Crypto World

The real race isn’t Bitcoin vs. Ethereum. It’s the US vs. China on digital money

While crypto Twitter argues about Bitcoin versus Ethereum, two superpowers are quietly running a different race. The United States is using dollar-backed stablecoins to extend the dollar’s reach into every corner of the digital economy. China is using its e-CNY and the mBridge platform to build an alternative settlement system that bypasses the dollar entirely. The outcome will shape the next century of global finance. And almost nobody outside policy circles is paying attention.

Summary

- The United States has used dollar-backed stablecoins and the GENIUS Act to expand the dollar’s role across global digital payments and crypto networks.

- China has accelerated cross-border use of the eCNY through mBridge and new interest-bearing wallet policies tied to its state-controlled digital currency system.

- Despite de-dollarization efforts from BRICS nations, dollar-pegged stablecoins still dominate global digital settlement activity and reinforce demand for U.S. dollar assets.

The argument that misses the actual fight

Open any crypto publication this year, and you will find some version of the same debate. Bitcoin maximalists versus Ethereum supporters. Solana versus Ethereum. Layer ones versus layer twos. The tribal warfare is loud, it is entertaining, and it is mostly beside the point.

While that argument fills the timelines, a different and far more consequential race is being run by people who do not post memes. The United States Treasury and the People’s Bank of China are competing to define what money looks like for the next century. They are doing it in plain sight, in policy documents and central bank press releases, with two completely different theories of the case.

The American theory: extend the dollar’s reach into every digital corner of the global economy by privatizing it, regulating it, and shipping it on open networks. The Chinese theory: build a sovereign digital currency under direct state control, and link it together with friendly central banks into a parallel settlement system that does not need American rails at all.

This is the real race. It will decide whether the global financial system of the 2030s and 2040s stays dollar-denominated and U.S.-administered, or whether it splits into competing blocs with different reserve assets, different settlement rails, and different rules. The stakes are not the price of a token. They are the architecture of money itself.

What the United States is actually doing

The American strategy is easier to miss because it is being run by the private sector with regulatory blessing rather than by a central bank. But the strategy is explicit, and it has been spelled out at the highest levels of the U.S. Treasury.

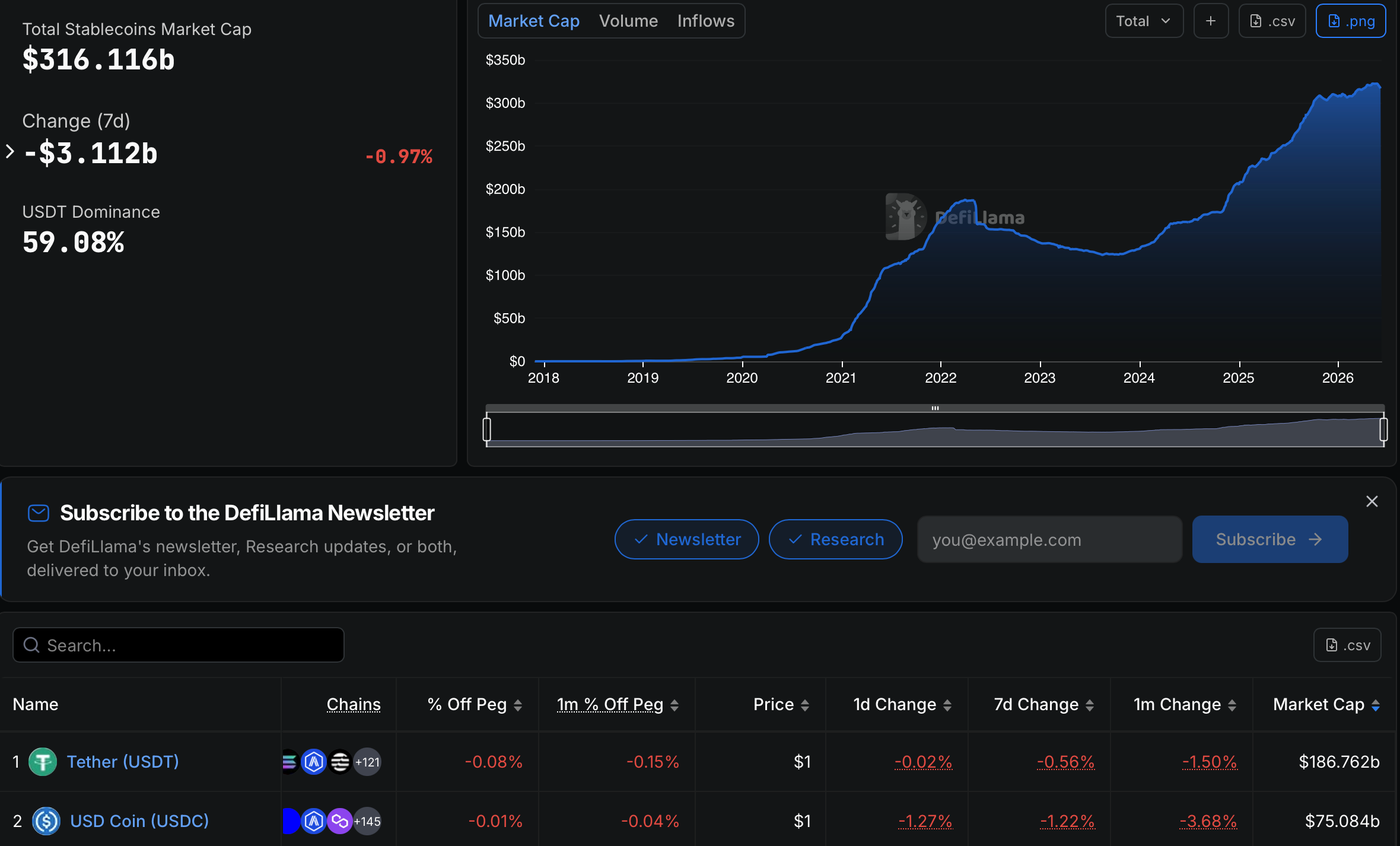

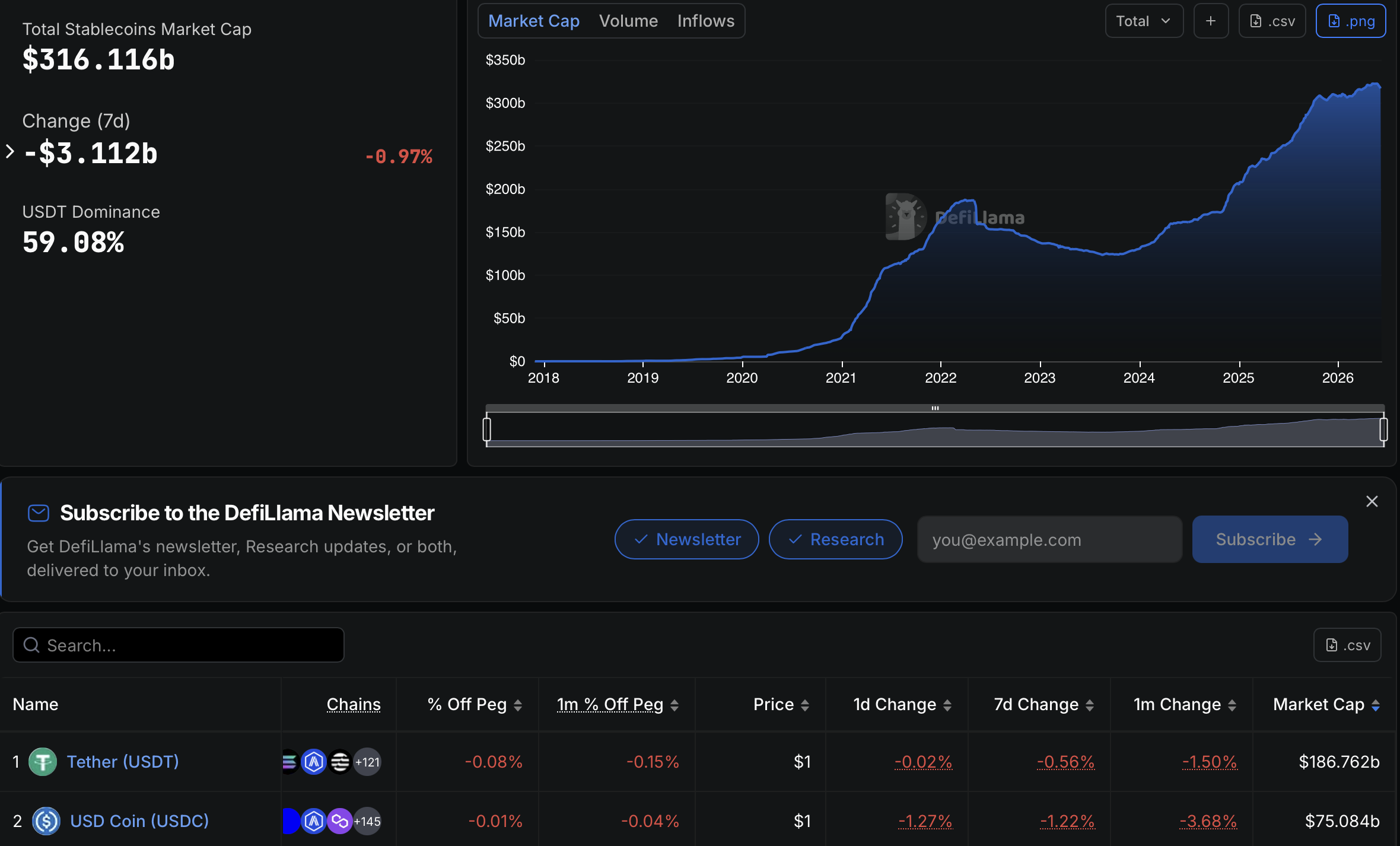

The instrument is the stablecoin. The framework is the GENIUS Act, signed into law in July 2025. The thesis was stated bluntly by Treasury Secretary Scott Bessent: stablecoins are a way to “extend the dollar’s reach” in decentralized finance and cross-border payments. Crypto commentator Arthur Hayes has put it more starkly. Stablecoins, in his framing, work as on-ramps that redirect offshore liquidity into U.S. Treasury bills. Every USDT or USDC in circulation requires reserves, and those reserves sit mostly in dollar-denominated assets. Tether alone now holds roughly $113 billion in U.S. Treasuries as of Q1 2026. The stablecoin sector, in aggregate, has become one of the largest non-sovereign buyers of U.S. government debt.

This is not an accident. It is the strategy. By making it easy, legal, and trusted to hold a dollar-pegged token on any blockchain in the world, the United States has effectively privatized dollar issuance and shipped it through global crypto networks. A small-business owner in Lagos who takes payment in USDT, a remittance recipient in Manila who saves in USDC, and a Lebanese citizen who holds stablecoins because the local currency is collapsing are each, without knowing it, deepening dollar penetration into their local economies. They are also indirectly financing the U.S. Treasury market.

The numbers are now large. Fiat-backed stablecoin supply crossed $319 billion in April 2026. Adjusted transaction volume hit $10.9 trillion in 2025, with some estimates putting total settlement volume past $33 trillion, more than Visa. Roughly ninety-nine percent of fiat-backed stablecoin value is pegged to the dollar. The euro, the yuan, the yen, and every other currency together account for the remaining one percent. In digital money, the dollar is not winning. It has, so far, lapped the field.

The genius of this approach, from the U.S. perspective, is that it works without the political baggage of a U.S. central bank digital currency. There is no Federal Reserve digital dollar to argue about. There is no surveillance state implication. There is only a regulated private sector building products that happen to pour offshore savings into U.S. debt and pull the global digital economy toward dollar-denominated settlement. The state does not have to build the rails. It just has to make them legal and trusted.

The GENIUS Act is the legal scaffolding. It defines payment stablecoins as a distinct regulated category, requires one-to-one reserve backing in high-quality liquid assets, opens issuance to banks under OCC supervision, and creates a U.S.-supervised path that competes structurally with foreign stablecoins. Tether’s planned U.S. domestic stablecoin launch fits this pattern. So does the Trump administration’s USD1 stablecoin, marketed openly as a “digital dollar for the world.” The U.S. is not building one digital dollar. It is building an entire ecosystem of them, each privately issued, each pushing toward the same outcome.

What China is actually doing

China is running a different play, executed by the state directly and aimed at a different goal.

The e-CNY, the digital yuan, is the world’s largest live central bank digital currency. By late 2025, cumulative transaction value had crossed $2.3 trillion. Twenty-nine pilot cities have integrated it into public transit and retail. 180 million wallets have been created. Domestic adoption still trails Alipay and WeChat Pay, but the gap is closing, and on January 1, 2026, the People’s Bank of China made a structural change that rewrote the asset’s economic logic.

Until that date, the e-CNY was classified as M0, basically digital cash, and could not earn interest. From January 1, 2026, banks are permitted to pay interest on verified digital yuan wallets, and the e-CNY is treated as a deposit-like instrument with commercial banks as counterparties. The currency is now covered by China’s national deposit insurance. In plain language: the e-CNY went from a digital substitute for paper money to a digital substitute for a bank account. The incentive to hold it just got dramatically larger.

That domestic change is half the story. The other half is happening across borders.

Project mBridge, the cross-border CBDC platform jointly developed by the People’s Bank of China, the Bank for International Settlements, and the central banks of Thailand, the UAE, and Hong Kong, processed over $55 billion in transactions by late 2025. The e-CNY accounts for more than 95 percent of mBridge settlement volume. Cross-border e-CNY activity overall reached roughly $2.38 trillion by November 2025, an 800 percent expansion since 2023. China launched its e-CNY International Operation Center in Shanghai in September 2025. Pan Gongsheng, the PBOC governor, has explicitly framed the goal as building “a more multi-polar monetary system less vulnerable to politicization.” It is a polite way of saying: a system the United States cannot weaponize.

The expansion is mapped. The PBOC’s 2026 work plan includes new cross-border pilots with Singapore, Thailand, Hong Kong, the UAE, and Saudi Arabia. A retail e-CNY pilot is now operating in Laos, where Chinese tourists can scan QR codes at participating local merchants and settle directly in digital yuan. The 15th Five-Year Plan (2026-2030) explicitly mandates active participation in international digital-currency governance. A new e-CNY measurement, management, and ecosystem framework took effect on January 1, 2026.

The pattern is consistent. China is building a digital settlement system that is sovereign, state-controlled, interest-bearing, and designed to operate at the edges of its trade and political alliances. It does not need to displace the dollar globally. It needs to offer a credible alternative for the share of the world economy that already does business inside China’s orbit, or that wants the option not to depend on U.S. payment infrastructure. That is a smaller target than “replace the dollar,” and a much more achievable one.

The paradox at the heart of the race

Here is where the story gets interesting, and where most coverage gets it wrong.

The de-dollarization push has not been a clean fight. The BRICS bloc, now expanded with Indonesia and partner status for nations from Belarus to Vietnam, represents close to forty percent of global GDP by purchasing power parity. Russia and China settle around ninety percent of their bilateral trade in rubles and yuan. The dollar’s share of BRICS trade has fallen from 79 percent in 2022 to 58 percent by mid-2025. BRICS Pay and mBridge are building a real alternative payment infrastructure. The political will to escape the dollar is the strongest it has been in decades.

And yet the dollar’s overall position has, on the most important metrics, strengthened.

The Bank for International Settlements’ 2025 Triennial Survey, the most authoritative measure of global currency usage, found the dollar was on one side of 89.2 percent of all foreign exchange transactions in April 2025, up from 88.4 percent in 2022. The renminbi’s share rose to 8.5 percent, a meaningful increase, but still a fraction of the dollar’s. The dollar’s reserve share has dropped gradually, from 72 percent in 2001 to roughly 58 percent in 2026, but the pace is erosion, not collapse.

The paradox is that stablecoins, the very instrument that lets a Russian importer or an Iranian merchant settle a transaction without touching the U.S. banking system, are themselves overwhelmingly dollar-pegged. Ninety-seven percent of the stablecoin market is denominated in dollars. So when a BRICS-aligned exporter in Brazil sells soybeans to a buyer in the UAE and they choose to settle in stablecoins to avoid U.S. correspondent banking, they are still, in effect, transacting in dollars. They have escaped American banks. They have not escaped the dollar.

This is the contradiction at the heart of the de-dollarization movement, and the unstated reason the U.S. is comfortable with stablecoins extending into hostile jurisdictions. Even the workarounds reinforce the system. As Tether’s CEO Paolo Ardoino has argued, stablecoins like USDT reinforce dollar hegemony precisely by offering a decentralized alternative that happens to be dollar-pegged. The political instinct to flee the dollar runs straight into the practical reality that no other currency offers comparable depth, liquidity, or trust.

The economist Brad Setser at the Council on Foreign Relations has flagged a related paradox. U.S. policy that tries to coerce countries into using the dollar, through tariff threats or sanctions, may actually speed up the search for alternatives. The dollar’s strength comes partly from being the path of least resistance. The moment it becomes a path of political compulsion, more actors will pay the cost of building around it.

The Trump administration’s repeated tariff threats against BRICS members for “de-dollarization” arguably did more to motivate alternative-payment-system construction than any Russian or Chinese initiative could have on its own.

So the race is not as simple as U.S. versus China. It is a contest in which the dominant power, the United States, is winning on infrastructure expansion while at the same time creating the political conditions that push counterparties to keep building alternatives. And it is one in which the challenger, China, is building a real, scaled alternative for a narrower slice of the world even as its broader currency, the renminbi, stays structurally constrained by capital controls and limited convertibility.

What the EU and the rest of the world are doing

The two-power framing of “U.S. versus China” is the loudest version of the race, but it is not complete. Two other actors matter.

The European Union has its own model, anchored by the Markets in Crypto-Assets regulation (MiCA), which has been in phased application since 2024. MiCA created a comprehensive licensing regime for stablecoin issuers operating in the EU and is widely considered the most carefully designed regulatory framework of the three. The European Central Bank is also developing a digital euro on a slower timeline, with implementation realistically running into 2027 and beyond. The euro’s share of global FX reserves has actually grown in 2025 as central banks diversify out of dollars, but the eurozone’s structural weakness, a shared currency without a shared treasury, limits how far the digital euro can carry the bloc’s monetary ambitions.

Other CBDC projects are real but smaller. The Bahamas, Jamaica, and Nigeria have launched retail CBDCs with mixed adoption. India’s UPI-linked CBDC pilot is one of the most operationally significant in the developing world. The UK and Japan are advancing slowly on their own digital currency designs. None of these projects threatens the dollar-yuan binary, but several stretch the architecture of state-backed digital money beyond the two superpowers.

The most interesting wildcard is the Global South. Stablecoins, particularly USDT, have quietly become a de facto financial layer in dozens of countries where local currencies are weak or banking is shallow. The 400 million-plus users who now rely on dollar-backed stablecoins are mostly outside the U.S., and many are in jurisdictions where their own governments would, politically, prefer they not use the dollar. The American digital-dollar empire is being built largely by people who do not live in America.

What actually matters from here

Three things to watch over the next two to three years will tell you which way this race is bending.

The first is how the e-CNY’s interest-bearing transition affects cross-border adoption. If digital yuan deposits become an attractive store of value in countries that already do significant trade with China, the dollar’s grip on those corridors weakens. If the transition is mostly a domestic event and the e-CNY remains a thin layer for cross-border trade between China and a handful of allies, the dollar holds.

The second is whether the United States can keep stablecoin expansion uncoupled from political backlash. The Hudson Institute and other Washington policy shops are openly arguing for stablecoin promotion as a counter to BRICS. That framing, useful in policy memos, becomes a liability the moment foreign governments start to see USD-pegged stablecoins as instruments of U.S. strategy rather than neutral infrastructure. The current strategy works because it does not look like a strategy. The moment it does, the political costs of using it rise sharply in target jurisdictions.

The third is the technology layer. The next decade of payments will involve programmable money, AI agents transacting on their own, tokenized real-world assets, and settlement networks that move money in seconds at near-zero cost. The system that wins those use cases at scale wins the next layer of finance. The U.S. has more developer momentum, more capital, and more open networks. China has more state coordination, more captive trade flows, and a willingness to mandate adoption that no democratic system can match. Both edges matter.

What this means in the end

The crypto industry has spent a decade explaining itself to outsiders as a fight between competing technologies. Bitcoin or Ethereum. Proof-of-work or proof-of-stake. Layer one or layer two. Those are interesting debates, and they will continue. But they are debates inside a smaller story.

The bigger story is that two states have realized digital money is now a geopolitical instrument, and they are competing to define what it looks like. The United States is using regulated private stablecoins to spread the dollar at internet speed into the global digital economy. China is using a state-issued, interest-bearing digital currency and a parallel settlement network to build an exit ramp for the share of world commerce that wants one. Every other digital money story is, in one way or another, downstream of those two strategies.

For an investor, the implication is that the assets sitting closest to that geopolitical contest, dollar stablecoin issuers, infrastructure providers, payment rails, on/off-ramp networks, will likely matter more over the next decade than the latest layer-one token battle. For a holder of any cryptocurrency, the implication is that the regulatory environment your asset operates in is being shaped by considerations far larger than crypto itself. The CLARITY Act will pass or not pass partly based on how policymakers read the U.S.-China contest. The GENIUS Act was already passed partly because of it.

For everyone else, the implication is simpler. The future of money is being decided right now, not in white papers or token launches but in central bank press releases and Treasury speeches. The next time you read a thread about whether Bitcoin or Ethereum is the future, remember that both of them will end up settling, on the margin, in dollar-pegged stablecoins or yuan-denominated CBDCs. The interesting question is not which crypto wins. It is which currency?

The race that matters is not Bitcoin versus Ethereum. It is the dollar versus the yuan, in digital form, for the architecture of how money moves for the next hundred years. And it is happening right now, while almost nobody is looking at the right scoreboard.

This article is for informational purposes and does not constitute financial or investment advice. Geopolitical and monetary policy developments evolve quickly; the figures and policy positions described reflect reporting available as of mid-May 2026. Always do your own research.

TLDR

- Stand With Crypto UK launched a campaign against bank transfer restrictions to crypto exchanges.

- The group urged its 286,000 UK advocates to file complaints with their banks.

- It cited a report showing 40% of attempted transfers face delays or blocks.

- The report said 80% of exchanges reported increased customer friction over the past year.

- One exchange recorded nearly £1 billion ($1.3 billion) in cancelled transactions due to bank rejections.

A UK crypto advocacy group has launched a public campaign against bank limits on exchange transfers. Stand With Crypto UK urged supporters to challenge what it calls blanket restrictions. The group said banks are blocking legal access to regulated crypto platforms and slowing adoption.

UK Campaign Targets Bank Transfer Blocks

Stand With Crypto UK asked its 286,000 registered advocates to file formal complaints with their banks. The group said banks restrict transfers to exchanges registered with the Financial Conduct Authority. It argued that these policies prevent customers from accessing a legal asset class.

The campaign cited the UK Cryptoassets Business Council’s “Locked Out” report released earlier this year. The report found that 40% of attempted transfers are delayed or outright blocked. It also stated that 80% of exchanges reported rising customer friction during the past year.

One exchange reported nearly £1 billion ($1.3 billion) in cancelled transactions over one year. The report attributed those cancellations to bank rejections. Stand With Crypto UK said such restrictions undermine the government’s digital asset goals.

Adriana Ennab, director of Stand With Crypto UK, criticised the current banking approach. She said, “People across the UK are being blocked from accessing a legal asset class.” She added that banks impose one-size-fits-all policies instead of assessing customers individually.

Katie Harries, Coinbase’s head of policy for Europe, also addressed the issue.

She said, “The banks are choking off the crucial on-ramp from fiat money into crypto.”

Harries linked the restrictions to barriers that limit access to digital assets.

Regulators Outline Gradual Integration Steps

The campaign unfolded as UK authorities advanced measured steps toward crypto integration. The House of Lords Financial Services Regulations Committee recently issued a warning. It said the UK risks falling behind the United States and the European Union on stablecoin regulation.

At the same time, the Financial Conduct Authority proposed new rules for investment funds. The FCA suggested allowing funds to allocate up to 10% of assets to crypto exchange-traded notes. Regulators framed the proposal as part of a broader review of market access.

Earlier this year, retail investors regained tax-advantaged exposure to crypto exchange-traded notes. The government allowed access through the Innovative Finance ISA framework. This move reopened a channel for regulated crypto investment products.

Despite these measures, access to banking services remains disputed. Crypto advocates said restrictions limit entry from fiat into digital assets. Stand With Crypto UK said its complaint drive aims to address those barriers.

The group stated that it seeks direct engagement with financial institutions. It encouraged supporters to request clear explanations for blocked transfers. The campaign continues as regulators review crypto policy and market access rules.

TLDR

- CryptoQuant identifies $53,600 as Bitcoin’s realized price and a potential bottom zone.

- Bitcoin traded near $62,150 after falling to around $59,000 last week.

- Total Bitcoin demand dropped by 652,000 BTC, the largest weekly contraction since January 2022.

- One-year apparent demand growth turned negative and fell below its moving average.

- Thirty-day ETF demand growth declined to negative 74,000 BTC since January 2024 launch.

Bitcoin could approach $53,600 as a potential floor while demand metrics remain weak, CryptoQuant reported on Wednesday. The firm said this level matches the current realized price, which tracks the aggregate onchain cost basis. However, research head Julio Moreno stated that demand conditions remain “deeply unfavorable” and no durable recovery has formed.

Bitcoin Realized Price Signals Possible Bottom Zone

CryptoQuant identified $53,600 as Bitcoin’s realized price and a possible bottom area. Moreno said Bitcoin historically bottoms near or slightly below this metric in bear cycles. He told The Block, “Historically, it’s a level that would confirm a bottom.”

However, Moreno added that price may not necessarily hit that level. He said demand weakness keeps that possibility open for now. Bitcoin fell to about $59,000 last week, placing it 9% above $53,600.

After the drop, Bitcoin rebounded and traded near $62,150. In November 2022, Bitcoin briefly fell below its realized price during the FTX selloff. It later recovered, reinforcing that level as a key valuation reference.

Demand Metrics Show Persistent Weakness

CryptoQuant reported a 652,000 Bitcoin contraction in total demand last week. The firm combines speculative futures activity and apparent spot demand in that measure. Moreno wrote that both segments weakened as Bitcoin dropped below $60,000.

Long liquidations increased and spot selling accelerated during that period. Meanwhile, one-year apparent demand growth turned negative and declined below its moving average. Moreno said this marked the fastest pace of decline since February 2024.

He wrote that fewer buyers exist today compared with a year ago. He added that this trend “removes the demand foundation required to sustain any price recovery.” The report also pointed to slowing institutional demand through spot exchange-traded funds.

Thirty-day ETF demand growth fell to negative 74,000 Bitcoin. CryptoQuant said this marked the weakest reading since U.S. spot ETFs launched in January 2024. Moreno wrote that ETFs now contribute to net supply expansion as investors reduce exposure.

At the same time, realized losses have not reached capitulation levels. Bitcoin holders realized 187,000 Bitcoin in losses over the past 30 days. That compares with 400,000 Bitcoin during the February 2026 drop below $60,000.

During the November 2022 market bottom, realized losses reached 1.2 million Bitcoin. Moreno said, “The absence of a capitulation-level spike in realized losses indicates that a large cohort of holders is still above water at $59,000.” He added that heavy selling and seller exhaustion usually precede major bottoms.

Moreno concluded that the current price should serve as a valuation floor candidate. He said a bull market requires a constructive demand recovery. He stated that such a recovery does not yet appear in the data.

Tether is leading a funding round of as much as $1.4 billion for German tech company NEURA Robotics, deepening the stablecoin issuer’s push into artificial intelligence and robotics.

The round, which values NEURA at roughly $7 billion, is expected to include a mix of strategic and financial investors. Tether said it is leading the raise through its investment arm, which deploys capital from the company’s profits and excess reserves across sectors including AI, energy and digital infrastructure.

NEURA said it expects to integrate Tether’s Wallet Development Kit into its robotic systems, enabling machines to receive payments and execute transactions within predefined parameters. The companies also plan to deploy Tether’s QVAC AI runtime, which is designed to run models directly on devices rather than through cloud-based infrastructure.

Tweet from Paolo Ardoino, CEO of Tether. Source: Tether on X.com

Founded in 2019 and headquartered in Metzingen, Germany, NEURA Robotics develops humanoid robots, robotic arms, autonomous mobile robots and other AI-powered systems for industrial and commercial applications. It is building an ecosystem called Neuraverse, a software platform intended to connect robots, AI models, data and services.

The investment follows reports from November 2025 that Tether was considering a 1 billion euro ($1.15 billion) investment in the company. The Financial Times reported at the time that the deal could value the tech maker at between $9.3 billion and $11.6 billion, though neither company confirmed the discussions.

Today’s announcement did not disclose how much money Tether is contributing to the current funding round.

Related: Tether, Georgia plan lari-backed stablecoin GELT under new rules

Tether expands AI and payments push

The NEURA investment is part of Tether’s broader push beyond stablecoins into artificial intelligence, payments and emerging technologies. The company reported $1.04 billion in net profit during the first quarter of 2026 and said its excess reserves reached a record $8.23 billion, providing additional capital for investments outside its core USDT (USDT) business.

Source: DefiLlama

In recent months, Tether has accelerated its push into AI through its QVAC platform. In March, the company introduced a training framework that enables AI models to be trained and run on consumer hardware, including smartphones and non-Nvidia chips. Two months later, it unveiled QVAC MedPsy, a family of medical AI models designed to run directly on smartphones and other devices rather than through cloud-based infrastructure.

The company has also sought to expand the ecosystem around its technology stack. In May, Tether launched a grants program to fund developers building local-first AI and payment applications using its open-source tools, including QVAC and its Wallet Development Kit.

In a January 2025 interview, CEO Paolo Ardoino said AI-powered humanoid robots could become commonplace within the next decade as advances in computing and automation reshape the workforce.

Tether issues the $187 billion USDT stablecoin, which controls roughly 59% of the global stablecoin market, giving it one of the largest balance sheets in the digital asset industry.

Magazine: Kraken’s $600M stablecoin firm, Huione scandal deepens: Asia Express

US President Donald Trump told reporters he “loves” inflation on Wednesday after government data showed consumer prices rising at the fastest annual pace in three years. The Consumer Price Index (CPI) climbed 4.2% from a year earlier.

The reading lands one week before the Federal Reserve’s June policy meeting under new Chair Kevin Warsh. Traders now lean toward rate hikes rather than cuts, which could pressure risk assets like Bitcoin (BTC).

Energy Prices Push US Inflation to a 3-Year High

Inflation rose 0.5% in May after a 0.6% jump in April, the Bureau of Labor Statistics reported. Energy drove most of the increase, climbing 3.9% after a 3.8% rise the prior month.

Gasoline now averages $4.15 per gallon, according to AAA. That compares with an average of $2.98 when the US and Israel first struck Iran on February 28. Meanwhile, real wages fell 0.1% in May, marking a second straight month of declines.

When asked about the latest inflation numbers, Trump embraced them.

“The numbers were great…I love the inflation,” he said.

Trump went on to acknowledge a covert effort to route millions of barrels of oil through the Strait of Hormuz. The president predicted oil would “come down like a rock” once the war ends. He previously insisted that blocking Iran’s path to a nuclear weapon is the “only thing” he considers.

Follow us on X to get the latest news as it happens

Bitcoin Faces Pressure as Rate Hike Odds Climb

Persistent inflation complicates Trump’s repeated calls for lower borrowing costs. CME FedWatch shows a 98.4% chance the Fed holds at 3.5%–3.75% next week. However, markets now price more than 70% odds of a rate hike by the end of 2026.

That shift matters for Bitcoin. Higher rates typically strengthen the dollar and Treasury yields, drawing capital away from non-yielding assets.

BTC trades near $62,000, down almost 24% over the past 30 days, according to BeInCrypto Markets. The token now sits roughly 51% below its all-time high of over $126,000. A 1% bounce over the past day has done little to repair the broader downtrend.

Warsh inherits a Fed facing accelerating prices and softening real incomes. If next week’s meeting signals tightening ahead, Bitcoin’s macro headwinds could strengthen into the summer.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post President Trump Loves Inflation, and Bitcoin Could Feel the Impact appeared first on BeInCrypto.

Botanix Labs is winding down its Spiderchain Bitcoin Layer 2, giving users until July 9 to withdraw all assets before the network goes dark. The Polychain-backed project cited insufficient demand for Bitcoin-native DeFi as the reason it could not sustain itself economically. In a post on X Tuesday,… Read the full story at The Defiant

Curve Finance has launched Llamalend v2 on Optimism with support for isolated lending markets and non-crvUSD borrowing pairs, opening the first phase of a lending system upgrade ahead of a planned Ethereum mainnet rollout later this year.

Summary

- Curve has launched Llamalend v2 on Optimism, expanding lending beyond crvUSD-only borrowing markets.

- Users can now use Curve LP tokens as collateral while maintaining exposure to liquidity pool rewards.

- The rollout starts with three isolated markets and a 250,000 OP incentive program ahead of an Ethereum mainnet launch.

According to Curve Finance, the new version removes a key limitation from Llamalend v1, which was built around crvUSD as the borrowed asset. Markets can now be created using supported assets on both sides of a lending pair, subject to governance approval, allowing collateral and borrowed assets to be selected without requiring crvUSD.

The deployment begins on Optimism, where Curve said users will initially be able to access three isolated markets: ETH against wstETH, wstETH against USDC, and WBTC against USDC.

All three markets will launch with borrow caps set at zero, meaning users can lend assets but cannot borrow until governance approves debt limits through a DAO vote expected to take about seven days.

LP tokens can now support borrowing activity

Alongside the expansion beyond crvUSD markets, Curve has introduced support for LP tokens as collateral. According to the protocol, liquidity providers can deposit Curve LP tokens, continue earning trading fees from liquidity pools, and borrow against those positions simultaneously.

The update ties lending activity more closely to Curve’s exchange infrastructure. Curve said the framework could also support other productive collateral types in the future, including yield-bearing vault assets and principal tokens used in fixed-yield strategies.

Llamalend v2 retains the liquidation model introduced with the original protocol in early 2024. Rather than liquidating a position at a single price point, the system uses a liquidation range that gradually converts collateral into the borrowed asset as prices move through predefined levels.

Curve previously said the design was created to reduce concentrated liquidation pressure during periods of market stress and give borrowers more time to manage positions.

Risk controls remain separated on a market-by-market basis. According to Curve, each lending market carries its own collateral asset, borrowed asset, oracle configuration, borrowing limits, and risk parameters. Borrow caps start at zero and must receive governance approval before debt can accumulate.

LlamaRisk reviews markets before borrowing begins

For the initial rollout, Curve said LlamaRisk will review proposed collateral assets and oversee market assessments before markets move through governance. The protocol noted that isolated markets reduce the possibility of risks spreading between unrelated lending pairs.

Support for the launch includes a 250,000 OP token grant from the Optimism Foundation, according to Curve’s announcement. The incentives are expected to be distributed over roughly two months to encourage liquidity and participation.

Curve’s technical documentation also states that an initial incentives campaign will distribute 100,000 OP tokens through Merkl across the first markets.

Before enabling borrowing, Curve said it chose to deploy on Optimism to observe contract behavior, integrations, and user activity in a lower-risk environment. A launch on the Ethereum Mainnet is expected during the second half of the year.

The rollout follows other recent lending-related initiatives from Curve. As previously reported by crypto.news, the protocol introduced a bad-debt recovery framework for LlamaLend markets that converts distressed lending positions into tradable on-chain claims.

Curve founder Michael Egorov described that mechanism as an investment tool that could eventually be applied to other markets if successful.

Binance has moved its tokenized-equity program from announcement to live product, introducing bStocks, a first batch of five US equities that eligible users can convert into on-chain tokens and trade around the clock, seven days a week. The exchange posted the launch Wednesday to its official… Read the full story at The Defiant

XRP’s on-chain activity has cooled dramatically since its 2025 surge, according to Glassnode’s latest on-chain metrics. The 90-day average of total XRP network fees has plunged to about 500 XRP from roughly 5,900 XRP in February, a 91.5% drop that points to a sharp slowdown in on-chain demand after the mid-2025 price spike that briefly pushed XRP above $3. The pullback in on-chain activity mirrors a broader shift in trader behavior and market structure after a period of intense speculation.

Compounding the view of a cooling market, XRP’s 90-day realized profit-to-loss ratio has collapsed to 0.38, suggesting that more coins are being realized at losses than profits on-chain. At the height of its price run in January and July 2025, when XRP traded near $3.40, the ratio reached around 50 as profit-taking dominated flows. The current regime, by contrast, signals a possible capitulation environment where selling pressure is less about wholesale distribution by big holders and more about risk-off sentiment and leverage-driven liquidations.

Key takeaways

- On-chain demand for XRP has slumped sharply since the 2025 rally, with the 90-day average of network fees falling 91.5% to around 500 XRP.

- The 90-day realized profit-to-loss ratio has fallen to 0.38, indicating losses are being realized more than profits as investors exit positions.

- Exchange-related activity shows a cooling dynamic: large XRP transfers to centralized venues like Binance have declined since the 2025 peak, hinting at a shift away from mass whale distribution.

- A defined accumulation zone between roughly $1.00 and $0.65 is taking shape, anchored by technical levels such as a fair value gap and a high-volume node around $0.50–$0.65.

- Despite near-term weakness, a subset of analysts maintains a longer-term bullish thesis, with a target range of about $15–$18, underscoring the ongoing debate over XRP’s eventual fundamental trajectory.

On-chain activity and what it signals

Glassnode’s analysis stresses that XRP’s on-chain activity has cooled substantially after the explosive run that pushed the token above $3 in the first half of 2025. The drastic drop in the 90-day fee average—from thousands of XRP to a few hundred—suggests a cooling in the network’s transaction activity and a retrenchment of speculative demand. In practical terms, the fee data are often treated as a proxy for everyday transactional use on the XRP ledger, and the current readings imply a lull in users and a normalization after a period of exuberant activity.

Observers are watching whether this cooling translates into a more stable or even depressed price regime. The price action that followed the mid-2025 spike created a technical environment where traders now see a broad band between $1.00 and $0.65 as a critical zone. The question is whether buyers will accumulate enough demand to defend that range or if the market will test lower levels in a broader risk-off cycle.

Profit dynamics: from profit-taking to capitulation?

The realized profit-to-loss ratio offers a window into how investors are managing their XRP positions as market conditions shift. The ratio’s plunge to 0.38 means that for every $1 of realized profit, approximately $2.63 of losses have been realized, a pattern often observed when a market moves from a distribution phase into capitulation, albeit without the same intensity of selling by large holders as in prior cycles.

For context, the ratio reached about 50 during the weeks when XRP hovered near $3.40 in 2025, indicating heavy profit-taking at those price points. The reversal to a low ratio is consistent with a broader shift away from aggressive on-chain profit-taking and toward a more cautious posture among market participants. While this doesn’t preclude a return to stronger hands pushing prices higher, it does highlight a renewed emphasis on risk controls and stop-out dynamics in a market that has already experienced substantial speculative fervor.

Whale flows, exchanges, and the bigger picture

On the exchange-front, data from CryptoQuant offers a complementary view to Glassnode’s on-chain activity. Analysts have flagged a decline in transfers of XRP to major exchanges, particularly among the higher-cohort holders. Notably, inflows of 100,000–1,000,000 XRP and those above 1,000,000 XRP have weakened since the 2025 peak, with declines of about 15% and 20%, respectively, since October 2025. The trend points to a reduction in the step-like distribution that often accompanies top-of-cycle sell-offs.

Analysts caution that the near-term price weakness appears more connected to leverage-driven liquidations and a risk-off mindset than to a broad, coordinated dump by large holders. In other words, while large holders are still active participants in the space, their activity does not appear to be the dominant force shaping XRP’s price action at this juncture. The combination of fading on-chain demand and shifting exchange dynamics creates a nuanced backdrop for traders who must weigh potential liquidity gaps against the possibility of renewed demand in a broader crypto-market upcycle.

In terms of regional and behavioral signals, the XRP ecosystem still shows a classic pattern: from a few clear acceleration points to a more cautious phase where traders hunt for lower-risk entries. CryptoQuant’s analysis highlights how inflows to exchanges from large holders have cooled, which historically has preceded or accompanied broader corrections in the XRP market. Yet, as ever in volatile crypto markets, these trends must be contextualized within macro conditions, liquidity cycles, and evolving regulatory dynamics that continue to shape investor risk appetite.

Technical map: where buyers are watching

From a chart perspective, XRP has been consolidating within a zone that many traders view as a potential bottoming region. The weekly price action points to a cluster of technical levels between $1.00 and $0.65. A notable fair value gap created during XRP’s late-2024 rally spans roughly $0.63 to $1.00, and price has shown movement back toward this zone after breaching the $1.40 level on the downside. Visible-range volume profile data indicate relatively light activity below current prices until a high-volume node sits around $0.50–$0.65, suggesting a meaningful area of liquidity in that neighborhood.

The point of control—the price area with the most traded volume—sits near $0.52–$0.55, reinforcing the idea that this range has become a magnet for immediate supply and demand. In addition, XRP’s five-year ascending trendline projects to intersect near $0.60–$0.65 in the coming months, a confluence of support that could anchor a potential bounce if macro conditions support renewed risk appetite.

On the community front, market observers have begun highlighting the $0.60–$0.65 band as a practical accumulation zone. Traders such as Crypto Patel have identified $1.00–$0.60 as a preferred range to accumulate, while others like Javon Marks continue to model a longer-term bull scenario with a target of roughly $15–$18 per XRP—a move that would imply roughly 1,100% upside from current levels. While such a trajectory remains contingent on a sustainable macro and market-driven re-pricing of risk, the convergence of on-chain, exchange, and technical signals keeps the narrative alive for those investors betting on a reacceleration in XRP’s adoption and liquidity cycle.

What to watch next

As the market digests a quieter on-chain environment and a shift in exchange activity, XRP traders will be closely watching whether demand can re-emerge around key support around $0.60–$0.65 and whether buying interest can sustain a move back toward the $1.00 threshold and beyond. The overarching question remains whether the longer-term bull thesis can absorb another round of macro shocks or if a fresh catalyst—regulatory clarity, improved liquidity conditions, or institutional participation—could reframe XRP’s trajectory in 2026.

Japan's three largest banks have moved from exploratory talks into formal infrastructure deployment, establishing a joint stablecoin council targeting live transactions by March 2027. Mitsubishi UFJ Bank (MUFG), Mizuho Bank, and Sumitomo Mitsui Banking Corporation (SMBC) published a joint press… Read the full story at The Defiant

Brad Garlinghouse has endorsed claims that Wall Street firms are increasingly pursuing the same institutional finance strategy that XRP was once criticized for supporting.

Summary

- Brad Garlinghouse backed Hugo Philion’s claim that Wall Street and crypto firms are increasingly adopting XRP’s institutional finance vision.

- Philion said Ripple’s payments strategy has remained consistent despite years of regulatory challenges and industry criticism.

- The comments come as the XRP Ledger prepares its v3.2.0 upgrade and Ripple supports Mastercard’s new AI payments network.

According to comments shared on X, Ripple CEO Brad Garlinghouse responded with a one-word endorsement after Flare co-founder Hugo Philion argued that many parts of the crypto industry are now embracing the bank-focused approach that XRP and Ripple promoted from the beginning.

The exchange began after an X user highlighted remarks Philion made during a recent interview discussing Ripple’s long-standing role in digital payments. The user wrote that parts of the crypto sector had mocked XRP’s institutional vision in the past but were now attempting to replicate it. Garlinghouse replied simply, “True.”

Philion’s comments centered on how perceptions of Ripple have changed over time. During the interview, he said XRP and Ripple were once criticized for working closely with banks and financial institutions. According to Philion, many projects across the crypto market are now seeking similar relationships with traditional finance firms.

Ripple’s institutional strategy gains fresh attention

Speaking in the interview, Philion said he had always been interested in XRP and viewed Ripple’s payments strategy as being largely on the right track. He argued that regulatory challenges have created more obstacles for the company than issues related to its business model.

While discussing the criticism Ripple faced in its early years, Philion said XRP was often labeled a “banker coin.” He contrasted that view with the current market environment, where many crypto companies are actively pursuing partnerships with banks, payment providers, and financial institutions.

Philion also stated that Ripple has remained consistent with its original objective of improving payments infrastructure. According to his comments, the company has continued building around that use case while maintaining one of the most active communities in the digital asset industry.

Recent developments involving Ripple have added context to the discussion. As previously reported by crypto.news, Mastercard recently launched an AI-powered payments network called Agent Pay for Machines with support from more than 30 companies, including Ripple, Coinbase, the Solana Foundation, Stripe, Adyen, Cloudflare, and OKX.

According to Mastercard, the platform is designed to allow autonomous software agents to carry out transactions, settlements, and machine-to-machine payments. Ripple said fast settlement infrastructure remains an important component for such systems, reinforcing the company’s long-standing focus on payment efficiency.

XRP Ledger prepares next software release

Alongside the renewed debate over Ripple’s role in financial infrastructure, development work on the XRP Ledger continues ahead of a scheduled software update.

According to the XRP Ledger Foundation, version 3.2.0 is expected to be released on June 15 following last month’s rollout of version 3.1.3. The previous release included updates affecting NFTs, Multi-Purpose Tokens, Vaults, the Lending Protocol, and Permissioned Domains.

One of the most notable changes in the upcoming release is a rebranding of the network’s core server software. According to the XRP Ledger Foundation, the software currently known as “rippled” will be renamed “xrpld.”

The foundation said the change is intended to better represent the expanding open-source ecosystem surrounding the XRP Ledger.

UK Advocates Say Banks Restrict Legal Crypto Access

Karmelo Anthony’s New Mugshot Photo Sparks Reactions Online

#prosperidade#financas#motivacao

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Evereve – Corporette.com

-

Crypto World6 days ago

Crypto World6 days agoJensen Huang Approves Samsung, SK Hynix, and Micron for NVIDIA (NVDA) HBM4 Memory Supply

-

Crypto World3 days ago

Crypto World3 days agoAnatomy of the June crypto crash: Fed, Iran, Saylor

-

Entertainment4 days ago

Entertainment4 days agoThe Best Mystery Series of All Time Is Surging on Streaming 30 Years After It Ended

-

NewsBeat3 days ago

NewsBeat3 days agoAlexander Zverev wins the French Open to finally earn a 1st Grand Slam title

-

Tech5 days ago

Tech5 days agoSuspicious Polyfill login prompts pop up on Toshiba, Muji websites

-

Crypto World4 days ago

Senator Cynthia Lummis Calls CLARITY Act the Most Consequential Financial Legislation of This Generation

-

Tech6 days ago

Tech6 days agoMicrosoft launches MXC, an OS-level sandbox for AI agents, with OpenAI and Nvidia already on board

-

Tech4 days ago

Tech4 days agoMicrosoft unveils seven homegrown AI models in new bid for ‘long term self-sufficiency’

-

Business6 days ago

Business6 days ago(VIDEO) Justin Bieber Delivers Surprise Happy Birthday Serenade to Diners at Los Angeles Mexican Restaurant

-

Business4 days ago

Business4 days agoThe Pain Points Taking a Fragile Tech Rally Down a Notch

-

Crypto World3 days ago

Crypto World3 days agoEli Lilly (LLY) Stock Surges 4% Following Breakthrough Sleep Apnea Trial Results

-

Crypto World6 days ago

LBank Surpasses 25 Million Users Worldwide as AFA Partnership Continues to Drive Global Growth

-

Tech5 days ago

Tech5 days agoVon der Leyen’s AI envoy pick draws conflict-of-interest fire

-

Tech6 days ago

Tech6 days agoMeta steals a tactic from Tesla and builds data centers in tents

-

Crypto World4 days ago

Crypto World4 days agoTrump’s AI Ownership Plan Could Benefit Anthropic at OpenAI’s Expense

-

Sports1 day ago

Sports1 day agoBangladesh beat Australia after 20 years in ODIs, register only their second win over six-time world champions | Cricket News

-

Business3 days ago

Business3 days agoHigh Stakes for Wembanyama as New York Pushes for 3-0 Lead

-

Tech5 days ago

Tech5 days agoHackers now exploit SolarWinds Serv-U flaw to crash servers

-

Tech3 days ago

Tech3 days agoNotion restores access to Anthropic after service disruption

You must be logged in to post a comment Login