablecoin payment rails. As autonomous software becomes more common, decentralized networks may become the default settlement layer for machine commerce.

From “Vibes” to Value

Another important shift is occurring beneath the surface.

Global regulation is gradually pushing crypto beyond its speculative origins.

Frameworks such as Markets in Crypto-Assets Regulation are establishing clearer rules for digital asset markets, while regulators in the United States continue developing more standardized oversight for crypto businesses.

As legal uncertainty decreases, blockchain projects face increasing pressure to operate like mature financial infrastructure rather than experimental internet communities.

Ironically, AI’s dominance has accelerated this transition.

With speculative capital flowing elsewhere, blockchain builders have been forced to focus on products that solve real-world problems.

The industry has become leaner, more disciplined, and arguably stronger.

Is AI Becoming Overvalued?

History suggests that no investment narrative dominates forever.

Today’s AI market is attracting enormous amounts of capital, producing increasingly expensive funding rounds and premium valuations.

While artificial intelligence undoubtedly represents a transformative technology, concentrated investment can also create valuation risk.

If future funding becomes more selective or AI valuations begin normalizing, investors will naturally search for underpriced sectors with strong long-term fundamentals.

Blockchain infrastructure may become one of the most attractive destinations.

Especially projects enabling:

- AI payments

- Stablecoin infrastructure

- Decentralized identity

- Compute marketplaces

- Agent coordination

- Cross-chain settlement

Rather than competing with AI, these technologies enhance AI’s ability to operate autonomously.

The Future Is Convergence, Not Competition

The narrative that AI and crypto are enemies reflects a short-term investment mindset rather than a long-term technological reality.

Artificial intelligence may become the brain of tomorrow’s digital economy, making decisions, learning continuously, and performing increasingly sophisticated work.

But every brain requires a nervous system.

Blockchain provides that infrastructure.

It supplies programmable ownership, verifiable identity, decentralized coordination, and instant global settlement—the economic rails that autonomous machines will increasingly depend upon.

The future is unlikely to belong exclusively to AI or crypto.

It belongs to the intersection where intelligent agents transact securely, coordinate independently, and exchange value without friction.

Investors abandoning blockchain entirely in pursuit of AI’s latest megadeals may be overlooking the next major opportunity.

The smartest capital rarely chases yesterday’s headline.

It quietly positions itself where two transformative technologies begin to converge.

And that convergence—where autonomous AI meets decentralized economic infrastructure—could become the foundation of the next multi-trillion-dollar digital economy.

REQUEST AN ARTICLE

The UK Financial Conduct Authority (FCA) has published a wide-ranging blueprint for how retail financial services should be regulated as “agentic” AI pushes firms toward near-total automation. In its landmark report, “AI and the future of retail financial services”, FCA executive director Sheldon Mills argues that the industry is moving away from human-led, episodic decisions and toward continuous services delegated to AI systems.

The review, issued as regulators grapple with the speed of generative AI deployment and growing experimentation with blockchain-based finance, frames settlement infrastructure as a key constraint. It suggests that advanced automation will require financial plumbing capable of processing transactions instantly and reliably—something the FCA implicitly contrasts with slower legacy settlement processes.

Key takeaways

- The FCA says retail financial services are shifting from human-led decisions to AI-enabled, continuous and delegated activity.

- The report calls for regulatory work that supports “agentic finance,” including trusted agent protocols.

- It highlights governance and accountability challenges that emerge when AI systems operate autonomously on consumers’ behalf.

- The FCA’s research indicates consumer openness to AI-assisted choices is already material, with 20% of UK adults reportedly willing to let AI make autonomous financial decisions.

An “autonomy spectrum” for retail finance

At the center of the Mills Review is what the FCA describes as an “autonomy spectrum,” reflecting how AI capabilities are evolving from recommending actions to executing them. Mills argues that as models become more independent, humans may increasingly shift into a more passive role—sometimes acting only as observers while AI continuously manages capital.

In the report’s framing, this evolution is not merely about better predictions. Instead, it is about delegation: systems that can be empowered, trained, and authorized to act. That creates a regulatory problem that is different in kind from earlier AI use cases, because the risk no longer rests only with advice or decision support. It rests with operational authority.

The FCA also links the acceleration of this shift to the pace of generative AI. The review notes that more than 20 “frontier models” have been released since late 2025, suggesting firms are moving faster than prior regulatory timetables.

Why settlement speed becomes a regulatory issue

The report connects autonomy to execution. The FCA says that for AI agents to carry out multi-layer transaction strategies smoothly, they require programmable and near-instant settlement mechanisms. By contrast, traditional processes with multi-day latency are described as an operational bottleneck for fully automated finance.

In the FCA’s discussion, systemic stablecoins and tokenized assets are positioned as a potential fit for this need. Because these instruments can be natively issued and transferred on programmable ledger networks, they may enable atomic settlement—where transactions are coordinated in a way that reduces friction and dependency on human clearance.

Importantly, the review does not claim that tokenized settlement is automatically “the answer.” Rather, it highlights a structural challenge: automation at the agent level will stress-test existing financial infrastructure that was built for human workflows and periodic actions.

Accountability, governance, and the “human on the hook” principle

Automation at retail scale also raises questions about who is legally responsible when agents act in unexpected ways. The Mills Review warns that allowing autonomous systems to make and execute decisions introduces severe corporate governance risks, particularly around legal accountability.

The FCA notes industry anxiety about the ambiguity of intention—whether it is possible to reliably distinguish human intent from algorithmic behavior once systems can act continuously and at speed. The report references this concern through industry commentary, including the view that the sector may eventually need something akin to a “Turing test” to separate human intent from machine-driven actions.

In separate remarks, Mills told the Financial Times ahead of the report’s release that accountability must remain anchored to humans. According to his comments, “You need a human on the hook for what they’re doing,” reflecting the FCA’s broader emphasis that operational delegation must not eliminate responsibility.

The Payments Association CEO Emma Banymandhub echoed the governance theme in a statement, saying the FCA’s review “reinforces that firms should treat agentic AI as an accountability and governance issue now,” while maintaining that governance, clear accountability, and consumer trust will determine whether AI’s potential can be realized responsibly.

Recommendations for “agentic finance” and the FCA’s AI capabilities

In its 147-page review, the FCA sets out seven recommendations it says should inform how it responds to the next phase of AI in retail financial services. Among them is an explicit push toward enabling “the foundations for agentic finance”—work intended to support trusted agent protocols that underpin how agentic AI can be used safely.

The report also flags the FCA’s internal capacity, recommending that it consider scaling up its AI Lab to support AI models and system innovation in financial services. The underlying message is that regulatory capability has to evolve alongside the technology it is designed to oversee.

That aligns with the FCA’s earlier steps. The regulator launched the review in January to examine the implications of advanced AI for consumers, retail financial markets, and regulatory oversight (as noted in the FCA’s January press materials).

Still, the report’s most practical impact may be indirect: by framing agentic AI as a continuous, delegated operating model, it implicitly increases pressure on firms to rethink not just their AI tools, but their end-to-end control framework—from authorization and monitoring to dispute handling and accountability trails.

What to watch next

As the FCA turns its recommendations into concrete regulatory expectations, the key uncertainty is how it will balance innovation with enforcement—especially in cases where AI agents execute transactions at speed. Investors and builders should watch for clearer standards on governance, accountability, and how (or whether) tokenized settlement infrastructure fits into the FCA’s definition of safe, trusted automation.

President Donald Trump said Bitcoin (BTC) could eventually be added to Trump Accounts, the new tax-advantaged accounts for children. Asked directly on Monday whether the program could include the asset, he replied that something could happen.

Trump made the comments at an event tied to the program’s rollout, days after the accounts opened to families nationwide. His answer immediately fueled fresh speculation about crypto’s role in government-backed savings.

Could Bitcoin Join Trump Accounts?

Trump Accounts launched on July 4 under the One Big Beautiful Bill Act. Children born between 2025 and 2028 receive a one-time $1,000 Treasury seed deposit. Families can also contribute up to $5,000 per year until the beneficiary turns 18.

The Treasury tapped Robinhood and BNY to run the program’s app and account infrastructure. However, every contribution currently sits in one default fund, the State Street SPDR Portfolio S&P 500 ETF (SPYM).

The Treasury has approved just four other index ETFs, and even fund-switching is not live yet.

The deeper obstacle sits in the statute itself, not agency guidance. Congress limited qualifying investments to US equity index funds charging under 0.1% in fees.

The law lets the Treasury tighten those rules, not expand them. Therefore, Bitcoin would likely need new legislation before reaching any child’s portfolio.

Trump nonetheless kept the door open when pressed on the question.

“Something could happen,” he said.

Follow us on X to get the latest news as it happens

Trump Doubles Down on Pro-Crypto Agenda

The president tied his support to competition with China rather than market conviction.

“I’ve become a big crypto guy only for one reason: if we don’t have it China is going to have it.”

Trump also said he watched the industry grow into a major market. He added that heavy capital inflows convinced him Bitcoin has plenty of life left.

His enthusiasm is not disinterested. Trump’s latest financial disclosure reported more than $1 billion in 2025 income from family crypto ventures.

Last week, he questioned Bitcoin’s tax treatment while defending those earnings.

Meanwhile, the administration has weighed letting billionaires donate appreciated stock to the accounts in exchange for tax breaks.

Bitcoin showed little immediate reaction to the comments, reclaiming the $62,000 threshold after losing it earlier in the day on MicroStrategy’s account.

What Trump’s Track Record Suggests

Trump’s history shows he delivers on crypto pledges, though never overnight. He promised in Nashville in July 2024 to keep the government’s seized Bitcoin.

The Strategic Bitcoin Reserve executive order followed on March 6, 2025, roughly seven months later.

Notably, he avoided overpromising then. The reserve holds about 200,000 seized coins and allows only budget-neutral purchases, matching the modest pledge he made on stage.

The 401(k) push offers a closer parallel. Trump signed an executive order in August 2025 to open retirement plans to alternative assets.

However, the Labor Department only proposed its rule in March 2026, and it remains unfinalized 11 months on.

Measured against those timelines, Bitcoin in children’s accounts looks like a 2027 story at the earliest. It may also demand a congressional fight rather than a regulatory one.

Monday’s answer committed Trump to nothing, which may be exactly the point.

The post POTUS Says Bitcoin Could Join Trump Accounts, Calls Himself a ‘Big Crypto Guy’ appeared first on BeInCrypto.

The United Kingdom’s Financial Conduct Authority (FCA) has issued a broad regulatory blueprint for retail financial services, warning that retail financial services are hurtling toward total automation driven by autonomous “agentic AI.”

The landmark report, “AI and the future of retail financial services,” spearheaded by executive director Sheldon Mills, details a structural shift away from periodic, human-led decisions toward continuous, automated financial services that could increasingly rely on programmable financial infrastructure.

“The central shift is from human-led, episodic financial activity towards services that are AI-enabled, continuous and delegated,” Mills wrote. In January, the FCA launched a review into the implications of advanced AI on consumers, retail financial markets and regulators.

The 147-page report comes at an inflection point where generative AI meets institutional crypto adoption. As financial systems transition to autonomous portfolio and cash management, legacy fiat banking rails are seen as structurally incapable of matching machine transaction speeds. This positions systemic stablecoins and tokenized bank deposits as potential settlement infrastructure for AI-driven financial services.

It outlines seven recommendations for the FCA to consider, including enabling “the foundations for agentic finance,” which would support the development of trusted agent protocols that would underpin use of agentic AI and “scaling up the FCA’s AI Lab to support AI models and system innovation in financial services.”

Related: UK plans payments rule changes for stablecoins, tokenized deposits

FCA envisions agents on “autonomy spectrum”

The Mills Report suggests that the catalyst is the rapid evolution of AI from predictive models into independent agents operating on an “autonomy spectrum.” At the far end of this spectrum, humans act as mere “observers” while AI continuously manages capital.

Screenshot of table header that sets out how FCA sees operator activities may change as they move across the AI autonomy spectrum. Source: Financial Conduct Authority.

The acceleration of this shift has outpaced prior regulatory timelines, with more than 20 frontier models released since late 2025 alone.

“Firms are moving from systems that recommend actions to systems empowered and trained to take them, and consumers will soon gain agents that act on their behalf,” Mills said in the report’s foreword. FCA research shows that 20% of UK adults are already open to letting AI make autonomous financial choices.

For these AI agents to execute multi-layered transaction strategies seamlessly, they require programmable, instantaneous settlement mechanisms. Traditional multi-day settlement latency remains an operational bottleneck. Because systemic stablecoins and tokenized assets live natively on programmable ledger networks, they provide the friction-free, atomic settlement needed for automated protocols to move capital instantly without human clearance.

However, this automation introduces severe corporate governance risks regarding legal accountability.

The review highlights growing industry anxiety over this ambiguity, noting that one CEO observed that the financial sector may eventually require a “Turing test” to accurately distinguish between human intent and autonomous algorithmic behavior in the market.

“The FCA’s Mills Review reinforces that firms should treat agentic AI as an accountability and governance issue now, while providing greater confidence to innovate responsibly as AI adoption accelerates,” Emma Banymandhub, CEO of The Payments Association, said in a statement. “AI has enormous potential for financial services, but realising that potential will depend on strong governance, clear accountability and maintaining consumer trust.”

Mills, who is leaving after eight years at the FCA, told The Financial Times ahead of the report’s release that managers would still need to be accountable for the actions of their AI models. “You need a human on the hook for what they’re doing,” he said.

Magazine: AI is banking the unbanked in Africa… faster than crypto

Strategy has completed its second BTC sale in just over a month, announced the firm’s co-founder and former CEO, Michael Saylor.

The company has disposed of 3,588 BTC for $216 million to fund dividends on its Digital Credit securities. Its total holdings have dropped to 843,775 BTC, while its USD reserve remains at $2.55 billion.

Strategy has sold 3,588 $BTC for $216 million to fund dividends on our Digital Credit securities. As of 7/5/2026, we hodl ₿843,775 in our BTC Reserves and $2.55 billion in our USD Reserves. https://t.co/Cssgz29Psj

— Michael Saylor (@saylor) July 6, 2026

More BTC Sales

Recall that the NASDAQ-listed BTC accumulator announced in late May that it had sold a minor portion of its crypto fortune (32 units) to support preferred stock distributions.

Although the actual sale was quite negligible, the magnitude was felt for weeks. Bitcoin’s price nosedived in the week after the move became public, and kept plunging during June to under $58,000 at the end of it.

Strategy’s STRC plummeted from its par price of $100 to under $75 at one point, prompting numerous analysts to warn that the worst is yet to come. Some even speculated that the firm would have to sell over 50,000 BTC in the following couple of years.

Meanwhile, CryptoQuant urged the firm to halt its BTC purchases and focus on rebuilding its USD reserve, which appears to be unfolding now.

Saylor Said So

In contrast to today’s sale, the company announced a major restructuring last week. Instead of making continuous bitcoin-only buys, it launched the Digital Credit Capital Framework to enhance liquidity and long-term BTC exposure.

It increased its USD reserves to the aforementioned $2.55 billion, covering 17.4 months of dividend payments. However, it warned that it could sell up to $1.25 billion in BTC to expand that dividend payment period to over 25 months.

Before the latest and third-ever BTC sale, Saylor republished a recent post of his regarding the state of bitcoin and its future development. He believes the cryptocurrency and the blockchain behind it will evolve by “changing less at the protocol layer and mattering more everywhere else.”

He added that the base layer will eventually harden, the capital markets will deepen, and digital credit will expand, as the “world will build on Bitcoin.”

How Will BTC Respond Now?

All eyes are now on the cryptocurrency’s price, given what transpired after the previous Strategy sale. The asset has recovered some ground and tapped $64,000 earlier today, where it was stopped. However, it has dropped by over two grand since then, as a major portion of those losses came after Strategy’s announcement.

The post Saylor’s Strategy Sells More Bitcoin: Is Another BTC Crash Coming? appeared first on CryptoPotato.

Ethereum co-founder Vitalik Buterin has unveiled a multi-year roadmap that places native privacy, quantum resistance, and protocol simplification at the center of Ethereum’s next major upgrade, describing it as the network’s largest transformation since The Merge.

Summary

- Vitalik Buterin has proposed Ethereum’s biggest protocol overhaul since The Merge with a multi-year roadmap.

- The plan prioritizes native privacy, quantum-resistant cryptography, and more efficient transaction verification.

- The roadmap remains a draft, with the Hegotá fork expected to be the final upgrade before the Lean Ethereum era.

According to a roadmap published on Strawmap.org and shared by Buterin on X over July 6, the proposed changes are expected to be introduced over the next three to four years following discussions among Ethereum researchers in Berlin.

The document outlines coordinated upgrades spanning nearly every layer of the network and presents what Buterin describes as Ethereum’s third major evolution after its transition to proof-of-stake in 2022.

Native privacy becomes a core protocol feature

Instead of leaving privacy to applications built on Ethereum, the roadmap proposes making it a built-in property of the protocol itself. The document evaluates key components, including Frames, the transaction mempool, and future state designs, according to whether they can support intermediary-free, quantum-safe privacy while keeping computational costs low.

Building on ideas first outlined in May 2026, Buterin’s latest proposal expands an earlier privacy roadmap into a network-wide redesign. What previously focused on incremental improvements has now developed into a long-term architectural plan covering the protocol’s core infrastructure.

Among the document’s strongest statements is Buterin’s observation that “quantum safety has shifted up a LOT in priority.” The roadmap identifies work on quantum-safe blob designs, which support Ethereum’s rollup-based scaling model, as an urgent priority.

According to the proposal, several cryptographic systems currently used by Ethereum, including BLS signatures, KZG commitments, and ECDSA, would eventually be replaced with post-quantum alternatives. The direction aligns with the post-quantum cryptography standards finalized by the U.S. National Institute of Standards and Technology in 2024.

Protocol redesign targets faster verification and smaller overhead

Alongside cryptographic upgrades, the roadmap introduces changes intended to simplify how Ethereum validates transactions. Rather than requiring every node to re-execute every transaction, the proposal recommends recursive STARK-based verification, where one prover performs the intensive computation while the rest of the network verifies a compact cryptographic proof.

The proposal also continues work first discussed by the Ethereum Foundation earlier this year. In February 2026, the Foundation released an initial strawmap examining quantum threats facing Ethereum, while Buterin separately detailed the network’s quantum security risks. The latest roadmap develops those earlier discussions into a more detailed implementation strategy.

Meanwhile, the technical proposal arrives as the Ethereum Foundation continues internal restructuring. The organization has reduced its workforce by roughly 20%, eliminating about 54 positions, while also cutting its budget by a targeted 40%. Recent departures have included protocol contributors Hsiao-Wei Wang, Tomasz Stańczak, Tim Beiko, and Barnabé Monnot.

Community discussion on X has largely focused on the roadmap’s technical detail rather than broad ambitions. Several participants noted that the draft identifies specific signature schemes, cryptographic replacements, and state-size objectives instead of relying on high-level goals.

For now, the roadmap remains a working draft rather than a finalized implementation schedule. According to the document, the upcoming Hegotá fork is expected to be the final major network upgrade before Ethereum enters what Buterin describes as the Lean Ethereum era, where privacy, scalability, and quantum resistance are treated as core protocol requirements rather than optional additions.

Ethereum is attempting to recover after defending the $1.5K region once more, but the broader trend remains under pressure. The price is now approaching a major confluence resistance area that could determine whether this rebound develops into a larger trend reversal or remains another relief rally within the prevailing downtrend.

Ethereum Price Analysis: The Daily Chart

The daily chart continues to reflect a bearish market structure. ETH remains below the descending long-term trendline, as well as the 100-day and 200-day moving averages, all of which continue to slope lower. This alignment suggests sellers still maintain control from a broader perspective.

Following the sharp decline into the $1.5K support zone, buyers managed to trigger a recovery toward the $1.8K resistance area. This level coincides with the previous horizontal support that has now turned into resistance and sits just beneath the descending channel trendline, creating a significant supply zone.

A successful daily close above the trendline and the $1.8K region would be the first meaningful technical improvement and could expose the next resistance around $2K to $2.2K, where another major supply zone and moving average cluster await.

Failure to reclaim the current resistance would likely reinforce the broader bearish structure and increase the probability of another move toward the $1.5K support. Losing that area would pave the way toward the channel’s lower boundary below $1.2K.

ETH/USDT 4-Hour Chart

On the 4-hour timeframe, Ethereum has produced a stronger short-term recovery after defending the $1.5K demand zone for a second time. The rebound has carried the price back toward the upper boundary of the pattern that has entrapped the price since early June.

ETH is now testing the $1.75K to $1.8K resistance while simultaneously confronting the descending trendline. This makes the current area particularly important for short-term direction.

A confirmed breakout above both the trendline and horizontal resistance would invalidate the sequence of lower highs and could accelerate buying toward the $larger $2K to $2.2K supply zone also visible on the daily timeframe. On the other hand, rejection from this region would preserve the existing bearish structure. In that case, the first support remains around $1.7K, followed by the $1.6K area, while the key demand zone continues to sit near $1.5K.

Momentum has also improved considerably during the latest advance, with the RSI climbing toward overbought territory. While this reflects strengthening buying pressure, it also suggests that bulls may need a period of consolidation before attempting a decisive breakout.

On-Chain Analysis

The exchange reserve chart presents one of the more constructive long-term signals for Ethereum. Exchange balances have fallen significantly from above 21M ETH to roughly 15.5M ETH, marking a persistent multi-year decline in the amount of ETH held on centralized exchanges.

This trend generally indicates continued coin withdrawals into self-custody or long-term storage, reducing the immediately available supply for sale. Such behavior often reflects improving investor conviction and tends to provide a favorable backdrop during periods of sustained demand.

Despite Ethereum’s prolonged price correction from the 2025 highs, exchange reserves have continued to decline rather than rise, suggesting that long-term holders have not been aggressively distributing their holdings into weakness.

While on-chain data alone does not guarantee an immediate rally, the persistent reduction in exchange reserves supports the view that selling pressure from spot holders remains relatively limited. If ETH can reclaim the major technical resistance around $2K and attract renewed demand, this tightening exchange supply could become an important tailwind for a stronger medium-term recovery.

The post Ethereum Price Prediction: Is $1.5K or $2K Next for ETH? appeared first on CryptoPotato.

Crypto World

Ethereum (ETH) developers embrace Vitalik Buterin’s long-term vision but urge quicker execution

Ben-Sasson also welcomed Buterin’s decision to make privacy and quantum-resistant cryptography top priorities.

“Quantum safety—excellent,” he wrote on X. “Glad to see this as a high priority.”

But he argued Ethereum shouldn’t wait three to four years to get there.

“‘3-4 years’ as the timeline is way too long,” Ben-Sasson said. “Especially for quantum readiness.”

Former Ethereum Foundation researcher Dankrad Feist struck a similar tone. Calling the roadmap’s vision “really cool,” Feist said on X that features like near-instant transaction finality and dramatically higher throughput could transform the network.

His biggest concern, however, was speed. “But 3-4 years is very slow,” Feist wrote. “I think we should be ambitious and get it done in ~1 year.”

Feist even suggested recent advances in AI tools, including large language models, could help accelerate development.

Not every discussion centered on timing. Some researchers dug into the roadmap’s technical details.

Ben-Sasson questioned one of Buterin’s proposals to introduce new types of blockchain “state,” essentially the data Ethereum stores about accounts, balances and smart contracts.

“New kinds of state: what does that mean? Who is affected by it?” he asked, calling for more explanation.

Meanwhile, Ethereum Foundation researcher Barnabé Monnot focused on how the roadmap had changed from an earlier version released in February.

You think you research crypto brands on Forbes or CoinDesk. You don’t. You ask ChatGPT. And ChatGPT already picked its favorites.

The Gatekeeper Nobody Noticed

For twenty years, if you wanted to know whether a financial brand was trustworthy, you went to established media. Forbes. The Wall Street Journal. Bloomberg. CoinDesk for crypto specifically.

Those outlets shaped perception. Their coverage decided who was credible and who wasn’t. A positive Forbes profile moved markets. A negative Bloomberg investigation destroyed reputations.

That era just ended.

On July 2, 2026, PR firm 5W released The Crypto Trust Index, research scoring how ChatGPT, Claude, Perplexity, Gemini, and Google AI answer when a first-time buyer asks whether a crypto brand is safe.

The finding: AI engines do not stay neutral. They answer with a verdict, recommend, hedge, or warn.

There is no neutral tier.

The gatekeeper didn’t disappear. It just moved. And almost nobody noticed.

What The Research Actually Found

5W ran 60+ first-time-buyer prompts across six question types, five times per engine, across 25 crypto exchanges and brands.

The results are unambiguous:

Coinbase Trust Score 94. The default first-time-buyer recommendation across all five AI engines.

Kraken 87. Cited for proof-of-reserves and clean operating record.

Fidelity Crypto 82. Inherited trust from a traditional-finance brand the engines extend without re-litigation.

Gemini 77. Recommended on US regulatory posture.

And then there’s everyone else. Hedged. Warned about. Or simply absent from AI recommendations entirely.

If your brand doesn’t appear in an AI recommendation, you don’t exist for the majority of first-time buyers. Not because you’re not listed on Google. Because the AI didn’t mention you.

Why This Changes Everything About Crypto Marketing

Traditional crypto marketing operated on a simple premise: get coverage, build awareness, convert buyers.

The funnel looked like this:

- User hears about crypto

- User Googles crypto brand

- User reads reviews on media sites

- User decides to buy or not

AI just collapsed that funnel into a single step:

- User asks ChatGPT “is [brand] safe?”

- ChatGPT answers with a verdict

- User acts on the verdict

The media layer, the reviews, the coverage, the PR campaigns, still exists. But it now feeds AI training data rather than reaching users directly.

Your brand’s reputation isn’t built on the Forbes article anymore. It’s built on what Forbes said that the AI learned from.

And you can’t see what the AI learned. You can only see the verdict it delivers.

The Uncomfortable Finding AI Inherited Traditional Finance Bias

One of the most significant findings from the 5W research: brokerage-backed crypto brands inherit trust the engines extend on day one.

Fidelity Crypto scored 82, not because Fidelity has been in crypto longer or built better technology than native crypto companies. But because Fidelity has decades of traditional finance credibility, and AI engines absorbed that credibility without question.

This is a structural bias baked into how AI systems were trained. They learned from the same financial media, regulatory filings, and institutional coverage that already favored traditional finance brands.

So when a first-time buyer asks ChatGPT whether Fidelity Crypto is safe, ChatGPT answers with the confidence that comes from decades of institutional reputation, even if Fidelity’s crypto product launched last year.

Meanwhile, a crypto-native brand that’s been operating for ten years, has proof-of-reserves, and has never been hacked starts from zero in AI trust scores if it doesn’t have extensive mainstream media coverage.

The playing field isn’t level. The AI decided who starts with an advantage.

The New Rules Of Crypto Marketing

The 5W research identified exactly what moves AI trust scores:

What works:

- Proof-of-reserves (auditable, citable, verifiable)

- Clean regulatory record (no enforcement actions, no major incidents)

- Traditional finance association (legacy credibility transfers automatically)

- Mainstream media coverage (feeds the training data that shapes AI responses)

What doesn’t work:

- Marketing campaigns (AI doesn’t factor in ad spend)

- Social media presence (follower counts don’t move trust scores)

- Community building (Discord size is invisible to AI trust evaluation)

- Sponsored content (AI learns to discount promotional material)

This is a fundamental inversion of how crypto brands have marketed themselves for the last decade.

The entire playbook, build community, drive social engagement, get influencer coverage, sponsor events, doesn’t register in AI trust evaluations.

A clean audit moves your score. A viral tweet doesn’t.

Why “The On-Ramp Moved” Is The Most Important Sentence In Crypto Marketing Right Now

5W’s research includes one line that should be required reading for every crypto marketer:

“The on-ramp moved. The first trust decision now happens inside an AI answer, before a buyer reaches any site.”

Let that land.

Before a first-time buyer visits your website, reads your whitepaper, checks your social proof, or sees your ad, they’ve already formed an opinion based on what an AI told them.

If the AI recommended you, they arrive pre-convinced.

If the AI hedged on you, they arrive skeptical.

If the AI warned about you, they don’t arrive at all.

Your entire marketing infrastructure, your website, your content, your community, your influencer partnerships, is operating on users who’ve already been filtered by an AI they didn’t realize was making a judgment call.

The Winners And Losers This Creates

Established brands with clean records win.

Coinbase at 94 doesn’t need to convince AI engines. Years of regulatory engagement, mainstream media coverage, and transparent operations built a reputation that AI absorbed and now distributes to every first-time buyer who asks.

Traditional finance entrants win immediately.

Fidelity at 82 on day one of its crypto product. The institutional credibility transfers. No crypto track record required.

Crypto-native brands without mainstream coverage lose.

If your brand built its reputation on crypto Twitter, crypto influencer networks, and community Discord servers, none of that feeds AI training data in a way that builds trust scores. You’re invisible to the new gatekeeper.

Brands with any regulatory history lose badly.

The AI doesn’t forget. A 2019 enforcement action, a 2021 hack, a 2023 regulatory warning, all of it is in the training data. All of it surfaces when a first-time buyer asks if you’re safe.

The AI doesn’t distinguish between “resolved issue from five years ago” and “current problem.” It just knows it exists.

What This Means For Crypto’s Future

The trust infrastructure of crypto just got centralized, not by a government, not by a regulator, but by AI systems trained on data those systems chose.

This is ironic in the deepest possible way. Crypto was supposed to be decentralized. Trustless. Permissionless. No gatekeeper deciding who’s legitimate.

But now five AI engines, ChatGPT, Claude, Perplexity, Gemini, Google AI, are making trust judgments about 25 crypto brands, and their answers are shaping where billions of dollars flow.

That’s not decentralization. That’s a new kind of centralization that’s harder to see because it’s embedded in a conversational interface rather than a regulatory filing.

And unlike a regulator, you can’t appeal an AI trust score.

The Marketing Question Nobody’s Asking Yet

If AI engines are the new gatekeepers of crypto trust, and those engines are trained on data that favors traditional finance brands and mainstream media coverage, what happens to the next wave of crypto innovation?

A genuinely novel DeFi protocol, a new blockchain architecture, an innovative crypto product that launches without institutional backing or mainstream media coverage, starts from zero in AI trust scores.

Not because it’s less safe. Not because it’s less innovative. But because the AI hasn’t seen enough reliable coverage of it to form a verdict.

The early-stage crypto project that needs trust the most, to attract first-time users, to build legitimacy, to grow, is the one that AI trust evaluation helps the least.

That creates a structural disadvantage for innovation and a structural advantage for incumbents.

Which is exactly what crypto was supposed to fix in finance.

What Comes Next

Every crypto brand needs to answer a new strategic question: What does ChatGPT say about us when a first-time buyer asks if we’re safe?

Not “what does our marketing say.” Not “what do our users say on Twitter.” What does the AI say?

Because that’s the first answer the next billion users are going to get.

And the brands that understand this shift, that start building for AI trust evaluation rather than traditional marketing metrics, will have an enormous advantage over the next three years.

The gatekeeper moved. Most crypto brands are still marketing to the old one.

Ask ChatGPT right now if your favorite crypto brand is safe. Then tell me what it said, because that answer is shaping more buying decisions than any ad campaign you’ve ever seen.

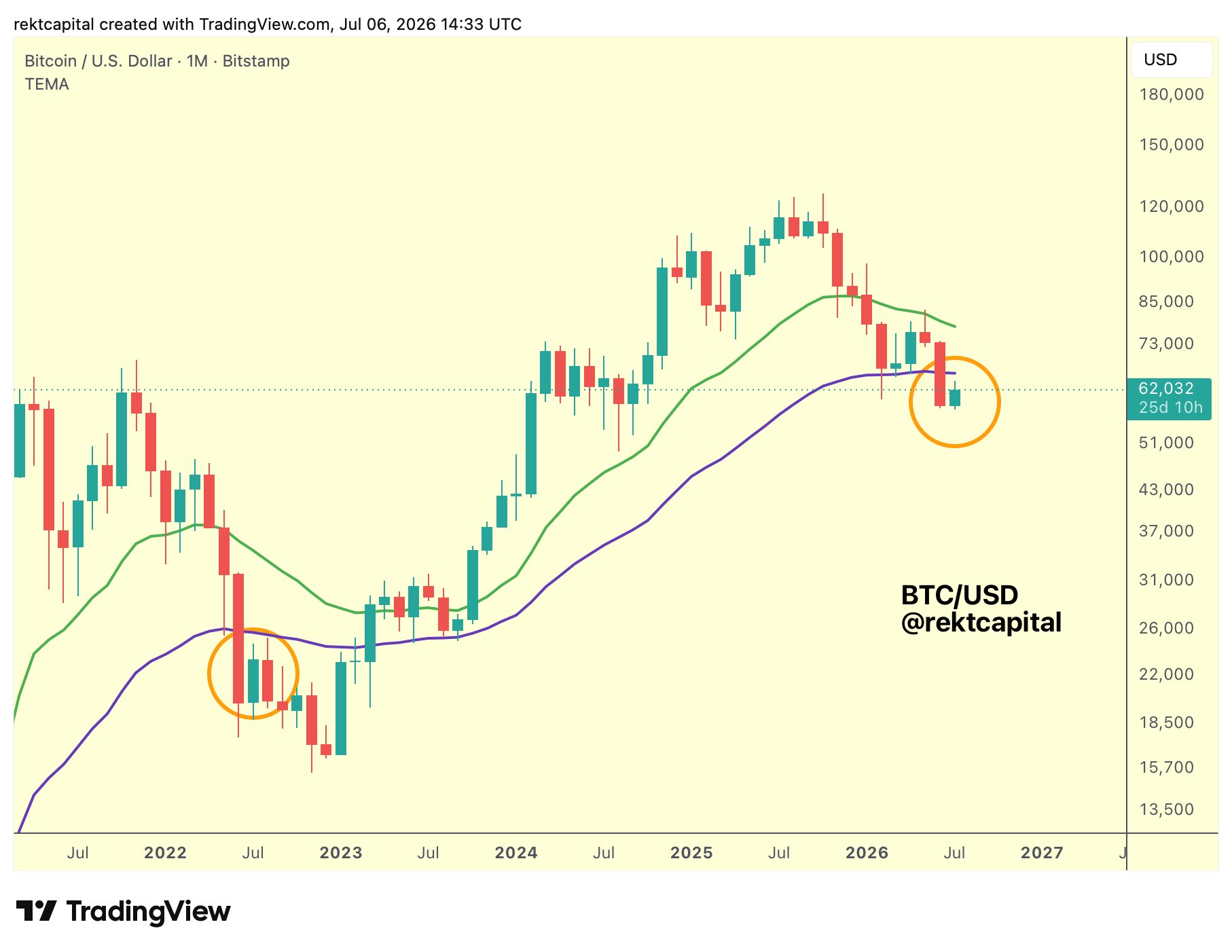

Bitcoin (BTC) saw flash volatility into Monday’s Wall Street open as markets reacted to tech company Strategy’s new BTC sales.

Key points:

- Bitcoin reacts sharply to news that Strategy had sold nearly 3,600 BTC.

- A rebound during the US trading session failed to recoup more than half of the day’s losses.

- Strategy may reveal a compensatory BTC buy, an analyst suggests.

Bitcoin erases holiday gains on Strategy sale

Data from TradingView showed BTC/USD dropping to near $61,000, sparking daily losses of more than 4%.

BTC/USD four-hour chart. Source: Cointelegraph/TradingView

A rebound at the start of the US session pushed the price higher before settling around the $62,000 mark at the time of writing.

Strategy revealed that it sold 3,588 BTC through July 5 to fund preferred stock dividend payments and replenish cash reserves.

Commenting on the latest BTC price moves, X commentator Exitpump suggested that the Strategy news was the catalyst for an already weakening market.

“Bearish signs were there, posted about it yesterday, news about Saylor selling just triggered more dump,” they wrote.

“Funding is still pretty positive. That was it i guess. Short term bounce from 61.2k and then more dump imo.”

Exitpump referred to funding rates across exchanges, with a post on Sunday eyeing a buyer entity using a time-weighted average price (TWAP) method to add exposure.

“Once the TWAP buyer backs off, I wouldn’t be surprised to see a fast flush lower,” they wrote, anticipating a price ceiling at $64,000.

BTC chart with funding rate data. Source: Exitpump/X

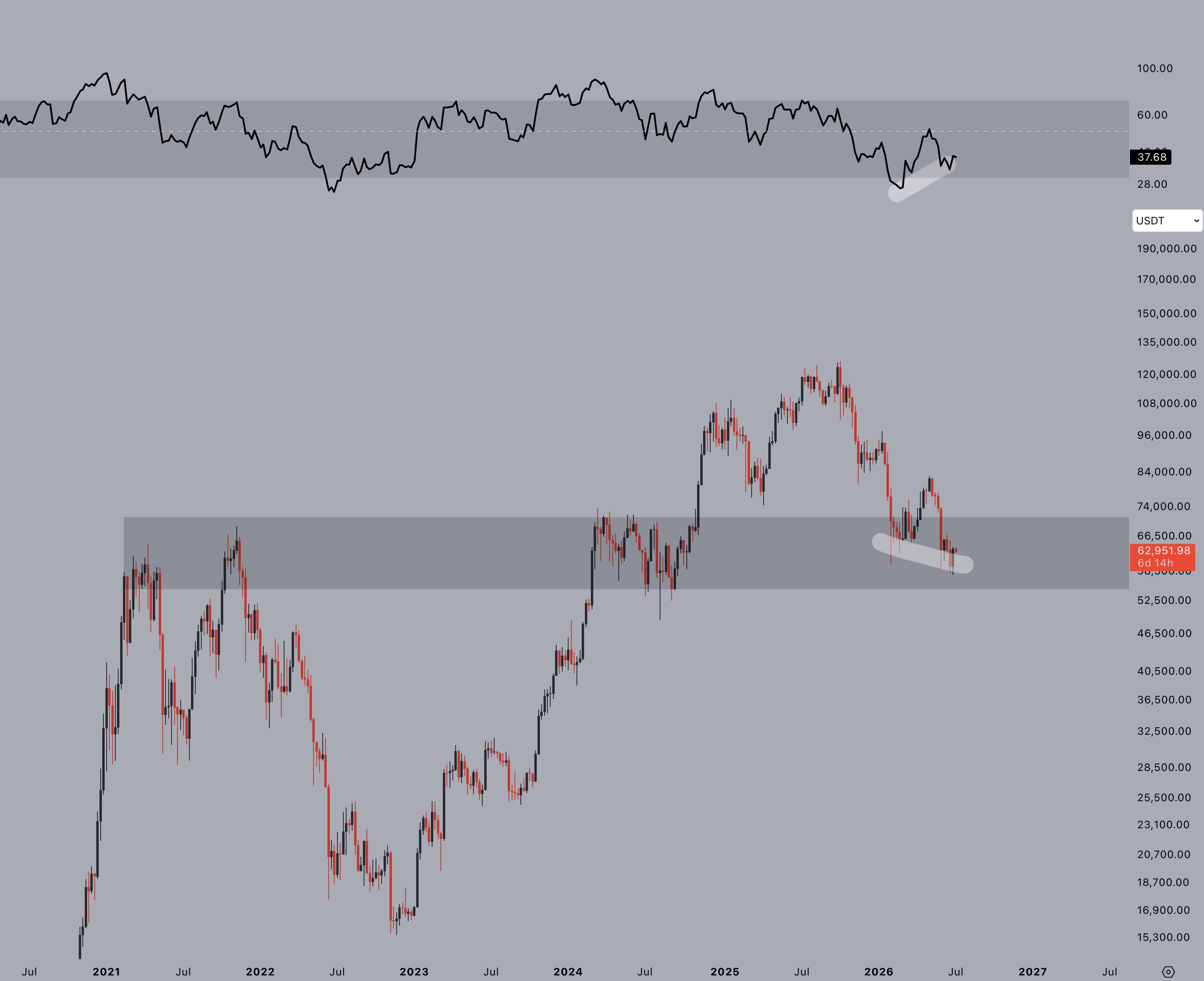

Trader and analyst Rekt Capital appeared unsurprised by the behavior, reiterating similarities between current price action and the latter portion of the 2022 bear market.

“Generally, Bitcoin is doing the same exact thing now as it was doing in the Summer of 2022,” he told X followers.

An accompanying chart showed the 50-month exponential moving average (EMA) trend line potentially becoming new resistance, just like four years ago.

BTC/USD one-month chart with 21, 50EMA. Source: Rekt Capital/X

Analyst: Strategy may reveal more BTC buys

Others remained upbeat, with trader Jelle eyeing bullish divergences on weekly time frames on the BTC/USD relative strength index (RSI).

Related: $60.4K Becomes ‘most important area’: Five things to know in Bitcoin this week

“I have seen the $BTC chart look much worse than this over the years,” he argued.

BTC/USDT one-week chart with RSI data. Source: Jelle/X

As Cointelegraph continues to report, various onchain indicators have printed reversal signals absent since late 2022.

Crypto trader and analyst Michaël van de Poppe, meanwhile, suggested that Strategy itself could end up delivering a market rebound.

“The markets are reacting with a shock response to this news. $BTC drops, and it’s clearly valuing the potential impact that Strategy can continue to sell Bitcoin going forward,” he wrote on X.

“However, I wouldn’t be surprised to see a message in the coming days that they’ve been buying more $BTC than they’ve sold.”

Sebastian Siemiatkowski, CEO and Co-Founder of Swedish fintech Klarna, gives an interview with CNBC during the company’s IPO at the New York Stock Exchange (NYSE) in New York City, U.S., September 10, 2025.

Brendan Mcdermid | Reuters

Klarna, the Swedish fintech firm best known for its buy now, pay later offerings, said Monday it applied to federal and state regulators to establish a U.S. bank subsidiary.

The firm said that, if approved, Klarna Bank USA would be a Federal Deposit Insurance Corporation-backed institution chartered in Utah. The proposed bank would be led by Gary Harding, former CEO of Milestone Bank and Prime Alliance Bank, according to Klarna.

“We’ve seen firsthand the appetite for a fairer, more transparent approach in the U.S., and our own banking license is the natural next step,” said Sebastian Siemiatkowski, co-founder and CEO of Klarna.

The move will give “customers tools to borrow responsibly and build financial confidence, while bringing greater competition, innovation, and choice” to the market, he said.

Klarna’s application is the latest sign that fintech firms, which mostly partner with U.S. banks to offer services, now see owning their own charters as a key advantage. In April, fintech provider Mercury said it won conditional approval to establish its own bank, joining a wave of fintech and crypto firms seeking entry to the traditional banking system.

Klarna said that its charter, if approved, would let it bring its banking operations in-house and strengthen reliability across payments, credit and merchant services.

The application marks Klarna’s latest step toward becoming a broader consumer bank rather than just a buy now, pay later provider. Last month, Klarna introduced high-yield savings accounts to U.S. customers, though its partner WebBank holds those accounts.

By owning a bank, fintech firms can fund loans with their own customer deposits instead of more expensive wholesale financing, directly offer checking accounts and credit cards, and rely less on third-party banking partners.

Klarna, which went public last September, is trading for about half of its IPO price of $40.

Panicked European leaders scramble to stop Trump ‘blow-up’ as one big NATO ally turns up without a plan

Microsoft to cut 4,800 jobs as AI reshapes work, says layoffs aren’t replacing employees

FCA Warns of Regulatory Overhaul as AI Agents Move Toward Tokenized Money

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: High Hopes

-

Politics3 days ago

Politics3 days agoThe House | “Reframing the debate from a binary discussion of winners and losers”: Yuan Yang reviews ‘We Are Not Machines’

-

Crypto World7 days ago

Crypto World7 days agoStrategy authorizes up to $1.25B in Bitcoin sales under new capital plan

-

News Videos6 days ago

News Videos6 days agoHow to Build INSANE Live Financial Dashboards With Claude

-

Tech7 days ago

Tech7 days agoAnonymous researcher drops 0-day ‘exploitarium’ repo

-

Business7 days ago

Business7 days agoAustralia treasurer says alleged access of prime minister’s bank data ’incredibly concerning’

-

NewsBeat2 days ago

NewsBeat2 days agoTaylor Swift and Travis Kelce wedding staffer hilariously struggles to keep her cool while checking in megastars

-

Crypto World5 days ago

Crypto World5 days agoAirdrop Registration Becomes Key Focus For Remittix As RTX Launch Updates Approach

-

Sports5 days ago

Sports5 days agoBroncos roster: OL Ben Powers (No. 74) entering final year of contract

-

Business7 days ago

Business7 days agoThe AI boom won’t burst all at once. It will pop in ‘rolling bubbles’: Macquarie

-

Crypto World4 days ago

Crypto World4 days agoBinance stock trading tops $1B in first month after launch

-

NewsBeat6 days ago

NewsBeat6 days agoPresenter Caroline Flack’s brother Paul Flack dies aged 55

-

Crypto World5 days ago

Crypto World5 days agoAlibaba-affiliate Ant Group enters the humanoid robot market with 12 deals

-

Crypto World3 days ago

Crypto World3 days agoStandard Chartered Secures MiCA License as ESMA Adds 37 New Crypto Firms

-

Crypto World1 day ago

Crypto World1 day agoSouth Africa proposes crypto tax guidance under existing rules

-

NewsBeat4 days ago

NewsBeat4 days agoNew exhibition reflects five decades of movement between island of Ireland and GB

-

Tech1 day ago

Tech1 day agoLenovo laptops are now shipping with YMTC SSDs, a sign of Chinese NAND entering the mainstream

-

Business5 days ago

Business5 days agoMeta Platforms Stock Jumps 7% Today as Bloomberg Reports Company Plans to Enter the Cloud Business

-

Business4 days ago

Business4 days agoWhat a 10 Percent Drop Means for Buyers, Sellers and Renters

-

Crypto World4 days ago

Crypto World4 days agoBinance Re-Enters Philippines As EU MiCA Rules Restrict Access

You must be logged in to post a comment Login