Crypto World

Trump Mobile buyers stuck without phones as TRUMP token sits 97% below peak

Two Trump-branded ventures aimed at retail buyers are both in difficult positions months after their debuts, though for different reasons.

Roughly 600,000 buyers have paid $100 deposits for the gold-colored Trump Mobile T1 phone since its initial announcement, putting around $60 million into a venture that has not delivered a single confirmed device as of May 2026, per Moneywise.

Deposits were paid to Trump Mobile’s registered company T1 Mobile LLC, which uses a limited liability agreement from DTTM Operations, LLC – the company that manages intellectual property, trademarks, and likeness on merchandise associated to U.S. president Donald Trump.

Wow those Gold Trump phones that 590,000 people paid a $100 deposit on still haven’t been delivered after told they would be by September so NBC who bought one tried to call the Company & there’s no phone number only a email.They asked if they could get a refund & were told NO!😂 pic.twitter.com/EucWcjyorm

— Suzie rizzio (@Suzierizzo1) November 26, 2025

Promised delivery dates have slipped from late summer 2025 to November, then to December, and finally to first-quarter 2026, before being removed from the website entirely.

According to IBTimes reporting, the company updated its terms of service in April to clarify that deposits represent a “conditional opportunity” to buy the device if the company chooses to sell it, removing any binding contract. (CoinDesk has not independently reviewed the previous version of the terms.)

Trump Mobile did not respond to a request for comment send by email as of publication time.

The TRUMP memecoin, a separately structured venture, has had its own difficult run. The token launched in January 2025 at $1.21, zoomed to $73 within 48 hours as retail speculators piled in around the inauguration, and has spent the 16 months since grinding lower.

TRUMP traded at $2.45 on Monday, down roughly 97% from its peak and 82% on the year, CoinGecko data show. Chainalysis estimated retail investors in TRUMP have collectively lost roughly $2 billion since its introduction.

TRUMP launched with 80% of supply held by Trump-affiliated entities CIC Digital and Fight Fight Fight, with those tokens scheduled to unlock at approximately $500,000 worth per day (at current prices) through mid-2028. The schedule was disclosed as part of the token’s launch terms, but has produced sustained sell-side supply during a period of declining buyer interest.

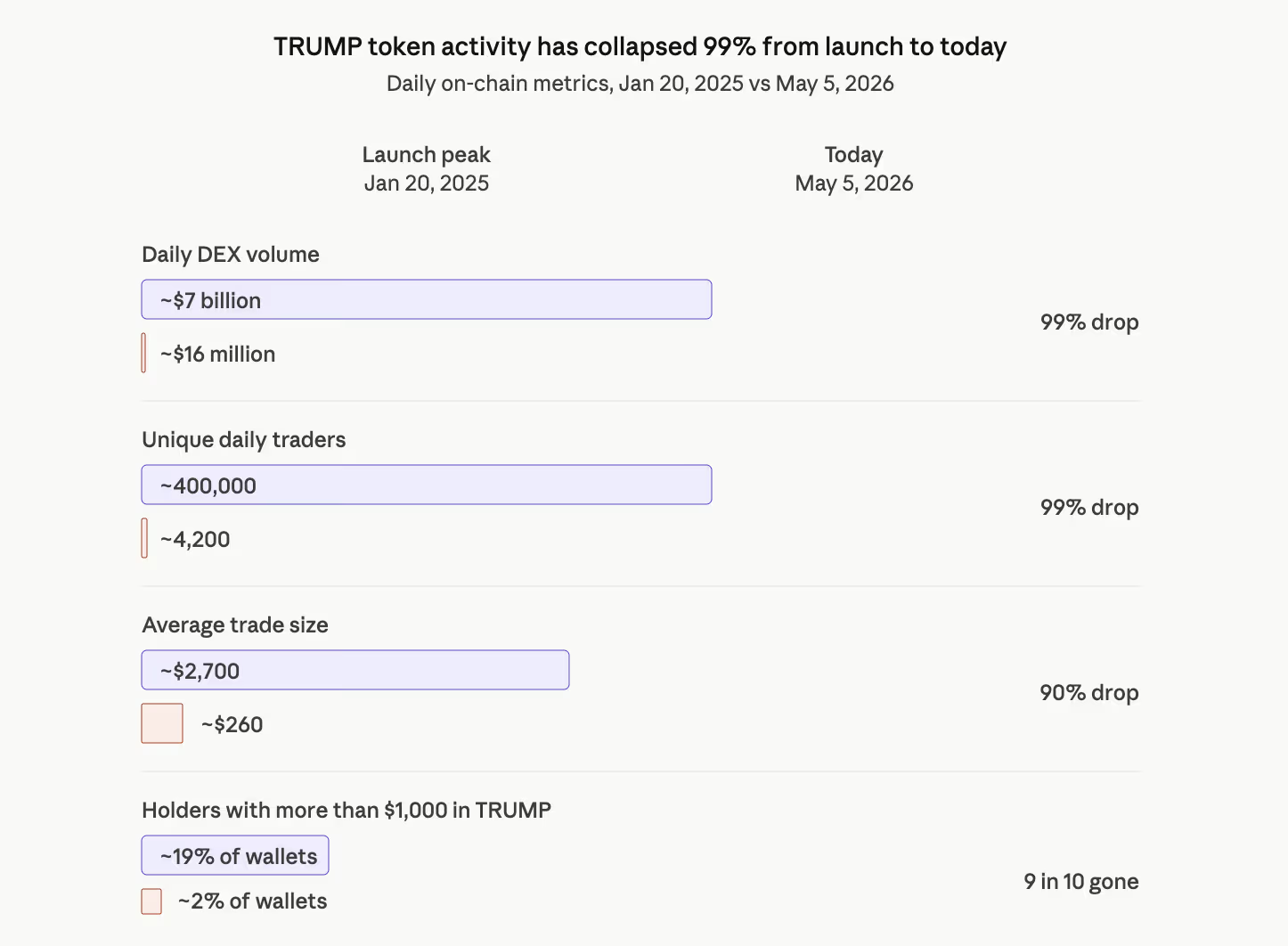

TRUMP’s daily DEX trading volume has dropped from a January 20, 2025 peak of nearly $7 billion across roughly 400,000 traders to about $16 million across just 4,200 traders on May 5, 2026, per Dune Analytics data tracked by user @seoul.

That is a 99% drop in both daily turnover and unique daily participants. Average trade size has fallen from around $2,700 to $260 over the same period, suggesting the remaining buyers are smaller retail accounts rather than the larger speculators who drove the original launch.

The share of TRUMP holders with more than $1,000 in the token has collapsed from roughly 19% at launch to about 2% today, meaning almost every remaining wallet now holds less than $1,000 worth of TRUMP. The token has effectively settled into a long tail of small bag-holders with no large position holders left to drive meaningful price action.

For TRUMP holders, the onchain math suggests that a return to launch-era valuations is becoming increasingly unlikely. At current prices, the remaining insider token unlocks represent more than $2.5 billion in potential supply overhang.

Absorbing that supply would require a demand event larger than anything the token has seen since launch, with the token down 13.6% over the past 30 days and roughly 0.1% on the day.

A dinner hosted by Trump for the top 220 token holders at his Virginia golf club in May 2025 produced a rally that faded within weeks. Tron founder Justin Sun pledged $100 million in TRUMP purchases ahead of the July 2025 unlock, with the token continuing to drift lower in the months that followed.

A separate Mar-a-Lago Crypto & Business Conference on April 25, 2026, limited to the top 297 TRUMP token holders with VIP access for the top 29, drew a letter from Senators Warren, Adam Schiff (Democrat, California), and Richard Blumenthal (Democrat, Connecticut) requesting documents about the President’s role in promoting the event.

While Trump tokens and the mobile ventures have different structures and mechanisms, they debuted on the back of front-loaded political enthusiasm, and have struggled in the months since to translate that initial momentum into either delivered product or sustained price support.

The U.S. Commodity Futures Trading Commission has unveiled a draft rule proposal for prediction markets, signaling a nuanced stance on the treatment of contracts tied to real-world events. The document indicates that sports-event contracts based on final scores and win-loss records may be permissible as price-discovery mechanisms under the public-interest standard, while bets linked to injuries, officiating decisions, or other outcomes that could invite manipulation are unlikely to meet that standard. The proposal also states that election contracts are not considered “gaming” under applicable federal law, a distinction that could reduce regulatory uncertainty for platforms such as Kalshi and Polymarket. The public comment period is set at 45 days, signaling a potential shift in how the United States defines and governs prediction markets going forward.

According to Reuters, the draft rules are intentionally principles-based rather than a blanket green light; each contract would still undergo a case-by-case public-interest analysis. The agency emphasizes that predication markets could play a legitimate role in price formation, but that not all event-based contracts will qualify. This approach reflects a broader regulatory aim to balance market innovation with safeguards against manipulation or consumer harm.

The push comes as platforms in the prediction-market space have gained traction with both retail and institutional participants. Kalshi and Polymarket, which surged in prominence during the 2024 U.S. presidential race, have seen their profiles rise as investors seek alternative channels for hedging and information discovery. The draft rules’ openness to categorizing certain event contracts as permissible could accelerate regulatory clarity for operators seeking to align with a formal public-interest standard.

The proposal’s impact on the legal status of event contracts was underscored by discussions with industry practitioners. Gary Kalbaugh, a partner at Cahill Gordon & Reindel LLP, described the framework as principles-based and contingent on a per-contract assessment. “Gaming is defined broadly enough to encompass sports events, but contracts that settle on aggregate outcomes—such as final scores or season statistics—are presumptively permissible,” he observed in commentary surrounding the draft.

Source: Gary Kalbaugh

Key takeaways

- The CFTC’s draft rule framework treats certain sports-event contracts—based on aggregate outcomes like final scores or win-loss records—as presumptively permissible under the public-interest standard, while contracts tied to injuries or officiating decisions face heightened scrutiny for potential manipulation.

- Election contracts are not considered gaming under the relevant federal laws, a designation that could reduce regulatory uncertainty for prediction-market platforms operating in the U.S.

- The rules are open for a 45-day public comment period and are described as asset-class oriented, signaling a potential shift in how prediction markets are categorized and overseen.

- Industry momentum remains robust, with Kalshi and Polymarket achieving high valuations and expanding institutional collaborations, including partnerships with Nasdaq and Dow Jones that integrate prediction-market data into broader market workflows.

- Analysts and academics emphasize a growing need to resolve whether event contracts are financial instruments or gambling instruments, a distinction with meaningful regulatory and compliance implications.

Regulatory stance and scope of the proposal

The draft rules articulate a clear distinction between types of event-based contracts, anchored in the mechanics of the underlying outcomes. Contracts tied to final scores, win-loss records, or other aggregate statistics are positioned as potential instruments for price discovery in efficiently priced markets. By contrast, contracts that could incentivize manipulation—such as those hinging on injuries, officiating judgments, or other sensitive event facets—may fail to satisfy the public-interest test. This nuanced approach reflects a tailored assessment rather than a universal endorsement or rejection of prediction-market activity.

Crucially, the proposal confirms that election contracts do not fall within the gaming category under federal law. This interpretation could reduce regulatory ambiguity for platforms that pivot to election outcomes, allowing for a more stable licensing and compliance pathway as operators expand their product offerings. The public-interest framework is described as case-by-case, meaning that even contracts based on seemingly permissible aggregate outcomes would still require a thoughtful, contract-specific evaluation by regulators before market access is granted.

Industry observers note the emphasis on a principles-based regime, which aims to balance innovation with investor protection and market integrity. The open-ended nature of the framework invites comments from a broad set of stakeholders, including exchanges, financial institutions, legal counsel, and researchers, potentially shaping a more mature U.S. regulatory regime for prediction markets.

From a legal and policy perspective, the proposal aligns with ongoing efforts to harmonize the treatment of market-based information tools with broader securities and derivatives frameworks, while maintaining safeguards against manipulation and fraud. While the draft does not provide a final license blueprint, it signals the CFTC’s willingness to define clear boundaries around permissible and impermissible market structures in this evolving space.

Market momentum and institutional engagement

The regulatory attention arrives as prediction markets have seen a surge in adoption and strategic collaboration. Kalshi and Polymarket now occupy prominent positions in this niche, with valuations reflecting substantial investor interest in market-based forecasting tools. The landscape has broadened beyond pure retail participation to include institutional interest and cross-sector partnerships that embed prediction-market data into traditional information ecosystems.

Notably, Kalshi has forged a collaboration with Nasdaq to launch a new category of prediction markets that allows forecasting of private-company valuations ahead of private financing rounds and potential IPO milestones. This initiative signals a practical pathway for using event-driven contracts to glean forward-looking signals about private markets, expanding the traditional suite of commodity- and equity-linked contracting.

Polymarket has partnered with Dow Jones to integrate real-time prediction-market data into its media brands, including The Wall Street Journal, illustrating how market-derived probabilities can inform financial journalism and decision-making processes. These partnerships demonstrate a trend toward mainstreaming prediction-market data as a source of dynamic information for investors, researchers, and policymakers alike.

Academia and research firms have commented on the practical significance of these developments. Melinda Roth, a professor of sports law and corporate finance at Georgetown University Law Center, notes that the central question remains whether event contracts should be treated as financial instruments or as gambling instruments. As markets grow and scale, the regulatory overlay will influence how institutions structure risk, comply with KYC/AML requirements, and manage legal risk across borders.

Industry analysts have also highlighted a broader shift toward institutional adoption. Bernstein’s researchers point to growing appetite among sophisticated market participants seeking hedge-like tools and macro-risk hedges through binary or probabilistic contracts. The rising integration of prediction-market data into traditional market infrastructure—whether for hedging, forecasting, or risk management—suggests that these markets are moving from a niche activity toward standard practice in some research and risk-management workflows.

As the sector expands, questions about market integrity, insider information, and governance persist. Academic and professional discourse emphasizes the need for robust compliance frameworks that address potential biases, conflicts of interest, and the risk of insider trading on event outcomes. The continued collaboration with media outlets and financial data providers also elevates the importance of reliable data feeds and transparent methodology to ensure that market signals remain credible and auditable.

Reuters notes that the CFTC’s approach to these markets could influence how other regulators view similar products, particularly in cross-border contexts where licensing, AML/KYC regimes, and consumer protections vary. The evolving policy environment underscores the importance for platforms and participants to align with evolving enforcement priorities, maintain clear governance structures, and implement rigorous surveillance to mitigate manipulation and fraud risks.

While the 45-day comment window leaves time for stakeholder input, the draft represents a meaningful step toward defining a stable regulatory framework for prediction markets in the United States. The outcome could shape licensing pathways, audit requirements, and enforcement expectations for exchanges and firms seeking to operate sophisticated, event-based markets on a compliant footing.

Related developments, including legal scholarship and industry analyses, continue to scrutinize whether these instruments function more like financial products or as forms of gambling, a distinction with material implications for investor protection standards and market oversight.

In the broader policy arena, the CFTC proposal intersects with ongoing conversations about how to regulate emerging data-driven markets while preserving innovation. The question of cross-border activity—where U.S. rules may diverge from other jurisdictions—adds another layer of complexity for platforms seeking global reach.

Overall, the proposal signals a pragmatic path forward: acknowledge predictive value in aggregated outcomes, guard against manipulation in sensitive event dimensions, and provide a regulatory corridor that could foster legitimate use cases in institutions and markets, while preserving the integrity of price discovery frameworks.

Closing note: as market participants prepare comments and refine product designs, the evolving regulatory dialogue will likely shape licensing regimes, compliance controls, and how these markets are integrated into traditional financial ecosystems.

What to watch next: how the CFTC finalizes the framework, the treatment of specific contract types, and the degree to which institutions adopt prediction-market tools within compliant, auditable risk-management architectures.

Robinhood Securities said it had secured approval to act as an IPO underwriter, moving from a distribution role into the main underwriting group alongside Wall Street banks.

Chief executive Vlad Tenev said in a Tuesday X post that Robinhood Securities is “now approved to serve as an underwriter,” without specifying which regulator granted the approval, a process that typically involves oversight from the Securities and Exchange Commission (SEC) and the Financial Industry Regulatory Authority (FINRA).

Framing the move as the “natural next step” after launching IPO Access in 2021, Tenev said the question in equity capital markets had shifted from “why allocate to retail at all?” to “how big can the allocation be?”

Robinhood secures underwriter status. Source: Vlad Tenev

His comments land as SpaceX reportedly considers making as much as 30% of its record-setting offering available to retail investors and as demand already runs at close to four times the planned size.

Crypto rails race for SpaceX

Robinhood’s push to sell IPO shares directly to app-based traders comes as crypto platforms race to build parallel rails around the same listings.

Major exchanges have begun offering alternative access to private markets through tokenized pre-IPO products, including Bybit’s xStocks, Kraken’s pre-IPO equity tokens and Coinbase’s secondary markets.

On the derivatives side, a Tuesday report from Talos and Coin Metrics argues that onchain pre-IPO perpetuals are becoming a meaningful price discovery venue in their own right.

Liquidity is increasingly a hybrid of retail traders, crypto-native funds and systematic market makers, according to the report, with SpaceX contracts on Hyperliquid generating billions in volume and hundreds of millions in open interest.

Related: Crypto entrepreneur Chun Wang joins SpaceX mission to Mars

The report highlights Cerebras Systems, where Hyperliquid’s pre-IPO futures tracked the stock’s eventual opening level within about 1%, while underwriters priced the IPO itself far lower.

Samar Sen, vice president of international markets at Talos, told Cointelegraph that underwriters and retail platforms like Robinhood are increasingly likely to monitor these signals for high-profile listings as a supplementary input for assessing demand, though not as a replacement for traditional book-building.

For an underwriter, pre-IPO perpetuals are “unlikely to determine retail versus institutional allocations on their own, but they can provide an additional signal around investor demand ahead of listing,” he said.

Magazine: How to fix suspected insider trading on Polymarket and Kalshi

A Citibank logo is displayed on a sign at one of their branches on Nov. 7, 2025 in Encinitas, CA.

Kevin Carter | Getty Images

Citigroup outperformed the broad market as well as some other major bank stocks Wednesday after President Donald Trump lauded the bank and its CEO Jane Fraser in a social media post.

At 9:30 a.m. ET, Trump praised Citigroup on Truth Social, writing: “Wow! CITI was ranked Number 1 in topping M&A Advisory Market by Value in Q1. Congratulations to Jane F and ALL of her great people. They’ve worked really hard! BIG comeback for CITI!!! President DONALD J. TRUMP”

The president’s post went up just as the stock market was opening, and at one point Citigroup shares touched a high of $137.12, up almost 1.8%. By the end of the day, however, Citi fell 1%, still less than JPMorgan and Goldman Sachs and the S&P 500.

It wasn’t immediately clear which investment banking league rankings President Trump was referring to. So far in 2026, for example, Goldman Sachs, JPMorgan, Morgan Stanley and BofA Securities all rank ahead of Citigroup in the latest Global M&A Advisor Ranking on Dealogic, a leading financial analytical platform.

While Goldman Sachs was the lead advisor on 196 deals worth a combined $992.3 billion this year, Citi was the lead on 97 deals worth $285.3 billion.

In fact, according to Dealogic, Citigroup has fallen to number 5 among leading mergers and acquisitions advisors in 2026, down from number 4 in 2025.

Leon Kalvaria, Citigroup’s global chair for banking, appeared on Fox Business News early Wednesday, where he was asked about Citi’s position as the leading advisor on power sector deals. Citi advised on four deals worth a combined $41.4 billion in the energy industry so far in 2026, according to Global Data Financial Deals Database.

What is clear is that Citigroup stock has outperformed the S&P 500 this year, climbing 14.3% against an S&P 500 gain of 6.2%, according to FactSet data. By contrast, Wells Fargo is down 12.1%, JPMorgan is lower by 4.1% and Bank of America is off 1% in 2026. Goldman is 13.9% higher, also trailing Citi.

Citigroup is in the midst of a multiyear turnaround under Fraser, involving streamlining business units, cutting jobs and focusing on high-margin markets and services. The stock has risen for three straight years after jumping more than 70% in 2025, almost 42% in 2024 and 19% in 2023.

Crypto World

Kalshi Reports 150+ Insider-Trading Investigations in Q1, Rolls Out Employer Checks for High-Risk Markets

Kalshi opened more than 150 insider-trading investigations in the first quarter of 2026, blocked over 100 potential insider trades using automated screening tools, and referred at least 20 cases to law enforcement. The CFTC-regulated prediction market paired the numbers Tuesday with three new… Read the full story at The Defiant

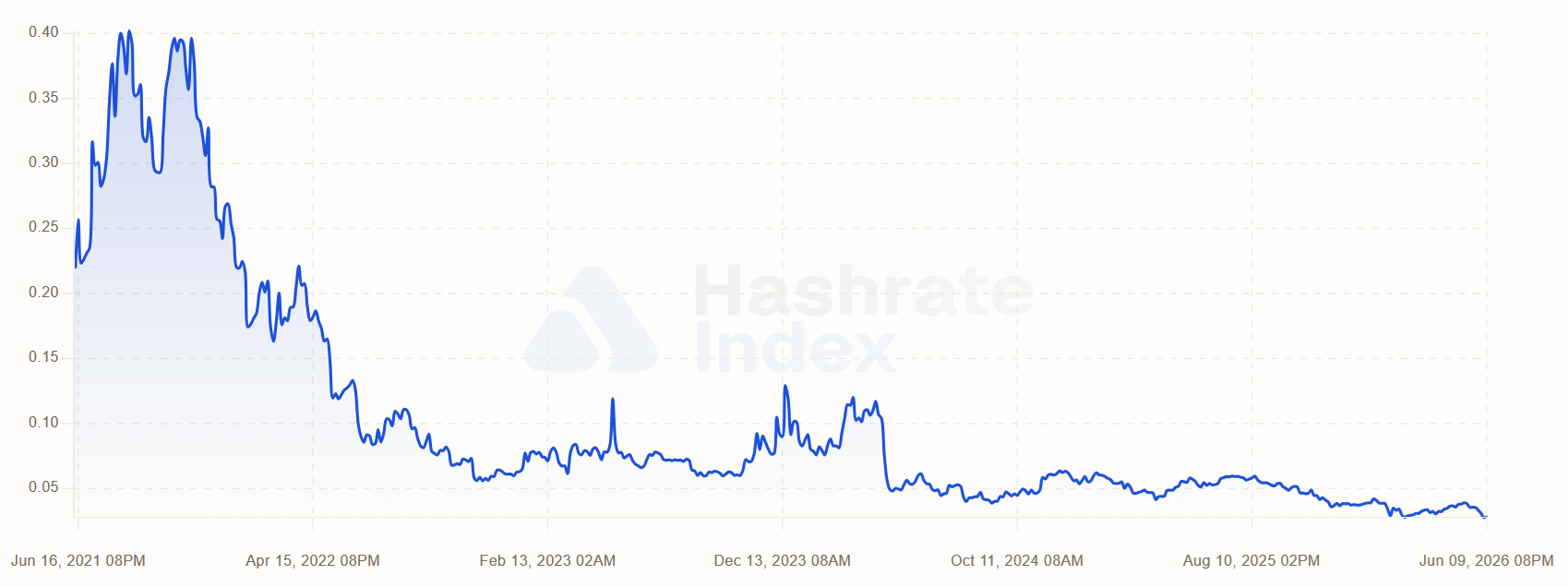

Bitcoin’s mining economics tightened further as on-chain activity cooled and miner revenues hit fresh lows. The Luxor Hashrate Index now estimates the daily return for 1 terahash per second of hashing power at just $0.28, down from $0.39 a month earlier, underscoring a profitability squeeze for operators who still hold substantial BTC exposure—the combined holdings of miners and mining pools exceed $110 billion in Bitcoin.

Meanwhile, a shift in demand toward AI infrastructure is influencing how miners allocate capital. Bernstein analysts have argued that the primary bottleneck for scaling AI data centers is electricity, a constraint that has prompted some miners to repurpose parts of their power assets to support AI workloads rather than pure mining. On the hardware profitability front, the estimated monthly gross profit for an Antminer S21 XP Hydro at an electricity rate of $0.07 per kilowatt-hour has slipped to about $137, from $192 last month.

Bitcoin’s price drifted toward the $60,000 level as these dynamics played out, with uncertainty about whether the market can sustain a meaningful move higher given the backdrop of cooling on-chain activity and tightening mining economics. The broader narrative remains that AI demand is reshaping how mining infrastructure is deployed, even as spot BTC demand from institutions continues to influence price formation.

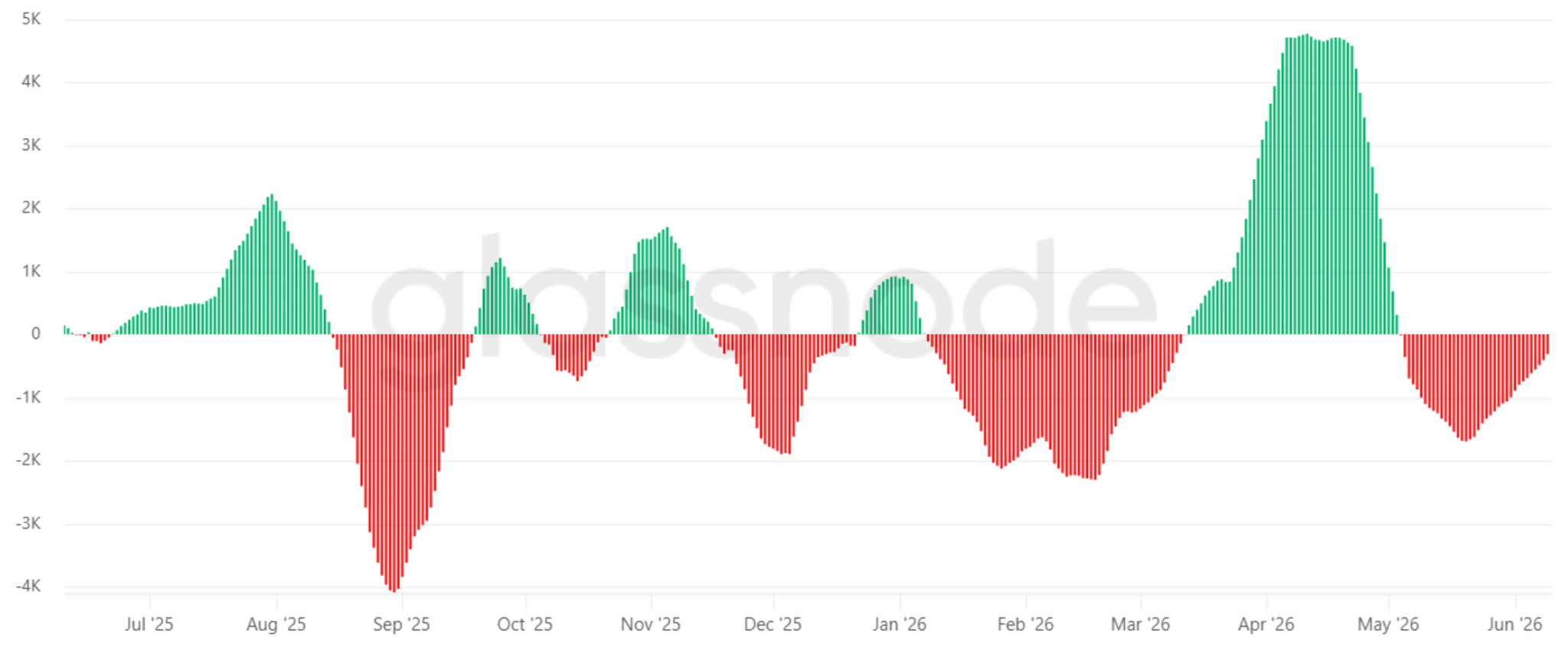

The on-chain picture also shows miners tightening liquidity. The 14-day average net position change for Bitcoin held in miner and mining pool addresses turned negative in early May and has stayed in the red since, a signal that liquidations or withdrawals from these addresses are persisting as operators fund ongoing operations or pursue balance-sheet adjustments. This dynamic adds a heavy drag on Bitcoin’s price discovery, even as macro factors attract other market participants.

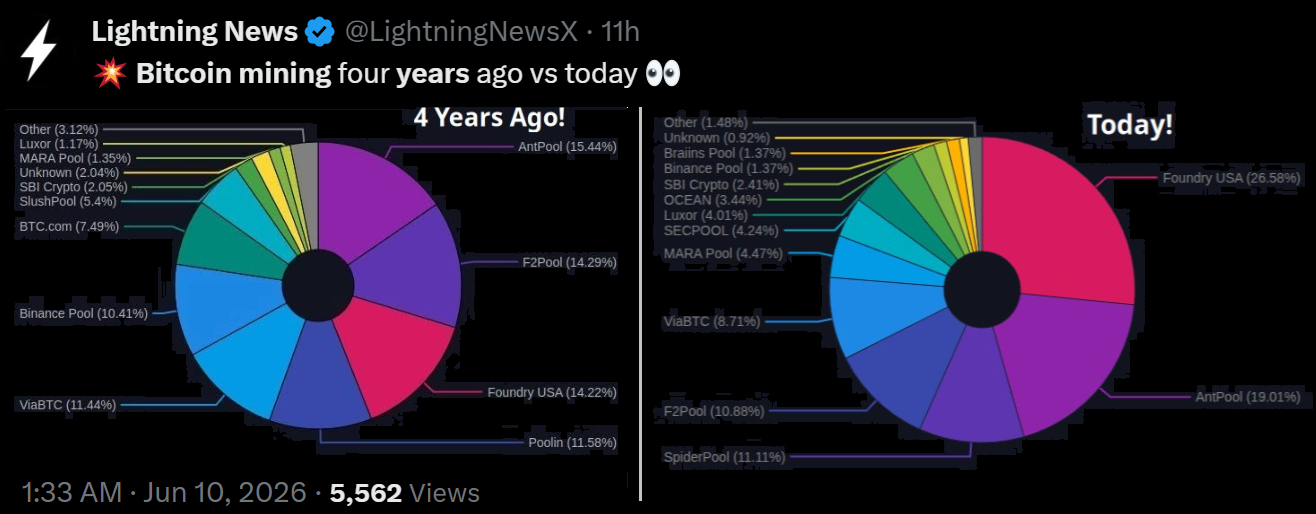

The balance of power in hashrate distribution continues to tilt toward the industry’s largest players. The combined share of the three biggest mining pools—Foundry USA, AntPool, and F2Pool—stood at about 59% over recent seven-day data. That concentration marks a meaningful contrast with 2022, when the top three pools controlled roughly 44% of hashrate, highlighting ongoing centralization concerns in Bitcoin mining as efficiency, scale, and electricity access drive consolidation.

Beyond efficiency and access to cheap power, energy availability remains the gating factor for broader AI infrastructure expansion. Bernstein’s assessment has fed into a wider industry narrative that the bottleneck for AI data centers is electricity, a constraint that is pushing some miners to repurpose energy assets to support AI workloads rather than purely cryptocurrency mining. This pivot partly explains why perceived mining profitability may diverge from the performance of AI compute assets that are funded by the same energy resources.

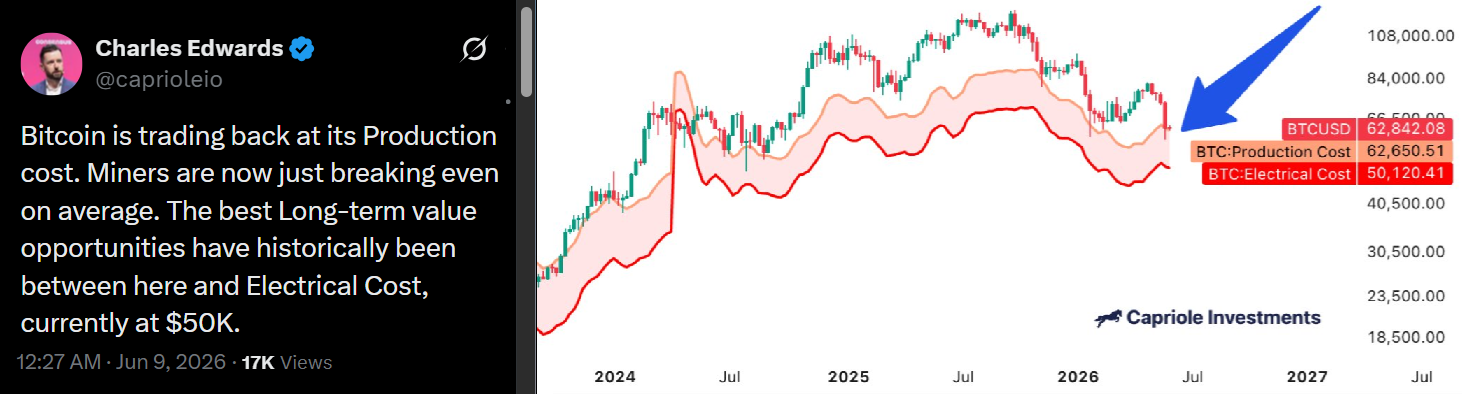

From a cost perspective, analysts note that production costs for Bitcoin mining vary widely by operator and region. Charles Edwards, founder of Capriole Investments, has highlighted that the Bitcoin mining production cost—accounting for depreciation and amortization—hovers around $62,650 per BTC, while the minimum electricity cost to break even sits near $50,120. Some publicly listed operators contend with more favorable economics thanks to newer ASIC models and industrial-scale power contracts. For American Bitcoin Corp (ABTC US), management reported gross operational costs near $36,200 per BTC mined in Q1 2026, illustrating how scale and efficiency can compress unit costs even as overall price pressures persist. Still, there is no single industry-wide figure, and some miners continue to run at losses for reasons such as tax planning or strategic positioning. Even with high-cost operations temporarily idling, spot institutional flows now vastly outweigh mined BTC output, underscoring macro forces as a primary driver of ongoing price dynamics.

Earlier coverage noted a related tension: as institutional demand for spot BTC has grown, Bitcoin has sometimes acted as a broader market canary in the coal mine during risk-off episodes, underscoring how macro liquidity can trump individual mining economics in the near term. For readers tracking this topic, see ongoing coverage on how risk-off dynamics influence BTC supply and price behavior.

Looking ahead, the key watchpoints are clear. Electricity prices and access to low-cost energy will continue to shape mining economics and any meaningful reallocation toward AI compute. At the same time, macro demand for Bitcoin as a risk-on or risk-off diversifier, plus regulatory developments around mining operations and energy contracts, will influence how miners navigate profitability, capacity deployment, and balance-sheet resilience. Investors and industry observers should monitor these intertwined threads to gauge whether mining margins recover, or if the AI-infrastructure pivot becomes the more durable driver of capital allocation in the Bitcoin ecosystem.

Watch for updates on energy pricing trends, AI data-center capacity expansion, and policy shifts that could impact the economics of large-scale mining. As the landscape evolves, the balance between profitability, energy constraints, and macro demand will continue to define Bitcoin’s mining narrative.

Sources and data references include the Luxor Hashrate Index for hashing-power returns, Glassnode Studio for miner net position changes, and statements from Bernstein on AI-data-center bottlenecks. Public disclosures from Capriole Investments and American Bitcoin Corp provide cross-checks on production costs and operational expenses, while market observers on X highlighted current hashrate concentration dynamics. Related context from Cointelegraph pieces on institutional flows and AI infrastructure themes complements the analysis.

Source notes: Daily return per 1 TH/s — Luxor Hashrate Index; 14-day miner net position change — Glassnode Studio; AI infrastructure bottlenecks — Bernstein (via Cointelegraph); 1) Antminer S21 XP Hydro profitability — Luxor Hashrate Index; Capriole Investments commentary — Capriole on X; ABTC Q1 2026 costs — ABTC via PR Newswire; broader context on institutional flows and AI infrastructure coverage — Cointelegraph.

Bill Gates has told a House panel that he regrets meeting Jeffrey Epstein while seeking support for global health work.

Summary

- Bill Gates said he regrets meeting Jeffrey Epstein while seeking support for global health work.

- Gates denied witnessing criminal conduct, visiting Epstein properties, or victimizing anyone.

- Lawmakers continue reviewing Epstein-related files and expect to release Gates’ testimony transcript soon.

The Microsoft co-founder denied witnessing criminal conduct and denied victimizing anyone in his prepared statement. His closed-door testimony came as lawmakers continue reviewing Epstein’s ties to wealthy and powerful figures.

Gates says Epstein meetings were a mistake

According to Bill Gates’ opening statement, he first met Epstein in 2011 through people he trusted professionally. Gates said the meetings focused on possible donations to the Gates Foundation and global health programs.

“I should never have met with Epstein in the first place,” Gates said. He added that any promised donors would not have justified the association. Gates said Epstein claimed he could raise billions of dollars from people connected to his tax and estate work. However, Gates said no charitable vehicle was created and no funds were raised.

He said he held three meetings with Epstein in 2011 and two meetings in 2012. Later talks in 2013 and 2014 focused on possible donor-advised funds. By 2014, Gates said he concluded Epstein would not deliver the promised support. He said he then stopped communicating and meeting with him.

Bill Gates denies seeing criminal conduct

Gates told lawmakers he never saw signs that Epstein engaged in ongoing criminal conduct. He also said he never visited Epstein’s island, ranch, or Florida home.

“I have never victimized anyone,” Gates said in the statement. He said Epstein may have sought a personal relationship, but he never reciprocated. Gates said he knew Epstein had prior legal issues, but not the full extent of his crimes. He said he accepted the introduction without the scrutiny he should have applied.

Epstein pleaded guilty in Florida in 2008 to charges linked to soliciting an underage girl for prostitution. He later died in a New York jail in 2019 after federal charges. Gates said Epstein later learned sensitive information about his personal life. He said Epstein tried to use those details and false claims to pressure him.

Lawmakers continue Epstein document review

The House Oversight and Government Reform Committee questioned Bill Gates behind closed doors on Wednesday. The committee interviewed Epstein’s former executive assistant, Lesley Groff, a day earlier. Gates left the interview around 3:50 p.m. ET without speaking to reporters. A transcript of his testimony is expected in the coming days.

Committee Chair James Comer said lawmakers may invite attorney Alan Dershowitz to testify. Dershowitz previously represented Epstein in legal matters. Rep. Robert Garcia said lawmakers wanted to understand who moved inside Epstein’s circle. He said the panel planned questions about emails tied to Gates and Epstein.

In his statement, Gates said he supports releasing all Epstein files. He also said survivors of Epstein’s crimes deserve justice. Gates said the association put the Gates Foundation’s work at risk. The foundation previously commissioned an external review of its past ties with Epstein.

Bitcoin remained under pressure near $61,750 as analysts warned that the upcoming SpaceX IPO could divert capital away from the crypto market at a time when ETF outflows and weak sentiment are already weighing on the market.

Summary

- Bitcoin fell 14% over the past week as ETF outflows, weak sentiment, and declining open interest weighed on the market.

- U.S. spot Bitcoin ETFs have recorded roughly $4.57 billion in net outflows over the past four weeks, signaling weaker institutional demand.

- Analysts warn SpaceX’s planned $75 billion IPO could compete with cryptocurrencies for investor capital and add further pressure to Bitcoin.

According to market data, Bitcoin (BTC) price has fallen about 14% over the past week, while the total cryptocurrency market capitalization slipped another 1.1% over the past 24 hours to $2.2 trillion. The decline comes as traders continue reducing exposure across derivatives markets, with Bitcoin open interest falling 0.57% to approximately $45 billion.

Sentiment has also deteriorated sharply. Data from Alternative’s Crypto Fear & Greed Index showed a reading of 9, marking another week in extreme fear territory as investors remain cautious amid growing macroeconomic and geopolitical uncertainty.

Bitcoin sentiment deteriorates as ETF outflows mount

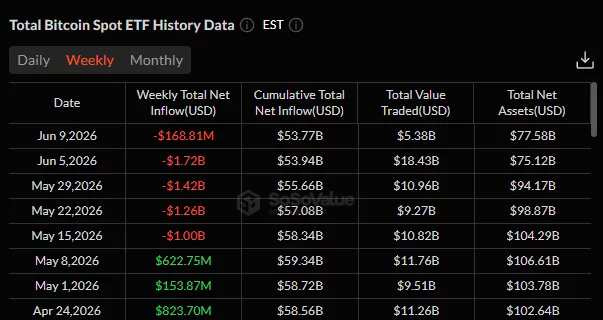

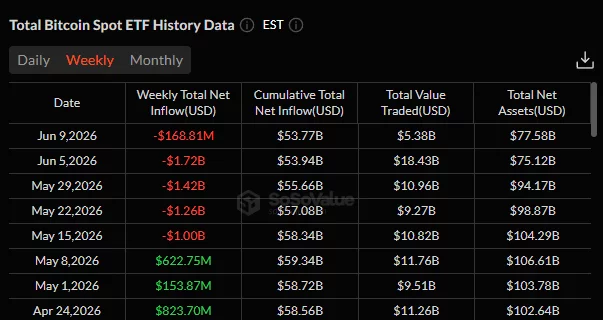

Institutional demand has also shown signs of weakening. Data from SoSoValue shows U.S. spot Bitcoin ETFs recorded net outflows of $168.8 million so far this week. The products also saw withdrawals of $1.72 billion, $1.42 billion, and $1.26 billion during the previous three weeks, bringing total outflows over the four-week period to roughly $4.57 billion.

The sustained withdrawals have coincided with a decline in total net assets held by spot Bitcoin ETFs. According to SoSoValue, combined assets under management fell from $104.29 billion in mid-May to $77.58 billion by June 9.

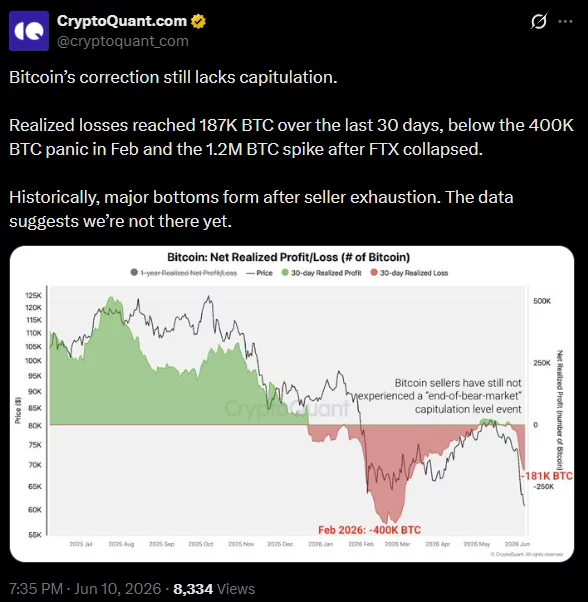

Additional on-chain data suggests the market may not have reached a capitulation phase typically associated with major cycle bottoms.

In a June 10 market update, CryptoQuant noted that realized losses totaled approximately 187,000 BTC over the past 30 days, below the roughly 400,000 BTC realized during the February panic and well below the 1.2 million BTC recorded following the FTX collapse.

“Historically, major bottoms form after seller exhaustion. The data suggests we’re not there yet.”

Technical indicators also remain fragile. Bitcoin is trading near the Murrey Math support zone around $62,500, while a break below the nearby $59,375 support level could expose the market to deeper downside risks.

Momentum indicators continue to favor sellers, with the MACD remaining in bearish territory after a recent negative crossover. The widening gap between the MACD and signal lines suggests downward momentum has yet to fully weaken, increasing the risk of further losses if buyers fail to defend key support levels.

SpaceX IPO could compete for crypto liquidity

Against that backdrop, analysts are increasingly focused on the potential impact of SpaceX’s long-awaited public debut.

The aerospace company founded by Elon Musk is reportedly preparing a $75 billion public offering at a projected valuation of approximately $1.75 trillion. Reuters reported that about 30% of the offering could be reserved for retail investors, an unusually large allocation for an IPO of that size.

Some market participants believe the listing could attract capital that might otherwise flow into cryptocurrencies.

“Crypto is a funding currency for a lot of this,” Spencer Hallarn, global head of over-the-counter trading at GSR, told Reuters. “We’ve got to find $75 billion for this IPO, and it’s got to come from somewhere.”

Thomas Puech, chief executive of crypto firm INDIGO, also told Reuters that the offering could divert funds away from digital assets in the short term because both markets compete for the same pool of risk capital.

According to Puech, artificial intelligence-related investments currently represent a more attractive trade for many growth-focused investors.

While there is no direct evidence that recent Bitcoin ETF outflows are being redirected toward SpaceX shares, analysts say the timing of the IPO could create another headwind for digital assets.

With institutional demand weakening, sentiment stuck in extreme fear territory, and on-chain data suggesting seller exhaustion has yet to emerge, Bitcoin may remain vulnerable to additional liquidity pressures in the weeks ahead.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Key takeaways:

- Record-low Bitcoin mining margins and rising demand for AI infrastructure incentivize miners to reduce their BTC positions.

- Institutional spot Bitcoin flows vastly surpass miner output, making macro trends more vital than miner profits alone.

Bitcoin’s price slide to $62,000 was paired with weak on-chain activity and declining BTC miner revenues, which have fallen to an all-time low. This revenue drop is fueling investor anxiety over potential sell pressure, especially since miners and mining pools still control over $110 billion in Bitcoin.

1 TH/second of hashing power per day returns, USD. Source: Luxor Hashrate Index

The estimated daily return for 1 terahash per second of hashing power plunged to an all-time low of $0.28 on Tuesday, down from $0.39 just a month ago. For context, the estimated monthly gross profit for an Antminer S21 XP Hydro (at an electricity cost of $0.07 per kilowatt-hour) has slid to $137, down from $192 last month.

This profitability crunch arrives as demand for AI capacity and infrastructure investments surged, dampening market sentiment just as the crucial $60,000 support level was put to the test.

Bitcoin miners’ 30-day net position change, BTC. Source: Glassnode Studio

The 14-day average net position change for Bitcoin held in miner and mining pool addresses flipped negative in early May and has remained negative since. Whether these liquidations are intended to fund ongoing operations, reduce debt leverage, or bankroll expansion into AI data center computing, the net effect remains a heavy drag on Bitcoin’s price discovery.

Source: X/LightningNewsX

The high concentration of Bitcoin hashrate among the three largest mining pools is a frequent target of analyst criticism. The latest 7-day data show that Foundry USA, AntPool, and F2Pool control a combined 59% market share. In contrast, the top three Bitcoin mining pools held a combined 44% hashrate market share back in 2022.

According to Bernstein analysts, the primary bottleneck for scaling AI data centers is access to electricity rather than chips. This constraint is prompting some Bitcoin miners to repurpose parts of their power infrastructure to support AI computing applications, a sector currently viewed as more stable and lucrative than traditional crypto mining.

Source: X/Capriole Investments

According to Charles Edwards, founder of Capriole Investments, the Bitcoin mining production cost, including depreciation and amortization, stands at $62,650, while the absolute minimum to break even on electricity is $50,120. However, certain publicly listed companies leverage much more efficient ASIC models and industrial-scale energy contracts.

American Bitcoin Corp (ABTC US) reported gross operational costs near $36,200 per Bitcoin mined in the first quarter of 2026. Ultimately, pinning down a single, industry-wide production cost is impossible, and some operations choose to mine at a loss for specific tax benefits. Even if these high-cost miners temporarily shut down, spot institutional flows now vastly surpass miners’ output.

Related: Bitcoin may act as a ‘canary in the coal mine’ as risk-off pressure spreads–Bitwise

Bitcoin traded below its estimated production cost for more than six months in 2019 and again in 2023, based on Capriole Investments data. Whether the current market stagnation persists depends on investor risk perception amid broader macroeconomic uncertainty, rather than miner profitability alone.

TLDR

- Tether led a Series C funding round worth up to $1.4 billion in Neura Robotics.

- The deal closed after several months of discussions between Tether and the German robotics firm.

- Neura Robotics develops humanoid robots, precision arms, and autonomous mobile machines.

- Tether will integrate its Wallet Development Kit directly into Neura’s robotic systems.

- Tether stated that autonomous robots require built-in financial tools to complete transactions.

Tether confirmed it led a Series C round worth up to $1.4 billion in Neura Robotics. The stablecoin issuer announced the deal on Wednesday and outlined plans for wallet integration. The agreement follows earlier reports that Tether considered investing in the German robotics firm last year.

Tether commits up to $1.4 billion to Neura Robotics

Tether said it backed the raise of up to $1.4 billion from strategic and financial investors. The company described the move as a step toward advancing machine intelligence and autonomy. It stated that the investment supports a firm reshaping how machines think and move.

The company said, “By supporting the raise of up to $1.4 billion, the group takes a decisive step.”

It added that Neura Robotics aims to redefine how machines interact and transact in the physical world. Tether confirmed the funding round closed after several months of negotiations.

Neura Robotics develops humanoid robots and precision robotic arms for industrial use. The company also builds autonomous mobile robots and service robots for multiple sectors. Tether stated that these systems will operate where human and machine collaboration creates value.

Neura raised nearly $140 million in January 2025 from BlueCrest, C4 Ventures, Lingotto, and Volvo Cars Tech Fund. That round expanded its capital base before the Series C financing. The company competes with Tesla, which also plans to mass-produce robots.

Tether has expanded its venture capital activity through profits from its USDT stablecoin business. The firm holds reserves in yield-bearing assets such as U.S. Treasurys. These investments generate income that supports strategic deals like the Neura round.

Tether wallet tools set for robotic ecosystem integration

Tether said it will deploy technology within the Neura robotics ecosystem. The company confirmed that Neura will integrate Tether’s Wallet Development Kit into robotic systems.

Tether stated, “To be truly autonomous, robots need financial tools.”

The integration will allow robots to access digital payment capabilities directly. Tether explained that the wallet tools will support transactions within machine environments. The statement outlined plans to embed payment functions into robotic workflows.

Tether did not disclose the exact timing for deploying the wallet technology. However, it confirmed that development teams will work on direct integration. The company linked the effort to its broader digital asset infrastructure strategy.

Neura operates from Germany and focuses on collaborative robotics platforms. The company builds systems designed for industrial and service applications. It stated that its products aim to function across varied environments.

Tether did not release further financial details beyond the $1.4 billion figure. The company emphasized that diversified investors participated in the round. It confirmed that the funding and integration plans form part of the closed Series C agreement.

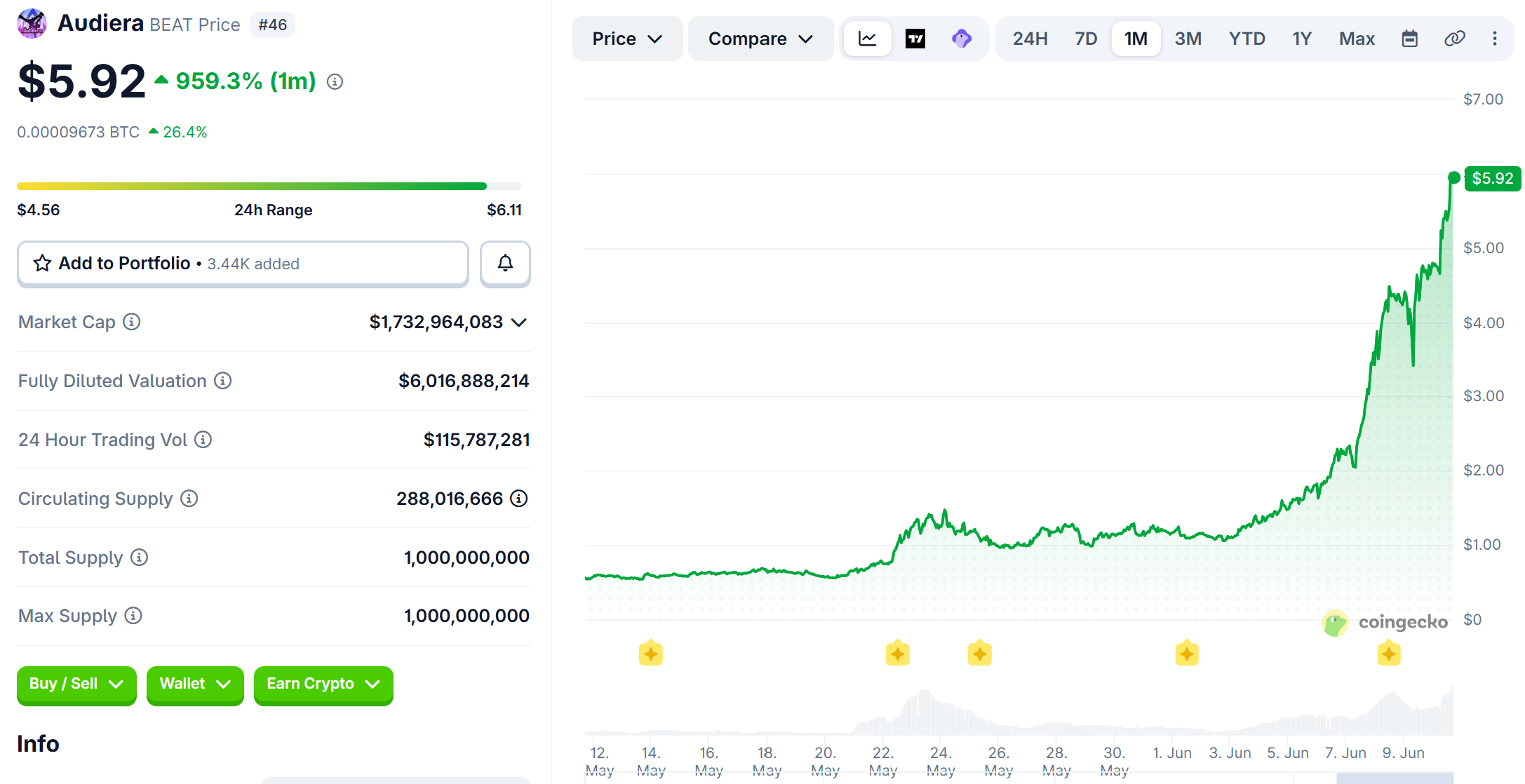

Audiera (BEAT) reached an all-time high of $6.11 on Wednesday, extending its weekly gain to 378% and monthly climb to nearly 960%. The surge has revived warnings that the token shares traits with RaveDAO (RAVE) and LAB before their collapses.

The rhythm gaming token now holds a $1.75 billion market cap and a fully diluted valuation (FDV) above $6 billion. However, less than a third of its supply circulates, a structure critics tie to recent manipulation episodes.

Why Audiera BEAT Draws RAVE and LAB Comparisons

Audiera’s circulating supply stands near 288 million BEAT, about 29% of its 1 billion maximum, according to CoinGecko.

RAVE and LAB launched with the same structure. Each caps supply at 1 billion tokens, and each traded with under a third of supply circulating.

On-chain investigator ZachXBT alleged insiders holding over 90% of RAVE’s supply coordinated the RAVE pump-dump scheme. The alleged activity spanned Binance, Bitget, and Gate.

RAVE shed more than 95% of its value in a day. It now trades near $0.32, almost 99% below its April peak of $27.88.

The pattern repeated when LAB crashed 77% in two hours on June 2, erasing close to $6 billion.

That collapse arrived days after LAB’s record high, with most holders still locked. LAB has since lost 53% in a week.

Audiera now faces similar scrutiny. Risk threads claim BEAT’s top 10 wallets control around 85% of supply.

BeInCrypto could not independently verify that figure.

“It looks like BEAT has the potential to become the next LAB/RAVE like scam coin It’s currently trading close to $6bn FDV. Strangely, it hasn’t been trading on negative funding at all. Maybe the funding will start pushing negative later to inflict max pain to shorts…,” one analyst noted.

Follow us on X to get the latest news as it happens

Pseudonymous trader DeFiVillain has flagged whale flows and funding dynamics resembling the RAVE playbook.

Similar warnings circulate in Telegram trading channels.

A Gaming Narrative Sets BEAT Apart, for Now

However, Audiera differs from its troubled predecessors in important ways.

The project is a Web3 revival of the Audition dance game on BNB Chain.

Binance ran a BEAT trading competition on Binance Alpha this spring, giving the token mainstream exchange exposure.

Moreover, no investigator has published a formal case against the project.

Warnings so far come from traders rather than hard evidence, though analysts flagged RaveDAO’s surge on similar grounds before its collapse.

Still, the gap between BEAT’s $6 billion FDV and $1.75 billion market cap leaves 712 million tokens to enter circulation.

How those tokens reach the market may decide whether BEAT escapes the pattern its critics describe.

The post This One Altcoin Flashes Red Flags That Preceded RaveDAO and LAB Crashes appeared first on BeInCrypto.

Firefighters rush to house blaze in Cambridgeshire village

Count slows in Peru as presidency likely hinges on contested votes

CFTC’s Prediction Markets Rules Proposal Signals Sports-Contract Edge

![Yelawolf - "Money" Ft: Jelly Roll & Struggle Jennings [MUSIC VIDEO]](https://wordupnews.com/wp-content/uploads/2026/01/1769894485_hqdefault-80x80.jpg)

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Evereve – Corporette.com

-

Crypto World5 days ago

Crypto World5 days agoJensen Huang Approves Samsung, SK Hynix, and Micron for NVIDIA (NVDA) HBM4 Memory Supply

-

Crypto World3 days ago

Crypto World3 days agoAnatomy of the June crypto crash: Fed, Iran, Saylor

-

Entertainment4 days ago

Entertainment4 days agoThe Best Mystery Series of All Time Is Surging on Streaming 30 Years After It Ended

-

NewsBeat3 days ago

NewsBeat3 days agoAlexander Zverev wins the French Open to finally earn a 1st Grand Slam title

-

Tech5 days ago

Tech5 days agoSuspicious Polyfill login prompts pop up on Toshiba, Muji websites

-

Crypto World4 days ago

Senator Cynthia Lummis Calls CLARITY Act the Most Consequential Financial Legislation of This Generation

-

Tech6 days ago

Tech6 days agoMicrosoft launches MXC, an OS-level sandbox for AI agents, with OpenAI and Nvidia already on board

-

Tech3 days ago

Tech3 days agoMicrosoft unveils seven homegrown AI models in new bid for ‘long term self-sufficiency’

-

Business5 days ago

Business5 days ago(VIDEO) Justin Bieber Delivers Surprise Happy Birthday Serenade to Diners at Los Angeles Mexican Restaurant

-

Business4 days ago

Business4 days agoThe Pain Points Taking a Fragile Tech Rally Down a Notch

-

Crypto World2 days ago

Crypto World2 days agoEli Lilly (LLY) Stock Surges 4% Following Breakthrough Sleep Apnea Trial Results

-

Crypto World6 days ago

LBank Surpasses 25 Million Users Worldwide as AFA Partnership Continues to Drive Global Growth

-

Tech5 days ago

Tech5 days agoVon der Leyen’s AI envoy pick draws conflict-of-interest fire

-

Crypto World3 days ago

Crypto World3 days agoTrump’s AI Ownership Plan Could Benefit Anthropic at OpenAI’s Expense

-

Tech5 days ago

Tech5 days agoMeta steals a tactic from Tesla and builds data centers in tents

-

Sports1 day ago

Sports1 day agoBangladesh beat Australia after 20 years in ODIs, register only their second win over six-time world champions | Cricket News

-

Business3 days ago

Business3 days agoHigh Stakes for Wembanyama as New York Pushes for 3-0 Lead

-

Tech5 days ago

Tech5 days agoHackers now exploit SolarWinds Serv-U flaw to crash servers

-

Tech3 days ago

Tech3 days agoNotion restores access to Anthropic after service disruption

You must be logged in to post a comment Login