Crypto World

What is a crypto trust bank? Charters, custody, and the Fed Master Account

A wave of crypto firms, from Ripple to Circle, have won national trust bank charters, and several are chasing a Federal Reserve master account. This guide explains what a crypto trust bank actually is, what a charter does and does not grant, and why the real prize sits at the central bank.

Summary

- A crypto trust bank is a chartered trust institution that custodies digital assets and manages stablecoin reserves, bringing crypto custody inside the regulated banking system without being a full retail bank.

- A national trust charter lets a crypto firm custody its own assets and reserves and obviate the patchwork of state money-transmitter licenses, but it cannot take ordinary deposits or carry federal deposit insurance.

- In 2025 and 2026, a wave of crypto firms, including Ripple, Circle, Paxos, Fidelity Digital Assets, and others, won conditional national trust charters.

- The bigger prize is a Federal Reserve master account, which would give direct access to the central bank’s payment rails and let a firm hold reserves at the Fed itself, something no crypto-native firm has yet achieved.

- Charters and master accounts primarily benefit stablecoins and custody businesses by deepening their regulatory standing, marking crypto’s convergence with traditional banking.

A crypto trust bank is a chartered financial institution, supervised like a bank, whose purpose is to custody assets and provide fiduciary services rather than to take deposits and make loans, and which a crypto firm uses to hold digital assets and manage stablecoin reserves inside the regulated banking system. That definition contains the key to understanding the whole subject: a trust bank is a real, regulated bank, but a specialized kind, built around safekeeping and trust services rather than the deposit-taking and lending that define ordinary retail banks.

In 2025 and 2026, a remarkable wave of crypto firms obtained or pursued these charters, transforming companies once seen as outside the financial system into federally supervised institutions, a shift that marks one of the clearest signs yet of crypto converging with traditional banking. This guide explains what a trust bank is, what a national trust charter actually grants a crypto firm and what it pointedly does not, why so many crypto companies suddenly wanted one, the even larger prize of a Federal Reserve master account, and what the whole development means for stablecoins, for the industry, and for users.

The reason this matters is that the relationship between crypto and the banking system has been one of the defining tensions of the industry’s history. For years, crypto firms depended on traditional banks to hold their customers’ money and connect them to the financial system, a dependence that became a serious vulnerability during periods of regulatory pressure and bank failures, when crypto companies found their accounts closed or their banking partners collapsing.

The move to obtain trust charters is, in large part, an effort to end that dependence by bringing crypto firms inside the regulated banking system on their own terms. This guide covers what a trust bank is, the powers and limits of a charter, the 2025-2026 wave of approvals, a worked example of how a charter changes a stablecoin issuer’s position, the central-bank master account that is the ultimate goal, what it all means for stablecoins, and the genuine limits and risks that the headlines often gloss over.

What a trust bank is

Start with the institution itself, because the word “bank” carries assumptions that a trust bank does not always meet. In traditional finance, a trust bank is a bank that specializes in custody and fiduciary services rather than in the deposit-taking and lending that most people associate with banking. Its core business is holding assets on behalf of clients, safeguarding them, and managing them in a fiduciary capacity, meaning with a legal duty to act in the client’s interest.

Trust banks have long existed to custody securities, manage estates and trusts, and provide safekeeping for institutions, and they are regulated as banks, but their activities are narrower and, in important ways, less risky than those of a full-service commercial bank, because they are not lending out customer money or running the maturity mismatches that make ordinary banking risky.

This specialization is exactly what makes the trust bank model attractive to crypto firms. A crypto company’s central regulated need is custody: safely holding digital assets and, for stablecoin issuers, holding and managing the reserve assets that back their tokens. A trust bank charter is purpose-built for precisely this kind of safekeeping and fiduciary activity, which is why crypto firms gravitated to it instead of to a full commercial banking charter that would saddle them with powers and obligations they neither need nor want.

By becoming a trust bank, a crypto firm gains the regulated standing and supervisory oversight of a banking institution while staying within the narrower scope of custody and trust services that match its actual business.

Understanding that a trust bank is a custody-and-fiduciary institution, not a deposit-and-lending one, is the foundation for understanding everything a crypto trust charter does and does not provide.

What a national trust charter grants, and what it does not

A national trust charter, granted in the United States by the federal regulator that oversees national banks, gives a crypto firm a specific and valuable set of capabilities, and it is important to be precise about both what it includes and what it excludes. On the positive side, the charter allows the firm to operate as a federally supervised trust bank, custodying digital assets and, under expanded rules, managing stablecoin reserves and providing certain payment-related services.

Crucially, it lets the firm custody its own assets and reserves directly, instead of depending on a third-party bank, and it can obviate the need for the patchwork of separate state money-transmitter licenses that crypto firms have historically had to collect state by state, replacing a fragmented compliance burden with a single federal charter. It also confers the legitimacy and oversight of a banking institution, which matters enormously to the institutional clients a crypto firm wants to serve.

The exclusions are just as important, and they are where headlines often mislead. A national trust charter does not make a crypto firm a full bank in the everyday sense. It does not permit the firm to take ordinary deposits, the way a retail bank accepts checking and savings accounts. It does not come with federal deposit insurance, the government protection that backs ordinary bank deposits up to a limit, because trust banks generally do not hold the kind of deposits that insurance covers.

And it does not authorize the firm to lend, to run the credit business at the heart of commercial banking. So when a crypto firm “becomes a bank” via a trust charter, it gains custody, reserve management, and regulated standing, but it does not gain the ability to take insured deposits or make loans. This distinction is not a quibble; it is central to understanding what these charters actually mean, because a customer who assumes a chartered crypto trust bank offers the same protections as an insured retail bank would be mistaken, and that misunderstanding could matter a great deal in a crisis.

Why crypto firms suddenly want them

The sudden rush of crypto firms toward trust charters in 2025 and 2026 was not coincidental, and understanding the motivations explains the strategic logic. The first and most fundamental driver is independence from third-party banks. For most of crypto’s history, firms relied on partner banks to hold customer funds, custody reserves, and connect to the financial system, and that dependence proved dangerous: during periods of regulatory pressure and amid a series of bank failures, crypto companies found their banking relationships severed or their partner banks collapsing, threatening their operations through no fault of their own. A trust charter lets a firm custody its own assets and reserves directly, removing that single point of failure and the strategic vulnerability it created.

The second driver is regulatory tailwind. A shift in the political and regulatory environment toward a more accommodating posture on crypto opened a path for these charters that had been effectively closed before, and the federal regulator approved a cluster of crypto firms in a coordinated wave, signaling a broader acceptance of crypto-native institutions in the banking system.

The third driver is the rise of stablecoin regulation: as comprehensive rules for stablecoins took shape, holding a trust charter aligned a firm with the likely requirements, particularly around the custody and management of reserves, positioning compliant issuers ahead of the curve. The fourth is simple competitive and reputational advantage: a federally chartered trust bank carries a legitimacy that a lightly regulated startup cannot match, and for firms courting banks, asset managers, and corporations as clients, that regulated standing is a powerful selling point.

Together, these drivers, independence, regulatory opening, stablecoin alignment, and legitimacy, explain why a long list of major crypto firms pursued charters at once, turning what had been a fringe idea into an industry-wide movement.

A worked example: a stablecoin issuer with and without a charter

To see why a charter matters in practice, compare a stablecoin issuer’s position before and after obtaining one, because the contrast makes the abstract benefits concrete.

Without a charter, a stablecoin issuer must rely on third-party banks to hold the reserve assets that back its tokens, the cash and short-term government securities that give the stablecoin its value. This dependence creates several vulnerabilities. The issuer is exposed to the health of its partner banks, so if one of them fails or freezes the account, the reserves and the stablecoin itself are jeopardized, a danger that became vividly real when a stablecoin temporarily lost its peg after a bank holding part of its reserves collapsed. The issuer must also navigate a patchwork of state-by-state money-transmitter licenses, a costly and fragmented compliance burden, and it lacks the regulated standing that would reassure cautious institutional users.

With a national trust charter, the same issuer’s position is transformed. It can custody its own reserve assets directly through its chartered trust bank, under federal supervision, removing the dependence on potentially fragile third-party banks. In some cases the firm gains oversight at both the federal and state level, a dual-supervision structure that few stablecoin issuers can match and that serves as a strong signal of credibility to institutions evaluating whether to trust the stablecoin.

The single federal charter can replace much of the state-by-state licensing burden, simplifying compliance. And the regulated standing of a trust bank reassures the banks, asset managers, and corporations the issuer wants as customers, lowering the barrier to adoption. The worked comparison shows the charter’s real value clearly: it converts a stablecoin issuer from a firm dependent on outside banks and a fragmented license patchwork into a federally supervised institution that controls its own reserves and carries banking-grade legitimacy. That transformation is precisely why stablecoin issuers were among the most eager pursuers of these charters.

The real prize: a Federal Reserve master account

As valuable as a trust charter is, it is a stepping stone to something larger, and the ultimate goal for the most ambitious crypto firms is a Federal Reserve master account. A master account is the account a financial institution holds directly with the central bank, and it represents the deepest possible integration into the financial system. It grants direct access to the central bank’s payment rails, the core networks through which money moves between institutions, and access to base money held at the central bank itself, instead of balances held at a commercial bank. For most of the financial system, this kind of direct central-bank access is reserved for traditional banks, and obtaining it is the difference between operating at the edge of the system and operating at its core.

For a crypto firm, particularly a stablecoin issuer, the appeal of a master account is profound. It would allow the firm to hold the reserves backing its stablecoin directly at the central bank, the safest possible place to keep them, eliminating the counterparty risk of relying on commercial banks and giving institutions unparalleled confidence in the stablecoin’s solvency and the safety of its redemptions. It would also allow direct settlement through the central bank’s payment systems, a powerful capability for a payments-focused firm.

The obstacle is that the bar is extraordinarily high, and no crypto-native firm has yet been granted a master account. The central bank has historically been cautious about extending this access to non-traditional institutions, uninsured trust banks face the most stringent review, and previous attempts by crypto-adjacent firms to win access have been denied. Several chartered crypto firms have applied and are waiting, with no guaranteed outcome and no clear timeline. The master account is the real prize precisely because it is so hard to win and so transformative if won, marking the moment a crypto-native firm would plug directly into the heart of the financial system.

What it means for stablecoins and the industry

Stepping back, the trust-charter wave is, more than anything, a stablecoin story, and seeing why clarifies the whole development. The firms most eager for charters were heavily those with stablecoin businesses, because the charter speaks directly to a stablecoin issuer’s central regulated needs: custodying and managing the reserve assets that back the token, doing so under credible supervision, and removing the dependence on third-party banks that has repeatedly threatened stablecoins in the past.

As comprehensive stablecoin regulation took shape, a trust charter became close to a prerequisite for operating a serious, institutionally trusted stablecoin in the United States, and the firms that obtained charters positioned their stablecoins as the most credible and best-supervised in the market. The dual oversight some of them gained, federal and state, became a competitive selling point, a way to signal to institutions that the stablecoin’s reserves are held to banking-grade standards.

The broader significance is the convergence of crypto and traditional banking. The trust-charter wave marks the moment when crypto firms stopped operating outside the regulated banking system and began entering it as supervised institutions, accepting the obligations of banking regulation in exchange for its legitimacy and stability. This is a profound shift from crypto’s early ethos of operating apart from, and often in opposition to, the traditional financial system. It signals a maturing industry in which the leading firms seek the same regulated standing as banks, and in which the line between a crypto company and a financial institution blurs. For the industry, this convergence brings legitimacy, stability, and access, the ability to custody assets safely, serve institutional clients, and integrate with the financial system.

It also brings the constraints of regulation, the compliance burdens, capital requirements, and supervision that come with a banking charter. The trust-charter wave is, in essence, crypto’s leading firms choosing to join the financial system instead of replacing it, which is one of the most consequential shifts in the industry’s trajectory.

Risks and limits to understand

For all the significance of the trust-charter movement, several risks and limits deserve clear attention, because the headlines tend to overstate what these charters mean. The most important point for any user is the one already emphasized: a crypto trust bank is not a full, insured retail bank. It does not carry federal deposit insurance, so assets held with a chartered crypto trust bank do not enjoy the government protection that backs ordinary bank deposits up to a limit.

A customer who assumes a “crypto bank” offers the same safety net as an insured retail bank is mistaken, and in a failure scenario, that misunderstanding could be costly. The charter brings supervision and legitimacy, which are real, but it does not transform custody into an insured deposit, and that distinction must not be lost.

Other limits and risks are substantial. The Federal Reserve master account that many firms seek remains unattained by any crypto-native firm and is far from assured, so the deepest integration into the financial system, and the reserve-safety benefits that come with it, are still aspirational instead of achieved. The charters themselves are often conditional, meaning the firms must still satisfy capital, governance, and risk-management standards before operating fully, and conditional approval is not the same as a fully operational bank.

Traditional banking groups have opposed extending charters and central-bank access to crypto firms, citing systemic-risk concerns, and that opposition could shape how far the privileges extend. There is also regulatory and political risk: the accommodating posture that opened the path to these charters could shift, and supervisory expectations could tighten. And the convergence itself carries a subtler risk, that bringing crypto firms inside the banking system concentrates new kinds of risk within the regulated perimeter in ways regulators are still learning to assess.

None of this negates the genuine progress the charters represent, but anyone evaluating a chartered crypto trust bank, whether as a user, an investor, or an observer, should hold a clear view of what the charter does and does not provide, treat the master account as a hope instead of a fact, and never mistake banking-grade supervision for deposit insurance.

Frequently Asked Questions

What is a crypto trust bank in simple terms?

A crypto trust bank is a chartered, bank-supervised institution built around custody and fiduciary services instead of deposits and lending, which a crypto firm uses to hold digital assets and manage stablecoin reserves inside the regulated banking system. It is a real, regulated bank, but a specialized kind: its job is safekeeping and trust services, not taking checking accounts or making loans. Crypto firms pursue this model because their central regulated need is custody, and a trust charter is purpose-built for exactly that, giving them banking-grade standing without the powers and obligations of a full commercial bank.

What does a national trust charter let a crypto firm do?

It lets the firm operate as a federally supervised trust bank, custodying digital assets and, under expanded rules, managing stablecoin reserves and providing certain payment-related services. Crucially, it lets the firm custody its own assets and reserves directly instead of depending on third-party banks, and it can replace the patchwork of state money-transmitter licenses with a single federal charter. It also confers the legitimacy and oversight of a banking institution. What it does not grant is the ability to take ordinary insured deposits or to make loans, so it is not a full retail bank.

Does a crypto trust bank have deposit insurance?

No, and this is one of the most important things to understand. National trust charters generally do not come with federal deposit insurance, the government protection that backs ordinary bank deposits up to a limit, because trust banks do not hold the kind of deposits that insurance covers. So assets held with a chartered crypto trust bank do not enjoy the safety net that an insured retail bank provides. A customer who assumes a “crypto bank” offers the same protection as an insured bank is mistaken, and that distinction could matter greatly in a failure. The charter brings supervision and legitimacy, not deposit insurance.

Why did so many crypto firms get charters in 2025 and 2026?

Several reasons converged. The biggest was independence from third-party banks, since crypto firms had repeatedly been hurt when partner banks closed their accounts or failed, and a charter lets a firm custody its own assets directly. A more accommodating regulatory environment opened a path that had been effectively closed, and the regulator approved a cluster of firms together. The rise of comprehensive stablecoin regulation made a charter close to a prerequisite for a serious stablecoin. And the legitimacy of a federal charter is a powerful selling point to institutional clients. Together these drove an industry-wide rush.

What is a Federal Reserve master account and why does it matter?

A master account is an account held directly with the central bank, granting direct access to its payment rails and to base money held at the central bank itself, instead of balances at a commercial bank. For a stablecoin issuer, it would allow holding reserves directly at the central bank, the safest possible place, eliminating commercial-bank counterparty risk and giving institutions strong confidence in the stablecoin’s safety. It is the real prize because it represents the deepest integration into the financial system, but the bar is extremely high, no crypto-native firm has yet been granted one, and applications remain pending with uncertain outcomes.

What does the trust-charter wave mean for the crypto industry?

It marks the convergence of crypto and traditional banking. The leading crypto firms are choosing to enter the regulated banking system as supervised institutions, accepting banking regulation in exchange for its legitimacy, stability, and access, a profound shift from crypto’s early ethos of operating apart from the traditional system. It is largely a stablecoin story, since charters speak directly to issuers’ need to custody reserves credibly. The convergence brings legitimacy and integration but also the constraints of regulation, and it signals a maturing industry whose leading firms increasingly resemble, and seek to operate alongside, traditional financial institutions.

This article is educational information, not legal, financial, or investment advice. Charter approvals, master account decisions, and regulations are evolving, and details reflect reporting available as of June 26, 2026, which can change quickly. Crucially, a chartered crypto trust bank is generally not covered by federal deposit insurance. Verify current information from primary sources before relying on anything described here.

Key Takeaways

- Prominent crypto trader Garrett Jin has initiated a $21.73M short position on Zcash via Hyperliquid at an entry price of $418.90

- Approximately $4.93M of the total order has been executed, leaving $16.8M unfilled

- Complete execution would position Jin as the platform’s largest ZEC position holder

- Jin’s previous two Zcash trades generated combined profits of $11.66M

- Simultaneously, his 1,268 BTC long position entered at $76,117 faces unrealized losses exceeding $20M

Prominent cryptocurrency trader Garrett Jin has initiated a substantial short position targeting Zcash on the Hyperliquid decentralized trading platform. The position, valued at $21.73 million, carries an entry price of $418.90 per ZEC token.

Blockchain analytics expert Yujin first identified and reported the transaction. Initial data showed that $4.93 million worth of the position had been successfully executed, while the bulk—$16.8 million—remained in the order book awaiting fulfillment.

Potential Impact on Hyperliquid’s Zcash Market

Should the entire order reach completion, Jin’s position would establish him as the dominant Zcash trader on the Hyperliquid platform. This concentration represents significant individual market exposure within the exchange’s ecosystem.

On-chain monitoring service Lookonchain verified the details of Jin’s position. Their analysis revealed the active short employs 2x leverage across 11,780 ZEC tokens, representing approximately $4.92 million in value at the moment of documentation.

Lookonchain’s research also highlighted Jin’s successful track record with Zcash trading. His two preceding ZEC positions collectively yielded profits totaling $11.66 million.

This newest short position continues Jin’s established strategy of betting against Zcash price appreciation. His current wager anticipates ZEC values declining from the $418 threshold.

Bitcoin Long Position Faces Significant Drawdown

Contrary to his Zcash success, Jin’s Bitcoin holdings present a contrasting narrative. He maintains a leveraged long position comprising 1,268 BTC with an average entry point of $76,117 per token.

This Bitcoin trade currently shows substantial negative performance. The unrealized deficit on this position approximates $20.09 million based on recent market data.

Bitcoin’s market price stood around $60,411 during the reporting period, creating a considerable distance from Jin’s $76,117 entry level. This substantial price differential explains the magnitude of unrealized losses.

Taken together, these positions illustrate contrasting outcomes. While Jin has demonstrated profitability through Zcash short strategies, his more substantial Bitcoin wager continues accumulating losses.

Market observers closely monitor Jin’s trading activity due to the considerable capital involved in his transactions. Blockchain analysts including Lookonchain and Yujin systematically document his positions as they materialize on Hyperliquid’s platform.

The $21.73 million Zcash short position remains partially unfilled. Traders following Jin’s activities continue monitoring whether he will complete the full order execution.

Zcash traded at $407.65 during this reporting window, positioning slightly beneath Jin’s $418.90 short entry level. This price differential currently generates modest unrealized gains on the position.

However, his Bitcoin long exposure presents the more pressing challenge. With unrealized losses surpassing $20 million, it constitutes substantial downside risk within his active trading portfolio.

Crypto World

Ripple’s Brad Garlinghouse Slams Michael Saylor’s Bitcoin Strategy as ‘Financial Engineering’

Key Takeaways

- Brad Garlinghouse, Ripple’s CEO, has publicly condemned Strategy’s approach to funding bitcoin acquisitions through preferred shares

- Garlinghouse labeled the strategy as unsustainable “financial engineering” lacking long-term value creation

- STRC preferred shares plummeted to an all-time low, sinking 25% beneath their $100 par value

- Strategy’s common shares fell to their weakest point since February 2024, settling near $82

- Industry analysts at CryptoQuant recommended Strategy halt bitcoin acquisitions and focus on cash reserve restoration

Brad Garlinghouse, CEO of Ripple, maintains his optimistic outlook on bitcoin. However, he has voiced sharp concerns about Michael Saylor’s acquisition methodology.

During a Friday appearance on CNBC, Garlinghouse took aim at Strategy’s practice of issuing preferred shares to generate capital for bitcoin investments. He characterized this approach as “financial engineering” and argued it has inflicted damage across the cryptocurrency sector.

“Financial engineering does not drive long-term value,” Garlinghouse stated. “Team Michael Saylor wasn’t focused on the right stuff and that has hurt the overall market.”

As the head of Ripple, the organization responsible for XRP—a digital asset competing with bitcoin—Garlinghouse clarified that his concerns target the funding mechanism rather than bitcoin itself.

Strategy’s Funding Mechanism Explained

Over the past twelve months, Strategy has relied on preferred share issuances to finance its bitcoin accumulation strategy. The STRC preferred stock offers an 11.5% annual dividend yield and was intended to maintain a value close to $100.

However, Thursday saw STRC crash to unprecedented lows, plunging as much as 26% below its designated $100 par value. Garlinghouse characterized this decline as a “damning indictment” of the company’s approach.

Strategy’s common equity also experienced significant deterioration, reaching levels not seen since February 2024. Shares settled around $82 on Friday. Meanwhile, bitcoin dropped below $59,000 during the trading week.

When STRC trades substantially below $100, Strategy loses the practical ability to issue additional shares and continue bitcoin purchases. The company has suspended this activity temporarily.

Expert Analysis and Recommendations

CryptoQuant published research this week recommending that Strategy suspend bitcoin buying operations and prioritize strengthening its cash position. According to the firm’s analysis, the financial buffer supporting STRC’s dividend obligations has eroded dramatically—from over seven years of coverage down to approximately 14 months.

Benchmark-StoneX analyst Mark Palmer challenged the most pessimistic assessments. He acknowledged that Strategy’s funding mechanism has become “less efficient” but maintains it remains functional. Palmer dismissed comparisons between STRC and completely failed financial instruments.

Pressure on Strategy’s business model has intensified throughout the week. The dual challenge of declining bitcoin valuations coupled with STRC’s deterioration has created a challenging operational environment.

Garlinghouse’s public criticism adds significant weight to mounting questions surrounding the sustainability of Strategy’s preferred-share framework. He directly connected the model’s shortcomings to bitcoin’s recent descent below $59,000.

His fundamental position emphasizes that enduring value in cryptocurrency emerges from practical utility rather than sophisticated financial arrangements.

As of Friday’s close, STRC remains significantly below its $100 par value, while Strategy’s common stock continues trading near multi-year lows.

XRP is trading just above $1, leaving the token at its weakest price level of the year, but onchain data paints a different picture.

The exchange-held XRP supply continues to fall, Binance withdrawals have exceeded deposits for seven straight days, whale flows are holding positive and spot XRP exchange-traded funds (ETFs) have attracted $243 million in inflows since April.

The improving onchain data points to healthy network positioning, even as XRP continues to search for a price bottom.

XRP supply on exchanges continues to shrink

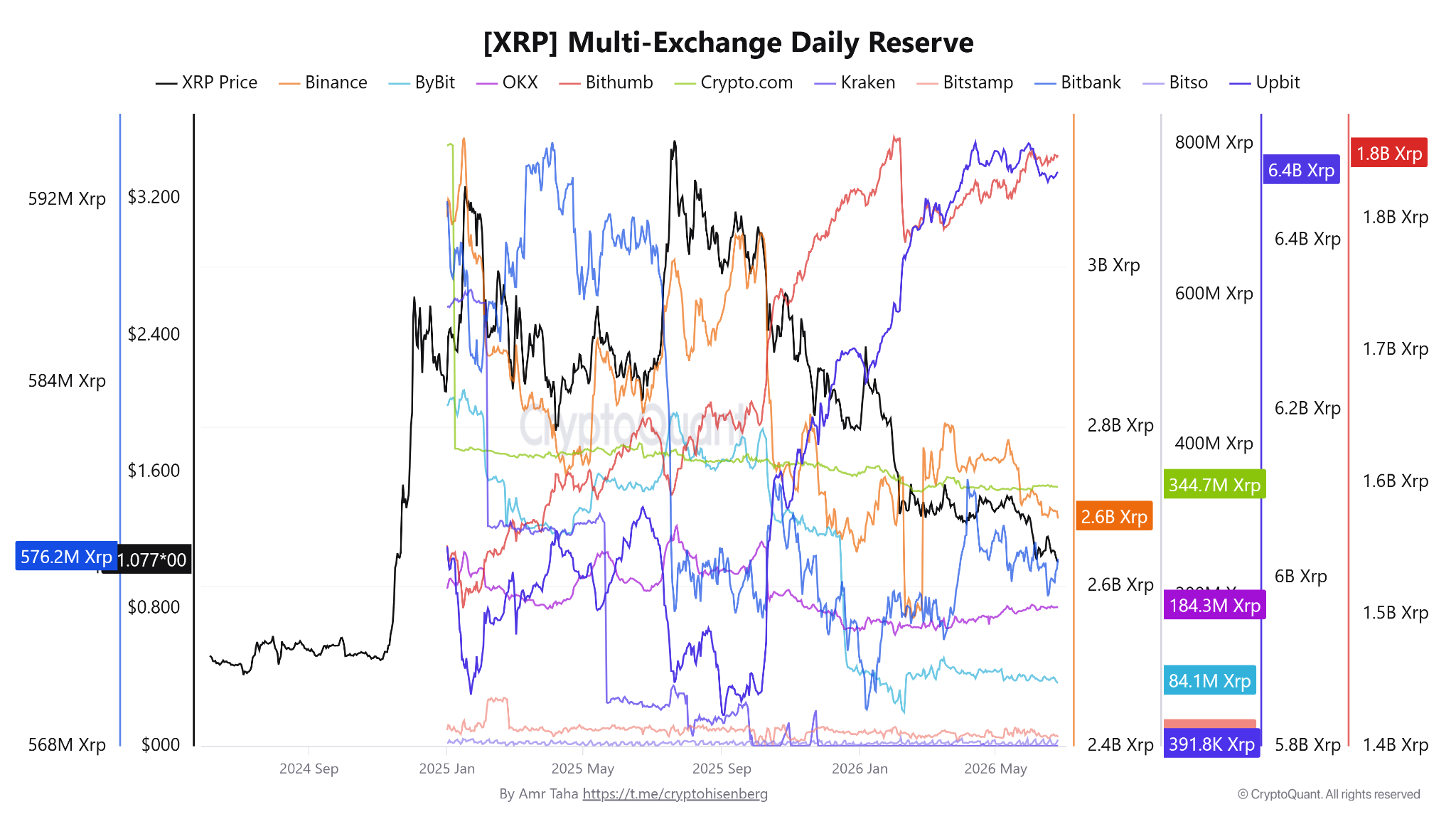

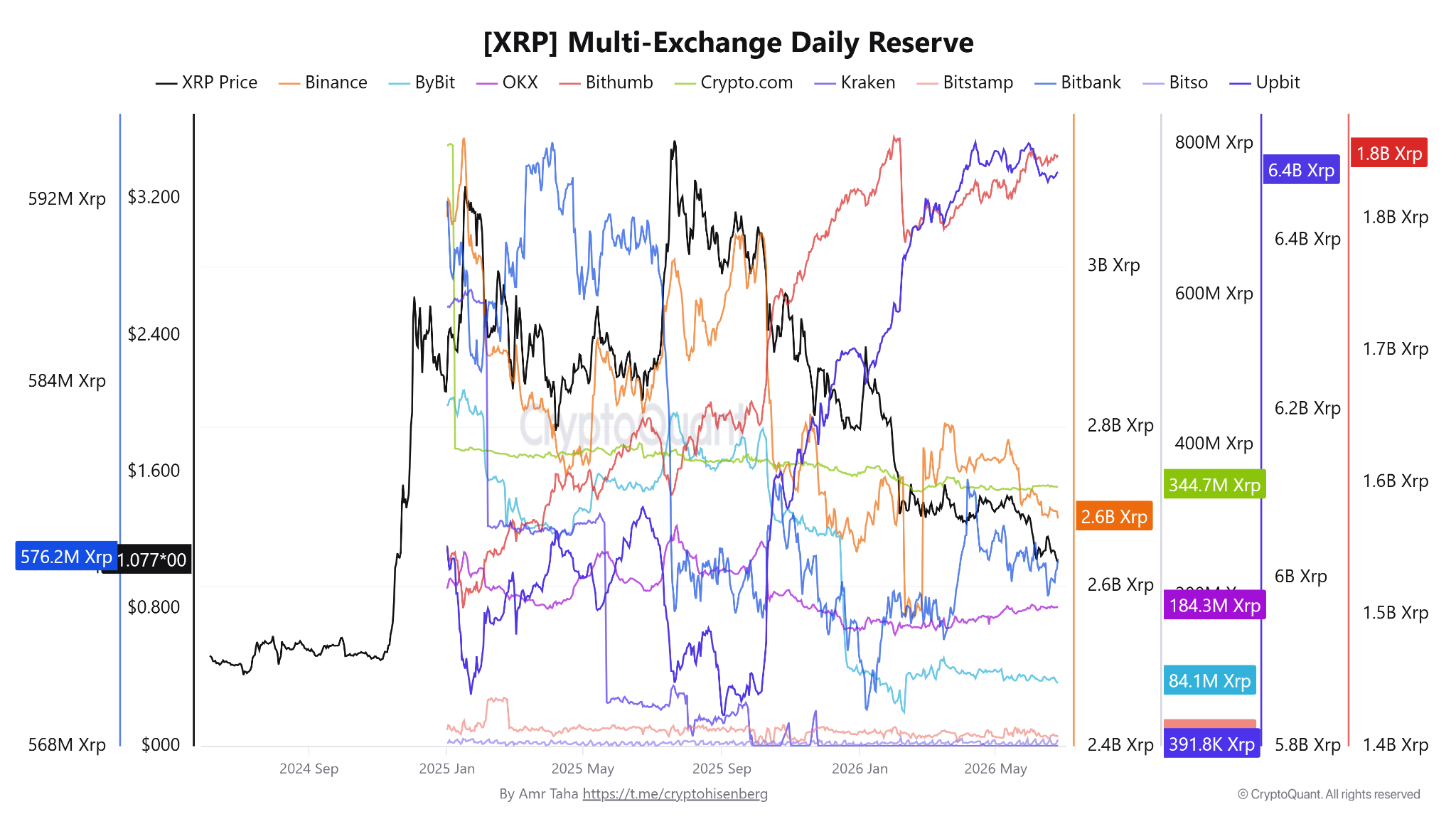

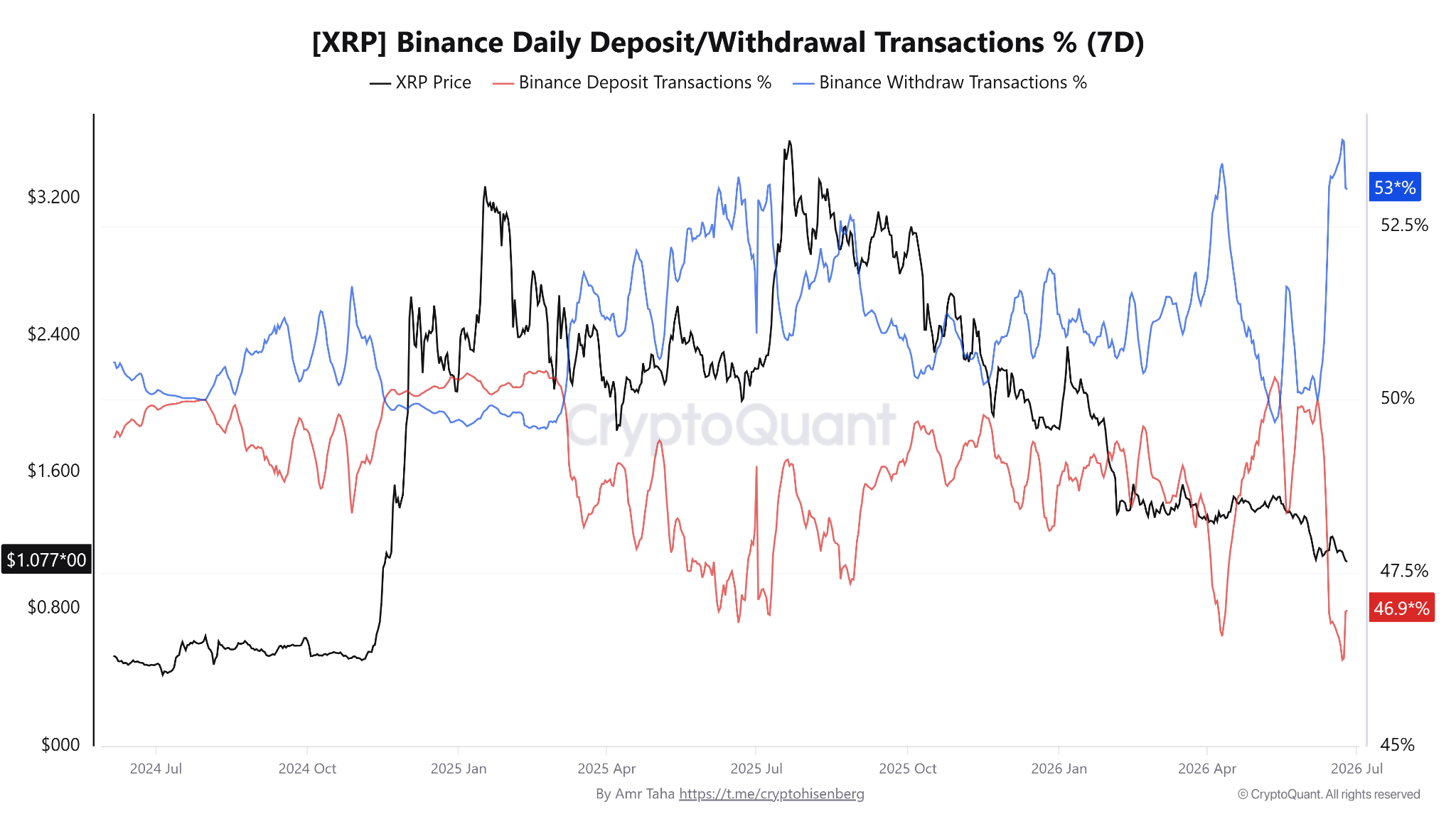

Crypto analyst Amr Taha noted that Binance’s XRP reserve has fallen to its lowest level since March after roughly 100 million XRP left the exchange over the past month. Binance’s balance stood at about 2.68 billion XRP on June 25, down from 2.78 billion XRP on May 12, accounting for the largest outflow among major trading platforms.

XRP multi-exchange daily reserve. Source: CryptoQuant

Other exchanges also posted smaller declines. Upbit’s reserve fell to 2.48 billion XRP on June 25 from 2.51 billion XRP on May 31, while Bybit’s holdings declined to 82 million XRP from 92 million XRP on June 2. Binance led in absolute outflows, while Bybit recorded the steepest percentage decline.

Taha also highlighted a significant shift in Binance transaction activity. XRP withdrawal transactions have exceeded deposits for seven consecutive days since June 17. The seven-day withdrawal share climbed to 53.8% on June 23, its highest reading since June 2024, while deposits fell to 46.1%, the weakest level since 2024.

XRP daily deposit/withdrawal transactions (%) on Binance. Source: CryptoQuant

The metric tracks transaction count rather than XRP volume. This indicates users are moving coins off Binance more frequently than sending them to the exchange, marking the longest withdrawal-led stretch in roughly a year.

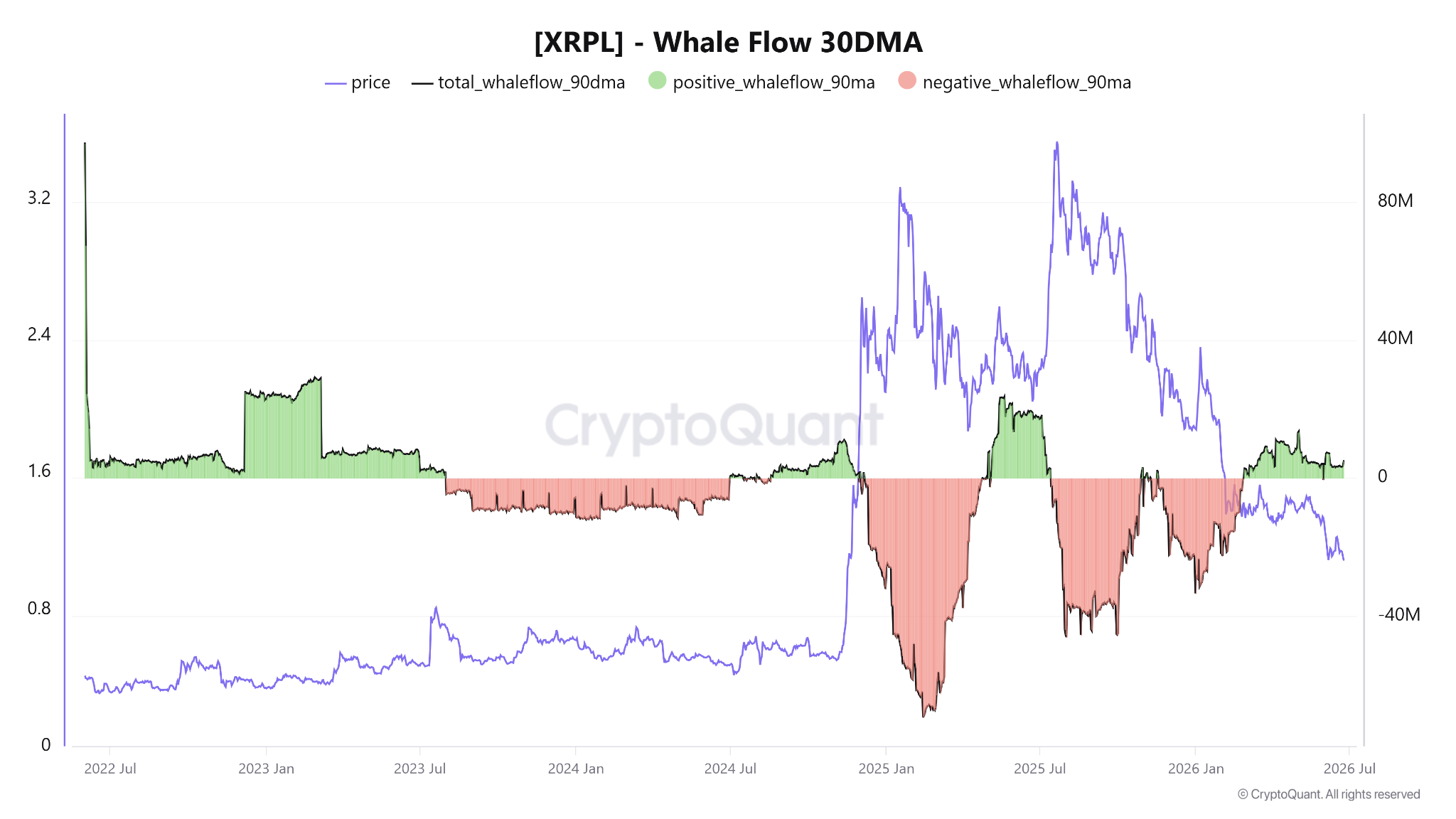

Large XRP holders supported the trend. XRP whale flow on the 90-day moving average has stayed positive throughout the quarter at 5.143 million XRP per day, showing consistent net accumulation by large wallets instead of distribution.

XRP whale flows. Source: CryptoQuant

Institutional demand has also added support. Spot XRP ETFs recorded $2 million in net inflows on June 24, lifting June’s total netflows to $31 million. Since April, the total cumulative inflows have reached $243 million.

Related: SBI to acquire Bitbank in $289M deal creating Japan’s biggest crypto exchange

XRP price approaches a major demand zone

From a technical standpoint, the higher-time-frame market structure remains bearish for the altcoin. XRP touched $1.01 on Thursday, its lowest price of 2026, leaving the token close to its first move below $1 since November 2024. The decline has pushed XRP down 43% year-to-date.

XRP/USDT, one-week chart. Source: Cointelegraph/TradingView

The next key area for XRP sits within the fair value gap between $1 and $0.63, an unfilled price gap created during the sharp rally in late 2024 that could attract buying interest if the decline extends in the coming weeks.

Black Swan Capitalist founder Versan Aljarrah continues to focus on the longer-term chart. The analyst said XRP has spent years building a large accumulation range with higher lows on both weekly and monthly timeframes.

XRP/USD, one-month chart analysis by Versan Aljarrah. Source: X

Aljarrah argued that extended consolidations often produce stronger breakout moves once the price eventually breaks out of the range, with the analyst targeting $10, i.e., a 900% increase from the current price.

Related: HYPE down 22% from record highs: Will spot demand revive the uptrend?

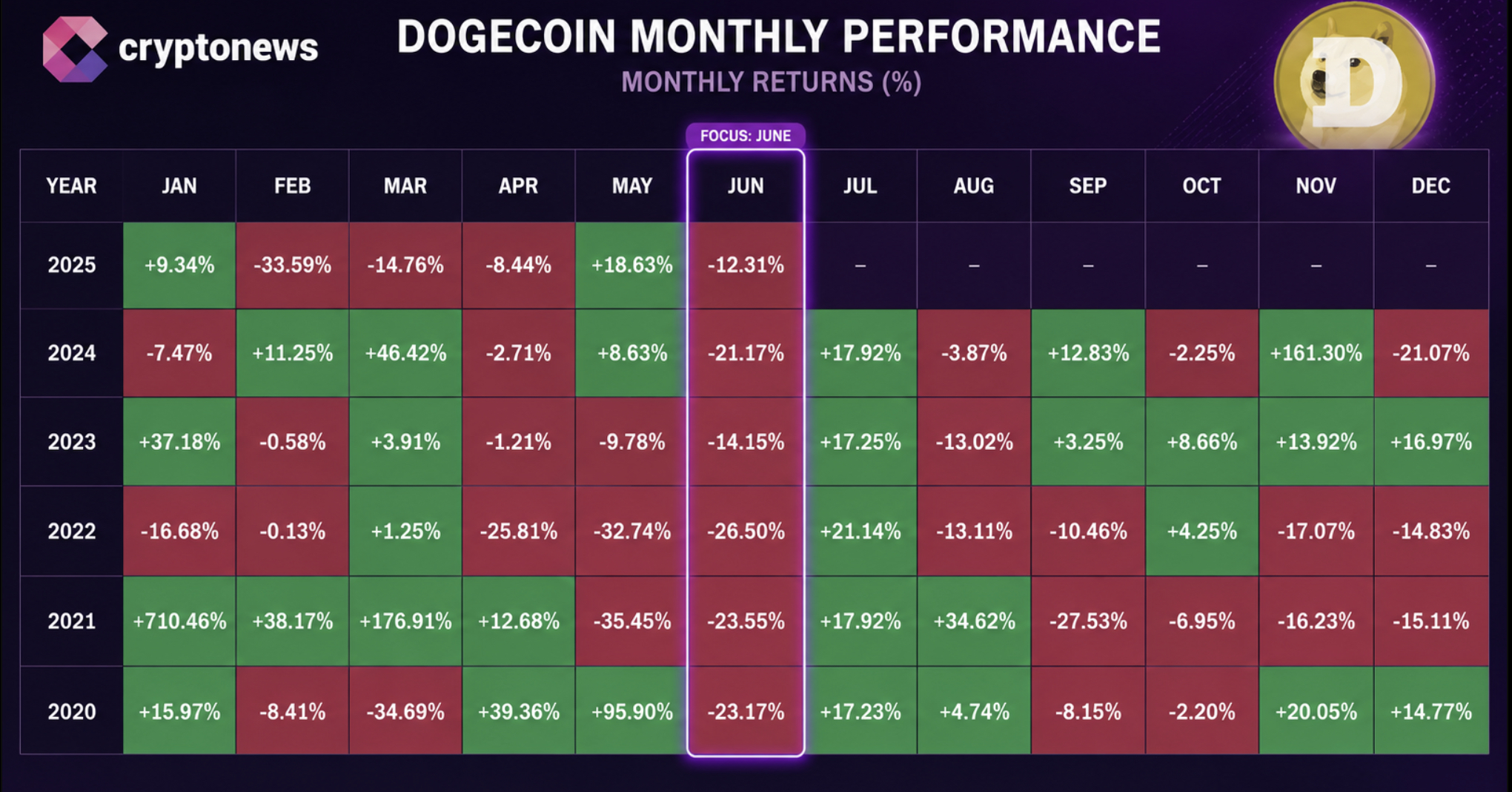

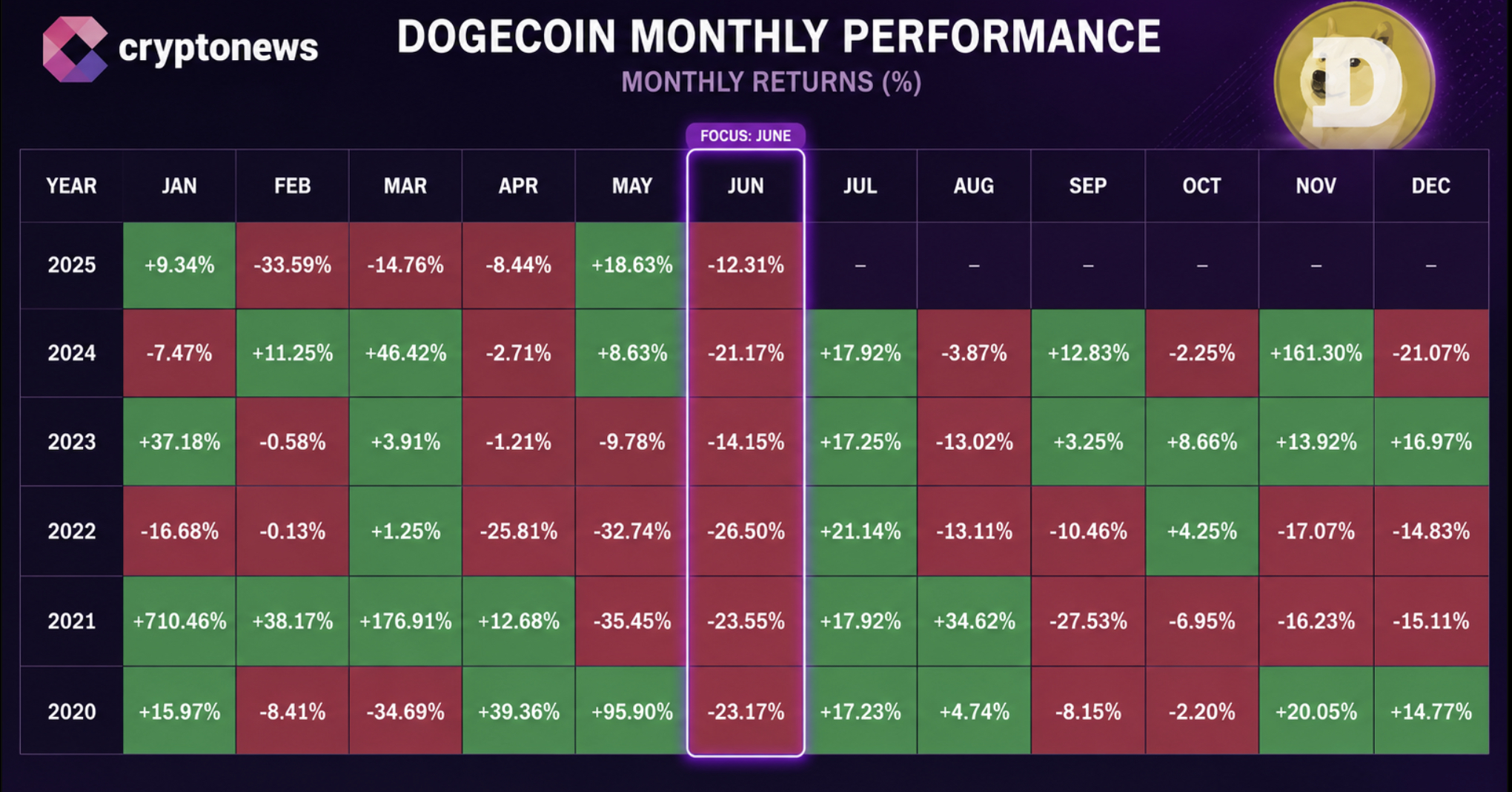

Dogecoin is trading at $0.073, down by more than 3% today, and something is about to make things worse. DOGE is entering its statistically worst month of the year with no confirmed catalyst in sight. What the seasonal data reveals about the next 7 days is not comfortable for holders.

Nine consecutive red Junes. That is the streak DOGE carries into mid-2026, with data confirming the current weakness stems from a technical breakdown in a risk-off market environment. Another metric puts the average June return at -7.29%, with a median loss of 9.94% across the streak. Applied to the current price, that average loss projects DOGE near $0.07 by month-end — and Long Forecast’s model goes further, projecting a 15.6% drop in July that could push the coin toward $0.066.

Will Dogecoin dip further?

Discover: The Best Crypto to Diversify Your Portfolio

Can Dogecoin Hold $0.07 Support or Is a Deeper Drop Coming?

DOGE is trading near $0.075, holding slightly above a key support zone around $0.074. Recent selling pressure pushed the price lower, while trading volume remained elevated during the decline. That points to persistent distribution rather than a sharp panic-driven selloff.

Momentum remains weak but not deeply oversold. RSI is hovering near neutral territory, suggesting sellers still have room to press prices lower. Meanwhile, technical signals continue to lean bearish, with resistance clustered around $0.080, followed by the $0.085 area.

Don’t Miss Out on Our $1,000 USDT Airdrop on ByBit

If DOGE maintains support above $0.074 and market sentiment improves, a recovery toward $0.080–$0.085 becomes possible. A rebound in Bitcoin could help drive that move, especially if buyers return near current levels.

The most likely near-term outcome is consolidation between $0.074 and $0.082. Price action has already shown repeated reactions around these levels, while momentum indicators remain mixed, and conviction from either side is limited.

However, a decisive break below $0.074 could expose the next support zone near $0.070. In that scenario, bearish momentum may accelerate as traders reduce risk and buyers wait for stronger signs of stabilization.

Discover: The Best Token Presales

Maxi Doge Eyes Early-Mover Upside as Doge Tests Critical Levels

DOGE, sitting 82% below its late-2024 peak, is in a drawdown that prompts traders to reassess meme coin exposure entirely. The original memecoin’s upside from current levels is capped by heavy resistance overhead and a seasonal headwind lasting at least another month. That gap between risk and potential return is exactly what rotational capital looks for.

Maxi Doge ($MAXI) is positioning itself as the presale-stage alternative for traders who want meme coin exposure without the baggage of an asset sitting deep in a nine-year seasonal downtrend. The project has raised $4.8 million at a current price of $0.0002826, an ERC-20 token built around a “1000x leverage trading mentality.”

Its community structure includes holder-only trading competitions with leaderboard rewards, a Maxi Fund treasury for liquidity and partnerships, and dynamic staking APY. The branding leans hard into gym-culture meme humor (“Never skip leg-day, never skip a pump”), which has demonstrated real viral traction in the meme coin space.

Don’t Miss Out on Our $1,000 USDT Airdrop on ByBit

The post Dogecoin Faces Danger: Data Shows DOGE Price Could Collapse appeared first on Cryptonews.

Securitize, a platform for issuing and managing tokenized securities, says it expects to raise roughly $400 million ahead of its planned public debut following a merger with Cantor Fitzgerald-backed SPAC Cantor Equity Partners II (CEPT). The update comes after the company reported final redemption results showing fewer shareholders than anticipated chose to exit the transaction.

In a statement released Friday, Securitize said that less than 30% of CEPT shareholders elected to redeem. With the deal structured to fund the company through merger proceeds and additional capital instruments, the firm estimates it will receive approximately $400 million in gross proceeds from the combination, including PIPE (private investment in public equity) financings, while excluding transaction-related expenses.

Key takeaways

- Securitize expects about $400 million in gross proceeds from its SPAC merger, supported by PIPE financing.

- Final redemption results from CEPT showed under 30% of shareholders redeemed, suggesting stronger-than-expected deal continuation.

- The transaction is scheduled to close on Wednesday, July 1, with trading expected to begin on the New York Stock Exchange on July 2 under the ticker SECZ.

- Securitize’s move highlights growing Wall Street engagement in tokenization as US regulators continue to scrutinize how tokenized securities are traded and implemented.

Redemptions come in lower than expected

SPAC mergers can hinge on whether public shareholders redeem their positions before the deal closes. In Securitize’s case, the company said its final redemption results indicate that fewer than 30% of CEPT investors opted out—an outcome that helped keep the merger on track and supported investor confidence.

Market reaction reflected that dynamic. CEPT shares rose on Friday, closing up 7% to $10.86 and extending gains in after-hours trading to around $11, according to available market listings.

For investors, the practical implication of lower redemptions is that less transaction capital is withdrawn at the last moment, which can reduce funding uncertainty right before a listing. While the merger’s final economics still depend on the deal’s full structure and closing conditions, redemption levels can serve as an early signal of whether the sponsor-backed plan has broad buy-in among the SPAC’s public shareholders.

Timeline: vote, closure, and expected NYSE debut

Securitize and CEPT said the business combination is expected to close on Wednesday, July 1, assuming shareholders approve the deal on Monday and other standard closing conditions are met. After the closing, the combined company is expected to begin trading on the New York Stock Exchange on Thursday, July 2, under the ticker SECZ.

The sequence matters for traders and market participants watching tokenization-linked listings. The gap between shareholder approval and the expected start of trading is when operational steps—such as completion of the transaction and readiness of post-merger listing—must align. Any changes in the schedule would be a key item for those tracking the tokenized-securities sector’s most prominent public-market entry points.

Why Securitize’s debut matters for tokenization

Securitize’s prospective public-market arrival is positioned as a milestone in the broader push to bring tokenized assets into mainstream finance—particularly as institutions increase their focus on tokenization infrastructure and regulated digital-asset rails.

“Reaching the public markets is a significant milestone for Securitize and a reflection of the growing momentum behind tokenization,” Securitize co-founder and CEO Carlos Domingo said in connection with the deal. Domingo also argued that the concept of major institutions embracing tokenized securities has shifted from “theoretical” to more mainstream over the past several years.

The company is backed by prominent financial institutions including BlackRock and Morgan Stanley, as well as established crypto players such as Coinbase and Circle. Securitize has also built credibility in the tokenization space by supporting the representation of assets on blockchains, and it has worked to translate that capability into regulated issuance and settlement processes.

Earlier this year, Securitize partnered with the New York Stock Exchange to create tokenized assets for the exchange’s upcoming tokenized securities platform, which is part of a wider trend of traditional venues exploring tokenized market infrastructure.

Regulatory backdrop: tokenized stocks still under scrutiny

The timing of Securitize’s public debut comes as US regulators continue to evaluate how tokenized securities should be handled in practice. Tokenization can span multiple categories—from tokenized real-world assets to digital representations of traditional stocks—raising questions about custody, transfer restrictions, market structure, and compliance.

Earlier coverage cited that the US Securities and Exchange Commission was reportedly prepared to allow trading of tokenized stocks under an innovation-related exemption, but that plan was delayed later after stock exchange officials raised implementation concerns. That context underscores why market participants will likely watch how Securitize and partners address operational and compliance details as public trading begins.

Other institutional commentary also points to growing expectations for tokenization adoption. For example, a report attributed to Standard Chartered suggested that tokenized assets active in decentralized finance could expand dramatically to $2.7 trillion by the end of 2030, projecting a 37-fold increase from earlier baselines. While such projections are longer-term and subject to change, they reflect how capital markets research firms are framing tokenization as an area with potential for significant expansion.

In the near term, what remains uncertain is how quickly regulatory clarity translates into broader market adoption beyond pilots and limited offerings—especially for tokenized equities where market structure questions can be complex. Investors should also keep an eye on whether tokenized-securities platforms built by major venues can achieve the liquidity, transferability, and compliance requirements needed for scale.

With CEPT’s lower-than-expected redemption rate and a clear path to an NYSE listing under SECZ, the next steps are straightforward: shareholder approval on Monday and the scheduled close on July 1. The bigger question for the sector is how regulatory guidance and real-world trading implementations evolve after these listings, and whether tokenization continues moving from concept and infrastructure into liquid, widely accessible markets.

Crypto World

Ethereum (ETH) Price Plummets as Whale Investors Face Historic Losses Not Seen Since 2019

Key Takeaways

- Ethereum has declined 23.5% in the past month, currently trading near $1,557

- Large ETH holder groups are experiencing unrealized losses for the first time in five years

- Ethereum ETF products are approaching their seventh consecutive week of capital withdrawals

- A protocol developer highlights potential funding shortfall of approximately $30M annually in coming months

- Critical price levels: support zone at $1,500–$1,510; overhead resistance begins at $1,710

The world’s second-largest cryptocurrency has faced relentless downward pressure during June, sliding from levels above $2,000 to approximately $1,557 by June 26. This represents a monthly decline of 23.5%, with an additional 6.7% drawdown occurring over the past seven days alone.

In a symbolic shift, Tether’s total market capitalization has now surpassed Ethereum’s for the first time in history — $186.06 billion compared to $185.66 billion — underscoring ETH’s recent underperformance in the broader cryptocurrency ecosystem.

Market analyst Ted Pillows commented via social media that Ethereum “tapped the lows again” and observed that “momentum is still weak due to broader market correction.” He suggested that if ETH can successfully reclaim the $1,750 threshold, a potential relief bounce could materialize in the following month.

Technical analysis of the daily timeframe reveals that ETH violated an ascending trendline established in February. Following this breakdown, the asset experienced rapid declines through the $1,900, $1,800, and ultimately into the $1,550 region.

Major Holder Groups Recording Rare Loss Scenario

Data from CryptoQuant indicates that all significant Ethereum whale categories — including addresses controlling more than 100,000 ETH — are currently experiencing unrealized losses. This phenomenon has occurred only once previously, during 2019, which ultimately marked a long-term price floor for the cryptocurrency.

Historically, capitulation among large holders has coincided with market bottoms rather than signaling further deterioration. While smaller whale categories have periodically entered loss territory, the participation of the largest stakeholders in this condition represents an exceptional occurrence.

The Estimated Leverage Ratio (ELR) metric has simultaneously contracted from 1.11 to 0.85 throughout the past three weeks. This movement indicates substantial closure or liquidation of leveraged trading positions, potentially alleviating additional downside risk.

Exchange-Traded Fund Withdrawals and Development Financing Concerns

Ethereum spot ETF products are tracking toward seven straight weeks of net capital outflows, with the current period positioned to register the most significant withdrawals since January, based on SoSoValue analytics.

Trent Van Epps, Protocol Guild coordinator who recently departed the Ethereum Foundation following a five-year tenure, has issued a cautionary statement regarding core development financing challenges. He calculates that Ethereum’s essential development operations require approximately $30 million annually, an amount the Ethereum Foundation’s reserves may struggle to consistently provide.

Van Epps noted that Protocol Guild has allocated nearly $40 million to developers across four years, but emphasized this remains insufficient. He anticipates new institutional participants will need to emerge within the coming months to address the gap.

Primary technical levels to monitor: downside support positioned at $1,510 and the psychologically significant $1,500 level; upside resistance located at $1,710 and $1,774. The MACD indicator has returned to negative territory, with the signal line currently registering -78.35.

Kalshi has secured World Cup branding exposure through a strategic partnership with ADI Predictstreet, FIFA’s official prediction market partner for the 2026 tournament.

Summary

- Kalshi will receive FIFA World Cup branding exposure through its partnership with ADI Predictstreet.

- The agreement expands Kalshi’s sports strategy as trading volume tops $1 billion per day.

- The deal comes as Kalshi pursues a $40 billion valuation and challenges Illinois’ licensing law.

According to Kalshi, the agreement will place the company’s branding alongside ADI Predictstreet across stadium, television, and digital coverage beginning with the FIFA World Cup knockout stage. Although Kalshi is not an official FIFA partner, the arrangement gives the prediction market operator visibility at the tournament while ADI Predictstreet retains its official designation.

The companies said the relationship extends beyond tournament marketing. Kalshi will support the continued expansion of markets available on ADI Predictstreet’s platform as the partnership develops after the World Cup.

Why is Kalshi increasing its presence in sports?

The World Cup agreement adds to a series of football-focused partnerships announced by Kalshi in recent months. According to the company, it has also partnered with the Argentine Football Association, the Croatian Football Federation, Luka Modric, and Men in Blazers as it increases its presence around major sporting events.

At the same time, trading activity on the platform has continued to accelerate. Kalshi said daily trading volume surpassed $1 billion last week during heightened World Cup engagement across prediction market platforms.

Bank of America estimated that Kalshi accounts for roughly 89% of measured U.S. prediction market volume, placing it well ahead of other regulated competitors.

Commenting on the partnership, ADI Predictstreet Chief Executive Dimitrios Psarrakis said combining Kalshi’s market reach with ADI Chain’s infrastructure would introduce regulated prediction markets to more users worldwide.

Kalshi Chief Executive Tarek Mansour described the FIFA World Cup as an opportunity to increase awareness of the platform while encouraging more fan participation through prediction markets.

According to FIFA, ADI Predictstreet became the governing body’s first official prediction market partner in April before launching its Gibraltar-licensed platform ahead of the tournament. The service currently focuses on football-related markets and plans to expand into news, technology, entertainment, culture, and other real-world events.

The expanded 48-team FIFA World Cup features 104 matches across the United States, Canada, and Mexico, creating one of the largest global audiences for sports-related prediction products.

What else is shaping Kalshi’s expansion?

The World Cup partnership comes as Kalshi continues expanding both commercially and legally.

Earlier this week, the company filed a federal lawsuit challenging Illinois Senate Bill 3019, arguing that the state cannot require separate licenses for federally regulated sports event contracts. In its complaint, Kalshi said the Commodity Futures Trading Commission has exclusive authority over its contracts under the Commodity Exchange Act and argued that complying with Illinois’ licensing system would conflict with its obligation to operate a single national market.

Separately, Kalshi has entered discussions to raise fresh capital at a valuation of about $40 billion, according to reports. If completed, the financing would represent an 82% increase from the company’s $22 billion valuation during its $1 billion funding round in May, which included Coatue, Sequoia Capital, Andreessen Horowitz, and Morgan Stanley.

The latest developments also coincide with increased attention on the prediction market sector. Earlier this week, U.S. senators urged the CFTC to investigate Polymarket over allegations that it used deceptive advertising to reach American users despite restricting access in the country. The lawmakers also questioned whether the federal regulator has sufficient authority and resources to oversee prediction markets while continuing to argue that federal law preempts state regulation.

Bitcoin (BTC) dropped below $60,000, a key psychological support, on Thursday as losses in megacap technology stocks weighed on investors’ broader risk appetite, adding pressure to an already fragile crypto market.

BTC/USD vs. Nasdaq and S&P 500 daily performance chart. Source: TradingView

The decline has triggered a classic bearish reversal setup that may push the BTC price under the $54,000 mark in the coming days.

Key takeaways:

- Bitcoin’s break below $60,000 has erased its June gains and activated multiple bearish setups.

- Bitcoin’s rounded top and daily bear flag breakdowns are both projecting a downside target below $54,000.

BTC’s rounded top breakdown signals more pain ahead

The BTC/USD pair fell as much as 4.8% on Thursday, hitting an intraday low near $58,000 and erasing its entire June advance. The pullback also completed what appears to be a rounded top pattern on the four-hour chart.

BTC/USD four-hour chart tracking the rounded top bearish setup. Source: TradingView

In technical analysis, a rounded top forms when buying momentum gradually exhausts, shifting the asset from an uptrend to a downtrend in an inverse-U-shaped structure. The pattern officially resolves when the price breaks below the “neckline” or the structure’s base support.

By measuring the distance from the top of the dome to the neckline and projecting that same distance downward from the breakdown point, analysts calculate a clear target.

For Bitcoin, this measured downside target sits just under the $54,000 level, representing an approximate 8.9% drop from current prices.

On the daily chart, Bitcoin has simultaneously triggered a bear flag breakdown.

BTC/USD daily chart tracking the bear flag breakdown setup. Source: TradingView

This secondary pattern independently projects an identical move toward the $54,000 zone, adding substantial weight to the bearish case.

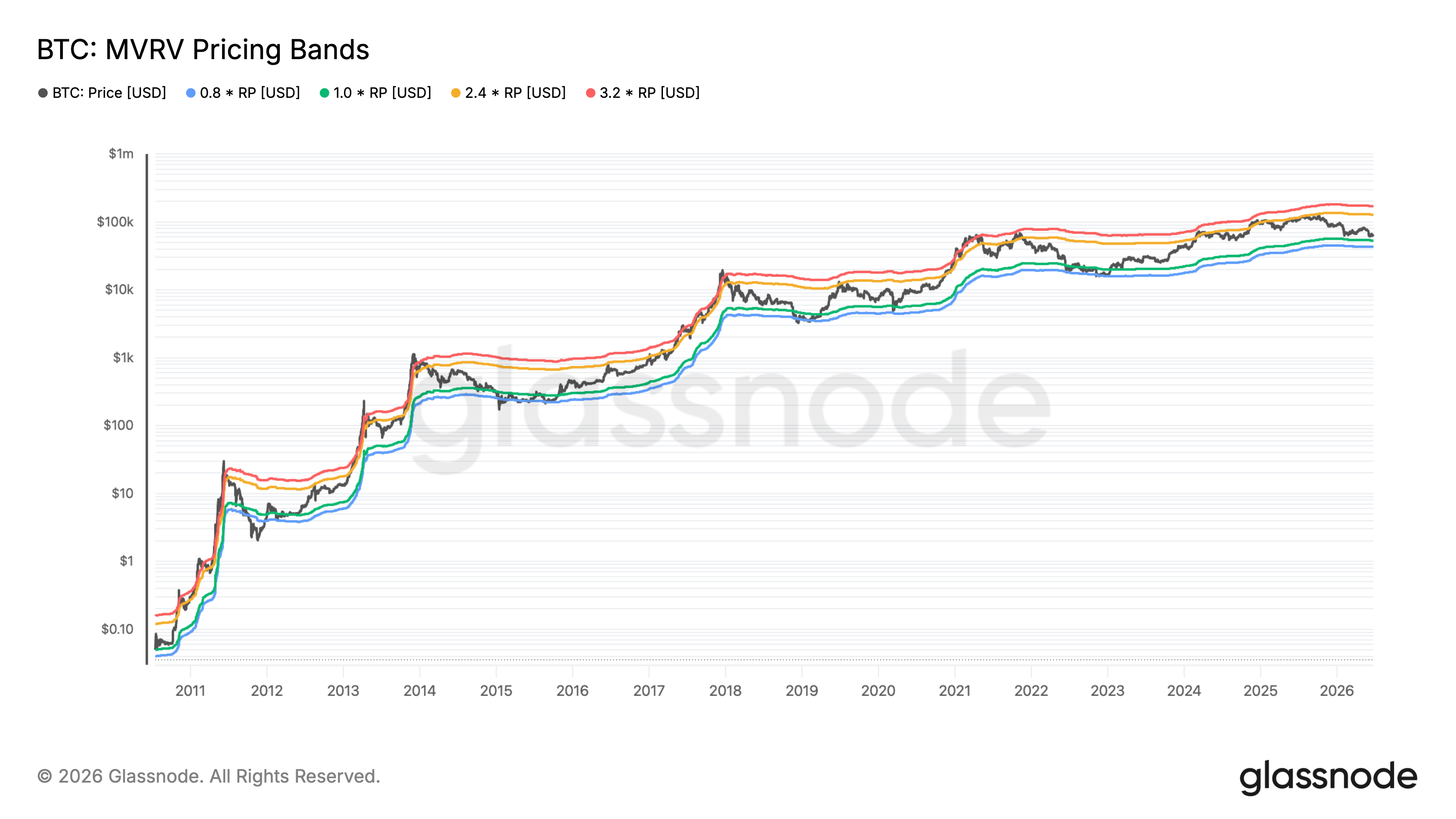

Bitcoin MVRV bands increase $54,000 target odds

Bitcoin’s on-chain price bands also point to the same downside area highlighted by the rounded-top and bear-flag setups.

Glassnode’s MVRV pricing bands compare Bitcoin’s market price with its realized price, or the average price at which coins last moved on-chain. In simple terms, they show whether the market is trading at unusually high profit or loss levels.

BTC MVRV pricing bands vs. price. Source: Glassnode

As of Wednesday, Bitcoin was trading near $60,997, while the 1.0 MVRV band, shown in green, sat around $53,390. That level closely matches the technical downside target near $54,000, making it an important support zone if BTC extends its decline.

Related: Bitcoin nearly loses $59K as DXY surges: Are traders bracing for more pain?

A deeper selloff, however, could push Bitcoin toward the 0.8 MVRV band, shown in blue, near $42,700. Historically, Bitcoin’s major bear-market bottoms have formed around this lower blue band, where unrealized losses become extreme, and capitulation risk rises.

XRP is trading near the $1.00 level, down about 9% in the last seven days and more than 52% over the past year.

But UK-based technical analyst ChartNerd is suggesting that the deeper the Ripple token falls from here, the better the potential risk-reward setup becomes, with a possible demand zone between $0.90 and $0.70 if $1.00 gives way.

What the Charts Are Saying

ChartNerd has been tracking this setup since at least June 12, when he published a thread laying out the macro picture. According to him, XRP spent most of 2023 and into late 2024, capped below $0.80/$0.70 resistance that acted as a ceiling up until there was a breakout in Q4 2024.

That breakout, he says, was what eventually pushed XRP to its all-time high of $3.65 in July 2025, and since then, the trend has gone the other way, with key moving averages lost and a weekly 20/50 EMA death cross confirming the structural change, and the asset dropping from its January 2026 peak of $2.40 all the way to where it is now.

Recall that in February, XRP hit a low of $1.12, after which it attempted a recovery, with a bunch of sideways trading eventually taking it near $1.55, where it was rejected. Per ChartNerd’s analysis, that rejection kick-started the current leg down to lows near $1.00 in June, putting it in what the market watcher called his “area of interest,” a zone where he has been keeping an eye out for a potential cycle bottom between now and Q4 2026.

In his view, the reason that zone matters is that the old resistance level from 2023 and 2024 could switch to support. And if XRP holds anywhere in the $0.90 to $0.70 range during any deeper market drop, the previous ceiling will become the floor.

“This is a high-interest support region, but confirmation still matters most, and we do not have it yet,” he wrote at the time.

But now, the analyst believes XRP’s decline is pushing it further into the area of interest, and the more it falls, “the stronger the risk-reward setup becomes.” He said that he’s also watching the 10-year Gaussian Channel, which, according to him, XRP is now entering, and which has not failed as a guardrail for as long as he has tracked it.

On the timing question, ChartNerd stated in a different post that there is a “very strong likelihood” that a market bounce could happen in the coming weeks as June ends, something that is consistent with what Bitcoin tends to do in midterm years. However, he added a caveat: it will probably be a relief rally that leads to a final drop in the last quarter of the year.

The On-Chain Picture

Elsewhere, analyst Ali Martinez said that XRP is testing a major volume block at $1.06, where on-chain data shows more than 830 million tokens changed hands. Below it, the next important clusters on the UTXO Realized Price Distribution are at $0.80, $0.62, and $0.51.

At the same time, another market watcher, CasiTrades, observed that XRP was at its “most critical moment” in the current cycle, with buy orders placed at $0.93 and a deeper Fibonacci level at $0.87, framing the current fear as part of how bottoms actually form, not as a reason to sell.

The post XRP’s Slide to Sub-$1.00 Could Set Up ‘Risk-Reward’ Zone: Analyst appeared first on CryptoPotato.

The European Parliament’s Committee on Economic and Monetary Affairs (ECON) has asked the European Commission to examine whether additional parts of the crypto sector—such as crypto lending and borrowing, staking, non-fungible tokens (NFTs), and decentralized finance (DeFi)—should be brought within the EU’s regulatory perimeter. The request is set out in an own-initiative resolution tabled for the Parliament’s plenary vote, where it is expected to be considered on July 7.

While the measure would not amend the EU’s Markets in Crypto-Assets Regulation (MiCA) or create new legal obligations, it signals how lawmakers may shape subsequent Commission proposals and supervisory priorities. For crypto-asset service providers, banks, and institutional investors, the resolution matters less for immediate enforceable change and more for how it could influence the direction of EU crypto policy—particularly around stablecoins and “tokenization” of traditional financial services.

Key takeaways

- ECON urges the European Commission to assess whether crypto lending/borrowing, staking, NFTs, and DeFi merit additional regulation beyond MiCA.

- The draft resolution supports the development of euro-denominated stablecoins within MiCA and frames them as potentially complementary to tokenized bank deposits and wholesale central bank digital currency models.

- ECON calls for consistent, EU-wide application of MiCA to avoid divergent national rules that could fragment the single market.

- If adopted, the resolution would become the Parliament’s official policy position, but it would not modify MiCA or impose new obligations.

ECON’s resolution: expanding the policy lens beyond MiCA

The recommendations were drafted by Belgian Member of the European Parliament Johan Van Overtveldt and advanced through ECON’s internal negotiations before being tabled for a plenary vote. According to the European Parliament’s procedure documents, the resolution is an own-initiative instrument designed to set out guidance for the Commission regarding the future shape of EU digital asset regulation.

ECON’s central request is forward-looking: the committee asks the Commission to evaluate regulatory coverage for activities that are not uniformly addressed by MiCA’s current scope. The resolution explicitly references crypto lending and borrowing, staking, NFTs, and DeFi—areas that, in practice, span multiple business models and may involve varying degrees of custody, asset pooling, market-making, governance structures, and cross-border service provision.

For compliance teams and regulated intermediaries, the key issue is not simply “whether” these activities should be regulated, but “how” and “under which regime.” MiCA already establishes licensing and authorization requirements for certain crypto-asset service providers, while other frameworks—such as rules on anti-money laundering (AML), consumer protection, and market conduct—may apply depending on structure and distribution. ECON’s call indicates lawmakers want clearer boundaries and regulatory coherence as these products evolve.

Stablecoins and tokenized finance: a more constructive regulatory stance

A major element of the ECON resolution relates to stablecoins, particularly those denominated in euros. The text frames euro stablecoins as potentially supportive of the EU’s payments ecosystem and encourages their development within MiCA’s framework.

That approach reflects a broader policy shift among some European institutions, including a recognition that stablecoins can operate alongside—rather than necessarily replace—existing money and payment rails. ECON links euro-denominated stablecoins to potential integration with tokenized commercial bank deposits and wholesale central bank digital currencies, suggesting that future EU financial infrastructure could incorporate multiple “digital money” channels.

The policy context is particularly sensitive given how stablecoin arrangements interact with banking liquidity and reserve management. In earlier discussions around the banking turbulence in the United States, concerns were tied to reserve custody and banking counterparties. For example, during the collapse of Silicon Valley Bank, USDC issuer Circle reportedly held a material portion of reserves at the bank, and USDC briefly lost its dollar peg. Although those events occurred outside the EU, they continue to influence how European policymakers evaluate reserve quality, redemption arrangements, and systemic risk controls for stablecoins.

ECON’s resolution also aligns with the committee’s parallel work on the euro’s digital future. It references legislative momentum supporting a “coexistence” model for a potential digital euro alongside private digital money solutions—an approach that suggests policymakers may view stablecoins and public digital currency designs as complementary components of a broader digital payments architecture.

MiCA implementation pressure and the question of national divergence

The resolution goes beyond new regulatory topics by focusing on execution and market structure. It urges consistent application of MiCA across member states to preserve a level playing field for crypto firms. This is a crucial compliance concern: when national regulators introduce additional or differing requirements, firms face increased operating cost, legal uncertainty, and fragmentation of distribution strategies within the EU.

ECON’s earlier draft, presented by Van Overtveldt in February, reportedly focused more tightly on MiCA’s existing framework—such as stablecoin classifications and legal certainty for multi-issued stablecoins. Over months of negotiation, the committee incorporated a broader set of policy questions, culminating in the current recommendation set that also calls for reconsideration of regulatory coverage for activities such as DeFi and staking.

At the EU level, the Commission is already working to reassess parts of MiCA’s scope. In May, the European Commission launched a public consultation seeking input on whether the framework should be expanded to cover areas that include DeFi, staking, lending, NFTs, and tokenized financial assets, while also revisiting debates around MiCA’s ban on interest-bearing stablecoins. Although consultations are not binding legislation, they typically shape the Commission’s next steps and can provide a timeline for future legislative proposals.

Implementation is also time-bound. MiCA’s transitional period is set to end on July 1, after which crypto-asset service providers generally need authorization under MiCA to continue operating across the EU. That deadline increases the practical stakes for firms regarding licensing strategy, supervision expectations, and product mapping—especially for services that may fall near the edges between crypto-asset activity and activities that regulators may treat differently under existing financial law.

Institutional implications: compliance, consumer protection, and legal clarity

For banks, payment firms, and institutional investors assessing crypto exposure, the resolution underscores that EU oversight is moving toward a more comprehensive assessment of how crypto activities affect market integrity and risk allocation. Even without immediate amendments to MiCA, the Parliament’s policy position can influence supervisory guidance, regulatory interpretation, and the Commission’s legislative drafting priorities.

Key open questions remain. ECON’s call does not specify a single mechanism for extending regulation, and the outcome of the plenary vote would only establish a non-binding political mandate for the Commission. In practice, the future direction could depend on how the Commission and co-legislators determine which activities are best addressed by MiCA extensions versus other EU regimes (for example, rules tied to financial services licensing, AML/KYC, consumer protection, or market abuse).

Cross-border coordination is also likely to remain a central theme. DeFi and tokenized asset activities often rely on service providers, intermediaries, or infrastructure operating across jurisdictions. As the EU considers regulatory scope expansion, compliance teams will need to monitor how authorization requirements, supervisory expectations, and governance standards may be applied to novel business models—particularly those with decentralized features that complicate “who is responsible” under traditional regulatory frameworks.

Closing perspective

As the July 7 plenary vote approaches, the resolution’s adoption would provide the European Parliament with an explicit mandate on crypto regulatory coverage, reinforcing pressure on the Commission’s ongoing MiCA review process. The central item for observers is how the Commission translates this political direction into concrete legislative options—if any—particularly for stablecoins, DeFi-adjacent services, and staking-related business models.

Garrett Jin Launches Massive $21.7M Short Position on Zcash (ZEC) via Hyperliquid

10 Intense Thriller Movies That Are Perfect From Start To Finish

World Cup third-place teams standings and how Scotland can qualify for round of 32

-

Entertainment7 days ago

Entertainment7 days agoRenter of Home in Anne Heche Crash Denies Settlement With Son

-

Sports4 days ago

Sports4 days agoTwo goals and an assist by sheer aura: Cristiano Ronaldo just entered the World Cup chat

-

Tech5 days ago

Tech5 days agoMicrosoft accidentally kills epic Outlook email threads

-

Fashion17 hours ago

Fashion17 hours agoWeekend Open Thread: Staud – Corporette.com

-

Business7 days ago

Business7 days agoSoccer-U.S. defends Iran World Cup travel restrictions, says discussions ongoing

-

Politics1 day ago

Politics1 day agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Politics1 day ago

Politics1 day agoPotential 2028er World Cup attendee leaderboard

-

Business1 day ago

Business1 day agoAsia stock markets slide as tech shares slump

-

Tech2 days ago

Tech2 days agoA Look At A Gaggle Of Transputer Boards

-

Crypto World3 days ago

Bitcoin (BTC) Dips Below $62K, Ethereum (ETH) Plunges 6% Daily: Market Watch

-

Crypto World3 days ago

Crypto World3 days agoSecuritize Wraps Roubini's SEC-Registered ETF as Dubai VARA Digital Security

-

Crypto World2 days ago

Crypto World2 days agoDell (DELL) Shares Tumble Over 5% Following Analyst Downgrade to Hold

-

Business3 days ago

Entergy settles forward sale agreements, raises $672 million in cash proceeds

-

Crypto World7 days ago

Crypto World7 days agoCan Charles Hoskinson Really Rescue Cardano?

-

Sports14 hours ago

Sports14 hours agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Crypto World5 hours ago

Crypto World5 hours agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Crypto World17 hours ago

Crypto World17 hours agoRTX holders must register wallets before token distribution begins

-

Crypto World20 hours ago

Hyperliquid Named on Singapore MAS Investor Alert Register

-

Crypto World7 days ago

Crypto World7 days agoJake Chervinsky accuses CME of protecting derivatives monopoly

-

Sports2 days ago

Sports2 days agoIndia vs Bangladesh LIVE Score, Women’s T20 World Cup: Bangladesh Opt To Bat; India Enter ‘Do-Or-Die’ Stage As Semi-Final Race Heats Up

You must be logged in to post a comment Login