Crypto World

What is impermanent loss? The hidden cost in DeFi

Providing liquidity to a decentralized exchange looks like easy passive income, until you withdraw and find you have less than if you had simply held your tokens. That gap is impermanent loss, the most misunderstood risk in DeFi. This guide explains what causes it, how to calculate it, and how to limit it.

Summary

- Impermanent loss is the opportunity cost a liquidity provider suffers when the value of tokens deposited in a liquidity pool ends up lower than if the same tokens had simply been held in a wallet.

- It is caused by price divergence: as the prices of the two paired tokens move apart, the automated market maker rebalances the pool, leaving the provider with more of the falling asset and less of the rising one.

- It is called “impermanent” because the loss reverses if prices return to their original ratio, and it only becomes permanent when the provider withdraws.

- Trading fees and token rewards offset impermanent loss, and a position is profitable when those earnings exceed the loss, but studies show that for many liquidity providers, the loss outweighs the fees.

- The main ways to limit it are choosing stablecoin or correlated pairs, which barely diverge, and understanding the trade-off before providing liquidity to volatile pairs.

Impermanent loss is the opportunity cost a liquidity provider suffers when the value of the tokens they deposited into a decentralized exchange’s liquidity pool ends up lower than it would have been had they simply held those same tokens in their own wallet. It is one of the simplest-sounding yet most misunderstood risks in decentralized finance, and it catches a great many people who are drawn to liquidity provision by the promise of passive income.

The mechanism trips people up because it is counterintuitive: you can deposit two tokens into a pool, watch their prices rise, earn fees the whole time, and still end up worse off than if you had done nothing at all. The word impermanent makes it sound harmless, almost like a temporary inconvenience, but for liquidity providers in volatile pools, it can be a substantial and very real drag on returns.

Understanding what causes it, how to estimate it, and how to limit it is essential for anyone thinking about supplying liquidity, because it is the single factor most likely to turn an apparently profitable strategy into a losing one.

The reason impermanent loss exists at all comes down to how decentralized exchanges work. Rather than matching buyers and sellers through an order book, most decentralized exchanges use automated market makers, pools of tokens governed by a mathematical formula that sets prices algorithmically. Liquidity providers fund these pools, and in return, they earn a share of the trading fees. The catch is that the same formula that lets the pool function also forces it to rebalance as prices move, and that rebalancing is what produces impermanent loss.

This guide walks through how liquidity pools and automated market makers work, exactly why price divergence creates the loss, a concrete worked example with numbers, how to calculate it, the role of fees and rewards in offsetting it, and the practical strategies that liquidity providers use to limit their exposure. The goal is to give you a clear enough mental model that you can judge, before committing any funds, whether providing liquidity to a given pool is likely to be worth it.

How liquidity pools and automated market makers work

To understand impermanent loss, you first have to understand the machinery that creates it, which is the automated market maker. A traditional exchange matches a buyer with a seller through an order book. A decentralized exchange built on an automated market maker, such as Uniswap or Curve, works differently: instead of matching counterparties, it holds pools of tokens that traders swap against directly, with prices set by a formula rather than by bids and offers.

To make this work, the pools need to be funded, and that is where liquidity providers come in. A liquidity provider deposits a pair of tokens into a pool, most commonly in a 50-50 split by value, and in exchange earns a portion of the fees that traders pay to swap against that pool.

The formula that governs the most common type of pool is elegantly simple. Many automated market makers use a constant product formula, often written as x*y = k, where x and y are the quantities of the two tokens in the pool and k is a constant that must stay the same. Because k cannot change, any trade that removes some of one token must add a corresponding amount of the other, and the ratio between the two tokens is what sets the price.

When a trader buys one token from the pool, they reduce its quantity and increase the other’s, which moves the price, and the formula guarantees the pool always quotes a price based on its current balances. This design is what makes decentralized trading possible without a central order book, and it works beautifully for traders.

For liquidity providers, however, the same rebalancing mechanism is the source of the problem, because it means the composition of their deposited tokens changes automatically as prices move, and not in their favor.

Why price divergence creates the loss

Here is the heart of the matter: impermanent loss arises specifically from divergence in the prices of the two tokens in a pool. When you deposit a pair of tokens, the automated market maker holds them in a balance dictated by its formula. If the market price of one token rises relative to the other, traders and arbitrageurs will buy the now-underpriced token from the pool until the pool’s price matches the wider market. That arbitrage is essential to keeping the pool’s prices accurate, but it has a consequence for you as a provider: the pool sells off some of the token that is rising in value and accumulates more of the token that is falling. In other words, the rebalancing leaves you holding more of the loser and less of the winner compared to what you started with.

When you later withdraw your liquidity, you receive your share of the pool in its rebalanced composition, and the total value of those tokens is less than the value you would have had if you had simply held your original deposit untouched. That shortfall is the impermanent loss. The critical insight is that it is driven entirely by how far the two tokens’ prices move relative to each other: the larger the divergence, the larger the loss, and it can occur whether the pool’s assets are rising or falling, because what matters is the change in the price ratio between them, not the direction.

The reason it is called impermanent is that the loss is only on paper as long as you stay in the pool; if the prices happen to return to the ratio at which you deposited, the loss disappears. It becomes a permanent, realized loss only at the moment you withdraw while the prices are still diverged. This is why impermanent loss is best understood not as money stolen from you but as an opportunity cost, the gap between what your pooled position is worth and what holding the tokens would have been worth.

A worked example with real numbers

Numbers make the concept click, so consider a concrete example. Suppose you want to provide liquidity to an Ether and dollar-stablecoin pool, and at the time you deposit, Ether is worth $1,600. Following the standard 50-50 split, you deposit 1 Ether and $1,600 of the stablecoin, for a total deposit worth $3,200. The pool now holds your tokens alongside everyone else’s, governed by the constant product formula.

Now suppose the price of Ether rises to $2,000 on the wider market. Arbitrageurs will buy Ether from the pool because it is briefly cheaper there, until the pool’s price catches up to $2,000. This rebalancing means the pool now holds less Ether and more of the stablecoin than before, and your share reflects that new mix. When you withdraw, you receive, say, an amount of Ether and stablecoin that together is worth less than if you had just held your original 1 Ether and $1,600.

Had you simply held, your 1 Ether would now be worth $2,000 and your stablecoin still $1,600, totaling $3,600. Your pooled position, after the rebalancing, might be worth around $3,500. That roughly $100 gap, before counting any fees, is the impermanent loss: the cost of having provided liquidity rather than held.

As a rule of thumb, when the price ratio between the two tokens doubles, the impermanent loss is around 5.7%, and the loss grows as the divergence grows. The example shows the unsettling truth that you can be up in dollar terms, since your position rose from $3,200 to $3,500, and still have lost relative to the simpler choice of holding.

How to calculate impermanent loss

For those who want to move beyond intuition to a precise figure, impermanent loss can be calculated with a standard formula, and understanding it helps demystify the phenomenon. The common estimator depends only on the price ratio, written as r, which is the ratio of the token pair’s price at the time of withdrawal to its price at the time of deposit.

The formula is:

Impermanent Loss = (2 × √r ÷ (1 + r)) − 1

The result is a negative percentage representing how much worse the liquidity position performed compared with simply holding the assets.

Using the doubling example:

- r = 2

- √2 ≈ 1.414

- 2 × 1.414 ≈ 2.828

- 2.828 ÷ 3 ≈ 0.943

- 0.943 − 1 ≈ -0.057

This equals an impermanent loss of approximately 5.7% before fees.

The formula also confirms several useful observations:

- If r = 1, meaning prices have not changed relative to one another, impermanent loss is zero.

- As r moves further away from 1, the loss increases.

- The formula depends on relative price movement, not whether prices rise or fall.

Many online calculators can perform this calculation automatically, but understanding the formula and remembering the 5.7% loss when prices double provides a useful mental shortcut when evaluating liquidity pools.

How fees and rewards offset the loss

Impermanent loss is only half the story, because liquidity providers are not giving their tokens away for nothing; they earn in return, and whether a position is profitable depends on the balance between what they earn and what they lose.

The primary source of earnings is trading fees. Every time a trader swaps against the pool, they pay a fee, and that fee is distributed to the liquidity providers in proportion to their share of the pool. In an active pool with heavy trading volume, those fees accumulate and can offset, or more than offset, the impermanent loss, leaving the provider with a net profit.

This is the entire economic proposition of providing liquidity: you accept the risk of impermanent loss in exchange for a stream of fee income, and you come out ahead when the fees exceed the loss.

Many protocols sweeten the deal further with additional token rewards, distributing their own governance or incentive tokens to liquidity providers on top of the trading fees, a practice often called yield farming or liquidity mining. These rewards can substantially boost returns and are frequently used by new protocols to attract liquidity. Some protocols also offer explicit impermanent loss protection, a form of insurance that partially reimburses providers for losses, typically funded by token emissions or a reserve pool, though the terms and caps vary.

The crucial point, however, is that the offsets are not guaranteed to win. Research on real pools has found that for a large share of liquidity providers, in some major pools, more than half, the impermanent loss actually exceeded the trading fees they earned, meaning they would have been better off simply holding.

This is the sobering reality behind the passive-income pitch: the fees are real, but so is the loss, and in volatile pools, the loss can swallow the fees. The honest way to approach liquidity provision is to weigh the expected fee income against the likely impermanent loss for a given pair before committing, instead of assuming the fees will automatically make it worthwhile.

How to limit your exposure

Because impermanent loss is driven by price divergence, the most effective ways to limit it all come down to choosing pairs whose prices move together, and understanding the trade-offs involved. The single most powerful technique is to provide liquidity to stablecoin pairs, such as a $1 stablecoin paired with another.

Because both tokens are pegged to the same dollar value, their prices barely diverge, which means the impermanent loss is close to 0. The trade-off is that such pools typically generate lower fee income, since they attract less volatile trading, but for a provider whose priority is avoiding impermanent loss, stablecoin pairs are the safest choice.

A related approach is to use pairs of assets that are closely correlated or pegged to each other, such as a token and its wrapped equivalent, where the two are designed to hold the same value and therefore experience essentially no divergence.

Beyond pair selection, some automated market makers allow providers to deposit in ratios other than the standard 50-50, or to concentrate their liquidity within a chosen price range, which can change the risk profile, though concentrated liquidity can also intensify impermanent loss if the price moves outside the chosen range.

Researching the historical volatility and price correlation of a potential pair before committing, and running the numbers through an impermanent loss calculator under different price scenarios, lets a provider find a pair that fits their risk tolerance.

The overarching principle is straightforward: the more the two tokens in a pool can move apart in price, the greater the impermanent loss risk, so providers who want to minimize that risk favor pairs that stay close in value, while those willing to accept more risk in pursuit of higher fees go in with clear eyes about the trade-off. There is no way to eliminate impermanent loss entirely on volatile pairs, but there are clear ways to manage and reduce it.

Risks and common mistakes

Beyond the mechanics, a few risks and recurring mistakes are worth flagging directly, because they are where liquidity providers most often get hurt. The most common mistake is treating advertised yields as guaranteed profit.

A pool may advertise an attractive annual yield from fees and rewards, but that headline figure does not account for impermanent loss, which can quietly erode or exceed it, so the real return can be far lower or even negative. Anyone evaluating a pool should mentally subtract the likely impermanent loss from the advertised yield to get a truer picture.

A second mistake is providing liquidity to highly volatile or uncorrelated pairs without appreciating the risk. The greater the price divergence between the two tokens, the larger the impermanent loss, so pairing a stablecoin with a volatile small-cap token, or two unrelated volatile tokens, exposes a provider to potentially severe losses if one moves sharply.

A third risk is withdrawing at the wrong moment, since impermanent loss only becomes permanent on withdrawal; pulling liquidity while prices are heavily diverged locks in the loss, whereas waiting, if the prices later converge, can reduce or erase it, though there is no guarantee they will.

Underlying all of this is the smart contract risk inherent in any decentralized finance protocol, since the pool is governed by code that could contain bugs or be exploited, a risk entirely separate from impermanent loss but always present.

The disciplined approach is to understand that providing liquidity is an active risk decision, not a passive income button: choose pairs deliberately, account for impermanent loss when judging returns, and recognize that the convenience of earning fees comes with a genuine cost that, in volatile pools, can outweigh the reward.

Frequently Asked Questions

What is impermanent loss in simple terms?

It is the opportunity cost you incur when you deposit tokens into a decentralized exchange’s liquidity pool and end up with less value than if you had simply held those tokens in your wallet. It happens because the pool automatically rebalances as the two tokens’ prices diverge, leaving you with more of the token that fell and less of the one that rose. It is called impermanent because the loss reverses if prices return to their starting ratio, and it only becomes a real, permanent loss when you withdraw your liquidity while the prices are still diverged.

Why does impermanent loss happen?

It happens because of how automated market makers work. These pools use a formula, commonly the constant product formula, that keeps the pool balanced by adjusting the ratio of the two tokens as their prices move. When one token’s price rises, arbitrageurs buy it from the pool until the pool’s price matches the market, which leaves the pool, and therefore your position, holding less of the rising token and more of the falling one. When you withdraw, that rebalanced mix is worth less than your original deposit would have been if simply held. The loss is driven by how far the two prices diverge.

How is impermanent loss calculated?

A common formula is:

Impermanent Loss = (2 × √r ÷ (1 + r)) − 1

where r is the ratio between the token pair’s price at withdrawal and its price at deposit.

For example, if the price ratio doubles (r = 2), the formula produces an impermanent loss of approximately 5.7% before fees.

When the ratio remains unchanged (r = 1), impermanent loss equals zero.

As the ratio moves farther away from one, the loss increases.

Many online calculators can perform this calculation automatically, but remembering the 5.7% benchmark is useful for quick estimates.

Can you avoid impermanent loss?

You cannot eliminate it entirely on volatile pairs, but you can limit it substantially. The most effective approach is to provide liquidity to stablecoin pairs, where both tokens hold the same dollar value and barely diverge, keeping impermanent loss near 0, though such pools typically earn lower fees. Using closely correlated or pegged pairs, such as a token and its wrapped version, has a similar effect. Researching a pair’s historical volatility and correlation, and modeling scenarios with a calculator before committing, helps you choose pairs that fit your risk tolerance and avoid the worst exposure.

Does impermanent loss mean I always lose money?

No. Impermanent loss is offset by the trading fees and token rewards you earn as a liquidity provider, and a position is profitable when those earnings exceed the loss. In an active, high-volume pool, fees can more than cover the impermanent loss, leaving a net gain. However, research has found that for a large share of providers in some major pools, the impermanent loss exceeded the fees earned, meaning they would have done better simply holding. So whether you end up ahead depends on the balance between fees and loss, which is why choosing the pair and pool carefully matters so much.

What is the difference between impermanent loss and a regular loss?

A regular loss is a straightforward decline in the value of an asset you hold. Impermanent loss is an opportunity cost: it compares your pooled position against the alternative of simply having held the same tokens, and it can occur even when your position has risen in dollar terms, as long as it rose less than holding would have. It is called impermanent because it can reverse if prices return to their starting ratio, unlike a realized loss. It only becomes a permanent, realized loss at the moment you withdraw your liquidity while the token prices are still diverged from where you deposited.

This article is educational information, not financial advice. Decentralized finance involves significant risks, including impermanent loss, smart contract vulnerabilities, and the potential loss of funds. Figures and formulas are illustrative and reflect general information available as of June 26, 2026. Verify the specifics of any protocol from primary sources and consider your own circumstances before providing liquidity or making any decision.

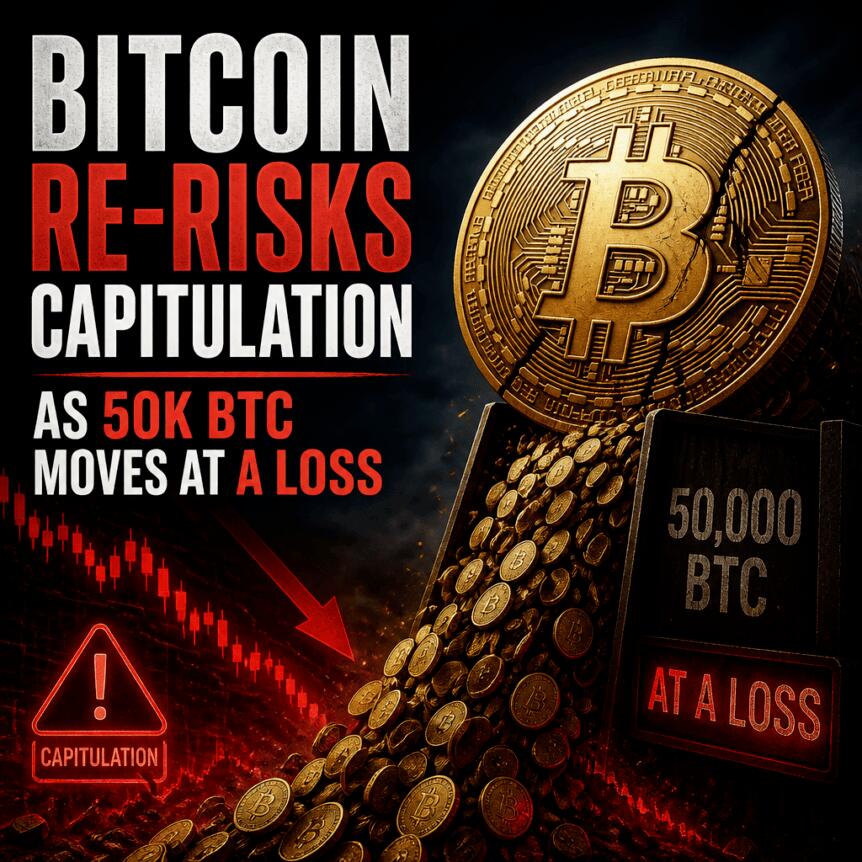

Bitcoin is flashing renewed signs of stress among short-term holders after a meaningful wave of coins moved to exchanges at losses over the past day. At the same time, the market value of short-term holder supply has dropped to $237.7 billion—its lowest point since October 2024—according to CryptoQuant.

While near-term sell pressure appears to be rising, the picture is not uniform. CryptoQuant also reported record inflows to long-term accumulation addresses, suggesting some longer-horizon investors are absorbing supply even as newer buyers reduce exposure.

Key takeaways

- CryptoQuant data shows Bitcoin’s short-term holder market capitalization fell to $237.7 billion on June 26, the lowest since Oct. 2, 2024.

- About 50,000 BTC moved to exchanges at a loss in the prior 24 hours, the largest such flow since June 4.

- Accumulation addresses saw record inflows of 181,000 BTC on Thursday, pointing to continued long-term buying.

- Multiple macro indicators and persistent institutional discount signals (Coinbase Premium Index below zero) have kept the risk-asset backdrop unfavorable.

- CryptoQuant flagged funding strains for Strategy (STRC) after its share-linked discount widened and its cash reserve declined in 2026.

Short-term holder capitulation signals return

CryptoQuant analyst Amr Taha said Bitcoin’s short-term holder (STH) market capitalization fell to $237.7 billion on June 26. That marks the lowest reading since Oct. 2, 2024, when the metric hovered near $239.7 billion.

The STH market cap tracks the market value of coins held by investors who bought Bitcoin within the past 155 days. When this measure drops below the cohort’s realized value, it typically implies that many of those relatively recent buyers are sitting on larger unrealized losses.

CryptoQuant notes a comparable pattern surfaced during the October 2024 correction, when the market later found an important bottom. However, the latest reading is framed as a stress signal rather than definitive confirmation that a low has already formed.

Exchange flows add a second, more immediate layer to the capitulation narrative. CryptoQuant reported that around 50,000 BTC from short-term holders moved to exchanges at a loss during the past 24 hours. Binance received about 9,500 BTC under similar conditions, the highest reading since June 3.

In practical terms, loss-to-exchange activity often reflects more aggressive sell decisions from near-term investors reacting to weaker prices—an asymmetry that can intensify downside pressure in the absence of fresh demand.

Long-term accumulation offsets the selling pressure

Despite the renewed loss-driven exchange activity, CryptoQuant highlighted a countervailing trend: Bitcoin inflows to accumulation addresses climbed to a record 181,000 BTC on Thursday.

CryptoQuant compared that figure with a prior peak of 94,700 BTC recorded in February 2022, emphasizing how unusual the current uptick is. Accumulation addresses typically receive coins with a history of low spending, and the reported surge suggests that longer-term investors are continuing to take supply off the table while short-term holders reduce exposure.

This divergence matters because it can help explain why sell-side pressure among newer holders does not automatically translate into a sustained, uninterrupted bear trend. Even if near-term holders keep capitulating, persistent absorption from long-term participants can limit how far the market extends downward.

Institutional demand remains constrained as rates stay tight

Several macro and institutional-demand indicators point to a cautious environment for Bitcoin buyers. Analyst Darkfost said institutional demand has continued to weaken, noting that the Coinbase Premium Index has remained below zero for 40 consecutive days since May 15.

The Coinbase Premium Index compares Bitcoin’s price on Coinbase Advanced with Binance. A persistent discount on Coinbase is generally interpreted as heavier selling from professional venues relative to more retail-linked pricing.

At the same time, US macro data contributed to expectations that monetary policy may not ease soon. The source cited headline PCE inflation at 4.1% versus an expectation of 4.0%, and core PCE at 3.4% versus 3.3%. GDP also came in above estimates at 2.1%, reinforcing a narrative of limited near-term relief for risk assets.

“This dynamic is a perfect reflection of the current macro backdrop, which remains deeply unfavorable for risk assets such as BTC.”

Asset manager Bitwise pointed to the Federal Reserve meeting referenced in its update as accelerating a hawkish shift. Bitwise said policymakers removed their easing bias and increased the median 2026 Fed funds projection to 3.8% from 3.4% in March.

Bitwise also linked tighter financial conditions to ongoing outflows from crypto exchange-traded products, including spot ETFs. The immediate takeaway for traders is that when funding conditions tighten and institutional inflows slow, dips can attract less immediate “buy-the-drop” behavior—even if long-term wallets continue to accumulate.

Strategy’s funding strain could matter for institutional flows

Attention has also shifted to Strategy, one of Bitcoin’s best-known institutional buyers. Bitwise estimated that Strategy accumulated 174,300 BTC in 2026, including about 96,000 BTC (55%) financed via STRC preferred equity issuances and another 77,500 BTC funded through MSTR common stock offerings.

CryptoQuant later argued that the purchasing capacity behind that activity may be weakening. In a report released this week, CryptoQuant said STRC traded at a record 17.5% discount to its $100 par value after falling to $82.5 last week, before slipping to around $73 in premarket trading on Friday.

CryptoQuant also said Strategy’s cash reserve has dropped 38% since the start of 2026 following the repurchase of a $1.5 billion convertible note. It further noted that annual dividend obligations tied to STRC have risen to $1.2 billion from $300 million, while dividend coverage has narrowed to about 14 months from as long as seven years.

Those constraints matter because Strategy’s continued buying has been a key element in the institutional-demand narrative around Bitcoin. If the company’s ability or willingness to finance additional acquisitions tightens, the market may face fewer incremental bids from one of its most prominent corporate participants—just as loss-to-exchange flows among short-term holders are rising.

For readers tracking the downside-to-absorption balance, the next developments to watch are whether short-term holder exchange inflows cool off after this day’s spike, and whether institutional demand signals improve as macro expectations evolve. At the same time, investors should monitor whether Strategy’s funding conditions stabilize—since that could influence how quickly large-scale institutional buying resumes if price volatility increases.

Nearly 50,000 BTC shifted to exchanges at a loss while short-term Bitcoin holders’ stress level reached 2-year highs. Is BTC headed toward new lows?

The crypto ecosystem rushed to help Venezuela after the devastating earthquakes of June 24. Humanitarian organizations, exchanges, and community campaigns activated channels to enable cryptocurrency donations.

The speed of the crypto industry is key to accelerating the arrival of funds to the most affected areas.

Crypto is Critical During Humanitarian Emergencies

A donation in cryptocurrencies allows funds to be sent directly between wallets without going through traditional banks. The transaction is completed in minutes, crosses borders without restrictions, and is especially useful in countries with financial systems under pressure or international sanctions.

The scale of the Venezuelan tragedy justifies the urgency. The 7.2 and 7.5 magnitude earthquakes shook the center-north of the country. La Guaira was among the hardest-hit areas, with collapsed apartments and rescuers digging by hand because heavy machinery was unavailable.

UN reports cited by the BBC speak of dramatic numbers. At least 920 dead, more than 3,300 injured, and over 50,000 people missing. These numbers could rise as families continue searching for loved ones among debris, in hospitals, and in improvised shelters throughout the region.

The prior context makes the response even harder. Venezuela has faced years of economic crisis, massive migration, and the deterioration of public services. Interruptions in electricity, water, communications, and transport complicate rescue efforts, while international aid is arriving from the Dominican Republic, Mexico, El Salvador, Spain, Switzerland, India, and Colombia.

Stablecoins are becoming the preferred vehicle. Assets like USDT and USDC reduce volatility and make it easier to pay locally for food, medicine, and rescue equipment.

This efficiency explains why so many initiatives choose crypto channels over traditional banking in emergency situations.

The Main Ways to Donate Crypto to Venezuelan Users

The world’s largest exchange by trading volume launched a corporate response. Binance announced a $3 million donation for affected users, offering 20 USDT coupons and temporarily eliminating P2P fees. The measure covers seven states impacted by the June 24 earthquakes.

El Dorado, the Latin American P2P exchange, also joined the effort, coordinating aid to the most affected regions and leveraging its reach among Venezuelan users who already regularly use stablecoins in bolivars.

In this regard, it enabled commission-free transfers to Venezuela for users outside the country.

The campaign led by Ana Ojeda Caracas has become one of the ecosystem’s most visible. The Venezuelan “Criptolawyer”, a well-known figure within the Latin American community, announced on X a partnership with the Decaf platform to channel international donations to families affected by the earthquakes.

Decaf Pay, the technical infrastructure behind the project, allows for contributions in USDC, card, and international bank transfer. The total amount raised is publicly visible, and the platform facilitates local payments in Venezuela through Airtm’s infrastructure to speed up conversion.

The BTC UCAB Academy activated an Emergency Earthquake Fund Venezuela 2026. This initiative from Universidad Católica Andrés Bello offers institutional custody and on-chain transparency.

Each donation and disbursement will be verifiable on the blockchain and communicated via official social media.

International organizations round out the map. Mercy Corps and World Vision accept crypto donations through The Giving Block, a platform specializing in digital asset donations. Both receive Bitcoin, Ethereum, USDC, and other popular cryptocurrencies for their global humanitarian response.

Community initiatives have also joined in. X user LIVRE is raising funds in Bitcoin, Ethereum, Solana, SUI, and USDC to buy gloves, gauze, alcohol, food, water, and rescue tools.

Caution and Verification When Donating in Times of Crisis

Cryptocurrencies offer speed, but also risks. Transactions are irreversible, addresses can be spoofed, and fake campaigns often proliferate after natural disasters. Emotional urgency can lead donors to skip basic verifications during an emergency.

Professional recommendations involve several filters:

- Verify official links, check original posts.

- Avoid copying addresses from unverified screenshots and prefer organizations with public traceability.

- Reports on the use of funds and a proven track record are the best indicators of reliability.

The diversity of initiatives also helps the donor. There are options for different profiles: community campaigns for direct impact in La Guaira, institutional funds with regulated custody, and global organizations with a presence in nearly one hundred countries. Each profile can choose the channel that best fits their needs.

This wave of solidarity confirms a broader trend. Cryptocurrencies are no longer just speculative assets but are becoming a global humanitarian response infrastructure.

Venezuela thus adds a new chapter to the record of disasters in which crypto has served as a bridge of solidarity.

The post Bitcoin and Stablecoins Become Lifelines After Venezuela Earthquakes appeared first on BeInCrypto.

Yuma, an investment firm backed by Digital Currency Group, has launched the Yuma Total Market Fund to give institutional investors diversified exposure to the Bittensor decentralized AI ecosystem in a single vehicle. The fund is designed to track both Bittensor’s native TAO token and a basket of AI-focused subnets without requiring investors to hold or select individual subnet tokens.

In a Thursday announcement, Yuma said the fund began with seed capital from an undisclosed anchor investor. The launch comes as asset managers increasingly look for regulated products tied to decentralized AI networks, following broader institutional interest in blockchain-based alternatives to centralized AI providers.

Key takeaways

- Yuma’s fund targets diversified exposure to Bittensor by combining TAO holdings with a basket of AI subnet exposure under one investment strategy.

- The fund is positioned as a simpler entry point for investors who want Bittensor exposure without manually building a subnet portfolio.

- Bittensor’s subnet economy is often cited as very large, but network data from Taostats indicates the combined subnet value is closer to $300 million than higher estimates.

- Institutional allocation shifts already signal growing interest in TAO and the broader decentralized AI theme, including changes in Grayscale’s Decentralized AI Fund.

- Regulatory product momentum continues, with filings and conversions aimed at bringing TAO exposure into ETF wrappers.

A one-stop fund for Bittensor exposure

According to Yuma, the Yuma Total Market Fund provides exposure to TAO and a basket of AI-oriented subnets through a single investment vehicle. The stated intent is to reduce complexity for institutions that want exposure to the ecosystem’s “total market” rather than picking specific subnets themselves.

Yuma also framed the timing around expanding institutional demand for decentralized AI products. Bittensor, the network behind the ecosystem, supports AI infrastructure and application development using specialized subnets that span areas including compute, marketplaces, and identity.

How big is the subnet economy?

Yuma pointed to Bittensor’s scale, stating that its 128 subnets represent more than $900 million in combined value. However, network tracker Taostats shows a combined subnet value closer to $300 million.

For investors, the difference matters because it can affect how the “basket” inside the fund is sized, weighted, and interpreted relative to the overall ecosystem. Even if TAO remains the focal point for market attention, subnet value is relevant for understanding how diversified exposure may behave when network activity, demand for specific subnet services, or token economics shift.

Institutional interest in TAO is evolving

Yuma’s announcement arrives amid a broader institutional pivot toward decentralized AI exposure, particularly through TAO. Earlier this year, Grayscale increased TAO’s weighting in its Grayscale Decentralized AI Fund to 43% during the fund’s quarterly rebalance in April. Since then, the allocation has reportedly fallen to about 20%.

As Grayscale’s rebalancing progressed, Near Protocol’s NEAR moved into the lead position within the fund at roughly 44%. The shifting weights underscore that decentralized AI exposure inside institutional portfolios is not static—asset managers are adjusting allocations as constituent components change in relative performance, risk, and market interest.

TAO’s broader institutional visibility has also been reflected in its market capitalization being cited at nearly $2.4 billion, according to CoinMarketCap.

ETF momentum and product building

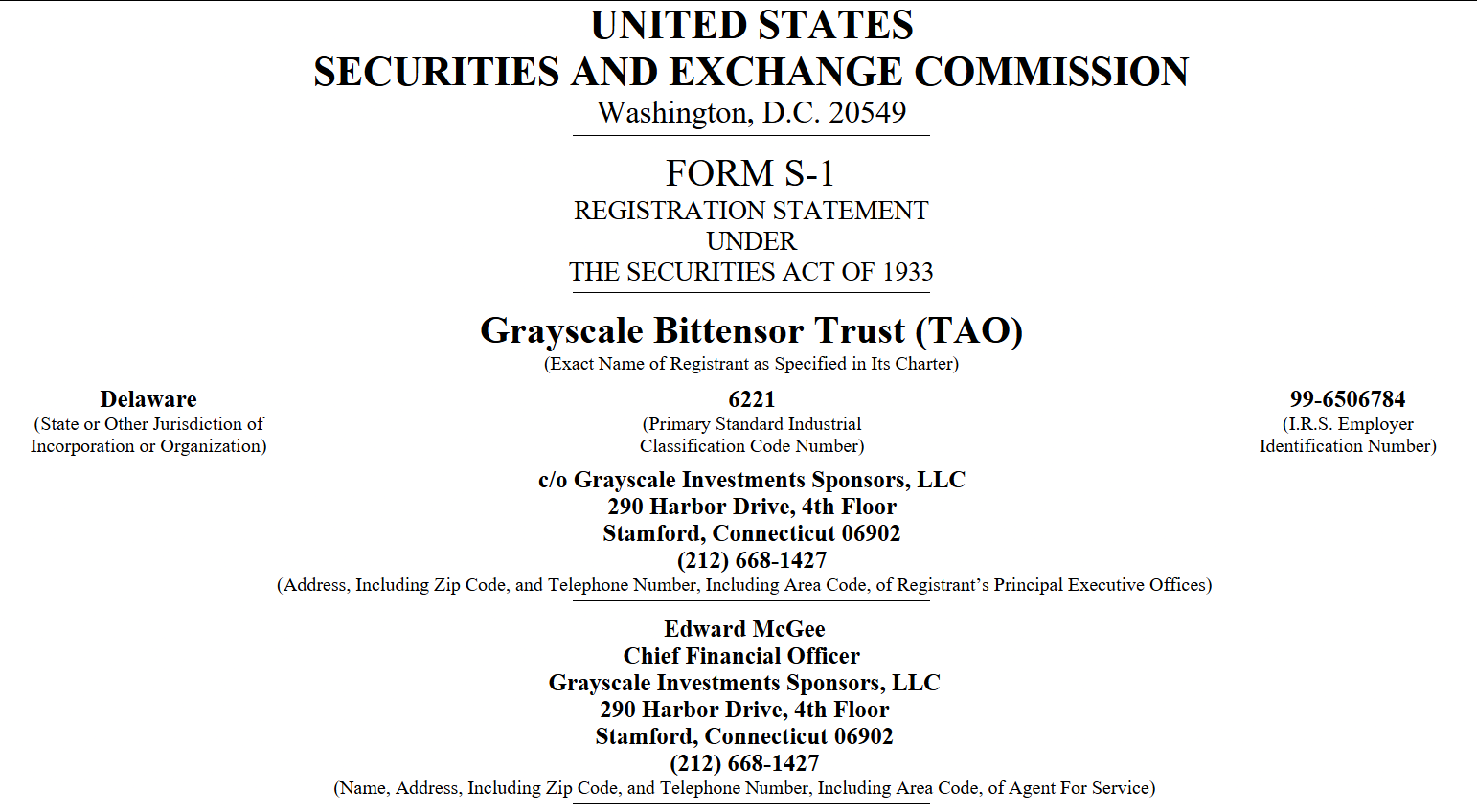

The fund launch also fits a larger wave of attempts to package TAO exposure into familiar exchange-traded wrappers. In April, Bitwise filed for a TAO Strategy ETF with the US Securities and Exchange Commission (SEC). Separately, Grayscale submitted an amended registration statement aimed at converting its existing Bittensor Trust into a spot TAO exchange-traded fund that—if approved—would list on NYSE Arca. The SEC filing is available through its public EDGAR archive.

While Yuma’s product is a fund and not necessarily an ETF, the parallel push highlights a shared strategy among managers: broaden access to TAO and decentralized AI networks in forms that institutions can more easily allocate to, benchmark, and trade compared with direct, token-by-token exposure.

Why decentralized AI is back in the spotlight

Interest in decentralized AI has also been reinforced by renewed attention to the risks of reliance on a single provider. The renewed debate picked up momentum after the US Commerce Department suspended public access to Anthropic’s Fable 5 and Mythos 5 models over national security and export control concerns.

Grayscale head of research Zach Pandl argued at the time that the restrictions highlighted the dangers of centralized control over AI systems, adding that he expected demand for decentralized AI such as Bittensor and its TAO token to rise as investors look for alternatives to centralized model providers. Earlier coverage also linked the shutdown to a broader case for decentralized approaches to AI infrastructure.

Since then, the situation appears to have eased: the Commerce Department restored access to Mythos 5 on Friday, and Axios reported Saturday that the Trump administration is expected to allow Anthropic to resume public access to Fable 5 as soon as next week.

Even with the access restoration, the episode illustrates the kind of operational and policy risk that can make “provider diversity” an investment theme—exactly the idea behind products that bundle exposure across decentralized ecosystems rather than hinging on a single company’s model availability.

Investors should watch how Yuma’s fund constructs its subnet basket over time and how quickly institutional allocations shift between TAO-centric exposure and broader subnet diversification. With multiple TAO ETF-related filings in motion and policy-driven headlines repeatedly reshaping the decentralized AI narrative, the next key signal will be how regulators and asset managers respond as demand for decentralized AI wrappers grows.

Digital asset infrastructure company BitGo is reducing its workforce by nearly 15% as it shifts its focus toward stablecoins, trading, security, settlement services, and AI-powered infrastructure.

BitGo co-founder and CEO Mike Belshe said the company made the decision because the financial services and crypto sectors have changed significantly, requiring the firm to become more focused and “deliberate” in how it operates.

Workforce Reduction

According to Belshe’s official tweet, the job cuts are intended to help BitGo concentrate its people and resources on areas considered most important for future growth and client needs. He described the move as a difficult decision and acknowledged the contributions of employees who helped build the company.

Belshe said all affected workers would be informed directly by their managers and human resources teams before the announcement became public. Addressing the remaining staff, Belshe urged employees to support one another and communicate closely as the company reorganizes.

The exec also stated that the layoffs are a one-time action, while adding that the company does not expect additional workforce reductions.

“To those of you who are leaving: thank you. You helped shape BitGo into what it is today, and the company will always be better because you were here. I wish you nothing but success ahead. To the team that remains: I know this is still hard. Be good to each other and overcommunicate as we reorganize. We have a clear, strong path forward, and this is a one-time action.”

AI and Market Slump

BitGo’s job cuts come as the crypto industry continues to see layoffs this year. Many firms have blamed weak market conditions and the growing use of artificial intelligence, which has improved efficiency and reduced the need for larger workforces. Coinbase cut roughly 14% of its workforce in May. Besides market conditions and cost discipline, CEO Brian Armstrong also pointed to AI tools helping teams become more efficient, making the company leaner.

Gemini also slashed about 30% of its workforce in March, in the same week as Crypto.com cut 12%.

The post BitGo Slashes Workforce as CEO Bets on AI, Stablecoin and Settlement Growth appeared first on CryptoPotato.

Yuma, a Digital Currency Group-backed investment company, has launched a fund that gives institutional investors diversified exposure to the Bittensor ecosystem, as asset managers expand investment products tied to decentralized AI.

According to a Thursday announcement, the Yuma Total Market Fund provides exposure to Bittensor’s native TAO token and a basket of AI-focused subnets through a single investment vehicle. The strategy is intended to simplify access to the broader Bittensor ecosystem without requiring investors to select individual subnet tokens.

The fund launched with seed capital from an undisclosed anchor investor.

Bittensor is a decentralized network that supports the development of AI infrastructure and applications through specialized subnets spanning areas such as compute, marketplaces and identity. According to Yuma, the network’s 128 subnets represent more than $900 million in combined value. However, data from network tracker Taostats shows a combined subnet value closer to $300 million.

TAO, the native token of the Bittensor ecosystem, has a market capitalization of nearly $2.4 billion. Source: CoinMarketCap

Institutional interest in the Bittensor ecosystem has grown alongside the network’s expanding subnet economy. In April, Grayscale increased TAO’s weighting in its Grayscale Decentralized AI Fund to 43% during the fund’s quarterly rebalance. TAO’s allocation has since fallen to about 20%, with Near Protocol’s NEAR now comprising the fund’s largest holding at roughly 44%.

Asset managers are also seeking to broaden investor access to TAO. Bitwise filed for a TAO Strategy ETF with the US Securities and Exchange Commission (SEC) in April, while Grayscale submitted an amended registration statement to convert its existing Bittensor Trust into a spot TAO exchange-traded fund that would list on NYSE Arca if approved.

Grayscale Bittensor Trust (TAO) application with the SEC. Source: SEC

Related: Amazon warning triggered US crackdown on Anthropic AI models: Reports

Anthropic restrictions renew focus on decentralized AI

The case for decentralized AI, which distributes AI infrastructure and computing across blockchain-based networks rather than relying on a single provider, gained renewed attention after the US Commerce Department suspended public access to Anthropic’s Fable 5 and Mythos 5 models over national security and export control concerns.

At the time, Grayscale head of research Zach Pandl said the restrictions underscored the risks of relying on centralized AI providers. The government order limiting access to Anthropic’s Fable 5 and Mythos 5 “highlights the risks of centralized control of AI,” Pandl said. “We expect demand for decentralized AI, like Bittensor and its TAO token, to rise as investors seek alternatives.”

The restrictions appear to be easing. The Commerce Department restored access to Mythos 5 on Friday, and Axios reported Saturday that the Trump administration is expected to allow Anthropic to resume public access to Fable 5 as soon as next week.

Magazine: How AI just dramatically sped up the quantum risk for Bitcoin

The ongoing artificial intelligence stock frenzy has pulled in capital from across the market, from traditional metals, considered the safest assets, to crypto, considered the riskiest.

Gold dropped below $4,000 for the first time since November earlier this week, silver has lost more than half its value from its high, and bitcoin has slipped to nearly $58,000.

The three selloffs are not a coincidence. For much of the past two years, they have been, to a large degree, the same trade, and now the same forces are unwinding it.

That trade even has a name, the “debasement” trade. It is the bet that heavy government spending and rising national debt will slowly erode the value of paper money, which pushes investors toward scarce assets that no government can print more of.

Gold and silver are the oldest versions of that bet, while bitcoin, with a supply capped at 21 million coins, got marketed as the digital version. Through 2025, as the dollar looked vulnerable, money poured into all three, and they were treated as one basket.

Sony Interactive Entertainment is removing 551 purchased films from UK PlayStation Store accounts on September 1, 2026, citing content licensing agreements with StudioCanal.

The affected library spans decades of cinema, from Terminator 2: Judgment Day and Rambo: First Blood to Bridget Jones’ Diary, Pan’s Labyrinth, and Paddington. Customers who paid for those titles will lose access regardless of their purchase history.

When a Purchase is Not Ownership

Sony published a formal legal notice confirming the removal, attributing it to the expiration of its licensing agreement with StudioCanal. The notice offered no refunds or alternative compensation for affected buyers.

The situation exposes a structural reality most consumers overlook at checkout. A digital “purchase” on any platform-controlled storefront functions more like a temporary license than outright ownership.

Therefore, Sony and StudioCanal can modify or terminate that license, and the buyer absorbs the loss.

With 551 titles set for deletion, this is one of the largest single-event disappearances of purchased digital content in recent memory.

PlayStation Digital Ownership and the Gaming Parallel

The concern is not limited to films. When GTA 6 pre-orders opened this week, Rockstar confirmed that physical retail editions would include only a digital download code, with no disc.

For buyers who assumed a boxed copy meant a physical artifact they owned outright, that detail reinforced a growing unease. The GTA launch also sent shockwaves through crypto markets that same day, highlighting how far the digital ownership question now extends across gaming and finance.

Together, the two events make the same point. Across entertainment and gaming, consumers are paying for access, not ownership.

The Web3 Argument Gets Louder

Non-fungible tokens (NFTs) were built to address exactly this problem by creating on-chain, portable title deeds that no single platform can revoke. If StudioCanal had issued film rights as NFTs, Sony could not have overridden them.

Those tokens would remain in the buyer’s wallet, transferable and verifiable, independent of any licensing dispute between corporations.

That argument is gaining fresh credibility. Earlier this year, market observers noted a shift in the NFT sector away from speculation toward tangible utility, with digital ownership emerging as the strongest long-term use case.

Meanwhile, Worldcoin’s biometric identity push brought parallel questions about who controls proof-of-ownership in digital spaces into mainstream debate. Across the broader GameFi sector, 2026 has already seen renewed investor appetite for blockchain-backed digital economies.

The PlayStation film deletions may appear to be a routine licensing dispute on paper.

However, they crystallize a question that streaming, gaming, and digital media platforms have not resolved: when a platform changes its terms, what does a consumer actually own?

For blockchain advocates, Sony just provided the most mainstream illustration yet.

The post Sony Deletes 500+ Purchased Movies From PlayStation, Reigniting Blockchain Debate appeared first on BeInCrypto.

Jeremy Grantham, the GMO co-founder who called both the 2000 dot-com crash and the 2008 housing collapse, branded Bitcoin (BTC) “a useless, speculative mechanism” and predicted it would dwindle over the next few decades.

The veteran strategist built his critique around three failures he sees in crypto. Bitcoin pays no yield, holds no stable value, and fails as a usable currency in daily life, he argued.

Proof of Work, Proof of Nothing

Grantham singled out Bitcoin’s proof-of-work design for particular scorn. The energy burned to validate transactions, he argued, generates no economic benefit for society.

“Proof of unnecessary work shouldn’t be worth a bucket of warm spit, and it will not be.”

Bitcoin Falls Short as Money and Store of Value

Beyond the mining critique, he said Bitcoin does not work as a practical currency. Regular users do not accept it at the supermarket, and serious investors do not settle large transactions with it. Without a functioning transaction layer, the asset cannot claim monetary legitimacy, he added.

He also dismissed Bitcoin as a store of value. Unlike equities, it pays no dividend and generates no cash flow. In his view, that leaves speculators with nothing to anchor a fair price.

A Skeptic With a Record

Grantham’s warnings carry weight because of his track record. He flagged the dot-com bubble before 2000 and warned of the US housing collapse before 2008. His more recent AI bubble stock warning extended that thesis to US equities, where he now sees downside of up to 70%.

However, his timing is not always precise. His 2021 epic-bubble call on US stocks arrived early, as markets climbed before their 2022 correction.

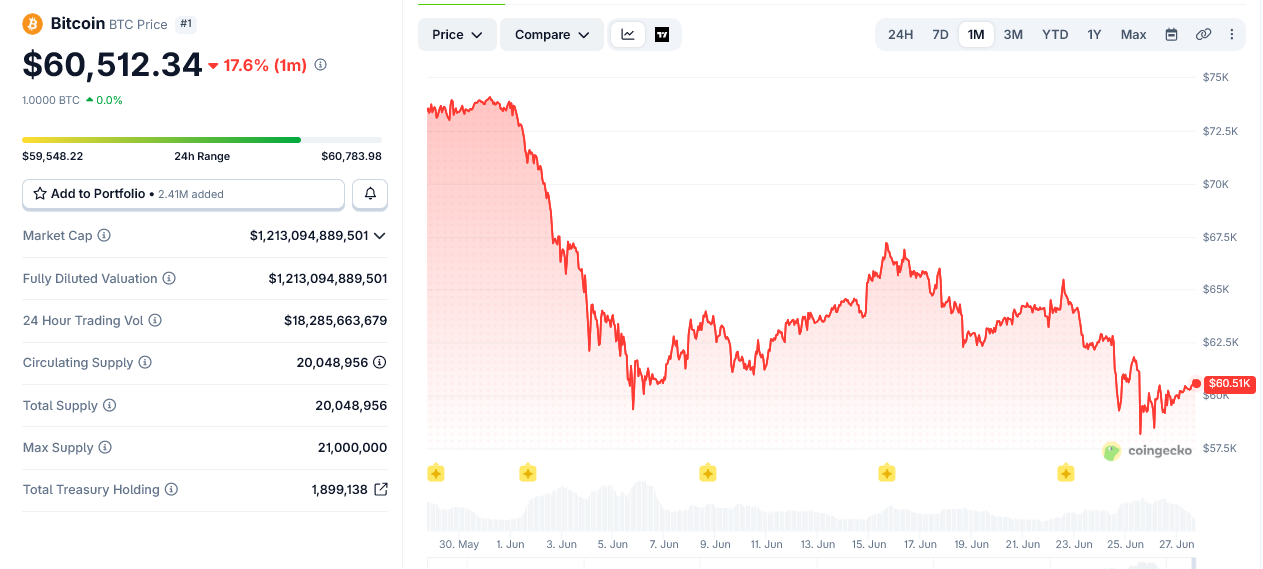

The Bitcoin remarks land as BTC trades near $60,500, down sharply from its late-2025 peak above $126,000. US spot Bitcoin ETF records outflows of $6.35 billion over 30 days through mid-June, reflecting cooling institutional demand.

Earlier, Coinbase CEO’s Bitcoin outlook has also flagged AI infrastructure costs as a variable reshaping crypto capital flows.

Grantham is not alone in his skepticism. Peter Schiff has made similar bearish arguments, contending that Bitcoin holds no intrinsic value.

Whether Bitcoin’s current price holds key support in Q3 2026 will test both camps. Grantham predicted the decline would come gradually, over years or even decades, not all at once.

The post Billionaire Grantham Uses Extreme Words to Describe Bitcoin appeared first on BeInCrypto.

Stocks tied to digital assets are sliding faster than the broader US market, reinforcing an increasingly visible split between crypto-focused equities and the S&P 500. The latest comparison comes from The Kobeissi Letter, which points to steep drawdowns at major crypto businesses as technology selloffs ripple through risk assets.

According to The Kobeissi Letter, Coinbase and Circle shares are down 69% and 72%, respectively, from their all-time highs. Those declines outpace drops seen in several large technology names—such as Oracle, Salesforce, Netflix and Palantir—each down between 48% and 57% from peak levels, while the S&P 500 has retreated about 3.5% from its recent high.

Key takeaways

- Crypto-related equities are falling much more sharply than the S&P 500, according to The Kobeissi Letter.

- Investor pressure is tied not only to broader risk-off moves, but also to weaker digital asset markets and policy uncertainty in the US.

- Bitcoin’s drop below $60,000 and Ether sliding toward $1,500 have intensified selling across the sector.

- Corporate earnings stress is compounding the downturn, with Coinbase missing Wall Street expectations in its latest quarterly report.

- Despite continued institutional activity, 21Shares says crypto’s four-year market cycle remains a key driver of prices into 2026.

Crypto equities break away from the broader market

The widening gap between crypto-adjacent stocks and the S&P 500 appears tied to a combination of macro pressure and sector-specific risk. The pullback in technology equities reflects growing concerns that rapid advances in artificial intelligence could disrupt existing business models across parts of the sector. Within that environment, crypto businesses face additional headwinds.

Even as semiconductor stocks have managed to hold up better through periods of volatility, crypto-related shares have remained under pressure. The Kobeissi Letter’s comparison suggests the underperformance is not just a beta story tied to general market weakness—it also reflects how quickly public equities react to sentiment around digital asset performance.

Digital asset selling feeds equity declines

Market conditions in crypto have worsened alongside equities. The article notes that Bitcoin fell below $60,000 this week and extended its decline to more than 54% from its October peak. Ether has likewise faced heavy selling, recently dropping to around $1,500—about 69% below last year’s high.

When crypto prices slide, revenue expectations for exchanges, custody providers, and payments platforms can come under pressure, and investors often reprice the sector more aggressively than the general market. That dynamic helps explain why Coinbase and Circle have experienced drawdowns that exceed those of several major technology companies.

Broader digital asset policy is also part of the backdrop. The report points to uneven progress on comprehensive crypto market structure legislation in the United States, a factor that continues to influence how investors value the long-term prospects of crypto businesses.

Earnings disappointment adds another layer

Financial results have not helped. The coverage highlights that Coinbase reported first-quarter results that missed Wall Street expectations. As described in earlier reporting from Cointelegraph, the company’s revenue fell 21% from the prior quarter and it posted a loss of $1.49 per share, compared with analysts’ expectations for earnings of $0.27 per share.

For investors, earnings misses during a period of declining crypto market activity can have outsized impact: they reinforce concerns about transaction-driven revenues and trading volume sensitivity. In short, equity investors appear to be dealing with both the market-level hit from weaker coin prices and company-level pressure from the latest quarterly numbers.

21Shares trims 2026 expectations, but sees institutional progress

While public equities are under strain, institutional participation remains a key part of the crypto narrative. In a midyear outlook, 21Shares lowered its expectations for 2026, arguing that digital asset prices have underperformed relative to underlying fundamentals.

According to the report, institutional adoption is still strengthening—particularly in stablecoins, tokenization, and prediction markets. However, 21Shares emphasizes that the dominant force behind crypto prices continues to be Bitcoin’s four-year cycle.

In the same outlook, 21Shares states that increasing institutional ownership may have moderated Bitcoin’s drawdowns but has not fundamentally changed the asset’s cyclical behavior. The firm also indicated it previously forecast the four-year cycle could become obsolete, but has since walked back that view, saying the cycle is “evolving, but it has not broken yet.”

The argument matters for investors because it frames market volatility as more structural than purely sentiment-driven. If Bitcoin’s cycle remains intact, rallies could be more dependent on timing and macro liquidity than on incremental improvements in on-chain or institutional usage metrics—an outlook that can influence positioning across both crypto assets and crypto equities.

What to watch next

Investors will likely focus on whether crypto price action stabilizes—especially around the $60,000 level for Bitcoin and the $1,500 area for Ether—as well as whether upcoming corporate reports from major crypto platforms show earnings pressure easing or continuing. At the same time, market participants will watch how US legislative progress advances, since regulatory clarity (or its absence) continues to shape valuation assumptions for the sector.

All-Ireland SFC: Kerry break Tyrone hearts in epic quarter-final

Buy vs Rent in Bangalore! #bangalore #budget #yeahkairushi #minivlog #asmr #househunting #money

Bournemouth beachgoers watch in horror as man dies after 100ft cliff fall

![BITCOIN & CRYPTO BLOODBATH. [THIS IS VERY BAD]](https://wordupnews.com/wp-content/uploads/2026/06/1782587546_maxresdefault-80x80.jpg)

-

Entertainment7 days ago

Entertainment7 days agoRenter of Home in Anne Heche Crash Denies Settlement With Son

-

Sports4 days ago

Sports4 days agoTwo goals and an assist by sheer aura: Cristiano Ronaldo just entered the World Cup chat

-

Tech5 days ago

Tech5 days agoMicrosoft accidentally kills epic Outlook email threads

-

Fashion1 day ago

Fashion1 day agoWeekend Open Thread: Staud – Corporette.com

-

Business7 days ago

Business7 days agoSoccer-U.S. defends Iran World Cup travel restrictions, says discussions ongoing

-

Politics2 days ago

Politics2 days agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Politics2 days ago

Politics2 days agoPotential 2028er World Cup attendee leaderboard

-

Business2 days ago

Business2 days agoAsia stock markets slide as tech shares slump

-

Tech2 days ago

Tech2 days agoA Look At A Gaggle Of Transputer Boards

-

Crypto World4 days ago

Bitcoin (BTC) Dips Below $62K, Ethereum (ETH) Plunges 6% Daily: Market Watch

-

Crypto World4 days ago

Crypto World4 days agoSecuritize Wraps Roubini's SEC-Registered ETF as Dubai VARA Digital Security

-

Crypto World2 days ago

Crypto World2 days agoDell (DELL) Shares Tumble Over 5% Following Analyst Downgrade to Hold

-

Business4 days ago

Entergy settles forward sale agreements, raises $672 million in cash proceeds

-

Sports23 hours ago

Sports23 hours agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Crypto World15 hours ago

Crypto World15 hours agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Crypto World1 day ago

Crypto World1 day agoRTX holders must register wallets before token distribution begins

-

Crypto World1 day ago

Crypto World1 day agoHyperliquid Named on Singapore MAS Investor Alert Register

-

Sports2 days ago

Sports2 days agoIndia vs Bangladesh LIVE Score, Women’s T20 World Cup: Bangladesh Opt To Bat; India Enter ‘Do-Or-Die’ Stage As Semi-Final Race Heats Up

-

Tech6 days ago

Tech6 days agoSignal’s Meredith Whittaker says AI chatbots ‘are not your friends’ and calls Copilot agents a backdoor

-

Crypto World2 days ago

The DATA Foundation Launches to Tackle AI’s Multi-Billion Dollar Training Data Bottleneck

You must be logged in to post a comment Login