Crypto World

Trump Cancels Signing of Housing Bill with CBDC Ban

US President Donald Trump cancelled the signing ceremony for a housing bill containing a ban on a central bank digital currency (CBDC) as he looked for Republicans in Congress to prioritize a controversial voting bill.

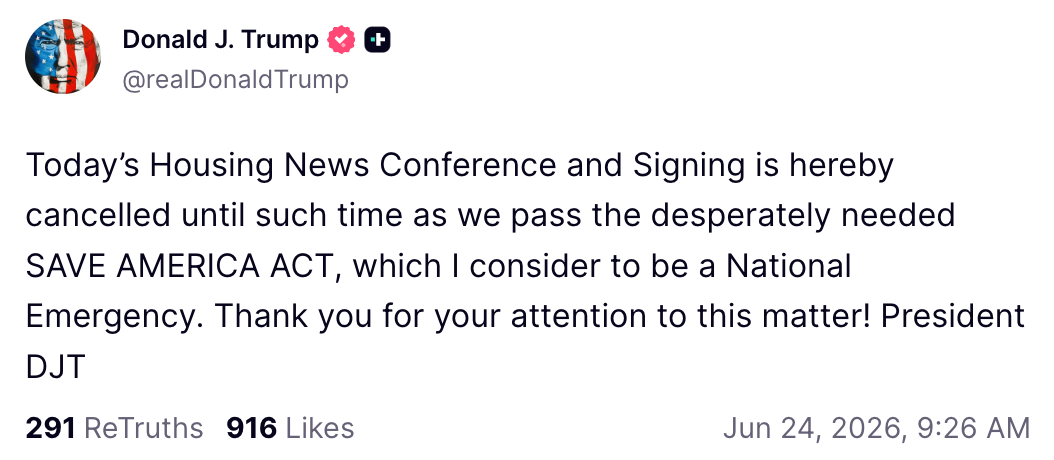

In a Wednesday morning Truth Social post, Trump said that the signing for the 21st Century ROAD to Housing Act, passed by the US Senate and House of Representatives, would be cancelled “until such time as we pass the desperately needed SAVE America Act.”

Source: Donald Trump

The housing bill, passed by the House on Tuesday, included a provision barring the US Federal Reserve from issuing or creating a CBDC “or any digital asset that is substantially similar” until the end of 2030. However, the legislation also included a carve-out for stablecoins, allowing “dollar-denominated currency that is open, permissionless and private.”

Many had expected Trump to sign the bill, aimed at tackling housing affordability, into law on Wednesday without issues. However, the president said in March that he would “not sign other bills” until the SAVE America Act was passed.

The legislation would require voters to provide proof of US citizenship in person to register.

Related: US Senate passes housing bill with CBDC ban until 2030

Senate Republicans largely supported the housing bill, which passed the chamber in a 85-5 vote on Monday. Tim Scott, the Republican who chairs the Senate Banking Committee, expressed support for the legislation as recently as Wednesday morning before Trump’s announcement.

Could Trump’s position also impact crypto market structure?

Given the president’s opposition to signing any bill into law other than the SAVE America Act, it’s unclear whether Trump also intends to veto or delay signing of crypto-related bills.

As of Wednesday, the US Senate was still waiting to potentially vote on the Digital Asset Market Clarity (CLARITY) Act, a bill expected to change the roles of financial regulators in overseeing and enforcing digital asset laws. However, Trump said in May that he intended to codify a “future-proof digital asset market structure,” likely referring to CLARITY.

Magazine: AI is banking the unbanked in Africa… faster than crypto

This is a developing story, and further information will be added as it becomes available.

TLDR:

- Over $2.2 trillion has been wiped from the crypto market in eight months since the October 2025 peak.

- Bitcoin dropped 53% from its $126,200 all-time high, hitting a new cycle low of $59,000 in June 2026.

- Ethereum fell 67% from its October top, while altcoins excluding both assets lost $538 billion in value.

- The four-year crypto cycle model places Bitcoin’s expected market bottom around October 2026.

Over $2.2 trillion has been wiped from the cryptocurrency market in the last eight months, with the total market cap falling from $4.27 trillion in October 2025 to $2.02 trillion in June 2026.

Bitcoin dropped 53% from its all-time high of $126,200 to a new cycle low of $59,000. Ethereum fell even harder, losing 67% over the same period. The altcoin market, excluding both assets, shed $538 billion alone.

Eight Months of Cascading Losses Across the Crypto Market

The wipeout traces back to October 6, 2025, when crypto hit its all-time high, and Bitcoin neared $126,000. Four days later, Trump announced new China tariffs, sparking what markets now call the “10/10 crash.” Within hours, $19 billion was liquidated, marking the largest single-day wipeout in crypto history.

Pressure continued building into the new year. On January 30, Trump nominated Kevin Warsh to replace Fed Chair Jerome Powell.

That single move shifted rate expectations and added a new layer of macro uncertainty to an already fragile market.

On February 23, the administration raised the global tariff rate to 15%, pushing Bitcoin below $65,000. Five days later, on February 28, the US and Israel launched military operations against Iran. Risk appetite across financial markets deteriorated further as a result.

As Bull Theory noted on X, the total market excluding Bitcoin and Ethereum is down 45%, wiping out $538 billion on its own. That figure illustrates how broad the damage has been, well beyond the two largest digital assets.

Corporate and Policy Shocks Deepen the Drawdown

In late May, Strategy sold 32 Bitcoin, marking the firm’s first-ever sale of its holdings. Though the transaction was small relative to the company’s total treasury, it broke a narrative that had held for years.

Strategy had been widely viewed as an unconditional Bitcoin accumulator, and the sale rattled investor confidence across the market.

June brought another blow. Kevin Warsh presided over his first FOMC meeting as Fed Chair, and the dot plot turned hawkish.

Rate cuts were effectively taken off the table, reinforcing a macro environment that continues to weigh on risk assets, including crypto.

Spot Bitcoin ETFs reflected the shift in sentiment. Consecutive sessions of net outflows stretched across weeks, with redemptions running into the billions. Institutional demand, which had been a pillar of the 2024 to 2025 rally, was now visibly reversing.

According to the four-year crypto cycle model, Bitcoin is expected to bottom around October 2026. As of June 24, the total market cap sits near yearly lows, still down more than 50% from the October 2025 peak, with $2.2 trillion yet to return.

Bitcoin slid below $60,000 and Ether fell harder still on Wednesday, as a selloff in AI and semiconductor stocks and rising bets on a Federal Reserve rate hike pushed investors out of risk assets across the board. Bitcoin dropped about 4% over the prior 24 hours, slipping under the $60,000 level… Read the full story at The Defiant

XRP (XRP) price has fallen 50% over the past year, even as activity on its network climbs toward record highs. The flood of money behind that activity may be part of the reason the price keeps struggling to recover.

The driver is RLUSD, Ripple’s stablecoin, a token built to hold a steady value near one US dollar. It is pulling fresh money onto the network, deepening the pools where XRP trades, while doing little to lift demand for the token itself. That shift has become a recurring thread in recent Ripple news.

XRP Price and Network Activity Have Split Apart

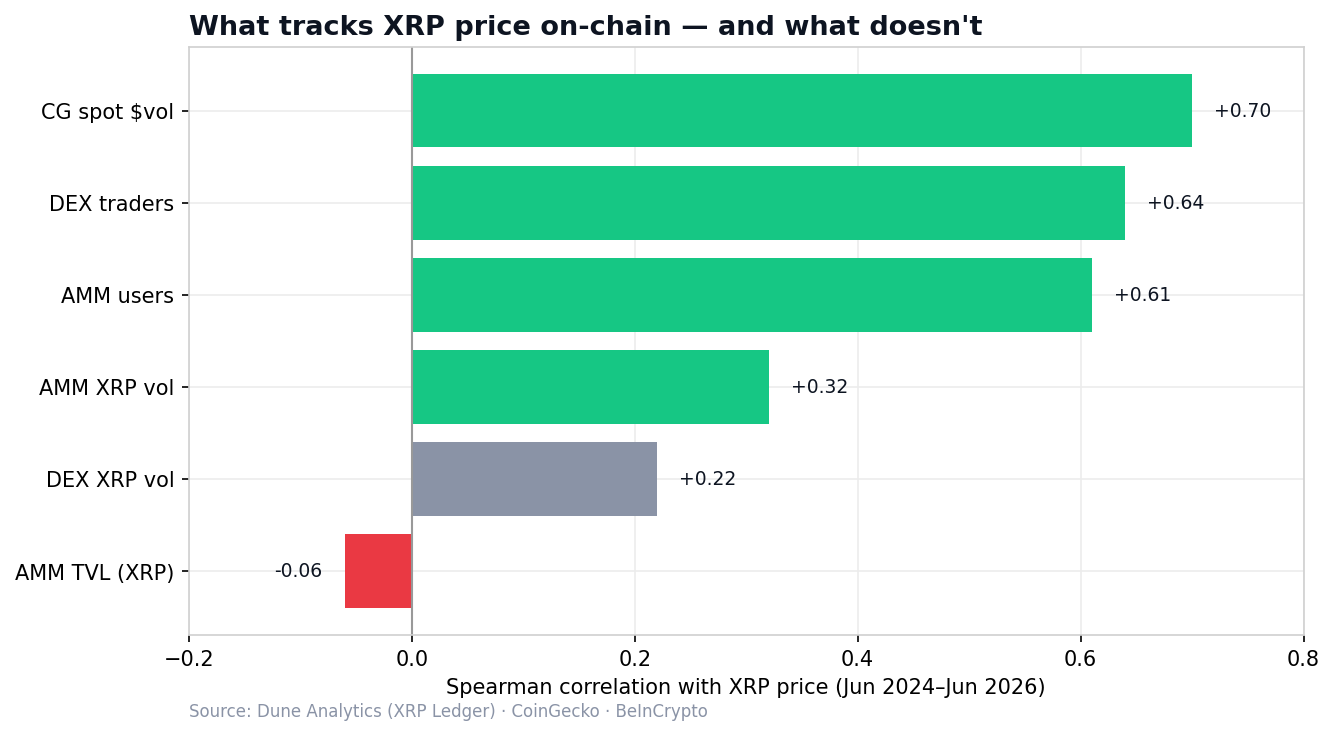

To understand why XRP is dropping even as its network grows, let us view one split in the data. For most of the past two years, on-chain activity moved loosely with the price. Usage climbed during rallies and faded during selloffs, and a correlation check over that period confirms the link.

Want more token insights like this? Sign up for Editor Harsh Notariya’s Daily Crypto Newsletter here.

Activity on the network’s decentralized exchange (DEX), a marketplace that settles trades directly on-chain without a central middleman, scores about +0.6 against price.

One metric breaks the pattern. Liquidity sitting in automated market maker (AMM) pools shows almost no positive link to price, and recently it has moved in the opposite direction.

An AMM lets people trade against a shared pool of deposited funds rather than against another trader, so the size of those pools reflects committed capital more than daily speculation. That single divergence is where the story begins.

Pool Liquidity Climbs as the Price Falls

Through 2026, the price has trended steadily lower, falling about 22% in the most recent two-month stretch, and the current XRP price now sits near its weakest level in a year, a decline that has dominated recent XRP news. The pools have done the opposite. Total value locked (TVL), the combined worth of all funds deposited across the AMM pools, more than tripled over the same window. Money kept arriving even as the token lost value.

Native DEX volume points the same way. Daily trading on the network’s on-chain exchange in 2026 has run at roughly three times its 2024 average, a steady climb that ignored the falling price. The build-up is not random, and it traces back to one asset arriving on the network in size.

RLUSD Is Quietly Filling the Pools

RLUSD now anchors the second-largest AMM pool on the network, with only one pool holding more XRP. Its broader footprint is large.

Supply on the network sits near $785 million across about 45,500 holders, after jumping nearly 30% in a single month.

The way that supply arrived matters. It climbed nearly 30% in a month. Yet the number of holders barely moved, rising less than 1% over the same stretch. Fresh dollars went to existing or a handful of wallets rather than a broad new base.

The growth appears to explain the liquidity surge, because a deep and regulated dollar pair gives traders a stable way to move in and out of XRP. The same data carries a warning, though.

Roughly 82% of RLUSD sits in just the top 10 wallets, so the holder base remains thin and concentrated. It also raises a harder question for the price.

Why the Stablecoin Boom May Weigh on XRP

Here the two halves of the story meet. The liquidity boom has not pulled in a wave of new buyers, and active traders and AMM users still rise and fall with the price. That suggests the growth reflects liquidity and settlement rather than fresh speculative demand for the token.

That points to a real risk for the token. If banks and firms settle value directly in RLUSD, they may never need to hold or buy XRP to move money across the network. A stablecoin can flood a network with dollars while quietly competing with its native asset, and the data so far fits that reading. The pools are filling, but XRP demand is not following. Derivatives traders, however, are positioned for the opposite outcome, betting that the price will rebound.

Derivatives Traders Lean Long Into Weakness

That bet shows up in the futures market. XRP open interest, the total value of futures contracts still active, sits near $3.45 billion across 125 perpetual venues. That is heavy exposure for a market trending down, and most of it leans long, meaning traders are wagering on higher prices. The funding rate, the recurring fee that longs and shorts pay each other to hold positions, stays positive on most venues. A positive rate means longs are paying shorts, a sign that bullish bets crowd the market.

A few venues show the reverse, with shorts paying instead, so the conviction is strong but not unanimous. This is the tension beneath the XRP price. On-chain, stablecoin money keeps flooding the network without lifting demand for the token. But in the futures market traders keep betting on a rebound, which could be riskier courtesy of a long flush possibility.

For now, any XRP price prediction depends on whether that liquidity finally turns into real demand for XRP. That could happen mechanically. RLUSD’s largest pool is paired against XRP, and the network often routes payments through XRP as a bridge.Therefore, heavier stablecoin use would pull more XRP into pools and transfers.

The same question hangs over any wider Ripple forecast built on network growth alone, and that single outcome separates a genuine recovery from another slow leg lower.

The post XRP Is Down 50%, and a $785 Million Stablecoin May Be Part of the Problem appeared first on BeInCrypto.

Baton Corporation, the UK-headquartered development company behind Pump.fun, is recruiting a Chief Legal Officer at a base salary of $1M to $5M, co-founder Alon Cohen posted Wednesday on X. A $1M base floor for a CLO is well above the median for senior in-house legal executives at most crypto… Read the full story at The Defiant

Yakovenko’s comments stood out because they came from one of Ethereum’s most prominent competitors. While debates between Ethereum and Solana supporters have often been contentious, Yakovenko’s reaction reflected a view shared by many currently at the top of the industry: that leaner organizations can sometimes make better decisions than larger, more bureaucratic ones.

The emergence of EthLabs is particularly significant because it arrived the day before the foundation’s layoffs and budget cuts, underscoring what supporters see as a broader trend: Ethereum’s research and development ecosystem increasingly extending beyond the foundation itself.

“I feel that the job cuts at the EF were necessary for their budget, longevity, and CROPs alignment,” said Hudson Jameson, head of ecosystems at CertiK and a former employee at the Ethereum Foundation. “As sad as the layoffs are, it was an inevitability to keep the EF lean long term.”

Jameson described EthLabs’ launch as exciting, noting that its founding team includes respected veterans of Ethereum’s research and development community. “The founding team at EthLabs are long-time, well-respected members of the Eth R&D community,” he said. “I can’t wait to see what they will accomplish.”

For years, critics and supporters alike have debated whether Ethereum relies too heavily on the Ethereum Foundation. As the ecosystem has grown into a global network of developers, infrastructure providers, layer-2 networks, institutions and companies, some leaders have argued that the foundation should become less central rather than more influential.

Crypto World

Ethereum Price Prediction: Kiyosaki Still Eyeing ETH, Solana Founder Bullish on EF Staff Cuts

Ethereum price is not looking good, and its prediction is at rock bottom, but it’s also holding attention from two directions at once. The Ethereum Foundation just confirmed 54 layoffs and a 40% budget reduction, but Solana co-founder Anatoly Yakovenko called it bullish. Meanwhile, Robert Kiyosaki is still publicly accumulating ETH, with bombastic targets.

Bullish, fr. Budget constraints force prioritization and focus. Ethereum isn’t going away. A smaller and leaner EF will be more decisive and will move faster and will be able to course correct faster. https://t.co/PMDplfApyM

— toly

(@toly) June 23, 2026

(@toly) June 23, 2026

The Foundation’s restructuring is deliberate. Co-founder Vitalik Buterin acknowledged concrete trade-offs: a smaller Devcon, the wind-down of Privacy and Scaling Explorations, and reduced scope beyond core Ethereum work. The organization now runs on a seven-cluster structure focused on protocol security, censorship resistance, and privacy.

Its treasury policy caps annual spending at 15% of holdings, with a 2.5-year cash buffer and a glide path to a 5% endowment baseline by 2030, funded increasingly by staking and DeFi yield rather than ETH sales. According to Yakovenko, a foundation that spends less and ships its priorities more tightly moves faster. But will price follow?

Discover: The Best Token Presales

Ethereum Price Prediction: Push Toward $4,500 After Foundation Reset?

ETH is trading at around $1,660 right now, and the key Fibonacci structure sits well above the current spot. The support clusters are at around the 23% retracement at $1,300, with the 62% level around $1,900 acting as meaningful resistance on any sustained rally. Until ETH reclaims that $1,800 buy-zone, the mid-term technical picture remains constructive only on a relative basis.

The bull case is straightforward: Foundation restructuring reads as a catalyst for faster protocol execution, Yakovenko’s public endorsement pulls cross-ecosystem attention, and Kiyosaki’s continued accumulation commentary, framing $4,000 ETH as “the next Bitcoin moment,” keeps retail sentiment tilted toward accumulation. Targets in that scenario run $2,000 near-term, with institutional consensus from firms like Citi and Fundstrat clustering in the $5,440–$15,000 range for 2026.

Don’t Miss Out on Our $1,000 USDT Airdrop on ByBit

However, invalidation arrives if ETH loses key support below $1,500 on volume, which would reopen the lower consolidation range and neutralize the Foundation narrative entirely. Ethereum’s price structure still hinges on whether protocol momentum translates into fee revenue and network demand, not on any single pundit’s call.

Discover: The Best Crypto to Diversify Your Portfolio

Bitcoin Hyper Positions Where Both ETH and Solana Are Pointing

The Ethereum Foundation restructuring and Yakovenko’s bullish take on it highlight a convergence traders should track: Bitcoin’s security model, Ethereum’s programmability ambitions, and Solana’s execution speed are no longer cleanly separate value propositions. Early-stage infrastructure projects are already trying to collapse that gap.

Bitcoin Hyper ($HYPER) is one presale worth examining in that context. It is the first Bitcoin Layer 2 with Solana Virtual Machine (SVM) integration, meaning smart contract execution at sub-Solana latency, anchored to Bitcoin’s security.

The project has raised $32 million at a current price of just cents, $0.0136821, with staking available at a high APY for early participants. The core pitch: programmable Bitcoin, fast enough to compete with Solana on throughput, without abandoning BTC’s trust model.

A Decentralized Canonical Bridge handles BTC transfers natively (no wrapped-token workarounds). That’s a technically differentiated position.

Research HYPER’s Full presale details here.

The post Ethereum Price Prediction: Kiyosaki Still Eyeing ETH, Solana Founder Bullish on EF Staff Cuts appeared first on Cryptonews.

Prediction markets firm Kalshi has filed a lawsuit against Illinois state officials, arguing that newly enacted legislation in the state “expressly bans sports event contracts” on its platform unless Kalshi complies with a licensing regime. The company says the law conflicts with federal oversight of prediction markets and could force it to make operational changes that would be costly and ultimately unrecoverable.

In a Tuesday filing in the U.S. District Court for the Northern District of Illinois, Kalshi named Illinois Governor JB Pritzker, Attorney General Kwame Raoul, and other officials connected to the state’s gaming board. The complaint asserts that the measure signed last week—Illinois Senate Bill 3019—improperly intrudes on authority Kalshi says belongs to the U.S. Commodity Futures Trading Commission (CFTC) under federal law. Kalshi is seeking to block the statute from taking effect on July 1.

Key takeaways

- Kalshi alleges Illinois Senate Bill 3019 conflicts with federal CFTC authority over prediction markets, including event contracts.

- The company argues compliance would force it to stop offering sports event contracts in Illinois or face potentially unlawful enforcement.

- Kalshi claims the July 1 start date could cause “irreparable harm,” including non-recoverable technical and compliance costs.

- The case adds to an ongoing federal-versus-state jurisdiction dispute over prediction markets and whether they fall under commodities rules.

- Legal experts cited in earlier coverage say these fights may ultimately reach the U.S. Supreme Court.

Illinois law brings prediction markets under sports betting rules

Illinois’ SB 3019 was signed as part of the state budget package for fiscal year 2027, according to earlier reporting by Cointelegraph. Among other provisions, the package included a 0.2% tax on crypto transactions, which drew significant criticism from parts of the industry.

The central issue for Kalshi is how SB 3019 changes the state’s definition of an “exchange wager.” The bill amends that definition to include “an agreement, contract, transaction, or swap” that is offered, traded, or executed on a prediction market tied to a sporting contest or event. Kalshi argues this effectively subjects prediction market companies to the same kind of regulatory framework applied to sports betting operators.

In its complaint, Kalshi contends that the state legislation violates federal requirements and infringes on the CFTC’s claimed role in regulating event contracts on prediction platforms. The company’s filing describes a scenario in which following the new Illinois rules could place Kalshi in conflict with what it characterizes as the CFTC’s “uniformity requirements.”

Kalshi warns of costly compliance hurdles and enforcement risk

Kalshi’s lawsuit frames the timing and practical implications as urgent. The company says it would be “irreparably harmed” when SB 3019 takes effect on July 1 if it is required to comply.

According to the complaint, Kalshi would face a difficult choice: either stop offering its sports event contracts in Illinois to meet the new state licensing and regulatory requirements, or attempt to continue but implement complex systems to restrict access to Illinois. Kalshi argues that building and operating such technology would be expensive, and it asserts that those costs would not be recoverable even if it ultimately prevails in the lawsuit.

The filing also highlights enforcement risk. Kalshi states it cannot simply ignore the state law because an Illinois enforcement action could expose the company to criminal penalties. “Irreparable harm” in this context is tied not just to immediate business restrictions, but also to compliance engineering, operational complexity, and the legal peril of being out of step with either federal or state frameworks.

A continuing jurisdiction fight: CFTC vs. state gaming regulators

This lawsuit is part of a broader dispute that has repeatedly surfaced across U.S. jurisdictions: whether prediction markets that trade on sports outcomes are primarily regulated as commodities under the Commodity Exchange Act—or instead should be governed through state-by-state sports betting rules.

Kalshi’s complaint centers on the CFTC’s position. The filing notes the regulator’s claim that it has exclusive authority over the relevant companies because Kalshi’s “event contracts” are “swaps” within the CFTC’s jurisdiction. The CFTC has pursued legal action against state authorities that, in its view, have moved beyond their role by restricting prediction market offerings.

Earlier coverage by Cointelegraph described CFTC lawsuits aimed at state governments following prediction market laws in places such as Kentucky. In those cases, the pattern has been consistent: state gaming officials assert that prediction market contracts tied to sports outcomes should be treated like sports betting products under state frameworks, while the CFTC argues that federal commodities rules control the market structure and offerings.

Illinois’ new approach, by tying prediction market activity tied to sports events to the definition of an “exchange wager,” is expected to intensify the same federal-state tension. Kalshi’s filing suggests that the state’s method of regulation—licensing and restrictions aligned with sports wagering—collides with federal claims of uniformity and CFTC jurisdiction.

What happens next, and why the outcome matters

Experts have previously suggested that the recurring jurisdictional battles could eventually end up before the U.S. Supreme Court, given the opposing legal theories coming from federal regulators and state gaming officials. Earlier Cointelegraph reporting on the legal trajectory of Kalshi’s dispute highlighted that possibility, particularly as courts grapple with how prediction markets should be classified.

For investors, traders, and the companies building prediction market infrastructure, the stakes are practical and immediate. If more states follow Illinois’ model, platforms could face a patchwork of licensing requirements and access restrictions—while the CFTC continues to argue for a federal, uniform regulatory approach. The legal outcome will likely influence whether the U.S. prediction market landscape can scale with consistent rules or remains fragmented by state-by-state compliance burdens.

Readers should watch SB 3019’s implementation status alongside court responses to Kalshi’s claims of “irreparable harm,” because early rulings on whether the statute can be enforced—or must be paused—could set an important precedent for other jurisdictions preparing to regulate sports-linked prediction markets.

Bitcoin network activity remains close to record highs, according to CryptoQuant’s Bitcoin Network Activity Index, even though the cryptocurrency is still trading below its all-time high.

The index tracks metrics such as active addresses, transaction volumes, unspent transaction outputs (UTXOs), and demand for block space to measure actual activity on the network.

Network Usage Surges

The Network Activity Index line is rising again and is moving back toward the levels seen during the 2024-2025 peak. It remains above its 365-day moving average, further indicating that network usage is stronger than its long-term average. According to CryptoQuant’s analysis, this trend differs from previous market cycles, in which rising prices were usually the main driver attracting new users. Instead, current network growth appears to be taking place independently of BTC’s price performance.

The report said that new applications built on Bitcoin are helping drive this increase in activity. Ordinals have enabled users to permanently attach images, text, and non-fungible tokens to individual satoshis. This has created a native digital asset ecosystem on the Bitcoin blockchain. BRC-20 tokens, which use the Ordinals protocol, have also allowed the creation of meme coins and community tokens without relying on smart contracts.

Meanwhile, Runes, a token standard developed by Ordinals creator Casey Rodarmor, uses Bitcoin’s UTXO model to improve efficiency while reducing network overhead.

These developments have increased demand for block space and expanded Bitcoin’s function beyond simple payments. The crypto analytics firm added that Bitcoin is increasingly being used to store and verify data, while network adoption continues to grow even as broader market factors such as ETF flows, institutional demand, and macroeconomic conditions continue to influence price movements.

Pressure on BTC

Bitcoin was trading below $63,000 on Wednesday as investors remained cautious about risk assets. The decline was also driven by continued outflows of money from spot Bitcoin ETFs, which are now on track for a seventh straight week of withdrawals.

So far this week, US-based spot Bitcoin ETFs have recorded nearly $182 million in net outflows, adding further pressure on the crypto asset’s price.

Geopolitical risks have also not disappeared, even as US-Iran talks in Switzerland moved into a negotiation phase. Bitunix analysts believe that investors may first need to see a turning point in broader liquidity conditions for crypto to attract meaningful new inflows. In a statement to CryptoPotato, the analysts explained

“In the near term, easing geopolitical tensions should help contain energy prices. But the next phase for risk assets will be determined less by whether the Strait of Hormuz remains open and more by whether markets become convinced that the Federal Reserve is preparing for another tightening cycle. That shift suggests that market volatility in the weeks ahead will increasingly be driven by inflation reports, labor market data, and Fed policy signals rather than developments on the geopolitical front.”

The post Bitcoin’s Network Is Booming Even as Prices Remain Below Record Highs appeared first on CryptoPotato.

Crypto World

Explore how the Condorcet paradox exposes the limits of perfect fairness in blockchain consensus.

Consensus guarantees today, focus on two properties: Consistency and Liveness. Consistency requires that all nodes eventually agree on the same set and sequence of transactions, while liveness ensures the system continues to process new transactions. What they do not address is whether the agreed-upon transaction order totally reflects fairness.

In public blockchains, transaction ordering has direct economic consequences. The order in which transactions execute determines who captures value and who pays the cost, particularly as validators, block builders, or sequencers can exploit their privileged role in block construction for financial gain. This practice is known as maximal extractable value (MEV) and includes the profitable frontrunning, backrunning, and sandwiching of transactions. Prima facie, there is no obvious way to prevent MEV extracting practices because block proposers hold unilateral power over transaction ordering, and no protocol rule inherently constrains how they exercise that power.

To address this, transaction order-fairness has been proposed as a third essential consensus property. A protocol is transaction order-fair if no participant can systematically bias transaction ordering beyond what objective network conditions and protocol rules imply. By limiting how much power a block proposer has to reorder transactions, fair-ordering protocols move blockchains closer to being transparent, predictable, and MEV-resistant.

However, even this intuitive idea of fairness encounters a structural limit. In an asynchronous distributed system, there is no globally defined reception order because each node observes messages at different times, and no shared clock exists. Therefore, no protocol can guarantee execution strictly according to a single universal arrival sequence. This limitation follows from the basic constraints of distributed consensus under asynchronous communication, not from any particular design choice.

The Condorcet Paradox and the Impossibility of Perfect Fairness

The most intuitive and strongest notion of fairness is called Receive-Order-Fairness (ROF). It simply means “first-come, first-served.” ROF dictates that if most nodes receive transaction A before transaction B, then A should be processed before B.

That sounds simple and fair. However, the problem is that nodes do not all see transactions at the exact same time. Messages travel at different speeds. Some computers might receive A first. Others might receive B first. Because of this, it is impossible to guarantee perfect “first-come, first-served” fairness unless every node can communicate instantly with no delays. In real networks, that never happens.

There is also a deeper problem called the Condorcet paradox. This idea comes from voting theory. It shows that even when each person (or node in this case) has a clear and consistent order in their own mind, the group as a whole can end up with a loop that makes no sense.

For example:

- Most nodes see A before B

- Most nodes see B before C

- Most nodes see C before A

This produces a majority preference cycle (A→B→C→A), meaning no single ordering satisfies the majority view across all pairs. The network cannot construct one sequence that matches what most nodes observed first.

Because perfect ROF is unachievable under these conditions, practical systems adopt some weaker fairness guarantees as outlined in the sections below.

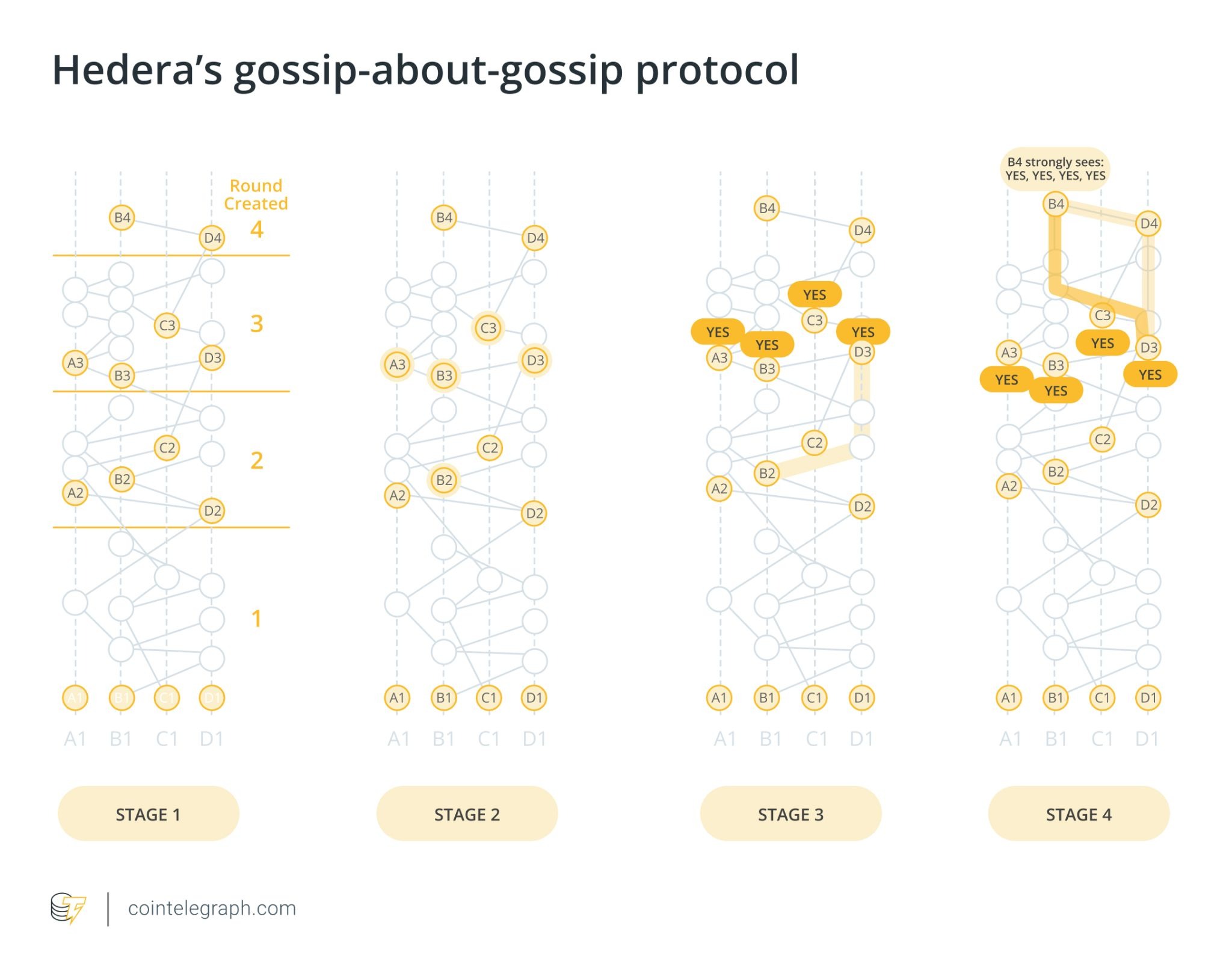

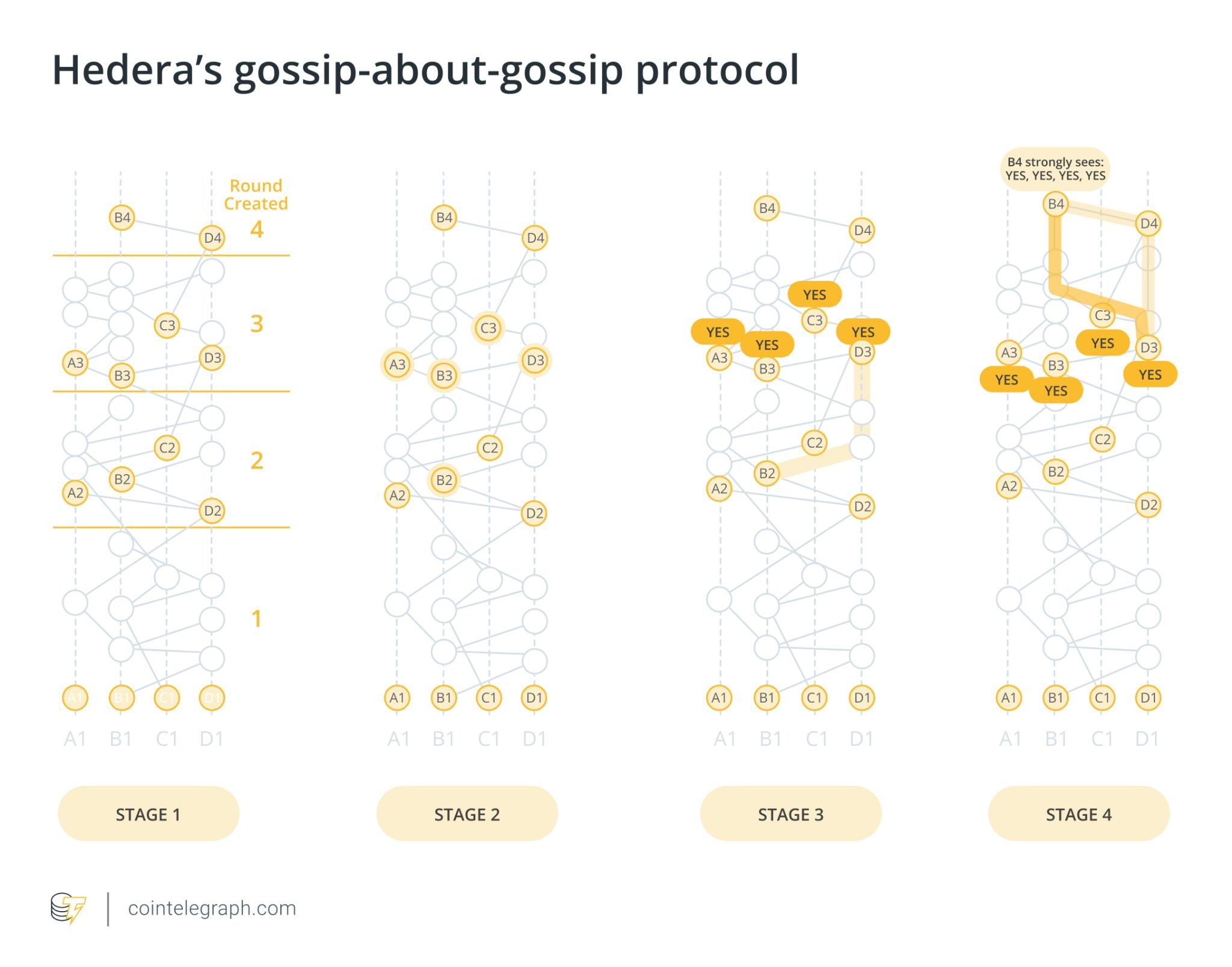

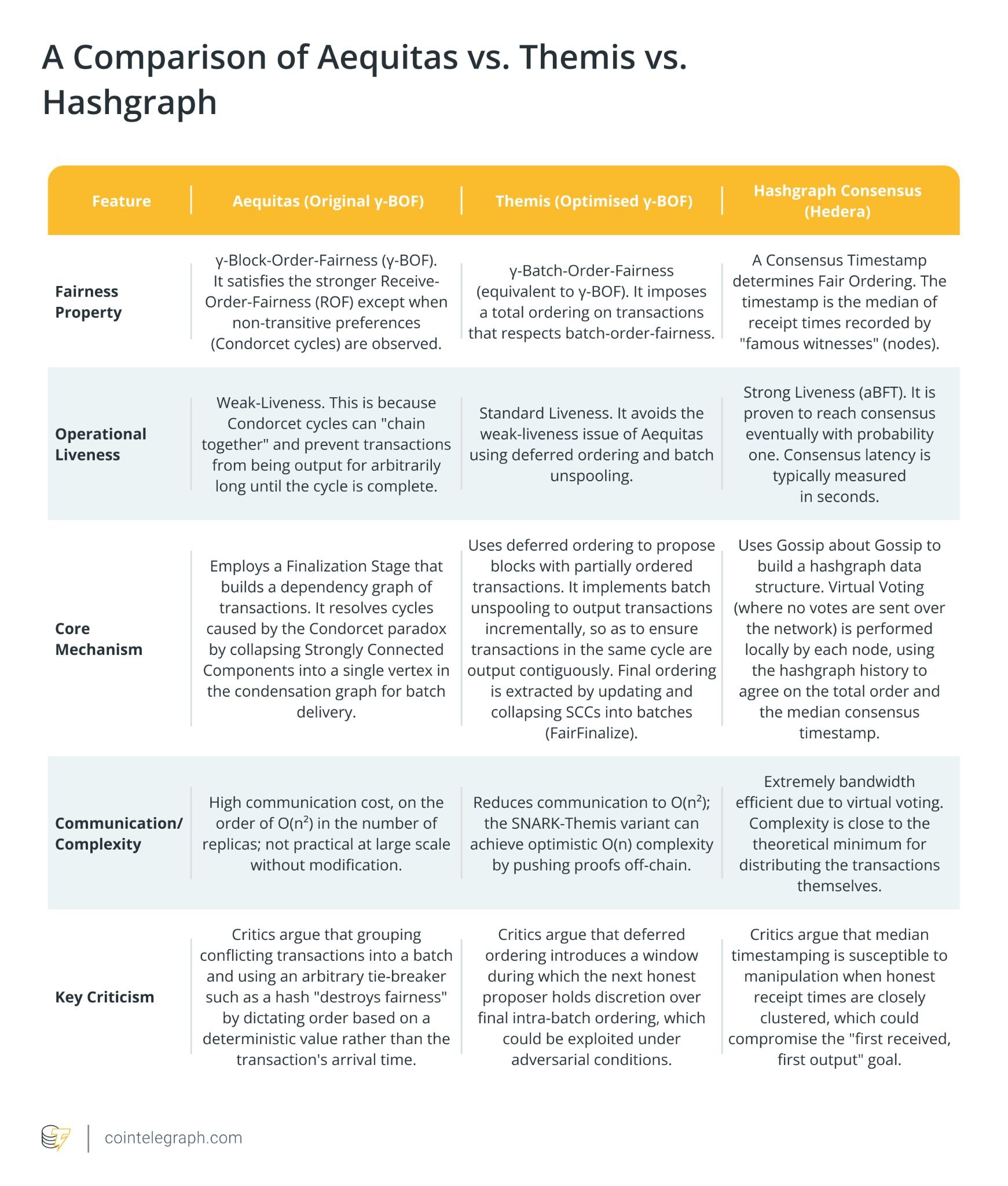

Hashgraph’s Fairness Model: Graph of Hashes, Median Timestamps, and aBFT Consensus

Hedera, which employs the hashgraph algorithm, approaches the fairness problem through a directed acyclic graph (DAG) of cryptographically linked events. It is a leaderless consensus algorithm that operates in a fully asynchronous setting and achieves Asynchronous Byzantine Fault Tolerant (aBFT). Under this model, honest nodes eventually reach agreement on the same transaction log even under unbounded message delays. Consensus ordering emerges from network-wide observation through a virtual voting process: the order is calculated collectively by nodes rather than assigned by a designated block producer.

When a node receives a transaction, it packages it into a message called an event and gossips it to peers. When another node creates a subsequent event, it records the hash of the events it has already seen and digitally signs the new event. This provides cryptographic proof that the node had seen prior events before signing the new one. The hashgraph, therefore, enforces causal order: once a node publishes an event, the ancestry embedded in that event proves which transactions preceded it.

This linkage can be represented as an edge in the DAG. If one event is a direct or indirect ancestor of another, a downward path exists between them in the graph, and the protocol provides a cryptographic guarantee that the ancestor event was created first. Transactions connected by such paths are ordered according to their causal relationships in the graph. When two events have no ancestor relationship, they are concurrent, and the protocol resolves their relative order through the round-received mechanism. Each event is assigned a round based on when a supermajority of nodes, defined as more than two-thirds, can be shown to have strongly seen it through the DAG structure. Events assigned to earlier rounds are ordered first.

For events that share the same round-received, the protocol uses median timestamps to determine ordering. Each node records a local timestamp when it first receives an event. The consensus timestamp assigned to an event is the median of the timestamps reported across the node set. This timestamp is not derived from arbitrary local clocks in isolation. It is constrained by the gossip ancestry preserved in the hashgraph: a node cannot claim to have received an event before its causal predecessors without producing a detectable inconsistency in the DAG.

Under the standard aBFT assumption that fewer than one-third of nodes are Byzantine, the median falls on an honest timestamp or between two honest timestamps, which prevents adversarial nodes from shifting the median beyond a bounded range.

The Condorcet paradox can still apply to concurrent events, specifically those with no ancestor relationship in the DAG, where different nodes may observe them in different orders. The DAG structure eliminates this ambiguity for causally linked events: no contradictory causal paths can exist because each event’s ancestry is cryptographically fixed at creation. Because gossip propagation typically causes new events to become descendants of prior events within fractions of a second, most transactions fall into clear causal chains. The remaining concurrent events are resolved through round-received assignment and median timestamps as described above.

However, the hashgraph’s fairness guarantees have a bounded adversarial surface. A node still determines when to gossip an event, which events to relay first, and how long to delay relaying. These choices reshape the first-seen patterns that feed into median timestamp computation. The DAG cannot misrepresent the causal order it records, but it can be strategically shaped by gossip behavior before that order is recorded.

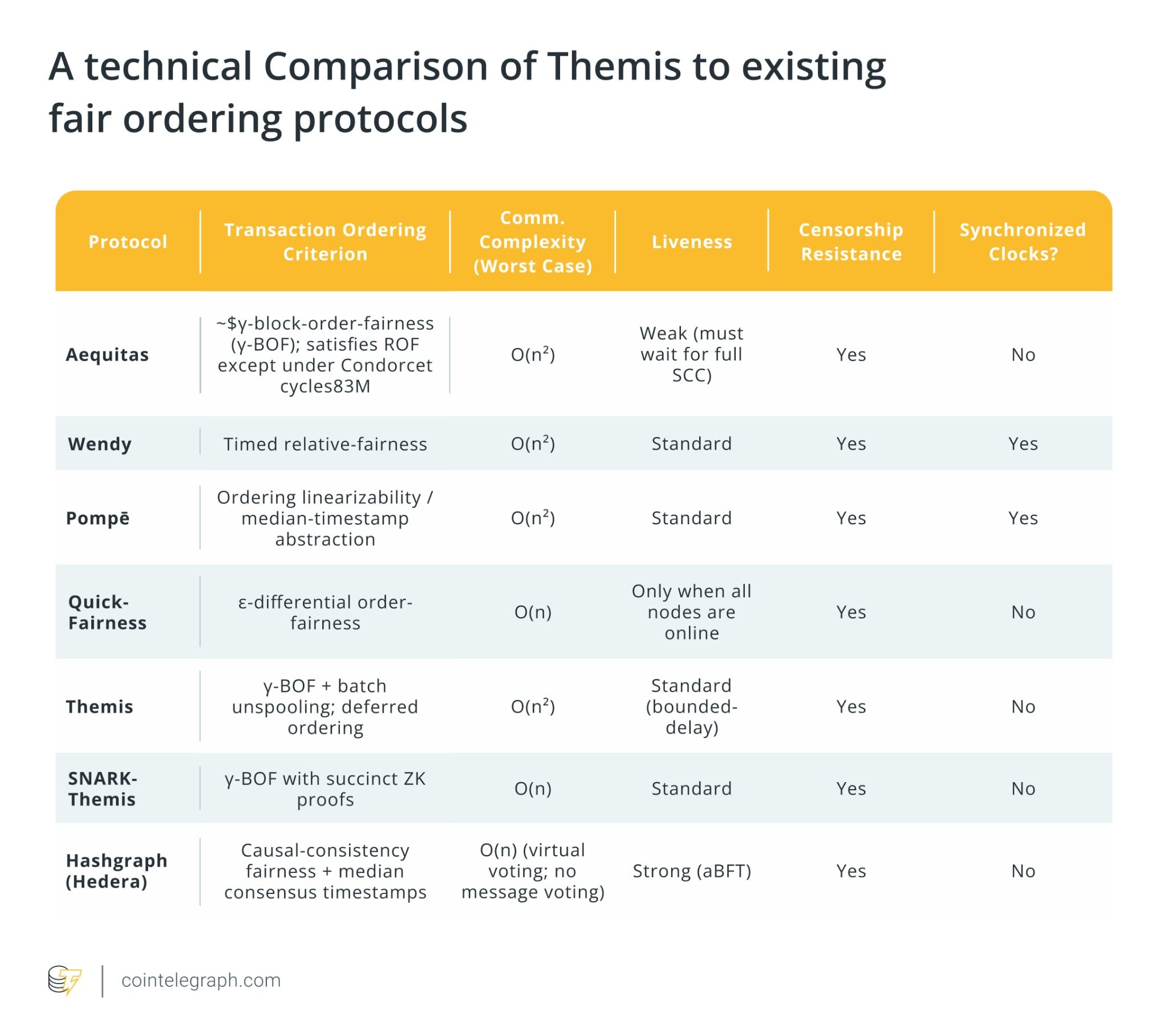

BOF Protocols: Fairness Through Batch Aggregation

BOF protocols define a “block” as the set of transactions forming a single Condorcet cycle, and then order these blocks fairly while ignoring the ordering inside the block. The BOF criterion was first introduced by Mahimna Kelkar et al. (2020) in “Order-Fairness for Byzantine Consensus,” which formalized the Aequitas family of protocols. In Aequitas, BOF requires that if a γ-fraction of nodes observe block (b) before block (b′), then no honest node may output (b) after (b′). The γ-fraction is the proportion of nodes that must agree on a block ordering for that ordering to be considered “fair” and enforced by the consensus protocol.

For BOF, if the fairness predicate indicates that a transaction tx should precede tx′, then tx cannot appear in a later block than tx′. When the fairness relation becomes cyclic, the protocol collapses the entire strongly connected component into a single block, because BOF treats that block, not the individual transaction, as the atomic fairness unit. Under γ-BOF, the only forbidden outcome is placing tx′ in a strictly earlier block than tx when a directed constraint tx→tx′ exists. The protocol permits both transactions to appear in the same block and places no restrictions on their ordering inside that block.

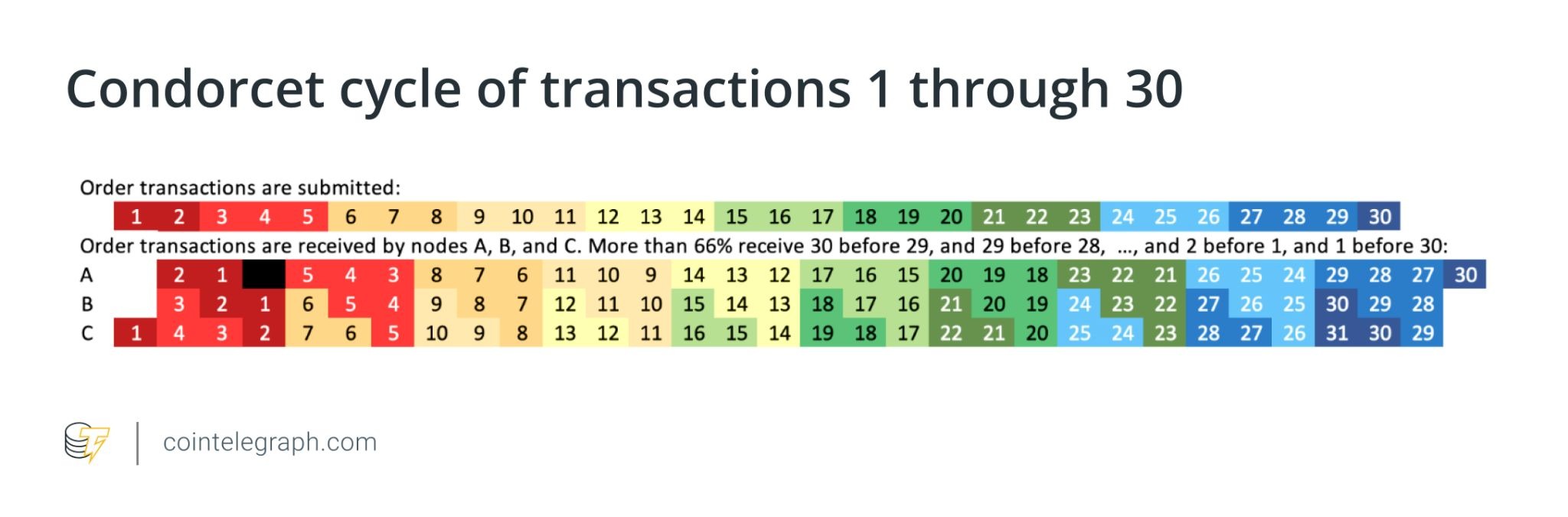

For example, Figure 2 below, is a Condorcet cycle of 30 transactions, so they would be in a single block. Sorting by hash might place 30 before 1 in the final ordering. However, a γ-fraction of nodes observed transaction 1 before transaction 30, yet placing 30 before 1 is still considered “fair” under γ-BOF. Because 1 and 30 are in the same block, and this notion of fairness only considers the order of the blocks, not the order of the transactions within a block.

When no cycles exist, BOF coincides with the strong form of ROF. When Condorcet cycles emerge, all transactions participating in the cycle are placed into a single block, and a deterministic method, such as a hash-based rule, orders events within that batch.

The protocol proceeds through three coordinated stages to ensure consistent transaction ordering across the network: the Gossip stage, the Agreement stage, and the Finalization stage.

In the gossip stage, nodes use FIFO broadcast to disseminate transactions in the order they were locally received per sender, preserving per-sender sequence so that each peer maintains a comparable transaction view. Once gossiping stabilizes, the agreement stage begins, where nodes execute a Set Byzantine Agreement (Set-BA) protocol to reach consensus on a unified set of local orderings that will serve as the foundation for the global order. In the finalization stage, nodes construct a dependency graph that captures transaction ordering relationships. Any transactions forming a cycle within this graph are grouped into the same strongly connected component and finalized together within a block.

However, Aequitas suffers from weak liveness, as its high communication cost and strict fairness constraints require the protocol to wait for the entire Condorcet cycle before finalizing the collapsed SCC. Because Condorcet cycles can chain indefinitely, this waiting period can grow without bound. Thus, transaction delivery can be delayed for an arbitrarily long time, and creates the “freeze” risk that defines Aequitas’ weak-liveness guarantee.

Themis was introduced to solve this. It preserves the same γ-BOF property while resolving these liveness and communication issues. Like Aequitas, Themis also constructs a dependency graph and collapses SCCs during its “FairFinalize” stage. The SCCs represent the same non-transitive Condorcet cycles underlying the γ-BOF relaxation, and Themis uses the condensation graph to derive the batch structure of the final output. The key difference is that Themis does not wait for a full cycle to complete. Instead, it uses deferred ordering and batch unspooling to output SCCs incrementally while allowing new transactions to continue flowing. This preserves γ-BOF but upgrades Aequitas’ weak liveness to standard liveness, and guarantees delivery within a delay bound.

In its standard form, Themis requires each participant to exchange messages with most other nodes in the network. As the number of participants increases, the amount of communication grows rapidly, roughly proportional to the square of the network size. However, in its optimized version, SNARK-Themis, nodes use succinct cryptographic proofs to verify fairness without needing to communicate directly with every other participant. This reduces the communication load so that it grows only in direct proportion to the number of nodes, thus allowing Themis to scale efficiently even in large networks.

If a malicious proposer attempts to exploit the situation by proposing an empty block, Themis employs deferred ordering, where the partially ordered batch (B₁) is still accepted, and the final, precise order of its transactions is determined later by the next honest proposer. That proposer finalizes the order based on verifiable transaction relationships, not personal discretion. This design ensures finalization depends only on bounded network delay, not on the arbitrary behavior of the current proposer, thus closing a key liveness gap that Aequitas could not guarantee.

This structure guarantees that every transaction is both included and executed deterministically, even in the presence of conflicting arrival orders. Because Themis leverages the internal dependency graph and SCC condensation to extract a final ordering, it is resilient to adversarial manipulation. Attackers cannot simply reorder or front-run other users’ transactions once they are included in the batch. Any attempt to alter dependencies would break the verified graph consistency.

In an empirical analysis by Mahimna Kelkar et al., γ-BOF resists adversarial reordering more strongly than timestamp-based approaches in geo-distributed networks. However, it requires significantly more computational and protocol complexity, which can also be seen as a downside.

Conclusion:

Perfect fairness in transaction ordering is structurally unattainable in distributed systems that lack synchronized clocks and instantaneous communication. The Condorcet paradox ensures that majority preferences can conflict in ways no single linear order can satisfy. The real question is how to find the most realistic and useful trade-offs.

Hashgraph and BOF represent two coherent answers. Neither approach is inherently superior. Both embed fairness directly into the consensus mechanism rather than relying on trust or authority. Both approaches demonstrate that fairness is not a binary property but a spectrum of trade-offs defined by formal impossibility results. Where synchrony is unavailable, and clocks are untrusted, the choice between median-timestamp aggregation and batch-order collapsing reflects different but equally principled responses to the same underlying constraint.

[Update 14:47 UTC, June 24: Updates with comments from Binance beginning in first paragraph.]

Crypto exchange Binance is withdrawing its MiCA application with Greece’s Hellenic Capital Market Commission (HCMC) and intends to pursue authorization in another member state just days before the deadline for EU licensing.

“When we are ready to announce that Member State, we will do so publicly,” the company said in a statement on Wednesday.

Earlier, Gillian Lynch, Binance’s head of Europe and the United Kingdom, told Reuters that the exchange is “not leaving Europe” and would pursue authorization in another EU jurisdiction if its application in Greece does not move forward.

Lynch said Binance contacted other regulators but submitted a formal application only in Greece. The exchange reportedly held talks with Ireland, Latvia and Greece but encountered resistance over its past money-laundering penalties, international structure and what officials viewed as a risk-taking culture.

The move comes days before the Markets in Crypto-Assets Regulation (MiCA) transitional period ends on July 1, a key deadline for crypto firms seeking to operate across the EU. The European Securities and Markets Authority (ESMA) said on Tuesday that crypto service providers that remain unauthorized by the deadline must take “immediate” steps to wind down their EU activities.

On June 16, Binance pushed back against an earlier Reuters report that EU regulators were preparing to reject its MiCA application, saying Greece’s Hellenic Capital Market Commission had reviewed the application and considered it compliant, subject to further review by ESMA. The exchange said at the time that it expected the process to advance toward authorization.

EU customers could see changes

In its statement, Binance said it plans to take the necessary steps before July 1 to remain “compliant with applicable requirements.”

“This means some users may be impacted, and we will communicate directly with affected users to provide clear information on next steps,” the representative said. “All user funds remain safe and secure. Our priority is to minimize disruption, provide clarity to users, and continue building a trusted and compliant digital asset ecosystem globally.”

The representative did not provide additional details.

MiCA deadline puts Binance’s European reach at risk

On Monday, CryptoQuant analyst Maartunn told Cointelegraph that euro-denominated pairs account for about 1% of Binance’s global spot trading volume, suggesting that a European licensing setback may have a limited effect on the business.

Source: CryptoQuant

However, Binance remains a significant trading venue for European users, handling between about $100 million and $250 million in daily euro-pair volume in 2026, with occasional spikes of about $600 million.

Binance held an estimated 18.5% share of euro-denominated spot trading during the year, placing it second behind Kraken’s 43.3% share, according to CryptoQuant’s data.

Exchanges emerge as MiCA compliance gatekeepers

Binance’s licensing difficulties could also affect token issuers, as authorized exchanges increasingly prepare and notify MiCA white papers for assets they list.

In a LinkedIn post, Ryan King, creator of the EU Crypto Register, said at least 380 of 867 white-paper entries he tracked were notified by third parties rather than token issuers. He said Kraken, LCX, OKX and Bitstamp accounted for 271 notifications, or about 31% of the total.

Related: Binance’s Yi He warns of alleged impersonation scam, CoinUp denies ties

King told Cointelegraph that the model was “symbiotic” because exchanges employ MiCA-trained compliance teams, maintain regulator relationships and retain large law firms. He added that exchanges increasingly request white papers during onboarding and may offer to prepare them, even for tokens covered by transitional arrangements.

“They also use standard templates,” King told Cointelegraph, recalling that one exchange told a token project to “fill it in and we’ll handle the rest.”

Magazine: Japanese pension fund tips 1% in crypto, G7 urges action on NK hackers: Asia Express

World Cup 2026: Bosnia boost knockout hopes after dominant win over Qatar

GTA VI Is a Worrying Sign For the Future of Physical Games

Crypto’s Public Market Disaster

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Miami – Corporette.com

-

Entertainment4 days ago

Entertainment4 days agoRenter of Home in Anne Heche Crash Denies Settlement With Son

-

Tech2 days ago

Tech2 days agoMicrosoft accidentally kills epic Outlook email threads

-

Sports1 day ago

Sports1 day agoTwo goals and an assist by sheer aura: Cristiano Ronaldo just entered the World Cup chat

-

Business4 days ago

Business4 days agoSoccer-U.S. defends Iran World Cup travel restrictions, says discussions ongoing

-

Politics6 days ago

Politics6 days agoBBC Reporter Discusses Cross Party Criticism Of Trumps Iran Deal

-

Crypto World18 hours ago

Bitcoin (BTC) Dips Below $62K, Ethereum (ETH) Plunges 6% Daily: Market Watch

-

Crypto World15 hours ago

Crypto World15 hours agoSecuritize Wraps Roubini's SEC-Registered ETF as Dubai VARA Digital Security

-

Business21 hours ago

Entergy settles forward sale agreements, raises $672 million in cash proceeds

-

Politics5 days ago

Politics5 days agoAndy Burnham and the meaning of Makerfield

-

Business5 days ago

Business5 days agoWall Street Week Ahead: Investors see Micron earnings as pulse check of AI rally momentum

-

NewsBeat5 days ago

NewsBeat5 days agoKeir Starmer Allies Question His Chances For No 10

-

Tech6 days ago

Tech6 days agoAWS enters the context layer race with a graph that learns from agents, not manual curation

-

Crypto World4 days ago

Crypto World4 days agoCan Charles Hoskinson Really Rescue Cardano?

-

Crypto World5 days ago

Crypto World5 days agoHIVE shares jump as $220M AI deal speeds Bitcoin mining pivot

-

Crypto World4 days ago

Crypto World4 days agoJake Chervinsky accuses CME of protecting derivatives monopoly

-

Tech3 days ago

Tech3 days agoSignal’s Meredith Whittaker says AI chatbots ‘are not your friends’ and calls Copilot agents a backdoor

-

Entertainment5 days ago

Entertainment5 days agoJose Alvarado Wants Taylor Swift at More Knicks Games

-

Tech2 days ago

Tech2 days agoNearly 7,000 fake Amazon domains registered ahead of Prime Day 2026, researchers warn

-

Business6 days ago

Business6 days agoBrexit cost 6% of UK economy, Bank of England company data suggests

You must be logged in to post a comment Login